BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

The theory emerged during a period when stock trading was dominated by institutions and wealthy individuals. Small investors, who could not afford 100‑share blocks, often purchased odd lots. Analysts observed that these traders tended to enter the market after prices had already risen significantly and to sell only after declines had already occurred. The odd‑lot theory formalized this observation into a broader claim: odd‑lot investors consistently act on emotion rather than analysis, making them a useful signal of crowd psychology.

Two assumptions sit at the heart of the theory:

Odd‑lot traders are generally uninformed. They are presumed to lack access to research, professional advice, or disciplined strategies.

Their behavior is reactive rather than predictive. They buy after feeling confident and sell after feeling fearful, which often means they are late to major turning points.

From these assumptions, analysts concluded that odd‑lot buying was a bearish sign and odd‑lot selling was bullish.

How the theory was used

Market services once tracked odd‑lot purchases and sales, publishing weekly statistics. Analysts interpreted these numbers in several ways:

Odd‑lot buying as a sell signal. If small investors were aggressively buying, it suggested optimism had peaked.

Odd‑lot selling as a buy signal. Heavy selling implied capitulation, a point at which fear had driven out the last hesitant holders.

Odd‑lot short selling as a bullish sign. Because odd‑lot traders were thought to be poor market timers, their attempts to short the market were interpreted as a sign that prices were likely to rise.

These interpretations were not mechanical rules but sentiment cues. The theory functioned similarly to modern contrarian indicators such as surveys of investor confidence or measures of retail trading activity.

Why the theory gained traction

The odd‑lot theory resonated for several reasons. First, it aligned with the broader belief that markets are driven by cycles of fear and greed. Small investors, lacking experience, were seen as especially vulnerable to these emotional swings. Second, the theory offered a simple, intuitive tool for identifying market extremes. In an era before sophisticated data analytics, any observable pattern in investor behavior was valuable. Finally, the theory fit the narrative that professional investors were more rational and disciplined, reinforcing the idea that the “smart money” moved opposite the crowd.

Limitations and criticisms

Despite its historical appeal, the odd‑lot theory has significant weaknesses.

Its assumptions about small investors are overly broad. Not all odd‑lot traders were uninformed; many simply lacked the capital to buy round lots.

Market structure has changed dramatically. Fractional shares, online brokerages, and algorithmic trading have blurred the distinction between small and large investors.

Retail investors today are more diverse. Some are inexperienced, but others are highly sophisticated, using advanced tools and strategies.

Empirical support is inconsistent. Studies over time have shown mixed results, with odd‑lot activity not reliably predicting market turning points.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Reputational risk has become one of the most consequential and complex challenges facing modern banks. In an industry built fundamentally on trust, reputation functions as a form of capital—intangible yet immensely valuable. When customers deposit money, purchase financial products, or rely on a bank for advice, they are placing confidence in the institution’s integrity, competence, and stability. Because of this, reputational damage can undermine a bank’s ability to attract customers, retain investors, and maintain regulatory goodwill. In severe cases, it can even threaten a bank’s survival. Understanding the nature, drivers, and management of reputational risk is therefore essential for any financial institution operating in today’s environment.

Reputational risk refers to the potential for negative public perception to harm a bank’s business operations, financial position, or stakeholder relationships. Unlike credit or market risk, reputational risk is not easily quantified. It is shaped by public sentiment, media narratives, and stakeholder expectations, all of which can shift rapidly. A single incident—whether a data breach, compliance failure, or poorly handled customer complaint—can escalate into a broader crisis if it signals deeper cultural or operational weaknesses. Because reputation is cumulative, built over years but vulnerable to sudden erosion, banks must treat it as a strategic asset requiring continuous attention.

One of the primary drivers of reputational risk is regulatory non‑compliance. Banks operate in a heavily regulated environment, and violations—such as money‑laundering failures, sanctions breaches, or misleading product disclosures—can quickly become public scandals. Even when fines are manageable, the reputational fallout can be far more damaging. Customers may question the bank’s ethical standards, while regulators may impose heightened scrutiny. In some cases, non‑compliance suggests systemic governance issues, prompting investors to reassess the bank’s long‑term stability. Because compliance failures often become headline news, they can shape public perception more powerfully than technical financial metrics.

Another major source of reputational risk is operational failure. Technology outages, cybersecurity breaches, and payment system disruptions can erode customer confidence, especially as banking becomes increasingly digital. A bank that cannot reliably safeguard data or provide uninterrupted access to accounts risks appearing incompetent or careless. Cyber incidents are particularly damaging because they raise concerns about privacy and financial security—two pillars of trust in the banking relationship. Even when the root cause is external, such as a sophisticated cyberattack, customers often hold the bank responsible for inadequate defenses.

Customer treatment also plays a central role in shaping reputation. Banks interact with millions of individuals and businesses, and each interaction contributes to the institution’s public image. Poor customer service, unfair fees, aggressive sales practices, or mishandled complaints can accumulate into a perception that the bank prioritizes profit over people. In the age of social media, individual negative experiences can spread rapidly, influencing broader sentiment. Conversely, banks that demonstrate empathy, transparency, and responsiveness can strengthen their reputational resilience, even when mistakes occur.

***

***

Corporate culture and leadership behavior are equally important. Scandals involving executives—such as conflicts of interest, unethical conduct, or mismanagement—can tarnish the entire organization. Stakeholders often interpret leadership failures as indicators of deeper cultural problems. A bank perceived as having a toxic or complacent culture may struggle to attract talent, maintain employee morale, or convince regulators that it can self‑govern effectively. Because culture influences decision‑making at every level, it is both a source of reputational vulnerability and a potential safeguard.

The consequences of reputational damage can be far‑reaching. Customers may withdraw deposits or move business to competitors, reducing liquidity and revenue. Investors may lose confidence, increasing funding costs or depressing share prices. Regulators may impose stricter oversight, limiting strategic flexibility. Business partners may distance themselves to avoid association with controversy. In extreme cases, reputational crises can trigger self‑reinforcing cycles: negative publicity leads to customer attrition, which weakens financial performance, which in turn fuels further negative publicity. The collapse of trust can be swift, even if the underlying financial fundamentals remain sound.

Given these stakes, effective management of reputational risk requires a proactive and integrated approach. Banks must embed reputational considerations into strategic planning, risk assessment, and daily operations. This begins with strong governance frameworks that emphasize ethical conduct, transparency, and accountability. Leadership must set the tone by modeling integrity and prioritizing long‑term trust over short‑term gains. Clear policies, robust internal controls, and continuous monitoring help prevent misconduct and operational failures before they escalate.

Communication is another critical component. When incidents occur, banks must respond quickly, honestly, and empathetically. Attempts to minimize or obscure problems often backfire, deepening public distrust. Transparent communication—acknowledging mistakes, explaining corrective actions, and demonstrating commitment to improvement—can mitigate reputational harm. Stakeholders are more forgiving when they perceive sincerity and responsibility.

Building reputational resilience also involves cultivating strong relationships with customers, employees, regulators, and communities. Banks that consistently demonstrate social responsibility, customer‑centric values, and community engagement create goodwill that can buffer against negative events. Investing in cybersecurity, customer service, and ethical training further strengthens the institution’s ability to prevent and withstand reputational shocks.

Ultimately, reputational risk is inseparable from the broader identity and purpose of a bank. It reflects not only what the institution does, but how it behaves and what it stands for. In a competitive and highly scrutinized industry, reputation is a differentiator that can drive loyalty, growth, and long‑term success. By treating reputation as a strategic priority—protected through strong governance, ethical culture, operational excellence, and transparent communication—banks can navigate the complexities of modern finance while maintaining the trust that underpins their existence.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Milton Friedman, one of the most influential economists of the twentieth century, devoted much of his work to understanding the nature of money and its role in the economy. Although he is best known for his advocacy of monetary policy rules and his critique of discretionary central banking, Friedman also offered a clear conceptual framework for understanding different forms of money. His discussion of the “four types of money” helps illuminate how money functions, how it evolves, and why its various forms matter for economic stability. These categories—commodity money, commodity‑backed money, fiat money, and fiduciary money—capture the historical progression of monetary systems and the institutional choices societies make in managing their currencies.

Friedman’s first category, commodity money, refers to money that has intrinsic value. Gold, silver, and other precious metals are the classic examples. In this system, the money itself is the valuable good; the coin is worth its weight in metal. Friedman appreciated the historical importance of commodity money because it emerged spontaneously in markets without central planning. People gravitated toward commodities that were durable, divisible, portable, and scarce. However, he also emphasized its limitations. Commodity money ties the money supply to the availability of the underlying resource, which can create instability. Gold discoveries can cause inflation, while shortages can cause deflation. For Friedman, the key issue was that commodity money makes the money supply dependent on mining rather than on the needs of the economy. This rigidity, he argued, is not ideal for modern economic systems that require flexibility and predictability.

The second type, commodity‑backed money, represents a transitional stage between pure commodity money and modern monetary systems. In this arrangement, paper notes or coins circulate, but they are redeemable for a fixed quantity of a commodity such as gold. The gold standard is the most famous example. Friedman acknowledged that commodity‑backed systems solved some of the practical problems of carrying and storing precious metals. They also introduced a degree of trust and institutional structure, since governments or banks promised convertibility. Yet Friedman was critical of the gold standard’s constraints. He argued that tying the money supply to gold reserves limited governments’ ability to respond to economic crises. The Great Depression, in his view, was worsened by the Federal Reserve’s failure to expand the money supply because it was constrained by gold convertibility. For Friedman, the gold standard was neither flexible enough nor stable enough to support a growing, complex economy.

***

***

The third category, fiat money, is the system used by most modern economies. Fiat money has no intrinsic value and is not backed by a commodity. Its value comes from government decree and, more importantly, from public confidence. Friedman recognized that fiat money allows for a more adaptable money supply, which can be adjusted to meet the needs of the economy. However, he also believed that fiat money introduces significant risks. Without the discipline imposed by a commodity standard, governments may be tempted to expand the money supply excessively, leading to inflation. Friedman’s famous statement—“inflation is always and everywhere a monetary phenomenon”—reflects his belief that fiat money systems require strict rules to prevent abuse. He argued that central banks should follow predictable, rule‑based policies, such as increasing the money supply at a constant rate, to avoid the destabilizing effects of discretionary monetary decisions.

The fourth type, fiduciary money, is closely related to fiat money but emphasizes the role of trust and financial institutions. Fiduciary money includes bank deposits, checks, and other forms of money that exist primarily as accounting entries rather than physical currency. These forms of money rely on the confidence that banks will honor withdrawals and that the financial system will remain stable. Friedman viewed fiduciary money as an essential component of modern economies, but he also saw it as a source of vulnerability. Bank failures, credit contractions, and financial panics can all disrupt the supply of fiduciary money. His work with Anna Schwartz in A Monetary History of the United States highlighted how the collapse of the banking system during the Great Depression caused a severe contraction in the money supply, deepening the economic downturn. For Friedman, the lesson was clear: a stable monetary system requires not only sound government policy but also a well‑regulated and resilient banking sector.

Taken together, Friedman’s four types of money illustrate the evolution of monetary systems from tangible commodities to abstract financial instruments. Each type reflects a different balance between stability, flexibility, and trust. Commodity money offers intrinsic value but lacks adaptability. Commodity‑backed money introduces institutional structure but remains constrained by physical resources. Fiat money provides flexibility but requires disciplined policy to maintain stability. Fiduciary money expands the money supply through financial intermediation but depends on the health of the banking system.

Friedman’s analysis ultimately underscores his broader belief that the key to a stable economy is a predictable and well‑managed money supply. Regardless of the form money takes, he argued that economic stability depends on avoiding large swings in the quantity of money. His framework for understanding the four types of money remains relevant today, especially as new forms of digital and electronic money continue to emerge. By examining the strengths and weaknesses of each type, Friedman provided a foundation for thinking about how monetary systems can best support economic growth, stability, and public confidence.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The Net Investment Income Tax (NIIT) occupies a distinctive place in the modern U.S. tax landscape. Introduced as part of the Affordable Care Act, it was designed to generate revenue from higher‑income households by taxing certain forms of unearned income. Although it affects a relatively small portion of taxpayers, its implications reach into investment strategy, tax planning, and broader debates about fairness and economic policy. Understanding how the NIIT works—and why it exists—offers insight into the evolving relationship between tax policy and wealth in the United States.

At its core, the NIIT is a 3.8 percent surtax applied to specific types of investment income for individuals whose modified adjusted gross income exceeds statutory thresholds. These thresholds—$200,000 for single filers and $250,000 for married couples filing jointly—are not indexed for inflation. As a result, over time, more taxpayers may find themselves subject to the tax even if their real purchasing power has not increased. This “bracket creep” is one of the subtle but important features of the NIIT, shaping its long‑term reach.

The tax applies only to “net investment income,” a term that includes interest, dividends, capital gains, rental income, royalties, and passive business income. It does not apply to wages, self‑employment earnings, or distributions from qualified retirement plans. The logic behind this distinction is straightforward: the NIIT targets income derived from wealth rather than labor. In practice, this means that two taxpayers with identical total income may face different NIIT liabilities depending on how much of their income comes from investments versus work.

The mechanics of the NIIT involve a comparison between two amounts: net investment income and the excess of modified adjusted gross income over the applicable threshold. The tax is applied to whichever of these two figures is smaller. This structure ensures that the NIIT functions as a surtax on high‑income households without taxing investment income for those below the threshold. It also means that taxpayers with large investment portfolios but modest overall income may avoid the tax entirely, while those with high wages and relatively small investment income may still owe it.

One of the most significant effects of the NIIT is its influence on investment behavior. Because the tax applies to capital gains, it can affect decisions about when to sell appreciated assets. Taxpayers may choose to time sales to avoid pushing their income above the threshold in a given year. Others may shift toward tax‑exempt investments, such as municipal bonds, or toward assets that generate unrealized rather than realized gains. The NIIT therefore becomes not just a revenue tool but a factor shaping the broader investment landscape.

The tax also interacts with other parts of the tax code in ways that can be complex. For example, rental real estate income is generally subject to the NIIT unless the taxpayer qualifies as a real estate professional and materially participates in the activity. Trusts and estates face their own NIIT rules, often reaching the surtax threshold at much lower income levels than individuals. These layers of complexity mean that the NIIT is often a central topic in tax planning for high‑income households, especially those with diverse investment portfolios.

Beyond its technical features, the NIIT reflects broader policy debates about equity and the distribution of tax burdens. Supporters argue that it helps ensure that high‑income individuals contribute a fair share to the cost of public programs, particularly those related to health care. Because investment income is disproportionately concentrated among wealthier households, the NIIT is seen as a way to align tax policy with ability to pay. Critics, however, contend that the tax discourages investment, adds unnecessary complexity, and imposes an additional layer of taxation on income that may already be subject to corporate taxes or other levies.

Despite these debates, the NIIT has become a stable part of the federal tax system. It raises billions of dollars annually and plays a role in funding health‑related initiatives. As discussions about tax reform continue, the NIIT often resurfaces as policymakers consider how best to balance revenue needs with economic incentives. Whether it remains unchanged, is expanded, or is modified in future legislation, the NIIT will continue to shape the financial decisions of high‑income taxpayers and contribute to the ongoing conversation about how the United States taxes wealth.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The term “INVEST Act” has appeared in multiple financial policy discussions over the past several years, and although it may sound like a single, well‑defined piece of legislation, it actually refers to a range of proposals aimed at encouraging investment, reforming tax treatment, and strengthening long‑term financial security. In the world of finance, the acronym has been used repeatedly because it signals a clear legislative intention: to stimulate economic growth by making investment easier, more attractive, or more accessible. Understanding the INVEST Act in a financial context therefore requires examining the major themes that these proposals share, the problems they attempt to solve, and the broader implications for investors, businesses, and households.

One of the most common uses of the INVEST Act label appears in proposals designed to increase capital investment within the United States. These versions of the act typically focus on adjusting the tax code to encourage companies to expand, innovate, and hire. They may include provisions such as accelerated depreciation schedules, expanded tax credits for research and development, or incentives for domestic manufacturing. The underlying logic is straightforward: when businesses face lower after‑tax costs for investing in equipment, technology, or facilities, they are more likely to undertake projects that boost productivity and create jobs. By lowering barriers to capital formation, these proposals aim to strengthen the country’s long‑term economic competitiveness.

Another major interpretation of the INVEST Act centers on reforming capital gains taxation. In this version, lawmakers propose changes intended to reward long‑term investment rather than short‑term speculation. These reforms might include simplified capital gains brackets, reduced tax rates for assets held over extended periods, or deferral options that allow investors to reinvest gains without immediate tax consequences. The goal is to encourage individuals and institutions to commit capital to productive, long‑horizon ventures such as infrastructure, innovation, or business expansion. Supporters argue that a tax system favoring patient investment helps stabilize financial markets and channels resources toward activities that generate sustainable economic growth.

A third category of INVEST Act proposals focuses on retirement savings. In these cases, the acronym is often used to highlight the importance of long‑term financial security for American workers. These proposals typically aim to expand access to retirement plans, increase contribution limits, or provide tax credits to small businesses that establish retirement programs for their employees. Some versions emphasize automatic enrollment or improved portability, making it easier for workers to maintain consistent savings even as they change jobs. By strengthening the retirement system, these proposals seek to address the growing concern that many households are not saving enough to support themselves later in life. The INVEST Act, in this context, becomes a tool for promoting financial stability and reducing future reliance on social safety nets.

In addition to these targeted reforms, the INVEST Act label has also been applied to broader economic‑development initiatives. These proposals aim to direct private capital into underserved or economically distressed regions. They may expand programs such as Opportunity Zones, offer tax incentives for investment in rural or low‑income areas, or support public‑private partnerships that fund infrastructure and community development. The intention is to use financial policy as a lever to reduce geographic inequality and stimulate growth in areas that have struggled to attract investment. By encouraging capital to flow into regions that need it most, these versions of the INVEST Act attempt to create more balanced and inclusive economic progress.

Although the specific details vary across proposals, the financial versions of the INVEST Act share a common philosophy: investment is a cornerstone of economic strength, and public policy can play a meaningful role in shaping how and where investment occurs. Whether the focus is corporate expansion, capital gains reform, retirement security, or regional development, each version reflects an effort to align financial incentives with long‑term national priorities. These proposals recognize that markets do not always allocate capital in ways that maximize social or economic well‑being, and that targeted policy interventions can help correct imbalances or encourage beneficial behavior.

The diversity of proposals that fall under the INVEST Act umbrella also highlights the complexity of financial policymaking. Encouraging investment is not a single, simple task; it touches on taxation, regulation, household behavior, business strategy, and regional development. As a result, the INVEST Act has become a flexible legislative brand—one that can be adapted to different economic challenges and political goals. While this flexibility can sometimes create confusion about what the act specifically entails, it also reflects the broad recognition that investment, in all its forms, is essential to the country’s future prosperity.

In sum, the INVEST Act in finance is best understood not as a single law but as a recurring legislative theme aimed at strengthening the nation’s economic foundation. Whether through tax incentives, retirement reforms, or development programs, these proposals share a commitment to promoting long‑term growth and financial stability. By examining the various interpretations of the INVEST Act, one gains insight into the evolving priorities of financial policy and the ongoing effort to create an economy that supports innovation, security, and opportunity.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The history of U.S. recessions reflects the nation’s evolving economy, shaped by wars, financial crises, policy shifts, and global events. Since 1857, the U.S. has experienced over 30 recessions, each offering lessons in resilience and reform.

The United States has endured a long and varied history of economic recessions, defined as periods of significant decline in economic activity lasting more than a few months. These downturns are typically marked by falling GDP, rising unemployment, and reduced consumer spending. Since the mid-19th century, recessions have been triggered by a range of factors—from banking panics and inflation to global conflicts and pandemics.

The earliest recorded U.S. recession began in 1857, sparked by a banking crisis and declining international trade. This was followed by the Long Depression of 1873–1879, which lasted a staggering 65 months, making it the longest in U.S. history. The downturn was triggered by the collapse of a major bank and a speculative bubble in railroad investments.

The Great Depression remains the most severe economic crisis in American history. Beginning in 1929 after the stock market crash, it lasted until 1933 and saw unemployment soar to 25%. The Depression reshaped U.S. economic policy, leading to the creation of Social Security, the FDIC, and other New Deal programs aimed at stabilizing the economy and protecting citizens.

Post-World War II recessions were generally shorter and less severe. The 1945 recession, for example, lasted eight months and was caused by the transition from wartime to peacetime production. The 1973–75 recession, however, was more prolonged, driven by an oil embargo and stagflation—a combination of stagnant growth and high inflation.

The early 1980s recession was triggered by the Federal Reserve’s aggressive interest rate hikes to combat inflation. Though painful, it ultimately helped stabilize prices and set the stage for a long period of growth. The early 1990s recession followed a savings and loan crisis and a slowdown in defense spending after the Cold War.

The Great Recession of 2007–2009 was the most significant downturn since the Great Depression. It was caused by the collapse of the housing bubble and widespread failures in financial institutions. Unemployment peaked at 10%, and the crisis led to sweeping reforms in banking and mortgage lending practices.

Most recently, the COVID-19 recession in 2020 was the shortest in U.S. history, lasting just two months. Despite its brevity, it was severe, with unemployment briefly reaching 14.7% due to lockdowns and global supply chain disruptions.

Throughout its history, the U.S. has shown remarkable resilience in recovering from recessions. Each downturn has prompted changes in fiscal and monetary policy, regulatory reform, and shifts in public perception about the role of government and markets. As the economy becomes more interconnected globally, future recessions may be shaped by international events as much as domestic ones.

SPEAKING: ME-P Editor Dr. David Edward Marcinko MBA MEd will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The economics of information explores how knowledge—or the lack of it—affects decision-making, market behavior, and resource allocation. It reveals why perfect competition rarely exists and why information itself can be a powerful economic asset.

Economics of Information: Understanding the Value and Impact of Knowledge

In traditional economic models, markets are often assumed to operate under perfect information—where all participants have equal access to relevant data. However, in reality, information is often incomplete, asymmetric, or costly to obtain. The field known as economics of information emerged to address these discrepancies, fundamentally reshaping how economists understand markets, incentives, and efficiency.

One of the core concepts in this field is information asymmetry, where one party in a transaction possesses more or better information than the other. This imbalance can lead to adverse selection and moral hazard. For example, in the insurance market, individuals who know they are high-risk are more likely to seek coverage, while insurers may struggle to differentiate between high- and low-risk clients. Similarly, in lending, borrowers may have private knowledge about their ability to repay, which lenders cannot easily verify.

To mitigate these problems, economists have developed mechanisms such as signaling and screening. Signaling occurs when the informed party takes action to reveal their type—like a job applicant earning a degree to signal competence. Screening, on the other hand, involves the uninformed party designing tests or contracts to elicit information—such as offering different insurance packages to separate risk levels.

Another important area is the cost of acquiring information. Gathering data, analyzing trends, or verifying facts requires time and resources. This leads to decisions being made under uncertainty, where individuals rely on heuristics or limited data. The economics of information examines how these costs influence behavior, pricing, and market structure. For instance, consumers may not compare every available product due to search costs, allowing firms to maintain price dispersion.

The rise of digital technology has intensified the relevance of this field. In the age of big data, companies like Google and Amazon thrive by collecting and analyzing vast amounts of user information. This data allows them to personalize services, predict behavior, and gain competitive advantages. However, it also raises concerns about privacy, market power, and inequality—issues that economists of information are increasingly addressing.

Moreover, information goods—such as software, media, and research—have unique economic properties. They are often non-rivalrous and can be reproduced at near-zero marginal cost. This challenges traditional pricing models and calls for innovative approaches like freemium strategies, bundling, and subscription services.

In public policy, the economics of information plays a crucial role in designing regulations, transparency standards, and consumer protections. Governments must balance the need for open access to information with incentives for innovation and investment. For example, patent laws aim to encourage research by granting temporary monopolies, while disclosure requirements in finance promote market integrity.

In conclusion, the economics of information reveals that knowledge is not just a passive input but a dynamic force shaping economic outcomes. By understanding how information is produced, distributed, and used, economists can better explain real-world phenomena and design systems that promote fairness, efficiency, and innovation.

Gold has long been regarded as a cornerstone of wealth preservation, and its role within modern investment portfolios continues to attract scholarly attention. As both a tangible asset and a financial instrument, gold embodies characteristics that distinguish it from equities, fixed income securities, and other commodities. Its historical resilience, inflation-hedging capacity, and diversification benefits render it a subject of considerable importance in portfolio construction and risk management.

Historical and Monetary Significance

Gold’s enduring appeal is rooted in its function as a monetary standard and store of value. For centuries, gold underpinned global currency systems, most notably through the gold standard, which provided stability in international trade and monetary policy. Although fiat currencies have supplanted gold in official circulation, its symbolic and practical role as a measure of wealth persists. This historical continuity reinforces investor confidence in gold as a reliable repository of value during periods of economic uncertainty.

Inflation Hedge and Safe-Haven Asset

A substantial body of empirical research demonstrates that gold serves as a hedge against inflation and currency depreciation. When consumer prices rise and fiat currencies weaken, gold tends to appreciate, thereby preserving purchasing power. Moreover, gold’s status as a safe-haven asset is particularly evident during geopolitical crises, financial market turbulence, and systemic shocks. In such contexts, investors reallocate capital toward gold, seeking protection from volatility in traditional asset classes. This defensive quality underscores gold’s utility in stabilizing portfolios during adverse conditions.

Diversification and Risk Management

From the perspective of modern portfolio theory, gold offers diversification benefits due to its low correlation with equities and bonds. Incorporating gold into a portfolio reduces overall variance and enhances risk-adjusted returns. Studies suggest that even modest allocations—typically ranging from 5 to 10 percent—can improve portfolio resilience by mitigating downside risk. This non-correlation is especially valuable in environments characterized by heightened uncertainty, where traditional diversification strategies may prove insufficient.

Investment Vehicles and Accessibility

Gold’s versatility as an investment is reflected in the variety of instruments available to investors. Physical bullion, in the form of coins and bars, provides tangible ownership but entails storage and insurance costs. Exchange-traded funds (ETFs) offer liquidity and ease of access, while mining equities provide leveraged exposure to gold prices, albeit with operational risks. Futures contracts and derivatives enable sophisticated strategies, though they demand expertise and tolerance for volatility. The breadth of these vehicles ensures that gold remains accessible across diverse investor profiles.

Limitations and Critical Considerations

Despite its strengths, gold is not without limitations. Unlike equities or bonds, gold does not generate income, such as dividends or interest. This absence of yield can constrain long-term portfolio growth, particularly in low-inflation environments. Furthermore, gold prices are subject to volatility, influenced by investor sentiment, central bank policies, and global demand dynamics. Overexposure to gold may therefore hinder portfolio performance, underscoring the necessity of balanced allocation.

Conclusion

Gold’s dual identity as a historical store of value and a contemporary financial instrument secures its relevance in portfolio construction. Its inflation-hedging capacity, safe-haven qualities, and diversification benefits justify its inclusion as a strategic asset. Nevertheless, prudent management is essential, given its lack of yield and susceptibility to volatility. Within a scholarly framework of portfolio theory, gold emerges not as a panacea but as a complementary asset, enhancing resilience and stability in the face of evolving economic landscapes.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on January 6, 2026 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

Corporate debt restructuring is a critical financial strategy that enables distressed companies to regain stability, avoid insolvency, and preserve stakeholder value. It involves renegotiating debt terms with creditors to ensure sustainable repayment while maintaining business continuity.

Introduction

Corporate debt restructuring (CDR) refers to the reorganization of a company’s outstanding financial obligations when it faces severe distress or risks defaulting on loans. Instead of proceeding to bankruptcy, firms often negotiate with creditors to modify repayment schedules, reduce interest rates, or even partially write off debt. This process is designed to restore liquidity, protect jobs, and safeguard the interests of shareholders, lenders, and employees.

Causes of Debt Restructuring

Companies typically resort to restructuring due to:

Economic downturns that reduce revenues and profitability

Poor financial management or over-leveraging, leaving firms unable to meet obligations

Sectoral disruptions, such as technological shifts or regulatory changes

Unexpected crises, including pandemics or geopolitical shocks, which strain cash flows

Methods of Debt Restructuring

Several strategies are employed depending on the severity of distress:

Rescheduling debt: Extending repayment periods to ease short-term cash flow pressures

Lowering interest rates: Negotiating reduced borrowing costs to make debt more manageable

Debt-to-equity swaps: Creditors convert debt into equity, reducing liabilities while gaining ownership stakes

Haircuts on principal: Creditors agree to accept less than the full amount owed, preventing total default

Benefits of Debt Restructuring

Avoidance of bankruptcy, preserving business operations

Protection of stakeholders, including employees, creditors, and shareholders

Contribution to economic stability by preventing systemic crises

Improved financial health, allowing companies to refocus on growth and innovation

Challenges in Implementation

Despite its advantages, corporate debt restructuring is complex:

Balancing interests between creditors and companies requires delicate negotiation

Legal and regulatory hurdles complicate cross-border restructuring

Creditor resistance can prolong distress

Reputational risks may reduce investor confidence

Conclusion

Corporate debt restructuring is not merely a reactive measure but a proactive tool for ensuring long-term sustainability. By renegotiating obligations, firms can avoid insolvency, stabilize operations, and contribute to broader economic recovery. While challenges exist, successful restructuring requires transparent communication, fair creditor engagement, and sound financial planning. Ultimately, CDR serves as a bridge between financial distress and renewed corporate viability, making it indispensable in modern business practice.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on January 4, 2026 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

Commodities are essential raw materials that fuel the global economy, traded in markets and used in everything from food production to energy and manufacturing. Their value lies in their universality, stability, and role in investment strategies.

A commodity is a basic good used in commerce that is interchangeable with other goods of the same type. These raw materials are the building blocks of the global economy, ranging from agricultural products like wheat and coffee to natural resources such as crude oil, gold, and copper. Because commodities are standardized and widely used, they are traded on exchanges where their prices fluctuate based on supply and demand.

There are two main types of commodities: hard and soft. Hard commodities include natural resources that are mined or extracted—such as oil, gas, and metals. Soft commodities are agricultural products or livestock—like corn, soybeans, cotton, and cattle. These categories help investors and analysts understand market behavior and economic trends.

Commodities play a vital role in global trade. Countries rich in natural resources often rely on commodity exports to drive their economies. For example, oil-exporting nations like Saudi Arabia and Venezuela depend heavily on petroleum revenues. Similarly, agricultural powerhouses like Brazil and the United States benefit from exporting soybeans, coffee, and wheat. The prices of these commodities can significantly impact national income, inflation rates, and currency strength.

Commodity markets are also important for investors. Many people invest in commodities to diversify their portfolios and hedge against inflation. Since commodity prices often rise when inflation increases, they can act as a buffer against declining purchasing power. Investors can gain exposure to commodities through futures contracts, exchange-traded funds (ETFs), or direct ownership of physical goods. However, commodity investing carries risks, including price volatility due to weather events, geopolitical tensions, and changes in global demand.

One of the key features of commodities is their fungibility. This means that a unit of a commodity is essentially the same regardless of its origin. For example, a barrel of crude oil from Saudi Arabia is considered equivalent to one from Texas, as long as it meets the same grade. This standardization allows commodities to be traded efficiently on global markets.

Commodities also influence consumer prices. When the cost of raw materials rises, it often leads to higher prices for finished goods. For instance, an increase in wheat prices can make bread more expensive, while rising oil prices can lead to higher transportation and heating costs. This ripple effect makes commodity prices a key indicator of economic health.

In conclusion, commodities are foundational to both economic activity and investment strategy. They represent the raw inputs that power industries and sustain daily life. Understanding commodities—how they’re categorized, traded, and priced—offers insight into global markets and helps individuals and nations make informed financial decisions.

Whether you’re a consumer, investor, or policymaker, commodities are a crucial part of the economic landscape.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on December 19, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

🎄 Introduction

The holiday season has long been synonymous with heightened consumer spending, as families allocate budgets for gifts, travel, food, and entertainment. In 2025, however, this tradition is unfolding against a backdrop of inflation, rising living costs, and shifting consumer priorities. While spending remains robust in certain segments, the overall picture reveals a more complex and cautious approach to holiday consumption.

📊 Spending Trends

Overall increase in spending: According to KPMG, consumers expect to spend 4.6% more than last year, though this rise is largely attributed to higher prices rather than stronger financial positions.

Income disparities: Higher‑income households are driving most of the gains, while lower‑income families anticipate cutting back.

Decline in discretionary spending: Growth in discretionary purchases is minimal, with real buying power declining.

Generational differences: Younger generations, especially Gen Z, plan to reduce holiday spending, reflecting financial strain and shifting values.

Gift spending contraction: Average gift spending is expected to drop, signaling a move toward more practical or meaningful purchases.

🛍️ Shopping Behavior

Timing of purchases: Many consumers are delaying shopping, avoiding the traditional early‑season surge.

Digital vs. physical stores: Online shopping continues to grow, but physical stores remain critical for driving results.

Technology in discovery: Tools powered by artificial intelligence are reshaping holiday shopping, helping consumers find deals and products more efficiently.

Concentration of spending: A large share of gift purchases occurs between Thanksgiving and Cyber Monday, reflecting the importance of promotional events.

🎁 Shifts in Priorities

Focus on essentials: Consumers are prioritizing tangible goods and essentials over luxury or experiential items.

Value‑driven choices: Shoppers are seeking value and meaning, often opting for fewer but more thoughtful gifts.

Travel and self‑spending: Many households are allocating more budget for travel and personal indulgence, even as they cut back on gifts.

🌍 Broader Implications

Holiday spending trends highlight the tension between tradition and economic reality. Retailers face challenges in predicting demand, as consumer sentiment remains cautious. Marketing strategies are shifting toward digital platforms, social media, and personalized promotions. For policymakers and economists, these spending patterns serve as indicators of household confidence and broader economic health.

🎯 Conclusion

In summary, consumer spending during the holiday season is marked by uneven growth, generational shifts, and a stronger emphasis on essentials and value. While higher‑income households sustain overall spending levels, many others are scaling back, reflecting the pressures of inflation and rising costs. The season remains festive, but it is increasingly defined by careful budgeting, strategic shopping, and evolving consumer values.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The U.S. faces a heightened risk of recession in 2026, with economic indicators, expert forecasts, and global instability contributing to widespread concern. While some analysts remain cautiously optimistic, the probability of a downturn is significant.

The potential for a U.S. recession in 2026 is a topic of growing concern among economists, policymakers, and investors. According to UBS, the probability of a recession has surged to 93% based on hard data analysis, including employment trends, industrial production, and credit market signals. This alarming figure reflects a convergence of economic stressors that could culminate in a downturn by the end of 2026.

One of the most prominent warning signs is the inverted yield curve, a historically reliable predictor of recessions. When short-term interest rates exceed long-term rates, it suggests that investors expect weaker growth ahead. This inversion, coupled with elevated federal debt and persistent inflationary pressures, has led many analysts to forecast a slowdown in consumer spending and business investment.

Despite these concerns, some sectors—particularly artificial intelligence (AI)—are providing temporary buoyancy. The AI infrastructure boom has fueled GDP growth and market optimism, with global AI investment projected to reach $500 billion by 2026.

However, experts warn that this surge may be masking underlying economic fragility. If AI-driven investment slows, the economy could quickly lose momentum, revealing vulnerabilities in other sectors such as manufacturing and retail.

Global factors also play a critical role. Trade tensions, geopolitical instability, and fluctuating oil prices have created an unpredictable environment. The lingering effects of tariff pass-throughs and policy uncertainty are expected to intensify in 2026, further straining the U.S. economy. Additionally, speculative forecasts—like those from mystic Baba Vanga—have captured public imagination by predicting a “cash crush” that could disrupt both virtual and physical currency systems, although such claims lack empirical support. Not all forecasts are dire. Oxford Economics suggests that while growth will moderate, the U.S. may avoid a full-blown recession thanks to continued investment incentives and robust AI-related spending. Their above-consensus GDP forecast hinges on the assumption that business confidence remains stable and that fiscal policy supports non-AI sectors effectively.

Nevertheless, the risks are real and multifaceted. The Polymarket prediction platform currently estimates a 43% chance of a U.S. recession by the end of 2026, based on criteria such as two consecutive quarters of negative GDP growth or an official declaration by the National Bureau of Economic Research.

In conclusion, while the U.S. economy may continue to navigate “choppy waters,” the potential for a recession in 2026 is substantial. Policymakers must remain vigilant, balancing stimulus with fiscal discipline, and addressing structural weaknesses before temporary growth drivers fade.

The coming year will be pivotal in determining whether the U.S. can steer clear of recession or succumb to the mounting pressures.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on December 10, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

***

***

The Federal Reserve’s decision today to reduce the federal funds rate marks a pivotal moment in the central bank’s ongoing effort to navigate a complicated economic landscape. Under the leadership of Chair Jerome Powell, the Federal Open Market Committee voted to cut its benchmark interest rate by 25 basis points, bringing the target range down to 3.50%–3.75%. This move, the third rate cut of the year, reflects the Fed’s attempt to balance persistent inflation pressures with signs of weakening momentum in the labor market and broader economy.

Powell’s approach has been defined by caution, flexibility, and a willingness to adjust policy as new data emerges. Today’s cut underscores that philosophy. Although inflation has eased from its peak, it remains elevated enough to warrant vigilance. At the same time, job growth has slowed, and several indicators point to cooling demand. By trimming rates, the Fed aims to support economic activity without reigniting the inflationary surge that dominated the previous two years.

The decision was not without internal debate. Members of the committee were divided, with some arguing that further easing risks undermining progress on inflation, while others warned that failing to act could deepen labor‑market weakness. Powell acknowledged these tensions in his remarks, emphasizing that there is “no risk‑free path” and that the committee must weigh competing risks carefully. His message suggested that while the Fed is open to additional cuts if conditions deteriorate, the bar for further action has risen now that rates are approaching what policymakers view as a neutral range.

Financial markets reacted swiftly. Equities rallied on expectations that lower borrowing costs will support corporate earnings and investment. Bond yields dipped as investors priced in a more accommodative policy stance. Yet the broader economic implications will unfold over time. For households, the cut may translate into slightly lower rates on mortgages, auto loans, and credit cards, offering modest relief. For businesses, cheaper financing could encourage expansion and hiring.

Today’s rate reduction highlights the delicate balancing act facing the Federal Reserve. Powell must steer the economy between the twin risks of inflation and recession, all while navigating political scrutiny and incomplete economic data. The latest move signals confidence that the economy can regain momentum without sacrificing price stability, but it also reflects the uncertainty that continues to shape monetary policy. As the year draws to a close, the Fed’s actions today will play a central role in shaping the economic trajectory of the months ahead.

Posted on November 21, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

BASIC DEFINITIONS

***

***

Money supply measures—M0, M1, M2, and M3—are essential tools used by economists and policymakers to assess liquidity, guide monetary policy, and understand economic health. Each measure reflects a different level of liquidity and plays a unique role in financial analysis.

The money supply refers to the total amount of monetary assets available in an economy at a specific time. It includes various forms of money, ranging from physical currency to more liquid financial instruments. To better understand and manage economic activity, central banks and economists categorize money into different measures based on liquidity: M0, M1, M2, and M3.

M0, also known as the monetary base or base money, includes all physical currency in circulation—coins and paper money—plus reserves held by commercial banks at the central bank. It represents the most liquid form of money and is directly controlled by the central bank through tools like open market operations and reserve requirements.

M1 builds on M0 by adding demand deposits (checking accounts) and other liquid deposits that can be quickly converted into cash. It includes:

Physical currency held by the public

Traveler’s checks

Demand deposits at commercial banks

M1 is a key indicator of immediate spending power in the economy. A rapid increase in M1 can signal rising consumer activity, while a decline may indicate tightening liquidity.

M2 expands further by including near-money assets—those that are not as liquid as M1 but can be converted into cash relatively easily. M2 includes:

All components of M1

Savings deposits

Money market securities

Certificates of deposit (under $100,000)

M2 is widely used by economists and the Federal Reserve to gauge intermediate-term economic trends. It reflects both spending and saving behavior, making it a critical tool for forecasting inflation and guiding interest rate decisions.

M3, though no longer published by the Federal Reserve since 2006, includes M2 plus large time deposits, institutional money market funds, and other larger liquid assets. M3 provides a broader view of the money supply, especially useful for analyzing long-term investment trends and credit expansion. Some countries, like the UK and India, still track M3 for macroeconomic planning.

These measures are not just academic—they have real-world implications. For instance, during the COVID-19 pandemic, the U.S. saw a historic surge in M2 due to stimulus payments and quantitative easing. This expansion raised concerns about future inflation, which materialized in subsequent years. Monitoring money supply helps central banks adjust monetary policy to maintain price stability and support economic growth.

In conclusion, money supply measures offer a layered view of liquidity in the economy, from the most liquid (M0) to broader aggregates (M3).

Understanding these categories helps policymakers, investors, and businesses anticipate economic shifts, manage inflation, and make informed financial decisions.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

BASIC DEFINITIONS

***

***

The velocity of money is a fundamental concept in macroeconomics that measures how quickly money circulates through the economy. It reflects the frequency with which a unit of currency is used to purchase goods and services within a given time period. This metric is crucial for understanding economic activity, inflation, and the effectiveness of monetary policy.

At its core, the velocity of money is calculated using the formula:

This equation shows how many times money turns over in the economy to support a given level of economic output. For example, if the GDP is $20 trillion and the money supply (say, M2) is $10 trillion, the velocity is 2—meaning each dollar is used twice in a year to purchase goods and services.

There are different measures of money supply used in this calculation, most commonly M1 and M2. M1 includes the most liquid forms of money, such as cash and checking deposits, while M2 includes M1 plus savings accounts and other near-money assets. The choice of which measure to use depends on the context and the specific economic analysis being conducted.

The velocity of money is influenced by several factors:

Consumer and business confidence: When people feel optimistic about the economy, they are more likely to spend rather than save, increasing velocity.

Interest rates: Higher interest rates can encourage saving and reduce spending, lowering velocity. Conversely, lower rates can stimulate borrowing and spending.

Inflation expectations: If people expect prices to rise, they may spend more quickly, increasing velocity.

Technological and structural changes: Innovations in digital payments and shifts in consumer behavior can also affect how quickly money moves.

Historically, the velocity of money has fluctuated with economic cycles. During periods of economic expansion, velocity tends to rise as spending increases. In contrast, during recessions or periods of uncertainty, velocity often falls as consumers and businesses hold onto cash. For instance, during the 2008 financial crisis and the early stages of the COVID-19 pandemic, velocity dropped sharply due to reduced consumer spending and increased saving.

In recent years, the U.S. has experienced persistently low velocity, even amid significant increases in the money supply. This phenomenon has puzzled economists and raised questions about the effectiveness of monetary policy. Despite aggressive stimulus measures, much of the new money has remained in savings or financial markets rather than circulating through the real economy.

Understanding the velocity of money is essential for policymakers. A low velocity may signal weak demand and justify expansionary fiscal or monetary policies. Conversely, a high velocity could indicate overheating and the need for tightening measures to prevent inflation.

In conclusion, the velocity of money is a dynamic indicator of economic vitality. It helps economists and central banks assess the flow of money, the strength of demand, and the potential for inflation.

While often overlooked by the public, it plays a vital role in shaping economic policy and understanding the broader health of the economy.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 12, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

Say’s Law, named after the French economist Jean‑Baptiste Say, is a foundational idea in classical economics. Often summarized as “supply creates its own demand,” the law suggests that the act of producing goods and services inherently generates the income necessary to purchase them. This principle shaped economic thought throughout the 19th century and continues to influence debates about markets, government intervention, and the causes of economic crises.

Origins and Meaning Jean‑Baptiste Say introduced his law in the early 1800s in his Treatise on Political Economy. He argued that production is the source of demand: when producers create goods, they pay wages, rents, and profits, which in turn become purchasing power. In this view, general overproduction is impossible because every supply of goods corresponds to an equivalent demand. If imbalances occur, they are temporary and limited to specific sectors, not the economy as a whole.

Core Principles Say’s Law rests on several assumptions:

Markets are self‑correcting: Any surplus in one area leads to adjustments in prices and production.

Money is neutral: It serves only as a medium of exchange, not as a driver of demand.

Production drives prosperity: Economic growth depends on increasing output, not stimulating consumption.

No long‑term unemployment: Since supply creates demand, workers displaced in one industry will eventually find employment elsewhere.

These ideas aligned with classical economists’ belief in minimal government intervention and the efficiency of free markets.

Influence on Classical Economics Say’s Law became a cornerstone of classical economics, reinforcing the belief that recessions or depressions were temporary and self‑correcting. Economists like David Ricardo and John Stuart Mill adopted versions of the law, using it to argue against policies aimed at stimulating demand. The law supported laissez‑faire approaches, suggesting that governments should avoid interfering with markets, as production itself would ensure economic balance.

Criticism and Keynesian Revolution Say’s Law faced its greatest challenge during the Great Depression of the 1930s. Widespread unemployment and idle factories contradicted the idea that supply automatically generates demand. John Maynard Keynes famously rejected Say’s Law in his General Theory of Employment, Interest, and Money (1936). Keynes argued that demand, not supply, drives economic activity. He showed that insufficient aggregate demand could lead to prolonged recessions, requiring government intervention through fiscal and monetary policies.

Keynes’s critique marked a turning point in economics. While Say’s Law emphasized production, Keynesian economics highlighted consumption and demand management. This shift reshaped economic policy, leading to active government roles in stabilizing economies.

Modern Perspectives Today, Say’s Law is not accepted in its original form, but elements of it remain relevant. Supply‑side economists, for example, argue that policies encouraging production—such as tax cuts and deregulation—can stimulate growth. In contrast, Keynesians stress the importance of demand management. The debate reflects a broader tension in economics: whether prosperity depends more on producing goods or ensuring people have the means and willingness to buy them.

Conclusion: Say’s Law was a bold attempt to explain the self‑sustaining nature of markets. While its claim that “supply creates its own demand” proved too simplistic in the face of modern economic realities, it remains a vital part of the history of economic thought. The controversy surrounding Say’s Law highlights the evolving nature of economics, where theories are tested against real‑world crises and adapted to new circumstances. Even today, discussions of supply‑side versus demand‑side policies echo the enduring influence of Say’s original insight.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 10, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

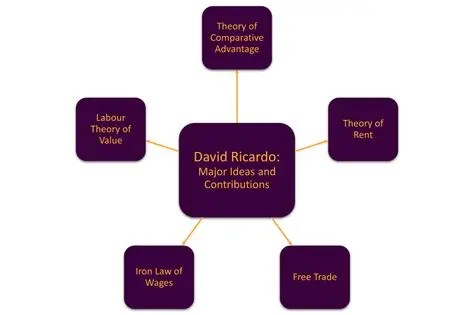

Ricardian economics, rooted in the theories of 19th-century economist David Ricardo, emphasizes comparative advantage, free trade, and the neutrality of government debt—most notably through the concept of Ricardian equivalence. While these ideas have shaped macroeconomic thought, their relevance to medicine and healthcare policy is less direct. Still, exploring Ricardian principles offers a provocative lens through which to examine the fiscal sustainability and efficiency of modern healthcare systems.

At the heart of Ricardian equivalence is the idea that consumers are forward-looking and internalize government budget constraints. If a government finances healthcare through debt rather than taxes, rational agents will anticipate future tax burdens and adjust their behavior accordingly. In theory, this undermines the effectiveness of deficit-financed healthcare spending as a stimulus. Applied to medicine, this suggests that long-term fiscal responsibility is crucial: expanding healthcare access through borrowing may not yield the intended economic or health benefits if citizens expect future costs to rise.

This insight could inform debates on healthcare reform, especially in countries grappling with ballooning medical expenditures. Ricardian economics warns against short-term fixes that ignore long-term fiscal implications. For example, expanding public insurance programs without sustainable funding mechanisms could lead to intergenerational inequities and economic distortions. Policymakers might instead focus on reforms that align incentives, reduce waste, and promote cost-effective care—principles that resonate with Ricardo’s emphasis on efficiency and comparative advantage.

***

***

However, Ricardian economics offers limited guidance on the unique moral and practical dimensions of medicine. Healthcare is not a typical market good. Patients often lack the information or autonomy to make rational choices, especially in emergencies. Moreover, the sector is rife with externalities: one person’s vaccination benefits the broader community, and untreated illness can strain public resources. These complexities challenge the assumption of rational, forward-looking behavior central to Ricardian equivalence.

Additionally, Ricardo’s theory of comparative advantage—where nations benefit by specializing in goods they produce most efficiently—has implications for global health. It supports international collaboration in pharmaceutical production, medical research, and telemedicine. Yet, over-reliance on global supply chains can expose vulnerabilities, as seen during the COVID-19 pandemic when countries faced shortages of critical medical supplies.

In conclusion, Ricardian economics provides valuable fiscal insights that can inform healthcare policy, particularly regarding debt sustainability and efficient resource allocation. Its emphasis on long-term planning and comparative advantage can guide reforms that make medicine more resilient and cost-effective. However, the theory’s assumptions about rational behavior and market dynamics limit its applicability to the nuanced realities of healthcare. Medicine requires not just economic efficiency but ethical considerations, equity, and compassion—areas where Ricardian economics falls short. Thus, while it can contribute to the conversation, it cannot “save” medicine alone.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

The NASDAQ, short for the National Association of Securities Dealers Automated Quotations, is one of the largest and most influential stock exchanges in the world. Founded in 1971, it was the first electronic stock market, revolutionizing how securities were traded by replacing traditional floor-based systems with computerized trading platforms. This innovation made transactions faster, more transparent, and accessible to a broader range of investors.

Unlike the New York Stock Exchange (NYSE), which historically operated through physical trading floors, the NASDAQ is entirely virtual. It connects buyers and sellers through a sophisticated network of computers, allowing for rapid execution of trades. This digital-first approach has made it particularly attractive to technology companies and growth-oriented firms, earning it a reputation as the go-to exchange for innovative and high-tech businesses.

Companies Listed on the NASDAQ The NASDAQ is home to some of the most prominent and influential companies in the world. Giants like Apple, Microsoft, Amazon, Google (Alphabet), Meta (formerly Facebook), and Tesla all trade on the NASDAQ. These companies are part of the NASDAQ-100, an index that tracks the performance of the 100 largest non-financial companies listed on the exchange. The NASDAQ Composite Index, which includes over 3,000 stocks, provides a broader snapshot of the market’s overall health and direction.

How It Works The NASDAQ operates as a dealer’s market, meaning transactions are facilitated by market makers—firms that stand ready to buy or sell securities at publicly quoted prices. These market makers help maintain liquidity and ensure that trades can be executed efficiently. Prices are determined by supply and demand, and the electronic nature of the exchange allows for real-time updates and high-speed trading.