BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on October 25, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Applications to MBA programs are up 12% in 2024 after declining for two years, according to the Graduate Management Admission Council, which surveys business school admissions offices.

Apple and Goldman Sachs were ordered to pay $89 million by the Consumer Financial Protection Bureau for failing to address thousands of consumer disputes of Apple Card transactions.

Apple is cutting production of Vision Pro due to slow sales. The tech giant is scaling down production of its $3,500 Vision Pro VR headset and might halt assembly of new ones next month,

UPS delivered a strong earnings report, with revenue beating analyst expectations for the first time in two years. Shares popped 5.28%.

ServiceNow rose 5.41% to a new all-time high thanks to a beat-and-raise third-quarter earnings report powered by higher AI demand for the enterprise software company.

Whirlpool climbed 11.20% after announcing solid earnings and reiterating guidance for the rest of the fiscal year, reassuring worried shareholders.

Molina Healthcare soared 17.67% after beating both top and bottom line estimates in the third quarter, thanks to the health insurer reaping the rewards of higher Medicaid payouts.

STOCKS DOWN

IBM dropped 6.17% on disappointing third-quarter results, missing on both top and bottom line forecasts thanks to lower consulting and infrastructure revenue.

Peloton pedaled higher yesterday after Greenlight Capital’s David Einhorn declared that the company was undervalued while he was pedaling on a Peloton. The stunt only worked for a quick sprint, though, with shares back down 2.07% today.

TKO Group Holdings got hit with a piledriver after the owner of the WWE and UFC announced it is acquiring several entertainment companies, including Professional Bull Riders. Investors bucked shares off 8.69%.

Keurig Dr. Pepper fizzled 4.80% thanks to lower sales last quarter, though the company is trying to bolster revenue by acquiring energy drink maker Ghost.

Air taxi startup Lilium crashed 61.50% on the news that its main subsidiaries have run out of cash and are filing for insolvency.

The S&P 500® index (SPX) rose 12.44 points (0.21%) to 5,809.86; the $DJI fell 140.59 points (–0.33%) to 42,374.36; and the NASDAQ Composite® ($COMP) added 138.83 points (0.76%) to 18,415.49.

The 10-year Treasury note yield fell four basis points to 4.20%.

The CBOE Volatility Index® (VIX) was about flat at 19.18.

Posted on October 24, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

QUESTION EVERYTHING?

By Staff Reporters

***

***

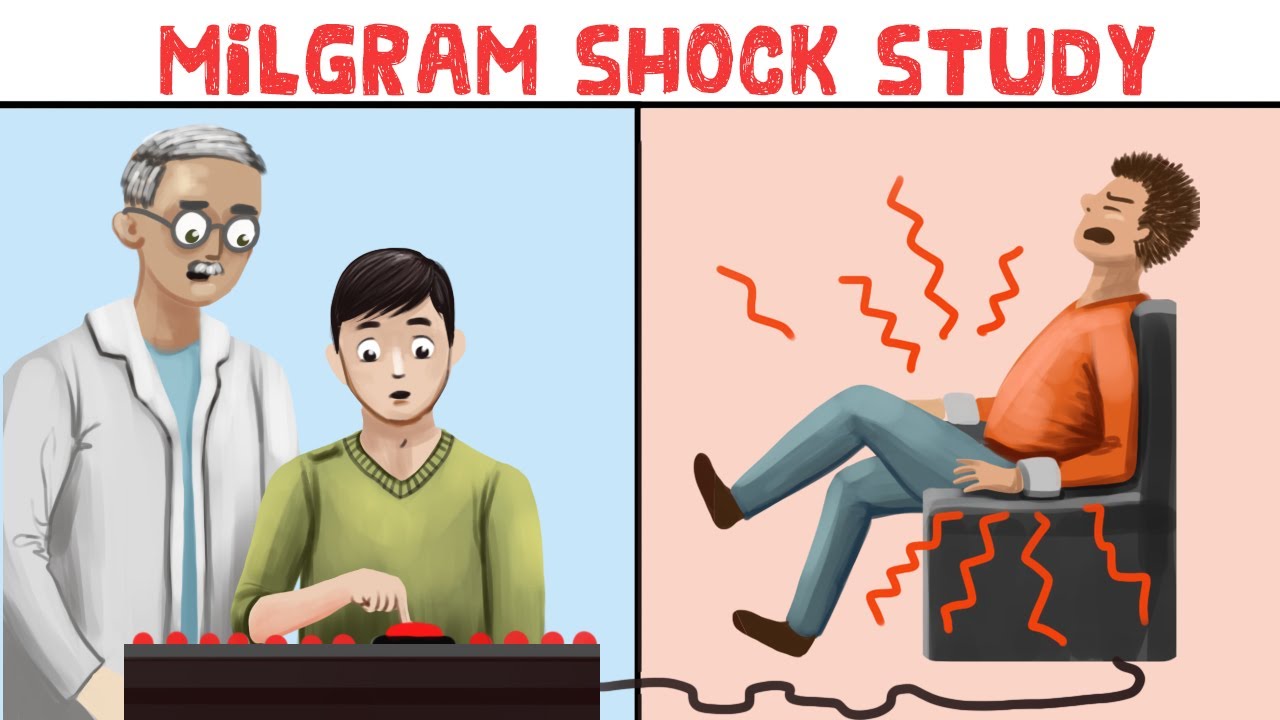

Question: Why do we follow orders, even when they seem wrong?

According to colleague Dan Ariely PhD,Obedience to Authority is a powerful force, making us do things we wouldn’t normally do. Think of the infamous Milgram experiment, where people shocked others because a guy in a lab coat told them to do so. It’s our brain’s way of outsourcing decision-making to someone else. While it can keep society orderly, it also explains why people sometimes follow questionable orders.

Milgram’s experiments posed the question: Would people obey orders, even if they believed doing so would harm another person?

Milgram’s findings suggested the answer was yes, they would. The experiments have long been controversial, both because of the startling findings and the ethical problems with the research. More recently, experts have re-examined the studies, suggesting that participants were often coerced into obeying and that at least some participants recognized that the other person was just pretending to be shocked. Such findings call into question the study’s validity and authenticity, but some replications suggest that people are surprisingly prone to obeying authority.

So, question authority [doctor, financial advisor, accountant, clergy, professor and lawyer, etc] – just not your GPS.

Posted on October 24, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Quote: “It looks like the global battle against inflation has largely been won, even if price pressures persist in some countries. In most countries, inflation is now hovering close to central bank targets…The decline in inflation without a global recession is a major achievement.”—IMF (CNN Business)

Spirit Airlines is back from the dead, soaring 46.67% on a Wall Street Journal report that it may end up merging with FrontierAirlines after all. Frontier Airlines rose 0.76% on the news.

AT&T climbed 4.65% after it beat earnings expectations in the third quarter, though it missed on revenue.

Starbucks fell hard late yesterday but recovered a bit this afternoon after new CEO Brian Niccol said the coffee chain is suspending its 2025 fiscal outlook. Shares rose 0.86% today.

Coca-Cola fizzled 2.07% after beating both top and bottom line expectations. The problem is that the only reason the soda giant performed well was because it raised prices, while demand for soft drinks slowed.

Enphase Energy plummeted 14.92% after the solar stock missed on both earnings and revenue expectations last quarter.

Boeing is a very familiar name in the “What’s down” section, and its latest earnings report did nothing to help. The manufacturing giant notched a $6 billion loss last quarter, and shares fell 1.76%.

The SPX fell 53.78 points (–0.92%) to 5,797.42; the Dow Jones Industrial Average® ($DJI) lost 409.94 points (–0.96%) to 42,514.95; and the NASDAQ Composite ($COMP) dropped 296.47 points (–1.60%) to 18,276.65.

The 10-year Treasury note yield gained four basis points to 4.24%.

Although some might view a budget as unnecessarily restrictive, sticking to a spending plan can be a useful tool in enhancing the wealth of a medical practice. So, I will emphasize keys to smart budgeting and how to track spending and savings in these tough economic times.

There is an aphorism that suggests, “Money cannot buy happiness.” Well, this may be true enough but there is also a corollary that states, “Having a little sure reduces the unhappiness.”

Unfortunately, today there is more than a little financial unhappiness in all medical specialties. The challenges range from the commoditization of medicine, aging demographics, Medicare reimbursement cutbacks and increased competition to floundering equity markets, the home mortgage crisis, the squeeze on credit and declines in the value of a practice. Few doctors seem immune to this “perfect storm” of economic woes.

Far too many physicians are hurting and it is not limited to above-average earning professionals. However, one can strive to reduce the pain by following some basic budgeting principles. By adhering to these principles, physicians can eliminate the “too many days at the end of the month” syndrome and instead develop a foundation for building real wealth and security, even in difficult economic climates like we face today.

There are three major budget types. A flexible budget is an expenditure cap that adjusts for changes in the volume of expense items. A fixed budget does not. Advancing to the next level of rigor, a zero-based budget starts with essential expenses and adds items until the money is gone. Regardless of type, budgets can be extremely effective if one uses them at home or the office in order to spot money troubles before they develop.

For the purpose of wealth building, doctors may think of this budget as a quantitative expression of an action plan. It is an integral part of the overall cost-control process for the individual, his or her family unit or one’s medical practice.

Preparing a net income statement (lifestyle cash flow budget) is often difficult because many doctors perceive it as punitive. Most doctors do not live a disciplined spending lifestyle and they view a budget as a compromise to it. However, a cash flow budget is designed to provide comfort when there is surplus income that can be diverted for other future needs. For example, if you treat retirement savings as just another periodic bill, you are more likely to save for it.

You may construct a personal cash budget by recording each cash receipt and cash disbursement on a spreadsheet. Only the date, amount and a brief description of the transaction are necessary. The cash budget is a simple tool that even doctors who lack accounting acumen can use. Since it is possible to track the cash-in and cash-out in the same format used for a standard check register, most doctors find that the process takes very little time. Such a budget will provide a helpful look at how well you are staying within available resources for a given period.

We then continue with an analysis of your operating checkbook and a review of various source documents such as one’s tax return, credit card statements, pay stubs and insurance policies. A typical statement will show all cash transactions that occur within one year. It is helpful to establish a monthly equivalent to all items of income and expense. For the purposes of getting started, note items of income and expense by the frequency you are accustomed to receiving or spending them.

What You Should Know About The ‘Action Plan’ Cash Budget

For a medical office, the first operations budget item might be salary for the doctor and staff. Operating assets and other big ticket items come next. Some of our doctors/clients review their office P&L statements monthly, line by line, in an effort to reduce expenses. Then they add back those discretionary business expenses they have some control over.

Now, do you still run out of money before the end of the month? If so, you had better cut back on entertainment, eating dinner out or that fancy, new but unproven piece of medical equipment. This sounds draconian until you remind yourself that your choice is either: live frugally later or live a simpler lifestyle now and invest the difference.

As a young doctor, it may be a difficult trade-off. By mid-life, however, you are staring retirement in the face. That is why the action plan depends on your actions concerning monetary scarcity, a plan that one can implement and measure using simple benchmarks or budgeting ratios. By using these statistics, perhaps on an annual basis, the doctor can spot problems, correct them and continue planning actively toward stated goals like building long-term wealth.

Useful Calculations To Assess Your Budgeting Success

In the past, generic budgeting ratios would emphasize not spending more than 15 to 20 percent of your net salary on food or 8 percent on medical care. Now these estimates have given way to more rigorous numbers. Personal budget ratios, much like medical practice financial ratios, represent comparable benchmarks for parameters such as debt, income growth and net worth. Although these ratios are still broad, the following represent some useful personal budgeting ratios for physicians.

• Basic liquidity ratio = liquid assets / average monthly expenses. Cash-on-hand should approach 12 to 24 months or more in the case of a doctor employed by a financially insecure HMO or fragile medical group practice. Yes, chances are you have heard of the standard notion of setting enough cash aside to cover three months in a rainy day scenario. However, we have decried this older laymen standard for many years in our textbooks, white papers and speaking engagements as being wholly insufficient for the competitively unstable environment of modern healthcare.

• Debt to assets ratio = total debt / total assets. This percentage is high initially but should decrease with age as the doctor approaches a debt-free existence

• Debt to gross income ratio = annual debt repayments / annual gross income. This represents the adequacy of current income for existing debt repayments. Doctors should try to keep this below 20 to 25 percent.

• Debt service ratio = annual debt repayment / annual take-home pay. Physicians should aim to keep this ratio below 25 to 30 percent or face difficulty paying down debt.

• Investment assets to net worth ratio = investment assets / net worth. This budget ratio should increase over time as retirement approaches.

• Savings to income ratio = savings / annual income. This ratio should also increase over time as one retires major obligations like medical school debt, a practice loan or a home mortgage.

• Real growth ratio = (income this year – income last year) / (income last year – inflation rate). This budget ratio should grow faster than the core rate of inflation.

• Growth of net worth ratio = (net worth this year – net worth last year) / net worth last year – inflation rate). Again, this budgeting ratio should stay ahead of inflation.

In other words, these ratios will help answer the question: “How am I doing?”

Pearls For Sticking To A Budget

Far from the burden that most doctors consider it to be, budgeting in one form or another is probably one of the greatest tools for building wealth. However, it is also one of the greatest weaknesses among physicians who tend to live a certain lifestyle.

In fact, we have found that less than one in 10 medical professionals have a personal budget. Fear, or a lack of knowledge, is a major cause of procrastination. Fortunately, the following guidelines assist in reversing this microeconomic disaster.

1. Set reasonable goals and estimate annual income. Do not keep large amounts of cash at home or office. Deposit it in an FDIC insured money-market account for safety. Do not deposit it in a money market mutual fund with net asset value (NAV) that may “break the buck” and fall below the one-dollar level. Track actual bills and expenses.

2. Do not pay bills early, do not have more taxes withheld from your salary than needed and develop spending estimates to pay fixed expenses first. Fixed expenses are usually contractual and usually include housing, utilities, food, Social Security, medical, debt repayments, homeowner’s or renter’s insurance, auto, life and disability insurance, etc. Reduce fixed expenses when possible. Ultimately, all expenses get paid and become variable in the long run.

3. Make it a priority to reduce variable expenses. Variable expenses are not contractual and may include clothing, education, recreational, travel, vacation, gas, cable TV, entertainment, gifts, furnishings, savings, investments, etc. Trim variable expenses by 5 to 20 percent.

4. Use “carve-outs or “set-asides” for big ticket items and differentiate true wants from frivolous needs.

5. Calculate both income and expenses as a percentage of your total budget. Determine if there is a better way to allocate resources. Review the budget on a monthly basis to notice any variance. Determine if the variance was avoidable, unavoidable or a result of inaccurate assumptions. Take corrective action as needed.

6. Know the difference between saving and investing. Savers tend to be risk adverse while investors understand risk and take steps to mitigate it. Watch mutual fund commissions and investment advisory fees, which cut into return-rates. Keep investments simple and diversified (stocks, bonds, cash, index, no-load mutual and exchange traded funds, etc.).

Sooner or later, despite the best of budgeting intentions, something will go awry. A doctor will be terminated or may be the victim of a reduction-in-force (RIF) because of cost containment initiatives.4 A medical practice partnership may dissolve or a local hospital or surgery center may close, hurting your practice and livelihood. Someone may file a malpractice lawsuit against you, a working spouse may be laid off or you may get divorced. Regardless of the cause, budgeting crisis management encompasses two different perspectives: awareness and execution.

First, if you become aware that you may lose your job, the following proactive steps will be helpful to your budget and overall financial condition.

• Decrease retirement contributions to the required minimum for company/practice match. • Place retirement contribution differences in an after-tax emergency fund. • Eliminate unnecessary payroll deductions and deposit the difference to cash. • Replace group term life insurance with personal term or universal life insurance. • Take your old group term life insurance policy with you if possible. • Establish a home equity line of credit to verify employment. • Borrow against your pension plan only as a last resort.

If you have lost your job or your salary has been depressed, negotiate your departure and get an attorney if you believe you lost your position through breach of contract or discrimination. Then execute the following steps to recalculate your budget and boost your wealth rebuilding activities.

• Prioritize fixed monthly bills in the following order: rent or mortgage; car payments; utility bills; minimum credit card payments; and restructured long-term debt.

• Consider liquidating assets to pay off debts in this order: emergency fund, checking accounts, investment accounts or assets held in your children’s names.

• Review insurance coverage and increase deductibles on homeowner’s and automobile insurance for needed cash.

• Then sell appreciated stocks or mutual funds; personal valuables such as furnishings, jewelry and real estate; and finally, assets not in pension or annuities if necessary.

• Keep or rollover any lump sum pension or savings plan distribution directly to a similar savings plan at your new employer, if possible, when you get rehired.

• Apply for unemployment insurance.

• Review your medical insurance and COBRA coverage after a “qualifying event” such as job loss, firing or even after quitting. It is a bit expensive due to a 2 percent administrative fee surcharge but this may be well worth it for those with preexisting conditions or who are otherwise difficult to insure. One may continue COBRA for up to 18 months.

• Consider a high deductible Health Savings Account (HSA), which allows tax-deferred dollars like a medical IRA, for a variety of costs not normally covered under traditional heath insurance plans. Self-employed doctors deduct both the cost of the premiums and the amount contributed to the HSA. Unused funds roll over until the age of 59½, when one can use the money as a supplemental retirement benefit.

• Eliminate unnecessary variable, charitable and/or discretionary expenses, and become very frugal.

Final Notes

The behavioral psychologist, Gene Schmuckler, PhD, MBA, sometimes asks exasperated doctors to recall the story of the old man who spent a day watching his physician son treating HMO patients in the office. The doctor had been working at his usual feverish pace all morning. Although he was working hard, he bitterly complained to his dad that he was not making as much money as he used to make. Finally, the old man interrupted him and said, “Son, why don’t you just treat the sick patients?” The doctor-son looked at his father with an annoyed expression and responded, “Dad, can’t you see, I do not have time to treat just the sick ones.”

Always remember to add a bit of emotional sanity into your budgeting and economic endeavors.

Regardless of one’s age or lifestyle, the insightful doctor realizes that it is never too late to take control of a lost financial destiny through prudent wealth building activities. Personal and practice budgeting is always a good way to start the journey.

NOTE: Dr. Marcinko is a former Certified Financial Planner and current Certified Medical Planner™. He has been a medical management advisor for more than a decade. He is the CEO of http://www.MarcinkoAssociates.com

The authors acknowledge the assistance of Mackenzie H. Marcinko PhD in the preparation of this article.

Posted on October 20, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Yep – Even the Smart Folks!

By Lon Jefferies MBA CMP® CFP®

Dr. David Edward Marcinko MBA MEd CMP®

In the Business Insider, Mandi Woodruff describes nine mental blocks that cause smart people to do dumb things. Review the list and itemize the factors that have negatively impacted your finances.

The Factors

Anchoring happens when we place too much emphasis on the first piece of information we receive regarding a given subject. For instance, when shopping for a wedding ring a salesman might tell us to spend three months’ salary. After hearing this, we may feel like we are doing something wrong if we stray from this advice, even though the guideline provided may cause us to spend more than we can afford.

Myopia (or nearsightedness) makes it hard for us to imagine what our lives might be like in the future. For example, because we are young, healthy, and in our prime earning years now, it may be hard for us to picture what life will be like when our health depletes and we know longer have the earnings necessary to support our standard of living. This short-sightedness makes it hard to save adequately when we are young, when saving does the most good.

Gambler’s fallacy occurs when we subconsciously believe we can use past events to predict the future. It is common for the hottest sector during one calendar year to attract the most investors the following year. Of course, just because an investment did well last year doesn’t mean it will continue to do well this year. In fact, it is more likely to lag the market.

Avoidance is simply procrastination. Even though you may only have the opportunity to adjust your health care plan through your employer once per year, researching alternative health plans is too much work and too boring for us to get around to it. Consequently, we stick with a plan that may not be best for us.

Confirmation bias causes us to place more emphasis on information that supports the opinion we already have. Consequently, we tend to ignore or downplay opinions that don’t mirror our own, leading us to make uninformed decisions.

NOTE: An interesting example of the confirmation bias is the case of David Rosenberg, who is one of the most well-known perpetual bears on Wall Street. In October, Mr. Rosenberg’s analysis forced him to warm to the current investment environment. His fans and followers, rather than appreciating his research and ability to adjust to new information, criticized him for changing his opinion.

As it turned out Mr. Rosenberg had fans not because of his expert analysis, but because he added intellectual heft to his followers pessimism and quasi-political desire for the system to collapse. Their view was that things were in permanent decline and his analysis, charts, and voice added respectability to their pre-existing bias. Mr. Rosenberg has now lost his fan base not because he was wrong for the last four years, but because he changed his mind.

Loss aversion affected many investors during the crash of 2008. During the crash, many people decided they couldn’t afford to lose more and sold their investments. Of course, this caused the investors to sell at market troughs and miss the quick, dramatic recovery.

Overconfident investing happens when we believe we can out-smart other investors via market timing or through quick, frequent trading. Data convincingly shows that people who trade most often underperform the market by a significant margin over time.

Mental accounting takes place when we assign different values to money depending on where we get it from. For instance, even though we may have an aggressive saving goal for the year, it is likely easier for us to save money that we worked for than money that was given to us as a gift.

Herd mentality makes it very hard for humans to not take action when everyone around us does. For example, we may hear stories of people making significant profits buying, fixing up, and flipping homes and have the desire to get in on the action, even though we have no experience in real estate.

Assessment

The good news is that being aware of these tendencies can help us avoid mistakes. We’ll never be perfect, but avoiding detrimental decisions based on mental prejudices can give us an advantage in our financial and retirement planning efforts.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

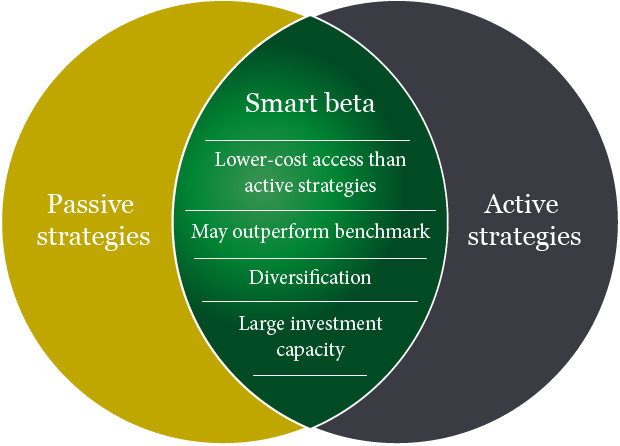

Offering a blend of active and passive styles of management, a smart beta portfolio is low cost due to the systematic nature of its core philosophy – achieving efficiency by way of tracking an underlying index (e.g., MSCI World Ex US). Combining with optimization techniques traditionally used by active managers, the strategy aims at risk/return potentials that are more attractive than a plain vanilla active or passive product.

Originally theorized by Harry Markowitz in his work on Modern Portfolio Theory (MPT), smart beta is a response to a question that forms the basis of MPT – how to best construct the optimally diversified portfolio. Smart beta answers this by allowing a portfolio to expand on the efficient frontier (post-cost) of active and passive. As a typical investor owns both the active and index fund, most would benefit from adding smart beta exposure to their portfolio in addition to their existing allocations.

Assessment: The smart beta approach is an arguably perfect intersection between traditional value investing and the efficient market hypothesis. But, is it worth the cost?

Posted on October 20, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The Gambler’s Fallacy occurs when we subconsciously believe we can use past events to predict the future. It is also called the Monte Carlo Fallacy, after the Casino de Monte-Carlo in Monaco where it was observed in 1913

For example, it is common for the hottest sector during one calendar year to attract the most investors the following year.

Of course, just because an investment did well last year doesn’t mean it will continue to do well this year. In fact, it is more likely to lag the market.

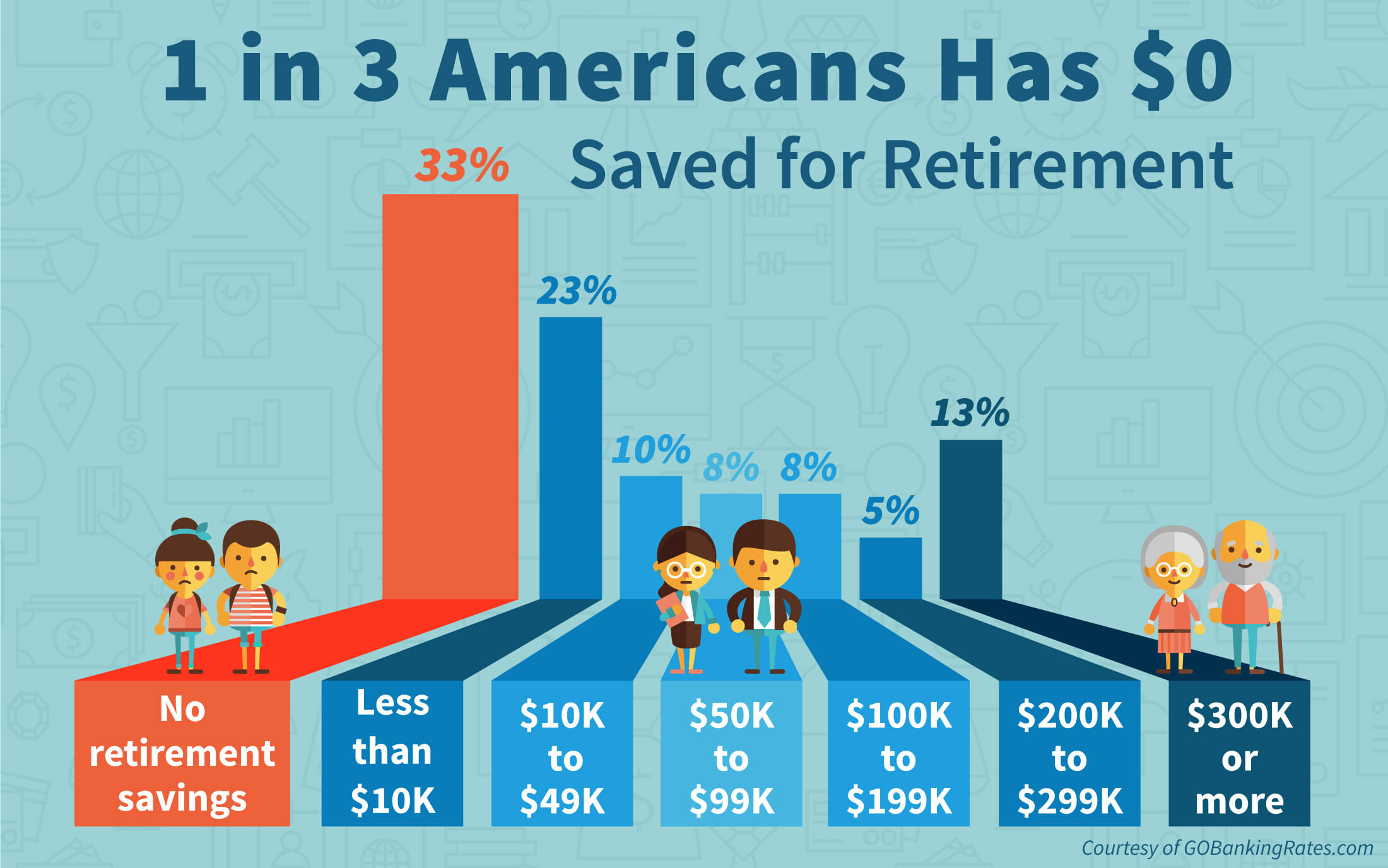

According to the National Institute on Retirement Security, almost 40 million households have no retirement savings at all. The Employee Benefit Research Institute (EBRI) estimates in its 2019 Retirement Security Projection Model that America’s current retirement savings deficit is $3.8 trillion.

What does that mean? Well, the EBRI report aggregates the savings deficit of all U.S. households headed by someone between the ages of 35 and 64, inclusive. In total, those households have $3.8 trillion fewer dollars in savings than they should have for retirement.

For more recent data, Fidelity Investments reported that in the third quarter of 2022 the average account balance for an IRA was $101,900. Employees with a 401(k) averaged $97,200, while those with a 403(b) had $87,400.

Fidelity also estimated that “an average retired couple age 65 in 2022 may need approximately $315,000 saved (after tax) to cover health care expenses in retirement.” Keeping in mind that more Americans are also living longer than ever before, they will face more challenges to cover medical expenses in retirement.

Posted on October 18, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Chip stocks recovered lost ground today thanks to a strong earnings report from TSMC (more on that below). Nvidia led the group higher, rising 0.89% to yet another new all-time high.

Blackstone rose 6.30% to a new record high after the world’s largest alternative asset manager reported an excellent quarter.

Expedia popped 4.75% after a report by the Financial Times revealed that Uber had explored an acquisition of the travel site. Expedia shareholders cheered the news, while Uber shares sank 2.45%.

Stocks Down

Robinhood fell 2.27% after announcing its new Legend trading platform geared specifically toward advanced traders.

Lucid Group plummeted 17.99% on the news that the EV automaker is offering over 262 million shares of its common stock in an attempt to raise funds.

CSX dropped 6.71% after missing both top- and bottom-line estimates last quarter thanks in no small part to hurricanes Helene and Milton.

Health insurance stocks took a beating today due to a not-great earnings report from ElevanceHealth (more on that below, too). Centene Corp. fell 9.09%, while Molina Healthcare tumbled 12.55%.

The S&P 500® index (SPX) slipped 1.00point (–0.02%) to 5,841.47; the $DJI added 161.35 points (0.37%) to 43,239.05; and the NASDAQ Composite®($COMP) rose 6.53 points (0.04%) to 18,373.61.

The 10-year Treasury note yield (TNX) climbed eight basis points to 4.1%.

The CBOE Volatility Index® (VIX) sank to 18.97 by late Thursday, a two-week low.

The average amount owed on “upside down” auto loans, in which the balance is more than the car is worth, hit a record high of $6,458 in the third quarter, according to Edmunds, a site that helps consumers research and buy cars

Financial planning as a concept has been around for a long time, but not as we know it today. When Loren Dunton set up the Society for Financial Counseling Ethics in 1969, or when the first graduating class of the College of Financial Planning graduated in 1973, financial planning was very different. It was centered around selling limited partnerships, which came to end with the Tax Reform Act of 1986.

However, financial planning re-emerged — all thanks to Richard Averitt III. The certified financial planner gave new meaning to financial planning, this time with a focus on who the client is and what their needs are. This approach was purely methodological in nature.

Soon after, financial planning picked up again. According to the Certified Financial Planner (C.F.P.) Board of Standards in Denver, today, there are more than 94,000 C.F.P.s worldwide, including over 48,000 in the U.S. Additionally, there are also organizations that have been set up for C.F.P.s, such as the Financial Planning Association (FPA), which has approximately 22,000 members.

And, don’t forget the emerging Certified Medical Planner™ professional fiduciary designation for physicians, dentists, nurses and allied healthcare clients.

Financial planning, as we know it now, includes investing, tax planning, retirement planning, and basically other ways to get your finances in order and create mindful budgets to ensure a safe and secure future. Getting a step ahead of your spending and finances is beneficial in the long run and Financial Planning Month in October is the perfect time to do that.

Posted on October 17, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Authors of the seminal textbook Why Nations Fail, Daron Acemoglu, James Robinson, and former International Monetary Fund chief economist Simon Johnson will split the roughly $1 million cash prize for their research, which found a link between a country’s prosperity and the institutions it established during European colonization.

Places developed either “inclusive” or “extractive” institutions based on population density. The former allowed for inclusive governance (i.e., democracy), while the latter extracted resources to benefit a small group of elites.

Countries that developed inclusive institutions have experienced long-term prosperity; those with exclusive institutions haven’t. “Broadly speaking, the work that we have done favors democracy,” Acemoglu said.

Eample: In the twin cities of Nogales, on the US-Mexico border, the north and south parts of the transborder city have the same climate and the same resources, but the section in the US is far richer because of the country’s institutions, according to the researchers.

Critics. Some academics argue the Nobel winners’ premise ignores the effects of culture on prosperity. Others point to an irrefutable counterexample: China continues to experience explosive growth despite having an autocratic government.

Posted on October 15, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters &The Medicare Team

Medicare open enrollment—which runs from October 15th through December 7th this year—is your chance to check in on your Medicare plan and, if needed, change it.

***

***

Mark your calendars — Medicare Open Enrollment starts October 15th! Did you know new benefits are coming to Medicare drug coverage next year?

Also starting next year, you can choose to participate in a program that spreads your out-of-pocket drug costs across the calendar year, instead of paying all at once at the pharmacy. It’s called the Medicare Prescription Payment Plan — and you can opt in with your plan throughout the 2025 plan year. Contact your plan for more details.

Remember, Medicare plans can change from one year to the next, and so can your health needs. Preview and compare all your health and drug options and see if you can save!

According to Wikipedia, Front Running, also known as Tailgating, is the prohibited practice of entering into an equity (stock) trade, option, futures contract, derivative, or security-based swap to capitalize on advance, nonpublic knowledge of a large pending transaction that will influence the price of the underlying security.

Front running is considered a form of market manipulation in many markets. Cases typically involve individual brokers or brokerage firms trading stock in and out of undisclosed, un-monitored accounts of relatives or confederates. Institutional and individual investors may also commit a front running violation when they are privy to inside information. A front running firm either buys for its own account before filling customer buy orders that drive up the price, or sells for its own account before filling customer sell orders that drive down the price.

Front running is prohibited since the front-runner profits from nonpublic information, at the expense of its own customers, the block trade, or the public market.

Scandals

In 2003, several hedge fund and mutual fund companies became embroiled in an illegal late trading scandal made public by a complaint against Bank of America brought by New York Attorney General Eliot Spitzer. A resulting U.S. Securities and Exchange Commission investigation into allegations of front-running activity implicated Edward D. Jones & Co., Inc., Goldman Sachs, Morgan Stanley, Strong Mutual Funds, Putnam Investments, Invesco, and Prudential Securities.

Following interviews in 2012 and 2013, the FBI said front running had resulted in profits of $50 million to $100 million for the bank. Wall Street traders may have manipulated a key derivatives market by front running Fannie Mae and Freddie Mac.

Term Origins

The terms originate from the era when stock market trades were executed via paper carried by hand between trading desks. The routine business of hand-carrying client orders between desks would normally proceed at a walking pace, but a broker could literally run in front of the walking traffic to reach the desk and execute his own personal account order immediately before a large client order.

Likewise, a broker could tail behind the person carrying a large client order to be the first to execute immediately after. Such actions amount to a type of insider trading, since they involve non-public knowledge of upcoming trades, and the broker privately exploits this information by controlling the sequence of those trades to favor a personal position.

Assessment

So, was front-running implicated in the market drop today? OR, a technical correction or Panic selling? Any thoughts.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements.

According to colleague Dan Ariely PhD, a Zero Sum Bias [ZSB] is the mistaken belief that one person’s gain is another’s loss. It’s like thinking the world is a giant pie with only so many slices. This mindset fuels competition and jealousy, making us forget that collaboration can create more pie. It’s why we sometimes root against others instead of working together.

Question: Is the stock market a zero-sum game? You frequently hear media refer to games and markets as zero-sum games.

Answer: Well, yes, we define the stock market as a zero-sum game, both in the short and in the long term, although it technically is incorrect. A zero-sum game is where one person’s gain is another person’s loss – thus there is no wealth created and the overall benefit is zero. This doesn’t apply to stocks, but it’s a zero-sum game in relation to a stock market benchmark.

For example, short-term trading in stocks is theoretically not a zero-sum game, and neither is long-term investing. But short-term trading is close to a zero-sum game, and long-term investing is a zero-sum game if we use a broad index as a benchmark.

Essentially, in other words, the stock market functions as an expansive network of zero-sum transactions; each trade engages a buyer and a seller–their perspectives on a security’s future value contrasting. These opposing views propel market prices: they mirror not only risk transfer but also potential reward—a dynamic process indeed! Traders and investors must grasp the crucial zero-sum aspect; it underscores trading’s inherent competitiveness. Effectively anticipating market trends and actions from other participants: therein lies success in this environment.

Medical Executive-Post Publisher-in-Chief, Dr. David Edward Marcinko MBA CMP™, and financial planner Paul Larson CFP™, were interviewed by Sharon Fitzgerald for Medical News, Inc. Here is a reprint of that interview.

Doctors Squeezed from both Ends

Physicians today “are getting squeezed from both ends” when it comes to their finances, according Paul Larson, president of Larson Financial Group. On one end, collections and reimbursements are down; on the other end, taxes are up. That’s why financial planning, including a far-sighted strategy for retirement, is a necessity.

Larson Speaks

“We help these doctors function like a CEO and help them quarterback their plan,” said Larson, a Certified Financial Planner™ whose company serves thousands of physicians and dentists exclusively. Headquartered in St. Louis, Larson Financial boasts 19 locations.

Larson launched his company after working with a few physicians and recognizing that these clients face unique financial challenges and yet have exceptional opportunities, as well.

What makes medical practitioners unique? One thing, Larson said, is because they start their jobs much later in life than most people. Physicians wrap up residency or fellowship, on average, at the age of 32 or even older. “The delayed start really changes how much money they need to be saving to accomplish these goals like retirement or college for their kids,” he said.

Another thing that puts physicians in a unique category is that most begin their careers with a student-loan debt of $175,000 or more. Larson said that there’s “an emotional component” to debt, and many physicians want to wipe that slate clean before they begin retirement saving.

Larson also said doctors are unique because they are a lawsuit target – and he wasn’t talking about medical malpractice suits. “You can amass wealth as a doctor, get sued in five years and then lose everything that you worked so hard to save,” he said. He shared the story of a client who was in a fender-bender and got out of his car wearing his white lab coat. “It was bad,” Larson said, and the suit has dogged the client for years.

The Three Mistake of Retirement Planning

Larson said he consistently sees physicians making three mistakes that may put a comfortable retirement at risk.

The first is assuming that funding a retirement plan, such as a 401(k), is sufficient. It’s not. “There’s no way possible for you to save enough money that way to get to that goal,” he said. That’s primarily due to limits imposed by the Internal Revenue Service, which allows a maximum contribution of $49,000 annually if self-employed and just $16,500 annually until the age of 50. He recommends that physicians throughout their career sock away 20 percent of gross income in vehicles outside of their retirement plan.

The second common mistake is making investments that are inefficient from a tax perspective. In particular, real estate or bond investments in a taxable account prompt capital gains with each dividend, and that’s no way to make money, he said.

The third mistake, and it’s a big one, is paying too much to have their money managed. A stockbroker, for example, takes a fee for buying mutual funds and then the likes of Fidelity or Janus tacks on an internal fee as well. “It’s like driving a boat with an anchor hanging off the back,” Larson said.

Marcinko Speaks

Dr. David E. Marcinko MBA MEd CPHQ, a physician and [former] certified financial planner] and founder of the more specific program for physician-focused fiduciary financial advisors and consultants www.CertifiedMedicalPlanner.org, sees another common mistake that wreaks havoc with a physician’s retirement plans – divorce.

He said clients come to him “looking to invest in the next Google or Facebook, and yet they will get divorced two or three times, and they’ll be whacked 50 percent of their net income each time. It just doesn’t make sense.”

Marcinko practiced medicine for 16 years until about 10 years ago, when he sold his practice and ambulatory surgical center to a public company, re-schooled and retired. Then, his second career in financial planning and investment advising began. “I’m a doctor who went to business school about 20 years ago, before it was in fashion. Much to my mother’s chagrin, by the way,” he quipped. Marcinko has written 27 books about practice management, hospital administration and business, physician finances, risk management, retirement planning and practice succession. He’s the founder of the Georgia-based Institute of Medical Business Advisors Inc.

Succession Planning for Doctors

Succession planning, Marcinko said, ideally should begin five years before retirement – and even earlier if possible. When assisting a client with succession, Marcinko examines two to three years of financial statements, balance sheets, cash-flow statements, statements of earnings, and profit and loss statements, yet he said “the $50,000 question” remains: How does a doctor find someone suited to take over his or her life’s work? “We are pretty much dead-set against the practice broker, the third-party intermediary, and are highly in favor of the one-on-one mentor philosophy,” Marcinko explained.

“There is more than enough opportunity to befriend or mentor several medical students or interns or residents or fellows that you might feel akin to, and then develop that relationship over the years.” He said third-party brokers “are like real-estate agents, they want to make the sale”; thus, they aren’t as concerned with finding a match that will ensure a smooth transition.

The only problem with the mentoring strategy, Marcinko acknowledged, is that mentoring takes time, and that’s a commodity most physicians have too little of. Nonetheless, succession is too important not to invest the time necessary to ensure it goes off without a hitch.

Times are different today because the economy doesn’t allow physicians to gradually bow out of a practice. “My overhead doesn’t go down if I go part-time. SO, if I want to sell my practice for a premium price, I need to keep the numbers up,” he noted.

Assessment

Dr. Marcinko’s retirement investment advice – and it’s the advice he gives to anyone – is to invest 15-20 percent of your income in an Vanguard indexed mutual fund or diversified ETF for the next 30-50 years. “We all want to make it more complicated than it really is, don’t we?” he said.

QUESTION: What makes a physician moving toward retirement different from most others employees or professionals? Marcinko’s answer was simple: “They probably had a better shot in life to have a successful retirement, and if they don’t make it, shame on them. That’s the difference.”

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on October 12, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Fastenal climbed 9.76% after the construction and hardware equipment manufacturer posted stronger-than-expected revenue last quarter.

Symbotic popped 8.80% on news of a deal with the Walmart division of Mexico and Central America for its AI-powered robots to help with warehouse automation.

Affirm soared 12.07% after Wells Fargo analysts upgraded the buy now, pay later company thanks to its partnership with Apple Pay.

Ferrari raced 3.54% higher thanks to an upgrade from JPMorgan analysts, citing the carmaker’s EV division and hopes of a Chinese market recovery.

Stocks down

Stellantis continued to tumble today, falling another 2.22% after the carmaker announced its CEO will step down in early 2026.

A.O. Smith probably doesn’t ring a bell, but there’s a good chance they made the water heater in your basement. Unfortunately, they’re not selling too many these days, and shares sank 6.25% after the company cut its full-year outlook.

The SPX rose 34.98 points (0.61%) to 5,815.03 to end the week up 1.11%; the $DJI added 409.74 points (0.97%) to 42,863.86 to end the week up 1.21%; and the $COMP gained 60.88 points (0.33%) to 18,342.94 to end the week up 1.13%.

The 10-year Treasury note yield (TNX) fell two basis points to 4.07% but rose nine basis points this week.

The CBOE Volatility Index® (VIX) slipped to 20.41, still up slightly for the week.

Fidelity Investments has notified 77,099 people that their personal information was stolen in an August data breach. he mega asset manager has not disclosed what data the digital crooks nabbed, but assured customers that the security snafu “did not involve any access to your Fidelity account(s).” But hey, no worries, the firm claimed no evidence of data misuse.

Not everyone believes in the efficient market. Numerous researchers over the previous decades have found stock market anomalies that indicate a contradiction with the hypothesis. The search for anomalies is effectively the hunt for market patterns that can be utilized to outperform passive strategies.

[White Swan of the EMH]

Such stock market anomalies that have been proven to go against the findings of the EMH theory include:

Low Price to Book Effect

January Effect

The Size Effect

Insider Transaction Effect

The Value Line Effect

The Anomalies

All the above anomalies have been proven over time to outperform the market. For example, the first anomaly listed above is the Low Price to Book Effect. The first and most discussed study on the performance of low price to book value stocks was by Dr. Eugene Fama and Dr. Kenneth R. French. The study covered the time period from 1963-1990 and included nearly all the stocks on the NYSE, AMEX and NASDAQ. The stocks were divided into ten subgroups by book/market and were re-ranked annually.

In the study, Fama and French found that the lowest book/market stocks outperformed the highest book/market stocks by a substantial margin (21.4 percent vs. 8 percent). Remarkably, as they examined each upward decile, performance for that decile was below that of the higher book value decile. Fama and French also ordered the deciles by beta (measure of systematic risk) and found that the stocks with the lowest book value also had the lowest risk.

What is Value?

Today, most researchers now deem that “value” represents a hazard feature that investors are compensated for over time. The theory being that value stocks trading at very low price book ratios are inherently risky, thus investors are simply compensated with higher returns in exchange for taking the risk of investing in these value stocks.

The Fama and French research has been confirmed through several additional studies. In a Forbes Magazine 5/6/96 column titled “Ben Graham was right–again,” author David Dreman published his data from the largest 1500 stocks on Compustat for the 25 years ending 1994. He found that the lowest 20 percent of price/book stocks appreciably outperformed the market.

***

[Ex-Cathedra or Black Swan Event]

Assessment

One item a medical professional should be aware of is the strong paradox of the efficient market theory. If each investor believes the stock market were efficient, then all investors would give up analyzing and forecasting. All investors would then accept passive management and invest in index funds.

But, if this were to happen, the market would no longer be efficient because no one would be scrutinizing the markets. In actuality, the efficient market hypothesis actually depends on active investors attempting to outperform the market through diligent research

Channel Surfing the ME-P

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Timothy J. McIntosh is Chief Investment Officer and founder of SIPCO. As chairman of the firm’s investment committee, he oversees all aspects of major client accounts and serves as lead portfolio manager for the firm’s equity and bond portfolios. Mr. McIntosh was a Professor of Finance at Eckerd College from 1998 to 2008. He is the author of The Bear Market Survival Guide and the The Sector Strategist. He is featured in publications like the Wall Street Journal, New York Times, USA Today, Investment Advisor, Fortune, MD News, Tampa Doctor’s Life, and The St. Petersburg Times. He has been recognized as a Five Star Wealth Manager in Texas Monthly magazine; and continuously named as Medical Economics’ “Best Financial Advisors for Physicians since 2004. And, he is a contributor to SeekingAlpha.com., a premier website of investment opinion. Mr. McIntosh earned a Bachelor of Science Degree in Economics from Florida State University; Master of Business Administration (M.B.A) degree from the University of Sarasota; Master of Public Health Degree (M.P.H) from the University of South Florida and is a CERTIFIED FINANCIAL PLANNER® practitioner. His previous experience includes employment with Blue Cross/Blue Shield of Florida, Enterprise Leasing Company, and the United States Army Military Intelligence.

Conclusion

So, what about the “January Effect for 2025“?

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on October 11, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

With the annual enrollment period for Medicare Advantage (MA) plans slated to open in less than two months, many MA plans are cutting benefits and provider payments, while approving fewer claims. Further, after a decade of accelerated growth in the MA market, several MA plan executives have announced MA market exits and decreases in membership for the upcoming plan year.

This Health Capital Topics article discusses recently announced MA market exits, the reasons for those exits, and the current environment in which MA plans are operating. (Read more...)

Posted on October 7, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters ***

***

Markets: Stocks soared last week despite concerns about geopolitics after new government data showed companies were hiring in full force last month.

Some other highlights:

The unemployment rate fell 0.1 percentage point to 4.1%.

The underemployment rate (for people working part-time but who want to be working more and so-called “discouraged workers”) also dropped for the first time in about a year.

The biggest employment gains last month came from sectors like hospitality and construction, and hourly pay inched up about 0.4%, which if you zoom out, means wages are up 4% compared to a year ago.

Plus, August’s revised jobs report showed the US actually created 159,000 jobs, up from 142,000 initially reported last month.

Posted on October 7, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The FDA just approved FluMist from AstraZeneca for self- or caregiver administration for the prevention of influenza virus subtypes A and B.

Plus, August’s revised jobs report showed the US actually created 159,000 jobs, up from 142,000 initially reported last month.

People in CA will have explicit rights to their own “neural data”—covering anything a person thinks or physically/emotionally feels—which is designed to prevent companies from gathering and selling that type of personal info

Posted on October 6, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Vitaliy Katsenelson, CFA

***

CABLE COMPANIES

CHTR, just like Comcast, showed only a very slight decline in broadband customers in the last quarter. Most of the decline came from the US government removing subsidies for rural customers. Overall, the business is doing very well.

I want to remind you that broadband is not a secularly challenged business, but an advantaged business that we believe will resume growth soon.

Cable companies continue to offer a great product on the market, which is actually improving in quality as I type this because they are upgrading their networks to be as fast as fiber. They should be done with their full network upgrade in a year or so.

Also, cable companies have shown that they are very good at attracting wireless customers from wireless carriers. (They have grown their wireless business by 25% in 2024). The more we analyzed this industry. the more bearish we became on AT&T and Verizon.

Though owning cable stocks has not been rewarding (I’m being very gentle to myself), the more research we’ve done into the industry, the more convinced we’ve become that once the dust settles, their market share will not decrease but likely increase. Fixed wireless has taken all the share it will take and will start donating share to cable companies as customers get frustrated with intermittency of the service and usage caps.

The industry is moving towards the bundle – one bill for broadband and wireless (and maybe TV service, though that has been marginalized by streamers). It’s a lot easier for cable companies to add wireless customers than for wireless companies to add wired broadband customers.

This point is paramount!

It costs very little for a cable company to add a wireless subscriber, as 80-90% of a subscriber’s data is traveling on Wi-Fi (i.e., the cable network is already there).

Meanwhile, the cost of building out broadband is pushing into uneconomical territory, for several reasons. First of all, all the low-hanging fruit has already been picked. It costs, let’s say, $50-100 thousand dollars to lay a mile of fiber, whether that covers one or a thousand homes. High-density areas already have cable or fiber service. With the latest upgrades the cable industry is doing, both their upload and download speeds are on par with fiber. Second, labor costs have gone up significantly over the last few years.

Verizon just announced buying Frontier Communications for $20 billion. Frontier has 2.2 million fiber subscribers. With this purchase, Verizon is paying $9,000 per fiber subscriber.

Let’s examine the economics of this transaction:

Frontier gets about $800 a year of revenues from these broadband customers (on a par with Charter and Comcast). Let’s say they achieve a 23% margin (Frontier is barely a profitable business, so I’m using Charter’s margins). Thus, each customer will generate $184 of profit for them. So Verizon is paying $9,000 for $184 of profit, and it will take Verizon 49 years to break even on this transaction.

As you can see, these economics make no sense. Verizon and AT&T are horrible at capital allocation, and this deal is a sign of supreme desperation. The market has been slow to see what we see in Charter and Comcast, and this is always our goal – we want the market to agree with us, later.

Our very conservative estimate of Charter’s 2028 free cash flow per share is $48-60. In this estimate we are assuming no customer growth in broadband and 2% price increases a year. At 13-15 times free cash flows, we get a price of around $630-900 in 2028. Charter is trading at about $320 as I write this.

We really like Charter’s management. We heard an anecdote about Charter CEO Chris Winfrey that warmed our soul. A week after he became CEO, Charter announced a huge, multibillion-dollar upgrade for its broadband network. This news sent the stock down 15%. (I wrote about it; we thought it was a great idea.) Anyway, someone met Chris at a party and told him, “That’s the right move, but very gutsy.” Chris said, “We build the company for our grandchildren.” This is what we want to see from our CEOs. They’re willing to sacrifice short-term profitability to improve the business’s moat.

Often, the idea of “creating shareholder value” is misunderstood. Paying employees poorly, abusing suppliers, and trying to rip off your customers is not going to create long-term (key term) shareholder value. It may bring short-term profits and boost the stock price, but it shortens the company’s growth runway and erodes its moat.

I don’t want to get off topic, but I’ve been thinking a lot about this. We’ve spent a lot of time studying the aircraft industry; our focus was Airbus, and thus we spent a lot of time looking at Boeing.

Boeing, under previous management, focused on “shareholder value creation.” It cut costs, laid off a lot of workers, including many quality control folks. Its “shareholder value creation” didn’t stop there; it willingly lied to regulators and took shortcuts in safety. Specifically, Boeing made critical design changes to its 737 MAX aircraft without fully informing regulators or pilots, and pushed for reduced pilot training requirements to save costs. These decisions directly contributed to two fatal crashes in 2018 and 2019, resulting in 346 deaths and the worldwide grounding of the 737 MAX for nearly two years.

Did its management actions maximize shareholder value? Well, it depends on the time frame. It boosted short-term earnings and drove the stock price higher. It may have made its CEO rich beyond belief.

But.

Over a longer time frame, these decisions have destroyed shareholder value. People used to say, “If it’s not Boeing, I’m not going.” Today, I become slightly more religious when I board a Boeing plane. The company has incurred over $20 billion in direct costs related to the 737 MAX crisis, including compensation to airlines and families of crash victims, and increased production costs.

This doesn’t account for the incalculable damage to Boeing’s reputation and loss of market share. It gave Airbus an opening to produce more planes and take market share, with Airbus surpassing Boeing in deliveries and orders in recent years, particularly in the crucial narrow-body market.

We want to own companies that aim to maximize long-term shareholder value by treating all their stakeholders fairly. We want our companies to play the infinite game. What does “fairly” mean in this context? I’ll borrow from US Supreme Court Justice Potter Stewart, who famously dodged defining pornography by saying, “I know it when I see it.”

Update: After I wrote the above, Charter proposed to buy Liberty through a merger. We don’t own Charter directly, but rather through Liberty Broadband, which holds a 25% stake in Charter. Liberty was trading at a significant discount (around 30%) to the value of its Charter shares. Liberty agreed, but at a higher price. Our estimate of Liberty’s net asset value is about $88. The shares are trading at $75 as of this writing (up from $60). If the deal goes through we’ll end up owning shares of Charter at a significant discount.

Posted on October 5, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

DUMB PHONES ANYONE?

By Anonymous Reporter[s]

***

***

Allow us [me] to suggest the use of Android and iOS shortcuts that disable bio-metric unlocking on your cell phone.

“If you use a bio-metric phone sensor [eye scan or fingerprint], you can be compelled to decrypt your device for law enforcement because a bio-metric is something you are,” lawyer Riana Pfefferkorn said in a 2019 talk at the Defcon security conference.

But, “If you use a pass-code to decrypt, typically, you can’t be compelled to unlock, because a pass-code is something that you know.” Her talk did not cover how claiming to have forgotten a pass-code would affect those issues.

In either case, if your cell phone becomes in possession of federal investigators, you may faces the risk of them determining the unlock code through other means, like using such third-party tools as Cellebrite’s unlocking kits to defeat the phone’s security.

Stay Legal! Or simply invoked your Fifth Amendment right against self-incrimination; if needed.

In conclusion: I [we] advise the awareness of cell phone privacy risks involved in having so much of your life stored on personal smart cell phone devices that you take almost everywhere. Stay Safe!

Posted on October 4, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

IN PRIVATE EQUITY AND MEDICINE

By Staff Reporters

***

***

PRIVATE EQUITY

In private equity, the J curve is used to illustrate the historical tendency of private equity funds to deliver negative returns in early years and investment gains in the outlying years as the portfolios of companies mature.

And, according to Wikipedia, in the early years of the fund, a number of factors contribute to negative returns including management fees, investment costs and under-performing investments that are identified early and written down. Over time the fund will begin to experience unrealized gains followed eventually by events in which gains are realized (e.g., IPOs, mergers and acquisitions, leveraged recapitalizations).

Historically, the J curve effect has been more pronounced in the US, where private equity firms tend to carry their investments at the lower of market value or investment cost and have been more aggressive in writing down investments than in writing up investments. As a result, the carrying value of any investment that is under performing will be written down but the carrying value of investments that are performing well tend to be recognized only when there is some kind of event that forces the PE to mark up the investment.

The steeper the positive part of the J curve, the quicker cash is returned to investors. A private equity firm that can make quick returns to investors provides investors with the opportunity to reinvest that cash elsewhere. Of course, with a tightening of credit markets, private equity firms have found it harder to sell businesses they previously invested in. Proceeds to investors have reduced. J curves have flattened dramatically. This leaves investors with less cash flow to invest elsewhere, such as in other private equity firms. The implications for private equity could well be severe. Being unable to sell businesses to generate proceeds and fees means some in the industry have predicted consolidation among private equity firms.

MEDICINE

In medicine, the “J curve” refers to a graph in which the x-axis measures either of two treatable symptoms (blood pressure or blood cholesterol level) while the y-axis measures the chance that a patient will develop cardiovascular disease (CVD). It is well known that high blood pressure or high cholesterol levels increase a patient’s risk.

Paradoxically, what is less well known is that plots of large populations against CVD mortality often take the shape of a J curve which indicates that patients with very low blood pressure and/or low cholesterol levels are also at increased risk.

Posted on October 3, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

NEBULOUS DEFINITIONS

By Staff Reporters

***

***

The simplest model of a market involves two things, supply and demand, and the price and quantity of the goods sold in the market are a function of both. When a natural disaster hits like Hurricane Helene, the immediate effect can be two-fold. In such situations, it is not unusual that the demand for certain products may increase. For example, if everyone is trying to leave the area, demand for gas may rise. The other effect is that supply for certain products may decrease. And, it may be more costly to transport gas in areas affected by a natural disaster, thus decreasing the supply of gas and in turn, increasing the price.

When supply decreases, the price of the good increases. And when demand increases, again the price of the good increases. So we would predict that the market price of gas, for example, would increase in areas recently affected by a hurricane. And in fact we do see this.

Price-gouging occurs when companies raise prices to unfair levels. There is no rule for what qualifies as price-gouging, but it is not an uncommon occurrence. For example in medicine, EpiPen costs is a current example of price increases that have been labeled unfair.

Note: An epinephrine auto-injector (or adrenaline auto-injector, also known by the trade mark EpiPen) is a medical device for injecting a measured dose or doses of epinephrine (adrenaline) by means of auto-injector technology. It is most often used for the treatment of anaphylaxis. The first epinephrine auto-injector was brought to market in 1983.

Posted on October 3, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

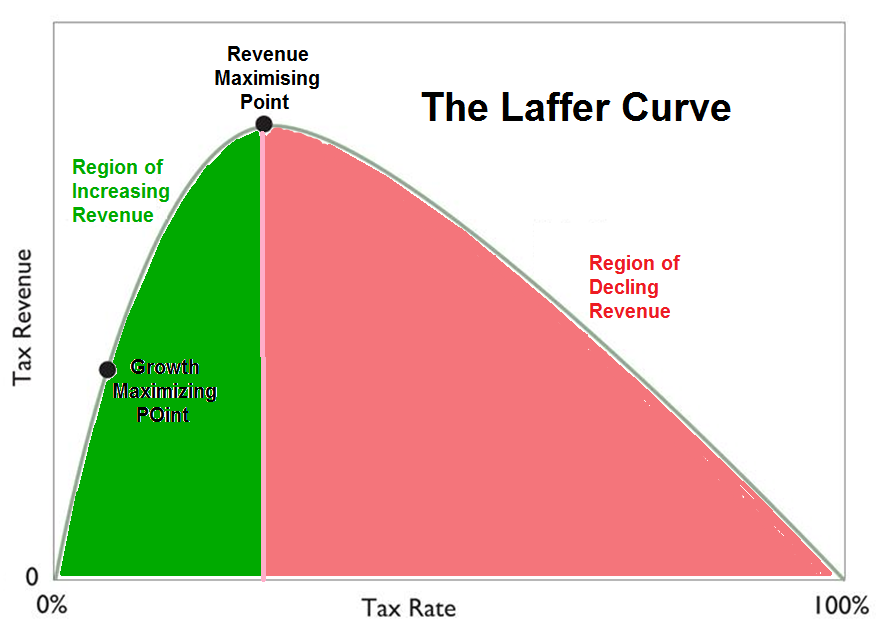

What it is – How it works By staff reporters

DEFINITION:

In economics, the Laffer curve is a representation of the relationship between rates of taxation and the resulting levels of government revenue.

The Laffer curve claims to illustrate the concept of taxable income elasticity—i.e., taxable income will change in response to changes in the rate of taxation.

The Laffer Curve is a theory developed by supply-side economist Arthur Laffer to show the relationship between tax rates and the amount of tax revenue collected by governments.

The curve is used to illustrate Laffer’s main premise that the more an activity such as production is taxed, the less of it is generated. Likewise, the less an activity is taxed, the more of it is generated.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. https://medicalexecutivepost.com/dr-david-marcinkos-bookings/

Posted on October 2, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

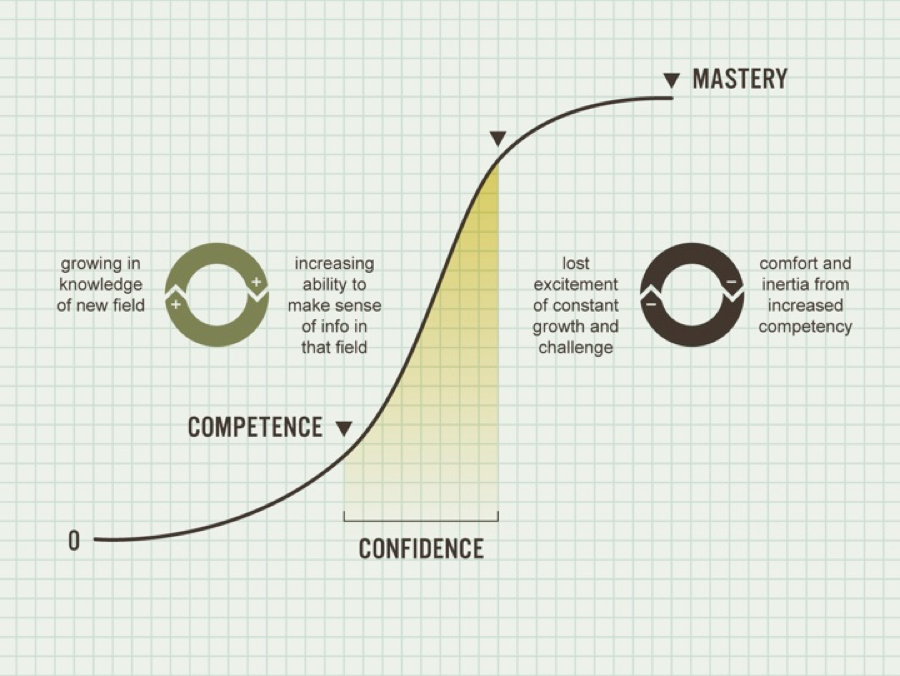

SIGMOID CURVE

By Staff Reporters

***

DEFINITION

The S curve refers to a chart that is used to describe, visualize, and predict the performance of a project or business overtime. More specifically, it is a logistic curve that plots the progress of a variable by relating it to another variable over time.

The term S curve was developed as a result of the shape that the data takes. Projects on the S curve often experience a slow growth at the beginning, rapid growth in the middle, and slow growth and at the end. The maximum point of acceleration is called the point of inflexion. It is at this point that the project or business returns to the initial slow growth it started from.

Posted on October 2, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Humana, the country’s second largest Medicare Advantage insurer, is aggressively culling its plan offerings after several quarters of spending more than expected on its members’ medical care, and getting hammered on Wall Street for it. The company will scrap Medicare Advantage plans in 2025 that currently cover about 560,000 members.

Markets: Stocks embraced the start of spooky season by falling yesterday, ending a hot streak as investors mulled the rising tensions in the Middle East.

General Motors: Reported slightly better-than-expected sales during the third quarter, thanks in part to increased sales of small crossovers and electric vehicles. The automaker reported a 2.2% decrease in sales, compared with a year earlier, an improvement over auto industry forecasts that projected a decline of more than 3% in the quarter.

Meanwhile:Nike’s beleaguered stock was up a bit ahead of its first earnings report since the company announced a CEO change. It withdrew its full-year guidance and postponed its investor day as longtime company veteran Elliott Hill prepares to take the top job at the sneaker giant. Instead, executives said Nike will provide quarterly guidance for the rest of the year. Shares of Nike fell about 7% in early trading Wednesday.

Posted on October 1, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

On August 31, 2024, the California legislature passed a bill that may curb private equity (PE) healthcare transactions in the state. The legislation is now on Governor Gavin Newsom’s desk for signature, who must sign or veto the bill by September 30, 2024. If signed into law, California will have the strictest regulation of PE deals of any state in the country.

Posted on September 29, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Markets: Wall Street life was looking good last week as all the major indexes clinched their third consecutive winning week. Stocks were a mixed bag for Friday, but the Dow Jones scored another record close. Bristol Myers Squibb rose after the FDA approved its schizophrenia drug as the first new treatment for the condition in decades.

Economy: The FOMC’s favorite inflation gauge came in lower than expected for last month, likely clearing the way for Jerome Powell and the Federal Reserve to keep cutting interest rates.

Posted on September 27, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS

By Staff Reporters

Tropical Storm Helene made landfall in Florida last night as a Category 4 hurricane, the strongest to ever hit the state’s Big Bend. It is a huge and powerful storm—with a wind field that could span the distance between tjhe State of Maryland/Washington, DC, and Indianapolis/Chicago—that has already caused historic flooding to some of Florida’s coastal communities.

How bad is it? The Waffle House Index, which has been used by FEMA as an indicator of a storm’s severity, closed all of its locations in Tallahassee, Florida. The Waffle House Index [WHI] is an informal metric named after the Waffle House restaurant chain, headquartered in Georgia, and used by the Federal Emergency Management Agency (FEMA) to determine the effect of a storm and the likely scale of assistance required for disaster recovery.

And, as of 8am EST, Helene has weakened to a Category 1 as it’s moved into Atlanta, Georgia. Nearly 2 million customers are without power across Florida, Georgia, and North/South Carolina. You can get real-time updates here, as we hope everyone in the region is staying safe.

***

Stock market yesterday: The S&P 500 clinched a fresh new record amid GDP data and micro chip stock gains.and Stonk Stocks. Stonk, a deliberate misspelling of stock (meaning “a share of the value of a company which can be bought, sold, or traded as an investment”), was coined in a 2017 meme. The word is often used humorously on the internet to imply a vague understanding of financial transactions or poor financial decisions.

Upbeat GDP data and new stimulus measures in China were largely to thank. One of the day’s big winners was Southwest Airlines, which soared after executives announced plans to revitalize the business.

COMMENTS APPRECIATED

Thank You

***

*** Designated a Doody’s Core Title!

To keep up with the ever-changing field of health care, we must learn new and re-learn old terminology in order to correctly apply it to practice. By bringing together the most up-to-date abbreviations, acronyms, definitions, and terms in the health care industry, the Dictionary offers a wealth of essential information that will help you understand the ever-changing policies and practices in health insurance and managed care today.

Posted on September 26, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

A behavioral scientist

By Rick Kahler MS CFP®

Human beings make most of our decisions—including financial ones—emotionally, not logically. Unfortunately, too much of the time, our emotions lead us into financial choices that aren’t good for our financial well-being. This is hardly news to financial planners or financial therapists. Nor is it a surprise to any parent who has ever struggled to teach kids how to manage money wisely.

Economic Model Assumptions