BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on November 27, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

DONATION: In “Name” Only?

Staff Reporters

***

Proponents of DAFs say that their structure encourages giving: The tax deduction encourages wealthy patrons to dedicate money for charity even before they’ve decided which cause to support. “Donors may have good reasons to postpone grants,” a Stanford Law School article says..

In one hypothetical, a tech founder who “sells a startup for millions of dollars” may want to donate her takings but is too busy to immediately decide how to direct the funds; a DAF is a good choice for this person, the law article notes.

However, while DAFs could in theory grow the charitable pie, in practice, they too often allow the donor the illusion of charity while letting them keep control of their funds, critics say.

While a gift to a DAF is treated the same as an outright gift to the Red Cross or United Way, in practice, it “effectively allows the donor to retain ongoing control over the charitable disposition and investment of the donated assets,” tax scholars Roger Colinvaux and Ray Madoff wrote in 2019. What’s more, “donors are under no obligation, and have no incentive, ever to release their advisory privileges to make the funds available for charitable use.”

And ultra wealthy donors get a substantially larger tax break than a middle-class worker. As much as 74 cents of every dollar given to charity comes back to the donor in the form of tax breaks, according to calculations by Colinvaux and Madoff, with the highest-earning donors getting the biggest benefits A person in the top tax bracket would save 37% of their federal income tax for every dollar they contribute with a charitable donation; a similar amount of state income tax; and, depending on what they donate and when, they can also avoid capital gains tax and estate tax. (By contrast, a typical worker who makes about $60,000 and doesn’t own stocks would save 22% from their cash contribution, in addition to any state tax savings.)

What’s more, because there’s no way to track donations from particular DAF accounts, they act as a form of “dark money,” allowing donors to give vast sums, essentially anonymously, to a range of potentially unsavory organizations, including nonprofits that advocate for specificpolitical causes or organizations classified as hate groups, IPS says.

“This allows DAFs to be used to hide transfers — similar to the way the ultra-wealthy use multiple shell companies to hide the movement of money among offshore accounts,” IPS writes.

All of these strategies are completely legal, the IPS notes, as are other potentially questionable tactics used by family foundations—such as paying family members to serve as foundation trustees or act as executives of foundations, sometimes at salaries in the hundreds of thousands of dollars a year. However, the IPS argues, they erode public trust in charities and the tax system overall.

“The fact that billionaires opt out of paying taxes, have these closely held family foundations and get to play God about where the money goes, that’s private power — unaccountable private power,” Collins said.

“At this point philanthropy is at risk of becoming taxpayer-subsidized private power.”

Posted on November 25, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

Technological advancements have accelerated the shift of healthcare services from inpatient to outpatient settings, creating both opportunities and challenges for hospitals. For instance, minimally invasive procedures often serve as alternatives to traditional, more invasive surgeries. Additionally, the integration of telehealth and artificial intelligence (AI) has the potential to enhance access to and quality of care while reducing expenditures and administrative burdens.

This final installment of a five-part series on the valuation of hospitals examines the technological advancements transforming the industry. (Read more…)

If you’ve found yourself worrying about the stock market or money lately, you definitely have company. Money anxiety, also called financial anxiety, has become more common than ever after the presidential election of November 2024.

In fact, the American Psychological Association’s 2022 Stress in America Survey, 87 percent of people who responded listed inflation as a source of significant stress. The rise in prices for everything from fuel to food has people from all backgrounds worried, today. The researchers say, in fact, that no other issue has caused this much stress since the survey began in 2007.

When money and financial concerns cause ongoing stress in your life, you could eventually begin to experience some feelings of anxiety as a result. This anxiety can, in turn, have a negative impact on your quality of life.

***

Chrometophobia, commonly known as fear of money, is a psychological condition characterized by overwhelming anxiety and avoidance of currency; according to colleague Dan Ariely PhD.

Physician Financial Fear is probably the most common emotion among physicians. The fear of being wrong – as well as the fear of being correct! It can be debilitating, as in the corollary expression on fear: the paralysis of analysis.

According to Paul Karasik, there are four common investor and physician fears, which can be addressed by financial advisors and psychologists in the following manner:

Fear of making the wrong decision: ameliorated by being a teacher and educator.

Fear of change: ameliorated by providing an agenda, outline and/or plan.

Fear of giving up control: ameliorated by asking for permission and agreement.

Fear of losing self-esteem: ameliorated by serving the client first and communicating that sentiment in a positive manner.

Posted on November 23, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Tobacco bonds are a form of municipal debt securities and securitized debt whose payment obligations are tied to a master medical lawsuit settlement agreement between 46 states and several major U.S. tobacco companies.

In exchange for the states settling their lawsuits against the tobacco industry for recovery of tobacco-related health care costs and exempting the tobacco companies from private tort liability regarding harm caused by tobacco use, the companies agreed to curtail or cease certain tobacco marketing practices and to pay, in perpetuity, various annual payments to the states to compensate for the medical costs of tobacco-related illnesses.

These tobacco industry payments have been securitized into municipal bonds. One underlying risk, among others, is that if certain conditions are met, the tobacco companies may reduce or suspend part of their payments.

Prepayment risk is typically used in reference to mortgage-backed securities. It refers to the risk that mortgage refinancing activity might increase when market interest rates decline, which is generally not favorable for MBS investors.

For example, when homeowners refinance their mortgages, MBS investors are “prepaid,” shortening the life of their investments and forcing investors to reinvest the proceeds under lower interest rate conditions than what were most likely prevailing at the time of the original MBS investment.

Price adjustments for prepayment risk are one factor that helps explain why MBS, despite their generally high credit quality, have higher yields than comparable-maturity Treasury securities.

Posted on November 22, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Robert F Kennedy Jr, who was selected by Donald Trump to run the U.S. health and human services department, is working on plans to rid the American Medical Association from its role in drawing up Medicare’s billing codes, which sets doctors’ fees for more than 10,000 procedures, Oliver Barnes of The Financial Times reports.

The plan would result in an upheaval of a system that has been in place for decades. Publicly traded companies in the healthcare space include CVS Health (CVS), Centene (CNC), Cigna (CI), Elevance Health (ELV), Humana (HUM), Molina Healthcare (MOH) and UnitedHealth (UNH).

Stocks sank yesterday on news that Russian President Vladimir Putin lowered the threshold for using nuclear weapons, retaliation against the US for allowing Ukraine to use American-made long-range missiles. The NASDAQ and S&P 500 managed to recover, but the DJIA stayed all day in the red.

Treasury yields dropped as bonds rose.

Gold popped as traders sought safety, as the commodity benefited from the US dollar pulling back from a recent one-year high.

Bitcoin continued to climb slowly but surely, reaching another new all-time high.

Classic Definition: A comprehensive review of a physician, clinic, facility, medical provider or hospital’s charges to ensure Medicare billing compliance through complete and accurate HCPCS/CPT and UB-92 revenue code assignments for all items including supplies and pharmaceuticals. The charge master captures the costs of each procedure, service, supply, prescription drug, and diagnostic test provided at the hospital, as well as any fees associated with services, such as equipment fees and room charges

Modern Circumstance: A charge master quizlet (charge description master [CDM]) document that contains a computer-generated list of procedures, services, and supplies with charges for each. Charge master rates are essentially the health care market equivalent of Manufacturer’s Suggested Retail Price (MSRP) in the car buying market. Poor charge master maintenance can lead to overpayments or underpayments. It can also lead to claim rejections from insurance companies, poor patient experience, or compliance violations.

Paradox Examples:

Superbills: An encounter form that is the financial record source document used by healthcare providers and other personnel to record treated diagnoses and services rendered to the patient during the current encounter. It is also called a superbill.

Payment rates: Almost no one actually pays the publicized charge master rates. The vast majority of health care consumers are represented by a payer of some kind, such as a commercial health insurance company, Medicaid, or Medicare. Commercial insurers negotiate the actual prices they pay during the process of contracting with providers. Medicare and Medicaid establish their own payment levels independent of hospitals’ charge master lists – Medicare through the federal government and Medicaid through state governments.

Cash pay: The sad irony of the charge master is that the uninsured are the most likely to be billed charge master rates because they are not represented by a third-party payer.

Problematic features: Other items also impede the ability of payers to have a comprehensive and accurate understanding of hospitals’ financial positions. For example, nonprofit hospitals are required to report charity care, bad debt expenses, community benefit initiatives, and uncompensated care. When these expenses are reported at the charge master level, expenses can be paradoxically overstated, potentially making a hospital’s financial position look worse than it actually is.

Posted on November 19, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Stocks ended the day mixed, with the Dow sinking into the red while the S&P 500 and NASDAQ kicked off the week on a positive note thanks to gains from tech stocks.

Oil popped on a double-whammy of news: Long-range, US-made ballistic missiles launched from Ukraine into Russia might disrupt oil supply, while the shutdown of Norway’s Johan Sverdrup oil field due to a power outage will definitelydisrupt oil supply.

Crypto continued its hot streak today: Bitcoin popped back above $90,000, giving other cryptocurrencies a boost.

Bitcoin’s boom has certainly helped MicroStrategy, which announced today that it purchased 51,780 bitcoins for approximately $4.6 billion in cash, or roughly $88,627 per bitcoin, in the last week alone.

The new Trump Trade continues: The president-elect’s selection of Liberty Energy CEO Chris Wright to lead the Department of Energy gave Liberty a 4.85% boost today. Wright is also on the board of nuclear company Oklo, which popped 14.83%.

Netflix disappointed viewers with its glitchy showing of Jake Paul vs. Mike Tyson, but shareholders forgave the company after it announced record viewership of the fight. Shares climbed 2.80%.

CVS Health gained 5.41% on news that it struck a deal with activist investor Glenview Capital Management to add four new seats to its board.

Robinhood jumped 8.29% to a new all-time high thanks to an upgrade from Needham analysts giving the investing app a “buy” rating due to its crypto offerings under a pro-crypto Trump presidency.

Warner Bros. Discovery rose 2.71% on a Wall Street Journal report that it has settled its legal dispute with the NBA, guaranteeing broadcast rights for the next decade.

STOCKS DOWN

Nvidia isn’t often in this section of the newsletter, but the semiconductor leader sank 1.29% today on a report from The Information that its new Blackwell chips are prone to overheating.

Palantir popped after moving over to the Nasdaq last week, but the red-hot software stock dropped 6.86% as investors collected profits.

Redfin may help you buy a house, but the online real estate brokerage is a “sell,” according to Goldman Sachs. The Wall Street firm cited low home sales, low affordability, and low chances of success in a competitive market. Shares fell 4.42%.

Uber dropped 5.35% to a new 52-week low on the threat of Tesla’s robotaxis ruling the road thanks to a Trump administration that seems keen on cutting self-driving regulations.

The SPX was up 23.00 points (0.4%) to 5893.62; the Dow Jones Industrial Average® ($DJI) fell 55.39 points (0.1%) to 43,389.6; and the NASDAQ Composite®($COMP) was up 111.69 points (0.6%) to 18,791.81.

The 10-year Treasury note yield fell one basis point to 4.41%.

Posted on November 17, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Dedicated short bias strategies short stocks expected to depreciate as a result of company-specific catalysts or falling markets. These strategies maintain a net short exposure to the equity market, seeking to reduce equity portfolio volatility and offer the potential to earn returns in falling equity markets. Of course, they may be challenged in periods of rising equity markets.

From Shorting to a Short Bias

Prior to the long-term bull market for U.S. equities that took place in the 1980s and 1990s, many hedge funds used a dedicated short strategy, rather than a dedicated short bias strategy.

The dedicated short strategy was one that exclusively took short positions. The dedicated short funds were virtually destroyed during the bull market, so the dedicated short bias fund emerged and took a more balanced approach. The long holdings are enough to keep losses manageable, although funds can still run into problems with leverage and capital flight if losses continue for too long.

Social Proof is a subtle but powerful reality that having others agree with a decision one makes, gives that person more conviction in the decision, and having others disagree decreases one’s confidence in that decision.

This bias is even more exaggerated when the other parties providing the validating/questioning opinions are perceived to be experts in a relevant field, or are authority figures, like doctors, attorneys, financial advisors, teachers and/or people on television. In many ways, the short term moves in the stock market are the ultimate expression of social proof – the price of a stock one owns going up is proof that a lot of other people agree with the decision to buy, and a dropping stock price means a stock should be sold.

According to colleague Dan Ariely PhD, when these stressors become extreme, it is of paramount importance that all participants in the financial planning and investing process have a clear understanding of what the long-term goals are, and what processes are in place to monitor the progress towards these goals.

Without these mechanisms it is very hard to resist the enormous pressure to follow the crowd; think social media and related influences.

Yield: For bonds and other fixed-income securities, yield is a rate of return on those securities. There are several types of yields and yield calculations. “Yield to maturity” is a common calculation for fixed-income securities, which takes into account total annual interest payments, the purchase price, the redemption value, and the amount of time remaining until maturity.

Yield curve: A line graph showing the yields of fixed income securities from a single sector (such as Treasuries or municipals), but from a range of different maturities (typically three months to 30 years), at a single point in time (often at month-, quarter- or year-end). Maturities are plotted on the x-axis of the graph, and yields are plotted on the y-axis. The resulting line is a key bond market benchmark and a leading economic indicator.

Yield to maturity [real yield to maturity]: Yield to maturity is a common performance calculation for fixed-income securities, which takes into account total annual interest payments, the purchase price, the redemption value, and the amount of time remaining until maturity. Real yield to maturity is simply yield to maturity minus any “inflation premium” that had been added/priced in. (See Real yield.)

Yield ratio: A ratio of one yield divided by another. Most often used as a relative value measurement.

Yield spread: A “spread,” in fixed income parlance, is simply a difference. Yield spreads measure yield differences, typically between debt securities with high credit ratings (which typically have lower yields) and those with lower ratings (which typically have higher yields). Yield spreads can also be measured between debt securities with different maturities (shorter-maturity securities typically have lower yields and longer-maturity securities typically have higher yields).

Yield trap: An investment that can lure investors with an attractive yield that may not be fundamentally sustainable, or that may lead to undesired price volatility. Yield traps can lurk in both the equity and fixed income markets. They have a tendency to prey on those who can least afford them, including retirement investors looking for increased relative income and stability, who may have been too focused on their income goals and not enough on stability.

Posted on November 13, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The operator of the longest-running money laundering machine in dark web history, Bitcoin Fog, has been sentenced to 12 years and six months in US prison. Roman Sterlingov, 36, a Russian-Swedish national, was also ordered to repay more than half a billion dollars accrued from the cryptocurrency mixing service that he ran for a decade between 2011 and 2021.

r Elliott Investment Management is at it again, this time with a $5 billion stake in industrial conglomerate Honeywell. Shares gained 3.87% on the news.

Shopify announced its ninth consecutive quarter of beating analyst revenue expectations, pushing shares up 21.04%.

Bad news is good news: 40% of the workforce at 23andMe is getting laid off to cut costs. Shareholders cheered, and shares climbed 2.17%.

Where’s the beef? Tyson Foods popped 6.55% after announcing strong earnings thanks to higher beef and chicken prices last quarter.

Sentinel One climbed 2.01% after Deutsche Bank analysts upgraded the cybersecurity stock from “hold” to “buy,” noting it should profit from CrowdStrike’s outage earlier this year.

Holding company IAC is considering a spinoff of home improvement services platform Angi (formerly Angie’s List). Nobody liked that: Shares of IAC fell 12.56%, and Angi plummeted 26.34%.

Payments processor Shift4 Payments sank 5.69% after crushing revenue expectations but missing on earnings.

Mosaic dropped 7.74% thanks to Hurricane Milton, which disrupted the fertilizer company’s business across the board.

The S&P 500® index (SPX) fell 17.36 points (–0.29%) to 5,983.99; the Dow Jones Industrial Average® ($DJI) lost 382.15 points (–0.86%) to 43,910.98; and the NASDAQ Composite®($COMP) decreased 17.36 points (–0.09%) to 19,281.40.

The 10-year Treasury note yield added 12 basis points to 4.43%.

The CBOE Volatility Index® (VIX) fell to 14.81, unusual on a day when stocks lost ground.

Posted on November 12, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Doctors, Facing Another Pay Cut, Call for Permanent Medicare Payment Reform

The Centers for Medicare and Medicaid Services (CMS) is moving forward with a 2.9% cut to physician payments in 2025 despite protest from major industry groups. CMS has finalized the calendar year 2025 Medicare Physician Fee Schedule rule that sets payment rates for next year and also outlines new policies focused on primary care, preserved telehealth flexibilities, and a strengthened Medicare Shared Savings Program (MSSP).

But, provider groups were quick to condemn CMS’ decision to go ahead with the pay cut, which was proposed in the draft rule released in July. In a statement, Bruce Scott, MD, president of the American Medical Association (AMA), pointed out that that while physicians are receiving a 2.8% payment cut next year, medical practice costs for physicians will increase by 3.5% in 2025. After adjusted for inflation, Medicare reimbursement to physicians has decreased 29% since 2001, the AMA says.

According to Wikipedia, a fundamental tenet of the paradox is that the customer, i.e. the potential purchaser of the information describing a technology (or other information having some value, such as facts), wants to know the technology and what it does in sufficient detail as to understand its capabilities or have information about the facts or products to decide whether or not to buy it. Once the customer has this detailed knowledge, however, the seller has in effect transferred the technology to the customer without any compensation. This has been argued to show the need for patent protection [HIPPA].

If the buyer trusts the seller or is protected via contract, then they only need to know the results that the technology will provide, along with any caveats for its usage in a given context. A problem is that sellers lie, they may be mistaken, one or both sides overlook side consequences for usage in a given context, or some unknown-unknown affects the actual outcome.

Stocks surged and stayed higher all yesterday day on news of Donald Trump’s presidential victory. The Dow rocketed over 1,350 points as soon as markets opened, and all three indexes ended the day at record highs.

Treasuryyields have paralleled Trump’s chances of taking the White House for the last few weeks, and his election sent them soaring to over 4.46% at one point today.

Oil and gold both fell as the dollar rose after Trump’s win. The greenback popped on the promise of Trump’s protectionist tariff policies and the lower likelihood of the Fed cutting interest rates as fast as previously expected.

Bitcoin surged as traders celebrated the beginning of the new, friendlier regulatory environment that Trump promised during his campaign.

Classic: Investment purchases and private expenditures of healthcare firms, the value of related construction, and the change in inventory during the year.

Modern: Gross Revenue Per Day is the average amount charged by a hospital for one day of inpatient care (gross inpatient revenue divided by patient-census days).

Gross Revenue Per Discharge: The average amount charged by a hospital to treat an inpatient from admission to discharge (gross inpatient revenue divided by discharges).

Gross Revenue Per Visit: The average amount charged by a hospital for an outpatient visit (gross outpatient revenue divided by outpatient visits).

HFRI: Fund of Funds invests with multiple managers through funds or managed accounts. The strategy designs a diversified portfolio of managers with the objective of significantly lowering the risk (volatility) of investing with an individual manager.

The Fund of Funds manager may allocate funds to numerous managers within a single strategy, or with numerous managers in multiple strategies. The investor has the advantage of diversification among managers and styles with significantly less capital than investing with separate managers.

Posted on November 3, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

Two recent court actions may serve as harbingers for the future of healthcare fraud and abuse laws. In September 2024, a federal judge in the Southern District of West Virginia ordered parties in a qui tamFalse Claims Act and Stark Law case to brief the court on the implications of Loper Bright Enterprises v. Raimondo on the interpretation of the Stark Law to the case at hand.

That same month, a federal judge in the Middle District of Florida dismissed a qui tam lawsuit on a novel theory that the False Claims Act’s whistleblower provisions are unconstitutional.

This Health Capital Topics article discusses these cases and the potential impact on federal fraud and abuse laws. (Read more…)

In-network refers to a health care provider that has a contract with your health plan to provide health care services to its plan members at a pre-negotiated rate. Because of this relationship, you pay a lower cost-sharing when you receive services from an in-network doctor.

What does out-of-network mean?

Out-of-network refers to a health care provider who does not have a contract with your health insurance plan. If you use an out-of-network provider, health care services could cost more since the provider doesn’t have a pre-negotiated rate with your health plan. Or, depending on your health plan, the health care services may not be covered at all.

Classic: Any medical provider, supplier or facility that is in-network is one that has contracted with your health insurer to provide services;as above.

Modern: Depending on your plan, if you visit an out-of-network provider, it may not be covered or might be only partially covered. When making appointments with various doctors and service providers, you may notice some are listed as “in-network” while others are “out-of-network.”

THINK: Medicare Advantage {Part C] Plans

Example: You can expect a higher deductible and out-of-pocket limit at out-of-network providers. Your coinsurance and co-payment may also be higher for out-of-network providers.

Classic Definition: Employers write checks that cover most health insurance premiums for employees and their dependents. But as the late Princeton health economist Uwe Reinhardt PhD once explained, employer-sponsored insurance is like a pickpocket taking money out of your wallet at a bar and buying you a drink. You appreciate the cocktail until you realize you paid for it yourself.

Modern Circumstance: With health coverage, employers write the check to the insurer, but employees bear the cost of the premium — the entire premium, not just the portion listed as their contribution on their pay stub. The premium money that goes to the insurance company is cash that employers would otherwise deposit in employees’ accounts like the rest of their salary.

Paradox Example: The fallacy paradox is in thinking an employer’s contribution comes out of profits. In fact, higher health insurance premiums mean lower wages for workers. Since 1999, health insurance premiums have increased 147 percent and employer profits have increased 148 percent. But in that time, average wages have hardly moved, increasing just 7 percent. Clearly workers’ wages, not corporate profits, have been paying for higher health insurance premiums. Health care costs are one — though not the only — reason wages have stagnated over the last few decades. With health insurance costs rising faster than growth in the economy, more labor costs go to benefits like health insurance and less to take-home pay. Yet the paradox that employees don’t pay for their own health insurance is widespread:

The first reason is that individuals cannot be sure what causes their wages to change or remain stagnant for decades.

The second reason is that employers want Americans to believe that they pay for their workers’ health insurance.

The third reason is that there are those who profit from the employment-based system: drug companies, device manufacturers, specialty physicians and high-income individuals.

And so, they all want you to believe companies are being magnanimous in giving you insurance, but they are not!

What Is CREDIT? Credit is a contractual agreement in which a borrower receives a sum of money or something else of value and commits to repaying the lender later, typically with interest. Credit is also the creditworthiness or credit history of an individual or a company. Good credit tells lenders you have a history of reliably repaying what you owe on loans. Establishing good credit is essential to getting a loan.

***

Credit Analysis is a form of financial analysis used primarily to determine the financial strength of the issuer of a security, and the ability of that issuer to provide timely payment of interest and principal to investors in the issuer’s debt securities. Credit analysis is typically an important component of security analysis and selection in credit-sensitive bond sectors such as the corporate bond market and the municipal bond market.

Credit Default Swap Index (CDX) is a credit derivative, based on a basket of CDS, which can be used to hedge credit risk or speculate on changes in credit quality.

Credit Default Swaps (CDS) are credit derivative contracts between two counter parties that can be used to hedge credit risk or speculate on changes in the credit quality of a corporation or government entity.

Credit Quality reflects the financial strength of the issuer of a security, and the ability of that issuer to provide timely payment of interest and principal to investors in the issuer’s securities. Common measurements of credit quality include the credit ratings provided by credit rating agencies such as Standard & Poor’s and Moody’s. Credit quality and credit quality perceptions are a key component of the daily market pricing of fixed-income securities, along with maturity, inflation expectations and interest rate levels.

Credit Rating Agency (CRA) is a company that assigns credit ratings for issuers of certain types of debt obligations as well as the debt instruments themselves. In the United States, the Securities and Exchange Commission (SEC) permits investment banks and broker-dealers to use credit ratings from “Nationally Recognized Statistical Rating Organizations” (NRSRO) for similar purposes. As of January 2012, nine organizations were designated as NRSROs, including the “Big Three” which are Standard and Poor’s, Moody’s Investor Services and Fitch Ratings.

A Credit Rating Downgrade by a credit rating agency (such as Standard & Poor’s, Moody’s or Fitch), of reducing its credit rating for a debt issuer and/or security. This is based on the agency’s evaluation, indicating, to the agency, a decline in the issuer’s financial stability, increasing the possibility of default (defined below). A downgrade should not to be confused with a default; a debt security can be downgraded without defaulting. (And, conversely, a debt issuer can suddenly default without being downgraded first–credit ratings and credit rating agencies are not infallible.)

Credit Ratings are measurements of credit quality provided by credit rating agencies). Those provided by Standard & Poor’s typically are the most widely quoted and distributed, and range from AAA (highest quality; perceived as least likely to default) down to D (in default). Securities and issuers rated AAA to BBB are considered/perceived to be “investment-grade”; those below BBB are considered/perceived to be non-investment-grade or more speculative.

Credit Risk is the risk that the inability or perceived inability of the issuers of debt securities to make interest and principal payments will cause the value of those securities to decrease. Changes in the credit ratings of debt securities could have a similar effect.

Credit Risk Transfer Securities (CRTS) are the unsecured obligations of the GSEs (Government Sponsored Enterprises). Although cash flows are linked to prepays and defaults of the reference mortgage loans, the securities are unsecured loans, backed by general credit rather than by specified assets.

Investors waited for the Magnificent 7 stock reports to begin rolling last evening. The NASDAQ rose to a new high on optimism while the Dow Jones fell, and the S&P 500 split the difference.

Alphabet announced earnings after the bell yesterday, Microsoft and MetaPlatforms reveal their latest quarters today, Amazon and Apple on Thursday afternoon.

The 10-year Treasury yield hit a 4-month high this afternoon before paring back a bit as traders struggle to find a signal in all the market noise.

Oil rebounded a bit from yesterday’s terrible day, though it still ended the trading session lower.

Posted on October 28, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Peak earnings season: Five of the Magnificent SevenStocks will be among the 181 companies reporting their earnings this week. Alphabet is in the Mag Seven lead-off spot on Tuesday, Microsoft and Meta step to the plate on Wednesday, and Apple and Amazon rounding out the lineup and this baseball metaphor on Thursday. These companies account for almost 25% of the S&P 500, which is up 40% over the past year and not far off its record closing number from earlier this month. But, the approaching election, it could be a volatile week in the stock markets.

***

Markets: Stocks are currently driving the narrative on Wall Street. Last week, bonds sold off in a big way (driving yields to their highest level since July) in a sign investors are dialing back expectations of more aggressive rate cuts from the Federal Reserve.

Stocks nevertheless handled the bond volatility with aplomb, and with help from Tesla’s 22% one-day rise, the NASDAQ is sitting within 2% of its record high.

It’s good to have money stashed in the stock market when the market is doing well. The number of people with at least $1 million in their 401(k) and IRA accounts jumped 12% in the second quarter 2024, according to a report from Fidelity Investments, largely tracking the market’s gain during that period. It’s the third straight quarter of growth in $1+ million accounts and close to a record high.

But start saving now, because building a hard-boiled nest egg through retirement accounts takes time: The average age of a 401(k) millionaire is 59, Fidelity said.

Posted on October 25, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By: Christian Hernandez MBA – Apple Health Care Services

Richard Melnyck MBA MS

Mark Friedman PhD Department of Accounting

Howard Gitlow PhD Department of Management Science University Miami

***

BACKGROUND

***

Homecare has long been one the most cost-effective methods of treating patients. Yet today, homecare providers face significant challenges: reimbursement cuts, mandatory accreditation, and influencing policy changes. So, how can homecare managers efficiently sustain a cutting edge, consistent and quality focused practice amidst this changing landscape?

***

It is time the homecare industry tap into the high-tech tools and proven management theories that together make up “Six sigma” management. This article will provide a solid point of reference for managers interested in adopting “Six Sigma” management. In today’s stiff economic climate, organizations are once again turning to “Six Sigma”strategies as a means to reduce their bottom lines.

***

However, its cost cutting aspect is technically more of a by product than the core of its theory. “Six Sigma” management is practiced in many organizations across all sectors of the global economy. Companies such as drug giant Merck, Cadbury, and Dunkin’ Brands are increasingly turning to Six Sigma to lift their bottom lines.

***

The term “Lean Management” is an old buzz word that still excites managers. Lean Management stems from the term Lean Manufacturing, which was a derivative of Total Quality Management (TQM) —considered one of the earlier versions of “Six Sigma”.

***

Over the years, “Six Sigma” has evolved from a ground-breaking management system to one of the most proven methods for instituting change, reducing errors and eliminating inefficiencies. These management utilities run through the entire spectrum of organizational applications, from confronting the serious issues mentioned above to routine business functions.

***

The resurgence of Japan’s economy in the 70’s and 80’s is largely attributed to TQM. “In the auto industry, manufacturers such as Toyota and Honda became major players. In the consumer goods market, companies such as Toshiba and Sony led the way. These foreign competitors were producing lower-priced products with considerably higher quality.”

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

A young clinician representative advising to consider the cost versus value of medicine. Health care concept for economic cost-effectiveness analysis, driving down medical costs, improved access.

***

Value Based CareClassic Definition: Value-based care is a type of payment model that pays doctors and hospitals for treating patients in the right place, at the right time and with just the right amount of care. You can look at it as a financial incentive to motivate healthcare providers to meet specific performance measures related to the quality and efficiency of the process. The same way, it penalizes weaker experiences, such as medical errors. The concept is often counter-intuitive.

Modern Circumstance: As healthcare costs continue to rise, value-based care has been growing in popularity compared to the traditional fee-for-service method.

Think: HMOs, PPOs, capitation payments and Medicare Advantage [Part C].

Paradox Examples:

Payment: A physician paid through fee-for-service compensation might like to see a packed medical office waiting room. More patients and services equate to higher pay. But, the same doctor paid through a VBC contract might wish to see an emptier waiting room as s/he will get the exact same daily pay for seeing fewer patients and working much less.

Prospectivity: Traditional Fee-for-Service medicine treats sick patients. VBC medicine seeks to keep patients healthy and out of the doctor’s office.

Posted on October 23, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The IRS has announced the annual inflation adjustments for the year 2025, including tax rate schedules, tax tables and cost-of-living adjustments. These are the official numbers for the tax year 2025—that tax year begins January 1, 2025. These are not the numbers that you’ll use to prepare your 2024 tax returns in 2025 (you’ll find those official 2024 tax numbers here). These are the numbers that you’ll use to prepare your 2025 tax returns in 2026.

Trump Media & Technology Group rose 9.87% to its highest level since July as the “Trump trade” wagering on the former president to regain the White House picks up steam.

Quest Diagnostics isn’t just a sad, windowless building where you get your blood drawn—it’s also been a pretty profitable investment. Shares rose 6.88% on strong earnings and revenue growth.

STOCKS DOWN

Stop us if you’ve heard this one before: Target is cutting the price of 2,000 products ahead of the holiday season. Shares sank 1.13% as shareholders digest what appears to be a desperate move to boost sales.

Verizon Communications dropped 5.03% after missing on both revenue and earnings estimates. But the real problem was slowing customer growth and phone sales.

Defense contractors were in the earnings spotlight today, and none of them did well. GE Aerospace tumbled 9.07% despite beating analyst forecasts and Lockheed Martin fell 6.12% after sales missed estimates.

Genuine Parts, better known as NAPA Auto Parts, plummeted 20.96% after earnings missed estimates and the company announced lower fiscal year forecasts.

The SPX fell 2.78 points (–0.05%) to 5,851.20; the Dow Jones Industrial Average® ($DJI) lost 6.71 points (–0.02%) to 42,924.89; and the $COMP gained 33.12 points (0.18%) to 18,573.13.

The 10-year Treasury note yield (TNX) added two basis points to 4.2%.

The CBOE Volatility Index® (VIX) fell to 18.15, down from above 20 a week ago.

Although some might view a budget as unnecessarily restrictive, sticking to a spending plan can be a useful tool in enhancing the wealth of a medical practice. So, I will emphasize keys to smart budgeting and how to track spending and savings in these tough economic times.

There is an aphorism that suggests, “Money cannot buy happiness.” Well, this may be true enough but there is also a corollary that states, “Having a little sure reduces the unhappiness.”

Unfortunately, today there is more than a little financial unhappiness in all medical specialties. The challenges range from the commoditization of medicine, aging demographics, Medicare reimbursement cutbacks and increased competition to floundering equity markets, the home mortgage crisis, the squeeze on credit and declines in the value of a practice. Few doctors seem immune to this “perfect storm” of economic woes.

Far too many physicians are hurting and it is not limited to above-average earning professionals. However, one can strive to reduce the pain by following some basic budgeting principles. By adhering to these principles, physicians can eliminate the “too many days at the end of the month” syndrome and instead develop a foundation for building real wealth and security, even in difficult economic climates like we face today.

There are three major budget types. A flexible budget is an expenditure cap that adjusts for changes in the volume of expense items. A fixed budget does not. Advancing to the next level of rigor, a zero-based budget starts with essential expenses and adds items until the money is gone. Regardless of type, budgets can be extremely effective if one uses them at home or the office in order to spot money troubles before they develop.

For the purpose of wealth building, doctors may think of this budget as a quantitative expression of an action plan. It is an integral part of the overall cost-control process for the individual, his or her family unit or one’s medical practice.

Preparing a net income statement (lifestyle cash flow budget) is often difficult because many doctors perceive it as punitive. Most doctors do not live a disciplined spending lifestyle and they view a budget as a compromise to it. However, a cash flow budget is designed to provide comfort when there is surplus income that can be diverted for other future needs. For example, if you treat retirement savings as just another periodic bill, you are more likely to save for it.

You may construct a personal cash budget by recording each cash receipt and cash disbursement on a spreadsheet. Only the date, amount and a brief description of the transaction are necessary. The cash budget is a simple tool that even doctors who lack accounting acumen can use. Since it is possible to track the cash-in and cash-out in the same format used for a standard check register, most doctors find that the process takes very little time. Such a budget will provide a helpful look at how well you are staying within available resources for a given period.

We then continue with an analysis of your operating checkbook and a review of various source documents such as one’s tax return, credit card statements, pay stubs and insurance policies. A typical statement will show all cash transactions that occur within one year. It is helpful to establish a monthly equivalent to all items of income and expense. For the purposes of getting started, note items of income and expense by the frequency you are accustomed to receiving or spending them.

What You Should Know About The ‘Action Plan’ Cash Budget

For a medical office, the first operations budget item might be salary for the doctor and staff. Operating assets and other big ticket items come next. Some of our doctors/clients review their office P&L statements monthly, line by line, in an effort to reduce expenses. Then they add back those discretionary business expenses they have some control over.

Now, do you still run out of money before the end of the month? If so, you had better cut back on entertainment, eating dinner out or that fancy, new but unproven piece of medical equipment. This sounds draconian until you remind yourself that your choice is either: live frugally later or live a simpler lifestyle now and invest the difference.

As a young doctor, it may be a difficult trade-off. By mid-life, however, you are staring retirement in the face. That is why the action plan depends on your actions concerning monetary scarcity, a plan that one can implement and measure using simple benchmarks or budgeting ratios. By using these statistics, perhaps on an annual basis, the doctor can spot problems, correct them and continue planning actively toward stated goals like building long-term wealth.

Useful Calculations To Assess Your Budgeting Success

In the past, generic budgeting ratios would emphasize not spending more than 15 to 20 percent of your net salary on food or 8 percent on medical care. Now these estimates have given way to more rigorous numbers. Personal budget ratios, much like medical practice financial ratios, represent comparable benchmarks for parameters such as debt, income growth and net worth. Although these ratios are still broad, the following represent some useful personal budgeting ratios for physicians.

• Basic liquidity ratio = liquid assets / average monthly expenses. Cash-on-hand should approach 12 to 24 months or more in the case of a doctor employed by a financially insecure HMO or fragile medical group practice. Yes, chances are you have heard of the standard notion of setting enough cash aside to cover three months in a rainy day scenario. However, we have decried this older laymen standard for many years in our textbooks, white papers and speaking engagements as being wholly insufficient for the competitively unstable environment of modern healthcare.

• Debt to assets ratio = total debt / total assets. This percentage is high initially but should decrease with age as the doctor approaches a debt-free existence

• Debt to gross income ratio = annual debt repayments / annual gross income. This represents the adequacy of current income for existing debt repayments. Doctors should try to keep this below 20 to 25 percent.

• Debt service ratio = annual debt repayment / annual take-home pay. Physicians should aim to keep this ratio below 25 to 30 percent or face difficulty paying down debt.

• Investment assets to net worth ratio = investment assets / net worth. This budget ratio should increase over time as retirement approaches.

• Savings to income ratio = savings / annual income. This ratio should also increase over time as one retires major obligations like medical school debt, a practice loan or a home mortgage.

• Real growth ratio = (income this year – income last year) / (income last year – inflation rate). This budget ratio should grow faster than the core rate of inflation.

• Growth of net worth ratio = (net worth this year – net worth last year) / net worth last year – inflation rate). Again, this budgeting ratio should stay ahead of inflation.

In other words, these ratios will help answer the question: “How am I doing?”

Pearls For Sticking To A Budget

Far from the burden that most doctors consider it to be, budgeting in one form or another is probably one of the greatest tools for building wealth. However, it is also one of the greatest weaknesses among physicians who tend to live a certain lifestyle.

In fact, we have found that less than one in 10 medical professionals have a personal budget. Fear, or a lack of knowledge, is a major cause of procrastination. Fortunately, the following guidelines assist in reversing this microeconomic disaster.

1. Set reasonable goals and estimate annual income. Do not keep large amounts of cash at home or office. Deposit it in an FDIC insured money-market account for safety. Do not deposit it in a money market mutual fund with net asset value (NAV) that may “break the buck” and fall below the one-dollar level. Track actual bills and expenses.

2. Do not pay bills early, do not have more taxes withheld from your salary than needed and develop spending estimates to pay fixed expenses first. Fixed expenses are usually contractual and usually include housing, utilities, food, Social Security, medical, debt repayments, homeowner’s or renter’s insurance, auto, life and disability insurance, etc. Reduce fixed expenses when possible. Ultimately, all expenses get paid and become variable in the long run.

3. Make it a priority to reduce variable expenses. Variable expenses are not contractual and may include clothing, education, recreational, travel, vacation, gas, cable TV, entertainment, gifts, furnishings, savings, investments, etc. Trim variable expenses by 5 to 20 percent.

4. Use “carve-outs or “set-asides” for big ticket items and differentiate true wants from frivolous needs.

5. Calculate both income and expenses as a percentage of your total budget. Determine if there is a better way to allocate resources. Review the budget on a monthly basis to notice any variance. Determine if the variance was avoidable, unavoidable or a result of inaccurate assumptions. Take corrective action as needed.

6. Know the difference between saving and investing. Savers tend to be risk adverse while investors understand risk and take steps to mitigate it. Watch mutual fund commissions and investment advisory fees, which cut into return-rates. Keep investments simple and diversified (stocks, bonds, cash, index, no-load mutual and exchange traded funds, etc.).

Sooner or later, despite the best of budgeting intentions, something will go awry. A doctor will be terminated or may be the victim of a reduction-in-force (RIF) because of cost containment initiatives.4 A medical practice partnership may dissolve or a local hospital or surgery center may close, hurting your practice and livelihood. Someone may file a malpractice lawsuit against you, a working spouse may be laid off or you may get divorced. Regardless of the cause, budgeting crisis management encompasses two different perspectives: awareness and execution.

First, if you become aware that you may lose your job, the following proactive steps will be helpful to your budget and overall financial condition.

• Decrease retirement contributions to the required minimum for company/practice match. • Place retirement contribution differences in an after-tax emergency fund. • Eliminate unnecessary payroll deductions and deposit the difference to cash. • Replace group term life insurance with personal term or universal life insurance. • Take your old group term life insurance policy with you if possible. • Establish a home equity line of credit to verify employment. • Borrow against your pension plan only as a last resort.

If you have lost your job or your salary has been depressed, negotiate your departure and get an attorney if you believe you lost your position through breach of contract or discrimination. Then execute the following steps to recalculate your budget and boost your wealth rebuilding activities.

• Prioritize fixed monthly bills in the following order: rent or mortgage; car payments; utility bills; minimum credit card payments; and restructured long-term debt.

• Consider liquidating assets to pay off debts in this order: emergency fund, checking accounts, investment accounts or assets held in your children’s names.

• Review insurance coverage and increase deductibles on homeowner’s and automobile insurance for needed cash.

• Then sell appreciated stocks or mutual funds; personal valuables such as furnishings, jewelry and real estate; and finally, assets not in pension or annuities if necessary.

• Keep or rollover any lump sum pension or savings plan distribution directly to a similar savings plan at your new employer, if possible, when you get rehired.

• Apply for unemployment insurance.

• Review your medical insurance and COBRA coverage after a “qualifying event” such as job loss, firing or even after quitting. It is a bit expensive due to a 2 percent administrative fee surcharge but this may be well worth it for those with preexisting conditions or who are otherwise difficult to insure. One may continue COBRA for up to 18 months.

• Consider a high deductible Health Savings Account (HSA), which allows tax-deferred dollars like a medical IRA, for a variety of costs not normally covered under traditional heath insurance plans. Self-employed doctors deduct both the cost of the premiums and the amount contributed to the HSA. Unused funds roll over until the age of 59½, when one can use the money as a supplemental retirement benefit.

• Eliminate unnecessary variable, charitable and/or discretionary expenses, and become very frugal.

Final Notes

The behavioral psychologist, Gene Schmuckler, PhD, MBA, sometimes asks exasperated doctors to recall the story of the old man who spent a day watching his physician son treating HMO patients in the office. The doctor had been working at his usual feverish pace all morning. Although he was working hard, he bitterly complained to his dad that he was not making as much money as he used to make. Finally, the old man interrupted him and said, “Son, why don’t you just treat the sick patients?” The doctor-son looked at his father with an annoyed expression and responded, “Dad, can’t you see, I do not have time to treat just the sick ones.”

Always remember to add a bit of emotional sanity into your budgeting and economic endeavors.

Regardless of one’s age or lifestyle, the insightful doctor realizes that it is never too late to take control of a lost financial destiny through prudent wealth building activities. Personal and practice budgeting is always a good way to start the journey.

NOTE: Dr. Marcinko is a former Certified Financial Planner and current Certified Medical Planner™. He has been a medical management advisor for more than a decade. He is the CEO of http://www.MarcinkoAssociates.com

The authors acknowledge the assistance of Mackenzie H. Marcinko PhD in the preparation of this article.

The science of the modern medical practice valuation can be traced to the Estate of Edgar A. Berg v. Commissioner (T. C. Memo 1991-279). In this case, the Court criticized CPAs as not being qualified to perform business valuations, failing to provide analysis of an appropriate discount rates, and making only general references to justify their “Opinion of Value.”

In rejecting accountants, the Court accepted IRS economists because of background, education and training, as well as discount rate calculations and reproducible evidence applied to the assets being examined. This marked the beginning of the Tax Court leaning toward the side with the most comprehensive appraisal. Previously, it had a tendency to “split the difference.” Now, some feel the Berg case launched the valuation profession; especially for contemporaneous health economists.

But, it was not until after 1995 that the IRS issued guidelines for the valuation of physician practices. As a result, the Uniform Standards of Professional Appraisal Practice [USPAP] requires that a blended constellation of three recognized valuation approaches (income, market, and cost approaches) be considered when estimating fair market value.

Operative Valuation Definitions

When pursuing any discussion of medical practice worth, two key elements must be understood: (1) the valuation process, and (2) fair market value. According to the Dictionary of Health Economics and Finance

Practice valuation is the “the formal process of determining the worth of a healthcare or other medical business entity, at a specific point in time, and the act or process of determining fair market value.”

Fair market value [FMV] is “a legal term generally meaning the price at which a willing buyer will buy, and a willing seller will sell an asset in an open free market with full disclosure.” IRS Revenue Ruling 59-60 clearly states that FMV “is essentially a future prophesy and must be based on facts available at the required date of appraisal”

Unfortunately, the value of a medical practice cannot be directly observed by activity in thinly traded private markets. Perhaps this is why we continually observe the following valuation blunders? They are committed by both sellers and buyers who are pursuing opposite objectives; sale price maximization versus price minimization?

Top 10 Blunders:

Not Understanding What a Medical Practice Valuation Is and Is Not

Valuations are not source document fraud audits.

Valuations are material representations providing a range of transferable worth.

Valuations are reproducible estimates based on economic assumptions.

Valuations are not “back-of-the envelope multiples” using specious benchmarks.

Valuations are defensible and “signed-off” attesting to USPAP/IRS formats.

Financial accounting value [book-value] is not fair market value.

Professional valuators represent only one party at arm’s length; not both sides.

Engagement solicitor and/or valuation payer is the client.

Unbiased valuators do not provide financing or equity-participation schemes. Although not standardized, the Institute of Medical Business Advisors, Inc uses the following three levels that approximate engagement types for the industry.

2. A Limited Valuation lacks additional suggested USPAP procedures. It is considered an “agreed-upon-procedure”, used in circumstances where the client is the only user [i.e., updating a buy-sell agreement, or practice buy-in for a valued associate] and not for external purposes. No onsite visit is needed. A formal Opinion of Value is not rendered.

3. Not Observing Industry Standards, Rules and Regulations

Specifically, in USPAP transactions involving physician practices, the IRS implied:

Ad-Hoc Valuation is low level engagement that provides a gross and non-specific approximation of value based on limited meters by involved parties. Neither a written report, nor an Opinion of Value is rendered. It is often used periodically as an internal organic growth / decline gauge.

A Comprehensive Valuation is an extensive service designed to provide an unambiguous Opinion of Value range. It is supported by all procedures that valuators deem relevant with mandatory onsite review. This “gold-standard” is suitable for contentious situations like divorce, partnership dissolution, estate planning and gifting, etc. The written Opinion of Value is applicable for litigation support activities like depositions and trial. It is also useful for external reporting to bankers, investors, the public and IRS, etc.

4. Not Understanding Engagement Types and Levels

Discounted cash flow (DCF) analysis is the most relevant income approach and must be done on an “after-tax” basis.

Practice collections must be projected based on reasonable assumptions for the practice and market; etc.

Physician compensation must be based on market rates consistent with age, experience and productivity.

Majority premiums and minority discounts are to be considered.Goodwill represents the difference between practice purchase price and the value of the net assets. Personal goodwill results from the charisma, skills and reputation of a specific doctor. Its attributes accrue solely to the individual, are not transferable and can’t be sold. It has little or no economic value as it “goes to the grave” with the doctor. Transferable medical practice goodwill has value, may be transferred, and is defined as the unidentified residual attributes that contribute to the propensity of patients and managed care contracts (and their revenue streams) to return in the future (Schilbach v. Commissioner, T.C. Memo 1991-556). And so, one must also appreciate the: (i) impact of a changing environment; (ii) practice transfer in a local market which can augment or blunt goodwill value; and the (iii) determination of whether patients or HMOs return because of true goodwill, or are mandated by contractual obligations; among many other multi-variable determinants.

Even the Goodwill Registry however, a classic source used to determine the average percentage of revenue contributed to practice goodwill, may be dated for some specialties leading to abnormally high values.

5. Not Understanding the Value of Practice Goodwill: Unlimited life span.

6. Not Understanding the Value of Personal Goodwill: Limited life span.

Now, to further confuse the issue, how each kind of goodwill is allocated in situations like divorce depends on state law. For example, some courts include both kinds of goodwill to be apportioned – some exclude both – and others pursue a case-by-case approach.

7. Not Understanding “Excess Earnings Capitalization”

Another way to determine goodwill value is through “excess earnings capitalization.” This economic method looks at the difference between salary, and what you’d have to pay a comparable doctor replacement.

As an example, when you subtract the numbers, and divide the result by 20%, an important percentage referred to as the Capitalization Rate emerges. The final number gives a dollar value for practice goodwill. Courts seem to prefer this method in divorces because it tends to reflect a practice’s current value.

8. Not Understanding the Present Compensation versus Future Value Paradox

Regardless of practice business model, physician compensation is inversely related to practice value. In other words, the more a doctor takes home in above-average salary, the less the practice is generally worth, and vice versa; ceteris paribus

9. Substituting Benchmarks and Formulas for Practice Specificity

In the stable economic past, industry benchmarks might have been used as quick and inexpensive substitutes for professionally prepared valuations. Muck like preparing one’s own income tax return today – while legal – it is a fraught with peril if challenged. The Courts seem to frown on this simplistic and dated methodology.

Moreover, generic benchmark formulas assume a financial statement reporting standard that just does not exist in public accounting.

Therefore, most every competitive issue that impacts value should be addressed with each practice engagement. This includes, but is not limited to contemporary dislocations by third parties, Medicare and commercial payers; retail clinics and changes in supply/demand and specialty trends; rise of ambulatory surgery centers and specialty hospitals; outsourced care and medical tourism, alterations in resource based-relative value units, APCs, DRGs and newer MS-DRGs; the Medicare Modernization Act, HIPAA, OSHA, EEOC, Sarbanes-Oxley and US Patriot Acts, PP-CA, and ACOs; among other regulations.

Current employee trends to high-deductible health care plans [HD-HCPs] and private concierge medicine must also be considered, as well as demographic and employer shifts to defined contribution plans – from defined benefits plans – to name just a few more complicating issues.

10. Not Aggregating or “Normalizing” Financial Information

Employees may be interviewed and financial information must be gathered before a medical practice can be properly valued. The following data, for the most recent three year period, serves as a starting point:

Sample medical record chart review is increasingly being demanded.

It is especially important to eliminate one-time, non-recurring practice expenses. These are adjusted for excessive or below normal expenses on the profit and loss statement. Such “normalization” can produce a big surprise for benchmark proponents and formula-driven advocates when a selling doctor runs personal expenditures through the practice that a buyer [or Court] wouldn’t consider legitimate. Of course, such shenanigans are less noted using professional USPAP/IRS guidelines. Conversely, you may have to defend legitimate business expenses that an appraiser may seek to normalize. For example, doctors may pay for a vehicle through their practice, but if used to travel between multiple offices and hospitals, the expense may be legitimate. Of course, normalization is a sophisticated and time-intensive process. But, it is where the expert earns his/her professional fee, and defends the resulting valuation range when challenged.The most important credential to look for is fiduciary experience, specificity and independence. Some doctors mistakenly turn to those who may have never appraised a practice before. And, just because an appraiser has initials behind his name, doesn’t mean he understands the peculiarities of medical specialties, especially podiatry. We believe that only an independent health economist, who will be your advocate under Securities Exchange Commission [SEC] fiduciary [not lower “suitability”] guidelines, should be selected. Of course, it is almost impossible to answer concerns regarding fees without specific information. The cost of a valuation can range from $0 (benchmarks-rule of thumb) to $50,000 for an onsite team of experts for behemoth practices and ambulatory surgery centers. Keep in mind that in most cases you want to ensure the value determination will stand up to IRS scrutiny, so the $0 rule-of-thumb is not an optionExternal appraisals, or poorly aggregated financial information, onsite reviews and litigation support services incur additional costs; yet most doctors find the money well spent. Expect to pay a retainer and sign a formal professional engagement letter.

Assessment

Don’t be surprised if a sales-broker does not consider the above issues as the modern health era emerges. Most agent-appraisers are predominantly concerned with earning commissions by working both transaction parties, and may not represent your best interests. And, they are usually not obliged to disclose conflicts-of-interest and don’t provide legal testimony.

As a result, a good medical practice is no longer necessarily a good business; and retiring doctors can no longer automatically expect to extract premium sales prices. Moreover, uninformed young physicians should not be goaded to over-pay. Regardless of your dismay – or delight – in the changing healthcare milieu, always be foreword thinking and remember the admonition, Trust-but Verify, for any business transaction.

But, it is a fait accompli that medical practice worth is presently deteriorating. As the population ages and third-party reimbursements plummet, doctors are commoditized and traditional retail medicine is replaced by more efficient wholesale business models like workplace health clinics. The recent sub-prime mortgage de-fault fiasco, potential tax-reform law expiration and the political specter of a nationalized healthcare system, only adds fuel to the macro-economic fires of uncertainly.

Finally, once practice price is mutually agreed upon, sales contract terms and agreements present a plethora of financing challenges for both involved parties to consider [bank loan payment rates and length, personal promissory guarantees, down-payment offsets, earn-out arrangements, Uniform Commercial Codes-1 asset guarantees, etc] in their due-diligence efforts.

However, most reputable firms use a blended fee-schedule of fixed and hourly rates (plus expenses). So, doctors should expect to spend approximately $5,000-15,000 for an average sized – limited appraisal – that is completely suitable for most internal activities.

Moreover, look-out if the valuation not done at an-arm’s-length and independent manner; or worse still, if it is performed for both parties simultaneously.

Selecting the Wrong Valuator and Not Understanding Professional Fees

Realize too, that the appraiser may also add expenses that have not been incurred; like an office manager’s salary if your spouse is in that role for free. This produces a lower appraised value and is common in small medical practices. Honoraria are another example that does not figure into value calculations.

For example, we recall one doctor who painted his personal residence and wrote it-off as a valid business expense. Deleting other major expenses such as country club memberships, make a practice look more profitable—good news if you’re selling it, bad news if you’re getting a divorce.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

Posted on October 12, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

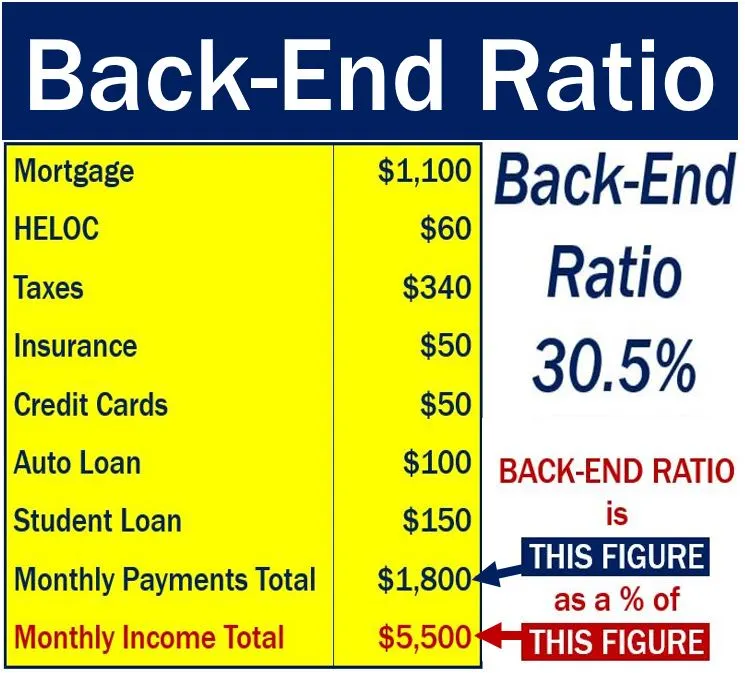

Back-End Ratio or Back Ratio

DEFINITION: The sum of your monthly mortgage payment and all other monthly debts (credit cards, car payments, student loans, etc.) divided by your monthly pre-tax income.

Traditionally, lenders wouldn’t give people loans that increased this ratio past 36%, but they often do now.

Posted on October 10, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Kamala Harris announced a plan to broaden Medicare to cover home healthcare for the first time in an effort to help the “sandwich generation” of Americans who are taking care of both their children and their parents.

WeightWatchers said it will offer cheaper copycat versions of Novo Nordisk’s weight loss drug, Wegovy.

Reddit gained 0.31% thanks to Jefferies analysts, who debuted their coverage of the social media stock with a “buy” rating, praising the company’s AI potential.

Biogen climbed 1.90% after the FDA gave its treatment for kidney transplant patients a special Breakthrough Therapy Designation.

Cruise stocks sailed higher today, in spite of the oncoming hurricane in the Gulf of Mexico. Norwegian Cruise Line, Carnival, and Royal Caribbean popped 10.91%, 7.05%, and 5.26%, respectively, on upgrades from Citi analysts.

Astera Labs jumped 15.60% after it debuted a new family of data center switches built specifically for AI.

Helen of Troy soared 17.88% thanks to a stronger-than-expected earnings report from the struggling consumer goods manufacturer.

Arcadium Lithium continued to rocket higher today after mining behemoth Rio Tinto announced it’s buying the lithium miner for $5.85 per share. Arcadium shares rose 30.90%.

Stocks down

Boeing just can’t catch a break: Talks with striking machinists broke down and the airplane manufacturer withdrew its recent contract offer. Shares sank 3.41% on the news.

US-traded shares of German life sciences company Bayer dropped 6.96% after a US court decided it will hear arguments that products from Bayer brand Monsanto allegedly harmed people.

Trump Media & Technology Group finally settled down after a wild rally following a wild rally in Pennsylvania featuring Elon Musk, falling 5.64% today.

The S&P 500® index (SPX) rose 40.91 points (0.71%) to 5,792.04, a new record-high close; the Dow Jones Industrial Average® ($DJI) added 431.63 points (1.03%) to 42,512.00, also a new closing high; and the NASDAQ Composite® ($COMP) increased 108.70 points (0.60%) to 18,291.62.

The 10-year Treasury note yield (TNX) climbed three basis points to 4.06%, the highest since late July.

In 2023, about 36% of Hispanic or Latino candidates waiting for a transplant received one, compared to 58% of non-Hispanic white candidates, according to the US Department of Health and Human Services Office of Minority Health.

Stat: $1.8 trillion. That eye-watering number is the federal budget deficit as of September 30th, according to the Congressional Budget Office. Higher interest rates, and increases in Social Security and Medicare, are driving the budget gap. (the Wall Street Journal)

Posted on October 9, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

ByNeal Baum MD

***

There’s a saying by John Wanamaker who pontificated, “Half the money I spend on advertising is wasted; the trouble is, I don’t know which half”.

Today you have opportunities to determine which parts of your marketing efforts are effective and what is wasted. However, you have to measure your marketing results.

This article will discuss marketing metrics and how to use them to get the best bang for your marketing buck.

***

***

The cost per acquisition (CPA)

Not all initial phone callers to a medical practice will convert to paying patients. The 50 patients who made appointments can be plugged into the equation, i.e., campaign costs divided by patients who became paying patients or $2,000 divided by 50 equals $40, representing the patient acquisition cost (PAC).

Now, if each patient who entered the practice spends $800 over the patient’s lifetime, that’s an increase in income of $40,000, not shabby for $2,000 in marketing expenses.

Source: Neil Baum, MD, Physicians Practice [8/26/22]

According to the Dupont Decomposition Equation – which involves the conglomeration of net operating income, revenues, expenses and average operating assets – ROI and economic profit is increased in three prioritized ways:

Cost and expense reductions.

Revenue increases [Rev]

Reduced average operating assets [AOO]

Note: ROI = NOI / Rev X Rev / AOO

Cost and expense reductions

Although many hospitals have reduced expenses, postponed projects and put clinical or information technology projects on hold because of the current healthcare conundrum, this may be unwise and quality may suffer. And, mental health care programs are almost always the first cost center to be reduced in tough times.