BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on October 4, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

OVERHEARD IN THE DOCTOR’S LOUNGE

***

***

By D. Kellus Pruitt DDS

According to money journalists Max Tailwagger and Allan Roth of MoneyWatch, the trade publication Medical Economics Magazine [“advertising supplement”] nearly listed a dog on its’ 2013 list of Best Financial Advisors for Doctors. Indeed, being listed as a top financial advisor in this publication would enhance any advisor’s credibility as well as reach a high income readership.

For example, several advisors in the Financial Planning Association, mentions this prestigious award year after year. And, the NAPFA organization of fee-only financial planners has issued press releases when member advisors make this annual list. In fact, in 2008, it touted that 52/150 listed FAs were NAPFA members.

Yet, the dog is well known in the financial advisory world, having allegedly received a plaque as one of 2009 America’s Top Financial Planners by the Consumers’ Research Council of America, and has appeared in several books including Pound Foolish and Money for Life. The fee for Maxwell Tailwagger CFP® [a five year old Dachshund] was reported to be $750 with $1,000 for a bold listing. Colorado Securities Commissioner Fred Joseph is reported to have said, “Once again, Max is gaining national notoriety for his astute, and almost superhuman, abilities in the financial arena.”

The only two qualifications for the listing were to pay the fee and not have a complaint against them. In 2009, James Putman, then the NAPFA chairman who touted his own Medical Economics award, was charged by the SEC for securities fraud. NAPFA spokesperson Laura Fisher allegedly opined that “NAPFA no longer promotes the Medical Economics Top Advisors for Doctors list. We felt promoting a list that included stock-brokers was inconsistent with NAPFA’s mission to advance the fee-only profession.” When an advisor name drops an honor to you, congratulate him and then ask how s/he achieved the award. Ask how many nominees versus award recipients there were. What were the criteria for selection and how were they nominated. Ask if they had to pay for the honor, and go online to check out the organization.

Then ask yourself this question: If your financial advisor is buying credibility, do you really want to trust your financial future to him or her?

Asset allocation is one of the key factors contributing to long-term investment success.

When designing a portfolio that represents their risk tolerance, investors should be aware that a portfolio that is 50% stocks is likely to obtain approximately half of the gain when the market advances but suffer only half the loss when the market declines.

This general principle frequently holds true over extended investing cycles, but can waiver during shorter holding periods.

Case Model

For example, a fairly typical physician client of mine who has a 50% stock, 50% bond portfolio has obtained a return of 4.62% over the last 12 months, while the S&P 500 has obtained a return of 14.31% over the same time period (as of 10/30/14).

An investor expecting to obtain half the return of the index would anticipate a return of 7.15%, and by this measuring stick, has underperformed the market by over 2.50% during the last year.

What caused this differential?

Answer

The issue resides in how we define “the market.” In this example, we use the S&P 500 index as a measure for how the market as a whole is performing. As you may know, the S&P 500 (and the Dow Jones Industrial Average, for that matter) consists solely of large company U.S. stocks.

Of course, a diversified portfolio owns a mixture of large, mid, and small cap U.S. stocks, as well as international and emerging market equities. Consequently, comparing the performance of a basket of only large cap stocks to the performance of a diversified portfolio made up of a variety of different asset classes isn’t an apples-to-apples comparison.

***

***

Frequently, the diversified portfolio will outperform the non-diversified large cap index because several of the components of the diversified portfolio will obtain higher returns than those achieved by large cap holdings.

However, the past 12 months has been a case where a diversified portfolio underperformed the large cap index because large cap stocks were the best performing asset class over the time period. In fact, over the last twelve months, there has been a direct correlation between company size and stock performance (as of 10/30/14):

Large Cap Stocks (S&P 500): 14.92%

Mid Cap Stocks (Russell Mid Cap): 11.08%

Small Cap Stocks (Russell 2000): 4.45%

International Stocks (Dow Jones Developed Markets): -1.05%

Since large cap stocks were the best performing element of a diversified portfolio over the last 12 months, in retrospect, an investor would have obtained a superior return by owning only large cap stocks during the period as opposed to owning a diversified mix of different equities. Does this mean owning only large cap stocks rather than a diversified portfolio is the best investment approach going forward? Of course not.

Year after year, we don’t know which asset category will provide the best return and a diversified portfolio ensures we have exposure to each year’s big winner. Additionally, although large caps were this year’s winner, they could easily be next year’s big loser, and a diversified portfolio ensures we don’t have all our investment eggs in one basket.

Don’t be overly concerned if your diversified portfolio is underperforming a non-diversified benchmark over a short period of time. As always, long-term results should be more heavily weighted than short-term swings, and having a diversified portfolio is likely to maximize the probability of coming out ahead over an extended period.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Classic: A pre-payment plan refers to health insurance plans that provide medical or hospital benefits in service rather than dollars, such as the plans offered by various Health Maintenance Organizations. A method providing in advance for the cost of predetermined benefits for a population group, through regular periodic payments in the form of premiums, dues, or contributions including those contributions that are made to a health and welfare fund by employers on behalf of their employees!

Modern: A Prepaid Group Practice Plan specifies health services are rendered by participating physicians to an enrolled group of persons, with a fixed periodic payment made in advance by (or on behalf of) each person or family. If a health insurance carrier is involved, a contract to pay in advance for the full range of health services to which the insured is entitled under the terms of the health insurance contract.

Examples:

Pre-Paid Hospital Service Plan: The common name for a health maintenance organization (HMO), a plan that provides comprehensive health care to its members, who pay a flat annual fee for services.

Pre-Paid Premium: An insurance or other premium payment paid prior to the due date. In insurance, payment by the insured of future premiums, through paying the present (discounted) value of the future premiums or having interest paid on the deposit.

Pre-Paid Prescription Plan: A drug reimbursement plan that is paid in advance.

ME-P readers might believe the hedge fund industry is a small, exclusive club of elites, rich investors. But a new count by Preqin shows that it’s actually a large—and growing—sector of investing.

In fact, there may be more hedge funds globally (30,000+) than Burger King locations (18,700), and more more hedge fund managers than Taco Bell managers, per the FTE

Posted on October 1, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS!

UNITED STATES GOVERNMENT SHUTS DOWN

***

By Health Capital Consultants, LLC

***

***

With hours to go until the midnight deadline on September 30th, 2025 to fund the government, lawmakers appear deadlocked over whether certain healthcare provisions should be included in the temporary funding bill.

Should this deadlock continue, the federal government will shut down beginning today October 1st and remain shut down until that deadlock is resolved.

This Health Capital Topics article provides an update on the developing saga. (Read more…)

The major indexes ticked lower last week, though, as artificial intelligence names like Oracle got hit after some analysts expressed concerns over the eye-watering costs of the AI build-out.

In the case of financial investments, compounding interest relies on time to reveal its true magic.

Here’s how: a young investor can invest less money over a longer period of time than an older investor who invests more money over a shorter period and ends up with more in the end. Compounding returns grow exponentially, making time more than an ally – but a force of the universe driving growth.

Time is certainly our ally in investing, but according to ME-P Editor Dr. David Edward Marcinko MBA MEd, you’ll kick yourself wishing you had invested earlier when you witness compounding after a few years (or a decade).

Posted on September 29, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I. and Staff Reporters

***

A meme is an idea, behavior, or style that spreads by means of imitation from person to person within a culture and often carries symbolic meaning representing a particular phenomenon or theme. A meme acts as a unit for carrying cultural ideas, symbols, or practices, that can be transmitted from one mind to another through writing, speech, gestures, rituals, or other imitable phenomena with a mimicked theme. Supporters of the concept regard memes as cultural analogues to genes in that they self-replicate, mutate, and respond to selective pressure. In popular language, a meme may refer to an internet meme, typically an image, that is remixed, copied, and circulated in a shared cultural experience online.

EXAMPLE Investing Meme:

“Sell in May and Go Away” is an investment strategy for stocks based on a theory (sometimes known as the Halloween indicator) that the period from November to April inclusive has significantly stronger stock market growth on average than the other months. In such strategies, stock holdings are sold or minimized at about the start of May and the proceeds held in cash; stocks are bought again in the autumn. So, “Sell in May” can be characterized as the memetic belief that it is better to avoid holding stock during the summer period.

The Wall Street adage — ‘Sell Rosh Hashana; buy Yom Kippur’ — focuses on the market’s performance between these two Jewish holidays. This seasonal stock-market trading pattern is upon us — and worth observing.

Rosh Hashanah is the Jewish New Year while Yom Kippur is the Day of Atonement. So, according to Mark Hulbert, it might seem arbitrary to make stock-investment decisions by blending religious observance with financial strategy, but there’s one old trading folklore commonly or meme mentioned during this time of year: “Sell Rosh Hashanah, buy Yom Kippur.”

This Wall Street adage suggests that U.S. stocks tend to fall over the 10 days the Jewish High Holidays are observed, so investors would be better off selling beforehand and buying afterward. But some market analysts believe investors should be wary of this seasonal trading pattern this year.

Historically, the “sell Rosh Hashanah, buy Yom Kippur” strategy is closely tied to the stock market’s tendency to under perform in September, with investors often looking to “minimize exposure” during this period, according to Yehuda Leibler, chief strategy and technology officer at ARX Advisory.

The Series 65 exam — the NASAA Investment Advisers Law Examination — is a North American Securities Administrators Association (NASAA) exam administered by FINRA.

The exam consists of 130 scored questions and 10 unscored questions. Candidates have 180 minutes to complete the exam. In order for a candidate to pass the Series 65 exam, they must correctly answer at least 92 of the 130 scored questions.

As human beings, our brains are booby-trapped with psychological barriers that stand between making smart financial decisions and making dumb ones. The good news is that once you realize your own mental weaknesses, it’s not impossible to overcome them.

In fact, Mandi Woodruff, a financial reporter whose work has appeared in Yahoo! Finance, Daily Finance, The Wall Street Journal, The Fiscal Times and the Financial Times among others; related the following mind-traps in a September 2013 essay for the finance vertical Business Insider; as these impediments are now entering the lay-public zeitgeist:

Anchoring happens when we place too much emphasis on the first piece of information we receive regarding a given subject. For instance, when shopping for a wedding ring a salesman might tell us to spend three months’ salary. After hearing this, we may feel like we are doing something wrong if we stray from this advice, even though the guideline provided may cause us to spend more than we can afford.

Myopia makes it hard for us to imagine what our lives might be like in the future. For example, because we are young, healthy, and in our prime earning years now, it may be hard for us to picture what life will be like when our health depletes and we know longer have the earnings necessary to support our standard of living. This short-sightedness makes it hard to save adequately when we are young, when saving does the most good.

Gambler’s fallacy occurs when we subconsciously believe we can use past events to predict the future. It is common for the hottest sector during one calendar year to attract the most investors the following year. Of course, just because an investment did well last year doesn’t mean it will continue to do well this year. In fact, it is more likely to lag the market.

Avoidance is simply procrastination. Even though you may only have the opportunity to adjust your health care plan through your employer once per year, researching alternative health plans is too much work and too boring for us to get around to it. Consequently, we stick with a plan that may not be best for us.

Loss aversion affected many investors during the stock market crash of 2008. During the crash, many people decided they couldn’t afford to lose more and sold their investments. Of course, this caused the investors to sell at market troughs and miss the quick, dramatic recovery.

Overconfident investing happens when we believe we can out-smart other investors via market timing or through quick, frequent trading. Data convincingly shows that people who trade most often under perform the market by a significant margin over time.

Mental accounting takes place when we assign different values to money depending on where we get it from. For instance, even though we may have an aggressive saving goal for the year, it is likely easier for us to save money that we worked for than money that was given to us as a gift.

Herd mentality makes it very hard for humans to not take action when everyone around us does. For example, we may hear stories of people making significant profits buying, fixing up, and flipping homes and have the desire to get in on the action, even though we have no experience in real estate.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Economy: Headline PCE rose from 2.6% on an annual basis in July to 2.7% in August, while core PCE stayed flat at 2.9%—all in line with analyst expectations.

Stocks: Solid inflation numbers helped equities arrest their recent selloff and offset the latest batch of tariffs. However, all three major indexes still ended the week lower than where they started.

Commodities: Oil climbed as Ukrainian drones continue to strike Russian energy infrastructure. Meanwhile, gold hit another all-time high, and rose above $3,800 for the first time ever at one point today.

Posted on September 26, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I. and Staff Reporters

***

***

Bonds: The 10-year Treasury yield popped on solid economic data yesterday, including weekly jobless claims falling to their lowest since mid-July and Q2 GDP rising unexpectedly.

Stocks: But good news for the labor market and economy is bad news for anyone hoping the Federal Reserve cuts interest rates next month, and the major indexes sank for a third day in a row yesterday. All eyes now turn to today’s key PCE reading.

Crypto: Digital assets continued to tumble yesterday with ether falling below $4,000 for the first time in months. There may be more pain ahead: $22 billion in crypto options expire today.

An app, which is short for “application,” is a type of software that can be installed and run on a computer, tablet, smartphone or other electronic devices. An app most frequently refers to a mobile application or a piece of software that is installed and used on a computer. Most apps have a specific and narrow function.

An easy and fairly cheap way for novices to get into investing is to use a robo-advisor. Basically, the funds you contribute will be invested by an algorithm based upon your goals, which are usually determined by taking a survey. This helps keep fees low; the algorithm doesn’t rely on a human expert to make trades, and you don’t have to spend significant amounts of time researching your investments. While this is a good way to start, it may not be the best option in the long run.

Online Brokerage or Investment Apps

More options are becoming available all the time, and they have opened trading to a much larger percentage of the population. That is a great thing, but it’s important to remember that “easier to invest” doesn’t necessarily mean it’s easy to invest well.

Be wary of apps that “gamify” trading and encourage risky choices. Keep in mind that trusted names offer more security, so do your research when you are selecting a platform.

The Series 6 exam — the Investment Company and Variable Contracts Products Representative Qualification Examination (IR) — assesses the competency of an entry-level representative to perform their job as an investment company and variable contracts products representative.

The exam measures the degree to which each candidate possesses the knowledge needed to perform the critical functions of an investment company and variable contract products representative, including sales of mutual funds and variable annuities.

Candidates must pass the Securities Industry Essentials (SIE) exam and the Series 6 exam to obtain the Investment Company and Variable Contracts Products registration.

The bargain-hunting value style is looking for shares that are under priced in relation to the company’s future potential. A physician value investor will invest in a company in the expectation that its shares will increase in value over time. Value investing is based essentially on quantitative criteria; asset values, cash flow, and discounted future earnings. The key properties of value shares are low Price/Earnings, Price/Sales ratios, and normally higher dividend yields.

On observing a company’s earnings growth, a value manager will decide whether to buy shares based on the company’s consistency or recovery prospects.

The key research questions are: 1) Does the current P/E ratio warrant an investment in a slow growth company or, 2) Is the company a higher growth candidate that has dropped in price due to a temporary problem. If this is the case, will the company’s earnings growth recover, and if so, when? The key to value investing is to find bargain shares (priced low historically or for temporary and/or irrational reasons), avoiding shares that are merely cheap (priced low because the company is failing).

The buying opportunity is identified when a company undergoing some immediate problems is perceived to have good chances of recovery in the medium to long term. If there is a loss in market confidence in the company, the share price may fall, and the value investor can step in. Once the share price has achieved a suitable value, reflecting the predicted turnaround in company performance, the shareholding is sold, realizing a capital gain.

And, a potential risk in value investing is that the company may not turn around, in which case the share price may stay static or fall.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Despite their high salaries, not all doctors are wealthy, and some live paycheck to paycheck. Here are 5 reasons why many doctors today are broke, according to https://medschoolinsiders.com

1 | Believing They Are Universally Smart

The first reason so many doctors are broke is that many doctors believe they are universally smart. While most doctors have deep specialized knowledge, there’s a big difference between being smart in your profession and being smart with money. A physician’s schooling is quite thorough when it comes to the human body, but med school doesn’t include a prerequisite class on how to handle finances.

Graduating medical school is a major feat and certainly demonstrates superior work ethic and cognitive abilities. But many new doctors believe these accomplishments transcend all aspects of life. If you’re smart enough to earn an MD, you’re certainly smart enough to handle your finances, but only once you properly and intentionally educate yourself.

The truth is doctors, especially traditional graduates, haven’t had an opportunity to manage large sums of money until they become fully trained attending physicians and start pulling in low to mid six figures in income. Prior to that, there was very little of it to manage.

Far too many aspiring doctors, and students in general, don’t take the time to learn financial basics, in part because it’s uncomfortable and seems like something they can figure out “later”, whenever that may be. Their poor spending habits and lack of investment knowledge carry over into their careers, causing many to make irresponsible decisions.

The second factor is overspending too soon, and this comes up at two points in training.

First, it’s natural to want to start spending more as soon as you get into residency and start making a little more money. After all, you’ve been a broke student for 8 or more years, and now you’re finally making a reasonable and reliable wage. But that’s where young doctors get into trouble. Residency pays, but not nearly as much as you will be making once you become an attending physician. The average resident makes about $60K a year, and if you begin spending all of that money right away, thinking you’ll handle your loans once you become an attending, you delay paying off your medical school debt, which means the compounding effect through your student loan interest rate works against you.

Now that $250,000 in student loans has ballooned to over $350,000 by the time you finish residency. The compounding effect, which can be one of your greatest allies in your financial life, becomes an equally powerful enemy when working against you through debt. But of course, pinching pennies is easier said than done, especially when you’re in residency and are surrounded by peers in different professions. They’ve been earning good money much longer than you have, and they can afford more luxurious lifestyles.

They may not be worried about indulging in fine dining or how much a hotel costs when traveling. Students in college and medical school are often confident they will resist the temptations, but the desire to keep up with your friends and family can be difficult to ignore, which causes many to overspend before they technically have the money to do so.

The same is true of attending physicians. As soon as those six-figure salaries come rolling in, many physicians go overboard with spending, trying to make up for lost time and to treat yourself.

Now, we are not suggesting you shouldn’t reward yourself for completing residency, but that reward shouldn’t be a Lamborghini. It’s best to continue living like a resident in your first few years after becoming an attending to pay off loans, put a down payment on a home, and get your financial foundation built before loosening the purse strings.

3 | Decreasing Salaries

Third, doctors continue to make less money than they did before. And this includes nearly all 44 medical specialties. For example, while physician compensation technically rose from $343k to $391k between 2017 and 2022, this rise does not keep up with inflation. The real average compensation in 2022 was less than $325k—a $20k decrease in purchasing power in only six years.

For doctors who are already spending to the limits of their salaries with huge mortgages, car payments, business costs, and other luxuries, a decreased salary can have a huge impact. You might be able to cut back by going on fewer vacations or eating out less frequently, but many accrued costs are locked in, such as a mortgage payment, car loan, or leased rental space for your practice.

4 | Increasing Costs of Private Practice

In the past, running a private practice was much simpler, but recent stricter guidelines and regulations have made it difficult for solo practices to keep up. While regulations like the Health Insurance Privacy and Portability Act, or HIPAA, and mandatory Electronic Medical Records, or EMRs, are necessary to protect patients, they make costs higher for physicians who run their own private practice. These physicians need to spend their own money to set up and maintain EMRs as well as invest in security to ensure patient data is protected.

With the steep rise of inflation we’ve seen over the past couple of years, everything is more expensive, which means costs, such as business space, equipment, and even office supplies, have gone up for private practice physicians while salaries have not. 2013 to 2020 saw an annual inflation rate of anywhere from 0.7% to 2.3%. This skyrocketed to an annual inflation rate of 7.0% in 2021 and another 6.5% in 2022. In fact, the cost of running a private practice has increased by almost 40% between 2001 and 2021.

These increased costs are exacerbated by another problem plaguing private practices; decreased reimbursement. While costs increased by almost 40%, Medicare reimbursement only increased by 11%. When doctors see patients who are insured, the insurance companies pay the physicians for their time. For Medicare, the new proposed rules for 2023 would cut reimbursement by around 5%. When adjusting for inflation, Medicare reimbursement decreased by 20% in the last 20 years.

These costs add up, making it extremely difficult for physicians to thrive financially while running a private practice.

5 | Tuition Debt

Lastly, we can’t talk about a doctor’s finances without mentioning the exorbitant debt so many graduating physicians are left with. It won’t shock you to hear that med school is expensive. Extremely expensive. The average cost of tuition for a single year is nearly $60k, with significant variance from school to school, and that’s before accounting for living expenses.

In-state applicants pay less than out-of-state applicants, and students at private schools typically pay more than students at public medical schools. The astronomical costs mean the vast majority of students can’t pay for medical school out of their own pockets. And unless your family is part of the 1%, even with your parents footing the bill, it’s difficult to cover tuition, let alone rent, groceries, transportation, tech, social activities, exam fees, and application costs.

The average total student debt after college and med school is over $250k. But keep in mind that’s the average, which includes 27% of students who graduate with no debt at all. This means the vast majority of students leave medical school owing much more than $250k.

For some perspective, in 1978, the average debt for graduating MDs was $13,500, which, when adjusted for inflation, is a little over $60,000. There are multiple ways to eventually repay these loans, but time and discipline are essential to ensure this money is paid off as quickly as possible.

According to financial advisor Dr. David Edward Marcinko MEd MBA CMP™; consider the following:

Place a portion of your salary (15-20% or more) into a savings account, and another portion (10-20% or more) into wise investments [stocks, bonds, mutual funds, and/or ETFs].

Pay off your bills each month, and then use leftover spending money to purchase fun things like vacations and fancy dinners, within your means. Shop sales, buy used clothes, and use credit card points for travel.

Hire an excellent tax professional and meet with an investment advisor once or twice a year about your investment status and strategy. http://www.MarcinkoAssociates.com

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on September 22, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Authentication:

The verification of the identity of an individual, system, machine, or any other unique entity

Authorization:

The process of allowing access to specific areas of a system based on the role and needs of the user

Committee Charter:

A document that defines the purposes and responsibilities of the oversight committee

Compliance Risk Profile:

The current and prospective risk to earnings or capital arising from violations of or nonconformance with laws, rules, regulations, prescribed practices, internal policies and procedures, or ethical standards

Control Assessment:

A high-level review and analysis of controls relating to a process; should encompass both current and missing controls

Controls:

Methods that preserve the integrity of important information, meet operational or financial targets, and/or communicate management policies (See also: Key Control, Secondary Control, Tertiary Control)

ERM Policy Statement:

Defines an organization’s approach to and method of enterprise risk management

Governance:

Processes and structures implemented to communicate, manage, and monitor organizational activities

Impact:

The influence and effect of a risk

Inherent Risk:

Risk that is inherent to a process, taking into consideration the likelihood and impact of a risk

Key Control:

A primary control that is essential for a business process; typically takes place during the process it applies to

Key Indicators:

Measurements that are important for organizations to monitor for potential issues; examples include key performance indicators (KPIs) and key risk indicators (KRIs)

Key Performance Indicator (KPI):

A measurement with a defined set of goals and tolerances that gauges the performance of an important business activity

Key Risk Indicator (KRI):

A proactive measurement for future and emerging risks that indicates the possibility of an event that adversely affects business activities

Likelihood:

The probability of a risk occurring

Mitigation Actions:

The necessary steps, or action items, to reduce the likelihood and/or impact of a potential risk

Operation Risk Profile:

1) The risk arising from the execution of an organization’s business processes; 2) The risk of loss resulting from failed or inadequate internal processes, systems, people, or other entities

Price Risk Profile:

The risk to earning or capital arising from adverse changes in portfolio values

Process:

1) The principle elements of essential business functions within work groups or business units; 2) A set of tasks completed by business continuity plan owners within a department

Reputation Risk Profile:

The current and prospective risk to earnings or capital arising from negative public opinion or perception

Residual Risk:

Risk remaining after considering the existing control environment

Risk:

A potential event or action that would have an adverse effect on the organization

Risk Appetite:

A statement that broadly considers the risk levels that management deems acceptable

Risk Assessment:

The prioritization of potential business disruptions based on the impact and likelihood of occurrence; includes an analysis of threats based on the impact to the organization, its customers, and financial markets

Risk Tolerance:

A metric that sets the acceptable level of variation around organizational objectives and provides assurance that the organization remains within its risk appetite

Secondary Control:

An important control that typically takes place after the process it applies to (i.e., reporting or ongoing monitoring)

Strategic Risk Profile:

The current and prospective risk to earnings or capital raising from adverse business decisions, improperly implemented decisions, or lack of responsiveness to industry changes

Tertiary Control:

A non-essential control that can still be applied effectively to a business process

Velocity:

The time it takes a risk event to manifest itself

Vulnerability:

An entity’s susceptibility to a risk event as determined by the entity’s preparedness, agility, and adaptability

Investment bankers are not really bankers at all. The fact that the word banker appears in the name is partially responsible for the false impressions that exist in the medical community regarding the functions they perform.

For example, they are not permitted to accept deposit, provide checking accounts, or perform other activities normally construed to be commercial banking activities. An investment bank is simply a firm that specializes in helping other corporations obtain money they need under the most advantageous terms possible. When it comes to the actual process of having securities issued, the corporation approaches an investment banking firm, either directly, or through a competitive selection process and asks it to act as adviser and distributor.

Investment bankers, or under writers, as they are sometimes called, are middlemen in the capital markets for corporate securities. The corporation requiring the funds discusses the amount, type of security to be issued, price and other features of the security, as well as the cost to issuing the securities. All of these factors are negotiated in a process known as negotiated underwriting. If mutually acceptable terms are reached, the investment banking firm will be the middle man through which the securities are sold to the general public. Since such firms have many customers, they are able to sell new securities, without the costly search that individual corporations may require to sell its own security.

Thus, although the firm in need of additional capital must pay for the service, it is usually able to raise the additional capital at less expense through the use of an investment banker, than by selling the securities itself. The agreement between the investment banker and the corporation may be one of two types. The investment bank may agree to purchase, or underwrite, the entire issue of securities and to re-offer them to the general public. This is known as a firm commitment.

When an investment banker agrees to underwrite such a sale; it agrees to supply the corporation with a specified amount of money. The firm buys the securities with the intention to resell them. If it fails to sell the securities, the investment banker must still pay the agreed upon sum.

Thus, the risk of selling rests with the underwriter and not with the company issuing the securities.

The alternative agreement is a best efforts agreement in which the investment banker makes his best effort to sell the securities acting on behalf of the issuer, but does not guarantee a specified amount of money will be raised. When a corporation raises new capital through a public offering of stock, one might inquire where the stock comes from. The only source the corporation has is authorized, but previously un-issued stock. Anytime authorized, but previously un-issued stock (new stock) is issued to the public, it is known as a primary offering.

If it’s the very first time the corporation is making the offering, it’s also known as the Initial Public Offering (IPO). Anytime there is a primary offering of stock, the issuing corporation is raising additional equity capital.

A secondary offering, or distribution, on the other hand, is defined as an offering of a large block of outstanding stock. Most frequently, a secondary offering is the sale of a large block of stock owned by one or more stockholders. It is stock that has previously been issued and is now being re-sold by investors. Another case would be when a corporation re-sells its treasury stock.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The Series 7 exam — the General Securities Representative Qualification Examination (GS) — assesses the competency of an entry-level registered representative to perform their job as a general securities representative.

The exam measures the degree to which each candidate possesses the knowledge needed to perform the critical functions of a general securities representative, including sales of corporate securities, municipal securities, investment company securities, variable annuities, direct participation programs, options and government securities.

Stocks: The Russell 2000 went 967 days without hitting a new record high until Thursday. But, it looks like it will have to keep waiting for the next one—the small-cap-focused index fell, even as the DJIA, NASDAQ and S&P 500 rose to new closing highs on Friday.* Bonds: 2-year yields and 10-year yields both hit two-week intra-day highs even after the FOMC cut interest rates, indicating that traders still aren’t sure how the economy will perform in the months ahead. Commodities: Arabica futures fell on reports that lawmakers will introduce a bipartisan bill to exempt coffee from tariffs.

Posted on September 17, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS!

By Staff Reporters

***

***

Federal Reserve Chairman Jerome Powell just announced that the central bank [FOMC] would cut interest rates amid President Donald Trump’s attempts to reshape the Fed’s independence.

The chairman announced that the Federal Reserve would cut the interest rate by .25 points, the first time that it cut interest rates since December.

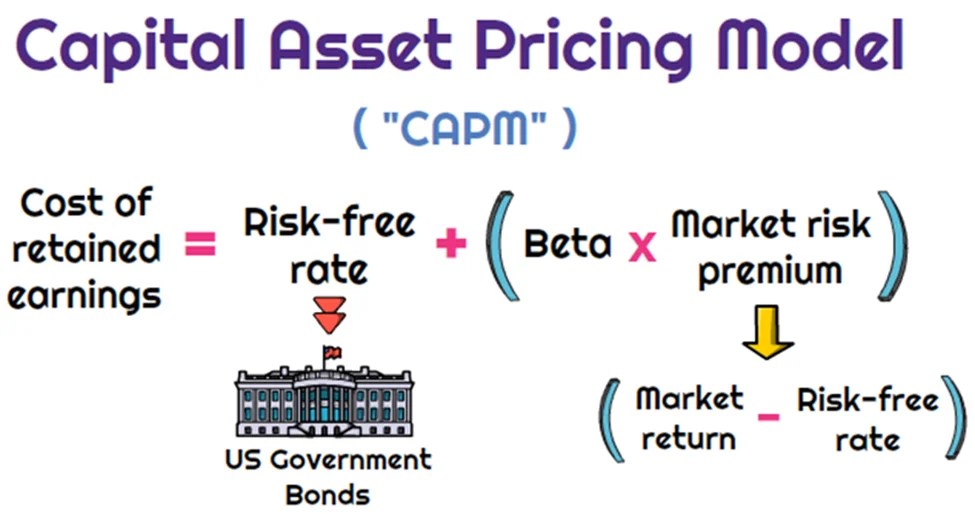

Dr. Harry Markowitz is credited with developing the framework for constructing investment portfolios based on the risk-return tradeoff. William Sharpe, John Lintner, and Jan Mossin are credited with developing the Capital Asset Pricing Model (CAPM).

CAPM is an economic model based upon the idea that there is a single portfolio representing all investments (i.e., the market portfolio) at the point of the optimal portfolio on the Capital Market Line (CML) and a single source of systematic risk, beta, to that market portfolio. The resulting conclusion is that there should be a “fair” return investors should expect to receive given the level of risk (beta) they are willing to assume.

The excess return, or return above the risk-free rate, that may be expected from an asset is equal to the risk-free return plus the excess return of the market portfolio times the sensitivity of the asset’s excess return to the market portfolio excess return. Beta, then, is a measure of the sensitivity of an asset’s returns to the market as a whole. A particular security’s beta depends on the volatility of the individual security’s returns relative to the volatility of the market’s returns, as well as the correlation between the security’s returns and the markets returns.

While a stock may have significantly greater volatility than the market, if that stock’s returns are not highly correlated with the returns of the overall market (i.e., the stock’s returns are independent of the overall market’s returns), then the stock’s beta would be relatively low. A beta in excess of 1.0 implies that the security is more exposed to systematic risk than the overall market portfolio, and likewise, a beta of less 1.0 means that the security has less exposure to systematic risk than the overall market.

MPT has helped focus investors on two extremely critical elements of investing that are central to successful investment strategies.

First, MPT offers the first framework for investors to build a diversified portfolio. Furthermore, an important conclusion that can be drawn from MPT is that diversification does in fact help reduce portfolio risk.

Thus, MPT approaches are generally consistent with the first investment rule of thumb, “understand and diversify risk to the extent possible.”

Additionally, the risk/return tradeoff (i.e., higher returns are generally consistent with higher risk) central to MPT based strategies has helped investors recognize that if it looks too good to be true, it probably is.

Passive Investing

Passive investing is a monetary plan in which an investor invests in accordance with a pre-determined strategy that doesn’t necessitate any forecasting of the economy or an individual company’s prospects. The primary premise is to minimize investing fees and to avoid the unpleasant consequences of failing to correctly predict the future. The most accepted method to invest passively is to mimic the performance of a particular index. Investors typically do this today by purchasing one or more ‘index funds’. By tracking an index, an investor will achieve solid diversification with low expenses.

An ivestor could potentially earn a higher rate of return than an investor paying higher management fees. Passive management is most widespread in the stock markets. But with the explosion of exchange traded funds on the major exchanges, index investing has become more popular in other categories of investing. There are now literally hundreds of different index funds.

Passive management is based upon the Efficient Market Hypothesis theory. The Efficient Market Hypothesis (EMH) states that securities are fairly priced based on information regarding their underlying cash flows and that investors should not anticipate to consistently out-perform the market over the long-term.

The Efficient Market Hypothesis evolved in the 1960s from the Ph.D. dissertation of Eugene Fama. Fama persuasively made the case that in an active market that includes many well-informed and intelligent investors, securities will be appropriately priced and reflect all available information. If a market is efficient, no information or analysis can be expected to result in out-performance of an appropriate benchmark. There are three distinct forms of EMH that vary by the type of information that is reflected in a security’s price:

Weak Form

This form holds that investors will not be able to use historical data to earn superior returns on a consistent basis. In other words, the financial markets price securities in a manner that fully reflects all information contained in past prices.

Semi-Strong Form

This form asserts that security prices fully reflect all publicly available information. Therefore, investors cannot consistently earn above normal returns based solely on publicly available information, such as earnings, dividend, and sales data.

Strong Form

This form states that the financial markets price securities such that, all information (public and non-public) is fully reflected in the securities price; investors should not expect to earn superior returns on a consistent basis, no matter what insight or research they may bring to the table.

While a rich literature has been established regarding whether EMH actually applies in any of its three forms in real world markets, probably the most difficult evidence to overcome for backers of EMH is the existence of a vibrant money management and mutual fund industry charging value-added fees for their services.

The notion of passive management is counterintuitive to many investors. Passive investing proponents follow the strong market theory of EMH. These proponents argue several points including;

In the long term, the average investor will have a typical before-costs performance equal to the market average. Therefore the standard investor will gain more from reducing investment costs than from attempting to beat the market over time.

The efficient-market hypothesis argues that equilibrium market prices fully reflect all existing market information. Even in the case where some of the market information is not currently reflected in the price level, EMH indicates that an individual investor still cannot make use of that information. It is widely interpreted by many academics that to try and systematically “beat the market” through active management is a fools game.

Not everyone believes in the efficient market. Numerous researchers over the previous decades have found stock market anomalies that indicate a contradiction with the hypothesis. The search for anomalies is effectively the hunt for market patterns that can be utilized to outperform passive strategies. Such stock market anomalies that have been proven to go against the findings of the EMH theory include;

Low Price to Book Effect

January Effect

The Size Effect

Insider Transaction Effect

The Value Line Effect

All the above anomalies have been proven over time to outperform the market. For example, the first anomaly listed above is the Low Price to Book Effect. The first and most discussed study on the performance of low price to book value stocks was by Dr. Eugene Fama and Dr. Kenneth R. French. The study covered the time period from 1963-1990 and included nearly all the stocks on the NYSE, AMEX and NASDAQ. The stocks were divided into ten subgroups by book/market and were re-ranked annually. In the study, Fama and French found that the lowest book/market stocks outperformed the highest book/market stocks by a substantial margin (21.4 percent vs. 8 percent). Remarkably, as they examined each upward decile, performance for that decile was below that of the higher book value decile. Fama and French also ordered the deciles by beta (measure of systematic risk) and found that the stocks with the lowest book value also had the lowest risk.

Today, most researchers now deem that “value” represents a hazard feature that investors are compensated for over time. The theory being that value stocks trading at very low price book ratios are inherently risky, thus investors are simply compensated with higher returns in exchange for taking the risk of investing in these value stocks. The Fama and French research has been confirmed through several additional studies. In a Forbes Magazine 5/6/96 column titled “Ben Graham was right–again,” author David Dreman published his data from the largest 1500 stocks on Compustat for the 25 years ending 1994. He found that the lowest 20 percent of price/book stocks appreciably outperformed the market.

One item a medical professional should be aware of is the strong paradox of the efficient market theory. If each investor believes the stock market were efficient, then all investors would give up analyzing and forecasting. All investors would then accept passive management and invest in index funds. But if this were to happen, the market would no longer be efficient because no one would be scrutinizing the markets. In actuality, the efficient market hypothesis actually depends on active investors attempting to outperform the market through diligent research.

The case for passive investing and in favor of the EMH is that a preponderance of active managers do actually underperform the markets over time. The latest study by Standard and Poor’s (S&P) confirms this fact. S&P recently compared the performance of actively-managed mutual funds to passive market indexes twice per year. The 2012 S&P study indicated that indexes were once again outperforming actively-managed funds in nearly every asset class, style and fund category. The lone exception in the 2012 report was international equity, where active outperformed the index that S&P chose. The study examined one-year, three-year and five-year time periods. Within the U.S. equity space, active equity managers in all the categories failed to outperform the corresponding benchmarks in the past five year period. More than 65 percent of the large-cap active managers lagged behind the S&P 500 stock index. More than 81 percent of mid-cap mutual funds were outperformed by the S&P MidCap 400 index.

Lastly, 77 percent of the small-cap mutual funds were outperformed by the S&P SmallCap 600 index. U.S. bond active managers fared no better that equity managers over a five year period. More than 83 percent of general municipal mutual funds under-performed the S&P National AMT-Free Municipal Bond index, 93 percent of government long-term funds under-performed the Barclays Long Government index, nearly 95 percent of high yield corporate bond funds under-performed the Barclays High Yield index. Although the performance measurements for index investing are very strong, many analysts find three negative elements of passive investing;

Downside Protection: When the stock market collapses like in 2008, an index investor will assume the same loss as the market. In the case of 2008, the S&P 500 stock index fell by more than 50 percent, offering index investors no downside protection.

Portfolio Control: An index investor has no control over the holdings in the fund. In the event that a certain sector becomes over-owned (i.e. technology stocks in 2000), an index investor maintains the same weight as the index.

Average Returns: An index investor will never have the opportunity to outperform the market, but will always follow. Although the markets are very efficient, an investor can perhaps take advantage of market anomalies and invest with those managers who have maintained a long-term performance edge over the respective index.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on September 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I. and Staff Reporters

***

***

Stocks: The NASDAQ rose to its fifth record high of the week, while the S&P 500 and the Dow sank late in the day as investors turned their attention to the FOMC meeting next week.

Bonds: While equities climbed all week long, the bond market has been sending signals that weak economic data really isn’t great news.

Commodities: Oil rallied after President Trump expressed his growing frustration with Vladimir Putin and threatened further energy and financial sanctions. Meanwhile, the US may ask its G7 counterparts to apply 100% tariffs against China and India for purchasing Russian crude.

Posted on September 12, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I. and Staff Reporters

***

***

BIAS

Bias is a prejudice in favor of or against one thing, person, or group compared with another, usually in a way considered to be unfair.

MYOPIA

Myopia (nearsightedness) is a common condition that’s usually diagnosed before age 20. It affects your distance vision — you can see objects that are near, but you have trouble viewing objects that are farther away like grocery store aisle markers or road signs. Myopia treatments include glasses, contact lenses or surgery.

MYOPIA BIAS

Myopia Bias makes it hard for us to imagine what our lives might be like in the future.

FinancialExample: When we are young, healthy and in our prime economic earning years it may be hard for us to picture what life will be like when our health depletes and we no longer have the earnings necessary to support our standard of living.

Irony: This short-sightedness makes it hard to save adequately when we are young … when saving does the most good.

Here are some of the most common risks associated with fixed income securities.

Interest Rate Risk

The market value of the securities will be inversely affected by movements in interest rates. When rates rise, market prices of existing debt securities fall as these securities become less attractive to investors when compared to higher coupon new issues. As prices decline, bonds become cheaper so the overall return, when taking into account the discount, can compete with newly issued bonds at higher yields. When interest rates fall, market prices on existing fixed income securities tend to rise because these bonds become more attractive when compared to the newly issued bonds priced at lower rates.

Price Risk

Investors who need access to their principal prior to maturity have to rely on the secondary market to sell their securities. The price received may be more or less than the original purchase price and may depend, in general, on the level of interest rates, time to term, credit quality of the issuer and liquidity.

Among other reasons, prices may also be affected by current market conditions, or by the size of the trade (prices may be different for 10 bonds versus 1,000 bonds), etc. It is important to note that selling a security prior to maturity may affect actual yield received, which may be different than the yield at which the bond was originally purchased. This is because the initially quoted yield assumed holding the bond to term. As mentioned above, there is an inverse relationship between interest rates and bond prices. Therefore, when interest rates decline, bond prices increase, and when interest rates increase, bond prices decline.

Generally, longer maturity bonds will be more sensitive to interest rate changes. Dollar for dollar, a long-term bond should go up or down in value more than a short-term bond for the same change in yield. Price risk can be determined through a statistic called duration, which is featured at the end of the fixed income section.

Liquidity risk is the risk that an investor will be unable to sell securities due to a lack of demand from potential buyers, sell them at a substantial loss and/or incur substantial transaction costs in the sale process. Broker/dealers, although not obligated to do so, may provide secondary markets.

Reinvestment Risk

Downward trends in interest rates also create reinvestment risk, or the risk that the income and/or principal repayments will have to be invested at lower rates. Reinvestment risk is an important consideration for investors in callable securities. Some bonds may be issued with a call feature that allows the issuer to call, or repay, bonds prior to maturity. This generally happens if the market rates fall low enough for the issuer to save money by repaying existing higher coupon bonds and issuing new ones at lower rates. Investors will stop receiving the coupon payments if the bonds are called. Generally, callable fixed income securities will not appreciate in value as much as comparable non-callable securities.

Similar to call risk, prepayment risk is the risk that the issuer may repay bonds prior to maturity. This type of risk is generally associated with mortgage-backed securities. Homeowners tend to prepay their mortgages at times that are advantageous to their needs, which may be in conflict with the holders of the mortgage-backed securities. If the bonds are repaid early, investors face the risk of reinvesting at lower rates.

Purchasing Power Risk

Fixed income investors often focus on the real rate of return, or the actual return minus the rate of inflation. Rising inflation has a negative impact on real rates of return because inflation reduces the purchasing power of the investment income and principal.

When owners of a security spread false information to pump up the price of the security and subsequently sell off their shares, making a profit—the “dump.”

Refer to attempts by investors to move the price of a stock opportunistically by selling large numbers of shares short. The investors pocket the difference between the initial price and the new, lower price after this maneuver. This technique is illegal under SEC rules, which stipulate that every short sale must be on an uptick. For more information on this complex tactic, read on in this piece from the Wharton School of Business.

Wash Trading

Involves the simultaneous or near-simultaneous sale and repurchase of the same security for the purpose of generating activity and increasing the price.

When fraudsters manipulate the market through matched orders, they enter trades to buy or sell securities with the knowledge that a matching order on the opposite side has been or will be entered. During his tenure at the Commission, our partner Jordan Thomas was involved in a case where the SEC won summary judgement and obtained settlements with an astonishing 16 defendants who engaged in matched trades, among other illicit tactics.

Painting the Tape

Painting the tape refers to placing successive orders in small amounts at increasing or decreasing prices.

Spoofing & Layering

High frequency traders are known to use the tactics of Spoofing & Layering to manipulate share prices. Spoofing is the placing of a bid or offer with the intent to cancel before execution. Layering is a form of spoofing in which the trader places multiple orders on one side of the book, in order to create a false impression of heavy buying or selling.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on September 10, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITIONS

By Staff Reporters

***

***

Rate Review & the 80/20 Rule

The health care law provides 2 ways to hold insurance companies accountable and help keep your costs down: Rate Review and the 80/20 rule.

Rate Review

Rate Review helps protect you from unreasonable rate increases. Insurance companies must now publicly explain any rate increase of 15% or more before raising your premium. This does not apply to grandfathered plans.

The 80/20 Rule generally requires insurance companies to spend at least 80% of the money they take in from premiums on health care costs and quality improvement activities. The other 20% can go to administrative, overhead, and marketing costs.

The 80/20 rule is sometimes known as Medical Loss Ratio, or MLR. If an insurance company uses 80 cents out of every premium dollar to pay for your medical claims and activities that improve the quality of care, the company has a Medical Loss Ratio of 80%.

Insurance companies selling to large groups (usually more than 50 employees) must spend at least 85% of premiums on care and quality improvement.

If your insurance company doesn’t meet these requirements, you’ll get a rebate on part of the premium that you paid.

Will I get a rebate check from my insurance company?

If your insurance company doesn’t meet its 80/20 targets for the year, you’ll get back some of the premium that you paid.

You may see the rebate in a number of ways:

A rebate check in the mail

A lump-sum deposit into the same account that was used to pay the premium, if you paid by credit card or debit card

A direct reduction in your future premium

Your employer may also use one of the above rebate methods, or apply the rebate in a way that benefits employees

If you or your employer will get a rebate, your insurance company must notify you by August 1.

If you have an individual insurance policy, you’ll get the rebate directly from your insurance company.

For small group and large group plans, the rebate is usually paid to the employer. It may use one of the above rebate methods, or apply the rebate in a way that benefits employees.

FYI: The 80/20 rebate rules don’t apply when an insurance company has fewer than 1000 enrollees in a particular state or market.

For Rate Review: These requirements don’t apply to grandfathered plans. Check your plan’s materials or ask your employer or your benefits administrator to find out if your health plan is grandfathered.

For the 80/20 Rule: These rights apply to all individual, small group, and large group health plans, whether your plan is grandfathered or not.

According to Medical Economics, there were 10 clinic and physician practices filing bankruptcy in 2024, making it the highest level of the last six years, according to a new analysis of cases with liabilities of at least $10 million.

Meanwhile, the Steward Health Care System bankruptcy, which was based in Massachusetts but making headlines across the nation, has become “the largest hospital sector bankruptcy by far in the last 30 years,” according to a new analysis by Gibbins Advisors, based in Nashville, Tennessee.

Health care bankruptcy filings totaled 57 last year, down from 79 in 2023, said “Healthcare Restructuring: Trends and Outlook.” The report analyzed Chapter 11 health care bankruptcy cases with liabilities of at least $10 million, since 2019.

Last year’s total was down 28% from 2023’s peak, but greater than the 2019 to 2022 average of 42 filings a year, the report said.

Bankruptcy, often considered a last financial resort, is a legal process that can help alleviate outstanding debts for individuals and businesses. Reasons to file for bankruptcy can include divorce, job loss, exorbitant medical bills or credit card debt.

There are several types of bankruptcy — six, as a matter of fact. The two most common types of bankruptcy for individuals are Chapter 7 and Chapter 13.

But there are four other types as well: Chapter 9, Chapter 11, Chapter 12 and Chapter 15. And, the type of bankruptcy filed depends on the situation.

Regardless of which type, the process is typically the same: You’ll usually retain an attorney and make your case before a judge, who will then erase some debts or set up a repayment plan.

Also note that an eligibility requirement — for all bankruptcy chapters — is that you must undergo credit counseling within the 180 days before filing.

Posted on September 7, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

A recent study of hospital physician acquisition and employment found that such acquisitions decrease competition and raise prices. A National Bureau of Economic Research (NBER) working paper, released in July 2025, “empirically analyze[d] the effects of mergers between complementary firms on competition and pricing,” and found hospital prices increased by an average of 3.3%, while physician prices increased by an average of 15.1%.

This Health Capital Topics article reviews the study’s findings and implications for the healthcare industry. (Read more…)

Posted on September 6, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters and A.I.

***

***

Markets: Stocks started off Friday on a high note after a weak jobs report raised hopes that the Fed will cut interest rates this month. But the rally faded as the afternoon wore on, while 10-year bond yields tumbled to their lowest level since April.

Trade: President Trump said “fairly substantial” tariffs for semi-conductors are coming “very shortly,” but hinted that companies like Apple will be spared. He also clapped back at EU regulators for fines against Google.

Offbeat commodities: Raw sugar prices hit a two-month low as Brazilian producers churn out more of the sweet stuff, cocoa prices are expected to pop after Cargill paused production in Ivory Coast, and corn hit its highest price since July thanks to strong export demand.

Posted on September 5, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

U.S. Department for Health & Human Services & Centers for Medicare & Medicaid Services

By Health Capital Consultants, LLC

***

***

On August 21, 2025, the U.S. Department for Health & Human Services (HHS) and the Centers for Medicare & Medicaid Services (CMS) announced the formation of a new Healthcare Advisory Committee.

The Committee is expected to be comprised of a group of experts who will make strategic recommendations to HHS Secretary Robert F. Kennedy Jr. and CMS Administrator Dr. Mehmet Oz.

This Health Capital Topics article discusses this announcement and potential implications on the healthcare industry. (Read more…)

Ikea Effect Bias describes the tendency of people to place a higher value on products they have partially created or assembled themselves. This phenomenon is named after the Swedish furniture retailer Ikea, known for selling furniture in flat-pack kits that customers must assemble at home.

he IKEA effect was identified and named by Michael Norton of Harvard Business School, Daniel Mochon of Yale University and colleague Dan Ariely PhD of Duke University, who published the results of three studies in 2011. They described the IKEA effect as “labor alone can be sufficient to induce greater liking for the fruits of one’s labor: even constructing a standardized bureau, an arduous, solitary task, can lead people to overvalue their (often poorly constructed) creations.”

Example: A prospect is more likely to pursue his/her own financial plan than that one from an informed financial planner, CPA or professional advisor.

2011 study found that subjects were willing to pay 63% more for furniture they had assembled themselves than for equivalent pre-assembled items.

IN FINANCE AND INVESTING

The IKEA effect can contribute to reducing panic selling. Investors typically reduce their stock market exposure after a financial crash which often results in “buy high, sell low” strategy that is detrimental to long-run wealth accumulation.

Ashtiani et al.’s study proposes a nudge utilizing the IKEA effect to counteract this phenomenon: “actively involving investors in the selection process of the risky investments, while restricting their selections in a way that preserves a large degree of diversification.”

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on September 4, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

A.I. by Artificial Intelligence

***

***

Artificial intelligence (AI) refers to computer systems capable of performing complex tasks that historically only humans could do, such as reasoning, making decisions, or solving problems. Today, the term “AI” describes a wide range of technologies that power many of the services and goods we use every day – from apps that recommend TV shows to chatbots that provide customer support in real time. And yet, there is a hierarchy among related concepts such as machine learning and deep learning.

So, to summarize the hierarchy:

AI is the goal: machines that can think and act intelligently.

Machine learning is a method within AI that lets machines learn from data.

Deep learning is a specialized form of machine learning that uses multi-layered neural networks to analyze data in a way that mimics the human brain.

It’s a feature, not a bug

And, there’s no shortage of companies leveraging AI today to remain profitable, to the delight of Salesforce investors: among others:

Wells Fargo’s CEO has touted trimming its workforce for 20 straight quarters. Its stock is up 228% over the past five years.

Bank of America CEO Brian Moynihan wasn’t hiding it during a recent earnings call when he said the company has let go of 88,000 employees over the past 15 years. BofA stock is up 95% since 2020.

Amazon, with its share value up 28% over the past year, recently told staff that AI implementation would lead to layoffs.

Microsoft has cut 15,000 jobs in the past two months as the company pivots to AI—and its stock is also up since the beginning of July.

Posted on September 4, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I. and Staff Reporters

***

***

Stocks: Markets slowed along yesterday with the S&P 500 and NASDAQ buoyed after a pivotal antitrust ruling for Alphabet pushed big tech stocks higher across the board.

Bonds: The 30-year Treasury pushed 5% yesterday as traders fret about the Fed’s independence and the odds of interest rate cuts.

Commodities: Oil sank on reports that OPEC+ is contemplating increasing its crude output next month, while gold reached yet another new record high as uncertainty swirling around the future of tariffs continued to rise. JPMorgan analysts now think the precious metal could climb as high as $4,250 by the end of next year.

If an insurer uses 80 cents out of every premium dollar to pay its customers’ medical claims and activities that improve the quality of care, the company has a medical loss ratio of 80%. A medical loss ratio of 80% indicates that the insurer is using the remaining 20 cents of each premium dollar to pay overhead expenses, such as marketing, profits, salaries, administrative costs, and agent commissions.

The Affordable Care Act sets minimum medical loss ratios for different markets, as do some state laws.

Posted on September 3, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

Medicare Inpatient Prospective Payment System

***

***

By Health Capital Consultants, LLC

On July 31, 2025, the Centers for Medicare & Medicaid Services (CMS) released its finalized payment and policy updates for the Medicare Inpatient Prospective Payment System (IPPS) and the Long-Term Care Hospital (LTCH) Prospective Payment System (PPS) for fiscal year (FY) 2026.

The final rule authorized Medicare inpatient reimbursement increases for 2026 and moved forward with improvements to quality measurement, and provided more information on a new value-based payment model.

This Health Capital Topics article will discuss the IPPS final rule and stakeholder reactions. (Read more…)

Posted on September 3, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Bonds: Treasury yields rose yesterday as investors dug into a Federal appeals court ruling last Friday stating that most of President Trump’s tariffs are illegal. The 30-year yield closed in on the key 5% level. Stocks: Equities tumbled across the board as technology stocks sold off and pulled the rest of the market down with them. Commodities: Gold hit a new record high as traders hedged against tariff uncertainty and braced themselves for an extremely important US jobs report on Friday that could make or break the case for the Fed to start cutting rates.

Posted on September 2, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Markets: After a day off for Labor Day, Wall Street is entering September with little confidence as stocks shrugle with tariffs and AI-slowdown jitters to rise for four straight months. September has historically been the weakest month for US stocks, plus a hugely consequential Federal Reserve meeting looms on September17th.

Stock spotlight: An already booming Celsius hit a 52-week high last week after Pepsi said it would up its stake in the energy drink maker.

Posted on August 31, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Rick Kahler; MSFP CFP™

***

***

This month, the U.S. government demanded a direct cut of a company’s foreign sales as the price for letting those sales happen.

Tech companies Nvidia and AMD had been stuck in regulatory limbo over selling their newest AI chips to China. According to an August 12, 2025, Reuters article by Karen Freifeld, Nvidia CEO Jensen Huang had even received a public “green light” for the company’s H20 chip, but the Commerce Department would not issue the export licenses.

The stalemate ended only after Huang met with President Trump and agreed to a deal: the licenses would be granted, but the U.S. Treasury would get 15% of all H20 revenue from China. AMD agreed to identical terms for its MI308 chip. Two days later, both companies had their licenses.

The numbers are staggering. Bernstein Research estimates Nvidia could sell $15 billion worth of H20 chips in China this year, and AMD about $800 million of MI308s. That is more than $2 billion flowing straight to Washington, not as taxes but as a contractual price for market access. The legality of this arrangement is questionable, and the deal also raises security concerns.

It is worth noting the administration first asked for 20% before “settling” on 15%. This was not a polite request but a “take it or leave it” demand. From a behavioral economics standpoint, the decision was predictable. The pain of losing an entire market is far greater than the pain of losing a fraction of it.

How is this any different from a tariff? A tariff is a standardized, legally defined tax that applies broadly to certain goods and is collected under public trade policy. This 15% cut is a one-off, privately negotiated condition aimed at just two companies, tied to export license approval. It is taken from gross revenue, not profit, meaning the government gets paid on every dollar of sales before the companies cover a single expense.