BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

In 1972, Nobel Laureate Kenneth J. Arrow, PhD shocked academe’ by identifying health economics as a separate and distinct field. Yet, the seemingly disparate insurance, tax, risk management and financial planning principles that he also studied are just now becoming transparent to some medical professionals and their financial advisors. Despite the fact that a basic, but hardly promoted premise of this new wave financial planning era, is imprecision.

Nevertheless, to informed cognoscenti like Certified Medical Planners™, the principles served as predecessors to the modern physician-focused financial advisory niche sector. In 2004, Arrow was selected as one of eight recipients of the National Medal of Science for his innovative views.

And now, as a long bull market may be over, and if the current “new-normal” prevails – meaning a 4.5% real annualized rate of return on equities and a 1.5% real rate on bonds – wealth accumulation for all may be reduced.

An Imprecise Science

There is a major variable, dominant in any marketplace that pushes an economy in a forward direction. It is called consumerism. This became apparent while waiting in a doctor’s office one recent afternoon.

Scenario:

The front office receptionist, who appeared to be about 21 years old, was breaking for lunch and her replacement, who appeared not much older, came over to assist. Realizing the propensity for a long wait, one was taken by the size of waiting room and the number of patients coming in and out of the office. [Americans consume healthcare and a lot of it]. There was another notable peculiarity. The sample prescription bags being carried out the door were no match for the bags under everyone’s eyes, including the doctor’s. The office staff was probably working overtime, if not two jobs, and the doctor was working harder and faster in a managed care system.

Assessment

Why? So they all could afford to buy and voraciously consume for their children and themselves. Americans indeed work longer hours than any other industrialized nation.

Conclusion

Finally, as women medical professionals entered the workforce in unprecedented numbers, the stock markets reached an all time high in 2025, even as money was spent at a feverish pace as the Federal Reserve pumped out money in inflammatory fashion.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com

Investing in Growth Stocks – Catching the Momentum [BIG-MO]

The growth style of investing focuses on companies with strong earnings and accelerating capital growth. A growth investor will make investment decisions based on forecasts of continuing growth in earnings. Growth investing emphasizes qualitative criteria, including value judgments about the company, its markets, its management, and its ability to extract future earnings growth from the particular industry.

Quantitative indicators of interest to the growth investor include high Price/Earnings ratios, Price/Sales ratios, and low dividend yields. A high P/E ratio suggests that the market is prepared to pay more per share in anticipation of future earnings. A low dividend yield suggests that the company is reinvesting rather than distributing profits. These indicators are considered in relation to the company’s immediate competitors. The companies with the highest P/E ratios relative to their industry will often be dominant within their market segment and have strong growth prospects. Growth investors will generally focus on premium and leading-edge companies.

***

***

Some industry sectors by their nature have stronger growth characteristics, particularly more innovative and speculative industries.

For example, during the bull market run on the U.S. stock markets during the late 1990s, the technology sector was a major area of growth investment. On observing strong earnings growth, a growth investor will decide whether to buy shares based on whether the company’s growth is going to continue at its present rate, to increase, or to decrease. If it is expected to increase, the growth investor will consider it a candidate for purchase. The key research question is: at what point will the company’s growth flatten out, or fall? If a company’s growth rate slows or reverses, it is no longer attractive to a growth investor. Growth investors are normally prepared to pay a premium for what they believe to be high quality shares. The potential downside in growth investing is that if a company goes into sudden decline and the share price falls, you can lose capital value rapidly.

Growth stocks, like the current “Magnificent-Seven“, carry high expectations of above-average future growth in earnings and above-average valuations. Investors expect these stocks to perform well in the future and are willing to pay high P/E multiples for this expected growth. The danger is that the price may become too high. Generally, once a company sports a P/E ratio above 50, the risk significantly escalates. Many technology growth stocks traded at a P/E ratio of above 100 during 1999. This is unsustainable. No company in the history of the stock market has been able to maintain such a high P/E level for a sustained period of time.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

While health care is not “do-it-yourself,” an informed patient can be an asset. A poorly informed patient, on the other hand, clearly complicates treatment. Assume the responsibility of being the primary information source and educator for your patient. To help deal with a self-diagnosing patient, consider the following as suggested by: David B. Troxel, MD, Medical Consultant to The Doctors Company:

Encourage patients to always check with you about the accuracy of information obtained from external sources. Use the intake time to find out what Internet information the patient has found.

Directly discuss what the patient has read, even if the patient’s external source is a good one in your professional opinion. The exchange enhances your relationship with the patient and can increase treatment compliance. Welcome questions, and help put the patient’s information in the appropriate context.

Provide your patient with a list of Web sites that provide accurate information, such as the Centers for Disease Control and Prevention (www.cdc.gov). Make sure the patient understands the limitations of the Internet.

Document in the patient’s chart your diagnosis, your treatment management plan, and medication prescribed, as well as the reasons behind your decisions.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Posted on February 21, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dan Ariely PhD

THE IRRATIONAL ECONOMIST

***

***

Of course you don’t need a human financial advisor … until you do. Today, we’ve had unfettered internet access to a wide range of investments, opinions and models for at least two decades. So, why the bravado to go it alone; fifteen positive years for equities, since 2009! Yet, the DJIA, S&P 500 and NASDAQ just plunged and plummeted today!

The financial advisor’s role is to remove the human element and emotion from investing decisions for something as personal as your wealth. Emotion drives the retail investor to sell low (fear) and buy high (greed). This is the reason why the average equity returns for retail investors is less than half of the S&P 500’s returns.

No, of course you don’t need a human financial advisor … until you do.

Posted on February 9, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

ACADEMIC DEFINITIONS

By Staff Reporters

***

***

What Is a PhD?

A PhD is a doctorate degree and is the highest postgraduate qualification awarded by universities. It involves undertaking original research in a narrow subject field and typically takes 4 years to complete.

A PhD in Business Administration provides an individual with a specialized and research-based background for a topic in the business management field. This is one of the key reasons it’s sought after by those who wish to work in business-related academia or research.

What Is a DBA?

A Doctor of Business Administration (DBA) is a business-orientated professional doctorate. Like a PhD, it is the highest-level postgraduate qualification which you can obtain from a university.

The degree program focuses on providing practical and innovative business management knowledge which can apply to any workplace. DBAs are designed for experienced practitioners such as senior managers, consultants and entrepreneurs who want to further their practical abilities.

This form of doctorate was first introduced as a way of allowing a distinction to be made between experienced practitioners and expert practitioners. The doctorate is an equal alternative to a traditional PhD and is an advanced follow-up for a Master’s in Business Administration (MBA).

Is a DBA and PhD Equivalent?

A Doctor of Business Administration (DBA) is equivalent to a Doctor of Philosophy (PhD); however, there are fundamental differences between these two doctoral degrees. These differences are nearly always at the center of DBA vs PhD discussions, and they stem from the intended career path of the student following their degree.

A PhD focuses on the ‘theory’ underpinning business management, whereas a DBA focuses on the ‘practical’ concepts. Those who complete a PhD in business management usually do so as they wish to pursue a career in research or academia. Those who complete a DBA do so as they want to pursue a more advanced role in the business industry or within their organization.

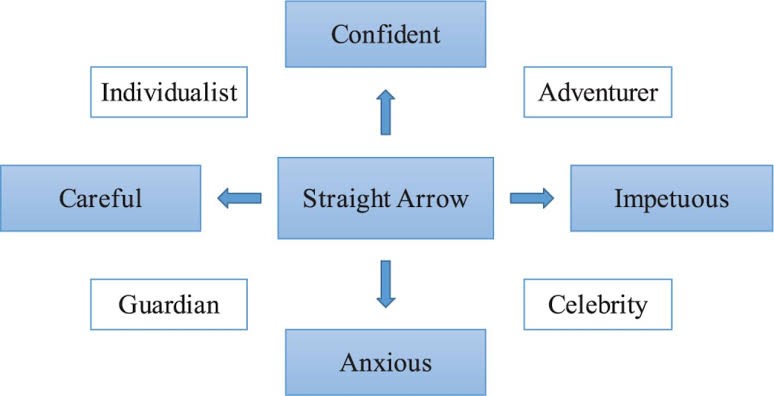

Fund managers Tom Bailard, Larry Biehl and Ron Kaiser identified five types of investors, each type characterized by their investment preferences and actions. These 5 types are: Individualists, Adventurers, Celebrities, Guardians and Straight Arrows. Key to the different categories is their different attitude to seeking professional financial advice. Defined below:

Individualists have faith in their own investment abilities so do not approach a financial adviser. But they are also cautious.

Adventurers are what may be called high rollers, in that they like big bets, tend not to diversify and are happy to put all their eggs in one basket. They, too, are unlikely to seek financial advice.

Celebrities tend to follow the crowd in investment terms but are aware of their lack of expertise so frequently consult advisers.

Guardians are fearful of losing money, thus prefer rock-solid investments such as government bonds. They, too, are likely to seek professional investment advice.

Straight Arrows exhibit some of the characteristics of individualists and some of adventurers.

(“Informed Voice of a New Generation of Fiduciary Advisors for Healthcare”)

For most lay folks, personal financial planning typically involves creating a personal budget, planning for taxes, setting up a savings account and developing a debt management, retirement and insurance recovery plan. Medicare, Social Security and Required Minimal Distribution [RMD] analysis is typical for lay retirement. Of course, we can assist in all of these activities, but lay individuals can also create and establish their own financial plan to reach short and long-term savings and investment goals.

But, as fellow doctors, we understand better than most the more complex financial challenges doctors can face when it comes to their financial planning. Of course, most physicians ultimately make a good income, but it is the saving, asset and risk management tolerance and investing part that many of our colleagues’ struggle with. Far too often physicians receive terrible guidance, have no time to properly manage their own investments and set goals for that day when they no longer wish to practice medicine.

For the average doctor or healthcare professional, the feelings of pride and achievement at finally graduating are typically paired with the heavy burden of hundreds of thousands of dollars in student loan debt.

You dedicated countless hours to learning, studying, and training in your field. You missed birthdays and holidays, time with your families, and sacrificed vacations to provide compassionate and excellent care for your patients. Amidst all of that, there was no time to give your finances even a second thought.

Between undergraduate, medical school, and then internship and residency, most young physicians do not begin saving for retirement until late into their 20s, if not their 30s. You’ve missed an entire decade or more of allowing your money and investments to compound and work for you. When it comes to addressing your financial health and security, there’s no time to waste.

Posted on January 3, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

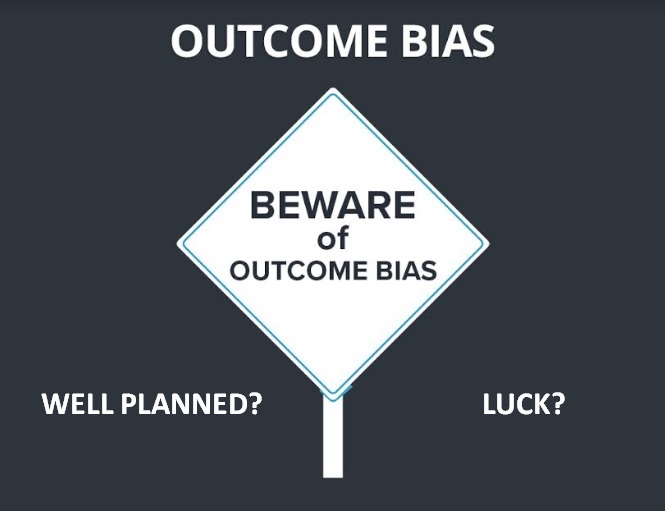

Outcome bias is judging a decision based on its result rather than the quality of the decision at the time it was made.

It’s like saying a bad poker play was smart because you won the hand. Or, a bad stock picker or financial advisor was good because the price went up!

According to psychologist and colleague Dan Ariely PhD, this bias ignores the process and focuses solely on the outcome. It’s why we celebrate lucky breaks and criticize thoughtful risks that didn’t pan out.

So, the next time you’re evaluating a decision, focus on the reasoning behind it, not just the end result.

Choice Overload is the difficulty in making a decision when faced with too many options. It’s like standing in front of an ice cream counter with 31 flavors and feeling paralyzed.

Among personal decision-makers, a prevention focus is activated and people are more satisfied with their choices after choosing among few options compared to many options, i.e. choice overload. However, individuals can also experience a reverse choice overload effect when acting as proxy decision-maker, too.

It is widely accepted that having more choices is inherently positive. When there are more available options from which to choose, an individual is more likely to be able to select the particular option that is the best fit and most likely to satisfy them. Choice is typically thought to be related to personal freedom and enhanced well-being.

Therefore, according to colleague Neal Baum MD, for most individuals the ultimate goal is to constantly maximize their choices in life to increase their overall satisfaction and well-being. The decision-making process, however, is a complex cognitive task that does not always lead to positive outcomes.

Thus, while having options is generally good, too many choices can lead to anxiety and decision fatigue. This is why curated selections and recommendations are so popular – they simplify the decision-making process’ according to another colleague Dan Ariely PhD.

So, when you’re overwhelmed by choices, narrow them down to a manageable number and make your decision easier.

OK – I was a Certified Financial Planner® before my academic team launched the Certified Medical Planner™ online and on-ground chartered education and board certification designation program a few years ago. I am now CFP reformed and in remission.

Enter the Certified Medical Planner™ CharteredDesignation

Today, we are of course, gratified that Certified Medical Planner™ mark notoriety is growing organically in the healthcare, as well as financial services, industry.

Even uber-blogger Mike Kitces MSFS, MTAX, CFP, CLU, ChFC, RHU, REBC, CASL has taken note of us in his musings on the Nerd’s Eye View website. And, the reality is that there are a growing number of CFP educational programs at the post-CFP niche market level.

But, none for healthcare industrial complex: for doctors … by doctors!

Popularity of our Text Books

However, it is our modern, innovative and proprietary Certified Medical Planner™ textbooks and dictionaries that have exploded in the academic marketplace.

In fact, they are now redacted in thousands of medical, graduate, law and B-schools and libraries, as well as colleges and universities throughout the nation. This includes the Library of Congress, National Institute of Health and the Library of Congress.

What Gives?

We have been told that this textbook popularity and publishing success is because of their balanced and peer-reviewed nature; something not very widespread in the financial services industry that is prone to gross and overstated advertising, salesmanship and marketing hyperbole. And, for this we are very gratified.

But, is there another reason our books are so popular?

A bit of networking and research suggests that interested folks may be eschewing the actual course work in favor of just the high quality textbooks! UGH!

So, what do you think? Matriculation with the professional mark versus self study without the designation mark. Please opine.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements.

Subscribe: MEDICAL EXECUTIVE POST for curated news, essays, opinions and analysis from the public health, economics, finance, marketing, IT, business and policy management ecosystem.

Sensation, emotion and cognition work by Contrast Effect [cognitive bias].

Now, such perception is not only on an absolute scale, it also functions relative to prior stimuli. This is why room temperature water feels hot when experienced after being exposed to the cold. It is also why the cessation of negative emotions “feels” so good.

Cognitive bias functioning also works on this principle. So one’s ability to analyze information and draw conclusions is very much related to the context with in which the analysis takes place, and to what information was originally available. This is why it is so important to manage one’s own expectations as well as those of a financial advisor’s or stock broker’s clients.

For example, a client is much more likely to be satisfied with a 10% portfolio return if they were expecting 7% than if they were hoping for 15%.

The www.MedicalBusinessAdvisors.com is focused solely on appraising medical practices, surgery centers [ASCs], medicine, podiatry, optometry and allied healthcare businesses.

Working with our affiliated partners, like the ME-P and others, we are also available for behemoth multi-specialty medical practices, major clinics, hospitals, related healthcare organizations and networks, and PHOs, etc.

We are backed by the expertise of dedicated appraisers and valuation analysts who are trained by the foremost organizations in our industry www.CertifiedMedicalPlanner.org

Practice owners, attorneys and accountants retain us for projects including, but not limited to the following:.

There are a Myriad of Reasons for Obtaining a Medical Practice Valuation and Appraisal Engagement

Outright selling-buying

Partnership and Associate buy-in / buy-out

Mergers and Acquisitions

Organic growth tracking

Hospital integrations

Private and public reporting

Financing and Venture Capital

Estate and tax planning

Our Capability

We have the ability to provide extensive analysis of value components in healthcare practices and provide appraisals based on business, economic, and market conditions. This involves detailed examination of financials and clinical data in the context of numerous factors including medical specialty, physician supply and demand, payer mix, regulatory environment, regional dynamics, and risk premium.

Assessment

Our methods and approaches adhere to accepted standards of healthcare practice appraisal and utilize direct market data to reach justifiable conclusions. These are documented in a comprehensive report which is tailored to meet the need of the specific engagement.

SAMPLE ENGAGEMENTS: See partial engagement list below.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

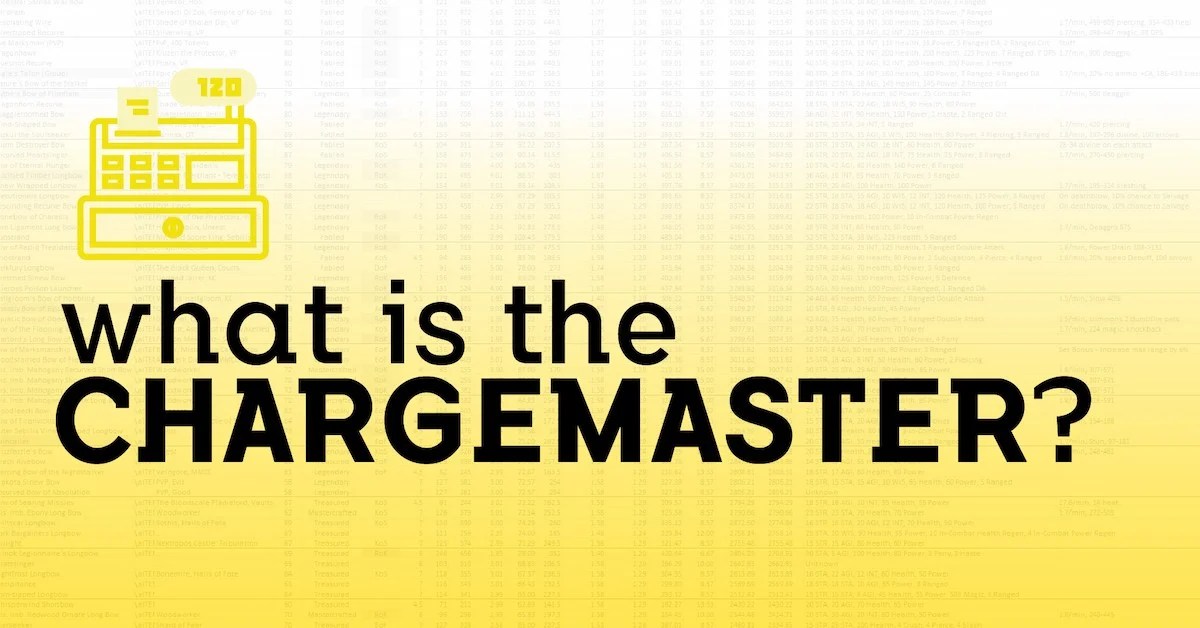

Classic Definition: A comprehensive review of a physician, clinic, facility, medical provider or hospital’s charges to ensure Medicare billing compliance through complete and accurate HCPCS/CPT and UB-92 revenue code assignments for all items including supplies and pharmaceuticals. The charge master captures the costs of each procedure, service, supply, prescription drug, and diagnostic test provided at the hospital, as well as any fees associated with services, such as equipment fees and room charges

Modern Circumstance: A charge master quizlet (charge description master [CDM]) document that contains a computer-generated list of procedures, services, and supplies with charges for each. Charge master rates are essentially the health care market equivalent of Manufacturer’s Suggested Retail Price (MSRP) in the car buying market. Poor charge master maintenance can lead to overpayments or underpayments. It can also lead to claim rejections from insurance companies, poor patient experience, or compliance violations.

Paradox Examples:

Superbills: An encounter form that is the financial record source document used by healthcare providers and other personnel to record treated diagnoses and services rendered to the patient during the current encounter. It is also called a superbill.

Payment rates: Almost no one actually pays the publicized charge master rates. The vast majority of health care consumers are represented by a payer of some kind, such as a commercial health insurance company, Medicaid, or Medicare. Commercial insurers negotiate the actual prices they pay during the process of contracting with providers. Medicare and Medicaid establish their own payment levels independent of hospitals’ charge master lists – Medicare through the federal government and Medicaid through state governments.

Cash pay: The sad irony of the charge master is that the uninsured are the most likely to be billed charge master rates because they are not represented by a third-party payer.

Problematic features: Other items also impede the ability of payers to have a comprehensive and accurate understanding of hospitals’ financial positions. For example, nonprofit hospitals are required to report charity care, bad debt expenses, community benefit initiatives, and uncompensated care. When these expenses are reported at the charge master level, expenses can be paradoxically overstated, potentially making a hospital’s financial position look worse than it actually is.

Yield: For bonds and other fixed-income securities, yield is a rate of return on those securities. There are several types of yields and yield calculations. “Yield to maturity” is a common calculation for fixed-income securities, which takes into account total annual interest payments, the purchase price, the redemption value, and the amount of time remaining until maturity.

Yield curve: A line graph showing the yields of fixed income securities from a single sector (such as Treasuries or municipals), but from a range of different maturities (typically three months to 30 years), at a single point in time (often at month-, quarter- or year-end). Maturities are plotted on the x-axis of the graph, and yields are plotted on the y-axis. The resulting line is a key bond market benchmark and a leading economic indicator.

Yield to maturity [real yield to maturity]: Yield to maturity is a common performance calculation for fixed-income securities, which takes into account total annual interest payments, the purchase price, the redemption value, and the amount of time remaining until maturity. Real yield to maturity is simply yield to maturity minus any “inflation premium” that had been added/priced in. (See Real yield.)

Yield ratio: A ratio of one yield divided by another. Most often used as a relative value measurement.

Yield spread: A “spread,” in fixed income parlance, is simply a difference. Yield spreads measure yield differences, typically between debt securities with high credit ratings (which typically have lower yields) and those with lower ratings (which typically have higher yields). Yield spreads can also be measured between debt securities with different maturities (shorter-maturity securities typically have lower yields and longer-maturity securities typically have higher yields).

Yield trap: An investment that can lure investors with an attractive yield that may not be fundamentally sustainable, or that may lead to undesired price volatility. Yield traps can lurk in both the equity and fixed income markets. They have a tendency to prey on those who can least afford them, including retirement investors looking for increased relative income and stability, who may have been too focused on their income goals and not enough on stability.

More than 20 years ago I crafted a comprehensive holistic financial plan for a young doctor colleague who was born in 1959. In fact, he was not even a medical student at the time; so “canned off-the-shelf plans”, computer generated software or generic spread sheets were not a viable creation option. It was all a granular, detailed, specific and cognitive work-product. Today, he is a board-certified internist.

So, in 2023, it is right and just to take a look back and see how well, or poorly, we’ve fared.

Now, I appreciate more than most how financial planning is a “process”; and not an isolated event. Yet, all sorts of “advisors” and “consultants” create and charge hefty fees for same, and on-going monitoring, every day.

The ME-P Challenge

Nevertheless, I challenge all you mid-career or senior financial planners /advisors to this competition; regardless of degree, certification or designation.

“Show me your financial plan” – AND – “I’ll show you my financial plan”

Here Comes the Judge

Then, our community of ME-P readers, subscribers, visitors and “judges” will decide the winner.

The contest is open to any financial advisor, planner, consultant, wealth manager, CFP®, CFA, insurance agent, CPA or CLU, ChFC, or stock-broker, etc., who is not afraid of transparency in his or her work product and purported expertise.

***[Creating and Evaluating a physician focused financial plan]

***

Assessment

So, just send in a copy of any “blinded” physician-focused financial plan that is about 21 years old. We will post for all to see and review …. warts and all … including my own; three part mega-plan!

The winner will receive bragging rights, academic swagger, and expert promotion to our entire ME-P ecosystem and network of medical, business, law and graduate school communities; as well as physicians, nurses, healthcare executives and allied health care professionals.

An informed sought-after and lucrative sector – indeed!

IOW: Free publicity and positive “new-wave” PR – PRICELESS!

Of course, as an educator and professor of health economics and finance, we are pleased to present you with the deep medical business knowledge and detailed financial,managerial and accounting techniques used, with some real-life “tips and pearls” developed over the last two decades of R&D, right here:

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

A paradox is a logic and self-contradictory statement or a statement that runs contrary to one’s expectation. It is a statement that, despite apparently valid reasoning from true or apparently true premises, leads to a seemingly self-contradictory or a logically unacceptable conclusion. A paradox usually involves contradictory-yet-interrelated elements that exist simultaneously and persist over time. They result in “persistent contradiction between interdependent elements” leading to a lasting “unity of opposites”.

***

And so, as we plan for our financial future thru a New Year Resolution for 2025, it’s helpful to be cognizant of these paradoxes. While there’s nothing we can do to control or change them, there is great value in being aware of them, so we can approach them with the right tools and the right mindset.

According to Adam Grossman, here are seven [7] of the paradoxes that can bedevil financial decision-making, clients and financial advisors, alike:

There’s the paradox that all of the greatest fortunes—Carnegie, Rockefeller, Buffett, Gates—have been made by owning just one stock. And yet the best advice for individual investors is to do the opposite: to own broadly diversified index funds. More:https://tinyurl.com/285vftx4

There’s the paradox that the stock market may appear over valued and yet it could become even more overvalued before it eventually declines. And when it does decline, it may be to a level that is even higher than where it is today.

There’s the paradox that we make plans based on our understanding of the rules—and yet Congress can change the rules on us at any time, as the recent 2024 election results attest.

There’s the paradox that we base our plans on historical averages—average stock market returns, average interest rates, average inflation rates and so on—and yet we only lead one life, so none of us will experience the average.

There’s the paradox that we continue to be attracted to the prestige of high-cost colleges, even though rational analysis that looks at return on investment tells us that lower-cost state schools are usually the better bet.

There’s the paradox that early retirement seems so appealing—and has even turned into a movement—and yet the reality of early retirement suggests that we might be better off staying at our desks.

There’s the paradox that retirees’ worst fear is outliving their money and yet few choose the financial product that is purpose-built to solve that problem: the single-premium immediate annuity.

Classic Definition: Despite rising costs, health care often is of poor quality. Evidence from a classic medical improvement outcomes study assessed care of patients with several chronic diseases. This study found that patients’ functional health status outcomes are similar to care rendered by specialists and generalists but that generalists use far fewer resources. Similar outcome at lower cost represents higher value.

Modern Circumstance: Current solutions to improving care quality may do more harm than good if they focus more on diseases than on people. Efforts to improve the parts (evidence-based care of specific diseases) may not necessarily improve the whole (the health of people and populations).

Expanding access to specialty care, for example, has been proposed as both a source of and a solution for deficiencies in quality of care. Primary care is touted as an essential building block of a high-value health care system even as it is undermined by systems attempting to improve the quality, effectiveness, and value of their health care..

Paradox Example: The above contradictions plague improvement efforts in health care systems around the world, particularly the United States The paradox is that compared with specialty care or with systems dominated by specialty medical care, primary care is associated with the following: (1) poorer quality care for individual diseases, yet (2) similar functional health status at lower cost for people with chronic disease, and (3) better quality, better health, greater health equity and lower costs for whole peoples and populations.

And so, this contradiction plagues improvement efforts in health care systems around the world, particularly the United States.

Classic: Investment purchases and private expenditures of healthcare firms, the value of related construction, and the change in inventory during the year.

Modern: Gross Revenue Per Day is the average amount charged by a hospital for one day of inpatient care (gross inpatient revenue divided by patient-census days).

Gross Revenue Per Discharge: The average amount charged by a hospital to treat an inpatient from admission to discharge (gross inpatient revenue divided by discharges).

Gross Revenue Per Visit: The average amount charged by a hospital for an outpatient visit (gross outpatient revenue divided by outpatient visits).

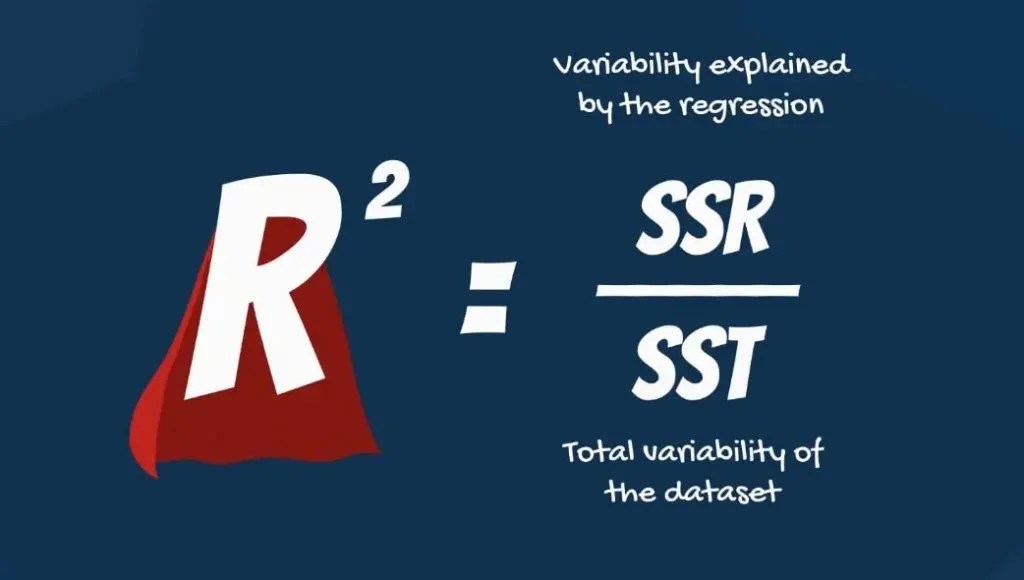

R-squared is an investment portfolio performance and risk measure that indicates how much of a portfolio’s performance fluctuations were attributable to movements in the portfolio’s benchmark index. R-squared can range from 0-100%.

IOW: R Squared, also known as the coefficient of determination, is a statistical measure used in the context of regression analysis. It represents the proportion of the variance in the dependent variable that is predictable from the independent variable(s). Essentially, it provides a measure of how well the observed outcomes are replicated by the model, based on the proportion of total variation of outcomes explained by the mode

For example, an R-squared of 100% indicates that all portfolio performance movements were attributable to movements in the benchmark index—they correlate perfectly to the benchmark.

Conversely, an r-squared of 0% indicates that there is no correlation between the performance movements of the portfolio and the benchmark.

Classic Definition: Employers write checks that cover most health insurance premiums for employees and their dependents. But as the late Princeton health economist Uwe Reinhardt PhD once explained, employer-sponsored insurance is like a pickpocket taking money out of your wallet at a bar and buying you a drink. You appreciate the cocktail until you realize you paid for it yourself.

Modern Circumstance: With health coverage, employers write the check to the insurer, but employees bear the cost of the premium — the entire premium, not just the portion listed as their contribution on their pay stub. The premium money that goes to the insurance company is cash that employers would otherwise deposit in employees’ accounts like the rest of their salary.

Paradox Example: The fallacy paradox is in thinking an employer’s contribution comes out of profits. In fact, higher health insurance premiums mean lower wages for workers. Since 1999, health insurance premiums have increased 147 percent and employer profits have increased 148 percent. But in that time, average wages have hardly moved, increasing just 7 percent. Clearly workers’ wages, not corporate profits, have been paying for higher health insurance premiums. Health care costs are one — though not the only — reason wages have stagnated over the last few decades. With health insurance costs rising faster than growth in the economy, more labor costs go to benefits like health insurance and less to take-home pay. Yet the paradox that employees don’t pay for their own health insurance is widespread:

The first reason is that individuals cannot be sure what causes their wages to change or remain stagnant for decades.

The second reason is that employers want Americans to believe that they pay for their workers’ health insurance.

The third reason is that there are those who profit from the employment-based system: drug companies, device manufacturers, specialty physicians and high-income individuals.

And so, they all want you to believe companies are being magnanimous in giving you insurance, but they are not!

Frequently, we hear the axiom that asset allocation is the most important investment decision, explaining 93.6% of portfolio returns. The presumption has been that once the risk tolerance and time horizon have been established, investing is simply a matter of implementing a fixed mix of stocks, bonds, and cash using mutual funds selected for this purpose. This axiom is based on a famous study by Brinson, Hood, and Beebower (BHB) published in the Financial Analysts Journal in July/August 1986. It is the stuff of most modern business school and graduate students in economics and finance.

Enter the Critics

One critic claims that BHB’s conclusions and the interpretation of their conclusions are wrong, stating that because of several methodological problems, BHB needed to make certain assumptions for their analysis to go forward. They assumed that the average asset-class weights for the 10-year period studied are the same as the actual normal policy weights; that investments in foreign stocks, real estate, private placements, and venture capital can be proxied by a mix of stocks, bonds, and cash; and that the benchmarks for stocks, bonds, and cash against which fund performance was measured are appropriate. The author believes that each of these assumptions can lead to a faulty measurement of success or failure at market timing and stock selection.

The Jahnke Study

William Jahnke claims that BHB erred in their focus on explaining the variation of quarterly portfolio returns rather than portfolio returns over the 10-year period studied. According to the study, asset allocation policy explains only a small fraction of the range of 10-year portfolio returns earned by the pension funds reported in the study. The author concluded that this discrepancy is caused by the effect of compounding returns. He adds that BHB were wrong to use variance of quarterly returns rather than the standard deviation. Use of standard deviation would reduce the often cited 93.6% to about 79%. Moreover, BHB did not consider the cost of investing, such as operating expenses, management fees, brokerage commissions, and other trading costs, which are more significant for individual investors than for the pension plans studied. Jahnke claims that excessive costs can reduce wealth accumulation by 50%.

Note: (“The Asset Allocation Hoax,” William W. Jahnke, Journal of Financial Planning, February 1997, Institute of Certified Financial Planners [303] 759-4900).

Assessment

Finally, the author takes issue with establishing long-term fixed asset class weights. Asset allocation should be a dynamic process. Higher equity return expectations should in turn produce larger equity allocations, other things being equal.

Conclusion

Are doctors different than the average investor noted in this essay?

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Financial planning as a concept has been around for a long time, but not as we know it today. When Loren Dunton set up the Society for Financial Counseling Ethics in 1969, or when the first graduating class of the College of Financial Planning graduated in 1973, financial planning was very different. It was centered around selling limited partnerships, which came to end with the Tax Reform Act of 1986.

However, financial planning re-emerged — all thanks to Richard Averitt III. The certified financial planner gave new meaning to financial planning, this time with a focus on who the client is and what their needs are. This approach was purely methodological in nature.

Soon after, financial planning picked up again. According to the Certified Financial Planner (C.F.P.) Board of Standards in Denver, today, there are more than 94,000 C.F.P.s worldwide, including over 48,000 in the U.S. Additionally, there are also organizations that have been set up for C.F.P.s, such as the Financial Planning Association (FPA), which has approximately 22,000 members.

And, don’t forget the emerging Certified Medical Planner™ professional fiduciary designation for physicians, dentists, nurses and allied healthcare clients.

Financial planning, as we know it now, includes investing, tax planning, retirement planning, and basically other ways to get your finances in order and create mindful budgets to ensure a safe and secure future. Getting a step ahead of your spending and finances is beneficial in the long run and Financial Planning Month in October is the perfect time to do that.

The following are some of the most common psychological biases. Some are learned while others are genetically determined (and often socially reinforced). While this essay focuses on the financial implications of these biases, they are prevalent in most areas in life.

[A] Incentives

It is broadly accepted that incenting someone to do something is effective, whether it be paying office staff a commissions to sell more healthcare products, or giving bonuses to office employees if they work efficiently to see more HMO patients. What is not well understood is that the incentives cause a sub-conscious distortion of decision-making ability in the incented person. This distortion causes the affected person – whether it is yourself or someone else – to truly believe in a certain decision, even if it is the wrong choice when viewed objectively. Service professionals, including financial advisors and lawyers, are affected by this bias, and it causes them to honestly offer recommendations that may be inappropriate, and that they would recognize as being inappropriate if they did not have this bias. The existence of this bias makes it important for each one of us to examine our incentive biases and take extra care when advising physician clients, or to make sure we are appropriately considering non-incented alternatives.

[B] Denial

Denial is a well known, but under-appreciated, psychological force. Physicians, clients and professionals (like everyone else) are prone to the mistake of ignoring a painful reality, like putting off an unpleasant call (thus prolonging a problematic situation and potentially making it worse) or not opening account statements because of the desire not to see quantitative proof of losses. Denial also manifests itself by causing human beings to ignore evidence that a mistake has been made. If you think of yourself as a smart person (and what professional doesn’t?), then evidence pointing to the conclusion that a mistake has been made will call into question that belief, causing cognitive dissonance. Our brains function to either avoid cognitive dissonance or to resolve it quickly, usually by discounting or rationalizing the disconfirming evidence. Not surprisingly, colleagues at Kansas State University and elsewhere, found that financial denial, including attempts to avoid thinking about or dealing with money, is associated with lower income, lower net worth, and higher levels of revolving credit.

[C] Consistency and Commitment Tendency

Human beings have evolved – probably both genetically and socially – to be consistent. It is easier and safer to deal with others if they honor their commitments and if they behave in a consistent and predictable manner over time. This allows people to work together and build trust that is needed for repeat dealings and to accomplish complex tasks. In the jungle, this trust was necessary to for humans to successfully work as a team to catch animals for dinner, or fight common threats. In business and life it is preferable to work with others who exhibit these tendencies. Unfortunately, the downside of these traits is that people make errors in judgment because of the strong desire not to change, or be different (“lemming effect” or “group-think”). So the result is that most people will seek out data that supports a prior stated belief or decision and ignore negative data, by not “thinking outside the box”. Additionally, future decisions will be unduly influenced by the desire to appear consistent with prior decisions, thus decreasing the ability to be rational and objective. The more people state their beliefs or decisions, the less likely they are to change even in the face of strong evidence that they should do so. This bias results in a strong force in most people causing them to avoid or quickly resolve the cognitive dissonance that occurs when a person who thinks of themselves as being consistent and committed to prior statements and actions encounters evidence that indicates that prior actions may have been a mistake. It is particularly important therefore for advisors to be aware that their communications with clients and the press clouds the advisor’s ability to seek out and process information that may prove current beliefs incorrect. Since this is obviously irrational, one must actively seek out negative information, and be very careful about what is said and written, being aware that the more you shout it out, the more you pound it in.

[D] Pattern Recognition

On a biological level, the human brain has evolved to seek out patterns and to work on stimuli-response patterns, both native and learned. What this means is that we all react to something based on our prior experiences that had shared characteristics with the current stimuli. Many situations have so many possible inputs that our brains need to take mental short cuts using pattern recognition we would not gain the benefit from having faced a certain type of problem in the past. This often-helpful mechanism of decision-making fails us when past correlations or patterns do not accurately represent the current reality, and thus the mental shortcuts impair our ability to analyze a new situation. This biologic and social need to seek out patterns that can be used to program stimuli-response mechanisms is especially harmful to rational decision-making when the pattern is not a good predictor of the desired outcome (like short term moves in the stock market not being predictive of long term equity portfolio performance), or when past correlations do not apply anymore.

[E] Social Proof

It is a subtle but powerful reality that having others agree with a decision one makes, gives that person more conviction in the decision, and having others disagree decreases one’s confidence in that decision. This bias is even more exaggerated when the other parties providing the validating/questioning opinions are perceived to be experts in a relevant field, or are authority figures, like people on television. In many ways, the short term moves in the stock market are the ultimate expression of social proof – the price of a stock one owns going up is proof that a lot of other people agree with the decision to buy, and a dropping stock price means a stock should be sold. When these stressors become extreme, it is of paramount importance that all participants in the financial planning process have a clear understanding of what the long-term goals are, and what processes are in place to monitor the progress towards these goals. Without these mechanisms it is very hard to resist the enormous pressure to follow the crowd; think social media.

[F] Contrast

Sensation, emotion and cognition work by contrast. Perception is not only on an absolute scale, it also functions relative to prior stimuli. This is why room temperature water feels hot when experienced after being exposed to the cold. It is also why the cessation of negative emotions “feels” so good. Cognitive functioning also works on this principle. So one’s ability to analyze information and draw conclusions is very much related to the context with in which the analysis takes place, and to what information was originally available. This is why it is so important to manage one’s own expectations as well as those of clients. A client is much more likely to be satisfied with a 10% portfolio return if they were expecting 7% than if they were hoping for 15%.

[G] Scarcity

Things that are scarce have more impact and perceived value than things present in abundance. Biologically, this bias is demonstrated by the decreasing response to constant stimuli (contrast bias) and socially it is widely believed that scarcity equals value. People who feel an opportunity may “pass them by” and thus be unavailable are much more likely to make a hasty, poorly reasoned decision than they otherwise would. Investment fads and rising security prices elicit this bias (along with social proof and others) and need to be resisted. Understanding that analysis in the face of perceived scarcity is often inadequate and biased may help professionals make more rational choices, and keep clients from chasing fads.

[H] Envy / Jealousy

This bias also relates to the contrast and social proof biases. Prudent financial and business planning and related decision-making are based on real needs followed by desires. People’s happiness and satisfaction is often based more on one’s position relative to perceived peers rather than an ability to meet absolute needs. The strong desire to “keep up with the Jones” can lead people to risk what they have and need for what they want. These actions can have a disastrous impact on important long-term financial goals. Clear communication and vivid examples of risks is often needed to keep people focused on important financial goals rather than spurious ones, or simply money alone, for its own sake.

[I] Fear

Financial fear is probably the most common emotion among physicians and all clients. The fear of being wrong – as well as the fear of being correct! It can be debilitating, as in the corollary expression on fear: the paralysis of analysis.

According to Paul Karasik, there are four common investor and physician fears, which can be addressed by financial advisors in the following manner:

Fear of making the wrong decision: ameliorated by being a teacher and educator.

Fear of change: ameliorated by providing an agenda, outline and/or plan.

Fear of giving up control: ameliorated by asking for permission and agreement.

Fear of losing self-esteem: ameliorated by serving the client first and communicating that sentiment in a positive manner.

Now, as human beings, our brains are booby-trapped with psychological barriers that stand between making smart financial decisions and making dumb ones. The good news is that once you realize your own mental weaknesses, it’s not impossible to overcome them.

In fact, Mandi Woodruff, a financial reporter whose work has appeared in Yahoo! Finance, Daily Finance, The Wall Street Journal, The Fiscal Times and the Financial Times among others; related the following mind-traps in a September 2013 essay for the finance vertical Business Insider; as these impediments are now entering the lay-public zeitgeist:

Anchoring happens when we place too much emphasis on the first piece of information we receive regarding a given subject. For instance, when shopping for a wedding ring a salesman might tell us to spend three months’ salary. After hearing this, we may feel like we are doing something wrong if we stray from this advice, even though the guideline provided may cause us to spend more than we can afford.

Myopia makes it hard for us to imagine what our lives might be like in the future. For example, because we are young, healthy, and in our prime earning years now, it may be hard for us to picture what life will be like when our health depletes and we know longer have the earnings necessary to support our standard of living. This short-sightedness makes it hard to save adequately when we are young, when saving does the most good.

Gambler’s fallacy occurs when we subconsciously believe we can use past events to predict the future. It is common for the hottest sector during one calendar year to attract the most investors the following year. Of course, just because an investment did well last year doesn’t mean it will continue to do well this year. In fact, it is more likely to lag the market.

Avoidance is simply procrastination. Even though you may only have the opportunity to adjust your health care plan through your employer once per year, researching alternative health plans is too much work and too boring for us to get around to it. Consequently, we stick with a plan that may not be best for us.

Loss aversion affected many investors during the stock market crash of 2008. During the crash, many people decided they couldn’t afford to lose more and sold their investments. Of course, this caused the investors to sell at market troughs and miss the quick, dramatic recovery.

Overconfident investing happens when we believe we can out-smart other investors via market timing or through quick, frequent trading. Data convincingly shows that people who trade most often under-perform the market by a significant margin over time.

Mental accounting takes place when we assign different values to money depending on where we get it from. For instance, even though we may have an aggressive saving goal for the year, it is likely easier for us to save money that we worked for than money that was given to us as a gift.

Herd mentality makes it very hard for humans to not take action when everyone around us does. For example, we may hear stories of people making significant profits buying, fixing up, and flipping homes and have the desire to get in on the action, even though we have no experience in real estate.

The modern medical practice is both similar, and unlike, other businesses today. This disparity often adds to confusion for the private practitioner. And so, the experts at iMBA Inc, list the top 25 most urgent questions in practice financial management, asked by clients to date.

Assessment

Since inception in 2000, the Institute of Medical Business Advisors Inc., has become one of North America’s leading professional health consulting and valuation firms; and focused provider of textbooks, CDs, tools, templates, onsite and distance education for the health economics, administration and financial management policy space. As competition and litigation support activities increase and the cognitive demands of the global marketplace change, iMBA Inc is well positioned with offices in five states and Europe, to meet the needs of medical colleagues, related advisory clients and corporate customers today; and into the future.

And so, your thoughts and comments on this Medical Executive-Post are appreciated. Tell us what you think. Send in your own questions. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, be sure to subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

Subscribe Now: Did you like this Medical Executive-Post, or find it helpful, interesting and informative? Want to get the latest ME-Ps delivered to your email box each morning? Just subscribe using the link below. You can unsubscribe at any time. Security is assured.

Sponsors Welcomed

And, credible sponsors and like-minded advertisers are always welcomed.

Do you ever wish you could acquire specific information for your career activities without having to complete a university Master’s Degree or finish our entire Certified Medical Planner™ professional designation program? Well, Micro-Certifications from the Institute of Medical Business Advisors, Inc., might be the answer. Read on to learn how our three Micro-Certifications offer new opportunities for professional growth in the medical practice, business management, health economics and financial planning, investing and advisory space for physicians, nurses and healthcare professionals.

Micro-Certification Basics

Stock-Brokers, Financial Advisors, Investment Advisors, Accountants, Consultants, Financial Analyists and Financial Planners need to enhance their knowledge skills to better serve the changing and challenging healthcare professional ecosystem. But, it can be difficult to learn and demonstrate mastery of these new skills to employers, clients, physicians or medical prospects. This makes professional advancement difficult. That’s where Micro-Certification and Micro-Credentialing enters the online educational space. It is the process of earning a Micro-Certification, which is like a mini-degree or mini-credential, in a very specific topical area.

Micro-Certification Requirements

Once you’ve completed all of the requirements for our Micro-Certification, you will be awarded proof that you’ve earned it. This might take the form of a paper or digital certificate, which may be a hard document or electronic image, transcript, file, or other official evidence that you’ve completed the necessary work.

Uses of Micro-Certifications

Micro-Certifications may be used to demonstrate to physicians prospective medical clients that you’ve mastered a certain knowledge set. Because of this, Micro-Certifications are useful for those financial service professionals seeking medical clients, employment or career advancement opportunities.

Examples of iMBA, Inc., Micro-Certifications

Here are the three most popular Micro-Certification course from the Institute of Medical Business Advisors, Inc:

1. Health Insurance and Managed Care: To keep up with the ever-changing field of health care physician advice, you must learn new medical practice business models in order to attract and assist physicians and nurse clients. By bringing together the most up-to-date business and medical prctice models [Medicare, Medicaid, PP-ACA, POSs, EPOs, HMOs, PPOs, IPA’s, PPMCs, Accountable Care Organizations, Concierge Medicine, Value Based Care, Physician Pay-for-Performance Initiatives, Hospitalists, Retail and Whole-Sale Medicine, Health Savings Accounts and Medical Unions, etc], this iMBA Inc., Mini-Certification offers a wealth of essential information that will help you understand the ever-changing practices in the next generation of health insurance and managed medical care.

2. Health Economics and Finance: Medical economics, finance, managerial and cost accounting is an integral component of the health care industrial complex. It is broad-based and covers many other industries: insurance, mathematics and statistics, public and population health, provider recruitment and retention, health policy, forecasting, aging and long-term care, and Venture Capital are all commingled arenas. It is essential knowledge that all financial services professionals seeking to serve in the healthcare advisory niche space should possess.

3. Health Information Technology and Security: There is a myth that all physician focused financial advisors understand Health Information Technology [HIT]. In truth, it is often economically misused or financially misunderstood. Moreover, an emerging national HIT architecture often puts the financial advisor or financial planner in a position of maximum uncertainty and minimum productivity regarding issues like: Electronic Medical Records [EMRs] or Electronic Health Records [EHRs], mobile health, tele-health or tele-medicine, Artificial Intelligence [AI], benefits managers and human resource professionals.

Other Topics include: economics, finance, investing, marketing, advertising, sales, start-ups, business plan creation, financial planning and entrepreneurship, etc.

How to Start Learning and Earning Recognition for Your Knowledge

Now that you’re familiar with Micro-Credentialing, you might consider earning a Micro-Certification with us. We offer 3 official Micro-Certificates by completing a one month online course, with a live instructor consisting of twelve asynchronous lessons/online classes [3/wk X 4/weeks = 12 classes]. The earned official completion certificate can be used to demonstrate mastery of a specific skill set and shared with current or future employers, current clients or medical niche financial advisory prospects.

Mini-Certification Tuition, Books and Related Fees

The tuition for each Mini-Certification live online course is $1,250 with the purchase of one required dictionary handbook. Other additional guides, white-papers, videos, files and e-content are all supplied without charge. Alternative courses may be developed in the future subject to demand and may change without notice.

***

Contact: For more information, or to speak with an academic representative, please contact Ann Miller RN MHA CMP™ at: MarcinkoAdvisors@msn.com [24/7].

Posted on September 26, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Physician Due Diligence is Important

[By Daniel B. Moisand; CFP®, and the ME-P Staff]

While the merits of hiring the right financial advisor [FA] may be clear, hiring the wrong one can be devastating. Medical professionals still tend to have higher incomes and are an attractive target for most financial institutions and scam artists. This fear is a poor excuse for not getting the assistance necessary. Advice about who to engage for financial assistance comes from a hodge-podge of disjointed sources. This leads to good intentions and bad results. Take caution when using the following as sources of advice.

Relying on Family and Friends

By far more people seek financial advice from trusted family members and friends than any other source. This is only natural. It is essential to trust that you are getting advice from a source that means well. It is also important that you get along well with your advisors. Hesitating to communicate with your advisor, even a great advisor, can cause problems even more problematic that getting bad advice from someone you like. While these sources have a good handle on the essential elements of trust and rapport, it is the competence of the advice that is most often the issue. The life and money experiences of those who are close to you certainly have value, but they are not necessarily relevant to your unique goals and circumstances. THINK: Bernie Madoff.

Media

A few years ago, the dominant media force in consumer oriented financial matters was the print media. Magazines and newsletters proliferated with the bull market. More recently however, television has supplanted print even in the bear market. For example, a study now estimates that 80 percent of what the average American knows about current events comes from TV. Why wait three weeks for the next issue when you can get a commentary instantly on the television? There is nothing wrong with watching shows that cover the markets or subscribing to a consumer finance magazine. It is certainly a good idea to be informed. However, be wary of the quality and applicability of information put out by the media.

The Internet

It is easy to run across an ad for prescriptions drugs on television. Images prance across the screen followed by a litany of potential side effects and the obligatory, “Ask your doctor about”. With the expansion of the information superhighway, more and more companies are going direct to the consumer in some manner or another.

Financially speaking this information can be of great benefit but should also generate more concern. It is very easy to project a particular image via the web. The webmaster controls the interaction from what you see to what you hear. One of the results of this is that the Internet has already garnered a reputation as a breeding ground for new scams. More prevalent, however, is the presentation of information meant to be useful that is simply wrong, misinterpreted, or misapplied. The most terrifying source of misinformation on the net is the chat rooms. Here the entire interaction is clouded by anonymity. Some people enter chat rooms because there is a comfort in anonymity when asking a question. There is also a danger in an anonymous answer. When it comes to something as important as your finances or your health, the prudent course should be to take all the advice with a grain of salt. A great deal of consideration to the quality of the source is in order. It is also essential that one understand the level of accountability a source may possess.

Assessment

Much has been written on financial advisor selection, here on the ME-P and elsewhere; but little on how not to select an advisor. We trust this information will be of assistance to the medical professional in some small increment. Send in your FA stories; both good and bad.

Channel Surfing the ME-P

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

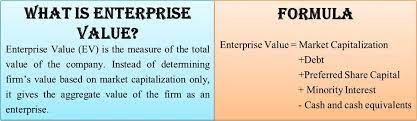

The enterprise value [EV] tends to be thought of as a theoretical takeover price if a company were to be bought. It is calculated as market capitalization plus debt, minority interest and preferred shares, minus total cash and cash equivalents.

Enterprise value = common equity at market value (this line item is also known as “market cap”) + debt at market value (here debt refers to interest-bearing liabilities, both long-term and short-term) + minority interest at market value, if any + preferred equity at market value + unfunded pension liabilities and other debt-deemed provisions – value of associate companies – cash and cash equivalents.

Echoing Elon Musk and my colleague medical Michael Burry MD has warned about American consumers’ debt woes.

Echoing the likes of Tesla’s Elon Musk and “The Big Short” investor Michael Burry, a veteran economist has warned that American households have racked up historic amounts of debt — and the economy will pay the price.

“Consumers are just waking up to the fact that they’re financing their spending by running up their credit cards, and that the interest on those credit cards is over the top, out of control, and off the hook right now,” Carl Weinbergtold CNBC. Record credit-card debt threatens to spark a consumer-spending slowdown soon, Carl Weinberg said.

“That’s going to lead to a retrenchment in consumer spending as we get into the new year” the chief economist at High Frequency Economics said. Weinberg expects the US economy to cool but not slide into recession, and he sees inflation fading.

PS: Mike Burry contributed to our 800 page textbook on investing for physicians.

Did you know that Federal and state laws require Registered Investment Advisors [RIAs] be held to a fiduciary standard? To satisfy this extremely high legal standard, an advisor must act solely in the best interest of the client, even if that interest is in conflict with the advisor’s own financial interests. Investment Advisors [IAs] must disclose any conflict, or potential conflict, to the client prior to and throughout a business engagement. Investment Advisors must fully disclose, in writing, how they are compensated. In addition, most adopt a Code of Ethics to ensure that fiduciary obligations are achieved.

Brokers or Advisors

Unfortunately, not all “financial advisors” work for federally or state-registered investment advisory firms. Many so-called financial advisors are registered representatives, better known as stock-brokers, and are employed by brokerage firms [broker-dealers]. Generally, these registered representatives [RRs] need not comply with the fiduciary duty standard that is owed when you are dealing with a registered investment advisory firm. Because broker-dealers are not necessarily acting in your best interest, the SEC [remember what a fine job former Commissioner Chris Cox did for investors in the Bernie Madoff incident?] and FINRA [NASD] require them to add the following disclosure to your client agreement.

Disclosure

Read this disclosure, and decide if this is the type of relationship you want to dictate your financial security:

“Your account is a brokerage account and not an advisory account. Our interests may not always be the same as yours. Please ask us questions to make sure you understand your rights and our obligations to you, including the extent of our obligations to disclose conflicts of interest and to act in your best interest. We are paid both by you and, sometimes, by people who compensate us based on what you buy. Therefore, our profits, and our salespersons’ compensation, may vary by product and over time.”

Disclaimers

If this disclaimer appears in agreements you are signing, or have already signed, you should ask questions of your advisor. S/he’s probably a broker. Obtain complete disclosure about how he or she is compensated, and where his or her first loyalties lie. Then decide if the relationship is in your best interest [Source: www.focusonfiduciary.com NAPFA Consumer Education Foundation]. Also, consider mediation and arbitration clauses very carefully. Do not wave your rights to litigation. Your patients do not; and neither should you!

Assessment

I am a doctor, former stock-broker, registered-rep, certified financial planner and licensed insurance agent who decided there must be a better way to help physician colleagues. As a health economist, and Founder of www.CertifiedMedicalPlanner.org I’ve believe I’ve found that way.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on September 4, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Fundamentals of Physician Investing

By Daniel B. Moisand CFP®, and ME-P staff

It used to be that the only way to get investments and investment information was through paying commissions to a traditional broker. Then in the 70’s (specifically, May, 1975) the brokerage industry went through significant deregulation allowing for the discounting of commissions. Charles Schwab and Company, among others, was able to eliminate the advice component and offer trades at dramatically reduced rates. The full service brokerage business responded by emphasizing the scope of their services namely research and advice in order to compete. The demand for both has continued to grow, even though research information is now readily available through many sources. These brokerage firms continue to thrive despite their poor performance in analyzing tech stocks and the Enron and Global Grossing debacles. More recent debacles in 2008-09, the flash crash a decade ago and more recent developments are legion, as well.

Fundamental Flaws

The fundamental flaw with these firms is the array of conflicts of interest between the firm and its customers. While the incentive to trade has been well chronicled as a conflict, these firms have not let consumer’s demand for a better-aligned compensation arrangement go unnoticed. Fee-based account relationships have proliferated accordingly. In theory, this type of arrangement, usually a percentage of assets, gives an incentive for performance and service rather than trade activity. This certainly has merit. However, conflicts remain that should be considered.

Pay to Play

The practice of paying brokers, higher levels of compensation for in-house products was commonplace. Today, explicitly higher payouts still exist but are less common. Instead, many firms use the sale of proprietary mutual funds and other products as part of management’s compensation. Other forms of non-monetary compensation such as a better office can be used as incentive for the brokers. The greater profitability of these in-house offerings will keep this conflict around for some time.

Subtle Conflicts of Interest

Less obvious is the conflict between the investment banking arm, the research department, and the retail brokerage operations of a firm. Even firms with no proprietary funds to sell may grapple with this issue. Here, research is pressured to say favorable things about a particular company’s stock by the investment bankers in hopes of obtaining more of that company’s business. When a firm brings a company public odds are great that a “strong buy” rating will come with the IPO. Of course, the lesson remains – consider the source.

Assessment

Traditional brokers have a somewhat higher standard of accountability than the on-line firms as to their accountability. If you buy the stock of a company that goes bankrupt through an on-line broker you have little recourse. After all, that was your choice. If a full-service broker recommended the stock to you, that broker will have to defend the recommendation.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Crowdfunding is a popular way to raise money online. People often use crowdfunding to fund raise for a business, for charity, or for gifts. It’s important to know that money raised through crowdfunding may be taxable.

Do you have to pay taxes on the money you receive from GoFundMe, etc?

Generally, you will not owe taxes on donated funds you receive from a crowdfunding platform. The IRS considers the money received from GoFundMe to be a gift instead of income, so it is typically not taxable. A gift is any transfer of cash or property you make to an individual without receiving full consideration in return, according to the IRS. People who donate money to GoFundMe to help pay for medical expenses are typically doing it out of generosity and do not expect anything in return.

Some money raised through crowdfunding may NOT be considered a gift.