BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

A hedge fund is a limited partnership of private investors whose money is pooled and managed by professional fund managers. These managers use a wide range of strategies, including leverage (borrowed money) and the trading of nontraditional assets, to earn above-average investment returns. A hedge fund investment is often considered a risky, alternative investment choice and usually requires a high minimum investment or net worth. Hedge funds typically target wealthy investors.

QUESTION:Can I invest my Individual Retirement Account [IRA] in a Hedge Fund?

This is up to the manager, but there is no legal restriction on a hedge fund accepting individual retirement account (IRA) assets. IRA accounts are not well suited for funds that make extensive use of leverage, however. In such cases, the fund is likely to generate significant amounts of unrelated business taxable income (UBTI) – profits of the fund attributable to the use of leverage. The holder of an IRA account must pay taxes on UBTI, even if the UBTI was generated in an IRA account.

But, today’s hedge funds may or may not use leverage. Many hedge funds are not hedged at all, but rather are just specialized versions of regular long stock portfolios. If such funds do not use much leverage, IRA investors will not encounter much difficulty with UBTI and should not hesitate in considering these funds.

In considering whether to accept IRA money, hedge fund managers must consider several factors. If the only type of retirement money accepted by the hedge funds is IRA money, then the manager has no limit on how much retirement money the fund can accept. If, however, there are other types of retirement money invested in the fund, such as pension funds, IRA money will be counted towards a total of 25 percent of fund assets that can be invested in retirement accounts before the fund becomes subject to the Employment Retirement Income Security Act of 1974 (ERISA). Funds subject to ERISA regulations face a heavy administrative burden and more restrictions than most fund managers like.

Finally, IRA distributions from a hedge fund are subject to the standard 20 percent withholding unless the funds are directly rolled over to other qualified plans.

Suppose that in a new Accountable Care Organization [ACO] contract, a certain medical practice was awarded a new global payment or capitation styled contract that increased revenues by $100,000 for the next fiscal year. The practice had a gross margin of 35% that was not expected to change because of the new business. However, $10,000 was added to medical overhead expenses for another assistant and all Account’s Receivable (AR) are paid at the end of the year, upon completion of the contract.

Cost of Medical Services Provided (COMSP):

The Costs of Medical Services Provided (COMSP) for the ACO business contract represents the amount of money needed to service the patients provided by the contract. Since gross margin is 35% of revenues, the COMSP is 65% or $65,000. Adding the extra overhead results in $75,000 of new spending money (cash flow) needed to treat the patients. Therefore, divide the $75,000 total by the number of days the contract extends (one year) and realize the new contract requires about $ 205.50 per day of free cash flows.

Assumptions

Financial cash flow forecasting from operating activities allows a reasonable projection of future cash needs and enables the doctor to err on the side of fiscal prudence. It is an inexact science, by definition, and entails the following assumptions:

All income tax, salaries and Accounts Payable (AP) are paid at once.

Durable medical equipment inventory and pre-paid advertising remain constant.

Gains/losses on sale of equipment and depreciation expenses remain stable.

Gross margins remain constant.

The office is efficient so major new marginal costs will not be incurred.

***

***

Physician Reactions:

Since many physicians are still not entirely comfortable with global reimbursement, fixed payments, capitation or ACO reimbursement contracts; practices may be loath to turn away short-term business in the ACA era. Physician-executives must then determine other methods to generate the additional cash, which include the following general suggestions:

1. Extend Account’s Payable

Discuss your cash flow difficulties with vendors and emphasize their short-term nature. A doctor and her practice still has considerable cache’ value, especially in local communities, and many vendors are willing to work them to retain their business

2. Reduce Accounts Receivable

According to most cost surveys, about 30% of multi-specialty group’s accounts receivable (ARs) are unpaid at 120 days. In addition, multi-specialty groups are able to collect on only about 69% of charges. The rest was written off as bad debt expenses or as a result of discounted payments from Medicare and other managed care companies. In a study by Wisconsin based Zimmerman and Associates, the percentages of ARs unpaid at more than 90 days is now at an all time high of more than 40%. Therefore, multi-specialty groups should aim to keep the percentage of ARs unpaid for more than 120 days, down to less than 20% of the total practice. The safest place to be for a single specialty physician is probably in the 30-35% range as anything over that is just not affordable.

The slowest paid specialties (ARs greater than 120 days) are: multi-specialty group practices; family practices; cardiology groups; anesthesiology groups; and gastroenterologists, respectively. So work hard to get your money, faster. Factoring, or selling the ARs to a third party for an immediate discounted amount is not usually recommended.

3. Borrow with Short-Term Bridge Loans

Obtain a line of credit from your local bank, credit union or other private sources, if possible in an economically constrained environment. Beware the time value of money, personal loan guarantees, and onerous usury rates. Also, beware that lenders can reduce or eliminate credit lines to a medical practice, often at the most inopportune time.

4. Cut Expenses

While this is often possible, it has to be done without demoralizing the practice’s staff.

5. Reduce Supply Inventories

If prudently possible; remember things like minimal shipping fees, loss of revenue if you run short, etc.

6. Taxes

Do not stop paying withholding taxes in favor of cash flow because it is illegal.

Hyper-Growth Model:

Now, let us again suppose that the practice has attracted nine more similar medical contracts. If we multiple the above example tenfold, the serious nature of potential cash flow problem becomes apparent. In other words, the practice has increased revenues to one million dollars, with the same 35% margin, 65% COMSP and $100,000 increase in operating overhead expenses.

Using identical mathematical calculations, we determine that $750,000 / 365days equals $2,055.00 per day of needed new free cash flows! Hence, indiscriminate growth without careful contract evaluation and cash flow analysis is a prescription for potential financial disaster.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com

In the first month of 2025, hospital revenue and expenses both increased, balancing each other out and resulting in continued steady financial performance for hospitals, according to Kaufman Hall’s January 2025 National Hospital Flash Report.

Revenues grew more quickly in the inpatient setting, as more patients were treated in the hospital and emergency department than in outpatient settings. While expense increases were largely driven by drug costs, the rate of that growth has significantly slowed.

This Health Capital Topics article reviews the report and the current state of hospital operations. (Read more…)

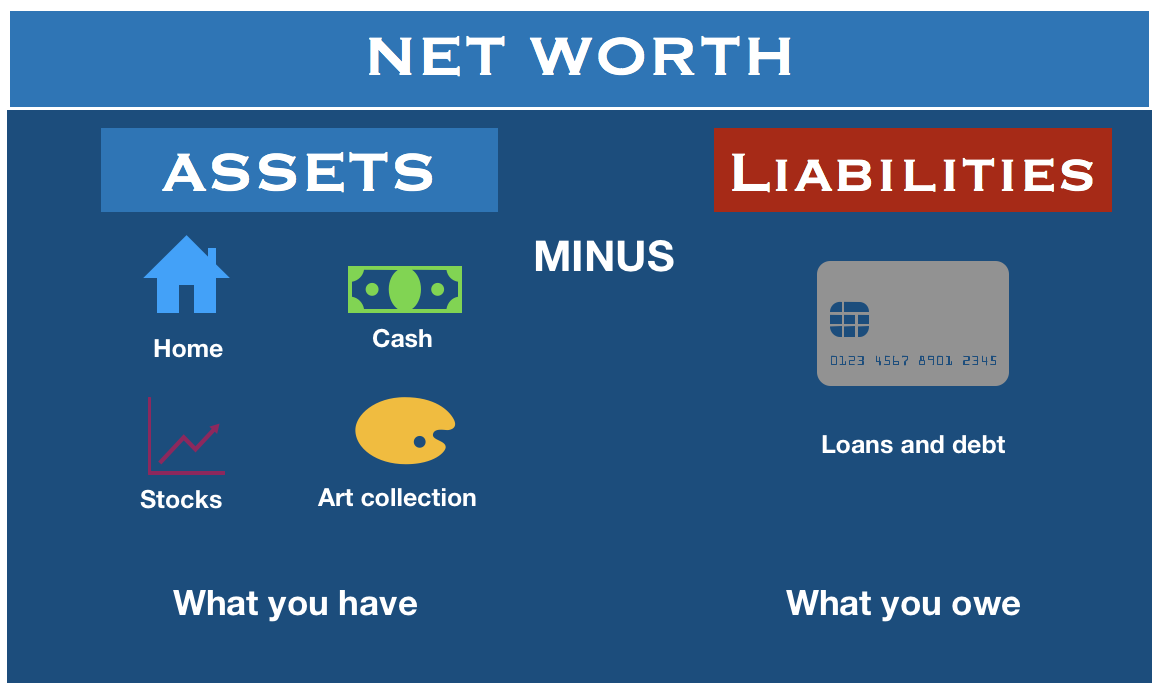

Both median and average family net worth surged between 2019 and 2022, according to the U.S. Federal Reserve. Average net worth increased by 23% to $1,063,700, the Fed reported in October 2023, the most recent year it published the data. Median net worth, on the other hand, rose 37% over that same period to $192,900.

You might wonder why the average and median net worth figures are so different. That’s because when you take the average of something, you add together every value in a data set and then divide that figure by the number of individual values.

When calculating a median, you simply look at the middle figure within a data set. That said, an average figure can be significantly higher or lower than a median figure if there are extreme outliers – meaning a group of people with significantly more net worth than the rest of the group can bring the average higher.

Average Net Worth by Age

The average net worth of someone younger than 35 years old is $183,500, as of 2022. From there, average net worth steadily rises within each age bracket. Between 35 to 44, the average net worth is $549,600, while between 45 and 54, that number increases to $975,800. Average net worth surges above the $1 million mark between 55 to 64, reaching $1,566,900.

Average net worth again rises for those ages 65 to 74, to $1,794,600, before falling to $1,624,100 for the 75 and older group. The median net worth within every single age bracket, however, is much lower than the average net worth.

***

***

Physicians [MD/DO]Net Worth by Specialty

A 2023 Medscape report shows the top 10 specialties with the most survey respondents saying they are worth more than $5 million.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com

An important concept for all medical professionals to understand is the current rate of return (CCR).

According to this principle, the current rate of a taxable return must be evaluated in reference to a similar non-taxable rate of return. This allows you to focus on your portfolio’s real (after-tax return), rather than its’ nominal, or stated return.

Now, since most medical professionals own a combination of both vehicles, it is important to calculate the average rate of return (ARR), as demonstrated in the following matrix. Usually, this will result in the assumption of more risk, for the possibility of great return.

To compare after tax yields, with taxable yields, use the following formulas:

Tax equivalent yield = yield / (1 – MTB), while taxable yield X (1-tax rate) = tax exempt yield.

Example: if the yield on a tax exempt municipal bond was 6%, and you are in a 28% tax bracket; the equivalent taxable yield (ETY), is 8.3%, calculated in the following manner: 06 / 1.00 – .28 =.083, or, 8.3% ETY. This means that you would need a taxable instrument paying almost 9 % to equal the 6 percent tax exempt bond.

Posted on March 27, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS

By Staff Reporters

***

***I

Intel (NASDAQ: INTC) just said today, that three members of its board of directors would be stepping down as the embattled chip maker reshapes itself under new Chief Executive Lip Bu-Tan.

Omar Ishrak, the former CEO of medical device maker Medtronic (MDT), University of California, Berkeley Dean Tsu-Jae King Liu and University of Pennsylvania professor Risa Lavizzo-Mourey are leaving Intel’s board, the company said in a filing.

For years, I thought of cryptocurrency as a digital replacement for traditional money. After all, Bitcoin has “coin” right in the name. But let’s be honest: if Bitcoin is a currency, then my mother’s old Beanie Baby collection is a retirement fund.

A real currency needs to be stable. It should allow you to buy a coffee today without wondering whether, by tomorrow, that same amount could buy a car—or be worth nothing at all. Bitcoin and its kin like Ethereum and Dogecoin fail this test spectacularly.

Recently I have realized that cryptocurrency might be something even bigger and stranger than currency. It is not just digital money; it’s a bet on the huge global demand for financial autonomy.

In an age where every dollar is tracked, crypto offers an escape from traditional financial oversight. That makes it attractive not just to cybercriminals and tax evaders, but also to privacy advocates, speculators, and people living under restrictive financial policies. It doesn’t replace traditional money, it sidesteps it. It allows people to move, store, create, and destroy wealth outside of conventional banking systems. Some use it for transactions. Others see it as a hedge against inflation or a bet on the future of decentralized finance. Governments and banks don’t quite know what to do with it.

Crypto exists in a financial gray zone. It’s not widely accepted for everyday purchases, yet it can hold immense value. Unlike cash, which is limited by geography, or gold, which requires secure storage, crypto can be transferred globally in seconds. That’s part of its appeal, especially in countries with strict capital controls or volatile economies.

At the heart of cryptocurrency’s identity is the way it is produced. Crypto isn’t just a speculative asset—it’s an industrialized wealth-creation system. Imagine a massive warehouse filled with powerful computers “manufacturing” cryptocurrency. These mining operations exist solely to create new “coins” and process transactions, consuming enormous amounts of electricity in the process. The larger the operation, the more crypto it produces.

This is not how traditional currencies work. Fiat currencies are managed by central banks aiming for economic stability. Crypto, by contrast, is controlled by a decentralized network of miners and participants [block-chain]. Its supply is fixed, immune to government intervention. Some see this as a weakness. Others argue it is crypto’s greatest strength.

As Bitcoin and other major cryptocurrencies become more integrated into mainstream finance, the risks evolve. Even as regulators warn about crypto’s role in illicit activity, major corporations and investment firms are offering crypto-backed products. Some politicians, including President Trump, are discussing national Bitcoin reserves. This growing legitimacy makes crypto harder to ignore. But if crypto-backed funds become widespread, a crash could ripple far beyond crypto traders. That said, crypto remains a small fraction of global finance. Unless institutional adoption grows significantly, even a major downturn likely wouldn’t trigger systemic collapse.

Crypto’s increasing presence in finance does not make it a sound retirement investment. It is still a speculation. And speculations—whether in Bitcoin, meme stocks, or dot-com startups—are high-risk and not suitable for long-term financial security. Retirement portfolios should be built on diversification, stability, and predictable returns. Crypto offers none of these.

For years, I saw crypto as a failed currency. What I now think it to be is a decentralized speculative asset, driven by a growing demand to bypass traditional financial systems. Its future remains uncertain. As regulation increases and mainstream adoption expands, its role will continue to shift. But crypto is no longer just a niche experiment. It has become a financial force that governments, institutions, and individuals must reckon with—whether they embrace it or try to control it.

Posted on March 26, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Donald Trump has officially dropped a stablecoin. It’s called USD1, and it’s pegged 1:1 with the US dollar, according to a statement from his family company World Liberty Financial Inc, (WLFI) today. The company says the token is fully backed by short-term US government treasuries, USD deposits, and other cash equivalents. Every token equals one dollar, no exceptions. WLFI says it built the whole thing to give people a stablecoin they don’t have to second guess.

US stocks rose for a third day in a row despite souring consumer confidence — and as investors weighed whether President Trump would temper his plans for upcoming tariffs.

The benchmark S&P 500 (^GSPC) rose more than 0.1%, while the Dow Jones Industrial Average (^DJI) ticked just above the flatline. The tech-heavy NASDAQ Composite (^IXIC) rose nearly 0.5%, bolstered by a more than 3% jump from Tesla (TSLA).

Posted on March 25, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Wikipedia and Staff Reporters

***

***

Congestion pricing or congestion charges is a system of surcharging users of public goods that are subject to congestion through excess demand, such as through higher peak charges for use of bus services, electricity, railways, telephones, and road pricing to reduce traffic congestion; airlines and shipping companies may be charged higher fees for slots at airports and through canals at busy times. This pricing strategy regulates demand, making it possible to manage congestion without increasing supply.

According to the economic theory behind congestion pricing, the objective of this policy is to use the price mechanism to cover the social cost of an activity where users otherwise do not pay for the negative externalities they create (such as driving in a congested area during peak demand).

By setting a price on an over-consumed product, congestion pricing encourages the redistribution of the demand in space or in time, leading to more efficient outcomes.

A hostile takeover happens when an entity takes control of a company without the knowledge and against the wishes of the company’s management. A hostile takeover is an acquisition strategy requiring that the entity acquire and control more than 50% of the voting shares issued by the company.

In mergers and acquisitions (M&A), a hostile takeover is the acquisition of a target company by an acquiring company that goes directly to the target company’s shareholders, either by making a tender offer or through a proxy vote.

Ideally, an entity interested in acquiring a company should seek approval from the target company’s Board of Directors. The difference between a hostile and a friendly takeover is that, in a friendly takeover, the target company’s board of directors approve of the transaction and recommend shareholders vote in favor of the deal.

Defenses against a hostile takeover

These defense mechanisms can be preemptive or reactive, depending on how prepared the company is for the possibility of a hostile bid.

Poison pill is one of the most common defenses against a hostile takeover. Officially known as a “shareholder rights plan,” the poison pill allows existing shareholders to purchase additional shares at a discount, diluting the ownership interest of the acquiring company. The goal is to make it prohibitively expensive for the acquirer to complete the takeover.

A golden parachute is another defense strategy, which involves providing lucrative compensation packages (bonuses, severance pay, stock options, etc.) to key executives in the event they are terminated as a result of the takeover. This creates a financial disincentive for the acquiring company, as it would need to pay out these large sums upon completing the takeover.

In a Crown jewel defense, the target company sells or threatens to sell its most valuable assets—its “crown jewels”—if the takeover is completed. This reduces the attractiveness of the company to the acquirer, as the most desirable assets would no longer be part of the deal.

The Pac-Man defenses a more aggressive strategy in which the target company turns the tables by attempting to buy shares of the acquiring company, effectively launching a counter-takeover. While rare, this defense can deter hostile bids by making the takeover battle more costly and complex.

A White-Knight defense involves the target company seeking out a more favorable acquirer, or “white knight,” to make a friendly takeover bid. This allows the target company to avoid the hostile acquirer while still securing the benefits of a merger or acquisition.

The hostile takeover between Sanofi-Aventis and Genzyme Corp. occurred in 2010 when Sanofi, a French pharmaceutical company, wanted to buy Genzyme, a US biotech firm specializing in rare diseases. Genzyme resisted the offer, leading to conflict. Sanofi started a public campaign to pressure Genzyme’s shareholders into selling.

After months of negotiations, the two companies reached a deal in 2011. Sanofi agreed to pay $74 per share, with additional payments tied to Genzyme’s future performance, bringing the total deal value to around $20.1 billion. This acquisition allowed Sanofi to expand into the lucrative market for rare disease treatment.

Posted on March 24, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Futures attached to the benchmark S&P 500 (ES=F) rose 0.6%, with NASDAQ 100 (NQ=F) futures up 0.7%. Futures tied to the Dow Jones Industrial Average (YM=F) advanced around 0.4%.

Posted on March 23, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

ByJ. Chris Miller JD

***

***

Your personal and financial life is constantly changing. Significant changes always necessitate the need to review your life. However, a few key events trigger the need to review your estate plan. If any of the events below have occurred since you reviewed your estate plan, see a competent adviser to help you achieve your goals.

Birth of a child or grandchild.

Death of a spouse, beneficiary, guardian, trustee or personal representative.

Marriage of you or your children.

Divorce. (Review beneficiary designations and asset titling)

Move out of state. An estate is settled under the laws of the state in which the decedent resided. Certain provisions of a will that are valid in one state may not be in another.

Change in estate value. A large increase or decrease in the size of an estate may greatly affect some of the strategies that were implemented.

Changes in business. Starting, buying or selling a medical practice or other business has an impact on your estate. The addition or death of a business owner will cause a review.

Tax law changes. EGTRRA has dramatically changed the way we plan for estate taxes. It is important to note that only planning for estate taxes has been effected. Estate planning involves much more than just the motivation to reduce or eliminate taxes. Assuring that your family is financially taken care of, that children have the opportunity to go to college, that your debts are paid, that charitable desires are achieved, provisions for a needy child, proper selection of a guardian, the list goes on. Please do not use the new law as an excuse to not plan your estate.

***

OVERHEARD IN THE FINANCIAL ADVISOR’S LOUNGE

From my perspective, estate planning is a team sport, and lawyers rely on financial advisers all the time to spot issues for clients. We do not share the opinion that non-lawyers are incapable of giving good advice.

Absolute Return – the goal is to have a positive return, regardless of market direction. An absolute return strategy is not managed relative to a market index.

Accredited Investor – wealthy individual or well-capitalized institutions covered under Regulation D of the Securities Act of 1933.

Alpha – the return to a portfolio over and above that of an appropriate benchmark portfolio (the manager’s “value added”).

Arbitrage – any strategy that invests long in an asset, and short in a related asset, hoping the prices will converge.

Attribution – the process of “attributing” returns to their sources. For example, did the returns to a portfolio (over and above some benchmark) come from stock selection, industry/sector over- or under-weighting or factor weighting. Software programs are helpful in reporting an attribution.

Beta – a measure of systematic (i.e., non-diversifiable) risk. The goal is to quantify how much systematic risk is being taken by the fund manager vis-à-vis different risk factors, so that one can estimate the alpha or value-added on a risk-adjusted basis.

Correlation – a measure of how strategy returns move with one another, in a range of –1 to +1. A correlation of –1 implies that the strategies move in opposite directions. In constructing a portfolio of hedge funds, one usually wants to combine a number of non-correlated strategies (with decent expected returns) to be well diversified.

Drawdown – the percentage loss from a fund’s highest value to its lowest, over a particular time frame. A fund’s “maximum drawdown” is often looked at as a measure of potential risk.

Hurdle Rate – the return where the manager begins to earn incentive fees. If the hurdle rate is 5% and the fund earns 15% for the year, then incentive fees are applied to the 10% difference.

Leverage – one uses leverage if he borrows money to increase his position in a security. If one uses leverage and makes good investment decisions, leverage can magnify the gain. However, it can also magnify a loss.

Opportunistic – a general term that describes an aggressive strategy with a goal of making money (as opposed to holding on to the money one already has).

***

***

Pairs Trading – usually refers to a long/short strategy where one stock is bought long, and a similar stock is sold short, often within the same industry. Buying the stock of Home Depot and shorting Lowe’s in an equal amount would be an example.

Portfolio Simulation – involves testing an investment strategy by “simulating” it with a database and analytic software. Often referred to as “backtesting” a strategy. The simulated returns of the strategy are compared to those of a benchmark over a specific time frame to see if it can beat that benchmark.

Sharpe Ratio – a measure of risk-adjusted return, computed by dividing a fund’s return over the risk-free rate by the standard deviation of returns. The idea is to understand how much risk was undertaken to generate the alpha.

Short Rebate – if you borrow stock and then sell it short, you have cash in your account. The short rebate is the interest earned on that cash.

R-Squared – a measure of how closely a portfolio’s performance varies with the performance of a benchmark, and thus a measure of what portion of its performance can be explained by the performance of the overall market or index. Hedge fund investors want to know how much performance can be explained by market exposure versus manager skill.

Transportable Alpha – the alpha of one active strategy can be combined with another asset class. For example, an equity market-neutral strategy’s value-added can be “transported” to a fixed income asset class by simply buying a fixed income futures contract. The total return comes from both sources.

Value at Risk – a technique which uses the statistical analysis of historical market trends and volatilities to estimate the likelihood that a specific portfolio’s losses will exceed a certain amount.

Posted on March 21, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

Beware – Public Improvement Fees

Beware – Public Improvement Districts

By Staff Reporters

***

***

A Public Improvement Fee (PIF) is a fee that developers may require their tenants to collect on sales transactions to pay for on-site improvements. The PIF is a fee and NOT a tax; therefore, it becomes a part of the overall cost of the sale/service and is subject to sales tax

Examples of these improvements include curbs and sidewalks, parking facilities, storm management system, sanitary sewer systems, road development (within the site) and outdoor public plazas.

Public Improvement Districts (PIDs) are a financing mechanism used to fund new developments and infrastructure improvements. PIDs are relatively easy to create and can be done by the local municipality. A majority of property owners within the district may petition a local government to create the district. Bonds can then be issued to fund a development or infrastructure improvements. Through an industry analysis and view of the current political environment, PIDs are certainly a beneficial mechanism to fund projects otherwise not feasible due to constraints on city budgets. Local elected officials will want PIDs monitored and only used in proper circumstances.

Posted on March 21, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

The term “value” has many different meanings and definitions to different parties. Therefore, at the outset of each valuation engagement, it is critical to define appropriately (and have all parties agree to) the standard of value to be employed in developing the valuation opinion.

The standard of value defines the type of value to be determined and answers the question “value to whom?” There are several standards of value that may be sought, including: Fair Market Value (FMV), Fair Value, Investment Value, and Liquidation Value. (Read more...)

Posted on March 19, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS!

***

***

The Federal Reserve just opted to hold interest rates steady as officials reckon with fearful markets and concerns of an economic slowdown sparked by the trade wars launched by President Donald Trump and his efforts to overhaul and dismantle government agencies.

After a two-day meeting of its monetary policy committee in Washington, D.C., the Fed announced it would hold its rate target at a range of 4.25% to 4.50%. Investors anticipated the move. The Fed’s target rate remains a full percentage point lower than it was when the Fed pivoted to cutting rates last September.

Posted on March 19, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Split-Dollar Life Insurance: An arrangement under which a life insurance policy’s premium, cash values, and death benefit are split between two parties—usually a corporation and a key employee or executive. Under such an arrangement an employer may own the policy and pay the premiums and give a key employee or executive the right to name the recipient of the death benefit.

***

***

Several factors will affect the cost and availability of life insurance, including age, health, and the type and amount of insurance purchased. Life insurance policies have expenses, including mortality and other charges. If a policy is surrendered prematurely, the policy holder also may pay surrender charges and have income tax implications. You should consider determining whether you are insurable before implementing a strategy involving life insurance.

Any guarantees associated with a policy are dependent on the ability of the issuing insurance company to continue making claim payments.

“Malta has quietly leveraged the rising tide of the financial transparency imperative to attract hedge funds.“

There was a time when the quaint island sought to play on the traditional terrain, offering anonymity and a “laissez-faire regulatory regime,” not to mention very low taxes, as in no capital gains taxes and no taxes on dividends; all while English speaking and USD currency denominated.

***

***

While many leading domiciles for offshore hedge funds remain in the Caribbean – notably the Cayman Islands, the British Virgin Islands, Bermuda, and the Bahamas – the island of Malta is drawing attention, especially from European funds.

SO – HOW MUCH IS A “FINANCIAL ADVISOR” REALLY WORTH?

This blog holds a rather uncomplimentary opinion of financial advisors, and the financial services and brokerage industry as a whole; deserved, or not? The entire site hints at this attitude as well, in favor of a going it alone or ME, Inc investing when possible. Nevertheless, it is reasonable to wonder how much boost in net-returns might an educated and informed, fee transparent and honest, fiduciary focused “financial advisor” add to a clients’ investment portfolio; all things being equal [ceteris paribus].

And, can it be quantified?

Well, according to Vanguard Brokerage Services®, perhaps as much as 3%? In a decade long paper from the Valley Forge, PA based mutual fund and ETF giant, Vanguard said financial advisors can generate returns through a framework focused on five wealth management principles:

• Being an effective behavioral coach: Helping clients maintain a long-term perspective and a disciplined approach is arguably one of the most important elements of financial advice. (Potential value added: up to 1.50%).

• Applying an asset location strategy: The allocation of assets between taxable and tax-advantaged accounts is one tool an advisor can employ that can add value each year. (Potential value added: from 0% to 0.75%).

• Employing cost-effective investments: This component of every advisor’s tool kit is based on simple math: Gross return less costs equals net return. (Potential value added: up to 0.45%).

• Maintaining the proper allocation through rebalancing: Over time, as investments produce various returns, a portfolio will likely drift from its target allocation. An advisor can add value by ensuring the portfolio’s risk/return characteristics stay consistent with a client’s preferences. (Potential value added: up to 0.35%).

• Implementing a spending strategy: As the retiree population grows, an advisor can help clients make important decisions about how to spend from their portfolios. (Potential value added: up to 0.70%).

Source: Financial Advisor Magazine, page 20, April 2014.

Assessment

However, Vanguard notes that while it’s possible all of these principles could add up to 3% in net returns for clients, it’s more likely to be an intermittent number than an annual one because some of the best opportunities to add value happen during extreme market lows and highs when angst or giddiness [fear and greed] can cause investors to bail on their well-thought-out investment plans.

And, is the study applicable to doctors and allied healthcare providers? Doe Vanguard have a vested interest in the topic. What about fee based versus fee-only financial advice?

Conclusion

Finally, recognize the plethora of other financial planning life-cycle topics addressed in this ME-P were not included in the Vanguard investment portfolio-only study a decade ago.

And what about today with contemporaneous internet advising, chat-rooms, linkedin, robo-advisors, reddit and the like?

When analyzing a set of financial statements to determine practice value, adjustments (normalizations) generally are needed to produce a clearer picture of likely future income and distributable cash flow. It also allows more of an “apples to apples” line item comparison. This normalization process usually consists of making three main adjustments to a medical practice’s net income (profit and loss) statement.

1. Non-Recurring Items: Estimates of future distributable cash flow should exclude non-recurring items. Proceeds from the settlement of litigation, one-time gains/losses from the selling of assets or equipment, and large write-offs that are not expected to reoccur, each represent potential nonrecurring items. The impact of nonrecurring events should be removed from the practice’s financial statements to produce a clearer picture of likely future income and cash flow.

2. Perquisites: The buyer of a medical practice may plan to spend more or less than the current doctor-owner for physician executive compensation, travel and entertainment expenses, and other perquisites of current management. When determining future distributable cash flow, income adjustments to the current level of expenditures should be made for these items.

3. Non-cash Expenses: Depreciation expense, amortization expense, and bad debt expense are all non-cash items which impact reported profitability. When determining distributable cash flow, you must analyze the link between non-cash expenses and expected cash expenditures.

The annual depreciation expense is a proxy for likely capital expenditures over time. When capital expenditures and depreciation are not similar over time, an adjustment to expected cash flow is necessary. Some practices reduce income through the use of bad debt expense rather than direct write-offs. Bad debt expense is a non-cash expense that represents an estimate of the dollar volume of write-offs that are likely to occur during a year. If bad debt expense is understated, practice profitability will be overstated.

***

***

Balance Sheet Adjustments

Adjustments also can be made to a practice’s balance sheet to remove non-operating assets and liabilities, and to restate asset and liability value at market rates (rather than cost rates). Assets and liabilities that are unrelated to the core practice being valued should be added to or subtracted from the value, depending on whether they are acquired by the buyer.

Examples include the asset value less outstanding debt of a vacant parcel of land, and marketable securities that are not needed to operate the practice. Other non-operating assets, such as the cash surrender value of officer life insurance, generally are liquidated by the seller and are not part of the business transaction.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com

Health actuaries analyze potential risks, profits and trends that will affect their employers, which are often in the health insurance, government health services and medical provider industries. They advise companies on issuing policies to consumers based on risks, calculated premiums and upcoming changes in health-care costs.

It’s common for an actuary to have a bachelor’s degree or higher in actuary studies, mathematics or statistics. Coursework on medical terminology and hierarchy of the medical field is also beneficial. In addition to academic education, certification is also necessary to reach “professional status,” which is required by most employers.

***

***

The professional organization, Society of Actuaries, certifies actuaries in the health and medical field. Their statistical work is commonly done with predictive tables, probability tables and life tables that are created on customized statistical analysis software such as Stata or XLSTAT.

The actuary field as a whole is growing faster than other fields, according to the Bureau of Labor Statistics [BLS]. In 2020, it expanded by 27 percent. The average annual salary for an actuary in 2010 was $87,650. More specifically, in the health insurance field, the salary was slightly higher at $91,000.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com

Posted on March 16, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

DEFINITION

***

***

According to Wikipedia, a tontine (/ˈtɒntaɪn, -iːn, ˌtɒnˈtiːn/) is an investment linked to a living person which provides an income for as long as that person is alive. Such schemes originated as plans for governments to raise capital in the 17th century and became relatively widespread in the 18th and 19th centuries.

Tontines enable subscribers to share the risk of living a long life by combining features of a group annuity with a kind of mortality lottery. Each subscriber pays a sum into a trust and thereafter receives a periodical payout. As members die, their payout entitlements devolve to the other participants, and so the value of each continuing payout increases. On the death of the final member, the trust scheme is usually wound up.

Tontines are still common in France. They can be issued by European insurers under the Directive 2002/83/EC of the European Parliament. The Pan-European Pension Regulation passed by the European Commission in 2019 also contains provisions that specifically permit next-generation pension products that abide by the “tontine principle” to be offered in the 27 EU member states.

Questionable practices by U.S. life insurers in 1906 led to the Armstrong Investigation in the United States restricting some forms of tontines. Nevertheless, in March 2017, The New York Times reported that tontines were getting fresh consideration as a way for people to get steady retirement income.

Posted on March 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS

By Staff Reporters

***

***

The Consumer Price Index (CPI) for February found that the cost of goods and services rose 0.2% on the month. The annual rate of inflation was also up 2.8% — slightly less than expected.

Here’s a breakdown of several price changes for February:

Food: increase 0.2%

Energy: increase 0.2%

Electricity: increase 1.0%

New vehicles: decrease 0.1%

Used vehicles: increase 0.9%

Apparel: increase 0.6%

Shelter: increase 0.3%

Transportation: decrease 0.8%

Medical care services: increase 0.3%

The Bureau of Labor Statistics reported that according to its indexes, over the month the cost of medical care rose 0.3%, physicians’ services were 0.4% higher, hospital services added 0.1%, and prescription-drug costs were unchanged.

Posted on March 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

What is Pi?

Pi is the ratio of the circumference of a circle to its diameter, or approximately 3.14.

What is Pi Day?

Pi Day occurs on March 14, because the date is written as 3/14 in the United States. If you’re a serious math geek, celebrate the day exactly at 1:59 a.m. or p.m. so you can reach the first six numbers of pi, 3.14159.

Posted on March 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BEHAVIORAL ECONOMICS

By Staff Reporters

***

***

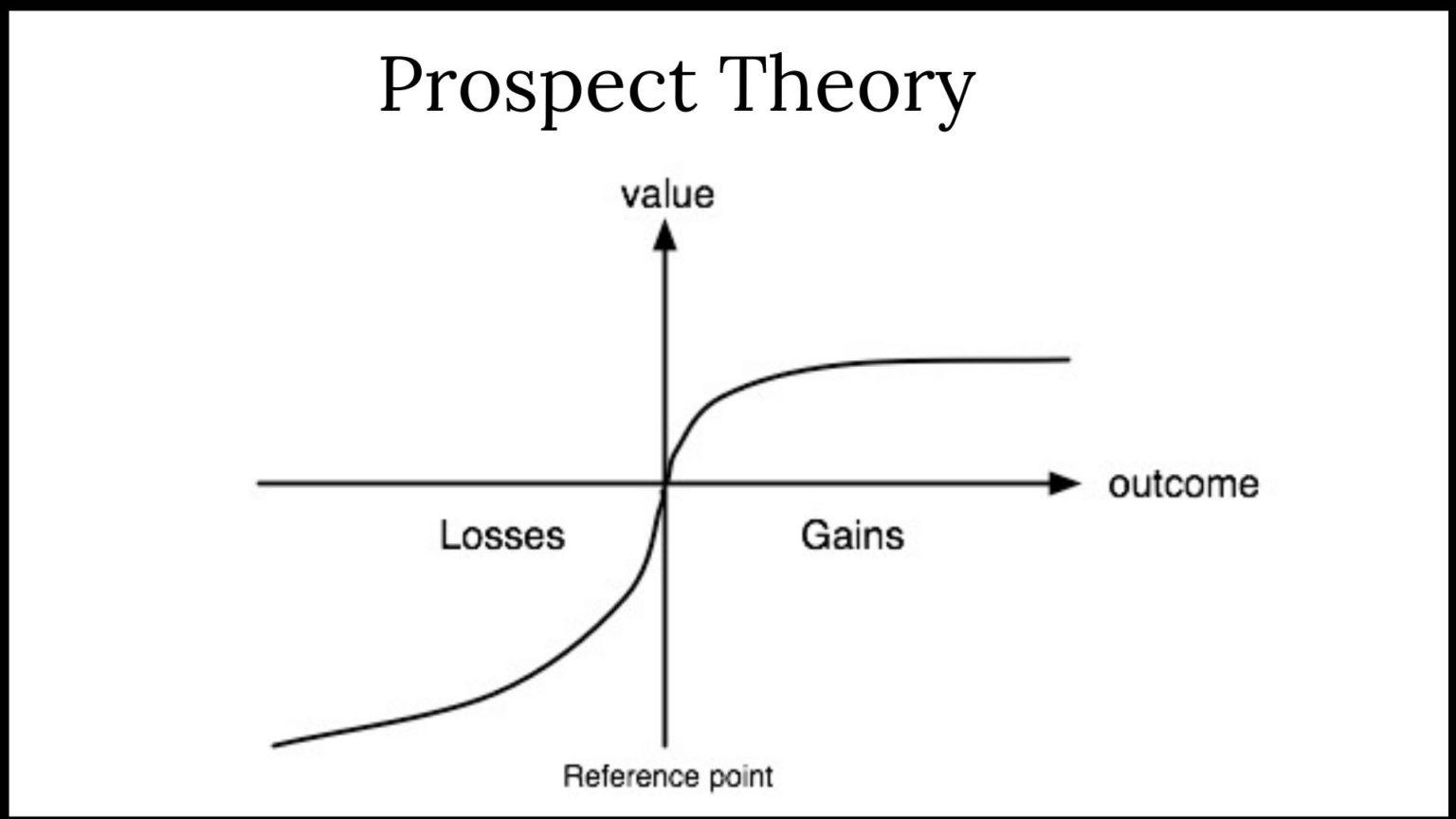

Prospect theory is a psychological and behavioral economics theory developed by Daniel Kahneman and Amos Tversky in 1979. It explains how people make decisions when faced with alternatives involving risk, probability, and uncertainty. According to this theory, decisions are influenced by perceived losses or gains.

Example:

Amanda, a DO client, was just informed by her financial advisor that she needed to re-launch her 403-b retirement plan. Since she was leery about investing, she quietly wondered why she couldn’t DIY. Little does her FA know that she doesn’t intend to follow his advice, anyway! So, what went wrong?

The answer may be that her advisor didn’t deploy a behavioral economics framework to support her decision-making. One such framework is the “prospect theory” model that boils client decision-making into a “three step heuristic.”

Prospect theory makes the unspoken biases that we all have more explicit. By identifying all the background assumptions and preferences that clients [patients] bring to the office, decision-making can be crafted so that everyone [family, doctor and patient] or [FA, client and spouse] is on the same page. Briefly, the three steps are:

1. Simplify choices by focusing on the key differences between investment [treatment] options such as stock, bonds, cash, and index funds.

2. Understanding that clients [patients] prefer greater certainty when it comes to pursuing financial [health] gains and are willing to accept uncertainty when trying to avoid a loss [illness].

3. Cognitive processes lead clients and patients to overestimate the value of their choices thanks to survivor bias, cognitive dissonance, appeals to authority and hindsight biases.

Assessment

Much like healthcare today, the current mass-customized approaches to the financial services industry falls short of recognizing more personalized advisory approaches like prospect theory and assisted client-centered investment decision-making.

Posted on March 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITION

By Staff Reporters

***

***

1035 Exchange

DEFINITION: A method of exchanging insurance-related assets without triggering a taxable event. Cash-value life insurance policies and annuity contracts are two products that may qualify for a 1035 exchange.

***

A 1035 exchange is a feature in the tax code that permits individuals to transfer funds from an existing life insurance endowment, or annuity policy to a new one without tax consequences.

These transactions are not subject to tax deductions or tax credits but rather tax deferrals, meaning that individuals would only pay taxes on any earnings once they receive money from the policy later.

Without this provision, policyholders would have to close their previous accounts and be subjected to both taxes and surrender charges before they could open a new account.

Posted on March 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters and IRS

***

***

Straddles: A straddle is any set of offsetting positions on personal property. For example, a straddle may consist of a purchased option to buy and a purchased option to sell on the same number of shares of the security, with the same exercise price and period.

Personal property.

This is any actively traded property. It includes stock options and contracts to buy stock but generally does not include stock.

Straddle rules for stock.

Although stock is generally excluded from the definition of personal property when applying the straddle rules, it is included in the following two situations.

The stock is of a type that is actively traded, and at least one of the offsetting positions is a position on that stock or substantially similar or related property.

The stock is in a corporation formed or availed of to take positions in personal property that offset positions taken by any shareholder.

Note

For positions established before October 22, 2004, condition 1 above does not apply. Instead, personal property includes stock if condition 2 above applies or the stock was part of a straddle in which at least one of the offsetting positions was:

An option to buy or sell the stock or substantially identical stock or securities,

A securities futures contract on the stock or substantially identical stock or securities, or

A position on substantially similar or related property (other than stock).

Position

A position is an interest in personal property. A position can be a forward or futures contract or an option.

An interest in a loan denominated in a foreign currency is treated as a position in that currency. For the straddle rules, foreign currency for which there is an active inter bank market is considered to be actively traded personal property.

Offsetting position

This is a position that substantially reduces any risk of loss you may have from holding another position. However, if a position is part of a straddle that is not an identified straddle, do not treat it as offsetting to a position that is part of an identified straddle.

Presumed offsetting positions

Two or more positions will be presumed to be offsetting if:

The positions are established in the same personal property (or in a contract for this property), and the value of one or more positions varies inversely with the value of one or more of the other positions;

The positions are in the same personal property, even if this property is in a substantially changed form, and the positions’ values vary inversely as described in the first condition;

The positions are in debt instruments with a similar maturity, and the positions’ values vary inversely as described in the first condition;

The positions are sold or marketed as offsetting positions, whether or not the positions are called a straddle, spread, butterfly, or any similar name; or

The aggregate margin requirement for the positions is lower than the sum of the margin requirements for each position if held separately.

Related persons

To determine if two or more positions are offsetting, you will be treated as holding any position your spouse holds during the same period. If you take into account part or all of the gain or loss for a position held by a flow-through entity, such as a partnership or trust, you are also considered to hold that position.

Posted on March 12, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

The IRS 1099-k Tax Form

By Staff Reporters and IRS

***

***

Third party payment platforms are required to send you a 1099-K tax form if you made more than $5,000 on the platform in 2024. This reporting change will give the IRS a clearer picture of how much you earned in untaxed income this year to help ensure you pay your taxes properly. For the 2025 tax year, the threshold will drop to $2,500.

The IRS originally rolled out a plan to implement new reporting requirements for anyone earning over $600 via payment apps in 2023. After two years of delays, the tax agency has decided to implement a phased rollout, lifting the reporting threshold to $5,000 for the 2024 tax year.

If you earn freelance or self-employment income, you’re likely no stranger to 1099 tax forms. You’re required to report any net earnings over $400 to the IRS when you file your tax return, even if you don’t receive a 1099. The 1099-K tax change places a reporting requirement on payment apps so the IRS can keep better tabs on income earnings that might otherwise go unreported.

Posted on March 10, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS

By Staff Reporters

***

***

US stocks plunged on Monday as investors processed growing concerns about the health of the US economy after President Trump and his top economic officials acknowledged the possibility of a potential rough patch.

The Dow Jones Industrial Average (^DJI) fell nearly 900 points, or over 2%, while the benchmark S&P 500 (^GSPC) dropped around 2.7% after the index posted its worst week since September.

The tech-heavy NASDAQ Composite (^IXIC) fell 4% in its worst day since 2022, as the “Magnificent Seven” stocks led the sell-off. Tesla’s (TSLA) rout continued, plunging 15% and officially wiping out the gains it had made in the wake of Trump’s election win. Nvidia (NVDA), Apple (AAPL), Google parent Alphabet (GOOG), and Meta (META) all each lost more than 4%.

I was having lunch with a close friend of mine. He mentioned that he had accumulated a significant sum of money and did not know what to do with it. It was sitting in bonds, and inflation was eating its purchasing power at a very rapid rate.

He is a dentist and had originally thought about expanding his business, but a shortage of labor and surging wages turned expanding into a risky and low-return investment. He complained that the stock market was extremely expensive. I agreed.*

He said that the only thing left was residential real estate. I pushed back. “What do you think will happen to the affordability of houses if – and most likely when – interest rates go up? Inflation is now 6%. I don’t know where it will be in a year or two, but what if it becomes a staple of the economy? Interest rates will not be where they are today. Even at 5% interest rates [I know, a number unimaginable today] houses become unaffordable to a significant portion of the population. Yes, borrowers’ incomes will be higher in nominal terms, but the impact of the doubling of interest rates on the cost of mortgages will be devastating to affordability.”

He rejoined, “But look at what happened to housing over the last twenty years. Housing prices have consistently increased, even despite the financial crisis.”

I agreed, but I qualified his statement: “Over the past twenty, actually thirty, years interest rates declined. I honestly don’t know where interest rates will be in the future. But probabilistically, knowing what we know now, the chances that they are going to be higher, much higher, are more likely than their staying low. Especially if you think that inflation will persist.”

We quickly shifted our conversation toward more meaningful topics, like kids.

It seems that every year I think we have finally reached the peak of crazy, only to be proven wrong the next year. The stock market and thus index funds, just like real estate, have only gone one way – up. Index funds became the blunt instrument of choice in an always-rising market. So far, this choice has paid off nicely.

The market is the most expensive it has ever been, and thus future returns of the market and index funds will be unexciting. (I am being gentle here.)

You don’t have to be a stock market junkie to notice the pervasive feeling of euphoria. But euphoria is a temporary, not a permanent emotion; and at least when it comes to the stock market, it is usually supplanted by despair. Market appreciation that was driven by expanding valuations was not a gift but a loan – the type of loan that must always be paid back with a high rate of interest.

I don’t know what straw will break the feeble back of this market or what will cause the music to stop (there, you got two analogies for the price of none). We are in an environment where there are very few good options. If you do nothing, your savings will be eaten away by inflation. If you do something, you find that most assets, including the stock market as a whole, are incredibly overvalued.

We are doing the only sensible thing that you can do today. We spend very little time thinking about straws or what will cause the music to stop or how overvalued the market is. We are focusing all our energy on patiently building a portfolio of high-quality, cash-generative, significantly undervalued businesses that have pricing power.

This has admittedly been less rewarding than taking risky bets on unimaginably expensive assets. It may lack the excitement of sinking money into the darlings you see in the news every day, but we hope that our stocks will look like rare gems when the euphoria condenses into despair. As we keep repeating in every letter, the market is insanely overvalued. Our portfolio is anything but – we don’t own “the market”.

*A question may arise:Why did I not tell my dentist friend to pick individual stocks? He runs a busy dental practice and wouldn’t have the time or the training to pick stocks.

Why didn’t I offer him our services? IMA manages all my and my family’s liquid assets, but I have a rule that I never (ever!) break – I don’t manage my friends’ money. I’ll help them as much as possible with free advice but will never have a professional relationship with them. I intentionally create a separation between my personal and professional lives. After a difficult day in the market, I want to be able to go for beers with friends and leave the market at the office.

Also, this simplifies my relationships with my friends. There is no ambiguity in our friendship.

Posted on March 9, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITION

By Staff Reporters

***

***

FACILITY CHARGEDEFINED

Classic: Service fee submitted for payment by a healthcare facility, such as a clinic, hospital or ambulatory care center.

Modern: Facility fees are expenses charged by hospitals to cover their overhead – the funding needed to keep the lights on, machines running, and doors open, etc. People who receive outpatient care at hospital-owned buildings are charged a facility fee, in addition to treatment costs and fees charged, individually, by doctors.

Examples: How to Fight Facility Fees:

Check with your health agent or insurer. Many insurers don’t cover facility fees or cover only a portion.

Talk to your doctor. It’s hard to tell whether a facility is hospital-run or whether your doctor works for a health system.

You can also listen to a professional narration of this article on iTunes & online.

ENCORE: March 22, 2004

A basic property of religion is that the believer takes a leap of faith: to believe without expecting proof. Often you find this property of religion in other, unexpected places – for example, in the stock market. It takes a while for a company to develop a “religious” following: only a few high-quality, well-respected companies with long track records ever become worshipped by millions of investors. My partner, Michael Conn, calls these “religion stocks.” The stock has to make a lot of shareholders happy for a long period of time to form this psychological link.

The stories (which are often true) of relatives or friends buying few hundred shares of the company and becoming millionaires have to fester a while for a stock to become a religion. Little by little, the past success of the company turns into an absolute – and eternal – truth. Investors’ belief becomes set: the past success paints a clear picture of the future.

Gradually, investors turn from cautious shareholders into loud cheerleaders. Management is praised as visionary. The stock becomes a one-decision stock: buy. This euphoria is not created overnight. It takes a long time to build it, and a lot of healthy pessimists have to become converted into believers before a stock becomes a “religion.”

Once a stock is lifted up to “religion” status, beware: Logic is out the window. Analysts start using T-bills to discount the company’s cash flows in order to justify extraordinary valuations. Why, they ask, would you use any other discount rate if there is no risk? When a T-bill doesn’t do the trick, suddenly new and “more appropriate” valuation metrics are discovered.

Other investors don’t even try to justify the valuation – the stock did well for me in the past, why would it stop working in the future? Faith has taken over the stock. Fundamentals became a casualty of “stock religion.” These stocks are widely held. The common perception is that they are not risky.

The general public loves these companies because they can relate to the companies’ brands. A dying husband would tell his wife, “Never sell _______ (fill in the blank with the company name).” Whenever a problem surfaces at a “religion stock,” it is brushed away with the comment that “it’s not like the company is going to go out of business.” True, a “religion stock” company is a solid leader in almost every market segment where it competes and the company’s products carry a strong brand name. However, one should always remember to distinguish between good companies and good stocks.

Coca-Cola is a classic example of a “religion stock.” There are very few companies that have delivered such consistent performance for so long and have such a strong international brand name as Coca-Cola. It is hard not to admire the company.

But admiration of Coca-Cola achieved an unbelievable level in the late nineties. In the ten years leading up to 1999, Coca-Cola grew earnings at 14.5% a year, very impressive for a 103-year-old company. It had very little debt, great cash flow and a top-tier management. This admiration came at a steep price: Coca-Cola commanded a P/E of 47.5. That P/E was 2.7 times the market P/E. Even after T-bills could no longer justify Coke’s valuation, analysts started to price “hidden” assets – Coke’s worldwide brand. No money manager ever got fired for owning Coca-Cola.

The company may not have had a lot of business risk. But in 1999, the high valuation was pricing in expectations that were impossible for any mature company to meet. “The future ain’t what it used to be” – Yogi Berra never lets us down. Success over a prolonged period of time brings a problem to any company – the law of large numbers.

Enormous domestic and international market share, combined with maturity of the soft drink market, has made it very difficult for Coca-Cola to grow earnings and sales at rates comparable to the pre-1999 years. In the past five years, earnings and sales have grown 2.5% and 1.5% respectively. After Roberto C. Goizueta’s death, Coke struggled to find a good replacement – which it acutely needed.

Old age and arthritis eventually catch up with “religion stocks.” No company can grow at a fast pace forever. Growth in earnings and sales eventually decelerates. That leads to a gradual deflation of the “religion” premium. For Coke, the descent from its “religious” status resulted in a drop of nearly 20% in the share price – versus an increase of 65% in the broad market over the same time. And at current prices, the stock still is not cheap by any means. It trades at 25 times December 2004 earnings, despite expectations for sales growth in the mid single digits and EPS growth in the low double digits.

It takes a while for the religion premium to be totally deflated because faith is a very strong emotion. A lot of frustration with sub-par performance has to come to the surface.

Disappointment chips away at faith one day at a time. “Religion” stocks are not safe stocks. The leap of faith and perception of safety come at a large cost: the hidden risk of reduction in the “religion premium.” The risk is hidden because it never showed itself in the past. “Religion” stocks by definition have had an incredibly consistent track record. Risk was rarely observed.

However, this hidden risk is unique because it is not a question of if it will show up but a question of when. It is very hard to predict how far the premium will inflate before it deflates – but it will deflate eventually. When it does, the damage to the portfolio can be huge.

Religion stocks generally have a disproportionate weight in portfolios because they are never sold – exposing the trying-to-be-cautious investor to even greater risks. Coca-Cola is not alone in this exclusive club. General Electric, Gillette, Berkshire Hathaway are all proud members of the “religion stock” club as well. Past members would include: Polaroid – bankrupt; Eastman Kodak – in a major restructuring; AT&T – struggling to keep its head above water. That stock is down from over $80 in 1999 to $18 today.

Emotions have no place in investing. Faith, love, hate, and disgust should be left for other aspects of our life. More often than not, emotions guide us to do the opposite of what we need to do to be successful. Investors need to be agnostic towards “religion stocks.” The comfort and false sense of certainty that those stocks bring to the portfolio come at a huge cost: prolonged under performance.

My thoughts today (20+ years later)

This is one of the first investment articles I ever wrote. I had just started writing for TheStreet.com. It’s interesting to read this article more than 20 years later. I am surprised my writing was not as bad as I had feared (though in many cases it was worse than I feared when I read my other early articles).

So much has happened since then – I am a different person today than I was back then. I have two more kids; I have written three more books and a thousand articles. The last two decades were my formative years as an investor and adult.

The goal of the article was not to make predictions but to warn readers that the long-term success of certain companies creates a cult-like following and deforms thinking. In fact, my original article – the one I submitted to TheStreet.com – did not mention any companies other than Coke. The editors wanted me to include more names so that the article would show up on more pages of Yahoo! Finance.

With the exception of Berkshire Hathaway, all of these companies have produced mediocre or horrible returns. In the best case, their fundamental returns in their old age were only a fraction of what they were when these companies were younger and the world was their oyster.

To my surprise, Coke’s stock is still trading at a high valuation. Its business has performed like the old-timer it is, with revenue and earnings growing by only 3–4% a year. The days of double-digit revenue and earnings growth were left in the 80s and 90s, though the high valuation remained.

Posted on March 7, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

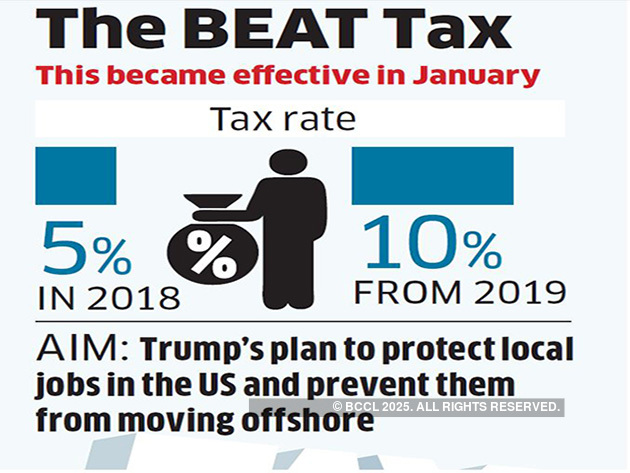

Base-Erosion Anti-Abuse Tax (BEAT): The 2017 tax reforms moved the U.S. from a worldwide taxation system to a quasi-territorial system, so foreign earnings are no longer included in a company’s domestic tax base.

To discourage companies operating in the U.S. from avoiding tax liability by shifting profits out of the country, Congress imposed a 10% minimum tax called Base-Erosion Anti-Abuse Tax (BEAT). The BEAT rate will increase from 10% to 12.5% in 2026.

Leverage ratios measure the amount of capital that comes from debt. In other words, leverage financial ratios are used to evaluate a company’s debt levels. Common leverage ratios include the following:

The debt ratio measures the relative amount of a company’s assets that are provided from debt:

Debt ratio = Total liabilities / Total assets

The debt to equity ratio calculates the weight of total debt and financial liabilities against shareholders’ equity:

Debt to equity ratio = Total liabilities / Shareholder’s equity

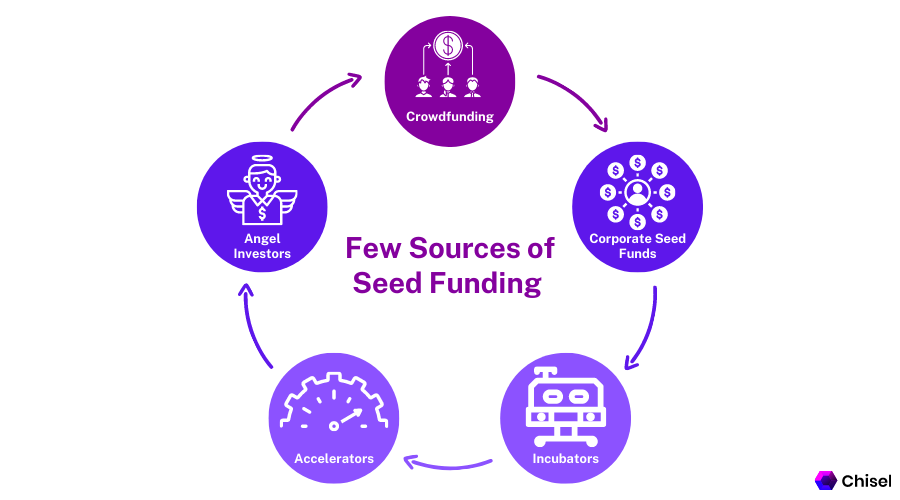

The term seed suggests that this is a very early investment, meant to support the business until it can generate cash of its own, or until it is ready for further investments. Seed money options include friends and family funding, seed venture capital funds, angel funding, and crowdfunding.

Types of Seed funding

Friends and family funding: This type of seed funding involves raising money from friends and family members.

Angel investing: As mentioned above, angel investors are wealthy individuals who provide seed funding in exchange for equity ownership.

Seed accelerators: These are programs that provide startups with seed funding, mentorship, and resources to help them grow their businesses.

Crowdfunding: This type of funding allows startups to raise money from a large number of people, typically through an online platform.

Incubators: These are organizations that provide startups with seed funding, office space, and resources to help them grow their businesses.

Government grants: Some government agencies provide seed funding for startups working on specific projects or in specific industries.

Corporate ventures: Some big companies set up venture arms to provide seed funding to startups in their industry or complementary field.

Micro-Venture Capital: A type of venture capital that provides seed funding to new startups and early-stage companies with a small amount of money.

Posted on March 4, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

Electronic Data Gathering, Analysis, and Retrieval

By Staff Reporters

***

***

EDGAR (Electronic Data Gathering, Analysis, and Retrieval) is an internal database system operated by the U.S. Securities and Exchange Commission (SEC) that performs automated collection, validation, indexing, and accepted forwarding of submissions by companies and others who are required by law to file forms with the SEC. The database contains a wealth of information about the commission and the securities industry which is freely available to the public via the Internet.

In September 2017, SEC Chairman Jay Clayton revealed the database had been hacked and that companies’ data may have been used by criminals for insider trading.

In general, a roadshow is a series of meetings or presentations in which key members of a private company, usually executives, pitch the initial public offering, or IPO, to prospective investors. Effectively, the company is taking its branding message on the road to meet with investors in different cities, hence the name.

The IPO roadshow presentation is an important part of the IPO process in which a company sells new shares to the public for the first time. Whether a company’s IPO succeeds or not can hinge on interest generated among investors before the stock makes its debut on an exchange.

There are also some cases where company executives will embark on a road show to meet with investors to talk about their company, even if they’re not planning an IPO.

Pros and Cons of a Roadshow

According to Rebecca Lake, if the company goes public and no one buys its shares, then the IPO ends up being a flop, which can affect the company’s success in the near and long term. If the company experiences an IPO pop, in which its price goes much higher than its initial offering price, it could be a sign that underwriters mispriced the stock.

A roadshow is also important for helping determine how to price the company’s stock when the IPO launches. If the roadshow ends up being a smashing success, for example, that can cause the underwriters to adjust their expectations for the stock’s IPO price.

On the other hand, if the roadshow doesn’t seem to be generating much buzz around the company at all, that could cause the price to be adjusted downward.

In a worst-case scenario, the company may decide to pull the plug on the IPO altogether or to go a different route, such as a private IPO placement.

Posted on March 2, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Copilot

***

***

The “Magnificent Seven” refers to a group of seven technology giants that have significantly influenced the stock market. These companies are:

Alphabet (GOOGL)

Amazon (AMZN)

Apple (AAPL)

Meta Platforms (META)

Microsoft (MSFT)

Nvidia (NVDA)

Tesla (TSLA)

Why Are They Significant?

These companies are at the forefront of technological innovation, driving advancements in artificial intelligence, cloud computing, e-commerce, social media, and electric vehicles. Their market dominance and financial performance have a substantial impact on major stock indices like the S&P 5002.

Performance

Alphabet: Despite a 31% climb over the past year, Alphabet remains the cheapest of the group, trading at 20 times forward earnings estimates.

Amazon: Amazon’s cloud unit is delivering an annual revenue run rate of $115 billion thanks to its AI offerings.

Apple: Apple has seen a 989% total return for investors over the past decade.

Meta Platforms: Meta is the best-performing stock year-to-date among the Magnificent Seven, up over 25%.

Microsoft: Microsoft has generated a 989% total return for investors over the past decade.

Nvidia: Nvidia remains the best performer over the past year, up 55%.

Tesla: Tesla is the worst-performing stock in the group for 2025, down 25.66% year-to-date.

These companies have reshaped industries and become powerhouses in the global economy, wielding significant influence over market trends and investor sentiment.

While in Omaha for the Berkshire Hathaway annual meeting one year, I participated in an investment panel hosted by a local chapter of the Young Presidents’ Organization. I had the privilege of sharing the stage with such industry giants as Tom Russo, a partner of Gardner Russo & Gardner (famous for knowing more about consumer stocks than the management that runs them), and Tom Gayner, president and CIO of Markel Corp., a specialty insurance company that on many levels resembles the Berkshire of 30 years ago.

We were asked how much time a value investor should spend on macro forecasting. Usually macro forecasting is frowned upon in the value investing community, and Berkshire CEO Warren Buffett has everything to do with that. He is famous for saying (and I am paraphrasing), “My decision making would not change even if I knew what the Federal Reserve will do with interest rates next month.” There is sound logic behind this: Forecasting the economy is incredibly difficult in the short run. The economy is not unlike a black box with hundreds of gauges on it that in the near term give you conflicting readings about what’s inside it.

For this reason macro forecasting was disapproved of by value investors, and for 20 years this attitude paid off. The economic climate was favorable, the stock market was in overdrive, price-earnings ratios were expanding. Macro did not matter — until the housing bubble and financial crisis. Value investors who had had their heads in the sand got annihilated.

Things in life often swing, pendulum-like, from one extreme to another. Right after a crisis every investor is a macro expert. It’s kind of hilarious: Investors who just a few years earlier didn’t even know the names of most economic indicators are now spitting them out in conversations as though they had absorbed them with their mother’s milk. So what should investors do — become macro experts or economic ignoramuses?

Believe it or not, there is a logical and, more important, a practical answer to this question. As an investor you want to spend very little time on forecasting the weather (that is, what the Fed will do with interest rates next month or the rate of growth of the economy). Weather forecasting, first of all, is not always accurate, but it will certainly consume a lot of time and energy, and the forecasts have a very finite shelf life. Yesterday’s weather is irrelevant today. As long as you own companies that can survive rain without catching pneumonia — even a few weeks of rain — weather forecasting is a waste of time. This is what Buffett was implying by saying he didn’t want to be a macro forecaster.

However, instead of being a weatherman (or weatherwoman), as an investor you want to pay serious attention to “climate change” — significant shifts in the global economy that can impact your portfolio. This is exactly what Buffett did over the past few decades — he was warning about the weak dollar because of trade-deficit imbalances (he even put on a trade that bet against the dollar). He also warned about derivatives — “weapons of mass destruction” — and tried to cleanse them from the portfolio of General Re (an insurance company Berkshire acquired) as fast as he could.

Posted on February 24, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

FULL ARTICLE WITH TAKE AWAY POINTS

By Vitaliy Katsenelson CFA

***

***

Key Take Away Points

The Consumer Electronics Show revealed that robotaxis are expanding beyond just Waymo, with multiple players entering the market – this fragmentation could actually benefit Uber’s switchboard system and transform sectors like school transportation.

Chinese EV manufacturers have leapfrogged traditional auto manufacturing much like Africa skipped landlines for mobile phones – their fresh designs and cost advantages could seriously challenge Western incumbents if tariffs weren’t a factor.