BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on October 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

STOCKHOLM (AP) — Three researchers who probed the process of business innovation won the Nobel memorial prize in economics Monday for explaining how new products and inventions promote economic growth and human welfare, even as they leave older companies in the dust.

Their work was credited with helping economists better understand how ideas and technology succeed by disrupting established ways — a process as old as steam locomotives replacing horse-drawn wagons and as contemporary as e-commerce shuttering shopping malls.

The award was shared by Dutch-born Joel Mokyr, 79, who is at Northwestern University; Philippe Aghion, 69, who works at the Collège de France and the London School of Economics; and Canadian-born Peter Howitt, 79, who is at Brown University.

Investment fees still matter for physicians and all of us, despite dropping dramatically over the past several decades due to computer automation, algorithms and artificial intelligence, etc. And, they can make a big difference to your financial health. So, before buying any investment thru a financial advisor, planner, manager, stock broker, etc., it’s vital to understand these two often confusing costs.

***

***

Fee Only: Paid directly by clients for their services and can’t receive other sources of compensation, such as payments from fund providers. Act as a fiduciary, meaning they are obligated to put their clients’ interests first

Fee Based: Paid by clients but also via other sources, such as commissions from financial products that clients purchase. Brokers and dealers (registered representatives) are simply required to sell products that are “suitable” for their clients. Not a fiduciary.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Posted on October 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

ByAI and Staff Reporters

***

***

Alpha Male and Beta Male are terms for men derived from the designations of alpha and beta animals in ethology. They may also be used with other genders, such as women, or additionally use other letters of the Greek alphabet (such as sigma. The popularization of these terms to describe humans has been widely criticized by scientists. Both terms have been frequently used in internet memes.

The term beta is used as a pejorative self-identifier among some members of the manosphere, particularly incels, who do not believe they are assertive and/or traditionally masculine, and feel overlooked by women. It is also used to negatively describe other men who are not deemed to be assertive, particularly with women. In internet culture, the term sigma male is also frequently used, gaining popularity in the late 2010s, but has since been used jokingly, often being used with incel.

Note: Incel is a portmateau of “involuntary celibate”) is a term associated with an online subculture of mostly male and heterosexual people who define themselves as unable to find a romantic or sexual despite desiring one. They often blame, objectify and denigrate women and girls as a result.

Delta Males are very responsible and keep the world moving. Highly adaptable, deltas are known for their competence and work ethic rather than their leadership and ambition. Delta Males love learning new skills for the sake of improving themselves, not for power or extrinsic successes. Because of this, they often have a very healthy work-life balance. They’re dependable and unpretentious. Common personality traits: hardworking, loyal and responsible. Careers they excel at are accountant, dentist, engineer and firefighter. If you’re a delta male, your work often speaks for itself. People trust you, so consider being more proactive and taking initiative at work; you’ll be rewarded for it and won’t necessarily need to be in the spotlight.

Gammas Males tend to be insecure about status and may overestimate their status. They’re unhappy with their position, so they try to convince themselves that they’re Sigmas. A Gamma Male is described as intelligent, romantic, and empathetic. While he has some female traits, he has difficulty understanding and dating women. But, unlike alphas, gammas avoid conflict at all costs and care deeply about what other people think of them. They lack the leadership skills and confidence to be on top.

Omega Males are skilled introverts who don’t need external validation. Pop culture portrays them as the shyer, more reserved yin to the zeta male’s yang. They’re independent and very comfortable in their own company. They’d rather spend time coming up with (usually brilliant) new ideas and inventions of their own instead of socializing with others. They have uncouth but delightful senses of humor and their theories often change the world for the better. Common personality traits are self-motivated, strategic and quiet. Careers they excel at are chemist, composer, inventor and mathematician. If you’re an omega male, your ideas are likely ingenious.

Sigma Males are rebellious leaders with lots of life experience while delta males are responsible companions who you want by your side.Common personality traits are nurturing and wise. Careers they excel at areentrepreneur, philosopher, professor, or therapist.

Zeta Males are one-of-a-kind progressives. There’s a reason the zeta male is the least talked about personality type in pop culture. They’re rare nonconformists who don’t care what other people think. They know themselves and refuse to change to fit into the rigid social standards of society. Zeta males are fierce creatives who blaze new paths for themselves and others. Zeta Males are nonconformist creatives, gamma males are charismatic nomads, and omega males are sharp intellectuals with boundless ideas. Careers they excel at are actor, artist, musician or writer. Common personality traits are creative, independent and self-aware.

QUESTION: Doctors, Agents, Accountants and Financial Advisors: What is your male personality type?

The Looming Cryptocurrency Crisis: Risks on the Horizon

Cryptocurrency has revolutionized the financial landscape, offering decentralized alternatives to traditional banking and investment systems. However, as digital assets become more integrated into global markets, concerns about a potential future cryptocurrency crisis are mounting. From regulatory uncertainty to systemic vulnerabilities, the risks associated with crypto are increasingly being scrutinized by economists, governments, and investors.

One of the most pressing concerns is regulatory instability. Cryptocurrencies operate in a fragmented legal environment, with different countries adopting varying stances—from full embrace to outright bans. The lack of unified global regulation creates loopholes that can be exploited for money laundering, tax evasion, and fraud. If major economies suddenly impose strict regulations or sanctions, it could trigger a rapid devaluation of crypto assets and erode investor confidence.

Another risk stems from market volatility and speculative behavior. Unlike traditional assets backed by tangible value or government guarantees, cryptocurrencies are often driven by hype, social media trends, and speculative trading. This creates a fragile ecosystem where prices can swing wildly. A sudden crash—similar to the 2022 Terra/Luna collapse—could wipe out billions in investor wealth and destabilize related financial institutions.

***

***

Technological vulnerabilities also pose a threat. While blockchain is considered secure, the platforms built on it are not immune to hacks, bugs, or exploitation. High-profile breaches of exchanges and wallets have already resulted in massive losses. As crypto adoption grows, so does the incentive for cybercriminals to target these systems. A coordinated attack on a major exchange or blockchain network could have cascading effects across the entire crypto economy. Geopolitical tensions may also catalyze a crisis. For instance, recent reports suggest that aggressive trade policies—such as the U.S. imposing 100% tariffs on Chinese imports—can indirectly impact crypto markets by shaking investor sentiment and triggering sell-offs.

The interconnection with traditional finance is another area of concern. As banks and hedge funds increasingly invest in crypto, the line between decentralized finance and conventional markets blurs. This integration means that a crypto collapse could spill over into broader financial systems, potentially triggering a global crisis. The 2023 banking collapses, which were partially linked to crypto exposure, serve as a warning of how intertwined these systems have become.

Geopolitical tensions may also catalyze a crisis. For instance, recent reports suggest that aggressive trade policies—such as the U.S. imposing 100% tariffs on Chinese imports—can indirectly impact crypto markets by shaking investor sentiment and triggering sell-offs. In such scenarios, cryptocurrencies may not serve as the safe haven they were once believed to be.

Lastly, overreliance on stablecoins and algorithmic assets introduces systemic risk. Many investors use stablecoins to hedge volatility, but these assets are only as stable as their underlying reserves and governance. If a major stablecoin fails, it could lead to a liquidity crunch and panic across exchanges and DeFi platforms.

In conclusion, while cryptocurrency offers transformative potential, it also carries significant risks that could culminate in a future crisis. To mitigate these dangers, stakeholders must push for clearer regulations, stronger technological safeguards, and more transparent financial practices. Without proactive measures, the next financial meltdown may not come from Wall Street—but from the blockchain.

NOTE: A crypto mogul has been found dead inside his luxury car in Ukraine after the digital currency market nosedived. Konstantin Galich, 32, also known as Kostya Kudo, has died after one of the worst turmoils shook the cryptocurrency market. The entrepreneur, who became a well-known figure in the crypto industry, was reportedly found with a gunshot wound to his head in his black Lamborghini parked up in Kyiv’s Obolonskyi neighbourhood. His death was later confirmed on his Telegram channel in a post saying ‘Konstantin Kudo tragically passed away. The causes are being investigated. We will keep you posted on any further news.’

Critical thinking allows a Financial Advisor [FA] to analyze information and make an objective judgment. By impartially evaluating the facts related to a matter, Financial Planners [FPs] can draw realistic conclusions that will help make a sound decision. The ability of being able to properly analyze a situation and come up with a logical and reasonable conclusion is highly valued by employers, as well as current and potential clients.

Now, according to Indeed, we present the six main critical thinking and examples that will help you evaluate your own thought process as a FA, FP or Wealth Manager, etc.

What is critical thinking?

Critical thinking is the ability to objectively analyze information and draw a rational conclusion. It involves gathering information on a subject and determining which pieces of information apply to the subject and which don’t, based on deductive reasoning. The ability to think critically helps people in both their personal and professional lives and is valued by most clients and employers.

Why do employers value critical thinking?

Critical thinking skills are a valuable asset for an employee, as employers, brokerages and Registered Investment Advisors [RIAs] typically appreciate candidates who can correctly assess a situation and come up with a logical resolution. Time is a valuable resource for most managers, and an employee able to make correct decisions without supervision will save both that manager and the whole company much valuable time.

***

***

Six main types of critical thinking skills

There are six main critical thinking skills you can develop to successfully analyze facts and situations and come up with logical conclusions:

1. Analytical thinking

Being able to properly analyze information is the most important aspect of critical thinking. This implies gathering information and interpreting it, but also skeptically evaluating data. When researching a work topic, analytical thinking helps you separate the information that applies to your situation from that which doesn’t.

2. Good communication

Whether you are gathering information or convincing others that your conclusions are correct, good communication is crucial in the process. Asking people to share their ideas and information with you and showing your critical thinking can help step further towards success. If you’re making a work-related decision, proper communication with your coworkers can help you gather the information you need to make the right choice.

3. Creative thinking

Being able to discover certain patterns of information and make abstract connections between seemingly unrelated data helps improve your critical thinking. When analyzing a work procedure or process, you can creatively come up with ways to make it faster and more efficient. Creativity is a skill that can be strengthened over time and is valuable in every position, experience level and industry.

4. Open-mindedness

Previous education and life experiences leave their mark on a person’s ability to objectively evaluate certain situations. By acknowledging these biases, you can improve your critical thinking and overall decision process. For example, if you plan to conduct a meeting in a certain way and your firm suggests using a different strategy, you should let them speak and adjust your approach based on their input.

5. Ability to solve problems

The ability to correctly analyze a problem and work on implementing a solution is another valuable skill.

6. Asking thoughtful questions:

In both private and professional situations, asking the right questions is a crucial step in formulating correct conclusions. Questions can be categorized in various forms as mentioned below:

***

***

* Open-ended questions

Asking open-ended questions can help the person you’re communicating with provide you with relevant and necessary information. These are questions that don’t allow a simple “yes” or “no” as an answer, requiring the respondent to elaborate on the answer.

* Outcome-based questions

When you feel like another person’s experience and skills could help you work more effectively, consider asking outcome-based questions. Asking someone how they would act in a certain hypothetical situation, such as a stock market correction, can give you an insight into their perspective, helping you see things you hadn’t thought about before.

Reflective questions

You can gain insight by asking a client to reflect and evaluate an experience and explain their thought processes during that time. This can help you develop your critical thinking by providing you real-world examples.

* Structural questions

An easy way to understand something is to ask how something works. Any working system results from a long process of trial and error, and properly understanding the steps that needed to be taken for a positive result could help you be more efficient in your own endeavors.

CONCLUSION

Critical thinking is like a muscle that can be exercised and built over time. It is a skill that can help propel your career to new heights. You’ll be able to solve workplace issues, use trial and error to troubleshoot ideas, and more.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

The October 2025 Stock Market Crash: A Perfect Storm of Geopolitics and Investor Panic

The weekend of October 10–12, 2025, marked one of the most dramatic downturns in global financial markets in recent memory. What began as a series of unsettling headlines quickly snowballed into a full-blown market crash, sending shockwaves through economies and portfolios worldwide. This event was not the result of a single catalyst but rather a convergence of geopolitical tensions, speculative excess, and investor psychology.

At the heart of the crisis was a sudden escalation in U.S.–China trade relations. President Donald Trump abruptly canceled a scheduled diplomatic meeting with Chinese President Xi Jinping and announced a sweeping 100% tariff on all Chinese imports. This move reignited fears of a prolonged trade war, reminiscent of the economic standoff that rattled markets in the late 2010s. Investors, already jittery from months of uncertainty, interpreted the announcement as a signal of deteriorating global cooperation and retaliatory economic measures to come.

The impact was immediate and severe. Major U.S. indices plummeted: the S&P 500 dropped 2.7%, the Nasdaq fell 3.6%, and the Dow Jones Industrial Average lost 1.9%. These declines marked the worst single-day performance since April and triggered automatic trading halts in several sectors. The selloff was not confined to the United States; European and Asian markets mirrored the panic, with steep losses across the board.

Compounding the crisis was a massive liquidation in the cryptocurrency market. As traditional assets tumbled, investors rushed to offload digital holdings, leading to the largest crypto wipeout in history. Trillions of dollars in value evaporated within hours, further destabilizing investor confidence and draining liquidity from the broader financial system.

Another underlying factor was growing concern over the valuation of artificial intelligence (AI) stocks. The International Monetary Fund (IMF) had recently issued a warning that the AI sector was exhibiting signs of a speculative bubble, drawing parallels to the dot-com era. With many AI companies trading at astronomical price-to-earnings ratios, the crash exposed the fragility of investor sentiment and the dangers of overexuberance in emerging technologies.

Perhaps most telling was the psychological shift among investors. The weekend saw widespread capitulation, with many choosing to exit the market entirely rather than weather further volatility. This behavior—marked by fear-driven decision-making and herd mentality—is often a hallmark of deeper financial crises. It underscores the importance of trust and stability in maintaining market equilibrium.

In conclusion, the October 2025 stock market crash was a multifaceted event driven by geopolitical shocks, speculative risk, and emotional contagion. It serves as a stark reminder of how interconnected and fragile global markets have become. As policymakers and investors assess the damage, the focus must shift toward restoring confidence, recalibrating risk, and ensuring that future growth is built on sustainable foundations rather than speculative fervor.

COMMENTS APPRECIATED

SPEAKING: ME-P Editor Dr. David Edward Marcinko MBA MEd will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Classic: Acute care is a branch of secondary health care where a patient receives active but short-term treatment for a severe injury or episode of illness, an urgent medical condition, or during recovery from surgery. In medical terms, care for acute health conditions is the opposite from chronic care, or longer term care.

Modern: Acute care is active, short-term treatment for a severe injury or episode related to illness, an urgent medical condition or recovery from surgery.

Buying or selling stocks requires access to one of the major exchanges, such as the New York Stock Exchange (NYSE) or the National Association of Securities Dealers Automated Quotations (NASDAQ). To trade on these exchanges, you must be a member of the exchange or belong to a member firm. Member firms and many individuals who work for them are licensed as brokers or broker-dealers by the Financial Industry Regulatory Authority (FINRA).

And so, a stockbroker executes orders in the market on behalf of clients. A stockbroker may also be known as a registered representative or investment advisor. Most stockbrokers work for a brokerage firm and handle transactions for several individual and institutional customers. Stockbrokers are often paid on commission, although compensation methods vary by employer.

Remember: SBs work for their firm and not the client. Stock brokers are not fiduciaries.

The Medical Executive-Post is a news and information aggregator and social media professional network for medical and financial service professionals.

Feel free to submit education content to the site as well as links, text posts, images, opinions and videos which are then voted up or down by other members. Comments and dialog are especially welcomed.

Daily posts are organized by subject. ME-P administrators moderate the activity. Moderation may also conducted by community-specific moderators who are unpaid volunteers.

Posted on October 12, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I. and Staff Reporters

***

***

The VIX, or CBOE Volatility Index, is often called the “fear gauge” of the stock market. It measures the market’s expectations for volatility over the next 30 days, based on options prices for the S&P 500.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements.

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on October 11, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

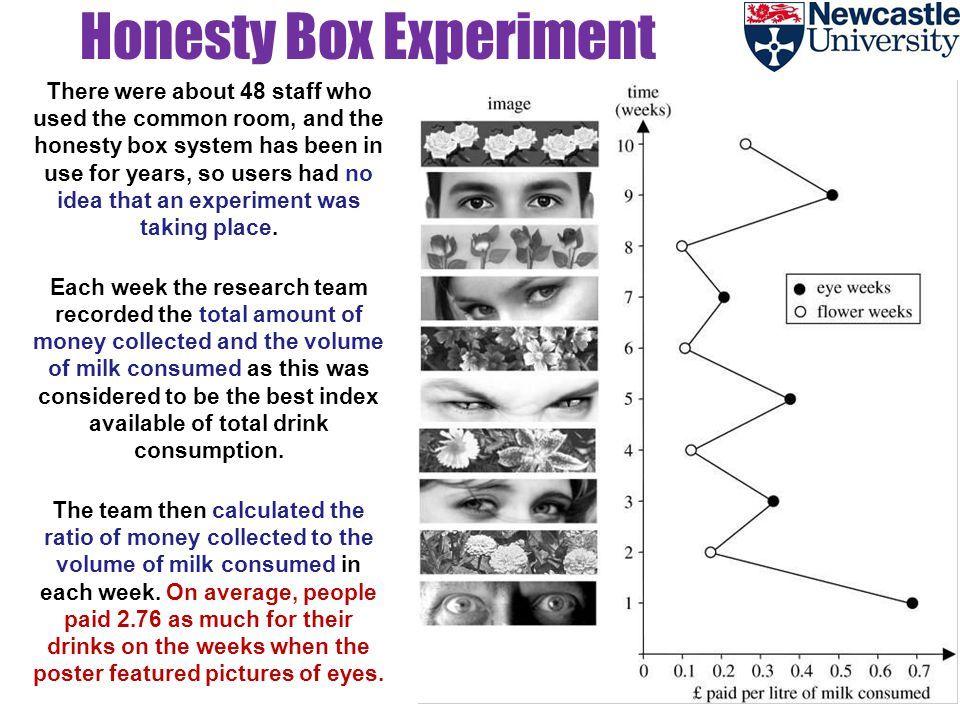

“BIG BROTHER” IS WATCHING

[From the Newcastle Division of Psychology]

By Dr. David Edward Marcinko MBA

***

It’s no surprise that people are more honest when they know that they’re being watched. But what about just reminding them of the idea of being watched, without them actually being watched?

For years, people at the University of Newcastle’s Division of Psychology have an honor (or trust) system where they are requested to deposit payment for coffee in an “honesty box.” There was a note saying how much they should pay.

In 2006, Melissa Bateson and colleagues decided to do a little experiment: they placed an image above the note. They alternate between two pictures: one week they would use a picture of eyes and the other week, flowers.

After 10 weeks, they plotted the amount of money received versus drinks consumed and found that people paid nearly three times as much for their drinks when eyes were displayed!

Posted on October 10, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

DEFINITIONS

***

***

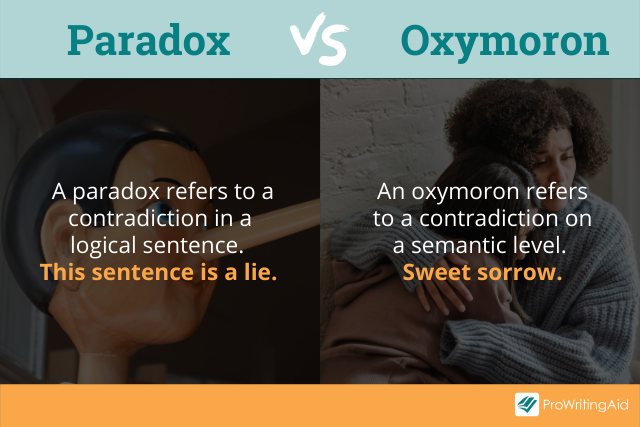

Difference between Paradox and Oxymoron

According to Mackenzie Marcinko PhD, many people tend to confuse a paradox with an oxymoron, and it’s not hard to see why. Most oxymoron examples appear to be compressed version of a paradox, in which it is used to add a dramatic effect and to emphasize contrasting thoughts. Although they may seem greatly similar in form, there are slight differences that set them apart.

A paradox consists of a statement with opposing definitions, while an oxymoron combines two contradictory terms to form a new meaning. But because an oxymoron can play out with just two words, it is often used to describe a given object or idea imaginatively.

As for a paradox, the statement itself makes you question whether something is true or false. It appears to contradict the truth, but if given a closer look, the truth is there but is merely implied.

COMMENTS APPRECIATED

The Medical Executive-Post is a news and information aggregator and social media professional network for medical and financial service professionals. Feel free to submit education content to the site as well as links, text posts, images, opinions and videos which are then voted up or down by other members. Comments and dialog are especially welcomed. Daily posts are organized by subject. ME-P administrators moderate the activity. Moderation may also conducted by community-specific moderators who are unpaid volunteers.

The Dow Jones Industrial Average (DJIA), often referred to simply as “the Dow,” is one of the oldest and most well-known stock market indices in the world. It was created in 1896 by Charles Dow, the co-founder of The Wall Street Journal, and is designed to represent the performance of the broader U.S. stock market, specifically focusing on 30 large, publicly traded companies. These companies are considered leaders in their respective industries and serve as a barometer for the overall health of the U.S. economy.

The Composition of the DJIA

The DJIA includes 30 companies, which are selected by the editors of The Wall Street Journal based on various factors such as market influence, reputation, and the stability of the company. These companies represent a wide array of sectors, including technology, finance, healthcare, consumer goods, and energy. Notably, the companies chosen for the DJIA are not necessarily the largest companies in the U.S. by market capitalization, but rather those that are most indicative of the broader economy. Some of the prominent companies listed in the DJIA include names like Apple, Microsoft, Coca-Cola, and Johnson & Johnson.

However, the list of 30 companies is not static. Over time, companies may be added or removed to reflect changes in the economic landscape. For example, if a company experiences significant decline or no longer represents a leading sector, it might be replaced with another company that better reflects modern economic trends. This periodic reshuffling ensures that the DJIA continues to be a relevant measure of economic activity.

How the DJIA is Calculated

The DJIA is a price-weighted index, which means that the value of the index is determined by the share price of the component companies, rather than their market capitalization. To calculate the DJIA, the sum of the stock prices of all 30 companies is divided by a special divisor. This divisor adjusts for stock splits, dividends, and other corporate actions to maintain the integrity of the index over time. The price-weighted method means that higher-priced stocks have a greater impact on the movement of the index, regardless of the overall size or economic weight of the company.

For instance, if a company with a higher stock price like Apple experiences a significant change in value, it will influence the DJIA more than a company with a lower stock price, even if the latter has a larger market capitalization. This makes the DJIA somewhat different from other indices, like the S&P 500, which is weighted by market cap and gives more weight to larger companies in terms of their economic impact.

Significance of the DJIA

The DJIA is widely regarded as a barometer of the U.S. stock market’s performance. Investors and analysts closely monitor the movements of the Dow to gauge the overall health of the economy. When the DJIA rises, it generally suggests that investors are optimistic about the economic outlook and that large companies are performing well. Conversely, when the DJIA falls, it often signals economic uncertainty or a downturn in market conditions.

Despite being a narrow index, with only 30 companies, the DJIA holds substantial sway in financial markets. It is widely covered in the media and is often cited in discussions about the state of the economy. In fact, the performance of the DJIA is considered a key indicator of investor sentiment and economic confidence.

However, the DJIA has its limitations. Since it only includes 30 companies, it does not necessarily represent the broader market or capture the performance of smaller companies. Other indices, like the S&P 500, which includes 500 companies, offer a more comprehensive view of the market’s performance.

Conclusion

The Dow Jones Industrial Average is a key metric for understanding the state of the U.S. economy and the stock market. Although it has evolved over the years, it continues to provide valuable insights into the performance of large, influential companies. While it is not a perfect reflection of the market as a whole, the DJIA remains one of the most important and widely recognized indices in global finance. Through its historical significance and its role in shaping market sentiment, the Dow has cemented its place as a cornerstone of financial analysis.

“THE INVESTOR’S CHIEF problem—even his worst enemy—is likely to be himself.” So wrote Benjamin Graham, the father of modern investment analysis.

With these words, written in 1949, Graham acknowledged the reality that investors are human. Though he had written an 800 page book on techniques to analyze stocks and bonds, Graham understood that investing is as much about human psychology as it is about numerical analysis.

In the decades since Graham’s passing, an entire field has emerged at the intersection of psychology and finance. Known as behavioral finance, its pioneers include Daniel Kahneman, Amos Tversky and Richard Thaler. Together, they and their peers have identified countless human foibles that interfere with our ability to make good financial decisions. These include hindsight bias, recency bias and overconfidence, among others. On my bookshelf, I have at least as many volumes on behavioral finance as I do on pure financial analysis, so I certainly put stock in these ideas.

At the same time, I think we’re being too hard on ourselves when we lay all of these biases at our feet. We shouldn’t conclude that we’re deficient because we’re so susceptible to biases. Rather, the problem is that finance isn’t a scientific field like math or physics. At best, it’s like chaos theory. Yes, there is some underlying logic, but it’s usually so hard to observe and understand that it might as well be random. The world of personal finance is bedeviled by paradoxes, so no individual—no matter how rational—can always make optimal decisions.

As we plan for our financial future, I think it’s helpful to be cognizant of these paradoxes. While there’s nothing we can do to control or change them, there is great value in being aware of them, so we can approach them with the right tools and the right mindset.

Here are just seven of the paradoxes that can bedevil financial decision-making:

There’s the paradox that all of the greatest fortunes—Carnegie, Rockefeller, Buffett, Gates—have been made by owning just one stock. And yet the best advice for individual investors is to do the opposite: to own broadly diversified index funds.

There’s the paradox that the stock market may appear overvalued and yet it could become even more overvalued before it eventually declines. And when it does decline, it may be to a level that is even higher than where it is today.

There’s the paradox that we make plans based on our understanding of the rules—and yet Congress can change the rules on us at any time, as it did just last year.

There’s the paradox that we base our plans on historical averages—average stock market returns, average interest rates, average inflation rates and so on—and yet we only lead one life, so none of us will experience the average.

There’s the paradox that we continue to be attracted to the prestige of high-cost colleges, even though a rational analysis that looks at return on investment tells us that lower-cost state schools are usually the better bet.

There’s the paradox that early retirement seems so appealing—and has even turned into a movement—and yet the reality of early retirement suggests that we might be better off staying at our desks.

There’s the paradox that retirees’ worst fear is outliving their money and yet few choose the financial product that is purpose-built to solve that problem: the single-premium immediate annuity.

How should you respond to these paradoxes? As you plan for your financial future, embrace the concept of “loosely held views.”

In other words, make financial plans, but continuously update your views, question your assumptions and rethink your priorities.

Active Immunity develops after exposure to a disease-causing infectious microorganism or other foreign substance, such as following infection or vaccination.

Acquired Immunity develops during a person’s lifetime. There are two types of acquired immunity: active immunity and passive immunity.

Passive Immunity develops after a person receives immune system components, most commonly antibodies, from another person. Passive immunity can occur naturally, such as when an infant receives a mother’s antibodies through the placenta or breast milk, or artificially, such as when a person receives antibodies in the form of an injection (gamma globulin injection). Passive immunity provides immediate protection against an antigen, but does not provide long-lasting protection.

Posted on October 9, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Co-Pilot

***

***

Artificial Intelligence in Finance: Revolutionizing the Industry

Artificial Intelligence (AI) is rapidly transforming the financial services industry, reshaping how institutions operate, manage risk, and serve customers. By leveraging machine learning, natural language processing, and predictive analytics, AI is enabling smarter decision-making, greater efficiency, and enhanced customer experiences across banking, investing, insurance, and regulatory compliance.

One of the most impactful applications of AI in finance is in fraud detection and prevention. Traditional systems rely on rule-based algorithms that often fail to catch sophisticated schemes. AI, however, can analyze vast amounts of transaction data in real time, identifying patterns and anomalies that signal fraudulent behavior. Machine learning models continuously improve as they process more data, making them increasingly effective at detecting threats and reducing false positives.

AI also plays a pivotal role in algorithmic trading, where decisions are made at lightning speed based on complex data inputs. These systems can process news articles, social media sentiment, and market data to execute trades with precision. Hedge funds and investment banks use AI to optimize portfolios, forecast market trends, and identify arbitrage opportunities that human analysts might miss.

In personal finance and banking, AI enhances customer service through chatbots and virtual assistants. These tools handle routine inquiries, assist with transactions, and offer financial advice based on user behavior. AI-driven platforms like robo-advisors provide personalized investment strategies, adjusting portfolios automatically based on market conditions and individual goals. This democratizes access to financial planning, making it more affordable and scalable.

Credit scoring and lending have also been revolutionized by AI. Traditional credit models often rely on limited data and can be biased against certain demographics. AI can incorporate alternative data sources—such as utility payments, social media activity, and online behavior—to assess creditworthiness more accurately and inclusively. This opens up lending opportunities for underserved populations and reduces default risk for lenders.

In insurance, AI streamlines underwriting and claims processing. By analyzing historical data and customer profiles, AI can assess risk more precisely and tailor policies to individual needs. During claims, AI can automate document review, detect fraud, and expedite payouts, improving both operational efficiency and customer satisfaction.

Regulatory compliance, or RegTech, is another area where AI shines. Financial institutions face increasing scrutiny and complex regulations. AI tools can monitor transactions, flag suspicious activity, and ensure adherence to legal standards. Natural language processing helps parse regulatory documents and automate reporting, reducing the burden on compliance teams.

Despite its benefits, AI in finance raises ethical and operational challenges. Data privacy, algorithmic bias, and transparency are critical concerns. Financial institutions must ensure that AI systems are explainable, fair, and secure. Regulatory bodies are beginning to address these issues, but ongoing collaboration between technologists, policymakers, and industry leaders is essential.

In conclusion, artificial intelligence is not just enhancing finance—it’s redefining it. From fraud prevention to personalized banking, AI is driving innovation and efficiency. As the technology matures, its integration must be guided by ethical principles and robust governance to ensure that the financial system remains fair, resilient, and inclusive.

Posted on October 8, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

Efficient New Patient-Scheduling Models

[By Staff Writers]

Most doctors follow a linear (series-singular) time allocation strategy for scheduling patients (i.e., every 15 or 20 minutes). This can create bottlenecks because of emergencies, late patients, traffic jams, absent office personal, paperwork delays, etc.

Therefore, as first proposed by Dr. Neal Baum, a practicing urologist in New Orleans, one of these three newer scheduling approaches might prove more useful.

Customized Scheduling

The bottleneck problem may be reduced by trying to customize, estimate or project the time needed for the patient’s next office visit.

For example: CPT #99211 (15 minutes), #99212 (25 minutes), #99213 (35 minutes), or #99214 (45 minutes). Occasionally, extra time is need, and can be accommodated, if the allocated times are not too tightly scheduled.

Wave Scheduling

Most patients do not mind a brief 20-30 minute wait prior to seeing the doctor. Wave scheduling assumes that no patient will wait longer than this time period, and that for every three patients; two will be on time and one will be late.

This model begins by scheduling the three patients on the hour; and works like this.The first patient is seen on schedule, while the second and third wait for a few minutes. The later two patients are booked at 20 minutes past the hour and one or both may wait a brief time. One patient is scheduled for 40 minutes past the hour. The doctor then has 20 minutes to finish with the last three patients and may then get back on schedule before the end of the hour.

Bundle Scheduling

Bundling involves scheduling like-patient activities in blocks of time to increase efficiency.

For example, schedule minor surgical checkups on Monday morning, immunizations on Tuesday afternoon, and routine physical examinations on Wednesday evening, or make Thursday kid’s day and Friday senior citizens day. Do not be too rigid, but by scheduling similar activities together, assembly-line efficiency is achieved without assembly line mentality, and allows you to develop the most economically profitable operational flow process possible for the office.

Patient Self Scheduling (Internet Based Access Management)

New software programs allow patients to schedule their own appointments over the internet. The software allows solo or individual group physicians with a practice to set their own parameters of time, availability and even insurance plans. Through a series of interrogatories, the program confirms each appointment. When the patient arrives, a software tracker communicates with office staff and follows the patients from check-in, to procedures, to checkout.

Today, many hospitals have even abandoned the check-in or admissions, department. It has been replaced by Access Management.

Assessment

The traditional inear patient scheduling system is slowly being abandoned by modern medical practitioners; an all venues (medical practices, clinics, hospitals and various other healthcare entireties).

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on October 8, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A. I.

***

***

Value-Based Medical Care: A Paradigm Shift in Healthcare

In recent years, the healthcare industry has undergone a transformative shift from volume-driven services to outcome-focused care. This evolution is embodied in the concept of value-based medical care, a model that emphasizes delivering high-quality healthcare while controlling costs and improving patient outcomes. Unlike traditional fee-for-service systems, which reward providers for the quantity of services rendered, value-based care aligns incentives with the value of care provided—measured by patient health outcomes relative to the cost of achieving them.

Core Principles of Value-Based Care

At its heart, value-based medical care is built on several foundational principles:

Patient-Centeredness: Care is tailored to individual needs, preferences, and values, promoting shared decision-making and holistic treatment.

Quality Over Quantity: Providers are rewarded for improving health outcomes, reducing hospital readmissions, and preventing disease rather than performing more procedures.

Integrated Care Delivery: Coordination among healthcare professionals ensures seamless transitions between services, reducing fragmentation and duplication.

Data-Driven Accountability: Performance metrics and health analytics guide clinical decisions and track progress toward better outcomes.

Cost Efficiency: By focusing on prevention and effective management of chronic conditions, value-based care aims to reduce unnecessary spending.

Benefits for Patients and Providers

For patients, value-based care offers a more personalized and proactive approach to health. It encourages preventive screenings, chronic disease management, and wellness programs that lead to longer, healthier lives. Providers benefit from shared savings programs, performance bonuses, and stronger relationships with their patients. Moreover, healthcare systems can allocate resources more effectively, reducing waste and improving overall population health.

Posted on October 7, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A. I.

***

***

A trio of scientists — two of them American and one Japanese — have won the Nobel Prize in Medicine for their discoveries concerning peripheral immune tolerance, a mechanism by which the body helps prevent itself from attacking its own tissues instead of foreign invaders.

Mary E. Brunkow, Fred Ramsdell and Shimon Sakaguchi will share the prize for discoveries that “launched the field of peripheral tolerance, spurring the development of medical treatments for cancer and autoimmune diseases,” the Nobel Assembly said in a news release. The trio will now share the prize money of 11 million Swedish kronor (nearly $1.2 million).

Posted on October 7, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Stocks: The S&P 500 hit its seventh record close in a row today, its longest win streak since May. The NASDAQ was buoyed by big tech, while the DJIA fell.

Commodities: Oil climbed thanks to a decision by OPEC+ to boost crude production at a more modest rate than experts expected. Gold continued its record run, rising above $3,900 for the first time ever, while bitcoin hovered just below a new all-time high.

Japan and France: Japanese stocks rose after the country elected its first female prime minister, and French stocks dropped after its prime minister quit less than a month into the job.

Posted on October 6, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Fierce Healthcare [7/29/25]

***

***

UnitedHealthcare CEO Tim Noel offered investors a deeper look at the medical cost spike that’s plaguing the insurance giant’s finances. He said during the company’s earnings call that pricing assumptions set by the company “were well short of actual medical costs” for 2025. UHC’s current outlook, he said, instead reflects an additional $6.5 billion in medical costs, with more than half, or about $3.6 billion, coming from its Medicare plans.

Noel said that in Medicare Advantage specifically, the team is looking to adjust pricing and benefit designs to account for the cost pressures, which they anticipate will stretch into much of 2026.

It has also decided to exit certain markets largely with plans that are more loosely designed, such as PPOs, in a move that will impact 600,000 beneficiaries.

SPEAKING: ME-P Editor Dr. David Edward Marcinko MBA MEd will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Population health has been defined as “the health outcomes of a group of individuals, including the distribution of such outcomes within the group”. It is an approach to health that aims to improve the health of an entire human population or cohort. http://www.HealthDictionarySeries.org

History

In fact, the nominal “father of population health” is colleague and Dean David B. Nash MD MBA of Jefferson Medical School in Philadelphia. And, although I attended Temple University down the street, David still wrote the Foreword to my textbook years later; Financial Management Strategies for Hospitals and Healthcare Organizations [Tools, Techniques, Checklists and Case Studies].

Now age, income, location, race, gender and education are just a few characteristics that differentiate the world’s population. These are called ”disparities” and they have a major impact on people’s lives; especially their healthcare. And, I’ve written about them before. Perform a ME-P “search” for more.

So, it’s only natural that we’re keeping an eye on two major demographic trends: aging baby boomers and maturing Millennials [1982-2002 approximately].

Why it’s important

The impact of large population shifts propagate throughout an economy benefitting certain sectors more than others and influencing a country’s growth prospects; tantalizing investing ideas?

Example:

For example, as baby boomers retire, we’ll likely see higher spending on health care, but less on education and raising children. Likewise, tech-savvy Millennials will likely prioritize consumption on experiences over cars and houses [leading economic indicator].

So, can we profit from these trends?

Assessment

Well maybe – maybe not! Overall economic prospects may not be completely affected by these trends. Spending habits on combined goods and services will shift, rather than rise or decline.

So, be careful. What matters most for your investment success is your demographics and investing according to your personal circumstances and goals [paradox-of-thrift].

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. https://medicalexecutivepost.com/dr-david-marcinkos-bookings/

Subscribe: MEDICAL EXECUTIVE POST for curated news, essays, opinions and analysis from the public health, economics, finance, marketing, IT, business and policy management ecosystem.

Artificial Intelligence and Investing: A Transformative Partnership

Artificial Intelligence (AI) is revolutionizing the world of investing, reshaping how decisions are made, risks are assessed, and portfolios are managed. As financial markets grow increasingly complex and data-driven, AI offers powerful tools to navigate this landscape with greater precision, speed, and insight.

At its core, AI refers to systems that can perform tasks typically requiring human intelligence—such as learning, reasoning, and problem-solving. In investing, this translates into algorithms that can analyze vast amounts of financial data, detect patterns, and make predictions with remarkable accuracy. Machine learning, a subset of AI, enables these systems to improve over time by learning from new data, making them especially valuable in dynamic markets.

One of the most significant applications of AI in investing is algorithmic trading. These systems can execute trades at lightning speed, responding to market fluctuations in milliseconds. By analyzing historical data and real-time market conditions, AI-driven trading platforms can identify optimal entry and exit points, often outperforming human traders. High-frequency trading firms have long relied on such technologies to gain competitive advantages.

AI also enhances portfolio management through robo-advisors—digital platforms that use algorithms to provide personalized investment advice. These tools assess an investor’s goals, risk tolerance, and time horizon, then construct and manage a diversified portfolio accordingly. Robo-advisors democratize access to financial planning, offering low-cost, automated solutions to individuals who might not afford traditional advisory services.

Risk assessment is another area where AI shines. By processing alternative data sources—such as social media sentiment, news articles, and satellite imagery—AI can uncover hidden risks and opportunities. For instance, a sudden spike in negative sentiment around a company on Twitter might signal reputational issues, prompting investors to reevaluate their positions. AI models can also forecast macroeconomic trends, helping investors anticipate shifts in interest rates, inflation, or geopolitical events.

Moreover, AI is transforming fundamental analysis. Natural language processing (NLP) allows machines to read and interpret earnings reports, SEC filings, and analyst commentary. This enables investors to extract insights from unstructured data that would be time-consuming to analyze manually. AI can even detect subtle linguistic cues that may indicate a company’s future performance or management’s confidence.

Despite its advantages, AI in investing is not without challenges. Models can be opaque, making it difficult to understand how decisions are made—a phenomenon known as the “black box” problem. There’s also the risk of overfitting, where algorithms perform well on historical data but fail in real-world scenarios. Ethical concerns, such as bias in data and the potential for market manipulation, must also be addressed.

In conclusion, AI is reshaping the investing landscape, offering tools that enhance efficiency, accuracy, and accessibility. While it’s not a panacea, its integration into financial markets marks a profound shift in how capital is allocated and wealth is managed. As technology continues to evolve, investors who embrace AI will be better positioned to thrive in an increasingly data-driven world.

A hedge fund is a limited partnership of private investors whose money is pooled and managed by professional fund managers. These managers use a wide range of strategies, including leverage (borrowed money) and the trading of nontraditional assets, to earn above-average investment returns. A hedge fund investment is often considered a risky, alternative investment choice and usually requires a high minimum investment or net worth. Hedge funds typically target wealthy investors.

The hedge fund manager I am considering also runs an offshore fund under a “master feeder” arrangement.

A PHYSICIAN’S QUESTION:What does this mean? In which fund should I invest?

The master feeder arrangement is a two-tiered investment structure whereby investors invest in the feeder fund. The feeder fund in turn invests in the master fund. The master fund is therefore the one that is actually investing in securities. There may be multiple feeder funds under one master fund. Feeder funds under the same master can differ drastically in terms of fees charged, minimums required, types of investors, and many other features – but the investment style will be the same because only the master actually invests in the market.

A master feeder structure is a very popular arrangement because it allows a portfolio manager to pool both onshore and offshore assets into one investment vehicle (the master fund) that allocates gains and losses in an asset-based, proportional manner back to the onshore and offshore investors. All investors, both offshore and onshore, get the same return. In this manner, the portfolio manager, despite offering more than one fund with different characteristics to different populations, is not faced with the dilemma of which fund to favor with the best investment ideas.

A manager may offer an offshore fund because there is demand for that manager’s skill either abroad, where investors may wish to preserve anonymity, or more commonly where investors simply do not wish to become entangled with the United States tax code. American citizens should generally avoid the offshore fund, since American citizens are taxed on their allocated share of offshore corporation profits whether or not a distribution occurs. Therefore, there is no benefit for most American taxpayers investing in an offshore fund.

Tax-exempt institutions, such as medical foundations, in the United States may have reason to consider an offshore hedge fund, however. Domestic tax-exempt organizations are generally not subject to unrelated business taxable income (UBTI) – the portion of hedge fund income that comes about as a result of the use of leverage – when investing with an offshore corporation. If the same tax-exempt organization were to invest in a domestic fund, and if UBTI was generated, then the organization would have to pay taxes on that UBTI. Most domestic hedge funds generate UBTI.

Posted on October 5, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

On September 22, 2025, the Government Accountability Office (GAO) released a report estimating “the Extent and Effects of Physician Consolidation.” The GAO, the non-partisan audit, evaluation, and investigative arm of Congress, undertook the analysis of physician consolidation in response to lawmakers’ request.

This Health Capital Topics article reviews the GAO report and stakeholder reactions. (Read more…)

Posted on October 5, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITION

By Staff Reporters

***

***

What is distillation? In machine learning, distillation is a technique for transferring knowledge from a large, complex model (often called the teacher model) to a smaller, simpler model (the student model). This process helps the smaller model achieve similar performance to the larger one while being more efficient in terms of computation and memory usage.

Distillation steps: The main steps in knowledge distillation are: [1.] Train the student model by using these predictions, along with the original dataset, to mimic the teacher model’s behavior. And, [2.] use the teacher model to generate predictions for the dataset.

Posted on October 4, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

On September 5, 2025, the Federal Trade Commission (FTC) voted to dismiss its appeals in two court cases, effectively terminating the Biden Administration’s pursuit of a comprehensive noncompete ban. The 3-1 Commission vote represents a fundamental shift in federal competition enforcement strategy.

This Health Capital Topics article reviews the history of the noncompete ban, the FTC’s recent activities regarding competition, and the implications for healthcare organizations. (Read more…)

After a lifetime of hard work practicing medicine and saving, you’re at the retirement finish line. Instead of a paycheck, you’re relying on your nest egg and investment income to cover the bills. Picking the right investments is even more important, as you won’t have much chance to recover as a retired MD, DO, DPM or DDS.

“You made it to the top of the mountain through a systematic approach and are trying to make your way down safely,” says retirement planner John Gillet John Gillet in Hollywood, Fla. “Why throw all caution to the wind and try something different now?”

***

***

Definitions

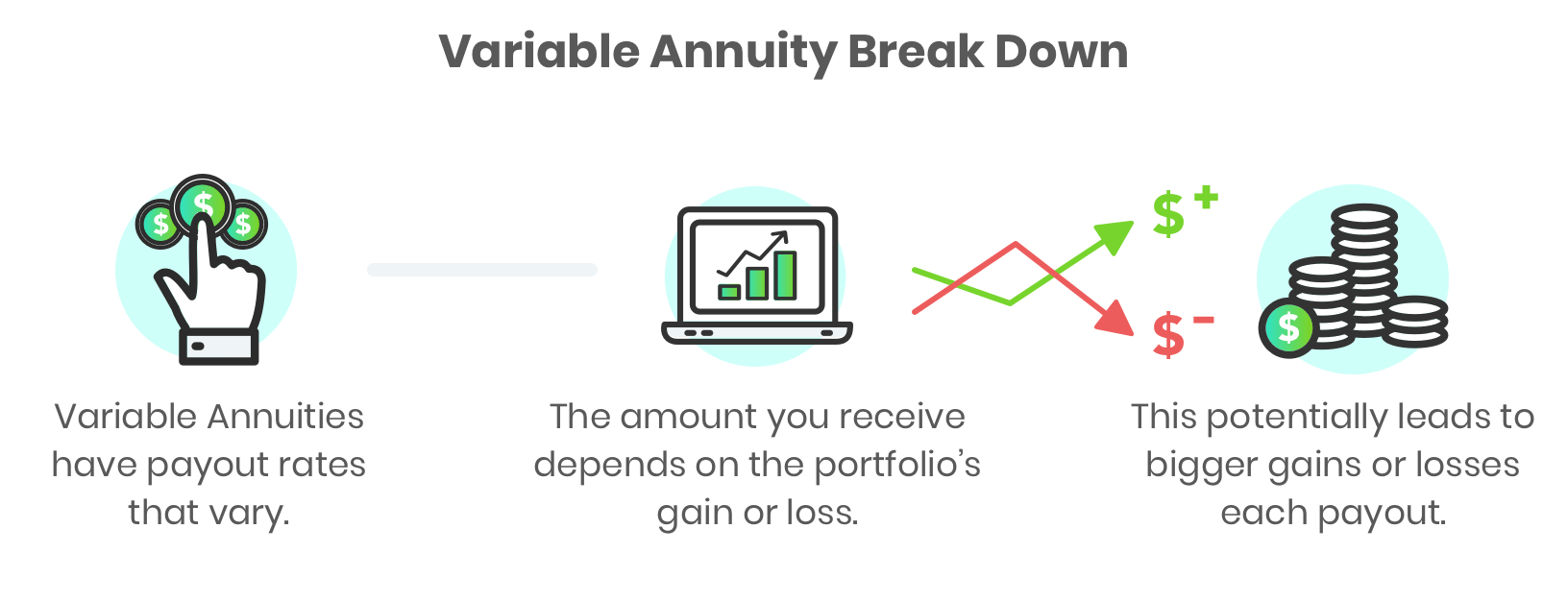

An annuity is an insurance contract designed to grow your money and then repay it as income. There are different versions. An immediate annuity turns your lump sum into future guaranteed income payments, like your own personal pension. They are simple to understand with no or small fees.

Fixed annuities pay a guaranteed interest rate over a set period to grow your money, like 5% a year for five years. These options could make sense as part of a retirement plan.

A variable annuity, on the other hand, invests your savings in mutual funds. While you can buy riders that guarantee a minimum income, you’ll be paying very much for it. “All in, the annual fees can be 3% or more of your balance,” says Jeff Bailey, an advisor from Nashville. “That’s a huge withdrawal rate from your portfolio versus investing on your own.”

The variable annuity will lock up your money for years. If you cancel early, you owe a surrender charge that could start at 7% or more of your annuity balance before gradually going down as time goes by. “Clients believe they can walk away with their contract value, but that’s often not true,” says Bailey.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on October 4, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

OVERHEARD IN THE DOCTOR’S LOUNGE

***

***

By D. Kellus Pruitt DDS

According to money journalists Max Tailwagger and Allan Roth of MoneyWatch, the trade publication Medical Economics Magazine [“advertising supplement”] nearly listed a dog on its’ 2013 list of Best Financial Advisors for Doctors. Indeed, being listed as a top financial advisor in this publication would enhance any advisor’s credibility as well as reach a high income readership.

For example, several advisors in the Financial Planning Association, mentions this prestigious award year after year. And, the NAPFA organization of fee-only financial planners has issued press releases when member advisors make this annual list. In fact, in 2008, it touted that 52/150 listed FAs were NAPFA members.

Yet, the dog is well known in the financial advisory world, having allegedly received a plaque as one of 2009 America’s Top Financial Planners by the Consumers’ Research Council of America, and has appeared in several books including Pound Foolish and Money for Life. The fee for Maxwell Tailwagger CFP® [a five year old Dachshund] was reported to be $750 with $1,000 for a bold listing. Colorado Securities Commissioner Fred Joseph is reported to have said, “Once again, Max is gaining national notoriety for his astute, and almost superhuman, abilities in the financial arena.”

The only two qualifications for the listing were to pay the fee and not have a complaint against them. In 2009, James Putman, then the NAPFA chairman who touted his own Medical Economics award, was charged by the SEC for securities fraud. NAPFA spokesperson Laura Fisher allegedly opined that “NAPFA no longer promotes the Medical Economics Top Advisors for Doctors list. We felt promoting a list that included stock-brokers was inconsistent with NAPFA’s mission to advance the fee-only profession.” When an advisor name drops an honor to you, congratulate him and then ask how s/he achieved the award. Ask how many nominees versus award recipients there were. What were the criteria for selection and how were they nominated. Ask if they had to pay for the honor, and go online to check out the organization.

Then ask yourself this question: If your financial advisor is buying credibility, do you really want to trust your financial future to him or her?

Asset allocation is one of the key factors contributing to long-term investment success.

When designing a portfolio that represents their risk tolerance, investors should be aware that a portfolio that is 50% stocks is likely to obtain approximately half of the gain when the market advances but suffer only half the loss when the market declines.

This general principle frequently holds true over extended investing cycles, but can waiver during shorter holding periods.

Case Model

For example, a fairly typical physician client of mine who has a 50% stock, 50% bond portfolio has obtained a return of 4.62% over the last 12 months, while the S&P 500 has obtained a return of 14.31% over the same time period (as of 10/30/14).

An investor expecting to obtain half the return of the index would anticipate a return of 7.15%, and by this measuring stick, has underperformed the market by over 2.50% during the last year.

What caused this differential?

Answer

The issue resides in how we define “the market.” In this example, we use the S&P 500 index as a measure for how the market as a whole is performing. As you may know, the S&P 500 (and the Dow Jones Industrial Average, for that matter) consists solely of large company U.S. stocks.

Of course, a diversified portfolio owns a mixture of large, mid, and small cap U.S. stocks, as well as international and emerging market equities. Consequently, comparing the performance of a basket of only large cap stocks to the performance of a diversified portfolio made up of a variety of different asset classes isn’t an apples-to-apples comparison.

***

***

Frequently, the diversified portfolio will outperform the non-diversified large cap index because several of the components of the diversified portfolio will obtain higher returns than those achieved by large cap holdings.

However, the past 12 months has been a case where a diversified portfolio underperformed the large cap index because large cap stocks were the best performing asset class over the time period. In fact, over the last twelve months, there has been a direct correlation between company size and stock performance (as of 10/30/14):

Large Cap Stocks (S&P 500): 14.92%

Mid Cap Stocks (Russell Mid Cap): 11.08%

Small Cap Stocks (Russell 2000): 4.45%

International Stocks (Dow Jones Developed Markets): -1.05%

Since large cap stocks were the best performing element of a diversified portfolio over the last 12 months, in retrospect, an investor would have obtained a superior return by owning only large cap stocks during the period as opposed to owning a diversified mix of different equities. Does this mean owning only large cap stocks rather than a diversified portfolio is the best investment approach going forward? Of course not.

Year after year, we don’t know which asset category will provide the best return and a diversified portfolio ensures we have exposure to each year’s big winner. Additionally, although large caps were this year’s winner, they could easily be next year’s big loser, and a diversified portfolio ensures we don’t have all our investment eggs in one basket.

Don’t be overly concerned if your diversified portfolio is underperforming a non-diversified benchmark over a short period of time. As always, long-term results should be more heavily weighted than short-term swings, and having a diversified portfolio is likely to maximize the probability of coming out ahead over an extended period.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Classic: A pre-payment plan refers to health insurance plans that provide medical or hospital benefits in service rather than dollars, such as the plans offered by various Health Maintenance Organizations. A method providing in advance for the cost of predetermined benefits for a population group, through regular periodic payments in the form of premiums, dues, or contributions including those contributions that are made to a health and welfare fund by employers on behalf of their employees!

Modern: A Prepaid Group Practice Plan specifies health services are rendered by participating physicians to an enrolled group of persons, with a fixed periodic payment made in advance by (or on behalf of) each person or family. If a health insurance carrier is involved, a contract to pay in advance for the full range of health services to which the insured is entitled under the terms of the health insurance contract.

Examples:

Pre-Paid Hospital Service Plan: The common name for a health maintenance organization (HMO), a plan that provides comprehensive health care to its members, who pay a flat annual fee for services.

Pre-Paid Premium: An insurance or other premium payment paid prior to the due date. In insurance, payment by the insured of future premiums, through paying the present (discounted) value of the future premiums or having interest paid on the deposit.

Pre-Paid Prescription Plan: A drug reimbursement plan that is paid in advance.

ME-P readers might believe the hedge fund industry is a small, exclusive club of elites, rich investors. But a new count by Preqin shows that it’s actually a large—and growing—sector of investing.

In fact, there may be more hedge funds globally (30,000+) than Burger King locations (18,700), and more more hedge fund managers than Taco Bell managers, per the FTE

Posted on October 1, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS!

UNITED STATES GOVERNMENT SHUTS DOWN

***

By Health Capital Consultants, LLC

***

***

With hours to go until the midnight deadline on September 30th, 2025 to fund the government, lawmakers appear deadlocked over whether certain healthcare provisions should be included in the temporary funding bill.

Should this deadlock continue, the federal government will shut down beginning today October 1st and remain shut down until that deadlock is resolved.

This Health Capital Topics article provides an update on the developing saga. (Read more…)

Sometimes debt is a necessary tool in building wealth

Using debt to build wealth might seem counterintuitive. After all, when you calculate your wealth, you look at what you own (assets) and subtract what you owe (debts and liabilities) to determine what your net worth (wealth) is.

It’s easy to oversimplify that debt is bad and is harmful to your wealth. Because some debt is really harmful, like credit cards, automobile, debt gets lumped into the category of “bad.”

But some types of debt can be useful and sometimes necessary to create wealth; home, education, business, etc. For folks that don’t readily have access to large sums of cash or capital, debt may be the tool that allows them to expand.

Yourmedical practice. Your personal goals. Your financial plan. Our experienced confirmation guide.

***

***

When you know exactly where you are today, have a vision of where you want to be tomorrow, and have trusted counsel at your side, you have already achieved so much success. Marcinko Associates works to keep you at that level of confidence every day. We use a comprehensive economic process to uncover what’s most important to you and then develop a financial strategy that gives you the highest probability of achieving your monetary goals.

We assess, plan, and opine for your success

To accurately see where you are today, chart a strategic path to your goals and help you make the most informed decisions to keep you on financial track, our key services for physicians and high net worth medical clients include:

Investment Portfolio Review

Fee, Charge and Cost Review

Comprehensive Financial Planning

Insurance Reviews

Estate Planning

Investment and Asset Management Second Opinions

We take a deep dive into your financial retirement plans

Physicians and dental employers now have options for how to design and deliver retirement benefits and we can help you make the best choice for your healthcare business. Our services for retirement plans include:

Fee, Charges & Fiduciary Review

Portfolio Analysis

Single Employer Retirement Plan Advisory

Retirement Plans Risk Analysis

Capital Funding and Financing

Business Planning and Practice Valuations

Career Development

and more!

We take a broad and balanced look at your financial life life

We coordinate our recommendations with your other advisors, including attorneys, accountants, insurance professionals and others, to ensure each decision is consistent with your goals and overall strategy. For example, through our partnerships we offer physician colleagues deeper expanded advisory services, like:

The major indexes ticked lower last week, though, as artificial intelligence names like Oracle got hit after some analysts expressed concerns over the eye-watering costs of the AI build-out.

In the case of financial investments, compounding interest relies on time to reveal its true magic.

Here’s how: a young investor can invest less money over a longer period of time than an older investor who invests more money over a shorter period and ends up with more in the end. Compounding returns grow exponentially, making time more than an ally – but a force of the universe driving growth.

Time is certainly our ally in investing, but according to ME-P Editor Dr. David Edward Marcinko MBA MEd, you’ll kick yourself wishing you had invested earlier when you witness compounding after a few years (or a decade).

Posted on September 29, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I. and Staff Reporters

***

A meme is an idea, behavior, or style that spreads by means of imitation from person to person within a culture and often carries symbolic meaning representing a particular phenomenon or theme. A meme acts as a unit for carrying cultural ideas, symbols, or practices, that can be transmitted from one mind to another through writing, speech, gestures, rituals, or other imitable phenomena with a mimicked theme. Supporters of the concept regard memes as cultural analogues to genes in that they self-replicate, mutate, and respond to selective pressure. In popular language, a meme may refer to an internet meme, typically an image, that is remixed, copied, and circulated in a shared cultural experience online.

EXAMPLE Investing Meme:

“Sell in May and Go Away” is an investment strategy for stocks based on a theory (sometimes known as the Halloween indicator) that the period from November to April inclusive has significantly stronger stock market growth on average than the other months. In such strategies, stock holdings are sold or minimized at about the start of May and the proceeds held in cash; stocks are bought again in the autumn. So, “Sell in May” can be characterized as the memetic belief that it is better to avoid holding stock during the summer period.

The Wall Street adage — ‘Sell Rosh Hashana; buy Yom Kippur’ — focuses on the market’s performance between these two Jewish holidays. This seasonal stock-market trading pattern is upon us — and worth observing.

Rosh Hashanah is the Jewish New Year while Yom Kippur is the Day of Atonement. So, according to Mark Hulbert, it might seem arbitrary to make stock-investment decisions by blending religious observance with financial strategy, but there’s one old trading folklore commonly or meme mentioned during this time of year: “Sell Rosh Hashanah, buy Yom Kippur.”

This Wall Street adage suggests that U.S. stocks tend to fall over the 10 days the Jewish High Holidays are observed, so investors would be better off selling beforehand and buying afterward. But some market analysts believe investors should be wary of this seasonal trading pattern this year.

Historically, the “sell Rosh Hashanah, buy Yom Kippur” strategy is closely tied to the stock market’s tendency to under perform in September, with investors often looking to “minimize exposure” during this period, according to Yehuda Leibler, chief strategy and technology officer at ARX Advisory.

Hobson’s choice is a free choice in which only one thing is actually offered. The term is often used to describe an illusion that choices are available. The best known example is “I’ll give you a choice: Take it or leave it”, wherein “leaving it” is strongly undesirable.

The phrase is said to have originated with Thomas Hobson (1544–1631), a livery stable owner in Cambridge, England, who offered customers the choice of either taking the horse in the stall nearest to the door or taking none at all.

A CASE MODEL

Half of Physicians Plan to Change Career Paths

The Physicians Foundation recently conducted a survey on physician practice patterns and perspectives. Here are some key findings from the report:

• 31% of physicians identify as independent practice owners or partners. • Almost half (47%) of physicians plan to change career paths. • 78% of physicians sometimes, often or always experience feelings of burnout. • Nearly a quarter of physician time is spent on non-clinical paperwork.

This result is not a good Hobson’s Choice in Medicine.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com