BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

The idea of a physician who is also an accountant might sound unusual at first, almost like two worlds that rarely intersect. One is rooted in diagnosing illnesses, understanding human physiology, and providing compassionate care. The other revolves around financial statements, regulatory compliance, and strategic fiscal planning. Yet when these two disciplines come together in a single professional, the result is a uniquely capable individual who can navigate both the complexities of modern healthcare and the equally intricate world of financial management. As healthcare systems grow more complicated and financially pressured, the combination of medical expertise and accounting acumen becomes not only valuable but transformative.

Physicians traditionally focus on clinical decision‑making, patient outcomes, and the ethical dimensions of care. Their training emphasizes scientific reasoning, empathy, and the ability to make high‑stakes decisions under uncertainty. Accountants, on the other hand, are trained to think in terms of precision, structure, and long‑term financial sustainability. They understand how organizations allocate resources, manage risk, and maintain compliance with regulatory frameworks. When one person embodies both sets of skills, they gain a rare vantage point: the ability to see how clinical decisions ripple through the financial health of a practice, hospital, or healthcare system.

One of the most significant advantages of this dual expertise is the ability to bridge the communication gap between clinicians and administrators. In many healthcare organizations, physicians and financial officers often struggle to fully understand each other’s priorities. Physicians may feel that financial constraints undermine their ability to provide optimal care, while administrators may worry that clinical decisions are made without regard for cost efficiency or long‑term sustainability. A physician‑accountant can translate between these two perspectives, helping each side understand the other’s reasoning. This can lead to more balanced decision‑making, where patient care remains central but financial realities are acknowledged and managed responsibly.

Another area where this combination shines is in private practice management. Running a medical practice is, at its core, running a business. Physicians who lack financial training often find themselves overwhelmed by budgeting, billing systems, tax obligations, and regulatory compliance. Mistakes in these areas can be costly, both financially and legally. A physician who is also an accountant is far better equipped to manage these responsibilities. They can design efficient billing workflows, interpret financial reports, and make informed decisions about staffing, equipment purchases, and long‑term investments. This not only strengthens the practice but also allows the physician to maintain greater autonomy and stability in an increasingly competitive healthcare landscape.

***

***

Beyond individual practices, physician‑accountants can play influential roles in healthcare policy and leadership. Healthcare spending is a major concern in many countries, and policymakers often struggle to balance cost control with quality of care. Professionals who understand both the clinical and financial dimensions of healthcare are uniquely positioned to contribute to policy development, hospital administration, and health‑system reform. They can evaluate the economic impact of clinical guidelines, assess the cost‑effectiveness of new technologies, and design reimbursement models that incentivize high‑quality care without creating unnecessary financial burdens.

The dual training also enhances ethical decision‑making. Financial pressures in healthcare can sometimes lead to conflicts of interest or difficult trade‑offs. A physician‑accountant is better prepared to navigate these dilemmas because they understand the financial implications without losing sight of the ethical obligations inherent in medical practice. They can advocate for solutions that protect patient welfare while ensuring that resources are used responsibly. This balanced perspective can help organizations avoid short‑sighted decisions that might compromise care or create long‑term financial instability.

Of course, becoming both a physician and an accountant requires an extraordinary level of dedication. Medical training alone demands years of study, residency, and ongoing professional development. Adding accounting education—whether through a degree, certification, or extensive coursework—requires additional time and effort. Yet for those who pursue this path, the rewards can be substantial. They gain a level of professional versatility that few others possess, and they can shape healthcare environments in ways that purely clinical or purely financial professionals cannot.

In a rapidly evolving healthcare landscape, the intersection of medicine and accounting is becoming increasingly relevant. Rising costs, complex insurance systems, and the growing emphasis on value‑based care all demand professionals who can think across traditional disciplinary boundaries. Physicians who are also accountants embody this interdisciplinary approach. They bring clarity to financial decisions, insight to clinical operations, and a holistic understanding of how healthcare systems function. Their unique skill set positions them as leaders who can help shape a more efficient, ethical, and sustainable future for healthcare.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on January 7, 2026 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

Tariffs on medicines and healthcare products increase costs, disrupt supply chains, and ultimately harm patient access and public health. They raise prices for essential drugs and medical devices, create shortages, and undermine innovation in the healthcare sector.

The Economic Burden of Tariffs

Tariffs are taxes imposed on imported goods. In healthcare, this means pharmaceuticals, medical devices, and raw materials like active pharmaceutical ingredients (APIs) become more expensive. Since the United States imports a significant share of these products from countries such as China, India, and the European Union, tariffs directly raise costs for hospitals, clinics, and patients.

Drug prices rise because manufacturers pass on higher import costs to consumers.

Medical devices such as surgical instruments, diagnostic equipment, and imaging technology become more expensive, straining hospital budgets.

Insurance premiums may increase as healthcare providers face higher operating costs.

This economic burden is not abstract—it translates into higher bills for patients and reduced affordability of care.

Supply Chain Disruptions

Healthcare supply chains are highly globalized. APIs, raw materials, and specialized equipment often come from multiple countries. Tariffs disrupt this delicate balance by:

Creating shortages when suppliers cannot afford to export to tariff-heavy markets.

Delaying shipments as companies seek alternative routes or suppliers.

Reducing resilience by concentrating production in fewer regions, making systems more vulnerable to shocks.

For example, if tariffs make APIs prohibitively expensive, pharmaceutical companies must scramble to find new suppliers, often at higher cost and with longer lead times. This can delay drug availability and compromise patient care.

***

***

Impact on Public Health

The consequences of tariffs extend beyond economics into public health outcomes.

Patients face reduced access to life-saving medicines and devices.

Hospitals may ration supplies, prioritizing urgent cases while delaying elective procedures.

Preventive care suffers, as higher costs discourage investment in vaccines, diagnostic tools, and routine screenings.

In the long run, tariffs can exacerbate health inequities, disproportionately affecting low-income populations who are least able to absorb rising costs.

Innovation and Research Setbacks

Healthcare innovation relies on global collaboration. Tariffs discourage cross-border partnerships by raising costs and creating uncertainty.

Research institutions may struggle to import specialized lab equipment.

Pharmaceutical companies face higher costs for clinical trials and drug development.

Digital health technologies that depend on imported components (like sensors and chips) become more expensive, slowing adoption.

This stifles progress in areas such as cancer treatment, biotechnology, and precision medicine.

Conclusion

Tariffs in healthcare are a blunt economic tool with unintended consequences. While they aim to protect domestic industries, they increase costs, disrupt supply chains, reduce access to care, and hinder innovation. In medicine and healthcare, where lives depend on timely and affordable access to products, tariffs are particularly damaging. Policymakers must weigh these human costs carefully before imposing trade barriers on essential goods.

Posted on January 6, 2026 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

Professor Eugene Schmuckler PhD MBA MEd CTS

***

***

Navigating the Challenges of Passive-Aggressive Patients in Healthcare

In the complex landscape of healthcare, effective communication between providers and patients is essential for accurate diagnosis, treatment adherence, and overall patient satisfaction. However, passive-aggressive behavior—characterized by indirect resistance, subtle obstruction, and veiled hostility—can significantly hinder this process. Passive-aggressive patients present unique challenges that require emotional intelligence, patience, and strategic communication skills from healthcare professionals.

Passive-aggressive behavior often stems from underlying feelings of fear, resentment, or a perceived lack of control. Patients may feel overwhelmed by their diagnosis, skeptical of medical advice, or frustrated by systemic issues such as long wait times or insurance complications. Rather than expressing these concerns openly, they may resort to behaviors such as missed appointments, vague complaints, sarcasm, or noncompliance with treatment plans. These actions, though subtle, can disrupt care continuity and erode trust between patient and provider.

One of the most difficult aspects of managing passive-aggressive patients is identifying the behavior early. Unlike overt aggression, passive-aggression is cloaked in ambiguity. A patient might nod in agreement during a consultation but later ignore medical instructions. They may offer compliments laced with sarcasm or express dissatisfaction through third parties rather than directly. These indirect signals can leave providers confused and uncertain about the patient’s true feelings or intentions.

***

***

Addressing passive-aggressive behavior requires a nuanced approach. First, providers must cultivate a nonjudgmental environment where patients feel safe expressing concerns. Active listening, empathy, and validation can encourage more direct communication. For example, acknowledging a patient’s frustration with wait times or side effects can open the door to honest dialogue. Providers should also be mindful of their own reactions, avoiding defensiveness or dismissiveness, which can exacerbate the behavior.

Setting clear boundaries and expectations is another key strategy. Passive-aggressive patients often test limits subtly, so it’s important to reinforce the importance of mutual respect and accountability. Documenting interactions, treatment plans, and patient responses can help track patterns and ensure consistency. In some cases, involving mental health professionals may be beneficial, especially if the behavior is rooted in deeper psychological issues.

Ultimately, the goal is to transform passive-aggressive dynamics into constructive partnerships. This requires time, effort, and a willingness to engage with patients beyond surface-level interactions. When successful, it can lead to improved outcomes, greater patient satisfaction, and a more harmonious clinical environment.

In conclusion, passive-aggressive patients pose a unique challenge in healthcare, but they also offer an opportunity for providers to refine their communication skills and deepen their understanding of patient psychology. By fostering openness, setting boundaries, and responding with empathy, healthcare professionals can navigate these interactions effectively and promote better health outcomes for all.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

Posted on November 17, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

Retirement planning has evolved significantly over the past several decades, with employers and employees seeking solutions that balance security, flexibility, and predictability. Among the various retirement plan options available today, cash balance plans stand out as a hybrid design that combines features of both traditional defined benefit pensions and defined contribution plans. Their unique structure makes them an attractive choice for employers aiming to provide meaningful retirement benefits while maintaining financial predictability.

At their core, cash balance plans are a type of defined benefit plan. Unlike traditional pensions, which promise retirees a monthly income based on years of service and final salary, cash balance plans define the benefit in terms of a hypothetical account balance. Each participant’s account grows annually through two components: a “pay credit” and an “interest credit.” The pay credit is typically a percentage of the employee’s salary or a flat dollar amount, while the interest credit is either a fixed rate or tied to an index such as U.S. Treasury yields. Although the account is hypothetical—meaning the funds are not actually segregated for each employee—the structure provides participants with a clear, understandable statement of their retirement benefit.

One of the primary advantages of cash balance plans is their transparency. Employees can easily track the growth of their account balance, much like they would with a 401(k). This clarity helps workers better understand the value of their retirement benefits and fosters a sense of ownership. Additionally, cash balance plans are portable: when employees leave a company, they can roll over the vested balance into an IRA or another qualified plan, ensuring continuity in retirement savings.

***

***

From the employer’s perspective, cash balance plans offer several benefits as well. Traditional pensions often create unpredictable liabilities, as they depend on factors such as longevity and investment performance. Cash balance plans, by contrast, provide more predictable costs because the employer commits to specific pay and interest credits. This predictability makes them easier to manage and budget for, particularly in industries where workforce mobility is high. Moreover, cash balance plans can be designed to reward long-term employees while still appealing to younger workers who value portability.

Despite these advantages, cash balance plans are not without challenges. Because they are defined benefit plans, employers bear the investment risk and must ensure the plan is adequately funded. Regulatory requirements, including nondiscrimination testing and funding rules, add complexity and administrative costs. Additionally, while cash balance plans are generally more equitable across generations of workers, transitions from traditional pensions to cash balance designs have sometimes sparked controversy, particularly among older employees who may perceive a reduction in benefits.

In recent years, cash balance plans have gained popularity among professional firms, such as law practices and medical groups, as well as small businesses seeking tax-efficient retirement solutions. These plans allow owners and highly compensated employees to accumulate larger retirement savings than would be possible under defined contribution limits, while still providing benefits to rank-and-file workers. As such, they serve as a valuable tool for both talent retention and financial planning.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 15, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

For centuries, doctors have occupied one of the highest earning and most respected positions in society. Their extensive education, specialized knowledge, and critical role in preserving human life have traditionally guaranteed them financial security and social prestige. Yet in recent years, a growing conversation has emerged: could skilled tradesmen—electricians, plumbers, welders, carpenters, and other hands‑on professionals—eventually out‑earn doctors in the future? While the answer is complex, shifting economic dynamics suggest that the gap between these professions may narrow, and in certain contexts, tradesmen could indeed surpass doctors in earnings.

One of the most significant factors driving this possibility is supply and demand. The medical profession requires years of schooling, residency, and licensing, which creates a steady pipeline of doctors but also limits entry. By contrast, skilled trades have suffered from declining interest among younger generations, many of whom were encouraged to pursue college degrees instead of vocational training. As a result, there is now a shortage of tradesmen in many regions. When demand for services like plumbing or electrical work rises but supply remains low, wages naturally increase. Already, some master tradesmen charge hourly rates that rival or exceed those of general practitioners.

Another consideration is student debt and overhead costs. Doctors often graduate with hundreds of thousands of dollars in debt, and many must work in hospital systems or private practices with high administrative expenses. Tradesmen, on the other hand, typically face lower educational costs and can enter the workforce much earlier. Many start their own businesses with relatively modest investments, allowing them to keep a larger share of their earnings. In an era where entrepreneurship and independence are highly valued, tradesmen may find themselves financially freer than doctors burdened by debt and bureaucracy.

***

***

The changing economy also plays a role. Automation and artificial intelligence are beginning to reshape medicine, with diagnostic tools, telehealth, and robotic surgery reducing the need for certain human tasks. While doctors will always be essential, parts of their work may become less lucrative as technology takes over. Skilled trades, however, are far harder to automate. Repairing a leaking pipe, rewiring a house, or welding a custom structure requires physical presence, adaptability, and problem‑solving in unpredictable environments—skills machines struggle to replicate. This resilience against automation could make tradesmen’s work increasingly valuable.

That said, doctors will likely continue to command high salaries in specialized fields such as surgery, cardiology, or oncology. The prestige and necessity of medical expertise ensure that society will always reward them. Yet the notion that tradesmen are “lesser” careers is fading. In fact, many tradesmen already earn six‑figure incomes, particularly those who own successful businesses or operate in regions with acute labor shortages.

Ultimately, whether tradesmen will out‑earn doctors depends on how society values different forms of expertise. If current trends continue—rising demand for trades, shortages of skilled labor, resistance to automation, and lower educational barriers—it is plausible that many tradesmen will match or surpass doctors in income. The future may not be defined by one profession dominating the other, but by a more balanced recognition that both healers and builders are indispensable to modern life. In that sense, the financial gap may close, reflecting a broader cultural shift toward valuing practical skills as highly as academic ones.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

BASIC DEFINITIONS

***

***

The Direct Reimbursement Payment Model allows physicians to receive payment directly from patients or employers, bypassing traditional insurance systems. This model emphasizes transparency, autonomy, and personalized care, offering an alternative to fee-for-service and managed care structures.

The Direct Reimbursement Payment Model is a healthcare financing approach in which physicians are paid directly by patients or sponsoring entities—such as employers—rather than through insurance companies or government programs. This model is gaining traction as a response to the administrative burdens, opaque billing practices, and fragmented care often associated with traditional insurance-based systems.

One prominent example of direct reimbursement is Direct Primary Care (DPC). In DPC, patients pay a recurring fee—monthly, quarterly, or annually—that covers a broad range of primary care services. These include routine checkups, preventive screenings, chronic disease management, and basic lab work. By eliminating third-party billing, DPC practices reduce overhead costs and administrative complexity, allowing physicians to spend more time with patients and focus on quality care.

***

***

Employers have also embraced direct reimbursement models to manage healthcare costs and improve employee wellness. In such arrangements, employers reimburse physicians or clinics directly for services rendered to their employees, often through a defined benefit structure. This can be part of a self-funded health plan or a supplemental offering alongside high-deductible insurance policies. The goal is to provide accessible, cost-effective care while avoiding the inefficiencies of traditional insurance networks.

Key advantages of the direct reimbursement model include:

Price transparency: Patients know upfront what services cost, reducing surprise billing and financial stress.

Improved access: Physicians often offer same-day or next-day appointments, extended visits, and direct communication via phone or email.

Lower administrative burden: Without insurance paperwork, practices can operate more efficiently and focus on patient care.

Stronger patient-physician relationships: More time per visit fosters trust, continuity, and better health outcomes.

However, the model is not without limitations. Direct reimbursement may not cover specialist care, hospitalization, or emergency services, requiring patients to maintain supplemental insurance. Additionally, the model may be less accessible to low-income populations who cannot afford recurring fees or out-of-pocket payments. Critics also argue that widespread adoption could fragment care and reduce risk pooling, undermining the broader goals of universal coverage.

Despite these concerns, the direct reimbursement model aligns with broader trends in healthcare reform, including value-based care, consumer empowerment, and decentralized service delivery. It offers a viable path for physicians seeking autonomy and for patients desiring personalized, transparent care. As healthcare continues to evolve, hybrid models that combine direct reimbursement with traditional insurance may emerge, offering flexibility and choice across diverse patient populations.

In conclusion, the Direct Reimbursement Payment Model represents a meaningful shift in how healthcare services are financed and delivered.

By prioritizing simplicity, transparency, and patient-centered care, it challenges the status quo and opens new possibilities for sustainable, high-quality medical practice.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

For generations, the prevailing belief in healthcare has been that physicians [MD, DO and DPM], with their high salaries and prestige, inevitably retire wealthier than nurses. Yet this assumption overlooks the financial realities of different nursing specialties and the long‑term impact of debt, lifestyle, and retirement planning. In fact, some Registered Nurses (RNs)—particularly Certified Registered Nurse Anesthetists (CRNAs), visiting nurses, and those who participate in structured pay programs like the Baylor plan—can retire richer than physicians. The reasons lie in the interplay of education costs, career flexibility, income potential, and disciplined financial planning.

Education Costs and Debt Burden

One of the most decisive factors shaping retirement wealth is the cost of education. Physicians often spend over a decade in training, including undergraduate studies, medical school, and residency. This path not only delays their earning years but also saddles them with substantial student debt. The median medical school debt in the United States exceeds $200,000, and many physicians spend years paying it down.

By contrast, RNs typically complete their training in two to four years, with advanced practice nurses such as CRNAs requiring graduate‑level education. Even so, their debt burden is far lighter, often less than half of what physicians carry. This difference means nurses can begin earning earlier, save for retirement sooner, and avoid the crushing interest payments that erode physicians’ wealth. A CRNA who starts practicing in their late twenties may already be investing in retirement accounts while a physician is still in residency earning a modest stipend.

Income Potential of Specialized Nurses

While physicians generally earn more annually than nurses, the gap is narrower in certain specialties. CRNAs, for example, are among the highest‑paid nursing professionals, with average salaries often exceeding $200,000 per year. This places them in direct competition with some physician specialties, especially primary care doctors, who may earn similar or even lower salaries.

Visiting nurses also benefit from unique financial advantages. Many work on flexible schedules, contract arrangements, or per‑visit compensation models. This allows them to maximize income while minimizing burnout. By avoiding the overhead costs of private practice and the administrative burdens physicians face, visiting nurses can channel more of their earnings directly into savings and investments.

When combined with lower debt and earlier career starts, these income streams can compound into significant retirement wealth.

The Baylor plan, a structured pay program used by some hospitals, allows nurses to work full‑time hours compressed into fewer days—often weekends—while still receiving full‑time pay and benefits. This arrangement provides several financial advantages. First, it enables nurses to earn competitive wages while freeing up weekdays for additional work, education, or entrepreneurial ventures. Second, it reduces commuting and childcare costs, allowing more income to be saved. Third, the plan often includes robust retirement benefits, such as employer‑matched contributions to 401(k) or pension programs.

Nurses who consistently participate in such structured pay plans can accumulate substantial nest eggs, often surpassing physicians who delay retirement savings due to debt repayment or lifestyle inflation. The Baylor plan highlights the importance of systematic investing: by automating contributions and focusing on long‑term growth, nurses can harness the power of compound interest. A nurse who invests steadily for 35 years may accumulate more wealth than a physician who begins saving late and inconsistently, despite earning a higher salary.

Lifestyle and Work‑Life Balance

Another overlooked factor is lifestyle. Physicians often face grueling schedules, high stress, and the temptation to maintain expensive lifestyles commensurate with their social status. Luxury homes, cars, and vacations can erode their financial base. Nurses, while not immune to lifestyle inflation, often maintain more modest spending habits.

Visiting nurses, in particular, enjoy flexibility that allows them to balance work with personal life. This reduces burnout and healthcare costs while enabling consistent employment into later years. By living within their means and prioritizing savings, nurses can accumulate wealth steadily without the financial pitfalls that sometimes accompany physician lifestyles.

Retirement Wealth Beyond Salary

Retirement wealth is not solely determined by annual income. It is shaped by debt management, savings discipline, investment strategies, and lifestyle choices. Nurses who leverage high‑paying specialties like anesthesia, flexible arrangements like visiting nursing, and structured programs like the Baylor plan can outperform physicians in these areas.

Consider two professionals: a physician earning $250,000 annually but burdened by $200,000 in debt and high living expenses, and a CRNA earning $200,000 with minimal debt and disciplined savings. Over decades, the CRNA may accumulate more net wealth, retire earlier, and enjoy greater financial security.

Conclusion

The assumption that physicians always retire richer than nurses is outdated. While physicians command higher salaries, their delayed earnings, heavy debt, and lifestyle pressures often undermine long‑term wealth. Nurses, particularly CRNAs, visiting nurses, and those who participate in structured pay programs like the Baylor plan, can retire wealthier by combining lower debt, earlier savings, competitive incomes, and disciplined financial planning.

Ultimately, retirement wealth is not about prestige but about strategy. Nurses who recognize this truth and act accordingly may find themselves enjoying more financial freedom than the very physicians they once assisted.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 8, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

The Pitfalls of Capitation in Medicine

Capitation, a payment model in healthcare where providers receive a fixed amount per patient regardless of the services rendered, has been promoted as a way to control costs and incentivize efficiency. However, despite its theoretical appeal, capitation medicine presents significant drawbacks that can compromise patient care, distort provider incentives, and exacerbate systemic inequities.

One of the most concerning aspects of capitation is the potential for under-treatment. Since providers are paid a set fee per patient, regardless of how much care that patient requires, there is a financial incentive to minimize services. This can lead to situations where necessary tests, referrals, or treatments are delayed or denied in order to preserve profit margins. Patients with complex or chronic conditions—who require more frequent and intensive care—may be especially vulnerable under this model. The risk is that medical decisions become driven by cost containment rather than clinical need, undermining the ethical foundation of healthcare.

Capitation also introduces challenges in maintaining quality standards. Unlike value-based care, which ties reimbursement to outcomes, capitation focuses solely on cost predictability. Without robust oversight and accountability mechanisms, providers may cut corners or avoid high-risk patients altogether. This can result in cherry-picking, where healthier individuals are favored, and sicker patients are subtly discouraged from enrolling. Such practices not only distort the patient pool but also deepen health disparities, particularly among marginalized populations who already face barriers to care.

Furthermore, capitation can strain the provider-patient relationship. Physicians may feel pressured to limit time spent with each patient or avoid costly interventions, leading to a sense of transactional care rather than personalized attention. This erosion of trust can diminish patient satisfaction and reduce adherence to treatment plans. In a system where providers are rewarded for doing less, the intrinsic motivation to go above and beyond for patients may be compromised.

Operationally, capitation demands sophisticated infrastructure to manage risk, track utilization, and ensure compliance. Smaller practices or those serving underserved communities may lack the resources to implement such systems effectively. This can create a two-tiered system where well-funded organizations thrive while others struggle to deliver basic care. Additionally, the administrative burden of managing capitation contracts, monitoring performance metrics, and navigating complex reimbursement rules can divert attention from clinical priorities.

Critics also argue that capitation may stifle innovation. When providers are locked into fixed budgets, there is little room to experiment with new technologies, therapies, or care models that might improve outcomes but carry upfront costs. This conservative approach can hinder progress and limit access to cutting-edge treatments.

In conclusion, while capitation medicine aims to control costs and streamline care, its inherent risks—under-treatment, inequity, and diminished quality—make it a problematic model when not carefully regulated. To truly reform healthcare, payment systems must balance financial sustainability with ethical responsibility, ensuring that every patient receives the care they need, not just the care that fits a budget.

What Medical School Didn’t Teach Doctors About Money

Medical school is designed to mold students into competent, compassionate physicians. It teaches anatomy, pathology, pharmacology, and clinical skills with precision and rigor. Yet, despite the depth of medical knowledge imparted, one critical area is often overlooked: financial literacy. For many doctors, the transition from student to professional comes with a steep learning curve—not in medicine, but in money. From managing debt to understanding taxes, investing, and retirement planning, medical school leaves a financial education gap that can have long-term consequences.

The Debt Dilemma

One of the most glaring omissions in medical education is how to manage student loan debt. The average medical student graduates with over $200,000 in debt, yet few are taught how to navigate repayment options, interest accrual, or loan forgiveness programs. Many doctors enter residency with little understanding of income-driven repayment plans or Public Service Loan Forgiveness (PSLF), missing opportunities to reduce their financial burden. Without guidance, some make costly mistakes—such as refinancing federal loans prematurely or choosing repayment plans that don’t align with their career trajectory.

Income ≠ Wealth

Medical students often assume that a high salary will automatically lead to financial security. While physicians do earn more than most professionals, income alone doesn’t guarantee wealth. Medical school rarely addresses the importance of budgeting, saving, and investing. As a result, many doctors fall into the “HENRY” trap—High Earner, Not Rich Yet. They spend lavishly, assuming their income will always cover expenses, only to find themselves living paycheck to paycheck. Without a solid financial foundation, even high earners can struggle to build net worth.

***

***

Taxes and Business Skills

Doctors are also unprepared for the complexities of taxes. Whether employed by a hospital or running a private practice, physicians face unique tax challenges. Medical school doesn’t teach how to track deductible expenses, optimize retirement contributions, or navigate self-employment taxes. For those who open their own clinics, the lack of business education is even more pronounced. Understanding profit margins, payroll, insurance billing, and compliance regulations is essential—but rarely covered in medical training.

Investing and Retirement Planning

Another blind spot is investing. Medical students are rarely taught the basics of compound interest, asset allocation, or retirement accounts. Many don’t know the difference between a Roth IRA and a traditional 401(k), or how to evaluate mutual funds and index funds. This lack of knowledge delays retirement planning and can lead to missed opportunities for long-term growth. Some doctors rely on financial advisors without understanding the fees or conflicts of interest involved, putting their wealth at risk.

Insurance and Risk Management

Medical school also fails to educate students on insurance—life, disability, malpractice, and health. Doctors need robust coverage to protect their income and assets, but many don’t know how to evaluate policies or understand terms like “own occupation” or “elimination period.” Inadequate coverage can leave physicians vulnerable to financial disaster in the event of illness, injury, or litigation.

Emotional and Behavioral Finance

Beyond technical knowledge, medical school overlooks the emotional side of money. Physicians often face pressure to maintain a certain lifestyle, especially after years of sacrifice. The desire to “catch up” can lead to impulsive spending, luxury purchases, and financial stress. Without tools to manage money mindset and behavioral habits, doctors may struggle with guilt, anxiety, or burnout related to finances.

The Case for Financial Education

Fortunately, awareness of this gap is growing. Organizations like Medics’ Money and podcasts such as “Docs Outside the Box” are working to fill the void by offering financial education tailored to physicians.

These resources cover everything from budgeting and debt management to investing and entrepreneurship. Some medical schools are beginning to incorporate financial literacy into their curricula, but progress is slow and inconsistent.

Conclusion

Medical school equips doctors to save lives, but it doesn’t prepare them to secure their own financial future. The lack of financial education leaves many physicians vulnerable to debt, poor investment decisions, and lifestyle inflation. To thrive both professionally and personally, doctors must seek out financial knowledge beyond the classroom. Whether through self-study, mentorship, or professional guidance, understanding money is as essential as understanding medicine. After all, financial health is a cornerstone of overall well-being—and every doctor deserves to master both.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Why It Is Difficult to Practice Medicine Part-Time Today?

In the past, part-time medical practice offered physicians a flexible way to balance professional responsibilities with personal or family commitments. Today, however, the healthcare environment has evolved in ways that make part-time medicine increasingly challenging. From administrative burdens to economic pressures and patient expectations, the obstacles are both systemic and personal.

One of the most significant barriers is the rise in administrative complexity. Physicians are now required to navigate electronic health records (EHRs), comply with insurance documentation, and meet regulatory standards such as HIPAA and MACRA. These tasks consume hours of non-clinical time, which is difficult to compress into a part-time schedule. Even seeing fewer patients doesn’t exempt part-time doctors from the same documentation and compliance requirements as their full-time counterparts.

***

***

Another challenge is financial viability. Many physicians are paid based on productivity metrics, such as Relative Value Units (RVUs), which reward volume over quality. Part-time practitioners often struggle to meet these benchmarks, resulting in lower compensation and reduced benefits. Additionally, malpractice insurance premiums and licensing fees remain fixed regardless of hours worked, further eroding the financial appeal of part-time practice.

Continuity of care is also a concern. Patients increasingly expect immediate access to their providers, especially in primary care and specialties like psychiatry or pediatrics. Part-time physicians may not be available for urgent issues, leading to fragmented care and dissatisfaction. This can strain relationships with patients and colleagues who must cover gaps in availability.

From a professional standpoint, part-time physicians may face limited career advancement. Leadership roles, academic appointments, and research opportunities often favor full-time commitment. There’s also a perception—sometimes unfair—that part-time doctors are less dedicated or less competent, which can affect peer respect and influence within medical institutions.

Technology, while beneficial, adds another layer of complexity. Telemedicine, remote monitoring, and digital communication tools have expanded access but also increased the expectation for constant availability. Part-time physicians may find it difficult to manage asynchronous messages, follow-ups, and virtual visits without extending their work hours beyond what they intended.

***

***

Lastly, burnout and work-life balance—ironically one of the reasons doctors seek part-time roles—can still be elusive. The pressure to maintain clinical excellence, stay updated with medical advancements, and meet patient needs doesn’t diminish with reduced hours. In fact, squeezing these responsibilities into fewer days can intensify stress rather than alleviate it.

In conclusion, while part-time medical practice may seem like a solution to modern work-life challenges, the reality is far more complex. The structure of today’s healthcare system, combined with economic, technological, and cultural pressures, makes it difficult for physicians to thrive in part-time roles. Addressing these challenges will require systemic reform, flexible compensation models, and a cultural shift in how we value and support diverse medical careers.

SPEAKING: ME-P Editor Dr. David Edward Marcinko MBA MEd will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Hobson’s choice is a free choice in which only one thing is actually offered. The term is often used to describe an illusion that choices are available. The best known example is “I’ll give you a choice: Take it or leave it”, wherein “leaving it” is strongly undesirable.

The phrase is said to have originated with Thomas Hobson (1544–1631), a livery stable owner in Cambridge, England, who offered customers the choice of either taking the horse in the stall nearest to the door or taking none at all.

A CASE MODEL

Half of Physicians Plan to Change Career Paths

The Physicians Foundation recently conducted a survey on physician practice patterns and perspectives. Here are some key findings from the report:

• 31% of physicians identify as independent practice owners or partners. • Almost half (47%) of physicians plan to change career paths. • 78% of physicians sometimes, often or always experience feelings of burnout. • Nearly a quarter of physician time is spent on non-clinical paperwork.

This result is not a good Hobson’s Choice in Medicine.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

A Financial Self Discovery Questionnairefor Medical Professionals

For understanding your relationship with money, it is important to be aware of yourself in the contexts of culture, family, value systems and experience. These questions will help you. This is a process of self-discovery. To fully benefit from this exploration, please address them in writing. You will simply not get the full value from it if you just breeze through and give mental answers. While it is recommended that you first answer these questions by yourself, many people relate that they have enjoyed the experience of sharing them with others who are important to them.

As you answer these questions, be conscious of your feelings, actually describing them in writing as part of your process.

Childhood

What is your first memory of money?

What is your happiest moment with Money? Your most unhappy?

Name the miscellaneous money messages you received as a child.

How were you confronted with the knowledge of differing economic circumstances among people, that there were people “richer” than you and people “poorer” than you?

Cultural heritage

What is your cultural heritage and how has it interfaced with money?

To the best of your knowledge, how has it been impacted by the money forces? Be specific.

To the best of your knowledge, does this circumstance have any motive related to Money?

Speculate about the manners in which your forebears’ money decisions continue to affect you today?

Family

How is/was the subject of money addressed by your church or the religious traditions of your forebears?

What happened to your parents or grandparents during the Depression?

How did your family communicate about money?

How? Be as specific as you can be, but remember that we are more concerned about impacts upon you than historical veracity.

When did your family migrate to America (or its current location)?

What else do you know about your family’s economic circumstances historically?

Your parents

How did your mother and father address money?

How did they differ in their money attitudes?

How did they address money in their relationship?

Did they argue or maintain strict silence?

How do you feel about that today?

Please do your best to answer the same questions regarding your life or business partner(s) and their parents.

Childhood: Revisited

How did you relate to money as a child? Did you feel “poor” or “rich”? Relatively? Or, absolutely? Why?

Were you anxious about money? Did you receive an allowance? If so, describe amounts and responsibilities.

Did you have household responsibilities?

Did you get paid regardless of performance?

Did you work for money?

If not, please describe your thoughts and feelings about that.

***

***

Same questions, as a teenager, young adult, older adult.

Credit

When did you first acquire something on credit?

When did you first acquire a credit card?

What did it represent to you when you first held it in your hands?

Describe your feelings about credit.

Do you have trouble living within your means?

Do you have debt?

Adulthood

Have your attitudes shifted during your adult life? Describe.

Why did you choose your personal path? a) Would you do it again? b) Describe your feelings about credit.

Adult attitudes

Are you money motivated? If so, please explain why? If not, why not? How do you feel about your present financial situation? Are you financially fearful or resentful? How do you feel about that?

Will you inherit money? How does that make you feel?

If you are well off today, how do you feel about the money situations of others? If you feel poor, same question.

How do you feel about begging? Welfare? If you are well off today, why are you working?

Do you worry about your financial future?

Are you generous or stingy? Do you treat? Do you tip?

Do you give more than you receive or the reverse? Would others agree?

Could you ask a close relative for a business loan? For rent/grocery money?

Could you subsidize a non-related friend? How would you feel if that friend bought something you deemed frivolous?

Do you judge others by how you perceive they deal with their Money? Do you feel guilty about your prosperity? Are your siblings prosperous?

What part does money play in your spiritual life?

Do you “live” your Money values?

Conclusion

There may be other questions that would be useful to you. Others may occur to you as you progress in your life’s journey. The point is to know your personal money issues and their ramifications for your life, work, and personal mission.

This will be a “work-in-process” with answers both complex and incomplete. Don’t worry.

Just incorporate fine-tuning into your life’s process.

Despite their high salaries, not all doctors are wealthy, and some live paycheck to paycheck. Here are 5 reasons why many doctors today are broke, according to https://medschoolinsiders.com

1 | Believing They Are Universally Smart

The first reason so many doctors are broke is that many doctors believe they are universally smart. While most doctors have deep specialized knowledge, there’s a big difference between being smart in your profession and being smart with money. A physician’s schooling is quite thorough when it comes to the human body, but med school doesn’t include a prerequisite class on how to handle finances.

Graduating medical school is a major feat and certainly demonstrates superior work ethic and cognitive abilities. But many new doctors believe these accomplishments transcend all aspects of life. If you’re smart enough to earn an MD, you’re certainly smart enough to handle your finances, but only once you properly and intentionally educate yourself.

The truth is doctors, especially traditional graduates, haven’t had an opportunity to manage large sums of money until they become fully trained attending physicians and start pulling in low to mid six figures in income. Prior to that, there was very little of it to manage.

Far too many aspiring doctors, and students in general, don’t take the time to learn financial basics, in part because it’s uncomfortable and seems like something they can figure out “later”, whenever that may be. Their poor spending habits and lack of investment knowledge carry over into their careers, causing many to make irresponsible decisions.

The second factor is overspending too soon, and this comes up at two points in training.

First, it’s natural to want to start spending more as soon as you get into residency and start making a little more money. After all, you’ve been a broke student for 8 or more years, and now you’re finally making a reasonable and reliable wage. But that’s where young doctors get into trouble. Residency pays, but not nearly as much as you will be making once you become an attending physician. The average resident makes about $60K a year, and if you begin spending all of that money right away, thinking you’ll handle your loans once you become an attending, you delay paying off your medical school debt, which means the compounding effect through your student loan interest rate works against you.

Now that $250,000 in student loans has ballooned to over $350,000 by the time you finish residency. The compounding effect, which can be one of your greatest allies in your financial life, becomes an equally powerful enemy when working against you through debt. But of course, pinching pennies is easier said than done, especially when you’re in residency and are surrounded by peers in different professions. They’ve been earning good money much longer than you have, and they can afford more luxurious lifestyles.

They may not be worried about indulging in fine dining or how much a hotel costs when traveling. Students in college and medical school are often confident they will resist the temptations, but the desire to keep up with your friends and family can be difficult to ignore, which causes many to overspend before they technically have the money to do so.

The same is true of attending physicians. As soon as those six-figure salaries come rolling in, many physicians go overboard with spending, trying to make up for lost time and to treat yourself.

Now, we are not suggesting you shouldn’t reward yourself for completing residency, but that reward shouldn’t be a Lamborghini. It’s best to continue living like a resident in your first few years after becoming an attending to pay off loans, put a down payment on a home, and get your financial foundation built before loosening the purse strings.

3 | Decreasing Salaries

Third, doctors continue to make less money than they did before. And this includes nearly all 44 medical specialties. For example, while physician compensation technically rose from $343k to $391k between 2017 and 2022, this rise does not keep up with inflation. The real average compensation in 2022 was less than $325k—a $20k decrease in purchasing power in only six years.

For doctors who are already spending to the limits of their salaries with huge mortgages, car payments, business costs, and other luxuries, a decreased salary can have a huge impact. You might be able to cut back by going on fewer vacations or eating out less frequently, but many accrued costs are locked in, such as a mortgage payment, car loan, or leased rental space for your practice.

4 | Increasing Costs of Private Practice

In the past, running a private practice was much simpler, but recent stricter guidelines and regulations have made it difficult for solo practices to keep up. While regulations like the Health Insurance Privacy and Portability Act, or HIPAA, and mandatory Electronic Medical Records, or EMRs, are necessary to protect patients, they make costs higher for physicians who run their own private practice. These physicians need to spend their own money to set up and maintain EMRs as well as invest in security to ensure patient data is protected.

With the steep rise of inflation we’ve seen over the past couple of years, everything is more expensive, which means costs, such as business space, equipment, and even office supplies, have gone up for private practice physicians while salaries have not. 2013 to 2020 saw an annual inflation rate of anywhere from 0.7% to 2.3%. This skyrocketed to an annual inflation rate of 7.0% in 2021 and another 6.5% in 2022. In fact, the cost of running a private practice has increased by almost 40% between 2001 and 2021.

These increased costs are exacerbated by another problem plaguing private practices; decreased reimbursement. While costs increased by almost 40%, Medicare reimbursement only increased by 11%. When doctors see patients who are insured, the insurance companies pay the physicians for their time. For Medicare, the new proposed rules for 2023 would cut reimbursement by around 5%. When adjusting for inflation, Medicare reimbursement decreased by 20% in the last 20 years.

These costs add up, making it extremely difficult for physicians to thrive financially while running a private practice.

5 | Tuition Debt

Lastly, we can’t talk about a doctor’s finances without mentioning the exorbitant debt so many graduating physicians are left with. It won’t shock you to hear that med school is expensive. Extremely expensive. The average cost of tuition for a single year is nearly $60k, with significant variance from school to school, and that’s before accounting for living expenses.

In-state applicants pay less than out-of-state applicants, and students at private schools typically pay more than students at public medical schools. The astronomical costs mean the vast majority of students can’t pay for medical school out of their own pockets. And unless your family is part of the 1%, even with your parents footing the bill, it’s difficult to cover tuition, let alone rent, groceries, transportation, tech, social activities, exam fees, and application costs.

The average total student debt after college and med school is over $250k. But keep in mind that’s the average, which includes 27% of students who graduate with no debt at all. This means the vast majority of students leave medical school owing much more than $250k.

For some perspective, in 1978, the average debt for graduating MDs was $13,500, which, when adjusted for inflation, is a little over $60,000. There are multiple ways to eventually repay these loans, but time and discipline are essential to ensure this money is paid off as quickly as possible.

According to financial advisor Dr. David Edward Marcinko MEd MBA CMP™; consider the following:

Place a portion of your salary (15-20% or more) into a savings account, and another portion (10-20% or more) into wise investments [stocks, bonds, mutual funds, and/or ETFs].

Pay off your bills each month, and then use leftover spending money to purchase fun things like vacations and fancy dinners, within your means. Shop sales, buy used clothes, and use credit card points for travel.

Hire an excellent tax professional and meet with an investment advisor once or twice a year about your investment status and strategy. http://www.MarcinkoAssociates.com

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on September 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

BREAKING NEWS

Law enforcement officials in Utah released a video of the suspected shooter in the assassination of Turning Point USA co-founder and CEO Charlie Kirk, saying that the person wore Converse tennis shoes and left a hand print and a shoe print at the scene.

The suspect in Charlie Kirk’s assassination has been identified as Tyler Robinson, a 22-year-old Utah resident. Law enforcement sources told the Daily Mail that Robinson was taken into custody as the alleged assassin who killed Kirk at a rally at Utah Valley University on Wednesday.

Before today, forensic podiatry has even made it into the public zeitgeist with the hit TV show “Bones” which premiered on September 13, 2005, and concluded on March 28, 2017, airing for 246 episodes over 12 seasons. The show was based on forensic anthropology and forensic archaeology, with each episode focusing on the mystery behind human body remains brought in for examination and identification.

In one show, eight pairs of dismembered feet washed ashore after a flood on the U.S.-Canada border, but things didn’t add up when only seven pairs of feet were identified as research corpses from a nearby university body farm.

When the fictional Canadian forensic podiatrist Dr. Douglas Filmore took the remains back to Canada, he had to form a jurisdictional alliance with the United States to match the pairs of feet and identify the victims. A rare and expensive pair of sneakers led the team to the victim’s murderer.

In 2016, an actual forensic podiatry club was started at the Barry University School of Podiatric Medicine. And, a formal class covering aspects of forensic podiatry is held at the New York College of Podiatric Medicine. Students exit the class with an in depth knowledge of forensic podiatry and other legal knowledge applicable to current cases.

More expertly, real-life colleague Michael Steven Nirenberg DPMactually testified in the murder trial of defendants Kailie Brackett and Donnell Dana with the state calling three witnesses to testify, including the podiatrist who claimed Brackett’s footprints match the ones found in blood at the apartment of the victim, Kimberly Neptune. The forensic podiatrist focused on the footprints discovered at Neptune’s apartment, using prints and images of the defendant’s feet taken by law enforcement. After study, he claimed the prints at the scene bore a resemblance to Kailie Brackett’s in the width of the foot. The defense questioned the field of forensic podiatry and pressed Dr. Nirenberg on whether the measurements would be altered depending on how thick the sock covering the foot was woven.

Dr. Nirenberg was also interviewed on National Public Radio’s Morning Edition on April 14th 2023 about the gait of the bombing suspect associated with the capital riot on Wednesday January 6th, 2021. Dr. Nirenberg is president of the American Society of Forensic Podiatry and co-editor of the textbook: “Forensic Gait Analysis: Principles and Practice”. The bombing suspect had placed bombs at the DNC and RNC headquarters in Washington, DC on the night before. NPR asked Dr. Nirenberg to comment on the features of the person’s gait.

Additionally, Nirenberg was interviewed by Nancy Grace on her TV show Crime Stories. Grace interviewed Nirenberg about his forensic podiatry work in helping to solve the murder of a mother of 3 who was killed in a church. The case remains unsolved. The episode, “Fitness-Mom Missy Bevers Bludgeoned Dead in Creekside Church” aired June 6th, 2024 and is available online at Merit+ TV.

And, Netflix’s 2023 docu-series, “Till Murder Do Us Part”, recounts the killings of Derek and Nancy Haysom by including a series of interviews with a cast of real people. The four-part docu-series revolves around the unpacking of how a wealthy couple was murdered in Virginia in 1985. It also focuses on how the suspects, Elizabeth Haysom, and her boyfriend, Jens Soehring, betrayed each other during the trial. Dr. Sarah Reel DPM was the forensic podiatrist who was involved with Jens’ and Elizabeth’s footprint examination. Dr. Reel pointed out that, statistically, there was no difference “between a bare footprint and a socked footprint.” The doctor suggested that Jens’ reference footprint matched closely with the crime scene footprint.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

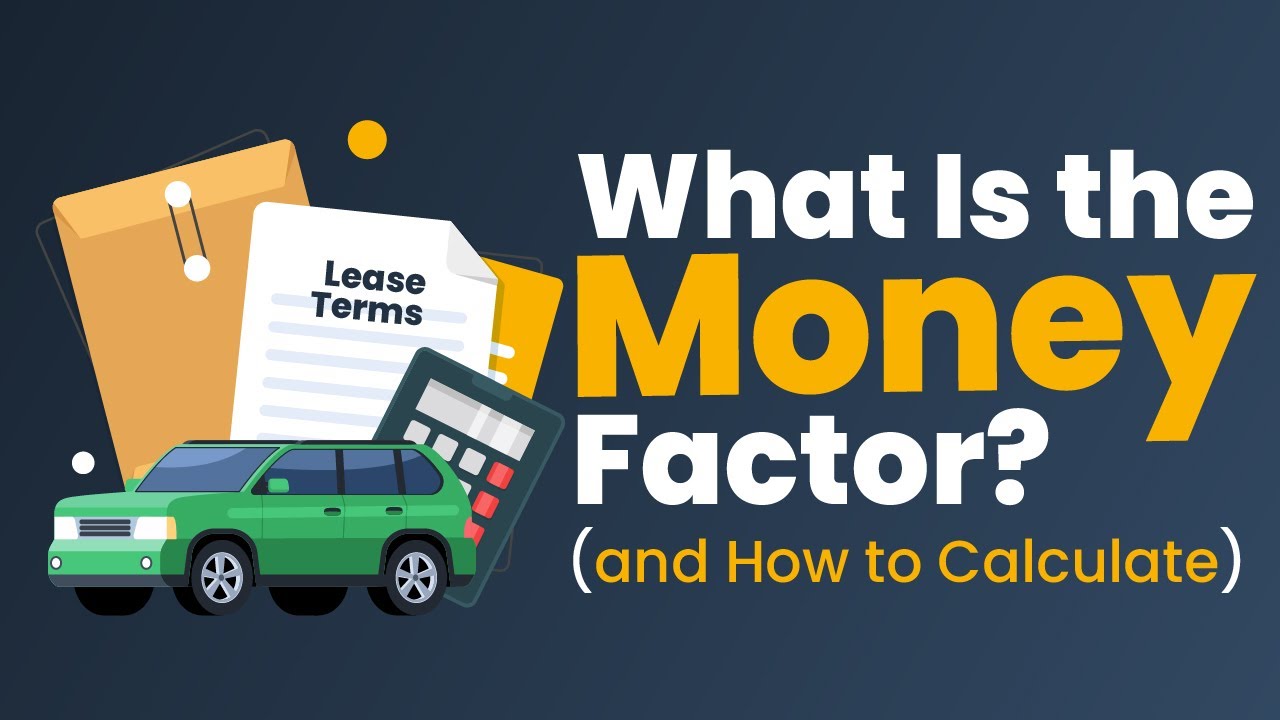

The so-called money factor (abbreviated as MF on invoices) is a number in a decimal form that dealers use to calculate the APR of a car lease. It’s a major part of your monthly payment and dealers are known to jack up the money factor to pad their profits.

Most doctors don’t ask to see it because they’re not aware of it or don’t know how to calculate it. Ask to see the money factor, then multiply it by 2,400.

For example, if the money factor is .00150, you multiply it by 2,400 to get 3.6%. If that’s higher than the prevailing rate, you have room to talk them down.

How to reduce it

So how do you get a good interest rate when you lease a vehicle? The same way you do when borrowing for any other reason, whether it’s buying a home or applying for a personal loan: by having good credit. This may reduce your interest rate because you’ll represent a lower risk to a lender.

A high residual value on the car could also help you get a better interest rate. A higher residual value means you’d have lower monthly payments because there would be less depreciation on the vehicle. Since interest is applied to your monthly payment, a lower monthly payment would equate to reduced interest charges.

The money factor is one of the many numbers you may want to learn about when leasing a car. It’s one of the transactional costs that come with leasing, and allows dealers and finance companies to make a profit on every lease they execute. As a consumer, it’s a smart idea to learn the financial implications of this number and how it’ll affect your overall costs over the course of a multi-year lease.

***

***

If the interest rate is too high, you may need to shop around for a better rate, negotiate with the dealer or lender to lower the money factor, or consider leasing another vehicle that’s more in line with your budget. Either way, make sure you explore all your financial options before taking a car off the lot.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on August 24, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

Dr. David Edward Marcinko with non-VIP patients

***

The House Committee on Oversight and Government Reform expanded its investigation of the cover-up of former President Joe Biden’s health, prostate cancer, and mental decline.

On June 4th, Chairman James Comer subpoenaed five former senior White House aides to appear for transcribed interviews in addition to Biden’s physician, Kevin O’Connor, M.D. In May, Biden revealed he was diagnosed with advanced prostate cancer. The announcement left the public dumbfounded.

At 82, having spent more than five decades as a president, vice president and senator, Biden had access to world-class medical care. Donald Trump Jr. was one of many political observers who speculated the diagnosis might have been covered up to win the 2020 election. And, Biden’s doctors may have followed standard medical guidelines, and the recommendations about screenings for people of different ages can be controversial, writes health care economist Devon Herrick at the Goodman Institute Health Care Blog.

“Experts often say that men are more apt to die with prostate cancer than from prostate cancer,” wrote Herrick. “There is even some disagreement about whether doctors should treat most occurrences of prostate cancer in older men. That partly explains why Biden had not been screened in a decade.”

Screenings can be costly, time-consuming and uncomfortable, and false positive results can lead to invasive procedures that do not markedly extend life or health. Biden made his first public remarks about his cancer after a Memorial Day event. Biden said he was “feeling good” and expected to “be able to beat this.”

QUESTION: So, was this a case of VIP Patient Paradox?

***

DEFINITION: “VIP medical patient paradox syndrome” is a term coined in 1964 by the psychiatrist Walter Weintraub to describe an intriguing paradox: Throughout history, the rich and famous, with all their resources and fancy doctors, have often received worse medical treatment, and suffered from worse health outcomes, than the average person.

Example: When physicians afford “special privileges” to their powerful patients, from “Mad King” George III to Michael Jackson, they seem to get sicker and even die.

While Weintraub, a psychoanalyst, attributed the problem in part to doctors unconsciously resenting their influential patients, it seems doctors simply get starstruck around famous people and high-ranking figures. Despite their medical expertise, these physicians find themselves opting out of basic tests for “privacy” or prescribing dangerous medications for “comfort.”

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on August 22, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

Medicine today is vastly different than a generation ago, and all health care professionals need new skills to be successful and reduce the emerging risks outlined in this textbook, as well as the “unknown-unknowns” elsewhere. Traditionally, the physician was viewed as the “captain of the ship”. Today, their role may be more akin to a ship’s navigator, using clinical, teaching skills and knowledge to chart the patient’s course through a confusing morass of insurance requirements, fees, choices, rules and regulations to achieve the best attainable clinical outcomes.

This new leadership paradigm includes many classic business school principles, now modified to fit the decade long PP-ACA, the era of health reform, and modern technical connectivity and EMRs.

Thus, the physician must be a subtle guide on the side; not bombastic sage on the stage. These, newer health 3.0 leadership philosophies might include:

•Negotiation – working to optimize appropriate treatment plans; ie., quality of life versus quantity of life, •Team play – working in concert with other allied healthcare professionals to coordinate care delivery ,ithin a clinically appropriate and cost-effective framework; •Working within the limits of competence – avoiding the pitfalls of the medical generalist versus the specialist that may restrict access to treatment, medications, physicians and facilities by clearly acknowledging when a higher degree of service is needed on behalf of the patient – all while embracing holistic primary care; •Respecting different cultures and values – inherent in the support of the medical Principle of Autonomy is the acceptance of values that may differ from one’s own. As the US becomes more culturally hetero geneous, medical providers are called upon to work within, and respect, the socio-cultural and/or spiritual framework of patients, students and their families; •Seeking clarity on what constitutes marginal care – within a system of finite resources; providers are called upon to openly communicate with patients regarding access to marginal medical information and/or treatments. •Supporting evidence-based practice – healthcare providers, should utilize outcomes data to reduce variation in treatments to achieve higher efficiencies and improved care delivery thru evidence based medicine [EBM]; •Fostering transparency and openness in communications – healthcare professionals should be willing, and prepared, to discuss all aspects of care, especially when discussing end-of-life issues or when problems arise; •Exercising decision-making flexibility – treatment algorithms, templates and clinical pathways are useful tools when used within their scope; but providers must have the authority to adjust the plan if circumstances warrant.

Becoming skilled in the art of listening and interpreting — In her ground-breaking book, Narrative Ethics: Honoring the Stories of Illness, Rita Charon, MD PhD, a professor at Columbia University, writes of the extraordinary value of using the patient’s personal story in the treatment plan. She notes that, “medicine practiced with narrative competence will more ably recognize patients and diseases; convey knowledge and regard, join humbly with colleagues, and accompany patients and their families through ordeals of illness.” In many ways, attention to narrative returns medicine full circle to the compassionate and caring foundations of the patient-physician relationship.

These thoughts represent only a handful of examples to illustrate the myriad of new skills that tomorrows’ healthcare professionals must master in order to meet their timeless professional obligations of compassionate care and contemporary treatment effectiveness; all within the context modern risk management principles.