BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

A hedge fund is a limited partnership of private investors whose money is pooled and managed by professional fund managers. These managers use a wide range of strategies, including leverage (borrowed money) and the trading of nontraditional assets, to earn above-average investment returns. A hedge fund investment is often considered a risky, alternative investment choice and usually requires a high minimum investment or net worth. Hedge funds typically target wealthy investors.

***

The Hedge Fund manager I am considering is a Registered Investment Adviser [RIA]

QUESTION: What is a Registered Investment Advisor?

If the fund manager is an entity, then any individual you deal with will be a registered investment adviser representative. If the fund manager is an individual, then that individual is a registered investment adviser. In either case, the designation implies several steps have been taken.

In order to become a registered investment adviser, an individual must register for and pass the Series 65 Uniform Investment Adviser Law Exam, a three-hour, 130-question computer-based exam administered by the North American Securities Administrators Association. Topics covered include economics and analysis, investment vehicles, investment recommendations and strategies, and ethics and legal guidelines. A passing score is 70 percent or higher.

Once an individual has passed the Series 65, he or she must then apply via Form ADV to become a registered investment adviser. This application is made to either a state authority or to the SEC, depending on the adviser’s assets under management. If assets under management exceed $30 million, then the adviser must register with the SEC.

Form ADV consists of two parts. Part I provides general information to the regulatory authority. Part II is designed to be distributed to potential clients, and includes disclosure of a decent amount of information about the adviser. If the manager is a registered investment adviser, then you should expect to receive as part of the offering documentation either a current copy of Part II of the adviser’s Form ADV or a brochure that contains all the current information in Part II of Form ADV.

In addition to filing Form ADV and paying a small fee, the registered investment adviser becomes subject to extra administrative/regulatory burden as well as capital adequacy requirements that state the Adviser must maintain certain net worth levels.

By and large, because of the extra administrative burden as well as restrictions on certain activities, hedge fund managers attempt to avoid registering as investment advisers. Whether such managers can or cannot avoid such registration is largely dependent upon the state in which the manager operates. In California, for instance, hedge fund managers must register as investment advisers. In New York, such registration is not necessary. Not surprisingly, hedge fund managers located in California are rare, while they are quite plentiful in New York.

Posted on April 2, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Ann Miller RN MHA CPHQ CMP™

***

***

Finally … Fiduciary second investing and financial planning opinions right here!

Telephonic or electronic advice for medical professionals that is:

Objective, affordable, medically focused and financially personalized

Rendered by a pre-screened financial consultant for doctors and medical professionals

Offered on a pay-as-you-go basis, by phone or secure e-mail transmission

The iMBA Discussion Forum™ is a physician-to-financial advisor telephone or e-mail portal that connects independent financial professionals to doctors, nurses or healthcare executives desiring affordable and unbiased financial planning advice.

Medical professionals and healthcare executives can now receive direct access to pre-screened iMBA professionals in the areas of Investing, Financial Planning, Asset Allocation, Portfolio Management, Insurance, Mortgage and Lending, Human Resources, Retirement Planning and Employee Benefits. To assist our medical professional and healthcare executive members, we can be contracted with per-minute or per-project fees, and contacted by client phone, email or secure instant messaging.

A hedge fund is a limited partnership of private investors whose money is pooled and managed by professional fund managers. These managers use a wide range of strategies, including leverage (borrowed money) and the trading of nontraditional assets, to earn above-average investment returns. A hedge fund investment is often considered a risky, alternative investment choice and usually requires a high minimum investment or net worth. Hedge funds typically target wealthy investors.

QUESTION:Can I invest my Individual Retirement Account [IRA] in a Hedge Fund?

This is up to the manager, but there is no legal restriction on a hedge fund accepting individual retirement account (IRA) assets. IRA accounts are not well suited for funds that make extensive use of leverage, however. In such cases, the fund is likely to generate significant amounts of unrelated business taxable income (UBTI) – profits of the fund attributable to the use of leverage. The holder of an IRA account must pay taxes on UBTI, even if the UBTI was generated in an IRA account.

But, today’s hedge funds may or may not use leverage. Many hedge funds are not hedged at all, but rather are just specialized versions of regular long stock portfolios. If such funds do not use much leverage, IRA investors will not encounter much difficulty with UBTI and should not hesitate in considering these funds.

In considering whether to accept IRA money, hedge fund managers must consider several factors. If the only type of retirement money accepted by the hedge funds is IRA money, then the manager has no limit on how much retirement money the fund can accept. If, however, there are other types of retirement money invested in the fund, such as pension funds, IRA money will be counted towards a total of 25 percent of fund assets that can be invested in retirement accounts before the fund becomes subject to the Employment Retirement Income Security Act of 1974 (ERISA). Funds subject to ERISA regulations face a heavy administrative burden and more restrictions than most fund managers like.

Finally, IRA distributions from a hedge fund are subject to the standard 20 percent withholding unless the funds are directly rolled over to other qualified plans.

Suppose that in a new Accountable Care Organization [ACO] contract, a certain medical practice was awarded a new global payment or capitation styled contract that increased revenues by $100,000 for the next fiscal year. The practice had a gross margin of 35% that was not expected to change because of the new business. However, $10,000 was added to medical overhead expenses for another assistant and all Account’s Receivable (AR) are paid at the end of the year, upon completion of the contract.

Cost of Medical Services Provided (COMSP):

The Costs of Medical Services Provided (COMSP) for the ACO business contract represents the amount of money needed to service the patients provided by the contract. Since gross margin is 35% of revenues, the COMSP is 65% or $65,000. Adding the extra overhead results in $75,000 of new spending money (cash flow) needed to treat the patients. Therefore, divide the $75,000 total by the number of days the contract extends (one year) and realize the new contract requires about $ 205.50 per day of free cash flows.

Assumptions

Financial cash flow forecasting from operating activities allows a reasonable projection of future cash needs and enables the doctor to err on the side of fiscal prudence. It is an inexact science, by definition, and entails the following assumptions:

All income tax, salaries and Accounts Payable (AP) are paid at once.

Durable medical equipment inventory and pre-paid advertising remain constant.

Gains/losses on sale of equipment and depreciation expenses remain stable.

Gross margins remain constant.

The office is efficient so major new marginal costs will not be incurred.

***

***

Physician Reactions:

Since many physicians are still not entirely comfortable with global reimbursement, fixed payments, capitation or ACO reimbursement contracts; practices may be loath to turn away short-term business in the ACA era. Physician-executives must then determine other methods to generate the additional cash, which include the following general suggestions:

1. Extend Account’s Payable

Discuss your cash flow difficulties with vendors and emphasize their short-term nature. A doctor and her practice still has considerable cache’ value, especially in local communities, and many vendors are willing to work them to retain their business

2. Reduce Accounts Receivable

According to most cost surveys, about 30% of multi-specialty group’s accounts receivable (ARs) are unpaid at 120 days. In addition, multi-specialty groups are able to collect on only about 69% of charges. The rest was written off as bad debt expenses or as a result of discounted payments from Medicare and other managed care companies. In a study by Wisconsin based Zimmerman and Associates, the percentages of ARs unpaid at more than 90 days is now at an all time high of more than 40%. Therefore, multi-specialty groups should aim to keep the percentage of ARs unpaid for more than 120 days, down to less than 20% of the total practice. The safest place to be for a single specialty physician is probably in the 30-35% range as anything over that is just not affordable.

The slowest paid specialties (ARs greater than 120 days) are: multi-specialty group practices; family practices; cardiology groups; anesthesiology groups; and gastroenterologists, respectively. So work hard to get your money, faster. Factoring, or selling the ARs to a third party for an immediate discounted amount is not usually recommended.

3. Borrow with Short-Term Bridge Loans

Obtain a line of credit from your local bank, credit union or other private sources, if possible in an economically constrained environment. Beware the time value of money, personal loan guarantees, and onerous usury rates. Also, beware that lenders can reduce or eliminate credit lines to a medical practice, often at the most inopportune time.

4. Cut Expenses

While this is often possible, it has to be done without demoralizing the practice’s staff.

5. Reduce Supply Inventories

If prudently possible; remember things like minimal shipping fees, loss of revenue if you run short, etc.

6. Taxes

Do not stop paying withholding taxes in favor of cash flow because it is illegal.

Hyper-Growth Model:

Now, let us again suppose that the practice has attracted nine more similar medical contracts. If we multiple the above example tenfold, the serious nature of potential cash flow problem becomes apparent. In other words, the practice has increased revenues to one million dollars, with the same 35% margin, 65% COMSP and $100,000 increase in operating overhead expenses.

Using identical mathematical calculations, we determine that $750,000 / 365days equals $2,055.00 per day of needed new free cash flows! Hence, indiscriminate growth without careful contract evaluation and cash flow analysis is a prescription for potential financial disaster.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com

Posted on March 30, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Negativity bias is not totally separate from pessimism bias, but it is subtly and importantly distinct. In fact, it works according to similar mechanics as the sunk cost fallacy in that it reflects our profound aversion to losing. We like to win, but we hate to lose even more.

And so, according to cognitive scientist Mackenzie Marcinko PhD, when we make a decision, we generally think in terms of outcomes—either positive or negative. The bias comes into play when we irrationally weigh the potential for a negative outcome as more important than that of a positive outcome.

***

***

Pessimism bias on the other hand, is a cognitive bias that causes people to overestimate the likelihood of negative things and underestimate the likelihood of positive things, especially when it comes to assuming that future events will have a bad outcome.

For example, the pessimism bias could cause someone to believe that they’re going to fail an exam, even though they’re well-prepared and are likely to get a good grade.

According to colleague Dan Ariely PhD, The pessimism bias can distort people’s thinking, including your own, in a way that leads to irrational decision-making, as well as to various issues with your mental health and emotional well being.

Both median and average family net worth surged between 2019 and 2022, according to the U.S. Federal Reserve. Average net worth increased by 23% to $1,063,700, the Fed reported in October 2023, the most recent year it published the data. Median net worth, on the other hand, rose 37% over that same period to $192,900.

You might wonder why the average and median net worth figures are so different. That’s because when you take the average of something, you add together every value in a data set and then divide that figure by the number of individual values.

When calculating a median, you simply look at the middle figure within a data set. That said, an average figure can be significantly higher or lower than a median figure if there are extreme outliers – meaning a group of people with significantly more net worth than the rest of the group can bring the average higher.

Average Net Worth by Age

The average net worth of someone younger than 35 years old is $183,500, as of 2022. From there, average net worth steadily rises within each age bracket. Between 35 to 44, the average net worth is $549,600, while between 45 and 54, that number increases to $975,800. Average net worth surges above the $1 million mark between 55 to 64, reaching $1,566,900.

Average net worth again rises for those ages 65 to 74, to $1,794,600, before falling to $1,624,100 for the 75 and older group. The median net worth within every single age bracket, however, is much lower than the average net worth.

***

***

Physicians [MD/DO]Net Worth by Specialty

A 2023 Medscape report shows the top 10 specialties with the most survey respondents saying they are worth more than $5 million.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com

*** Several years ago we noted that far too many mid-career, mature and physician clients using traditional stock brokers, management consultants and “financial advisors”, seemed to be less successful than those who went it alone. These Do-it-Yourselfers [DIYs] had setbacks and made mistakes, for sure. But, the ME Inc,. doctors seemed to learn from their mistakes and did not incur the high management and service fees demanded from general or retail one-size-fits-all “advisors.”

In fact, an informal inverse related relationship was noted, and dubbed the “Doctor Effect.” In other words, the more consultants an individual doctor retained; the less well they did in all disciplines of the financial planning, professional portfolio and investing continuum.

Of course, the reason for this discrepancy eluded many of them as Wall Street brokerages and wire-houses flooded the media with messages, infomercials, print, radio, TV, texts, tweets, and internet ads to the contrary. Rather than self-learn the basics, the prevailing sentiment seemed to purse the holy grail of finding the “perfect financial advisor.” This realization was a confirmation of the industry culture which seemed to be: Bread for the advisor – Crumbs for the client!

And so, we at the the Institute of Medical Business Advisors Inc. (iMBA), and this Medical Executive-Post, formed a cadre’ of technology focused and highly educated doctors, financial advisors, attorneys, accountants, psychologists and educational visionaries who decided there must be a better way for their healthcare colleagues to receive financial planning advice, products and related management services within a culture of fiduciary responsibility.

We trust you agree with this ME Inc philosophy as illustrated in this free white paper available upon request.

PROFESSIONAL PORTFOLIO CONSTRUCTION [Investing Assets and their Management] Subscribe, Read, Like and Refer

Email whiote paper request here:MarcinkoAdvisors@outlook.com

Posted on March 16, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Vitaliy Katsenelson CFA

***

***

Today, I’m going to share stories about my best and worst investment decisions. But don’t worry, this isn’t just a brag-and-cringe session about making or losing money. These stories are about the valuable lessons learned, and how these adventures in investing helped shape my current approach.

The Best Investment Decision

In investing, you don’t get extra points for creativity or difficulty. A million dollars earned while you are smiling buys as many potatoes as a million dollars that cost you your marriage and hair.

However, from a personal, creative satisfaction perspective, our investment in Uber was one of our best. That’s not to say that it has been the most successful decision from a financial perspective, at least not yet.

Uber doesn’t fit into the traditional value stock category. Until 2023, the third year of our ownership, it never made money. It was a stock everyone hated. After we bought it, I had clients reach out to me asking if I had been kidnapped and someone else was making these purchases of Uber.

We bought more shares very opportunistically during and after the pandemic. I wrote a long research report on it, which you can read here.

On one hand, Uber’s switchboard is a digital business, but the company also has a physical presence in thousands of cities, which incurs costs (the analog side of the business). Additionally, the availability of cheap money caused the ride-share market to go crazy and act rationally irrational, as competitors jostled in a land grab.

My thesis consisted of several insights:

Unlike traditional-tech, digital-only companies, Uber is a hybrid, both digital and analog. Thus, its cost structure is much higher than that of other companies. This, in part, explains the higher losses.

It has a strong brand; its name has become a verb.

The rideshare market is inevitable and will only continue to grow. Uber is not just in competition with taxis, second cars, or seldomly used cars; it is also in competition with the favors we ask of friends and relatives, such as dropping us off at the mechanic or picking us up from the doctor’s office.

Uber has global scale, which its competitors lack, allowing it to spread R&D across more markets.

As its revenue grows, each incremental dollar comes with a very high margin, which directly drops to the bottom line. Therefore, at some point, its earnings will explode to the upside as fixed costs stop growing, allowing it to scale.

The Uber story is not over; we still own the stock. I don’t want to do a celebratory dance. But this idea came with a lot of creative satisfaction. There is another point of pride here. Despite our very tumultuous ownership of this stock, we remained rational (I have written about that here). We bought more when it became extremely undervalued, and I would be lying if I said that was psychologically easy – it was not, but we followed our research and process.

The Worst Investment Decision

My worst investments that resulted in losses had several things in common: They were low-quality companies; their financials were complex and not transparent (for instance, one-time items were labeled as “one-time” every quarter); and they had questionable management.

However, they were all considered “cheap”… until they were not. Now, I hope you see why I am dogmatic about quality.

However.

When you are wrong on an investment and you lose money, the most you can lose is 100%. I have learned a lot from those. But they were not my worst investments. Those were the ones where I left 300–400% on the table when I sold too soon. Let me detail two examples.

EA – Electronic Arts

We bought EA in the early 2010s. I wrote about it – you can read my investment case for it here. To sum up, games were moving from being sold in stores to being digital downloads, which would lead to higher margins (don’t have to pay for packaging and Best Buy to sell them). The market for games was exploding, as every adult and teenager had a gaming device in their hands – a smartphone. The market for video games was going to be much larger. EA was the largest player in that space, with great franchises.

The following two years of ownership were very painful. EA had a few big game flops, and the market did not care about improving fundamentals. The stock kept declining. We continued to buy more. Every time we bought more shares, the stock fell further. Fast-forward a year or two. The stock doubled from our original purchase, but I was mentally exhausted. I did a celebratory dance and sold the stock. The stock then went up another 4x within a few years after we sold it. It went up for the right reasons – its earnings exploded to the upside, in line with my original thesis.

The sale was a mistake, not because the price went up but because I let frustration over the stock-price decline (volatility) get to me. Investing is a mental game. I learned from this adventure that it is important to zoom out and not obsess over individual stocks in the portfolio. This is why we have a portfolio. It was a very costly but educational mistake. Our ownership of Uber was not a walk in the park, either – just look at the stock price over the last few years. But I had learned my lesson from EA and was able to do the analysis, update our model, and zoom out.

In investing, there is a big difference between intellectual and tactile knowledge. I am going to go PG-13 on you for a second and quote the irascible Charlie Munger: “Learning about investing through a model portfolio is like learning about sex through romantic novels.” A big part of investing is observing yourself as an investor – your thoughts and emotions as you ride the actual rollercoaster of owning a stock.

I also made an important modification to our process.

We always value every company in the portfolio on earnings (free cash flows) at least four years out. Why four years? Three seems too short. There is no magic in this number, other than it being longer than most analyst estimates. We do this for all stocks in the portfolio, and then the total return for each is calculated and annualized. If a company has strong growth potential, it may appear to be expensive based on current earnings; but in reality, it may actually be cheap based on earnings projected four years from now.

On the other side of the spectrum, a company that has no growth or dividends may seem “cheap” based on its current earnings multiple, but this cheapness may quickly dissipate once a total return is calculated using future earnings. Time is on the side of growing businesses and the enemy of the ones that stand still. Therefore, a non-growing or slow-growing business needs a much greater discount (margin of safety) to secure a spot in our portfolio.

I want to stress another point. We sometimes sell a stock and then it goes higher. If we sold it for the right fundamental reasons, this doesn’t bother me. There is very little to learn.

Twilio

I’ll give you another crazy example. We bought Twilio at $25 in 2017 or so. Our thesis was that they had built the largest digital telecommunications network, which gave them a brief competitive advantage. They were also spending 5x more on R&D than competitors to build applications around this network, which would give them long-term advantages.

The stock price went up to $60 in a few months without anything significantly changing, so we sold a third of our position. Then it went up to $90, and we sold some more. To our disbelief, we sold the rest at around $120, a bit before the pandemic.

During the pandemic, Twilio’s price hit $400. I had zero regret about not holding on to the shares. Absolutely none. Twilio’s profitability did not match the stock market’s opinion of its price. Twilio’s stock price was as crazy to me at $250 as it was at $300 or $400. After reviewing our models, we concluded that even $120 was at the extreme end of our optimistic assumptions. Fast-forward to today, where the stock is at $60 or so. We are currently sharpening our pencils, but we have not bought the stock – yet.

Selling EA was a mistake; selling Twilio was not.

***

Key takeaways

My “best investment decision” with Uber wasn’t just about financial gains, but the creative satisfaction it brought. It taught me the value of sticking to our research and process, even when it’s psychologically challenging.

The worst investments often share common traits: low-quality companies, complex financials, questionable management, and the illusion of being “cheap.” This reinforces my dogmatic stance on prioritizing quality.

Sometimes, the costliest mistakes aren’t the ones where you lose money, but those where you leave significant gains on the table by selling too soon. My experience with EA taught me this lesson the hard way.

There’s a crucial difference between intellectual and tactile knowledge in investing. Actually owning stocks and experiencing the emotional roller coaster is invaluable for developing as an investor.

Selling a stock that later increases in value isn’t always a mistake if the decision was based on sound fundamental reasons. My experience with Twilio illustrates this point – sometimes it’s right to sell even if the price continues to climb.

NOTE:Please read the following important disclosure here.

In the United States, the difference between a Ph.D and a Sc.D is that the former is awarded to most, if not all, disciplines, while a Sc.D is awarded to science or STEM (science, technology, engineering, mathematics) disciplines.

This means that, in the United States at least, a Ph.D and a Sc.D are equal to one another in terms of telling people about an individual’s mastery of a particular skill, training, and prestige. A Ph.D holder and a Sc.D holder are viewed as peers and equals by most, if not all, American universities.

Meanwhile in Europe, according to Emily Summer, the difference between a Ph.D and a Sc.D is that the former is awarded at the start of an academic career, while the Sc.D is awarded much later, after the individual has built up an impressive body of work.

Posted on March 7, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

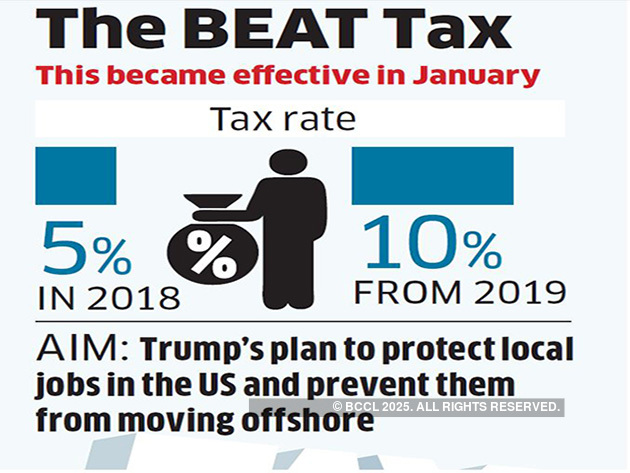

Base-Erosion Anti-Abuse Tax (BEAT): The 2017 tax reforms moved the U.S. from a worldwide taxation system to a quasi-territorial system, so foreign earnings are no longer included in a company’s domestic tax base.

To discourage companies operating in the U.S. from avoiding tax liability by shifting profits out of the country, Congress imposed a 10% minimum tax called Base-Erosion Anti-Abuse Tax (BEAT). The BEAT rate will increase from 10% to 12.5% in 2026.

As in the case of Declinism, to better understand the Forer effect (commonly known as the Barnum Effect), it’s helpful to acknowledge that people like their world to make sense. If it didn’t, we would have no pre-existing routine to fall back on and we’d have to think harder to contextualise new information.

Note: Phineas Taylor Barnum (July 5, 1810 – April 7, 1891) was an American showman, businessman, and politician remembered for promoting celebrated hoaxes and founding with Jim Bailey the Ringling Bros. and Barnum & Bailey Circus. He was also an author, publisher, and philanthropist although he said of himself: “I am a showman by profession … and all the gilding shall make nothing else of me.” According to Barnum’s critics, his personal aim was “to put money in his own coffers”. According to Wikipedia, the adage “there’s a sucker born every minute” has frequently been attributed to him, although no evidence exists that he had coined the phrase

With that, if there are gaps in our thinking of how we understand things, we will try to fill those gaps in with what we intuitively think makes sense, subsequently reinforcing our existing schema(s). As our minds make such connections to consolidate our own personal understanding of the world, it is easy to see how people can tend to process vague information and interpret it in a manner that makes it seem personal and specific to them. Given our egocentric nature (along with our desire for nice, neat little packages and patterns), when we process vague information, we hold on to what we deem meaningful to us and discard what is not. Simply, we better process information we think is specifically tailored to us, regardless of ambiguity.

More specifically, according to colleague Dan Ariely PhD, the Forer effect refers to the tendency for people to accept vague and general personality descriptions as uniquely applicable to themselves without realizing that the same description could be applied to just about everyone else (Forer, 1949). For example, when people read their horoscope, even vague, general information can seem like it’s advising something relevant and specific to them.

Remember, we make thousands of decisions every day, some more important than others. Make sure that the ones that do matter are not made based on bias, but rather on reflective judgment and critical thinking.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

If the definition of a security is title to a stream of cash flows, then the dividends a company is expected to pay to equity shareholders on a periodic basis (e.g., quarterly) are a clear source of return for an investor. A dividend is simply a distribution of (some portion of) the company’s earnings to equity shareholders. Like a bond yield, a stock’s dividend yield can be used to measure the income return on the stock.

To determine a stock’s dividend yield, the trailing year’s dividends per share paid are divided by the current stock price. However, a key difference between a dividend yield and a bond yield is the level of certainty that can be assumed regarding future payments, since a bond’s coupon is generally predetermined and its payment is expected to be senior to the payment of dividends.

After a company has determined that it has earned a profit, management has to decide what to do with those profits. One choice is to distribute the earnings to shareholders in the form of dividends, while another option is to reinvest the profits in the company. A company’s management may determine that the shareholders interest is best served by using the earnings to pursue growth opportunities (e.g., capital expansion, research & development, etc.) at the corporate level. Thus, when management believes that its investment opportunities are likely to produce a higher return than what investors’ could generate with their dividends or that reinvestment is needed to maintain its financial strength, the company will retain the earnings.

One of the biggest myths in investing is capital appreciation accounts for the largest part of investors’ gains. Dividends, or cash payments to shareholders, actually account for a substantial part of an equity investor’s total return. In fact since 1926, dividends have accounted for more than 40% of the total return of the S&P 500 stock index. In the last decade (2000-2009), the S&P 500’s total return of -9% would have been a heftier loss of -24% had it not been for the 15% contribution from dividends.

History has shown that dividends have been a powerful source of total return in a diversified investment portfolio, especially during periods of market turbulence. In examining the prior eight decades of stock market performance, dividends often account for more than 2/3 of the total return (1930s, 1940s, 1970s, & 2000s). If an investor avoided dividend paying stocks during these elongated time periods, most of the total gains would be lost.

***

DIVIDEND CONTRIBUTION OF S&P 500 RETURN BY DECADE

S&P 500

Cumulative

Dividends

Average

Price %

Dividend

Total

% of Total

Payout

Years

Change

Contribution*

Return

Return

Ratio**

1930s

-41.9%

56.0%

14.1%

>100%

90.1%

1940s

34.8%

100.3%

135.0%

74.3%

59.4%

1950s

256.7%

180.0%

436.7%

41.2%

54.6%

1960s

53.7%

54.2%

107.9%

50.2%

56.0%

1970s

17.2%

59.1%

76.4%

77.4%

45.5%

1980s

227.4%

143.1%

370.5%

38.6%

48.6%

1990s

315.7%

117.1%

432.8%

27.0%

47.6%

2000s

-24.1%

15.0%

-9.1%

>100%

35.3%

2010s

27.9%

8.4%

36.3%

23.1%

28.4%

as of 12/31/12

Source: Strategas

During those decades such as the 2000s where the stock market struggled to advance, dividends were a significant element for investor survival. This is not only due to the dividends alone, but also the risk element of stocks that pay dividends. Dividend stocks have historically provided lower overall volatility and stronger downside protection when markets decline. Since 1927, dividend stocks have consistently held up better than the broader market during downturns. You can measure downside risk through a statistic known as downside capture ratio.

Downside capture ratio is a statistical measure of overall performance in a down stock market. An investment category, or investment manager, who has a down-market ratio less than 100 has outperformed the index during a falling stock market.

For example, a down-market capture ratio of 80 indicates that the portfolio measure declined only 80% as much as the index during the period. The downside capture ratio of high-dividend-yielding stocks, since 1927, has been 81% or lower over various long-term periods. Put a better way, during months that the S&P 500 stock index fell, dividend stocks declined by nearly 19% less than the broader market.

***

DOWNSIDE AND UPSIDE CAPTURE RATIOS OF HIGH DIVIDEND STOCKS – 1927 TO 2011

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com

Posted on February 19, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

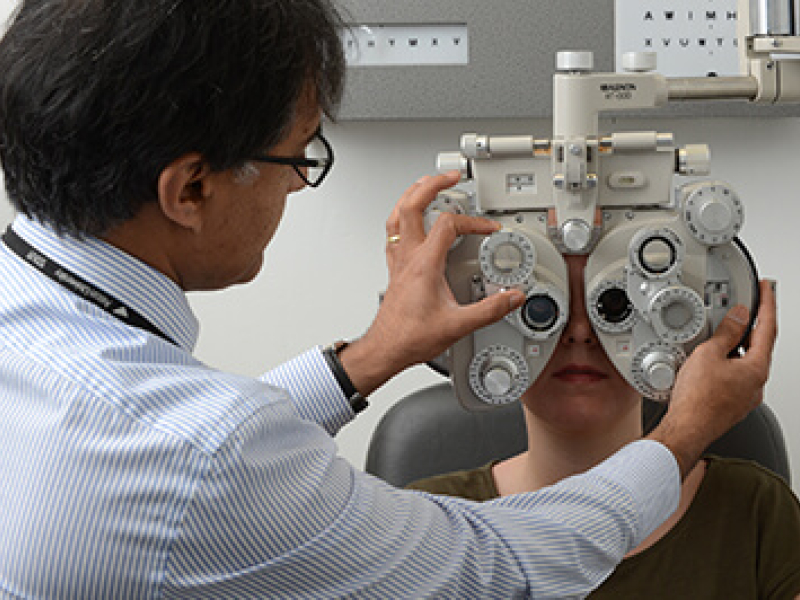

Optometry Doctor [OD]: An optometrist has an Optometry Doctor (OD) degree and can assess overall eye health and the quality of a person’s vision through a comprehensive examination. They diagnose and treat many eye disorders that do not require surgery or further specialized care. An optometrist can also identify symptoms of other health conditions that may affect the eyes, such as diabetes. Some also specialize in a field like pediatric care.

Optometrists [OD] and ophthalmologists [MD/DO] are both eye doctors, but they have different types of training and areas of expertise. If you need an eye exam—and think you may need glasses or contact lenses—an optometrist is a good first choice. To become an optometrist, a person needs to complete four years of additional education after a bachelor’s degree. Sometimes they complete a residency as well.

Now, ODs are licensed doctors and can prescribe medication. However, optometrists have a defined scope of practice that that revolves largely around the eyes. Optometrists can not prescribe all the same medications that your family doctor or ophthalmologist can.

So, if your eye issue requires surgery, or for specific conditions related to your eyes or overall health, you’ll want to visit an ophthalmologist [MD/DO].

On average, an optometrist in the U.S. makes about $131,860 per year, according to 2023 statistics.

Posted on February 16, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

***

INFLUENCERS

Reach Industry Pros, Executives and Decision-Makers with Ease!

Thank you for your interest in advertising on, or sponsoring the ME-P, the web’s only site integrating medical practice management with personal financial planning for all industry professionals.

Why should your company sponsor or advertise on the ME-P?

• Reader loyalty. Not only does the ME-P receive a mind-boggling number of page views and visits each month, its readers are loyal. • Reader stature. ME-P readers are experienced industry pros, executives and decision-makers. • Selective advertising. The ME-P is a free read that’s off the radar of the big-ad companies. Your ad here stands out as personal and different. • Supporting the ME-P makes a big difference and costs only a fraction of other online publications with far fewer readers. • Cost. CPM is reasonable and low compared to other sites.

E-mail us for a full packet, but give a look to these results from the ME-P’s annual reader survey:

* 89% of readers said the ME-P influences their perception of products and companies * 34% said that ME-P sponsorship alone give them a higher interest or appreciation for those companies * 754% said the ME-P has some, a good bit, or a lot of industry influence

Contact me and I’ll e-mail you a rate card. Your support makes a difference!

Posted on February 9, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

ACADEMIC DEFINITIONS

By Staff Reporters

***

***

What Is a PhD?

A PhD is a doctorate degree and is the highest postgraduate qualification awarded by universities. It involves undertaking original research in a narrow subject field and typically takes 4 years to complete.

A PhD in Business Administration provides an individual with a specialized and research-based background for a topic in the business management field. This is one of the key reasons it’s sought after by those who wish to work in business-related academia or research.

What Is a DBA?

A Doctor of Business Administration (DBA) is a business-orientated professional doctorate. Like a PhD, it is the highest-level postgraduate qualification which you can obtain from a university.

The degree program focuses on providing practical and innovative business management knowledge which can apply to any workplace. DBAs are designed for experienced practitioners such as senior managers, consultants and entrepreneurs who want to further their practical abilities.

This form of doctorate was first introduced as a way of allowing a distinction to be made between experienced practitioners and expert practitioners. The doctorate is an equal alternative to a traditional PhD and is an advanced follow-up for a Master’s in Business Administration (MBA).

Is a DBA and PhD Equivalent?

A Doctor of Business Administration (DBA) is equivalent to a Doctor of Philosophy (PhD); however, there are fundamental differences between these two doctoral degrees. These differences are nearly always at the center of DBA vs PhD discussions, and they stem from the intended career path of the student following their degree.

A PhD focuses on the ‘theory’ underpinning business management, whereas a DBA focuses on the ‘practical’ concepts. Those who complete a PhD in business management usually do so as they wish to pursue a career in research or academia. Those who complete a DBA do so as they want to pursue a more advanced role in the business industry or within their organization.

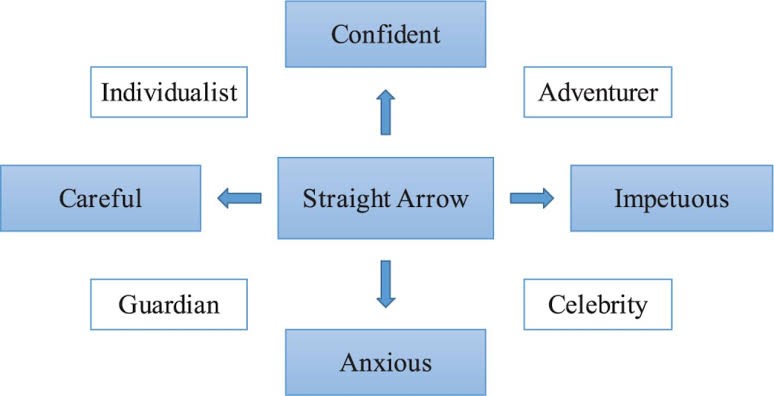

Fund managers Tom Bailard, Larry Biehl and Ron Kaiser identified five types of investors, each type characterized by their investment preferences and actions. These 5 types are: Individualists, Adventurers, Celebrities, Guardians and Straight Arrows. Key to the different categories is their different attitude to seeking professional financial advice. Defined below:

Individualists have faith in their own investment abilities so do not approach a financial adviser. But they are also cautious.

Adventurers are what may be called high rollers, in that they like big bets, tend not to diversify and are happy to put all their eggs in one basket. They, too, are unlikely to seek financial advice.

Celebrities tend to follow the crowd in investment terms but are aware of their lack of expertise so frequently consult advisers.

Guardians are fearful of losing money, thus prefer rock-solid investments such as government bonds. They, too, are likely to seek professional investment advice.

Straight Arrows exhibit some of the characteristics of individualists and some of adventurers.

Posted on February 5, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITION

By Staff Reporters ***

***

Naturopathic Doctors are educated and trained in accredited naturopathic medical colleges. They diagnose, prevent, and treat acute and chronic illness to restore and establish optimal health by supporting the person’s inherent self-healing process.

Rather than just suppressing symptoms, naturopathic doctors work to identify underlying causes of illness, and develop personalized treatment plans to address them. Their Therapeutic Order™, identifies the natural order in which all therapies should be applied to provide the greatest benefit with the least potential for damage.

Posted on January 31, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

In the first days of his second (nonconsecutive) presidential term, Donald Trump and his administration took a number of actions that will affect the healthcare industry in the near- and long-term. Further, the Trump Administration is reportedly poised to take a number of additional actions to pause, end, or otherwise change Biden-era initiatives.

Meanwhile, President Trump’s cabinet pick for the Department of Health & Human Services (HHS) hangs in the balance. This Health Capital Topics article reviews the new administration’s actions impacting the healthcare industry as of the date of publication. (Read more...)

Posted on January 28, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

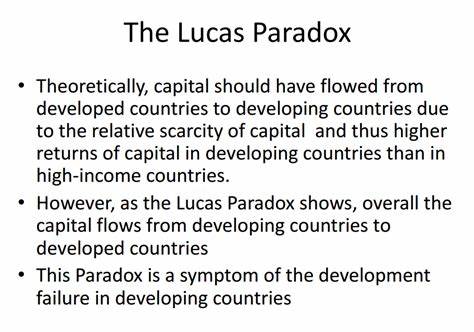

Capital is not flowing from developed countries to developing countries despite the fact that developing countries have lower levels of capital per worker, and therefore higher returns to capital.

Classical economic theory predicts that capital should flow from rich countries to poor countries, due to the effect of diminishing returns of capital. Poor countries have lower levels of capital per worker – which explains, in part, why they are poor. In poor countries, the scarcity of capital relative to labor should mean that the returns related to the infusion of capital are higher than in developed countries.

In response, savers in rich countries should look at poor countries as profitable places in which to invest. In reality, things do not seem to work that way. Surprisingly little capital flows from rich countries to poor countries.

This puzzle, famously discussed in a paper by Robert Lucas in 1990, is often referred to as the “Lucas Paradox”.

Posted on January 26, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Cognitive Dissonance is the discomfort experienced when holding conflicting cognitions, like believing in healthy eating while munching on a doghnut. It’s a mental tug-of-war that makes us squirm.

To reduce this discomfort according to colleague Dan Ariely PhD, we often change our beliefs or behaviors to align them. This is why smokers might downplay the health risks of smoking. Understanding cognitive dissonance helps us recognize these mental gymnastics and strive for consistency in our beliefs and actions.

So, next time you feel that mental itch, it’s cognitive dissonance asking for some resolution.

Posted on January 24, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Nash equilibrium, in game theory, is an outcome in a noncooperative game for two or more players in which no player’s expected outcome can be improved by changing one’s own strategy.

The Nash equilibrium is a key concept in game theory, in which it defines the solution of N-player non-cooperative games. It is named for American mathematician John Nash, who was awarded the 1994 Nobel Prize for Economics for his contributions to game theory.

MBA is the common abbreviation for a Master of Business Administration degree, and recipients typically stop attending school after receiving it.

However, those who are interested in conducting business research may decide to pursue a doctorate in business or management. Such students can earn a Ph.D. or a Doctor of Business Administration degree, commonly known as a DBA.

What ‘MSHA’ Stands For?

Master of Health Administration (MHA) and Master of Science in Health Administration (MSHA) are largely equivalent designations for degree programs that focus primarily on leadership and management of hospitals, healthcare organizations, and businesses that operate in the healthcare sector.

In contrast, an MBA in Health Administration is a Master of Business Administration degree program with a concentration, track, or specialization that provides students with several courses in topics specific to healthcare management and administration. Most of the coursework in an MBA program is devoted to general training in business functions, such as accounting, finance, logistics, marketing, personnel and project management.

MHA and MHSA programs devote all or most of their curriculum to studying the healthcare system, healthcare policy, and the application of business principles in the field of healthcare. MBA in Healthcare Administration programs devote only a portion of their curricula to topics specific to the healthcare sector.

MBBS Degree [Bachelor of Medicine, Bachelor of Surgery]

The MBBS is usually a five-year undergraduate degree that medical students complete when they want to become doctors. However, some programs take six years to complete because the institution expects you to earn a Bachelor of Science (BSc) in your training.

By the time a student applies to a medical program, they have likely taken several foundational science courses as part of their high school (or secondary) education. For example, medical applicants in the United Kingdom are often expected to show high scores on their General Certificate of Secondary Education (GCSE) and A-levels.

Earning an MBBS means that students are certified to care for patients as junior physicians without specialized training. Graduates are expected to complete two years of additional training, which rotates them through different specialties. Once they identify a specialty they like, they can apply for additional training, which can take anywhere between three and eight years.

MD Degree [Doctor of Medicine]

The acronym “MD” stands for the Latin term “Medicinae Doctor,” which translates to “Doctor of Medicine” in English.

It refers to the title that students from the United States of America obtain after finishing medical school. Some countries consider the “MD” title a postgraduate doctoral degree that MBBS graduates can obtain with additional years of training.

The CPA and CMA designations cater to distinct professional focuses within the accounting and finance fields. A CPA is often seen as the gold standard for public accounting, emphasizing auditing, tax, and regulatory compliance. This certification is highly regarded for roles that require a deep understanding of financial reporting and external auditing. CPAs are frequently employed by public accounting firms, government agencies, and corporations that need to ensure their financial statements adhere to strict regulatory standards.

On the other hand, the CMA designation is tailored for professionals who aim to excel in management accounting and strategic financial management. CMAs are trained to analyze financial data to inform business decisions, focusing on internal processes and performance management. This makes the CMA particularly valuable for roles in corporate finance, strategic planning, and management consulting. Companies looking to optimize their internal financial operations and drive business strategy often seek out CMAs for their expertise in cost management, budgeting, and financial analysis.

The educational and experiential requirements for these certifications also differ. To become a CPA, candidates typically need to complete 150 semester hours of college education, which often includes a bachelor’s degree in accounting or a related field. Additionally, CPAs must pass the Uniform CPA Examination and meet specific state licensing requirements, which usually include a certain amount of professional experience.

In contrast, the CMA certification requires a bachelor’s degree in any discipline, two years of relevant work experience, and passing the two-part CMA exam. This flexibility in educational background can make the CMA more accessible to a broader range of professionals.

The Bloomberg U.S. Universal Index represents the union of the U.S. Aggregate Index, U.S. Corporate High Yield Index, Investment Grade 144A Index, Eurodollar Index, U.S. Emerging Markets Index, and the non-ERISA eligible portion of the CMBS Index.

The index covers USD-denominated, taxable bonds that are rated either investment grade or high-yield. Some Bloomberg U.S. Universal Index constituents may be eligible for one or more of its contributing sub-components that are not mutually exclusive. These securities are not double-counted in the index.

The Bloomberg U.S. Universal Index was created on January 1st, 1999, with index history back-filled to January 1st, 1990.

A Junk Rally is a general trend of out performance by companies that tend to score poorly along several dimensions, such as price-to-earnings (P/E) ratios, return on assets (ROA), balance sheet strength, levels of debt and volatility.

Posted on January 10, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

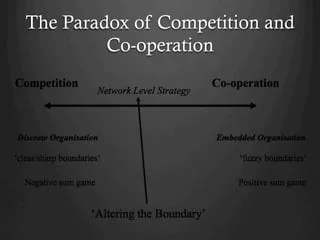

Definition of the Paradox of Competition

The Paradox of Competition refers to the complex and often counterintuitive effects competitive behaviors can have within markets and industries. Generally, competition is seen as a positive force that drives innovation, lowers prices, and improves quality and choice for consumers. However, the paradox lies in the fact that intense competition can sometimes lead to negative outcomes, such as diminished profitability for companies, reduced incentives to innovate, and the potential for a race to the bottom in terms of quality and sustainability.

According to colleague Dan Ariely PhD, understanding the nuances of the Paradox of Competition reveals the complexity of market dynamics and the importance of strategic, informed approaches to competition, both from businesses and regulators.

This paradox challenges the conventional wisdom that competition is universally beneficial, highlighting the need for a more nuanced view of how competitive forces shape markets and societies.

Posted on January 5, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Morality Priming refers to subtle reminders of ethical principles that can make us behave more responsibly. It’s like an internal nudge that brings our conscience to the surface.

And, according to colleague Dan Ariely PhD, by focusing on moral standards, people are often encouraged to act more honestly, even in small, everyday decisions.

Posted on January 3, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

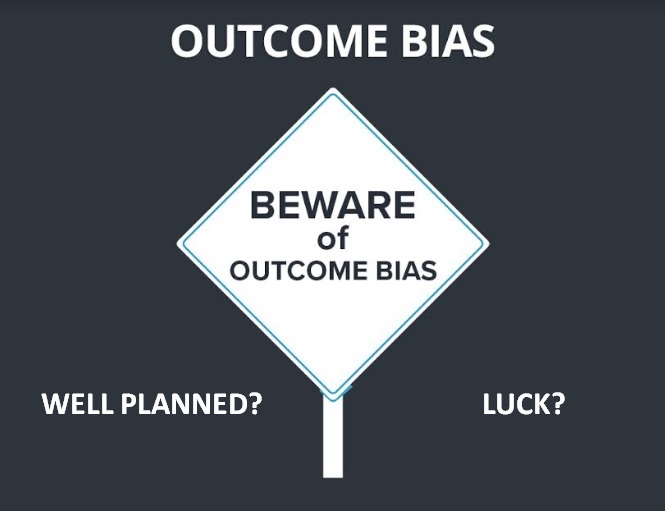

Outcome bias is judging a decision based on its result rather than the quality of the decision at the time it was made.

It’s like saying a bad poker play was smart because you won the hand. Or, a bad stock picker or financial advisor was good because the price went up!

According to psychologist and colleague Dan Ariely PhD, this bias ignores the process and focuses solely on the outcome. It’s why we celebrate lucky breaks and criticize thoughtful risks that didn’t pan out.

So, the next time you’re evaluating a decision, focus on the reasoning behind it, not just the end result.

Posted on December 31, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The Li Keqiang Index was created in 2010 by The Economist and measure’s China’s economy using three indicators: railway cargo volume, electricity consumption and bank loans.

The index is seen as an alternative to official gross domestic product numbers released by the Chinese government.

Posted on December 29, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS!

Former President Jimmy Carter has died at the age of 100.

The 39th president of the United States was a Georgia peanut farmer who sought to restore trust in government when he assumed the presidency in 1977 and then built a reputation for tireless work as a humanitarian.

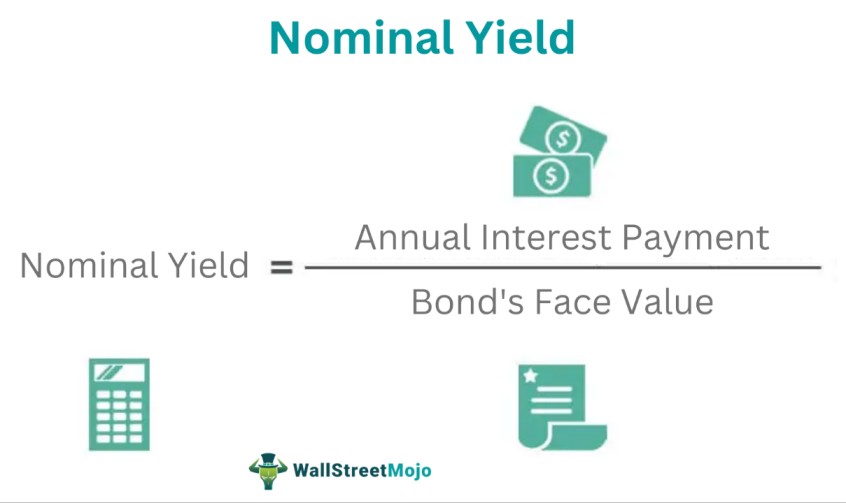

Nominal yield, for most bonds and other fixed-income securities, is simply the yield you see listed online or in newspapers. Most nominal fixed-income yields include some extra yield, an “inflation premium,” that is typically priced/added into the yields to help offset the effects of inflation.

Real yields, such as those for TIPS, don’t have the inflation premium. As a result, nominal yields are typically higher than TIPS yields and other real yields.

Posted on December 23, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA

[CEO – iMBA Inc]

To Our ME-P Subscribers, iMBA Inc., Clients and Friends

As we look forward to sharing the holidays with family and friends, we also remember those less fortunate.

And, as has been our practice in recent years, rather than sending holiday greeting cards, the iMBA Inc will provide support to several charities dedicated to helping those in need.

We hope this gesture provides happier holidays for others and serves to express our gratitude to you, in the spirit of the season, for your continued support and loyalty to this ME-P.

Happy New Year 2024

We also extend our hope that the New Year 2022 brings you and your loved ones good health, happiness and a world that comes to know peace and understanding.

***

***

Channel Surfing the ME-P

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Choice Overload is the difficulty in making a decision when faced with too many options. It’s like standing in front of an ice cream counter with 31 flavors and feeling paralyzed.

Among personal decision-makers, a prevention focus is activated and people are more satisfied with their choices after choosing among few options compared to many options, i.e. choice overload. However, individuals can also experience a reverse choice overload effect when acting as proxy decision-maker, too.

It is widely accepted that having more choices is inherently positive. When there are more available options from which to choose, an individual is more likely to be able to select the particular option that is the best fit and most likely to satisfy them. Choice is typically thought to be related to personal freedom and enhanced well-being.

Therefore, according to colleague Neal Baum MD, for most individuals the ultimate goal is to constantly maximize their choices in life to increase their overall satisfaction and well-being. The decision-making process, however, is a complex cognitive task that does not always lead to positive outcomes.

Thus, while having options is generally good, too many choices can lead to anxiety and decision fatigue. This is why curated selections and recommendations are so popular – they simplify the decision-making process’ according to another colleague Dan Ariely PhD.

So, when you’re overwhelmed by choices, narrow them down to a manageable number and make your decision easier.

Posted on December 21, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Ann Miller RN MHACMP™

INTRODUCING OUR NEXT GENERATION e-BOOK LIBRARYFROM iMBA, Inc.

An e-book is an electronic or digital book that can be read on a computer or a handheld device.

Our new e-books consists of text, images, and are fixed to a specific spot on the page.

And, our e-books are a data files similar in content and structure to a word-processing document that comes in a PDF format. To use our e-books, you need to purchase and download it to a device that has a .pdf file reader app, such as ADOBE® or similar on a smartphone, tablet or computer. A PDF, also known as a portable document format, is the format most people are familiar with and used in our e-books. PDFs are known for their ease of use and ability to hold custom layouts. They are the most commonly used e-Book formats, especially by professionals and adult-learners.

You can then access the e-book and read it, or highlight pages and even take side notes.

e-Books Save Money

With no manufacturing, printing, binding or shipping costs, e-Books are cheaper than traditional hard or paper back books.The price of each specialized and highly niche focused e-Book [50-100 pages] is only $25, whereas similar paperback printed books of this type generally cost $145, or more!

The breakeven inflation rate is the difference between the nominal yield (usually the market yield, which includes an inflation premium) on a fixed-income investment and the real yield (with no inflation premium) on an inflation-linked investment of similar maturity and credit quality.

So, if inflation averages more than the breakeven rate, the inflation-linked investment will outperform the investment with the nominal yield.

Conversely, if inflation averages below the breakeven rate, the investment with the nominal yield will outperform the inflation-linked investment.

Breakeven inflation rates are also considered useful measures of inflation expectations—higher breakeven rates represent higher inflation expectations (and higher relative prices for inflation-linked investments), while lower breakeven rates represent lower inflation expectations (and lower relative prices for inflation-linked investments).

Therefore, ideally, investors want to purchase inflation-linked investments when breakeven rates are relatively low because that’s typically when prices are also relatively low.

Commodities: Commodities are raw materials or primary agricultural products that can be bought or sold on an exchange or market. Examples include grains such as corn, foods such as coffee, and metals such as copper.

Commodity Futures: Agreements to buy or sell a specific amount of a commodity or financial instrument at a particular price on a stipulated future date related to basic raw materials such as precious metals and natural resources.

Commodity Intensity: Commodity intensity refers to commodity usage per unit of economic growth. An emerging, more manufacturing-based economy will usually be more commodity intensive in terms of its growth than will a more developed, service-oriented economy.

The Rule of 20 is a dimensionless number that adds the current 12-month trailing Price to Earnings Ratio to the annual change in an index of the annual consumer inflation rate. A reading below 20, while a market is trending lower, means that we could be near a bottom.

In the United States, the most common index used is the broad-based S&P 500, and CPI-U is used as a proxy for inflation.

The Rule of 20 is purportedly a rule from Peter Lynch. In chapter 39 of Graham and Dodd’s seminal Security Analysis, they mention: “We would suggest that about 20 times average earnings is as high a price as can be paid in an investment purchase of a common stock” … with no mention of inflation.

Lynch’s formulation attempts to factor the ‘gravity’ of interest rates into the fair value of a stock. And, as you can see, the measure has fluctuated quite a bit. However, it has returned to roughly the 20 level repeatedly.

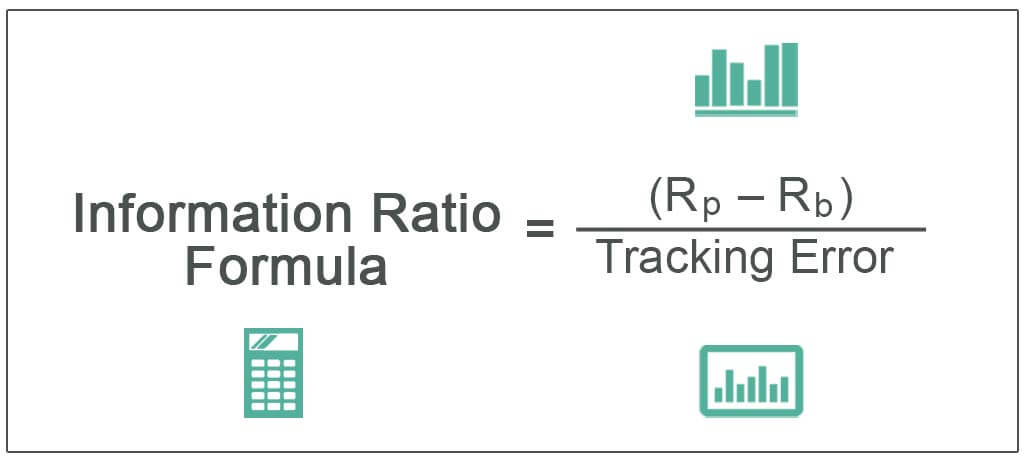

The Information Ratio (IR) is a risk-adjusted rate of return measure for comparing the performance of active investment managers over time. Its purpose is to help determine how much return an active portfolio manager has added per unit of active management risk.

Think of IR as a Sharpe Ratiofor active investment management; the IR is more focused than the Sharpe Ratio. Starting with the Sharpe Ratio’s formula, if we replace the excess return in the numerator with a portfolio’s active return (the average annualized return of an actively managed portfolio minus the average annualized return of the portfolio’s benchmark over a given period, adjusted for the portfolio’s market risk exposure), and you replace the Sharpe Ratio’s standard deviation of excess returns in the denominator with the standard deviation of a portfolio’s active returns over the period, you have the IR.

While the Sharpe Ratio expresses the amount of excess return per unit of overall risk, the IR computes only the active management-driven (alpha) returns per unit of alpha-driven risk. And while the Sharpe Ratio’s excess returns are calculated with regard to what is considered to be a relatively risk-free asset, such as a U.S. Treasury bill, the IR’s active returns are calculated with regard to each portfolio’s specific market benchmark.

The higher the IR, the better. The IR should be measured over a meaningful period of time, typically at least three to five years. The IR is not perfect–it can be influenced by external factors such as changes in market volatility. The standard deviation of active returns in the IR’s denominator is called tracking error. Tracking error will tend to increase in volatile markets for even the best active managers.

Collateralized Mortgage Obligations (CMOs) are a form of securitized debt derived from mortgage-backed securities. It’s a form of derivative security. Like most MBS pass-through securities, CMOs are typically backed by pools of residential mortgages and their payments. But not all investors want to receive the monthly payments of principal and interest that “plain vanilla” MBS pass-throughs offer–some prefer just the principal, some prefer just the interest, or some want payments with other particular/special characteristics.

For them, the cash flows from MBS can be pooled and structured into many classes of CMOs with different maturities and payment schedules, creating securities with very specific characteristics and behaviors. These characteristics and behaviors can vary widely. Some CMOs can offer less risk than “plain-vanilla” MBS, or can help offset other forms of risk in a diversified portfolio, but others can be much more volatile.

CMOs typically have two or more bond classes, called tranches. Each tranche has its own expected maturity and cash flow pattern. The unique cash flow patterns of each CMO tranche allow investors to tailor their mortgage exposure to meet a range of investment objectives, since different classes can have different risk/return characteristics.

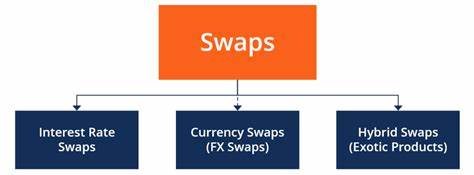

Swaps (a.k.a. swap agreements) are two-party contracts entered into primarily by institutional investors for periods ranging from a few weeks to more than one year.

In a standard “swap” transaction, two parties agree to exchange the returns (or differentials in rates of return) earned or realized on particular predetermined investments or instruments. The gross returns to be exchanged or “swapped” between the parties are generally calculated with respect to a “notional amount,” i.e., the return on or increase in value of a particular dollar amount invested at a particular interest rate, in a particular foreign currency, or in a “basket” of securities representing a particular index.

Forms of swap agreements include interestrate swaps (under which fixed- or floating-rate interest payments on a specific principal amount are exchanged) and total return swaps (under which one party agrees to pay the other the total return of a defined underlying asset in exchange for fee payments).

In addition, credit default swaps enable an investor to buy/sell protection against a credit event of a specific issuer. The seller of credit protection against a security or basket of securities receives an up-front or periodic payment to compensate against potential default(s).

Two years ago, prior to the 2022 election, mental health experts alerted the medical world to their version of an assessment scale for yet another new condition – “doomscrolling.”

As defined by the National Library of Medicine in the article, “Constant exposure to negative news on social media and news feeds could take the form of ‘doomscrolling’ which is commonly defined as a habit of scrolling through social media and news feeds where users obsessively seek for depressing and negative information.”

And so, formally Doomscrolling or doomsurfing is the act of spending an excessive amount of time reading large quantities of news, particularly negative news, on the web and social media. Doomscrolling can also be defined as the excessive consumption of short-form videos or social media content for an excessive period of time without stopping. The concept was coined around 2020, particularly in the context of the COVID pandemic.

Surveys and studies suggest doomscrolling is predominant among youth. It can be considered a form of internet addiction disorder. In 2019, a study by the National Academy of Sciences found that it can be linked to a decline in mental and physical health. Numerous reasons for doomscrolling have been cited, including negativity bias and FOMO [fear of missing out], and attempts at gaining control over uncertainty.

QUERY: What about the roaring stock market, post the 2024 presidential election. Fundamental analysis or FOMO?

Market Capitalization: Market capitalization is the market value of all the equity of a company’s common and preferred shares. It is usually estimated by multiplying the stock price by the number of shares for each share class and summing the results.

Market Depth: The degree to which a market can execute large market orders without impacting the price of a security. For example, a “deep” market for a stock will have a sufficient number of both bid and ask orders to keep a big order from significantly moving the security’s price.

Market Maker: A market maker exists to “create a market” for specific company securities by being willing to buy and sell those securities at a specified displayed price and quantity to broker-dealer firms that are members of the exchange. These firms help keep financial markets liquid by making it easier for investors to buy and sell securities–they ensure that there is always someone to buy and sell to at the time of trade.

Market Neutral: Equity market neutral strategies seek to eliminate the risks of the equity market by holding up to 100% of net assets in long equity positions and up to 100% of net assets in short equity positions. These strategies attempt to exploit differences in stock prices by being long and short in stocks within the same sector, industry, market capitalization, etc. If successful, these strategies should generate returns independent of the equity market. Equity market neutral portfolios have two key sources of return:

the Treasury Bill return (the interest on proceeds from short sales held in cash as collateral)

the difference (the “spread”) between the return on the long positions and the return on the short positions. Stock picking, rather than broad market moves, should drive most of a market-neutral strategy’s total return (save for any return from the 100% cash position).

It’s important to point out that here is the risk of theoretical unlimited amount of loss with short selling, (i.e. the price of the short-sold stocks increases; the long position can only go down to $0).

Market Order: An order placed with a bank or brokerage firm to immediately buy or sell a security at the best available current price. May also be referred to as an “unrestricted order.”

Posted on December 7, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The Shadow Self is like the dark twin you never knew you had. It’s the part of your personality that lurks in the background, hiding your less-than-perfect traits. Think of it as the villain in your personal movie, full of suppressed desires and impulses.

According to colleague Dan Ariely PhD, acknowledging your shadow self can be a bit like therapy – uncomfortable but ultimately enlightening.

So, embrace your inner Darth Vader, and you might just find a better balance between light and dark.

Municipal Securities (munis): Debt securities typically issued by or on behalf of U.S. state and local governments, their agencies or authorities to raise money for a variety of public purposes, including financing for state and local governments as well as financing for specific projects and public facilities. In addition to their specific set of issuers, the defining characteristic of munis is their tax status. The interest income earned on most munis is exempt from federal income taxes. Interest payments are also generally exempt from state taxes if the bond owner resides within the state that issued the security. The same rule applies to local taxes.

Another interesting characteristic of munis: Individuals, rather than institutions, make up the largest investor base. In part because of these characteristics, munis tend to have certain performance attributes, including higher after-tax returns than other fixed income securities of comparable maturity and credit quality and low volatility relative to other fixed-income sectors.

The two main types of munis are general obligation bonds (GOs) and revenue bonds. GOs are munis secured by the full faith and credit of the issuer and usually supported by the issuer’s taxing power. Revenue bonds are secured by the charges tied to the use of the facilities financed by the bonds.

Municipal Yield Curve: The yield curve that illustrates the yields of a certain type of municipal security at its various maturities.

Municipal Yield Ratio: A yield ratio most often used to determine the relative value of municipal securities compared with U.S. Treasury securities. The ratio consists of the yield of a municipal security of a certain maturity divided by the yield of a U.S. Treasury security of the same maturity.

Posted on December 6, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

BREAKING NEWS!

***

***

The internet web page listing the corporate leadership team behind Anthem Blue Cross Blue Shield (BCBS), one of America’s biggest health insurers, has disappeared from the company’s website.

The disappearance of the page listing the provider’s 25 highest-ranking employees was highlighted in a post shared to the r/antiwork subreddit on Reddit by the user u/wendysdriv

Posted on December 5, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

LTC

By Anonymous Insurance Agent

***

***

Some retired people live on a fixed income and many of them live right on the edge of their financial capability. At some time in their life, they may have to make a choice regarding many purchases. In this case, we will illustrate “choice” using a couple’s purchase of Long-Term-Care Insurance [LTCI].

Of course, economics is the study of choice; wants, needs and scarcity, etc. In our case, if they decide to make the purchase they commit to a lifetime of premium payments. The financial tradeoff is this; if they make the commitment to purchase LTCI, they must give up something else.

Example: In order to maintain a monthly premium of $100 ($1,200per year), an elderly patient, retired layman or couple must essentially relegate about $30,000 of financial assets to generate the $100 necessary to make an average premium payment (assumes a 7% rate of return with 4% withdrawal rate) or [4% X $30,000 = $1,200 year]. Thus, if the monthly premium cost is $500 per month, the elder must give up the use of $150,000 of retirement asset just to generate enough cash flow to pay for the LTC insurance.

The married elder couple has to make the decision among lifestyle (dinners, vacations, gifts to children, prescription drugs, medical care or food and shelter) versus paying an insurance premium to provide for nursing home coverage for a need, which may be very real, but will not occur until sometime in the ambiguous future.

And so, when faced with such a tough economics, neither of which delivers peace of mind or a respectable solution; many will simply decide that, in either case, they may already end up impoverished.

Thus, many will often opt for the better lifestyle now … while they can enjoy it … together.

Posted on December 5, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Beneficial Ownership Information

By Staff Reporters

***

***

Small business owners face severe penalties if they don’t report to the federal government by year’s end. And, thousands of businesses may not realize they are subject to a new reporting process mandated under the Corporate Transparency Act, which went into effect in January 2024. Even lawyers, doctors, financial advisors and accountants are affected; along with “mom and pop”business owners.

For most eligible businesses, the filing deadline is Jan. 1, 2025, according to the U.S. Chamber of Commerce. “Those who fail to file by this deadline — or fail to update this information if needed — could face up to two years imprisonment and fines up to $10,000, in addition to civil penalties of up to $591 per day,” the U.S. Chamber of Commerce website reads.

The law was created “to combat illicit activity including tax fraud, money laundering and financing for terrorism by capturing more ownership information for specific U.S. businesses operating in or accessing the country’s market,” the chamber website explained.