BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

A hostile takeover happens when an entity takes control of a company without the knowledge and against the wishes of the company’s management. A hostile takeover is an acquisition strategy requiring that the entity acquire and control more than 50% of the voting shares issued by the company.

In mergers and acquisitions (M&A), a hostile takeover is the acquisition of a target company by an acquiring company that goes directly to the target company’s shareholders, either by making a tender offer or through a proxy vote.

Ideally, an entity interested in acquiring a company should seek approval from the target company’s Board of Directors. The difference between a hostile and a friendly takeover is that, in a friendly takeover, the target company’s board of directors approve of the transaction and recommend shareholders vote in favor of the deal.

Defenses against a hostile takeover

These defense mechanisms can be preemptive or reactive, depending on how prepared the company is for the possibility of a hostile bid.

Poison pill is one of the most common defenses against a hostile takeover. Officially known as a “shareholder rights plan,” the poison pill allows existing shareholders to purchase additional shares at a discount, diluting the ownership interest of the acquiring company. The goal is to make it prohibitively expensive for the acquirer to complete the takeover.

A golden parachute is another defense strategy, which involves providing lucrative compensation packages (bonuses, severance pay, stock options, etc.) to key executives in the event they are terminated as a result of the takeover. This creates a financial disincentive for the acquiring company, as it would need to pay out these large sums upon completing the takeover.

In a Crown jewel defense, the target company sells or threatens to sell its most valuable assets—its “crown jewels”—if the takeover is completed. This reduces the attractiveness of the company to the acquirer, as the most desirable assets would no longer be part of the deal.

The Pac-Man defenses a more aggressive strategy in which the target company turns the tables by attempting to buy shares of the acquiring company, effectively launching a counter-takeover. While rare, this defense can deter hostile bids by making the takeover battle more costly and complex.

A White-Knight defense involves the target company seeking out a more favorable acquirer, or “white knight,” to make a friendly takeover bid. This allows the target company to avoid the hostile acquirer while still securing the benefits of a merger or acquisition.

The hostile takeover between Sanofi-Aventis and Genzyme Corp. occurred in 2010 when Sanofi, a French pharmaceutical company, wanted to buy Genzyme, a US biotech firm specializing in rare diseases. Genzyme resisted the offer, leading to conflict. Sanofi started a public campaign to pressure Genzyme’s shareholders into selling.

After months of negotiations, the two companies reached a deal in 2011. Sanofi agreed to pay $74 per share, with additional payments tied to Genzyme’s future performance, bringing the total deal value to around $20.1 billion. This acquisition allowed Sanofi to expand into the lucrative market for rare disease treatment.

The genetic testing company 23andMe went from biotech superstar to the brink of collapse. And, its most valuable asset might be its controversial customer DNA data trove.

Now, 23andMe filed for bankruptcy late Sunday night and announced the resignation of its chief executive officer Anne Wojcicki who is stepping down from her position but remains on the board of directors.

Wojcicki has so far tried unsuccessfully to rescue the business by buying it back and capping a precipitous fall for the DNA-testing company.

Posted on March 24, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Futures attached to the benchmark S&P 500 (ES=F) rose 0.6%, with NASDAQ 100 (NQ=F) futures up 0.7%. Futures tied to the Dow Jones Industrial Average (YM=F) advanced around 0.4%.

Absolute Return – the goal is to have a positive return, regardless of market direction. An absolute return strategy is not managed relative to a market index.

Accredited Investor – wealthy individual or well-capitalized institutions covered under Regulation D of the Securities Act of 1933.

Alpha – the return to a portfolio over and above that of an appropriate benchmark portfolio (the manager’s “value added”).

Arbitrage – any strategy that invests long in an asset, and short in a related asset, hoping the prices will converge.

Attribution – the process of “attributing” returns to their sources. For example, did the returns to a portfolio (over and above some benchmark) come from stock selection, industry/sector over- or under-weighting or factor weighting. Software programs are helpful in reporting an attribution.

Beta – a measure of systematic (i.e., non-diversifiable) risk. The goal is to quantify how much systematic risk is being taken by the fund manager vis-à-vis different risk factors, so that one can estimate the alpha or value-added on a risk-adjusted basis.

Correlation – a measure of how strategy returns move with one another, in a range of –1 to +1. A correlation of –1 implies that the strategies move in opposite directions. In constructing a portfolio of hedge funds, one usually wants to combine a number of non-correlated strategies (with decent expected returns) to be well diversified.

Drawdown – the percentage loss from a fund’s highest value to its lowest, over a particular time frame. A fund’s “maximum drawdown” is often looked at as a measure of potential risk.

Hurdle Rate – the return where the manager begins to earn incentive fees. If the hurdle rate is 5% and the fund earns 15% for the year, then incentive fees are applied to the 10% difference.

Leverage – one uses leverage if he borrows money to increase his position in a security. If one uses leverage and makes good investment decisions, leverage can magnify the gain. However, it can also magnify a loss.

Opportunistic – a general term that describes an aggressive strategy with a goal of making money (as opposed to holding on to the money one already has).

***

***

Pairs Trading – usually refers to a long/short strategy where one stock is bought long, and a similar stock is sold short, often within the same industry. Buying the stock of Home Depot and shorting Lowe’s in an equal amount would be an example.

Portfolio Simulation – involves testing an investment strategy by “simulating” it with a database and analytic software. Often referred to as “backtesting” a strategy. The simulated returns of the strategy are compared to those of a benchmark over a specific time frame to see if it can beat that benchmark.

Sharpe Ratio – a measure of risk-adjusted return, computed by dividing a fund’s return over the risk-free rate by the standard deviation of returns. The idea is to understand how much risk was undertaken to generate the alpha.

Short Rebate – if you borrow stock and then sell it short, you have cash in your account. The short rebate is the interest earned on that cash.

R-Squared – a measure of how closely a portfolio’s performance varies with the performance of a benchmark, and thus a measure of what portion of its performance can be explained by the performance of the overall market or index. Hedge fund investors want to know how much performance can be explained by market exposure versus manager skill.

Transportable Alpha – the alpha of one active strategy can be combined with another asset class. For example, an equity market-neutral strategy’s value-added can be “transported” to a fixed income asset class by simply buying a fixed income futures contract. The total return comes from both sources.

Value at Risk – a technique which uses the statistical analysis of historical market trends and volatilities to estimate the likelihood that a specific portfolio’s losses will exceed a certain amount.

Posted on March 22, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The S&P 500 edged up 0.1%. The index finished with a 0.5% gain for the week. It’s still down 4.8% so far this month. The Dow Jones Industrial Average eked out a 0.1% gain, while the NASDAQ composite rose 0.5%.

It appears Medicare coverage for tele-health is here to stay—at least for the next six months. When the House of Representatives and Senate passed a budget on March 11t and 14th, respectively, they not only avoided a government shutdown, but also extended a resolution for Medicare to cover non-behavioral health tele-health appointments until September 30th.

Visualize: How private equity tangled banks in a web of debt, from the Financial Times.

Posted on March 21, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

U.S. stock indexes edged lower Thursday following another reminder that big, unsettling policy changes are underway because of President Donald Trump, along with more signals suggesting the U.S. economy remains solid for now.

The S&P 500 slipped 0.2% after flipping between modest gains and losses through the day. The Dow Jones Industrial Average dipped by 11 points, or less than 0.1 %, and the NASDAQ composite fell 0.3%.

Posted on March 20, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Stat: $1.2 billion. That’s how much San Diego-based Scripps Health plans to spend building a new hospital in San Marcos, California. (Becker’s Hospital Review)

Read: What WHO Director-General Tedros Adhanom Ghebreyesus said about USAID cuts. (Stat)

Pharm fresh: Check out in-depth strategies designed to help increase engagement between pharma reps and primary care clinicians. It’s all right here in Pri-Med’s research. Read the report.

Shares of Charles Schwab Corp. SCHW+1.51% rallied 1.51% to $78.73 Wednesday, on what proved to be an all-around favorable trading session for the stock market, with the S&P 500 IndexSPX+1.08% rising 1.08% to 5,675.29 and the Dow Jones Industrial AverageDJIA+0.92% rising 0.92% to 41,964.63.

Posted on March 19, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS!

***

***

The Federal Reserve just opted to hold interest rates steady as officials reckon with fearful markets and concerns of an economic slowdown sparked by the trade wars launched by President Donald Trump and his efforts to overhaul and dismantle government agencies.

After a two-day meeting of its monetary policy committee in Washington, D.C., the Fed announced it would hold its rate target at a range of 4.25% to 4.50%. Investors anticipated the move. The Fed’s target rate remains a full percentage point lower than it was when the Fed pivoted to cutting rates last September.

Posted on March 19, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

Rocking Financial Planning … Old School Advice!

By Dr. David E. Marcinko MBBS MBA MEd CMP®

The economic platitude of the past, such as don’t spend more than 15-20 percent of your net salary on food, or 5-10 percent on medical care, among others, have given rise to the more individualized personal financial ratio concept. Personal ratios, like business ratios, represent benchmarks to compare such parameters as debt, income growth and net worth.

According to Edward McCarthy MIB CFP® – a personal financial expert from Warwick, Rhode Island whom I interviewed about a decade ago – the following represented useful ratios for the lay as well as medical professional [personal communication].

The Ratios:

Basic Liquidity Ratio = liquid assets / average monthly expenses. Should be 4-6 months, or even longer, in the case of a medical professional employed by a financially insecure HMO. In a low interest rate environment, iMBA Inc offers 12-24 months for consideration.

Debt to Assets Ratio = total debt / total assets. A percentage which is high initially, and should decrease with age as the medical professional approaches a debt free existence

Debt to Gross Income Ratio = annual debt repayments / annual gross income. A percentage representing the adequacy of current income for existing debt repayments. Medial professionals should try to keep this below 25-30%.

Debt Service Ratio = annual debt re-payment / annual take-home pay. Medical professionals should try to keep this ratio below about 40%, or have difficulty paying down debt.

Investment Assets to Net Worth-Ratio = investment assets / net worth. This ratio should increase over time, as retirement for the medical professional approaches.

Savings to Income Ratio = savings / annual income. This ratio should also increase over time, especially as major obligations are retired.

Real Growth Ratio = (income this year – income last year) / (income last year – inflation rate). It is desirable for the medical professional to keep this ratio growing faster than the core rate f inflation.

Growth of Net-Worth Ratio = (net worth this year – net worth last year) / net worth last year – inflation rate. Again, this ratio should stay ahead of inflation.By calculating these ratios, perhaps on an annual basis, the medical professional can spot problems, correct them, and continue progressing toward stated financial goals.

Assessment

Now, after ten years, are these traditional ratios and advice still valid today: why or why not?

***

***

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

9. We act with honesty, integrity and are always straightforward. 8. We strive to be innovative, creative, iconoclastic, and flexible. 7. We admit and learn from mistakes and don’t repeat them. 6. We work hard always as competitors are trying to catch up. 5. We treat others with dignity and respect. 4. We are the onus of consulting advice for the well being of others. 3. We fight complacency as former success is in the past. 2. The best management styles are timeless, not timely. 1. Our clients are colleagues and always come first.

SPEAKING: Dr. David Edward Marcinko MBA MEd will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements.

***

***

CONTACT: Ann Miller RN MHA at: MarcinkoAdvisors@outlook.com

Posted on March 19, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

US stocks pulled back on Tuesday, led by a nearly 2% decline in the NASDAQ, following two days of gains as investors concerned about an economic slowdown looked to the Federal Reserve’s policy meeting for insights.

The tech-heavy NASDAQ Composite (^IXIC) plummeted about 1.7% as Nvidia (NVDA) shares fell roughly 3% as its annual GTC event failed to impress investors. Other “Magnificent Seven” names also dragged down the tech-heavy index. Notably, those stocks are having their worst quarter in more than two years.

The Dow Jones Industrial Average (^DJI) and S&P 500 (^GSPC) also moved to the downside on Tuesday, dropping about 0.6% and 1.1%, respectively.

“Malta has quietly leveraged the rising tide of the financial transparency imperative to attract hedge funds.“

There was a time when the quaint island sought to play on the traditional terrain, offering anonymity and a “laissez-faire regulatory regime,” not to mention very low taxes, as in no capital gains taxes and no taxes on dividends; all while English speaking and USD currency denominated.

***

***

While many leading domiciles for offshore hedge funds remain in the Caribbean – notably the Cayman Islands, the British Virgin Islands, Bermuda, and the Bahamas – the island of Malta is drawing attention, especially from European funds.

SO – HOW MUCH IS A “FINANCIAL ADVISOR” REALLY WORTH?

This blog holds a rather uncomplimentary opinion of financial advisors, and the financial services and brokerage industry as a whole; deserved, or not? The entire site hints at this attitude as well, in favor of a going it alone or ME, Inc investing when possible. Nevertheless, it is reasonable to wonder how much boost in net-returns might an educated and informed, fee transparent and honest, fiduciary focused “financial advisor” add to a clients’ investment portfolio; all things being equal [ceteris paribus].

And, can it be quantified?

Well, according to Vanguard Brokerage Services®, perhaps as much as 3%? In a decade long paper from the Valley Forge, PA based mutual fund and ETF giant, Vanguard said financial advisors can generate returns through a framework focused on five wealth management principles:

• Being an effective behavioral coach: Helping clients maintain a long-term perspective and a disciplined approach is arguably one of the most important elements of financial advice. (Potential value added: up to 1.50%).

• Applying an asset location strategy: The allocation of assets between taxable and tax-advantaged accounts is one tool an advisor can employ that can add value each year. (Potential value added: from 0% to 0.75%).

• Employing cost-effective investments: This component of every advisor’s tool kit is based on simple math: Gross return less costs equals net return. (Potential value added: up to 0.45%).

• Maintaining the proper allocation through rebalancing: Over time, as investments produce various returns, a portfolio will likely drift from its target allocation. An advisor can add value by ensuring the portfolio’s risk/return characteristics stay consistent with a client’s preferences. (Potential value added: up to 0.35%).

• Implementing a spending strategy: As the retiree population grows, an advisor can help clients make important decisions about how to spend from their portfolios. (Potential value added: up to 0.70%).

Source: Financial Advisor Magazine, page 20, April 2014.

Assessment

However, Vanguard notes that while it’s possible all of these principles could add up to 3% in net returns for clients, it’s more likely to be an intermittent number than an annual one because some of the best opportunities to add value happen during extreme market lows and highs when angst or giddiness [fear and greed] can cause investors to bail on their well-thought-out investment plans.

And, is the study applicable to doctors and allied healthcare providers? Doe Vanguard have a vested interest in the topic. What about fee based versus fee-only financial advice?

Conclusion

Finally, recognize the plethora of other financial planning life-cycle topics addressed in this ME-P were not included in the Vanguard investment portfolio-only study a decade ago.

And what about today with contemporaneous internet advising, chat-rooms, linkedin, robo-advisors, reddit and the like?

Posted on March 18, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

A group of current and former employees of JPMorgan Chase (NYSE:JPM) has filed a lawsuit alleging that the company, through its prescription drug plan run by CVS Health (NYSE:CVS), overpaid for medicines, resulting in higher expenses for its workers, according to Bloomberg News.

The S&P 500 (^GSPC) gained about 0.6% to rebound for a second day in row, while the Dow Jones Industrial Average (^DJI) gained more than 350 points, or more than 0.8%. The tech-heavy NASDAQ Composite (^IXIC) rose 0.3% as “Magnificent 7” stocks, including Nvidia (NVDA) and Tesla (TSLA), faltered.

When analyzing a set of financial statements to determine practice value, adjustments (normalizations) generally are needed to produce a clearer picture of likely future income and distributable cash flow. It also allows more of an “apples to apples” line item comparison. This normalization process usually consists of making three main adjustments to a medical practice’s net income (profit and loss) statement.

1. Non-Recurring Items: Estimates of future distributable cash flow should exclude non-recurring items. Proceeds from the settlement of litigation, one-time gains/losses from the selling of assets or equipment, and large write-offs that are not expected to reoccur, each represent potential nonrecurring items. The impact of nonrecurring events should be removed from the practice’s financial statements to produce a clearer picture of likely future income and cash flow.

2. Perquisites: The buyer of a medical practice may plan to spend more or less than the current doctor-owner for physician executive compensation, travel and entertainment expenses, and other perquisites of current management. When determining future distributable cash flow, income adjustments to the current level of expenditures should be made for these items.

3. Non-cash Expenses: Depreciation expense, amortization expense, and bad debt expense are all non-cash items which impact reported profitability. When determining distributable cash flow, you must analyze the link between non-cash expenses and expected cash expenditures.

The annual depreciation expense is a proxy for likely capital expenditures over time. When capital expenditures and depreciation are not similar over time, an adjustment to expected cash flow is necessary. Some practices reduce income through the use of bad debt expense rather than direct write-offs. Bad debt expense is a non-cash expense that represents an estimate of the dollar volume of write-offs that are likely to occur during a year. If bad debt expense is understated, practice profitability will be overstated.

***

***

Balance Sheet Adjustments

Adjustments also can be made to a practice’s balance sheet to remove non-operating assets and liabilities, and to restate asset and liability value at market rates (rather than cost rates). Assets and liabilities that are unrelated to the core practice being valued should be added to or subtracted from the value, depending on whether they are acquired by the buyer.

Examples include the asset value less outstanding debt of a vacant parcel of land, and marketable securities that are not needed to operate the practice. Other non-operating assets, such as the cash surrender value of officer life insurance, generally are liquidated by the seller and are not part of the business transaction.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com

Posted on March 17, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

The Power of Attorney Mistake That Could Cost You Everything

By Rick Kahler CFP®

***

***

Recently, reading a training manual on elder abuse, I was reminded of a financial risk that is often overlooked. One of the fastest and easiest ways to unravel your financial security is to have the wrong person gain control of your money.

The example in the manual mirrored a heartbreaking situation I once experienced with a long-term client. As her mental and physical health declined, this single woman moved into assisted living. Her newly designated power of attorney, a relative from out of town, took control of her financial affairs.

Almost immediately, without consulting us, the relative began making large withdrawals, closed her accounts, and transferred funds elsewhere. They challenged the financial plan, investments, and strategies we had established to safeguard the client’s financial security and provide for her long-term care. Even though their actions threatened the client’s wellbeing, we were powerless to stop them. Our only recourse was to report the behavior to the authorities.

This heartbreaking and frustrating experience underscored just how critical it is to be mindful when executing a Power of Attorney. Besides designating someone you trust, it is wise to build in safeguards to prevent even a well-meaning relative from inadvertently derailing a carefully constructed financial plan.

***

***

One such safeguard is to include a financial advisor in your POA—as long as that person is a fee-only, fiduciary advisor with an obligation to act in your best interests. In many cases, advisors are hesitant to suggest this option because they are sensitive to the potential conflict of interest and do not want to appear self-serving. An unfortunate reality is that you should be cautious if an advisor, particularly one who sells products on commission, seems eager to be added to your POA.

Including your financial advisor in your POA does not mean you designate them as your agent to manage your affairs. Instead, you include a clause naming them as the professional of record you want your designated agent to continue working with. This creates continuity and accountability. It prevents your agent from replacing your advisor with someone who may be unfamiliar with your needs and goals, unqualified, or untrustworthy.

Your advisor might also recommend adding a secondary safeguard, such as naming an attorney or accountant to oversee the selection of a successor advisor in case your current advisor is unable to continue. This additional layer of protection ensures that the financial professionals guiding your portfolio remain aligned with your best interests. Taking these extra steps can save you—and your loved ones—from significant financial stress down the road.

Including safeguards in your POA is not about mistrusting your loved ones, but about equipping them with the right resources and support to act in your best interest. Financial management is complex, and it requires expertise that most people, even those with the best intentions, may not possess.

One of the hardest parts about planning for diminished financial capacity is the emotional aspect. No one likes to imagine a time when they might not be able to manage their own money. But in reality, taking steps now to protect your financial future is the ultimate act of control. It can help ensure that your wishes are respected and the financial foundation you’ve worked so hard to build remains intact.

Remember, too, that avoiding conversations often increases financial vulnerability. If you don’t have a POA or aren’t comfortable with what you do have, now is the time to bring it up with your advisor, attorney, or a trusted family member. These safeguards are about protecting yourself. They also support those you will rely on to care for you and your financial legacy,

Posted on March 16, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Vitaliy Katsenelson CFA

***

***

Today, I’m going to share stories about my best and worst investment decisions. But don’t worry, this isn’t just a brag-and-cringe session about making or losing money. These stories are about the valuable lessons learned, and how these adventures in investing helped shape my current approach.

The Best Investment Decision

In investing, you don’t get extra points for creativity or difficulty. A million dollars earned while you are smiling buys as many potatoes as a million dollars that cost you your marriage and hair.

However, from a personal, creative satisfaction perspective, our investment in Uber was one of our best. That’s not to say that it has been the most successful decision from a financial perspective, at least not yet.

Uber doesn’t fit into the traditional value stock category. Until 2023, the third year of our ownership, it never made money. It was a stock everyone hated. After we bought it, I had clients reach out to me asking if I had been kidnapped and someone else was making these purchases of Uber.

We bought more shares very opportunistically during and after the pandemic. I wrote a long research report on it, which you can read here.

On one hand, Uber’s switchboard is a digital business, but the company also has a physical presence in thousands of cities, which incurs costs (the analog side of the business). Additionally, the availability of cheap money caused the ride-share market to go crazy and act rationally irrational, as competitors jostled in a land grab.

My thesis consisted of several insights:

Unlike traditional-tech, digital-only companies, Uber is a hybrid, both digital and analog. Thus, its cost structure is much higher than that of other companies. This, in part, explains the higher losses.

It has a strong brand; its name has become a verb.

The rideshare market is inevitable and will only continue to grow. Uber is not just in competition with taxis, second cars, or seldomly used cars; it is also in competition with the favors we ask of friends and relatives, such as dropping us off at the mechanic or picking us up from the doctor’s office.

Uber has global scale, which its competitors lack, allowing it to spread R&D across more markets.

As its revenue grows, each incremental dollar comes with a very high margin, which directly drops to the bottom line. Therefore, at some point, its earnings will explode to the upside as fixed costs stop growing, allowing it to scale.

The Uber story is not over; we still own the stock. I don’t want to do a celebratory dance. But this idea came with a lot of creative satisfaction. There is another point of pride here. Despite our very tumultuous ownership of this stock, we remained rational (I have written about that here). We bought more when it became extremely undervalued, and I would be lying if I said that was psychologically easy – it was not, but we followed our research and process.

The Worst Investment Decision

My worst investments that resulted in losses had several things in common: They were low-quality companies; their financials were complex and not transparent (for instance, one-time items were labeled as “one-time” every quarter); and they had questionable management.

However, they were all considered “cheap”… until they were not. Now, I hope you see why I am dogmatic about quality.

However.

When you are wrong on an investment and you lose money, the most you can lose is 100%. I have learned a lot from those. But they were not my worst investments. Those were the ones where I left 300–400% on the table when I sold too soon. Let me detail two examples.

EA – Electronic Arts

We bought EA in the early 2010s. I wrote about it – you can read my investment case for it here. To sum up, games were moving from being sold in stores to being digital downloads, which would lead to higher margins (don’t have to pay for packaging and Best Buy to sell them). The market for games was exploding, as every adult and teenager had a gaming device in their hands – a smartphone. The market for video games was going to be much larger. EA was the largest player in that space, with great franchises.

The following two years of ownership were very painful. EA had a few big game flops, and the market did not care about improving fundamentals. The stock kept declining. We continued to buy more. Every time we bought more shares, the stock fell further. Fast-forward a year or two. The stock doubled from our original purchase, but I was mentally exhausted. I did a celebratory dance and sold the stock. The stock then went up another 4x within a few years after we sold it. It went up for the right reasons – its earnings exploded to the upside, in line with my original thesis.

The sale was a mistake, not because the price went up but because I let frustration over the stock-price decline (volatility) get to me. Investing is a mental game. I learned from this adventure that it is important to zoom out and not obsess over individual stocks in the portfolio. This is why we have a portfolio. It was a very costly but educational mistake. Our ownership of Uber was not a walk in the park, either – just look at the stock price over the last few years. But I had learned my lesson from EA and was able to do the analysis, update our model, and zoom out.

In investing, there is a big difference between intellectual and tactile knowledge. I am going to go PG-13 on you for a second and quote the irascible Charlie Munger: “Learning about investing through a model portfolio is like learning about sex through romantic novels.” A big part of investing is observing yourself as an investor – your thoughts and emotions as you ride the actual rollercoaster of owning a stock.

I also made an important modification to our process.

We always value every company in the portfolio on earnings (free cash flows) at least four years out. Why four years? Three seems too short. There is no magic in this number, other than it being longer than most analyst estimates. We do this for all stocks in the portfolio, and then the total return for each is calculated and annualized. If a company has strong growth potential, it may appear to be expensive based on current earnings; but in reality, it may actually be cheap based on earnings projected four years from now.

On the other side of the spectrum, a company that has no growth or dividends may seem “cheap” based on its current earnings multiple, but this cheapness may quickly dissipate once a total return is calculated using future earnings. Time is on the side of growing businesses and the enemy of the ones that stand still. Therefore, a non-growing or slow-growing business needs a much greater discount (margin of safety) to secure a spot in our portfolio.

I want to stress another point. We sometimes sell a stock and then it goes higher. If we sold it for the right fundamental reasons, this doesn’t bother me. There is very little to learn.

Twilio

I’ll give you another crazy example. We bought Twilio at $25 in 2017 or so. Our thesis was that they had built the largest digital telecommunications network, which gave them a brief competitive advantage. They were also spending 5x more on R&D than competitors to build applications around this network, which would give them long-term advantages.

The stock price went up to $60 in a few months without anything significantly changing, so we sold a third of our position. Then it went up to $90, and we sold some more. To our disbelief, we sold the rest at around $120, a bit before the pandemic.

During the pandemic, Twilio’s price hit $400. I had zero regret about not holding on to the shares. Absolutely none. Twilio’s profitability did not match the stock market’s opinion of its price. Twilio’s stock price was as crazy to me at $250 as it was at $300 or $400. After reviewing our models, we concluded that even $120 was at the extreme end of our optimistic assumptions. Fast-forward to today, where the stock is at $60 or so. We are currently sharpening our pencils, but we have not bought the stock – yet.

Selling EA was a mistake; selling Twilio was not.

***

Key takeaways

My “best investment decision” with Uber wasn’t just about financial gains, but the creative satisfaction it brought. It taught me the value of sticking to our research and process, even when it’s psychologically challenging.

The worst investments often share common traits: low-quality companies, complex financials, questionable management, and the illusion of being “cheap.” This reinforces my dogmatic stance on prioritizing quality.

Sometimes, the costliest mistakes aren’t the ones where you lose money, but those where you leave significant gains on the table by selling too soon. My experience with EA taught me this lesson the hard way.

There’s a crucial difference between intellectual and tactile knowledge in investing. Actually owning stocks and experiencing the emotional roller coaster is invaluable for developing as an investor.

Selling a stock that later increases in value isn’t always a mistake if the decision was based on sound fundamental reasons. My experience with Twilio illustrates this point – sometimes it’s right to sell even if the price continues to climb.

NOTE:Please read the following important disclosure here.

Posted on March 15, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITION

By Staff Reporters and FTC

***

***

Surveillance pricing is a broad term to describe the practice of linking pricing to individualized consumer data.

Companies employing it might use algorithms, personal information, and AI to set a price for their goods based on everything from where you live to your age to your browsing or credit history. The practice, sometimes called dynamic pricing or personalized pricing, is growing increasingly common, but isn’t completely new.

In 2012, the travel website Orbitz began directing people on Macs to higher hotels after realizing they often had more purchasing power. It stopped the practice after the Wall Street Journalreported on it.

Is surveillance pricing the same thing as surge pricing?Yes and no.

You might know about surge pricing from the last time you tried to call an Uber during a rainstorm. As demand skyrockets for a ride share, so does the price. This is one kind of surveillance pricing, but what the FTC is targeting appears more specific. The FTC said its probe concerns “when the pricing is based on surveillance of an individual’s personal characteristics and behavior.”

Is surveillance pricing bad?

The FTC opened its probe into companies using surveillance pricing because it’s worried about the risks it might pose to consumers

“Firms that harvest Americans’ personal data can put people’s privacy at risk. Now firms could be exploiting this vast trove of personal information to charge people higher prices,” FTC Chair Lina M. Khan said in a statement. “Americans deserve to know whether businesses are using detailed consumer data to deploy surveillance pricing, and the FTC’s inquiry will shed light on this shadowy ecosystem of pricing middlemen.”

The FTC is looking into four major areas of the practice: types of products being offered, data collection, customer and sales information, and impacts on consumers and prices.

Many Americans, it fears, don’t know when their data is being harvested and how it is affecting what they pay. “Consumers may now be subjected to surveillance pricing when they shop for anything, big or small, online or in person: a house, a car, even their weekly groceries,” the FTC said.

The FTC sent the orders for more information to Accenture, Bloomreach, Chase, Mastercard, McKinsey & Co., Pros, Revionics, and Task.

“Advancements in machine learning make it cheaper for these systems to collect and process large volumes of personal data, which can open the door for price changes based on information like your precise location, your shopping habits, or your web browsing history,” the FTC wrote.

Posted on March 15, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

At least eight agencies are investigating a recent fire at a Bayer executive’s New Jersey home as a possible arson, authorities said. The fire happened around 7:30 a.m. March 4th “at an occupied residence on East Lane in Madison,” the Morris County Prosecutor’s Office told CNN yesterday.

US stocks bounced back sharply on Friday to cap a volatile week on Wall Street as the risk of a government shutdown eased while investors stayed on watch for the next move in an escalating trade war. The S&P 500 (^GSPC) climbed more than 2.1% after the benchmark index sank on Thursday to close in correction territory. The NASDAQ Composite (^IXIC) jumped over 2.6% as tech stocks soared. The Dow Jones Industrial Average (^DJI) moved up more than 600 points, or 1.6%.

Yesterday March 14th was Pi Day! (Yes, the mathematical constant, although we fully support celebrating with actual pie.) Put simply, Pi—aka π—is the ratio of a circle’s circumference to its diameter. It also sneaks its way into medicine. For one, it’s part of Poiseuille’s Law, an equation that helps explain how fluid flows through tubes, including arteries and IV lines. So, whether you’re crunching numbers or crunching on a slice, Pi is definitely worth celebrating

And, today is the Ides of March!

Visualize: How private equity tangled banks in a web of debt, from the Financial Times.

Posted on March 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS

By Staff Reporters

***

***

The Consumer Price Index (CPI) for February found that the cost of goods and services rose 0.2% on the month. The annual rate of inflation was also up 2.8% — slightly less than expected.

Here’s a breakdown of several price changes for February:

Food: increase 0.2%

Energy: increase 0.2%

Electricity: increase 1.0%

New vehicles: decrease 0.1%

Used vehicles: increase 0.9%

Apparel: increase 0.6%

Shelter: increase 0.3%

Transportation: decrease 0.8%

Medical care services: increase 0.3%

The Bureau of Labor Statistics reported that according to its indexes, over the month the cost of medical care rose 0.3%, physicians’ services were 0.4% higher, hospital services added 0.1%, and prescription-drug costs were unchanged.

Posted on March 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

Over Heard in the Doctor’s Lounge

By Staff Reporters

***

***

Statistics is a discipline that deals with data, facts, and figures from which meaningful information is inferred. It involves gathering, summarizing, and analyzing data to understand trends and patterns. Statistics can be divided into two main types: descriptive statistics, which summarize data, and inferential statistics, which make predictions or inferences about a population based on a sample

But, reading statistical income information can be full of pitfalls. One needs to look at the mean and median. Both give useful information. By comparing the two, one can ascertain if there are outliers that affect the results.

Example:

If a sample of 10 physicians has one earning $1,000,000 and the other nine earning $100,000, the average (mean) income is $190,000; but the median income is $100,000.

Just using this information alone, one can tell there are some outliers that could affect the results.

–Dr. Edmond F. Mertzenich, DPM MBA [Rockford, IL]

***

***

Example:

“Lies, damned lies, and statistics” is a phrase describing the persuasive power of statistics to bolster weak arguments, “one of the best, and best-known” critiques of applied statistics. It is also sometimes colloquially used to doubt statistics used to prove an opponent’s point.

Posted on March 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

An executive for insurance giant State Farm was fired this week after he was recorded on an undercover video making comments about the insurer’s premium increases in response to Southern California wildfires. Haden Kirkpatrick, who worked as State Farm’s vice president for innovation and venture capital, was surreptitiously recorded on a video published by O’Keefe Media Group. The Los Angeles Times reported that he claims he was fired over the recording.

US stocks fell on Thursday, with the S&P 500 (^GSPC) officially entering into correction territory, as economic concerns grew and investors digested the latest inflation data, President Trump’s trade offensive, and a looming US government shutdown.

The S&P 500 (^GSPC) dropped 1.4% to officially enter a correction, as it is now more than 10% off its February record high. The tech-heavy NASDAQ Composite (^IXIC), which itself entered into a correction last week, shed nearly 2% on the heels of a rebound for both gauges. The Dow Jones Industrial Average (^DJI) slid 1.3%, or nearly 550 points.

Posted on March 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

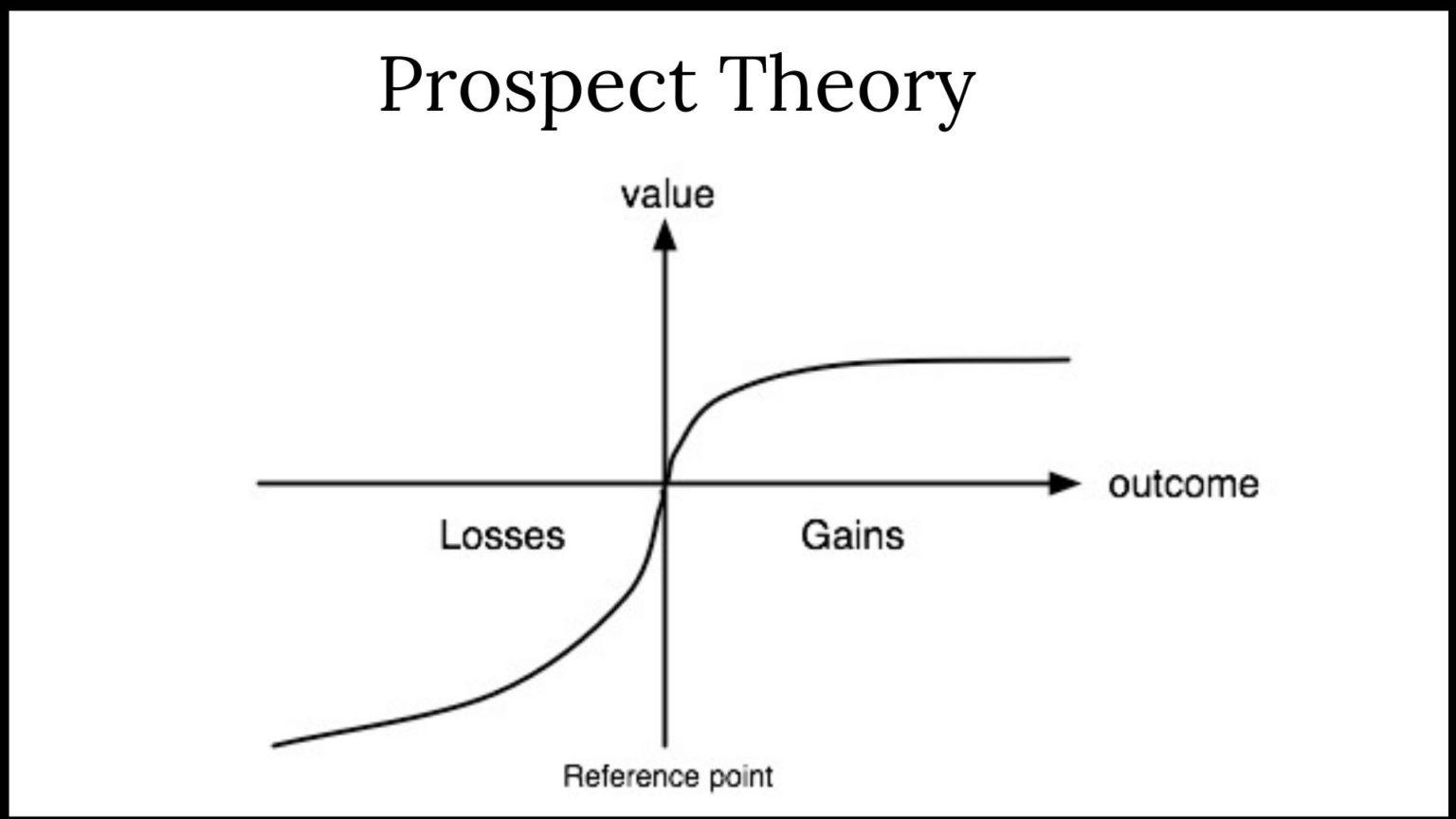

BEHAVIORAL ECONOMICS

By Staff Reporters

***

***

Prospect theory is a psychological and behavioral economics theory developed by Daniel Kahneman and Amos Tversky in 1979. It explains how people make decisions when faced with alternatives involving risk, probability, and uncertainty. According to this theory, decisions are influenced by perceived losses or gains.

Example:

Amanda, a DO client, was just informed by her financial advisor that she needed to re-launch her 403-b retirement plan. Since she was leery about investing, she quietly wondered why she couldn’t DIY. Little does her FA know that she doesn’t intend to follow his advice, anyway! So, what went wrong?

The answer may be that her advisor didn’t deploy a behavioral economics framework to support her decision-making. One such framework is the “prospect theory” model that boils client decision-making into a “three step heuristic.”

Prospect theory makes the unspoken biases that we all have more explicit. By identifying all the background assumptions and preferences that clients [patients] bring to the office, decision-making can be crafted so that everyone [family, doctor and patient] or [FA, client and spouse] is on the same page. Briefly, the three steps are:

1. Simplify choices by focusing on the key differences between investment [treatment] options such as stock, bonds, cash, and index funds.

2. Understanding that clients [patients] prefer greater certainty when it comes to pursuing financial [health] gains and are willing to accept uncertainty when trying to avoid a loss [illness].

3. Cognitive processes lead clients and patients to overestimate the value of their choices thanks to survivor bias, cognitive dissonance, appeals to authority and hindsight biases.

Assessment

Much like healthcare today, the current mass-customized approaches to the financial services industry falls short of recognizing more personalized advisory approaches like prospect theory and assisted client-centered investment decision-making.

Posted on March 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITION

By Staff Reporters

***

***

1035 Exchange

DEFINITION: A method of exchanging insurance-related assets without triggering a taxable event. Cash-value life insurance policies and annuity contracts are two products that may qualify for a 1035 exchange.

***

A 1035 exchange is a feature in the tax code that permits individuals to transfer funds from an existing life insurance endowment, or annuity policy to a new one without tax consequences.

These transactions are not subject to tax deductions or tax credits but rather tax deferrals, meaning that individuals would only pay taxes on any earnings once they receive money from the policy later.

Without this provision, policyholders would have to close their previous accounts and be subjected to both taxes and surrender charges before they could open a new account.

Posted on March 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Stock markets mostly rose Wednesday on both sides of the Atlantic as investors shrugged off Washington’s latest tariffs to focus on cooling US inflation and a Ukraine ceasefire plan.

Markets have worried that the tariffs could spark a surge in US inflation and drive a stake into the chances that the Federal Reserve cuts interest rates further. But government data released Wednesday showed US consumer inflation had slowed slightly to 2.8 percent in February — the first full month of Trump’s White House return.

That was slightly better than analysts expected. Core inflation, which excludes volatile food and energy prices, dipped to an annual rate of 3.1 percent. “The inflation data are a bright spot in the Federal Reserve’s battle against rising prices. They reinforce the expectation of three rate cuts later in 2025,” said Jochen Stanzl, chief market analyst at CMC Markets.

“Sentiment on Wall Street is so negative that these positive inflation figures could spark a broader recovery in stock prices,” he added.

Wall Street’s main stock indices mostly closed higher with the tech-heavy NASDAQ Composite rising 1.2 percent. But the Dow dipped into the red, losing 0.2 percent.

Posted on March 12, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Stocks inched up overnight after Monday’s ugly plunge to six-month lows, but positive catalysts were scattered and the rocky economy has begun affecting earnings forecasts. Delta Airlines (DAL) lowered its outlook yesterday amid what it called “macro uncertainty,” raising concerns it could be first on a crowded runway.

One theme as stocks plunged recently was that despite the suffering was that earnings outlooks remained strong. The latest FactSet forecasts for first quarter and 2025 S&P 500 earnings growth are 7.3% and 11.6%, respectively. Both are down from December 31st, though, and further setbacks in expectations could hurt confidence. Oracle (ORCL) missed analysts’ estimates late Monday. “The longer the tariff turmoil and related uncertainty about trade policy lasts, the more likely economic and earnings growth may take a hit,” said Jeffrey Kleintop, chief global investment strategist at Schwab.

Job openings data later yesterday morning and the Consumer Price Index (CPI) tomorrow could help set the tone, though economic growth seems to have replaced inflation as the prime concern. Yesterday’s steep losses reflected less confidence in either the administration or the Federal Reserve potentially stepping in to rescue a slumping economy. Growth fears have pummeled the Magnificent Seven, with six of them among the bottom 350 in S&P 500 index (SPX) year-to-date performance.

For now, the S&P 500 (^GSPC) avoided correction territory but still fell about 0.8% to trade at just under 5,600. The Dow Jones Industrial Average (^DJI) shed roughly 500 points, or 1.1%, dragged down by shares of Verizon (VZ). The tech-heavy NASDAQ Composite (^IXIC) reversed gains in the last few minutes of trading to fall about 0.2%. All three indexes closed at their lowest levels since September.

Visualize: How private equity tangled banks in a web of debt, from the Financial Times.

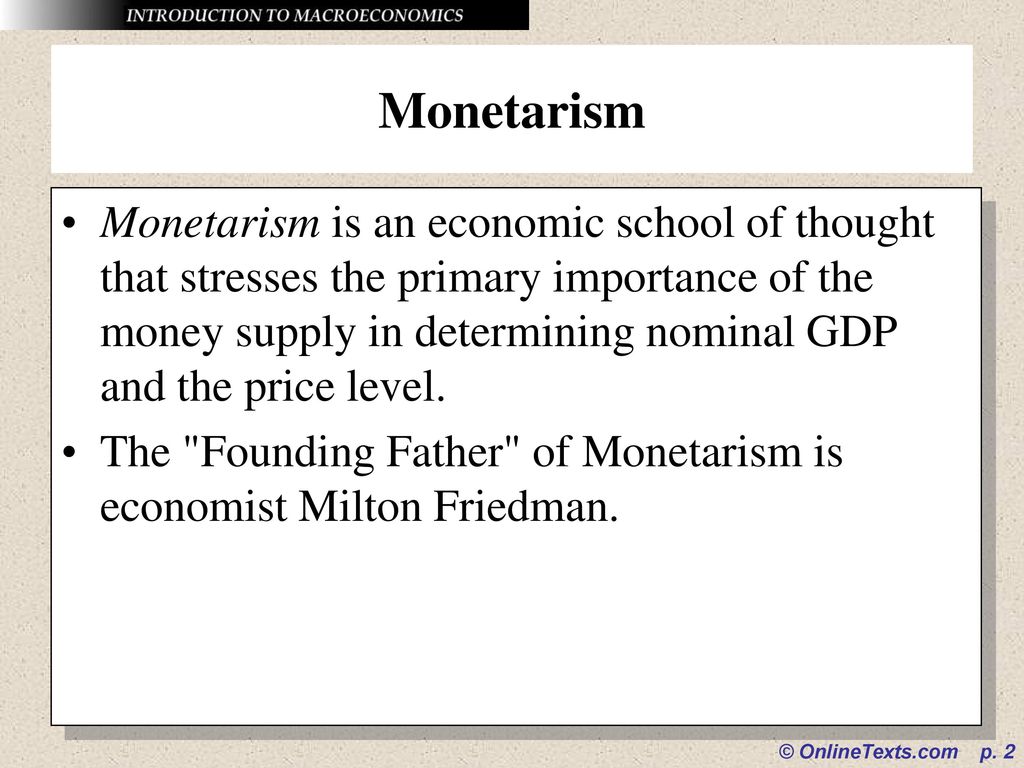

Monetarism is the belief that changes in the money supply are the main determinant of changes in inflation, associated especially with Milton Friedman, an American economist. Cases of hyperinflation have indeed been associated with the rapid printing of money. But when governments adopted monetarist policies in the late 1970s and early 1980s, they found money supply hard to control and also struggled to decide which measure of money supply was best to target. Monetarist policies were abandoned in favor of inflation targeting.

Monetary financing is the direct financing of government spending by the central bank. This happened during the hyperinflation in Germany in 1923 and was thus regarded as anathema for a long period afterwards. As a result, some commentators viewed quantitative easing after the financial crisis of 2007-09 with great suspicion. Technically, however, QE is not monetary financing, because central banks only buy government bonds in the secondary market and because they pay interest on reserves (the money they create).

Monetary policy The use, normally by the central bank, of interest rates and other tools to try to influence the economy. Interest rates are raised when the bank is trying to control inflation and lowered when inflation is low and it is trying to revive the economy. The financial crisis of 2007-09 led central banks to face the zero lower bound. This prompted many of them to use a new tool, quantitative easing, which was designed to bring down long-term rates or bond yields.

Posted on March 11, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

US stocks plunged on Monday as investors processed growing concerns about the health of the US economy after President Trump and his top economic officials acknowledged the possibility of a potential rough patch.

The Dow Jones Industrial Average (^DJI) fell nearly 900 points, or over 2%, while the benchmark S&P 500 (^GSPC) dropped around 2.7% after the index posted its worst week since September. The tech-heavy NASDAQ Composite (^IXIC) fell 4% in its worst day since 2022, as the “Magnificent Seven” stocks led the sell-off. Tesla’s (TSLA) rout continued, plunging 15% and officially wiping out the gains it had made in the wake of Trump’s election win. Nvidia (NVDA), Apple (AAPL), Google parent Alphabet (GOOG), and Meta (META) all each lost more than 4%.

Key inflation data includes the Consumer Price Index (CPI) and Producer Price Index (PPI) on Wednesday and Thursday could help set the tone, though economic growth concerns seem to have replaced inflation as the prime concern. The S&P 500 index (SPX) dropped more than 3% last week, the worst performance since September.

However, the U.S. economy “is in a good place” despite recent policy uncertainty, Federal Reserve Chairman Jerome Powell said Friday. He sees no need to hurry rate cuts until there’s more policy clarity, Bloomberg reported. Stocks rallied on Powell’s words late Friday, but Monday’s early action indicates that rallies continue being sold, and the Cboe Volatility Index (VIX) rose above 26 as investors piled into risk-off assets like bonds. The 200-day moving average of 5,734 for the SPX remains a key technical support area, and the SPX was on pace to open below that Monday, now more than 6% off of all-time highs but not yet in –10% correction territory.

Posted on March 10, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS

By Staff Reporters

***

***

US stocks plunged on Monday as investors processed growing concerns about the health of the US economy after President Trump and his top economic officials acknowledged the possibility of a potential rough patch.

The Dow Jones Industrial Average (^DJI) fell nearly 900 points, or over 2%, while the benchmark S&P 500 (^GSPC) dropped around 2.7% after the index posted its worst week since September.

The tech-heavy NASDAQ Composite (^IXIC) fell 4% in its worst day since 2022, as the “Magnificent Seven” stocks led the sell-off. Tesla’s (TSLA) rout continued, plunging 15% and officially wiping out the gains it had made in the wake of Trump’s election win. Nvidia (NVDA), Apple (AAPL), Google parent Alphabet (GOOG), and Meta (META) all each lost more than 4%.

During the January 2025 J.P. Morgan Healthcare Conference, Teladoc’s executives announced the company has partnered with Amazon Health Services, joining its Health Benefits Connector program. The program was rolled out in January 2024 and connects Amazon customers with virtual care benefits covered by their insurance plan or employer; if eligible, customers are able to apply to join the program(s).

Teladoc is the fifth company to join Amazon’s Health Benefits Connector program (formerly known as Health Conditions Programs), along with digital physical therapy company Hinge Health; chronic condition management company Omada; online therapy and mental health firm Rula; and behavioral healthcare provider Talkspace. (Read more…)

I was having lunch with a close friend of mine. He mentioned that he had accumulated a significant sum of money and did not know what to do with it. It was sitting in bonds, and inflation was eating its purchasing power at a very rapid rate.

He is a dentist and had originally thought about expanding his business, but a shortage of labor and surging wages turned expanding into a risky and low-return investment. He complained that the stock market was extremely expensive. I agreed.*

He said that the only thing left was residential real estate. I pushed back. “What do you think will happen to the affordability of houses if – and most likely when – interest rates go up? Inflation is now 6%. I don’t know where it will be in a year or two, but what if it becomes a staple of the economy? Interest rates will not be where they are today. Even at 5% interest rates [I know, a number unimaginable today] houses become unaffordable to a significant portion of the population. Yes, borrowers’ incomes will be higher in nominal terms, but the impact of the doubling of interest rates on the cost of mortgages will be devastating to affordability.”

He rejoined, “But look at what happened to housing over the last twenty years. Housing prices have consistently increased, even despite the financial crisis.”

I agreed, but I qualified his statement: “Over the past twenty, actually thirty, years interest rates declined. I honestly don’t know where interest rates will be in the future. But probabilistically, knowing what we know now, the chances that they are going to be higher, much higher, are more likely than their staying low. Especially if you think that inflation will persist.”

We quickly shifted our conversation toward more meaningful topics, like kids.

It seems that every year I think we have finally reached the peak of crazy, only to be proven wrong the next year. The stock market and thus index funds, just like real estate, have only gone one way – up. Index funds became the blunt instrument of choice in an always-rising market. So far, this choice has paid off nicely.

The market is the most expensive it has ever been, and thus future returns of the market and index funds will be unexciting. (I am being gentle here.)

You don’t have to be a stock market junkie to notice the pervasive feeling of euphoria. But euphoria is a temporary, not a permanent emotion; and at least when it comes to the stock market, it is usually supplanted by despair. Market appreciation that was driven by expanding valuations was not a gift but a loan – the type of loan that must always be paid back with a high rate of interest.

I don’t know what straw will break the feeble back of this market or what will cause the music to stop (there, you got two analogies for the price of none). We are in an environment where there are very few good options. If you do nothing, your savings will be eaten away by inflation. If you do something, you find that most assets, including the stock market as a whole, are incredibly overvalued.

We are doing the only sensible thing that you can do today. We spend very little time thinking about straws or what will cause the music to stop or how overvalued the market is. We are focusing all our energy on patiently building a portfolio of high-quality, cash-generative, significantly undervalued businesses that have pricing power.

This has admittedly been less rewarding than taking risky bets on unimaginably expensive assets. It may lack the excitement of sinking money into the darlings you see in the news every day, but we hope that our stocks will look like rare gems when the euphoria condenses into despair. As we keep repeating in every letter, the market is insanely overvalued. Our portfolio is anything but – we don’t own “the market”.

*A question may arise:Why did I not tell my dentist friend to pick individual stocks? He runs a busy dental practice and wouldn’t have the time or the training to pick stocks.

Why didn’t I offer him our services? IMA manages all my and my family’s liquid assets, but I have a rule that I never (ever!) break – I don’t manage my friends’ money. I’ll help them as much as possible with free advice but will never have a professional relationship with them. I intentionally create a separation between my personal and professional lives. After a difficult day in the market, I want to be able to go for beers with friends and leave the market at the office.

Also, this simplifies my relationships with my friends. There is no ambiguity in our friendship.

Posted on March 8, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

AGREE or DISAGREE?

By Staff Reporters

***

***

US Treasury Secretary Scott Bessent made waves yesterday with his comment that the American economy is facing a “detox period.”

Should we be seeing that this economy that we inherited [is] starting to roll a bit? Sure. And look, there’s going to be a natural adjustment as we move away from public spending to private spending. The market and the economy have just become hooked, and we’ve become addicted to this government spending, and there’s going to be a detox period. There’s going to be a detox” .

Bessent, a former hedge-fund manager, said during a CNBC interview.

“Employment should be from private companies, not from government. And I’m confident, if we have the right policies, it will be a very smooth transition.”

Bessent said, in an apparent reference to the layoffs of federal workers executed in large part by the entity known as the Department of Government Efficiency, which is run by Trump adviser Elon Musk.

You can also listen to a professional narration of this article on iTunes & online.

ENCORE: March 22, 2004

A basic property of religion is that the believer takes a leap of faith: to believe without expecting proof. Often you find this property of religion in other, unexpected places – for example, in the stock market. It takes a while for a company to develop a “religious” following: only a few high-quality, well-respected companies with long track records ever become worshipped by millions of investors. My partner, Michael Conn, calls these “religion stocks.” The stock has to make a lot of shareholders happy for a long period of time to form this psychological link.

The stories (which are often true) of relatives or friends buying few hundred shares of the company and becoming millionaires have to fester a while for a stock to become a religion. Little by little, the past success of the company turns into an absolute – and eternal – truth. Investors’ belief becomes set: the past success paints a clear picture of the future.

Gradually, investors turn from cautious shareholders into loud cheerleaders. Management is praised as visionary. The stock becomes a one-decision stock: buy. This euphoria is not created overnight. It takes a long time to build it, and a lot of healthy pessimists have to become converted into believers before a stock becomes a “religion.”

Once a stock is lifted up to “religion” status, beware: Logic is out the window. Analysts start using T-bills to discount the company’s cash flows in order to justify extraordinary valuations. Why, they ask, would you use any other discount rate if there is no risk? When a T-bill doesn’t do the trick, suddenly new and “more appropriate” valuation metrics are discovered.

Other investors don’t even try to justify the valuation – the stock did well for me in the past, why would it stop working in the future? Faith has taken over the stock. Fundamentals became a casualty of “stock religion.” These stocks are widely held. The common perception is that they are not risky.

The general public loves these companies because they can relate to the companies’ brands. A dying husband would tell his wife, “Never sell _______ (fill in the blank with the company name).” Whenever a problem surfaces at a “religion stock,” it is brushed away with the comment that “it’s not like the company is going to go out of business.” True, a “religion stock” company is a solid leader in almost every market segment where it competes and the company’s products carry a strong brand name. However, one should always remember to distinguish between good companies and good stocks.

Coca-Cola is a classic example of a “religion stock.” There are very few companies that have delivered such consistent performance for so long and have such a strong international brand name as Coca-Cola. It is hard not to admire the company.

But admiration of Coca-Cola achieved an unbelievable level in the late nineties. In the ten years leading up to 1999, Coca-Cola grew earnings at 14.5% a year, very impressive for a 103-year-old company. It had very little debt, great cash flow and a top-tier management. This admiration came at a steep price: Coca-Cola commanded a P/E of 47.5. That P/E was 2.7 times the market P/E. Even after T-bills could no longer justify Coke’s valuation, analysts started to price “hidden” assets – Coke’s worldwide brand. No money manager ever got fired for owning Coca-Cola.

The company may not have had a lot of business risk. But in 1999, the high valuation was pricing in expectations that were impossible for any mature company to meet. “The future ain’t what it used to be” – Yogi Berra never lets us down. Success over a prolonged period of time brings a problem to any company – the law of large numbers.

Enormous domestic and international market share, combined with maturity of the soft drink market, has made it very difficult for Coca-Cola to grow earnings and sales at rates comparable to the pre-1999 years. In the past five years, earnings and sales have grown 2.5% and 1.5% respectively. After Roberto C. Goizueta’s death, Coke struggled to find a good replacement – which it acutely needed.

Old age and arthritis eventually catch up with “religion stocks.” No company can grow at a fast pace forever. Growth in earnings and sales eventually decelerates. That leads to a gradual deflation of the “religion” premium. For Coke, the descent from its “religious” status resulted in a drop of nearly 20% in the share price – versus an increase of 65% in the broad market over the same time. And at current prices, the stock still is not cheap by any means. It trades at 25 times December 2004 earnings, despite expectations for sales growth in the mid single digits and EPS growth in the low double digits.

It takes a while for the religion premium to be totally deflated because faith is a very strong emotion. A lot of frustration with sub-par performance has to come to the surface.

Disappointment chips away at faith one day at a time. “Religion” stocks are not safe stocks. The leap of faith and perception of safety come at a large cost: the hidden risk of reduction in the “religion premium.” The risk is hidden because it never showed itself in the past. “Religion” stocks by definition have had an incredibly consistent track record. Risk was rarely observed.

However, this hidden risk is unique because it is not a question of if it will show up but a question of when. It is very hard to predict how far the premium will inflate before it deflates – but it will deflate eventually. When it does, the damage to the portfolio can be huge.

Religion stocks generally have a disproportionate weight in portfolios because they are never sold – exposing the trying-to-be-cautious investor to even greater risks. Coca-Cola is not alone in this exclusive club. General Electric, Gillette, Berkshire Hathaway are all proud members of the “religion stock” club as well. Past members would include: Polaroid – bankrupt; Eastman Kodak – in a major restructuring; AT&T – struggling to keep its head above water. That stock is down from over $80 in 1999 to $18 today.

Emotions have no place in investing. Faith, love, hate, and disgust should be left for other aspects of our life. More often than not, emotions guide us to do the opposite of what we need to do to be successful. Investors need to be agnostic towards “religion stocks.” The comfort and false sense of certainty that those stocks bring to the portfolio come at a huge cost: prolonged under performance.

My thoughts today (20+ years later)

This is one of the first investment articles I ever wrote. I had just started writing for TheStreet.com. It’s interesting to read this article more than 20 years later. I am surprised my writing was not as bad as I had feared (though in many cases it was worse than I feared when I read my other early articles).

So much has happened since then – I am a different person today than I was back then. I have two more kids; I have written three more books and a thousand articles. The last two decades were my formative years as an investor and adult.

The goal of the article was not to make predictions but to warn readers that the long-term success of certain companies creates a cult-like following and deforms thinking. In fact, my original article – the one I submitted to TheStreet.com – did not mention any companies other than Coke. The editors wanted me to include more names so that the article would show up on more pages of Yahoo! Finance.

With the exception of Berkshire Hathaway, all of these companies have produced mediocre or horrible returns. In the best case, their fundamental returns in their old age were only a fraction of what they were when these companies were younger and the world was their oyster.

To my surprise, Coke’s stock is still trading at a high valuation. Its business has performed like the old-timer it is, with revenue and earnings growing by only 3–4% a year. The days of double-digit revenue and earnings growth were left in the 80s and 90s, though the high valuation remained.

Posted on March 8, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Walgreens Boots Alliance says it has agreed to be acquired by private equity firm Sycamore Partners as the struggling retailer looks to turn itself around after years of losing money. Walgreens said Thursday that Sycamore will pay $11.45 per share, giving the deal an equity value just under $10 billion. Shareholders could eventually receive up to an

Leverage ratios measure the amount of capital that comes from debt. In other words, leverage financial ratios are used to evaluate a company’s debt levels. Common leverage ratios include the following:

The debt ratio measures the relative amount of a company’s assets that are provided from debt:

Debt ratio = Total liabilities / Total assets

The debt to equity ratio calculates the weight of total debt and financial liabilities against shareholders’ equity:

Debt to equity ratio = Total liabilities / Shareholder’s equity

A common stock is the least senior of securities issued by a company. A preferred stock, in contrast, is slightly more senior to common stock, since dividends owed to the preferred stockholders should be paid before distributions are made to common stockholders.

However, distributions to preferred stockholders are limited to the level outlined in the preferred stock agreement (i.e., the stated dividend payments). Like a fixed income security, preferred stocks have a specific periodic payment that is either a fixed dollar amount or an amount adjusted based upon short-term market interest rates. However, unlike fixed income securities, preferred stocks typically do not have a specific maturity date and preferred stock dividend payments are made from the corporation’s after tax income rather than its pre-tax income. Likewise, dividends paid to preferred stockholders are considered income distributions to the company’s equity owners rather than creditors, so the issuing corporation does not have the same requirement to make dividend distributions to preferred stockholders.

Preferred Stock

Thus, preferred stock is generally referred to as a “hybrid” security, since it has elements similar to both fixed income securities (i.e., a stated periodic payments) and equity securities (i.e., shareholders are considered owners of the issuing company rather than creditors).

Hybrid Securities