![]()

Understanding Mutual Fund Share Classes and Costs

[By Rick Kahler MS CFP® ChFC CCIM]

Doctors – Do you want to add $500,000 or more to your retirement nest egg? Pay attention to the fees that mutual funds charge you for investing your money. Few physicians or small investors understand that the same mutual fund can charge a wide range of fees, depending on the share class you select.

Doctors – Do you want to add $500,000 or more to your retirement nest egg? Pay attention to the fees that mutual funds charge you for investing your money. Few physicians or small investors understand that the same mutual fund can charge a wide range of fees, depending on the share class you select.

For many medical professionals and most Americans, the best way to build wealth is to live on less than you make and invest 15% to 35% of your paycheck into mutual funds. It’s essential to find funds that are diversified among five or more asset classes.

The Choice After Mutual Fund Selection

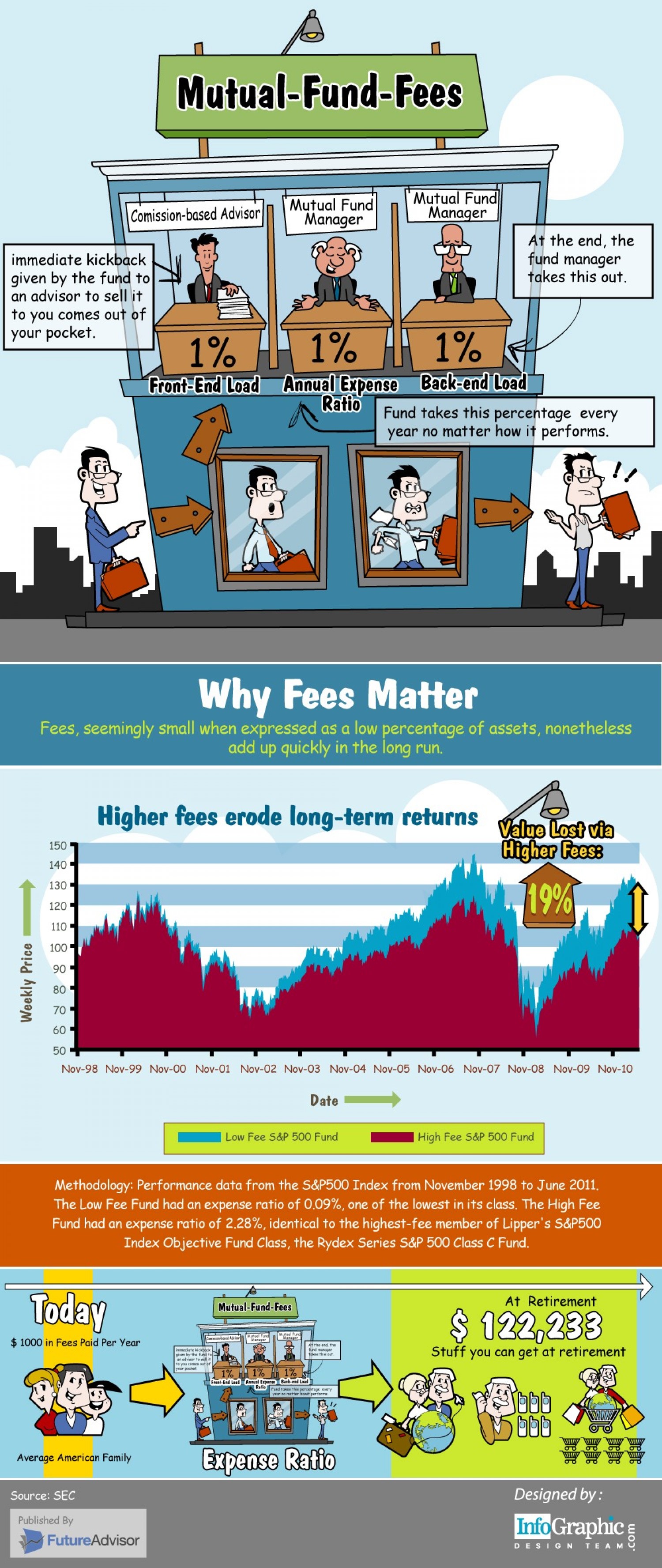

Once you’ve found a mutual fund with a mix of appropriate asset classes, there’s one more choice to make. What class of shares should you buy? The most popular classes are A, B, and I shares; however, many funds offer even more classes like C, F, and R shares.

The difference between the classes has nothing to do with the underlying management or structure of the mutual fund. All share classes own the same stocks or bonds. The difference lies in the fees you pay the mutual fund for their services and for commissions to brokers who sell the funds.

Types of Share Classes

Many A shares and almost all B, C, F, and R shares impose sales commissions, often called “loads,” which are based on the amount you invest. For example, A shares usually charge you a one-time commission ranging from 4.0% to 5.75% of your initial investment. With B shares there is no up-front commission, but they will charge you a stiff penalty to sell the funds in the early years and will impose an additional annual commission often ranging from .25% to 1.00% a year. Some discount brokers will waive the upfront commission on A shares for their customers.

Typically the best shares to purchase are the I class, which don’t have any commissions associated with them and offer the lowest management fees of any other share class. The downside is that I shares often require a minimum investment ranging from $10,000 to $1,000,000. Financial advisors often have relationships with discount brokers that allow them to purchase the shares for clients in smaller amounts.

Fee Comparisons

It pays to compare fees.

For example, a comparison of fees available at the website of the Financial Industry Regulatory Authority (finra.org/fundanalyzer) shows that a $10,000 investment in the Invesco S&P 500 Index fund’s A shares will cost you $129 a year, while the same investment in the C shares will run $163. If instead you invest in the Fidelity Spartan 500 Index fund you will pay just $11.50 annually, which is over 1% less than the Invesco A shares.

The Savings

It’s surprising what a 1% savings means to your retirement nest egg. According to a study by the Vanguard Group reported by Jack Hough in SmartMoney.com, if a 25-year old saves 9% of his pay in a mutual fund, paying .25% a year in expenses versus 1.25% amounts to having an additional $500,000 by age 65.

Assessment

With all that said, most investors don’t have either the knowledge or the time to construct a diversified portfolio of mutual funds that will carry them through to retirement. Paying a fee or commission for advice can ultimately save you a lot of money. There are advisors who will help smaller investors select investments for an hourly or flat fee. Others charge fees based on the size of your portfolio, which normally range from .3% to 1.5%.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

- PRACTICES: www.BusinessofMedicalPractice.com

- HOSPITALS: http://www.crcpress.com/product/isbn/9781466558731

- CLINICS: http://www.crcpress.com/product/isbn/9781439879900

- ADVISORS: www.CertifiedMedicalPlanner.org

- FINANCE: Financial Planning for Physicians and Advisors

- INSURANCE: Risk Management and Insurance Strategies for Physicians and Advisors

- Dictionary of Health Economics and Finance

- Dictionary of Health Information Technology and Security

- Dictionary of Health Insurance and Managed Care

![]()

![]()

Share this:

Filed under: Investing, Portfolio Management, Retirement and Benefits | Tagged: discount brokers, Financial Industry Regulatory Authority, FINRA, Index Funds, Invesco, Mutual Fund fees, mutual fund share classes, Mutual Funds, retirement planning, Rick Kahler CFP®, stock-brokers |

On Fund Fees

Rick – Nice post but too much work and far TMI.

IMHO: Just index it with Vanguard; and forget it!

Dr. Damian

LikeLike

Fees

http://www.ajc.com/weblogs/atlanta-bargain-hunter/2013/may/06/wes-moss/

Remember, when it comes to getting advice a good well respected financial advisor won’t be free.

Martin

LikeLike

Invisible Fees

As a stock-broker, when I left a wire-house brokerage firm to start my own fee-only RIA firm, I had to explain our advisory fees, which had previously been embedded in products.

Yep, that’s right; my commission sales-fees were embedded in financial “products.” Just, par for the course for the industry.

Anonymous

LikeLike

Merrill Lynch Fees

Report Finds Merrill Lynch Charges Investors Highest Fees.

https://wealthmanagement.com/blog/report-finds-merrill-lynch-charges-investors-highest-fees?NL=WM-27&Issue=WM-27_20150919_WM-27_904&sfvc4enews=42&cl=article_2&utm_rid=CPG09000002702210&utm_campaign=3761&utm_medium=email&elq2=e836cc105ce64feb8153cdac88335260

“The seemingly trivial cost of fees, compounded over decades, adds up to astounding losses for retirement savers”

Bill Harris [Founder and CEO of Personal Capital]

via Clayton

LikeLike