BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

SO – HOW MUCH IS A “FINANCIAL ADVISOR” REALLY WORTH?

This blog holds a rather uncomplimentary opinion of financial advisors, and the financial services and brokerage industry as a whole; deserved, or not? The entire site hints at this attitude as well, in favor of a going it alone or ME, Inc investing when possible. Nevertheless, it is reasonable to wonder how much boost in net-returns might an educated and informed, fee transparent and honest, fiduciary focused “financial advisor” add to a clients’ investment portfolio; all things being equal [ceteris paribus].

And, can it be quantified?

Well, according to Vanguard Brokerage Services®, perhaps as much as 3%? In a decade long paper from the Valley Forge, PA based mutual fund and ETF giant, Vanguard said financial advisors can generate returns through a framework focused on five wealth management principles:

• Being an effective behavioral coach: Helping clients maintain a long-term perspective and a disciplined approach is arguably one of the most important elements of financial advice. (Potential value added: up to 1.50%).

• Applying an asset location strategy: The allocation of assets between taxable and tax-advantaged accounts is one tool an advisor can employ that can add value each year. (Potential value added: from 0% to 0.75%).

• Employing cost-effective investments: This component of every advisor’s tool kit is based on simple math: Gross return less costs equals net return. (Potential value added: up to 0.45%).

• Maintaining the proper allocation through rebalancing: Over time, as investments produce various returns, a portfolio will likely drift from its target allocation. An advisor can add value by ensuring the portfolio’s risk/return characteristics stay consistent with a client’s preferences. (Potential value added: up to 0.35%).

• Implementing a spending strategy: As the retiree population grows, an advisor can help clients make important decisions about how to spend from their portfolios. (Potential value added: up to 0.70%).

Source: Financial Advisor Magazine, page 20, April 2014.

Assessment

However, Vanguard notes that while it’s possible all of these principles could add up to 3% in net returns for clients, it’s more likely to be an intermittent number than an annual one because some of the best opportunities to add value happen during extreme market lows and highs when angst or giddiness [fear and greed] can cause investors to bail on their well-thought-out investment plans.

And, is the study applicable to doctors and allied healthcare providers? Doe Vanguard have a vested interest in the topic. What about fee based versus fee-only financial advice?

Conclusion

Finally, recognize the plethora of other financial planning life-cycle topics addressed in this ME-P were not included in the Vanguard investment portfolio-only study a decade ago.

And what about today with contemporaneous internet advising, chat-rooms, linkedin, robo-advisors, reddit and the like?

Posted on March 17, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

The Power of Attorney Mistake That Could Cost You Everything

By Rick Kahler CFP®

***

***

Recently, reading a training manual on elder abuse, I was reminded of a financial risk that is often overlooked. One of the fastest and easiest ways to unravel your financial security is to have the wrong person gain control of your money.

The example in the manual mirrored a heartbreaking situation I once experienced with a long-term client. As her mental and physical health declined, this single woman moved into assisted living. Her newly designated power of attorney, a relative from out of town, took control of her financial affairs.

Almost immediately, without consulting us, the relative began making large withdrawals, closed her accounts, and transferred funds elsewhere. They challenged the financial plan, investments, and strategies we had established to safeguard the client’s financial security and provide for her long-term care. Even though their actions threatened the client’s wellbeing, we were powerless to stop them. Our only recourse was to report the behavior to the authorities.

This heartbreaking and frustrating experience underscored just how critical it is to be mindful when executing a Power of Attorney. Besides designating someone you trust, it is wise to build in safeguards to prevent even a well-meaning relative from inadvertently derailing a carefully constructed financial plan.

***

***

One such safeguard is to include a financial advisor in your POA—as long as that person is a fee-only, fiduciary advisor with an obligation to act in your best interests. In many cases, advisors are hesitant to suggest this option because they are sensitive to the potential conflict of interest and do not want to appear self-serving. An unfortunate reality is that you should be cautious if an advisor, particularly one who sells products on commission, seems eager to be added to your POA.

Including your financial advisor in your POA does not mean you designate them as your agent to manage your affairs. Instead, you include a clause naming them as the professional of record you want your designated agent to continue working with. This creates continuity and accountability. It prevents your agent from replacing your advisor with someone who may be unfamiliar with your needs and goals, unqualified, or untrustworthy.

Your advisor might also recommend adding a secondary safeguard, such as naming an attorney or accountant to oversee the selection of a successor advisor in case your current advisor is unable to continue. This additional layer of protection ensures that the financial professionals guiding your portfolio remain aligned with your best interests. Taking these extra steps can save you—and your loved ones—from significant financial stress down the road.

Including safeguards in your POA is not about mistrusting your loved ones, but about equipping them with the right resources and support to act in your best interest. Financial management is complex, and it requires expertise that most people, even those with the best intentions, may not possess.

One of the hardest parts about planning for diminished financial capacity is the emotional aspect. No one likes to imagine a time when they might not be able to manage their own money. But in reality, taking steps now to protect your financial future is the ultimate act of control. It can help ensure that your wishes are respected and the financial foundation you’ve worked so hard to build remains intact.

Remember, too, that avoiding conversations often increases financial vulnerability. If you don’t have a POA or aren’t comfortable with what you do have, now is the time to bring it up with your advisor, attorney, or a trusted family member. These safeguards are about protecting yourself. They also support those you will rely on to care for you and your financial legacy,

Health actuaries analyze potential risks, profits and trends that will affect their employers, which are often in the health insurance, government health services and medical provider industries. They advise companies on issuing policies to consumers based on risks, calculated premiums and upcoming changes in health-care costs.

It’s common for an actuary to have a bachelor’s degree or higher in actuary studies, mathematics or statistics. Coursework on medical terminology and hierarchy of the medical field is also beneficial. In addition to academic education, certification is also necessary to reach “professional status,” which is required by most employers.

***

***

The professional organization, Society of Actuaries, certifies actuaries in the health and medical field. Their statistical work is commonly done with predictive tables, probability tables and life tables that are created on customized statistical analysis software such as Stata or XLSTAT.

The actuary field as a whole is growing faster than other fields, according to the Bureau of Labor Statistics [BLS]. In 2020, it expanded by 27 percent. The average annual salary for an actuary in 2010 was $87,650. More specifically, in the health insurance field, the salary was slightly higher at $91,000.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com

Posted on March 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEdCMP®

***

***

Your Executor or personal representative is named in your Will and is responsible for management of assets subject to probate. A basic checklist of the duties of the personal representative looks like this:

Gather all estate assets;

Collect all amounts owed the decedent;

Notify creditors and paying all valid debts;

Selling assets as needed to pay expenses or as directed by the Will;

Distribute assets to beneficiaries;

File decedents final federal income tax return;

File an estate tax return if the estate is large enough; and

File inventories and annual returns with the probate court, if required.

The position requires a lot of responsibility and involves many duties and a considerable commitment of time. The personal representative must petition the probate court for formal appointment.

Selection of your personal representative should not be made lightly, or as a favor to a friend. It requires a lot of work and very often for little or no pay. Friends and family typically will not charge the estate for their time and work. Outside advisers like attorneys and accountants will not hesitate to bill for their work effort. A few items for your selection criteria should be:

Longevity – the person should have a likelihood of being able to serve after your death;

Skill in managing legal and financial affairs;

Familiarity with your estate and wishes;

Integrity and loyalty; and

Impartiality and absence of conflicts of interest.

Alternatives to family or friends might be a corporate executor, such as a bank, an attorney, or other adviser. Similar criteria should be used in the selection of a trustee.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Posted on March 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

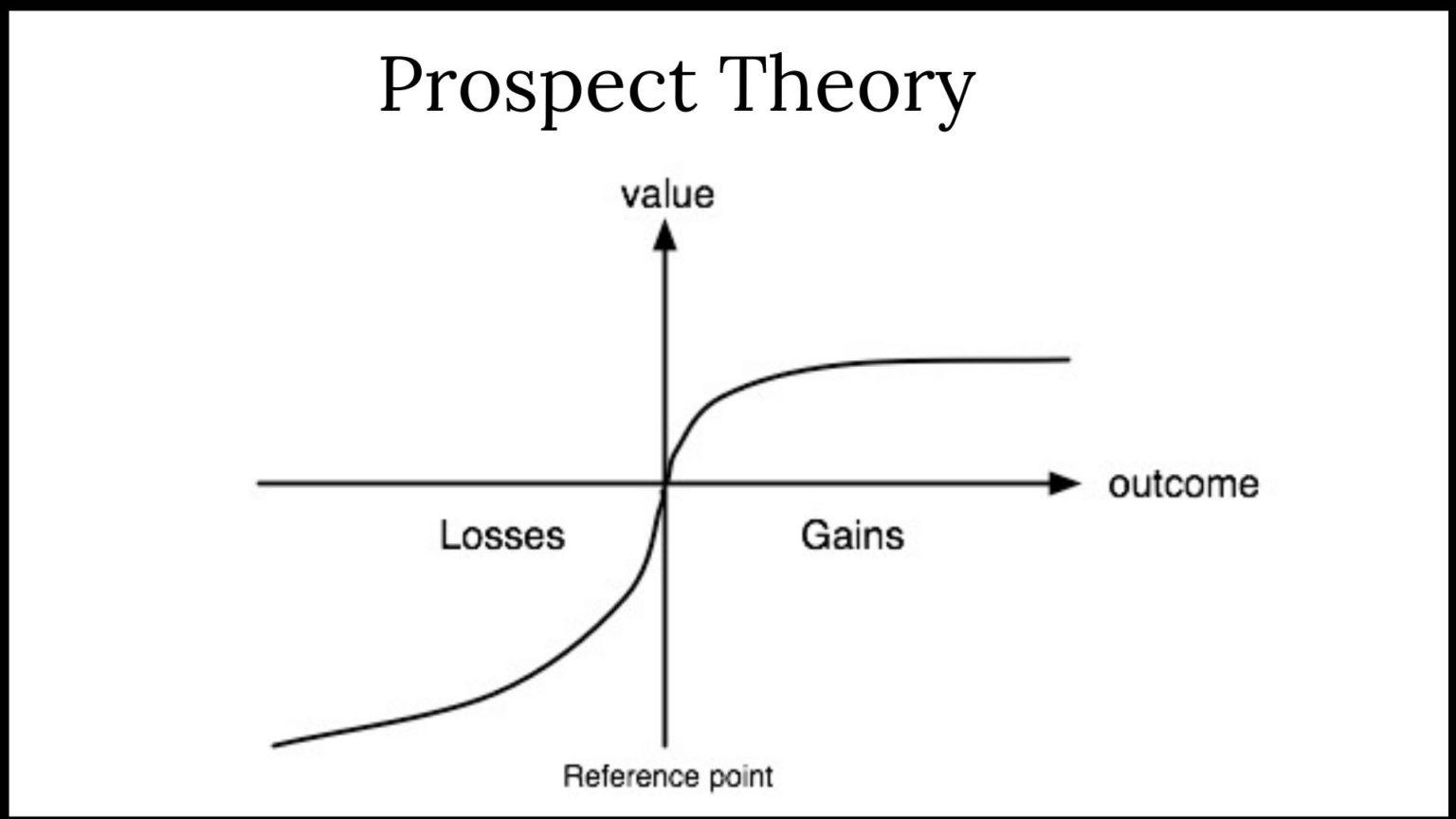

BEHAVIORAL ECONOMICS

By Staff Reporters

***

***

Prospect theory is a psychological and behavioral economics theory developed by Daniel Kahneman and Amos Tversky in 1979. It explains how people make decisions when faced with alternatives involving risk, probability, and uncertainty. According to this theory, decisions are influenced by perceived losses or gains.

Example:

Amanda, a DO client, was just informed by her financial advisor that she needed to re-launch her 403-b retirement plan. Since she was leery about investing, she quietly wondered why she couldn’t DIY. Little does her FA know that she doesn’t intend to follow his advice, anyway! So, what went wrong?

The answer may be that her advisor didn’t deploy a behavioral economics framework to support her decision-making. One such framework is the “prospect theory” model that boils client decision-making into a “three step heuristic.”

Prospect theory makes the unspoken biases that we all have more explicit. By identifying all the background assumptions and preferences that clients [patients] bring to the office, decision-making can be crafted so that everyone [family, doctor and patient] or [FA, client and spouse] is on the same page. Briefly, the three steps are:

1. Simplify choices by focusing on the key differences between investment [treatment] options such as stock, bonds, cash, and index funds.

2. Understanding that clients [patients] prefer greater certainty when it comes to pursuing financial [health] gains and are willing to accept uncertainty when trying to avoid a loss [illness].

3. Cognitive processes lead clients and patients to overestimate the value of their choices thanks to survivor bias, cognitive dissonance, appeals to authority and hindsight biases.

Assessment

Much like healthcare today, the current mass-customized approaches to the financial services industry falls short of recognizing more personalized advisory approaches like prospect theory and assisted client-centered investment decision-making.

Posted on March 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITION

By Staff Reporters

***

***

1035 Exchange

DEFINITION: A method of exchanging insurance-related assets without triggering a taxable event. Cash-value life insurance policies and annuity contracts are two products that may qualify for a 1035 exchange.

***

A 1035 exchange is a feature in the tax code that permits individuals to transfer funds from an existing life insurance endowment, or annuity policy to a new one without tax consequences.

These transactions are not subject to tax deductions or tax credits but rather tax deferrals, meaning that individuals would only pay taxes on any earnings once they receive money from the policy later.

Without this provision, policyholders would have to close their previous accounts and be subjected to both taxes and surrender charges before they could open a new account.

Posted on March 12, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

The IRS 1099-k Tax Form

By Staff Reporters and IRS

***

***

Third party payment platforms are required to send you a 1099-K tax form if you made more than $5,000 on the platform in 2024. This reporting change will give the IRS a clearer picture of how much you earned in untaxed income this year to help ensure you pay your taxes properly. For the 2025 tax year, the threshold will drop to $2,500.

The IRS originally rolled out a plan to implement new reporting requirements for anyone earning over $600 via payment apps in 2023. After two years of delays, the tax agency has decided to implement a phased rollout, lifting the reporting threshold to $5,000 for the 2024 tax year.

If you earn freelance or self-employment income, you’re likely no stranger to 1099 tax forms. You’re required to report any net earnings over $400 to the IRS when you file your tax return, even if you don’t receive a 1099. The 1099-K tax change places a reporting requirement on payment apps so the IRS can keep better tabs on income earnings that might otherwise go unreported.

Posted on March 12, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Stocks inched up overnight after Monday’s ugly plunge to six-month lows, but positive catalysts were scattered and the rocky economy has begun affecting earnings forecasts. Delta Airlines (DAL) lowered its outlook yesterday amid what it called “macro uncertainty,” raising concerns it could be first on a crowded runway.

One theme as stocks plunged recently was that despite the suffering was that earnings outlooks remained strong. The latest FactSet forecasts for first quarter and 2025 S&P 500 earnings growth are 7.3% and 11.6%, respectively. Both are down from December 31st, though, and further setbacks in expectations could hurt confidence. Oracle (ORCL) missed analysts’ estimates late Monday. “The longer the tariff turmoil and related uncertainty about trade policy lasts, the more likely economic and earnings growth may take a hit,” said Jeffrey Kleintop, chief global investment strategist at Schwab.

Job openings data later yesterday morning and the Consumer Price Index (CPI) tomorrow could help set the tone, though economic growth seems to have replaced inflation as the prime concern. Yesterday’s steep losses reflected less confidence in either the administration or the Federal Reserve potentially stepping in to rescue a slumping economy. Growth fears have pummeled the Magnificent Seven, with six of them among the bottom 350 in S&P 500 index (SPX) year-to-date performance.

For now, the S&P 500 (^GSPC) avoided correction territory but still fell about 0.8% to trade at just under 5,600. The Dow Jones Industrial Average (^DJI) shed roughly 500 points, or 1.1%, dragged down by shares of Verizon (VZ). The tech-heavy NASDAQ Composite (^IXIC) reversed gains in the last few minutes of trading to fall about 0.2%. All three indexes closed at their lowest levels since September.

Visualize: How private equity tangled banks in a web of debt, from the Financial Times.

If you have ever filed a homeowners insurance claim, you know it can feel more like an endurance test than a straightforward process. While insurers are legally required to honor valid claims, they have strong financial incentives to delay, underpay, or deny them whenever possible.

Over the years, I’ve learned this the hard way. The most recent lesson started when a hailstorm hit my home in June 2023. I promptly filed an insurance claim. I also made up a story that leaving someone more qualified than me in charge would free me from a part-time job as a contractor, so I relied on a roofing contractor to handle the whole claim, including the gutter and siding damage. That was my first mistake.

About 15 months later, my roof and gutters were replaced, but the siding repairs and painting remained undone. Every time the insurance company reassigned my claim to a new adjuster, I had to start over. When I called the contractor after a period of inactivity, they said the adjuster had ghosted them, so they’d given up—and I still owed them the full roofing bill.

At that point, I had two choices: pay out of pocket for the unfinished work or escalate. I chose the latter. I filed a complaint with the state insurance division, contacted my agent, reached out to the last adjuster, hired my own painter, and withheld final payment to the contractor. I also made it clear that I was prepared to take legal action if necessary. That was not a bluff.

Within a week, things started moving. Seven days later, the insurance company reinspected my home and sent a check covering all but $3,000 of the painting costs. After nearly two years of delays and excuses, progress finally happened when I took matters into my own hands.

Delay is a common insurer tactic. They’ll repeatedly ask for more documentation, take months to respond, or swap adjusters to force you to restart the process—all in hopes that you’ll give up or accept a lower payout.

Another common tactic is the lowball offer. Insurers often rely on software that underestimates damages or send adjusters unfamiliar with actual repair costs. Accepting their first offer without question can be a costly mistake. It’s wise to get independent repair estimates or even hire a public adjuster who works for you rather than the insurance company.

Insurers also deny claims based on fine print, arguing that damage was pre-existing, caused by poor maintenance, or excluded under some obscure clause. Knowing your policy inside out and keeping pre-loss photos can help you counter these claims.

Another trick? Steering homeowners toward “preferred” contractors who work at discounted rates and may prioritize the insurer’s interests over yours. Getting independent estimates ensures repairs are done properly.

For homeowners stuck in an insurance battle, persistence is key. Withholding final payment until work is complete, filing a complaint with the state insurance division, and even considering small claims court can help push a claim forward. If the dispute is within your state’s small claims limit—often between $10,000 and $25,000—filing may push the insurer to settle.

Assuming my contractor would handle everything was my biggest mistake, and it cost me nearly two years of frustration. Even though progress happened quickly once I took control, my claim isn’t over. I suspect I will be filing legal action in small claims court against the insurance company, contractor, and insurance agent.

If you need to navigate an insurance claim, be persistent and attentive. Keeping records, pushing back on delays, and escalating when necessary can mean the difference between being shortchanged and getting the settlement you deserve.

Posted on March 10, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS

By Staff Reporters

***

***

US stocks plunged on Monday as investors processed growing concerns about the health of the US economy after President Trump and his top economic officials acknowledged the possibility of a potential rough patch.

The Dow Jones Industrial Average (^DJI) fell nearly 900 points, or over 2%, while the benchmark S&P 500 (^GSPC) dropped around 2.7% after the index posted its worst week since September.

The tech-heavy NASDAQ Composite (^IXIC) fell 4% in its worst day since 2022, as the “Magnificent Seven” stocks led the sell-off. Tesla’s (TSLA) rout continued, plunging 15% and officially wiping out the gains it had made in the wake of Trump’s election win. Nvidia (NVDA), Apple (AAPL), Google parent Alphabet (GOOG), and Meta (META) all each lost more than 4%.

I was having lunch with a close friend of mine. He mentioned that he had accumulated a significant sum of money and did not know what to do with it. It was sitting in bonds, and inflation was eating its purchasing power at a very rapid rate.

He is a dentist and had originally thought about expanding his business, but a shortage of labor and surging wages turned expanding into a risky and low-return investment. He complained that the stock market was extremely expensive. I agreed.*

He said that the only thing left was residential real estate. I pushed back. “What do you think will happen to the affordability of houses if – and most likely when – interest rates go up? Inflation is now 6%. I don’t know where it will be in a year or two, but what if it becomes a staple of the economy? Interest rates will not be where they are today. Even at 5% interest rates [I know, a number unimaginable today] houses become unaffordable to a significant portion of the population. Yes, borrowers’ incomes will be higher in nominal terms, but the impact of the doubling of interest rates on the cost of mortgages will be devastating to affordability.”

He rejoined, “But look at what happened to housing over the last twenty years. Housing prices have consistently increased, even despite the financial crisis.”

I agreed, but I qualified his statement: “Over the past twenty, actually thirty, years interest rates declined. I honestly don’t know where interest rates will be in the future. But probabilistically, knowing what we know now, the chances that they are going to be higher, much higher, are more likely than their staying low. Especially if you think that inflation will persist.”

We quickly shifted our conversation toward more meaningful topics, like kids.

It seems that every year I think we have finally reached the peak of crazy, only to be proven wrong the next year. The stock market and thus index funds, just like real estate, have only gone one way – up. Index funds became the blunt instrument of choice in an always-rising market. So far, this choice has paid off nicely.

The market is the most expensive it has ever been, and thus future returns of the market and index funds will be unexciting. (I am being gentle here.)

You don’t have to be a stock market junkie to notice the pervasive feeling of euphoria. But euphoria is a temporary, not a permanent emotion; and at least when it comes to the stock market, it is usually supplanted by despair. Market appreciation that was driven by expanding valuations was not a gift but a loan – the type of loan that must always be paid back with a high rate of interest.

I don’t know what straw will break the feeble back of this market or what will cause the music to stop (there, you got two analogies for the price of none). We are in an environment where there are very few good options. If you do nothing, your savings will be eaten away by inflation. If you do something, you find that most assets, including the stock market as a whole, are incredibly overvalued.

We are doing the only sensible thing that you can do today. We spend very little time thinking about straws or what will cause the music to stop or how overvalued the market is. We are focusing all our energy on patiently building a portfolio of high-quality, cash-generative, significantly undervalued businesses that have pricing power.

This has admittedly been less rewarding than taking risky bets on unimaginably expensive assets. It may lack the excitement of sinking money into the darlings you see in the news every day, but we hope that our stocks will look like rare gems when the euphoria condenses into despair. As we keep repeating in every letter, the market is insanely overvalued. Our portfolio is anything but – we don’t own “the market”.

*A question may arise:Why did I not tell my dentist friend to pick individual stocks? He runs a busy dental practice and wouldn’t have the time or the training to pick stocks.

Why didn’t I offer him our services? IMA manages all my and my family’s liquid assets, but I have a rule that I never (ever!) break – I don’t manage my friends’ money. I’ll help them as much as possible with free advice but will never have a professional relationship with them. I intentionally create a separation between my personal and professional lives. After a difficult day in the market, I want to be able to go for beers with friends and leave the market at the office.

Also, this simplifies my relationships with my friends. There is no ambiguity in our friendship.

Posted on March 8, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

AGREE or DISAGREE?

By Staff Reporters

***

***

US Treasury Secretary Scott Bessent made waves yesterday with his comment that the American economy is facing a “detox period.”

Should we be seeing that this economy that we inherited [is] starting to roll a bit? Sure. And look, there’s going to be a natural adjustment as we move away from public spending to private spending. The market and the economy have just become hooked, and we’ve become addicted to this government spending, and there’s going to be a detox period. There’s going to be a detox” .

Bessent, a former hedge-fund manager, said during a CNBC interview.

“Employment should be from private companies, not from government. And I’m confident, if we have the right policies, it will be a very smooth transition.”

Bessent said, in an apparent reference to the layoffs of federal workers executed in large part by the entity known as the Department of Government Efficiency, which is run by Trump adviser Elon Musk.

You can also listen to a professional narration of this article on iTunes & online.

ENCORE: March 22, 2004

A basic property of religion is that the believer takes a leap of faith: to believe without expecting proof. Often you find this property of religion in other, unexpected places – for example, in the stock market. It takes a while for a company to develop a “religious” following: only a few high-quality, well-respected companies with long track records ever become worshipped by millions of investors. My partner, Michael Conn, calls these “religion stocks.” The stock has to make a lot of shareholders happy for a long period of time to form this psychological link.

The stories (which are often true) of relatives or friends buying few hundred shares of the company and becoming millionaires have to fester a while for a stock to become a religion. Little by little, the past success of the company turns into an absolute – and eternal – truth. Investors’ belief becomes set: the past success paints a clear picture of the future.

Gradually, investors turn from cautious shareholders into loud cheerleaders. Management is praised as visionary. The stock becomes a one-decision stock: buy. This euphoria is not created overnight. It takes a long time to build it, and a lot of healthy pessimists have to become converted into believers before a stock becomes a “religion.”

Once a stock is lifted up to “religion” status, beware: Logic is out the window. Analysts start using T-bills to discount the company’s cash flows in order to justify extraordinary valuations. Why, they ask, would you use any other discount rate if there is no risk? When a T-bill doesn’t do the trick, suddenly new and “more appropriate” valuation metrics are discovered.

Other investors don’t even try to justify the valuation – the stock did well for me in the past, why would it stop working in the future? Faith has taken over the stock. Fundamentals became a casualty of “stock religion.” These stocks are widely held. The common perception is that they are not risky.

The general public loves these companies because they can relate to the companies’ brands. A dying husband would tell his wife, “Never sell _______ (fill in the blank with the company name).” Whenever a problem surfaces at a “religion stock,” it is brushed away with the comment that “it’s not like the company is going to go out of business.” True, a “religion stock” company is a solid leader in almost every market segment where it competes and the company’s products carry a strong brand name. However, one should always remember to distinguish between good companies and good stocks.

Coca-Cola is a classic example of a “religion stock.” There are very few companies that have delivered such consistent performance for so long and have such a strong international brand name as Coca-Cola. It is hard not to admire the company.

But admiration of Coca-Cola achieved an unbelievable level in the late nineties. In the ten years leading up to 1999, Coca-Cola grew earnings at 14.5% a year, very impressive for a 103-year-old company. It had very little debt, great cash flow and a top-tier management. This admiration came at a steep price: Coca-Cola commanded a P/E of 47.5. That P/E was 2.7 times the market P/E. Even after T-bills could no longer justify Coke’s valuation, analysts started to price “hidden” assets – Coke’s worldwide brand. No money manager ever got fired for owning Coca-Cola.

The company may not have had a lot of business risk. But in 1999, the high valuation was pricing in expectations that were impossible for any mature company to meet. “The future ain’t what it used to be” – Yogi Berra never lets us down. Success over a prolonged period of time brings a problem to any company – the law of large numbers.

Enormous domestic and international market share, combined with maturity of the soft drink market, has made it very difficult for Coca-Cola to grow earnings and sales at rates comparable to the pre-1999 years. In the past five years, earnings and sales have grown 2.5% and 1.5% respectively. After Roberto C. Goizueta’s death, Coke struggled to find a good replacement – which it acutely needed.

Old age and arthritis eventually catch up with “religion stocks.” No company can grow at a fast pace forever. Growth in earnings and sales eventually decelerates. That leads to a gradual deflation of the “religion” premium. For Coke, the descent from its “religious” status resulted in a drop of nearly 20% in the share price – versus an increase of 65% in the broad market over the same time. And at current prices, the stock still is not cheap by any means. It trades at 25 times December 2004 earnings, despite expectations for sales growth in the mid single digits and EPS growth in the low double digits.

It takes a while for the religion premium to be totally deflated because faith is a very strong emotion. A lot of frustration with sub-par performance has to come to the surface.

Disappointment chips away at faith one day at a time. “Religion” stocks are not safe stocks. The leap of faith and perception of safety come at a large cost: the hidden risk of reduction in the “religion premium.” The risk is hidden because it never showed itself in the past. “Religion” stocks by definition have had an incredibly consistent track record. Risk was rarely observed.

However, this hidden risk is unique because it is not a question of if it will show up but a question of when. It is very hard to predict how far the premium will inflate before it deflates – but it will deflate eventually. When it does, the damage to the portfolio can be huge.

Religion stocks generally have a disproportionate weight in portfolios because they are never sold – exposing the trying-to-be-cautious investor to even greater risks. Coca-Cola is not alone in this exclusive club. General Electric, Gillette, Berkshire Hathaway are all proud members of the “religion stock” club as well. Past members would include: Polaroid – bankrupt; Eastman Kodak – in a major restructuring; AT&T – struggling to keep its head above water. That stock is down from over $80 in 1999 to $18 today.

Emotions have no place in investing. Faith, love, hate, and disgust should be left for other aspects of our life. More often than not, emotions guide us to do the opposite of what we need to do to be successful. Investors need to be agnostic towards “religion stocks.” The comfort and false sense of certainty that those stocks bring to the portfolio come at a huge cost: prolonged under performance.

My thoughts today (20+ years later)

This is one of the first investment articles I ever wrote. I had just started writing for TheStreet.com. It’s interesting to read this article more than 20 years later. I am surprised my writing was not as bad as I had feared (though in many cases it was worse than I feared when I read my other early articles).

So much has happened since then – I am a different person today than I was back then. I have two more kids; I have written three more books and a thousand articles. The last two decades were my formative years as an investor and adult.

The goal of the article was not to make predictions but to warn readers that the long-term success of certain companies creates a cult-like following and deforms thinking. In fact, my original article – the one I submitted to TheStreet.com – did not mention any companies other than Coke. The editors wanted me to include more names so that the article would show up on more pages of Yahoo! Finance.

With the exception of Berkshire Hathaway, all of these companies have produced mediocre or horrible returns. In the best case, their fundamental returns in their old age were only a fraction of what they were when these companies were younger and the world was their oyster.

To my surprise, Coke’s stock is still trading at a high valuation. Its business has performed like the old-timer it is, with revenue and earnings growing by only 3–4% a year. The days of double-digit revenue and earnings growth were left in the 80s and 90s, though the high valuation remained.

Posted on March 7, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

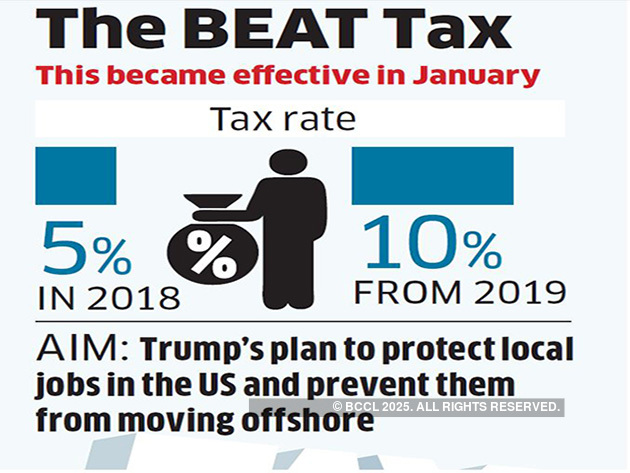

Base-Erosion Anti-Abuse Tax (BEAT): The 2017 tax reforms moved the U.S. from a worldwide taxation system to a quasi-territorial system, so foreign earnings are no longer included in a company’s domestic tax base.

To discourage companies operating in the U.S. from avoiding tax liability by shifting profits out of the country, Congress imposed a 10% minimum tax called Base-Erosion Anti-Abuse Tax (BEAT). The BEAT rate will increase from 10% to 12.5% in 2026.

Leverage ratios measure the amount of capital that comes from debt. In other words, leverage financial ratios are used to evaluate a company’s debt levels. Common leverage ratios include the following:

The debt ratio measures the relative amount of a company’s assets that are provided from debt:

Debt ratio = Total liabilities / Total assets

The debt to equity ratio calculates the weight of total debt and financial liabilities against shareholders’ equity:

Debt to equity ratio = Total liabilities / Shareholder’s equity

Separate Account Management offers medical professionals customized personal money management services. In the typical separate account structure, a money manager invests the individual’s assets in stocks and bonds (as opposed to mutual funds providing exposure to specific asset classes) on a discretionary basis.

For physicians and healthcare providers with significant investment assets (e.g., $100,000), a separately managed portfolio can be customized to reflect their tax situation, social investment guidelines, and cash flow needs.

An additional benefit of the separate account management structure is that a client’s portfolio may be positioned over time as opportunities arise, rather than forcing stocks into the portfolio without regard to current conditions.

Although separate account management generally offers a higher degree of customization than mutual funds, fees for separate account management are generally consistent with mutual funds fees, especially given that separate account managers may discount their fees for larger portfolios.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Dying Broke. It’s a goal for those retirees who embrace the idea of spending their hard-earned wealth during their lifetimes. Their aim is to enjoy the fruits of their labor while they can and spend the last penny just as they take their last breath. The concept feels both pragmatic and poetic.

But here’s the twist: While the concept may conjure images of lavish spending sprees and exotic vacations, that’s rarely what I see in practice. Many of my clients who identify as Die Brokers aren’t recklessly burning through their wealth. In fact, the opposite is often true.

This is because their approach to spending and giving is shaped by a lifetime of frugal money scripts that are incredibly hard to shake. Many Boomers grew up with financial uncertainty, learning to save and sacrifice to protect themselves and their families. Even after decades of financial success, those habits don’t just disappear. The idea of “spending down” their wealth, even intentionally, feels unnatural and irresponsible. There is an internal tug-of-war between their stated desire to enjoy their wealth and their deeply rooted fear of running out.

This paradox can significantly affect retirees’ financial planning. While Die Brokers may express a strong commitment to living fully, their money behavior often reveals a need for reassurance that their money will last for their lifetime.

For many Boomers, including myself, those frugal money scripts have served us well for decades. They’ve provided financial stability and peace of mind. But in this stage of life, they can also hold us back from experiencing the freedom we’ve worked so hard to achieve—especially in the time we have left when we can still physically enjoy it. The challenge is finding balance, honoring the values that got us here while allowing ourselves permission to live fully.

Here are four ways to start turning those old money scripts into permission to spend and give intentionally:

Reframe wealth as a tool rather than a safety net. Recognize that money is about opportunity as well as security. Spending with intention can bring joy and meaning, whether it’s funding a family trip, supporting a cause, or splurging on a bucket list item.

Work with your financial advisor to analyze your retirement spending and the probability of running out of money. The amount they suggest you can spend may surprise you—it’s often far higher than your frugal money scripts would lead you to believe.

Experiment with incremental giving. If parting with your wealth feels daunting, start small. Gift modest amounts to family, friends, or charities and notice how it feels. Seeing the immediate impact of your generosity can help ease the transition and loosen the grip of those old money scripts.

Set intentional spending goals instead of vaguely aiming to “enjoy your wealth.” Identify specific ways you want to use your money to enhance your life or the lives of others. Having a clear plan can turn spending into a meaningful act rather than an exercise in guilt.

For many of us, the Die Broke mentality is not about recklessness or extravagance. It’s about learning to let go. Despite our bold talk of spending down to the last penny, most of us will likely leave behind more than we planned. And maybe that’s just fine—especially for our kids and grand kids. Perhaps being a Die Broker is really about giving ourselves permission to live with intention, to savor what we’ve built, and to enjoy living to the fullest the rich life our frugality has helped provide.

Posted on March 3, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

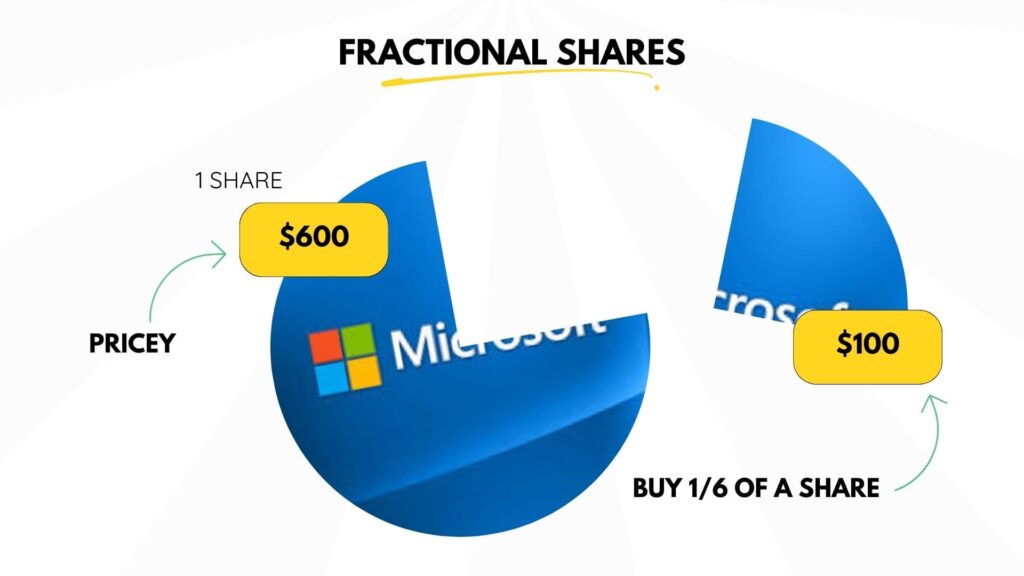

Suppose, as a medical or nursing school student, or new practitioner, you want to invest in a company, but its stock price may be higher than what you want, or can afford, to pay.

Instead of buying a whole share of stock, you can buy a fractional share, which is a “slice” of stock that represents a partial share, for very little money (ie., $5 at Charles Schwab).

***

***

Example: If a company’s stock is selling at $1,000 a share and you were buying $200 worth of it, you would own 0.2 (20%) of a share. With stock slices, investing has never been more accessible.

Posted on March 2, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Copilot

***

***

The “Magnificent Seven” refers to a group of seven technology giants that have significantly influenced the stock market. These companies are:

Alphabet (GOOGL)

Amazon (AMZN)

Apple (AAPL)

Meta Platforms (META)

Microsoft (MSFT)

Nvidia (NVDA)

Tesla (TSLA)

Why Are They Significant?

These companies are at the forefront of technological innovation, driving advancements in artificial intelligence, cloud computing, e-commerce, social media, and electric vehicles. Their market dominance and financial performance have a substantial impact on major stock indices like the S&P 5002.

Performance

Alphabet: Despite a 31% climb over the past year, Alphabet remains the cheapest of the group, trading at 20 times forward earnings estimates.

Amazon: Amazon’s cloud unit is delivering an annual revenue run rate of $115 billion thanks to its AI offerings.

Apple: Apple has seen a 989% total return for investors over the past decade.

Meta Platforms: Meta is the best-performing stock year-to-date among the Magnificent Seven, up over 25%.

Microsoft: Microsoft has generated a 989% total return for investors over the past decade.

Nvidia: Nvidia remains the best performer over the past year, up 55%.

Tesla: Tesla is the worst-performing stock in the group for 2025, down 25.66% year-to-date.

These companies have reshaped industries and become powerhouses in the global economy, wielding significant influence over market trends and investor sentiment.

If the definition of a security is title to a stream of cash flows, then the dividends a company is expected to pay to equity shareholders on a periodic basis (e.g., quarterly) are a clear source of return for an investor. A dividend is simply a distribution of (some portion of) the company’s earnings to equity shareholders. Like a bond yield, a stock’s dividend yield can be used to measure the income return on the stock.

To determine a stock’s dividend yield, the trailing year’s dividends per share paid are divided by the current stock price. However, a key difference between a dividend yield and a bond yield is the level of certainty that can be assumed regarding future payments, since a bond’s coupon is generally predetermined and its payment is expected to be senior to the payment of dividends.

After a company has determined that it has earned a profit, management has to decide what to do with those profits. One choice is to distribute the earnings to shareholders in the form of dividends, while another option is to reinvest the profits in the company. A company’s management may determine that the shareholders interest is best served by using the earnings to pursue growth opportunities (e.g., capital expansion, research & development, etc.) at the corporate level. Thus, when management believes that its investment opportunities are likely to produce a higher return than what investors’ could generate with their dividends or that reinvestment is needed to maintain its financial strength, the company will retain the earnings.

One of the biggest myths in investing is capital appreciation accounts for the largest part of investors’ gains. Dividends, or cash payments to shareholders, actually account for a substantial part of an equity investor’s total return. In fact since 1926, dividends have accounted for more than 40% of the total return of the S&P 500 stock index. In the last decade (2000-2009), the S&P 500’s total return of -9% would have been a heftier loss of -24% had it not been for the 15% contribution from dividends.

History has shown that dividends have been a powerful source of total return in a diversified investment portfolio, especially during periods of market turbulence. In examining the prior eight decades of stock market performance, dividends often account for more than 2/3 of the total return (1930s, 1940s, 1970s, & 2000s). If an investor avoided dividend paying stocks during these elongated time periods, most of the total gains would be lost.

***

DIVIDEND CONTRIBUTION OF S&P 500 RETURN BY DECADE

S&P 500

Cumulative

Dividends

Average

Price %

Dividend

Total

% of Total

Payout

Years

Change

Contribution*

Return

Return

Ratio**

1930s

-41.9%

56.0%

14.1%

>100%

90.1%

1940s

34.8%

100.3%

135.0%

74.3%

59.4%

1950s

256.7%

180.0%

436.7%

41.2%

54.6%

1960s

53.7%

54.2%

107.9%

50.2%

56.0%

1970s

17.2%

59.1%

76.4%

77.4%

45.5%

1980s

227.4%

143.1%

370.5%

38.6%

48.6%

1990s

315.7%

117.1%

432.8%

27.0%

47.6%

2000s

-24.1%

15.0%

-9.1%

>100%

35.3%

2010s

27.9%

8.4%

36.3%

23.1%

28.4%

as of 12/31/12

Source: Strategas

During those decades such as the 2000s where the stock market struggled to advance, dividends were a significant element for investor survival. This is not only due to the dividends alone, but also the risk element of stocks that pay dividends. Dividend stocks have historically provided lower overall volatility and stronger downside protection when markets decline. Since 1927, dividend stocks have consistently held up better than the broader market during downturns. You can measure downside risk through a statistic known as downside capture ratio.

Downside capture ratio is a statistical measure of overall performance in a down stock market. An investment category, or investment manager, who has a down-market ratio less than 100 has outperformed the index during a falling stock market.

For example, a down-market capture ratio of 80 indicates that the portfolio measure declined only 80% as much as the index during the period. The downside capture ratio of high-dividend-yielding stocks, since 1927, has been 81% or lower over various long-term periods. Put a better way, during months that the S&P 500 stock index fell, dividend stocks declined by nearly 19% less than the broader market.

***

DOWNSIDE AND UPSIDE CAPTURE RATIOS OF HIGH DIVIDEND STOCKS – 1927 TO 2011

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com

In 1972, Nobel Laureate Kenneth J. Arrow, PhD shocked academe’ by identifying health economics as a separate and distinct field. Yet, the seemingly disparate insurance, tax, risk management and financial planning principles that he also studied are just now becoming transparent to some medical professionals and their financial advisors. Despite the fact that a basic, but hardly promoted premise of this new wave financial planning era, is imprecision.

Nevertheless, to informed cognoscenti like Certified Medical Planners™, the principles served as predecessors to the modern physician-focused financial advisory niche sector. In 2004, Arrow was selected as one of eight recipients of the National Medal of Science for his innovative views.

And now, as a long bull market may be over, and if the current “new-normal” prevails – meaning a 4.5% real annualized rate of return on equities and a 1.5% real rate on bonds – wealth accumulation for all may be reduced.

An Imprecise Science

There is a major variable, dominant in any marketplace that pushes an economy in a forward direction. It is called consumerism. This became apparent while waiting in a doctor’s office one recent afternoon.

Scenario:

The front office receptionist, who appeared to be about 21 years old, was breaking for lunch and her replacement, who appeared not much older, came over to assist. Realizing the propensity for a long wait, one was taken by the size of waiting room and the number of patients coming in and out of the office. [Americans consume healthcare and a lot of it]. There was another notable peculiarity. The sample prescription bags being carried out the door were no match for the bags under everyone’s eyes, including the doctor’s. The office staff was probably working overtime, if not two jobs, and the doctor was working harder and faster in a managed care system.

Assessment

Why? So they all could afford to buy and voraciously consume for their children and themselves. Americans indeed work longer hours than any other industrialized nation.

Conclusion

Finally, as women medical professionals entered the workforce in unprecedented numbers, the stock markets reached an all time high in 2025, even as money was spent at a feverish pace as the Federal Reserve pumped out money in inflammatory fashion.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com

Investing in Growth Stocks – Catching the Momentum [BIG-MO]

The growth style of investing focuses on companies with strong earnings and accelerating capital growth. A growth investor will make investment decisions based on forecasts of continuing growth in earnings. Growth investing emphasizes qualitative criteria, including value judgments about the company, its markets, its management, and its ability to extract future earnings growth from the particular industry.

Quantitative indicators of interest to the growth investor include high Price/Earnings ratios, Price/Sales ratios, and low dividend yields. A high P/E ratio suggests that the market is prepared to pay more per share in anticipation of future earnings. A low dividend yield suggests that the company is reinvesting rather than distributing profits. These indicators are considered in relation to the company’s immediate competitors. The companies with the highest P/E ratios relative to their industry will often be dominant within their market segment and have strong growth prospects. Growth investors will generally focus on premium and leading-edge companies.

***

***

Some industry sectors by their nature have stronger growth characteristics, particularly more innovative and speculative industries.

For example, during the bull market run on the U.S. stock markets during the late 1990s, the technology sector was a major area of growth investment. On observing strong earnings growth, a growth investor will decide whether to buy shares based on whether the company’s growth is going to continue at its present rate, to increase, or to decrease. If it is expected to increase, the growth investor will consider it a candidate for purchase. The key research question is: at what point will the company’s growth flatten out, or fall? If a company’s growth rate slows or reverses, it is no longer attractive to a growth investor. Growth investors are normally prepared to pay a premium for what they believe to be high quality shares. The potential downside in growth investing is that if a company goes into sudden decline and the share price falls, you can lose capital value rapidly.

Growth stocks, like the current “Magnificent-Seven“, carry high expectations of above-average future growth in earnings and above-average valuations. Investors expect these stocks to perform well in the future and are willing to pay high P/E multiples for this expected growth. The danger is that the price may become too high. Generally, once a company sports a P/E ratio above 50, the risk significantly escalates. Many technology growth stocks traded at a P/E ratio of above 100 during 1999. This is unsustainable. No company in the history of the stock market has been able to maintain such a high P/E level for a sustained period of time.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

While in Omaha for the Berkshire Hathaway annual meeting one year, I participated in an investment panel hosted by a local chapter of the Young Presidents’ Organization. I had the privilege of sharing the stage with such industry giants as Tom Russo, a partner of Gardner Russo & Gardner (famous for knowing more about consumer stocks than the management that runs them), and Tom Gayner, president and CIO of Markel Corp., a specialty insurance company that on many levels resembles the Berkshire of 30 years ago.

We were asked how much time a value investor should spend on macro forecasting. Usually macro forecasting is frowned upon in the value investing community, and Berkshire CEO Warren Buffett has everything to do with that. He is famous for saying (and I am paraphrasing), “My decision making would not change even if I knew what the Federal Reserve will do with interest rates next month.” There is sound logic behind this: Forecasting the economy is incredibly difficult in the short run. The economy is not unlike a black box with hundreds of gauges on it that in the near term give you conflicting readings about what’s inside it.

For this reason macro forecasting was disapproved of by value investors, and for 20 years this attitude paid off. The economic climate was favorable, the stock market was in overdrive, price-earnings ratios were expanding. Macro did not matter — until the housing bubble and financial crisis. Value investors who had had their heads in the sand got annihilated.

Things in life often swing, pendulum-like, from one extreme to another. Right after a crisis every investor is a macro expert. It’s kind of hilarious: Investors who just a few years earlier didn’t even know the names of most economic indicators are now spitting them out in conversations as though they had absorbed them with their mother’s milk. So what should investors do — become macro experts or economic ignoramuses?

Believe it or not, there is a logical and, more important, a practical answer to this question. As an investor you want to spend very little time on forecasting the weather (that is, what the Fed will do with interest rates next month or the rate of growth of the economy). Weather forecasting, first of all, is not always accurate, but it will certainly consume a lot of time and energy, and the forecasts have a very finite shelf life. Yesterday’s weather is irrelevant today. As long as you own companies that can survive rain without catching pneumonia — even a few weeks of rain — weather forecasting is a waste of time. This is what Buffett was implying by saying he didn’t want to be a macro forecaster.

However, instead of being a weatherman (or weatherwoman), as an investor you want to pay serious attention to “climate change” — significant shifts in the global economy that can impact your portfolio. This is exactly what Buffett did over the past few decades — he was warning about the weak dollar because of trade-deficit imbalances (he even put on a trade that bet against the dollar). He also warned about derivatives — “weapons of mass destruction” — and tried to cleanse them from the portfolio of General Re (an insurance company Berkshire acquired) as fast as he could.

It has been said that most ordinary people should have at least three to six months of living expenses (not including taxes) in a cash-equivalent reserve fund that is easily accessible (i.e., liquid). The amount needed for a one-month reserve is equal to the amount of expenses for the month, rather than the amount of monthly income. This is because during no-income months there is no income tax.

However, the situation might not be the same for physicians in today’s harsh economic climate.

The New Realities

Now, some physician-focused financial advisors, financial planners and Certified Medical Planners™ suggest even more reserve fund savings; up to two years. That’s because many factors come into play when determining how much a particular doctor’s family should have.

For example:

Does the family have one income or two? If the doctor is in a dual-income family with stable incomes and they live on a single income, the need for a liquid reserve is less.

How stable is the doctor’s income source? If a sole provider with an unstable income who spends all of the income each month, the need for a liquid cash reserve is high.

Does the doctor own the practice, work in a clinic, medical group, hospital or healthcare system? In other words – employee (less control) or employer (more control).

What is the doctor’s medical specialty and how has managed care penetrated his locale, or affected her focus? What about a DO, DDS/DMD or DPM, etc.

How does the family use its income each month; does it have a saver, spender, or investor mentality?

Does the family anticipate the possibility of large expenses occurring in the future (medical practice start-up costs or practice purchase; children, medical school student debts; auto or home loans; and/or liability suits, etc)?

Pan physician lifestyle?

The Past

In the ancient past, a doctor may have opted for a nine-twelve month reserve if the need for security was high – and a six-to-nine month reserve if the need for security was low. But today, even more may be needed. How about 15-18 months, or more? Perhaps even 24 months!

So, the following questions may be helpful in determining the amount of reserve needed by the physician:

1. How long would it take you to find another job in your medical specialty if you suddenly found yourself unemployed – same for your spouse?

2. Would you have to relocate – same for your spouse?

3. How much do you spend each month on fixed or discretionary expenses and would you be willing to lower your monthly expenses if you were unemployed?

Assessment

Once the amount of reserve is determined, the doctor should use the appropriate investment vehicles for the funds.

At minimum, the reserve should be invested in a money market fund. For larger reserves, an ultra-short-term bond fund might be appropriate for amounts over three-six months. While even larger reserves might be kept in a short term bond fund depending on interest rates and trends.

So, what do the initials M.D. really mean? … More Dough!

How much reserve do you have and where is it stashed?

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

9. We act with honesty, integrity and are always straightforward. 8. We strive to be innovative, creative, iconoclastic, and flexible. 7. We admit and learn from mistakes and don’t repeat them. 6. We work hard always as competitors are trying to catch up. 5. We treat others with dignity and respect. 4. We are the onus of consulting advice for the well being of others. 3. We fight complacency as former success is in the past. 2. The best management styles are timeless, not timely. 1. Our clients are colleagues and always come first.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Posted on February 21, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dan Ariely PhD

THE IRRATIONAL ECONOMIST

***

***

Of course you don’t need a human financial advisor … until you do. Today, we’ve had unfettered internet access to a wide range of investments, opinions and models for at least two decades. So, why the bravado to go it alone; fifteen positive years for equities, since 2009! Yet, the DJIA, S&P 500 and NASDAQ just plunged and plummeted today!

The financial advisor’s role is to remove the human element and emotion from investing decisions for something as personal as your wealth. Emotion drives the retail investor to sell low (fear) and buy high (greed). This is the reason why the average equity returns for retail investors is less than half of the S&P 500’s returns.

No, of course you don’t need a human financial advisor … until you do.

Understanding how economic behavior factors into health and health care decisions can benefit anyone interested in this field. However, the following groups of individuals may benefit most from the study of health economics:

Medical providers: Doctors, nurses, and assistants can evaluate new treatments, technologies, and services to determine ways to deliver value-based care. Medical providers benefit from understanding the economics behind these developments [MD/DO, DPM, DDS/DMD, RN, PA, etc].

Administrators: Health care administrators process insurance co-payments and manage financial metrics for health care providers. Learning the intricacies of health care economics can provide the necessary context as they liaise with insurance providers and use new technologies to process payments.

Policymakers or public health officials: Those who are in charge of policy decisions at the local, state, federal, or international levels benefit from understanding the economic relationship between stakeholders and the general public.

Business leaders: Because many Americans receive private insurance, health care becomes a major expense for employers. Business leaders must understand the health economics outlook to appease their employees, shareholders, and even their customers.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Posted on February 20, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

FDA recently approved the first new kind of painkiller since 1998. The drug, called Journavx and made by Vertex Pharmaceuticals, is a non-opioid medication, and the company says it comes with “no evidence of addictive potential.” One downside? At $15.50 per pill, it’s not cheap, and it’s not clear yet how much insurers will cover.

US stocks closed higher on Wednesday as investors weighed President Trump’s latest 25% tariff salvo and digested the Federal Reserve minutes for insight into future policy.

Wednesday’s minutes from the Fed’s January meeting revealed most central bank officials supported holding policy at restrictive levels amid concerns about persistent inflation.

Posted on February 19, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

SPONSOR: MarcinkoAssociates.com

***

***

Capital Market: This is a market where buyers and sellers engage in the trade of financial assets, including stocks and bonds. Capital markets feature several participants, including:

Companies: Firms that sell stocks and bonds to investors

Institutional investors: Investors who purchase stocks and bonds on behalf of a large capital base

Mutual funds: A mutual fund is an institutional investor that manages the investments of thousands of individuals

Hedge funds: A hedge fund is another type of institutional investor, which controls risk through hedging—a process of buying one stock and then shorting a similar stock to make money from the difference in their relative performance

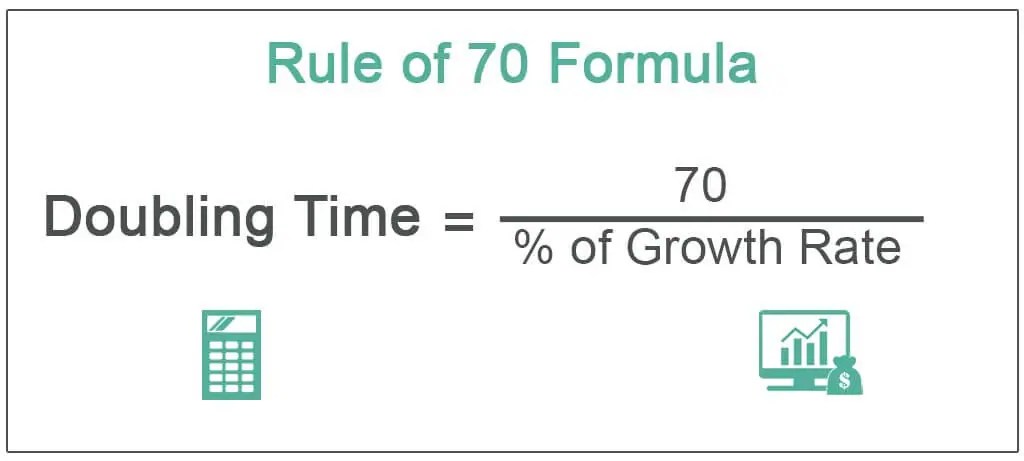

Whether you know it, or not, inflation is your biggest financial and investing enemy. Fortunately, the rule of 70 will tell you in how many years the value of money will be halved.

For example, you just need to divide 70 with the rate of inflation. So if the rate of inflation is 7%, then 70/7 = 10 years. Therefore, in 10 years, your 100 note will be worth 50.

Note: The phrase rule of thumb refers to an approximate method for doing something, based on practical experience rather than theory. This usage of the phrase can be traced back to the 17th century and has been associated with various trades where quantities were measured by comparison to the width or length of a human adult thumb.

Posted on February 17, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITIONS

By SBA and Staff Reporters

***

***

Acquisition

The acquiring of supplies or services by the federal government with appropriated funds through purchase or lease.

Affiliates

Business concerns, organizations, or individuals that control each other or that are controlled by a third party. Control may include shared management or ownership; common use of facilities, equipment, and employees; or family interest.

Best and Final Offer

For negotiated procurements, a contractor’s final offer following the conclusion of discussions.

Certificate of Competency

A certificate issued by the Small Business Administration (SBA) stating that the holder is “responsible” (in terms of capability, competency, capacity, credit, integrity, perseverance, and tenacity) for the purpose of receiving and performing a specific government contract.

Certified 8(a) Firm

A firm owned and operated by socially and economically disadvantaged individuals and eligible to receive federal contracts under the Small Business Administration’s 8(a) Business Development Program.

Contract

A mutually binding legal relationship obligating the seller to furnish supplies or services (including construction) and the buyer to pay for them.

Contracting

Purchasing, renting, leasing, or otherwise obtaining supplies or services from nonfederal sources. Contracting includes the description of supplies and services required, the selection and solicitation of sources, the preparation and award of contracts, and all phases of contract administration. It does not include grants or cooperative agreements.

Contracting Officer

A person with the authority to enter into, administer, and/or terminate contracts and make related determinations and findings.

Contractor Team Arrangement

An arrangement in which (a) two or more companies form a partnership or joint venture to act as potential prime contractor; or (b) an agreement by a potential prime contractor with one or more other companies to have them act as its subcontractors under a specified government contract or acquisition program.

Defense Acquisition Regulatory Council (DARC)

A group composed of representatives from each Military department, the Defense Logistics Agency, and the National Aeronautics and Space Administration and that is in charge of the Federal Acquisition Regulation (FAR) on a joint basis with the Civilian Agency Acquisition Council (CAAC).

Defense Contractor

Any person who enters into a contract with the United States for the production of material or for the performance of services for the national defense.

Electronic Data Interchange

Transmission of information between computers using highly standardized electronic versions of common business documents.

Emerging Small Business

A small business concern whose size is no greater than 50 percent of the numerical size standard applicable to the Standard Industrial Classification code assigned to a contracting opportunity.

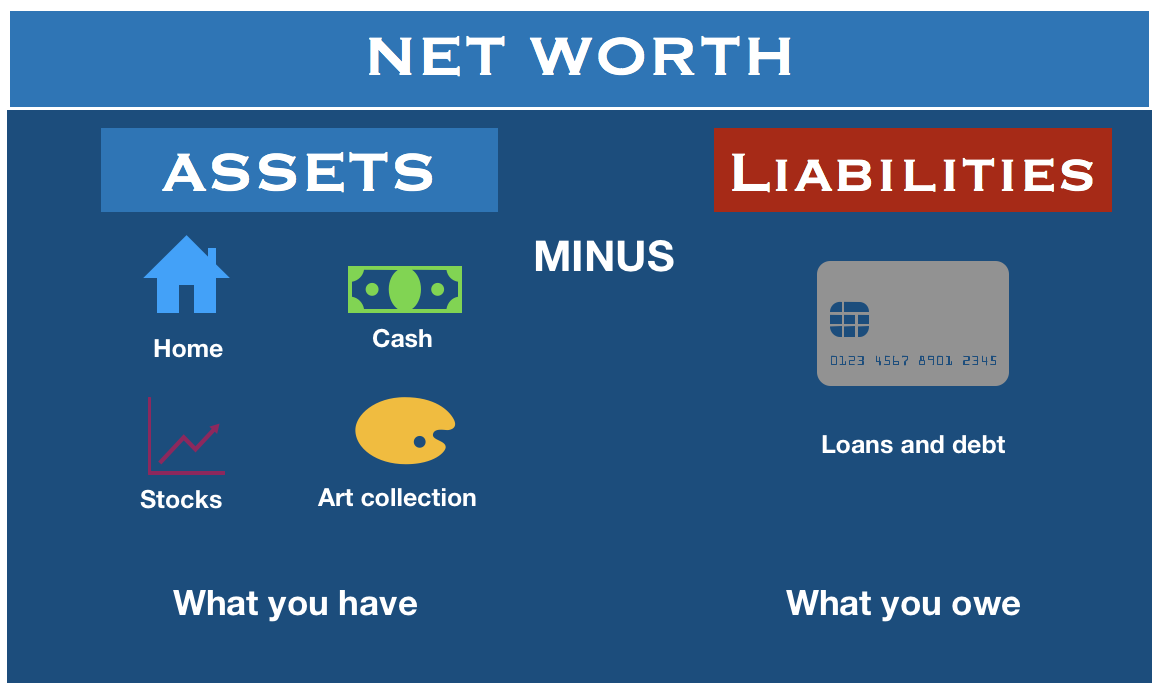

Equity

An accounting term used to describe the net investment of owners or stockholders in a business. Under the accounting equation, equity also represents the result of assets less liabilities.

Fair and Reasonable Price

A price that is fair to both parties, considering the agreed-upon conditions, promised quality, and timeliness of contract performance. “Fair and reasonable” price is subject to statutory and regulatory limitations.

Federal Acquisition Regulation (FAR)

The body of regulations which is the primary source of authority governing the government procurement process. The FAR, which is published as Chapter 1 of Title 48 of the Code of Federal Regulations, is prepared, issued, and maintained under the joint auspices of the Secretary of Defense, the Administrator of General Services Administration, and the Administrator of the National Aeronautics and Space Administration. Actual responsibility for maintenance and revision of the FAR is vested jointly in the Defense Acquisition Regulatory Council (DARC) and the Civilian Agency Acquisition Council (CAAC).

Full and Open Competition

With respect to a contract action, “full and open” competition means that all responsible sources are permitted to compete.

Intermediary Organization

Organizations that play a fundamental role in encouraging, promoting, and facilitating business-to-business linkages and mentor-protégé partnerships. These can include both nonprofit and for-profit organizations: chambers of commerce; trade associations; local, civic, and community groups; state and local governments; academic institutions; and private corporations.

Joint Venture

In the SBA Mentor-Protégé Program, an agreement between a certified 8(a) firm and a mentor firm to perform a specific federal contract.

Mentor

A business, usually large, or other organization that has created a specialized program to advance strategic relationships with small businesses.

Negotiation

Contracting through the use of either competitive or other-than-competitive proposals and discussions. Any contract awarded without using sealed bidding procedures is a negotiated contract.

Partnering

A mutually beneficial business-to-business relationship based on trust and commitment and that enhances the capabilities of both parties.

Prime Contract

A contract awarded directly by the Federal government.

Protégé

A firm in a developmental stage that aspires to increasing its capabilities through a mutually beneficial business-to-business relationship.

Request for Proposal (RFP)

A document outlining a government agency’s requirements and the criteria for the evaluation of offers.

SCORE

Counselors to America’s Small Business is a 12,400-member volunteer association sponsored by the SBA. SCORE matches volunteer business-management counselors with present prospective small business owners in need of expert advice.

Small Business

A business smaller than a given size as measured by its employment, business receipts, or business assets.

Small Business Development Centers (SBDC)

SBDCs offer a broad spectrum of business information and guidance as well as assistance in preparing loan applications.

Small Business Innovative Research (SBIR) Contract

A type of contract designed to foster technological innovation by small businesses with 500 or fewer employees. The SBIR contract program provides for a three-phased approach to research and development projects: technological feasibility and concept development; the primary research effort; and the conversion of the technology to a commercial application.

Small Disadvantaged Business Concern

A small business concern that is at least 51 percent owned by one or more individuals who are both socially and economically disadvantaged. This can include a publicly owned business that has at least 51 percent of its stock unconditionally owned by one or more socially and economically disadvantaged individuals and whose management and daily business is controlled by one or more such individuals.

Standard Industrial Classification (SIC) Code

A code representing a category within the Standard Industrial Classification System administered by the Statistical Policy Division of the U.S. Office of Management and Budget. The system was established to classify all industries in the US economy. A two-digit code designates each major industry group, which is coupled with a second two-digit code representing subcategories.

Subcontract