BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

After a lifetime of hard work practicing medicine and saving, you’re at the retirement finish line. Instead of a paycheck, you’re relying on your nest egg and investment income to cover the bills. Picking the right investments is even more important, as you won’t have much chance to recover as a retired MD, DO, DPM or DDS.

“You made it to the top of the mountain through a systematic approach and are trying to make your way down safely,” says retirement planner John Gillet John Gillet in Hollywood, Fla. “Why throw all caution to the wind and try something different now?”

***

***

Definitions

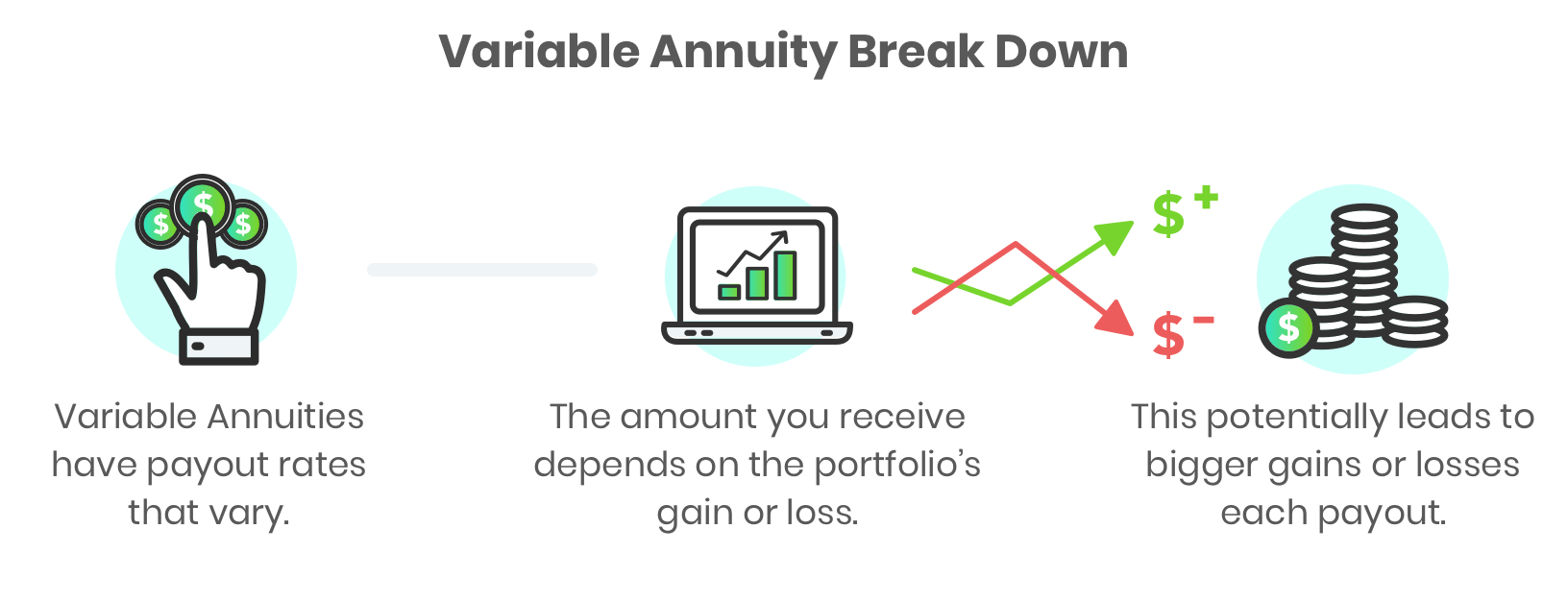

An annuity is an insurance contract designed to grow your money and then repay it as income. There are different versions. An immediate annuity turns your lump sum into future guaranteed income payments, like your own personal pension. They are simple to understand with no or small fees.

Fixed annuities pay a guaranteed interest rate over a set period to grow your money, like 5% a year for five years. These options could make sense as part of a retirement plan.

A variable annuity, on the other hand, invests your savings in mutual funds. While you can buy riders that guarantee a minimum income, you’ll be paying very much for it. “All in, the annual fees can be 3% or more of your balance,” says Jeff Bailey, an advisor from Nashville. “That’s a huge withdrawal rate from your portfolio versus investing on your own.”

The variable annuity will lock up your money for years. If you cancel early, you owe a surrender charge that could start at 7% or more of your annuity balance before gradually going down as time goes by. “Clients believe they can walk away with their contract value, but that’s often not true,” says Bailey.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Classic: A pre-payment plan refers to health insurance plans that provide medical or hospital benefits in service rather than dollars, such as the plans offered by various Health Maintenance Organizations. A method providing in advance for the cost of predetermined benefits for a population group, through regular periodic payments in the form of premiums, dues, or contributions including those contributions that are made to a health and welfare fund by employers on behalf of their employees!

Modern: A Prepaid Group Practice Plan specifies health services are rendered by participating physicians to an enrolled group of persons, with a fixed periodic payment made in advance by (or on behalf of) each person or family. If a health insurance carrier is involved, a contract to pay in advance for the full range of health services to which the insured is entitled under the terms of the health insurance contract.

Examples:

Pre-Paid Hospital Service Plan: The common name for a health maintenance organization (HMO), a plan that provides comprehensive health care to its members, who pay a flat annual fee for services.

Pre-Paid Premium: An insurance or other premium payment paid prior to the due date. In insurance, payment by the insured of future premiums, through paying the present (discounted) value of the future premiums or having interest paid on the deposit.

Pre-Paid Prescription Plan: A drug reimbursement plan that is paid in advance.

ME-P readers might believe the hedge fund industry is a small, exclusive club of elites, rich investors. But a new count by Preqin shows that it’s actually a large—and growing—sector of investing.

In fact, there may be more hedge funds globally (30,000+) than Burger King locations (18,700), and more more hedge fund managers than Taco Bell managers, per the FTE

The major indexes ticked lower last week, though, as artificial intelligence names like Oracle got hit after some analysts expressed concerns over the eye-watering costs of the AI build-out.

In the case of financial investments, compounding interest relies on time to reveal its true magic.

Here’s how: a young investor can invest less money over a longer period of time than an older investor who invests more money over a shorter period and ends up with more in the end. Compounding returns grow exponentially, making time more than an ally – but a force of the universe driving growth.

Time is certainly our ally in investing, but according to ME-P Editor Dr. David Edward Marcinko MBA MEd, you’ll kick yourself wishing you had invested earlier when you witness compounding after a few years (or a decade).

The Series 65 exam — the NASAA Investment Advisers Law Examination — is a North American Securities Administrators Association (NASAA) exam administered by FINRA.

The exam consists of 130 scored questions and 10 unscored questions. Candidates have 180 minutes to complete the exam. In order for a candidate to pass the Series 65 exam, they must correctly answer at least 92 of the 130 scored questions.

As human beings, our brains are booby-trapped with psychological barriers that stand between making smart financial decisions and making dumb ones. The good news is that once you realize your own mental weaknesses, it’s not impossible to overcome them.

In fact, Mandi Woodruff, a financial reporter whose work has appeared in Yahoo! Finance, Daily Finance, The Wall Street Journal, The Fiscal Times and the Financial Times among others; related the following mind-traps in a September 2013 essay for the finance vertical Business Insider; as these impediments are now entering the lay-public zeitgeist:

Anchoring happens when we place too much emphasis on the first piece of information we receive regarding a given subject. For instance, when shopping for a wedding ring a salesman might tell us to spend three months’ salary. After hearing this, we may feel like we are doing something wrong if we stray from this advice, even though the guideline provided may cause us to spend more than we can afford.

Myopia makes it hard for us to imagine what our lives might be like in the future. For example, because we are young, healthy, and in our prime earning years now, it may be hard for us to picture what life will be like when our health depletes and we know longer have the earnings necessary to support our standard of living. This short-sightedness makes it hard to save adequately when we are young, when saving does the most good.

Gambler’s fallacy occurs when we subconsciously believe we can use past events to predict the future. It is common for the hottest sector during one calendar year to attract the most investors the following year. Of course, just because an investment did well last year doesn’t mean it will continue to do well this year. In fact, it is more likely to lag the market.

Avoidance is simply procrastination. Even though you may only have the opportunity to adjust your health care plan through your employer once per year, researching alternative health plans is too much work and too boring for us to get around to it. Consequently, we stick with a plan that may not be best for us.

Loss aversion affected many investors during the stock market crash of 2008. During the crash, many people decided they couldn’t afford to lose more and sold their investments. Of course, this caused the investors to sell at market troughs and miss the quick, dramatic recovery.

Overconfident investing happens when we believe we can out-smart other investors via market timing or through quick, frequent trading. Data convincingly shows that people who trade most often under perform the market by a significant margin over time.

Mental accounting takes place when we assign different values to money depending on where we get it from. For instance, even though we may have an aggressive saving goal for the year, it is likely easier for us to save money that we worked for than money that was given to us as a gift.

Herd mentality makes it very hard for humans to not take action when everyone around us does. For example, we may hear stories of people making significant profits buying, fixing up, and flipping homes and have the desire to get in on the action, even though we have no experience in real estate.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Posted on September 27, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

A paradox is a statement that appears at first to be contradictory, but upon reflection then makes sense. This literary device is commonly used to engage a reader to discover an underlying logic in a seemingly self-contradictory statement or phrase. As a result, paradox allows readers to understand concepts in a different and even non-traditional

***

***

GOVERNMENT HEALTH INFORMATION IS TRUSTED?

Classic Definition: Despite the PP-ACA, there is ambivalence about the role of the US Government as a source of quality healthcare information.

Modern Circumstance: Of brands presented to respondents in a Consumer Reports (50 percent), and AARP (37 percent) survey, they outpolled the “US Government Healthcare Quality Reporting Website” (36 percent) and Medicare Website (32 percent).

Paradox Example: The focus groups expressed “mixed reactions and raised doubts about government involvement in quality ratings information. At least one participant in each group expressed skepticism about trusting ‘the government’ to compile information.”

Younger consumers especially questioned the relevance of Medicare measures to the non-elderly population. Yet participants gravitated to “.gov” websites over “.org” websites as a more authoritative source.

CITE: Williams, Jason: Health Affairs, December 28, 2016

Economy: Headline PCE rose from 2.6% on an annual basis in July to 2.7% in August, while core PCE stayed flat at 2.9%—all in line with analyst expectations.

Stocks: Solid inflation numbers helped equities arrest their recent selloff and offset the latest batch of tariffs. However, all three major indexes still ended the week lower than where they started.

Commodities: Oil climbed as Ukrainian drones continue to strike Russian energy infrastructure. Meanwhile, gold hit another all-time high, and rose above $3,800 for the first time ever at one point today.

Public Relations [PR] is differentiated than advertising in that an advertiser pays for and has control over the message. It differs from personal selling in that the message is non-personal, i.e., not directed to a particular individual patient. We pay for advertising but pray for public relations. Public relations are not controllable but it is free; advertising is not free. PR suggests that “good news or bad news”; just spell the doctors name correctly

Change Management is the discipline that guides how we prepare, equip and support individuals to successfully adopt to change in order to drive organizational success and outcomes.

For example, a senior doctor may retire, become ill, or a junior associate might become a practice partner. How will patients be affected?

Crisis Management is the precautions and identification of threats to an organization and its stakeholders, and the methods used by the organization to deal with these threats.

For example, recall in 1982, that Tylenol™ commanded 35 percent of the over-the-counter analgesic market in America and it represented nearly 17 percent of Johnson & Johnson’s profits. But, when seven people died from consuming the tainted drug, a national panic ensued. Moreover, Americans started to question the safety of all over-the-counter medications.

Fortunately, J&J commenced the proto-typical positive crisis response in the following way:

J&J acted quickly, with complete candidness about what happened and within hours of learning of the deaths, J&J installed toll-free numbers for consumers, sent alerts to healthcare providers nationwide, and stopped advertising the product. J&J recalled 31 million bottles of Tylenol™ capsules and offered replacement products free of charge. J&J did not wait for evidence to see whether the contamination might be more widespread.

J&J’s leadership was in the lead and seemed in full control throughout the crisis. The chairman was admired for his leadership to pull Tylenol™ capsules off the market and his forthrightness in dealing with the media. The Tylenol™ crisis led the news every night on every station for six weeks.

J&J placed consumers first. J&J spent more than $100 million for the recall and re-launch of Tylenol™. The stock which had been trading near a 52-week high just before the tragedy, dropped for a time, but recovered to its highs only two months later.

J&J accepted responsibility. The disaster could have been described in many different ways: as an assault on the company, as a problem somewhere in the process of getting Tylenol™ from J&J factories to retail stores, or as the acts of a crazed criminal. Yet, the company accepted full responsibility.

J&J sought to ensure that measures were taken to prevent a recurrence of the problem. J&J introduced tamper-proof packaging that would make it much more difficult for a similar incident to occur in the future.

J&J presented itself prepared to handle the short-term damage in the name of consumer safety. Within a year of the disaster, J&J’s share of the analgesic market, which had fallen to 7 percent from 37 percent following the poisoning, had climbed back to 30 percent.

This wildly successful response in now the stuff of graduate and business school case models for excellence in teaching!

PRM stands for Patient Relationship Management, which is a system for managing all interactions with current and potential patients, families, friends, referring physicians, clinics and hospitals. The goal is simple: improve relationships to grow your medical practice. PRM technology helps medical practices and clinics stay connected to patients, streamline processes, and improve profitability.

When people talk about PRM, they’re usually referring to a PRM system: software that helps track each interaction with a patient or elated others. That can include practice sales calls, treatment or service plans, marketing e-mails, website, social media and more. PRM tools can unify patient and practice data from many sources and even use Artificial Intelligence [AI] to help better manage relationships across the entire doctor– patient lifecycle – spanning departments described elsewhere in the Marketing, Advertising and Sales ME-Ps.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

References:

1. Purcarea, Victor: The impact of marketing strategies in healthcare systems. J. Med Life. 2019 Apr-Jun;12(2):93–96. doi: 10.25122/jml-2019-1003

READINGS:

Marcinko, DE and Hetico, HR: The Business of Medical Practice [3rd Edition]. Springer Publishing, New York, 2010.

Marcinko, DE and Hetico, HR: Hospitals & Healthcare Organizations [Management Strategies, Operational Techniques, Tools, Templates and Case Studies]. Productivity Press, New York, 2012.

Marcinko, DE and Hetico, HR: Financial Management Strategies for Hospitals and Healthcare Organizations [Tools, Techniques, Checklists and Case Studies]. Productivity Press, New York, 2012.

Posted on September 26, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I. and Staff Reporters

***

***

Bonds: The 10-year Treasury yield popped on solid economic data yesterday, including weekly jobless claims falling to their lowest since mid-July and Q2 GDP rising unexpectedly.

Stocks: But good news for the labor market and economy is bad news for anyone hoping the Federal Reserve cuts interest rates next month, and the major indexes sank for a third day in a row yesterday. All eyes now turn to today’s key PCE reading.

Crypto: Digital assets continued to tumble yesterday with ether falling below $4,000 for the first time in months. There may be more pain ahead: $22 billion in crypto options expire today.

[An Internet WIKI CROWD-SOURCED Curation Project]*

To keep up with the ever-changing healthcare industrial complex, we must learn new definitions and re-learn old terminology in order to correctly apply it to practice. By aggregating the most up-to-date abbreviations, acronyms, definitions and terms, the Health DictionarySeries offers a wealth of information to help understand the ever-changing terms-of-art in healthcare today.

Each 10,000 item handbook is essential for doctors, nurses, benefits managers and insurance agents, CPAs, and administrators; as well as graduate and under graduate students and professors. Our goal to for each dictionary to be designated as a Doody’s Core Title.

Dictionary of Health Insurance and Managed Care

With more than 8,000 definitions, 4,000 abbreviations and acronyms, and a 3,000 item oeuvre of resources, readings, and nomenclature derivatives, this dictionary covers the Medicare, managed care and Medicaid, private insurance, Veteran’s Administration and PP-ACA language of the entire health and long-term care insurance sector.

Dictionary of Health Economics and Finance

Health economics and finance is an integral component of the health care industrial complex. Its language is a diverse and broad-based concept covering many other industries: accounting, mathematics, the actuarial sciences, stochastics and statistics, salary reimbursements, physician payments, compensation and forecasting are all commingled arenas.

Dictionary of Health Information Technology Security

There is a myth that all healthcare stakeholders understand the meaning of information technology jargon. In truth, the vernacular of contemporary systems is unique, and often misused or misunderstood. Moreover, emerging Heath Information Technology (HIT) thru the HITECG initiatives; in the guise of terms, definitions, acronyms, abbreviations and standards; often puts the non-expert in a position of maximum uncertainty and minimum productivity.

*NOTE: A wiki website allows users to add or update content using their browser thru a hosted server created by the collaborative effort of site visitors. The Hawaiian term “wiki wiki” means “super fast.”

A Financial Self Discovery Questionnairefor Medical Professionals

For understanding your relationship with money, it is important to be aware of yourself in the contexts of culture, family, value systems and experience. These questions will help you. This is a process of self-discovery. To fully benefit from this exploration, please address them in writing. You will simply not get the full value from it if you just breeze through and give mental answers. While it is recommended that you first answer these questions by yourself, many people relate that they have enjoyed the experience of sharing them with others who are important to them.

As you answer these questions, be conscious of your feelings, actually describing them in writing as part of your process.

Childhood

What is your first memory of money?

What is your happiest moment with Money? Your most unhappy?

Name the miscellaneous money messages you received as a child.

How were you confronted with the knowledge of differing economic circumstances among people, that there were people “richer” than you and people “poorer” than you?

Cultural heritage

What is your cultural heritage and how has it interfaced with money?

To the best of your knowledge, how has it been impacted by the money forces? Be specific.

To the best of your knowledge, does this circumstance have any motive related to Money?

Speculate about the manners in which your forebears’ money decisions continue to affect you today?

Family

How is/was the subject of money addressed by your church or the religious traditions of your forebears?

What happened to your parents or grandparents during the Depression?

How did your family communicate about money?

How? Be as specific as you can be, but remember that we are more concerned about impacts upon you than historical veracity.

When did your family migrate to America (or its current location)?

What else do you know about your family’s economic circumstances historically?

Your parents

How did your mother and father address money?

How did they differ in their money attitudes?

How did they address money in their relationship?

Did they argue or maintain strict silence?

How do you feel about that today?

Please do your best to answer the same questions regarding your life or business partner(s) and their parents.

Childhood: Revisited

How did you relate to money as a child? Did you feel “poor” or “rich”? Relatively? Or, absolutely? Why?

Were you anxious about money? Did you receive an allowance? If so, describe amounts and responsibilities.

Did you have household responsibilities?

Did you get paid regardless of performance?

Did you work for money?

If not, please describe your thoughts and feelings about that.

***

***

Same questions, as a teenager, young adult, older adult.

Credit

When did you first acquire something on credit?

When did you first acquire a credit card?

What did it represent to you when you first held it in your hands?

Describe your feelings about credit.

Do you have trouble living within your means?

Do you have debt?

Adulthood

Have your attitudes shifted during your adult life? Describe.

Why did you choose your personal path? a) Would you do it again? b) Describe your feelings about credit.

Adult attitudes

Are you money motivated? If so, please explain why? If not, why not? How do you feel about your present financial situation? Are you financially fearful or resentful? How do you feel about that?

Will you inherit money? How does that make you feel?

If you are well off today, how do you feel about the money situations of others? If you feel poor, same question.

How do you feel about begging? Welfare? If you are well off today, why are you working?

Do you worry about your financial future?

Are you generous or stingy? Do you treat? Do you tip?

Do you give more than you receive or the reverse? Would others agree?

Could you ask a close relative for a business loan? For rent/grocery money?

Could you subsidize a non-related friend? How would you feel if that friend bought something you deemed frivolous?

Do you judge others by how you perceive they deal with their Money? Do you feel guilty about your prosperity? Are your siblings prosperous?

What part does money play in your spiritual life?

Do you “live” your Money values?

Conclusion

There may be other questions that would be useful to you. Others may occur to you as you progress in your life’s journey. The point is to know your personal money issues and their ramifications for your life, work, and personal mission.

This will be a “work-in-process” with answers both complex and incomplete. Don’t worry.

Just incorporate fine-tuning into your life’s process.

The bargain-hunting value style is looking for shares that are under priced in relation to the company’s future potential. A physician value investor will invest in a company in the expectation that its shares will increase in value over time. Value investing is based essentially on quantitative criteria; asset values, cash flow, and discounted future earnings. The key properties of value shares are low Price/Earnings, Price/Sales ratios, and normally higher dividend yields.

On observing a company’s earnings growth, a value manager will decide whether to buy shares based on the company’s consistency or recovery prospects.

The key research questions are: 1) Does the current P/E ratio warrant an investment in a slow growth company or, 2) Is the company a higher growth candidate that has dropped in price due to a temporary problem. If this is the case, will the company’s earnings growth recover, and if so, when? The key to value investing is to find bargain shares (priced low historically or for temporary and/or irrational reasons), avoiding shares that are merely cheap (priced low because the company is failing).

The buying opportunity is identified when a company undergoing some immediate problems is perceived to have good chances of recovery in the medium to long term. If there is a loss in market confidence in the company, the share price may fall, and the value investor can step in. Once the share price has achieved a suitable value, reflecting the predicted turnaround in company performance, the shareholding is sold, realizing a capital gain.

And, a potential risk in value investing is that the company may not turn around, in which case the share price may stay static or fall.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Posted on September 23, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

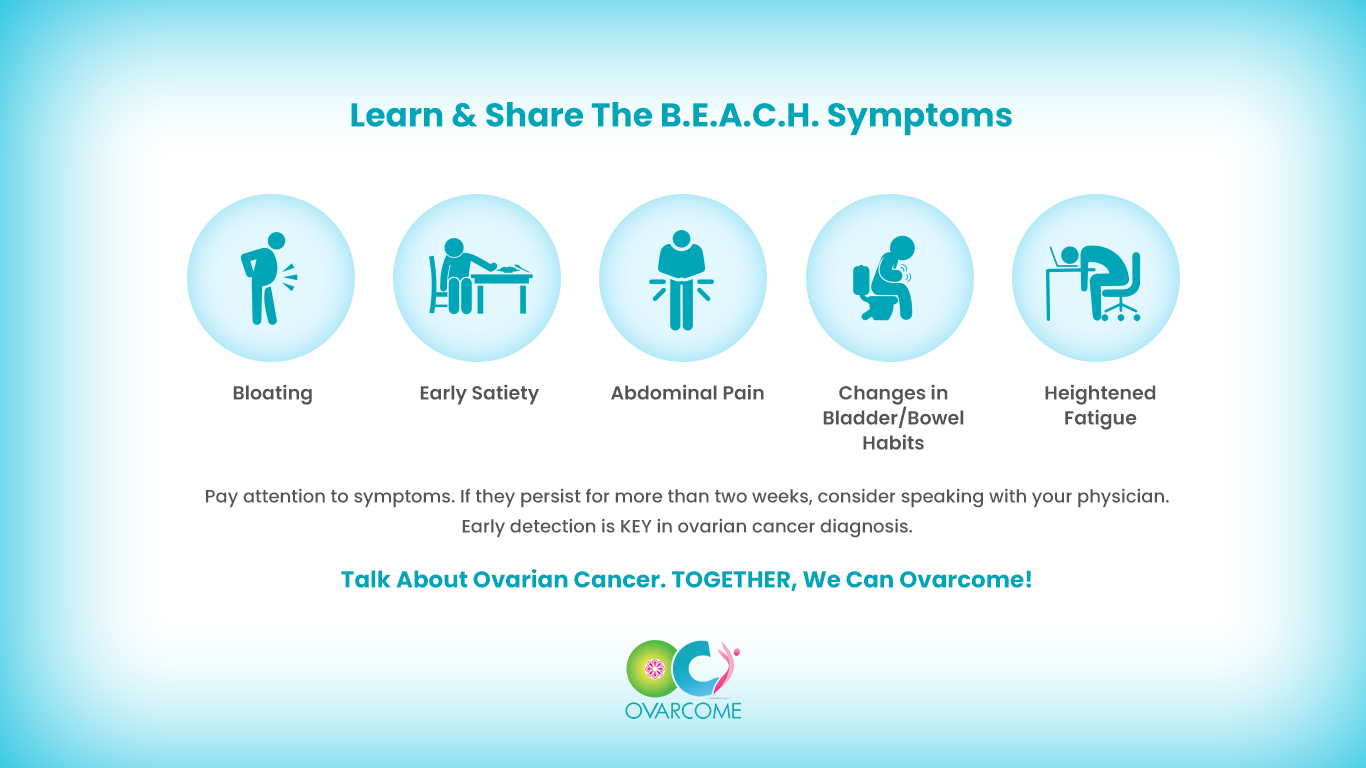

BEACH

By A.I. and Staff Reporters

***

***

Let’s talk.

September 23rd is Global Teal Talk Day, founded by Ovarcome.

Over 300,000 women are diagnosed annually with ovarian cancer, worldwide. Gather your friends, wear teal for a day out together and talk. Wearing teal is not enough.

The study of behavioral economics has revealed much about how different biases can affect our finances—often for the worse.

Take loss aversion: Because we feel a financial setback more acutely than a commensurate gain, we often cling to failed investments to avoid realizing the loss. Another potential hazard is present bias, or the tendency to prefer instant gratification over long-term reward, even if the latter gain is greater.

When it comes to money, sometimes it’s difficult to make rational decisions. Here, are three behavioral financial biases that could be impeding financial goals.

ANCHORING BIAS

Anchoring Bias happens when we place too much emphasis on the first piece of information we receive regarding a given subject. Anchoring is the mental trick your brain plays when it latches onto the first piece of information it gets, no matter how irrelevant. You might know this as a ‘first impression’ when someone relies on their own first idea of a person or situation.

Example: When shopping for a wedding ring a salesman might tell us to spend three months’ salary. After hearing this, we may feel like we are doing something wrong if we stray from this financial advice, even though the guideline provided may cause us to spend more than we can afford.

Example: Imagine you’re buying a car, and the salesperson starts with a high price. That number sticks in your mind and influences all your subsequent negotiations. Anchoring can skew our decisions and perceptions, making us think the first offer is more important than it is. Or, subsequent offers lower than they really are.

Example: Imagine an investor named Jane who purchased 100 shares of XYZ Corporation at $100 per share several years ago. Over time, the stock price declined to $60 per share. Jane is anchored to her initial price of $100 and is reluctant to sell at a loss because she keeps hoping the stock will return to her original purchase price. She continues to hold onto the stock, even as it declines, due to her anchoring bias. Eventually, the stock price drops to $40 per share, resulting in significant losses for Jane.

In this example, Jane’s nchoring bias to the original purchase price of $100 prevents her from rationalizing to sell the stock and cut her losses, even though market conditions have changed. So, the next time you’re haggling for your self, a potential customer or client, or making another big financial decision, be aware of that initial anchor dragging you down.

HERD MENTALITY BIAS

Herd Mentality Bias makes it very hard for humans to not take action when everyone around us does.

Example: We may hear stories of people making significant monetary profits buying, fixing up, and flipping homes and have the desire to get in on the action, even though we have no experience in real estate.

Example: During the dotcom bubble of the late 1990’s many investors exhibited a herd mentality. As technology stocks soared to astronomical valuations, investors rushed to buy these stocks driven by the fear of missing out on the gains others were enjoying. Even though some of these stocks had questionable fundamentals, the herd mentality led investors to follow the crowd.

In this example, the herd mentality contributed to the overvaluation of technology stocks. Eventually, it led to the dot-com bubble’s burst, causing significant losses for those who had unthinkingly followed the crowd without conducting proper research or analysis.

OVERCONFIDENT INVESTING BIAS

Overconfident Investing Bias happens when we believe we can out-smart other investors via market timing or through quick, frequent trading. This causes the results of a study to be unreliable and hard to reproduce in other research settings.

Example: Data convincingly shows that people and financial planners/advisors and wealth managers who trade most often under-perform the market by a significant margin over time. Active traders lose money.

Example: Overconfidence Investing Bias moreover leads to: (1) excessive trading (which in turn results in lower returns due to costs incurred), (2) underestimation of risk (portfolios of decreasing risk were found for single men, married men, married women, and single women), (3) illusion of knowledge (you can get a lot more data nowadays on the internet) and (4) illusion of control (on-line trading).

ASSESSMENT

Finally, questions remain after consuming this cognitive bias review.

Question: Can behavioral cognitive biases be eliminated by financial advisors in prospecting and client sales endeavors?

A: Indeed they can significantly reduce their impact by appreciating and understanding the above and following a disciplined and rational decision-making sales process.

Question: What is the role of financial advisors in helping clients and prospects address behavioral biases?

A: Financial advisors can provide an objective perspective and help investors recognize and address their biases. They can assist in creating well-structured investment and financial plans, setting realistic goals, and offering guidance to ensure investment decisions align with long-term objectives.

Question:How important is self-discipline in overcoming behavioral biases?

A; Self-discipline is crucial in overcoming behavioral biases. It helps investors and advisors adhere to their investment plans, avoid impulsive decisions, and stay focused on long-term goals reducing the influence of emotional and cognitive biases.

CONCLUSION

Remember, it is far more useful to listen to client beliefs, fears and goals, and to suggest options and offer encouragement to help them discover their own path toward financial well-being. Then, incentivize them with knowledge of the above psychological biases to your mutual success!

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

REFERENCES:

Marcinko, DE; Dictionary of Health Insurance and Managed Care. Springer Publishing Company, New York, 2007.

Marcinko, DE: Comprehensive Financial Planning Strategies for Doctors and Advisors: Best Practices from Leading Consultants and Certified Medical Planners™. Productivity Press, NY, 2016.

Marcinko, DE: Risk Management, Liability and Insurance Strategies for Doctors and Advisors: Best Practices from Leading Consultants and Certified Medical Planners™. Productivity Press, NY, 2017.

Nofsinger, JR: The Psychology of Investing. Rutledge Publishing, 2022

Winters, Scott: The 10X Financial Advisor: Your Blueprint for Massive and Sustainable Growth. Absolute Author Publishing House, 2020.

The Memory Palace Fallacy – Learning Styles Don’t Actually Exist

Remember being told you’re a “visual learner” or an “auditory learner”? Well, turns out that whole learning styles theory is pretty much bunk.

Common Learning Myths have been thoroughly debunked by modern educational research, and this is a big one. Studies consistently show that matching teaching methods to supposed learning styles doesn’t improve outcomes at all.

What actually matters is matching the teaching method to the content itself – you learn geography better with maps because geography is visual, not because you’re a “visual person.” It’s like trying to learn piano by reading about it versus actually playing keys. The activity should match what you’re trying to learn, not some made-up category about how your brain supposedly works.

Posted on September 22, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Authentication:

The verification of the identity of an individual, system, machine, or any other unique entity

Authorization:

The process of allowing access to specific areas of a system based on the role and needs of the user

Committee Charter:

A document that defines the purposes and responsibilities of the oversight committee

Compliance Risk Profile:

The current and prospective risk to earnings or capital arising from violations of or nonconformance with laws, rules, regulations, prescribed practices, internal policies and procedures, or ethical standards

Control Assessment:

A high-level review and analysis of controls relating to a process; should encompass both current and missing controls

Controls:

Methods that preserve the integrity of important information, meet operational or financial targets, and/or communicate management policies (See also: Key Control, Secondary Control, Tertiary Control)

ERM Policy Statement:

Defines an organization’s approach to and method of enterprise risk management

Governance:

Processes and structures implemented to communicate, manage, and monitor organizational activities

Impact:

The influence and effect of a risk

Inherent Risk:

Risk that is inherent to a process, taking into consideration the likelihood and impact of a risk

Key Control:

A primary control that is essential for a business process; typically takes place during the process it applies to

Key Indicators:

Measurements that are important for organizations to monitor for potential issues; examples include key performance indicators (KPIs) and key risk indicators (KRIs)

Key Performance Indicator (KPI):

A measurement with a defined set of goals and tolerances that gauges the performance of an important business activity

Key Risk Indicator (KRI):

A proactive measurement for future and emerging risks that indicates the possibility of an event that adversely affects business activities

Likelihood:

The probability of a risk occurring

Mitigation Actions:

The necessary steps, or action items, to reduce the likelihood and/or impact of a potential risk

Operation Risk Profile:

1) The risk arising from the execution of an organization’s business processes; 2) The risk of loss resulting from failed or inadequate internal processes, systems, people, or other entities

Price Risk Profile:

The risk to earning or capital arising from adverse changes in portfolio values

Process:

1) The principle elements of essential business functions within work groups or business units; 2) A set of tasks completed by business continuity plan owners within a department

Reputation Risk Profile:

The current and prospective risk to earnings or capital arising from negative public opinion or perception

Residual Risk:

Risk remaining after considering the existing control environment

Risk:

A potential event or action that would have an adverse effect on the organization

Risk Appetite:

A statement that broadly considers the risk levels that management deems acceptable

Risk Assessment:

The prioritization of potential business disruptions based on the impact and likelihood of occurrence; includes an analysis of threats based on the impact to the organization, its customers, and financial markets

Risk Tolerance:

A metric that sets the acceptable level of variation around organizational objectives and provides assurance that the organization remains within its risk appetite

Secondary Control:

An important control that typically takes place after the process it applies to (i.e., reporting or ongoing monitoring)

Strategic Risk Profile:

The current and prospective risk to earnings or capital raising from adverse business decisions, improperly implemented decisions, or lack of responsiveness to industry changes

Tertiary Control:

A non-essential control that can still be applied effectively to a business process

Velocity:

The time it takes a risk event to manifest itself

Vulnerability:

An entity’s susceptibility to a risk event as determined by the entity’s preparedness, agility, and adaptability

The Series 7 exam — the General Securities Representative Qualification Examination (GS) — assesses the competency of an entry-level registered representative to perform their job as a general securities representative.

The exam measures the degree to which each candidate possesses the knowledge needed to perform the critical functions of a general securities representative, including sales of corporate securities, municipal securities, investment company securities, variable annuities, direct participation programs, options and government securities.

Stocks: The Russell 2000 went 967 days without hitting a new record high until Thursday. But, it looks like it will have to keep waiting for the next one—the small-cap-focused index fell, even as the DJIA, NASDAQ and S&P 500 rose to new closing highs on Friday.* Bonds: 2-year yields and 10-year yields both hit two-week intra-day highs even after the FOMC cut interest rates, indicating that traders still aren’t sure how the economy will perform in the months ahead. Commodities: Arabica futures fell on reports that lawmakers will introduce a bipartisan bill to exempt coffee from tariffs.

Posted on September 19, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

What Is Pure Risk?

Pure risk is a category of risk that cannot be controlled and has two outcomes: complete loss or no loss at all. There are no opportunities for gain or profit when pure risk is involved. Pure risk is generally prevalent in situations such as natural disasters, fires, or death. These situations cannot be predicted and are beyond anyone’s control. Pure risk is also referred to as absolute risk.

***

1. Personal Risks

Now, there are basically 3 types of pure risks that concern individual physicians. These incur losses like loss of income, additional expenses and devaluation of property. There are 4 risk factors affecting them:

Premature death. This is death of a breadwinner who leaves behind financial responsibilities.

Old age / retirement. The risk of being retired without sufficient savings to support retirement years.

Health crisis. Individual with health problem may face a potential loss of income and increase in medical expenditures.

Unemployment. Jobless individual may have to live on their savings. If savings are depleted, a bigger crisis is awaiting.

2. Property Risks

This means the possibility of damage or loss to the property owned due to some cause. There are two types of losses involved.

Direct loss which means financial loss as a result of property damage.

Consequential loss which means financial loss due to the happenings of direct loss of the property.

For instance, a medical practice that burned down may incur repair costs as the direct loss. The consequential loss is being unable to run the practice business to generate income.

3. Liability Risks

A doctor is legally liable to his wrongful act that cause damage to a third party; physically, by reputation or property. S/he can be legally sued with no maximum in the compensation amount if found guilty.

Knowing how risks are classified, and the types of pure risks an individual is exposed to, will provide a fundamental overview on these risk topics and prepare you to further acquire the knowledge of how to deal with and manage them as a physician executive, leader, or manager.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on September 17, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS!

By Staff Reporters

***

***

Federal Reserve Chairman Jerome Powell just announced that the central bank [FOMC] would cut interest rates amid President Donald Trump’s attempts to reshape the Fed’s independence.

The chairman announced that the Federal Reserve would cut the interest rate by .25 points, the first time that it cut interest rates since December.

A paradox is a statement or situation that seems contradictory but actually makes sense when you think about it more deeply. It challenges logic and often reveals a hidden truth.

FLEXIBLY DOGMATIC PARADOX

The Flexibly Dogmatic Paradox suggests that no matter how sensible your financial planning, investing or wealth management process is there will be uncomfortably long periods when it looks broken. And process is the best way of ensuring you keep standing for something because if you don’t stand for something, you’ll fall for anything. This is why, when assessing an investment fund, focus 50% on the manager’s character and 50% on their process. Everything else is detail. There are few guarantees in investing, but the fact that markets will batter you emotionally is one of them.

Example: During volatile times, the temptation to abandon the process is strong. But that’s why it’s there. Process is what forces one fund manager to keep buying unbroken companies when everyone else thinks they’re bust, and another to keep faith with a top-quality company when the mob says it’s too expensive The best fund managers dogmatically stick to their process when it’s out of favor. Then, when it returns to favor, the elastic pings back: they recapture lost ground surprisingly fast. However, every rule has an exception. And spotting the exceptions to their process is something the true greats have a knack for buying and selling.

***

***

Example: In 2007, US value manager Bill Miller had the makings of an investment legend, but the financial crisis wrecked all that. His process told him to double down into falling share prices, which had worked well for years. But it doesn’t work if the companies go bust, which many of his financial stocks did in 2008.

The fact is that no matter how good it is, a process operated without human judgment is just an algorithm. The best fund managers and financial prospectors and sales men/women know this.

They stick dogmatically to their process but somehow remain flexible enough to spot the occasions when it’s about to drive them into a brick wall.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

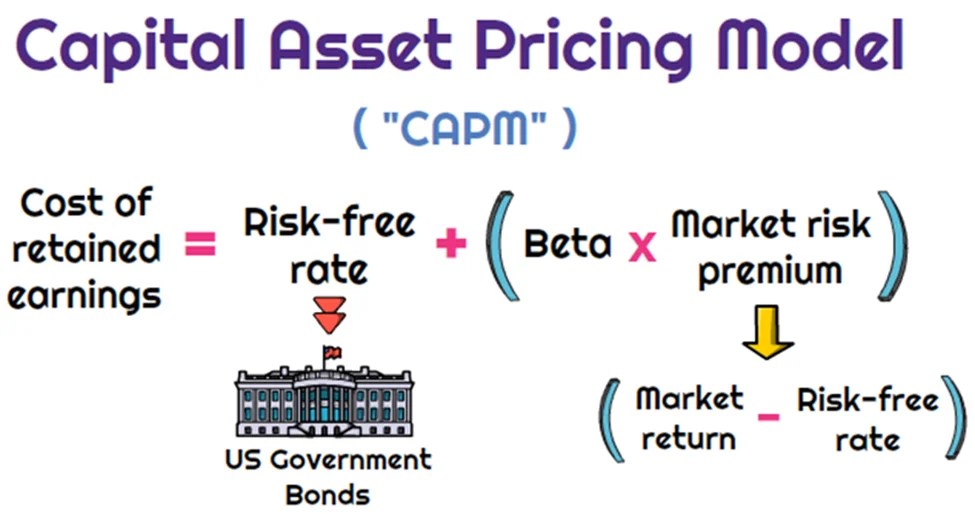

Dr. Harry Markowitz is credited with developing the framework for constructing investment portfolios based on the risk-return tradeoff. William Sharpe, John Lintner, and Jan Mossin are credited with developing the Capital Asset Pricing Model (CAPM).

CAPM is an economic model based upon the idea that there is a single portfolio representing all investments (i.e., the market portfolio) at the point of the optimal portfolio on the Capital Market Line (CML) and a single source of systematic risk, beta, to that market portfolio. The resulting conclusion is that there should be a “fair” return investors should expect to receive given the level of risk (beta) they are willing to assume.

The excess return, or return above the risk-free rate, that may be expected from an asset is equal to the risk-free return plus the excess return of the market portfolio times the sensitivity of the asset’s excess return to the market portfolio excess return. Beta, then, is a measure of the sensitivity of an asset’s returns to the market as a whole. A particular security’s beta depends on the volatility of the individual security’s returns relative to the volatility of the market’s returns, as well as the correlation between the security’s returns and the markets returns.

While a stock may have significantly greater volatility than the market, if that stock’s returns are not highly correlated with the returns of the overall market (i.e., the stock’s returns are independent of the overall market’s returns), then the stock’s beta would be relatively low. A beta in excess of 1.0 implies that the security is more exposed to systematic risk than the overall market portfolio, and likewise, a beta of less 1.0 means that the security has less exposure to systematic risk than the overall market.

MPT has helped focus investors on two extremely critical elements of investing that are central to successful investment strategies.

First, MPT offers the first framework for investors to build a diversified portfolio. Furthermore, an important conclusion that can be drawn from MPT is that diversification does in fact help reduce portfolio risk.

Thus, MPT approaches are generally consistent with the first investment rule of thumb, “understand and diversify risk to the extent possible.”

Additionally, the risk/return tradeoff (i.e., higher returns are generally consistent with higher risk) central to MPT based strategies has helped investors recognize that if it looks too good to be true, it probably is.

Passive Investing

Passive investing is a monetary plan in which an investor invests in accordance with a pre-determined strategy that doesn’t necessitate any forecasting of the economy or an individual company’s prospects. The primary premise is to minimize investing fees and to avoid the unpleasant consequences of failing to correctly predict the future. The most accepted method to invest passively is to mimic the performance of a particular index. Investors typically do this today by purchasing one or more ‘index funds’. By tracking an index, an investor will achieve solid diversification with low expenses.

An ivestor could potentially earn a higher rate of return than an investor paying higher management fees. Passive management is most widespread in the stock markets. But with the explosion of exchange traded funds on the major exchanges, index investing has become more popular in other categories of investing. There are now literally hundreds of different index funds.

Passive management is based upon the Efficient Market Hypothesis theory. The Efficient Market Hypothesis (EMH) states that securities are fairly priced based on information regarding their underlying cash flows and that investors should not anticipate to consistently out-perform the market over the long-term.

The Efficient Market Hypothesis evolved in the 1960s from the Ph.D. dissertation of Eugene Fama. Fama persuasively made the case that in an active market that includes many well-informed and intelligent investors, securities will be appropriately priced and reflect all available information. If a market is efficient, no information or analysis can be expected to result in out-performance of an appropriate benchmark. There are three distinct forms of EMH that vary by the type of information that is reflected in a security’s price:

Weak Form

This form holds that investors will not be able to use historical data to earn superior returns on a consistent basis. In other words, the financial markets price securities in a manner that fully reflects all information contained in past prices.

Semi-Strong Form

This form asserts that security prices fully reflect all publicly available information. Therefore, investors cannot consistently earn above normal returns based solely on publicly available information, such as earnings, dividend, and sales data.

Strong Form

This form states that the financial markets price securities such that, all information (public and non-public) is fully reflected in the securities price; investors should not expect to earn superior returns on a consistent basis, no matter what insight or research they may bring to the table.

While a rich literature has been established regarding whether EMH actually applies in any of its three forms in real world markets, probably the most difficult evidence to overcome for backers of EMH is the existence of a vibrant money management and mutual fund industry charging value-added fees for their services.

The notion of passive management is counterintuitive to many investors. Passive investing proponents follow the strong market theory of EMH. These proponents argue several points including;

In the long term, the average investor will have a typical before-costs performance equal to the market average. Therefore the standard investor will gain more from reducing investment costs than from attempting to beat the market over time.

The efficient-market hypothesis argues that equilibrium market prices fully reflect all existing market information. Even in the case where some of the market information is not currently reflected in the price level, EMH indicates that an individual investor still cannot make use of that information. It is widely interpreted by many academics that to try and systematically “beat the market” through active management is a fools game.

Not everyone believes in the efficient market. Numerous researchers over the previous decades have found stock market anomalies that indicate a contradiction with the hypothesis. The search for anomalies is effectively the hunt for market patterns that can be utilized to outperform passive strategies. Such stock market anomalies that have been proven to go against the findings of the EMH theory include;

Low Price to Book Effect

January Effect

The Size Effect

Insider Transaction Effect

The Value Line Effect

All the above anomalies have been proven over time to outperform the market. For example, the first anomaly listed above is the Low Price to Book Effect. The first and most discussed study on the performance of low price to book value stocks was by Dr. Eugene Fama and Dr. Kenneth R. French. The study covered the time period from 1963-1990 and included nearly all the stocks on the NYSE, AMEX and NASDAQ. The stocks were divided into ten subgroups by book/market and were re-ranked annually. In the study, Fama and French found that the lowest book/market stocks outperformed the highest book/market stocks by a substantial margin (21.4 percent vs. 8 percent). Remarkably, as they examined each upward decile, performance for that decile was below that of the higher book value decile. Fama and French also ordered the deciles by beta (measure of systematic risk) and found that the stocks with the lowest book value also had the lowest risk.

Today, most researchers now deem that “value” represents a hazard feature that investors are compensated for over time. The theory being that value stocks trading at very low price book ratios are inherently risky, thus investors are simply compensated with higher returns in exchange for taking the risk of investing in these value stocks. The Fama and French research has been confirmed through several additional studies. In a Forbes Magazine 5/6/96 column titled “Ben Graham was right–again,” author David Dreman published his data from the largest 1500 stocks on Compustat for the 25 years ending 1994. He found that the lowest 20 percent of price/book stocks appreciably outperformed the market.

One item a medical professional should be aware of is the strong paradox of the efficient market theory. If each investor believes the stock market were efficient, then all investors would give up analyzing and forecasting. All investors would then accept passive management and invest in index funds. But if this were to happen, the market would no longer be efficient because no one would be scrutinizing the markets. In actuality, the efficient market hypothesis actually depends on active investors attempting to outperform the market through diligent research.

The case for passive investing and in favor of the EMH is that a preponderance of active managers do actually underperform the markets over time. The latest study by Standard and Poor’s (S&P) confirms this fact. S&P recently compared the performance of actively-managed mutual funds to passive market indexes twice per year. The 2012 S&P study indicated that indexes were once again outperforming actively-managed funds in nearly every asset class, style and fund category. The lone exception in the 2012 report was international equity, where active outperformed the index that S&P chose. The study examined one-year, three-year and five-year time periods. Within the U.S. equity space, active equity managers in all the categories failed to outperform the corresponding benchmarks in the past five year period. More than 65 percent of the large-cap active managers lagged behind the S&P 500 stock index. More than 81 percent of mid-cap mutual funds were outperformed by the S&P MidCap 400 index.

Lastly, 77 percent of the small-cap mutual funds were outperformed by the S&P SmallCap 600 index. U.S. bond active managers fared no better that equity managers over a five year period. More than 83 percent of general municipal mutual funds under-performed the S&P National AMT-Free Municipal Bond index, 93 percent of government long-term funds under-performed the Barclays Long Government index, nearly 95 percent of high yield corporate bond funds under-performed the Barclays High Yield index. Although the performance measurements for index investing are very strong, many analysts find three negative elements of passive investing;

Downside Protection: When the stock market collapses like in 2008, an index investor will assume the same loss as the market. In the case of 2008, the S&P 500 stock index fell by more than 50 percent, offering index investors no downside protection.

Portfolio Control: An index investor has no control over the holdings in the fund. In the event that a certain sector becomes over-owned (i.e. technology stocks in 2000), an index investor maintains the same weight as the index.

Average Returns: An index investor will never have the opportunity to outperform the market, but will always follow. Although the markets are very efficient, an investor can perhaps take advantage of market anomalies and invest with those managers who have maintained a long-term performance edge over the respective index.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

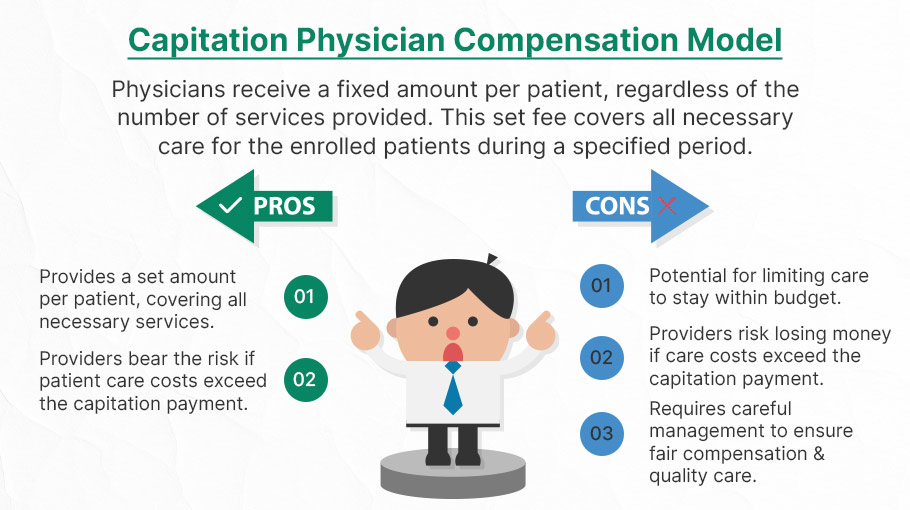

Capitation is a type of healthcare payment system in which a physician or hospital is paid a fixed amount of money per patient for a prescribed period by an insurer or physician association. The cost is based on the expected healthcare utilization costs for a group of patients for that year.

With capitation, the physician—otherwise known as the primary care physician— is paid a set amount for each enrolled patient whether a patient seeks care or not. The PCP is usually contracted with an HMO whose role it is to recruit patients.

According to Richard Eskow, CEO of Health Knowledge Systems of Los Angeles, capitated medical reimbursement has been used in one form or another, in every attempt at healthcare reform since the Norman Conquest. Some even say an earlier variant existed in ancient China [personal communication].

Initially, when Henry I assumed the throne of the newly combined kingdoms of England and Normandy, he initiated a sweeping set of healthcare reforms. Historical documents, though muddled, indicate that soon thereafter at least one “physician,” John of Essex, received a flat payment honorarium of one penny per day for his efforts. Historian Edward J. Kealey opined that sum was roughly equal to that paid to a foot-soldier or a blind person. Clearer historical evidence suggests that American doctors in the mid-19th century were receiving capitation-like payments. No less an authoritative figure than Mark Twain, in fact, is on record as saying that during his boyhood in Hannibal, MO his parents paid the local doctor $25/year for taking care of the entire family regardless of their state of health.

Later, Sidney Garfield MD [1905-1984] is noted as one of the great under-appreciated geniuses of 20th century American medicine stood in the shadow cast by his more celebrated partner, Henry J. Kaiser. Garfield was not the first physician to embrace the notion of prepayment capitation, nor was he the first to understand that physicians working together in multi-specialty groups could, through collaboration and continuity of care, outperform their solo practice colleagues in almost every measure of quality and efficiency. The Mayo brothers, of course, had prior claim to that distinction. What Garfield did, was marry prepayment to group practice, providing aligned financial incentives across every physician and specialty in his medical group, as well as a culture of group accountability for the care of every member of the affiliated health plan. He called it “the new economics of medicine,” and at its heart was a fundamentally new paradigm of care that emphasized – prevention before treatment – and health before sickness. Under his model: the fewer the sick – the greater the remuneration. And: the less serious the illness, the better off the patient and the doctors.

Such ideas were heresy to the reigning fee-for-service, solo practice, ideologues of the mainstream medical establishment of the 1940s and ‘50s, of course. Throughout the period, Garfield and his group physicians were routinely castigated by leaders of the AMA and county medical associations as socialistic and unethical. The local medical associations in Garfield’s expanding service areas – the San Francisco Bay Area, Los Angeles, and Portland, Oregon – blocked group practice physicians from association membership, effectively shutting them out of local hospitals, denying them patient referrals or specialty society accreditation. Twice in the 1940s, formal medical association charges were brought against Garfield personally, at one time temporarily succeeding in suspending his license to practice medicine.

Of course, capitation payments made a comeback in the first cost-cutting managed care era of the 1980-90s because fee-for-service medicine created perverse incentives for physicians by paying more for treating illnesses and injuries than it does for preventing them — or even for diagnosing them early and reducing the need for intensive treatment later. Nevertheless, the modern managed care industry’s experience with capitation wasn’t initially a good one. The 1980-90s saw a number of HMOs attempt to put independent physicians, especially primary care doctors, into a capitation reimbursement model. The result was often negative for patients, who found that their doctors were far less willing to see them — and saw them for briefer visits — when they were receiving no additional income for their effort. Attempts were also made to aggregate various types of health providers — including hospitals and physicians in multiple specialties — into “capitation groups” that were collectively responsible for delivering care to a defined patient group. These included healthcare facilities and medical providers of all types: physicians, osteopaths, podiatrists, dentists, optometrists, pharmacies, physical therapists, hospitals and skilled nursing homes, etc.

However, the healthcare industry isn’t collective by nature, and these efforts tended to be too complicated to succeed. One lesson that these experiments taught is that provider behavior is difficult to change unless the relationship between that behavior and its consequences is fairly direct and easy to understand.

Today, the concept of prepayment and medical capitation is to uncouple compensation from the actual number of patients seen, or treatments and interventions performed. This is akin to a fixed price restaurant menu, as opposed to an àla carte eatery.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on September 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

BREAKING NEWS

Law enforcement officials in Utah released a video of the suspected shooter in the assassination of Turning Point USA co-founder and CEO Charlie Kirk, saying that the person wore Converse tennis shoes and left a hand print and a shoe print at the scene.

The suspect in Charlie Kirk’s assassination has been identified as Tyler Robinson, a 22-year-old Utah resident. Law enforcement sources told the Daily Mail that Robinson was taken into custody as the alleged assassin who killed Kirk at a rally at Utah Valley University on Wednesday.

Before today, forensic podiatry has even made it into the public zeitgeist with the hit TV show “Bones” which premiered on September 13, 2005, and concluded on March 28, 2017, airing for 246 episodes over 12 seasons. The show was based on forensic anthropology and forensic archaeology, with each episode focusing on the mystery behind human body remains brought in for examination and identification.

In one show, eight pairs of dismembered feet washed ashore after a flood on the U.S.-Canada border, but things didn’t add up when only seven pairs of feet were identified as research corpses from a nearby university body farm.

When the fictional Canadian forensic podiatrist Dr. Douglas Filmore took the remains back to Canada, he had to form a jurisdictional alliance with the United States to match the pairs of feet and identify the victims. A rare and expensive pair of sneakers led the team to the victim’s murderer.

In 2016, an actual forensic podiatry club was started at the Barry University School of Podiatric Medicine. And, a formal class covering aspects of forensic podiatry is held at the New York College of Podiatric Medicine. Students exit the class with an in depth knowledge of forensic podiatry and other legal knowledge applicable to current cases.

More expertly, real-life colleague Michael Steven Nirenberg DPMactually testified in the murder trial of defendants Kailie Brackett and Donnell Dana with the state calling three witnesses to testify, including the podiatrist who claimed Brackett’s footprints match the ones found in blood at the apartment of the victim, Kimberly Neptune. The forensic podiatrist focused on the footprints discovered at Neptune’s apartment, using prints and images of the defendant’s feet taken by law enforcement. After study, he claimed the prints at the scene bore a resemblance to Kailie Brackett’s in the width of the foot. The defense questioned the field of forensic podiatry and pressed Dr. Nirenberg on whether the measurements would be altered depending on how thick the sock covering the foot was woven.

Dr. Nirenberg was also interviewed on National Public Radio’s Morning Edition on April 14th 2023 about the gait of the bombing suspect associated with the capital riot on Wednesday January 6th, 2021. Dr. Nirenberg is president of the American Society of Forensic Podiatry and co-editor of the textbook: “Forensic Gait Analysis: Principles and Practice”. The bombing suspect had placed bombs at the DNC and RNC headquarters in Washington, DC on the night before. NPR asked Dr. Nirenberg to comment on the features of the person’s gait.

Additionally, Nirenberg was interviewed by Nancy Grace on her TV show Crime Stories. Grace interviewed Nirenberg about his forensic podiatry work in helping to solve the murder of a mother of 3 who was killed in a church. The case remains unsolved. The episode, “Fitness-Mom Missy Bevers Bludgeoned Dead in Creekside Church” aired June 6th, 2024 and is available online at Merit+ TV.

And, Netflix’s 2023 docu-series, “Till Murder Do Us Part”, recounts the killings of Derek and Nancy Haysom by including a series of interviews with a cast of real people. The four-part docu-series revolves around the unpacking of how a wealthy couple was murdered in Virginia in 1985. It also focuses on how the suspects, Elizabeth Haysom, and her boyfriend, Jens Soehring, betrayed each other during the trial. Dr. Sarah Reel DPM was the forensic podiatrist who was involved with Jens’ and Elizabeth’s footprint examination. Dr. Reel pointed out that, statistically, there was no difference “between a bare footprint and a socked footprint.” The doctor suggested that Jens’ reference footprint matched closely with the crime scene footprint.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on September 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I. and Staff Reporters

***

***

Stocks: The NASDAQ rose to its fifth record high of the week, while the S&P 500 and the Dow sank late in the day as investors turned their attention to the FOMC meeting next week.

Bonds: While equities climbed all week long, the bond market has been sending signals that weak economic data really isn’t great news.

Commodities: Oil rallied after President Trump expressed his growing frustration with Vladimir Putin and threatened further energy and financial sanctions. Meanwhile, the US may ask its G7 counterparts to apply 100% tariffs against China and India for purchasing Russian crude.

Posted on September 12, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I. and Staff Reporters

***

***

BIAS

Bias is a prejudice in favor of or against one thing, person, or group compared with another, usually in a way considered to be unfair.

MYOPIA

Myopia (nearsightedness) is a common condition that’s usually diagnosed before age 20. It affects your distance vision — you can see objects that are near, but you have trouble viewing objects that are farther away like grocery store aisle markers or road signs. Myopia treatments include glasses, contact lenses or surgery.

MYOPIA BIAS

Myopia Bias makes it hard for us to imagine what our lives might be like in the future.

FinancialExample: When we are young, healthy and in our prime economic earning years it may be hard for us to picture what life will be like when our health depletes and we no longer have the earnings necessary to support our standard of living.

Irony: This short-sightedness makes it hard to save adequately when we are young … when saving does the most good.

When owners of a security spread false information to pump up the price of the security and subsequently sell off their shares, making a profit—the “dump.”

Refer to attempts by investors to move the price of a stock opportunistically by selling large numbers of shares short. The investors pocket the difference between the initial price and the new, lower price after this maneuver. This technique is illegal under SEC rules, which stipulate that every short sale must be on an uptick. For more information on this complex tactic, read on in this piece from the Wharton School of Business.

Wash Trading

Involves the simultaneous or near-simultaneous sale and repurchase of the same security for the purpose of generating activity and increasing the price.

When fraudsters manipulate the market through matched orders, they enter trades to buy or sell securities with the knowledge that a matching order on the opposite side has been or will be entered. During his tenure at the Commission, our partner Jordan Thomas was involved in a case where the SEC won summary judgement and obtained settlements with an astonishing 16 defendants who engaged in matched trades, among other illicit tactics.

Painting the Tape

Painting the tape refers to placing successive orders in small amounts at increasing or decreasing prices.

Spoofing & Layering

High frequency traders are known to use the tactics of Spoofing & Layering to manipulate share prices. Spoofing is the placing of a bid or offer with the intent to cancel before execution. Layering is a form of spoofing in which the trader places multiple orders on one side of the book, in order to create a false impression of heavy buying or selling.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on September 10, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITIONS

By Staff Reporters

***

***

Rate Review & the 80/20 Rule

The health care law provides 2 ways to hold insurance companies accountable and help keep your costs down: Rate Review and the 80/20 rule.

Rate Review

Rate Review helps protect you from unreasonable rate increases. Insurance companies must now publicly explain any rate increase of 15% or more before raising your premium. This does not apply to grandfathered plans.

The 80/20 Rule generally requires insurance companies to spend at least 80% of the money they take in from premiums on health care costs and quality improvement activities. The other 20% can go to administrative, overhead, and marketing costs.

The 80/20 rule is sometimes known as Medical Loss Ratio, or MLR. If an insurance company uses 80 cents out of every premium dollar to pay for your medical claims and activities that improve the quality of care, the company has a Medical Loss Ratio of 80%.

Insurance companies selling to large groups (usually more than 50 employees) must spend at least 85% of premiums on care and quality improvement.

If your insurance company doesn’t meet these requirements, you’ll get a rebate on part of the premium that you paid.

Will I get a rebate check from my insurance company?

If your insurance company doesn’t meet its 80/20 targets for the year, you’ll get back some of the premium that you paid.

You may see the rebate in a number of ways:

A rebate check in the mail

A lump-sum deposit into the same account that was used to pay the premium, if you paid by credit card or debit card

A direct reduction in your future premium

Your employer may also use one of the above rebate methods, or apply the rebate in a way that benefits employees

If you or your employer will get a rebate, your insurance company must notify you by August 1.

If you have an individual insurance policy, you’ll get the rebate directly from your insurance company.

For small group and large group plans, the rebate is usually paid to the employer. It may use one of the above rebate methods, or apply the rebate in a way that benefits employees.

FYI: The 80/20 rebate rules don’t apply when an insurance company has fewer than 1000 enrollees in a particular state or market.

For Rate Review: These requirements don’t apply to grandfathered plans. Check your plan’s materials or ask your employer or your benefits administrator to find out if your health plan is grandfathered.

For the 80/20 Rule: These rights apply to all individual, small group, and large group health plans, whether your plan is grandfathered or not.

Classic: The portion of medical expenses a patient is responsible for paying.

Modern: Refers to the maximum you will pay during your policy period, which is typically a year, before your plan starts to pay 100% of your allowed amount. The costs of your deductible, co-pay, and co-insurance are included here, but not your premium.