BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on March 12, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

The IRS 1099-k Tax Form

By Staff Reporters and IRS

***

***

Third party payment platforms are required to send you a 1099-K tax form if you made more than $5,000 on the platform in 2024. This reporting change will give the IRS a clearer picture of how much you earned in untaxed income this year to help ensure you pay your taxes properly. For the 2025 tax year, the threshold will drop to $2,500.

The IRS originally rolled out a plan to implement new reporting requirements for anyone earning over $600 via payment apps in 2023. After two years of delays, the tax agency has decided to implement a phased rollout, lifting the reporting threshold to $5,000 for the 2024 tax year.

If you earn freelance or self-employment income, you’re likely no stranger to 1099 tax forms. You’re required to report any net earnings over $400 to the IRS when you file your tax return, even if you don’t receive a 1099. The 1099-K tax change places a reporting requirement on payment apps so the IRS can keep better tabs on income earnings that might otherwise go unreported.

Monetarism is the belief that changes in the money supply are the main determinant of changes in inflation, associated especially with Milton Friedman, an American economist. Cases of hyperinflation have indeed been associated with the rapid printing of money. But when governments adopted monetarist policies in the late 1970s and early 1980s, they found money supply hard to control and also struggled to decide which measure of money supply was best to target. Monetarist policies were abandoned in favor of inflation targeting.

Monetary financing is the direct financing of government spending by the central bank. This happened during the hyperinflation in Germany in 1923 and was thus regarded as anathema for a long period afterwards. As a result, some commentators viewed quantitative easing after the financial crisis of 2007-09 with great suspicion. Technically, however, QE is not monetary financing, because central banks only buy government bonds in the secondary market and because they pay interest on reserves (the money they create).

Monetary policy The use, normally by the central bank, of interest rates and other tools to try to influence the economy. Interest rates are raised when the bank is trying to control inflation and lowered when inflation is low and it is trying to revive the economy. The financial crisis of 2007-09 led central banks to face the zero lower bound. This prompted many of them to use a new tool, quantitative easing, which was designed to bring down long-term rates or bond yields.

Posted on March 9, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

A Morton’s fork is a type of false dilemma in which contradictory observations lead to the same conclusion.

Morton’s Fork:Claims its origin from John Morton, the Archbishop of Canterbury, a public policymaker who used convoluted and contradictory logic to establish tax laws in the mid-15th century.

He contended that whoever lived humbly must be saving much money and hence would be able to pay higher taxes; and those that lived lavish lives were obviously rich, so they could also pay higher taxes.

In other words: a Hobsons Choice between two equally unpleasant alternatives.

Posted on March 7, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

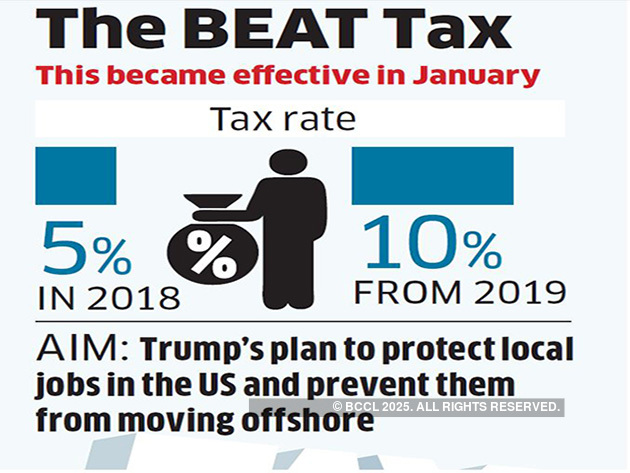

Base-Erosion Anti-Abuse Tax (BEAT): The 2017 tax reforms moved the U.S. from a worldwide taxation system to a quasi-territorial system, so foreign earnings are no longer included in a company’s domestic tax base.

To discourage companies operating in the U.S. from avoiding tax liability by shifting profits out of the country, Congress imposed a 10% minimum tax called Base-Erosion Anti-Abuse Tax (BEAT). The BEAT rate will increase from 10% to 12.5% in 2026.

Posted on March 3, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITION

By Staff Reporters

***

***

The IRS three-year rule, formally known as the statute of limitations, establishes a three-year window from the date you file your tax return or the due date of the return, whichever is later. During this period, both you and the IRS can make changes to your tax return. This means you have three years to claim a refund if you discover you overpaid, and the IRS has three years to audit your return or assess additional taxes if they find discrepancies.

This rule isn’t just about setting deadlines — it’s about creating a fair playing field. It gives taxpayers enough time to discover and correct mistakes while also allowing the IRS a reasonable time frame to verify the accuracy of returns. The clock typically starts ticking on April 15th of the year following the tax year, unless you filed early or received an extension.

However, there are important exceptions to this rule. If you underreport your income by more than 25%, the IRS gets six years to audit your return. And if you never file a return or file a fraudulent one, there is no statute of limitations. The IRS can come knocking at any time.

For most taxpayers, though, once three years have passed, the IRS can no longer come back and demand more money.

Posted on February 28, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

CLARINET LESSONS

By Staff Reporters

***

***

In 1962, a parent was able to deduct the cost of their child’s clarinet lessons and the instrument itself, after they were prescribed by an orthodontist to fix the child’s overbite, according to a report by Boston University School of Law.

Unsurprisingly, it initially went to court, where it was ruled that it qualified as a legitimate medical expense (despite not being the most traditional treatment).

So, when it comes to the IRS, it’s not always about prescriptions or surgeries — sometimes, even clarinet lessons can count.

Posted on February 25, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITION

“Show Me the Money”

By Staff Reporters

***

***

In some situations, an inheritance might complicate an estate and add to the estate tax burden. If there are sufficient assets and income to accomplish financial goals, more assets are not needed. A disclaimer may be useful. This is an unqualified refusal to accept a gift or inheritance, that is, when you “just say no”. You have decided not to accept a sizable gift made under a will, trust or other document.

When you disclaim the property, certain requirements must be met:

The disclaimer must be irrevocable;

The refusal must be in writing;

The refusal must be received within nine months;

You must not have accepted any interest in the property; and

As a result of the refusal, the property will pass to someone else.

The property passes under the terms of the decedents will, as if you had predeceased the decedent. If the filer of the disclaimer has control, the property will be included in the disclaimant’s estate and can only be passed to another as a gift for as an inheritance. The intent of the disclaimer is to renounce and never take control of the property.

Understanding how economic behavior factors into health and health care decisions can benefit anyone interested in this field. However, the following groups of individuals may benefit most from the study of health economics:

Medical providers: Doctors, nurses, and assistants can evaluate new treatments, technologies, and services to determine ways to deliver value-based care. Medical providers benefit from understanding the economics behind these developments [MD/DO, DPM, DDS/DMD, RN, PA, etc].

Administrators: Health care administrators process insurance co-payments and manage financial metrics for health care providers. Learning the intricacies of health care economics can provide the necessary context as they liaise with insurance providers and use new technologies to process payments.

Policymakers or public health officials: Those who are in charge of policy decisions at the local, state, federal, or international levels benefit from understanding the economic relationship between stakeholders and the general public.

Business leaders: Because many Americans receive private insurance, health care becomes a major expense for employers. Business leaders must understand the health economics outlook to appease their employees, shareholders, and even their customers.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Posted on February 20, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

UPDATE

By PayPal and Staff Reporters

***

***

NOTE: Information provided by PayPal is not intended to be and should not be construed as tax advice. For questions about your specific tax situation, please consult a tax professional.

Payment processors, including PayPal, are required to provide information to the US Internal Revenue Service (IRS) about customers who receive payments for the sale of goods and services above the reporting threshold in a calendar year.

Will I have to pay taxes when sending and receiving money on PayPal – what exactly is changing?

The Internal Revenue Service (IRS) announced transitional reporting requirements for payments received for goods and services. These requirements will lower the Form 1099-K reporting threshold over a 3-year period from the previous threshold of more than $20,000 in goods and services transactions and more than 200 goods and services transactions in a calendar year. We’ve summarized the IRS thresholds for Form 1099-K below.

Posted on February 20, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS OF NEW DEADLINE

By Staff Reporters

***

***

The Treasury Department has set a new deadline of March 21st 2025 for millions of businesses to fulfill a new reporting requirement on “beneficial ownership information,” after a court order allowed the federal agency to start enforcing the measure.

The Corporate Transparency Act, which Congress enacted in 2021, requires small businesses to disclose the identity of people who directly or indirectly own or control the company. The measure aims to prevent criminals from hiding illicit activity conducted through shell companies or opaque ownership structures, according to the Treasury.

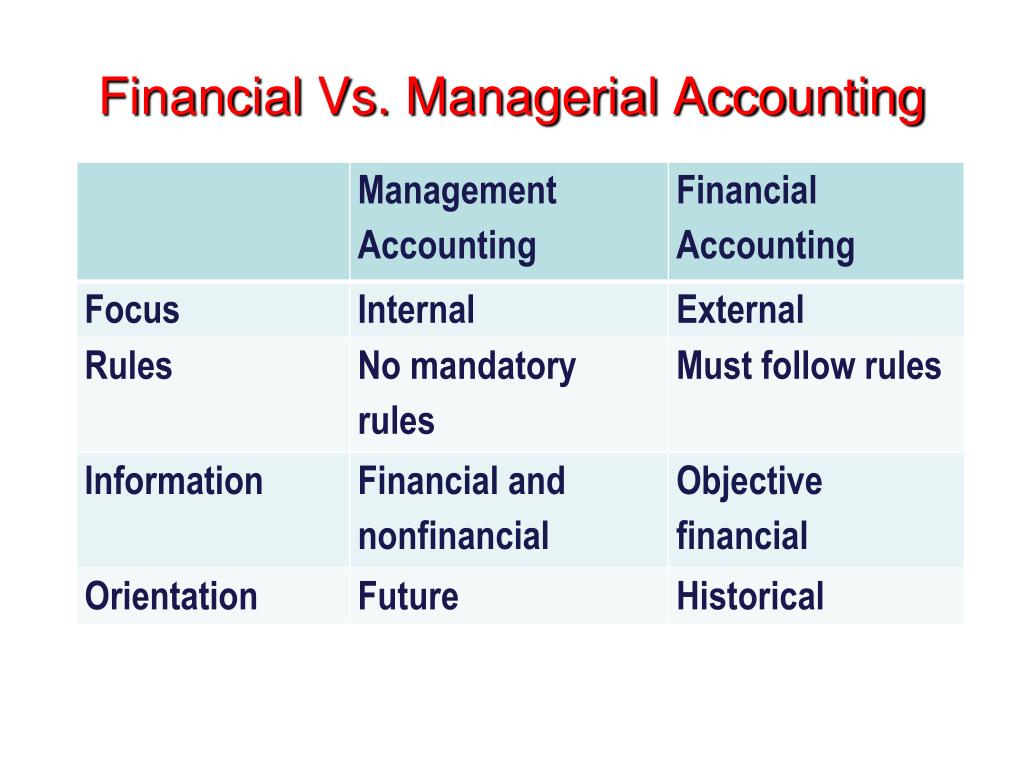

Financial accounting and managerial accounting are two distinct branches of the accounting field, each serving different purposes and stakeholders. Financial accounting focuses on creating external reports that provide a snapshot of a company’s financial health for investors, regulators, and other outside parties. Managerial accounting, meanwhile, is an internal process aimed at aiding managers in making informed business decisions.

Objectives of Financial Accounting

Financial accounting is primarily concerned with the preparation and presentation of financial statements, which include the balance sheet, income statement, and cash flow statement. These documents are meticulously crafted to reflect the company’s financial performance over a specific period, providing insights into its profitability, liquidity, and solvency. The objective is to offer a clear, standardized view of the financial state of the company, ensuring that external entities have a reliable basis for evaluating the company’s economic activities.

The process of financial accounting also involves the meticulous recording of all financial transactions. This is achieved through the double-entry bookkeeping system, where each transaction is recorded in at least two accounts, ensuring that the accounting equation remains balanced. This systematic approach provides accuracy and accountability, which are paramount in financial reporting. CPA = Certified Public Accountant.

Objectives of Managerial Accounting

Managerial accounting is designed to meet the information needs of the individuals who manage organizations. Unlike financial accounting, which provides a historical record of an organization’s financial performance, managerial accounting focuses on future-oriented reports. These reports assist in planning, controlling, and decision-making processes that guide the day-to-day, short-term, and long-term operations.

At the heart of managerial accounting is budgeting. Budgets are detailed plans that quantify the economic resources required for various functions, such as production, sales, and financing. They serve as benchmarks against which actual performance can be measured and evaluated. This enables managers to identify variances, investigate their causes, and implement corrective actions. Another objective of managerial accounting is cost analysis. Managers use cost accounting methods to understand the expenses associated with each aspect of production and operation. By analyzing costs, they can determine the profitability of individual products or services, control expenditures, and optimize resource allocation.

Performance measurement is another key objective. Managerial accountants develop metrics and key performance indicators (KPIs) to assess the efficiency and effectiveness of various business processes. These performance metrics are crucial for setting goals, evaluating outcomes, and aligning individual and departmental objectives with the overall strategy of the organization. CMA = Certified Managerial Accountant

Reporting Standards in Financial Accounting

The bedrock of financial accounting is the adherence to established reporting standards, which ensure consistency, comparability, and transparency in financial statements. Globally, the International Financial Reporting Standards (IFRS) are widely adopted, setting the guidelines for how particular types of transactions and other events should be reported in financial statements. In the United States, the Financial Accounting Standards Board (FASB) issues the Generally Accepted Accounting Principles (GAAP), which serve a similar purpose. These standards are not static; they evolve in response to changing economic realities, stakeholder needs, and advances in business practices.

For instance, the shift towards more service-oriented economies and the rise of intangible assets have led to updates in revenue recognition and asset valuation guidelines. The convergence of IFRS and GAAP is an ongoing process aimed at creating a unified set of global standards that would benefit multinational corporations and investors by reducing the complexity and cost of complying with multiple accounting frameworks.

Generative artificial intelligence (AI) is the utilization of algorithms to create content—such as text, code, imagery, videos, and even simulations—in mere seconds. The goal of AI in general is to mimic the intelligence of humans to perform tasks. “Generative” AI aims to learn from data without the assistance of humans. While today’s generative AI bots are not yet prepared for widespread utilization in patient care settings, AI is garnering significant interest in the healthcare industry as providers begin to test its capabilities in clinics and offices.

This article reviews the role that generative AI is beginning to play in the U.S. healthcare system, the potential of AI in healthcare, and concerns related to the technology.

(“Informed Voice of a New Generation of Fiduciary Advisors for Healthcare”)

For most lay folks, personal financial planning typically involves creating a personal budget, planning for taxes, setting up a savings account and developing a debt management, retirement and insurance recovery plan. Medicare, Social Security and Required Minimal Distribution [RMD] analysis is typical for lay retirement. Of course, we can assist in all of these activities, but lay individuals can also create and establish their own financial plan to reach short and long-term savings and investment goals.

But, as fellow doctors, we understand better than most the more complex financial challenges doctors can face when it comes to their financial planning. Of course, most physicians ultimately make a good income, but it is the saving, asset and risk management tolerance and investing part that many of our colleagues’ struggle with. Far too often physicians receive terrible guidance, have no time to properly manage their own investments and set goals for that day when they no longer wish to practice medicine.

For the average doctor or healthcare professional, the feelings of pride and achievement at finally graduating are typically paired with the heavy burden of hundreds of thousands of dollars in student loan debt.

You dedicated countless hours to learning, studying, and training in your field. You missed birthdays and holidays, time with your families, and sacrificed vacations to provide compassionate and excellent care for your patients. Amidst all of that, there was no time to give your finances even a second thought.

Between undergraduate, medical school, and then internship and residency, most young physicians do not begin saving for retirement until late into their 20s, if not their 30s. You’ve missed an entire decade or more of allowing your money and investments to compound and work for you. When it comes to addressing your financial health and security, there’s no time to waste.

Posted on January 28, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

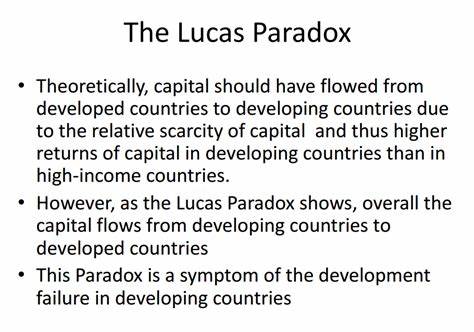

Capital is not flowing from developed countries to developing countries despite the fact that developing countries have lower levels of capital per worker, and therefore higher returns to capital.

Classical economic theory predicts that capital should flow from rich countries to poor countries, due to the effect of diminishing returns of capital. Poor countries have lower levels of capital per worker – which explains, in part, why they are poor. In poor countries, the scarcity of capital relative to labor should mean that the returns related to the infusion of capital are higher than in developed countries.

In response, savers in rich countries should look at poor countries as profitable places in which to invest. In reality, things do not seem to work that way. Surprisingly little capital flows from rich countries to poor countries.

This puzzle, famously discussed in a paper by Robert Lucas in 1990, is often referred to as the “Lucas Paradox”.

MBA is the common abbreviation for a Master of Business Administration degree, and recipients typically stop attending school after receiving it.

However, those who are interested in conducting business research may decide to pursue a doctorate in business or management. Such students can earn a Ph.D. or a Doctor of Business Administration degree, commonly known as a DBA.

What ‘MSHA’ Stands For?

Master of Health Administration (MHA) and Master of Science in Health Administration (MSHA) are largely equivalent designations for degree programs that focus primarily on leadership and management of hospitals, healthcare organizations, and businesses that operate in the healthcare sector.

In contrast, an MBA in Health Administration is a Master of Business Administration degree program with a concentration, track, or specialization that provides students with several courses in topics specific to healthcare management and administration. Most of the coursework in an MBA program is devoted to general training in business functions, such as accounting, finance, logistics, marketing, personnel and project management.

MHA and MHSA programs devote all or most of their curriculum to studying the healthcare system, healthcare policy, and the application of business principles in the field of healthcare. MBA in Healthcare Administration programs devote only a portion of their curricula to topics specific to the healthcare sector.

While IAs and FAs may seem the same, they are not the same. The Financial Industry Regulatory Authority (FINRA) and the Securities Exchange Commission (SEC) have clearly defined investment advisors as distinct from financial advisors.

The term financial advisor is a generic one that can encompass many different financial professionals, although it most commonly refers to stock brokers (individuals or companies that buy and sell securities).

Investment advisor, on the other hand, is a legal term and thus has a more clear-cut definition – or at least as clear as legalese is apt to be.

KEY DIFFERENCES:

Financial advisors help with all aspects of your finances, including saving, budgeting, insurance, retirement planning, and taxes.

Investment advisors focus specifically on choosing and managing investment portfolios.

Financial advisors offer broader financial guidance, while investment advisors concentrate solely on investments.

Investment advisors are held to the fiduciary standard, while financial advisors who work as brokers may operate under different rules.

The CPA and CMA designations cater to distinct professional focuses within the accounting and finance fields. A CPA is often seen as the gold standard for public accounting, emphasizing auditing, tax, and regulatory compliance. This certification is highly regarded for roles that require a deep understanding of financial reporting and external auditing. CPAs are frequently employed by public accounting firms, government agencies, and corporations that need to ensure their financial statements adhere to strict regulatory standards.

On the other hand, the CMA designation is tailored for professionals who aim to excel in management accounting and strategic financial management. CMAs are trained to analyze financial data to inform business decisions, focusing on internal processes and performance management. This makes the CMA particularly valuable for roles in corporate finance, strategic planning, and management consulting. Companies looking to optimize their internal financial operations and drive business strategy often seek out CMAs for their expertise in cost management, budgeting, and financial analysis.

The educational and experiential requirements for these certifications also differ. To become a CPA, candidates typically need to complete 150 semester hours of college education, which often includes a bachelor’s degree in accounting or a related field. Additionally, CPAs must pass the Uniform CPA Examination and meet specific state licensing requirements, which usually include a certain amount of professional experience.

In contrast, the CMA certification requires a bachelor’s degree in any discipline, two years of relevant work experience, and passing the two-part CMA exam. This flexibility in educational background can make the CMA more accessible to a broader range of professionals.

The ICE 3-Month USD LIBOR interest rate is the average interest rate at which a selection of banks in London are prepared to lend to one another in American dollars with a maturity of 3 months.

The Bank of America US High Yield Constrained Index is a market value-weighted index of all domestic high-yield bonds and Yankee high-yield bonds (issued by a foreign entity and denominated in U.S. dollars), including deferred interest bonds and payment-in-kind securities.

The ICE BofA BB-B US High Yield Constrained Index is composed of U.S. dollar-denominated corporate debt publicly issued in the U.S. market rated BB through B, based on an average of Moody’s, S&P and Fitch ratings, with issuer exposure capped at 2%.

ICE BofA U.S. Convertible Index tracks the performance of publicly issued, exchange-listed US dollar denominated convertible securities of US companies with at least $50 million face amount outstanding and at least one month remaining to the final conversion date. Index constituents are market capitalization-weighted and rebalanced monthly.

ICE BofA ML MOVE Index is a widely used measure of bond market volatility, similar to the VIX Index for stocks. The MOVE Index (also known as the Merrill Lynch Option Volatility Estimate) is a yield-curve-weighted index that tracks the market’s expectation of volatility in the U.S. bond market based on 1-month Treasury options.

ICE Exchange-Listed Preferred & Hybrid Securities Index tracks the performance of exchange-listed US dollar denominated hybrid debt, preferred stock and convertible preferred stock publicly issued by corporations in the US domestic market. Preferred stock and notes must have a minimum amount outstanding of $100 million; convertible preferred stock must have at least $50 million face amount outstanding. Index constituents are market capitalization-weighted subject to certain constraints. The index is re-balanced monthly.

HFRX Equity Hedge Index serves as a daily-priced proxy for alternative strategies that maintain positions long and short, primarily in equity and equity derivative securities.

HFRX Fixed Income – Credit Index serves as a daily-priced proxy for alternative strategies that provide exposure to credit strategies. Credit strategies refers to a wide range of sub-strategies and may include corporate, sovereign, distressed, asset-backed, capital structure arbitrage, and other relative value approaches. Strategies may also include and utilize equity securities, credit derivatives, commodities, or currencies.

Academic Team of Internationally Known Contributors

D. E. Marcinko & Associates is one of the most academically published authorities on the topic of financial planning and private wealth management for physicians, nurses and medical professionals. We have published 33 major peer reviewed textbooks redacted in the Library of Medicine, Institute of Health and the Library of Congress, in four languages, with over 5,025 online white papers, web-posts and related publications. These cover a range of financial planning topics from medical malpractice, risk management and insurance, to investment policy statement analysis and endowment funding management, and to taxation, retirement, estate and legacy planning.

Financial planning, business and strategic management, FMV for practice and clinics and related “hard” topics are included.

***

We also include “soft” subjects from investor psychology, ethics and lost fortunes to luxury spending, from understanding the middle-class millionaire to the political philosophies of physicians and the affluent. Our corpus of work is regularly consulted by doctors, medical, business, graduate and nursing schools, to elite advisors, private and investment bankers, wealth managers, venture capitalists, academics and the press.

Posted on January 11, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Credit report with score on a desk

***

Credit analysis is a form of financial analysis used primarily to determine the financial strength of the issuer of a security, and the ability of that issuer to provide timely payment of interest and principal to investors in the issuer’s debt securities. Credit analysis is typically an important component of security analysis and selection in credit-sensitive bond sectors such as the corporate bond market and the municipal bond market.

Credit default swap index (CDX) is a credit derivative, based on a basket of CDS, which can be used to hedge credit risk or speculate on changes in credit quality.

Credit default swaps (CDS) are credit derivative contracts between two counterparties that can be used to hedge credit risk or speculate on changes in the credit quality of a corporation or government entity.

Credit quality reflects the financial strength of the issuer of a security, and the ability of that issuer to provide timely payment of interest and principal to investors in the issuer’s securities. Common measurements of credit quality include the credit ratings provided by credit rating agencies such as Standard & Poor’s and Moody’s. Credit quality and credit quality perceptions are a key component of the daily market pricing of fixed-income securities, along with maturity, inflation expectations and interest rate levels.

Credit Rating Agency (CRA) is a company that assigns credit ratings for issuers of certain types of debt obligations as well as the debt instruments themselves. In the United States, the Securities and Exchange Commission (SEC) permits investment banks and broker-dealers to use credit ratings from “Nationally Recognized Statistical Rating Organizations” (NRSRO) for similar purposes. As of January 2012, nine organizations were designated as NRSROs, including the “Big Three” which are Standard and Poor’s, Moody’s Investor Services and Fitch Ratings.

Credit rating downgrade, by a credit rating agency (Standard & Poor’s, Moody’s or Fitch) means reducing its credit rating for a debt issuer and/or security. This is based on the agency’s evaluation, indicating, to the agency, a decline in the issuer’s financial stability, increasing the possibility of default. A downgrade should not to be confused with a default; a debt security can be downgraded without defaulting. And, conversely, a debt issuer can suddenly default without being downgraded first–credit ratings and credit rating agencies are not infallible.

Credit ratings are measurements of credit quality provided by credit rating agencies. Those provided by Standard & Poor’s typically are the most widely quoted and distributed, and range from AAA (highest quality; perceived as least likely to default) down to D (in default). Securities and issuers rated AAA to BBB are considered/perceived to be “investment-grade”; those below BBB are considered/perceived to be non-investment-grade or more speculative.

Credit risk is the inability or perceived inability of the issuers of debt securities to make interest and principal payments will cause the value of those securities to decrease. Changes in the credit ratings of debt securities could have a similar effect.

Credit Risk Transfer Securities (CRTS) are unsecured obligations of the GSEs (Government Sponsored Enterprises). Although cash flows are linked to prepays and defaults of the reference mortgage loans, the securities are unsecured loans, backed by general credit rather than by specified assets.

Posted on January 3, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

What is a Revenue Agent?

IRS revenue agents are unarmed, civil agency employees that are skilled auditors who typically conduct in-person field audits. These are normally scheduled at the taxpayer’s home, place of business or accountant’s office where the organization’s financial books and records are located.

What is a Revenue Officer?

IRS revenue officers are unarmed civil agency employees whose duties include visiting households and businesses to help taxpayers resolve their account balances. Their job is to collect taxes that are delinquent and have not been paid to the IRS and to secure tax returns that are overdue from taxpayers.

The IRS currently has about 2,300 revenue officers working cases across the country. Revenue officers educate taxpayers on their tax filing and paying obligations and provide guidance and service on a wide range of financial issues to help the taxpayer resolve their tax issues. They also ensure taxpayers are aware of their rights under the law and provide them with quality customer service.

Confirming if it’s the IRS

Revenue officers and revenue agents are unarmed and carry two forms of official credentials with a serial number and their photo. Taxpayers have the right to see each of these credentials and can also request an additional method to verify their identification.

Remember, taxpayers should know they have a tax issue before these visits occur since multiple mailings occur. And, IRS-CI special agents are the only armed IRS personnel and always present their law enforcement credentials when conducting investigations.

Posted on December 29, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The anti-trust paradox suggests that antitrust enforcement artificially raised prices by protecting inefficient competitors from competition.

The Antitrust Paradox Book is an influential 1978 book by Robert Bork that criticized the state of US anti-trust law in the 1970s. A second edition, updated to reflect substantial changes in the law, was published in 1993. Bork has credited Aaron Director as well as other economists from the University of Chicago as influences.

Bork argued that the original intent of antitrust laws as well as economic efficiency makes consumer welfare and the protection of competition, rather than competitors, were the only goals of antitrust law.

Thus, while it was appropriate to prohibit cartels that fix prices and divide markets and mergers that create monopolies, practices that are allegedly exclusionary, such as vertical agreements and price discrimination, did not harm consumers and so should not be prohibited.

The paradox of antitrust enforcement was that legal intervention artificially raised prices by protecting inefficient enterprises from competition.

“Phantom Tax” or “Phantom Income” for direct owners of Treasury inflation-protected securities (TIPS) TIPS adjust their principal values and interest payments for inflation. As with other directly owned Treasury securities, TIPS principal, including the inflation adjustments, is not paid back to investors until the securities mature.

However, the principal adjustments are taxed by the IRS as income in the year in which they occur, even though no actual payments are made in those years to investors who own TIPS directly. This is why this income is called “phantom income” and the tax on it is known as the “phantom tax.”

Investors can avoid the phantom income/tax issue for TIPS by holding TIPS in tax-deferred retirement accounts. Mutual funds and Exchange Traded Funds (ETFs) typically take the “phantom” factor out of TIPS ownership by distributing the principal adjustments as taxable dividends.

As with direct ownership of TIPS, the tax consequences of these distributions by mutual funds and ETFs can be reduced by holding TIPS-owning instruments in tax-deferred retirement accounts

Posted on December 27, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

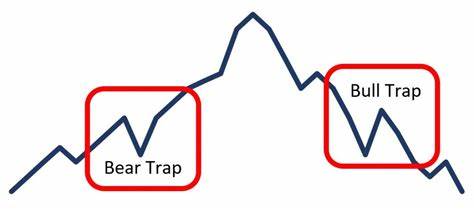

What Is a Bull Trap?

A bull trap, according to James Chen, is a false signal, referring to a declining trend in a stock, index, or other security that reverses after a convincing rally and breaks a prior support level. The move “traps” traders or investors that acted on the buy signal and generates losses on resulting long positions. A bull trap may also refer to a whipsaw pattern. Read: “Bull Trap.”

What is a Bear Trap

The opposite of a bull trap is a bear trap, which occurs when sellers fail to press a decline below a breakdown level.

PCE or the Personal Consumption Expenditures (“PCE”) price deflator—comes from the Bureau of Economic Analysis’ quarterly report on U.S. gross domestic product—and is based on a survey of businesses and is intended to capture the price changes in all final goods, no matter the purchaser.

Because of its broader scope and certain differences in the methodology used to calculate the PCE price index, the Federal Reserve (“the Fed”) holds the PCE deflator as its preferred, consistent measure of inflation over time.

Posted on December 26, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITION

By Staff Reporters

***

***

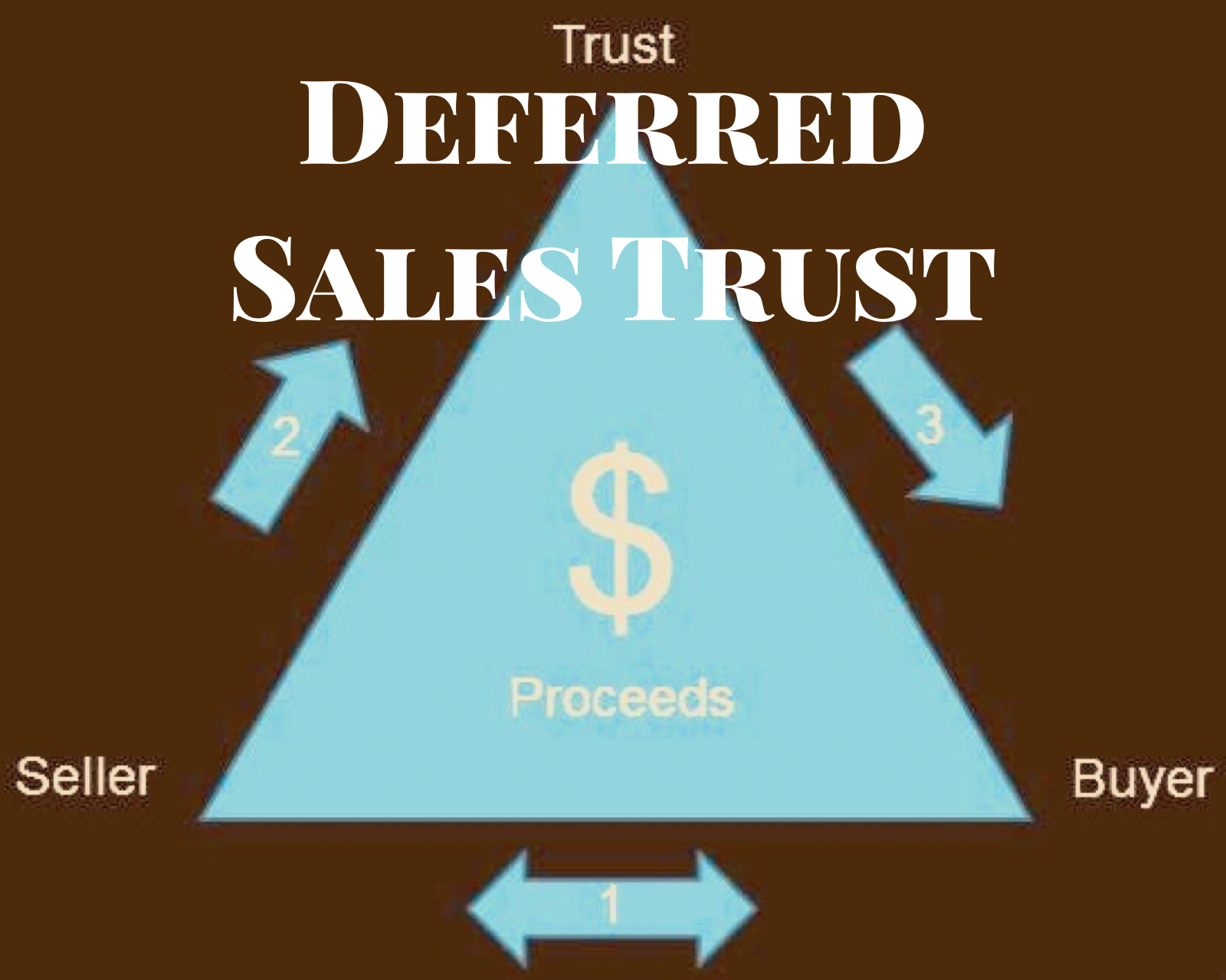

A deferred sales trust (DST) is an advanced tax strategy that allows investors to delay capital gains taxes on the sale of assets that have significantly risen in value, such as real estate or businesses. By selling the asset to a trust, the seller can receive payments over time, spreading out tax liabilities and allowing the profits to grow tax-deferred.

For example, a business owner may sell their company to a DST, avoiding a large tax bill upfront and instead receive income over multiple years. However, DSTs can be complex, and there are often fees involved in setting up and maintaining the trust.

Now, let’s point out some of the pros and cons of Deferred Sales Trusts.

One potential positive feature of using an installment sale to defer your capital gains taxes rather than a 1031 exchange is that installment sales don’t come with the same strict guidelines that govern 1031 exchanges. In particular, in light of the Tax Cuts and Jobs Act of 2017, 1031 exchanges are restricted to real property, whereas Deferred Sales Trusts and other installment sale arrangements can be used to defer capital gains for any kind of asset.

Conversely, the IRS has provided little to no guidance on how to defer taxes using an installment sale.

The basic rationale behind why you don’t receive capital gain is that you are not profiting immediately from the sale made with a Deferred Sales Trust. Given this rationale, there are various constraints on how a Deferred Sales Trust must be organized so that no capital gains taxes are in fact realized.

The third party to whom you transfer your asset generally cannot be a “related person” to you, such as a family member or a corporation in which you hold an interest. Except in special circumstances, if you attempt to set up a Deferred Sales Trust with a related person it will be viewed as a “sham trust” made just for the purposes of avoiding capital gains taxes, and will not be protected by the provisions in Section 453.

As with the 1031 exchange, you, the seller, cannot at any point in the transfer of your asset be in constructive receipt of the proceeds from the third party’s sale of that asset. To successfully defer capital gains taxes, either the third party or the trust of which they are trustee must be the only party which receives cash in the sale of the transferred asset. This includes receipt of a bond which is payable on demand.

This has been a general, informal introduction to Deferred Sales Trusts. As always, before attempting to carry out any important financial decision, investors should consult with a qualified tax or legal advisor regarding the specifics of their situation.

HFRI Fund of Funds Composite Index invests with multiple managers through funds or managed accounts. The strategy designs a diversified portfolio of managers with the objective of significantly lowering the risk (volatility) of investing with an individual manager. The Fund of Funds manager may allocate funds to numerous managers within a single strategy, or with numerous managers in multiple strategies. The investor has the advantage of diversification among managers and styles with significantly less capital than investing with separate managers. The HFRI Fund of Funds Index is not included in the HFRI Fund Weighted Composite Index.

HFRI Fund Weighted Composite Index is a global, equal-weighted index of over 2,000 single-manager funds that report to HFR Database. Constituent funds report monthly net of all fees performance in U.S. Dollar and have a minimum of $50 Million under management or a twelve (12) month track record of active performance. The HFRI Fund Weighted Composite Index does not include Funds of Hedge Funds.

Posted on December 21, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Metzler’s Paradox is the imposition of a tariff [tax] on imports that may reduce the relative internal price of that good.

It was proposed by Lloyd Metzler PhD in 1949 upon examination of tariffs within the Heckscher-Ohlin Model. The paradox has roughly the same status as immiserizing growth and a transfer that makes the recipient worse off.

Posted on December 21, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The winter solstice, also called the hibernal solstice, occurs when either of Earth’s poles reaches its maximum tilt away from the Sun. This happens twice yearly, once in each hemisphere (North and South). For that hemisphere, the winter solstice is the day with the shortest period of daylight and longest night of the year, and when the Sun is at its lowest daily maximum elevation in the sky. Each polar region experiences continuous darkness or twilight around its winter solstice.

Stat: $200 million. That’s how much drug manufacturer Endo Health Solutions paid the federal government for profiting from the opioid crisis and racking up $4 billion in unpaid taxes. (ProPublica)

US stocks bounced back Friday as investors digested key inflation data that showed a deceleration in price increases during the month of November.

The tech-heavy NASDAQ Composite (^IXIC) gained 1%. The Dow Jones Industrial Average (^DJI) added 1.2%, while the S&P 500 (^GSPC) rose 1.1%.

But the rebound wasn’t enough to overcome losses earlier in the week. All three major gauges finished the week lower. The NASDAQ gave up 1.8% while the Dow and the S&P both shed around 2%.

Revenue bonds are one of the biggest sectors in the municipal debt market.

Unlike a general obligation (GO) bond, revenue bonds are not backed by a municipal issuer’s taxing authority. Instead, interest and principal are secured by the net revenues (tolls, fees, or other charges tied to usage) from the project or facility being financed.

Revenue bonds are issued to finance a variety of capital projects, including construction or refurbishment of utility and waste disposal systems, highways, bridges, tunnels, air and seaport facilities, schools and hospitals.

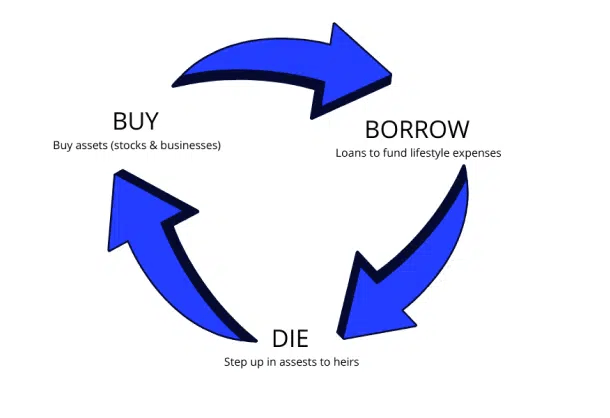

Here’s how the Buy, Borrow, Die strategy works step-by-step:

Step 1. Buy Assets

This step, broadly known as the accumulation phase, is about acquiring or creating valuable assets. It’s the most critical step taken by wealthy individuals to secure their wealth. Billionaires, for instance, often created startups that eventually turned into massive corporations. The asset here is the company they’ve established.

However, this isn’t the only way to accumulate assets. For professionals like doctors and lawyers, this phase involves securing a high-paying job and buying assets that have the potential to appreciate over time—like stocks, real estate, and private capital. Once an individual reaches a substantial level of wealth, they can leverage these assets in interesting ways using the next step of this strategy.

Step 2. Borrow Against Your Assets

This where the assets you’ve acquired are used as collateral to borrow money—all without triggering a taxable event.

Suppose you’ve got a robust stock portfolio. You can then take out a Securities Backed Line of Credit (SBLOC). This kind of loan lets you tap into the value of your portfolio without having to sell off any assets and subsequently paying capital gains taxes. What makes SBLOCs attractive to lenders is the relative ease with which the securities can be seized and sold, making them a low-risk lending option.

The ceiling for such a loan is usually around 50% of your portfolio’s value. However, we often caution against borrowing more than 25% of your account balance, especially for long-term loans. This will provide a cushion against stock market volatility, much like what we experienced in 2022 and 2023.

Borrowing against assets isn’t limited to stock portfolios either. Let’s say you own a home and have built up a certain amount of equity in it. You could opt for a Home Equity Line of Credit (HELOC), using your home as collateral. Banks tend to favor real estate-backed loans due to their stability compared to the fluctuating value of stocks.

Step 3. Die and Pass Your Wealth On

The final step in the strategy is where the proverbial tax baton is handed off to the next generation.

Under the existing tax code, when you pass away, your heirs receive a “stepped-up basis” on the assets they inherit from you. This means that their cost basis—the original amount paid for an asset—is stepped up to the market value of the asset at the time of your death. Meaning once you have passed away, your heirs would be able to sell the assets without having to pay taxes on the capital gain. Imagine you had purchased a building 20 years ago for $1 million and over the years, the value of that building increased to $2.5 million. If you were to pass away at this point, your heirs would inherit the building with the stepped-up cost basis of $2.5 million. This implies that if they decide to sell the property at this valuation, they wouldn’t owe any capital gains tax. This is because for tax purposes, their gain is calculated from the $2.5 million, not the original $1 million.

By utilizing this loophole, families can pass on their wealth without incurring a hefty tax bill. This is why many wealthy families set up trusts – it’s a way to manage and pass on their wealth at a stepped-up cost basis.

Posted on December 13, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

What Is a Public Benefit Corporation?

A benefit corporation—also known as a B Corporation—has shareholders who own the company, unlike a non-profit. So making money is the point, just not the whole point.

While non-profits (or not-for-profits) serve a public benefit and don’t make any profits, benefit corporations want to make money while still serving a greater purpose than itself “and a desire for the corporation to help make the world a better place,” according to Rick Bell of Harvard Business Services.

Posted on December 12, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

ALMOST ALL ABOUT CREDIT

By Staff Reporters

***

***

Credit Rating and Scoring

The category in which a credit agency classifies you is based upon payment history. Recently, credit reporting agencies have shifted away from ratings to a system known as credit scoring. Your score is determined by proprietary formulas that are based on your credit history, the higher the better. The practical benefits of this scoring system are numerous.

First, medical professionals do not need to be experts at deciphering credit reports since the same scoring system is used by many different companies.

Correcting Credit Report Errors

A credit bureau is not the place to get an item to be fixed on your credit report. Rather, you must take it up directly with the credit issuer. In any case, a late payment noted on a credit report by a durable medical equipment vendor, for example, has to be addressed directly with that merchant. The DME merchant then has 30 days to acknowledge your complaint and respond to you. In the meantime, you do not have to pay for the disputed items. Most credit errors cannot be reported or kept on your credit report for more than seven years.

For legitimate late payments you should contact the credit grantor and negotiate to take one of the following steps. Be tenacious, and either remove the late payment or write a letter explaining that the problem has been resolved and you now are a good credit risk again. This letter is a powerful tool and should be saved with other permanent financial records. The industry term for it is a letter of correction.

Credit Repair Services

Credit repair services are oversold and their claims tend to be exaggerated. They do not have an inside track to the consumer reporting agencies. Good credit repair services are experienced in communicating with creditors and can help with legitimate repairs. They cannot restore your credit rating or your good name.

However, realize that with some time and effort you can accomplish the same results yourself.

Achieving your financial, wealth and medical practice management goals is important, but handling everything on your own can be overwhelming. That’s where we come in. At D. E. Marcinko & Associates, our team of dual degree experienced physician advisors and medical consultants is here to guide you every step of the way. We believe in providing unbiased, high-quality financial and business advice.

For example, we offer a one-time written financial plan with oral evaluation for a flat fee with no ongoing sales or assets under management fees or commissions. Together, we can create a personalized financial plan tailored to your unique goals, empowering you to make confident, informed decisions as you navigate your financial future.

Other Services Include:

Estate Planning We have a network of qualified legal professionals that we can refer you to for state specific estate planning needs.

Tax Strategy We can work alongside your CPA for tax planning purposes. If needed, we can refer you to a qualified tax professional.

Investment Analysis If you have investments, we review your accounts to make sure they are aligned with your long-term goals.

401-k Allocations We evaluate your 401(k) allocations and provide recommendations that align with your goals.

Education Savings We help you explore the various ways to plan and save for education expenses.

Insurance & Risk Management We assess your insurance coverage to ensure it adequately protects you against potential risks; as well as evaluate and provide expert litigation witnesses, as needed.

Medical Practice Management We evaluate your current or potential medical practice to determine value and/or private equity offers or physician practice management formats [PPMC] for new, mid-career or retiring physicians, nurses and dentists.

D. E. Marcinko & Associates is unique and fully committed to all phases of a medical professionals personal and business life cycle. We are at your service 24/7: Email MarcinkoAdvisors@outlook.com

Think of synthetic equity as a communal garden. You don’t own the plot, and you don’t necessarily have a say in what’s planted, but you’re guaranteed a share of the crops that are harvested.

Synthetic equity is a form of deferred compensation that mirrors some of the benefits of real stock ownership without granting actual shares. It’s a contractual agreement between you and your employer that entitles you to a payout upon certain events—such as an IPO, acquisition, or surpassing earnings milestones.

Companies use synthetic equity plans to motivate their personnel through growth-related incentives. In other words, it grants employees a sense of ownership without issuing shares or altering the business’s ownership structure. As the company succeeds and appreciates in value, so does your potential payout. Although you don’t own actual shares of company stock, you are compensated as if you did.

According to Carla McCabe, synthetic equity programs also have a significant tax advantage to both business owners and the key employees.

For example, when a key employee receives shares under the firm’s synthetic equity program, the IRS does not recognize that receipt as taxable income to the employee until he or she actually receives the money. This usually occurs when the firm is sold or when the employee retires and is cashed out (assuming the employee’s synthetic shares are vested). This is very attractive considering that regular shares are taxed as ordinary income and the employee basically has to pay the associated tax even though he or she didn’t receive any cash.

Of course, all this begs the question: Why would a company offer synthetic equity instead of actual equity?

Posted on December 5, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Beneficial Ownership Information

By Staff Reporters

***

***

Small business owners face severe penalties if they don’t report to the federal government by year’s end. And, thousands of businesses may not realize they are subject to a new reporting process mandated under the Corporate Transparency Act, which went into effect in January 2024. Even lawyers, doctors, financial advisors and accountants are affected; along with “mom and pop”business owners.

For most eligible businesses, the filing deadline is Jan. 1, 2025, according to the U.S. Chamber of Commerce. “Those who fail to file by this deadline — or fail to update this information if needed — could face up to two years imprisonment and fines up to $10,000, in addition to civil penalties of up to $591 per day,” the U.S. Chamber of Commerce website reads.

The law was created “to combat illicit activity including tax fraud, money laundering and financing for terrorism by capturing more ownership information for specific U.S. businesses operating in or accessing the country’s market,” the chamber website explained.

Posted on December 5, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

2024 LATE YEAR UPDATE

Who sends Form 1099-K?

Payment card companies, payment apps and online marketplaces are required to fill out Form 1099-K and send it to the IRS each year. They must also send a copy to you by January 31st. 2025

1. If you take direct payment by credit or bank card for selling goods or providing services

If your customers or clients pay you directly by credit, debit or gift card, you’ll get a Form 1099-K from your payment processor or payment settlement entity, no matter how many payments you got or how much they were for.

2. If you used a payment app or online marketplace and received a Form 1099-K

A payment app or online marketplace is required to send you a Form 1099-K if the payments you received for goods or services total over $5,000. However, they can send you a Form 1099-K with lower amounts. Whether or not you receive a Form 1099-K, you must still report any income on your tax return.

This includes payments for any:

Goods you sell, including personal items such as clothing or furniture

Services you provide

Property you rent

The payments can be made through any:

Payment app

Online community marketplace

Craft or maker marketplace

Auction site

Car sharing or ride-hailing platform

Ticket exchange or resale site

Crowdfunding platform

Freelance marketplace

If you accept payments on different platforms, you could get more than one Form 1099-K.

Posted on December 1, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

ACCOUNTABLE CARE ORGANIZATIONS

By Health Capital Consultants, LLC

***

On October 29, 2024, CMS announced Performance Year (PY) 2023 results for accountable care organizations (ACOs) participating its Medicare Shared Savings Program (MSSP). Notably, MSSP ACOs garnered the largest net savings in MSSP’s history – more than $2.1 billion.

This Health Capital Topics article discusses MSSP performance in 2023 and how this may inform value-based care going forward. (Read more…)

Posted on November 30, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

In a sign of legislative momentum, 41 senators are supporting efforts to prevent a pending 2.8 percent cut in Medicare physician payments that will go into effect January 1st. The bipartisan letter led by Sens. John Boozman, R-Ark., and Peter Welch, D-Vt., to Senate leaders says the cuts would interfere with the ability of physicians to provide high-quality care. “These continued payment cuts undermine the ability of independent clinical practices – especially in rural and under served areas – to care for their communities,” the letter said.

The Senate letter follows one from the American Medical Association (AMA) and 127 other state medical associations and national medical societies asking Congress to use these last few congressional days to prevent the scheduled cuts. The letter to congressional leaders also urges Congress to provide a positive payment update for 2025. All 50 state medical societies – and DC— as well as 77 national medical societies signed.

Posted on November 25, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

Technological advancements have accelerated the shift of healthcare services from inpatient to outpatient settings, creating both opportunities and challenges for hospitals. For instance, minimally invasive procedures often serve as alternatives to traditional, more invasive surgeries. Additionally, the integration of telehealth and artificial intelligence (AI) has the potential to enhance access to and quality of care while reducing expenditures and administrative burdens.

This final installment of a five-part series on the valuation of hospitals examines the technological advancements transforming the industry. (Read more…)

Prepayment risk is typically used in reference to mortgage-backed securities. It refers to the risk that mortgage refinancing activity might increase when market interest rates decline, which is generally not favorable for MBS investors.

For example, when homeowners refinance their mortgages, MBS investors are “prepaid,” shortening the life of their investments and forcing investors to reinvest the proceeds under lower interest rate conditions than what were most likely prevailing at the time of the original MBS investment.

Price adjustments for prepayment risk are one factor that helps explain why MBS, despite their generally high credit quality, have higher yields than comparable-maturity Treasury securities.

Posted on November 22, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Robert F Kennedy Jr, who was selected by Donald Trump to run the U.S. health and human services department, is working on plans to rid the American Medical Association from its role in drawing up Medicare’s billing codes, which sets doctors’ fees for more than 10,000 procedures, Oliver Barnes of The Financial Times reports.

The plan would result in an upheaval of a system that has been in place for decades. Publicly traded companies in the healthcare space include CVS Health (CVS), Centene (CNC), Cigna (CI), Elevance Health (ELV), Humana (HUM), Molina Healthcare (MOH) and UnitedHealth (UNH).

Yield: For bonds and other fixed-income securities, yield is a rate of return on those securities. There are several types of yields and yield calculations. “Yield to maturity” is a common calculation for fixed-income securities, which takes into account total annual interest payments, the purchase price, the redemption value, and the amount of time remaining until maturity.

Yield curve: A line graph showing the yields of fixed income securities from a single sector (such as Treasuries or municipals), but from a range of different maturities (typically three months to 30 years), at a single point in time (often at month-, quarter- or year-end). Maturities are plotted on the x-axis of the graph, and yields are plotted on the y-axis. The resulting line is a key bond market benchmark and a leading economic indicator.

Yield to maturity [real yield to maturity]: Yield to maturity is a common performance calculation for fixed-income securities, which takes into account total annual interest payments, the purchase price, the redemption value, and the amount of time remaining until maturity. Real yield to maturity is simply yield to maturity minus any “inflation premium” that had been added/priced in. (See Real yield.)

Yield ratio: A ratio of one yield divided by another. Most often used as a relative value measurement.

Yield spread: A “spread,” in fixed income parlance, is simply a difference. Yield spreads measure yield differences, typically between debt securities with high credit ratings (which typically have lower yields) and those with lower ratings (which typically have higher yields). Yield spreads can also be measured between debt securities with different maturities (shorter-maturity securities typically have lower yields and longer-maturity securities typically have higher yields).

Yield trap: An investment that can lure investors with an attractive yield that may not be fundamentally sustainable, or that may lead to undesired price volatility. Yield traps can lurk in both the equity and fixed income markets. They have a tendency to prey on those who can least afford them, including retirement investors looking for increased relative income and stability, who may have been too focused on their income goals and not enough on stability.

Posted on October 28, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Peak earnings season: Five of the Magnificent SevenStocks will be among the 181 companies reporting their earnings this week. Alphabet is in the Mag Seven lead-off spot on Tuesday, Microsoft and Meta step to the plate on Wednesday, and Apple and Amazon rounding out the lineup and this baseball metaphor on Thursday. These companies account for almost 25% of the S&P 500, which is up 40% over the past year and not far off its record closing number from earlier this month. But, the approaching election, it could be a volatile week in the stock markets.

***

Markets: Stocks are currently driving the narrative on Wall Street. Last week, bonds sold off in a big way (driving yields to their highest level since July) in a sign investors are dialing back expectations of more aggressive rate cuts from the Federal Reserve.

Stocks nevertheless handled the bond volatility with aplomb, and with help from Tesla’s 22% one-day rise, the NASDAQ is sitting within 2% of its record high.

Posted on October 23, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The IRS has announced the annual inflation adjustments for the year 2025, including tax rate schedules, tax tables and cost-of-living adjustments. These are the official numbers for the tax year 2025—that tax year begins January 1, 2025. These are not the numbers that you’ll use to prepare your 2024 tax returns in 2025 (you’ll find those official 2024 tax numbers here). These are the numbers that you’ll use to prepare your 2025 tax returns in 2026.

Trump Media & Technology Group rose 9.87% to its highest level since July as the “Trump trade” wagering on the former president to regain the White House picks up steam.

Quest Diagnostics isn’t just a sad, windowless building where you get your blood drawn—it’s also been a pretty profitable investment. Shares rose 6.88% on strong earnings and revenue growth.

STOCKS DOWN

Stop us if you’ve heard this one before: Target is cutting the price of 2,000 products ahead of the holiday season. Shares sank 1.13% as shareholders digest what appears to be a desperate move to boost sales.

Verizon Communications dropped 5.03% after missing on both revenue and earnings estimates. But the real problem was slowing customer growth and phone sales.

Defense contractors were in the earnings spotlight today, and none of them did well. GE Aerospace tumbled 9.07% despite beating analyst forecasts and Lockheed Martin fell 6.12% after sales missed estimates.

Genuine Parts, better known as NAPA Auto Parts, plummeted 20.96% after earnings missed estimates and the company announced lower fiscal year forecasts.

The SPX fell 2.78 points (–0.05%) to 5,851.20; the Dow Jones Industrial Average® ($DJI) lost 6.71 points (–0.02%) to 42,924.89; and the $COMP gained 33.12 points (0.18%) to 18,573.13.

The 10-year Treasury note yield (TNX) added two basis points to 4.2%.

The CBOE Volatility Index® (VIX) fell to 18.15, down from above 20 a week ago.

Although some might view a budget as unnecessarily restrictive, sticking to a spending plan can be a useful tool in enhancing the wealth of a medical practice. So, I will emphasize keys to smart budgeting and how to track spending and savings in these tough economic times.

There is an aphorism that suggests, “Money cannot buy happiness.” Well, this may be true enough but there is also a corollary that states, “Having a little sure reduces the unhappiness.”

Unfortunately, today there is more than a little financial unhappiness in all medical specialties. The challenges range from the commoditization of medicine, aging demographics, Medicare reimbursement cutbacks and increased competition to floundering equity markets, the home mortgage crisis, the squeeze on credit and declines in the value of a practice. Few doctors seem immune to this “perfect storm” of economic woes.

Far too many physicians are hurting and it is not limited to above-average earning professionals. However, one can strive to reduce the pain by following some basic budgeting principles. By adhering to these principles, physicians can eliminate the “too many days at the end of the month” syndrome and instead develop a foundation for building real wealth and security, even in difficult economic climates like we face today.

There are three major budget types. A flexible budget is an expenditure cap that adjusts for changes in the volume of expense items. A fixed budget does not. Advancing to the next level of rigor, a zero-based budget starts with essential expenses and adds items until the money is gone. Regardless of type, budgets can be extremely effective if one uses them at home or the office in order to spot money troubles before they develop.

For the purpose of wealth building, doctors may think of this budget as a quantitative expression of an action plan. It is an integral part of the overall cost-control process for the individual, his or her family unit or one’s medical practice.

Preparing a net income statement (lifestyle cash flow budget) is often difficult because many doctors perceive it as punitive. Most doctors do not live a disciplined spending lifestyle and they view a budget as a compromise to it. However, a cash flow budget is designed to provide comfort when there is surplus income that can be diverted for other future needs. For example, if you treat retirement savings as just another periodic bill, you are more likely to save for it.

You may construct a personal cash budget by recording each cash receipt and cash disbursement on a spreadsheet. Only the date, amount and a brief description of the transaction are necessary. The cash budget is a simple tool that even doctors who lack accounting acumen can use. Since it is possible to track the cash-in and cash-out in the same format used for a standard check register, most doctors find that the process takes very little time. Such a budget will provide a helpful look at how well you are staying within available resources for a given period.

We then continue with an analysis of your operating checkbook and a review of various source documents such as one’s tax return, credit card statements, pay stubs and insurance policies. A typical statement will show all cash transactions that occur within one year. It is helpful to establish a monthly equivalent to all items of income and expense. For the purposes of getting started, note items of income and expense by the frequency you are accustomed to receiving or spending them.

What You Should Know About The ‘Action Plan’ Cash Budget

For a medical office, the first operations budget item might be salary for the doctor and staff. Operating assets and other big ticket items come next. Some of our doctors/clients review their office P&L statements monthly, line by line, in an effort to reduce expenses. Then they add back those discretionary business expenses they have some control over.

Now, do you still run out of money before the end of the month? If so, you had better cut back on entertainment, eating dinner out or that fancy, new but unproven piece of medical equipment. This sounds draconian until you remind yourself that your choice is either: live frugally later or live a simpler lifestyle now and invest the difference.

As a young doctor, it may be a difficult trade-off. By mid-life, however, you are staring retirement in the face. That is why the action plan depends on your actions concerning monetary scarcity, a plan that one can implement and measure using simple benchmarks or budgeting ratios. By using these statistics, perhaps on an annual basis, the doctor can spot problems, correct them and continue planning actively toward stated goals like building long-term wealth.

Useful Calculations To Assess Your Budgeting Success

In the past, generic budgeting ratios would emphasize not spending more than 15 to 20 percent of your net salary on food or 8 percent on medical care. Now these estimates have given way to more rigorous numbers. Personal budget ratios, much like medical practice financial ratios, represent comparable benchmarks for parameters such as debt, income growth and net worth. Although these ratios are still broad, the following represent some useful personal budgeting ratios for physicians.

• Basic liquidity ratio = liquid assets / average monthly expenses. Cash-on-hand should approach 12 to 24 months or more in the case of a doctor employed by a financially insecure HMO or fragile medical group practice. Yes, chances are you have heard of the standard notion of setting enough cash aside to cover three months in a rainy day scenario. However, we have decried this older laymen standard for many years in our textbooks, white papers and speaking engagements as being wholly insufficient for the competitively unstable environment of modern healthcare.

• Debt to assets ratio = total debt / total assets. This percentage is high initially but should decrease with age as the doctor approaches a debt-free existence

• Debt to gross income ratio = annual debt repayments / annual gross income. This represents the adequacy of current income for existing debt repayments. Doctors should try to keep this below 20 to 25 percent.

• Debt service ratio = annual debt repayment / annual take-home pay. Physicians should aim to keep this ratio below 25 to 30 percent or face difficulty paying down debt.

• Investment assets to net worth ratio = investment assets / net worth. This budget ratio should increase over time as retirement approaches.

• Savings to income ratio = savings / annual income. This ratio should also increase over time as one retires major obligations like medical school debt, a practice loan or a home mortgage.

• Real growth ratio = (income this year – income last year) / (income last year – inflation rate). This budget ratio should grow faster than the core rate of inflation.

• Growth of net worth ratio = (net worth this year – net worth last year) / net worth last year – inflation rate). Again, this budgeting ratio should stay ahead of inflation.

In other words, these ratios will help answer the question: “How am I doing?”

Pearls For Sticking To A Budget

Far from the burden that most doctors consider it to be, budgeting in one form or another is probably one of the greatest tools for building wealth. However, it is also one of the greatest weaknesses among physicians who tend to live a certain lifestyle.

In fact, we have found that less than one in 10 medical professionals have a personal budget. Fear, or a lack of knowledge, is a major cause of procrastination. Fortunately, the following guidelines assist in reversing this microeconomic disaster.

1. Set reasonable goals and estimate annual income. Do not keep large amounts of cash at home or office. Deposit it in an FDIC insured money-market account for safety. Do not deposit it in a money market mutual fund with net asset value (NAV) that may “break the buck” and fall below the one-dollar level. Track actual bills and expenses.

2. Do not pay bills early, do not have more taxes withheld from your salary than needed and develop spending estimates to pay fixed expenses first. Fixed expenses are usually contractual and usually include housing, utilities, food, Social Security, medical, debt repayments, homeowner’s or renter’s insurance, auto, life and disability insurance, etc. Reduce fixed expenses when possible. Ultimately, all expenses get paid and become variable in the long run.

3. Make it a priority to reduce variable expenses. Variable expenses are not contractual and may include clothing, education, recreational, travel, vacation, gas, cable TV, entertainment, gifts, furnishings, savings, investments, etc. Trim variable expenses by 5 to 20 percent.

4. Use “carve-outs or “set-asides” for big ticket items and differentiate true wants from frivolous needs.

5. Calculate both income and expenses as a percentage of your total budget. Determine if there is a better way to allocate resources. Review the budget on a monthly basis to notice any variance. Determine if the variance was avoidable, unavoidable or a result of inaccurate assumptions. Take corrective action as needed.

6. Know the difference between saving and investing. Savers tend to be risk adverse while investors understand risk and take steps to mitigate it. Watch mutual fund commissions and investment advisory fees, which cut into return-rates. Keep investments simple and diversified (stocks, bonds, cash, index, no-load mutual and exchange traded funds, etc.).

Sooner or later, despite the best of budgeting intentions, something will go awry. A doctor will be terminated or may be the victim of a reduction-in-force (RIF) because of cost containment initiatives.4 A medical practice partnership may dissolve or a local hospital or surgery center may close, hurting your practice and livelihood. Someone may file a malpractice lawsuit against you, a working spouse may be laid off or you may get divorced. Regardless of the cause, budgeting crisis management encompasses two different perspectives: awareness and execution.

First, if you become aware that you may lose your job, the following proactive steps will be helpful to your budget and overall financial condition.

• Decrease retirement contributions to the required minimum for company/practice match. • Place retirement contribution differences in an after-tax emergency fund. • Eliminate unnecessary payroll deductions and deposit the difference to cash. • Replace group term life insurance with personal term or universal life insurance. • Take your old group term life insurance policy with you if possible. • Establish a home equity line of credit to verify employment. • Borrow against your pension plan only as a last resort.

If you have lost your job or your salary has been depressed, negotiate your departure and get an attorney if you believe you lost your position through breach of contract or discrimination. Then execute the following steps to recalculate your budget and boost your wealth rebuilding activities.

• Prioritize fixed monthly bills in the following order: rent or mortgage; car payments; utility bills; minimum credit card payments; and restructured long-term debt.

• Consider liquidating assets to pay off debts in this order: emergency fund, checking accounts, investment accounts or assets held in your children’s names.

• Review insurance coverage and increase deductibles on homeowner’s and automobile insurance for needed cash.

• Then sell appreciated stocks or mutual funds; personal valuables such as furnishings, jewelry and real estate; and finally, assets not in pension or annuities if necessary.

• Keep or rollover any lump sum pension or savings plan distribution directly to a similar savings plan at your new employer, if possible, when you get rehired.

• Apply for unemployment insurance.

• Review your medical insurance and COBRA coverage after a “qualifying event” such as job loss, firing or even after quitting. It is a bit expensive due to a 2 percent administrative fee surcharge but this may be well worth it for those with preexisting conditions or who are otherwise difficult to insure. One may continue COBRA for up to 18 months.