BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

A company that invests in real estate and whose shares trade on a public exchange.

Real Estate Investment Trust (REIT)

A real estate operating company (REOC) is similar to a real estate investment trust (REIT), except that an REOC will reinvest its earnings into the business, rather than distributing them to unit holders like REITs do.

Also, REOCs are more flexible than REITs in terms of what types of real estate investments they can make.

Derivatives are securities whose performance and/or structure is derived from the performance and/or structure of other assets, interest rates, or indexes. If used moderately and in appropriate situations, derivatives can help stabilize portfolios and/or enhance returns. However, if used in excess and/or in inappropriate circumstances, they can be harmful, potentially causing portfolio instability and/or losses. Derivatives are similar to medicine in their behavior–usually safe when used as directed, potentially toxic when abused.

There are many different types of derivative securities and many different ways to use them. Some derivative securities, such as mortgage-related and other asset-backed securities, are in many respects like any other investment, although they may be more volatile or less liquid than more traditional debt securities.

Futures and options are commonly used for traditional hedging purposes to attempt to protect portfolios from exposure to changing interest rates, securities prices or currency exchange rates, and for cash management purposes as a low-cost method of gaining exposure to a particular securities market without investing directly in those securities.

Certain other derivative securities may be described as structured investments. A structured investment is a security whose value or performance is linked to an underlying index or other security or asset class. Structured investments include collateralized mortgage obligations (CMOs). Structured investments also include securities backed by other types of collateral.

According to Wikipedia, a fundamental tenet of the paradox is that the customer, i.e. the potential purchaser of the information describing a technology (or other information having some value, such as facts), wants to know the technology and what it does in sufficient detail as to understand its capabilities or have information about the facts or products to decide whether or not to buy it. Once the customer has this detailed knowledge, however, the seller has in effect transferred the technology to the customer without any compensation. This has been argued to show the need for patent protection [HIPPA].

If the buyer trusts the seller or is protected via contract, then they only need to know the results that the technology will provide, along with any caveats for its usage in a given context. A problem is that sellers lie, they may be mistaken, one or both sides overlook side consequences for usage in a given context, or some unknown-unknown affects the actual outcome.

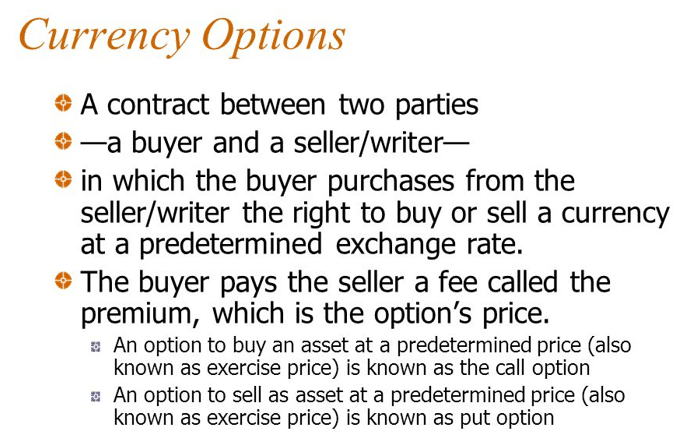

Currency Hedging is a risk-management strategy, as part of a foreign investment strategy, currency hedging is designed to reduce the impact from changes in the relative values of currencies involved in the foreign investment strategy.

In any foreign investment strategy, a significant part of the potential risk and return comes from exposure to relative currency value fluctuations. If exposure to those currency fluctuations is minimized, investors can experience more of a “pure play” exposure to the foreign investments. There is a variety of possible currency hedging strategies, ranging from swaps, options, and spot contracts to simply buying foreign currencies.

Currency Overlay is a financial trading strategy used to separate the management of currency risk from other portfolio strategies. A currency overlay manager can seek to hedge the risk from adverse movements in exchange rates, and/or attempt to profit from tactical currency views.

Posted on November 8, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The Federal Reserve cut interest rates by 0.25 percentage points Thursday, the second consecutive cut after a two-year rate-hike run to curb post-pandemic inflation.

Lyft announced impressive earnings results thanks to more commuters using the ride-hailing service, as well as upbeat guidance for the future. Shares rose 22.92%.

Shareholders worried about a housing market slowdown hurting Zillow had nothing to fear: The real estate website crushed earnings estimates, and shares popped 23.77%.

Warner Bros. Discovery enjoyed its biggest single-quarter surge in subscribers ever thanks to streaming service Max, which sent shares soaring 11.81%.

UnderArmour rocketed 23.33% higher after its cost-savings plan paid off last quarter and management guided for a strong quarter ahead.

Planet Fitness surprised shareholders with a solid quarter for the gym giant, as well as forecasts of more growth ahead. Shares climbed 11.26%.

Prison operators GEOGroup and CoreCivic both surged on Trump’s election, and their rally continued today—in-spite of very different paths forward for each stock. GEO Group gained 13.63%, while CoreCivic rose 25.60%.

What’s down

Trump Media & Technology Group was one of the biggest winners on election night, and although the stock soared over the last few days, investors decided to take profits today. Shares sank 22.97%.

Wolfspeed plummeted 39.24% after announcing larger-than-expected losses last quarter, poor forecasts for next quarter, and layoffs to cut costs.

Match Group shareholders were heartbroken to hear that Tinder’s revenue fell last quarter, though strong revenue growth from Hinge helped ease the pain. Shares dropped 17.87%.

Virgin Galactic isn’t just a mean nickname from your high school years—it’s also a space stock that can’t make money to save its life. Shares fell 11.87%.

The S&P 500®index (SPX) rose 44.06 points (0.74%) to 5,973.10; the Dow Jones Industrial Average® ($DJI) fell 0.59 points (0.00%) to 43,729.34; and the NASDAQ Composite®($COMP) gained 285.99 points (1.51%) to 19,269.46.

The 10-year Treasury note yield (TNX) fell nine basis points to 4.34%, with most of the drop coming long before the Fed decision.

The CBOE Volatility Index® (VIX) continued its post-election plunge to 15.21.

Stocks surged and stayed higher all yesterday day on news of Donald Trump’s presidential victory. The Dow rocketed over 1,350 points as soon as markets opened, and all three indexes ended the day at record highs.

Treasuryyields have paralleled Trump’s chances of taking the White House for the last few weeks, and his election sent them soaring to over 4.46% at one point today.

Oil and gold both fell as the dollar rose after Trump’s win. The greenback popped on the promise of Trump’s protectionist tariff policies and the lower likelihood of the Fed cutting interest rates as fast as previously expected.

Bitcoin surged as traders celebrated the beginning of the new, friendlier regulatory environment that Trump promised during his campaign.

Posted on November 7, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

One more group of stocks that soared on a Trump election: Big Tech companies with antitrust problems. Another Trump presidency should go a long way toward clearing up the regulatory hurdles many companies have faced recently, which is why Alphabet popped 3.99% and Amazon rose 3.8%.

CVS Health surged 11.33% after meeting revenue forecasts but missing earnings expectations. However, the miss was due to a one-time charge, so shareholders quickly forgave the healthcare retailer.

Planet Fitness gained 6.09% on a surprise bid for bankrupt fitness chain Blink Holdings in an attempt to bolster its own gym business.

Stocks Down

Super Micro Computer had a chance to show the world it wasn’t committing the fraud it has recently been accused of. Instead, the company announced it is still unable to determine when it will file the quarterly report due August 29. Shares crashed 18.05%.

Home builder stocks sank on fears that a Trump presidency will slow the rate of Fed rate cuts, keeping mortgage rates higher for longer. DR Horton fell 3.8%, Lennar dropped 4.84%, PulteGroup lost 3.09%, and TollBrothers tumbled 1.46%.

Cannabis stocks were betting big on a ballot measure in Florida to allow the sale of recreational marijuana. The initiative’s failure sent shares of Curaleaf plummeting 29.17%, TrulieveCannabis plunged 38.8%, and AyrWellness sank 55.87%.

The S&P 500®index (SPX) rose 146.28 points (2.53%) to 5,929.04; the Dow Jones Industrial Average® ($DJI) added 1,508.05 points (3.57%) to 43,729.93; and the NASDAQ Composite®($COMP) gained 544.29 points (2.95%) to 18,983.47—a new closing high.

The 10-year Treasury note yield (TNX) surged 14 basis points to 4.43%, its highest level since July.

The CBOE Volatility Index® (VIX) fell sharply to 16.3 as election-related uncertainty diminished.

Stocks just roared out of the gate this Wednesday morning following news that former President Donald Trump has secured a second term in the White House and Republicans won a majority in the Senate.

The Dow Jones Industrial Average rose 1,341 points, or about 3.1 percent, as the market opened, reaching a record high. It was the first time it has jumped more than 1,000 points in a single day since November 2022.

The S&P 500 also gained 1.9 percent, and the NASDAQ climbed 1.8 percent.

Despite concern from big business about Trump’s plan to impose blanket tariffs on imports to the U.S., Wall Street is anticipating tax cuts and deregulation during a second Trump presidency.

Retained Earnings Risk: Profits generated by a company that are not distributed to stockholders as dividends. Instead, they are either reinvested in the business or kept as a reserve for specific objectives, such as paying off debt or purchasing equipment. Retained earnings risks are also called “undistributed profits,” “undistributed earnings,” or “earned surplus.”

Risk-Weighted (or risk-adjusted) Assets: Within the context of measuring the financial stability of banks and other financial institutions, the risk-weighted assets figure is an aggregate of a financial institution’s assets (usually loans to its customers) after the loans have been individually adjusted for their risk. This involves multiplying each loan by a factor that reflects its risk. Low-risk loans are multiplied by a low number, high-risk by high. The aggregate number can then be used to calculate the financial institution’s capital ratio. Lower risk-weighted assets typically result in higher capital ratios, and higher risk-weighted assets usually translate to lower capital ratios.

Sequence-of-Returns Risk: The risk of market conditions impacting the overall returns of an investment portfolio during the period when a retiree is first starting to withdrawal money from investments as income. For example, if a retiree has to withdrawal income from his or her portfolio when market prices are depressed, the portfolio may lose out on the potential returns that income could have made once market prices recovered.

Posted on November 6, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

First-time homebuyers in 2024 had a median income of $97,000, and their median age was 38. OpenAI and Jeff Bezos invested in Physical Intelligence, a robot startup with the aim of “bringing general-purpose AI into the physical world.”

Cybersecurity darling Palantir soared 23.38% to a record high thanks to strong earnings, high AI demand, and big spending from the Department of Defense.

Astera Labs skyrocketed 37.70% after the semiconductor parts maker (and one of Nvidia’s key suppliers) announced strong earnings.

Crypto stocks had a great day thanks to a widespread cryptocurrency rally. Coinbase rose 4.13%, MicroStrategy gained 2.16%, and RiotPlatforms jumped 8.13%.

Stocks Down

Trump Media & Technology Grouparrested its recent downturn and popped 12% at one point today, but gave all those gains up and ended the day down 1.16%.

You’d think the end of a multi-week labor dispute costing billions of dollars would be a relief for shareholders, but Boeing still sank 2.62% on news that it’s reached an agreement with striking machinists.

It’s a me, lower revenue forecasts! Nintendo fell 1.68% after announcing that sales of its Switch console are starting to sag.

Some of the smaller semiconductor stocks on the market took a beating today. NXP Semiconductor dropped 5.17% after announcing weaker-than-expected Q4 guidance, Lattice Semiconductor tumbled 1.37% after missing on sales forecasts and announcing job cuts, and while Cirrus Logic beat expectations this quarter, it still fell 7.09% on lower forecasts.

The S&P 500®index (SPX) rose 70.07 points (1.23%) to 5,782.76; the Dow Jones Industrial Average® ($DJI) added 427.28 points (1.02%) to 42,221.88; and the NASDAQ Composite®($COMP) increased 259.19 points (1.43%) to 18,439.17.

The 10-year Treasury note yield (TNX) dropped two basis points to 4.29%.

The CBOE Volatility Index® (VIX) slipped to 20.72.

Classic: Investment purchases and private expenditures of healthcare firms, the value of related construction, and the change in inventory during the year.

Modern: Gross Revenue Per Day is the average amount charged by a hospital for one day of inpatient care (gross inpatient revenue divided by patient-census days).

Gross Revenue Per Discharge: The average amount charged by a hospital to treat an inpatient from admission to discharge (gross inpatient revenue divided by discharges).

Gross Revenue Per Visit: The average amount charged by a hospital for an outpatient visit (gross outpatient revenue divided by outpatient visits).

Posted on November 5, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

After its AI-related earnings disappointed Wall Street last quarter, Big Tech doubled down in the latest period:

Amazon spent $22.6 billion on property and equipment like data centers and chips. That’s an 81% spike from the same time last year.

Meta raised its low-end guidance for capex (capital expenditures), which could reach $40 billion by the end of the year. It beat earnings estimates, even with AR glasses subsidiary Reality Labs costing $4.4 billion in operating losses.

Apple is still betting on Apple Intelligence to boost sales. Most revenue came from the new iPhone 16, Apple Watch, and AirPods, but Apple services like TV+ and iCloud also grew massively to account for a quarter of the business.

Google crushed earnings estimates and revealed that more than 25% of all new code it writes is generated by AI (and reviewed by engineers).

Posted on November 5, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Among consideration for CVS is splitting up its assets: CVS Pharmacy, pharmacy benefit managerCVS Caremark, and insurance arm Aetna. The company has reportedly been in talks with bankers about the move, Reuters reported early this month.

Just as Nvidia will replace Intel, Sherwin Williamswill replaceDow Inc. on the Dow (how embarrassing, getting kicked off an index you share a name with). Sherwin Williams popped 4.59%, while Dow Inc. fell 2.08%.

Peloton pedaled 3.59% higher on a double upgrade from Bank of America analysts, who like the bike company’s higher profit outlook and hiring of new CEO Peter Stern from Ford.

Yum! China, the company that operates Pizza Hut and KFC restaurants in China, climbed 7.12% after announcing that new store openings translated into better-than-expected revenue and earnings last quarter.

STOCKS DOWN

Nuclear energy stocks took a big hit today after the Federal Energy Regulatory Commission ruled that Talen Energycould not increase the amount of energy its nuclear plant in Susquehanna, PA, produces in order to power an Amazon data center. Talen fell 2.23%, Vistra Corp sank 3.18%, and Constellation Energy plummeted 12.46%.

Clinical data from a Viking Therapeutics trial shows its weight-loss pill is effective. Shares soared then sank 13.36% as investors took profits.

The S&P 500®index (SPX) dipped 16.11 points (–0.28%) to 5,712.69; the $DJI dropped 257.59 points (–0.61%) to 41,794.60; and the $COMP lost 59.93 points (–0.33%) to 18,179.98.

The 10-year Treasury note yield (TNX) fell five basis points to 4.31%.

The CBOE Volatility Index® (VIX)edged up to 22.11, still below last week’s peaks.

Posted on November 3, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

Two recent court actions may serve as harbingers for the future of healthcare fraud and abuse laws. In September 2024, a federal judge in the Southern District of West Virginia ordered parties in a qui tamFalse Claims Act and Stark Law case to brief the court on the implications of Loper Bright Enterprises v. Raimondo on the interpretation of the Stark Law to the case at hand.

That same month, a federal judge in the Middle District of Florida dismissed a qui tam lawsuit on a novel theory that the False Claims Act’s whistleblower provisions are unconstitutional.

This Health Capital Topics article discusses these cases and the potential impact on federal fraud and abuse laws. (Read more…)

STRIPS (Separate Trading of Registered Interest and Principal of Securities) is an acronym that describes both a government bond issuance program and the securities issued by the program. STRIPS are a form of zero-coupon security (defined below) created under the U.S. Treasury’s STRIPS program.

Originally, zero-coupon securities were created by broker-dealers who bought Treasury bonds and deposited these securities with a custodian bank. The broker-dealers then sold receipts representing ownership interests in the coupons or principal portions of the bonds.

Some examples of zero-coupon securities sold through custodial receipt programs are CATS (Certificates of Accrual on Treasury Securities), TIGRs (Treasury Investment Growth Receipts) and generic TRs (Treasury Receipts). The U.S. Treasury subsequently introduced a program called Separate Trading of Registered Interest and Principal of Securities (STRIPS), through which it exchanges eligible securities for their component parts and then allows the component parts to trade in book-entry form.

STRIPS are direct obligations of the U.S. government and have the same credit risks as other U.S. Treasury securities. STRIPS are generally considered the most liquid (easily bought and sold) zero-coupon securities.

Posted on November 2, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Ford paused production of its F-150 Lightning electric truck from mid-November to early January as demand for the once-coveted EV dwindles.

Peloton named Peter Stern, the co-founder of Apple Fitness+, as its next CEO.

Starbucksis bringing back Sharpied names on cups for the first time in four years as new CEO Brian Niccol tries to shake up the struggling coffee chain.

Boeing offered striking machinists yet another new contract offer, including a 38% pay raise over the next four years. The union will vote on the contract on Monday. Shares climbed 3.54%.

Avis Budget motored 10.92% higher despite missing forecasts on both earnings and revenue. Shareholders celebrated the rental car company’s strong growth expectations from management and took advantage of a cheap valuation.

Globalstar rocketed 32.38% after the satellite communications company announced an expanded deal with Apple.

Charter Communications soared 11.87% after losing fewer subscribers than expected, which is like a back-handed compliment in the investing world.

STOCKS DOWN

Trump Media & Technology Group remains on the roller coaster, falling another 13.53% today as early exit polls show Vice President Kamala Harris with a lead in several key states.

Wayfair may have met earnings expectations last quarter, but the online home goods retailer also lost customers and fulfilled fewer orders. Shares fell 6.26%.

Super Micro Computer continued to sell off after the resignation of its financial auditor, an almost-sure sign of fraud. Shares sank another 10.51%.

The S&P 500®index (SPX) rose 23.35 (0.41%) to 5,728.80 to end the week down 1.37%; the Dow Jones Industrial Average® ($DJI) added 288.73 points (0.69%) to 42,052.19 to end the week down 0.15%; and the NASDAQ Composite®($COMP) gained 144.76 points (0.80%) to 18,239.92 to end the week down 1.50%.

The 10-year Treasury note yield (TNX) climbed eight points to 4.36%, the highest since early July.

The CBOE Volatility Index® (VIX)remained elevated at 21.88.

Posted on November 1, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Comcast popped 3.39% on the news that it is exploring a separation of its cable business. The network operator got a boost this quarter from the Olympics, but still lost 365,000 cable TV customers.

Peloton Interactive pedaled 27.82% higher after the bike maker beat earnings expectations and introduced a new CEO.

Carvana accelerated 19.23% on an impressive beat-and-raise earnings report that caps off the car seller’s incredible comeback.

Booking Holdings, owner of Kayak and Priceline, hit a record high after the travel company reported shockingly strong earnings. Shares rose 4.76%

What was down

Trading in shares of Trump Media & Technology Group was halted yet again today after the meme stock sank dramatically to start the day. Shares ended the trading session down 11.72%.

Estee Lauder plummeted 20.84% on a triple whammy of bad news: The cosmetics retailer missed earnings estimates, pulled its forecast, AND cut its dividend. Ouch.

Super Micro Computer continued to tumble today, declining another 11.97% as the fallout from the resignation of its financial auditor raises the threat of the semiconductor stock getting delisted from the Nasdaq.

eBay sank 8.18% after beating earnings expectations but issuing disappointing earnings guidance heading into the holiday season.

The SPX fell 108.22 (–1.86%) to 5,705.45; the Dow Jones Industrial Average® ($DJI) dropped 378.08 points (–0.90%) to 41,763.46; and the NASDAQ Composite®($COMP) lost 512.78 points (–2.76%) to 18,095.15 and has now fallen in two of the last four months.

The 10-year Treasury note yield (TNX) added two basis points to 4.28%.

The VIX rose to 22.6, the highest since October 8.

What Is CREDIT? Credit is a contractual agreement in which a borrower receives a sum of money or something else of value and commits to repaying the lender later, typically with interest. Credit is also the creditworthiness or credit history of an individual or a company. Good credit tells lenders you have a history of reliably repaying what you owe on loans. Establishing good credit is essential to getting a loan.

***

Credit Analysis is a form of financial analysis used primarily to determine the financial strength of the issuer of a security, and the ability of that issuer to provide timely payment of interest and principal to investors in the issuer’s debt securities. Credit analysis is typically an important component of security analysis and selection in credit-sensitive bond sectors such as the corporate bond market and the municipal bond market.

Credit Default Swap Index (CDX) is a credit derivative, based on a basket of CDS, which can be used to hedge credit risk or speculate on changes in credit quality.

Credit Default Swaps (CDS) are credit derivative contracts between two counter parties that can be used to hedge credit risk or speculate on changes in the credit quality of a corporation or government entity.

Credit Quality reflects the financial strength of the issuer of a security, and the ability of that issuer to provide timely payment of interest and principal to investors in the issuer’s securities. Common measurements of credit quality include the credit ratings provided by credit rating agencies such as Standard & Poor’s and Moody’s. Credit quality and credit quality perceptions are a key component of the daily market pricing of fixed-income securities, along with maturity, inflation expectations and interest rate levels.

Credit Rating Agency (CRA) is a company that assigns credit ratings for issuers of certain types of debt obligations as well as the debt instruments themselves. In the United States, the Securities and Exchange Commission (SEC) permits investment banks and broker-dealers to use credit ratings from “Nationally Recognized Statistical Rating Organizations” (NRSRO) for similar purposes. As of January 2012, nine organizations were designated as NRSROs, including the “Big Three” which are Standard and Poor’s, Moody’s Investor Services and Fitch Ratings.

A Credit Rating Downgrade by a credit rating agency (such as Standard & Poor’s, Moody’s or Fitch), of reducing its credit rating for a debt issuer and/or security. This is based on the agency’s evaluation, indicating, to the agency, a decline in the issuer’s financial stability, increasing the possibility of default (defined below). A downgrade should not to be confused with a default; a debt security can be downgraded without defaulting. (And, conversely, a debt issuer can suddenly default without being downgraded first–credit ratings and credit rating agencies are not infallible.)

Credit Ratings are measurements of credit quality provided by credit rating agencies). Those provided by Standard & Poor’s typically are the most widely quoted and distributed, and range from AAA (highest quality; perceived as least likely to default) down to D (in default). Securities and issuers rated AAA to BBB are considered/perceived to be “investment-grade”; those below BBB are considered/perceived to be non-investment-grade or more speculative.

Credit Risk is the risk that the inability or perceived inability of the issuers of debt securities to make interest and principal payments will cause the value of those securities to decrease. Changes in the credit ratings of debt securities could have a similar effect.

Credit Risk Transfer Securities (CRTS) are the unsecured obligations of the GSEs (Government Sponsored Enterprises). Although cash flows are linked to prepays and defaults of the reference mortgage loans, the securities are unsecured loans, backed by general credit rather than by specified assets.

Posted on October 30, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Trump Media & Technology Group rocketed higher at the opening bell, prompting the Nasdaq to halt trading on what has quickly become the meme stock du jour. Shares ended the day 8.76% higher.

23andMe clawed 1.86% higher after introducing three new board members about a month after the entire board resigned.

VF Corp, parent company of clothing brands JanSport, Vans, and North Face, surged 27.01% thanks to an impeccable earnings report that revealed its turnaround plans are coming to fruition.

Trex, the stuff your dad built an awesome deck out of, saw sales fall last quarter but still managed to beat earnings expectations. Shares popped 6.19%.

STOCKS DOWN

JetBlue Airways sank 17.08% in spite of reporting a smaller loss than analysts expected. The problem is all the turbulence that lies ahead.

D.R. Horton is the largest homebuilder by market cap, so when it says that 2025 will be a bad year, investors should listen. Shares dropped 7.29% on the news.

Crocs stumbled 19.17% after beating earnings but announcing that its fiscal year would be bogged down by poor sales of its HeyDude shoe brand.

Stanley Black & Decker fell 8.77% after missing on both profits and sales, citing weaker consumer spending.

Xerox plummeted 17.41% after the company that can’t make a printer that works for longer than 3 months without needing a new ink cartridge announced weaker sales than expected.

The S&P 500® index (SPX) rose 9.40(0.16%) to 5,832.92; the Dow Jones Industrial Average® ($DJI) fell 154.52 points (–0.36%) to 42,233.05; and the $COMP added points 145.55 (0.78%) to 18,712.75.

The 10-year Treasury note yield (TNX) finished unchanged at 4.27% after reaching nearly 4.34% earlier today.

The five most valuable US companies in the S&P 500 report earnings this week, and updates on three key economic indicators are set to be released: 1. gross domestic product, 2. inflation, and 3. jobs report. Then, next week brings the election and another expected rate cut from the Federal Reserve.

Markets:All three stock indexes rose to start a week that will be filled with high-stakes data.

Stock spotlight: Trump Media & Technology Group gained almost 22% on Monday, following the former president and current GOP candidate’s Madison Square Garden rally. The rose means that Trump Media, which includes Truth Social, is now more valuable than Elon Musk’s X.

Russell 1000® Growth Index: Measures the performance of those Russell 1000 Index companies (the 1,000 largest publicly traded U.S. companies, based on total market capitalization) with higher price-to-book ratios and higher forecasted growth values.

Russell 1000® Index: A market-capitalization weighted, large-cap index created by Frank Russell Company to measure the performance of the 1,000 largest publicly traded U.S. companies, based on total market capitalization.

Russell 1000® Value Index: Measures the performance of those Russell 1000 Index companies (the 1,000 largest publicly traded U.S. companies, based on total market capitalization) with lower price-to-book ratios and lower forecasted growth values.

Russell 2000® Growth Index: Measures the performance of those Russell 2000 Index companies (the 2,000 smallest of the 3,000 largest publicly traded U.S. companies, based on total market capitalization) with higher price-to-book ratios and higher forecasted growth values.

Russell 2000® Index: Market-capitalization weighted index created by Frank Russell Company to measure the performance of the 2,000 smallest of the 3,000 largest publicly traded U.S. companies, based on total market capitalization.

Russell 2000® Value Index: Measures the performance of those Russell 2000 Index companies (the 2,000 smallest of the 3,000 largest publicly traded U.S. companies, based on total market capitalization) with lower price-to-book ratios and lower forecasted growth values.

Russell 2500™ Growth Index: Measures the performance of those Russell 2500 Index companies (the 2,500 smallest of the 3,000 largest publicly traded U.S. companies, based on total market capitalization) with higher price-to-book ratios and higher forecasted growth values.

Russell 2500™ Index: A market-capitalization weighted index created by Frank Russell Company to measure the performance of the 2,500 smallest of the 3,000 largest publicly traded U.S. companies, based on total market capitalization.

Russell 2500™ Value Index: Measures the performance of those Russell 2500 Index companies (the 2,500 smallest of the 3,000 largest publicly traded U.S. companies, based on total market capitalization) with lower price-to-book ratios and lower forecasted growth values.

Russell 3000® Growth Index: Measures the performance of the broad growth segment of the U.S. equity universe. It includes those Russell 3000 companies with higher price-to-book ratios and higher forecasted growth values.

Russell 3000® Index: Measures the performance of the largest 3,000 U.S. companies representing approximately 98% of the investable U.S. equity market.

Russell 3000® Utilities Index: A sub-index of the Russell 3000 Index, is a capitalization weighted index of companies in industries heavily affected by government regulation, including among others, basic public service providers (electricity, gas and water), telecommunication services, and oil and gas companies.

Russell 3000® Value Index: Measures the performance of the broad value segment of the U.S. equity universe. It includes those Russell 3000 companies with lower price-to-book ratios and lower forecasted growth values.

Russell Midcap® Growth Index: Measures the performance of those Russell Midcap Index companies (the 800 smallest of the 1,000 largest publicly traded U.S. companies, based on total market capitalization) with higher price-to-book ratios and higher forecasted growth values.

Russell Midcap® Index: Measures the performance of the 800 smallest of the 1,000 largest publicly traded U.S. companies, based on total market capitalization.

Russell Midcap® Value Index: Measures the performance of those Russell Midcap Index companies (the 800 smallest of the 1,000 largest publicly traded U.S. companies, based on total market capitalization) with lower price-to-book ratios and lower forecasted growth values.

Russell Top 200® Index: Measures the performance of the 200 largest securities of the 3,000 publicly traded U.S. companies in the Russell 3000® Index, based on total market capitalization. It is not an investment product available for purchase.

Posted on October 28, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Peak earnings season: Five of the Magnificent SevenStocks will be among the 181 companies reporting their earnings this week. Alphabet is in the Mag Seven lead-off spot on Tuesday, Microsoft and Meta step to the plate on Wednesday, and Apple and Amazon rounding out the lineup and this baseball metaphor on Thursday. These companies account for almost 25% of the S&P 500, which is up 40% over the past year and not far off its record closing number from earlier this month. But, the approaching election, it could be a volatile week in the stock markets.

***

Markets: Stocks are currently driving the narrative on Wall Street. Last week, bonds sold off in a big way (driving yields to their highest level since July) in a sign investors are dialing back expectations of more aggressive rate cuts from the Federal Reserve.

Stocks nevertheless handled the bond volatility with aplomb, and with help from Tesla’s 22% one-day rise, the NASDAQ is sitting within 2% of its record high.

Posted on October 28, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

401(k) vs. pension: There’s pros and cons to both. While pension plans guarantee a steady income stream, payments sometimes aren’t indexed by inflation, which can erode their value over time. On the flip side, 401(k)s are subject to market fluctuations and require financial literacy.

It’s good to have money stashed in the stock market when the market is doing well. The number of people with at least $1 million in their 401(k) and IRA accounts jumped 12% in the second quarter 2024, according to a report from Fidelity Investments, largely tracking the market’s gain during that period. It’s the third straight quarter of growth in $1+ million accounts and close to a record high.

But start saving now, because building a hard-boiled nest egg through retirement accounts takes time: The average age of a 401(k) millionaire is 59, Fidelity said.

Posted on October 26, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The SPX fell 1.74 points (–0.03%) to 5,808.12 to end the week down 0.96%; the $DJI lost 259.96 points (–0.61%) to 42,114.40 to end the week down 2.68%; and the $COMP rose 103.12 points (0.56%) to 18,518.61 to end the week up 0.16%.

The 10-year Treasury note yield (TNX) added three basis points to 4.23%.

The CBOE Volatility Index® (VIX) climbed sharply to 19.95, nearing recent highs. The 20 level is an area to watch next week, as it traditionally signals more volatile markets.

Pick a direction already: On Wednesday, Spirit Airlines soared 30% on news of a possible merger with Frontier. On Thursday, shares plunged 21% as investors took their profits. Today, shares are back up 15.05% after Spirit announced it will cut jobs and sell planes in an effort to boost profits.

Texas Roadhouse sizzled like a porterhouse T-bone, rising 3.58% after announcing that earnings rose 32% last quarter.

Deckers Outdoor popped 10.57% thanks to soaring demand for Hoka shoes, helping the footwear company beat earnings estimates and raise forecasts.

Newell Brands may not be a household name, but they make household goods like Sharpies, Elmer’s Glue, and Crock-Pot—all things that people bought a ton of last quarter, which is why shares soared 21.59% today.

Apple is just fine, thanks: The Market Cap King got a rare analyst downgrade from KeyBanc, which is worried about lower demand from China. Shareholders were unfazed, and the stock rose 0.36%.

STOCKS DOWN

AutoNation hasn’t shaken off the aftereffects of a major cyberattack in July just yet, which is why revenue and earnings both missed estimates last quarter. Shares fell 4.46% today.

Colgate-Palmolive announced a beat-and-raise quarter, but it wasn’t enough to impress shareholders, who pushed the consumer staples giant down 4.14%.

Mohawk Industries was the worst-performing stock on the market at one point today, falling 13.70% after the flooring manufacturer reported disappointing earnings and lowered its fiscal forecast.

Online education company Coursera got an F from shareholders after the company lowered its revenue guidance for the full fiscal year. Shares dropped 9.83%.

Newmont had its worst day in over a decade yesterday after the gold miner reported shockingly bad earnings, with higher costs offsetting the rising price of gold. Shares continued to fall 1.69% today.

A young clinician representative advising to consider the cost versus value of medicine. Health care concept for economic cost-effectiveness analysis, driving down medical costs, improved access.

***

Value Based CareClassic Definition: Value-based care is a type of payment model that pays doctors and hospitals for treating patients in the right place, at the right time and with just the right amount of care. You can look at it as a financial incentive to motivate healthcare providers to meet specific performance measures related to the quality and efficiency of the process. The same way, it penalizes weaker experiences, such as medical errors. The concept is often counter-intuitive.

Modern Circumstance: As healthcare costs continue to rise, value-based care has been growing in popularity compared to the traditional fee-for-service method.

Think: HMOs, PPOs, capitation payments and Medicare Advantage [Part C].

Paradox Examples:

Payment: A physician paid through fee-for-service compensation might like to see a packed medical office waiting room. More patients and services equate to higher pay. But, the same doctor paid through a VBC contract might wish to see an emptier waiting room as s/he will get the exact same daily pay for seeing fewer patients and working much less.

Prospectivity: Traditional Fee-for-Service medicine treats sick patients. VBC medicine seeks to keep patients healthy and out of the doctor’s office.

Posted on October 25, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Applications to MBA programs are up 12% in 2024 after declining for two years, according to the Graduate Management Admission Council, which surveys business school admissions offices.

Apple and Goldman Sachs were ordered to pay $89 million by the Consumer Financial Protection Bureau for failing to address thousands of consumer disputes of Apple Card transactions.

Apple is cutting production of Vision Pro due to slow sales. The tech giant is scaling down production of its $3,500 Vision Pro VR headset and might halt assembly of new ones next month,

UPS delivered a strong earnings report, with revenue beating analyst expectations for the first time in two years. Shares popped 5.28%.

ServiceNow rose 5.41% to a new all-time high thanks to a beat-and-raise third-quarter earnings report powered by higher AI demand for the enterprise software company.

Whirlpool climbed 11.20% after announcing solid earnings and reiterating guidance for the rest of the fiscal year, reassuring worried shareholders.

Molina Healthcare soared 17.67% after beating both top and bottom line estimates in the third quarter, thanks to the health insurer reaping the rewards of higher Medicaid payouts.

STOCKS DOWN

IBM dropped 6.17% on disappointing third-quarter results, missing on both top and bottom line forecasts thanks to lower consulting and infrastructure revenue.

Peloton pedaled higher yesterday after Greenlight Capital’s David Einhorn declared that the company was undervalued while he was pedaling on a Peloton. The stunt only worked for a quick sprint, though, with shares back down 2.07% today.

TKO Group Holdings got hit with a piledriver after the owner of the WWE and UFC announced it is acquiring several entertainment companies, including Professional Bull Riders. Investors bucked shares off 8.69%.

Keurig Dr. Pepper fizzled 4.80% thanks to lower sales last quarter, though the company is trying to bolster revenue by acquiring energy drink maker Ghost.

Air taxi startup Lilium crashed 61.50% on the news that its main subsidiaries have run out of cash and are filing for insolvency.

The S&P 500® index (SPX) rose 12.44 points (0.21%) to 5,809.86; the $DJI fell 140.59 points (–0.33%) to 42,374.36; and the NASDAQ Composite® ($COMP) added 138.83 points (0.76%) to 18,415.49.

The 10-year Treasury note yield fell four basis points to 4.20%.

The CBOE Volatility Index® (VIX) was about flat at 19.18.

Although some might view a budget as unnecessarily restrictive, sticking to a spending plan can be a useful tool in enhancing the wealth of a medical practice. So, I will emphasize keys to smart budgeting and how to track spending and savings in these tough economic times.

There is an aphorism that suggests, “Money cannot buy happiness.” Well, this may be true enough but there is also a corollary that states, “Having a little sure reduces the unhappiness.”

Unfortunately, today there is more than a little financial unhappiness in all medical specialties. The challenges range from the commoditization of medicine, aging demographics, Medicare reimbursement cutbacks and increased competition to floundering equity markets, the home mortgage crisis, the squeeze on credit and declines in the value of a practice. Few doctors seem immune to this “perfect storm” of economic woes.

Far too many physicians are hurting and it is not limited to above-average earning professionals. However, one can strive to reduce the pain by following some basic budgeting principles. By adhering to these principles, physicians can eliminate the “too many days at the end of the month” syndrome and instead develop a foundation for building real wealth and security, even in difficult economic climates like we face today.

There are three major budget types. A flexible budget is an expenditure cap that adjusts for changes in the volume of expense items. A fixed budget does not. Advancing to the next level of rigor, a zero-based budget starts with essential expenses and adds items until the money is gone. Regardless of type, budgets can be extremely effective if one uses them at home or the office in order to spot money troubles before they develop.

For the purpose of wealth building, doctors may think of this budget as a quantitative expression of an action plan. It is an integral part of the overall cost-control process for the individual, his or her family unit or one’s medical practice.

Preparing a net income statement (lifestyle cash flow budget) is often difficult because many doctors perceive it as punitive. Most doctors do not live a disciplined spending lifestyle and they view a budget as a compromise to it. However, a cash flow budget is designed to provide comfort when there is surplus income that can be diverted for other future needs. For example, if you treat retirement savings as just another periodic bill, you are more likely to save for it.

You may construct a personal cash budget by recording each cash receipt and cash disbursement on a spreadsheet. Only the date, amount and a brief description of the transaction are necessary. The cash budget is a simple tool that even doctors who lack accounting acumen can use. Since it is possible to track the cash-in and cash-out in the same format used for a standard check register, most doctors find that the process takes very little time. Such a budget will provide a helpful look at how well you are staying within available resources for a given period.

We then continue with an analysis of your operating checkbook and a review of various source documents such as one’s tax return, credit card statements, pay stubs and insurance policies. A typical statement will show all cash transactions that occur within one year. It is helpful to establish a monthly equivalent to all items of income and expense. For the purposes of getting started, note items of income and expense by the frequency you are accustomed to receiving or spending them.

What You Should Know About The ‘Action Plan’ Cash Budget

For a medical office, the first operations budget item might be salary for the doctor and staff. Operating assets and other big ticket items come next. Some of our doctors/clients review their office P&L statements monthly, line by line, in an effort to reduce expenses. Then they add back those discretionary business expenses they have some control over.

Now, do you still run out of money before the end of the month? If so, you had better cut back on entertainment, eating dinner out or that fancy, new but unproven piece of medical equipment. This sounds draconian until you remind yourself that your choice is either: live frugally later or live a simpler lifestyle now and invest the difference.

As a young doctor, it may be a difficult trade-off. By mid-life, however, you are staring retirement in the face. That is why the action plan depends on your actions concerning monetary scarcity, a plan that one can implement and measure using simple benchmarks or budgeting ratios. By using these statistics, perhaps on an annual basis, the doctor can spot problems, correct them and continue planning actively toward stated goals like building long-term wealth.

Useful Calculations To Assess Your Budgeting Success

In the past, generic budgeting ratios would emphasize not spending more than 15 to 20 percent of your net salary on food or 8 percent on medical care. Now these estimates have given way to more rigorous numbers. Personal budget ratios, much like medical practice financial ratios, represent comparable benchmarks for parameters such as debt, income growth and net worth. Although these ratios are still broad, the following represent some useful personal budgeting ratios for physicians.

• Basic liquidity ratio = liquid assets / average monthly expenses. Cash-on-hand should approach 12 to 24 months or more in the case of a doctor employed by a financially insecure HMO or fragile medical group practice. Yes, chances are you have heard of the standard notion of setting enough cash aside to cover three months in a rainy day scenario. However, we have decried this older laymen standard for many years in our textbooks, white papers and speaking engagements as being wholly insufficient for the competitively unstable environment of modern healthcare.

• Debt to assets ratio = total debt / total assets. This percentage is high initially but should decrease with age as the doctor approaches a debt-free existence

• Debt to gross income ratio = annual debt repayments / annual gross income. This represents the adequacy of current income for existing debt repayments. Doctors should try to keep this below 20 to 25 percent.

• Debt service ratio = annual debt repayment / annual take-home pay. Physicians should aim to keep this ratio below 25 to 30 percent or face difficulty paying down debt.

• Investment assets to net worth ratio = investment assets / net worth. This budget ratio should increase over time as retirement approaches.

• Savings to income ratio = savings / annual income. This ratio should also increase over time as one retires major obligations like medical school debt, a practice loan or a home mortgage.

• Real growth ratio = (income this year – income last year) / (income last year – inflation rate). This budget ratio should grow faster than the core rate of inflation.

• Growth of net worth ratio = (net worth this year – net worth last year) / net worth last year – inflation rate). Again, this budgeting ratio should stay ahead of inflation.

In other words, these ratios will help answer the question: “How am I doing?”

Pearls For Sticking To A Budget

Far from the burden that most doctors consider it to be, budgeting in one form or another is probably one of the greatest tools for building wealth. However, it is also one of the greatest weaknesses among physicians who tend to live a certain lifestyle.

In fact, we have found that less than one in 10 medical professionals have a personal budget. Fear, or a lack of knowledge, is a major cause of procrastination. Fortunately, the following guidelines assist in reversing this microeconomic disaster.

1. Set reasonable goals and estimate annual income. Do not keep large amounts of cash at home or office. Deposit it in an FDIC insured money-market account for safety. Do not deposit it in a money market mutual fund with net asset value (NAV) that may “break the buck” and fall below the one-dollar level. Track actual bills and expenses.

2. Do not pay bills early, do not have more taxes withheld from your salary than needed and develop spending estimates to pay fixed expenses first. Fixed expenses are usually contractual and usually include housing, utilities, food, Social Security, medical, debt repayments, homeowner’s or renter’s insurance, auto, life and disability insurance, etc. Reduce fixed expenses when possible. Ultimately, all expenses get paid and become variable in the long run.

3. Make it a priority to reduce variable expenses. Variable expenses are not contractual and may include clothing, education, recreational, travel, vacation, gas, cable TV, entertainment, gifts, furnishings, savings, investments, etc. Trim variable expenses by 5 to 20 percent.

4. Use “carve-outs or “set-asides” for big ticket items and differentiate true wants from frivolous needs.

5. Calculate both income and expenses as a percentage of your total budget. Determine if there is a better way to allocate resources. Review the budget on a monthly basis to notice any variance. Determine if the variance was avoidable, unavoidable or a result of inaccurate assumptions. Take corrective action as needed.

6. Know the difference between saving and investing. Savers tend to be risk adverse while investors understand risk and take steps to mitigate it. Watch mutual fund commissions and investment advisory fees, which cut into return-rates. Keep investments simple and diversified (stocks, bonds, cash, index, no-load mutual and exchange traded funds, etc.).

Sooner or later, despite the best of budgeting intentions, something will go awry. A doctor will be terminated or may be the victim of a reduction-in-force (RIF) because of cost containment initiatives.4 A medical practice partnership may dissolve or a local hospital or surgery center may close, hurting your practice and livelihood. Someone may file a malpractice lawsuit against you, a working spouse may be laid off or you may get divorced. Regardless of the cause, budgeting crisis management encompasses two different perspectives: awareness and execution.

First, if you become aware that you may lose your job, the following proactive steps will be helpful to your budget and overall financial condition.

• Decrease retirement contributions to the required minimum for company/practice match. • Place retirement contribution differences in an after-tax emergency fund. • Eliminate unnecessary payroll deductions and deposit the difference to cash. • Replace group term life insurance with personal term or universal life insurance. • Take your old group term life insurance policy with you if possible. • Establish a home equity line of credit to verify employment. • Borrow against your pension plan only as a last resort.

If you have lost your job or your salary has been depressed, negotiate your departure and get an attorney if you believe you lost your position through breach of contract or discrimination. Then execute the following steps to recalculate your budget and boost your wealth rebuilding activities.

• Prioritize fixed monthly bills in the following order: rent or mortgage; car payments; utility bills; minimum credit card payments; and restructured long-term debt.

• Consider liquidating assets to pay off debts in this order: emergency fund, checking accounts, investment accounts or assets held in your children’s names.

• Review insurance coverage and increase deductibles on homeowner’s and automobile insurance for needed cash.

• Then sell appreciated stocks or mutual funds; personal valuables such as furnishings, jewelry and real estate; and finally, assets not in pension or annuities if necessary.

• Keep or rollover any lump sum pension or savings plan distribution directly to a similar savings plan at your new employer, if possible, when you get rehired.

• Apply for unemployment insurance.

• Review your medical insurance and COBRA coverage after a “qualifying event” such as job loss, firing or even after quitting. It is a bit expensive due to a 2 percent administrative fee surcharge but this may be well worth it for those with preexisting conditions or who are otherwise difficult to insure. One may continue COBRA for up to 18 months.

• Consider a high deductible Health Savings Account (HSA), which allows tax-deferred dollars like a medical IRA, for a variety of costs not normally covered under traditional heath insurance plans. Self-employed doctors deduct both the cost of the premiums and the amount contributed to the HSA. Unused funds roll over until the age of 59½, when one can use the money as a supplemental retirement benefit.

• Eliminate unnecessary variable, charitable and/or discretionary expenses, and become very frugal.

Final Notes

The behavioral psychologist, Gene Schmuckler, PhD, MBA, sometimes asks exasperated doctors to recall the story of the old man who spent a day watching his physician son treating HMO patients in the office. The doctor had been working at his usual feverish pace all morning. Although he was working hard, he bitterly complained to his dad that he was not making as much money as he used to make. Finally, the old man interrupted him and said, “Son, why don’t you just treat the sick patients?” The doctor-son looked at his father with an annoyed expression and responded, “Dad, can’t you see, I do not have time to treat just the sick ones.”

Always remember to add a bit of emotional sanity into your budgeting and economic endeavors.

Regardless of one’s age or lifestyle, the insightful doctor realizes that it is never too late to take control of a lost financial destiny through prudent wealth building activities. Personal and practice budgeting is always a good way to start the journey.

NOTE: Dr. Marcinko is a former Certified Financial Planner and current Certified Medical Planner™. He has been a medical management advisor for more than a decade. He is the CEO of http://www.MarcinkoAssociates.com

The authors acknowledge the assistance of Mackenzie H. Marcinko PhD in the preparation of this article.

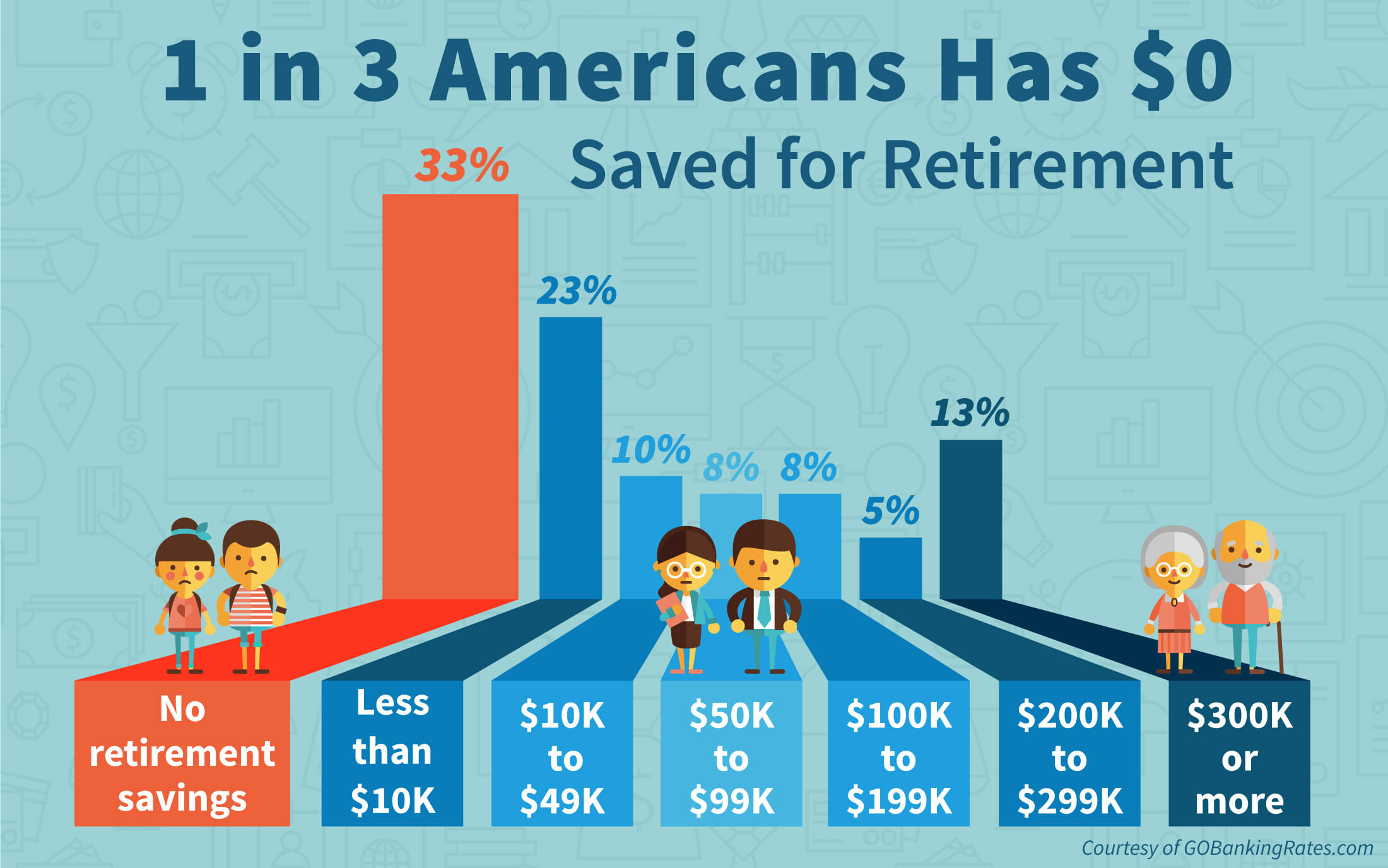

According to the National Institute on Retirement Security, almost 40 million households have no retirement savings at all. The Employee Benefit Research Institute (EBRI) estimates in its 2019 Retirement Security Projection Model that America’s current retirement savings deficit is $3.8 trillion.

What does that mean? Well, the EBRI report aggregates the savings deficit of all U.S. households headed by someone between the ages of 35 and 64, inclusive. In total, those households have $3.8 trillion fewer dollars in savings than they should have for retirement.

For more recent data, Fidelity Investments reported that in the third quarter of 2022 the average account balance for an IRA was $101,900. Employees with a 401(k) averaged $97,200, while those with a 403(b) had $87,400.

Fidelity also estimated that “an average retired couple age 65 in 2022 may need approximately $315,000 saved (after tax) to cover health care expenses in retirement.” Keeping in mind that more Americans are also living longer than ever before, they will face more challenges to cover medical expenses in retirement.

Posted on October 17, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Authors of the seminal textbook Why Nations Fail, Daron Acemoglu, James Robinson, and former International Monetary Fund chief economist Simon Johnson will split the roughly $1 million cash prize for their research, which found a link between a country’s prosperity and the institutions it established during European colonization.

Places developed either “inclusive” or “extractive” institutions based on population density. The former allowed for inclusive governance (i.e., democracy), while the latter extracted resources to benefit a small group of elites.

Countries that developed inclusive institutions have experienced long-term prosperity; those with exclusive institutions haven’t. “Broadly speaking, the work that we have done favors democracy,” Acemoglu said.

Eample: In the twin cities of Nogales, on the US-Mexico border, the north and south parts of the transborder city have the same climate and the same resources, but the section in the US is far richer because of the country’s institutions, according to the researchers.

Critics. Some academics argue the Nobel winners’ premise ignores the effects of culture on prosperity. Others point to an irrefutable counterexample: China continues to experience explosive growth despite having an autocratic government.

A class action lawsuit has been filed in Minnesota against UnitedHealth Group (NYSE:UNH) over allegations that the health insurer and its subsidiary, NaviHealth, used a faulty algorithm to deny rehabilitation care for Medicare Advantage beneficiaries. California-based Clarkson Law Firm filed the lawsuit in the U.S. District Court of Minnesota on Tuesday following an investigative report published by the health-focused news site Stat.

It alleges that UnitedHealth and its subsidiary, NaviHealth, used the computer algorithm named nH Predict to “systematically deny claims” of patients recovering from debilitating illnesses in nursing homes. According to the lawsuit, despite its 90% error rate, the company used the algorithm to deny claims, knowing that only 0.2% would appeal its decision. According to Stat, Humana (HUM), the nation’s second-largest player in the Medicare Advantage market behind UnitedHealth (UNH), also uses nH Predict. UnitedHealth (UNH) denied it used the NaviHealth predict tool to arrive at coverage decisions.

***

***

Ironically, UnitedHealth’s (NYSE:UNH) Optum Rx unit announced plans to move eight insulin products to “preferred” status on formularies to further expand the number of patients benefiting from $35 or less monthly out-of-pocket costs for the lifesaving therapy.

Optum Rx, UNH’s pharmacy benefit manager (PBM), said that effective January 1, 2024, all short- and rapid-acting insulins will move to Tier 1 in commercial formularies, a list of drugs the company maintains to indicate coverage for insured patients.

Posted on October 9, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

ByNeal Baum MD

***

There’s a saying by John Wanamaker who pontificated, “Half the money I spend on advertising is wasted; the trouble is, I don’t know which half”.

Today you have opportunities to determine which parts of your marketing efforts are effective and what is wasted. However, you have to measure your marketing results.

This article will discuss marketing metrics and how to use them to get the best bang for your marketing buck.

***

***

The cost per acquisition (CPA)

Not all initial phone callers to a medical practice will convert to paying patients. The 50 patients who made appointments can be plugged into the equation, i.e., campaign costs divided by patients who became paying patients or $2,000 divided by 50 equals $40, representing the patient acquisition cost (PAC).

Now, if each patient who entered the practice spends $800 over the patient’s lifetime, that’s an increase in income of $40,000, not shabby for $2,000 in marketing expenses.

Source: Neil Baum, MD, Physicians Practice [8/26/22]

Posted on October 8, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

October continues to be a tough month for stocks, with all three major indexes spending yesterday afternoon in the red. The Dow in particular had a horrible day and dropped over 500 points, while major tech stocks were pushed lower by a series of analyst downgrades.

Oil continued its hot streak yesterday, rising above $77 on the back of geopolitical conflict in the Middle East. That helped ensure that, while everything else fell, energy was the only positive sector in the S&P 500.

Gold has often found itself rising in tandem with crude, though it broke that habit, with the shiny safe haven dropping a hair as investors digest the idea that the Fed’s next interest rate cut may be smaller than they thought.

Bitcoin broke above $64,000 for a moment yesterday only to be yanked back down, as crypto traders ride out the recent volatility.

Posted on October 4, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

IN PRIVATE EQUITY AND MEDICINE

By Staff Reporters

***

***

PRIVATE EQUITY

In private equity, the J curve is used to illustrate the historical tendency of private equity funds to deliver negative returns in early years and investment gains in the outlying years as the portfolios of companies mature.

And, according to Wikipedia, in the early years of the fund, a number of factors contribute to negative returns including management fees, investment costs and under-performing investments that are identified early and written down. Over time the fund will begin to experience unrealized gains followed eventually by events in which gains are realized (e.g., IPOs, mergers and acquisitions, leveraged recapitalizations).

Historically, the J curve effect has been more pronounced in the US, where private equity firms tend to carry their investments at the lower of market value or investment cost and have been more aggressive in writing down investments than in writing up investments. As a result, the carrying value of any investment that is under performing will be written down but the carrying value of investments that are performing well tend to be recognized only when there is some kind of event that forces the PE to mark up the investment.

The steeper the positive part of the J curve, the quicker cash is returned to investors. A private equity firm that can make quick returns to investors provides investors with the opportunity to reinvest that cash elsewhere. Of course, with a tightening of credit markets, private equity firms have found it harder to sell businesses they previously invested in. Proceeds to investors have reduced. J curves have flattened dramatically. This leaves investors with less cash flow to invest elsewhere, such as in other private equity firms. The implications for private equity could well be severe. Being unable to sell businesses to generate proceeds and fees means some in the industry have predicted consolidation among private equity firms.

MEDICINE

In medicine, the “J curve” refers to a graph in which the x-axis measures either of two treatable symptoms (blood pressure or blood cholesterol level) while the y-axis measures the chance that a patient will develop cardiovascular disease (CVD). It is well known that high blood pressure or high cholesterol levels increase a patient’s risk.

Paradoxically, what is less well known is that plots of large populations against CVD mortality often take the shape of a J curve which indicates that patients with very low blood pressure and/or low cholesterol levels are also at increased risk.

Posted on October 1, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

On August 31, 2024, the California legislature passed a bill that may curb private equity (PE) healthcare transactions in the state. The legislation is now on Governor Gavin Newsom’s desk for signature, who must sign or veto the bill by September 30, 2024. If signed into law, California will have the strictest regulation of PE deals of any state in the country.

Posted on September 29, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Markets: Wall Street life was looking good last week as all the major indexes clinched their third consecutive winning week. Stocks were a mixed bag for Friday, but the Dow Jones scored another record close. Bristol Myers Squibb rose after the FDA approved its schizophrenia drug as the first new treatment for the condition in decades.

Economy: The FOMC’s favorite inflation gauge came in lower than expected for last month, likely clearing the way for Jerome Powell and the Federal Reserve to keep cutting interest rates.

Echoing Elon Musk and my colleague medical Michael Burry MD has warned about American consumers’ debt woes.

Echoing the likes of Tesla’s Elon Musk and “The Big Short” investor Michael Burry, a veteran economist has warned that American households have racked up historic amounts of debt — and the economy will pay the price.

“Consumers are just waking up to the fact that they’re financing their spending by running up their credit cards, and that the interest on those credit cards is over the top, out of control, and off the hook right now,” Carl Weinbergtold CNBC. Record credit-card debt threatens to spark a consumer-spending slowdown soon, Carl Weinberg said.

“That’s going to lead to a retrenchment in consumer spending as we get into the new year” the chief economist at High Frequency Economics said. Weinberg expects the US economy to cool but not slide into recession, and he sees inflation fading.

PS: Mike Burry contributed to our 800 page textbook on investing for physicians.

Once the value of all personal assets and liabilities is known, net worth can be determined with the following formula: Net worth = assets minus liabilities. Obviously, higher is better.

In The Millionaire Next Door, Thomas H. Stanley, PhD, and William H. Danko give the following benchmark for net worth accumulation. Although conservative for physicians of a past generation, it may be more applicable in the future because of current managed care environment. Here is the guide: Multiple your age by your annual pre-tax income from all sources; except inheritances, and then divide by ten.

Example:

As an HMO pediatrician, Dr. Curtis earned $ 90,000 last year. So, if she is 35, her net worth should be at least $ 315,000.

How do you get to that point? In a word, consume less and save more. Stanley and Danko found that the typical millionaire set aside 15 percent of earned income annually and has enough invested to survive 10 years, at current income levels if he stopped working.

Question: If Dr. Curtis lost her job tomorrow, how long could she pay herself the same salary? Could you?

Posted on September 19, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The Russell 2000 Index is a stock market index that measures the performance of the 2,000 smaller companies included in the Russell 3000 Index. The Russell 2000 is managed by London’s FTSE Russell Group, widely regarded as a bellwether of the U.S. economy because of its focus on smaller companies in the U.S. market.

As of 31st December 2022, the weighted average market capitalization of a company in the index is approximately $2.76 billion and the median market capitalization is approximately $950 million. The market capitalization of the largest company in the index is approximately $8.1 billion. It first traded above the 1,000 level on May 20th, 2013, and above the 2,000 level on December 23rd, 2020.

Similar small-cap indices include the S&P 600 from Standard & Poor’s, which is less commonly used, along with those from other financial information providers.

Posted on September 18, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

BREAKING NEWS

***

***

Jerome Powell and the Federal Reserve Bank just said that it is cutting its benchmark interest rate by 0.50 percentage points, marking the first reduction in four years and moving to ease borrowing costs as inflation-weary consumers are grappling with high rates on everything from mortgages to credit cards.

It is the first drop in the federal funds rate — or what banks charge each other for short-term loans — since the U.S. central bank lowered rates to nearly zero in March 2020 amid an economic standstill caused by the pandemic.

But as prices surged during the health crisis, the FOMC repeatedly hiked rates into a target range of 5.25% to 5.5%, the highest in 23 years, in an effort to curb inflation.

Posted on September 18, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

At 2 pm EST Today

By Staff Reporters

***

***

ABOUT THE FEDERAL OPEN MARKET COMMITTEE

The term “monetary policy” refers to the actions undertaken by a central bank, such as the Federal Reserve, to influence the availability and cost of money and credit to help promote national economic goals. The Federal Reserve Act of 1913 gave the Federal Reserve responsibility for setting monetary policy.

The Federal Reserve controls the three tools of monetary policy–open market operations, the discount rate, and reserve requirements. The Board of Governors of the Federal Reserve System is responsible for the discount rate and reserve requirements, and the Federal Open Market Committee is responsible for open market operations. Using the three tools, the Federal Reserve influences the demand for, and supply of, balances that depository institutions hold at Federal Reserve Banks and in this way alters the federal funds rate. The federal funds rate is the interest rate at which depository institutions lend balances at the Federal Reserve to other depository institutions overnight.

Changes in the federal funds rate trigger a chain of events that affect other short-term interest rates, foreign exchange rates, long-term interest rates, the amount of money and credit, and, ultimately, a range of economic variables, including employment, output, and prices of goods and services.

And so, the macroeconomic FOMC is kicking off at 2pm ET today, when the Fed will announce the first interest rate cut in over four years. But, financial watchers are split between two predictions: a standard 0.25% cut or a more aggressive one of 0.5% (investors are betting on the latter, while many analysts think the former).

Regardless of its size, today’s rate cut and subsequent ones are expected to make borrowing cheaper for consumers and businesses, with ripple effects throughout the economy.

Posted on September 15, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

What a difference a week makes: The S&P 500 and the NASDAQ just had their best weeks of the year—only one week after suffering their worst weeks of 2024. Investors are gaining confidence as they wait for the Federal Reserve and Jerome Powell to cut interest rates next week.

Warner Bros. Discovery jumped following the news that it clinched a renewal deal with Charter Communications that’ll give the cable company’s subscribers access to its streamer Max.

Posted on September 11, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

It’s the most wonderful time of the year – Survey Season! Beginning in late May each year, numerous industry normative benchmark physician production and compensation surveys begin publishing the most recent year’s reports. These healthcare and specialty specific surveys annually report specific types of physician compensation and productivity metrics across the country for various specialties and are widely used by hospitals, physician practices, and healthcare compensation and valuation experts, are often used for the determination of Fair Market Value (FMV) physician compensation for regulatory compliance purposes.