BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

The Financial Times reports that the ChatGPT-maker is discussing changing its corporate structure, which currently has it governed by a nonprofit entity, to make it more attractive to investors as the company works to complete a funding round that values it at $100 billion.

Crowdfunding is a popular way to raise money online. People often use crowdfunding to fund raise for a business, for charity, or for gifts. It’s important to know that money raised through crowdfunding may be taxable.

Do you have to pay taxes on the money you receive from GoFundMe, etc?

Generally, you will not owe taxes on donated funds you receive from a crowdfunding platform. The IRS considers the money received from GoFundMe to be a gift instead of income, so it is typically not taxable. A gift is any transfer of cash or property you make to an individual without receiving full consideration in return, according to the IRS. People who donate money to GoFundMe to help pay for medical expenses are typically doing it out of generosity and do not expect anything in return.

Some money raised through crowdfunding may NOT be considered a gift.

Under federal tax law, gross income includes all income from any source, unless it’s excluded from gross income by law. In most cases, gifts aren’t included in the gross income of the person receiving the gift. Here’s what people involved in crowdfunding should know:

If a crowdfunding organizer is raising money on behalf of others, the money may not be included in the organizer’s gross income, as long as the organizer gives the money to the person for whom they organized the crowdfunding campaign.

If people donate to a crowdfunding campaign out of generosity and without expecting anything in return, the donations are gifts. Therefore, they will not be included in the gross income of the person for whom the campaign was organized.

However, not all contributions to crowdfunding campaigns are gifts and may be taxable.

When employers give to crowdfunding campaigns for an employee, those contributions are generally included in the employee’s gross income.

Taxpayers may want to consult a trusted tax pro for information and advice regarding how to treat amounts received from crowdfunding campaigns.

Beside market, limit and stop orders, there are some other miscellaneous orders for the physician or guided investor, to know:

A stop limit order is a stop order that, once triggered or activated, becomes a limit order. Realize that it is possible for a stop limit to be triggered and not executed, as the limit price specified by the doctor may not be available.

In addition, there are all or none and fill or kill orders, and even though both require the entire order to be filled, there are distinct differences. An all or none (AON) is an order in which the broker is directed to fill the entire order or none of it.

A fill or kill (FOK) is an order either to buy or to sell a security in which the broker is directed to attempt to fill the entire’ amount of the order immediately and in full, or that it be canceled.

The difference between an all or none and a fill or kill order is that with an all or none order, immediate execution is not required, while immediate execution is a critical component of the fill or kill. Because of the immediacy requirement,

FOK orders are never found on the specialist’s book. Another difference is that AON orders are only permitted for bonds, not stocks, while FOK orders may be used for either.

Also, there exists an immediate or cancel order (IOC), which is an order to buy or sell a security in which the broker is directed to attempt to fill immediately as much of the order as possible and cancel any part remaining. This type of order differs from a fill-or-kill order which requires the entire order to be filled. An IOC order will permit a partial fill. Because of the immediacy requirement, IOC and FOK orders are never found on the specialist’s book.

Long and Short Positions

A long buy position means that shares are for sale from a market makers inventory or owned by the medical investor outright. Market makers take long positions when customers and other firms wish to sell, and they take short positions when customers and other firms want to buy in quantities larger than the market maker’s inventory. By always being ready, willing, and able to handle orders in this way, market makers assure the investing public of a ready market in the securities in which they are interested. When a security can be bought and sold at firm prices very quickly and easily the security is said to have a high degree of liquidity, also known as marketability.

A short position investor seeks to make a profit by participating in the decline in the market price of a security.

Now; let’s see how these terms, long and short, apply to transactions by medical investors [rather than market makers] in the securities markets.

When a doctor buys any security – he is said to be taking a long position in that security. This means the investor is an owner of the security. Why does a doctor take a long position in a security? Well, receiving dividend income to make a profit from an increase in the market price is one reason. Once the security has risen sufficiently in price to satisfy the investor’s profit needs, the investor will liquidate his long position, or sell his stock. This would officially be known as a long sale of stock, though few people in the securities business use the label “long sale”. This is the manner in which the above investor had made a profit is the traditional method used; buy low, sell high.

Let’s look at an actual investment in General Motors to investigate this principle further. A medical investor has taken a long position in 100 shares of General Motors stock at a price of $70 per share. This means that the manner in which he can do that is by placing a market order which will be executed at the best “available market price at the time, or by the placing of a buy limit order with a limit price of $70 per share. The investor firmly believes, on the basis of reports that he has read about the automobile industry and General Motors specifically, that at $70 a share, General Motors is a real bargain. He believes that based on its current level of performance, it should be selling for a price of between $80 and $85 per share. But, the doctor investor has a dilemma. He feels certain that the price is going to rise but he cannot watch his computer, or call his broker, every hour of every day. The reason he can’t watch is because patients have to be seen in the office. The only people who watch a computer screen all day are those in the offices of brokerage firms (stock broker registered representatives), and doctor day traders, among others.

In the above example, with a sell limit order, if the doctor investor was willing to settle for a profit of $12 per share, what order would he place at this time? If you said, “sell at $82 good ’til canceled”, you are correct. Why GTC rather than a day order? Because our doctor investor knows that General Motors is probably not going to rise from $70 to $82 in one day. If he had placed an order to sell at $82 without the GTC qualification, his order would have been canceled at the end of this trading day. He would have had to re-enter the order each morning until he got an execution at 82. Marking the order GTC (or open) relieves him of any need to replace the order every morning. Several weeks later, when General Motors has reached $82 per share in the market, his order to sell at 82 is executed. The medical investor has bought at 70 and sold at 82 and realized a $12 per share profit for his efforts.

Let’s suppose that the medical investor, who has just established a $12 per share profit, has evaluated the performance of General Motors common stock by looking at the market performance over a period of many years. Let’s further assume that the investor has found by evaluating the market price statistics of General Motors that the pattern of movement of General Motors is cyclical. By cyclical, we mean that it moves up and down according to a regular pattern of behavior.

Let’s say the investor has observed that in the past, General Motors had repeated a pattern of moving from prices in the $60 per share range as a low, to a high of approximately $90 per share. Further, our investor has observed that this pattern of performance takes approximately 10 to l2 months to do a full cycle; that is, it moves from about 60 to about 90 and back to about 60 within a period of roughly l2 months. If this pattern repeats itself continually, the investor would be well advised to buy the stock at prices in the low to mid 60’s hold onto it until it moves well into the 80’s, and then sell his long position at a profit. However, what this means is that our investor is going to be invested in General Motors only 6 months of each year. That is, he will invest when the price is low and, usually within half a year, it will reach its high before turning around and going back to its low again. How can the doctor-investor make a profit not only on the rise in price of General Motors in the first 6 months of the cycle, but on the fall in price of General Motors in the second half of the cycle? One technique that is available is the use of the short sale.

The Short Sale

If a doctor investor feels that GM is at its peak of $ 90 per share, he may borrow 100 shares from his brokerage firm and sell the 100 shares of borrowed GM at $ 90. This is selling stock that is not owned and is known as a short sale. The transaction ends when the doctor returns the borrowed securities at a lower price and pockets the difference as a profit. In this case, the doctor investor has sold high, and bought low.

Odd Lots

Most of the thousands of buy and sell orders executed on a typical day on the NYSE are in 100 share or multi-100 share lots. These are called round lots. Some of the inactive stocks traded at post 30, the non-horseshoe shaped post in the northwest corner of the exchange, are traded in 70 share round lots due to their inactivity. So, while a round lot is normally 700 shares, there are cases where it could be 10 shares. Any trade for less than a round lot is known as an odd lot. The execution of odd lot orders is somewhat different than round lots and needs explanation.

When a stock broker receives an odd lot order from one of his doctor customers, the order is processed in the same manner as any other order. However, when it gets to the floor, the commission broker knows that this is an order that will not be part of the regular auction market. He takes the order to the specialist in that stock and leaves the order with the specialist. One of the clerks assisting the specialist records the order and waits for the next auction to occur in that particular stock. As soon as a round lot trade occurs in that particular stock as a result of an auction at the post, which may occur seconds later, minutes later, or maybe not until the next day, the clerk makes a record of the trade price.

Every odd lot order that has been received since the last round lot trade, whether an order to buy or sell, is then executed at the just noted round lot price, the price at which the next round lot traded after receipt of the customer’s odd lot order, plus or minus the specialist’s “cut “. Just like everything else he does, the specialist doesn’t work for nothing. Generally, he will add 1/8 of a point to the price per share of every odd lot buy order and reduce the proceeds of each odd lot sale order by 1/8 per share. This is the compensation he earns for the effort of breaking round lots into odd lots. Remember, odd lots are never auctioned but, there can be no odd lot trade unless a round lot trades after receipt of the odd lot order.

Posted on August 30, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

DEFINITION: Consumer confidence index (CCI) is a standardized confidence indicator providing an indication of future developments of households’ consumption and saving.

The index is based upon answers regarding household’s expected financial situation, their sentiment about the general economic situation, unemployment and capability of savings. An indicator above 100 signals a boost in the consumers’ confidence towards the future economic situation, as a consequence of which they are less prone to save, and more inclined to spend money on major purchases in the next 12 months. Values below 100 indicate a pessimistic attitude towards future developments in the economy, possibly resulting in a tendency to save more and consume less.

The decline in inflation and the expectation of an imminent interest rate cut have Americans feeling better about the economy than they have in a while, according to the latest update of the Conference Board’s consumer confidence index [CCI].

On the other hand, consumers are worried about the softening labor market. While the unemployment rate remains below historical standards at 4.3%, it has increased for four straight months—likely enough to convince J. Powell and the Federal Reserve to cut rates in September.

Posted on August 19, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

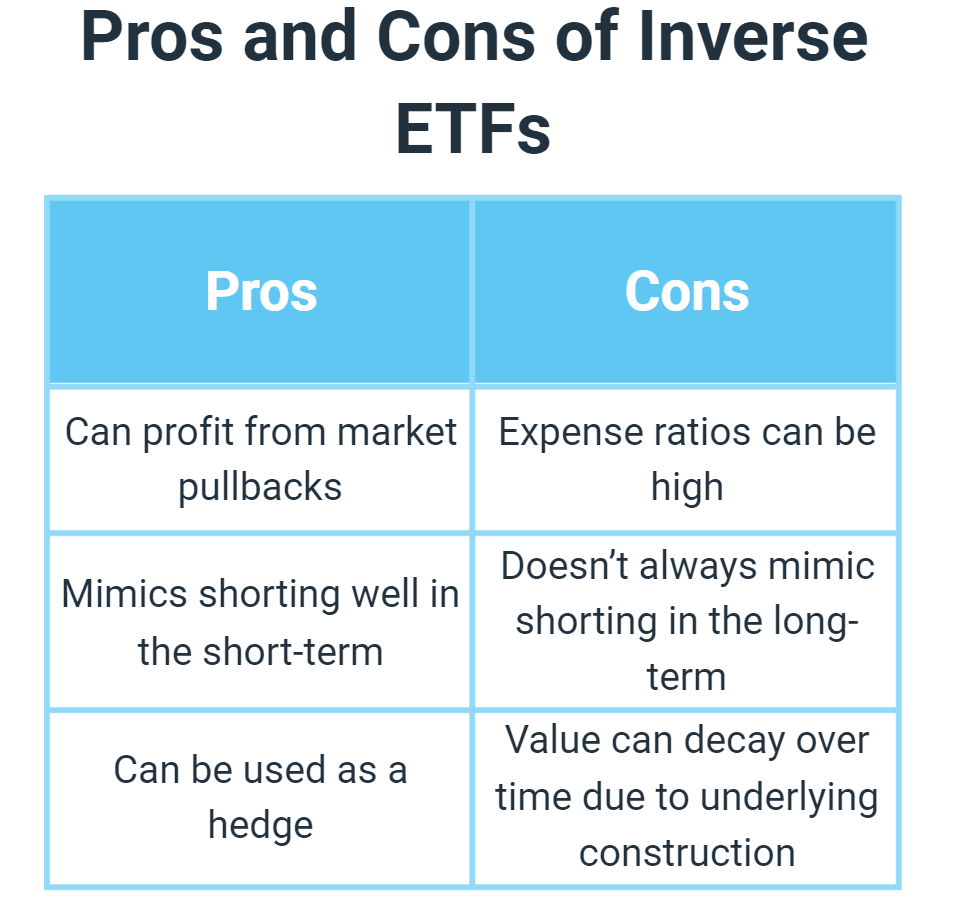

What are inverse ETFs?

An inverse ETF, often known as a bear or short ETF, is an exchange-traded fund designed to profit from a market decline. These short-term, publicly traded investments are utilized by investors who believe that a particular market or individual security will lose value in the near future. They may use inverse ETFs as a way of hedging losses during a downturn.

“Inverse ETFs are a tool to hedge a stock portfolio,” according to John DeYonker. “If the S&P 500 is your benchmark, and it goes up 1%, then your hedge will go down 1% and vice versa. Hedging with inverse ETFs can reduce volatility for investors—it’s like insurance.”

Investors may also use inverse ETFs as a way to take advantage of a predicted decline. In this way, they may be used as an alternative to short selling. For example, if an investor believes that the oil industry will have a setback in the immediate future, they may choose to purchase an inverse ETF of securities tied to energy producers. If correct in their prediction, the investor’s inverse ETF may recognize a profit. If the investor is incorrect, and the market or individual security increases in price, they may see a loss.

An investor who believes that the S&P 500 will decline, for example, may choose to purchase shares of the ProShares Short S&P 500. This inverse ETF’s value is inversely proportional to the overall S&P 500 index.

Inverse ETFs are generally considered to be highly volatile investments, as their losses typically compound daily. This makes inverse ETFs more risky than the index to which they are tied.

Posted on August 17, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Visa and Mastercard agree to $30 billion deal to cap credit card swipe fees

By Staff Reporters

***

***

After a nearly 20-year legal battle, the credit card behemoths said they’ll slightly reduce the 2% fees that they charge retailers every time a consumer uses one of their cards.

Retailers will also be able to adjust prices at checkout depending on the type of card used. The banks that issue cards—like JPMorgan Chase, Citigroup, and Bank of America—will likely bear the brunt of the changes, as they typically receive most of the revenue from swipe fees.

Posted on August 16, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The S&P 500 index rose 88.02 points (1.61%) to 5,543.23; the Dow Jones Industrial Average® ($DJI) added 554.67 points (1.39%) to 40,563.06; the NASDAQ Composite advanced 401.89 points (2.34%) to 17,594.50.

The 10-year Treasury note yield (TNX) rebounded about 10 basis points to nearly 3.93%, lifted by strong U.S. data.

The CBOE Volatility Index® (VIX) finished at 15.45, the lowest since July 23 and back under the historic average near 19.

Posted on August 14, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The Fierce Healthcare team recapped second quarter earnings for the country’s biggest payers and health tech companies. See how UnitedHealth, CVS, Talkspace and Health Catalyst fared.

And … Texas Children’s Hospital reduced its workforce by 5%, or approximately 1,000 jobs. Keep up with other cuts with Fierce Healthcare’s layoff tracker.

The S&P 500® index (SPX)rose 90.04points (1.68%) to 5,434.43; the Dow Jones Industrial Average® ($DJI) added 408.63 points (1.04%) to 39,765.64; the NASDAQ Composite®($COMP)rallied406.99points (2.43%) to 17,187.61.

The 10-year Treasury note yield (TNX) fell about six basis points to 3.85%.

The CBOE Volatility Index dropped nearly 13% to 18.04, its lowest close since July 31.

Every S&P sector besides energy finished higher today, with info tech and consumer discretionary in the lead and both gaining more than 2%.

Visualize: How private equity tangled banks in a web of debt, from the Financial Times.

Posted on August 8, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

You might be affected by one of the biggest data breaches ever and not even know it. A recent class action lawsuit filed against Jerico Pictures Inc., a background check company that does business under the name National Public Data, claims that the company was breached by hackers earlier this year.

The SPX dipped 40.5 points (0.8%) to 5,199.5; the Dow Jones Industrial Average® ($DJI) fell 234.2 points (0.6%) to 38,763.45 the NASDAQ Composite ($COMP) fell 171 points (1.1%) to 16,195.8.

The 10-year Treasury note yield (TNX) rose to 3.96%.

Fortinet skyrocketed 25.30% after the cybersecurity company posted strong second-quarter earnings that only served to underline its potential as a CrowdStrike alternative.

Lumen Technologies continued to power higher, rising another 32.90% today as the investors poured money into the telecom due to its AI business boom.

Shopify tore 17.80% higher after posting a beat-and-raise earnings report highlighted by strong demand despite weak consumer spending.

Lyft drove 17.23% lower in spite of strong ridership in the second quarter. Shareholders, however, did not like management’s dour financial forecast for the third quarter.

CVS Health sank 3.19% after it slashed its profit guidance for the full year, though it also announced a new cost-cutting program.

TripAdvisor took a trip south today, falling 16.61% due to a mixed earnings report and dire warnings of lower revenue in the coming quarter.

Novo Nordisk sales thinned on Ozempic earnings miss. Shares of Danish pharmaceutical giant Novo Nordisk sank 8.27% today after the company missed expectations on its sales of popular weight-loss drugs Ozempic and Wegovy. Novo reported $1.7 billion in Wegovy sales, below the $2 billion analysts expected, while Ozempic sales came in $0.2 billion lower than analyst estimates. Overall, the company reported a net profit of $1.86 billion in the second quarter.

You can also listen to a professional narration of this article on iTunes & online.

Despite the S&P 500 showing gains in the mid-teens, the average stock on the market is either up slightly or flat for the year. Most of the gains in the index came from the Magnificent 7 stocks, which constitute 35% of the index! The equal-weighted index, where the Magnicent 7 have only a 1.4% weight, is up only about 4% this year (as of this writing).

The Magnificent 7 are starting to look like the Nifty Fifty stocks from the 1970s (Kodak, Polaroid, Avon, Xerox, and others) – stocks you “had to own” or you were left behind – until all your gains were taken away or you faced a decade or two of no returns. Forty years later, it’s easy to dismiss these companies as has-beens. They’ve all either gone bankrupt or become irrelevant.

But back then, they were the stars of corporate America, just like the Magnificent 7 are today. As an investor, it’s crucial to know which games you play and which ones you don’t.

Posted on July 26, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

What’s the difference between an IPO, a special purpose acquisition company (SPAC), and a direct listing?

[By staff reporters]

IPOs are a 6–12 month journey where a company works with investment banks and underwriters, who buy a bunch of shares and then sell them to investors in the public market during the actual IPO. Early investors are able to liquidate their shares, and the company raises new funds.

Direct listings skip the underwriting hullabaloo. But without that stability guarantee, direct listings can result in a more volatile opening. Some companies, like Coinbase, find that it’s worth it to keep their hard-earned money out of bankers’ hands.

SPACs, aka “blank-check companies,” offer yet another alternative path to public markets. A SPAC is a shell company that raises money through the traditional IPO process, then merges with a private company and takes it public.

Posted on July 26, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

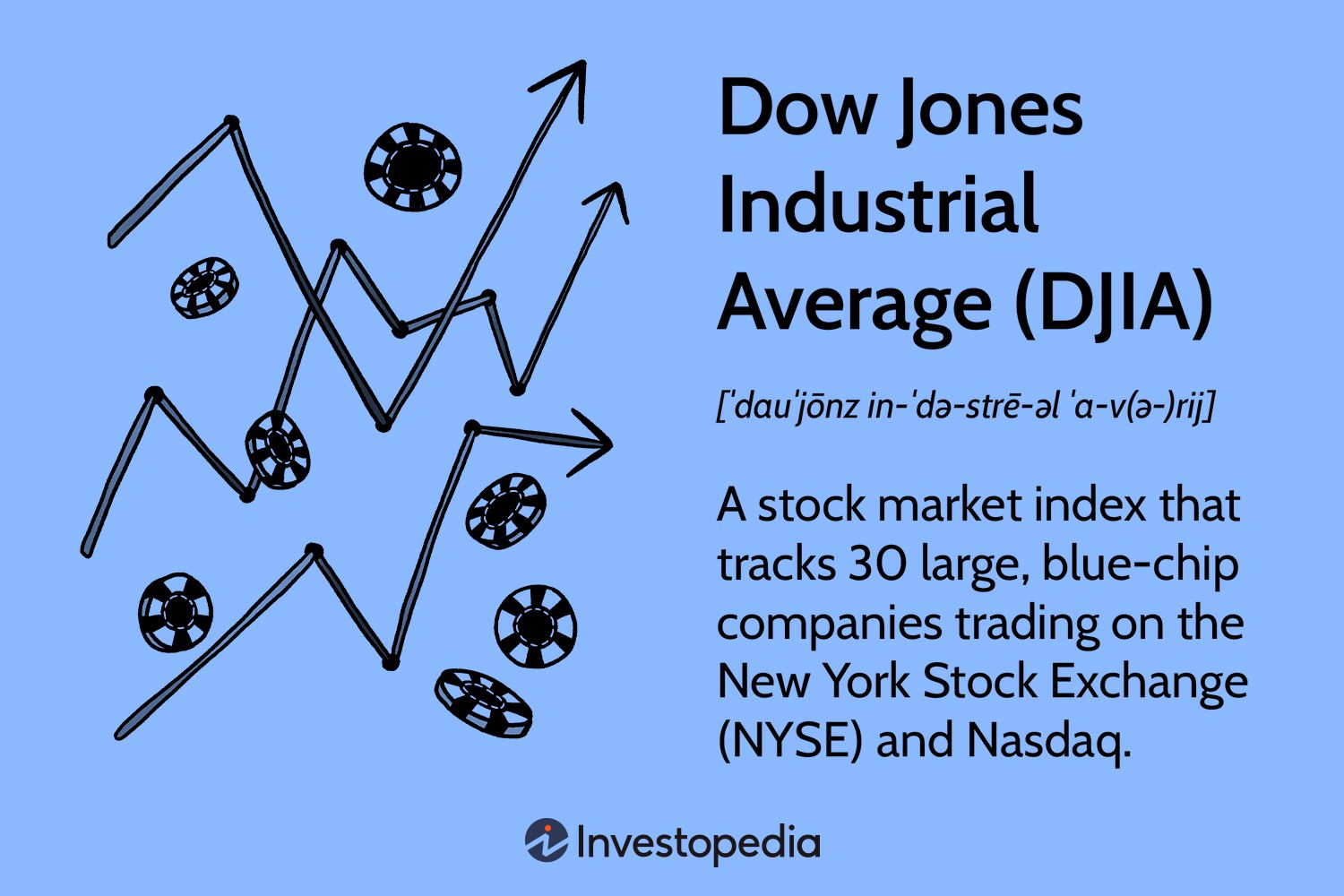

The Dow Jones Industrial Average is a collection of 30 “blue-chip” U.S. stocks. Blue chip = big, established, and influential companies like Microsoft, JPMorgan, Disney, and McDonald’s. The Dow recently updated its roster, swapping ExxonMobil, Pfizer, and Raytheon for Salesforce, biotech Amgen, and manufacturing heavyweight Honeywell.

The Dow is weighted by share price, so higher-priced stocks have more influence on the index’s total value. Price-weighting also means that if the price of any stock in the Dow changes by $1, it has the same impact on the index, even though a $1 increase to a stock worth $20 is more significant (relatively) than a $1 change to a stock worth, say, $40.

During stock splits—when a company increases its number of outstanding shares and chops prices by the same factor—a company’s influence in the Dow can fall even if their market value doesn’t change. The Dow has some mechanisms to account for stock splits, but they can still lead to a shakeup in the index (like what happened last summer).

At 124 years old, the Dow has had plenty of time to cement its reputation as a leading indicator of the stock market. But with only 30 stocks representing a smattering of U.S. corporate titans, it’s not exactly representative.

***

At one point the Dow Jones Industrial Average was up 585 points before it sold off later yesterday afternoon, though it wrapped the trading session with a small win. The S&P 500 fought its way into positive territory but struggled to stay there, eventually sinking into negative territory at the end of the day.

As for the NASDAQ, the tech selloff continued to punish the index for most of yesterday afternoon. Treasury yields fell a bit on positive GDP news, though the big PCE [personal consumption expenditures] announcement is the one investors have been waiting for.

Oil popped on a stronger than expected GDP reading, with traders banking on future economic growth and stronger oil demand.

Bitcoin sank a bit yesterday ahead of a major conference that could set the tone for the entire digital asset industry for years to come.

Posted on July 22, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Earnings announcements are a public statement of a company’s profitability for a specific period of time, such as a quarter (90 days) or a year. Equities research analysts will issue estimates of the company’s earnings numbers prior to its announcement date, which is generally set weeks or months in advance. If a company releases better results than analysts predict, its share price will generally rise after the announcement. Below you will find a list of public companies announcing their earnings results this week.

Earnings reports to feast on them this week. About one-quarter of S&P 500 companies will release their Quarter 2nd financials, including Alphabet, Coca-Cola, Tesla, UPS, Visa, Chipotle, Comcast, GM, and Southwest Airlines.

And if you have room for more economic data, the government will release its first estimate of Q2 GDP on Thursday and an important inflation gauge on Friday.

Posted on July 13, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

INFLATION EASING

By Staff Reporters

***

***

For the first time since May 2020, the average cost of goods and services in the US made like a remote worker with wanderlust and dipped last month, the Labor Department just reported in July 2024, bolstering confidence that inflation is easing.

Carried by softening gas and rent prices, the consumer price index (CPI) decreased 0.1% in June, beating economists’ forecasts of a 0.1% monthly increase.

That dip brought down the annual CPI, which also beat expectations, to record a 3% year over year gain in June—a one-year price growth low and a rate last seen in early 2021.

Average gas prices fell 3.8% in June, after dropping 3.6% in May.

Shelter prices, which account for about one-third of the CPI, only rose 0.2% in June as rents cooled. It was the category’s smallest monthly rise in three years.

Posted on July 11, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

More on DAFs

By Rick Kahler CFP®

In A Christmas Carol, Charles Dickens has a scene where two charity workers raising funds for the poor approach Ebenezer Scrooge on Christmas Eve.

” What shall I put you down for?” “Nothing!” Scrooge replied. “You wish to be anonymous?” “I wish to be left alone,” said Scrooge.”

Scrooge may not be alone in his desire to be left alone. With 60% of Americans supporting presidential candidates’ proposals for wealth taxes, financial transaction taxes, higher capital gains tax rates, and increases in income taxes, many of our affluent neighbors are just not feeling the love this Christmas.

Nevertheless, there are still millions more who want to give. Charitable giving, though, can be more complicated than it was in Scrooge’s time. For example:

Are you bunching your itemized deductions into every other year and would like to give a substantial amount to charities this year, but you haven’t had time to research which charity you want to support or you want to spread the giving out over time as opposed to giving it all this month?

Do you support a number of charities and would like to support even more, but find the IRS requirements for documenting your gifts to be burdensome?

Would you like to set aside a sum of money for your favorite charities that could generate an annual income forever, but forming a foundation or charitable trust is beyond your reach?

All the above are possible with a donor-advised fund.

Let’s say you wanted to give small amounts to fifty different charities. Rather than write fifty checks and obtain fifty receipts, you can make one gift to the fund, which distributes the money to the fifty charities. You only have to provide one receipt to the IRS.

You can also make a charitable gift to the donor-advised fund that qualifies as a deduction on your 2019 tax return, but you can delay the distribution of the funds until sometime in the future. This gives you time to explore the various causes you may want to support.

What really sets a donor-advised fund apart from other types of charitable giving is that you can decide how your donations are used, much as you would if you set up your own foundation. You can even create either an endowed or a non-permanent fund for a particular purpose, such as a specifically-designated scholarship fund in memory of a loved one.

***

***

Case Example:

One example of a donor-advised fund is the Black Hills Area Community Foundation. The BHACF supports scores of local charities and special projects. However, almost all financial institutions like Fidelity, TD Ameritrade, and Schwab have relationships with donor-advised funds.

While DAFs create an easy-to-establish, low-cost, flexible vehicle for charitable giving as an alternative to an expensive and complex private foundation, they are not hassle-free or without costs. Many charge a combination of fixed quarterly fees and an annual percentage of the undistributed funds. There is also a reasonable amount of administrative work involved. One DAF that I use assesses a penalty of $500 if the account is closed in under a year. They work best when a person anticipates significant contributions and a long-term giving plan.

Every donor-advised fund has different charities, minimums, processes, and costs, so it’s important to do your homework. Research whether the fund approves of the charities you want to support, as well as the costs involved.

Assessment

A donor advised fund may be a good way to take a large deduction this year, reduce the administrative hassles and costs of setting up a foundation, and still give to causes you choose to support.

Your thoughts are appreciated.

BUSINESS, FINANCE, INVESTING AND INSURANCE TEXTS FOR DOCTORS:

Private equity and venture capital investments typically involve ownership of shares in a company and represent title to a portion of the company’s future earnings. However, private equity is an equity interest in a company or venture whose stock is not yet traded on a stock exchange.

Venture capital is typically a special case of private equity in which the investment is in a company or venture that has little financial history or is embarking on a high risk/high potential reward business strategy.

Like real estate, private equity and venture capital investments generally share a general lack of liquidity and a lack of comparability across different individual investments. The lack of liquidity comes from the fact that private equity and venture capital investments are typically not tradable on a stock exchange until the company has an IPO.

The lack of comparability is due to the fact that most private equity and venture capital investments are the result of direct negotiation between the investor/venture capitalist and the existing owners of the company /venture.

With widely divergent terms and provisions across different investments, it is difficult to make general claims regarding the characteristics of private equity and venture capital investments.

Posted on July 5, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Vitaliy Katsenelson CFA

***

*** Today I am sharing with you an excerpt from a letter I wrote to IMA clients in the winter of 2023.

I discussed my condensed views on the stock market, economy, and our investment strategy. I think it is a good overview of where we are still today, almost a year and a half later. If you’ve read it before, skip to the end, where I share my updated thoughts on the Magnificent Seven and Nvidia.

Posted on July 2, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Employers expect health benefit costs to rise by more than 5% on average in 2024 as factors like high inflation, health labor shortages, and expensive new therapies put pressure on plan spending after years of 3%–4% annual growth, early data suggests.

Preliminary results from Mercer’s 2023 National Survey of Employer-Sponsored Health Plans found that total health benefit costs could increase by as much as 6.6% per employee if companies do nothing to control spending, or an average of 5.4% if employers take steps to hold down costs.

That slight gap suggests most employers don’t plan to make cost-cutting changes to their plans—likely due to concerns about healthcare affordability, the analysis noted. Many large companies (with 500+ employees) have avoided shifting costs to employees over the last five years, resulting in little growth in deductibles and other cost-sharing requirements.

Posted on June 15, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Emerging Transportation Models

By Rick Kahler CFP

For elderly people facing the reality of diminishing capabilities, a service that can help maintain their independence is ridesharing.

Ride – Sharing

Ridesharing is hardly news for most Americans, particularly those in urban areas. After all, it has been around for a decade. In more rural areas of the US, however, ridesharing is just becoming an option. In my home town of Rapid City, South Dakota, for example, Lyft started operations only recently, and Uber began last September.

Many of us in rural parts of the US, myself included, use ridesharing primarily when we travel. It has changed the way I travel in large cities, and I appreciate it for its convenience, flexibility, and economical cost.

For many others outside of big cities, however, especially senior citizens, ridesharing has the potential to be a game changer for those willing to take advantage of it.

There are a lot of emotional benefits and pitfalls to ridesharing for seniors. The greatest benefit is that, instead of relying on the gratuity and schedules of friends, family, and limited public transportation, they can literally reclaim most of the freedom they once had when they could drive. This alone can be uplifting and empowering. It allows seniors who may be isolated socially to reenter their communities and gives them a renewed sense of independence and autonomy.

However, I find many seniors emotionally resistant and reluctant to embrace the benefits of ridesharing. Many fear the unknown and unfamiliarity of ridesharing. Using the app inherently means owning a smart phone, which many seniors resist. Even those who have smartphones may feel overwhelmed about downloading and learning the app. This is where reaching out to younger family and friends to show you the ropes can be critical.

Another factor that often contributes to reluctance to use the freedom and convenience of ridesharing is a money script of frugality. The assumption may be “I can’t afford it.” While this can be absolutely true for some, many who could easily afford ridesharing also buy into that belief.

Economically, using ridesharing can cost the same as or less than owning a car. This is especially the case if you don’t have a demanding schedule and your need for transportation is moderate for activities like grocery shopping, medical appointments, and occasional social events.

Example:

Let’s assume you average one 10-mile round trip per day, or seven per week. If you owned a car the gas would cost $50 a month. Insurance could run about $100. Oil, changing tires, servicing, and periodic repairs could average another $50 a month. That’s a total of $200 a month in out-of-pocket costs. The biggest cost is the depreciation on your car. Let’s assume your car is worth $20,000. You could expect it to depreciate 1% per month or around $200. That puts the total cost of owning the car at $400 per month.

Ridesharing costs about $7.00 each way when you are traveling up to 5 miles. That puts the daily average cost at $14.00 per trip, or $420 a month, about the same cost as owning a car—and a cost that could be covered for months through selling your vehicle.

***

***

Assessment

Ridesharing can open up a whole new world of convenience, autonomy, and choices. Its benefits can even be a matter of life and death when seniors reach that difficult time when they can still legally drive but in reality they should not. With physical impairments like deteriorating vision and slower reaction time, driving means putting themselves and others at risk. Having the option of ridesharing can make that tough decision to give up driving just a little easier.

Robin Milcowitz, a Florida woman who found herself enrolled in an AccessOne loan at a Tampa hospital in 2018 after having a hysterectomy for ovarian cancer, said she was appalled by the financing arrangements.“Hospitals have found yet another way to monetize our illnesses and our need for medical help,” said Milcowitz, a graphic designer.

She was charged 11.5% interest — almost three times what she paid for a separate bank loan. “It’s immoral,” she said.

We have produced Investment Policy Statements of a hundred pages or more for our esteemed physician clients and colleagues. Or, others were just a few pages or a conversation.

But, before deciding on any investment direction and philosophy in brief, however, we typically first focus on how much medical clients need to live on. For the income part of a client’s portfolio, that entails locking in rates of at least 4-5%, whether through municipal and corporate bonds, certificates of deposits, Treasury ladders, utilities or conservative dividend producing equities or ETFs, etc.

Once income requirements are fulfilled, whatever money is left over gets diversified into a portfolio of growth and value stocks—with some alternative investments. We limit making tactical shifts like putting money into cash when markets fell last year, or more recently, buying CDs and Treasuries as rates went up. But, we do re-direct cash income, rather than sell assets in real time, as our philosophy trends to a “Buy and Hold” strategy.

Currently, we’re sitting on the sidelines with cash, some of which we are getting ready to deploy into the market as we position for any pullbacks later this 2024 year.

So, what is your investing philosophy for today, and or, tomorrow?

Many physicians and other investors — even those that meet net worth guidelines — are surprised to learn that there exists a $500 – 999 billion, or more, alternative investment industry that is not generally marketed to the public. Such alternative investments have also been known as hedge funds or private investment funds.

Unlike mutual funds, these alternative investments can be structured in a wide variety of ways. Because of the very same regulations discussed above, these funds cannot be advertised, but they are far from illegal or illicit.

In fact, physicians were among the most significant early investors in one of the last century’s most successful hedge funds. Mr. Warren Buffett, Chairman of Berkshire Hathaway, Inc. and a legendary investor got his start in 1957 running the Buffett Partnership, an alternative investment fund not open to the general public. Mr. Buffett’s first public appearance as a money manager was before a group of physicians in Omaha, Nebraska. Eleven decided to put some money with him. A few of these original investors followed him into Berkshire Hathaway, now among the most highly valued companies in the world.

The alternative investment, or hedge, funds of today are similar to the original Buffett Partnership in many ways. So, we will discuss several unique terms which potential investors should be aware.

Hedge funds may feature a hurdle rate as part of the calculation of the fund manager’s performance incentive compensation. Also known as a “benchmark,” the hurdle rate is the amount, expressed in percentage points, an investor’s capital account must appreciate before the account becomes subject to a performance incentive fee. Potential medical investors should view the hurdle rate as a form of protection in context with other features of the fee arrangement.

The hurdle rate, which benchmarks a single year’s performance, may be considered mutually exclusive of any other year, or the hurdle rate may compound each year. The former case is more common. In the latter case, a portfolio manager failing to attain a hurdle rate in the first year will find the effective hurdle rate considerably higher during the second year.

Once a fund manager attains the hurdle rate for an investor, the medical investor’s capital account may be charged a performance incentive fee only on the performance above and beyond the hurdle rate. Alternatively, the account may be charged a performance fee for the entire level of performance, including the performance required to attain the hurdle rate. Other variations on the use of the hurdle rate exist, and are limited only by the contract signed between the fund manager and the investor. The hurdle rate is not generally a negotiating point, however.

Example:

A fund charges a performance fee with a 6 percent hurdle rate, calculated in mutually exclusive manner. Dr. Lanouettea, a radiologist investor places $100,000 with the fund. The first year’s performance is 5 percent. The investor therefore owes no performance fee during the first year because the portfolio manager did not attain the hurdle rate. During year two, the portfolio manager guides the fund to a 7 percent return. Because the hurdle rate is mutually exclusive of any other year, the portfolio manager has attained the 6 percent hurdle rate and is entitled to a performance fee.

Highwater Mark

Some funds feature a highwater mark provision, also known as a ”loss-carryforward” provision. As with the hurdle rate, potential investors should consider the highwater mark a form of protection. A high water mark is an amount equal to the greatest value of an investor’s capital account, adjusted for contributions and withdrawals. The high water mark ensures that the hedge fund manager charges a performance incentive fee only on the amount of appreciation over and above the highwater mark set at the time the performance fee was last charged. The current trend is for newer funds to feature this highwater mark, while older, larger funds may not feature it.

Example:

A fund charges a 20 percent performance fee with a highwater mark but no hurdle rate. Dr. Butalak, a dentist investor contributes $100,000 to the fund. During the first year, the hedge fund manager grows that capital account to $110,000 and charges a 20 percent performance fee, or $2,000. The ending capital account balance and highwater mark is therefore $108,000. During year two, the account falls back to $100,000, but the highwater mark remains $108,000. During year three, in order for the manager to charge a performance fee, the manager must grow the capital account to a level above $108,000.

Clawback Provision

Rarely, a fund may provide investors with a clawback provision. This term, borrowed from the venture capital fund world, such provisions result in a refund to the investor of all or part of a previously charged performance fee if a certain level of performance is not attained in subsequent years. Such refunds in the face of poor or inadequate performance may not be legal in some states or under certain authorities.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

When You May Need a Business, Management or Financial Second Opinion?

The Marcinko & Associates second opinion service is a physician-to-advisor telephone or e-mail portal that connects independent financial and business management professionals and consultants, with doctors or healthcare executives desiring affordable and unbiased financial or business advice on an as-needed, pay-per-use basis.

Medical professionals and healthcare executives can now receive direct access to us in the areas of Practice Enhancement, Investing, Financial Planning, Asset Allocation, Portfolio Management, Insurance, Mortgage and Lending, Practice Management, Information Technology, Human Resources and Employee Benefits.

This Marcinko & Associates service is designed to fill a growing need for medically focused financial or managerial advice that traditional consultants have not been able to serve. For example, situations in which you could benefit from a personal financial planning second opinion include:

Posted on May 21, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Historical Review

As can now be discerned 15 years later, two trends emerged from the aftermath of the 2008 financial crisis. One was a new type of investment that concentrated capital among a small number of firms. The other was left-wing activism in the style of Occupy Wall Street. Combined, these trends helped empower Wall Street behemoths to push much of the corporate wokeness that is so common today. The financial meltdown precipitated a transition from active to passive investment.

Definitions

Active investment is what one typically thinks of as investing — making risky stock purchases in an attempt to beat the market in the short-term.

Passive investment, on the other hand, requires much less effort. According to Investopedia, it is a long-term strategy where investors try to “replicate market performance by constructing well-diversified portfolios” (e.g. mutual funds) typically based on a “representative benchmark” like the S&P 500 index. In other words, it bets on the market rather than against it.

Passive investing took off after the financial crisis when investors realized it wasn’t worth trying to beat the market. Why pay a broker a one to two percent fee every year to actively manage your assets, especially when the downturn revealed they often under-performed the regular market returns? Many opted for passive asset management that cost a fraction of a brokerage fee.

In fact, one study found that between 2008 and 2015, active funds lost $800 billion while passive funds gained over $1 trillion in new investment. As of 2019, more money is now invested in passive than in active funds.

Posted on May 20, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

For last the week, the NASDAQ Composite (^IXIC) rose more than 2% while the S&P 500 (^GSPC) popped more than 1.5%. The Dow Jones Industrial Average (^DJI) rose more than 1%, closing above 40,000 for the first time ever on Friday.

The week is also expected to be quieter on the economic front, with updates on activity in the manufacturing and services sectors as well as the final reading of consumer sentiment for May on tap. Minutes from the Fed’s May meeting are also expected on Wednesday afternoon.

The rule, finalized last month by the Labor Department, requires investment advisers to provide “prudent, loyal, honest advice free from overcharges” and avoid recommendations that favor their interests at the expense of their clients. It also updates the definition of an investment advice fiduciary under the Employee Retirement Income Security Act (ERISA) and Internal Revenue Code.

Under the new definition, a fiduciary includes any financial services provider who offers investment advice to a retirement investor for a fee and who claims to be acting as a fiduciary or who a reasonable investor understands to be a trusted adviser acting in their best interest. The update removes the requirement that fiduciaries provide advice on a regular basis, bringing one-time advice under the rule. The Biden administration has argued that the previous definition, which was written in 1975, is outdated and has not kept pace with changes to the retirement landscape.

And, confidence in the U.S. dollar has waned, as forecasts suggest that a dip in inflation might allow the Federal Reserve to slash interest rates. With a notable 5% climb earlier this year, the dollar is now bracing for its first loss of 2024, triggered by a promising inflation report.

Finally, fourteen of the world’s 20 largest stock markets have hit all-time highs recently, including England, Japan, Brazil, India, and Canada, according to Bloomberg. In the USA, the S&P 500 (also at a record) hasn’t dropped more than 2% in a trading session in 311 days, the longest streak in five years.

Check back periodically for practical updates. Our catalogue library of major books, texts, case models and dictionaries is suggested for additional financial, economic, business and medical practice management information and education.

Posted on May 16, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The Dow Jones Industrial Averagebriefly crossed 40,000 for the first time, a milestone that appeared implausible little more than two years ago when the Federal Reserve began raising interest rates to cool an overheated economy.

Gloom and doom forecasts abounded. When the central bank ended the era of low rates that prevailed in the years following the global financial crisis, economists predicted painful consequences: a U.S. recession and rising unemployment.

Posted on May 13, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Women’s health startups are still closing multi million-dollar funding deals despite a challengingventure capital (VC) landscape in which VC dollars are on track to fall by 73% this year compared to last.

For example, in the last year, virtual maternity care program Pomelo Careraised $33 million in seed and Series A rounds led by Andreessen Horowitz; Caraway Health, a digital mental, physical, and reproductive health services platform, raised almost $17 million in a Series A round led by Maveron and GV (formerly Google Ventures); and Intrinsic, which acquires brands that make women’s health products, announced a $15 million equity fund raise (which is when a company raises money by selling its shares).

Financial benchmarking can assist healthcare managers and professional financial advisors in understanding the operational and financial status of their organization or practice.

The general process of financial benchmarking analysis may include three elements: (1) Historical subject benchmarking; (2) Benchmarking to industry norms; and, (3) Financial ratio analysis.

History

Historical subject benchmarking compares a healthcare organization’s most recent performance with its reported performance in the past in order to: examine performance over time; identify changes in performance within the organization (e.g., extraordinary and non-recurring events); and, to predict future performance.

As a form of internal benchmarking, historical subject benchmarking avoids issues such as: differences in data collection and use of measurement tools; and, benchmarking metrics that often cause problems in comparing two different organizations.

However, it is necessary to common size data in order to account for company differences over time that may skew results.

Benchmarking

Benchmarking to industry norms, analogous to Fong and colleagues’ concept of industry benchmarking, involves comparing internal company-specific data to survey data from other organizations within the same industry. This method of benchmarking provides the basis for comparing the subject entity to similar entities, with the purpose of identifying its relative strengths, weaknesses, and related measures of risk.

***

***

Financial Ratio Analysis

The process of benchmarking against industry averages or norms will typically involve the following steps:

Identification and selection of appropriate surveys to use as a benchmark, i.e., to compare with data from the organization of interest. This involves answering the question, “In which survey would this organization most likely be included?”;

If appropriate, re-categorization and adjustment of the organization’s revenue and expense accounts to optimize data compatibility with the selected survey’s structure and definitions (e.g., common sizing); and,

Calculation and articulation of observed differences of organization from the industry averages and norms, expressed either in terms of variance in ratio, dollar unit amounts, or percentages of variation.

Trends

Financial ratio analysis typically involves the calculation of ratios that are financial and operational measures representative of the financial status of an enterprise. These ratios are evaluated in terms of their relative comparison to generally established industry norms, which may be expressed as positive or negative trends for that industry sector. The ratios selected may function as several different measures of operating performance or financial condition of the subject entity.

The Selected Ratios

Common types of financial indicators that are measured by ratio analysis include:

Liquidity. Liquidity ratios measure the ability of an organization to meet cash obligations as they become due, i.e., to support operational goals. Ratios above the industry mean generally indicate that the organization is in an advantageous position to better support immediate goals. The current ratio, which quantifies the relationship between assets and liabilities, is an indicator of an organization’s ability to meet short-term obligations. Managers use this measure to determine how quickly assets are converted into cash.

Activity. Activity ratios, also called efficiency ratios, indicate how efficiently the organization utilizes its resources or assets, including cash, accounts receivable, salaries, inventory, property, plant, and equipment. Lower ratios may indicate an inefficient use of those assets.

Leverage.Leverage ratios, measured as the ratio of long-term debt to net fixed assets, are used to illustrate the proportion of funds, or capital, provided by shareholders (owners) and creditors to aid analysts in assessing the appropriateness of an organization’s current level of debt. When this ratio falls equal to or below the industry norm, the organization is typically not considered to be at significant risk.

Profitability. Indicates the overall net effect of managerial efficiency of the enterprise. To determine the profitability of the enterprise for benchmarking purposes, the analyst should first review and make adjustments to the owner(s) compensation, if appropriate. Adjustments for the market value of the “replacement cost” of the professional services provided by the owner are particularly important in the valuation of professional medical practices for the purpose of arriving at an ”economic level” of profit.

Data Homogeneity

The selection of financial ratios for analysis and comparison to the organization’s performance requires careful attention to the homogeneity of data. Benchmarking of intra-organizational data (i.e., internal benchmarking) typically proves to be less variable across several different measurement periods.

However, the use of data from external facilities for comparison may introduce variation in measurement methodology and procedure. In the latter case, use of a standard chart of accounts for the organization or recasting the organization’s data to a standard format can effectively facilitate an appropriate comparison of the organization’s operating performance and financial status data to survey results.

Operational benchmarking is used to target non-central work or business processes for improvement. It is conceptually similar to both process and performance benchmarking, but is generally classified by the application of the results, as opposed to what is being compared. Operational benchmarking studies tend to be smaller in scope than other types of benchmarking, but, like many other types of benchmarking, are limited by the degree to which the definitions and performance measures used by comparing entities differ. Common sizing is a technique used to reduce the variations in measures caused by differences (e.g., definition issues) between the organizations or processes being compared.

Common Sizing

Common sizing is a technique used to alter financial operating data prior to certain types of benchmarking analysis and may be useful for any type of benchmarking that requires the comparison of entities that differ on some level (e.g., scope of respective benchmarking measurements, definitions, business processes). This is done by expressing the data for differing entities in relative (i.e., comparable) terms.

Example:

For example, common sizing is often used to compare financial statements of the same company over different periods of time (e.g., historical subject benchmarking), or of several companies of differing sizes (e.g., benchmarking to industry norms). The latter type may be used for benchmarking an organization to another in its industry, to industry averages, or to the best performing agency in its industry. Some examples of common size measures utilized in healthcare include:

Percent of revenue or per unit produced, e.g., relative value unit (RVU);

Per provider, e.g., physician;

Per capacity measurement, e.g., per square foot; or,

Other standard units of comparison.

Assessment

As with any data, differences in how data is collected, stored, and analyzed over time or between different organizations may complicate the use of it at a later time. Accordingly, appropriate adjustments must be made to account for such differences and provide an accurate and reliable dataset for benchmarking.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on May 3, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Job growth slowed and unemployment ticked higher last month, marking a break from a string of data showing surprising strength in the labor market.

U.S. employers added a seasonally adjusted 175,00 jobs in April, the Labor Department reported on Friday. That was far less than in March, when gains exceeded 300,000, and also below what economists had expected. The unemployment rate ticked up to 3.9% from March’s 3.8%.

According to the WSJ, wages also rose less than anticipated, increasing 3.9% from a year earlier after rising 4.1% in March.

Friday’s report today is sure to stir immediate debate among economists and investors about whether the labor market is merely cooling in a welcome fashion or starting to show more serious strains under the pressure of higher interest rates.

Treasury yields, which largely reflect investors’ expectations for short-term rates set by the Federal Reserve, fell after the report. The yield on the benchmark 10-year U.S. Treasury note was 4.471% in recent trading, according to Tradeweb, down from 4.569% Thursday.

Stock futures climbed, suggesting investors were pleased with the data, which could increase optimism about the outlook for inflation.

Posted on April 29, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

A SPECIAL REPORT

By Vitaliy N. Katsenelson CFA

***

Uber’s business is doing extremely well. It has reached escape velocity – the company’s expenses have grown at a slow rate while its revenues are growing at 22% a year. This caused profit margins to expand and earnings and free cash flows to skyrocket. Our investment in Uber was based on the assumption that its services would become a utility – just like water and electricity. The company’s name is synonymous with ride sharing.

I must confess that the biggest risk to our investment in Uber is me. Yes, you read that right. Uber has an incredible growth runway. It is not just going after ride sharing and food delivery, where it still has plenty of room to grow, it is also making serious inroads into the grocery market. It has terrific management that is putting a lot of daylight between Uber and its competitors.

It is critical for physician executives to understand and to measure the total cost of hospital capital. Lack of understanding and appreciation of the total cost of capital is widespread, particularly among not-for-profit hospital and physician executives. The capital structure includes long-term debt and equity; total capital is the sum of these two, and, each of these components has cost associated with it.

For the long-term debt portion, this cost is explicit—it is the interest rate plus associated costs of placement and servicing. For the equity portion, the cost is not explicit and is widely misunderstood. In many cases, hospital capital structures include significant amounts of equity that has accumulated over many years of favorable operations.

Far too many executives wrongly attribute zero cost to the equity portion of their capital structure. Although it is correct that generally accepted accounting principles continue to assign a zero cost to equity, there is opportunity cost associated with equity that needs to be considered. This cost is the opportunity available to utilize that capital in alternative ways.

***

***

In general, the cost attributed to equity is the return expected by the equity markets on hospital equity. This can be observed by evaluating the equity prices of hospital companies whose equity is traded on public stock exchanges. Usually, the equity prices will imply cost of equity in the range of 10%–14%. Almost always, the cost of equity implied by hospital equity prices traded on public stock exchanges will substantially exceed the cost of long-term debt. Thus, while many hospital executives will view the cost of equity to be substantially less than the cost of debt (i.e., to be zero) in nearly all cases, the appropriate cost of equity will be substantially greater than the cost of debt.

Hospitals need to measure their weighted average cost of capital (WACC). WACC is the cost of long-term debt multiplied by the ratio of long-term debt to total capital plus the cost of equity multiplied by the ratio of equity to total capital (where total capital is the sum of long-term debt and equity).

WACC is then used as the basis for capital charges associated with all capital investments. Capital investments should be expected to generate positive returns after applying this capital charge based on the WACC. Capital investments that do not generate returns exceeding the WACC consume enterprise value; those that generate returns exceeding WACC increase enterprise value. Therefore, physician and hospital executives need to be rewarded for increasing enterprise value.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

Our Other Print Books and Related Information Sources:

Posted on April 25, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

An uptick in corporate dealmaking fueled investment banking growth at the four largest US banks—JPMorgan Chase, Bank of America, Wells Fargo, and Citibank—as well as at Goldman Sachs and Morgan Stanley. The result was “one of [investment banking’s] best quarters” since the Fed began hiking rates in 2022, the Wall Street Journal reported. Their earnings releases over the last week either matched or beat the consensus forecasts for revenue and earnings per share, according to the WSJ.

“It’s clear that we’re in the early stages of a reopening of the capital markets,” Goldman Sachs CEO David Solomon said in an earnings call last Monday. Goldman reported that growth in its investment banking and trading pushed its net income up 28% year over year, beating analyst expectations. Solomon said he expects more M&A activity will keep boosting the demand for debt underwriting at Goldman, which saw a 32% Year over Year jump in internet-banking revenue.

Solomon’s sunny outlook was beclouded the next day by Fed Chair Jerome Powell. The Fed had hoped inflation reports would show it could cut rates soon without overheating the economy, but instead inflation has continued to tick up.

Posted on April 17, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

If you need a reprieve to prevent the government from raiding your bank account, you’re not alone—the IRS expects 19 million people to file for an extensionthis year. The agency will automatically grant you a six-month extension, although it’s recommended you remit a payment by April 15th if you expect to owe money to avoid interest and penalties. The good news is you probably won’t have to fork over as much as Mark Cuban, who said he is sending the IRS $288 million today and is proud to pay his fair share.

The stock market is coming off its worst week of the year, and the road ahead is no less bumpy. A direct military confrontation between Iran and Israel has investors on edge about a wider regional war that threatens energy supplies. Amid the uncertainty, safe-haven assets are seeing major interest: The US dollar just had its best week in more than 18 months.

A closed-end fund (CEF) or closed-ended fund is a collective investment model based on issuing a fixed number of shares which are not redeemable from the fund.

Unlike open-end funds, new shares in a closed-end fund are not created by managers to meet demand from investors. Instead, the shares can be purchased and sold only in the market, which is the original design of the mutual fund, which predates open-end mutual funds but offers the same actively-managed pooled investments.

Questions – from doctors – like these remind me that the workings of the financial services industry which I tend to take for granted but can be confusing to people outside the field.

The following analogy may help to explain.

Orchestra Analogy

Think of an orchestra. The investment adviser is the equivalent of the director/conductor and the money managers are the instrumentalists. Each one is a specialist who plays a particular type of instrument, and it takes a variety of these specialists to make up the orchestra.

Specialists

The broad specialties are the types of instruments, such as strings, brass, winds, and percussion. These are the equivalent of fund managers who specialize in asset classes like equities, bonds, real estate, commodities, and absolute returns.

Sub-Specialists

Within each specialty are a variety of subspecialists. Winds, for example, include clarinets, oboes, and saxophones—which are further divided into alto, soprano, tenor, and bass. The brass section has French horns, trumpets, and trombones. The divisions and sub-divisions go on and on. Similarly, within the various asset classes are a great many mutual fund managers who specialize in narrower subcategories.

Conductor

The task of the orchestra conductor-director is to pick, not just the best musicians, but the best mix of musicians. A group with only trumpets or every subspecialty of percussion, no matter how skilled, isn’t an orchestra. Before auditioning a single musician, the director’s first task is to clarify the purpose of the ensemble being created. A different mix of instruments will be required for a symphony, a marching band, an intimate chamber group, or a dance band. It all depends on what the audience wants.

The conductor-director needs to weigh the various musicians’ abilities against their cost and their specific specialties against the needs of the orchestra. When the right mix of players has been chosen, the director needs to pick the appropriate music, assemble the group, and rehearse. The director’s talent, experience, and leadership skills all serve to help the right players produce the right sound for their audiences.

***

***

It takes similar coordination and skill to put together the right mix of asset classes and mutual fund managers to produce the best results for various clients, especially since there are some 17,000 mutual funds to choose from.

Fees

Just as both the orchestra director and the musicians are paid based on their skills and their work, both mutual fund managers and investment advisers are paid based on the assets they manage. Mutual fund managers earn 0.05% to 3.0%. Financial advisers earn 0.30% to 3.0%. An informed consumer could pay as low as 0.35% while an uninformed consumer could pay up to 6% a year, which would eat up most of the investment returns.

One essential responsibility for an adviser, then, is to choose mutual fund managers whose fees are low.

However, the cost of the mutual fund manager isn’t the be-all and end-all. One must also weigh performance, just as an orchestra director might pay more to get an outstanding musician who would add significant value to the performances.

Example:

For example, my firm’s overall average fee for mutual fund managers is 0.5%. We could get that as low as 0.1%, which might be impressive at first glance.

However, we would give up 0.25% to 1.00% of net return in some areas, resulting in poorer outcomes for the clients.

***

***

Assessment

Skilled direction of an orchestra is obviously more art than science. Skilled coordination of mutual fund managers is the same. Both require knowledge, integrity, and commitment to the quality of the final product.

Channel Surfing the ME-P

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

The paradox of thrift (saving) states that an increase in autonomous saving leads to a decrease in aggregate demand and thus a decrease in gross output which will in turn lower total saving. The paradox is that total saving may fall because of individuals’ attempts to increase their saving, and, broadly speaking, that increase in saving may be harmful to an economy.

Both the narrow and broad claims are paradoxical within the assumption underlying the fallacy of composition, namely that which is true of the parts must be true of the whole. The narrow claim transparently contradicts this assumption, and the broad one does so by implication, because while individual thrift is generally averred to be good for the economy, the paradox of thrift holds that collective thrift may be bad for the economy.

Private equity and venture capital investments typically involve ownership of shares in a company and represent title to a portion of the company’s future earnings. However, private equity is an equity interest in a company or venture whose stock is not yet traded on a stock exchange.

Venture capital is typically a special case of private equity in which the investment is in a company or venture that has little financial history or is embarking on a high risk/high potential reward business strategy.

Like real estate, private equity and venture capital investments generally share a general lack of liquidity and a lack of comparability across different individual investments. The lack of liquidity comes from the fact that private equity and venture capital investments are typically not tradable on a stock exchange until the company has an IPO.

The lack of comparability is due to the fact that most private equity and venture capital investments are the result of direct negotiation between the investor/venture capitalist and the existing owners of the company /venture.

With widely divergent terms and provisions across different investments, it is difficult to make general claims regarding the characteristics of private equity and venture capital investments.

Posted on April 3, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

PATIENT COMPLICATION RATES

By Staff Reporters

***

***

Hospitals under private equity (PE) ownership reported higher rates of patient complications when compared to other facilities, according to a recent JAMA study—raising questions about how the business model might affect staffing and subsequent quality of care.

The surveyed Medicare beneficiaries saw a 25.4% increase in “hospital-acquired conditions,” which the Centers for Medicare and Medicaid Services defines as falls, infections, and other adverse events, when they received treatment at a PE-acquired hospital compared to those run under other forms of ownership.

On the whole, the study found that Medicare enrollees at hospitals under PE control were not only younger and less likely to additionally qualify for Medicaid but also more likely to experience complications.

Posted on March 29, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

DIVIDEND REINVESTMENT PLANS

By Staff Reporters

***

DEFINITION

DRIPs are merely an automated strategy in which a company’s dividends are reinvested into additional shares of that company. Instead of being paid dividends in cash, you get additional shares of ownership in the company.

There are three ways to get involved in DRIPs: directly through the company, through your broker, or through a transfer agent.

Company-run DRIPs are generally only available through large, blue-chip dividend stocks.That’s because smaller companies don’t want to take on the overhead costs of tracking all their shareholders and going through the paperwork headache of calculating how much each one gets in dividends and additional fractional shares. The company benefits from gaining an additional source of capital, but most of all in creating a more stable base of shareholders, ones who are less likely to panic and sell during a market decline. This can help decrease the volatility of a company’s shares.

Finally, most large discount brokers, such as Scottrade, TD Ameritrade, and E*Trade, also offer DRIPs, though with different requirements and limitations.

While dividend reinvestment is powerful, there are a couple reasons why you might not want to reinvest your dividends.