BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Closed‑end mutual funds occupy a curious corner of the investment world. Once a more prominent vehicle for accessing professional management and diversified portfolios, they now sit in the shadow of open‑end mutual funds and exchange‑traded funds (ETFs). The question of whether closed‑end funds are past their prime is not just about performance; it’s about relevance in a market that has evolved dramatically. While they still offer unique advantages, the broader trends in investor behavior and financial innovation suggest that their golden era may indeed be behind them.

Closed‑end funds were originally designed to give investors access to a professionally managed pool of assets without the liquidity constraints that come from daily redemptions. Unlike open‑end mutual funds, which issue and redeem shares based on investor demand, closed‑end funds issue a fixed number of shares at launch. Those shares then trade on an exchange like a stock. This structure frees managers from having to hold large cash reserves to meet redemptions, allowing them to invest more fully in their chosen strategies. In theory, this should give closed‑end funds an edge, especially in less liquid markets such as municipal bonds or emerging‑market debt.

However, the very feature that once made closed‑end funds appealing—their fixed capital structure—has become a double‑edged sword. Because shares trade on the open market, their price often diverges from the value of the underlying assets. This leads to persistent discounts or premiums relative to net asset value. For some investors, discounts represent an opportunity; for others, they are a source of frustration. The discount phenomenon can make closed‑end funds feel unpredictable, especially compared to ETFs, which are designed to keep market prices closely aligned with underlying asset values.

The rise of ETFs is perhaps the strongest argument that closed‑end funds have lost their prime position. ETFs offer intraday liquidity, tax efficiency, low fees, and tight tracking of net asset value. They have become the default choice for many investors seeking diversified exposure. In contrast, closed‑end funds often carry higher expense ratios, and many use leverage to enhance returns—an approach that can magnify both gains and losses. In a market increasingly focused on transparency and cost efficiency, these characteristics can make closed‑end funds seem outdated.

Investor behavior has also shifted. Modern investors value simplicity, liquidity, and low fees. Robo‑advisors, model portfolios, and passive strategies have reinforced these preferences. Closed‑end funds, with their idiosyncratic pricing and sometimes opaque strategies, do not fit neatly into this landscape. Their complexity can be a barrier for newer investors who are accustomed to the straightforward nature of ETFs and index funds.

***

***

Yet it would be a mistake to dismiss closed‑end funds entirely. They continue to offer advantages that other vehicles cannot easily replicate. Their ability to use leverage, for example, can be attractive in certain market environments. Skilled managers can exploit inefficiencies in niche markets without worrying about redemptions forcing them to sell assets at inopportune times. Income‑focused investors, particularly those seeking municipal bond exposure, often find closed‑end funds appealing because they can deliver higher yields than comparable open‑end funds or ETFs.

Moreover, the discounts that plague closed‑end funds can also be a source of opportunity. Contrarian investors who are willing to tolerate volatility may find value in purchasing shares at a discount and waiting for market sentiment to shift. In some cases, activist investors have stepped in to push for changes that unlock value, such as tender offers or fund reorganizations. These dynamics create a unique ecosystem that continues to attract a dedicated, if smaller, group of investors.

Still, the broader trend is hard to ignore. The investment industry has moved toward vehicles that emphasize liquidity, transparency, and low cost. Closed‑end funds, by design, struggle to compete on these dimensions. Their niche strengths are not enough to offset the structural advantages of ETFs for most investors. As a result, while closed‑end funds remain relevant in certain corners of the market, they no longer occupy the central role they once did.

So, are closed‑end mutual funds past their prime? In many ways, yes. Their peak influence has faded as the industry has embraced more modern, flexible, and cost‑effective investment vehicles. But “past their prime” does not mean obsolete. Closed‑end funds continue to serve a purpose for investors who understand their quirks and are willing to navigate their complexities. They may no longer be the star of the show, but they still play a meaningful supporting role in the broader investment landscape.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

“THE INVESTOR’S CHIEF problem—even his worst enemy—is likely to be himself.” So wrote Benjamin Graham, the father of modern investment analysis.

With these words, written in 1949, Graham acknowledged the reality that investors are human. Though he had written an 800 page book on techniques to analyze stocks and bonds, Graham understood that investing is as much about human psychology as it is about numerical analysis.

In the decades since Graham’s passing, an entire field has emerged at the intersection of psychology and finance. Known as behavioral finance, its pioneers include Daniel Kahneman, Amos Tversky and Richard Thaler. Together, they and their peers have identified countless human foibles that interfere with our ability to make good financial decisions. These include hindsight bias, recency bias and overconfidence, among others. On my bookshelf, I have at least as many volumes on behavioral finance as I do on pure financial analysis, so I certainly put stock in these ideas.

At the same time, I think we’re being too hard on ourselves when we lay all of these biases at our feet. We shouldn’t conclude that we’re deficient because we’re so susceptible to biases. Rather, the problem is that finance isn’t a scientific field like math or physics. At best, it’s like chaos theory. Yes, there is some underlying logic, but it’s usually so hard to observe and understand that it might as well be random. The world of personal finance is bedeviled by paradoxes, so no individual—no matter how rational—can always make optimal decisions.

As we plan for our financial future, I think it’s helpful to be cognizant of these paradoxes. While there’s nothing we can do to control or change them, there is great value in being aware of them, so we can approach them with the right tools and the right mindset.

Here are just seven of the paradoxes that can bedevil financial decision-making:

There’s the paradox that all of the greatest fortunes—Carnegie, Rockefeller, Buffett, Gates—have been made by owning just one stock. And yet the best advice for individual investors is to do the opposite: to own broadly diversified index funds.

There’s the paradox that the stock market may appear overvalued and yet it could become even more overvalued before it eventually declines. And when it does decline, it may be to a level that is even higher than where it is today.

There’s the paradox that we make plans based on our understanding of the rules—and yet Congress can change the rules on us at any time, as it did just last year.

There’s the paradox that we base our plans on historical averages—average stock market returns, average interest rates, average inflation rates and so on—and yet we only lead one life, so none of us will experience the average.

There’s the paradox that we continue to be attracted to the prestige of high-cost colleges, even though a rational analysis that looks at return on investment tells us that lower-cost state schools are usually the better bet.

There’s the paradox that early retirement seems so appealing—and has even turned into a movement—and yet the reality of early retirement suggests that we might be better off staying at our desks.

There’s the paradox that retirees’ worst fear is outliving their money and yet few choose the financial product that is purpose-built to solve that problem: the single-premium immediate annuity.

How should you respond to these paradoxes? As you plan for your financial future, embrace the concept of “loosely held views.”

In other words, make financial plans, but continuously update your views, question your assumptions and rethink your priorities.

After a lifetime of hard work practicing medicine and saving, you’re at the retirement finish line. Instead of a paycheck, you’re relying on your nest egg and investment income to cover the bills. Picking the right investments is even more important, as you won’t have much chance to recover as a retired MD, DO, DPM or DDS.

“You made it to the top of the mountain through a systematic approach and are trying to make your way down safely,” says retirement planner John Gillet John Gillet in Hollywood, Fla. “Why throw all caution to the wind and try something different now?”

***

***

Definitions

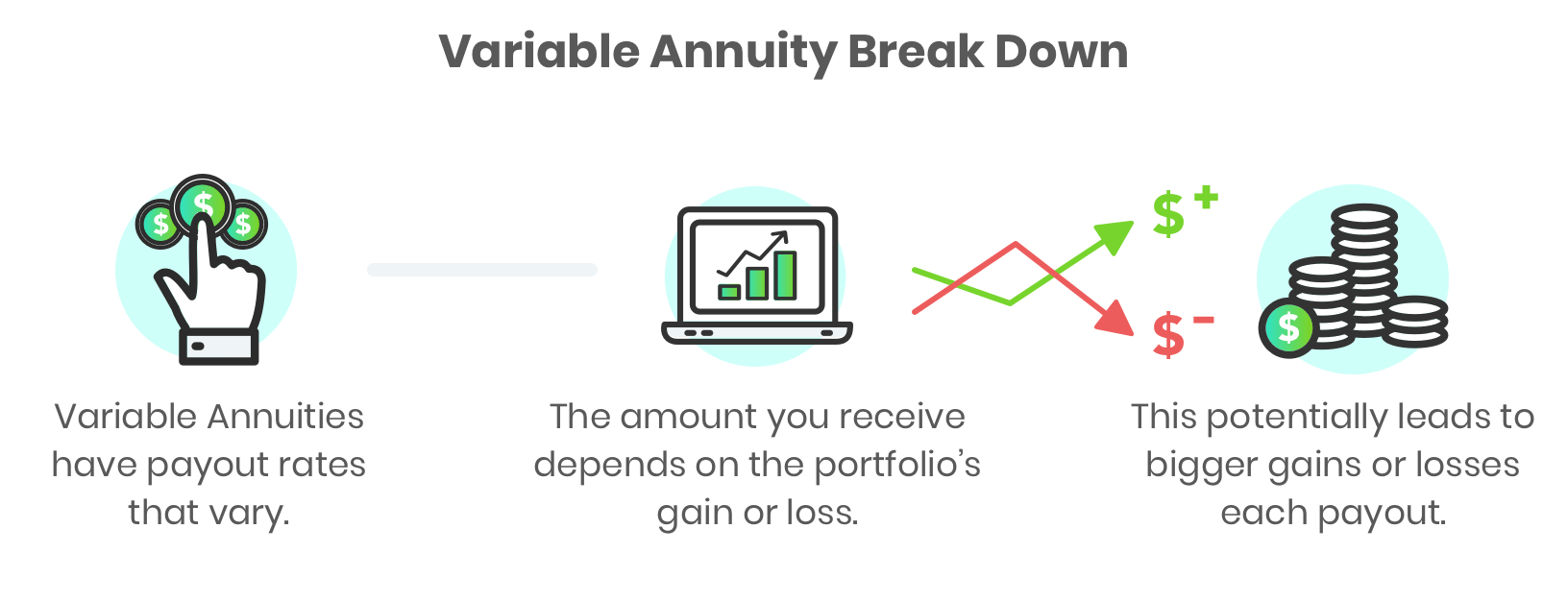

An annuity is an insurance contract designed to grow your money and then repay it as income. There are different versions. An immediate annuity turns your lump sum into future guaranteed income payments, like your own personal pension. They are simple to understand with no or small fees.

Fixed annuities pay a guaranteed interest rate over a set period to grow your money, like 5% a year for five years. These options could make sense as part of a retirement plan.

A variable annuity, on the other hand, invests your savings in mutual funds. While you can buy riders that guarantee a minimum income, you’ll be paying very much for it. “All in, the annual fees can be 3% or more of your balance,” says Jeff Bailey, an advisor from Nashville. “That’s a huge withdrawal rate from your portfolio versus investing on your own.”

The variable annuity will lock up your money for years. If you cancel early, you owe a surrender charge that could start at 7% or more of your annuity balance before gradually going down as time goes by. “Clients believe they can walk away with their contract value, but that’s often not true,” says Bailey.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on August 26, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

Types of investments

Once a physician [MD, DO, DPM or DDS] has a brokerage account, the young doctior will need to decide what to invest in. There are lots of options, and each comes with different benefits and drawbacks. Here are some of the most common options for new physician investors.

Stocks are the first thing most people think about when they are considering investing, but they are not the only option. The prices of stocks change daily, sometimes by large amounts, as the market adjusts to news and various cycles. For that reason, it’s important to do your research. If you’re just beginning with a retirement account, you could also consider the longer-term products listed below.

Index funds and mutual funds.

Index funds attempt to replicate the performance of an un-managed market index. The performance of mutual funds [open and closed] varies. You can often get involved for a lower initial investment, and they can provide good diversification,which makes your portfolio better equipped to handle market fluctuations [active and passive].

For that reason, many financial experts say they should form the core of your retirement portfolio. While they have many similar characteristics, there are important differences. Read more about some of the differences in index funds and mutual funds.

These technically aren’t investment products; they are a contract between you and an insurance company. However, they work to accomplish a similar goal. There are immediate annuities that convert some of your existing savings into lifetime payments, but if we’re talking about saving for retirement, a deferred income annuity is the closest comparison. You make premium payments into the deferred annuity on a regular or irregular basis depending on the contract terms, and when you reach retirement age, you annuitize those savings and receive payments for the rest of your life. They can make a valuable addition to a retirement savings strategy.

Other investments.

There are many other types of investments and financial vehicles: bonds [local, state or US], money market funds, certificates of deposit through a brokerage account or investment apps. Even the cash value of life insurance can play a part. They are all designed to address different needs and have benefits and drawbacks and may be important to your overall strategy.

Crypto.com is a cryptocurrency company based in Singapore that offers various financial services, including an app, exchange, and noncustodial DeFi wallet, NFT marketplace, and direct payment service in cryptocurrency. As of 2024, the company reportedly had more than 100 million customers and more than 4,000 employees.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Although many academics argue that value stocks outperform growth stocks, the returns for individuals investing through mutual funds demonstrate a near match.

Introduction

A 2005 study Do Investors Capture the Value Premium? written by Todd Houge at The University of Iowa and Tim Loughran at The University of Notre Dame found that large company mutual funds in both the value and growth styles returned just over 11 percent for the period of 1975 to 2002. This paper contradicted many studies that demonstrated owning value stocks offers better long-term performance than growth stocks.

The studies, led by Eugene Fama PhD and Kenneth French PhD, established the current consensus that the value style of investing does indeed offer a return premium. There are several theories as to why this has been the case, among the most persuasive being a series of behavioral arguments put forth by leading researchers. The studies suggest that the out performance of value stocks may result from investors’ tendency toward common behavioral traits, including the belief that the future will be similar to the past, overreaction to unexpected events, “herding” behavior which leads at times to overemphasis of a particular style or sector, overconfidence, and aversion to regret. All of these behaviors can cause price anomalies which create buying opportunities for value investors.

Another key ingredient argued for value out performance is lower business appraisals. Value stocks are plainly confined to a P/E range, whereas growth stocks have an upper limit that is infinite. When growth stocks reach a high plateau in regard to P/E ratios, the ensuing returns are generally much lower than the category average over time.

Moreover, growth stocks tend to lose more in bear markets. In the last two major bear markets, growth stocks fared far worse than value. From January 1973 until late 1974, large growth stocks lost 45 percent of their value, while large value stocks lost 26 percent. Similarly, from April 2000 to September 2002, large growth stocks lost 46 percent versus only 27 percent for large value stocks. These losses, academics insist, dramatically reduce the long-term investment returns of growth stocks.

***

***

However, the study by Houge and Loughran reasoned that although a premium may exist, investors have not been able to capture the excess return through mutual funds. The study also maintained that any potential value premium is generated outside the securities held by most mutual funds. Simply put, being growth or value had no material impact on a mutual fund’s performance.

Listed below in the table are the annualized returns and standard deviations for return data from January 1975 through December 2002.

Index Return SD

S&P 500 11.53% 14.88%

Large Growth Funds 11.30% 16.65%

Large Value Funds 11.41% 15.39%

Source: Hough/Loughran Study

The Hough/Loughran study also found that the returns by style also varied over time. From 1965-1983, a period widely known to favor the value style, large value funds averaged a 9.92 percent annual return, compared to 8.73 percent for large growth funds. This performance differential reverses over 1984-2001, as large growth funds generated a 14.1 percent average return compared to 12.9 percent for large value funds. Thus, one style can outperform in any time period.

However, although the long-term returns are nearly identical, large differences between value and growth returns happen over time. This is especially the case over the last ten years as growth and value have had extraordinary return differences – sometimes over 30 percentage points of under performance.

This table indicates the return differential between the value and growth styles since 1992.

YEARLY RETURNS OF GROWTH/VALUE STOCKS

Year

Growth

Value

1992

5.1%

10.5%

1993

1.7%

18.6%

1994

3.1%

-0.6%

1995

38.1%

37.1%

1996

24.0%

22.0%

1997

36.5%

30.6%

1998

42.2%

14.7%

1999

28.2%

3.2%

2000

-22.1%

6.1%

2001

-26.7%

7.1%

2002

-25.2%

-20.5%

2003

28.2%

27.7%

2004

6.3%

16.5%

2005

3.6%

6.1%

2006

10.8%

20.6%

2007

8.8%

1.5%

2008

-38.43%

-36.84%

2009

37.2%

19.69%

2010

16.71%

15.5%

2011

2.64%

0.39%

2012

15.25%

17.50%

Source: Ibbottson.

Between the third quarter of 1994 and the second quarter of 2000, the S&P Growth Index produced annualized total returns of 30 percent, versus only about 18 percent for the S&P Value Index. Since 2000, value has turned the tables and dramatically outperformed growth. Growth has only outperformed value in two of the past eight years. Since the two styles are successful at different times, combining them in one portfolio can create a buffer against dramatic swings, reducing volatility and the subsequent drag on returns.

Assessment

In our analysis, the surest way to maximize the benefits of style investing is to combine growth and value in a single portfolio, and maintain the proportions evenly in a 50/50 split through regular rebalancing. Research from Standard & Poor’s showed that since 1980, a 50/50 portfolio of value and growth stocks beats the market 75 percent of the time.

Conclusion

Due to the fact that both styles have near equal performance and either style can outperform for a significant time period, a medical professional might consider a blending of styles. Rather than attempt to second-guess the market by switching in and out of styles as they roll with the cycle, it might be prudent to maintain an equal balance your investment between the two.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

here are many ways for a doctor, osteopath, podiatrist or dentist to financially invest. Traditionally, this meant picking individual stocks and bonds. Today, there are many other ways to purchase securities en mass. For example:

MUTUAL FUND: A regulated investment company that manages a portfolio of securities for its shareholders.

Open End Mutual Funds: An investment company that invests money in accordance with specific objectives on behalf of investors. Fund assets expand or contract based on investment performance, new investments and redemptions. Trade at Net Asset Value or the price the fund shares scheduled with the US Securities and Exchange Commission (SEC) trade. NAV can change on a daily basis. Therefore, per-share NAV can, as well.

Closed End Mutual Funds: Older than open end mutual funds and more complex. A CEMF is an investment company that registers shares SEC regulations and is traded in securities markets at prices determined by investments. Shares of closed-end funds can be purchased and sold anytime during stock market hours. CEMF managers don’t need to maintain a cash reserve to redeem or / repurchase shares from investors. This can reduce performance drag that may otherwise be attributable to holding cash. CEMFs may be able to offer higher returns due to the heavier use of leverage [debt]. They are subject to volatility, less liquid than open-end funds, available only through brokers and may sells at a heavily discount or premium to [NAV] determined by subtracting its liabilities from its assets. The fund’s per-share NAV is then obtained by dividing NAV by the number of shares outstanding. .

Sector Mutual Funds: Sector funds are a type of mutual fund or Exchange-Traded Fund (ETF) that invests in a specific sector or industry such as technology, healthcare, energy, finance, consumer goods, or real estate. Sector funds focus on a particular industry, allowing investors to gain targeted exposure to specific market areas. The goal is to outperform the overall market by investing in companies within a specific sector that is expected to perform well. However, they are also more susceptible to market fluctuations and specific sector risks, making them a more specialized and potentially higher-risk investment option.

EXCHANGE TRADED FUNDS: ETFs are a type of fund that owns various kinds of securities, often of one type. For example, a stock ETF holds stocks, while a bond ETF holds bonds. One share of the ETF gives buyers ownership of all the stocks or bonds in the fund. If an ETF held 100 stocks, then those who owned the fund would own a stake – albeit a very tiny one – in each of those 100 stocks.

ETFs are typically passively managed, meaning that the fund usually holds a fixed number of securities based on a specific preset index of investments. These are tax efficient. In contrast, many mutual funds are actively managed, with professional investors trying to select the investments that will rise and fall.

The Standard & Poor’s 500 Index is perhaps the world’s best-known index, and it forms the basis of many ETFs. Other popular indexes include the Dow Jones Industrial Average and the National Association of Securities Dealers Automated Quotations [NASDAQ] Composite Index.

ETFs based on these funds are called Index Funds and just buy and hold whatever is in the index and make no active trading decisions. ETFs trade on a stock exchange during the day, unlike mutual funds that trade only after the market closes. With an ETF you can place a trade whenever the market is open and know exactly the price you’re paying for the fund.

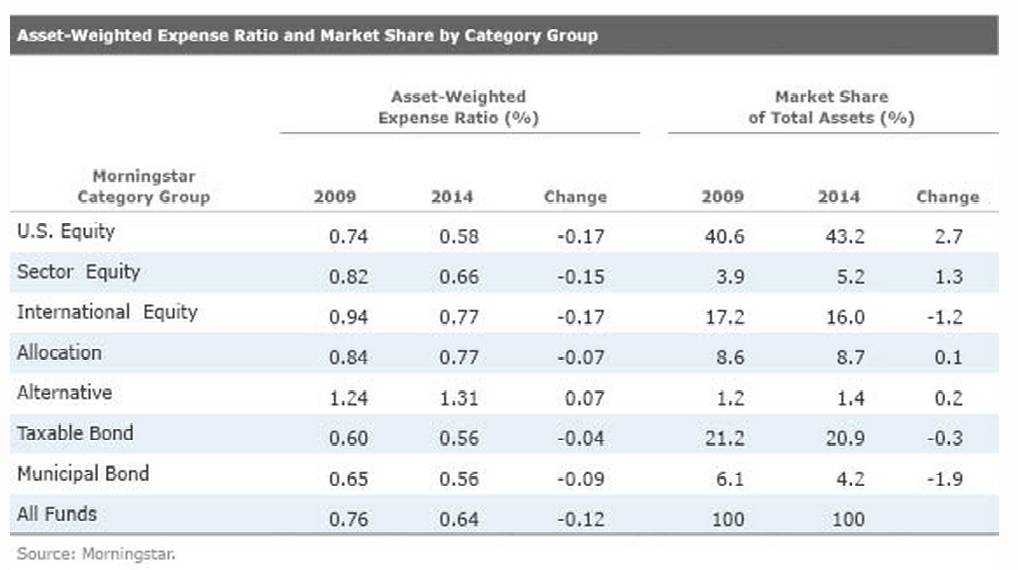

INDEX FUNDS: Index funds mirror the performance of benchmarks like the DJIA. These passive investments are an unimaginative way to invest. Passive index funds tracking market benchmarks accounted for just 21% of the U.S. equity fund market in 2012. By 2024, passive index funds had grown to about half of all U.S. fund assets. This rise of passive funds has come as they often outperform their actively managed peers. According to the widely followed S&P Indices Versus Active (SPIVA) scorecards, about 9 out of 10 actively managed funds didn’t match the returns of the S&P 500 benchmark in the past 15 years.

ASSESSMENT

Investing in individual stocks is psychologically and academically different than investing in the above funds, according to psychiatrist and colleague Ken Shubin-Stein MD, MPH, MS, CFA who is a professor of finance at the Columbia University Graduate School of Business When you buy shares of a company, you are putting all your eggs in one basket. If the company does well, your investment will go up in value. If the company does poorly, your investment will go down. Fund diversification helps reduce this risk.

CONCLUSION

Investing in the above fund types will help mitigate single company security risk.

References:

1. Fenton, Charles, F: Non-Disclosure Agreements and Physician Restrictive Covenants. In, Marcinko, DE and Hetico, HR: Risk Management, Liability Insurance, and Asset Protection Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™]. Productivity Press, New York, 2015.

Readings:

1. Marcinko, DE and Hetico, HR; Comprehensive Financial Planning Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™] Productivity Press, New York, 2017

2. Marcinko, DE: Dictionary of Health Economics and Finance. Springer Publishing Company, NY 2006

4. Shubin-Stein, Kenneth: Unifying the Psychological and Financial Planning Divide [Holistic Life Planning, Behavioral Economics, Trading Addiction and the Art of Money]. Marcinko, DE and Hetico, HR; Comprehensive Financial Planning Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™] Productivity Press, New York, 2017

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Posted on June 12, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

A Basic Overview for Emerging Physician and Medical Professional Investors

By Somnath Basu; PhD, MBA

There are three basic considerations in any investment decision.

1] The first is the understanding of the investment objective or why the investment is being made. While this may seem somewhat irrelevant at first – why would you be investing if you do not know what you are doing – combining investment objectives can pose problems down-stream.

For example, if you are saving for your retirement so that you can afford the retirement lifestyle you desire (the investment objective), your saving plan should not include any savings you are making for your children’s education (a separate investment objective). Compounding the two savings streams in one plan can very easily lead to one or both of the plans failing.

2] The second consideration is the time horizon of the investment. As a rough guide, investments that need to mature in the next 5-7 years can be considered as short term, 8-15 years as medium term and the rest as long term.

3] Finally, and probably the most important consideration of all is the importance you attach (priority) to achieving your investment objective; in other words, how safe and secure should your investments be. For example, if you are 70 years old and considering how you should invest your retirement funds so that your expenses are covered say for the next 25 years, you do not want a large margin of error in how your investments turn out; you can ill afford to be broke when you are older and hence you want your investments to be as secure as possible.

On the other hand, if the investment is for a second home or a boat, for example, you may wish to engage in some risk taking which may help in lowering your upfront investment needs. It is very important for any investor to clearly understand how much loss they can bear from any investment decision.

Decision Matrix

It is useful to express the investment framework described above as a simple decision matrix. Using the matrix (shown below) as a decision support system should clarify and simplify most investment decisions.

Understanding where in the matrix your decision falls is a very good first step of your decision. Both these elements (safety and time) will ultimately decide the kinds of financial instruments that will reside in your portfolio. We will examine the structure of each of the 9 possible combinations shown in the matrix. Before doing so, let us start by examining the various investment alternatives (e.g. stocks, bonds, etc.) since they have an implicit connection with the two dimensions portrayed in our matrix.

Stocks

Stocks are the most well known and popular form of financial investments. Stocks may be further segregated between large cap and small cap stocks, where the term “cap” is surrogate for the size of the underlying corporation or firm.

Stocks may represent investments in both domestic and international companies. Within the international category, stocks may represent corporations registered in developed (safer) or emerging (riskier) markets. In terms of our matrix dimensions, stocks are best suited when the decision is of medium or long term. In terms of safety, large cap (both domestic and international) stocks are the safest, while small cap and emerging market stocks are the most risky. The riskier the stock, the greater are the profit possibilities as are the chances of large losses.

Bonds

The second common type of investment are bonds Generally, bonds are much safer than stocks with the exception of a class of bonds known as high yield (or junk) bonds. Bonds are issued by companies, governments (domestic and international) and other agencies such as local governments (municipal bonds or “munis” which are especially desirable for those in high income tax rate categories) and quasi-government agencies such as Federal Home Loan Bank, Student Loan Administration, Agricultural Cooperative Banks, etc (collectively known as “Agency” bonds such as Ginnie/Fannie/Sallie Mae, Freddie Mac, etc.).

Government bonds are the safest, followed by agency and municipal bonds and then by bonds issues by corporations.

Corporate bonds may be safe (which are assigned credit safety ratings such as AAA, AA, BBB, etc.) or risky (junk bonds with ratings such as BB, CCC, CC etc.).

Bonds can be used for all time horizons, their maturities ranging from 3 months to 30 years. Very short term bond and bond like instruments (with maturities of one year or less) are known as money market securities which are generally safer than most other investments.

Alternate Investments

Other types of investments include real estate (long term, risky), commodities (such as energy, basic building materials, precious metals, etc.) which are also risky and which may be used for both short term and long term purposes and provide a good hedge (counter balance) in an inflationary environment, derivatives (options and futures) which are very risky and typically short term in nature. Derivatives are generally suggested for very sophisticated investors and are best left alone otherwise.

Risk Reduction

A very important feature about investments is that when various types of investments are bundled together in a portfolio, they help to reduce the risk of the investment decision without affecting the profits in a comparable way. This basic aspect of mixing various kinds of investments (stocks, bonds, etc) to reduce risk is known as diversification and it is a “must” for any investment portfolio. It is a “must” because this technique of risk reduction is generally costless (unless you are paying a financial advisor to do this for you) and it is very worthwhile. All other methods of risk reduction have cost implications.

Scenario Matrix

Armed with this nomenclature regarding various investment types we can now go about examining what the 9 combination (Scenario) portfolios may look like for investment purposes.

Starting with Scenario 1, if you wish to make a short term decision that is very important to you and needs to be very safe, investments should be made in very short term bonds (government or treasury bills)and other similar money market (short term, safe) securities. International short term bonds of developed countries may also be included. Such investment products are generally available through mutual funds or Exchange Traded Funds (or ETFs). ETFs are just like mutual funds except that they are usually cheaper, much easier to buy and sell and may provide tax deferral benefits.

If your investment falls in the Scenario 2 category, include agency/municipal bonds as well as some domestic and international (developed country) large cap stocks while for Scenario 3, smaller portions of small cap and emerging market stocks may be added proportionately while reducing some of the safer investments.

If your investment was a Scenario 4 type of investment, corporate large cap stocks (both domestic and international) could be added to agency or corporate (domestic and international) bonds. Before investing in stocks (in any Scenario) for this Scenario 4, a good question to ask is the following: how profitable were stock investments in the last 3-5 years? If the answer is “very profitable” then reduce the proportion of stocks as compared to bonds in the portfolio. If the last few years were not good, then it would be good to increase their comparable shares. The main reason for this “fine tuning” is that the fortunes of stocks (and many other types of investments) follow a cyclical pattern and the cycle is related to the general cycle of economic (GDP) growth and contraction.

It can be seen now how Scenarios 5 and 6 (as also 8 and 9) will follow a similar pattern as before, increasing proportionally in stocks (of all sizes, domestic/international), real estate, commodities, etc. Portfolios falling in these groups may also include some small cap and emerging market stocks as well as high yield or junk bonds. The proportion of these riskier investments would of course be higher for Scenario 6 over Scenario 5 (and Scenario 9 over 8).

For Scenario 7, the investment portfolio would typically resemble one that would be like an opposite of the portfolio in Scenario 1 and would include a greater proportion of large cap (domestic/international) stocks and a much smaller proportion of bonds. As we move towards Scenarios 8 and 9, the portfolios would be dominated by small cap and emerging market stocks as well as junk bonds.

Assessment

In the discussion above, I have tried to generalize the investment decision in a simplifying way. While the discussion may have centered more on stocks and bonds, it is important to note that all portfolios must “diversify” the investment risks by expanding upon the various types of investment products contained in the portfolios. The very fact that a portfolio contains various types of investments will ensure that the portfolio will perform better than those which are not as well diversified. This will be so in spite of any one of the investment types underperforming at any point in time and the diversification benefit will be received consistently over long periods of time. A popular analogy to this diversification benefit is the common phrase of not putting all eggs in one basket.

Editor’s Note: Somnath Basu PhD is program director of the California Institute of Finance in the School of Business at California Lutheran University where he’s also a professor of finance. He can be reached at (805) 493 3980 or basu@callutheran.edu

Conclusion

The above approach to investment decision-making can be considered as a basic template that can be used universally. For those seeking greater sophistication and who have a foundation built on the above model, expert advice is strongly recommended.

And so, your thoughts and comments on this ME-P are appreciated. Financial advisors please chime in on the debate? Is Basu correct; why or why not? Review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, be sure to subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@outlook.com

Subscribe Now: Did you like this Medical Executive-Post, or find it helpful, interesting and informative? Want to get the latest ME-Ps delivered to your email box each morning? Just subscribe using the link below. You can unsubscribe at any time. Security is assured.

Sponsors Welcomed

And, credible sponsors and like-minded advertisers are always welcomed.

FIVE INVESTING MISTAKES OF DOCTORS; PLUS 1 VITAL TIP

As a former US Securities and Exchange Commission [SEC] Registered Investment Advisor [RIA] and business school professor of economics and finance, I’ve seen many mistakes that doctors must be aware of, and most importantly, avoid. So, here are the top 5 investing mistakes along with suggested guideline solutions.

Mistake 1: Failing to Diversify Investment but Beware Di-Worsification

A single investment may become a large portion of your portfolio as a result of solid returns lulling you into a false sense of security. The Magnificent Seven stocks are a current example:

Apple, up +5,064%% since 1/18/2008

Amazon, up +30,328% since 9/6/2002

Alphabet, up +1,200% since 7/20/2012

Tesla, up +21,713% since 11/16/2012

Meta, up +684% since 2/20/2015

Microsoft, up +22% since 12/21/2023

Nvidia, up +80,797% since 4/15/2005

Guideline: The Magnificent Seven [7] has grown from 9% of the S&P 500 at the end of 2013 to 31% at the end of 2024! That means even if you don’t own them, you’re still very exposed if you have an Index Fund [IF] or Exchange Traded Fund [ETF] that tracks the market. Accordingly, diversification is the only free lunch in investing which can reduce portfolio risk. But, remember the Wall Street insider aphorism that states: “Di-Versification Means Always Having to Say Your Sorry.”

The term “Di-Worsification” was coined by legendary investor Peter Lynch in his book, One Up On Wall Street to refer to over-diversifying an investment portfolio in such a way that it reduces your overall risk-return characteristics. In other words, the potential return rises with an increase in risk and invested money can render higher profits only if willing to accept a higher possibility of losses [1].

A podiatrist can easily fall into the trap of chasing securities or mutual funds showing the highest return. It is almost an article of faith that they should only purchase mutual funds sporting the best recent performance. But in fact, it may actually pay to shun mutual funds with strong recent performance. Unfortunately, many struggle to appreciate the benefits of their investment strategy because in jaunty markets, people tend to run after strong performance and purchase last year’s winners.

Similarly, in a market downturn, investors tend to move to lower-risk investment options, which can lead to missed opportunities during subsequent market recoveries. The extent of underperformance by individual investors has often been the most awful during bear markets. Academic studies have consistently shown that the returns achieved by the typical stock or bond fund investors have lagged substantially.

Guideline: Understand chasing performance does not work.Continually monitor your investments and don’t feel the need to invest in the hottest fund or asset category. In fact, it is much better to increase investments in poor performing categories (i.e. buy low). Also keep in remind rebalancing of assets each year is key. If stocks perform poorly and bonds do exceptionally well, then rebalance at the end of the year. In following this strategy, this will force a doctor into buying low and selling high each year.

Often doctors make their investment decisions under the belief that stocks will consistently give them solid double-digit returns. But the stock markets go through extended long-term cycles.

In examining stock market history, there have been 6 secular bull markets (market goes up for an extended period) and 5 secular bear markets (market goes down) since 1900. There have been five distinct secular bull markets in the past 100+ years. Each bull market lasted for an extended period and rewarded investors.

For example, if an investor had started investing in stocks either at the top of the markets in 1966 or 2000, future stock market returns would have been exceptionally below average for the proceeding decade. On the other hand, those investors fortunate enough to start building wealth in 1982 would have enjoyed a near two-decade period of well above average stock market returns. They key element to remember is that future historical returns in stocks are not guaranteed. If stock market returns are poor, one must consider that he or she will have to accept lower projected returns and ultimately save more money to make up for the shortfall. For example,

The May 6th, 2010, flash crash, also known as the crash of 2:45, was a United States trillion-dollar stock market plunge which started at 2:32 pm EST and lasted for approximately 36 minutes.

And, investors who have embraced the “buy the dip” strategy in 2025 have been handsomely rewarded, with the S&P 500 delivering its strongest post-pull back returns in over three decades.

According to research from Bespoke Investment Group, the S&P 500 has gained an average of 0.36% in the trading session following a down day so far in 2025. The only year with a comparable performance was 2020, which saw a 0.32% average post-dip gain [2].

The most recent example came on May 27, 2025 when the S&P 500 surged more than 2% after falling 0.7% in the final session before the holiday weekend. The rally was sparked by President Trump’s decision to scale back huge previously threatened tariffs on EU —a recurring catalyst behind many of 2025’s rebound.

Guideline: Beware of projecting forward historical returns. Doctors should realize that the stock markets are inherently volatile and that, while it is easy to rely on past historical averages, there are long periods of time where returns and risk deviate meaningfully from historical averages.

Some doctors believe they are “smarter than the market” and can time when to jump in and buy stocks or sell everything and go to cash. Wouldn’t it be nice to have the clairvoyance to be out of stocks on the market’s worst days and in on the best days?

Using the S&P 500 Index, our agile imaginary doctor-investor managed to steer clear of the worst market day each year from January 1st, 1992 to March 31st, 2012. The outcome: s/he compiled a 12.42% annualized return (including reinvestment of dividends and capital gains) during the 20+ years, sufficient to compound a $10,000 investment into $107,100.

But what about another unfortunate doctor-investor that had the mistiming to be out of the market on the best day of each year. This ill-fated investor’s portfolio returned only 4.31% annualized from January 1992 – March 2012, increasing the $10,000 portfolio value to just $23,500 during the 20 years. The design of timing markets may sound easy, but for most all investors it is a losing strategy.

More contemporaneously on December 18th 2024, the DJIA plummeted 2.5%, while the S&P 500 declined 3% and the NASDAQ tumbled 3.5%

Guideline: If it looks too good to be true, it probably is. While jumping into the market at its low and selling right at the high is appealing in theory, we should recognize the difficulties and potential opportunity and trading costs associated with trying to time the stock market in practice. In general, colleagues are be best served by matching their investment with their time horizon and looking past the peaks / valleys along the way.

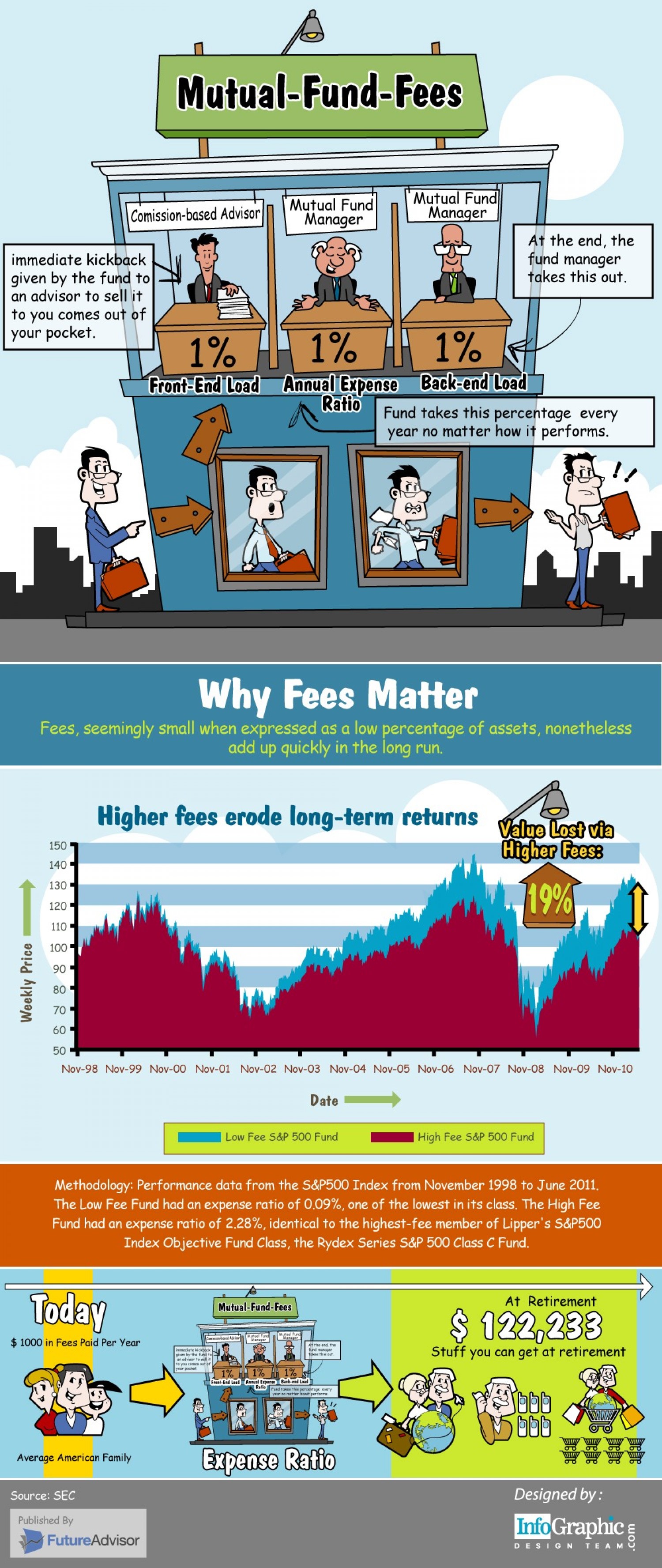

Mistake 5: Failing to Recognize the Impact of Fees and Expenses

A free dinner seminar or a polished stock-broker sales pitch may hide the total underlying costs of an investment. So, fees absolutely matter.

The first costing step is determining what the fees actually are. In a mutual fund, these costs are found in the company’s obligatory “Fund Facts”. This manuscript clearly outlines all the fees paid–including up front fees (commissions and loads), deferred sales charges and any switching fees. Fund management expense ratios are also part of the overall cost. Trading costs within the fund can also impact performance.

Here is a list of the traditional mutual fund fees:

Front End Load: The commission charged to purchase a fund through a stock broker or financial advisor. The commission reduces the amount you have available to invest. Thus, if you start with $100,000 to invest, and the advisor charges up to an 8 percent front end load, you end up actually investing $92,000.

Deferred Sales Charge (DSC) or Back End Load: Imposed if you sell your position in the mutual fund within a pre-specified period of time (normally one – five years). It is initiated at a higher start percentage (i.e. as high as 10 percent) and declines over a specific period of time.

Operating Fees: Costs of the mutual fund including the management fee rewarded to the manager for investment services. It also includes legal, custodial, auditing and marketing fees.

Annual Administration Fee: Many mutual fund companies also charge a fee just for administering the account – usually under $100-150 per year.

Guideline: Know and understand all fees.

For example: A 1 percent disparity in fees may not seem like much but it makes a considerable impact over a long time period.

Consider a $100,000 portfolio that earns 8 percent before fees, grows to $320,714 after 20 years if the investor pays a 2 percent operating fee. In comparison, if s/he opted for a fund that charged a more reasonable 1 percent fee, after 20 years, the portfolio grows to be $386,968 – a divergence of over $66,000!

This is the value of passive or index investing. In the case of an index fund, fees are generally under 0.5 percent, thus offering even more savings over a long period of time.

One Vital Tip: Investing Time is on Your Side

Despite thousands of TV shows, podcasts, textbooks, opinions and university studies on investing, it really only has three simple components. Amount invested, rate of return and time. By far, the most important item is time! For example:

Nvidia: if you invested $1,000 in 2009, you’d have $338,103 today.

Apple: if you invested $1,000 in 2008, you’d have $48,005 today.

Netflix: if you invested $1,000 in 2004, you’d have $495,679 today.

Unfortunately, this list of investing mistakes is still being made by many doctors. Fortunately, by recognizing and acting to mitigate them, your results may be more financially fruitful and mentally quieting.

REFERENCES:

1. Lynch, Peter: One Up on Wall Street [How to Use What You Already Know to Make Money in the Market]: Simon and Shuster (2nd edition) New York, 2000.

1. Marcinko, DE; Comprehensive Financial Planning Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™] Productivity Press, New York, 2017.

2. Marcinko, DE: Dictionary of Health Economics and Finance. Springer Publishing Company, New York, 2006.

3. Marcinko, DE; Risk Management, Liability Insurance, and Asset Protection Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™] CRC Press, New York, 2015.

BIO: As a former university Professor and Endowed Department Chair in Austrian Economics, Finance and Entrepreneurship, the author was a NYSE Registered Investment Advisor and Certified Financial Planner for a decade. Later, he was a private equity and wealth manager

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on April 30, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

FUNDAMENTAL INDUSTRY CHANGES

By Staff Reporters

***

***

Index Funds

An index mutual fund or ETF (exchange-traded fund) tracks the performance of a specific market benchmark—or “index,” like the popular S&P 500 Index—as closely as possible. That’s why you may hear people refer to indexing as a “passive” investment strategy.

Instead of hand-selecting which stocks or bonds the fund will hold, the fund’s manager buys all (or a representative sample) of the stocks or bonds in the index it tracks.

***

Quantum Computing

Unlike traditional computers that use bits, quantum computers utilize qubits. These qubits are capable of being in a state of superposition, where they can represent both 0 and 1 simultaneously, enabling the processing of multiple calculations at once. This could allow quantum computers to outperform classical computers in solving certain complex problems. However, the field is still overcoming challenges such as qubit stability and decoherence; especially in these three areas:

Quantum computing could fundamentally alter healthcare by accelerating drug discovery and improving individualized medicine. Rapid analysis of enormous volumes of biological data allows quantum computers to find trends that might guide the creation of more potent treatments. In addition to accelerating drug development, this will enable customized treatments tailored to unique genetic profiles.

Faster and more accurate financial models produced by quantum computing will transform the banking sector. Through real-time analysis of intricate financial systems, it can help investors to control risk and make better decisions. More precise market forecasts will help maximize portfolio management and trading strategies.

Through greatly enhanced medical diagnosis and patient care, quantum computing can transform the healthcare industry. Quantum computers can remarkably accurately find trends and possible health hazards by analyzing enormous volumes of medical data in a fraction of the time. Early diagnosis and more customized treatment alternatives follow from this.

B–QTUM Index Fund

Index Description: The BlueStar® Machine Learning and Quantum Computing Index (BQTUM) tracks liquid companies in the global quantum computing and machine learning industries, including products and services related to quantum computing or machine learning, such as the development or use of quantum computers or computing chips, superconducting materials, applications built on quantum computers, embedded artificial intelligence chips, or software specializing in the perception, collection, visualization, or management of big data.

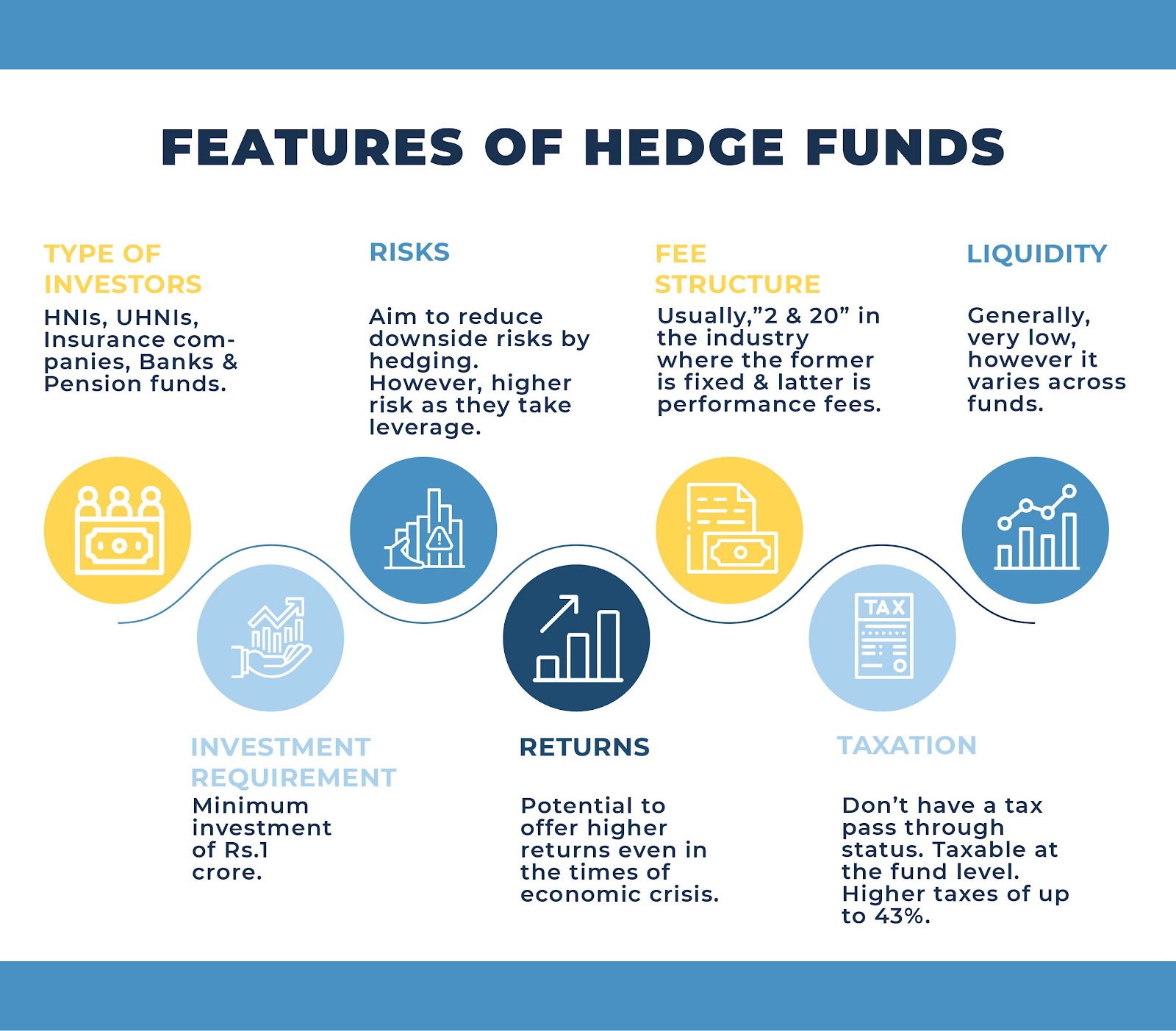

A hedge fund is a limited partnership of private investors whose money is pooled and managed by professional fund managers. These managers use a wide range of strategies, including leverage (borrowed money) and the trading of nontraditional assets, to earn above-average investment returns. A hedge fund investment is often considered a risky, alternative investment choice and usually requires a high minimum investment or net worth. Hedge funds typically target wealthy investors.

***

The Hedge Fund manager I am considering is a Registered Investment Adviser [RIA]

QUESTION: What is a Registered Investment Advisor?

If the fund manager is an entity, then any individual you deal with will be a registered investment adviser representative. If the fund manager is an individual, then that individual is a registered investment adviser. In either case, the designation implies several steps have been taken.

In order to become a registered investment adviser, an individual must register for and pass the Series 65 Uniform Investment Adviser Law Exam, a three-hour, 130-question computer-based exam administered by the North American Securities Administrators Association. Topics covered include economics and analysis, investment vehicles, investment recommendations and strategies, and ethics and legal guidelines. A passing score is 70 percent or higher.

Once an individual has passed the Series 65, he or she must then apply via Form ADV to become a registered investment adviser. This application is made to either a state authority or to the SEC, depending on the adviser’s assets under management. If assets under management exceed $30 million, then the adviser must register with the SEC.

Form ADV consists of two parts. Part I provides general information to the regulatory authority. Part II is designed to be distributed to potential clients, and includes disclosure of a decent amount of information about the adviser. If the manager is a registered investment adviser, then you should expect to receive as part of the offering documentation either a current copy of Part II of the adviser’s Form ADV or a brochure that contains all the current information in Part II of Form ADV.

In addition to filing Form ADV and paying a small fee, the registered investment adviser becomes subject to extra administrative/regulatory burden as well as capital adequacy requirements that state the Adviser must maintain certain net worth levels.

By and large, because of the extra administrative burden as well as restrictions on certain activities, hedge fund managers attempt to avoid registering as investment advisers. Whether such managers can or cannot avoid such registration is largely dependent upon the state in which the manager operates. In California, for instance, hedge fund managers must register as investment advisers. In New York, such registration is not necessary. Not surprisingly, hedge fund managers located in California are rare, while they are quite plentiful in New York.

Merger risk arbitrage, while a subset of a larger strategy called event-driven arbitrage, represents a sufficient portion of the market-neutral universe to warrant separate discussion.

Merger arbitrage earned a bad reputation in the 1980s when Ivan Boesky and others like him came to regard insider trading as a valid investment strategy. That notwithstanding, merger arbitrage is a respected strategy and when executed properly, can be highly profitable. It bets on the outcomes of mergers, takeovers and other corporate events involving two stocks which may become one.

Example:

A classic example is acquisition of SDL Inc. (SDLI) by JDS Uniphase Corp (JDSU). On July 10, 2010 JDSU announced its intent to acquire SDLI by offering to exchange 3.8 shares of its own shares for one share of SDLI. At that time, the JDSU shares traded at $101 and SDLI at $320.5. It was apparent that there was almost 20 percent profit to be realized if the deal went through (3.8 JDSU shares at $101 are worth $383 while SDLI was worth just $320.5).

This apparent mispricing reflected the market’s expectation about the deal’s outcome. Since the deal was subject to the approval of the U.S. Justice Department and shareholders, there was some doubt about its successful completion.

Risk arbitrageurs who did their homework and properly estimated the probability of success bought shares of SDLI and simultaneously sold short shares of JDSU on a 3.8 to 1 ratio, thus locking in the future profit. Convergence took place about eight months later, in February 2011, when the deal was finally approved and the two stocks began trading at exact parity, eliminating the mis-pricing and allowing arbitrageurs to realize a profit.

***

***

Hedge Fund Research defines the strategy as follows:

Merger Arbitrage,also known as risk arbitrage, involves investing in securities of companies that are the subject of some form of extraordinary corporate transaction, including acquisition or merger proposals, exchange offers, cash tender offers and leveraged buy-outs. These transactions will generally involve the exchange of securities for cash, other securities or a combination of cash and other securities. Typically, a manager purchases the stock of a company being acquired or merging with another company, and sells short the stock of the acquiring company. A manager engaged in merger arbitrage transactions will derive profit (or loss) by realizing the price differential between the price of the securities purchased and the value ultimately realized when the deal is consummated. The success of this strategy usually is dependent upon the proposed merger, tender offer or exchange offer being consummated.

When a tender or exchange offer or a proposal for a merger is publicly announced, the offer price or the value of the securities of the acquiring company to be received is typically greater than the current market price of the securities of the target company. Normally, the stock of an acquisition target appreciates while the acquiring company’s stock decreases in value. If a manager determines that it is probable that the transaction will be consummated, it may purchase shares of the target company and in most instances, sell short the stock of the acquiring company. Managers may employ the use of equity options as a low-risk alternative to the outright purchase or sale of common stock. Many managers will hedge against market risk by purchasing S&P put options or put option spreads.

SO – HOW MUCH IS A “FINANCIAL ADVISOR” REALLY WORTH?

This blog holds a rather uncomplimentary opinion of financial advisors, and the financial services and brokerage industry as a whole; deserved, or not? The entire site hints at this attitude as well, in favor of a going it alone or ME, Inc investing when possible. Nevertheless, it is reasonable to wonder how much boost in net-returns might an educated and informed, fee transparent and honest, fiduciary focused “financial advisor” add to a clients’ investment portfolio; all things being equal [ceteris paribus].

And, can it be quantified?

Well, according to Vanguard Brokerage Services®, perhaps as much as 3%? In a decade long paper from the Valley Forge, PA based mutual fund and ETF giant, Vanguard said financial advisors can generate returns through a framework focused on five wealth management principles:

• Being an effective behavioral coach: Helping clients maintain a long-term perspective and a disciplined approach is arguably one of the most important elements of financial advice. (Potential value added: up to 1.50%).

• Applying an asset location strategy: The allocation of assets between taxable and tax-advantaged accounts is one tool an advisor can employ that can add value each year. (Potential value added: from 0% to 0.75%).

• Employing cost-effective investments: This component of every advisor’s tool kit is based on simple math: Gross return less costs equals net return. (Potential value added: up to 0.45%).

• Maintaining the proper allocation through rebalancing: Over time, as investments produce various returns, a portfolio will likely drift from its target allocation. An advisor can add value by ensuring the portfolio’s risk/return characteristics stay consistent with a client’s preferences. (Potential value added: up to 0.35%).

• Implementing a spending strategy: As the retiree population grows, an advisor can help clients make important decisions about how to spend from their portfolios. (Potential value added: up to 0.70%).

Source: Financial Advisor Magazine, page 20, April 2014.

Assessment

However, Vanguard notes that while it’s possible all of these principles could add up to 3% in net returns for clients, it’s more likely to be an intermittent number than an annual one because some of the best opportunities to add value happen during extreme market lows and highs when angst or giddiness [fear and greed] can cause investors to bail on their well-thought-out investment plans.

And, is the study applicable to doctors and allied healthcare providers? Doe Vanguard have a vested interest in the topic. What about fee based versus fee-only financial advice?

Conclusion

Finally, recognize the plethora of other financial planning life-cycle topics addressed in this ME-P were not included in the Vanguard investment portfolio-only study a decade ago.

And what about today with contemporaneous internet advising, chat-rooms, linkedin, robo-advisors, reddit and the like?

I was having lunch with a close friend of mine. He mentioned that he had accumulated a significant sum of money and did not know what to do with it. It was sitting in bonds, and inflation was eating its purchasing power at a very rapid rate.

He is a dentist and had originally thought about expanding his business, but a shortage of labor and surging wages turned expanding into a risky and low-return investment. He complained that the stock market was extremely expensive. I agreed.*

He said that the only thing left was residential real estate. I pushed back. “What do you think will happen to the affordability of houses if – and most likely when – interest rates go up? Inflation is now 6%. I don’t know where it will be in a year or two, but what if it becomes a staple of the economy? Interest rates will not be where they are today. Even at 5% interest rates [I know, a number unimaginable today] houses become unaffordable to a significant portion of the population. Yes, borrowers’ incomes will be higher in nominal terms, but the impact of the doubling of interest rates on the cost of mortgages will be devastating to affordability.”

He rejoined, “But look at what happened to housing over the last twenty years. Housing prices have consistently increased, even despite the financial crisis.”

I agreed, but I qualified his statement: “Over the past twenty, actually thirty, years interest rates declined. I honestly don’t know where interest rates will be in the future. But probabilistically, knowing what we know now, the chances that they are going to be higher, much higher, are more likely than their staying low. Especially if you think that inflation will persist.”

We quickly shifted our conversation toward more meaningful topics, like kids.

It seems that every year I think we have finally reached the peak of crazy, only to be proven wrong the next year. The stock market and thus index funds, just like real estate, have only gone one way – up. Index funds became the blunt instrument of choice in an always-rising market. So far, this choice has paid off nicely.

The market is the most expensive it has ever been, and thus future returns of the market and index funds will be unexciting. (I am being gentle here.)

You don’t have to be a stock market junkie to notice the pervasive feeling of euphoria. But euphoria is a temporary, not a permanent emotion; and at least when it comes to the stock market, it is usually supplanted by despair. Market appreciation that was driven by expanding valuations was not a gift but a loan – the type of loan that must always be paid back with a high rate of interest.

I don’t know what straw will break the feeble back of this market or what will cause the music to stop (there, you got two analogies for the price of none). We are in an environment where there are very few good options. If you do nothing, your savings will be eaten away by inflation. If you do something, you find that most assets, including the stock market as a whole, are incredibly overvalued.

We are doing the only sensible thing that you can do today. We spend very little time thinking about straws or what will cause the music to stop or how overvalued the market is. We are focusing all our energy on patiently building a portfolio of high-quality, cash-generative, significantly undervalued businesses that have pricing power.

This has admittedly been less rewarding than taking risky bets on unimaginably expensive assets. It may lack the excitement of sinking money into the darlings you see in the news every day, but we hope that our stocks will look like rare gems when the euphoria condenses into despair. As we keep repeating in every letter, the market is insanely overvalued. Our portfolio is anything but – we don’t own “the market”.

*A question may arise:Why did I not tell my dentist friend to pick individual stocks? He runs a busy dental practice and wouldn’t have the time or the training to pick stocks.

Why didn’t I offer him our services? IMA manages all my and my family’s liquid assets, but I have a rule that I never (ever!) break – I don’t manage my friends’ money. I’ll help them as much as possible with free advice but will never have a professional relationship with them. I intentionally create a separation between my personal and professional lives. After a difficult day in the market, I want to be able to go for beers with friends and leave the market at the office.

Also, this simplifies my relationships with my friends. There is no ambiguity in our friendship.

Separate Account Management offers medical professionals customized personal money management services. In the typical separate account structure, a money manager invests the individual’s assets in stocks and bonds (as opposed to mutual funds providing exposure to specific asset classes) on a discretionary basis.

For physicians and healthcare providers with significant investment assets (e.g., $100,000), a separately managed portfolio can be customized to reflect their tax situation, social investment guidelines, and cash flow needs.

An additional benefit of the separate account management structure is that a client’s portfolio may be positioned over time as opportunities arise, rather than forcing stocks into the portfolio without regard to current conditions.

Although separate account management generally offers a higher degree of customization than mutual funds, fees for separate account management are generally consistent with mutual funds fees, especially given that separate account managers may discount their fees for larger portfolios.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Posted on February 19, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

SPONSOR: MarcinkoAssociates.com

***

***

Capital Market: This is a market where buyers and sellers engage in the trade of financial assets, including stocks and bonds. Capital markets feature several participants, including:

Companies: Firms that sell stocks and bonds to investors

Institutional investors: Investors who purchase stocks and bonds on behalf of a large capital base

Mutual funds: A mutual fund is an institutional investor that manages the investments of thousands of individuals

Hedge funds: A hedge fund is another type of institutional investor, which controls risk through hedging—a process of buying one stock and then shorting a similar stock to make money from the difference in their relative performance

With international stock markets comprising about 40 percent of the world’s capitalization as of 2023, a broad range of investment opportunities exist outside the borders of the U.S.

For investors who are looking to diversify their mutual fund portfolio with exposure to companies located outside the U.S., there exist two basic choices: A global mutual fund or an international mutual fund.

By definition, international funds invest in non-U.S. markets, while global funds may invest in U.S. stocks alongside non-U.S. stocks.

Make a Choice: The definition may seem clear, but what may seem less clear is why an investor might select one over the other. The reason that an investor may select a global fund is to provide the portfolio manager with the latitude to move the fund’s investments among non-U.S. markets and the U.S. market in order to take advantage of the shifts in relative opportunities these markets may present at any given moment.

By investing in a global fund, the challenge for the investor is that he or she may not know at any point in time their total exposure to the U.S. market within the context of their overall portfolio.

An Inside Look: As a consequence, some investors want to manage their allocation risk by setting the broad asset allocation for their portfolio and then identifying funds that are within those asset classes. For these investors, an international fund may make more sense since it allows them to maintain a greater adherence to their desired domestic/international stock allocation.

Keep in mind that asset allocation is an approach to help manage investment risk. Asset allocation does not guarantee against investment loss. As you consider a global or an international fund, you should also be aware of the fund’s approach to the inherent currency risks. Some funds choose to engage in strategies that may mitigate the effects of currency fluctuations, while others consider currency movements – up and down – to be an element of portfolio performance.

HFRI Fund of Funds Composite Index invests with multiple managers through funds or managed accounts. The strategy designs a diversified portfolio of managers with the objective of significantly lowering the risk (volatility) of investing with an individual manager. The Fund of Funds manager may allocate funds to numerous managers within a single strategy, or with numerous managers in multiple strategies. The investor has the advantage of diversification among managers and styles with significantly less capital than investing with separate managers. The HFRI Fund of Funds Index is not included in the HFRI Fund Weighted Composite Index.

HFRI Fund Weighted Composite Index is a global, equal-weighted index of over 2,000 single-manager funds that report to HFR Database. Constituent funds report monthly net of all fees performance in U.S. Dollar and have a minimum of $50 Million under management or a twelve (12) month track record of active performance. The HFRI Fund Weighted Composite Index does not include Funds of Hedge Funds.

Sector allocation in an equity or fixed-income context refers to a portfolio managers’ decision to invest in a particular broad market sector or industry.

A sector allocation or breakdown can help an investor observe the investment allocations of a mutual or other fund. Fund companies regularly provide sector reporting in their marketing materials. Sector investing can influence investments in the fund. A fund may target a specific sector such as technology, or seek to diversify among many sectors.

Some funds may have restraints on sector investments. This may occur with environmental, social, and governance (ESG) focused funds. These funds seek to exclude industries or companies that their investors consider undesirable for various reasons such as tobacco producers or oil exploration companies.

The ultimate sector allocation decision is likely to combine macroeconomic views with judgments about inter-sector and intra-sector relative values, among other reasons.

To most people the holiday season means decorations at home and at work, but it also can mean “window dressing” in your mutual fund.

This somewhat disparaging term is used to describe the practice of a mutual fund making cosmetic changes to its portfolio just before the end of each calendar quarter. It’s done because funds publish their exact holdings of securities four times a year based on what they own at the end of each quarter.

“The basic concept is that managers are either hiding their mistakes or adding winners to make themselves look a little smarter,” says Russ Kinnel, director of manager research at fund researcher Morningstar Inc. in Chicago. “Of course, it doesn’t necessarily help performance,” he adds.

HFRI: Fund of Funds invests with multiple managers through funds or managed accounts. The strategy designs a diversified portfolio of managers with the objective of significantly lowering the risk (volatility) of investing with an individual manager.

The Fund of Funds manager may allocate funds to numerous managers within a single strategy, or with numerous managers in multiple strategies. The investor has the advantage of diversification among managers and styles with significantly less capital than investing with separate managers.

Posted on October 28, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Peak earnings season: Five of the Magnificent SevenStocks will be among the 181 companies reporting their earnings this week. Alphabet is in the Mag Seven lead-off spot on Tuesday, Microsoft and Meta step to the plate on Wednesday, and Apple and Amazon rounding out the lineup and this baseball metaphor on Thursday. These companies account for almost 25% of the S&P 500, which is up 40% over the past year and not far off its record closing number from earlier this month. But, the approaching election, it could be a volatile week in the stock markets.

***

Markets: Stocks are currently driving the narrative on Wall Street. Last week, bonds sold off in a big way (driving yields to their highest level since July) in a sign investors are dialing back expectations of more aggressive rate cuts from the Federal Reserve.

Stocks nevertheless handled the bond volatility with aplomb, and with help from Tesla’s 22% one-day rise, the NASDAQ is sitting within 2% of its record high.

Thirty one years ago yesterday, the first exchange-traded fund (ETF) in the US launched. In the decades since, these once-niche investment products have become ubiquitous on Wall Street, disrupting the mutual fund industry and transforming people’s relationship with the stock market.

On January 29th, 1993, a spider decoration hanging in the American Stock Exchange heralded the arrival of the first US ETF—what’s now called the SPDR S&P 500 ETF Trust. It had a measly $6.5 million in assets and no one really paid much attention to it. The first US ETF is now the world’s biggest, with $375 billion in assets, and the ETF sector in total had amassed $6.5 trillion in assets by the end of 2022. While mutual funds still have 3x the amount of assets that ETFs have, the tide is turning: Investors poured $600 billion into US ETFs on a net basis last year, but pulled out almost $1 trillion from mutual funds.

Definition: An ETF is simply a security that tracks the performance of a particular basket of investments, like stocks. The SPDR S&P 500 ETF, for example, tracks the performance of companies in the S&P 500. Many other ETFs also track indexes, allowing people to park their money in funds that follow the ebbs and flows of the broader market.