By Dr. David Edward Marcinko; MBA MEd

SPONSOR: http://www.MarcinkoAssociates.com

***

***

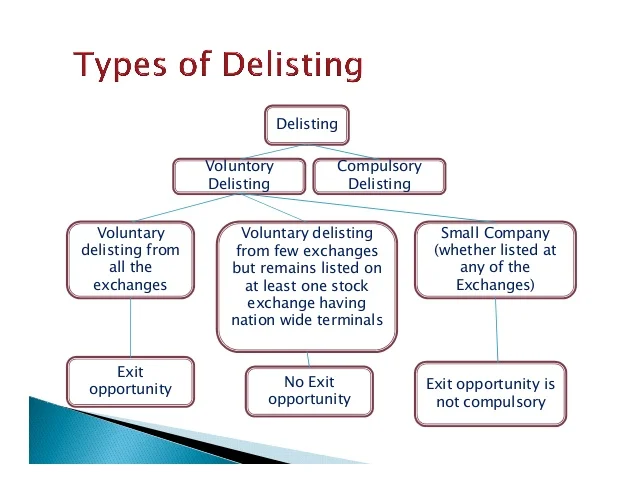

Stocks are delisted from major U.S. indexes and exchanges when they no longer meet the standards those systems are designed to uphold. Although the Dow Jones Industrial Average (DJIA), Nasdaq, and S&P 500 each serve different purposes, the underlying reasons for removal share a common theme: maintaining the integrity, stability, and representativeness of the market.

Delisting from an exchange such as NASDAQ typically occurs when a company fails to satisfy the exchange’s listing requirements. These requirements include maintaining minimum financial thresholds, such as a sufficient share price, market capitalization, or levels of shareholder equity. When a company falls short—whether due to financial distress, missed reporting deadlines, bankruptcy, or operational collapse—it may receive a notice of non‑compliance. If it cannot regain compliance within the allotted time, the stock is removed from the exchange. Once delisted, shares often migrate to over‑the‑counter markets, where trading becomes less liquid and less transparent, reflecting the diminished stability of the company’s financial condition.

Removal from the S&P 500 follows a similar logic but is driven by index eligibility rather than exchange rules. The S&P 500 is designed to represent the largest and most financially robust U.S. companies. When a company’s market capitalization shrinks, its liquidity declines, or it undergoes a merger, acquisition, or privatization, it may no longer meet the index’s criteria. In such cases, the index replaces the company with another that better reflects the size and structure of the broader market. This process ensures that the index continues to serve as an accurate benchmark for large‑cap U.S. equities.

The DJIA, by contrast, is a curated index of only thirty companies, selected to reflect the evolving U.S. economy. A company may be removed not because it has failed financially, but because it no longer represents the dominant forces shaping the economic landscape. As industries rise and fall, the index committee adjusts the components to maintain relevance. Companies that lose prominence, undergo structural changes, or no longer align with the index’s sector balance may be replaced by firms that better capture contemporary economic trends.

Across all three systems, delisting or removal serves a protective and corrective function. Exchanges safeguard investors by enforcing financial and reporting standards, while indexes preserve their usefulness by ensuring that their components accurately reflect the markets they aim to track. Although the consequences for companies vary—from reduced liquidity to diminished prestige—the underlying purpose remains consistent: maintaining a clear, reliable picture of the health and direction of the U.S. financial markets.

COMMENTS APPRECIATED

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR- http://www.MarcinkoAssociates.com

Like, Refer and Subscribe

HOSPITALS: http://www.crcpress.com/product/isbn/9781466558731

CLINICS: http://www.crcpress.com/product/isbn/9781439879900

ADVISORS: www.CertifiedMedicalPlanner.org

FINANCE:Financial Planning for Physicians and Advisors

INSURANCE:Risk Management and Insurance Strategies for Physicians and Advisors

Dictionary of Health Economics and Finance

Dictionary of Health Information Technology and Security

Dictionary of Health Insurance and Managed Care

***

Share this:

Filed under: iMBA, Inc. | Tagged: economy, finance, Investing, Marcinko, stock exchange, stock indexes, stock market, stocks | Leave a comment »