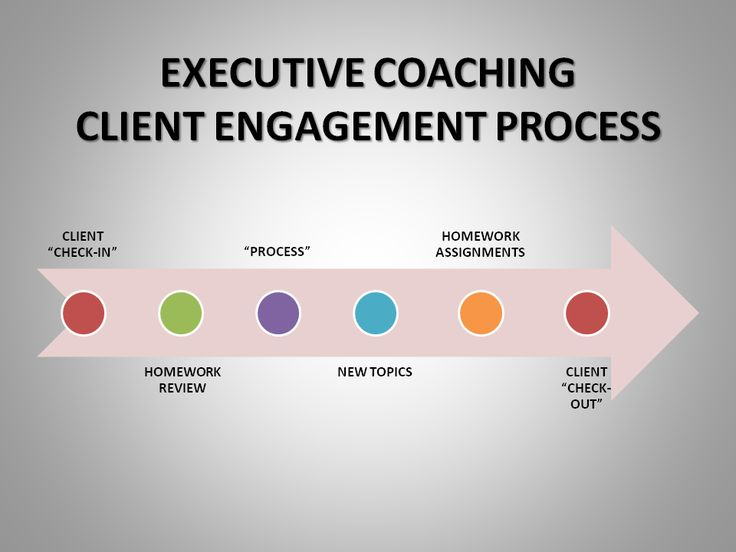

BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

New stock market indices are frequently created to track emerging sectors, regional markets, or particular investment strategies. However, some of the recent and notable stock market indices introduced in recent years focus on new trends or themes such as technology, sustainability, and ESG (Environmental, Social, and Governance) factors. Here are a few noteworthy examples:

1. S&P 500 ESG Index (2021)

One of the newer and increasingly popular indices is the S&P 500 ESG Index, launched in 2021. This index tracks the performance of the companies within the S&P 500 that meet certain environmental, social, and governance (ESG) criteria. The S&P 500 ESG Index aims to provide a more sustainable and socially responsible alternative to the traditional S&P 500 index. It excludes companies involved in industries like tobacco, firearms, or fossil fuels, reflecting the growing interest in socially responsible investing.

2. Nasdaq-100 ESG Index (2021)

Another significant ESG-focused index is the Nasdaq-100 ESG Index, also introduced in 2021. This index tracks the Nasdaq-100, which is typically made up of the 100 largest non-financial companies listed on the Nasdaq stock exchange, but it filters those companies to include only those with strong ESG scores. Given the rapid growth of ESG investing, indices like this one are becoming increasingly important for socially-conscious investors.

3. Global X Metaverse ETF Index (2022)

The Global X Metaverse ETF Index, introduced in 2022, is another example of a new market index targeting a specific, emerging sector. This index focuses on companies involved in the development of the metaverse, which encompasses technologies like virtual reality (VR), augmented reality (AR), and other digital experiences. As the concept of the metaverse gains popularity, this index is designed to provide investors with exposure to companies working within this new virtual space.

4. FTSE All-World High Dividend Yield ESG Index (2022)

This is an example of a more niche index, combining high-dividend yield investing with ESG factors. Introduced by FTSE Russell in 2022, this index is designed for investors looking for companies with high dividend yields while also considering sustainability and ethical investment criteria. It is part of a broader trend where investors seek to combine solid financial returns with socially responsible practices.

5. Bitcoin and Digital Assets Indices

As cryptocurrency continues to grow in prominence, more indices focused on digital assets and cryptocurrency have emerged. For instance, the S&P Bitcoin Index and the Nasdaq Crypto Index were created to provide benchmarks for the growing market of cryptocurrencies and blockchain technology companies. These indices help investors track the performance of digital currencies and crypto-related stocks or funds.

Why Are New Indices Created?

New stock market indices are created for several reasons:

Emerging Market Trends: As new sectors like the metaverse, AI, and ESG investing become more relevant, indices are developed to capture the performance of these new areas.

Investor Demand: As investors look for more targeted strategies, whether for ethical investing or to gain exposure to emerging technologies, indices are created to meet those demands.

Financial Innovation: As financial products like ETFs (Exchange-Traded Funds) gain popularity, they require benchmarks or indices to track performance.

Conclusion

While the S&P 500 ESG Index and Nasdaq-100 ESG Index are among the newest mainstream indices focusing on socially responsible investing, there are also many other niche indices targeting rapidly growing sectors like the metaverse, cryptocurrencies, and digital assets. These indices reflect the evolving nature of global markets and the increasing interest in themes such as sustainability and technological innovation. With such rapid change in the financial landscape, it’s likely that even more specialized indices will continue to emerge in the coming years.

Did you know that desperate doctors of all ages are turning to knowledgeable financial advisors and medical management consultants for help? Symbiotically too, generalist advisors are finding that the mutual need for knowledge and extreme niche synergy is obvious.

***

***

But, there was no established curriculum or educational program; no corpus of knowledge or codifying terms-of-art; no academic gravitas or fiduciary accountability; and certainly no identifying professional designation that demonstrated integrated subject matter expertise for the increasingly unique healthcare focused financial advisory niche … Until Now!

So, if you are looking to supplement your knowledge, income and designations; and find other qualified professionals you may want to consider the CMP® program.

Enter the Certified Medical Planner™ charter professional designation. And, CMPs™ are FIDUCIARIES, 24/7.

Channel Surfing the ME-P

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

***

***

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on January 26, 2026 by Dr. David Edward Marcinko MBA MEd CMP™

***

***

By Dr. David Edward Marcinko MBA MEd

***

Milton Friedman: Champion of Free Markets

Milton Friedman was a towering figure in the field of economics, renowned for his unwavering advocacy of free-market capitalism and limited government intervention. Born in 1912 in New York City and raised in Rahway, New Jersey, Friedman rose from modest beginnings to become a Nobel laureate and a leading voice of the Chicago School of Economics.

Friedman’s academic journey began at Rutgers University, where he earned a degree in mathematics and economics. He later pursued graduate studies at the University of Chicago and Columbia University, where he was mentored by prominent economists like Simon Kuznets. His intellectual foundation laid the groundwork for a career that would challenge prevailing economic thought and reshape public policy.

One of Friedman’s most significant contributions was his development of monetarism, a theory emphasizing the role of governments in controlling the money supply to manage inflation and economic stability. In contrast to Keynesian economics, which advocated for active fiscal policy and government spending, Friedman argued that excessive government intervention often led to inefficiencies and inflation. His research demonstrated that inflation is “always and everywhere a monetary phenomenon,” a principle that became central to modern macroeconomic policy.

Friedman’s influence extended beyond academia. His 1962 book, Capitalism and Freedom, articulated a powerful case for economic liberty as a foundation for political freedom. He argued that voluntary exchange and competitive markets were essential for individual choice and prosperity. The book also introduced the Friedman Doctrine, which posited that the primary responsibility of business is to increase its profits, a view that sparked ongoing debates about corporate social responsibility.

In 1976, Friedman was awarded the Nobel Memorial Prize in Economic Sciences for his work on consumption analysis, monetary history, and stabilization policy. His Permanent Income Hypothesis, which suggests that people base their consumption on expected long-term income rather than current income, revolutionized understanding of consumer behavior.

Friedman’s ideas had profound policy implications. He was a vocal critic of the draft and successfully advocated for an all-volunteer military. He also proposed the concept of school vouchers, allowing parents to choose schools for their children, which laid the foundation for modern school choice movements. His work influenced leaders like Ronald Reagan and Margaret Thatcher, who embraced free-market reforms during their administrations.

Despite his acclaim, Friedman’s views were not without controversy. Critics argued that his emphasis on deregulation and privatization sometimes overlooked social equity and environmental concerns. Nonetheless, his legacy remains deeply embedded in economic thought and public discourse.

Milton Friedman passed away in 2006, but his ideas continue to shape debates on economic policy, freedom, and the role of government. His belief in the power of markets and individual choice remains a cornerstone of classical liberalism and a guiding light for economists and policymakers around the world.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The economics of information explores how knowledge—or the lack of it—affects decision-making, market behavior, and resource allocation. It reveals why perfect competition rarely exists and why information itself can be a powerful economic asset.

Economics of Information: Understanding the Value and Impact of Knowledge

In traditional economic models, markets are often assumed to operate under perfect information—where all participants have equal access to relevant data. However, in reality, information is often incomplete, asymmetric, or costly to obtain. The field known as economics of information emerged to address these discrepancies, fundamentally reshaping how economists understand markets, incentives, and efficiency.

One of the core concepts in this field is information asymmetry, where one party in a transaction possesses more or better information than the other. This imbalance can lead to adverse selection and moral hazard. For example, in the insurance market, individuals who know they are high-risk are more likely to seek coverage, while insurers may struggle to differentiate between high- and low-risk clients. Similarly, in lending, borrowers may have private knowledge about their ability to repay, which lenders cannot easily verify.

To mitigate these problems, economists have developed mechanisms such as signaling and screening. Signaling occurs when the informed party takes action to reveal their type—like a job applicant earning a degree to signal competence. Screening, on the other hand, involves the uninformed party designing tests or contracts to elicit information—such as offering different insurance packages to separate risk levels.

Another important area is the cost of acquiring information. Gathering data, analyzing trends, or verifying facts requires time and resources. This leads to decisions being made under uncertainty, where individuals rely on heuristics or limited data. The economics of information examines how these costs influence behavior, pricing, and market structure. For instance, consumers may not compare every available product due to search costs, allowing firms to maintain price dispersion.

The rise of digital technology has intensified the relevance of this field. In the age of big data, companies like Google and Amazon thrive by collecting and analyzing vast amounts of user information. This data allows them to personalize services, predict behavior, and gain competitive advantages. However, it also raises concerns about privacy, market power, and inequality—issues that economists of information are increasingly addressing.

Moreover, information goods—such as software, media, and research—have unique economic properties. They are often non-rivalrous and can be reproduced at near-zero marginal cost. This challenges traditional pricing models and calls for innovative approaches like freemium strategies, bundling, and subscription services.

In public policy, the economics of information plays a crucial role in designing regulations, transparency standards, and consumer protections. Governments must balance the need for open access to information with incentives for innovation and investment. For example, patent laws aim to encourage research by granting temporary monopolies, while disclosure requirements in finance promote market integrity.

In conclusion, the economics of information reveals that knowledge is not just a passive input but a dynamic force shaping economic outcomes. By understanding how information is produced, distributed, and used, economists can better explain real-world phenomena and design systems that promote fairness, efficiency, and innovation.

The contrasting economic philosophies of John Maynard Keynes and Friedrich Hayek have shaped not only macroeconomic policy but also approaches to investing. While both thinkers sought to understand and improve economic systems, their views diverge sharply on the role of government, market behavior, and investor decision-making.

Keynesian economics emphasizes the importance of aggregate demand in driving economic growth. Keynes argued that markets are not always self-correcting and that government intervention is necessary during downturns to stimulate demand. In the context of investing, Keynesian theory supports counter-cyclical strategies. Investors following this approach might increase exposure to equities during recessions, anticipating that fiscal stimulus will boost corporate earnings and market performance. Keynes himself was a successful investor, known for his contrarian style and long-term focus. He advocated for active portfolio management, believing that markets are driven by psychological factors and herd behavior, which create mispricings that savvy investors can exploit.

In contrast, Hayekian economics is rooted in classical liberalism and the belief in spontaneous order. Hayek argued that markets are efficient information processors and that decentralized decision-making leads to better outcomes than centralized planning. From an investment standpoint, Hayekian theory favors passive strategies and minimal interference. Investors aligned with Hayek’s philosophy might prefer index funds or diversified portfolios that reflect market signals rather than attempting to time the market or predict government actions. Hayek was skeptical of the ability of any individual or institution to possess enough knowledge to outsmart the market consistently.

The Keynesian approach tends to be more optimistic about the power of policy to influence markets. For example, during economic crises, Keynesians may expect stimulus packages to revive demand and thus invest in sectors likely to benefit from increased government spending. Hayekians, on the other hand, may view such interventions as distortions that lead to malinvestment and eventual corrections. They might invest more cautiously during periods of heavy government involvement, anticipating inflation, asset bubbles, or regulatory overreach.

Risk perception also differs between the two schools. Keynesians may see risk as cyclical and manageable through diversification and active management. Hayekians view risk as inherent and unpredictable, best mitigated through adherence to market fundamentals and long-term discipline.

In practice, modern investors often blend elements of both approaches. For instance, they may use Keynesian insights to anticipate short-term market movements while relying on Hayekian principles for long-term portfolio construction. The rise of behavioral finance has also added nuance, validating Keynes’s view of irrational market behavior while reinforcing Hayek’s skepticism of centralized forecasting.

Ultimately, the choice between Keynesian and Hayekian investing reflects deeper beliefs about how economies function and how much control investors—or governments—really have. Keynesians embrace adaptability and intervention, while Hayekians champion restraint and trust in the market’s invisible hand. Both offer valuable lessons, and understanding their differences can help investors navigate complex financial landscapes with greater clarity.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Posted on December 20, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

A brokerage company serves as a vital intermediary in the financial markets, bridging the gap between investors and the securities they wish to buy or sell. At its core, the brokerage firm provides access to markets that would otherwise be difficult for individuals to navigate on their own. Whether dealing in stocks, bonds, commodities, or more complex financial instruments, the brokerage company simplifies transactions, ensures compliance with regulations, and offers guidance to clients seeking to grow their wealth.

The traditional brokerage model was built on personal relationships. Investors relied on brokers to provide advice, execute trades, and manage portfolios. These brokers often had deep knowledge of specific industries and cultivated trust with their clients over years of service. In this model, the brokerage company earned commissions on trades and fees for advisory services. The emphasis was on expertise and personalized attention, with brokers acting as both financial advisors and gatekeepers to the markets.

Over time, however, the industry underwent significant transformation. The rise of technology and the internet democratized access to financial markets. Online brokerage platforms emerged, offering investors the ability to trade directly from their computers or smartphones. This shift reduced the reliance on traditional brokers and lowered transaction costs. Brokerage companies adapted by creating user-friendly platforms, offering educational resources, and expanding their services to include research tools, real-time data, and automated trading options. The modern brokerage company thus became not only a facilitator of trades but also a provider of technology-driven solutions.

Despite these changes, the essence of a brokerage company remains the same: enabling investors to participate in financial markets. The firm must balance accessibility with responsibility. It ensures that trades are executed efficiently and in compliance with regulations, protecting both the investor and the integrity of the market. Brokerage companies also play a role in investor education, helping clients understand risks, diversify portfolios, and make informed decisions. In this way, they contribute to the overall stability and growth of the financial system.

Another important aspect of brokerage companies is their adaptability. As new asset classes emerge, such as cryptocurrencies or environmental credits, brokerage firms expand their offerings to meet demand. This flexibility allows them to remain relevant in a constantly evolving financial landscape. At the same time, they must manage risks associated with innovation, ensuring that clients are protected from volatility and fraud. The ability to innovate while maintaining trust is a hallmark of successful brokerage companies.

The competitive nature of the industry has also shaped brokerage strategies. With numerous firms vying for clients, differentiation becomes essential. Some companies focus on low-cost trading, appealing to price-sensitive investors. Others emphasize premium advisory services, targeting clients who value personalized guidance. Still others invest heavily in technology, offering advanced platforms with sophisticated analytics and automation. This diversity of approaches reflects the varied needs of investors and highlights the brokerage company’s role as a versatile service provider.

Looking ahead, brokerage companies face both opportunities and challenges. The continued integration of artificial intelligence and machine learning promises to enhance trading strategies, risk management, and customer service. At the same time, regulatory scrutiny is likely to increase, particularly as new financial products gain popularity. Brokerage firms must navigate these dynamics carefully, balancing innovation with compliance. Their success will depend on their ability to remain trusted intermediaries while embracing the tools of the future.

In conclusion, a brokerage company is more than just a facilitator of trades. It is an institution that embodies trust, expertise, and adaptability. From traditional broker-client relationships to modern digital platforms, the brokerage firm has evolved to meet the changing needs of investors. Its role in connecting individuals to financial markets, educating clients, and safeguarding transactions ensures its continued relevance. As the financial world grows more complex, the brokerage company will remain a cornerstone of investment activity, guiding investors through both opportunities and uncertainties.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Insurance agents are primarily paid through commissions, but may also earn salaries, bonuses, and fees depending on their employment model and the types of policies they sell.

Insurance agents play a vital role in helping individuals and businesses navigate the complex world of insurance. Their compensation structures vary widely, influenced by factors such as the type of insurance they sell, whether they work independently or for a company, and the specific agreements they have with insurers. Understanding how insurance agents are paid is essential for consumers who want to make informed decisions and for aspiring agents considering a career in the industry.

The most common form of compensation for insurance agents is commission-based pay. Agents earn a percentage of the premium paid by the customer when they successfully sell a policy. These commissions can vary depending on the type of insurance. For example, first-year commissions for auto and homeowners insurance typically range from 5% to 20%, while commercial property and casualty policies may offer 10% to 15%. Life insurance policies often provide higher initial commissions, sometimes exceeding 50% of the first-year premium, followed by smaller renewal commissions in subsequent years.

There are two main types of insurance agents: captive agents and independent agents. Captive agents work exclusively for one insurance company and usually receive a combination of salary and commissions. Their compensation may also include performance bonuses and incentives tied to sales targets. Independent agents, on the other hand, represent multiple insurers and rely more heavily on commissions. They have the flexibility to offer a wider range of products, but their income is directly tied to their ability to sell policies and maintain client relationships.

***

***

In addition to commissions, some agents earn fees for services such as policy reviews, risk assessments, or consulting. These fees are more common in commercial insurance or financial planning contexts, where agents provide specialized expertise. However, fee-based compensation is less prevalent in personal lines of insurance like auto or home coverage.

Bonuses and incentives are another component of agent compensation. Insurance companies often reward agents for meeting sales quotas, retaining clients, or selling specific types of policies. These bonuses can significantly boost an agent’s income, but they may also create potential conflicts of interest if agents prioritize higher-paying products over client needs.

Some agents, particularly those employed by large firms or call centers, receive a fixed salary. This model provides stability but may limit earning potential compared to commission-based roles. Salaried agents may still receive performance bonuses or profit-sharing depending on company policy.

Ultimately, an insurance agent’s earnings depend on their business model, experience, and ability to build a loyal client base. While commissions remain the cornerstone of insurance compensation, the rise of fee-based services and hybrid models reflects a shift toward more transparent and client-focused practices.

Consumers should feel empowered to ask agents about their compensation structure to ensure they receive unbiased advice tailored to their needs.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

A paradox is a figure of speech that can seem silly or contradictory in form, yet it can still be true, or at least make sense in the context given. This is sometimes used to illustrate thoughts or statements that differ from traditional ideas. So, instead of taking a given statement literally, an individual must comprehend it from a different perspective. Using paradoxes in speeches and writings can also add wit and humor to one’s work, which serves as the perfect device to grab a reader or a listener’s attention.

But paradoxes can be quite difficult to explain by definition alone, which is why it is best to refer to a few examples to further your understanding.

A good paradox example is in the famous television show House. Here, Dr. House is a rude, selfish, and narcissistic character who alienates everyone around him, even his own colleagues. However, he is also a brilliant doctor who is committed to saving lives. Regardless of his mean exterior, Dr. House is a moral and compassionate man who cares about his patients. The paradox here is how the character strives to save people’s lives despite his ruthless personality and behavior.

Modern health care appears to be rich in contradictions, and it is claimed to be paradoxical in a number of ways. In particular health care is held to be a paradox itself: it is supposed to do good; but is also accused of doing harm.

The expression “first do no harm,” which is a Latin phrase, is not part of the original or modern versions of the Hippocratic Oath, which was originally written in Greek (“primum non nocere,” the Latin translation from the original Greek.)

The Hippocratic Oath, written in the 5th century BCE, does contain language suggesting that the physician and his assistants should not cause physical or moral harm to a patient.

The first known published version of “do no harm” dates to medical texts from the mid-19th century, and is attributed to the 17th century English physician Thomas Sydenham.

Difference between Paradox and Oxymoron

Most people tend to confuse a paradox with an oxymoron, and it’s not hard to see why. Most oxymoron examples appear to be compressed version of a paradox, in which it is used to add a dramatic effect and to emphasize contrasting thoughts. Although they may seem greatly similar in form, there are slight differences that set them apart.

A paradox consists of a statement with opposing definitions, while an oxymoron combines two contradictory terms to form a new meaning. But because an oxymoron can play out with just two words, it is often used to describe a given object or idea imaginatively. As for a paradox, the statement itself makes you question whether something is true or false. It appears to contradict the truth, but if given a closer look, the truth is there but is merely implied.

The Paradox in Medicine and Health Care

Dr. Bernard Brom [Editor: SA Journal of Natural Medicine] suggests modem medicine is riddled with paradoxes. Most doctors live with these paradoxes without being aware of the conflict of interest that these paradoxes represent. Intrinsic to a general understanding of science is the idea that science frees us from misunderstanding and guides us towards clear decision making.

Most veteran doctors with experience know that medical science still does not give definitive answers, that each individual is unique, that one can never be sure how a patient will respond to a particular drug, or what the outcome of a particular operation will be. Human beings are not machines and therefore do not respond according to Newtonian logic, and therefore a paradox in medicine is not surprising. Medicine is an art which uses scientific techniques and approaches. It is, however, important to face these paradoxes. It is both humbling and enlightening, enriching those who consider the implications deeply enough.

The Compensation versus Value Paradox

Regardless of specialty, degree designation or delivery model, private practice physician salary is traditionally inversely related to independent medical practice business value.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on October 31, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Vitaliy Katsenelsen CFA

***

***

One of the biggest hazards of being a professional money manager is that you are expected to behave in a certain way.

One of the biggest hazards of being a professional money manager is that you are expected to behave in a certain way: You have to come to the office every day, work long hours, slog through countless emails, be on top of your portfolio (that is, check performance of your securities minute by minute), watch business TV and consume news continuously, and dress well and conservatively, wearing a rope around the only part of your body that lets air get to your brain. Our colleagues judge us on how early we arrive at work and how late we stay. We do these things because society expects us to, not because they make us better investors or do any good for our clients.

Somehow we let the mindless, Henry Ford–assembly-line, 8:00 a.m. to 5:00 p.m., widgets-per-hour mentality dictate how we conduct our business thinking. Though car production benefits from rigid rules, uniforms, automation and strict working hours, in investing — the business of thinking — the assembly-line culture is counterproductive. Our clients and employers would be better off if we designed our workdays to let us perform our best.

Investing is not an idea-per-hour profession; it more likely results in a few ideas per year. A traditional, structured working environment creates pressure to produce an output — an idea, even a forced idea. Warren Buffett once said at a Berkshire Hathaway annual meeting: “We don’t get paid for activity; we get paid for being right. As to how long we’ll wait, we’ll wait indefinitely.”

How you get ideas is up to you. I am not a professional writer, but as a professional money manager, I learn and think best through writing. I put on my headphones, turn on opera and stare at my computer screen for hours, pecking away at the keyboard — that is how I think. You may do better by walking in the park or sitting with your legs up on the desk, staring at the ceiling.

I do my best thinking in the morning. At 3:00 in the afternoon, my brain shuts off; that is when I read my emails. We are all different. My best friend is a brunch person; he needs to consume six cups of coffee in the morning just to get his brain going. To be most productive, he shouldn’t go to work before 11:00 a.m.

And then there’s the business news. Serious business news that lacked sensationalism, and thus ratings, has been replaced by a new genre: business entertainment (of course, investors did not get the memo). These shows do a terrific job of filling our need to have explanations for everything, even random events that require no explanation (like daily stock movements). Most information on the business entertainment channels — Bloomberg Television, CNBC, Fox Business — has as much value for investors as daily weather forecasts have for travelers who don’t intend to go anywhere for a year.

Yet many managers have CNBC, Fox or Bloomberg TV/Internet streaming on while they work.

The Evolving Landscape of Broker-Dealer Recruitment

Broker-dealer recruitment has become a dynamic and competitive arena within the financial services industry. As firms vie for top talent, the strategies and incentives used to attract and retain financial advisors have evolved significantly. In an environment shaped by regulatory changes, technological innovation, and shifting advisor expectations, broker-dealers must continuously refine their recruitment approaches to remain competitive and relevant.

At the heart of broker-dealer recruitment is the pursuit of experienced financial advisors who bring with them established client relationships and significant assets under management. These advisors are highly sought after because they can generate immediate revenue and enhance a firm’s market presence. According to recent industry reports, firms like LPL Financial, Commonwealth, and Cetera have ramped up their recruitment efforts by investing in platform enhancements, rebranding initiatives, and technology upgrades to appeal to both seasoned professionals and the next generation of advisors.

One of the most significant trends in broker-dealer recruitment is the emphasis on value-added services. Advisors today are not merely looking for the highest payout or signing bonus; they are increasingly drawn to firms that offer robust support systems, including compliance assistance, marketing resources, and advanced technology platforms. Broker-dealers that can demonstrate a commitment to advisor growth and client service excellence are more likely to attract top-tier talent.

The competitive nature of the industry has also led to the rise of aggressive recruitment tactics, including lucrative transition packages and equity offers. While these financial incentives can be effective, they are increasingly being supplemented by strategic differentiators such as flexible affiliation models, access to alternative investment platforms, and opportunities for practice acquisition or succession planning.

Moreover, the recruitment landscape is being reshaped by broader economic and regulatory forces. The implementation of Regulation Best Interest (Reg BI) and the ongoing impact of high interest rates have prompted advisors to reassess their affiliations and seek firms that provide clarity, stability, and strategic guidance. Broker-dealers that proactively address these concerns and offer transparent, advisor-centric solutions are better positioned to succeed in the recruitment race.

In conclusion, broker-dealer recruitment is no longer just about offering the biggest check. It is about creating a compelling value proposition that resonates with advisors’ professional goals and personal values. Firms that invest in technology, culture, and advisor support—while remaining agile in response to industry trends—will be best equipped to attract and retain the talent necessary for long-term success.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Do you ever wish you could acquire specific information for your career activities without having to complete a university Master’s Degree or finish our entire Certified Medical Planner™ professional designation program? Well, Micro-Certifications from the Institute of Medical Business Advisors, Inc., might be the answer. Read on to learn how our three Micro-Certifications offer new opportunities for professional growth in the medical practice, business management, health economics and financial planning, investing and advisory space for physicians, nurses and healthcare professionals.

Micro-Certification Basics

Stock-Brokers, Financial Advisors, Investment Advisors, Accountants, Consultants, Financial Analyists and Financial Planners need to enhance their knowledge skills to better serve the changing and challenging healthcare professional ecosystem. But, it can be difficult to learn and demonstrate mastery of these new skills to employers, clients, physicians or medical prospects. This makes professional advancement difficult. That’s where Micro-Certification and Micro-Credentialing enters the online educational space. It is the process of earning a Micro-Certification, which is like a mini-degree or mini-credential, in a very specific topical area.

Micro-Certification Requirements

Once you’ve completed all of the requirements for our Micro-Certification, you will be awarded proof that you’ve earned it. This might take the form of a paper or digital certificate, which may be a hard document or electronic image, transcript, file, or other official evidence that you’ve completed the necessary work.

Uses of Micro-Certifications

Micro-Certifications may be used to demonstrate to physicians prospective medical clients that you’ve mastered a certain knowledge set. Because of this, Micro-Certifications are useful for those financial service professionals seeking medical clients, employment or career advancement opportunities.

Examples of iMBA, Inc., Micro-Certifications

Here are the three most popular Micro-Certification course from the Institute of Medical Business Advisors, Inc:

1. Health Insurance and Managed Care: To keep up with the ever-changing field of health care physician advice, you must learn new medical practice business models in order to attract and assist physicians and nurse clients. By bringing together the most up-to-date business and medical prctice models [Medicare, Medicaid, PP-ACA, POSs, EPOs, HMOs, PPOs, IPA’s, PPMCs, Accountable Care Organizations, Concierge Medicine, Value Based Care, Physician Pay-for-Performance Initiatives, Hospitalists, Retail and Whole-Sale Medicine, Health Savings Accounts and Medical Unions, etc], this iMBA Inc., Mini-Certification offers a wealth of essential information that will help you understand the ever-changing practices in the next generation of health insurance and managed medical care.

2. Health Economics and Finance: Medical economics, finance, managerial and cost accounting is an integral component of the health care industrial complex. It is broad-based and covers many other industries: insurance, mathematics and statistics, public and population health, provider recruitment and retention, health policy, forecasting, aging and long-term care, and Venture Capital are all commingled arenas. It is essential knowledge that all financial services professionals seeking to serve in the healthcare advisory niche space should possess.

3. Health Information Technology and Security: There is a myth that all physician focused financial advisors understand Health Information Technology [HIT]. In truth, it is often economically misused or financially misunderstood. Moreover, an emerging national HIT architecture often puts the financial advisor or financial planner in a position of maximum uncertainty and minimum productivity regarding issues like: Electronic Medical Records [EMRs] or Electronic Health Records [EHRs], mobile health, tele-health or tele-medicine, Artificial Intelligence [AI], benefits managers and human resource professionals.

Other Topics include: economics, finance, investing, marketing, advertising, sales, start-ups, business plan creation, financial planning and entrepreneurship, etc.

How to Start Learning and Earning Recognition for Your Knowledge

Now that you’re familiar with Micro-Credentialing, you might consider earning a Micro-Certification with us. We offer 3 official Micro-Certificates by completing a one month online course, with a live instructor consisting of twelve asynchronous lessons/online classes [3/wk X 4/weeks = 12 classes]. The earned official completion certificate can be used to demonstrate mastery of a specific skill set and shared with current or future employers, current clients or medical niche financial advisory prospects.

Mini-Certification Tuition, Books and Related Fees

The tuition for each Mini-Certification live online course is $1,250 with the purchase of one required dictionary handbook. Other additional guides, white-papers, videos, files and e-content are all supplied without charge. Alternative courses may be developed in the future subject to demand and may change without notice.

***

Contact: For more information, or to speak with an academic representative, please contact Ann Miller RN MHA CMP™ at Email: MarcinkoAdvisors@msn.com [24/7].

Why It Is Difficult to Be a Part-Time Financial Planner Today

In theory, part-time financial planning offers flexibility and work-life balance, making it an attractive option for professionals seeking reduced hours. However, in practice, the role of a financial planner has evolved into a demanding, full-time commitment. The complexity of financial markets, client expectations, regulatory requirements, and technological advancements make part-time financial planning increasingly difficult to sustain.

One of the primary challenges is client relationship management. Financial planning is deeply personal and trust-based. Clients expect consistent communication, timely updates, and proactive advice. A part-time planner may struggle to maintain the same level of responsiveness as full-time counterparts, especially during volatile market conditions or life-changing events like retirement, divorce, or inheritance. Delayed responses or limited availability can erode client confidence and damage long-term relationships.

***

***

Another obstacle is the rapid pace of financial change. Tax laws, investment products, insurance regulations, and retirement planning strategies are constantly evolving. Staying current requires ongoing education, certifications, and industry engagement. For part-time planners, keeping up with these changes while managing clients and administrative tasks can be overwhelming. Falling behind risks offering outdated or suboptimal advice, which could lead to compliance issues or client dissatisfaction.

Regulatory compliance adds another layer of complexity. Financial planners must adhere to strict standards set by organizations like FINRA, the SEC, and state regulators. These include documentation, disclosures, fiduciary responsibilities, and continuing education. Compliance is non-negotiable and time-consuming, regardless of hours worked. Part-time planners face the same scrutiny and liability as full-time professionals, but with fewer hours to manage the workload.

Technology, while a powerful tool, also presents challenges. Clients increasingly expect digital access to their portfolios, real-time updates, and virtual meetings. Managing these platforms requires technical proficiency and regular maintenance. Part-time planners may find it difficult to keep systems updated, troubleshoot issues, or provide tech support, especially if they lack dedicated staff.

Business development is another hurdle. Building and maintaining a client base requires networking, marketing, and referrals. Part-time planners often have limited time to attend events, follow up with leads, or cultivate relationships. This can hinder growth and make it difficult to compete with full-time advisors who are more visible and accessible.

Finally, there’s the issue of income and scalability. Many financial planners earn through commissions, assets under management (AUM), or fee-based models. Part-time work often means fewer clients and lower revenue, which can make it hard to justify the costs of licensing, insurance, software, and office space. Without scale, profitability becomes a challenge.

In conclusion, while the idea of part-time financial planning may seem appealing, the realities of the profession make it difficult to execute effectively. The demands of client care, compliance, education, and business development require consistent attention and availability. Unless the industry adapts to support flexible models, part-time financial planners will continue to face significant barriers to success.

SPEAKING: ME-P Editor Dr. David Edward Marcinko MBA MEd will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Critical thinking allows a Financial Advisor [FA] to analyze information and make an objective judgment. By impartially evaluating the facts related to a matter, Financial Planners [FPs] can draw realistic conclusions that will help make a sound decision. The ability of being able to properly analyze a situation and come up with a logical and reasonable conclusion is highly valued by employers, as well as current and potential clients.

Now, according to Indeed, we present the six main critical thinking and examples that will help you evaluate your own thought process as a FA, FP or Wealth Manager, etc.

What is critical thinking?

Critical thinking is the ability to objectively analyze information and draw a rational conclusion. It involves gathering information on a subject and determining which pieces of information apply to the subject and which don’t, based on deductive reasoning. The ability to think critically helps people in both their personal and professional lives and is valued by most clients and employers.

Why do employers value critical thinking?

Critical thinking skills are a valuable asset for an employee, as employers, brokerages and Registered Investment Advisors [RIAs] typically appreciate candidates who can correctly assess a situation and come up with a logical resolution. Time is a valuable resource for most managers, and an employee able to make correct decisions without supervision will save both that manager and the whole company much valuable time.

***

***

Six main types of critical thinking skills

There are six main critical thinking skills you can develop to successfully analyze facts and situations and come up with logical conclusions:

1. Analytical thinking

Being able to properly analyze information is the most important aspect of critical thinking. This implies gathering information and interpreting it, but also skeptically evaluating data. When researching a work topic, analytical thinking helps you separate the information that applies to your situation from that which doesn’t.

2. Good communication

Whether you are gathering information or convincing others that your conclusions are correct, good communication is crucial in the process. Asking people to share their ideas and information with you and showing your critical thinking can help step further towards success. If you’re making a work-related decision, proper communication with your coworkers can help you gather the information you need to make the right choice.

3. Creative thinking

Being able to discover certain patterns of information and make abstract connections between seemingly unrelated data helps improve your critical thinking. When analyzing a work procedure or process, you can creatively come up with ways to make it faster and more efficient. Creativity is a skill that can be strengthened over time and is valuable in every position, experience level and industry.

4. Open-mindedness

Previous education and life experiences leave their mark on a person’s ability to objectively evaluate certain situations. By acknowledging these biases, you can improve your critical thinking and overall decision process. For example, if you plan to conduct a meeting in a certain way and your firm suggests using a different strategy, you should let them speak and adjust your approach based on their input.

5. Ability to solve problems

The ability to correctly analyze a problem and work on implementing a solution is another valuable skill.

6. Asking thoughtful questions:

In both private and professional situations, asking the right questions is a crucial step in formulating correct conclusions. Questions can be categorized in various forms as mentioned below:

***

***

* Open-ended questions

Asking open-ended questions can help the person you’re communicating with provide you with relevant and necessary information. These are questions that don’t allow a simple “yes” or “no” as an answer, requiring the respondent to elaborate on the answer.

* Outcome-based questions

When you feel like another person’s experience and skills could help you work more effectively, consider asking outcome-based questions. Asking someone how they would act in a certain hypothetical situation, such as a stock market correction, can give you an insight into their perspective, helping you see things you hadn’t thought about before.

Reflective questions

You can gain insight by asking a client to reflect and evaluate an experience and explain their thought processes during that time. This can help you develop your critical thinking by providing you real-world examples.

* Structural questions

An easy way to understand something is to ask how something works. Any working system results from a long process of trial and error, and properly understanding the steps that needed to be taken for a positive result could help you be more efficient in your own endeavors.

CONCLUSION

Critical thinking is like a muscle that can be exercised and built over time. It is a skill that can help propel your career to new heights. You’ll be able to solve workplace issues, use trial and error to troubleshoot ideas, and more.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Posted on September 29, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I. and Staff Reporters

***

A meme is an idea, behavior, or style that spreads by means of imitation from person to person within a culture and often carries symbolic meaning representing a particular phenomenon or theme. A meme acts as a unit for carrying cultural ideas, symbols, or practices, that can be transmitted from one mind to another through writing, speech, gestures, rituals, or other imitable phenomena with a mimicked theme. Supporters of the concept regard memes as cultural analogues to genes in that they self-replicate, mutate, and respond to selective pressure. In popular language, a meme may refer to an internet meme, typically an image, that is remixed, copied, and circulated in a shared cultural experience online.

EXAMPLE Investing Meme:

“Sell in May and Go Away” is an investment strategy for stocks based on a theory (sometimes known as the Halloween indicator) that the period from November to April inclusive has significantly stronger stock market growth on average than the other months. In such strategies, stock holdings are sold or minimized at about the start of May and the proceeds held in cash; stocks are bought again in the autumn. So, “Sell in May” can be characterized as the memetic belief that it is better to avoid holding stock during the summer period.

The Wall Street adage — ‘Sell Rosh Hashana; buy Yom Kippur’ — focuses on the market’s performance between these two Jewish holidays. This seasonal stock-market trading pattern is upon us — and worth observing.

Rosh Hashanah is the Jewish New Year while Yom Kippur is the Day of Atonement. So, according to Mark Hulbert, it might seem arbitrary to make stock-investment decisions by blending religious observance with financial strategy, but there’s one old trading folklore commonly or meme mentioned during this time of year: “Sell Rosh Hashanah, buy Yom Kippur.”

This Wall Street adage suggests that U.S. stocks tend to fall over the 10 days the Jewish High Holidays are observed, so investors would be better off selling beforehand and buying afterward. But some market analysts believe investors should be wary of this seasonal trading pattern this year.

Historically, the “sell Rosh Hashanah, buy Yom Kippur” strategy is closely tied to the stock market’s tendency to under perform in September, with investors often looking to “minimize exposure” during this period, according to Yehuda Leibler, chief strategy and technology officer at ARX Advisory.

Posted on September 22, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Authentication:

The verification of the identity of an individual, system, machine, or any other unique entity

Authorization:

The process of allowing access to specific areas of a system based on the role and needs of the user

Committee Charter:

A document that defines the purposes and responsibilities of the oversight committee

Compliance Risk Profile:

The current and prospective risk to earnings or capital arising from violations of or nonconformance with laws, rules, regulations, prescribed practices, internal policies and procedures, or ethical standards

Control Assessment:

A high-level review and analysis of controls relating to a process; should encompass both current and missing controls

Controls:

Methods that preserve the integrity of important information, meet operational or financial targets, and/or communicate management policies (See also: Key Control, Secondary Control, Tertiary Control)

ERM Policy Statement:

Defines an organization’s approach to and method of enterprise risk management

Governance:

Processes and structures implemented to communicate, manage, and monitor organizational activities

Impact:

The influence and effect of a risk

Inherent Risk:

Risk that is inherent to a process, taking into consideration the likelihood and impact of a risk

Key Control:

A primary control that is essential for a business process; typically takes place during the process it applies to

Key Indicators:

Measurements that are important for organizations to monitor for potential issues; examples include key performance indicators (KPIs) and key risk indicators (KRIs)

Key Performance Indicator (KPI):

A measurement with a defined set of goals and tolerances that gauges the performance of an important business activity

Key Risk Indicator (KRI):

A proactive measurement for future and emerging risks that indicates the possibility of an event that adversely affects business activities

Likelihood:

The probability of a risk occurring

Mitigation Actions:

The necessary steps, or action items, to reduce the likelihood and/or impact of a potential risk

Operation Risk Profile:

1) The risk arising from the execution of an organization’s business processes; 2) The risk of loss resulting from failed or inadequate internal processes, systems, people, or other entities

Price Risk Profile:

The risk to earning or capital arising from adverse changes in portfolio values

Process:

1) The principle elements of essential business functions within work groups or business units; 2) A set of tasks completed by business continuity plan owners within a department

Reputation Risk Profile:

The current and prospective risk to earnings or capital arising from negative public opinion or perception

Residual Risk:

Risk remaining after considering the existing control environment

Risk:

A potential event or action that would have an adverse effect on the organization

Risk Appetite:

A statement that broadly considers the risk levels that management deems acceptable

Risk Assessment:

The prioritization of potential business disruptions based on the impact and likelihood of occurrence; includes an analysis of threats based on the impact to the organization, its customers, and financial markets

Risk Tolerance:

A metric that sets the acceptable level of variation around organizational objectives and provides assurance that the organization remains within its risk appetite

Secondary Control:

An important control that typically takes place after the process it applies to (i.e., reporting or ongoing monitoring)

Strategic Risk Profile:

The current and prospective risk to earnings or capital raising from adverse business decisions, improperly implemented decisions, or lack of responsiveness to industry changes

Tertiary Control:

A non-essential control that can still be applied effectively to a business process

Velocity:

The time it takes a risk event to manifest itself

Vulnerability:

An entity’s susceptibility to a risk event as determined by the entity’s preparedness, agility, and adaptability

A brand is a name, term, design, symbol or any other feature that distinguishes one seller’s goods or service from those of other sellers. Brands are used in business, marketing and advertising for recognition and, importantly, to create and store value as brand equity for the object identified, to the benefit of the brand’s clients, patients, customers, its owners and shareholders. Brand names are sometimes distinguished from generic or store brands.

Brand management, also known as Marketing, is responsible for the overall management of a brand. This includes everything from product or service development and marketing to advertising and public relations. All of these aspects work together to create a particular image or reputation for a brand. The goal of brand management is to create a robust and positive reputation for a brand that will result in increased sales and market share.This process helps companies create a unique identity for their products or services in the marketplace. A successful brand management strategy can build client, patient and customer loyalty .

Branding is essential for financial advisors, doctors and businesses because it involves creating a unique identity for a company’s products, offerings and services. It can also help build customer, client and patient loyalty and emotionally connect with the practitioner. Branding can be complex, but it is essential to understand the basics before starting a brand strategy.

Thus, doctors, podiatrists, dentists, CPAs, insurance agents, financial advisors and their practices need to understand the different aspects of branding and brand management to create a strong brand identity.

Experts estimate that it can cost more than $1 million to recruit and train a replacement for a doctor who leaves the profession because of burnout. But, as no broad calculation of burnout costs exists, Dr. Tait Shanafelt [Mayo Clinic researcher and Stanford Medicine’s first Chief Physician Wellness Officer] said Stanford, Harvard Business School, Mayo Clinic and the American Medical Association (AMA) are further cost estimating the issue. Nevertheless, Shanafelt and other researchers have shown that burnout erodes job performance, increases medical errors, and leads doctors to leave a profession they once loved.

Fortunately, we can help. From formal coaching to second career opinions, mentoring and advising, we can help with our remediation executive career programs. Regardless of what is happening in your life, it is wonderful to have a non-partial, confidential and informed career coach and sounding board on your side.

CITE: JAMA Internal Medicine [Effect of a Professional Coaching Intervention on the Well-Being and Distress of Physicians].

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

If you are just starting out managing your finances and don’t know where to begin, a financial coach may be a good option for you. They are helpful for someone who wants to become proficient in the basics of finance, from learning how to budget or save money to building an emergency fund or creating a plan for paying off debt. If you have short-term money goals, like saving for a big purchase or just practicing better money habits, a financial coach can help you reach them by working with you to create a plan and holding you accountable. Even more for physicians and most all medical professionals.

Pros and Cons of Working with a Financial Coach A financial coach can have a positive impact on your financial well–being and your life in a number of ways:

Financial coaches see the bigger picture of how you relate to money. They can help you develop better habits, resulting in positive personal growth.

By providing education and encouragement, they can reduce financial stress, confusion, and what it is about money that overwhelms you.

Through accountability and support, they can help you accomplish your goals and help you feel more confident in your finances.

Available 24/7/365.

Modest fees.

At you service. Dr. David Edward Marcinko MBA MEd CMP

Posted on June 8, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

Call for Manuscripts, Articles, Essays, Comments or Opinions

Dear Medical and Financial Services Colleagues, Health Economists, CPAs, JDs, Insurance Agents and Consultants,

The Medical Executive-Post (ME-P), supported by iMBA Inc., with (ISSN 13: 978-1-4665-5873-1] is currently accepting manuscripts for publication.

The ME-P is an open access, multidisciplinary, international, blind peer-reviewed and non-peer-reviewed electronic forum which publishes high-quality solicited and unsolicited research, commentary, opinions, curated news and review articles in English, in all areas of Physician Focused Financial Planning, health economics, finance, accounting, medical practice management, health law, IT, policy and administration. We have over 50 topic channels.

Rapid Response Peer-Review

ME-P is a rapid response forum that publishes daily. One of our objectives is to inform contributors (authors) of the decision on their manuscript(s) within 48 hours of submission. Following acceptance, a paper would be published in the next available issue. The ME-P provides immediate open access to published articles without any barrier.

***

[ME-P Fast Review, Turn-Around and Publishing Time]

***

Broad Exposure Potential

Publishing your news, opinions or comments, essays or articles with the ME-P means that they will be available to millions of readers and researchers because our large and diverse readership base comprises millions of collaborators. Our forum supports the free downloading of published articles by scholars for use as materials for lecture, by government officials for policy making, professors, colleges, universities and educators, and by corporate researchers and FAs to selected firms and organizations world-wide.

Blog Citations

Assessment

Also, ME-P is a member of several local and international organizations, making it possible for the far and wide distribution of published materials. We ask you to support this initiative by publishing your thoughts, comments, articles and original paper(s) 0n this forum, and in our textbooks and white-papers, etc.

Posted on June 1, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters and AI

***

***

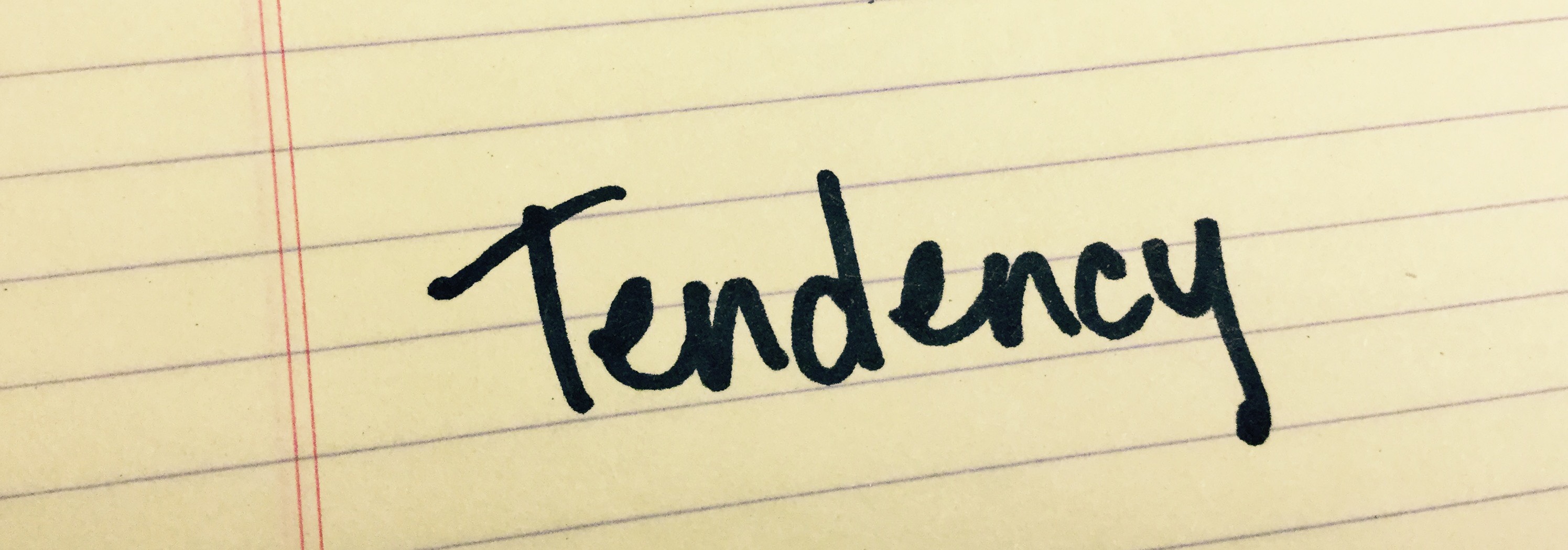

Consistency and Commitment Tendency: Human beings have evolved – probably both genetically and socially – to be consistent. It is easier and safer to deal with others if they honor their commitments and if they behave in a consistent and predictable manner over time. This allows people to work together and build trust that is needed for repeat dealings and to accomplish complex tasks.

In the jungle, this trust was necessary to for humans to successfully work as a team to catch animals for dinner, or fight common threats. In business and life it is preferable to work with others who exhibit these tendencies. Unfortunately, the downside of these traits is that people make errors in judgment because of the strong desire not to change, or be different (“lemming effect” or “group-think”). So the result is that most people will seek out data that supports a prior stated belief or decision and ignore negative data, by not “thinking outside the box”.

Additionally, future decisions will be unduly influenced by the desire to appear consistent with prior decisions, thus decreasing the ability to be rational and objective. The more people state their beliefs or decisions, the less likely they are to change even in the face of strong evidence that they should do so. This bias results in a strong force in most people causing them to avoid or quickly resolve the cognitive dissonance that occurs when a person who thinks of themselves as being consistent and committed to prior statements and actions encounters evidence that indicates that prior actions may have been a mistake.

According to colleague Dan Ariely PhD, it is particularly important therefore for advisors to be aware that their communications with clients and the press clouds the advisor’s ability to seek out and process information that may prove current beliefs incorrect. Since this is obviously irrational, one must actively seek out negative information, and be very careful about what is said and written, being aware that the more you shout it out, the more you pound it in.

Posted on May 16, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Oak Street Health, headquartered in Chicago and a wholly-owned subsidiary of CVS Health since 2023, has agreed to pay $60 million to resolve allegations that it violated the False Claims Act by paying kickbacks to third-party insurance agents in exchange for recruiting seniors to Oak Street Health’s primary care clinics.

The Anti-Kickback Statute prohibits anyone from offering or paying, directly or indirectly, any remuneration — which includes money or any other thing of value — to induce referrals of patients or to provide recommendations of items or services covered by Medicare, Medicaid and other federally funded programs. Under the Medicare Advantage (MA) Program, also known as Part C, Medicare beneficiaries have the option to obtain their health care through privately-operated insurance plans known as MA plans. Some MA Plans contract with health care providers, including Oak Street Health, to provide their plan members with primary care services.

The United States alleged that, in 2020, Oak Street Health developed a program to increase patient membership called the Client Awareness Program. Under the Program, third-party insurance agents contacted seniors eligible for or enrolled in Medicare Advantage and delivered marketing messages designed to generate interest in Oak Street Health. Agents then referred interested seniors to an Oak Street Health employee via a three-way phone call, otherwise known as a “warm transfer,” and/or an electronic submission.

In exchange, Oak Street Health paid agents typically $200 per beneficiary referred or recommended. These payments incentivized agents to base their referrals and recommendations on the financial motivations of Oak Street Health rather than the best interests of seniors. The settlement resolves allegations that, from September 2020 through December 2022, Oak Street Health knowingly submitted, and caused the submission of, false claims to Medicare arising from kickbacks to agents that violated the Anti-Kickback Statute.

Phantom equity is an increasingly popular tool within businesses, particularly startups and private companies, for incentivizing employees without diluting ownership. It allows firms to reward key personnel by linking compensation to the company’s performance, aligning employee interests with those of shareholders.

Basic Mechanisms of Phantom Equity

Phantom equity operates as a contractual agreement offering employees a simulated stake in the business without issuing actual stock. This arrangement appeals to companies aiming to maintain control over their equity structure while providing performance-based incentives. The benefits mimic stock ownership, such as dividends and capital appreciation, without the complexities of transferring actual shares.

The company establishes a phantom equity plan that defines terms such as vesting schedules, performance metrics, and payout conditions. Vesting schedules, often ranging from three to five years, encourage employee retention. Performance metrics may include revenue growth, profit margins, or other financial indicators aligned with strategic goals. Once vested, employees receive cash payments based on the value of the phantom shares, determined by the company’s valuation at payout.

Valuations, often conducted through third-party appraisals or internal financial metrics, directly affect payouts. If the company grows significantly, the value of phantom shares increases, resulting in higher payouts. Conversely, if performance declines, the value of these shares decreases, reducing compensation.

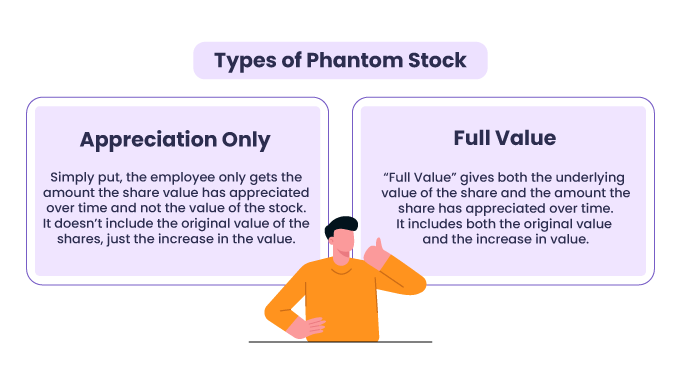

Types of Phantom Equity Plans

Phantom equity plans can be customized to suit a company’s goals, with two primary types being most common: appreciation-only arrangements and full-value arrangements.

Appreciation-Only Arrangements

Appreciation-only arrangements reward employees for the increase in the company’s value over a specified period. Employees are granted phantom shares that reflect the appreciation in the company’s valuation from the grant date to the payout date.

For instance, if phantom shares are initially valued at $10 each and the valuation rises to $15, the employee receives a payout of $5 per share. This structure ties employee rewards to company growth without affecting equity. Companies must rely on precise valuation methods, often adhering to GAAP or IFRS, to ensure fairness and compliance.

Full-Value Arrangements

Full-value arrangements provide payouts equivalent to the full value of phantom shares at vesting or payout. This includes both the initial value and any appreciation.

For example, if phantom shares are initially valued at $10 and later rise to $15, the employee receives $15 per share. While offering greater potential rewards, full-value arrangements require a larger financial commitment from the company. Careful financial planning and adherence to standards like ASC 718, which governs share-based compensation, are essential for managing these plans effectively.

Posted on April 24, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters and Lawrence Rosenberg

***

***

Cold calling is a term that is typically applied to telesales, but most new business relationships actually begin with a “cold” contact of some kind. Whether through social media, email over the phone or door-to-door, “cold calling” lives up to its name; you are contacting prospects (hopefully decision makers) sans introduction and without warning. In some, if not many cases, you will be presenting to customers who have never heard of you, your firm, or your product/service prior to you getting a hold of them. You will also find yourself coming up against the palace guards (secretaries and personal assistants) whose most important job is to run interference for the boss and thwart any and all attempts that an unfamiliar caller might make to reach them. But, as the sales game will readily teach anyone with the fortitude to last long enough to learn the lesson, the more resistance one faces in the pursuit of a successful outcome, the bigger the payoff will be if one can muster the grit necessary to tough it out.

However difficult the road to riches, cold calling allows for a complete leveling of the playing field. Those that sweep the streets could tomorrow talk with billionaires; a man of little status or worth could enter into a contract with the founder of a blue chip, multinational firm — all with a single, unexpected phone call. The sheer daring of such an approach, its impromptu nature, works for so many reasons, not least of which is that it opens doors. From the intrigue and urgency the suddenness of the call implies, to the instant access a bold overture provides, cold calling is the great equalizer among executives, and a path to achievement open to all, no matter one’s experience, education or connections. Not that there ever were any truly insurmountable barriers to climbing the corporate ladder or accessing its highest rungs that a motivated self-starter could not overcome, but with the advent of the telephone and the brashness of the cold sell perfected, the most entrenched and frustrating of impediments, bureaucracy and fraternalism, ceased to be an obstacle. Yesteryear’s power elite traditionally only did business with friends, acquaintances and family (or perhaps a member of their local country club or lodge), but at the very least, those that connected in business were routinely introduced through a referral. However, the audacity of the unscheduled contact, the inspired notion of a “cold call,” and the realization that it worked, that a person of great esteem or importance was willing to do business with an unusually forward individual, made the glad-handing salesman who relied on his father’s rolodex obsolete.