BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on March 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITION

By Staff Reporters

***

***

1035 Exchange

DEFINITION: A method of exchanging insurance-related assets without triggering a taxable event. Cash-value life insurance policies and annuity contracts are two products that may qualify for a 1035 exchange.

***

A 1035 exchange is a feature in the tax code that permits individuals to transfer funds from an existing life insurance endowment, or annuity policy to a new one without tax consequences.

These transactions are not subject to tax deductions or tax credits but rather tax deferrals, meaning that individuals would only pay taxes on any earnings once they receive money from the policy later.

Without this provision, policyholders would have to close their previous accounts and be subjected to both taxes and surrender charges before they could open a new account.

Posted on March 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters and IRS

***

***

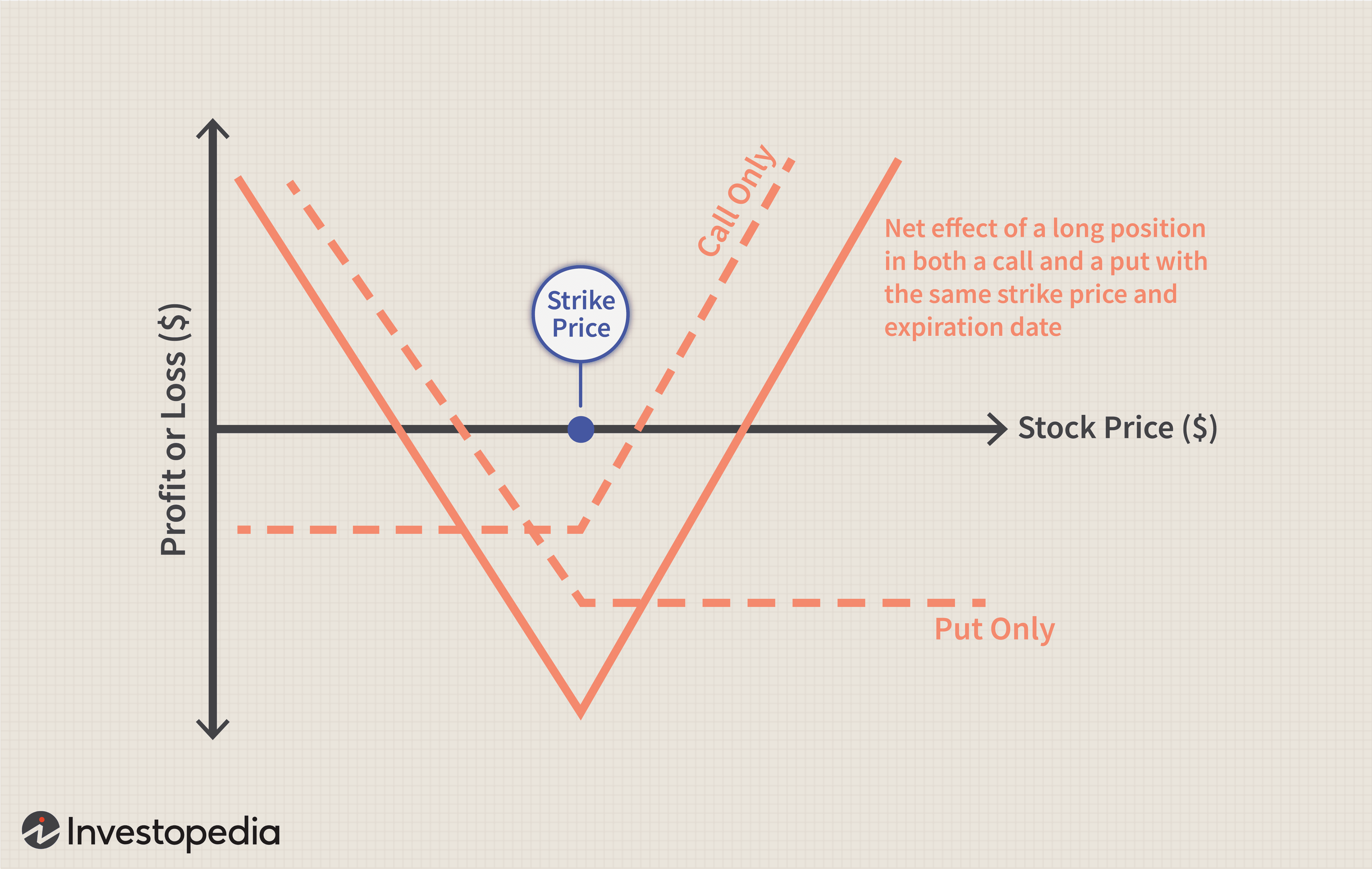

Straddles: A straddle is any set of offsetting positions on personal property. For example, a straddle may consist of a purchased option to buy and a purchased option to sell on the same number of shares of the security, with the same exercise price and period.

Personal property.

This is any actively traded property. It includes stock options and contracts to buy stock but generally does not include stock.

Straddle rules for stock.

Although stock is generally excluded from the definition of personal property when applying the straddle rules, it is included in the following two situations.

The stock is of a type that is actively traded, and at least one of the offsetting positions is a position on that stock or substantially similar or related property.

The stock is in a corporation formed or availed of to take positions in personal property that offset positions taken by any shareholder.

Note

For positions established before October 22, 2004, condition 1 above does not apply. Instead, personal property includes stock if condition 2 above applies or the stock was part of a straddle in which at least one of the offsetting positions was:

An option to buy or sell the stock or substantially identical stock or securities,

A securities futures contract on the stock or substantially identical stock or securities, or

A position on substantially similar or related property (other than stock).

Position

A position is an interest in personal property. A position can be a forward or futures contract or an option.

An interest in a loan denominated in a foreign currency is treated as a position in that currency. For the straddle rules, foreign currency for which there is an active inter bank market is considered to be actively traded personal property.

Offsetting position

This is a position that substantially reduces any risk of loss you may have from holding another position. However, if a position is part of a straddle that is not an identified straddle, do not treat it as offsetting to a position that is part of an identified straddle.

Presumed offsetting positions

Two or more positions will be presumed to be offsetting if:

The positions are established in the same personal property (or in a contract for this property), and the value of one or more positions varies inversely with the value of one or more of the other positions;

The positions are in the same personal property, even if this property is in a substantially changed form, and the positions’ values vary inversely as described in the first condition;

The positions are in debt instruments with a similar maturity, and the positions’ values vary inversely as described in the first condition;

The positions are sold or marketed as offsetting positions, whether or not the positions are called a straddle, spread, butterfly, or any similar name; or

The aggregate margin requirement for the positions is lower than the sum of the margin requirements for each position if held separately.

Related persons

To determine if two or more positions are offsetting, you will be treated as holding any position your spouse holds during the same period. If you take into account part or all of the gain or loss for a position held by a flow-through entity, such as a partnership or trust, you are also considered to hold that position.

Some Stupid Things Financial Advisors Say to Physician Clients

A few years ago and just for giggles, colleague Lon Jefferies MBA CFP® and I collected a list of dumb-stupid things said by some Financial Advisors to their doctor, dentist, nurse and and other medical professional clients, along with some recommended under-breath rejoinders:

“They don’t have any debt except for a mortgage and student loans.” OK. And I’m vegan except for bacon-wrapped steak.

“Earnings were positive before one-time charges.” This is Wall Street’s equivalent of, “Other than that Mrs. Lincoln; how was the play?”

“Earnings missed estimates.” No. Earnings don’t miss estimates; estimates miss earnings. No one ever says “the weather missed estimates.” They blame the weatherman for getting it wrong. Finance is the only industry where people blame their poor forecasting skills on reality.

“Earnings met expectations, but analysts were looking for a beat.” If you’re expecting earnings to beat expectations, you don’t know what the word “expectations” means.

“It’s a Ponzi scheme.” The number of things called Ponzi schemes that are actually Ponzi schemes rounds to zero. It’s become a synonym for “thing I disagree with.”

“The [thing not going perfectly] crisis.” Boy who cried wolf, meet analyst who called crisis.

“He predicted the market crash in 2008.” He also predicted a crash in 2006, 2004, 2003, 2001, 1998, 1997, 1995, 1992, 1989, 1984, 1971…

“More buyers than sellers.” This is the equivalent of saying someone has more mothers than fathers. There’s one buyer and one seller for every trade. Every single one.

“Stocks suffer their biggest drop since September.” You know September was only six weeks ago, right?

“We’re cautiously optimistic.” You’re also an oxymoron.

[Guy on TV]: “It’s time to [buy/sell] stocks.” Who is this advice for? A 20-year-old with 60 years of investing in front of him, or a 82-year-old widow who needs money for a nursing home? Doesn’t that make a difference?

“We’re neutral on this stock.” Stop it. You don’t deserve a paycheck for that.

“There’s minimal downside on this stock.” Some lessons have to be learned the hard way.

“We’re trying to maximize returns and minimize risks.” Unlike everyone else, who are just dying to set their money ablaze!

“Shares fell after the company lowered guidance.” Guys, they just proved their guidance can be wrong. Why are you taking this new one seriously?

“Our bullish case is conservative.” Then it’s not a bullish case. It’s a conservative case. Those words mean opposite things.

“We look where others don’t.” This is said by so many investors that it has to be untrue most of the time.

“Is [X] the next black swan?” Nassim Taleb’s blood pressure rises every time someone says this. You can’t predict black swans. That’s what makes them dangerous.

“We’re waiting for more certainty.” Good call. Like in 1929, 1999 and 2007, when everyone knew exactly what the future looked like. Can’t wait!

“The Dow is down 50 points as investors react to news of [X].” Stop it – you’re just making stuff up. “Stocks are down and no one knows why” is the only honest headline in this category.

“Investment guru [insert name] says stocks are [insert forecast].” Go to Morningstar.com. Look up that guru’s track record against their benchmark. More often than not, their career performance lags an index fund. Stop calling them gurus.

“We’re constructive on the market.” I have no idea what that means. I don’t think you do, either.

“[Noun] [verb] bubble.” (That’s a sarcastic observation from investor Eddy Elfenbein.)

“Investors are fleeing the market.” Every stock is owned by someone all the time.

“We expect more volatility.” There has never been a time when this was not the case. Let me guess, you also expect more winters?

“This is a strong buy.” What do I do with this? Click the mouse harder when placing the order in my brokerage account?

“He was tired of throwing his money away renting, so he bought a house.” He knows a mortgage is renting money from a bank, right?

“This is a cyclical bull market in a secular bear.” Vapid nonsense.

“Will Obamacare ruin the economy?” No. And get a grip.

So, don’t let these aphorisms blind you to the critical thinking skills you learned in college, honed in medical school and apply every day in life.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com

I was having lunch with a close friend of mine. He mentioned that he had accumulated a significant sum of money and did not know what to do with it. It was sitting in bonds, and inflation was eating its purchasing power at a very rapid rate.

He is a dentist and had originally thought about expanding his business, but a shortage of labor and surging wages turned expanding into a risky and low-return investment. He complained that the stock market was extremely expensive. I agreed.*

He said that the only thing left was residential real estate. I pushed back. “What do you think will happen to the affordability of houses if – and most likely when – interest rates go up? Inflation is now 6%. I don’t know where it will be in a year or two, but what if it becomes a staple of the economy? Interest rates will not be where they are today. Even at 5% interest rates [I know, a number unimaginable today] houses become unaffordable to a significant portion of the population. Yes, borrowers’ incomes will be higher in nominal terms, but the impact of the doubling of interest rates on the cost of mortgages will be devastating to affordability.”

He rejoined, “But look at what happened to housing over the last twenty years. Housing prices have consistently increased, even despite the financial crisis.”

I agreed, but I qualified his statement: “Over the past twenty, actually thirty, years interest rates declined. I honestly don’t know where interest rates will be in the future. But probabilistically, knowing what we know now, the chances that they are going to be higher, much higher, are more likely than their staying low. Especially if you think that inflation will persist.”

We quickly shifted our conversation toward more meaningful topics, like kids.

It seems that every year I think we have finally reached the peak of crazy, only to be proven wrong the next year. The stock market and thus index funds, just like real estate, have only gone one way – up. Index funds became the blunt instrument of choice in an always-rising market. So far, this choice has paid off nicely.

The market is the most expensive it has ever been, and thus future returns of the market and index funds will be unexciting. (I am being gentle here.)

You don’t have to be a stock market junkie to notice the pervasive feeling of euphoria. But euphoria is a temporary, not a permanent emotion; and at least when it comes to the stock market, it is usually supplanted by despair. Market appreciation that was driven by expanding valuations was not a gift but a loan – the type of loan that must always be paid back with a high rate of interest.

I don’t know what straw will break the feeble back of this market or what will cause the music to stop (there, you got two analogies for the price of none). We are in an environment where there are very few good options. If you do nothing, your savings will be eaten away by inflation. If you do something, you find that most assets, including the stock market as a whole, are incredibly overvalued.

We are doing the only sensible thing that you can do today. We spend very little time thinking about straws or what will cause the music to stop or how overvalued the market is. We are focusing all our energy on patiently building a portfolio of high-quality, cash-generative, significantly undervalued businesses that have pricing power.

This has admittedly been less rewarding than taking risky bets on unimaginably expensive assets. It may lack the excitement of sinking money into the darlings you see in the news every day, but we hope that our stocks will look like rare gems when the euphoria condenses into despair. As we keep repeating in every letter, the market is insanely overvalued. Our portfolio is anything but – we don’t own “the market”.

*A question may arise:Why did I not tell my dentist friend to pick individual stocks? He runs a busy dental practice and wouldn’t have the time or the training to pick stocks.

Why didn’t I offer him our services? IMA manages all my and my family’s liquid assets, but I have a rule that I never (ever!) break – I don’t manage my friends’ money. I’ll help them as much as possible with free advice but will never have a professional relationship with them. I intentionally create a separation between my personal and professional lives. After a difficult day in the market, I want to be able to go for beers with friends and leave the market at the office.

Also, this simplifies my relationships with my friends. There is no ambiguity in our friendship.

Dying Broke. It’s a goal for those retirees who embrace the idea of spending their hard-earned wealth during their lifetimes. Their aim is to enjoy the fruits of their labor while they can and spend the last penny just as they take their last breath. The concept feels both pragmatic and poetic.

But here’s the twist: While the concept may conjure images of lavish spending sprees and exotic vacations, that’s rarely what I see in practice. Many of my clients who identify as Die Brokers aren’t recklessly burning through their wealth. In fact, the opposite is often true.

This is because their approach to spending and giving is shaped by a lifetime of frugal money scripts that are incredibly hard to shake. Many Boomers grew up with financial uncertainty, learning to save and sacrifice to protect themselves and their families. Even after decades of financial success, those habits don’t just disappear. The idea of “spending down” their wealth, even intentionally, feels unnatural and irresponsible. There is an internal tug-of-war between their stated desire to enjoy their wealth and their deeply rooted fear of running out.

This paradox can significantly affect retirees’ financial planning. While Die Brokers may express a strong commitment to living fully, their money behavior often reveals a need for reassurance that their money will last for their lifetime.

For many Boomers, including myself, those frugal money scripts have served us well for decades. They’ve provided financial stability and peace of mind. But in this stage of life, they can also hold us back from experiencing the freedom we’ve worked so hard to achieve—especially in the time we have left when we can still physically enjoy it. The challenge is finding balance, honoring the values that got us here while allowing ourselves permission to live fully.

Here are four ways to start turning those old money scripts into permission to spend and give intentionally:

Reframe wealth as a tool rather than a safety net. Recognize that money is about opportunity as well as security. Spending with intention can bring joy and meaning, whether it’s funding a family trip, supporting a cause, or splurging on a bucket list item.

Work with your financial advisor to analyze your retirement spending and the probability of running out of money. The amount they suggest you can spend may surprise you—it’s often far higher than your frugal money scripts would lead you to believe.

Experiment with incremental giving. If parting with your wealth feels daunting, start small. Gift modest amounts to family, friends, or charities and notice how it feels. Seeing the immediate impact of your generosity can help ease the transition and loosen the grip of those old money scripts.

Set intentional spending goals instead of vaguely aiming to “enjoy your wealth.” Identify specific ways you want to use your money to enhance your life or the lives of others. Having a clear plan can turn spending into a meaningful act rather than an exercise in guilt.

For many of us, the Die Broke mentality is not about recklessness or extravagance. It’s about learning to let go. Despite our bold talk of spending down to the last penny, most of us will likely leave behind more than we planned. And maybe that’s just fine—especially for our kids and grand kids. Perhaps being a Die Broker is really about giving ourselves permission to live with intention, to savor what we’ve built, and to enjoy living to the fullest the rich life our frugality has helped provide.

In general, a roadshow is a series of meetings or presentations in which key members of a private company, usually executives, pitch the initial public offering, or IPO, to prospective investors. Effectively, the company is taking its branding message on the road to meet with investors in different cities, hence the name.

The IPO roadshow presentation is an important part of the IPO process in which a company sells new shares to the public for the first time. Whether a company’s IPO succeeds or not can hinge on interest generated among investors before the stock makes its debut on an exchange.

There are also some cases where company executives will embark on a road show to meet with investors to talk about their company, even if they’re not planning an IPO.

Pros and Cons of a Roadshow

According to Rebecca Lake, if the company goes public and no one buys its shares, then the IPO ends up being a flop, which can affect the company’s success in the near and long term. If the company experiences an IPO pop, in which its price goes much higher than its initial offering price, it could be a sign that underwriters mispriced the stock.

A roadshow is also important for helping determine how to price the company’s stock when the IPO launches. If the roadshow ends up being a smashing success, for example, that can cause the underwriters to adjust their expectations for the stock’s IPO price.

On the other hand, if the roadshow doesn’t seem to be generating much buzz around the company at all, that could cause the price to be adjusted downward.

In a worst-case scenario, the company may decide to pull the plug on the IPO altogether or to go a different route, such as a private IPO placement.

It has been said that most ordinary people should have at least three to six months of living expenses (not including taxes) in a cash-equivalent reserve fund that is easily accessible (i.e., liquid). The amount needed for a one-month reserve is equal to the amount of expenses for the month, rather than the amount of monthly income. This is because during no-income months there is no income tax.

However, the situation might not be the same for physicians in today’s harsh economic climate.

The New Realities

Now, some physician-focused financial advisors, financial planners and Certified Medical Planners™ suggest even more reserve fund savings; up to two years. That’s because many factors come into play when determining how much a particular doctor’s family should have.

For example:

Does the family have one income or two? If the doctor is in a dual-income family with stable incomes and they live on a single income, the need for a liquid reserve is less.

How stable is the doctor’s income source? If a sole provider with an unstable income who spends all of the income each month, the need for a liquid cash reserve is high.

Does the doctor own the practice, work in a clinic, medical group, hospital or healthcare system? In other words – employee (less control) or employer (more control).

What is the doctor’s medical specialty and how has managed care penetrated his locale, or affected her focus? What about a DO, DDS/DMD or DPM, etc.

How does the family use its income each month; does it have a saver, spender, or investor mentality?

Does the family anticipate the possibility of large expenses occurring in the future (medical practice start-up costs or practice purchase; children, medical school student debts; auto or home loans; and/or liability suits, etc)?

Pan physician lifestyle?

The Past

In the ancient past, a doctor may have opted for a nine-twelve month reserve if the need for security was high – and a six-to-nine month reserve if the need for security was low. But today, even more may be needed. How about 15-18 months, or more? Perhaps even 24 months!

So, the following questions may be helpful in determining the amount of reserve needed by the physician:

1. How long would it take you to find another job in your medical specialty if you suddenly found yourself unemployed – same for your spouse?

2. Would you have to relocate – same for your spouse?

3. How much do you spend each month on fixed or discretionary expenses and would you be willing to lower your monthly expenses if you were unemployed?

Assessment

Once the amount of reserve is determined, the doctor should use the appropriate investment vehicles for the funds.

At minimum, the reserve should be invested in a money market fund. For larger reserves, an ultra-short-term bond fund might be appropriate for amounts over three-six months. While even larger reserves might be kept in a short term bond fund depending on interest rates and trends.

So, what do the initials M.D. really mean? … More Dough!

How much reserve do you have and where is it stashed?

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Posted on February 21, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dan Ariely PhD

THE IRRATIONAL ECONOMIST

***

***

Of course you don’t need a human financial advisor … until you do. Today, we’ve had unfettered internet access to a wide range of investments, opinions and models for at least two decades. So, why the bravado to go it alone; fifteen positive years for equities, since 2009! Yet, the DJIA, S&P 500 and NASDAQ just plunged and plummeted today!

The financial advisor’s role is to remove the human element and emotion from investing decisions for something as personal as your wealth. Emotion drives the retail investor to sell low (fear) and buy high (greed). This is the reason why the average equity returns for retail investors is less than half of the S&P 500’s returns.

No, of course you don’t need a human financial advisor … until you do.

Posted on February 18, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITION

By Staff Reporters

***

***

Variable Universal Life Insurance: Permanent life insurance that allows the policyholder to vary the amount and timing of premiums and, by extension, the death benefit. Universal life insurance policies accumulate cash value which grows tax deferred. Within certain limits, policyholders can direct how this cash value will be allocated among sub-accounts offered within the policy.

Several factors will affect the cost and availability of life insurance, including age, health, and the type and amount of insurance purchased. Life insurance policies have expenses, including mortality and other charges. If a policy is surrendered prematurely, the policyholder also may pay surrender charges and have income tax implications. You should consider determining whether you are insurable before implementing a strategy involving life insurance.

Any guarantees associated with a policy are dependent on the ability of the issuing insurance company to continue making claim payments.

With international stock markets comprising about 40 percent of the world’s capitalization as of 2023, a broad range of investment opportunities exist outside the borders of the U.S.

For investors who are looking to diversify their mutual fund portfolio with exposure to companies located outside the U.S., there exist two basic choices: A global mutual fund or an international mutual fund.

By definition, international funds invest in non-U.S. markets, while global funds may invest in U.S. stocks alongside non-U.S. stocks.

Make a Choice: The definition may seem clear, but what may seem less clear is why an investor might select one over the other. The reason that an investor may select a global fund is to provide the portfolio manager with the latitude to move the fund’s investments among non-U.S. markets and the U.S. market in order to take advantage of the shifts in relative opportunities these markets may present at any given moment.

By investing in a global fund, the challenge for the investor is that he or she may not know at any point in time their total exposure to the U.S. market within the context of their overall portfolio.

An Inside Look: As a consequence, some investors want to manage their allocation risk by setting the broad asset allocation for their portfolio and then identifying funds that are within those asset classes. For these investors, an international fund may make more sense since it allows them to maintain a greater adherence to their desired domestic/international stock allocation.

Keep in mind that asset allocation is an approach to help manage investment risk. Asset allocation does not guarantee against investment loss. As you consider a global or an international fund, you should also be aware of the fund’s approach to the inherent currency risks. Some funds choose to engage in strategies that may mitigate the effects of currency fluctuations, while others consider currency movements – up and down – to be an element of portfolio performance.

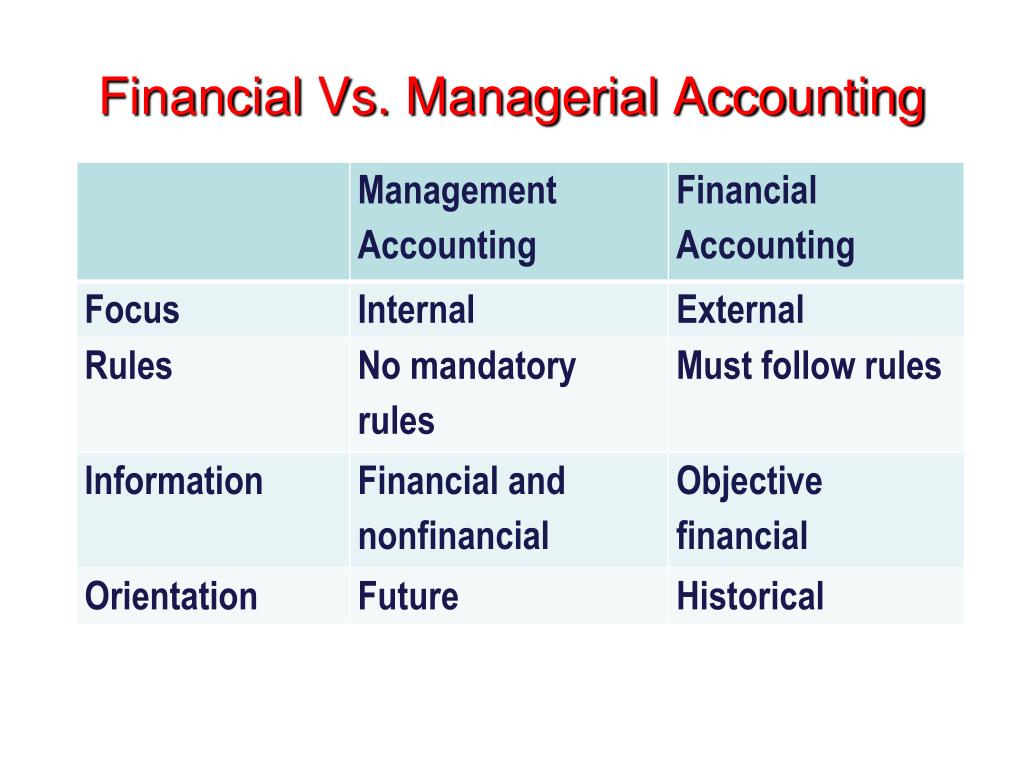

Financial accounting and managerial accounting are two distinct branches of the accounting field, each serving different purposes and stakeholders. Financial accounting focuses on creating external reports that provide a snapshot of a company’s financial health for investors, regulators, and other outside parties. Managerial accounting, meanwhile, is an internal process aimed at aiding managers in making informed business decisions.

Objectives of Financial Accounting

Financial accounting is primarily concerned with the preparation and presentation of financial statements, which include the balance sheet, income statement, and cash flow statement. These documents are meticulously crafted to reflect the company’s financial performance over a specific period, providing insights into its profitability, liquidity, and solvency. The objective is to offer a clear, standardized view of the financial state of the company, ensuring that external entities have a reliable basis for evaluating the company’s economic activities.

The process of financial accounting also involves the meticulous recording of all financial transactions. This is achieved through the double-entry bookkeeping system, where each transaction is recorded in at least two accounts, ensuring that the accounting equation remains balanced. This systematic approach provides accuracy and accountability, which are paramount in financial reporting. CPA = Certified Public Accountant.

Objectives of Managerial Accounting

Managerial accounting is designed to meet the information needs of the individuals who manage organizations. Unlike financial accounting, which provides a historical record of an organization’s financial performance, managerial accounting focuses on future-oriented reports. These reports assist in planning, controlling, and decision-making processes that guide the day-to-day, short-term, and long-term operations.

At the heart of managerial accounting is budgeting. Budgets are detailed plans that quantify the economic resources required for various functions, such as production, sales, and financing. They serve as benchmarks against which actual performance can be measured and evaluated. This enables managers to identify variances, investigate their causes, and implement corrective actions. Another objective of managerial accounting is cost analysis. Managers use cost accounting methods to understand the expenses associated with each aspect of production and operation. By analyzing costs, they can determine the profitability of individual products or services, control expenditures, and optimize resource allocation.

Performance measurement is another key objective. Managerial accountants develop metrics and key performance indicators (KPIs) to assess the efficiency and effectiveness of various business processes. These performance metrics are crucial for setting goals, evaluating outcomes, and aligning individual and departmental objectives with the overall strategy of the organization. CMA = Certified Managerial Accountant

Reporting Standards in Financial Accounting

The bedrock of financial accounting is the adherence to established reporting standards, which ensure consistency, comparability, and transparency in financial statements. Globally, the International Financial Reporting Standards (IFRS) are widely adopted, setting the guidelines for how particular types of transactions and other events should be reported in financial statements. In the United States, the Financial Accounting Standards Board (FASB) issues the Generally Accepted Accounting Principles (GAAP), which serve a similar purpose. These standards are not static; they evolve in response to changing economic realities, stakeholder needs, and advances in business practices.

For instance, the shift towards more service-oriented economies and the rise of intangible assets have led to updates in revenue recognition and asset valuation guidelines. The convergence of IFRS and GAAP is an ongoing process aimed at creating a unified set of global standards that would benefit multinational corporations and investors by reducing the complexity and cost of complying with multiple accounting frameworks.

Posted on February 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Consumer prices overall increased 3% from a year earlier, up from 2.9% the previous month, according to the Labor Department’s consumer price index, a measure of goods and service costs across the U.S. That’s the most since June and above the 2.9% expected by economists surveyed by Bloomberg.

Most U.S. stocks fell Wednesday after a report showed inflation is unexpectedly worsening for Americans.

The S&P 500 dropped 0.3%, though it had been on track for a much worse loss of 1.1% at the start of trading. The Dow Jones Industrial Average sank 225 points, or 0.5%, while the NASDAQ composite edged higher by less than 0.1%

Posted on February 12, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

DEFINITION BAR SLIDES LEFT TO RIGHT

Understanding Insurance Jargon

1. Premiums

When you purchase an insurance policy, you'll be required to make regular payments, known as premiums. These payments are typically made monthly or annually and are the cost of maintaining your insurance coverage.

2. Deductible

Think of a deductible as the money you have to shell out from your own pocket before your insurance kicks in to help cover your expenses. It's like the upfront cost you need to cover before your insurance really starts working for you.For example, if you have a $500 deductible and make a claim for $1,000, you'll need to pay $500, and your insurer will cover the remaining $500.

3. Policyholder

The policyholder is the person who owns an insurance policy. This individual is responsible for paying premiums and making claims under the policy.

4. Coverage Limit

Every insurance policy has a coverage limit, which is the maximum amount your insurer will pay out for a covered claim. It's crucial to understand your policy's limits to ensure you have adequate coverage.

5. Underwriting

Underwriting is the process insurers use to assess the risk of providing coverage to an individual or entity. It involves evaluating factors such as age, health, and driving record to determine premium rates and eligibility.

Types of Insurance

6. Auto Insurance

Auto insurance provides financial protection in case of accidents, theft, or damage to your vehicle. It's a legal requirement in many places and typically includes liability, collision, and comprehensive coverage.

7. Health Insurance

Health insurance covers medical expenses, including doctor visits, hospital stays, and prescription medications. It can be provided by employers or purchased individually.

8. Homeowners Insurance

Homeowners insurance is like a safety net for your home and stuff. It steps in to help if your place or belongings get damaged or stolen. Plus, it's got your back with liability coverage in case someone gets hurt while on your property.

9. Life Insurance

Life insurance pays out a death benefit to beneficiaries when the policyholder passes away. It can provide financial security to loved ones and cover funeral expenses.

10. Liability Insurance

Liability insurance covers you in case you're responsible for injuring someone or damaging their property. It's often included in auto and homeowners insurance policies.

Navigating Insurance Policies

11. Exclusions

Exclusions are specific events or circumstances that your insurance policy doesn't cover. It's essential to review these carefully to understand what situations won't be reimbursed.

12. Riders

Riders are add-ons to insurance policies that provide additional coverage for specific situations. For example, you can add a rider to your homeowners policy to cover expensive jewelry.

13. Claim

A claim is a formal request to your insurance company for coverage or reimbursement for a loss or damage. It's essential to follow the claims process outlined in your policy.

14. Grace Period

The grace period is the amount of time you have to pay your premium after the due date without your coverage lapsing. Be aware of your policy's grace period to avoid a lapse in coverage.

15. No-Claims Discount

Many insurance companies offer a no-claims discount to policyholders who haven't filed any claims within a specified period. This can lead to lower premiums over time.

Specialized Insurance Terms

16. Subrogation

Subrogation is the process by which an insurance company seeks reimbursement from a third party for a claim it has already paid out. This often occurs in auto accidents when your insurer goes after the at-fault driver's insurance company.

17. Actuary

An actuary is a professional who uses mathematics and statistics to assess risk and set premium rates for insurance policies. They play a crucial role in the insurance industry's financial stability.

18. Adjuster

An insurance adjuster is responsible for investigating claims, evaluating damage, and determining how much the insurance company should pay. They work to ensure fair settlements for policyholders.

19. Premium Credit

Premium credit is a discount offered by insurers to policyholders who meet specific criteria, such as having a good driving record or installing safety features in their home.

20. Salvage Value

When an insured item is damaged or totaled, it may still have some value. Salvage value refers to the amount the insurer can recover by selling the damaged item.

Protecting Your Financial Future

21. Risk Management

Effective risk management involves identifying potential risks and taking steps to minimize or mitigate them. Insurance is one tool in your risk management toolkit.

22. Beneficiary

A beneficiary is the person or entity designated to receive the proceeds of a life insurance policy when the policyholder passes away. It's essential to keep this information up to date.

23. Policy Term

The policy term is the duration for which your insurance policy is valid. It's crucial to renew your policy before it expires to maintain coverage.

24. Umbrella Policy

An umbrella policy provides additional liability coverage beyond the limits of your primary insurance policies. It can protect your assets in the event of a costly lawsuit.

25. Coinsurance

Coinsurance is the percentage of costs that you and your insurance company share after you've met your deductible. It's often seen in health insurance policies.

Insurance in Practice

26. Premium Increase

Your insurance premium may increase due to factors such as claims history, changes in coverage, or external economic conditions. It's essential to shop around for the best rates.

27. Depreciation

Depreciation is the decrease in the value of an asset over time. Insurance policies may account for depreciation when settling claims for damaged property.

28. Reinstatement

If your insurance policy lapses due to non-payment, you may have the option to reinstate it by paying any outstanding premiums and fees.

29. Excess

Excess, also known as a deductible, is the portion of a claim that you're responsible for paying. It's designed to prevent small, frequent claims.

30. Pre-Existing Condition

In health insurance, a pre-existing condition is a medical condition you had before obtaining coverage. Within the framework of the Affordable Care Act, insurance providers are prohibited from refusing coverage or imposing elevated premiums due to pre-existing medical conditions.

Insurance Regulations

31. State Insurance Department

Each state in the United States has a department or commission responsible for regulating insurance within its borders. They oversee insurers' operations and protect consumers.

32. Consumer Reports

Consumer reports provide information on insurance companies' financial strength, customer satisfaction, and claims-handling. They can help you choose a reputable insurer.

33. Guaranteed Renewal

Guaranteed renewal is a provision in some insurance policies that ensures the insurer cannot refuse to renew your policy as long as you pay your premiums.

34. Non-Cancelable Policy

A non-cancelable policy is one that the insurer cannot cancel or change the terms of as long as you pay your premiums. This provides certainty in coverage.

35. Market Conduct Examination

Insurance regulators conduct market conduct examinations to assess insurers' business practices and ensure they comply with laws and regulations.

Insurance for Businesses

36. Business Interruption Insurance

Business interruption insurance provides coverage for lost income and expenses when a covered event, such as a fire or natural disaster, forces your business to close temporarily.

37. Workers’ Compensation

Workers' compensation insurance covers medical expenses and lost wages for employees who are injured on the job. It's typically required by law for businesses with employees.

38. Professional Liability Insurance

Professional liability insurance, often called errors and omissions insurance, protects professionals from liability claims resulting from errors or negligence in their work.

39. Business Owner’s Policy (BOP)

A business owner's policy bundles essential coverages, such as property and liability insurance, into a single policy designed for small businesses. It's a cost-effective option.

40. D&O Insurance

Directors and officers (D&O) insurance protects the personal assets of company leaders in case they are sued for alleged wrongful acts while managing the business.

Advanced Insurance Concepts

41. Aggregate Limit

The aggregate limit is the maximum amount an insurance policy will pay out during a policy term, regardless of the number of claims made.

42. Risk Pooling

Insurance works on the principle of risk pooling, where policyholders collectively share the financial burden of covered losses.

43. Loss Ratio

The loss ratio is a measure of an insurance company's claims payouts compared to its earned premiums. A high loss ratio may indicate financial instability.

44. Surplus Lines Insurance

Surplus lines insurance covers risks that standard insurers won't or can't cover. It's often used for unique or high-risk situations.

45. Rescission

Rescission is the cancellation of an insurance policy retroactively, often due to misrepresentation or fraud on the policyholder's part.

Future of Insurance

46. Insurtech

Insurtech refers to the use of technology, such as artificial intelligence and data analytics, to streamline and improve the insurance industry's processes.

47. Telematics

Telematics devices track driving behavior and can lead to personalized auto insurance rates based on individual habits.

48. Microinsurance

Microinsurance provides affordable coverage to low-income individuals and communities, helping them mitigate risks and protect their assets.

49. Blockchain in Insurance

Blockchain technology can enhance transparency and security in insurance by creating immutable records of policies and claims.

50. Climate Change and Insurance

Climate change poses significant challenges to the insurance industry as it leads to more frequent and severe weather events. Insurers must adapt to these changing risk landscapes.

Insurance is a complex field with a language of its own, but understanding these 50 common insurance terms can help you navigate the world of insurance with confidence. Whether you're looking for auto, health, home, or any other type of insurance, being informed about these terms and concepts is essential to making informed decisions about your coverage.

The desire for security and feelings of insecurity are the same thing.

The idea of security, financial or otherwise, is an illusion; human life is inherently insecure. But, this doesn’t mean we shouldn’t be prudent with risk and diligent financial planning with strategies like saving and investing.

However, according to colleague Eugene Schmuckler PhD, MBA,MEd seeking security is like many things; the more you try to grasp and obsess about financial security, the more quickly you will reach a point of diminishing returns. You will feel increasingly less secure at a certain point.

Posted on February 5, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

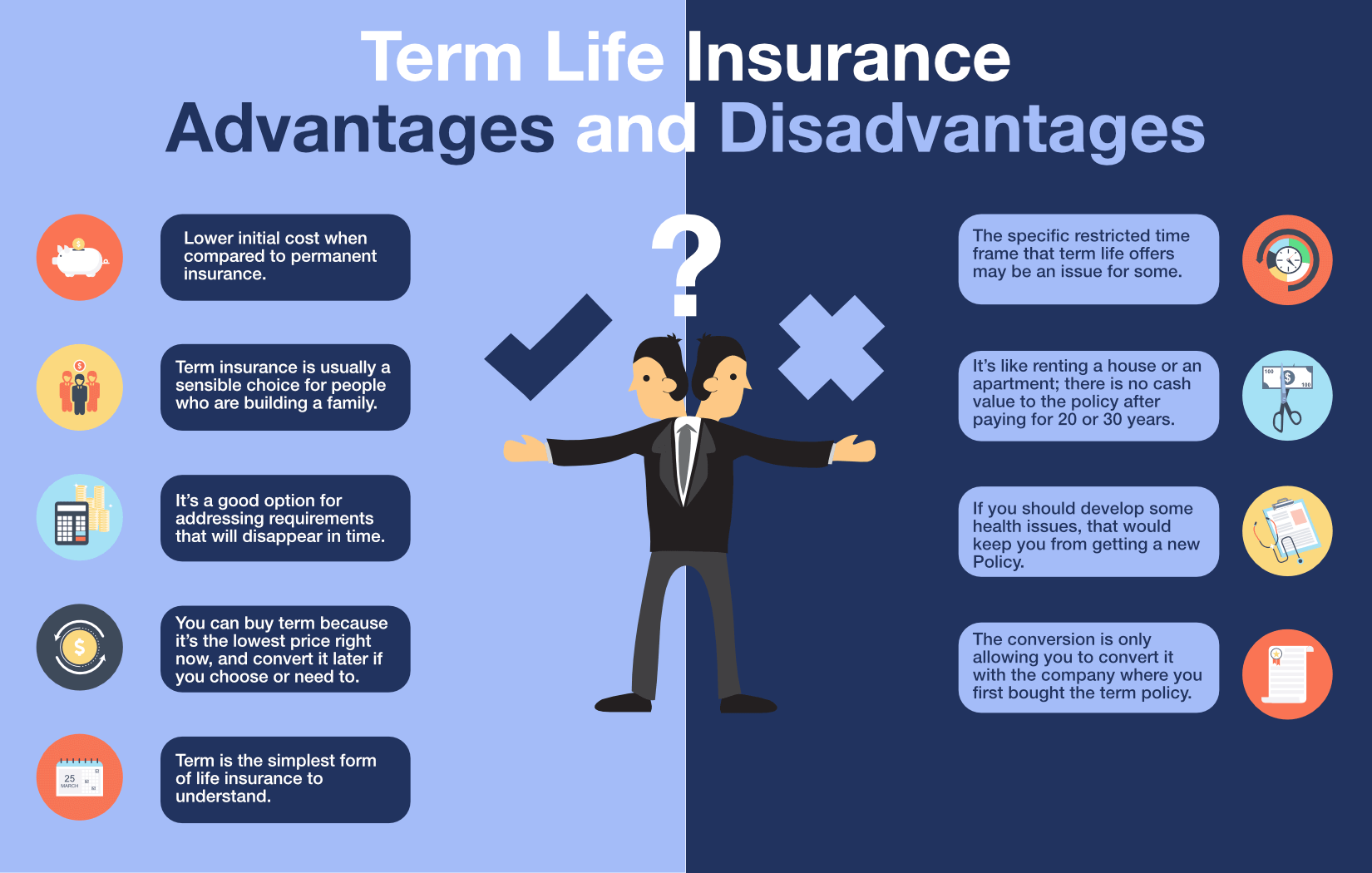

Term Insurance: Life insurance that provides coverage for a specific period. If the policyholder dies during that time, his or her beneficiaries receive the benefit from the policy. If the policyholder outlives the term of the policy, it is no longer in effect. Several factors will affect the cost and availability of life insurance, including age, health, and the type and amount of insurance purchased.

Life insurance policies have expenses, including mortality and other charges. If a policy is surrendered prematurely, the policyholder also may pay surrender charges and have income tax implications.

And, you should consider determining whether you are insurable before implementing a strategy involving life insurance. Any guarantees associated with a policy are dependent on the ability of the issuing insurance company to continue making claim payments.

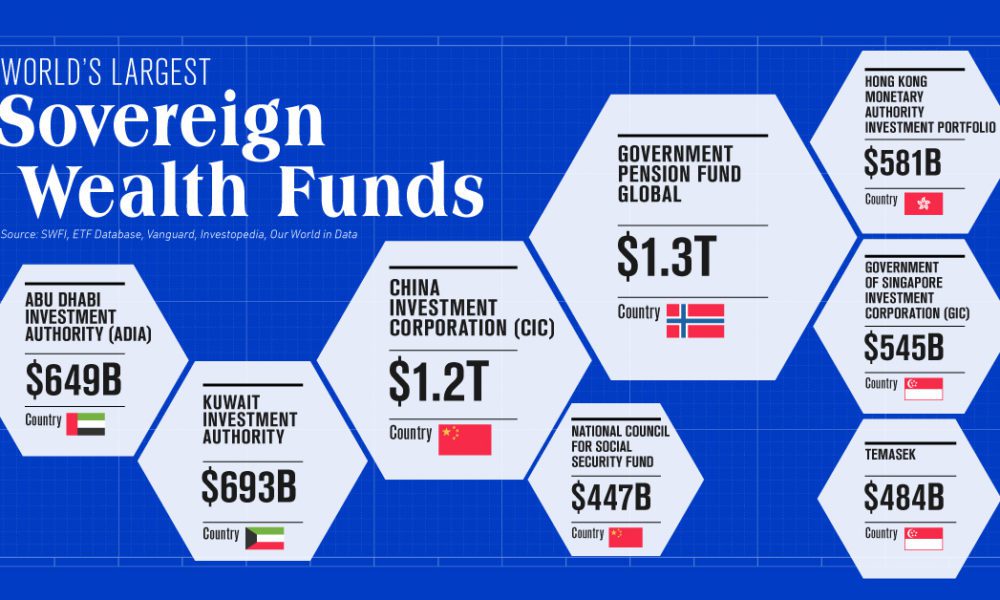

A Sovereign Wealth Fund (SWF) is a large pool of capital managed by a country’s government to achieve specific economic and social goals. These funds are invested in various assets such as stocks, bonds, real estate, commodities, and other financial instruments.

SWFs are typically funded from the savings of state-owned enterprises, foreign currency reserves from central banks, or commodity exports. The size and composition of each SWF can vary significantly between countries based on their respective economic circumstances. Each country has various reasons for setting up an SWF. However, the most common purpose of establishing one is to diversify and protect a country’s economy. For instance, this fund can be used as emergency reserves for potential future global financial shocks.

Purpose of a Sovereign Wealth Fund

Sovereign wealth funds invest a country’s wealth to achieve the government’s economic and social objectives. These funds provide countries with an additional method to diversify their economies and reduce risk exposure. They also give governments a chance to invest in global markets outside their own countries, which can get them better returns on their investments. This increases the earning potential on foreign exchanges and provides additional economic stability.

Furthermore, SWFs are a valuable tool to help countries build up buffers and savings for future generations to be better prepared for future economic shocks. Proper use of SWFs leads to long-term economic growth and stability.

In addition to providing an alternative form of investment for governments and enterprises worldwide, SWFs have also been used to increase financial transparency and accountability in many countries. By making their investment decisions public, these funds help promote corporate governance standards across the globe. This encourages market stability and reduces risks associated with certain types of investments.

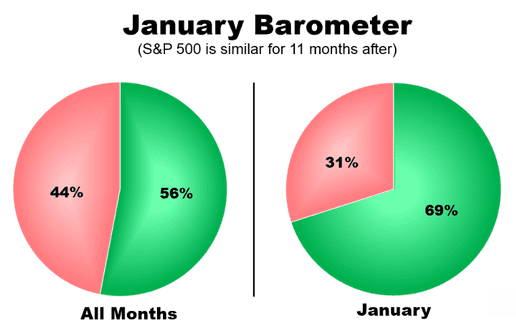

According to Rob Lenihan, of TheStreet, the January Barometer is a theory that says the investment performance of the S&P 500 in January is representative of the predicted performance of the entire year. The theory says that if stocks are higher in January, they should be higher for the year, and if they are lower in the first month, they’ll be lower for the year.

The S&P 500 finished down on January 31st, but the broad market ended up 2.6% for the month, so maybe we should heed the words of Wall Street legend Yale Hirsch, who first came up with the concept in 1972 in his Stock Trader’s Almanac, a widely read investment guide. Hirsch, by the way, also gave the world the Santa Claus Rally, which describes a rise in stock prices during the last five trading days in December and the first two trading days in the following January.

Analyst Stephen Guilfoyle said early this month in a post for TheStreet Pro that Santa Claus posted a loss this year, which was Santa’s second consecutive year in the red.

“No sweat,” the veteran trader said in his January 9th TheStreet Pro column. “That’s just a seasonal trade, and 2024 was a very nice year for U.S. equities in a broad sense.”

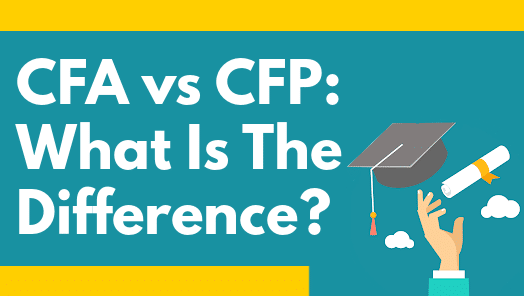

A certified financial planner (CFP®) helps individuals plan their financial futures. CFPs are not focused only on investments; they help their clients achieve specific long-term financial goals, such as saving for retirement, buying a house, or starting a college fund for their children.

To become a CFP®, a person must complete a course of study and then pass a two-part examination. The exam covers wealth management, tax palnning, insurance, retirement planning, estate planning, and other basic personal finance topics. These topics are all important for someone seeking to help clients achieve financial goals.

Chartered Financial Analyst (CFA)

A CFA, on the other hand, conducts investing in larger settings, normally for large investment firms on both the buy side and the sell side, mutual funds or hedge funds. CFAs can also provide internal financial analysis for corporations that are not in the investment industry. While a CFP® focuses on wealth management and planning for individual clients, a CFA focuses on wealth management for a corporation.

To become a CFA, a person must complete a rigorous course of study and pass three examinations over the course of two or more years. In addition, the candidate must adhere to a strict code of ethics and have four years of work experience in an investment decision-making setting.

(“Informed Voice of a New Generation of Fiduciary Advisors for Healthcare”)

For most lay folks, personal financial planning typically involves creating a personal budget, planning for taxes, setting up a savings account and developing a debt management, retirement and insurance recovery plan. Medicare, Social Security and Required Minimal Distribution [RMD] analysis is typical for lay retirement. Of course, we can assist in all of these activities, but lay individuals can also create and establish their own financial plan to reach short and long-term savings and investment goals.

But, as fellow doctors, we understand better than most the more complex financial challenges doctors can face when it comes to their financial planning. Of course, most physicians ultimately make a good income, but it is the saving, asset and risk management tolerance and investing part that many of our colleagues’ struggle with. Far too often physicians receive terrible guidance, have no time to properly manage their own investments and set goals for that day when they no longer wish to practice medicine.

For the average doctor or healthcare professional, the feelings of pride and achievement at finally graduating are typically paired with the heavy burden of hundreds of thousands of dollars in student loan debt.

You dedicated countless hours to learning, studying, and training in your field. You missed birthdays and holidays, time with your families, and sacrificed vacations to provide compassionate and excellent care for your patients. Amidst all of that, there was no time to give your finances even a second thought.

Between undergraduate, medical school, and then internship and residency, most young physicians do not begin saving for retirement until late into their 20s, if not their 30s. You’ve missed an entire decade or more of allowing your money and investments to compound and work for you. When it comes to addressing your financial health and security, there’s no time to waste.

While IAs and FAs may seem the same, they are not the same. The Financial Industry Regulatory Authority (FINRA) and the Securities Exchange Commission (SEC) have clearly defined investment advisors as distinct from financial advisors.

The term financial advisor is a generic one that can encompass many different financial professionals, although it most commonly refers to stock brokers (individuals or companies that buy and sell securities).

Investment advisor, on the other hand, is a legal term and thus has a more clear-cut definition – or at least as clear as legalese is apt to be.

KEY DIFFERENCES:

Financial advisors help with all aspects of your finances, including saving, budgeting, insurance, retirement planning, and taxes.

Investment advisors focus specifically on choosing and managing investment portfolios.

Financial advisors offer broader financial guidance, while investment advisors concentrate solely on investments.

Investment advisors are held to the fiduciary standard, while financial advisors who work as brokers may operate under different rules.

Extended equity strategies attempt to provide better returns than possible with long-only investments.

An example of an extended equity strategy is a 130/30 portfolio, which gets its designation from taking a 130% long position and a 30% short position. In practice, this would mean $100mm invested in stocks that are viewed as attractive. Next, the manager would borrow and sell short $30mm of unattractive stocks. Then the manager uses the proceeds from the short sale to buy an additional $30mm of attractive stocks. This results in a portfolio that has 130% long and 30% short exposure to stocks, or “extended” exposure to equities relative to a long-only, 100% stock portfolio.

Nevertheless, it’s important to point out that here is the risk of theoretical unlimited amount of loss with short selling, (i.e. the price of the short-sold stocks increases; the long position can only go down to $0).

Posted on December 31, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Is the Stock Market Open or Closed on New Year’s Eve?

Bond markets will close early at 2 p.m. Eastern on Tuesday, while the New York Stock Exchange and the NASDAQ Stock Market will hold regular hours from 9:30 a.m. to 4 p.m. Eastern. Over-the-counter markets, where securities trade over a broker-dealer network rather than a major exchange, will keep normal hours.

Is the Stock Market Open or Closed on New Year’s Day?

Both the U.S. bond and stock markets will be closed in observance of New Year’s Day. Over-the-counter markets will be shut, too.

What About International Markets?

Foreign exchanges, such as the London Stock Exchange, the Euronext Paris, the Stock Exchange of Hong Kong, the Shanghai Stock Exchange, and the Tokyo Stock Exchange, will be closed on Wednesday, January 1st.

Will Banks and Post Offices Be Open?

Federal Reserve banks and United States Post Service locations will be closed in observance of New Year’s Day.

Posted on December 30, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

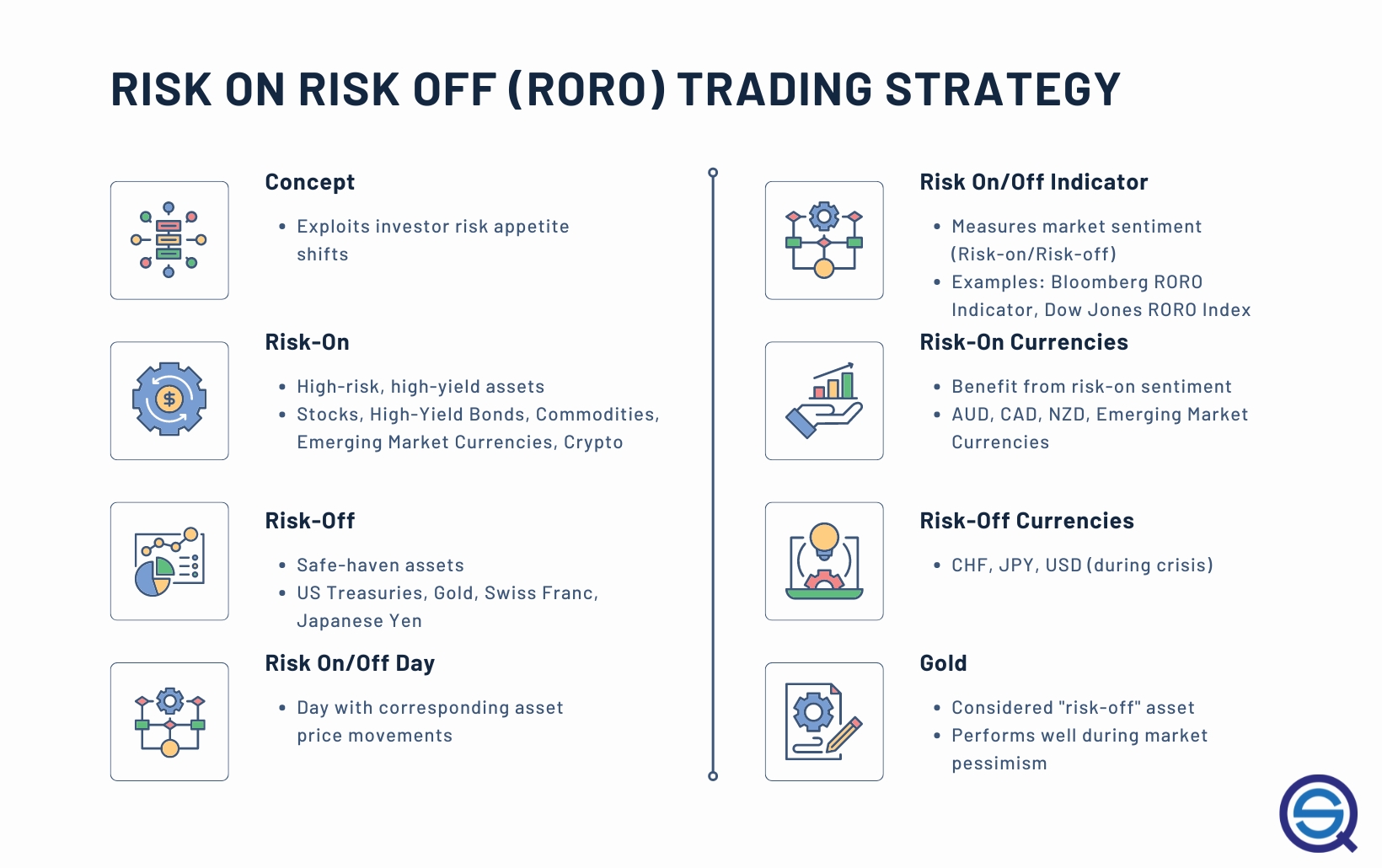

Risk-On

RO = Asset prices commonly follow the risk sentiment of the market. Investors look for changing sentiment through corporate earnings, macro-economic data, and global central bank action. An increase in the stock market or where stocks outperform bonds is said to be a risk-on environment.

Risk-on environments can be carried by expanding corporate earnings, optimistic economic outlook, accommodative central bank policies, and speculation. As the market displays strong influential fundamentals, investors perceive less risk about the market and its outlook.

Risk-Off

ROff = When stocks are selling off, and investors run for shelter to bonds or gold, the environment is said to be risk-off. Risk-off environments can be caused by widespread corporate earnings downgrades, contracting or slowing economic data, and uncertain central bank policy.

Just like the stock market rises in a risk-on environment, a drop in the stock market equals a risk-off environment. Investors jump from risky assets and pile into high grade bonds, U.S. Treasury bonds, gold, cash, and other safe havens

Risk-On Risk-Off?

Risk-on-risk-off investing relies on and is driven by changes in investor risk tolerance. Risk-on-risk-off (RORO) can also sway changes in investment activity in response to economic patterns. When risk is low, investors tend to engage in higher-risk investments. Investors tend to gravitate toward lower-risk investments when risk is perceived to be high.

“Phantom Tax” or “Phantom Income” for direct owners of Treasury inflation-protected securities (TIPS) TIPS adjust their principal values and interest payments for inflation. As with other directly owned Treasury securities, TIPS principal, including the inflation adjustments, is not paid back to investors until the securities mature.

However, the principal adjustments are taxed by the IRS as income in the year in which they occur, even though no actual payments are made in those years to investors who own TIPS directly. This is why this income is called “phantom income” and the tax on it is known as the “phantom tax.”

Investors can avoid the phantom income/tax issue for TIPS by holding TIPS in tax-deferred retirement accounts. Mutual funds and Exchange Traded Funds (ETFs) typically take the “phantom” factor out of TIPS ownership by distributing the principal adjustments as taxable dividends.

As with direct ownership of TIPS, the tax consequences of these distributions by mutual funds and ETFs can be reduced by holding TIPS-owning instruments in tax-deferred retirement accounts

HFRI Fund of Funds Composite Index invests with multiple managers through funds or managed accounts. The strategy designs a diversified portfolio of managers with the objective of significantly lowering the risk (volatility) of investing with an individual manager. The Fund of Funds manager may allocate funds to numerous managers within a single strategy, or with numerous managers in multiple strategies. The investor has the advantage of diversification among managers and styles with significantly less capital than investing with separate managers. The HFRI Fund of Funds Index is not included in the HFRI Fund Weighted Composite Index.

HFRI Fund Weighted Composite Index is a global, equal-weighted index of over 2,000 single-manager funds that report to HFR Database. Constituent funds report monthly net of all fees performance in U.S. Dollar and have a minimum of $50 Million under management or a twelve (12) month track record of active performance. The HFRI Fund Weighted Composite Index does not include Funds of Hedge Funds.

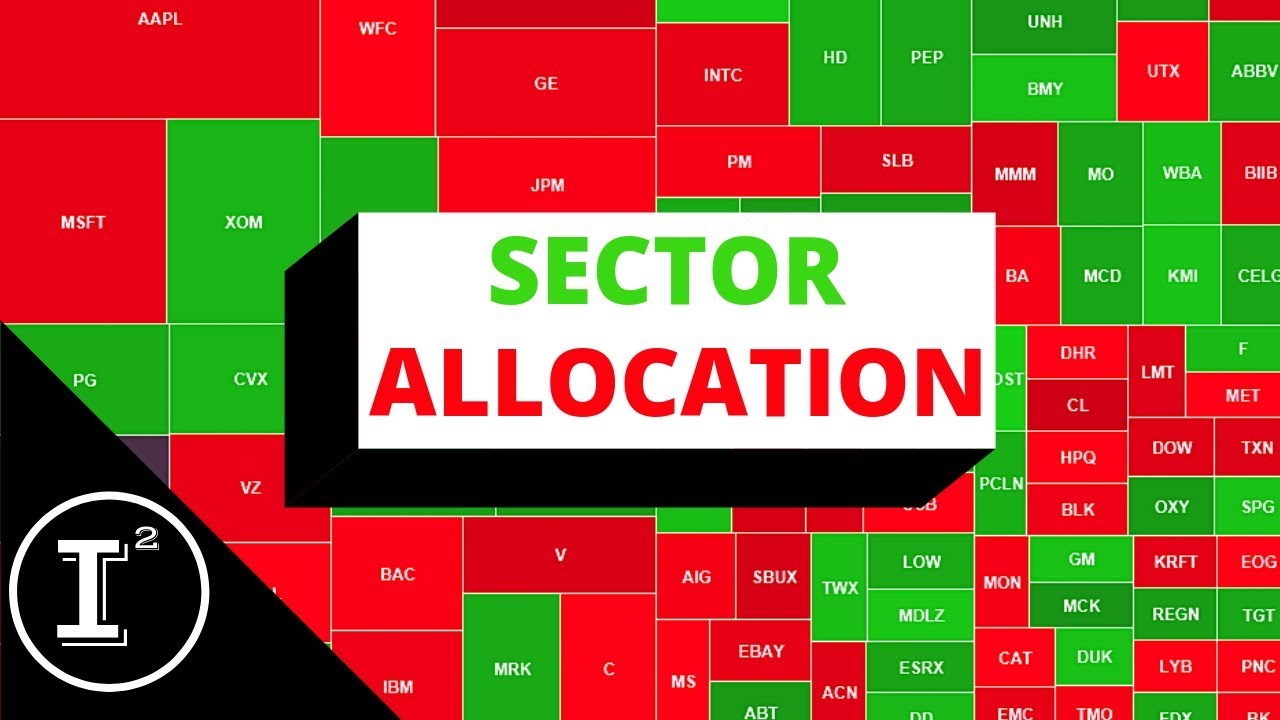

Sector allocation in an equity or fixed-income context refers to a portfolio managers’ decision to invest in a particular broad market sector or industry.

A sector allocation or breakdown can help an investor observe the investment allocations of a mutual or other fund. Fund companies regularly provide sector reporting in their marketing materials. Sector investing can influence investments in the fund. A fund may target a specific sector such as technology, or seek to diversify among many sectors.

Some funds may have restraints on sector investments. This may occur with environmental, social, and governance (ESG) focused funds. These funds seek to exclude industries or companies that their investors consider undesirable for various reasons such as tobacco producers or oil exploration companies.

The ultimate sector allocation decision is likely to combine macroeconomic views with judgments about inter-sector and intra-sector relative values, among other reasons.

Posted on December 24, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The stock market will be open on Christmas Eve 2024 but will close early at 1 p.m. ET in anticipation of Christmas Day. This early closure allows market participants to wind down ahead of the holiday.

The Federal Deposit Insurance Corporation has suspended pay bonuses for roughly two dozen executives under investigation for misconduct, a year after a Wall Street Journal investigation revealed a toxic and sexualized workplace culture at the bank regulator.

Stocks climbed on Monday as tech rallied and investors considered the path of interest rates next year after the Fed hinted they would stay higher for longer.

The S&P 500 (^GSPC) gained 0.7%, while the tech-heavy NASDAQ (^IXIC) rose almost 1%. The Dow Jones Industrial Average (^DJI) erased earlier losses to edge almost 0.2% higher.

Semiconductor stocks gained, as shares of chipmakers Nvidia (NVDA) and Broadcom (AVGO) rose more than 3% and 5%, respectively. And, robust gains from social media platform Meta (META) and EV giant Tesla (TSLA) also helped lead the broader market higher.

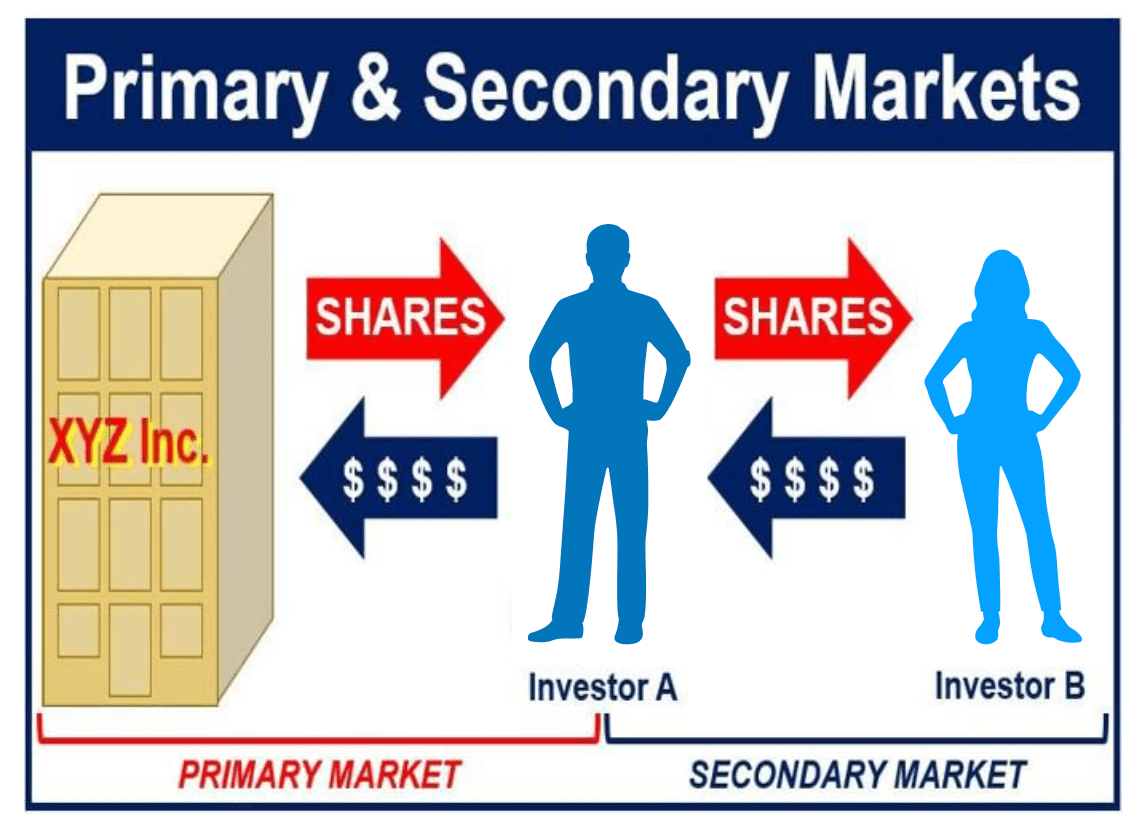

Primary Market: The primary market is also part of the stock market but differs from the secondary market because it only sells newly issued stocks.

Primary Market for Exchange Traded Funds: The primary market is where ETF shares are created and redeemed amongst ETF issuers and authorized participants. This is where the underlying basket of securities that make up an ETF is created. Shares of ETFs are made in large batches called Creation Units—usually 25,000 to 600,000 ETF shares are created at a time through this process.

Posted on December 20, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Freddie Mac (FHLMC-Federal Home Loan Mortgage Corporation)

Freddie Mac is a GSE [government-sponsored enterprise] established by Congress. It’s similar to Fannie Mae with a publicly owned corporate structure. (Freddie Mac’s stock (FRE) trades on the New York Stock Exchange.) These two giant GSEs increase liquidity in the U.S. mortgage market by purchasing mortgages from lenders, then typically repackaging (securitizing) the debt and reselling it to investors, helping to create a “secondary” market for mortgages.

The GSEs’ main purpose is to assure that mortgage money is available for borrowers. But they don’t lend money directly. Instead, they purchase mortgages from “primary” lenders like mortgage companies, banks, and credit unions. That allows the primary lenders to replenish their funds and lend more money to home buyers. The GSEs finance their mortgage purchases by issuing mortgage-backed securities (MBS) and other debt instruments (often referred to as agency debt, even though, technically, the GSEs aren’t government agencies). GSE debt is considered to have relatively high credit quality based on its implicit government backing, reinforced by what happened during the Financial Crisis in 2008.

Since Fannie Mae and Freddie Mac were placed into government conservatorship in September 2008, the government has pledged to support any shortfall in the balance sheets of the two GSEs. The U.S. Treasury has said it will ensure that both GSEs can maintain a positive net worth and fulfill all of their financial obligations. This statement of support lends credence to the very high credit ratings of MBS and other debt issued by Fannie and Freddie.

Posted on December 12, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

ALMOST ALL ABOUT CREDIT

By Staff Reporters

***

***

Credit Rating and Scoring

The category in which a credit agency classifies you is based upon payment history. Recently, credit reporting agencies have shifted away from ratings to a system known as credit scoring. Your score is determined by proprietary formulas that are based on your credit history, the higher the better. The practical benefits of this scoring system are numerous.

First, medical professionals do not need to be experts at deciphering credit reports since the same scoring system is used by many different companies.

Correcting Credit Report Errors

A credit bureau is not the place to get an item to be fixed on your credit report. Rather, you must take it up directly with the credit issuer. In any case, a late payment noted on a credit report by a durable medical equipment vendor, for example, has to be addressed directly with that merchant. The DME merchant then has 30 days to acknowledge your complaint and respond to you. In the meantime, you do not have to pay for the disputed items. Most credit errors cannot be reported or kept on your credit report for more than seven years.

For legitimate late payments you should contact the credit grantor and negotiate to take one of the following steps. Be tenacious, and either remove the late payment or write a letter explaining that the problem has been resolved and you now are a good credit risk again. This letter is a powerful tool and should be saved with other permanent financial records. The industry term for it is a letter of correction.

Credit Repair Services

Credit repair services are oversold and their claims tend to be exaggerated. They do not have an inside track to the consumer reporting agencies. Good credit repair services are experienced in communicating with creditors and can help with legitimate repairs. They cannot restore your credit rating or your good name.

However, realize that with some time and effort you can accomplish the same results yourself.

Achieving your financial, wealth and medical practice management goals is important, but handling everything on your own can be overwhelming. That’s where we come in. At D. E. Marcinko & Associates, our team of dual degree experienced physician advisors and medical consultants is here to guide you every step of the way. We believe in providing unbiased, high-quality financial and business advice.

For example, we offer a one-time written financial plan with oral evaluation for a flat fee with no ongoing sales or assets under management fees or commissions. Together, we can create a personalized financial plan tailored to your unique goals, empowering you to make confident, informed decisions as you navigate your financial future.

Other Services Include:

Estate Planning We have a network of qualified legal professionals that we can refer you to for state specific estate planning needs.

Tax Strategy We can work alongside your CPA for tax planning purposes. If needed, we can refer you to a qualified tax professional.

Investment Analysis If you have investments, we review your accounts to make sure they are aligned with your long-term goals.

401-k Allocations We evaluate your 401(k) allocations and provide recommendations that align with your goals.

Education Savings We help you explore the various ways to plan and save for education expenses.

Insurance & Risk Management We assess your insurance coverage to ensure it adequately protects you against potential risks; as well as evaluate and provide expert litigation witnesses, as needed.

Medical Practice Management We evaluate your current or potential medical practice to determine value and/or private equity offers or physician practice management formats [PPMC] for new, mid-career or retiring physicians, nurses and dentists.

D. E. Marcinko & Associates is unique and fully committed to all phases of a medical professionals personal and business life cycle. We are at your service 24/7: Email MarcinkoAdvisors@outlook.com

Municipal Securities (munis): Debt securities typically issued by or on behalf of U.S. state and local governments, their agencies or authorities to raise money for a variety of public purposes, including financing for state and local governments as well as financing for specific projects and public facilities. In addition to their specific set of issuers, the defining characteristic of munis is their tax status. The interest income earned on most munis is exempt from federal income taxes. Interest payments are also generally exempt from state taxes if the bond owner resides within the state that issued the security. The same rule applies to local taxes.

Another interesting characteristic of munis: Individuals, rather than institutions, make up the largest investor base. In part because of these characteristics, munis tend to have certain performance attributes, including higher after-tax returns than other fixed income securities of comparable maturity and credit quality and low volatility relative to other fixed-income sectors.

The two main types of munis are general obligation bonds (GOs) and revenue bonds. GOs are munis secured by the full faith and credit of the issuer and usually supported by the issuer’s taxing power. Revenue bonds are secured by the charges tied to the use of the facilities financed by the bonds.

Municipal Yield Curve: The yield curve that illustrates the yields of a certain type of municipal security at its various maturities.

Municipal Yield Ratio: A yield ratio most often used to determine the relative value of municipal securities compared with U.S. Treasury securities. The ratio consists of the yield of a municipal security of a certain maturity divided by the yield of a U.S. Treasury security of the same maturity.

Posted on December 5, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

LTC

By Anonymous Insurance Agent

***

***

Some retired people live on a fixed income and many of them live right on the edge of their financial capability. At some time in their life, they may have to make a choice regarding many purchases. In this case, we will illustrate “choice” using a couple’s purchase of Long-Term-Care Insurance [LTCI].

Of course, economics is the study of choice; wants, needs and scarcity, etc. In our case, if they decide to make the purchase they commit to a lifetime of premium payments. The financial tradeoff is this; if they make the commitment to purchase LTCI, they must give up something else.

Example: In order to maintain a monthly premium of $100 ($1,200per year), an elderly patient, retired layman or couple must essentially relegate about $30,000 of financial assets to generate the $100 necessary to make an average premium payment (assumes a 7% rate of return with 4% withdrawal rate) or [4% X $30,000 = $1,200 year]. Thus, if the monthly premium cost is $500 per month, the elder must give up the use of $150,000 of retirement asset just to generate enough cash flow to pay for the LTC insurance.

The married elder couple has to make the decision among lifestyle (dinners, vacations, gifts to children, prescription drugs, medical care or food and shelter) versus paying an insurance premium to provide for nursing home coverage for a need, which may be very real, but will not occur until sometime in the ambiguous future.

And so, when faced with such a tough economics, neither of which delivers peace of mind or a respectable solution; many will simply decide that, in either case, they may already end up impoverished.

Thus, many will often opt for the better lifestyle now … while they can enjoy it … together.

Real Bond Yield: For most bonds and other fixed-income securities, real yield is simply the yield you see listed online or in newspapers minus the premium added to help counteract the effects of inflation. Most “nominal” fixed-income yields include an “inflation premium” that is typically priced into the yields to help offset the effects of inflation.

Real yields, such as those for TIPS, don’t have the inflation premium. As a result, TIPS yields and other real yields are typically lower than most nominal yields

Negative Bond Yield: In a normal bond market environment, bond yields are positive, and bond issuers (including governments) make interest payments to investors who lend them money.

In an abnormal, or negative-yield environment, investors essentially pay the bond issuer to hold their money.

Spread duration is a risk measure, expressed in years, that estimates the price sensitivity of a fixed income investment to a 100 basis point change in credit spreads relative to similar-maturity Treasuries.

Spread sectors (aka “spread products,” “spread securities”) in fixed income parlance, are typically non-Treasury securities that usually trade in the fixed income markets at higher yields than same-maturity U.S. Treasury securities. The yield difference between Treasuries and non-Treasuries is called the “spread”), hence the name “spread sectors” for non-Treasuries.

These sectors–such as corporate-issued securities and mortgage-backed securities (MBS–typically trade at higher yields (spreads) than Treasuries because they usually have relatively lower credit quality and more credit / default risk and / or they have more prepayment risk.

Spread widening, tightening are changes in spreads that reflect changes in relative value, with “spread widening” usually indicating relative price depreciation and “spread tightening” indicating relative price appreciation.

In fixed income parlance, spreads are simply measured differences or gaps that exists between two interest rates or yields that are being compared with each other. Spreads typically exist and are measured between fixed income securities of the same credit quality, but different maturities, or of the same maturity, but different credit quality.

Changes in spreads typically reflect changes in relative value, with “spread widening” usually indicating relative price depreciation of the securities whose yields are increasing most, and “spread tightening” indicating relative price appreciation of the securities whose yields are declining most (or remaining relatively fixed while other yields are rising to meet them). Value-oriented investors typically seek to buy when spreads are relatively wide and sell after spreads tighten.

Posted on November 21, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Active investment management strategies are the opposite of passive investment strategies. Active portfolio managers regularly take investment positions that clearly differ from those of the portfolio’s performance benchmark, with the objective of outperforming the benchmark over time.

In addition to the upside potential of outperforming the benchmark, there’s also the downside possibility of under performing the benchmark. In an efficient market, there should be roughly the same magnitude of out performers and under performers for any given benchmark. But, markets are not always efficient.

Active non-transparent investment management strategies are Exchange Traded Funds that are actively managed by a portfolio manager or team of managers without daily disclosure of portfolio holdings. Active transparent strategies are daily disclosures of portfolio holdings as an attribute of traditional index-based Exchange Traded Funds (ETFs). Active transparent exchange traded funds are actively managed by a portfolio manager or team of managers. As with index-based ETFs, their portfolio holdings are disclosed daily.

NOTE: Absolute return as an investment vehicle seeks to make positive returns by employing investment management techniques that differ from traditional mutual funds. Absolute return investment techniques include using short selling, futures, options, derivatives, arbitrage, leverage and unconventional assets.

Posted on November 21, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Williams-Sonoma soared 27.50% to a record high after the home goods store beat top and bottom line earnings expectations. Its operating profit margin jumped to 17.8% from 17% last year, and the company said its board greenlit a $1 billion stock buyback plan.

Wix jumped 14.31% on a solid beat for its third quarter. Profit for the software firm reached $0.46 per share, compared to the $0.12 per share it reported last year.

Lemonade rose 16.04% after Morgan Stanley upgraded the insurance company from “underweight” to “equal-weight.” At its investor day, Lemonade unveiled a plan to juice its premiums from $1 billion to $10 billion over the next several years.

STOCKS DOWN

Ford said it was cutting 4,000 jobs in Europe, about 14% of its workforce on the continent, citing weak demand for EVs and competition from Chinese cars. Shares fell 2.90%.

Qualcomm dropped 6.34% after its first Investor Day in three years disappointed. On Tuesday, the chipmaker revealed its big plans to expand from its bread-and-butter smartphone business into making chips for cars and PCs.

Elf sank 2.23% after short seller Carson Block, the founder of Muddy Waters Research, accused the beauty company of inflating revenue.

The S&P 500® index (SPX) stayed mostly flat, up 0.13 points (0.0%) to 5,917.11; the Dow Jones Industrial Average® ($DJI) rose 139.53 points (0.32%) to 43,408.47; and the NASDAQ Composite®($COMP) fell 21.32 points (0.11%) to 18,966.14.

The 10-year Treasury note yield added four basis points to 4.41%.

The CBOE Volatility Index® (VIX) climbed to 17.26, near recent highs.