BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on May 17, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

America’s oldest popular stock index, the Dow Jones Industrial Average, hit a brief record high yesterday morning when it traded above 40,000, reflecting renewed hope for the market’s health after Wednesday’s promising inflation report.

The S&P 500® index (SPX) fell 11.05 points (0.2%) to 5,297.10; the Dow Jones Industrial Average declined 38.62 points (0.1%) to 39,869.38; the NASDAQ Composite® ($COMP) shed 44.07 points (0.3%) to 16,698.32.

The 10-year Treasury note yield (TNX) rose more than 2 basis points to 4.381%.

The CBOE Volatility Index® (VIX) dropped 0.03 to 12.42.

Walmart’s strength fueled a strong day for consumer staples shares. The S&P 500 Consumer Staples ($SP500#30), which includes Walmart as well as companies like Coca-Cola (KO) and Procter & Gamble (PG), surged 1.5% to its highest level in over two years.

Among other companies, Applied Materials (AMAT) fell 1.6% ahead of the semiconductor industry supplier’s quarterly earnings report, which is expected after Thursday’s close.

And, Core CPI, which tracks the price of goods and services excluding volatile food and energy prices and is closely watched as an inflation indicator, rose 3.6% from the same period last year. That’s the smallest annual increase since April 2021. On a monthly basis, core CPI rose 0.3%, marking the first time in six months that its growth slowed from the prior month. Other good signs include:

Grocery prices dropped 0.2% from March, the first decrease in a year.

Health insurance and car insurance increased more slowly in April than in March.

A separate report released yesterday showed consumer spending stayed steady last month.

Finally, Joe Manchin (D-W.Va.) and a group of Republican senators are moving to overturn a retirement investment planning rule that was finalized by the Labor Department last month. The Labor Department unveiled the new rule last month that would update the definition of an investment advice fiduciary under the Employee Retirement Income Security Act. Manchin and 15 Republican senators joined in co-sponsoring a Congressional Review Act (CRA) resolution that would overturn this new rule.

Posted on May 16, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

More people are interested in determining their “heart age” using new tests and tech tools, but some skeptics say it’s not a healthy data point to focus on. (the Wall Street Journal)

The Cathie Wood-led Ark Invest just made some significant trades. The most prominent among them were the increased stakes in Palantir Technologies Inc (NYSE:PLTR) and the reduced holdings in Coinbase Global Inc (NASDAQ: COIN).

Here’s where the major benchmarks ended:

The S&P 500 index rose 61.47 points (1.2%) to 5,308.15; the Dow Jones Industrial Average added 349.89 points (0.9%) to 39,908.00; the NASDAQ Composite rallied 231.21 points (1.4%) to 16,742.39.

The 10-year Treasury note yield fell almost 10 basis points to 4.348%.

The CBOE Volatility Index® (VIX) dropped 0.97 to 12.45.

Chipmaker shares led the way higher Wednesday, lifting the Philadelphia Semiconductor Index (SOX) almost 3% to a 10-week high. Interest-rate-sensitive sectors like real estate and utilities were also strong. The small-cap Russell 2000® Index (RUT) advanced 1.1% to a seven-week high. The U.S. Dollar Index ($DXY) slumped to its weakest level in five weeks, reflecting expectations for lower interest rates that may reduce the appeal of U.S. fixed income assets.

Among companies, Cisco Systems (CSC) surged 1.5% ahead of its quarterly results expected after Wednesday’s close. Dow member Walmart (WMT) is expected to release results Thursday morning as the unofficial retail earnings season accelerates.

And … The U.S. Department of Justice (DOJ) announced it has established a new task force to take on healthcare monopolies and collusion. The task force, made up of prosecutors, economists, healthcare industry experts and others, will guide the division’s enforcement strategy and policy approach in healthcare, including by facilitating policy advocacy, investigations and, where warranted, civil and criminal enforcement in healthcare markets.

CUSTOMIZABLE CMS & AGENCY FOR HEALTHCARE RESEARCH AND QUALITY STYLED PROTOCOLS, CHECKLISTS AND TEMPLATES

.… Specifically for Podiatrists ….

e-Podiatry Consent Forms™ is an innovative new suite of software programs from the Institute of Medical Business Advisors [iMBA, Inc]. Our products solve your informed consent problems and enhance the education, discussion and documentation of the informed consent process for all podiatrists performing foot, ankle and leg reconstructive surgical procedures.

THE PROBLEM

All podiatrists are being pressured by the Centers for Medicare and Medicaid Services [CMS], the Joint Commission on Accreditation of Healthcare Organizations [JCAHO], liability carriers and private insurance payers to make their consent process more patient-friendly, informed and easily understood. And, the pressure to standardize and comply is great.

Most recently, based on the need to make healthcare even safer, the Agency for Healthcare Research and Quality (AHRQ) undertook a major study to identify patient safety issues and develop recommendations for “best practices”.

The AHRQ Evidence Report

The AHRQ report identified the challenge of addressing shortcomings such as missed, incomplete or not fully comprehended informed consent, as a significant patient safety issue and opportunity for improvement.

The authors of the AHRQ report hypothesized that better informed patients:

“are less likely to experience errors by acting as another layer of protection.”

And, the AHRQ study ranked a “more interactive informed consent process” among the top 11 practices supporting more widespread implementation; especially for surgical consent forms.

One answer to the modern risk-management problem of “informed consent interactivity” may be e-Podiatry Consent Forms™ We license two core interactive surgical products, and a reference library, with related concepts and products in development:

Forefoot, Mid-Foot and Simple Rear-Foot Version

Complex Rear-Foot, Ankle and Lower Leg Version

Comprehensive content library for extreme customization.

Each e-Podiatry Consent Forms™ CD-ROM [secure email delivery is now available] is increasingly trusted as the simple solution to standardized communications across the entire office-enterprise; from managing-risk, informing-patients and complying with modern regulatory requirements through enhanced patient-centric informed consent encounters.

Thus, by improving the consistency, details, documentation and effectiveness of the informed consent process, e-Podiatry Consent Forms™ equips all podiatric surgeons with the tools needed to augment quality standards, reduce litigation potential and improve patient outcomes and safety.

Today’s electronic media makes physician-patient communication possible; yet there is another kind of intimacy. ICTs—information and communication technologies—enable 24/7 monitoring of basic information such as blood pressure, glucose levels, pulse, and respiration, etc.

Example:

In one study, an ICT not only made it easier for patients to stay in touch with their doctors, the outcomes were also significantly better.[i] Today, Hippocrates is no longer trailing patients around the house to keep track of their snacks and moods. But Hippocrates has gone digital in the form of a wearable device that records subtle changes in biological markers and communicates them instantaneously to a health provider.

While this is obviously a great advance, we suggest you pause for a moment before plugging in.

Why?

ICTs and social media tools can make a difference to one of the most important dimensions—physiological outcomes. But you can have the latest interactive technology at your disposal and still fail to be connected.

Example:

A story that a friend told me shows how.

***

One morning, her elderly father was touching up the paint on his sailboat. Nearby, another boat-owner, who happened to be an emergency medical technician, noticed her father was struggling to breathe and that his lips had turned purple. A trip to the local community hospital led to a barrage of high-tech tests and procedures, a diagnosis of emphysema, later complications with cerebral hematomas, and hospitalizations and re-hospitalizations that brought him into contact with a neurologist, a neurosurgeon, a cardiologist, and a pulmonologist.

Throughout her father’s medical ordeal, the team of specialists stayed in touch with each other and the primary care physician via various electronic media. But one person remained out of the loop—her father. One day, six months into the experience, the primary care physician phoned our friend’s mother to check on his patient. Her father recalls thinking, “Why was he calling her?”

The physician was communicating, but he was emotionally disconnected.

***

The Moral

The moral of the story: communication needs to be patient-centered in both electronic and psychological terms. That means understanding how someone likes to communicate and making sure the medium fits the message. Electronic media are just part of the equation. The other is the doctor-patient relationship. Once a relationship is established, it may be fine to use e-mail to send information about dosage.

But, delivering a new diagnosis may require the extra effort of scheduling a phone call or a face-to-face visit. Today, since you have so many Health 2.0 choices, it takes some effort to select the right way to communicate in a particular situation.

Use the Right Relationship Strategy

A colleague recently shared another story about an encounter with a specialist.

Example:

***

After an examination for a minor ailment, he was told that there might be a medicated lotion that could ameliorate his condition. The doctor thought for a moment, then swiveled around to the computer on his desk. As our colleague watched the screen, his physician typed a few words into a search engine. Up popped a list and he wrote out a script. “Try this,” his doctor concluded. “I think it will help.”

It did, almost overnight.

***

The Moral

Even though his physical problem had disappeared completely, our colleague felt there was something missing in the interaction. “It bothered me that my doctor turned to the Web for help at that moment. He found a cure, but I felt he wasn’t paying attention to me.”

The physician is supposed to be an authority who has a special relationship to the patient. “Anybody can Google,” our colleague complained. Was he being unreasonable? Maybe.

But; this story tells us something important about technology—it cuts both ways.

***

***

Assessment

Everyone has their own preferences when it comes to how they want to interact with each other and with technology. If these preferences are explicit and aligned, the chances for a productive partnership are high. The preferences, however, are many and complex. You can easily get lost in the tangled thicket of interpersonal styles and virtual mediums.

In the Web 2.0 environment, it helps to narrow down the endless choices to just a few options.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on May 15, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The S&P 500® index (SPX) rose 25.26 points (0.5%) to 5,246.68, the highest since a record close March 28; the Dow Jones Industrial Average® ($DJI) gained 126.60 points (0.3%) to 39,558.11; the NASDAQ Composite climbed 122.94 points (0.8%) to 16,511.18.

The 10-year Treasury note yield (TNX) fell more than 3 basis points to 4.449%.

The CBOE Volatility Index® (VIX) decreased 0.18 to 13.42.

Among companies, Home Depot’s (HD) quarterly results reported earlier Tuesday kicked off the unofficial start of the retail earnings season. The home improvement retailer’s earnings topped expectations, but revenue missed forecasts, initially sending the company’s shares down sharply.

Home Depot also reaffirmed its full-year guidance for a 1% decline in comparable-store sales and a 1% increase in total sales. The company’s shares bounced back to end with a 0.1% loss.

And, the Cathie Wood-led Ark Invest just made some significant trades. The most prominent among them were the increased stakes in Palantir Technologies Inc (NYSE PLTR) and the reduced holdings in Coinbase Global Inc (NASDAQ: COIN).

Moreover, the website-building platform Squarespace is to go private, which it announced it’ll be doing in an all-cash deal with Permira, a private equity firm. Squarespace, which was public for nearly three years, joins a group of other smaller tech companies like Qualtrics that have recently pulled themselves off the public market. (CNBC)

Employers and private insurers are paying hospitals more for inpatient and outpatient services than in previous years, a study from RAND Corporation finds. The American Hospital Association dismissed the report saying it offers a “skewed and incomplete picture.”

And finally … Kaiser Permanente began its 2024 earnings season with more than $2.7 billion in net income and $935 million in operating income, just months after sharing plans to lay off workers.

Posted on May 14, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The S&P 500® index (SPX) fell 1.26 points (0.02%) to 5,221.42; the Dow Jones Industrial Average lost 81.33 points (0.2%) to 39,431.51; the NASDAQ Composite® ($COMP) gained 47.37 points (0.3%) to 16,388.24.

The 10-year Treasury note yield (TNX) dropped almost 2 basis points to 4.487%.

The CBOE Volatility Index® (VIX) surged 1.05 to 13.60.

Biotechnology and food and beverage shares were among the market’s strongest sectors Monday, while communication services stocks were among the biggest laggards. Energy shares took pressure despite a jump of 1.2% in WTI Crude Oil (/CL) futures, which ended above $79 per barrel after slumping last week to two-month lows.

Moderna is “bleeding money” as its forthcoming RSV vaccine doesn’t appear to deliver better results than other RSV shots already on the market. (Bloomberg)

***

It’s ChatGPT-4o’s time to shine. The “o” stands for omni, and it’s the latest iteration of OpenAI’s signature chatbot. According to the company, it’s much faster with enhanced “capabilities across text, vision, and audio.”

One relatively recent performance evaluation approach that was developed to help improve the relevance of comparisons is the separation of stock universes and managers by style. This classification method attempts to distinguish between stocks or manager philosophies based upon general financial characteristics of the investments.

The Managers

In very general terms, a manager is often a growth manager if the investment approach that the manager uses focuses on stocks showing growth and momentum in its earnings and price.

A value manager is generally considered to be a manager that attempts to identify under-valued securities based upon fundamental analysis of the company. A stock may be considered either “growth” or “value” based on a given set of valuation measures such as price-to-earnings, price-to-book value, and dividend yield.

The Style

The goal of style-based performance comparisons is to take some of the biases of the market environment out of the comparison, since a portfolio’s returns will ideally be evaluated versus a universe of alternatives that represent similar investment characteristics facing the same basic market environment. Thus, if the environment is one in which investors in stocks with strong past earnings and price momentum have generally performed better than those using fundamental analysis to find under-valued stocks, comparing the growth/momentum portfolio to a growth index or universe should help eliminate the bias.

Style-based universes can help the medical professional better understand the basic environment captured over a given performance time period.

However, there are significant limitations with the various approaches to constructing style-based stock and manager universes that should be understood if they are to be used in direct performance comparisons. Taking style-based stock universes separately from style-based manager universe, one of the most significant issues regarding the categorization of stocks by “growth” and “value” styles is the lack of agreement in the specification of what a growth stock is versus a value stock. With some universes divided by price-to-book value, others by price-to-earnings and/or dividend yields and some by combinations of similar variables, stocks are often classified very differently by two different stock universes. Further, stocks move across a broad spectrum as their price and fundamentals change, resulting in stocks constantly moving between growth and value categories for any given universe. If there is ambiguity in the rating of a given stock, then the difficulty is only compounded when we attempt to boil what may be complex investment processes of an investment manager or mutual fund portfolio manager to a simple classification of growth or value. A beaten down cyclical stock that no self-respecting growth/momentum manager would purchase may be classified as “growth” because it has a high price-to-earnings ratio (i.e., from low earnings) or a high price-to-book value (i.e., from asset write-offs). Value managers are not the only ones to own low valuation stocks that have improving earnings.

***

***

The second problem with style categorization is that managers are often misclassified or they purposefully “game” the categorization of their own process in order to appear more competitive. As an example, if a manager that typically looks for relatively strong earnings/price momentum is lagging in a period when “growth” managers are outperforming, the rank of the manager can be improved simply by claiming a “value” approach. Morningstar’s “style box” classification of mutual funds by size and style of the current portfolio highlight this problem for any given fund by showing how their portfolio has changed its classification annually.

Current Events

The stock market has been booming lately. Up almost 100% since March 2009, after being down almost 50%. And so, perhaps this is a good time to re-evaluate the performance of your investment portfolio[s].

Assessment

However, this leads to an interesting question for the medical professional or his/her advisor: If a manager is still using the same basic investment philosophy and disciplines, but their “style” category has changed according to the ratings service, should you fire them? If the answer is “yes”, then the burden of monitoring and the cost of manager turnover are an inevitable part of narrow style based performance comparisons.

But, if the answer is “no,” then it is easy to see the difficulty of fitting every management approach into a simple style box. The more reasonable alternative is to use style-based stock and manager universes as a tool for understanding the environment, rather than an absolute performance benchmark.

Conclusion

And so, your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

Our Other Print Books and Related Information Sources:

Subscribe Now: Did you like this Medical Executive-Post, or find it helpful, interesting and informative? Want to get the latest ME-Ps delivered to your email box each morning? Just subscribe using the link below. You can unsubscribe at any time. Security is assured.

Sponsors Welcomed: And, credible sponsors and like-minded advertisers are always welcomed.

Posted on May 13, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

While Buy Now-Pay Later (BNPL) reduces friction when purchasing, it’s giving some economy watchers unease. As Americans’ budgets buckle under the weight of inflation and higher interest payments, some worry BNPL is more of an invisible burden than a boon, Bloomberg reports. Beware the “phantom debt,” a Wells Fargo economist recently warned, referring to the BNPL industry’s short-term loans, which go largely unaccounted for by those tracking Americans’ debt load. That’s because, unlike credit cards and auto loan providers, Afterpay, Affirm, Klarna, and other BNPL providers don’t usually report transactions to credit scoring agencies.

The Cathie Wood-led Ark Invest just made some significant trades. The most prominent among them were the increased stakes in Palantir Technologies Inc (NYSE: PLTR) and her reduced holdings in Coinbase Global Inc (NASDAQ: COIN).

Dell has recently seen a decline in its revenue. In its most recent earnings report, it revealed that its net revenue shrunk by 11% year-over-year during its fiscal 2024 fourth quarter. For full year 2023, the company’s revenue was down by 14% to $88.4 billion. Partly that was due to a weak personal-computer market and the costs associated with more than 6,000 layoffs. But investors are excited by Dell’s growth potential for its server and computer businesses because of artificial intelligence, the Motley Fool reported.

Posted on May 12, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Fat Brands is the parent company of Fatburger, Johnny Rockets, and a few other restaurant chains. Last year, former CEO Andy Wiederhornstepped down after the Los Angeles Times reported that the federal government was investigating him for fraud. He has since stayed on as the company’s chairman, but on Friday the Justice Department charged him with perpetuating a $47 million fraud against his own shareholders.

In a recent Becker’s Health Care Newsletter, it is reported that a large multi-state hospital system is suing Multiplan for illegal price fixing and automatic significant price reductions, in particular, for out-of-network providers. The story states that Multiplan, by bombarding healthcare providers with automatic reductions in pricing, has made it impossible for providers to deliver healthcare.

National Nurses Week, which ends today on May 12th, Florence Nightingale’s birthday

Rite Aid has announced that 39 stores are set to close their doors for good, this follows the decision to declare Chapter 11 bankruptcy back in October, 2023.

The strategy? Reduce the total number of stores to 1,600 nationwide.

A hedge fund in the United States is generally a limited partnership providing a limited number of qualified investors with access to general partner investment decisions with little restriction in the type of investments or use of leverage. While the flexibility available to a hedge fund from a regulatory standpoint implies a high degree of potential risk, there is a wide range of investment philosophies, strategies, security types and objectives captured under the broad title of hedge fund.

Thus, generalizations regarding the characteristics of hedge funds are even less appropriate than with mutual funds, and evaluation of the investment characteristics and merits of a hedge fund strategy must be on a case-by-case basis. Likewise, the cost structure of a hedge fund often includes a base management fee to the general partner plus a performance-based fee or percentage of the profits, and must be evaluated on a case-by-case basis.

Several different investment vehicles operate under the oversight of varying regulatory bodies which provide access to an investment-managers’ discretionary decisions. While each approach generally represents ownership of an underlying pool of securities, there is usually a great deal of flexibility for the manager to deviate from a specific asset class or investment approach. Also, the fee structure of each vehicle can vary greatly and be quite large once distribution fees and sales charges are taken into account.

Thus, it is important for a medical professional to remember the following:

1. Evaluate the features and costs of an investment vehicle carefully;

2. Consider the cash flows and valuations of the securities that the manager or management approach will focus on as if the investments were being made directly, and above all;

3. Read the prospectus or agreement carefully before making any investment.

Posted on May 11, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd CMP

Understanding the Prisoner’s Dilemma

[From Wikipedia, the free encyclopedia]

As all economists and psychologists know, the prisoner’s dilemma is a standard example of a game analyzed in game theory that shows why two completely “rational” individuals might not cooperate, even if it appears that it is in their best interests to do so. It was originally framed by Merrill Flood and Melvin Dresher working at RAND in 1950. Albert W. Tucker formalized the game with prison sentence rewards and named it, “prisoner’s dilemma” (Poundstone, 1992), presenting it as follows:

Two members of a criminal gang are arrested and imprisoned. Each prisoner is in solitary confinement with no means of communicating with the other. The prosecutors lack sufficient evidence to convict the pair on the principal charge. They hope to get both sentenced to a year in prison on a lesser charge.

Simultaneously, the prosecutors offer each prisoner a bargain. Each prisoner is given the opportunity either to: betray the other by testifying that the other committed the crime, or to cooperate with the other by remaining silent.

The offer is:

If A and B each betray the other, each of them serves 2 years in prison

If A betrays B but B remains silent, A will be set free and B will serve 3 years in prison (and vice versa)

If A and B both remain silent, both of them will only serve 1 year in prison (on the lesser charge)

It is implied that the prisoners will have no opportunity to reward or punish their partner other than the prison sentences they get, and that their decision will not affect their reputation in the future. Because betraying a partner offers a greater reward than cooperating with him, all purely rational self-interested prisoners would betray the other, and so the only possible outcome for two purely rational prisoners is for them to betray each other.

***

***

The interesting part of this result is that pursuing individual reward logically leads both of the prisoners to betray, when they would get a better reward if they both kept silent.

In reality, humans display a systemic bias towards cooperative behavior in this and similar games, much more so than predicted by simple models of “rational” self-interested action. A model based on a different kind of rationality, where people forecast how the game would be played if they formed coalitions and then they maximize their forecasts, has been shown to make better predictions of the rate of cooperation in this and similar games given only the payoffs of the game.

An extended “iterated” version of the game also exists, where the classic game is played repeatedly between the same prisoners, and consequently, both prisoners continuously have an opportunity to penalize the other for previous decisions. If the number of times the game will be played is known to the players, then (by backward induction) two classically rational players will betray each other repeatedly, for the same reasons as the single shot variant. In an infinite or unknown length game there is no fixed optimum strategy, and Prisoner’s Dilemma tournaments have been held to compete and test algorithms.

In Health Economics

Advertising is sometimes cited as a real-example of the prisoner’s dilemma.

When cigarette advertising was legal in the United States, competing cigarette manufacturers had to decide how much money to spend on advertising. The effectiveness of Firm A’s advertising was partially determined by the advertising conducted by Firm B. Likewise, the profit derived from advertising for Firm B is affected by the advertising conducted by Firm A. If both Firm A and Firm B chose to advertise during a given period, then the advertising cancels out, receipts remain constant, and expenses increase due to the cost of advertising. Both firms would benefit from a reduction in advertising.

***

***

However, should Firm B choose not to advertise, Firm A could benefit greatly by advertising. Nevertheless, the optimal amount of advertising by one firm depends on how much advertising the other undertakes. As the best strategy is dependent on what the other firm chooses there is no dominant strategy, which makes it slightly different from a prisoner’s dilemma. The outcome is similar, though, in that both firms would be better off were they to advertise less than in the equilibrium. Sometimes cooperative behaviors do emerge in business situations.

For instance, cigarette manufacturers endorsed the making of laws banning cigarette advertising, understanding that this would reduce costs and increase profits across the industry. This analysis is likely to be pertinent in many other business situations involving advertising

Without enforceable agreements, members of a cartel are also involved in a (multi-player) prisoners’ dilemma. ‘Cooperating’ typically means keeping prices at a pre-agreed minimum level. ‘Defecting’ means selling under this minimum level, instantly taking business (and profits) from other cartel members. Anti-trust authorities want potential cartel members to mutually defect, ensuring the lowest possible prices for consumers.

The prisoner’s dilemma game can be used as a model for many real world situations involving cooperative behavior. In casual usage, the label “prisoner’s dilemma” may be applied to situations not strictly matching the formal criteria of the classic or iterative games: for instance, those in which two entities could gain important benefits from cooperating or suffer from the failure to do so, but find it merely difficult or expensive, not necessarily impossible, to coordinate their activities to achieve cooperation.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

COMMENTS APPRECIATED

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on May 11, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Novavax, the Covid vaccine-maker’s value doubled after it announced a $1.2 billion deal to develop new shots with Sanofi.

And, Mortgage rates fell for the first time since March, to just over 7%.

Here’s where the major stock market benchmarks ended:

The S&P 500 index rose 8.60 points (0.2%) to 5,222.68, up 1.9% for the week; the Dow Jones Industrial Average® ($DJI) advanced 125.08 points (0.3%) to 39,512.84, up 2.2% for the week and its eighth straight daily gain; the NASDAQ Composite® ($COMP) fell 5.40 points (0.03%) to 16,340.87, up 1.1% for the week.

The 10-year Treasury note yield (TNX) increased more than 5 basis points to 4.50%.

The CBOE Volatility Index® (VIX) fell 0.14 to 12.55.

Chip makers ranked among top gainers Friday after Taiwan Semiconductor Manufacturing (TSM) shares surged 4.5% after the company said its April revenue soared 60% behind AI-driven demand. The Philadelphia Semiconductor Index (SOX) climbed 1% and posted a 1.9% gain for the week. Consumer staples and transportation shares were also strong. Energy shares slipped behind a 1.2% drop in WTI Crude Oil (/CL) futures, though oil still ended slightly higher for the week.

National hospital operator Ascension said a “cyber security event” has disrupted some of its clinical operations, according to a news release. Ascension, a St. Louis-based nonprofit and Catholic healthcare network, announced it had detected “unusual activity” on some of its systems. In response, the company kicked off an investigation and remediation efforts—including turning to outside cybersecurity firm Mandiant for help, as well as notifying the “appropriate authorities,” per the release.

Planet Fitness to raise membership price for the first time since 1998. It’s going to take more than $10/month to join a gym once Planet Fitness raises the price of a basic membership for new members to $15 per month this summer. The $10 amount, which has held steady for 26 years, was considered a sweet spot where people were happy to sign up and wouldn’t bother to cancel once they gave up on their fitness goals. But after posting weaker-than-expected Q1 results, the gym chain decided it’s time to change, even though execs acknowledged that customers are looking to save rather than spend.

Posted on May 10, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The S&P 500 index gained 26.41 points (0.5%) to 5,214.08; the Dow Jones Industrial Average rose 331.37 points (0.9%) to 39,387.76; the NASDAQ Composite® ($COMP) advanced 43.51 points (0.3%) to 16,346.26.

The 10-year Treasury note yield (TNX) lost more than 2 basis points to 4.459%.

The CBOE Volatility Index® (VIX) fell 0.31 to 12.69.

Interest-rate-sensitive sectors, such as real estate and utilities, were among the strongest performers Thursday. Energy shares were also strong after WTI Crude Oil (/CL) futures rose for a second straight day after sinking to a two-month low earlier this week. Semiconductor shares were under pressure after disappointing revenue guidance from chip designer Arm Holdings (ARM) sent its shares down 2.3%.

The Dowjumped for the seventh straight day while the S&P 500 closed above 5,200 for the first time in a month as stocks climbed across the board, possibly a reaction to data showing that the cooling labor market could translate into a Federal Reserve interest rate cut in a few months. But, Roblox,tanked 22% yesterday after the company cut its annual bookings forecast. The rough patch suggests that the game’s pandemic-induced popularity has likely peaked.

Last year, Uber boasted its first full-year profit since going public. But yesterday, the company reported a surprise loss for the first quarter of 2024, dashing investors’ hopes for steady profits and sending its stock way down.

Meanwhile, Uber’s smaller rival Lyft appears to have its foot on the gas pedal. It posted better-than-expected quarterly results on Tuesday and saw a stock bump yesterday.

Microsoft plans to put the cash toward creating an AI data center. President Biden was on hand in Wisconsin to help announce the news—and not just to tout a big investment that’s expected to create jobs.

Although some doctors might view a budget as unnecessarily restrictive, sticking to a spending plan can be a useful tool in enhancing the wealth of a practice. And so, I will emphasize keys to smart budgeting and how to track spending and savings in these tough economic times; like today with the stock market busts, venture capitalists invading health care, corona virus the pandemic, aging baby boomer physicians and the great resignation; etc.

There is an aphorism that suggests, “Money cannot buy happiness.” Well, this may be true enough but there is also a corollary that states, “Having a little money can sure reduces the unhappiness.”

Unfortunately, today there is still more than a little financial unhappiness in all medical specialties. The challenges range from the commoditization of medicine, aging demographics, Medicare reimbursement cutbacks, ACA, and increased competition to floundering equity markets, the squeeze on credit and declines in the value of a practice. Few doctors seem immune to this “perfect storm” of economic woes. And then Covid-19, corona, and covid.

Far too many physicians are hurting and it is not limited to above-average earning professionals. However, one can strive to reduce the pain by following some basic budgeting principles. By adhering to these principles, physicians can eliminate the “too many days at the end of the month” syndrome and instead develop a foundation for building real wealth and security, even in difficult economic climates like we face today.

There are three major budget types. A flexible budget is an expenditure cap that adjusts for changes in the volume of expense items. A fixed budget does not. Advancing to the next level of rigor, a zero-based budget starts with essential expenses and adds items until the money is gone. Regardless of type, budgets can be extremely effective if one uses them at home or the office in order to spot money troubles before they develop.

For the purpose of wealth building, doctors may think of this budget as a quantitative expression of an action plan. It is an integral part of the overall cost-control process for the individual, his or her family unit or one’s medical practice.1

How To Prepare A Personal Cash Flow Budget

Preparing a net income statement (lifestyle cash flow budget) is often difficult because many doctors perceive it as punitive. Most doctors do not live a disciplined spending lifestyle and they view a budget as a compromise to it. However, a cash flow budget is designed to provide comfort when there is surplus income that can be diverted for other future needs. For example, if you treat retirement savings as just another periodic bill, you are more likely to save for it.

You may construct a personal cash budget by recording each cash receipt and cash disbursement on a spreadsheet. Only the date, amount and a brief description of the transaction are necessary. The cash budget is a simple tool that even doctors who lack accounting acumen can use. Since it is possible to track the cash-in and cash-out in the same format used for a standard check register, most doctors find that the process takes very little time. Such a budget will provide a helpful look at how well you are staying within available resources for a given period.

We then continue with an analysis of your operating checkbook and a review of various source documents such as one’s tax return, credit card statements, pay stubs and insurance policies. A typical statement will show all cash transactions that occur within one year. It is helpful to establish a monthly equivalent to all items of income and expense. For the purposes of getting started, note items of income and expense by the frequency you are accustomed to receiving or spending them.

What You Should Know About The ‘Action Plan’ Cash Budget

For a medial office, the first operations budget item might be salary for the doctor and staff. Operating assets and other big ticket items come next. Some doctors/clients review their office P&L statements monthly, line by line, in an effort to reduce expenses. Then they add back those discretionary business expenses they have some control over.

Now, do you still run out of money before the end of the month? If so, you had better cut back on entertainment, eating dinner out or that fancy, new but unproven piece of medical equipment. This sounds draconian until you remind yourself that your choice is either: live frugally later or live a simpler lifestyle now and invest the difference.

As a young doctor, it may be a difficult trade-off. By mid-life, however, you are staring retirement in the face. That is why the action plan depends on your actions concerning monetary scarcity, a plan that one can implement and measure using simple benchmarks or budgeting ratios. By using these statistics, perhaps on an annual basis, the podiatrist can spot problems, correct them and continue planning actively toward stated goals like building long-term wealth.2

Useful Calculations To Assess Your Budgeting Success

In the past, generic budgeting ratios would emphasize not spending more than 15 to 20 percent of your net salary on food or 8 percent on medical care. Now these estimates have given way to more rigorous numbers. Personal budget ratios, much like medical practice financial ratios, represent comparable benchmarks for parameters such as debt, income growth and net worth. Although these ratios are still broad, the following represent some useful personal budgeting ratios for physicians.

• Basic liquidity ratio = liquid assets / average monthly expenses. Cash-on-hand should approach 12 to 24 months or more in the case of a doctor employed by a financially insecure HMO or fragile medical group practice. Yes, chances are you have heard of the standard notion of setting enough cash aside to cover three months in a rainy day scenario. However, we have decried this older laymen standard for many years in our textbooks, white papers and speaking engagements as being wholly insufficient for the competitively unstable environment of modern healthcare.

• Debt to assets ratio = total debt / total assets. This percentage is high initially but should decrease with age as the doctor approaches a debt-free existence

• Debt to gross income ratio = annual debt repayments / annual gross income. This represents the adequacy of current income for existing debt repayments. Doctors should try to keep this below 20 to 25 percent.

• Debt service ratio = annual debt repayment / annual take-home pay. Physicians should aim to keep this ratio below 25 to 30 percent or face difficulty paying down debt.

• Investment assets to net worth ratio = investment assets / net worth. This budget ratio should increase over time as retirement approaches.

• Savings to income ratio = savings / annual income. This ratio should also increase over time as one retires major obligations like medical school debt, a practice loan or a home mortgage.

• Real growth ratio = (income this year – income last year) / (income last year – inflation rate). This budget ratio should grow faster than the core rate of inflation.

• Growth of net worth ratio = (net worth this year – net worth last year) / net worth last year – inflation rate). Again, this budgeting ratio should stay ahead of the specter of rising inflation.

In other words, these ratios will help answer the question: “How am I doing?”

Pearls For Sticking To A Budget

Far from the burden that most doctors consider it to be, budgeting in one form or another is probably one of the greatest tools for building wealth. However, it is also one of the greatest weaknesses among physicians who tend to live a certain lifestyle.3

In fact, I have found that less than one in 10 medical professionals have a personal budget. Fear, or a lack of knowledge, is a major cause of procrastination. Fortunately, the following guidelines assist in reversing this microeconomic disaster.

1. Set reasonable goals and estimate annual income. Do not keep large amounts of cash at home or office. Deposit it in an FDIC insured money-market account for safety. Do not deposit it in a money market mutual fund with net asset value (NAV) that may “break the buck” and fall below the one-dollar level. The new limit is $250,000. Track actual bills and expenses.

2. Do not pay bills early, do not have more taxes withheld from your salary than needed and develop spending estimates to pay fixed expenses first. Fixed expenses are usually contractual and usually include housing, utilities, food, Social Security, medical, debt repayments, homeowner’s or renter’s insurance, auto, life and disability insurance, etc. Reduce fixed expenses when possible. Ultimately, all expenses get paid and become variable in the long run.

3. Make it a priority to reduce variable expenses. Variable expenses are not contractual and may include clothing, education, recreational, travel, vacation, gas, cable TV, entertainment, gifts, furnishings, savings, investments, etc. Trim variable expenses by 5 to 20 percent.

4. Use “carve-outs or “set-asides” for big ticket items and differentiate true wants from frivolous needs.

5. Calculate both income and expenses as a percentage of your total budget. Determine if there is a better way to allocate resources. Review the budget on a monthly basis to notice any variance. Determine if the variance was avoidable, unavoidable or a result of inaccurate assumptions. Take corrective action as needed.

6. Know the difference between saving and investing. Savers tend to be risk adverse while investors understand risk and take steps to mitigate it. Watch mutual fund commissions and investment advisory fees, which cut into return-rates. Keep investments simple and diversified (stocks, bonds, cash, index, no-load mutual and exchange traded funds, etc.).4

How To Budget In The Midst Of A [Corona] Crisis

Sooner or later, despite the best of budgeting intentions, something will go awry. A doctor will be terminated or may be the victim of a reduction-in-force (RIF) because of cost containment initiatives of the corona pandemic. A medical practice partnership may dissolve or a local hospital or surgery center may close, hurting your practice and livelihood. Someone may file a malpractice lawsuit against you, a working spouse may be laid off or you may get divorced. Regardless of the cause, budgeting crisis management encompasses two different perspectives: awareness and execution.

First, if you become aware that you may lose your job, the following proactive steps will be helpful to your budget and overall financial condition.

• Decrease retirement contributions to the required minimum for company/practice match. • Place retirement contribution differences in an after-tax emergency fund. • Eliminate unnecessary payroll deductions and deposit the difference to cash. • Replace group term life insurance with personal term or universal life insurance. • Take your old group term life insurance policy with you if possible. • Establish a home equity line of credit to verify employment. • Borrow against your pension plan only as a last resort.

If you have lost your job or your salary has been depressed, negotiate your departure and get an attorney if you believe you lost your position through breach of contract or discrimination. Then execute the following steps to recalculate your budget and boost your wealth rebuilding activities.

• Prioritize fixed monthly bills in the following order: rent or mortgage; car payments; utility bills; minimum credit card payments; and restructured long-term debt.

• Consider liquidating assets to pay off debts in this order: emergency fund, checking accounts, investment accounts or assets held in your children’s names.

• Review insurance coverage and increase deductibles on homeowner’s and automobile insurance for needed cash.

• Then sell appreciated stocks or mutual funds; personal valuables such as furnishings, jewelry and real estate; and finally, assets not in pension or annuities if necessary.

• Keep or rollover any lump sum pension or savings plan distribution directly to a similar savings plan at your new employer, if possible, when you get rehired.

• Apply for unemployment insurance.

• Review your medical insurance and COBRA coverage after a “qualifying event” such as job loss, firing or even after quitting. It is a bit expensive due to a 2 percent administrative fee surcharge but this may be well worth it for those with preexisting conditions or who are otherwise difficult to insure. One may continue COBRA for up to 18 months.

• Consider a high deductible Health Savings Account (HSA), which allows tax-deferred dollars like a medical IRA, for a variety of costs not normally covered under traditional heath insurance plans. Self-employed doctors deduct both the cost of the premiums and the amount contributed to the HSA. Unused funds roll over until the age of 59½, when one can use the money as a supplemental retirement benefit.

• Eliminate unnecessary variable, charitable and/or discretionary expenses, and become very frugal.

Final Notes

The behavioral psychologist, Gene Schmuckler, PhD, MBA, sometimes asks exasperated doctors to recall the story of the old man who spent a day watching his physician son treating HMO patients in the office. The doctor had been working at his usual feverish pace all morning. Although he was working hard, he bitterly complained to his dad that he was not making as much money as he used to make. Finally, the old man interrupted him and said, “Son, why don’t you just treat the sick patients?” The doctor-son looked at his father with an annoyed expression and responded, “Dad, can’t you see, I do not have time to treat just the sick ones.”5

Always remember to add a bit of emotional sanity into your budgeting and economic endeavors.6

Regardless of one’s age or lifestyle, the insightful doctor realizes that it is never too late to take control of a lost financial destiny through prudent wealth building activities. Personal and practice budgeting is always a good way to start the journey.7

The Author:

Dr. Marcinko is a former university endowed chairman and professor, former certified financial planner and has been a medical management advisor for more than two decades. He is the CEO of www.MedicalBusinessAdvisors.com, a health economics and business finance consulting firm.

References:

1. Marcinko DE (Ed). The Business of Medical Practice (Advanced Profit Maximizing Techniques for Savvy Doctors). Springer Publishers, New York, NY, 2000 and 2004 2. Marcinko DE (Ed). Financial Planning for Physicians and Advisors, Jones and Bartlett Publishers, Sudbury, MA, 2005 3. Marcinko DE (Ed). Risk Management and Insurance Panning for Physicians and Advisors, Jones and Bartlett Publishers, Sudbury, MA, 2006. 4. Marcinko DE, Hetico HR. The Dictionary of Health Insurance and Managed Care. Springer Publishing, New York, 2007. 5. Marcinko DE, Hetico HR. The Dictionary of Health Economics and Finance. Springer Publishing, New York, 2008. 6. Marcinko DE, Hetico HR. Healthcare Organizations (Financial Management Strategies). Standard Technical Publishers, Blaine, WA, 2009. Additional Reference 7. Schmuckler E. Bridging Financial Planning and Human and Human Psychology. In, Marcinko DE (Ed): Financial Planning for Physicians and Healthcare Professionals. Aspen Publications, New York, NY, 2001, 2002 and 2003.

Posted on May 9, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

It’s the first anniversary of the Medicaid unwinding for many states, a process that kicked off when federal rules that had kept people on Medicaid and the Children’s Health Insurance Program (CHIP) through the pandemic expired. And while states could redetermine eligibility again, things have “unwound” more than some experts predicted. Children were kicked off the rolls at higher rates than adults, according to a new study the Urban Institute released May 2. Twelve states—Montana, Iowa, South Dakota, Alabama, Idaho, Georgia, Texas, Arkansas, Oklahoma, Florida, Mississippi, Colorado—exceeded 100% of their total projections for disenrolling children.

The S&P 500® index (SPX) was little changed at 5,187.67; the Dow Jones Industrial Average gained 172.13 points (0.4%) to 39,056.39; the NASDAQ Composite® ($COMP) declined 29.80 points (0.2%) to 16,302.76.

The 10-year Treasury note yield (TNX) rose more than 3 basis points to 4.496%.

The CBOE Volatility Index® (VIX) fell 0.23 to 13.00.

Retail and real estate shares were among the weakest areas Wednesday, while banks and utilities were firm. Utility shares extended a nearly month-long rally, which may in part reflect greater expectations for Fed rate cuts. Lower interest rates can make utility shares with high dividend yields relative to Treasuries more appealing. The Dow Jones Utility Average ($DJU) rose 0.5% to end at its highest level since late July and is up 12% from a mid-April low.

And, Shopify’s value plunged by nearly $20 billion after the online payments company released a gloomy forecast for this quarter. It’s the latest pandemic darling to stumble: According to the Financial Times, the firms that skyrocketed during lockdowns have lost a collective $1.5 trillion in value since the end of 2020.

Steward Health Care System, the largest U.S. physician-owned hospital operator, is expected to file for chapter 11 bankruptcy as soon as Sunday, according to a WSJ report, which cited people familiar with the matter. Steward Health Care is the largest tenant of Medical Properties Trust (NYSE: MPW). Steward Health Care hired restructuring advisers to improve its liquidity and restore its balance sheet in January 2024.

DEFINITION: Mental accounting attempts to describe the process whereby people code, categorize and evaluate economic outcomes. The concept was first named by Richard Thaler. Mental accounting deals with the budgeting and categorization of expenditures. People budget money into mental accounts for expenses or expense categories

Mental Accounting is the act of bucketizing investments and then reviewing the performance of the individual buckets separately (e.g. investing at low savings rate while paying high credit card interest rates).

***

Examples of mental accounting are: (1) matching costs to benefits (wanting to pay for vacation before taking it and getting paid for work after it was done, even though from perspective of time value of money the opposite should be preferred0, (2) aversion to debt (don’t like long-term debt for short-term benefit), (3) sunk-cost effect (illogically considering non-recoverable costs when making forward-going decisions).

In investing, treating buckets separately and ignoring interaction (correlations) induces people not to sell losers (even though they get tax benefits), prevent them from investing in the stock market because it is too risky in isolation (however much less so when looked at as part of the complete portfolio including other asset classes and labor income and occupied real estate), thus they “do not maximize the return for a given level of risk taken).

Posted on May 8, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Here’s where the major stock market benchmarks ended:

The S&P 500 index rose 6.96 points (0.1%) to 5,187.70; the Dow Jones Industrial Average gained 31.99 points (0.1%) to 38,884.26; the NASDAQ Composite® ($COMP) eased 16.70 points (0.1%) to 16,332.56.

The 10-year Treasury note yield dropped more than 3 basis points to 4.457%.

The CBOE Volatility Index® (VIX) fell 0.26 to 13.23.

Interest-rate-sensitive sectors, such as real estate and utilities, were among the market’s strongest performers Tuesday. The Philadelphia Utility Index (UTY) rose 1.3%, its fifth straight daily gain, and hit its highest level in almost a year. The recent strength may in part reflect heightened expectations for lower interest rates, which may make utility shares with relatively high dividend yields compared to Treasuries more appealing. The utilities sector is also coming off a strong April, during which it was the only S&P 500 sector with a positive return, with chart patterns suggesting a bullish long-term momentum shift.

The semiconductor sector was among the weakest sectors Tuesday, partly behind a 1.7% drop in Nvidia (NVDA). The shares fell after billionaire investor Stanley Druckenmiller told CNBC he reduced his stake in the chipmaker in late March, saying that artificial intelligence may be a “little overhyped” for the short term.

***

Peloton is reportedly being circled by private equity firms for a potential buyout of the enfeebled fitness company.

The SEC is preparing to sue over Robinhood’s crypto business. Robinhood just revealed that it’s been notified that the SEC plans to bring an enforcement action against its crypto unit for alleged securities violations. But the online brokerage said it’s not sweating: “We firmly believe that the assets listed on our platform are not securities and we look forward to engaging with the SEC to make clear just how weak any case against Robinhood Crypto would be on both the facts and the law,” Dan Gallagher, Robinhood’s chief legal, compliance, and corporate affairs officer, wrote in a blog post. Such a notice doesn’t always mean a suit will follow, but crypto companies and the agency have been sparring for years over whether crypto tokens count as securities.

The Biden administration were quick to praise a new report that extends the lifespan of the Hospital Insurance Trust Fund, but the report renewed calls for increasing physician payments.

Amwell, a telehealth company, continues to struggle in the stock market, and both its bottom- and top-line results in the first quarter missed Street analysts’ estimates.

And … between the Change Healthcare cyberattack and Medicare Advantage headwinds, major insurers faced unique challenges in the first quarter.

Stat: 8.7%. That’s the level to which US consumers can expect the 30-year mortgage rate to rise over the next year, which marks a series high, according to a New York Federal Reserve survey (MarketWatch)

The investment profession has come a long way since the door-to-door stock salesmen of the 1920s sold a willing public on worthless stock certificates. The stock market crash of 1929 and ensuing Great Depression of the 1930s forever changed the way investment operations are run. A bewildering array of laws and regulations sprung up, all geared to protecting the individual investor from fraud. These laws also set out specific guidelines on what types of investment can be marketed to the general public – and allowed for the creation of a set of investment products specifically not marketed to the general public. These early-mid 20th century lawmakers specifically exempted from the definition of “general public,” for all practical purposes, those investors that meet certain minimum net worth guidelines.

The lawmakers decided that wealth brings the sophistication required to evaluate, either independently or together with wise counsel, investment options that fall outside the mainstream. Not surprisingly, an investment industry catering to such wealthy individuals, such as doctors and healthcare professionals, and qualifying institutions has sprung up.

EARLY DAYS

The original hedge fund was an investment partnership started by A.W. Jones in 1949. A financial writer prior to starting his investment management career, Mr. Jones is widely credited as being the prototypical hedge fund manager. His style of investment in fact gave the hedge fund its name – although Mr. Jones himself called his fund a “hedged fund.” Mr. Jones attempted to “hedge,” or protect, his investment partnership against market swings by selling short overvalued securities while at the same time buying undervalued securities. Leverage was an integral part of the strategy. Other managers followed in Mr. Jones’ footsteps, and the hedge fund industry was born.

In those early days, the hedge fund industry was defined by the types of investment operations undertaken – selling short securities, making liberal use of leverage, engaging in arbitrage and otherwise attempting to limit one’s exposure to market swings. Today, the hedge fund industry is defined more by the structure of the investment fund and the type of manager compensation employed.

The changing definition is largely a sign of the times. In 1949, the United States was in a unique state. With the memory of Great Depression still massively influencing common wisdom on stocks, the post-war euphoria sparked an interest in the securities markets not seen in several decades. Perhaps it is not so surprising that at such a time a particularly reflective financial writer such as A.W. Jones would start an investment operation featuring most prominently the protection against market swings rather than participation in them.

Apart from a few significant hiccups – 1972-73, 1987 and 2006-07 being most prominent – the U.S. stock markets have been on quite a roll for quite a long time now. So today, hedge funds come in all flavors – many not hedged at all. Instead, the concept of a private investment fund structured as a partnership, with performance incentive compensation for the manager, has come to dominate the mindscape when hedge funds are discussed. Hence, we now have a term in “hedge fund” that is not always accurate in its description of the underlying activity. In fact, several recent events have contributed to an even more distorted general understanding of hedge funds.

During 1998, the high profile Long Term Capital Management crisis and the spectacular currency losses experienced by the George Soros organization both contributed to a drastic reversal of fortune in the court of public opinion for hedge funds. Most hedge fund managers, who spend much of their time attempting to limit risk in one way or another, were appalled at the manner with which the press used the highest profile cases to vilify the industry as dangerous risk-takers. At one point during late 1998, hedge funds were even blamed in the lay press for the currency collapses of several developing nations; whether this was even possible got short thrift in the press.

Needless to say, more than a few managers have decided they did not much appreciate being painted with the same “hedge fund” brush. Alternative investment fund, private investment fund, and several other terms have been promoted but inadequately adopted. As the memory of 1998 and 2007 fades, “hedge fund” may once again become a term embraced by all private investment managers.

Photo by Alexander Mils

ASSESSMENT: Physicians, and all investors, should be aware, however, that several different terms defining the same basic structure might be used. Investors should therefore become familiar with the structure of such funds, independent of the label. The Securities Exchange Commission calls such funds “privately offered investment companies” and the Internal Revenue Service calls them “securities partnerships.”

Posted on May 6, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

A cooling labor market raises hopes for a rate cut in the summer. The latest Labor Department data shows the US added 175,000 jobs in April, but much less than the 300,000 added in March and also less than economists expected. Meanwhile, the unemployment rate ticked up to 3.9% from 3.8% in March, and wages rose less than anticipated. All that bad news for us was music to the ears of investors who are holding out hope that the Federal Reserve might still cut interest rates this summer despite most recent economic data showing that inflation is sticking around.

Rate cuts appear to be back on the 2024 menu following Friday’s softer-than-expected jobs report, fueling gains for all three major stock indexes last week. With the report calming worries that inflation is ticking back up, investors now project a 50% likelihood that the Federal Reserve will reduce rates in September.

Coinbase is benefiting from the hype around new bitcoin ETFs. The crypto exchange reported a $1.2 billion quarterly profit last week, and net revenue rose by 115%.

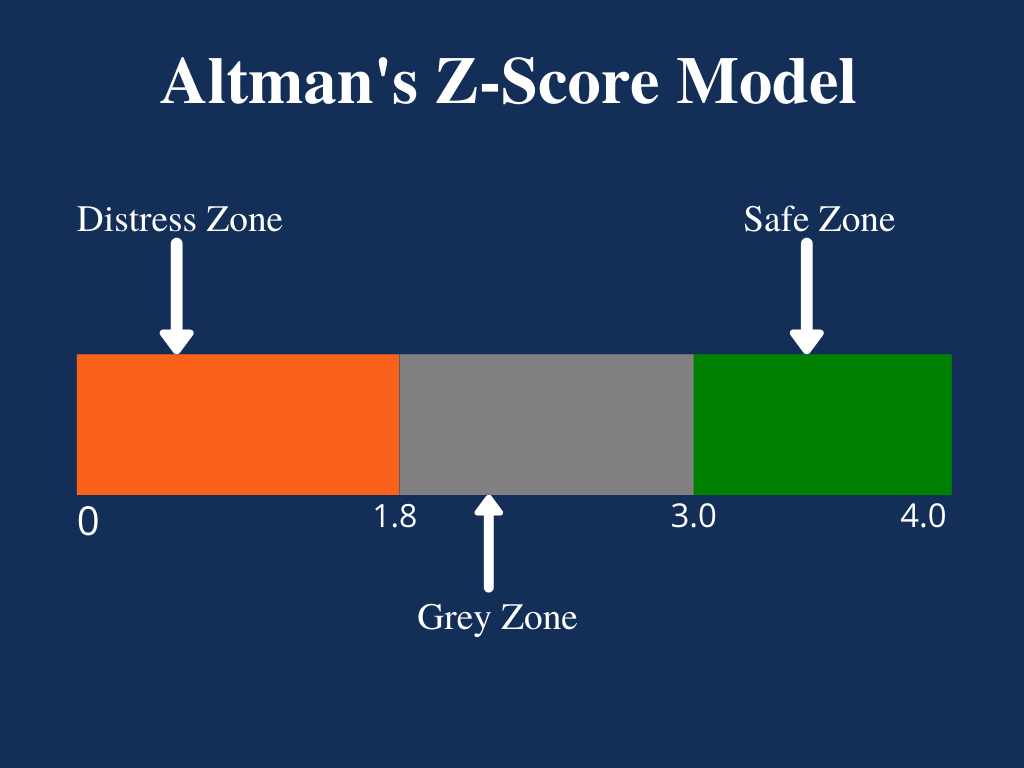

The Zeta Model is a mathematical model that estimates the chances of a public company going bankrupt within a two-year time period. The number produced by the model is referred to as the company’s Z-score (or zeta score) and is considered to be a reasonably accurate predictor of future bankruptcy.

The model was published in 1968 by New York University professor of finance Edward I. Altman. The resulting Z-score uses multiple corporate income and balance sheet values to measure the financial health of a company.

Posted on May 4, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The S&P 500 index rose 63.59 points (1.3%) to 5,127.79, up 0.6% for the week; the Dow Jones Industrial Average® ($DJI) gained 450.02 points (1.2%) to 38,675.68, up 1.1% for the week; the NASDAQ Composite surged 315.37 points (2.0%) to 16,156.33, up 1.4% for the week.

The 10-year Treasury note yield (TNX) fell about 7 basis points to 4.50%, down about 16 basis points for the week.

The CBOE Volatility Index® (VIX) fell 1.19 to 13.49.

Technology shares were among the strongest performers Friday behind a 6% rally in shares of Apple (AAPL), which late Thursday reported stronger-than-expected quarterly results and said it will repurchase $110 billion in shares. Amgen (AMGN) soared nearly 12%, leading Dow gainers after the biotechnology company beat earnings expectations.

In other markets, WTI Crude Oil futures (/CL) extended a week-long slump to end just above $78 per barrel, the lowest since mid-March. Crude futures dropped almost 7% this week, partly reflecting rising U.S. supplies and signs of slower fuel demand.

Posted on May 3, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Yesterday, sales of Wegovy more than doubled last quarter, and at least 25,000 people are starting to take it in the US per week. It also posted a $3.65 billion net profit and increased its sales outlook for 2024. But its stock Novo Nordisk still dropped yesterday.

***

iPhone sales are down but Apple share buybacks are up. Apple managed to keep investors happy, sending its stock shooting up after-hours yesterday, despite selling fewer iPhones last quarter. Sales of the signature phone dipped 10% year over year, and revenue fell 4.3% to $90.8 billion. But Apple also announced $110 billion in share buybacks, the largest in the company’s history, per CNBC. And sales in China, which has been a sore spot, came in at $16.4 billion, less than a year earlier but more than analysts had predicted.

***

Stocks rose yesterday as investors digested Jerome Powell’s recent comments and decided they only had to fear fear itself—and not interest rate hikes. Investors changed into the fast lane to buy Carvana after the used car sales site reported its best earnings ever Wednesday evening.

***

Stat: 16%. That’s the percentage by which CVS stocks plummeted Wednesday after the company reported earnings below expectations and cut its annual outlook, according to (CNBC).

But – Here’s where the major stock market benchmarks ended Thursday:

The S&P 500® index (SPX) rose 45.81 points (0.9%) to 5,064.20; the Dow Jones Industrial Average® ($DJI) added 322.37 points (0.9%) to 38,225.66; the NASDAQ Composite® ($COMP) surged 235.48 points (1.5%) to 15,840.96.

The 10-year Treasury note yield (TNX) dropped about 1 basis point to 4.583%.

The CBOE Volatility Index® (VIX) fell 0.71 to 14.68.

Transportation shares helped lead the market higher after C.H. Robinson (CHRW) reported stronger-than-expected quarterly results, sending the freight logistics and trucking company’s stock up 12%. The Dow Jones Transportation Average ($DJT) jumped 2.5%. Semiconductors were also strong after Qualcomm (QCOM) advanced 9.7% in the wake of the chip maker’s better-than-expected earnings.

Apple (AAPL) shares advanced 2.2% ahead of the company’s quarterly earnings report scheduled after Thursday’s close.

In other markets, WTI Crude Oil (/CL) futures bounced back to end with a slight gain after earlier dropping to a seven-week low under $78.50 per barrel.

Posted on May 3, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd CMP

***

***

Medicare [Dis] Advantage Plans [Medicare Part C] commenced in 2003 or so and I have railed against them since then. First, for their low physician payments. And then as a patient advocate for the last decade. And, today, for both reasons. As a doctor and independent health insurance agent myself, believe me when I speak thusly.

Now, while Medicare Advantage plans are undoubtedly not the right choice for everyone, insurance companies still say there are some folks who will get exactly what they need from the plans and at a moderate price.

Nevertheless, Ernesto Jaboneta, the IT Director of California-based Medicare insurance agency Agent Pitstop, acknowledged there are many predatory salespeople who will jump to have you join a plan that doesn’t end up helping you in the long run. Still, there are precautions you can take to make falling into this trap less likely.

“The first thing anyone can do is invite along a family member or trusted friend to any appointments with an insurance agent,” Jaboneta told Newsweek. “Don’t feel pressured to decide right away.”

Before you commit to anything, you should compare plans and find out if your doctors will remain in your network. And if you’re unsure about some of the information you received from an insurance agent, you can also call 1-800-MEDICARE for more assistance.

Jaboneta also said there’s a big difference between captive insurance agents and independent agents, as well, and seniors should take note of this.

“A captive agent is an insurance agent who works directly for an insurance carrier,” Jaboneta said. “They have no incentive to compare options outside their own company, which is different than an independent agent who can compare all the options available. In many cases, when a beneficiary calls into an insurance company to find information, they will be talked into enrolling.”

The open enrollment period lasts from October 15th to December 8th, but there’s another enrollment period from January 1st to March 31st for anyone unhappy with their Medicare Advantage plan who wants to switch or revert to Medicare.

INVESTING UPDATE: Managed-care companies are reporting that seniors on Medicare Advantage Part C plans used far more medical services than expected in the final months of 2023. The announcements have sparked two separate selloffs over the past week: The first came January 12th, when UnitedHealth Group announced its fourth-quarter earnings. The second came after Humana just laid out preliminary fourth-quarter results, and said the high utilization trends would have a material impact on its 2024 performance “if current trends continue.”

It is critical to understand and to measure the total cost of capital. Lack of understanding and appreciation of the total cost of capital is widespread, particularly among not-for-profit hospital executives. The capital structure includes long-term debt and equity; total capital is the sum of these two. Each of these components has cost associated with it. For the long-term debt portion, this cost is explicit: it is the interest rate plus associated costs of placement and servicing.

Equity portion