BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

“THE INVESTOR’S CHIEF problem—even his worst enemy—is likely to be himself.” So wrote Benjamin Graham, the father of modern investment analysis.

With these words, written in 1949, Graham acknowledged the reality that investors are human. Though he had written an 800 page book on techniques to analyze stocks and bonds, Graham understood that investing is as much about human psychology as it is about numerical analysis.

In the decades since Graham’s passing, an entire field has emerged at the intersection of psychology and finance. Known as behavioral finance, its pioneers include Daniel Kahneman, Amos Tversky and Richard Thaler. Together, they and their peers have identified countless human foibles that interfere with our ability to make good financial decisions. These include hindsight bias, recency bias and overconfidence, among others. On my bookshelf, I have at least as many volumes on behavioral finance as I do on pure financial analysis, so I certainly put stock in these ideas.

At the same time, I think we’re being too hard on ourselves when we lay all of these biases at our feet. We shouldn’t conclude that we’re deficient because we’re so susceptible to biases. Rather, the problem is that finance isn’t a scientific field like math or physics. At best, it’s like chaos theory. Yes, there is some underlying logic, but it’s usually so hard to observe and understand that it might as well be random. The world of personal finance is bedeviled by paradoxes, so no individual—no matter how rational—can always make optimal decisions.

As we plan for our financial future, I think it’s helpful to be cognizant of these paradoxes. While there’s nothing we can do to control or change them, there is great value in being aware of them, so we can approach them with the right tools and the right mindset.

Here are just seven of the paradoxes that can bedevil financial decision-making:

There’s the paradox that all of the greatest fortunes—Carnegie, Rockefeller, Buffett, Gates—have been made by owning just one stock. And yet the best advice for individual investors is to do the opposite: to own broadly diversified index funds.

There’s the paradox that the stock market may appear overvalued and yet it could become even more overvalued before it eventually declines. And when it does decline, it may be to a level that is even higher than where it is today.

There’s the paradox that we make plans based on our understanding of the rules—and yet Congress can change the rules on us at any time, as it did just last year.

There’s the paradox that we base our plans on historical averages—average stock market returns, average interest rates, average inflation rates and so on—and yet we only lead one life, so none of us will experience the average.

There’s the paradox that we continue to be attracted to the prestige of high-cost colleges, even though a rational analysis that looks at return on investment tells us that lower-cost state schools are usually the better bet.

There’s the paradox that early retirement seems so appealing—and has even turned into a movement—and yet the reality of early retirement suggests that we might be better off staying at our desks.

There’s the paradox that retirees’ worst fear is outliving their money and yet few choose the financial product that is purpose-built to solve that problem: the single-premium immediate annuity.

How should you respond to these paradoxes? As you plan for your financial future, embrace the concept of “loosely held views.”

In other words, make financial plans, but continuously update your views, question your assumptions and rethink your priorities.

A hedge fund is a limited partnership of private investors whose money is pooled and managed by professional fund managers. These managers use a wide range of strategies, including leverage (borrowed money) and the trading of nontraditional assets, to earn above-average investment returns. A hedge fund investment is often considered a risky, alternative investment choice and usually requires a high minimum investment or net worth. Hedge funds typically target wealthy investors.

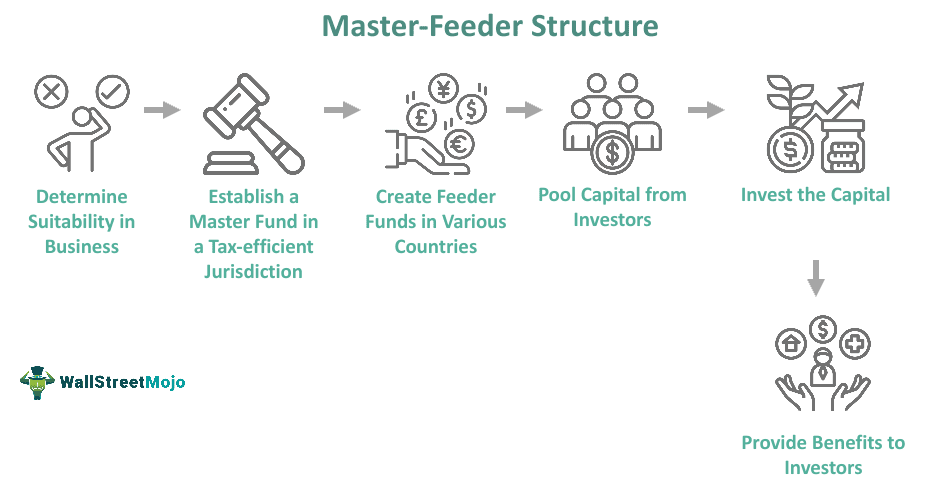

The hedge fund manager I am considering also runs an offshore fund under a “master feeder” arrangement.

A PHYSICIAN’S QUESTION:What does this mean? In which fund should I invest?

The master feeder arrangement is a two-tiered investment structure whereby investors invest in the feeder fund. The feeder fund in turn invests in the master fund. The master fund is therefore the one that is actually investing in securities. There may be multiple feeder funds under one master fund. Feeder funds under the same master can differ drastically in terms of fees charged, minimums required, types of investors, and many other features – but the investment style will be the same because only the master actually invests in the market.

A master feeder structure is a very popular arrangement because it allows a portfolio manager to pool both onshore and offshore assets into one investment vehicle (the master fund) that allocates gains and losses in an asset-based, proportional manner back to the onshore and offshore investors. All investors, both offshore and onshore, get the same return. In this manner, the portfolio manager, despite offering more than one fund with different characteristics to different populations, is not faced with the dilemma of which fund to favor with the best investment ideas.

A manager may offer an offshore fund because there is demand for that manager’s skill either abroad, where investors may wish to preserve anonymity, or more commonly where investors simply do not wish to become entangled with the United States tax code. American citizens should generally avoid the offshore fund, since American citizens are taxed on their allocated share of offshore corporation profits whether or not a distribution occurs. Therefore, there is no benefit for most American taxpayers investing in an offshore fund.

Tax-exempt institutions, such as medical foundations, in the United States may have reason to consider an offshore hedge fund, however. Domestic tax-exempt organizations are generally not subject to unrelated business taxable income (UBTI) – the portion of hedge fund income that comes about as a result of the use of leverage – when investing with an offshore corporation. If the same tax-exempt organization were to invest in a domestic fund, and if UBTI was generated, then the organization would have to pay taxes on that UBTI. Most domestic hedge funds generate UBTI.

Sometimes debt is a necessary tool in building wealth

Using debt to build wealth might seem counterintuitive. After all, when you calculate your wealth, you look at what you own (assets) and subtract what you owe (debts and liabilities) to determine what your net worth (wealth) is.

It’s easy to oversimplify that debt is bad and is harmful to your wealth. Because some debt is really harmful, like credit cards, automobile, debt gets lumped into the category of “bad.”

But some types of debt can be useful and sometimes necessary to create wealth; home, education, business, etc. For folks that don’t readily have access to large sums of cash or capital, debt may be the tool that allows them to expand.

Yourmedical practice. Your personal goals. Your financial plan. Our experienced confirmation guide.

***

***

When you know exactly where you are today, have a vision of where you want to be tomorrow, and have trusted counsel at your side, you have already achieved so much success. Marcinko Associates works to keep you at that level of confidence every day. We use a comprehensive economic process to uncover what’s most important to you and then develop a financial strategy that gives you the highest probability of achieving your monetary goals.

We assess, plan, and opine for your success

To accurately see where you are today, chart a strategic path to your goals and help you make the most informed decisions to keep you on financial track, our key services for physicians and high net worth medical clients include:

Investment Portfolio Review

Fee, Charge and Cost Review

Comprehensive Financial Planning

Insurance Reviews

Estate Planning

Investment and Asset Management Second Opinions

We take a deep dive into your financial retirement plans

Physicians and dental employers now have options for how to design and deliver retirement benefits and we can help you make the best choice for your healthcare business. Our services for retirement plans include:

Fee, Charges & Fiduciary Review

Portfolio Analysis

Single Employer Retirement Plan Advisory

Retirement Plans Risk Analysis

Capital Funding and Financing

Business Planning and Practice Valuations

Career Development

and more!

We take a broad and balanced look at your financial life life

We coordinate our recommendations with your other advisors, including attorneys, accountants, insurance professionals and others, to ensure each decision is consistent with your goals and overall strategy. For example, through our partnerships we offer physician colleagues deeper expanded advisory services, like:

As human beings, our brains are booby-trapped with psychological barriers that stand between making smart financial decisions and making dumb ones. The good news is that once you realize your own mental weaknesses, it’s not impossible to overcome them.

In fact, Mandi Woodruff, a financial reporter whose work has appeared in Yahoo! Finance, Daily Finance, The Wall Street Journal, The Fiscal Times and the Financial Times among others; related the following mind-traps in a September 2013 essay for the finance vertical Business Insider; as these impediments are now entering the lay-public zeitgeist:

Anchoring happens when we place too much emphasis on the first piece of information we receive regarding a given subject. For instance, when shopping for a wedding ring a salesman might tell us to spend three months’ salary. After hearing this, we may feel like we are doing something wrong if we stray from this advice, even though the guideline provided may cause us to spend more than we can afford.

Myopia makes it hard for us to imagine what our lives might be like in the future. For example, because we are young, healthy, and in our prime earning years now, it may be hard for us to picture what life will be like when our health depletes and we know longer have the earnings necessary to support our standard of living. This short-sightedness makes it hard to save adequately when we are young, when saving does the most good.

Gambler’s fallacy occurs when we subconsciously believe we can use past events to predict the future. It is common for the hottest sector during one calendar year to attract the most investors the following year. Of course, just because an investment did well last year doesn’t mean it will continue to do well this year. In fact, it is more likely to lag the market.

Avoidance is simply procrastination. Even though you may only have the opportunity to adjust your health care plan through your employer once per year, researching alternative health plans is too much work and too boring for us to get around to it. Consequently, we stick with a plan that may not be best for us.

Loss aversion affected many investors during the stock market crash of 2008. During the crash, many people decided they couldn’t afford to lose more and sold their investments. Of course, this caused the investors to sell at market troughs and miss the quick, dramatic recovery.

Overconfident investing happens when we believe we can out-smart other investors via market timing or through quick, frequent trading. Data convincingly shows that people who trade most often under perform the market by a significant margin over time.

Mental accounting takes place when we assign different values to money depending on where we get it from. For instance, even though we may have an aggressive saving goal for the year, it is likely easier for us to save money that we worked for than money that was given to us as a gift.

Herd mentality makes it very hard for humans to not take action when everyone around us does. For example, we may hear stories of people making significant profits buying, fixing up, and flipping homes and have the desire to get in on the action, even though we have no experience in real estate.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

A Financial Self Discovery Questionnairefor Medical Professionals

For understanding your relationship with money, it is important to be aware of yourself in the contexts of culture, family, value systems and experience. These questions will help you. This is a process of self-discovery. To fully benefit from this exploration, please address them in writing. You will simply not get the full value from it if you just breeze through and give mental answers. While it is recommended that you first answer these questions by yourself, many people relate that they have enjoyed the experience of sharing them with others who are important to them.

As you answer these questions, be conscious of your feelings, actually describing them in writing as part of your process.

Childhood

What is your first memory of money?

What is your happiest moment with Money? Your most unhappy?

Name the miscellaneous money messages you received as a child.

How were you confronted with the knowledge of differing economic circumstances among people, that there were people “richer” than you and people “poorer” than you?

Cultural heritage

What is your cultural heritage and how has it interfaced with money?

To the best of your knowledge, how has it been impacted by the money forces? Be specific.

To the best of your knowledge, does this circumstance have any motive related to Money?

Speculate about the manners in which your forebears’ money decisions continue to affect you today?

Family

How is/was the subject of money addressed by your church or the religious traditions of your forebears?

What happened to your parents or grandparents during the Depression?

How did your family communicate about money?

How? Be as specific as you can be, but remember that we are more concerned about impacts upon you than historical veracity.

When did your family migrate to America (or its current location)?

What else do you know about your family’s economic circumstances historically?

Your parents

How did your mother and father address money?

How did they differ in their money attitudes?

How did they address money in their relationship?

Did they argue or maintain strict silence?

How do you feel about that today?

Please do your best to answer the same questions regarding your life or business partner(s) and their parents.

Childhood: Revisited

How did you relate to money as a child? Did you feel “poor” or “rich”? Relatively? Or, absolutely? Why?

Were you anxious about money? Did you receive an allowance? If so, describe amounts and responsibilities.

Did you have household responsibilities?

Did you get paid regardless of performance?

Did you work for money?

If not, please describe your thoughts and feelings about that.

***

***

Same questions, as a teenager, young adult, older adult.

Credit

When did you first acquire something on credit?

When did you first acquire a credit card?

What did it represent to you when you first held it in your hands?

Describe your feelings about credit.

Do you have trouble living within your means?

Do you have debt?

Adulthood

Have your attitudes shifted during your adult life? Describe.

Why did you choose your personal path? a) Would you do it again? b) Describe your feelings about credit.

Adult attitudes

Are you money motivated? If so, please explain why? If not, why not? How do you feel about your present financial situation? Are you financially fearful or resentful? How do you feel about that?

Will you inherit money? How does that make you feel?

If you are well off today, how do you feel about the money situations of others? If you feel poor, same question.

How do you feel about begging? Welfare? If you are well off today, why are you working?

Do you worry about your financial future?

Are you generous or stingy? Do you treat? Do you tip?

Do you give more than you receive or the reverse? Would others agree?

Could you ask a close relative for a business loan? For rent/grocery money?

Could you subsidize a non-related friend? How would you feel if that friend bought something you deemed frivolous?

Do you judge others by how you perceive they deal with their Money? Do you feel guilty about your prosperity? Are your siblings prosperous?

What part does money play in your spiritual life?

Do you “live” your Money values?

Conclusion

There may be other questions that would be useful to you. Others may occur to you as you progress in your life’s journey. The point is to know your personal money issues and their ramifications for your life, work, and personal mission.

This will be a “work-in-process” with answers both complex and incomplete. Don’t worry.

Just incorporate fine-tuning into your life’s process.

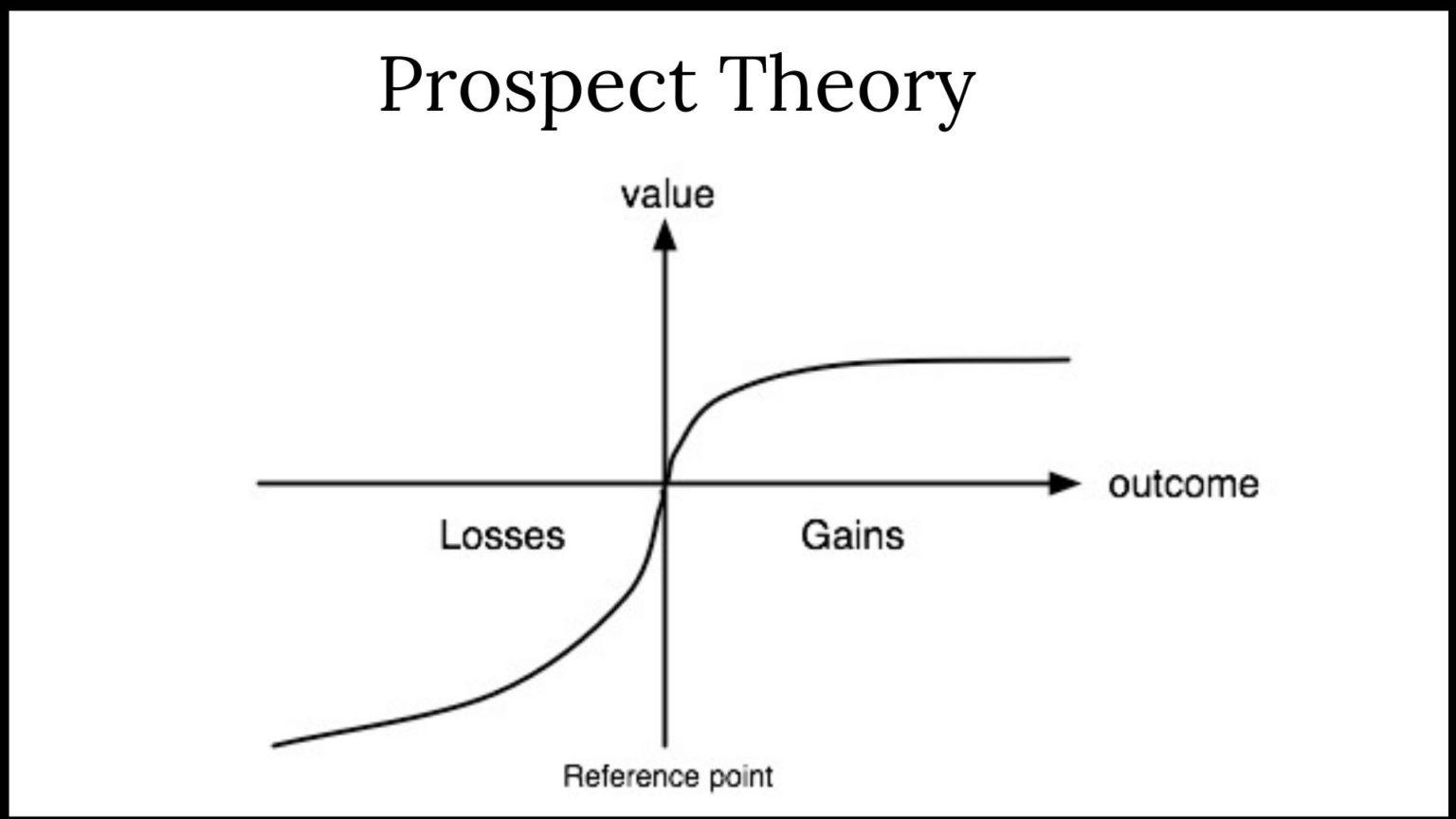

The study of behavioral economics has revealed much about how different biases can affect our finances—often for the worse.

Take loss aversion: Because we feel a financial setback more acutely than a commensurate gain, we often cling to failed investments to avoid realizing the loss. Another potential hazard is present bias, or the tendency to prefer instant gratification over long-term reward, even if the latter gain is greater.

When it comes to money, sometimes it’s difficult to make rational decisions. Here, are three behavioral financial biases that could be impeding financial goals.

ANCHORING BIAS

Anchoring Bias happens when we place too much emphasis on the first piece of information we receive regarding a given subject. Anchoring is the mental trick your brain plays when it latches onto the first piece of information it gets, no matter how irrelevant. You might know this as a ‘first impression’ when someone relies on their own first idea of a person or situation.

Example: When shopping for a wedding ring a salesman might tell us to spend three months’ salary. After hearing this, we may feel like we are doing something wrong if we stray from this financial advice, even though the guideline provided may cause us to spend more than we can afford.

Example: Imagine you’re buying a car, and the salesperson starts with a high price. That number sticks in your mind and influences all your subsequent negotiations. Anchoring can skew our decisions and perceptions, making us think the first offer is more important than it is. Or, subsequent offers lower than they really are.

Example: Imagine an investor named Jane who purchased 100 shares of XYZ Corporation at $100 per share several years ago. Over time, the stock price declined to $60 per share. Jane is anchored to her initial price of $100 and is reluctant to sell at a loss because she keeps hoping the stock will return to her original purchase price. She continues to hold onto the stock, even as it declines, due to her anchoring bias. Eventually, the stock price drops to $40 per share, resulting in significant losses for Jane.

In this example, Jane’s nchoring bias to the original purchase price of $100 prevents her from rationalizing to sell the stock and cut her losses, even though market conditions have changed. So, the next time you’re haggling for your self, a potential customer or client, or making another big financial decision, be aware of that initial anchor dragging you down.

HERD MENTALITY BIAS

Herd Mentality Bias makes it very hard for humans to not take action when everyone around us does.

Example: We may hear stories of people making significant monetary profits buying, fixing up, and flipping homes and have the desire to get in on the action, even though we have no experience in real estate.

Example: During the dotcom bubble of the late 1990’s many investors exhibited a herd mentality. As technology stocks soared to astronomical valuations, investors rushed to buy these stocks driven by the fear of missing out on the gains others were enjoying. Even though some of these stocks had questionable fundamentals, the herd mentality led investors to follow the crowd.

In this example, the herd mentality contributed to the overvaluation of technology stocks. Eventually, it led to the dot-com bubble’s burst, causing significant losses for those who had unthinkingly followed the crowd without conducting proper research or analysis.

OVERCONFIDENT INVESTING BIAS

Overconfident Investing Bias happens when we believe we can out-smart other investors via market timing or through quick, frequent trading. This causes the results of a study to be unreliable and hard to reproduce in other research settings.

Example: Data convincingly shows that people and financial planners/advisors and wealth managers who trade most often under-perform the market by a significant margin over time. Active traders lose money.

Example: Overconfidence Investing Bias moreover leads to: (1) excessive trading (which in turn results in lower returns due to costs incurred), (2) underestimation of risk (portfolios of decreasing risk were found for single men, married men, married women, and single women), (3) illusion of knowledge (you can get a lot more data nowadays on the internet) and (4) illusion of control (on-line trading).

ASSESSMENT

Finally, questions remain after consuming this cognitive bias review.

Question: Can behavioral cognitive biases be eliminated by financial advisors in prospecting and client sales endeavors?

A: Indeed they can significantly reduce their impact by appreciating and understanding the above and following a disciplined and rational decision-making sales process.

Question: What is the role of financial advisors in helping clients and prospects address behavioral biases?

A: Financial advisors can provide an objective perspective and help investors recognize and address their biases. They can assist in creating well-structured investment and financial plans, setting realistic goals, and offering guidance to ensure investment decisions align with long-term objectives.

Question:How important is self-discipline in overcoming behavioral biases?

A; Self-discipline is crucial in overcoming behavioral biases. It helps investors and advisors adhere to their investment plans, avoid impulsive decisions, and stay focused on long-term goals reducing the influence of emotional and cognitive biases.

CONCLUSION

Remember, it is far more useful to listen to client beliefs, fears and goals, and to suggest options and offer encouragement to help them discover their own path toward financial well-being. Then, incentivize them with knowledge of the above psychological biases to your mutual success!

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

REFERENCES:

Marcinko, DE; Dictionary of Health Insurance and Managed Care. Springer Publishing Company, New York, 2007.

Marcinko, DE: Comprehensive Financial Planning Strategies for Doctors and Advisors: Best Practices from Leading Consultants and Certified Medical Planners™. Productivity Press, NY, 2016.

Marcinko, DE: Risk Management, Liability and Insurance Strategies for Doctors and Advisors: Best Practices from Leading Consultants and Certified Medical Planners™. Productivity Press, NY, 2017.

Nofsinger, JR: The Psychology of Investing. Rutledge Publishing, 2022

Winters, Scott: The 10X Financial Advisor: Your Blueprint for Massive and Sustainable Growth. Absolute Author Publishing House, 2020.

A paradox is a statement or situation that seems contradictory but actually makes sense when you think about it more deeply. It challenges logic and often reveals a hidden truth.

FLEXIBLY DOGMATIC PARADOX

The Flexibly Dogmatic Paradox suggests that no matter how sensible your financial planning, investing or wealth management process is there will be uncomfortably long periods when it looks broken. And process is the best way of ensuring you keep standing for something because if you don’t stand for something, you’ll fall for anything. This is why, when assessing an investment fund, focus 50% on the manager’s character and 50% on their process. Everything else is detail. There are few guarantees in investing, but the fact that markets will batter you emotionally is one of them.

Example: During volatile times, the temptation to abandon the process is strong. But that’s why it’s there. Process is what forces one fund manager to keep buying unbroken companies when everyone else thinks they’re bust, and another to keep faith with a top-quality company when the mob says it’s too expensive The best fund managers dogmatically stick to their process when it’s out of favor. Then, when it returns to favor, the elastic pings back: they recapture lost ground surprisingly fast. However, every rule has an exception. And spotting the exceptions to their process is something the true greats have a knack for buying and selling.

***

***

Example: In 2007, US value manager Bill Miller had the makings of an investment legend, but the financial crisis wrecked all that. His process told him to double down into falling share prices, which had worked well for years. But it doesn’t work if the companies go bust, which many of his financial stocks did in 2008.

The fact is that no matter how good it is, a process operated without human judgment is just an algorithm. The best fund managers and financial prospectors and sales men/women know this.

They stick dogmatically to their process but somehow remain flexible enough to spot the occasions when it’s about to drive them into a brick wall.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Here are some of the most common risks associated with fixed income securities.

Interest Rate Risk

The market value of the securities will be inversely affected by movements in interest rates. When rates rise, market prices of existing debt securities fall as these securities become less attractive to investors when compared to higher coupon new issues. As prices decline, bonds become cheaper so the overall return, when taking into account the discount, can compete with newly issued bonds at higher yields. When interest rates fall, market prices on existing fixed income securities tend to rise because these bonds become more attractive when compared to the newly issued bonds priced at lower rates.

Price Risk

Investors who need access to their principal prior to maturity have to rely on the secondary market to sell their securities. The price received may be more or less than the original purchase price and may depend, in general, on the level of interest rates, time to term, credit quality of the issuer and liquidity.

Among other reasons, prices may also be affected by current market conditions, or by the size of the trade (prices may be different for 10 bonds versus 1,000 bonds), etc. It is important to note that selling a security prior to maturity may affect actual yield received, which may be different than the yield at which the bond was originally purchased. This is because the initially quoted yield assumed holding the bond to term. As mentioned above, there is an inverse relationship between interest rates and bond prices. Therefore, when interest rates decline, bond prices increase, and when interest rates increase, bond prices decline.

Generally, longer maturity bonds will be more sensitive to interest rate changes. Dollar for dollar, a long-term bond should go up or down in value more than a short-term bond for the same change in yield. Price risk can be determined through a statistic called duration, which is featured at the end of the fixed income section.

Liquidity risk is the risk that an investor will be unable to sell securities due to a lack of demand from potential buyers, sell them at a substantial loss and/or incur substantial transaction costs in the sale process. Broker/dealers, although not obligated to do so, may provide secondary markets.

Reinvestment Risk

Downward trends in interest rates also create reinvestment risk, or the risk that the income and/or principal repayments will have to be invested at lower rates. Reinvestment risk is an important consideration for investors in callable securities. Some bonds may be issued with a call feature that allows the issuer to call, or repay, bonds prior to maturity. This generally happens if the market rates fall low enough for the issuer to save money by repaying existing higher coupon bonds and issuing new ones at lower rates. Investors will stop receiving the coupon payments if the bonds are called. Generally, callable fixed income securities will not appreciate in value as much as comparable non-callable securities.

Similar to call risk, prepayment risk is the risk that the issuer may repay bonds prior to maturity. This type of risk is generally associated with mortgage-backed securities. Homeowners tend to prepay their mortgages at times that are advantageous to their needs, which may be in conflict with the holders of the mortgage-backed securities. If the bonds are repaid early, investors face the risk of reinvesting at lower rates.

Purchasing Power Risk

Fixed income investors often focus on the real rate of return, or the actual return minus the rate of inflation. Rising inflation has a negative impact on real rates of return because inflation reduces the purchasing power of the investment income and principal.

Posted on August 26, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

Types of investments

Once a physician [MD, DO, DPM or DDS] has a brokerage account, the young doctior will need to decide what to invest in. There are lots of options, and each comes with different benefits and drawbacks. Here are some of the most common options for new physician investors.

Stocks are the first thing most people think about when they are considering investing, but they are not the only option. The prices of stocks change daily, sometimes by large amounts, as the market adjusts to news and various cycles. For that reason, it’s important to do your research. If you’re just beginning with a retirement account, you could also consider the longer-term products listed below.

Index funds and mutual funds.

Index funds attempt to replicate the performance of an un-managed market index. The performance of mutual funds [open and closed] varies. You can often get involved for a lower initial investment, and they can provide good diversification,which makes your portfolio better equipped to handle market fluctuations [active and passive].

For that reason, many financial experts say they should form the core of your retirement portfolio. While they have many similar characteristics, there are important differences. Read more about some of the differences in index funds and mutual funds.

These technically aren’t investment products; they are a contract between you and an insurance company. However, they work to accomplish a similar goal. There are immediate annuities that convert some of your existing savings into lifetime payments, but if we’re talking about saving for retirement, a deferred income annuity is the closest comparison. You make premium payments into the deferred annuity on a regular or irregular basis depending on the contract terms, and when you reach retirement age, you annuitize those savings and receive payments for the rest of your life. They can make a valuable addition to a retirement savings strategy.

Other investments.

There are many other types of investments and financial vehicles: bonds [local, state or US], money market funds, certificates of deposit through a brokerage account or investment apps. Even the cash value of life insurance can play a part. They are all designed to address different needs and have benefits and drawbacks and may be important to your overall strategy.

Crypto.com is a cryptocurrency company based in Singapore that offers various financial services, including an app, exchange, and noncustodial DeFi wallet, NFT marketplace, and direct payment service in cryptocurrency. As of 2024, the company reportedly had more than 100 million customers and more than 4,000 employees.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The so-called money factor (abbreviated as MF on invoices) is a number in a decimal form that dealers use to calculate the APR of a car lease. It’s a major part of your monthly payment and dealers are known to jack up the money factor to pad their profits.

Most doctors don’t ask to see it because they’re not aware of it or don’t know how to calculate it. Ask to see the money factor, then multiply it by 2,400.

For example, if the money factor is .00150, you multiply it by 2,400 to get 3.6%. If that’s higher than the prevailing rate, you have room to talk them down.

How to reduce it

So how do you get a good interest rate when you lease a vehicle? The same way you do when borrowing for any other reason, whether it’s buying a home or applying for a personal loan: by having good credit. This may reduce your interest rate because you’ll represent a lower risk to a lender.

A high residual value on the car could also help you get a better interest rate. A higher residual value means you’d have lower monthly payments because there would be less depreciation on the vehicle. Since interest is applied to your monthly payment, a lower monthly payment would equate to reduced interest charges.

The money factor is one of the many numbers you may want to learn about when leasing a car. It’s one of the transactional costs that come with leasing, and allows dealers and finance companies to make a profit on every lease they execute. As a consumer, it’s a smart idea to learn the financial implications of this number and how it’ll affect your overall costs over the course of a multi-year lease.

***

***

If the interest rate is too high, you may need to shop around for a better rate, negotiate with the dealer or lender to lower the money factor, or consider leasing another vehicle that’s more in line with your budget. Either way, make sure you explore all your financial options before taking a car off the lot.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

There’s an aspect to retirement that many physicians do not plan for … the transition from work and practice to retirement. Your work has been an important part of your life. That’s why the emotional adjustments of retirement may be some of the most difficult ones.

For example, what would you like to do in retirement? Your retirement vision will be unique to you. You are retiring to something not from something that you envisioned. When you have more time, you would like to do more traveling, play golf or visit more often, family and friends. Would you relocate closer to your kids? Learn a new art or take a new class? Fund your grandchildren’s education? Do you have philanthropic goals? Perhaps you would like to help your church, school or favorite charity? If your net worth is above certain limits, it would be wise to take a serious look at these goals. With proper planning, there might be some tax benefits too. Then you have to figure how much each goal is going to cost you.

If you have a list of retirement goals, you need to prioritize which goal is most important. You can rate them on a scale of 1 to 10; 10 being the most important. Then, you can differentiate between wants and needs. Needs are things that are absolutely necessary for you to retire; while wants are things that still allow retirement but would just be nice to have.

Recent studies indicate there are three phases in retirement, each with a different spending pattern [Richard Greenberg CFP®, Gardena CA, personal communication]. The three phases are:

The Early Retirement Years. There is a pent-up demand to take advantage of all the free time retirement affords. You can travel to exotic places, buy an RV and explore forty-nine states, go on month-long sailing vacations. It’s possible during these years that after-tax expenses increase during these initial years, especially if the mortgage hasn’t been paid off yet. Usually the early years last about ten years until most retirees are in their 70’s.

Middle Years. People decide to slow down on the exploration. This is when people start simplifying their life. They may sell their house and downsize to a condo or townhouse. They may relocate to an area they discovered during their travels, or to an area close to family and friends, to an area with a warm climate or to an area with low or no state taxes. People also do their most important estate planning during these years. They are concerned about leaving a legacy, taking care of their children and grandchildren and fulfilling charitable intent. This a time when people spend more time in the local area. They may start taking extension or college classes. They spend more time volunteering at various non-profits and helping out older and less healthy retirees. People often spend less during these years. This period starts when a retiree is in his or her mid to late 70’s and can last up to 20 years, usually to mid to late-80’s.

Late Years. This is when you may need assistance in our daily activities. You may receive care at home, in a nursing home or an assisted care facility. Most of the care options are very expensive. It’s possible that these years might be more expensive than your pre-retirement expenses. This is especially true if both spouses need some sort of assisted care. This period usually starts when the retiree is their 80’s; however they can sometimes start in the middle to the late 70’s.

***

***

[A] Planning issues – early career

Most retirement lifestyle issues do not have to be addressed at this point. Keeping a healthy, balanced lifestyle will help to ensure a more productive retirement. This is the time to focus on the financial aspects of retirement planning.

[B] Planning issues – mid career

If early retirement is a major objective, start thinking about activities that will fill up your time during retirement. Maintaining your health is more critical, since your health habits at this time will often dictate how healthy you will be in retirement

[C] Planning issues – late career

Three to five years before you retire, start making the transition from work to retirement.

Try out different hobbies;

Find activities that will give you a purpose in retirement;

Establish friendships outside of the office or hospital;

Discuss retirement plans with your spouse.

If you plan to relocate to a new place, it is important to rent a place in that area and stay for few months and see if you like it. Making a drastic change like relocating and then finding you don’t like the new town or state might be very costly mistake. The key is to gradually make the transition.

For physicians, like most folks, retirement is the stage in life when one chooses to leave the workforce and live off sources of income or savings that do not require active work. The age at which a person retires, their lifestyle during retirement, and the way they fund that lifestyle, will vary from one person to the next, depending on individual preferences and financial planning. Usually it is age 65.

Some doctors may opt for early retirement to enjoy their hobbies and travel, while others may continue working part-time to stay engaged and supplement their income. Effective retirement planning often involves a combination of savings, investments, and possibly pension benefits to ensure a comfortable and secure post-work life.

SPEAKING: ME-P Editor Dr. David Edward Marcinko MBA MEd will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Since the financial crisis in 2008, several start-up companies from Silicon Valley and Boston [Learn Vest, Betterment, Financial Guard, Quovo, WealthFront, Nest Egg Wealth. Wealth-Front and Personal Capital] have emerged with the mantra that individual investors, younger and informed clients will receive portfolio strategies, financial advice and performance metrics directly from various internet and online advisory platforms. Termed “robo-advisors” by some, their existence heralds the doom of financial advisors; or at least drives down the value of Financial Advisory guidance; reduces fees and holds them more accountable to clients.

On the other hand, detractors say the financial advice may not be as good because the personalization will not be there; but pricing fees will be more competitive, at least initially. Going forward price will get even lower and service better. And ultimately, as consumers get more information on line, product and service will improve and be delivered to them faster than thru traditional human channels of distribution. The era of quarterly client meetings with TAMPs is fading. Clients will have access to their portfolios; in real time, all the time.

Turnkey Asset Management Program (TAMP) Defined

A turnkey asset management program offers a fee-account technology platform that financial advisers, broker-dealers, insurance companies, banks, law firms, and CPA firms can use to oversee their clients’ investment accounts.

Turnkey asset management programs are designed to help financial professionals save time and allow them to focus on providing clients with service in their areas of expertise, which may not include asset management tasks like investment research and portfolio allocation. In other words, TAMPs let financial professionals and firms delegate asset management and research responsibilities to another party that specializes in those areas.

The growth of more traditional direct to investment platforms like E-Trade and Schwab has outpaced Financial Advisors and recently human advisors must have the technology and niche space specificity to survive in the future. Realistically, robo-advisors, Artificial Intelligence and traditional flesh-and-blood FAs will seamlessly merge into a hybrid platform indistinguishable to most all.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

One of the major concepts that most investors should be aware of is the relationship between the risk and the return of a financial asset. It is common knowledge that there is a positive relationship between the risk and the expected return of a financial asset. In other words, when the risk of an asset increases, so does its expected return. What this means is that if an investor is taking on more risk, he/she is expected to be compensated for doing so with a higher return. Similarly, if the investor wants to boost the expected return of the investment, he/she needs to be prepared to take on more risk.

Harry Max Markowitz (August 24, 1927 – June 22, 2023) was an American economist who was a professor of finance at the Rady School of Management at UCSD. He is best known for his pioneering work in modern portfolio theory, studying the effects of asset risk, return, correlation and diversification on probable investment portfolio returns.

One important thing to understand about Modern Portfolio Theory (MPT) is Markowitz’s calculations treat volatility and risk as the same thing. In layman’s terms, Dr. Markowitz uses risk as a measurement of the likelihood that an investment will go up and down in value – and how often and by how much. The theory assumes that investors prefer to minimize risk. The theory assumes that given the choice of two portfolios with equal returns, investors will choose the one with the least risk. If investors take on additional risk, they will expect to be compensated with additional return.

According to MPT, risk comes in two major categories:

Systematic risk – the possibility that the entire market and economy will show losses negatively affecting nearly every investment; also called market risk

Unsystematic risk – the possibility that an investment or a category of investments will decline in value without having a major impact upon the entire market.

***

***

Diversification generally does not protect against systematic risk because a drop in the entire market and economy typically affects all investments. However, diversification is designed to decrease unsystematic risk. Since unsystematic risk is the possibility that one single thing will decline in value, having a portfolio invested in a variety of stocks, a variety of asset classes and a variety of sectors will lower the risk of losing much money when one investment type declines in value. Thus putting together assets with low correlations can reduce unsystematic risks.

Although broad risks can be quickly summarized as “the failure to achieve spending and inflation-adjusted growth goals,” individual assets may face any number of other subsidiary risks:

Call risk – The risk, faced by a holder of a callable bond that a bond issuer will take advantage of the callable bond feature and redeem the issue prior to maturity. This means the bondholder will receive payment on the value of the bond and, in most cases, will be reinvesting in a less favorable environment (one with a lower interest rate)

Capital risk – The risk an investor faces that he or she may lose all or part of the principal amount invested.

Commodity risk – The threat that a change in the price of a production input will adversely impact a producer who uses that input.

Company risk – The risk that certain factors affecting a specific company may cause its stock to change in price in a different way from stocks as a whole.

Concentration risk – Probability of loss arising from heavily lopsided exposure to a particular group of counterparties

Counterparty risk – The risk that the other party to an agreement will default.

Credit risk – The risk of loss of principal or loss of a financial reward stemming from a borrower’s failure to repay a loan or otherwise meet a contractual obligation.

Currency risk – A form of risk that arises from the change in price of one currency against another.

Deflation risk – A general decline in prices, often caused by a reduction in the supply of money or credit.

Economic risk – the likelihood that an investment will be affected by macroeconomic conditions such as government regulation, exchange rates, or political stability.

Hedging risk – Making an investment to reduce the risk of adverse price movements in an asset.

Inflation risk – The uncertainty over the future real value (after inflation) of your investment.

Interest rate risk – Risk to the earnings or market value of a portfolio due to uncertain future interest rates.

Legal risk – risk from uncertainty due to legal actions or uncertainty in the applicability or interpretation of contracts, laws or regulations.

Liquidity risk – The risks stemming from the lack of marketability of an investment that cannot be bought or sold quickly enough to prevent or minimize a loss.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

In order to create and monitor an investment portfolio for personal or institutional use, the physician executive, financial advisor, wealth manager, or healthcare institutional endowment fund manager, should ask three questions:

How much do we have invested?

How much did we make on our investments?

How much risk did we take to get that rate of return?

Introduction to the IPS

Most doctors, and hospital endowment fund executives, know how much money they have invested. If they don’t, they can add a few statements together to obtain a total. But, few can answers the questions above or actually know the rate of return achieved last year; or so far this year. Everyone can get this number by simply subtracting the ending balance from the beginning balance and dividing the difference. But, few take the time to do it. Why? A typical response to the question is, “We’re doing fine.”

Now, ask how much risk is in the portfolio and help is needed [risk adjusted rate of return]. In fact, Nobel laureate Harry Markowitz, Ph.D. said, “If you take more risk, you deserve more return.” Using standard deviation, he referred to the “variability of returns;” in other words, how much the portfolio goes up and down, its volatility [Markowitz, H: Portfolio Selection. Journal of Finance, March, 1952].

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on July 21, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Rick Kahler MSFP CFP™

***

***

When Maria needed $400,000 for a down payment on a new home, her broker at a large Wall Street firm offered a solution: “Don’t sell investments and trigger capital gains. Just take out a margin loan.”

A margin loan is a line of credit from a brokerage firm, secured by the client’s investment portfolio. It offers quick access to cash with no immediate tax consequences and minimal paperwork. But the convenience comes at a cost. As of mid-2025, margin loan interest rates range from 6.25% to over 11%.

Margin loan recommendations are often presented by brokers as tax-savvy strategies that allow clients to access “tax-free” cash while keeping their portfolios intact. In many cases, however, the math benefits the advisor more than the investor. The cost of borrowing often exceeds what an investor is likely to earn by holding on.

For example, let’s assume an interest rate of 7.5% on Maria’s $400,000 margin loan. While borrowing delayed the payment of $20,000 in capital gains tax, she will eventually have to pay that tax anyway unless she holds the investments until her death. Two years later, with portfolio returns of 4% annually, she had earned around $32,000 from the $400,000 in investments she might have sold. Meanwhile, she had paid $60,000 in interest—leaving her some $28,000 worse off. That’s without factoring in ongoing interest payments, or the risks of a margin call if the investments securing the loan drop in value.

Why do advisors keep recommending margin loans? Because selling investments reduces the portfolio size and the advisor’s fee. Borrowing keeps the portfolio intact and the compensation unchanged—while the firm receives additional income from interest on the loan. In some cases, advisors suggest using margin loans to buy more investments, increasing both the portfolio and the fee they collect.

None of this is illegal. But when the borrowing cost is higher than expected returns and the advisor benefits financially, the ethics are questionable. The client takes the risk, while the advisor keeps the revenue.

This kind of conflict appears more often in portfolios where compensation is tied to asset volume and the company’s primary culture rewards gathering assets over delivering unbiased advice. By contrast, fee-only financial planning and investment advisors typically operate on simpler hourly, flat, or tiered fee structures. Their compensation doesn’t depend on whether a client borrows, sells, or holds. The culture of the firm focuses on conflict-free advice aligned with the client’s best interest.

Wall Street brokers are often held to a fiduciary standard, but structure still matters. In 2024 the SEC reported their examinations of brokers would continue to focus on advisor recommendations unduly influenced by the company’s compensation and incentives.

There are rare situations where a margin loan may be appropriate. A client with large unrealized gains might use a short-term margin loan to minimize taxes. An elderly investor might borrow tax-free rather than sell assets that will receive a step-up in basis at their death. Even in those cases, the math must be exact and the client must clearly understand the risks, including the possibility of a margin call.

If your advisor recommends a margin loan, especially to buy more investments, ask strong questions. What’s the interest rate? What return is realistic? What are the tax consequences of selling? How does this affect the advisor’s income?

In a high-rate, low-return environment, margin loans rarely favor the client. The exceptions are narrow. The risks are significant. And the conflict of interest is measurable.

Sometimes the smartest move is the simplest: sell what you need, pay the tax, and leave leverage out of your plan.

As we plan for our financial future, I think it’s helpful to be cognizant of these paradoxes. While there’s nothing we can do to control or change them, there is great value in being aware of them, so we can approach them with the right tools and the right mindset.

Here are just seven of the paradoxes that can bedevil financial planning and investment decision-making:

There’s the paradox that all of the greatest fortunes—Carnegie, Rockefeller, Buffett, Gates—have been made by owning just one stock. And yet the best advice for individual investors is to do the opposite: to own broadly diversified index funds.

There’s the paradox that the stock market may appear overvalued and yet it could become even more overvalued before it eventually declines. And when it does decline, it may be to a level that is even higher than where it is today.

There’s the paradox that we make plans based on our understanding of the rules—and yet Congress can change the rules on us at any time, as it did just a few weeks ago.

There’s the paradox that we base our plans on historical averages—average stock market returns, average interest rates, average inflation rates and so on—and yet we only lead one life, so none of us will experience the average.

There’s the paradox that we continue to be attracted to the prestige of high-cost colleges, even though a rational analysis that looks at return on investment tells us that lower-cost state schools are usually the better bet.

There’s the paradox that early retirement seems so appealing—and has even turned into a movement—and yet the reality of early retirement suggests that we might be better off staying at our desks.

There’s the paradox that retirees’ worst fear is outliving their money and yet few choose the financial product that is purpose-built to solve that problem: the single-premium immediate annuity.

Assessment

QUESTION: How should you respond to these paradoxes? As you plan for your financial future, embrace the concept of “loosely held views.” In other words, make financial plans, but continuously update your views, question your assumptions and rethink your priorities.

Yes, you can contribute to both a Roth IRA and a 401(k), provided you don’t exceed annual contribution limits for each account.

Determining whether to contribute to a Roth IRA, 401(k), or both can be an important step in planning for your retirement. Here are the key differences, including tax advantages, employer contributions, and investment options.

Eligibility requirements are the first consideration when contributing to a Roth IRA and a 401(k). For Roth IRA contributions, your eligibility is determined by your income. Specifically, if your modified adjusted gross income (MAGI) exceeds certain thresholds, your ability to contribute to a Roth IRA may be reduced or eliminated. However, there are no income limits for contributing to a 401(k), making it accessible to anyone with earned income.

IRS rules do allow for contributions to both a Roth IRA and a 401(k), provided you adhere to the annual contribution limits for each account.

This means you can take advantage of the higher contribution limits of a 401(k) while also benefiting from the tax-free growth of a Roth IRA. This dual approach can be a strategy for maximizing your retirement savings. The advantages to contributing to both accounts present some key benefits, such as:

Tax diversification in retirement, allowing for better management of taxable income.

Potential reduction of overall tax burden.

Maximization of savings potential by taking full advantage of the benefits each account offers.3

Balancing contributions between a Roth IRA and a 401(k) requires careful planning. You might start by contributing enough to your 401(k) to receive the full employer match, which is essentially free money, if your employer offers this. Once you’ve secured the match, consider maxing out your Roth IRA contributions, if you’re eligible.

If you are just starting out managing your finances and don’t know where to begin, a financial coach may be a good option for you. They are helpful for someone who wants to become proficient in the basics of finance, from learning how to budget or save money to building an emergency fund or creating a plan for paying off debt. If you have short-term money goals, like saving for a big purchase or just practicing better money habits, a financial coach can help you reach them by working with you to create a plan and holding you accountable. Even more for physicians and most all medical professionals.

Pros and Cons of Working with a Financial Coach A financial coach can have a positive impact on your financial well–being and your life in a number of ways:

Financial coaches see the bigger picture of how you relate to money. They can help you develop better habits, resulting in positive personal growth.

By providing education and encouragement, they can reduce financial stress, confusion, and what it is about money that overwhelms you.

Through accountability and support, they can help you accomplish your goals and help you feel more confident in your finances.

Available 24/7/365.

Modest fees.

At you service. Dr. David Edward Marcinko MBA MEd CMP

Posted on June 28, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

A June 11th report from global professional services firm Alvarez & Marsal (A&M) predicts that more beneficiaries might soon ditch insurance coverage for options like short-term, limited duration plans or healthcare sharing ministries (HCSMs), which aren’t regulated like health insurance and aren’t required to comply with ACA protections like covering maternity care or pre-existing conditions.

Nvidia extended its winning streak to five days, rising another 1.73% as the AI trade continues to recover.

EchoStar climbed 13.16% after the parent company of Dish TV disclosed that President Trump did in fact prod the FCC to make a deal.

Cyngn soared another 20.07% following a big day of gains after the company that makes self-driving tech for industrial vehicles announced a partnership with Nvidia.

Strong earnings from Nike (more on that later) propelled sporting goods stocks higher today. ONHoldings rose 1.74%, while Dick’s Sporting Goods climbed 3.59%.

Domestic power producers popped on reports that Trump is planning to issue an executive order increasing energy production to meet AI demand. Vistra gained 2.44%, GE Vernova climbed 2.54%, and Vertiv added 2.71%.

What’s down

Coinbase Global ended its winning streak, tumbling 5.77% after GENIUS Act hype propelled the crypto stock skyward all week long. Traders took profits in Circle as well, pushing the stablecoin stock down 15.54%.

Chinese EV maker LiAuto fell 1.93% on its weaker-than-expected deliveries forecast for the second quarter.

Fellow Chinese EV maker Xiaomi stunned markets with reports that it received 240,000 orders for its new SUV within 18 hours of its debut, but shares still sank 4%.

Pony.ai lost 6.31% on a report that Uber is considering helping its founder Travis Kalanick fund his acquisition of the US subsidiary of the Chinese autonomous vehicle company.

Gold miners tumbled while the price of the precious metal fell as investors took a risk-on stance. Newmont lost 4.11%, BarrickMining fell 3.44%, and KinrossGold shed 6.18%.

Today’s trade deal reopens the door for Chinese rare earth imports, bad news for US producers like MPMaterials (down 8.59%) and USA Rare Earth (down 12.14%).

Here is a list of the most common and helpful investment terms you’ll come across and should know.

Ask. The price that someone looking to sell stock wants to receive.

Bid. The price that someone is willing to pay for stock.

Buy. To acquire shares and thereby take a position in a company.

Sell. To get rid of shares whether because you’ve reached your goal or to prevent losses.

Bull market. Market conditions in which investors expect prices to rise.

Bear market. Market conditions in which investors expect prices to fall.

Dividend. A portion of a company’s earnings paid to shareholders.

Blue chip stocks. Shares of large and well-recognized companies that have a long history of solid financial performance.

Earning per share. A company’s net profit divided by the number of outstanding common shares.

Mutual fund. A collection of investments — stocks, bonds, commodities, and more — bundled together and held in common by a group of investors.

Asset. Something you own that could generate a return in the form of more assets.

Asset allocation. Your investment strategy, essentially — the mix of assets you choose to put your money into, whether that be cash, bonds, stocks, commodities, real estate or something else.

Broker. A person or firm — or robot — that arranges transactions between buyers and sellers in exchange for a commission (that is, a fee).

Capital gain (or capital loss). The money you make (or lose) on the sale of an asset.

Diversification. Investing in a variety of sectors, such as health care, energy and IT as well as across different geographic locations.

Dow Jones Industrial Average. A price-weighted list of 30 blue-chip stocks. It’s often used to help get a sense of the overall health of the stock market, even though it only reflects a small portion of the players.

Index fund. A type of mutual fund or exchange-traded fund that allows you to invest in a portfolio that mimics a market index, which is basically a list that tracks the performance of a group of investments either for a specific sector or the overall market.

Hedge fund. A type of investment partnership. Partners pool money from investors and try out a few different investing strategies. Generally, hedge funds will make riskier investments than your typical investor. They’ll also often use leverage (that is, borrowed money) or place bets against the market to get bigger returns. They make their money by charging their investors management fees based on a percentage of their profits.

Expense ratio. The percentage-based fee that mutual fund managers charge you to manage your investments.

Market price. How much it would cost right now to buy or sell an asset or service.

Securities and Exchange Commission (SEC). An independent government body that was created to protect investors and the national banking system. The SEC enforces laws that maintain orderly, fair and efficient markets.

Short selling. A tactic available to investors who predict a stock’s price is about to drop. An investor borrows a quantity of shares through a broker and then sells them, intending to repurchase them later, at a lower price, and return them to the lender.

Stock exchange. A place buyers and sellers come together to buy, sell and trade stock during set business hours. The New York Stock Exchange (NYSE) is the most important stock exchange in the world, but there are a total of 16 exchanges around the world.

Stock market. Refers in general to the collection of markets and exchanges where the buying, selling and trading of investment vehicles takes place.

Price per share. A simple way of calculating a company’s market value at a given moment. To find the price per share, you take a company’s most recent share price and multiply it by its total number of outstanding shares.

Prospectus. A legal document that contains in-depth information about anything you might be planning to invest in: stocks, bonds or mutual funds.

Although many academics argue that value stocks outperform growth stocks, the returns for individuals investing through mutual funds demonstrate a near match.

Introduction

A 2005 study Do Investors Capture the Value Premium? written by Todd Houge at The University of Iowa and Tim Loughran at The University of Notre Dame found that large company mutual funds in both the value and growth styles returned just over 11 percent for the period of 1975 to 2002. This paper contradicted many studies that demonstrated owning value stocks offers better long-term performance than growth stocks.

The studies, led by Eugene Fama PhD and Kenneth French PhD, established the current consensus that the value style of investing does indeed offer a return premium. There are several theories as to why this has been the case, among the most persuasive being a series of behavioral arguments put forth by leading researchers. The studies suggest that the out performance of value stocks may result from investors’ tendency toward common behavioral traits, including the belief that the future will be similar to the past, overreaction to unexpected events, “herding” behavior which leads at times to overemphasis of a particular style or sector, overconfidence, and aversion to regret. All of these behaviors can cause price anomalies which create buying opportunities for value investors.

Another key ingredient argued for value out performance is lower business appraisals. Value stocks are plainly confined to a P/E range, whereas growth stocks have an upper limit that is infinite. When growth stocks reach a high plateau in regard to P/E ratios, the ensuing returns are generally much lower than the category average over time.

Moreover, growth stocks tend to lose more in bear markets. In the last two major bear markets, growth stocks fared far worse than value. From January 1973 until late 1974, large growth stocks lost 45 percent of their value, while large value stocks lost 26 percent. Similarly, from April 2000 to September 2002, large growth stocks lost 46 percent versus only 27 percent for large value stocks. These losses, academics insist, dramatically reduce the long-term investment returns of growth stocks.

***

***

However, the study by Houge and Loughran reasoned that although a premium may exist, investors have not been able to capture the excess return through mutual funds. The study also maintained that any potential value premium is generated outside the securities held by most mutual funds. Simply put, being growth or value had no material impact on a mutual fund’s performance.

Listed below in the table are the annualized returns and standard deviations for return data from January 1975 through December 2002.

Index Return SD

S&P 500 11.53% 14.88%

Large Growth Funds 11.30% 16.65%

Large Value Funds 11.41% 15.39%

Source: Hough/Loughran Study

The Hough/Loughran study also found that the returns by style also varied over time. From 1965-1983, a period widely known to favor the value style, large value funds averaged a 9.92 percent annual return, compared to 8.73 percent for large growth funds. This performance differential reverses over 1984-2001, as large growth funds generated a 14.1 percent average return compared to 12.9 percent for large value funds. Thus, one style can outperform in any time period.

However, although the long-term returns are nearly identical, large differences between value and growth returns happen over time. This is especially the case over the last ten years as growth and value have had extraordinary return differences – sometimes over 30 percentage points of under performance.

This table indicates the return differential between the value and growth styles since 1992.

YEARLY RETURNS OF GROWTH/VALUE STOCKS

Year

Growth

Value

1992

5.1%

10.5%

1993

1.7%

18.6%

1994

3.1%

-0.6%

1995

38.1%

37.1%

1996

24.0%

22.0%

1997

36.5%

30.6%

1998

42.2%

14.7%

1999

28.2%

3.2%

2000

-22.1%

6.1%

2001

-26.7%

7.1%

2002

-25.2%

-20.5%

2003

28.2%

27.7%

2004

6.3%

16.5%

2005

3.6%

6.1%

2006

10.8%

20.6%

2007

8.8%

1.5%

2008

-38.43%

-36.84%

2009

37.2%

19.69%

2010

16.71%

15.5%

2011

2.64%

0.39%

2012

15.25%

17.50%

Source: Ibbottson.

Between the third quarter of 1994 and the second quarter of 2000, the S&P Growth Index produced annualized total returns of 30 percent, versus only about 18 percent for the S&P Value Index. Since 2000, value has turned the tables and dramatically outperformed growth. Growth has only outperformed value in two of the past eight years. Since the two styles are successful at different times, combining them in one portfolio can create a buffer against dramatic swings, reducing volatility and the subsequent drag on returns.

Assessment

In our analysis, the surest way to maximize the benefits of style investing is to combine growth and value in a single portfolio, and maintain the proportions evenly in a 50/50 split through regular rebalancing. Research from Standard & Poor’s showed that since 1980, a 50/50 portfolio of value and growth stocks beats the market 75 percent of the time.

Conclusion

Due to the fact that both styles have near equal performance and either style can outperform for a significant time period, a medical professional might consider a blending of styles. Rather than attempt to second-guess the market by switching in and out of styles as they roll with the cycle, it might be prudent to maintain an equal balance your investment between the two.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

A psychological paradox is a figure of speech that can seem silly or contradictory in form, yet it can still be true, or at least make sense in the context given.

This is sometimes used to illustrate thoughts or statements that differ from traditional ideas. So, instead of taking a given statement literally, an individual must comprehend it from a different perspective. Using paradoxes in speeches and writings can also add wit and humor to one’s work, which serves as the perfect device to grab a reader or a listener’s attention and/or persuade them to action, sales and closing statements. But paradoxes for the financial sector can be quite difficult to explain by definition alone, which is why it is best to refer to a few examples to further your understanding.