BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

In the modern professional landscape, specialization is often celebrated, but it is the rare individual who bridges two highly technical, demanding fields that seem worlds apart. Podiatrists who are also Certified Public Accountants (CPAs) embody this uncommon duality. They combine the clinical precision of medical practice with the analytical rigor of financial expertise. While the pairing may appear unconventional at first glance, the intersection of podiatric medicine and accounting creates a powerful skill set that benefits not only the practitioners themselves but also the patients, healthcare organizations, and broader medical community they serve.

Podiatrists focus on diagnosing and treating conditions of the foot and ankle—areas of the body that are deceptively complex and essential to mobility. Their work requires deep anatomical knowledge, surgical skill, and the ability to manage chronic conditions such as diabetes‑related neuropathy. At the same time, podiatrists operate in a healthcare environment that is increasingly shaped by financial pressures, regulatory requirements, and business realities. Running a podiatry practice demands far more than clinical competence; it requires strategic financial management, compliance with tax and healthcare regulations, and the ability to navigate insurance reimbursement systems. This is where the CPA credential becomes a transformative asset.

A podiatrist who is also a CPA brings a level of financial literacy that most medical professionals simply do not possess. They understand the intricacies of tax law, financial reporting, and business planning. This dual expertise allows them to manage their practices with exceptional efficiency. They can evaluate overhead costs, optimize billing processes, and make informed decisions about equipment purchases or expansion plans. In an era where many private practices struggle to remain financially viable, this combination of skills can be the difference between sustainability and closure.

Beyond practice management, podiatrists with CPA credentials are uniquely positioned to contribute to healthcare policy and administration. They can analyze the financial impact of regulatory changes, assess the cost‑effectiveness of treatment protocols, and participate in leadership roles within hospitals or medical groups. Their ability to interpret financial data gives them a voice in discussions that shape the future of healthcare delivery. They can advocate for reimbursement models that reflect the true value of podiatric care, or design budgeting strategies that improve patient access without compromising quality.

This dual background also enhances patient care in subtle but meaningful ways. A podiatrist who understands the financial side of healthcare can help patients navigate insurance coverage, anticipate out‑of‑pocket costs, and make informed decisions about treatment options. They can design care plans that balance medical necessity with financial feasibility, especially for patients managing chronic conditions that require ongoing attention. In this sense, financial knowledge becomes an extension of patient advocacy.

***

***

The path to becoming both a podiatrist and a CPA is not an easy one. Each field requires years of education, rigorous examinations, and ongoing professional development. The commitment to mastering both disciplines speaks to a mindset of intellectual curiosity and resilience. These individuals are not content with a single lens through which to view their work; they seek a multidimensional understanding of the systems they operate within. This mindset is increasingly valuable in a healthcare environment that demands adaptability and interdisciplinary thinking.

Moreover, the combination of podiatry and accounting reflects a broader trend toward hybrid professional identities. As industries become more interconnected, the most impactful professionals are often those who can bridge gaps between disciplines. A podiatrist‑CPA exemplifies this evolution. They are clinicians who understand balance sheets, business owners who understand anatomy, and problem‑solvers who can approach challenges from both scientific and financial perspectives.

In the future, the healthcare system may see more professionals pursuing dual competencies like this. The pressures of modern medical practice—ranging from reimbursement challenges to the complexities of electronic health records—require a blend of clinical and administrative expertise. While not every podiatrist will become a CPA, the example set by those who do highlights the value of interdisciplinary knowledge. It encourages medical professionals to broaden their skill sets and engage more deeply with the financial and operational aspects of their work.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

A forensic accountant is a financial professional who blends traditional accounting expertise with investigative skills to uncover, analyze, and explain financial irregularities. While many people associate accounting with routine bookkeeping or tax preparation, forensic accounting operates in a very different arena—one where money trails intersect with legal disputes, fraud schemes, and complex financial conflicts. The role requires not only technical knowledge of accounting principles but also the curiosity of an investigator and the clarity of a communicator who can translate intricate financial data into understandable conclusions.

At its core, forensic accounting involves the examination of financial information for use in legal settings. The word “forensic” itself means “suitable for use in court,” which captures the essence of the profession. Forensic accountants are often called upon when financial information must be scrutinized with a level of detail and rigor that can withstand legal scrutiny. Their work may support civil litigation, criminal investigations, insurance claims, business valuations, or internal corporate inquiries. Because of this, they frequently collaborate with attorneys, law enforcement agencies, regulatory bodies, and corporate leadership.

One of the most recognized responsibilities of a forensic accountant is the detection and investigation of fraud. Fraud can take many forms—embezzlement, financial statement manipulation, asset misappropriation, or complex schemes involving shell companies and hidden transactions. Forensic accountants use a combination of analytical procedures, data mining techniques, and professional skepticism to identify patterns that suggest wrongdoing. They may trace the flow of funds through multiple accounts, reconstruct destroyed or incomplete records, or analyze inconsistencies in financial statements. Their goal is not only to uncover what happened but also to determine how it happened and who was responsible.

Beyond fraud detection, forensic accountants play a crucial role in litigation support. In legal disputes involving financial matters, attorneys rely on forensic accountants to provide objective, evidence‑based analysis. This may include calculating economic damages, evaluating the value of a business, assessing lost profits, or determining the financial impact of a breach of contract. In divorce proceedings, forensic accountants may help identify hidden assets or evaluate the true income of a spouse. Their findings often become part of expert reports submitted to the court, and they may be called to testify as expert witnesses. In this capacity, they must present complex financial information in a clear, concise manner that judges and juries can understand.

Another important aspect of forensic accounting is prevention. Organizations increasingly recognize the value of proactive measures to reduce the risk of fraud and financial misconduct. Forensic accountants may design internal controls, conduct risk assessments, or evaluate corporate governance practices to help organizations strengthen their defenses. By identifying vulnerabilities before they are exploited, they contribute to a healthier financial environment and help protect stakeholders from potential losses.

The skill set required for forensic accounting is broad and demanding. Technical proficiency in accounting and auditing is essential, but equally important are analytical thinking, attention to detail, and strong communication skills. Forensic accountants must be able to interpret large volumes of financial data, identify anomalies, and draw logical conclusions. They must also be comfortable working with digital tools, as modern investigations often involve electronic records, data analytics, and specialized software. Integrity and objectivity are critical, given the legal implications of their work and the trust placed in their findings.

The profession also requires adaptability. Every case is different, and forensic accountants must be prepared to navigate unfamiliar industries, evolving fraud techniques, and changing regulatory environments. They may work in public accounting firms, government agencies, law enforcement units, insurance companies, or as independent consultants. Regardless of the setting, the common thread is their role as financial detectives who bring clarity to situations where the truth is obscured by complexity or deception.

In summary, a forensic accountant is far more than a traditional number‑cruncher. They are investigators, analysts, communicators, and trusted advisors who operate at the intersection of finance and law. Their work uncovers hidden truths, supports the pursuit of justice, and helps organizations safeguard their financial integrity. As financial systems grow more complex and fraud schemes become more sophisticated, the role of the forensic accountant continues to expand in importance. Their unique blend of skills makes them indispensable in a world where transparency and accountability are more critical than ever.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The Net Investment Income Tax (NIIT) occupies a distinctive place in the modern U.S. tax landscape. Introduced as part of the Affordable Care Act, it was designed to generate revenue from higher‑income households by taxing certain forms of unearned income. Although it affects a relatively small portion of taxpayers, its implications reach into investment strategy, tax planning, and broader debates about fairness and economic policy. Understanding how the NIIT works—and why it exists—offers insight into the evolving relationship between tax policy and wealth in the United States.

At its core, the NIIT is a 3.8 percent surtax applied to specific types of investment income for individuals whose modified adjusted gross income exceeds statutory thresholds. These thresholds—$200,000 for single filers and $250,000 for married couples filing jointly—are not indexed for inflation. As a result, over time, more taxpayers may find themselves subject to the tax even if their real purchasing power has not increased. This “bracket creep” is one of the subtle but important features of the NIIT, shaping its long‑term reach.

The tax applies only to “net investment income,” a term that includes interest, dividends, capital gains, rental income, royalties, and passive business income. It does not apply to wages, self‑employment earnings, or distributions from qualified retirement plans. The logic behind this distinction is straightforward: the NIIT targets income derived from wealth rather than labor. In practice, this means that two taxpayers with identical total income may face different NIIT liabilities depending on how much of their income comes from investments versus work.

The mechanics of the NIIT involve a comparison between two amounts: net investment income and the excess of modified adjusted gross income over the applicable threshold. The tax is applied to whichever of these two figures is smaller. This structure ensures that the NIIT functions as a surtax on high‑income households without taxing investment income for those below the threshold. It also means that taxpayers with large investment portfolios but modest overall income may avoid the tax entirely, while those with high wages and relatively small investment income may still owe it.

One of the most significant effects of the NIIT is its influence on investment behavior. Because the tax applies to capital gains, it can affect decisions about when to sell appreciated assets. Taxpayers may choose to time sales to avoid pushing their income above the threshold in a given year. Others may shift toward tax‑exempt investments, such as municipal bonds, or toward assets that generate unrealized rather than realized gains. The NIIT therefore becomes not just a revenue tool but a factor shaping the broader investment landscape.

The tax also interacts with other parts of the tax code in ways that can be complex. For example, rental real estate income is generally subject to the NIIT unless the taxpayer qualifies as a real estate professional and materially participates in the activity. Trusts and estates face their own NIIT rules, often reaching the surtax threshold at much lower income levels than individuals. These layers of complexity mean that the NIIT is often a central topic in tax planning for high‑income households, especially those with diverse investment portfolios.

Beyond its technical features, the NIIT reflects broader policy debates about equity and the distribution of tax burdens. Supporters argue that it helps ensure that high‑income individuals contribute a fair share to the cost of public programs, particularly those related to health care. Because investment income is disproportionately concentrated among wealthier households, the NIIT is seen as a way to align tax policy with ability to pay. Critics, however, contend that the tax discourages investment, adds unnecessary complexity, and imposes an additional layer of taxation on income that may already be subject to corporate taxes or other levies.

Despite these debates, the NIIT has become a stable part of the federal tax system. It raises billions of dollars annually and plays a role in funding health‑related initiatives. As discussions about tax reform continue, the NIIT often resurfaces as policymakers consider how best to balance revenue needs with economic incentives. Whether it remains unchanged, is expanded, or is modified in future legislation, the NIIT will continue to shape the financial decisions of high‑income taxpayers and contribute to the ongoing conversation about how the United States taxes wealth.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

A concept of tax fairness that states that people with different amounts of wealth or different amounts of income should pay tax at different rates. Wealth includes assets such as houses, cars, stocks, bonds, and savings accounts. Income includes wages, interest and dividends, and other payments.

A business authorized by the IRS to participate in the IRS e-file Program. The business may be a sole proprietorship, a partnership, a corporation, or an organization. Authorized IRS e-file Providers include Electronic Return Originators (EROs), Transmitters, Intermediate Service Providers, and Software Developers. These categories are not mutually exclusive. For example, an ERO can at the same time, be a Transmitter, a Software Developer, or an Intermediate Service Provider, depending on the function being performed.

Assuming all other dependency tests are met, the citizen or resident test allows taxpayers to claim a dependency exemption for persons who are U.S. citizens for some part of the year or who live in the United States, Canada, or Mexico for some part of the year.

Amount that taxpayers can claim for a “qualifying child” or “qualifying relative”. Each exemption reduces the income subject to tax. The exemption amount is a set amount that changes from year to year. One exemption is allowed for each qualifying child or qualifying relative claimed as a dependent.

This allows tax refunds to be deposited directly to the taxpayer’s bank account. Direct Deposit is a fast, simple, safe, secure way to get a tax refund. The taxpayer must have an established checking or savings account to qualify for Direct Deposit. A bank or financial institution will supply the required account and routing transit numbers to the taxpayer for Direct Deposit.

The transmission of tax information directly to the IRS using telephones or computers. Electronic filing options include (1) Online self-prepared using a personal computer and tax preparation software, or (2) using a tax professional. Electronic filing may take place at the taxpayer’s home, a volunteer site, the library, a financial institution, the workplace, malls and stores, or a tax professional’s place of business.

Electronic preparation means that tax preparation software and computers are used to complete tax returns. Electronic tax preparation helps to reduce errors.

The Authorized IRS e-file Provider that originates the electronic submission of an income tax return to the IRS. EROs may originate the electronic submission of income tax returns they either prepared or collected from taxpayers. Some EROs charge a fee for submitting returns electronically.

Free from withholding of federal income tax. A person must meet certain income, tax liability, and dependency criteria. This does not exempt a person from other kinds of tax withholding, such as the Social Security tax.

Amount that taxpayers can claim for themselves, their spouses, and eligible dependents. There are two types of exemptions-personal and dependency. Each exemption reduces the income subject to tax. While each is worth the same amount, different rules apply to each.

A program sponsored by the IRS in partnership with participating states that allows taxpayers to file federal and state income tax returns electronically at the same time.

The federal government levies a tax on personal income. The federal income tax provides for national programs such as defense, foreign affairs, law enforcement, and interest on the national debt.

Provides benefits for retired workers and their dependents as well as for disabled workers and their dependents. Also known as the Social Security tax.

To mail or otherwise transmit to an IRS service center the taxpayer’s information, in specified format, about income and tax liability. This information-the return-can be filed on paper, electronically (e-file).

Determines the rate at which income is taxed. The five filing statuses are: single, married filing a joint return, married filing a separate return, head of household, and qualifying widow(er) with dependent child.

Spending and income records and items to keep for tax purposes, including paycheck stubs, statements of interest or dividends earned, and records of gifts, tips, and bonuses. Spending records include canceled checks, cash register receipts, credit card statements, and rent receipts.

A foster child is any child placed with a taxpayer by an authorized placement agency or by court order. Eligible foster children may be claimed by taxpayers for tax benefits.

Money, goods, services, and property a person receives that must be reported on a tax return. Includes unemployment compensation and certain scholarships. It does not include welfare benefits and nontaxable Social Security benefits.

You must meet the following requirements: 1. You are unmarried or considered unmarried on the last day of the year. 2. You paid more than half the cost of keeping up a home for the year. 3. A qualifying person lived with you in the home for more than half the year (except temporary absences, such as school). However, a dependent parent does not have to live with the taxpayer.

Taxes on income, both earned (salaries, wages, tips, commissions) and unearned (interest, dividends). Income taxes can be levied on both individuals (personal income taxes) and businesses (business and corporate income taxes).

Performs services for others. The recipients of the services do not control the means or methods the independent contractor uses to accomplish the work. The recipients do control the results of the work; they decide whether the work is acceptable. Independent contractors are self-employed.

A person who represents the concerns or special interests of a particular group or organization in meetings with lawmakers. Lobbyists work to persuade lawmakers to change laws in the group’s favor.

An economic system based on private enterprise that rests upon three basic freedoms: freedom of the consumer to choose among competing products and services, freedom of the producer to start or expand a business, and freedom of the worker to choose a job and employer.

You are married and both you and your spouse agree to file a joint return. (On a joint return, you report your combined income and deduct your combined allowable expenses.)

You must be married. This method may benefit you if you want to be responsible only for your own tax or if this method results in less tax than a joint return. If you and your spouse do not agree to file a joint return, you may have to use this filing status.

Used to provide medical benefits for certain individuals when they reach age 65. Workers, retired workers, and the spouses of workers and retired workers are eligible to receive Medicare benefits upon reaching age 65.

When the amount of a credit is greater than the tax owed, taxpayers can only reduce their tax to zero; they cannot receive a “refund” for any excess nonrefundable credit.

Allow taxpayers to “sign” their tax returns electronically. The PIN, a five-digit self-selected number, ensures that electronically submitted tax returns are authentic. Most taxpayers can qualify to use a PIN.

Taxes on property, especially real estate, but also can be on boats, automobiles (often paid along with license fees), recreational vehicles, and business inventories.

Benefits that cannot be withheld from those who don’t pay for them, and benefits that may be “consumed” by one person without reducing the amount of the product available for others. Examples include national defense, streetlights, and roads and highways. Public services include welfare programs, law enforcement, and monitoring and regulating trade and the economy.

To be a qualifying child, the dependent must meet eight tests: (1) relationship, (2) age, (3) residence, (4) support, (5) citizenship or residency, (6) joint return, (7) qualifying child of more than one person, and (8) dependent taxpayer.

There are tests that must be met to be a qualifying relative, they are: (1) not a qualifying child, (2) member of household or relationship, (3) citizenship or residency, (4) gross income, (5) support, (6) joint return, and (7) dependent taxpayer.

If your spouse died in 2010, you can use married filing jointly as your filing status for 2010 if you otherwise qualify to use that status. The year of death is the last year for which you can file jointly with your deceased spouse. You may be eligible to use qualifying widow(er) with dependent child as your filing status for two years following the year of death of your spouse. For example, if your spouse died in 2010, and you have not remarried, you may be able to use this filing status for 2011 and 2012. This filing status entitles you to use joint return tax rates and the highest standard deduction amount (if you do not itemize deductions). This status does not entitle you to file a joint return.

Compensation received by an employee for services performed. A salary is a fixed sum paid for a specific period of time worked, such as weekly or monthly.

Similar to Social Security and Medicare taxes. The self-employment tax rate is 15.3 percent of self-employment profit. The self-employment tax is calculated on Schedule SE—Self-Employment Tax. The self-employment tax is reported on Form 1040, U.S. Individual Income Tax Return.

If on the last day of the year, you are unmarried or legally separated from your spouse under a divorce or separate maintenance decree and you do not qualify for another filing status.

Provides benefits for retired workers and their dependents as well as for the disabled and their dependents. Also known as the Federal Insurance Contributions Act (FICA) tax.

Develops software for the purposes of (1) formatting electronic tax return information according to IRS specifications, and/or (2) transmitting electronic tax return information directly to the IRS.

For dependency test purposes, support includes food, clothing, shelter, education, medical and dental care, recreation, and transportation. It also includes welfare, food stamps, and housing provided by the state. Support includes all income, taxable and nontaxable.

Interest income that is not subject to income tax. Tax-exempt interest income is earned from bonds issued by states, cities, or counties and the District of Columbia.

The amount of tax that must be paid. Taxpayers meet (or pay) their federal income tax liability through withholding, estimated tax payments, and payments made with the tax forms they file with the government.

Money and goods received for services performed by food servers, baggage handlers, hairdressers, and others. Tips go beyond the stated amount of the bill and are given voluntarily.

Taxes on economic transactions, such as the sale of goods and services. These can be based on a set of percentages of the sales value (ad valorem-sales taxes), or they can be a set amount on physical quantities (“per unit”-gasoline taxes).

The concept that people in different income groups should pay different rates of taxes or different percentages of their incomes as taxes. “Unequals should be taxed unequally.”

A system of compliance that relies on individual citizens to report their income freely and voluntarily, calculate their tax liability correctly, and file a tax return on time.

This provides free income tax return preparation for certain taxpayers. The VITA program assists taxpayers who have limited or moderate incomes, have limited English skills, or are elderly or disabled. Many VITA sites offer electronic preparation and transmission of income tax returns.

Compensation received by employees for services performed. Usually, wages are computed by multiplying an hourly pay rate by the number of hours worked.

Money, for example, that employers withhold from employees paychecks. This money is deposited for the government. (It will be credited against the employees’ tax liability when they file their returns.) Employers withhold money for federal income taxes, Social Security taxes and state and local income taxes in some states and localities.

In the world of financial advising, few principles are as foundational—and as misunderstood—as diversification. Clients often come to advisors hoping for bold moves and big wins. Yet the most prudent strategy we offer is not a thrilling stock pick or a market-timing miracle, but a quiet, calculated spread of risk. Diversification, in essence, is the art of saying “sorry” in advance—for not chasing every hot trend, for not going all-in, and for not promising perfection. But it’s also the strategy that earns trust, builds resilience, and delivers long-term value.

Diversification means allocating assets across different sectors, geographies, and investment vehicles to reduce exposure to any single point of failure. For financial advisors, it’s not just a portfolio tactic—it’s a philosophy of humility. It acknowledges that markets are unpredictable, that no one can consistently forecast winners, and that protecting capital is just as important as growing it.

Clients may initially resist this approach. They might question why their portfolio includes lagging sectors or why we’re not doubling down on tech or crypto. This is where our role as educators becomes critical. We explain that diversification isn’t about avoiding risk—it’s about managing it. It’s the reason why, when tech stumbles, healthcare or consumer staples might hold steady. It’s why international exposure can buffer domestic volatility. And it’s why fixed income still matters, even in a rising-rate environment.

The challenge for advisors is that diversification rarely feels heroic. It doesn’t make headlines. It doesn’t deliver overnight gains. Instead, it delivers consistency. It smooths out the ride. It allows clients to sleep at night. And over time, it compounds into something powerful: confidence.

***

***

One of the most effective ways to communicate this is through behavioral coaching. We remind clients that diversification is designed to protect them from their own impulses—from chasing trends, reacting to headlines, or panicking during downturns. It’s a guardrail against emotional investing. And when markets inevitably wobble, diversified portfolios give us the credibility to say, “This is why we planned ahead.”

Moreover, diversification is a relationship tool. It shows clients that we’re not betting their future on a single idea. We’re building something durable. We’re thinking about their retirement, their children’s education, their legacy. And we’re doing it with a strategy that’s built to last.

In short, diversification may feel like an apology to the thrill-seeker in every investor. But it’s also a promise: that we’re here to protect, to guide, and to deliver results that matter—not just today, but for decades to come.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

The Sudden Money Paradox: When Wealth Disrupts Instead of Liberates

The “Sudden Money Paradox” refers to the counterintuitive reality that receiving a large financial windfall—whether through inheritance, lottery winnings, business sales, or legal settlements—can lead to emotional turmoil, poor decision-making, and even financial ruin. While most people assume that sudden wealth guarantees security and happiness, the paradox reveals that it often destabilizes lives instead.

At the heart of this paradox is the psychological shock that accompanies a dramatic change in financial status. Sudden wealth can trigger a cascade of emotions: excitement, guilt, anxiety, and confusion. Recipients may feel overwhelmed by the responsibility of managing their newfound resources, especially if they lack financial literacy or a support system. The windfall can also disrupt one’s sense of identity. Someone who previously lived modestly may struggle to reconcile their new status with their values, relationships, and lifestyle. This identity dissonance can lead to impulsive decisions, such as extravagant spending, quitting a job prematurely, or giving away money without boundaries.

Financial mismanagement is a common consequence of sudden wealth. Without a plan, recipients may fall prey to scams, make poor investments, or underestimate tax obligations. The phenomenon known as “Sudden Wealth Syndrome” describes the psychological stress and behavioral pitfalls that often follow a windfall. Studies show that lottery winners and professional athletes frequently go bankrupt within a few years of receiving large sums. The paradox lies in the fact that the very thing meant to provide freedom—money—can instead create chaos.

***

***

Relationships also suffer under the weight of sudden wealth. Friends and family may treat the recipient differently, leading to feelings of isolation or mistrust. Requests for financial help can strain bonds, and recipients may struggle to set boundaries. The paradox deepens when generosity becomes a source of conflict rather than connection.

Experts like Susan Bradley, founder of the Sudden Money® Institute, emphasize that financial transitions require more than technical advice—they demand emotional intelligence and structured support. Her work highlights the importance of pausing before making major decisions, assembling a transition team of advisors, and creating a personal vision for the money. These steps help recipients align their financial choices with their values and long-term goals.

Ultimately, the Sudden Money Paradox teaches that wealth is not just a numerical asset—it’s a psychological and relational force. Navigating it successfully requires self-awareness, education, and guidance. When approached thoughtfully, sudden money can be a catalyst for growth and purpose. But without preparation, it risks becoming a burden disguised as a blessing.

This paradox challenges society’s assumptions about wealth and reminds us that financial well-being is as much about mindset and meaning as it is about money itself.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Product costing deals with determining the total costs involved in the production of a good or service. Costs may be broken down into subcategories, such as variable, fixed, direct, or indirect costs. Cost accounting is used to measure and identify those costs, in addition to assigning overhead to each type of product created by the company.

Managerial accountants calculate and allocate overhead charges to assess the full expense related to the production of a good. The overhead expenses may be allocated based on the number of goods produced or other activity drivers related to production, such as the square footage of the facility. In conjunction with overhead costs, managerial accountants use direct costs to properly value the cost of goods sold and inventory that may be in different stages of production.

Marginal costing (sometimes called cost-volume-profit analysis) is the impact on the cost of a product by adding one additional unit into production. It is useful for short-term economic decisions. The contribution margin of a specific product is its impact on the overall profit of the company. Margin analysis flows into break-even analysis, which involves calculating the contribution margin on the sales mix to determine the unit volume at which the business’s gross sales equals total expenses. Break-even point analysis is useful for determining price points for products and services.

Cash Flow Analysis

Managerial accountants perform cash flow analysis in order to determine the cash impact of business decisions. Most companies record their financial information on the accrual basis of accounting. Although accrual accounting provides a more accurate picture of a company’s true financial position, it also makes it harder to see the true cash impact of a single financial transaction. A managerial accountant may implement working capital management strategies in order to optimize cash flow and ensure the company has enough liquid assets to cover short-term obligations.

When a managerial accountant performs cash flow analysis, he will consider the cash inflow or outflow generated as a result of a specific business decision. For example, if a department manager is considering purchasing a company vehicle, he may have the option to either buy the vehicle outright or get a loan. A managerial accountant may run different scenarios by the department manager depicting the cash outlay required to purchase outright upfront versus the cash outlay over time with a loan at various interest rates.

Inventory Turnover Analysis

Inventory turnover is a calculation of how many times a company has sold and replaced inventory in a given time period. Calculating inventory turnover can help businesses make better decisions on pricing, manufacturing, marketing, and purchasing new inventory. A managerial accountant may identify the carrying cost of inventory, which is the amount of expense a company incurs to store unsold items.

If the company is carrying an excessive amount of inventory, there could be efficiency improvements made to reduce storage costs and free up cash flow for other business purposes.

Constraint Analysis

Managerial accounting also involves reviewing the constraints within a production line or sales process. Managerial accountants help determine where bottlenecks occur and calculate the impact of these constraints on revenue, profit, and cash flow. Managers then can use this information to implement changes and improve efficiencies in the production or sales process.

Financial Leverage Metrics

Financial leverage refers to a company’s use of borrowed capital in order to acquire assets and increase its return on investments. Through balance sheet analysis, managerial accountants can provide management with the tools they need to study the company’s debt and equity mix in order to put leverage to its most optimal use.

Performance measures such as return on equity, debt to equity, and return on invested capital help management identify key information about borrowed capital, prior to relaying these statistics to outside sources. It is important for management to review ratios and statistics regularly to be able to appropriately answer questions from its board of directors, investors, and creditors.

Accounts Receivable (AR) Management

Appropriately managing accounts receivable (AR) can have positive effects on a company’s bottom line. An accounts receivable aging report categorizes AR invoices by the length of time they have been outstanding. For example, an AR aging report may list all outstanding receivables less than 30 days, 30 to 60 days, 60 to 90 days, and 90+ days.

Through a review of outstanding receivables, managerial accountants can indicate to appropriate department managers if certain customers are becoming credit risks. If a customer routinely pays late, management may reconsider doing any future business on credit with that customer.

Budgeting, Trend Analysis, and Forecasting

Budgets are extensively used as a quantitative expression of the company’s plan of operation. Managerial accountants utilize performance reports to note deviations of actual results from budgets. The positive or negative deviations from a budget also referred to as budget-to-actual variances, are analyzed in order to make appropriate changes going forward.

Managerial accountants analyze and relay information related to capital expenditure decisions. This includes the use of standard capital budgeting metrics, such as net present value and internal rate of return, to assist decision-makers on whether to embark on capital-intensive projects or purchases. Managerial accounting involves examining proposals, deciding if the products or services are needed, and finding the appropriate way to finance the purchase. It also outlines payback periods so management is able to anticipate future economic benefits.

Managerial accounting also involves reviewing the trendline for certain expenses and investigating unusual variances or deviations. It is important to review this information regularly because expenses that vary considerably from what is typically expected are commonly questioned during external financial audits. This field of accounting also utilizes previous period information to calculate and project future financial information. This may include the use of historical pricing, sales volumes, geographical locations, customer tendencies, or financial information.

Why It Is Difficult to Be a Part-Time Financial Planner Today

In theory, part-time financial planning offers flexibility and work-life balance, making it an attractive option for professionals seeking reduced hours. However, in practice, the role of a financial planner has evolved into a demanding, full-time commitment. The complexity of financial markets, client expectations, regulatory requirements, and technological advancements make part-time financial planning increasingly difficult to sustain.

One of the primary challenges is client relationship management. Financial planning is deeply personal and trust-based. Clients expect consistent communication, timely updates, and proactive advice. A part-time planner may struggle to maintain the same level of responsiveness as full-time counterparts, especially during volatile market conditions or life-changing events like retirement, divorce, or inheritance. Delayed responses or limited availability can erode client confidence and damage long-term relationships.

***

***

Another obstacle is the rapid pace of financial change. Tax laws, investment products, insurance regulations, and retirement planning strategies are constantly evolving. Staying current requires ongoing education, certifications, and industry engagement. For part-time planners, keeping up with these changes while managing clients and administrative tasks can be overwhelming. Falling behind risks offering outdated or suboptimal advice, which could lead to compliance issues or client dissatisfaction.

Regulatory compliance adds another layer of complexity. Financial planners must adhere to strict standards set by organizations like FINRA, the SEC, and state regulators. These include documentation, disclosures, fiduciary responsibilities, and continuing education. Compliance is non-negotiable and time-consuming, regardless of hours worked. Part-time planners face the same scrutiny and liability as full-time professionals, but with fewer hours to manage the workload.

Technology, while a powerful tool, also presents challenges. Clients increasingly expect digital access to their portfolios, real-time updates, and virtual meetings. Managing these platforms requires technical proficiency and regular maintenance. Part-time planners may find it difficult to keep systems updated, troubleshoot issues, or provide tech support, especially if they lack dedicated staff.

Business development is another hurdle. Building and maintaining a client base requires networking, marketing, and referrals. Part-time planners often have limited time to attend events, follow up with leads, or cultivate relationships. This can hinder growth and make it difficult to compete with full-time advisors who are more visible and accessible.

Finally, there’s the issue of income and scalability. Many financial planners earn through commissions, assets under management (AUM), or fee-based models. Part-time work often means fewer clients and lower revenue, which can make it hard to justify the costs of licensing, insurance, software, and office space. Without scale, profitability becomes a challenge.

In conclusion, while the idea of part-time financial planning may seem appealing, the realities of the profession make it difficult to execute effectively. The demands of client care, compliance, education, and business development require consistent attention and availability. Unless the industry adapts to support flexible models, part-time financial planners will continue to face significant barriers to success.

SPEAKING: ME-P Editor Dr. David Edward Marcinko MBA MEd will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Bettors are currently able to deduct 100% of their gambling losses, so they only pay taxes on their winnings. But starting next year, only 90% of gambling losses will be deductible.

So, if a professional gambler wins $100,000, then loses $100,000 that same year, according to the New York Times:

In 2025, that gambler would owe taxes on $0.

In 2026, that gambler would owe taxes on $10,000.

Bettors could even end up paying taxes if they finished the year with a net loss.

A brand is a name, term, design, symbol or any other feature that distinguishes one seller’s goods or service from those of other sellers. Brands are used in business, marketing and advertising for recognition and, importantly, to create and store value as brand equity for the object identified, to the benefit of the brand’s clients, patients, customers, its owners and shareholders. Brand names are sometimes distinguished from generic or store brands.

Brand management, also known as Marketing, is responsible for the overall management of a brand. This includes everything from product or service development and marketing to advertising and public relations. All of these aspects work together to create a particular image or reputation for a brand. The goal of brand management is to create a robust and positive reputation for a brand that will result in increased sales and market share.This process helps companies create a unique identity for their products or services in the marketplace. A successful brand management strategy can build client, patient and customer loyalty .

Branding is essential for financial advisors, doctors and businesses because it involves creating a unique identity for a company’s products, offerings and services. It can also help build customer, client and patient loyalty and emotionally connect with the practitioner. Branding can be complex, but it is essential to understand the basics before starting a brand strategy.

Thus, doctors, podiatrists, dentists, CPAs, insurance agents, financial advisors and their practices need to understand the different aspects of branding and brand management to create a strong brand identity.

Posted on May 28, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Rick Kahler MSFP CFP®

***

***

OVER HEARD IN THE FINANCIAl ADVISOR’S LOUNGE

A basic strategy for asset protection is to hold various assets in different entities. Putting real estate, small businesses, and other assets into trusts, corporations, or limited liability companies (LLCs) is effective protection that is relatively easy to put into practice. Not only do I recommend this strategy to clients, I use it myself. Recently, however, I discovered a potential downside.

About 25 years ago, I invested in some rare coins in a corporation I owned and put them into a safe deposit box owned by the corporation. When my business relocated 12 years ago, the safe deposit box billing was not forwarded to the new address and was never paid again. Last year I went to retrieve the coins from the safe deposit box, which I had not visited in 25 years. I discovered the box had been drilled open three years earlier and my collection turned over to the unclaimed property division of the State Treasurer’s office.

I was told getting the coins back would be simple enough. I just needed to verify that I owned the company which owned them by providing the corporation’s tax ID number. However, the corporation no longer existed. I didn’t have a record of its tax ID number. The IRS wouldn’t verify the number without my giving them the address the company had used. That address was a post office box number that I no longer used and couldn’t remember. The state’s position was “no tax ID, no coins.” The only verification of my identity as owner of the corporation was my signature on the bank’s safe deposit box application. Eventually, with the support of bank officers who were willing to swear that I was who I claimed to be, I got my coin collection back. The hassle involved in this process was a reminder of an important component of asset protection. Maintain accurate records so you don’t end up hiding assets from yourself.

***

***

A good start is to create a master file of all the entities that hold your assets. This can be any system that’s easy for you to use: a computer spreadsheet, a set of file folders, or a single paper list. Share it as appropriate with your CPA, attorney, or financial planner. The master list should include the name of each company, its date of incorporation, tax ID number, address, and other relevant information like phone or bank account numbers. Also keep an inventory of the assets each company owns.

Once you’ve created a master list, it’s essential to keep it up to date as you buy or sell assets, close companies, or transfer ownership. Set up a system, as well, to remind yourself of tasks like filing tax returns, completing minutes of annual meetings, and paying the annual safe deposit box rent. Make your record-keeping easier by eliminating unnecessary complications.

For example, you probably don’t need a separate address for each trust, corporation, or LLC. Instead of creating a separate company for each asset, you might consider grouping smaller assets within one entity. I’d suggest first discussing the pros and cons with an attorney or financial planner. For larger assets like real estate, I do recommend holding each one separately.

When I talk to clients about asset protection, I mention that part of the price we pay for it is an increase in paperwork. It’s easy to accept that idea with casual good intentions. The case of my reclaimed coin investment is a good reminder of the importance of keeping up with that paperwork. If we don’t, we might protect ourselves right out of access to our own assets.

A Certified Public Accountant (CPA) is a licensed professional who has passed an examination administered by a state’s Board of Accountancy. State CPA exams are created under guidelines issued by The American Institute of Certified Public Accountants (AICPA). The Uniform CPA Exam can only be taken by accountants who already have professional experience in the field and a bachelor’s degree.CPAs are not fiduciaries.

Not all accountants are CPAs. Accountants who are CPAs are licensed by their state’s Board of Accountancy after passing the Uniform CPA Exam. CPAs prepare reports that accurately reflect the business dealings of the companies and individuals that hire them. Many prepare tax returns for individuals or businesses and advise them on ways to minimize taxes. Obtaining the CPA designation requires a bachelor’s degree, typically with a major in business administration, finance, or accounting. Other majors are acceptable if the applicant meets the minimum requirements for accounting courses.

Enrolled Agent

Although not a CPA, an Enrolled Agent [EA] is a person who has earned the privilege of representing taxpayers before the Internal Revenue Service [IRS]. This is done by either passing a three-part comprehensive IRS test covering individual and business tax returns, or through experience as a former IRS employee. Enrolled agent status is the highest credential the IRS awards. Individuals who obtain this elite status must adhere to ethical standards and complete 72 hours of continuing education courses every three years.

Certified Managerial Accountant

A Certified Management Accountant (CMA), which is issued by the Institute of Management Accountants (IMA), builds on financial accounting proficiency by adding management skills that aid in making strategic business decisions based on financial data.

Oftentimes, the reports and analyses prepared by certified management accountants (CMAs) will go above and beyond those required by generally accepted accounting principles (GAAP).

For example, in addition to a company’s required GAAP financial statements, CMAs may prepare additional management reports that provide specific insights useful to corporate decision-makers, such as performance metrics on specific company departments, products, or even employees.

Certified Financial Analyst

A Certified Financial Analyst [CFA] is a globally-recognized professional designation offered by the CFA Institute, an organization that measures and certifies the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management, and security analysis. From 1963 through November 2023, more than 3.7 million candidates had taken the CFA exam. The overall pass rate was 45%. From 2014 through 2023, the 10-year average pass rate was 43%.1

CFA Institute. The CFA Institute was formerly the Association for Investment Management and Research (AIMR).

The CFA charter is one of the most respected designations in finance and is widely considered to be the gold standard in the field of investment analysis. To become a charter holder, candidates must pass three difficult exams, have a bachelors degree, and have at least 4,000 hours of relevant professional experience over a minimum of three years. Passing the CFA Program exams requires strong discipline and an extensive amount of studying.

There are more than 200,000 CFA charter holders worldwide in 164 countries.The designation is handed out by the CFA Institute, which has 11 offices worldwide and 160 local member societies.

Posted on April 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

OVER HEARD IN THE FINANCIAL ADVISOR’S LOUNGE

***

***

By Perry D’Alessio, CPA [D’Alessio Tocci & Pell LLP]

What I see in my accounting practice is that significant accumulation in younger physician portfolio growth is not happening as it once did. This is partially because confidence in the equity markets is still not what it was; but that doctors are also looking for better solutions to support their reduced incomes.

For example, I see older doctors with about 25 percent of their wealth in the market, and even in retirement years, do not rely much on that accumulation to live on. Of this 25 percent, about 80 percent is in their retirement plan, as tax breaks for funding are just too good to ignore.

What I do see is that about 50 percent of senior physician wealth is in rental real estate, both in a private residence that has a rental component, and mixed-use properties. It is this that provides a good portion of income in retirement.

***

***

QUESTION: So, could I add dialog about real estate as a long term solution for retirement?

Yes, as I believe a real estate concentration in the amount of 5 percent is optimal for a diversified portfolio, but in a very passive way through mutual or index funds that are invested in real estate holdings and not directly owning properties.

Today, as an option, we have the ability to take pension plan assets and transfer marketable securities for rental property to be held inside the plan collecting rents instead of dividends.

Real estate holdings never vary very much, tend to go up modestly, and have preferential tax treatment due to depreciation of the property against income.

Posted on April 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Beneficiary designations can provide a relatively easy way to transfer an account or insurance policy upon your death. However, if you’re not careful, missing or outdated beneficiary designations can easily cause your estate plan to go awry.

Where you can find them

Here’s a sampling of where you’ll find beneficiary designations:

In several states, so-called “lady bird” deeds for real estate

***

***

10 tips about beneficiary designations

Because beneficiary designations are so important, keep these things in mind in your estate planning:

Remember to name beneficiaries. If you don’t name a beneficiary, one of the following could occur:

The account or policy may have to go through probate. This process often results in unnecessary delays, additional costs, and unfavorable income tax treatment.

The agreement that controls the account or policy may provide for “default” beneficiaries. This could be helpful, but it’s possible the default beneficiaries may not be whom you intended.

Name both primary and contingent beneficiaries. It’s a good practice to name a “back up” or contingent beneficiary in case the primary beneficiary dies before you. Depending on your situation, you may have only a primary beneficiary. In that case, consider whether it may make sense to name a charity (or charities) as the contingent beneficiary.

Update for life events. Review your beneficiary designations regularly and update them as needed based on major life events, such as births, deaths, marriages, and divorces.

Read the instructions. Beneficiary designation forms are not all alike. Don’t just fill in names — be sure to read the form carefully. If necessary, you can draft your own customized beneficiary designation, but you should do this only with the guidance of an experienced attorney or tax advisor.

Coordinate with your will and trust. Whenever you change your will or trust, be sure to talk with your attorney about your beneficiary designations. Because these designations operate independently of your other estate planning documents, it’s important to understand how the different parts of your plan work as a whole.

Think twice before naming individual beneficiaries for particular assets. For example, you may establish three accounts of equal value initially and name a different child as beneficiary of each account. Over the years, the accounts may grow or be depleted unevenly, so the three children end up receiving different amounts — which is not what you originally intended.

Avoid naming your estate as beneficiary. If you designate a beneficiary on your 401(k), for example, it won’t have to go through probate court to be distributed to the beneficiary. If you name your estate as beneficiary, the account will have to go through probate. For IRAs and qualified retirement plans, there may also be unfavorable income tax consequences.

Use caution when naming a trust as beneficiary. Consult your attorney or CPA before naming a trust as beneficiary for IRAs, qualified retirement plans, or annuities. There are situations where it makes sense to name a trust — for example if:

Your beneficiaries are minor children

You’re in a second marriage

You want to control access to funds

Be aware of tax consequences. Many assets that transfer by beneficiary designation come with special tax consequences. It’s helpful to work with an experienced tax advisor to help provide planning ideas for your particular situation.

Use disclaimers when necessary — but be careful. Sometimes a beneficiary may actually want to decline (disclaim) assets on which they’re designated as beneficiary. Keep in mind that disclaimers involve complex legal and tax issues and require careful consultation with your attorney and CPA.

Suppose that in a new Accountable Care Organization [ACO] contract, a certain medical practice was awarded a new global payment or capitation styled contract that increased revenues by $100,000 for the next fiscal year. The practice had a gross margin of 35% that was not expected to change because of the new business. However, $10,000 was added to medical overhead expenses for another assistant and all Account’s Receivable (AR) are paid at the end of the year, upon completion of the contract.

Cost of Medical Services Provided (COMSP):

The Costs of Medical Services Provided (COMSP) for the ACO business contract represents the amount of money needed to service the patients provided by the contract. Since gross margin is 35% of revenues, the COMSP is 65% or $65,000. Adding the extra overhead results in $75,000 of new spending money (cash flow) needed to treat the patients. Therefore, divide the $75,000 total by the number of days the contract extends (one year) and realize the new contract requires about $ 205.50 per day of free cash flows.

Assumptions

Financial cash flow forecasting from operating activities allows a reasonable projection of future cash needs and enables the doctor to err on the side of fiscal prudence. It is an inexact science, by definition, and entails the following assumptions:

All income tax, salaries and Accounts Payable (AP) are paid at once.

Durable medical equipment inventory and pre-paid advertising remain constant.

Gains/losses on sale of equipment and depreciation expenses remain stable.

Gross margins remain constant.

The office is efficient so major new marginal costs will not be incurred.

***

***

Physician Reactions:

Since many physicians are still not entirely comfortable with global reimbursement, fixed payments, capitation or ACO reimbursement contracts; practices may be loath to turn away short-term business in the ACA era. Physician-executives must then determine other methods to generate the additional cash, which include the following general suggestions:

1. Extend Account’s Payable

Discuss your cash flow difficulties with vendors and emphasize their short-term nature. A doctor and her practice still has considerable cache’ value, especially in local communities, and many vendors are willing to work them to retain their business

2. Reduce Accounts Receivable

According to most cost surveys, about 30% of multi-specialty group’s accounts receivable (ARs) are unpaid at 120 days. In addition, multi-specialty groups are able to collect on only about 69% of charges. The rest was written off as bad debt expenses or as a result of discounted payments from Medicare and other managed care companies. In a study by Wisconsin based Zimmerman and Associates, the percentages of ARs unpaid at more than 90 days is now at an all time high of more than 40%. Therefore, multi-specialty groups should aim to keep the percentage of ARs unpaid for more than 120 days, down to less than 20% of the total practice. The safest place to be for a single specialty physician is probably in the 30-35% range as anything over that is just not affordable.

The slowest paid specialties (ARs greater than 120 days) are: multi-specialty group practices; family practices; cardiology groups; anesthesiology groups; and gastroenterologists, respectively. So work hard to get your money, faster. Factoring, or selling the ARs to a third party for an immediate discounted amount is not usually recommended.

3. Borrow with Short-Term Bridge Loans

Obtain a line of credit from your local bank, credit union or other private sources, if possible in an economically constrained environment. Beware the time value of money, personal loan guarantees, and onerous usury rates. Also, beware that lenders can reduce or eliminate credit lines to a medical practice, often at the most inopportune time.

4. Cut Expenses

While this is often possible, it has to be done without demoralizing the practice’s staff.

5. Reduce Supply Inventories

If prudently possible; remember things like minimal shipping fees, loss of revenue if you run short, etc.

6. Taxes

Do not stop paying withholding taxes in favor of cash flow because it is illegal.

Hyper-Growth Model:

Now, let us again suppose that the practice has attracted nine more similar medical contracts. If we multiple the above example tenfold, the serious nature of potential cash flow problem becomes apparent. In other words, the practice has increased revenues to one million dollars, with the same 35% margin, 65% COMSP and $100,000 increase in operating overhead expenses.

Using identical mathematical calculations, we determine that $750,000 / 365days equals $2,055.00 per day of needed new free cash flows! Hence, indiscriminate growth without careful contract evaluation and cash flow analysis is a prescription for potential financial disaster.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com

Without proper internal accounting controls, a medical practice [MD, DO, DPM, DDS, DMD] might never reach peak profitability. Internal controls designed and implemented by the physician-owner help prevent bad things from happening.

Embezzlement protection is the classic example. However, internal controls also help ensure good things happen most of the time; according to colleague Dr. Gary Bode; MSA, CPA.

Some Common Embezzlement “Old School” Schemes

Here are some ‘old-school” embezzlement schemes to avoid; however the list is imaginative and endless.

The physician-owner pocketing cash “off the books”. To the IRS, this is like embezzlement to intentionally defraud it out of tax money.

Employee’s pocketing cash from cash transactions. This is why you see cashiers following protocol that seems to take forever when you’re in the grocery check out line. This is also why you see signs offering a reward if he/she is not offered a receipt. This is partly why security cameras are installed.

Bookkeepers writing checks to themselves. This is easiest to do in flexible software programs like QuickBooks, Peachtree Accounting and related financial software. It is one of the hardest schemes to detect. The bookkeeper self-writes and cashes the check to their own name; and then the name on the check is changed in the software program to a vendor’s name. So a real check exists which looks legitimate on checking statements unless a picture of it is available.

Employees ordering personal items on practice credit cards.

Bookkeepers receiving patient checks and illegally depositing them in an unauthorized, pseudo practice checking account, set up by themselves in a bank different from yours. They then withdraw funds at will. If this scheme uses only a few patients, who are billed outside of the practice’s accounting software it is hard to detect. The doctor must have a good knowledge of existing patients to catch the ones “missing” from practice records. Monitoring the bookkeeper’s lifestyle might raise suspicion, but this scheme is generally low profile and protracted. Checking the accounting software “audit trail” shows the required original invoice deletions or credit memos in a less sophisticated version of this scheme.

Bookkeepers writing payroll checks to non-existent employees. This scheme works well in larger practices and medical clinics with high seasonal turnover of employees, and practices with multiple locations the podiatrist-owner doesn’t visit often.

Bookkeepers writing inflated checks to existing employees, vendors or subcontractors. Physician-owners should beware if romantic relationships between the bookkeeper and other practice related parties.

Bookkeepers writing checks to false vendors. This is another low profile, protracted scheme that exploits the podiatrists-owner’s indifference to accounts payable.

Assessment

Operating efficiency, safeguarding assets, compliance with existing laws and accuracy of financial transactions are common goals of internal managerial and cost accounting in medical practice.

CONCLUSION

Hopefully, the above is a good review to prevent common practice embezzlement schemes. Unfortunately, it is a never-ending endeavor.

References: Marcinko, DE: Dictionary of Health Economics and Finance. Springer Publishing Company, NY 2007.

Tax avoidance—An action taken to lessen tax liability and maximize after-tax income.

Tax evasion—The failure to pay or a deliberate underpayment of taxes.

Underground economy—Money-making activities that people don’t report to the government, including both illegal and legal activities.

Voluntary compliance—A system of compliance that relies on individual citizens to report their income freely and voluntarily, calculate their tax liability correctly, and file a tax return on time.

Posted on March 3, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITION

By Staff Reporters

***

***

The IRS three-year rule, formally known as the statute of limitations, establishes a three-year window from the date you file your tax return or the due date of the return, whichever is later. During this period, both you and the IRS can make changes to your tax return. This means you have three years to claim a refund if you discover you overpaid, and the IRS has three years to audit your return or assess additional taxes if they find discrepancies.

This rule isn’t just about setting deadlines — it’s about creating a fair playing field. It gives taxpayers enough time to discover and correct mistakes while also allowing the IRS a reasonable time frame to verify the accuracy of returns. The clock typically starts ticking on April 15th of the year following the tax year, unless you filed early or received an extension.

However, there are important exceptions to this rule. If you underreport your income by more than 25%, the IRS gets six years to audit your return. And if you never file a return or file a fraudulent one, there is no statute of limitations. The IRS can come knocking at any time.

For most taxpayers, though, once three years have passed, the IRS can no longer come back and demand more money.

Posted on February 25, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITION

“Show Me the Money”

By Staff Reporters

***

***

In some situations, an inheritance might complicate an estate and add to the estate tax burden. If there are sufficient assets and income to accomplish financial goals, more assets are not needed. A disclaimer may be useful. This is an unqualified refusal to accept a gift or inheritance, that is, when you “just say no”. You have decided not to accept a sizable gift made under a will, trust or other document.

When you disclaim the property, certain requirements must be met:

The disclaimer must be irrevocable;

The refusal must be in writing;

The refusal must be received within nine months;

You must not have accepted any interest in the property; and

As a result of the refusal, the property will pass to someone else.

The property passes under the terms of the decedents will, as if you had predeceased the decedent. If the filer of the disclaimer has control, the property will be included in the disclaimant’s estate and can only be passed to another as a gift for as an inheritance. The intent of the disclaimer is to renounce and never take control of the property.

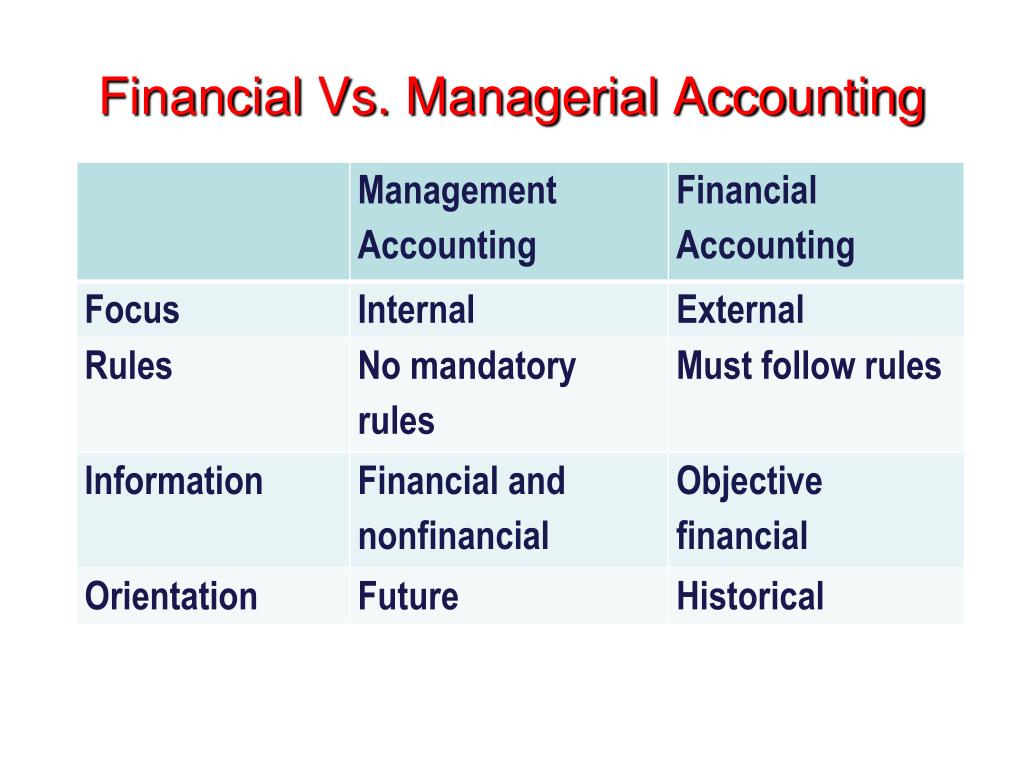

Financial accounting and managerial accounting are two distinct branches of the accounting field, each serving different purposes and stakeholders. Financial accounting focuses on creating external reports that provide a snapshot of a company’s financial health for investors, regulators, and other outside parties. Managerial accounting, meanwhile, is an internal process aimed at aiding managers in making informed business decisions.

Objectives of Financial Accounting

Financial accounting is primarily concerned with the preparation and presentation of financial statements, which include the balance sheet, income statement, and cash flow statement. These documents are meticulously crafted to reflect the company’s financial performance over a specific period, providing insights into its profitability, liquidity, and solvency. The objective is to offer a clear, standardized view of the financial state of the company, ensuring that external entities have a reliable basis for evaluating the company’s economic activities.

The process of financial accounting also involves the meticulous recording of all financial transactions. This is achieved through the double-entry bookkeeping system, where each transaction is recorded in at least two accounts, ensuring that the accounting equation remains balanced. This systematic approach provides accuracy and accountability, which are paramount in financial reporting. CPA = Certified Public Accountant.

Objectives of Managerial Accounting

Managerial accounting is designed to meet the information needs of the individuals who manage organizations. Unlike financial accounting, which provides a historical record of an organization’s financial performance, managerial accounting focuses on future-oriented reports. These reports assist in planning, controlling, and decision-making processes that guide the day-to-day, short-term, and long-term operations.

At the heart of managerial accounting is budgeting. Budgets are detailed plans that quantify the economic resources required for various functions, such as production, sales, and financing. They serve as benchmarks against which actual performance can be measured and evaluated. This enables managers to identify variances, investigate their causes, and implement corrective actions. Another objective of managerial accounting is cost analysis. Managers use cost accounting methods to understand the expenses associated with each aspect of production and operation. By analyzing costs, they can determine the profitability of individual products or services, control expenditures, and optimize resource allocation.

Performance measurement is another key objective. Managerial accountants develop metrics and key performance indicators (KPIs) to assess the efficiency and effectiveness of various business processes. These performance metrics are crucial for setting goals, evaluating outcomes, and aligning individual and departmental objectives with the overall strategy of the organization. CMA = Certified Managerial Accountant

Reporting Standards in Financial Accounting

The bedrock of financial accounting is the adherence to established reporting standards, which ensure consistency, comparability, and transparency in financial statements. Globally, the International Financial Reporting Standards (IFRS) are widely adopted, setting the guidelines for how particular types of transactions and other events should be reported in financial statements. In the United States, the Financial Accounting Standards Board (FASB) issues the Generally Accepted Accounting Principles (GAAP), which serve a similar purpose. These standards are not static; they evolve in response to changing economic realities, stakeholder needs, and advances in business practices.

For instance, the shift towards more service-oriented economies and the rise of intangible assets have led to updates in revenue recognition and asset valuation guidelines. The convergence of IFRS and GAAP is an ongoing process aimed at creating a unified set of global standards that would benefit multinational corporations and investors by reducing the complexity and cost of complying with multiple accounting frameworks.