BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

More than 20 years ago I crafted a comprehensive holistic financial plan for a young doctor colleague who was born in 1959. In fact, he was not even a medical student at the time; so “canned off-the-shelf plans”, computer generated software or generic spread sheets were not a viable creation option. It was all a granular, detailed, specific and cognitive work-product. Today, he is a board-certified internist.

So, in 2023, it is right and just to take a look back and see how well, or poorly, we’ve fared.

Now, I appreciate more than most how financial planning is a “process”; and not an isolated event. Yet, all sorts of “advisors” and “consultants” create and charge hefty fees for same, and on-going monitoring, every day.

The ME-P Challenge

Nevertheless, I challenge all you mid-career or senior financial planners /advisors to this competition; regardless of degree, certification or designation.

“Show me your financial plan” – AND – “I’ll show you my financial plan”

Here Comes the Judge

Then, our community of ME-P readers, subscribers, visitors and “judges” will decide the winner.

The contest is open to any financial advisor, planner, consultant, wealth manager, CFP®, CFA, insurance agent, CPA or CLU, ChFC, or stock-broker, etc., who is not afraid of transparency in his or her work product and purported expertise.

***[Creating and Evaluating a physician focused financial plan]

***

Assessment

So, just send in a copy of any “blinded” physician-focused financial plan that is about 21 years old. We will post for all to see and review …. warts and all … including my own; three part mega-plan!

The winner will receive bragging rights, academic swagger, and expert promotion to our entire ME-P ecosystem and network of medical, business, law and graduate school communities; as well as physicians, nurses, healthcare executives and allied health care professionals.

An informed sought-after and lucrative sector – indeed!

IOW: Free publicity and positive “new-wave” PR – PRICELESS!

Of course, as an educator and professor of health economics and finance, we are pleased to present you with the deep medical business knowledge and detailed financial,managerial and accounting techniques used, with some real-life “tips and pearls” developed over the last two decades of R&D, right here:

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on November 12, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Angus Deaton’s 1980s studies, including one called “Why is consumption so smooth?” gave birth to a concept called the Deaton Paradox — in short, sharp shocks to income didn’t seem to cause similarly large shocks to consumption.

IOW: Consumption varies surprisingly smoothly despite sharp variations in income.

According to David Henderson, this was an important development in understanding the actions of consumers, causing economists to rethink the “permanent income hypothesis” developed by Milton Friedman, which suggested that people spend based on their lifetime income.

And, Mike Bird wrote a good article on Deaton the highlighted the Nobel Prize in Economics Committee.

A paradox is a logic and self-contradictory statement or a statement that runs contrary to one’s expectation. It is a statement that, despite apparently valid reasoning from true or apparently true premises, leads to a seemingly self-contradictory or a logically unacceptable conclusion. A paradox usually involves contradictory-yet-interrelated elements that exist simultaneously and persist over time. They result in “persistent contradiction between interdependent elements” leading to a lasting “unity of opposites”.

***

And so, as we plan for our financial future thru a New Year Resolution for 2025, it’s helpful to be cognizant of these paradoxes. While there’s nothing we can do to control or change them, there is great value in being aware of them, so we can approach them with the right tools and the right mindset.

According to Adam Grossman, here are seven [7] of the paradoxes that can bedevil financial decision-making, clients and financial advisors, alike:

There’s the paradox that all of the greatest fortunes—Carnegie, Rockefeller, Buffett, Gates—have been made by owning just one stock. And yet the best advice for individual investors is to do the opposite: to own broadly diversified index funds. More:https://tinyurl.com/285vftx4

There’s the paradox that the stock market may appear over valued and yet it could become even more overvalued before it eventually declines. And when it does decline, it may be to a level that is even higher than where it is today.

There’s the paradox that we make plans based on our understanding of the rules—and yet Congress can change the rules on us at any time, as the recent 2024 election results attest.

There’s the paradox that we base our plans on historical averages—average stock market returns, average interest rates, average inflation rates and so on—and yet we only lead one life, so none of us will experience the average.

There’s the paradox that we continue to be attracted to the prestige of high-cost colleges, even though rational analysis that looks at return on investment tells us that lower-cost state schools are usually the better bet.

There’s the paradox that early retirement seems so appealing—and has even turned into a movement—and yet the reality of early retirement suggests that we might be better off staying at our desks.

There’s the paradox that retirees’ worst fear is outliving their money and yet few choose the financial product that is purpose-built to solve that problem: the single-premium immediate annuity.

Gibson’s paradox is based on an economic observation made by British economist Alfred Herbert Gibson regarding the positive correlation between interest rates and wholesale price levels. John Maynard Keynes later called this relationship a paradox because he claimed that it could not be explained by existing economic theories.

There have been possible explanations raised by economists to solve Gibson’s paradox over the decades. But as long as the relationship between interest rates and prices remains artificially de-linked, there may not be enough interest by today’s macro-economists to pursue it any further.

In the end, Gibson’s paradox was neither Gibson’s (having been previously discovered by others) nor a true paradox (as plausible explanations already existed at the time of Keynes’s writing and more have been explored since) and is of little interest beyond being a historical footnote to the gold standard era.

These are considered to be large developing economies that are part of a global, twenty-first century shift in economic power and influence away from the more established, traditional developed economies of the twentieth century.

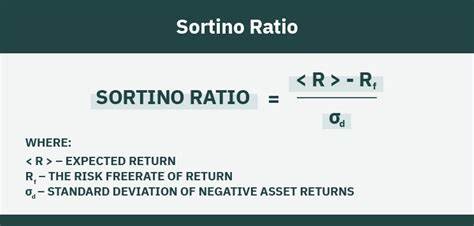

The Sortino Ratio is similar to the Sharpe Ratio, it is a measure of risk-adjusted performance which looks at returns through the lens of the risk taken to achieve that performance, but instead of volatility of return, it uses downside variance as its measure of risk.

A company that invests in real estate and whose shares trade on a public exchange.

Real Estate Investment Trust (REIT)

A real estate operating company (REOC) is similar to a real estate investment trust (REIT), except that an REOC will reinvest its earnings into the business, rather than distributing them to unit holders like REITs do.

Also, REOCs are more flexible than REITs in terms of what types of real estate investments they can make.

According to Wikipedia, a fundamental tenet of the paradox is that the customer, i.e. the potential purchaser of the information describing a technology (or other information having some value, such as facts), wants to know the technology and what it does in sufficient detail as to understand its capabilities or have information about the facts or products to decide whether or not to buy it. Once the customer has this detailed knowledge, however, the seller has in effect transferred the technology to the customer without any compensation. This has been argued to show the need for patent protection [HIPPA].

If the buyer trusts the seller or is protected via contract, then they only need to know the results that the technology will provide, along with any caveats for its usage in a given context. A problem is that sellers lie, they may be mistaken, one or both sides overlook side consequences for usage in a given context, or some unknown-unknown affects the actual outcome.

Posted on November 8, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Artificial Scarcity refers to the intentional limitation of the availability of a product or resource to create a sense of rarity, which often drives up its perceived value and price.

Think: surge pricing

And, circumstances with insufficient competition can lead to suppliers exercising enough market power to constrict supply. The clearest example is a monopoly, where a single producer has complete control over supply and can extract a additional price.

By creating a temporary shortage, sellers or producers can increase demand and capitalize on consumers’ fear of missing out, thereby influencing market dynamics to their advantage. This strategy is frequently used in marketing, particularly for limited-edition items or high-demand products.

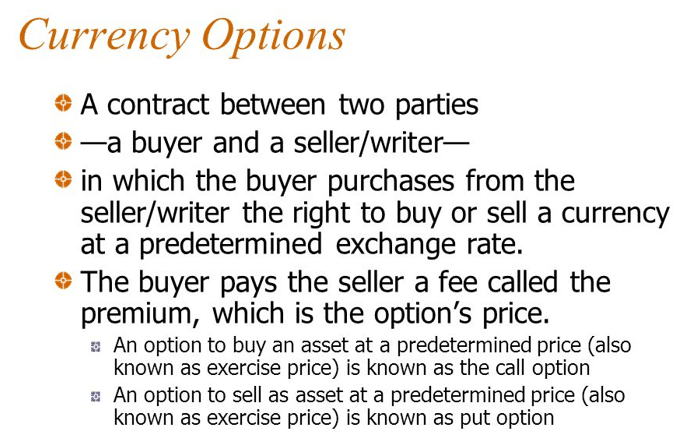

Currency Hedging is a risk-management strategy, as part of a foreign investment strategy, currency hedging is designed to reduce the impact from changes in the relative values of currencies involved in the foreign investment strategy.

In any foreign investment strategy, a significant part of the potential risk and return comes from exposure to relative currency value fluctuations. If exposure to those currency fluctuations is minimized, investors can experience more of a “pure play” exposure to the foreign investments. There is a variety of possible currency hedging strategies, ranging from swaps, options, and spot contracts to simply buying foreign currencies.

Currency Overlay is a financial trading strategy used to separate the management of currency risk from other portfolio strategies. A currency overlay manager can seek to hedge the risk from adverse movements in exchange rates, and/or attempt to profit from tactical currency views.

Posted on November 8, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The Federal Reserve cut interest rates by 0.25 percentage points Thursday, the second consecutive cut after a two-year rate-hike run to curb post-pandemic inflation.

Lyft announced impressive earnings results thanks to more commuters using the ride-hailing service, as well as upbeat guidance for the future. Shares rose 22.92%.

Shareholders worried about a housing market slowdown hurting Zillow had nothing to fear: The real estate website crushed earnings estimates, and shares popped 23.77%.

Warner Bros. Discovery enjoyed its biggest single-quarter surge in subscribers ever thanks to streaming service Max, which sent shares soaring 11.81%.

UnderArmour rocketed 23.33% higher after its cost-savings plan paid off last quarter and management guided for a strong quarter ahead.

Planet Fitness surprised shareholders with a solid quarter for the gym giant, as well as forecasts of more growth ahead. Shares climbed 11.26%.

Prison operators GEOGroup and CoreCivic both surged on Trump’s election, and their rally continued today—in-spite of very different paths forward for each stock. GEO Group gained 13.63%, while CoreCivic rose 25.60%.

What’s down

Trump Media & Technology Group was one of the biggest winners on election night, and although the stock soared over the last few days, investors decided to take profits today. Shares sank 22.97%.

Wolfspeed plummeted 39.24% after announcing larger-than-expected losses last quarter, poor forecasts for next quarter, and layoffs to cut costs.

Match Group shareholders were heartbroken to hear that Tinder’s revenue fell last quarter, though strong revenue growth from Hinge helped ease the pain. Shares dropped 17.87%.

Virgin Galactic isn’t just a mean nickname from your high school years—it’s also a space stock that can’t make money to save its life. Shares fell 11.87%.

The S&P 500®index (SPX) rose 44.06 points (0.74%) to 5,973.10; the Dow Jones Industrial Average® ($DJI) fell 0.59 points (0.00%) to 43,729.34; and the NASDAQ Composite®($COMP) gained 285.99 points (1.51%) to 19,269.46.

The 10-year Treasury note yield (TNX) fell nine basis points to 4.34%, with most of the drop coming long before the Fed decision.

The CBOE Volatility Index® (VIX) continued its post-election plunge to 15.21.

Stocks surged and stayed higher all yesterday day on news of Donald Trump’s presidential victory. The Dow rocketed over 1,350 points as soon as markets opened, and all three indexes ended the day at record highs.

Treasuryyields have paralleled Trump’s chances of taking the White House for the last few weeks, and his election sent them soaring to over 4.46% at one point today.

Oil and gold both fell as the dollar rose after Trump’s win. The greenback popped on the promise of Trump’s protectionist tariff policies and the lower likelihood of the Fed cutting interest rates as fast as previously expected.

Bitcoin surged as traders celebrated the beginning of the new, friendlier regulatory environment that Trump promised during his campaign.

Posted on November 7, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The cocktail party effect is the ability of the human hearing and auditory system to focus one’s listening attention on a particular speaker in a noisy environment, such as a crowded party. This allows people to focus on a specific conversation while filtering out other nearby conversations and background noise.

Consider that you’re at a crowded party, noise everywhere, but you hear your name mentioned across the room. How? Welcome to the Cocktail Party Effect.

Your brain is like a highly trained butler, filtering out the background chatter to catch something personally relevant. It’s not just your name, either; it could be juicy gossip or a mention of free pizza or an exciting new stock tip you’ve been considering; or even an IPO.

So, according to psychologist colleague Dan Ariely PhD, this selective attention keeps us sane in a noisy world, helping us focus on the things that matter – like whether that person just said “free drinks” or “freeloading, or “free-stock trading.”

Posted on November 7, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

One more group of stocks that soared on a Trump election: Big Tech companies with antitrust problems. Another Trump presidency should go a long way toward clearing up the regulatory hurdles many companies have faced recently, which is why Alphabet popped 3.99% and Amazon rose 3.8%.

CVS Health surged 11.33% after meeting revenue forecasts but missing earnings expectations. However, the miss was due to a one-time charge, so shareholders quickly forgave the healthcare retailer.

Planet Fitness gained 6.09% on a surprise bid for bankrupt fitness chain Blink Holdings in an attempt to bolster its own gym business.

Stocks Down

Super Micro Computer had a chance to show the world it wasn’t committing the fraud it has recently been accused of. Instead, the company announced it is still unable to determine when it will file the quarterly report due August 29. Shares crashed 18.05%.

Home builder stocks sank on fears that a Trump presidency will slow the rate of Fed rate cuts, keeping mortgage rates higher for longer. DR Horton fell 3.8%, Lennar dropped 4.84%, PulteGroup lost 3.09%, and TollBrothers tumbled 1.46%.

Cannabis stocks were betting big on a ballot measure in Florida to allow the sale of recreational marijuana. The initiative’s failure sent shares of Curaleaf plummeting 29.17%, TrulieveCannabis plunged 38.8%, and AyrWellness sank 55.87%.

The S&P 500®index (SPX) rose 146.28 points (2.53%) to 5,929.04; the Dow Jones Industrial Average® ($DJI) added 1,508.05 points (3.57%) to 43,729.93; and the NASDAQ Composite®($COMP) gained 544.29 points (2.95%) to 18,983.47—a new closing high.

The 10-year Treasury note yield (TNX) surged 14 basis points to 4.43%, its highest level since July.

The CBOE Volatility Index® (VIX) fell sharply to 16.3 as election-related uncertainty diminished.

Stocks just roared out of the gate this Wednesday morning following news that former President Donald Trump has secured a second term in the White House and Republicans won a majority in the Senate.

The Dow Jones Industrial Average rose 1,341 points, or about 3.1 percent, as the market opened, reaching a record high. It was the first time it has jumped more than 1,000 points in a single day since November 2022.

The S&P 500 also gained 1.9 percent, and the NASDAQ climbed 1.8 percent.

Despite concern from big business about Trump’s plan to impose blanket tariffs on imports to the U.S., Wall Street is anticipating tax cuts and deregulation during a second Trump presidency.

Retained Earnings Risk: Profits generated by a company that are not distributed to stockholders as dividends. Instead, they are either reinvested in the business or kept as a reserve for specific objectives, such as paying off debt or purchasing equipment. Retained earnings risks are also called “undistributed profits,” “undistributed earnings,” or “earned surplus.”

Risk-Weighted (or risk-adjusted) Assets: Within the context of measuring the financial stability of banks and other financial institutions, the risk-weighted assets figure is an aggregate of a financial institution’s assets (usually loans to its customers) after the loans have been individually adjusted for their risk. This involves multiplying each loan by a factor that reflects its risk. Low-risk loans are multiplied by a low number, high-risk by high. The aggregate number can then be used to calculate the financial institution’s capital ratio. Lower risk-weighted assets typically result in higher capital ratios, and higher risk-weighted assets usually translate to lower capital ratios.

Sequence-of-Returns Risk: The risk of market conditions impacting the overall returns of an investment portfolio during the period when a retiree is first starting to withdrawal money from investments as income. For example, if a retiree has to withdrawal income from his or her portfolio when market prices are depressed, the portfolio may lose out on the potential returns that income could have made once market prices recovered.

Posted on November 6, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

First-time homebuyers in 2024 had a median income of $97,000, and their median age was 38. OpenAI and Jeff Bezos invested in Physical Intelligence, a robot startup with the aim of “bringing general-purpose AI into the physical world.”

Cybersecurity darling Palantir soared 23.38% to a record high thanks to strong earnings, high AI demand, and big spending from the Department of Defense.

Astera Labs skyrocketed 37.70% after the semiconductor parts maker (and one of Nvidia’s key suppliers) announced strong earnings.

Crypto stocks had a great day thanks to a widespread cryptocurrency rally. Coinbase rose 4.13%, MicroStrategy gained 2.16%, and RiotPlatforms jumped 8.13%.

Stocks Down

Trump Media & Technology Grouparrested its recent downturn and popped 12% at one point today, but gave all those gains up and ended the day down 1.16%.

You’d think the end of a multi-week labor dispute costing billions of dollars would be a relief for shareholders, but Boeing still sank 2.62% on news that it’s reached an agreement with striking machinists.

It’s a me, lower revenue forecasts! Nintendo fell 1.68% after announcing that sales of its Switch console are starting to sag.

Some of the smaller semiconductor stocks on the market took a beating today. NXP Semiconductor dropped 5.17% after announcing weaker-than-expected Q4 guidance, Lattice Semiconductor tumbled 1.37% after missing on sales forecasts and announcing job cuts, and while Cirrus Logic beat expectations this quarter, it still fell 7.09% on lower forecasts.

The S&P 500®index (SPX) rose 70.07 points (1.23%) to 5,782.76; the Dow Jones Industrial Average® ($DJI) added 427.28 points (1.02%) to 42,221.88; and the NASDAQ Composite®($COMP) increased 259.19 points (1.43%) to 18,439.17.

The 10-year Treasury note yield (TNX) dropped two basis points to 4.29%.

The CBOE Volatility Index® (VIX) slipped to 20.72.

In what some are calling the next iteration of the internet, the metaverse is an unfamiliar digital world where you could be an avatar navigating computer-generated places and interacting with others in real time. In this space, the constraints of our physical, bricks and mortar world and travel habits fade. And new opportunities and challenges emerge.

Google in healthcare: The search giant has repeatedly successfully transferred its in-depth knowledge of algorithms in the field of medicine, particularly since it acquired DeepMind.

Apple in healthcare: Apple will keep on working on expanding the health features of its devices, Apple Watch and iPhones included.

Microsoft in healthcare: Microsoft’s cloud solutions provide integrated capabilities that make it easier to improve the healthcare experience.

Amazon in healthcare: Amazon will make further use of its vast knowledge of online shopping trends and behavior and will keep on providing what people need, from medicine to wearables.

IBM in healthcare: IBM has a lot to offer in federated learning, blockchain, and quantum computing.

Nvidia in healthcare: NVIDIA seems incredibly focused on its approach to healthcare. We can expect NVIDIA to be a leader in the use of artificial intelligence in healthcare.

Facebook in healthcare: The Metaverse developed by Facebook/Meta has incredible potential to revolutionize healthcare.

All this technology has huge potential because it uses both virtual reality (VR) and augmented reality (AR) technology to work in virtual spaces: All signs point to the metaverse being widely used as a disruptive change in healthcare, from better surgical precision to therapeutic uses to social-distance accommodations and more.

But along with these improvements come new problems that will change what we know about modern healthcare. The metaverse is a paradigm shift in healthcare that everyone involved needs to be aware of. This is because it changes how medical infrastructure is built, how startup costs are covered, and how data security and privacy are handled.

Posted on November 5, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

After its AI-related earnings disappointed Wall Street last quarter, Big Tech doubled down in the latest period:

Amazon spent $22.6 billion on property and equipment like data centers and chips. That’s an 81% spike from the same time last year.

Meta raised its low-end guidance for capex (capital expenditures), which could reach $40 billion by the end of the year. It beat earnings estimates, even with AR glasses subsidiary Reality Labs costing $4.4 billion in operating losses.

Apple is still betting on Apple Intelligence to boost sales. Most revenue came from the new iPhone 16, Apple Watch, and AirPods, but Apple services like TV+ and iCloud also grew massively to account for a quarter of the business.

Google crushed earnings estimates and revealed that more than 25% of all new code it writes is generated by AI (and reviewed by engineers).

Posted on November 5, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Among consideration for CVS is splitting up its assets: CVS Pharmacy, pharmacy benefit managerCVS Caremark, and insurance arm Aetna. The company has reportedly been in talks with bankers about the move, Reuters reported early this month.

Just as Nvidia will replace Intel, Sherwin Williamswill replaceDow Inc. on the Dow (how embarrassing, getting kicked off an index you share a name with). Sherwin Williams popped 4.59%, while Dow Inc. fell 2.08%.

Peloton pedaled 3.59% higher on a double upgrade from Bank of America analysts, who like the bike company’s higher profit outlook and hiring of new CEO Peter Stern from Ford.

Yum! China, the company that operates Pizza Hut and KFC restaurants in China, climbed 7.12% after announcing that new store openings translated into better-than-expected revenue and earnings last quarter.

STOCKS DOWN

Nuclear energy stocks took a big hit today after the Federal Energy Regulatory Commission ruled that Talen Energycould not increase the amount of energy its nuclear plant in Susquehanna, PA, produces in order to power an Amazon data center. Talen fell 2.23%, Vistra Corp sank 3.18%, and Constellation Energy plummeted 12.46%.

Clinical data from a Viking Therapeutics trial shows its weight-loss pill is effective. Shares soared then sank 13.36% as investors took profits.

The S&P 500®index (SPX) dipped 16.11 points (–0.28%) to 5,712.69; the $DJI dropped 257.59 points (–0.61%) to 41,794.60; and the $COMP lost 59.93 points (–0.33%) to 18,179.98.

The 10-year Treasury note yield (TNX) fell five basis points to 4.31%.

The CBOE Volatility Index® (VIX)edged up to 22.11, still below last week’s peaks.

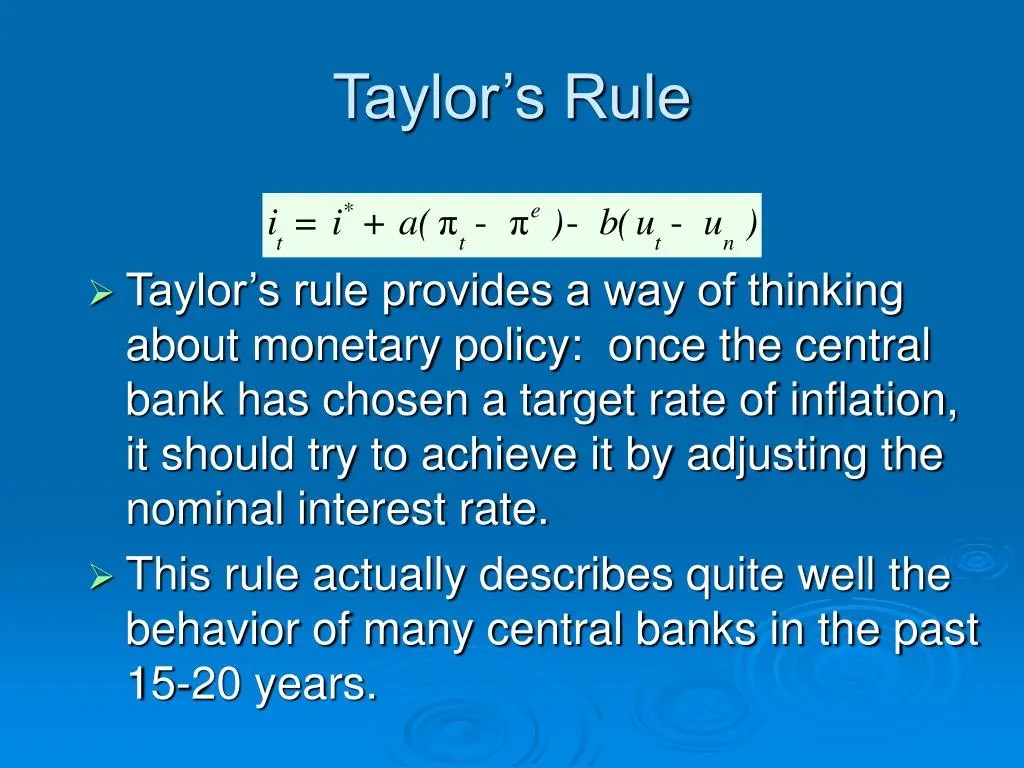

Named for a U.S. economist, the JB Taylor Rule is a mathematical monetary-policy formula that recommends how much a central bank should change its nominal short-term interest rate target (such as the U.S. Federal Reserve’s federal funds rate target) in response to changes in economic conditions, particularly inflation and economic growth. It’s typically viewed as guideline for raising short-term interest rates as inflation and potentially inflationary pressures increase. The rule recommends a relatively high interest rate (“tight” monetary policy) when inflation is above its target or when the economy is above its full employment level, and a relatively low interest rate (“easy” monetary policy) under the opposite conditions.

To illustrate, the monetary policy of the FOMC, changed throughout the 20th century. The period between the 1960s and the 1970s is evaluated by Taylor and others as a period of poor monetary policy; the later years typically characterized as stagflation. The inflation rate was high and increasing, while interest rates were kept low. Since the mid-1970s monetary targets have been used in many countries as a means to target inflation.

However, in the 2000s the actual interest rate in advanced economics, notably in the US, was kept below the value suggested by the Taylor rule.

Posted on November 4, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Nvidia is replacing Intel on the Dow Jones Industrial Average, a shakeup to the blue-chip index that replaces a flagging semiconductor company with the primary vendor of GPUs for AI.

Bipartisan Legislation Aims to Stop Medicare Cuts & Boost Physician Pay in 2025

Physicians and other healthcare practitioners may get a pay boost in 2025 through a bipartisan bill recently introduced in Congress. The proposed bill seeks to block planned Medicare pay cuts next year and would provide the first inflationary update to physician pay in years. The Medicare Patient Access and Practice Stabilization Act would counteract the 2.8% cut to the conversion factor proposed by the Centers for Medicare and Medicaid Services (CMS) in the draft CY-2025 Physician Fee Schedule. A stop-gap pay fix is usually enacted by Congress at the end of the year.

Source: Emma Beavins, Fierce Healthcare [10/30/24].

HFRI: Fund of Funds invests with multiple managers through funds or managed accounts. The strategy designs a diversified portfolio of managers with the objective of significantly lowering the risk (volatility) of investing with an individual manager.

The Fund of Funds manager may allocate funds to numerous managers within a single strategy, or with numerous managers in multiple strategies. The investor has the advantage of diversification among managers and styles with significantly less capital than investing with separate managers.

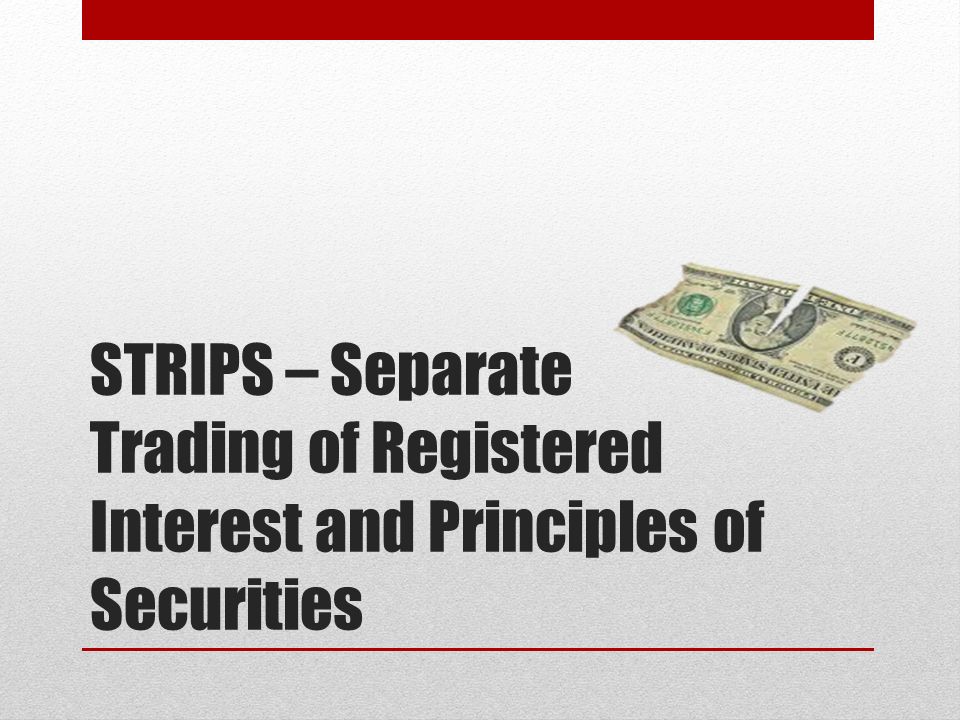

STRIPS (Separate Trading of Registered Interest and Principal of Securities) is an acronym that describes both a government bond issuance program and the securities issued by the program. STRIPS are a form of zero-coupon security (defined below) created under the U.S. Treasury’s STRIPS program.

Originally, zero-coupon securities were created by broker-dealers who bought Treasury bonds and deposited these securities with a custodian bank. The broker-dealers then sold receipts representing ownership interests in the coupons or principal portions of the bonds.

Some examples of zero-coupon securities sold through custodial receipt programs are CATS (Certificates of Accrual on Treasury Securities), TIGRs (Treasury Investment Growth Receipts) and generic TRs (Treasury Receipts). The U.S. Treasury subsequently introduced a program called Separate Trading of Registered Interest and Principal of Securities (STRIPS), through which it exchanges eligible securities for their component parts and then allows the component parts to trade in book-entry form.

STRIPS are direct obligations of the U.S. government and have the same credit risks as other U.S. Treasury securities. STRIPS are generally considered the most liquid (easily bought and sold) zero-coupon securities.

Posted on November 2, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Ford paused production of its F-150 Lightning electric truck from mid-November to early January as demand for the once-coveted EV dwindles.

Peloton named Peter Stern, the co-founder of Apple Fitness+, as its next CEO.

Starbucksis bringing back Sharpied names on cups for the first time in four years as new CEO Brian Niccol tries to shake up the struggling coffee chain.

Boeing offered striking machinists yet another new contract offer, including a 38% pay raise over the next four years. The union will vote on the contract on Monday. Shares climbed 3.54%.

Avis Budget motored 10.92% higher despite missing forecasts on both earnings and revenue. Shareholders celebrated the rental car company’s strong growth expectations from management and took advantage of a cheap valuation.

Globalstar rocketed 32.38% after the satellite communications company announced an expanded deal with Apple.

Charter Communications soared 11.87% after losing fewer subscribers than expected, which is like a back-handed compliment in the investing world.

STOCKS DOWN

Trump Media & Technology Group remains on the roller coaster, falling another 13.53% today as early exit polls show Vice President Kamala Harris with a lead in several key states.

Wayfair may have met earnings expectations last quarter, but the online home goods retailer also lost customers and fulfilled fewer orders. Shares fell 6.26%.

Super Micro Computer continued to sell off after the resignation of its financial auditor, an almost-sure sign of fraud. Shares sank another 10.51%.

The S&P 500®index (SPX) rose 23.35 (0.41%) to 5,728.80 to end the week down 1.37%; the Dow Jones Industrial Average® ($DJI) added 288.73 points (0.69%) to 42,052.19 to end the week down 0.15%; and the NASDAQ Composite®($COMP) gained 144.76 points (0.80%) to 18,239.92 to end the week down 1.50%.

The 10-year Treasury note yield (TNX) climbed eight points to 4.36%, the highest since early July.

The CBOE Volatility Index® (VIX)remained elevated at 21.88.

Classic Definition: Employers write checks that cover most health insurance premiums for employees and their dependents. But as the late Princeton health economist Uwe Reinhardt PhD once explained, employer-sponsored insurance is like a pickpocket taking money out of your wallet at a bar and buying you a drink. You appreciate the cocktail until you realize you paid for it yourself.

Modern Circumstance: With health coverage, employers write the check to the insurer, but employees bear the cost of the premium — the entire premium, not just the portion listed as their contribution on their pay stub. The premium money that goes to the insurance company is cash that employers would otherwise deposit in employees’ accounts like the rest of their salary.

Paradox Example: The fallacy paradox is in thinking an employer’s contribution comes out of profits. In fact, higher health insurance premiums mean lower wages for workers. Since 1999, health insurance premiums have increased 147 percent and employer profits have increased 148 percent. But in that time, average wages have hardly moved, increasing just 7 percent. Clearly workers’ wages, not corporate profits, have been paying for higher health insurance premiums. Health care costs are one — though not the only — reason wages have stagnated over the last few decades. With health insurance costs rising faster than growth in the economy, more labor costs go to benefits like health insurance and less to take-home pay. Yet the paradox that employees don’t pay for their own health insurance is widespread:

The first reason is that individuals cannot be sure what causes their wages to change or remain stagnant for decades.

The second reason is that employers want Americans to believe that they pay for their workers’ health insurance.

The third reason is that there are those who profit from the employment-based system: drug companies, device manufacturers, specialty physicians and high-income individuals.

And so, they all want you to believe companies are being magnanimous in giving you insurance, but they are not!

Posted on November 1, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Comcast popped 3.39% on the news that it is exploring a separation of its cable business. The network operator got a boost this quarter from the Olympics, but still lost 365,000 cable TV customers.

Peloton Interactive pedaled 27.82% higher after the bike maker beat earnings expectations and introduced a new CEO.

Carvana accelerated 19.23% on an impressive beat-and-raise earnings report that caps off the car seller’s incredible comeback.

Booking Holdings, owner of Kayak and Priceline, hit a record high after the travel company reported shockingly strong earnings. Shares rose 4.76%

What was down

Trading in shares of Trump Media & Technology Group was halted yet again today after the meme stock sank dramatically to start the day. Shares ended the trading session down 11.72%.

Estee Lauder plummeted 20.84% on a triple whammy of bad news: The cosmetics retailer missed earnings estimates, pulled its forecast, AND cut its dividend. Ouch.

Super Micro Computer continued to tumble today, declining another 11.97% as the fallout from the resignation of its financial auditor raises the threat of the semiconductor stock getting delisted from the Nasdaq.

eBay sank 8.18% after beating earnings expectations but issuing disappointing earnings guidance heading into the holiday season.

The SPX fell 108.22 (–1.86%) to 5,705.45; the Dow Jones Industrial Average® ($DJI) dropped 378.08 points (–0.90%) to 41,763.46; and the NASDAQ Composite®($COMP) lost 512.78 points (–2.76%) to 18,095.15 and has now fallen in two of the last four months.

The 10-year Treasury note yield (TNX) added two basis points to 4.28%.

The VIX rose to 22.6, the highest since October 8.

What Is CREDIT? Credit is a contractual agreement in which a borrower receives a sum of money or something else of value and commits to repaying the lender later, typically with interest. Credit is also the creditworthiness or credit history of an individual or a company. Good credit tells lenders you have a history of reliably repaying what you owe on loans. Establishing good credit is essential to getting a loan.

***

Credit Analysis is a form of financial analysis used primarily to determine the financial strength of the issuer of a security, and the ability of that issuer to provide timely payment of interest and principal to investors in the issuer’s debt securities. Credit analysis is typically an important component of security analysis and selection in credit-sensitive bond sectors such as the corporate bond market and the municipal bond market.

Credit Default Swap Index (CDX) is a credit derivative, based on a basket of CDS, which can be used to hedge credit risk or speculate on changes in credit quality.

Credit Default Swaps (CDS) are credit derivative contracts between two counter parties that can be used to hedge credit risk or speculate on changes in the credit quality of a corporation or government entity.

Credit Quality reflects the financial strength of the issuer of a security, and the ability of that issuer to provide timely payment of interest and principal to investors in the issuer’s securities. Common measurements of credit quality include the credit ratings provided by credit rating agencies such as Standard & Poor’s and Moody’s. Credit quality and credit quality perceptions are a key component of the daily market pricing of fixed-income securities, along with maturity, inflation expectations and interest rate levels.

Credit Rating Agency (CRA) is a company that assigns credit ratings for issuers of certain types of debt obligations as well as the debt instruments themselves. In the United States, the Securities and Exchange Commission (SEC) permits investment banks and broker-dealers to use credit ratings from “Nationally Recognized Statistical Rating Organizations” (NRSRO) for similar purposes. As of January 2012, nine organizations were designated as NRSROs, including the “Big Three” which are Standard and Poor’s, Moody’s Investor Services and Fitch Ratings.

A Credit Rating Downgrade by a credit rating agency (such as Standard & Poor’s, Moody’s or Fitch), of reducing its credit rating for a debt issuer and/or security. This is based on the agency’s evaluation, indicating, to the agency, a decline in the issuer’s financial stability, increasing the possibility of default (defined below). A downgrade should not to be confused with a default; a debt security can be downgraded without defaulting. (And, conversely, a debt issuer can suddenly default without being downgraded first–credit ratings and credit rating agencies are not infallible.)

Credit Ratings are measurements of credit quality provided by credit rating agencies). Those provided by Standard & Poor’s typically are the most widely quoted and distributed, and range from AAA (highest quality; perceived as least likely to default) down to D (in default). Securities and issuers rated AAA to BBB are considered/perceived to be “investment-grade”; those below BBB are considered/perceived to be non-investment-grade or more speculative.

Credit Risk is the risk that the inability or perceived inability of the issuers of debt securities to make interest and principal payments will cause the value of those securities to decrease. Changes in the credit ratings of debt securities could have a similar effect.

Credit Risk Transfer Securities (CRTS) are the unsecured obligations of the GSEs (Government Sponsored Enterprises). Although cash flows are linked to prepays and defaults of the reference mortgage loans, the securities are unsecured loans, backed by general credit rather than by specified assets.

Investors waited for the Magnificent 7 stock reports to begin rolling last evening. The NASDAQ rose to a new high on optimism while the Dow Jones fell, and the S&P 500 split the difference.

Alphabet announced earnings after the bell yesterday, Microsoft and MetaPlatforms reveal their latest quarters today, Amazon and Apple on Thursday afternoon.

The 10-year Treasury yield hit a 4-month high this afternoon before paring back a bit as traders struggle to find a signal in all the market noise.

Oil rebounded a bit from yesterday’s terrible day, though it still ended the trading session lower.

Ever tried making a decision when you’re angry or excited? According to colleague Dan Ariely PhD, that’s a hot state – when emotions run high and logic takes a backseat. It’s like trying to think clearly in the middle of a storm.

Be you a doctor, CPA, attorney, engineer, husband, wife, parent, teacher or all others. In a hot state, we’re impulsive, making choices we might regret later. It’s why cooling off before making big decisions is always a good idea.

So, when your emotions are boiling over, take a step back, breathe, and wait for the storm to pass. You’ll make better choices when you’re in a calm, cool state.

It is a multi-factor model measures the overall risk associated with a security relative to the market. And, it incorporates over 40 data metrics, including earnings growth, share turnover and senior debt rating.

The five most valuable US companies in the S&P 500 report earnings this week, and updates on three key economic indicators are set to be released: 1. gross domestic product, 2. inflation, and 3. jobs report. Then, next week brings the election and another expected rate cut from the Federal Reserve.

Markets:All three stock indexes rose to start a week that will be filled with high-stakes data.

Stock spotlight: Trump Media & Technology Group gained almost 22% on Monday, following the former president and current GOP candidate’s Madison Square Garden rally. The rose means that Trump Media, which includes Truth Social, is now more valuable than Elon Musk’s X.

Russell 1000® Growth Index: Measures the performance of those Russell 1000 Index companies (the 1,000 largest publicly traded U.S. companies, based on total market capitalization) with higher price-to-book ratios and higher forecasted growth values.

Russell 1000® Index: A market-capitalization weighted, large-cap index created by Frank Russell Company to measure the performance of the 1,000 largest publicly traded U.S. companies, based on total market capitalization.

Russell 1000® Value Index: Measures the performance of those Russell 1000 Index companies (the 1,000 largest publicly traded U.S. companies, based on total market capitalization) with lower price-to-book ratios and lower forecasted growth values.

Russell 2000® Growth Index: Measures the performance of those Russell 2000 Index companies (the 2,000 smallest of the 3,000 largest publicly traded U.S. companies, based on total market capitalization) with higher price-to-book ratios and higher forecasted growth values.

Russell 2000® Index: Market-capitalization weighted index created by Frank Russell Company to measure the performance of the 2,000 smallest of the 3,000 largest publicly traded U.S. companies, based on total market capitalization.

Russell 2000® Value Index: Measures the performance of those Russell 2000 Index companies (the 2,000 smallest of the 3,000 largest publicly traded U.S. companies, based on total market capitalization) with lower price-to-book ratios and lower forecasted growth values.

Russell 2500™ Growth Index: Measures the performance of those Russell 2500 Index companies (the 2,500 smallest of the 3,000 largest publicly traded U.S. companies, based on total market capitalization) with higher price-to-book ratios and higher forecasted growth values.

Russell 2500™ Index: A market-capitalization weighted index created by Frank Russell Company to measure the performance of the 2,500 smallest of the 3,000 largest publicly traded U.S. companies, based on total market capitalization.

Russell 2500™ Value Index: Measures the performance of those Russell 2500 Index companies (the 2,500 smallest of the 3,000 largest publicly traded U.S. companies, based on total market capitalization) with lower price-to-book ratios and lower forecasted growth values.

Russell 3000® Growth Index: Measures the performance of the broad growth segment of the U.S. equity universe. It includes those Russell 3000 companies with higher price-to-book ratios and higher forecasted growth values.

Russell 3000® Index: Measures the performance of the largest 3,000 U.S. companies representing approximately 98% of the investable U.S. equity market.

Russell 3000® Utilities Index: A sub-index of the Russell 3000 Index, is a capitalization weighted index of companies in industries heavily affected by government regulation, including among others, basic public service providers (electricity, gas and water), telecommunication services, and oil and gas companies.

Russell 3000® Value Index: Measures the performance of the broad value segment of the U.S. equity universe. It includes those Russell 3000 companies with lower price-to-book ratios and lower forecasted growth values.

Russell Midcap® Growth Index: Measures the performance of those Russell Midcap Index companies (the 800 smallest of the 1,000 largest publicly traded U.S. companies, based on total market capitalization) with higher price-to-book ratios and higher forecasted growth values.

Russell Midcap® Index: Measures the performance of the 800 smallest of the 1,000 largest publicly traded U.S. companies, based on total market capitalization.

Russell Midcap® Value Index: Measures the performance of those Russell Midcap Index companies (the 800 smallest of the 1,000 largest publicly traded U.S. companies, based on total market capitalization) with lower price-to-book ratios and lower forecasted growth values.

Russell Top 200® Index: Measures the performance of the 200 largest securities of the 3,000 publicly traded U.S. companies in the Russell 3000® Index, based on total market capitalization. It is not an investment product available for purchase.

Posted on October 28, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Peak earnings season: Five of the Magnificent SevenStocks will be among the 181 companies reporting their earnings this week. Alphabet is in the Mag Seven lead-off spot on Tuesday, Microsoft and Meta step to the plate on Wednesday, and Apple and Amazon rounding out the lineup and this baseball metaphor on Thursday. These companies account for almost 25% of the S&P 500, which is up 40% over the past year and not far off its record closing number from earlier this month. But, the approaching election, it could be a volatile week in the stock markets.

***

Markets: Stocks are currently driving the narrative on Wall Street. Last week, bonds sold off in a big way (driving yields to their highest level since July) in a sign investors are dialing back expectations of more aggressive rate cuts from the Federal Reserve.

Stocks nevertheless handled the bond volatility with aplomb, and with help from Tesla’s 22% one-day rise, the NASDAQ is sitting within 2% of its record high.

Posted on October 28, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

401(k) vs. pension: There’s pros and cons to both. While pension plans guarantee a steady income stream, payments sometimes aren’t indexed by inflation, which can erode their value over time. On the flip side, 401(k)s are subject to market fluctuations and require financial literacy.

It’s good to have money stashed in the stock market when the market is doing well. The number of people with at least $1 million in their 401(k) and IRA accounts jumped 12% in the second quarter 2024, according to a report from Fidelity Investments, largely tracking the market’s gain during that period. It’s the third straight quarter of growth in $1+ million accounts and close to a record high.

But start saving now, because building a hard-boiled nest egg through retirement accounts takes time: The average age of a 401(k) millionaire is 59, Fidelity said.

Posted on October 27, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Vitaliy Katenselson CFA

***

***

Today, we’re diving into two thought-provoking questions:

1. What’s a famous investment rule I don’t agree with? 2. Which key characteristics should a good investor have?

1. A Famous Investment Rule I Don’t Agree With: “Buy and Hold”

Buy and hold becomes a religion during bull markets. Then, holding a stock because you bought it is often rewarded through higher and higher valuations. There’s a Pavlovian bull market reinforcement – every time you don’t sell (hold) a stock, it goes higher.

Buying is a decision. So is holding, but it should not be a religion but a decision. The value of any company is the present value of its cash flows. When the present value of cash flows (per share) is less than the price of the stock, the stock should not be “held” but sold.

WarrenBuffett is looked upon as the deity of buy and hold.

Look at Coca Cola when it hit $40 in 1999. Its earnings power at the time was about $0.80. It was trading at 50 times earnings. It was significantly overvalued, considering that most of the growth for this company was in the past.

Fast-forward almost a quarter of a century – literally a generation. Today the stock is at $60. It took more than a decade to reclaim its 1999 high. Today, Coke’s earnings power is around $1.50–1.90. Earnings have stagnated for over a decade. If you did not sell the stock in 1999, you collected some dividends, not a lot but some. The stock is still trading at 30–40x earnings. Unless they discover that Coke cures diabetes (not causes it), its earnings will not move much. It’s a mature business with significant health headwinds against it.

“Long-term” and “buy-and-hold” investing are often confused.

People should not own stocks unless they have a long-term time horizon. Long-term investing is an attitude, an analytical approach. When you build a discounted cash flow model, you are looking decades ahead. However, this doesn’t mean that you should stop analyzing the company’s valuation and fundamentals after you buy the stock, as they may change and affect your expected return. After you put in a lot of analytical work and buy the stock, you should not simply switch off your brain and become a mindless buy-and-hold investor.

This doesn’t mean you shouldn’t be patient, which I’ll discuss next; but holding, not selling, a stock is a decision.

2. Key Characteristics of a Good Investor

I’m going to sound a bit more preachy than usual, but it’s very difficult to answer this question in any other way.

You need three Ps – passion, patience, process.

Passion

Investing is not a 9-to-5 job; it’s a 24/7 adventure. Unlike flipping burgers or processing insurance claims, where you can clock in at 9 AM, fall into a stupor, and then reawaken at 5 PM when you clock out.

This should be your test: If you catch yourself treating investing as a 9-to-5 job, then you have little passion for it.

If this is the case, don’t do it (this probably applies to any choice of a profession). You don’t stand a chance against people for whom investing is a never-ending puzzle to be solved on their life’s journey. All of my investment friends are dripping with passion for investing; they are obsessed with it. None of them are in it only for the money.

You won’t last long in this profession if you’re not passionate about stocks. Patience

Investing is like real life – the connection between effort and result is nonlinear. It is very loose.

You may be making all of the right rational decisions: You are buying stocks that lie within your EQ/IQ spectrum, and they are significantly undervalued, but the market simply doesn’t care. It just keeps sending your stocks down. To make things even more frustrating, while your stocks are declining, speculators who treat the stock market as a craps table at Caesars Palace are killing it, making money hand over fist. It’s painful. It is excruciatingly painful if you have the wrong client base.

This is where patience comes in. My father told me this story, which happened right before I was born.

My family lived in Murmansk, a city 125 miles north of the Arctic Circle in northwest Russia. My mom went to give birth to my brothers and me in Saratov, a city in central Russia, about 1200 miles from Murmansk. She wanted to be closer to her parents. My father could not leave work, so he stayed in Murmansk.

A few weeks before I was born, he went to visit his best friend, Alexander. He told him that he was worried about my mom and the birth. His friend told him something that I remember to this day (with a chuckle): “Naum, you did your part; you cannot go back and correct what you did. Now you just have to wait.”

Investing is patience punctuated by decisions.

As the French mathematician Blaise Pascal said, “All of humanity’s problems stem from man’s inability to sit quietly in a room alone.”

One more thought here: I try to take the temperature of my emotions and the mental activity of my brain. When I find myself overheating, with the stock market occupying my entire brain, I forcibly disconnect and unplug myself from it. The quality of my thoughts and decisions when my brain is overheating is likely to be low. So, I go for a walk in the park, read a fiction book, go see a movie, or visit an art museum. Process

Managing someone else’s money is an incredible responsibility, which you may not fully appreciate during bull markets. But sideways and bear markets will remind you quickly.

I don’t want to over-glorify what we do – we are not curing cancer or saving people from burning buildings. But IMA clients entrust us with their life savings and tell me, “Vitaliy, please don’t screw it up.”

My decisions may determine whether our clients get to retire, pay for their medical expenses, or help their kids buy houses.

Staying rational when the world around you is melting up with greed or melting down in fear isn’t a capacity that one accidentally stumbles upon. You engineer it through a series of small, repeatable decisions – your investment process.

Posted on October 26, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

“What is good for the goose is good for the gander”

By Rick Kahler CFP®

There is an old adage that says, “What is good for the goose is good for the gander.”

In today’s urbanized world, most of us probably wouldn’t have the slightest idea what’s good for geese. Yet we still know that this saying reminds us to be cautious about anyone who makes recommendations they don’t follow themselves.

This is especially important when it comes to investment advice.

Duopoly

Have you ever wondered how your investment advisor invests their money? Have you wondered if the agent selling you cash value life insurance as a retirement investment is investing their retirement in the same? Or whether an advisor recommending a specific mutual fund, stock investment, or bond issue buys the same for their own portfolio?

Ask

My suggestion is to stop wondering and ask. I rarely have a client or prospective client ask me whether I invest my own money in the same way I invest the funds of clients. Most people think it is just too personal to ask how an advisor is investing their own funds and that the advisor may take offense.

Yet knowing how anyone offering investment advice to you invests their own funds is highly relevant. It’s especially wise to ask this if someone is trying to sell you on an “exciting opportunity” that sounds too good to be true. An evasive or vague answer is an obvious red flag. But even with a fiduciary advisor, I believe asking how they invest their own money is a legitimate question. I for one am happy to answer it. Yes, the investment vehicles and strategies I recommend for clients are the same ones I use for myself.

If an advisor is recommending a strategy or investment for you that they don’t subscribe to or invest in themselves, then it’s a good idea to ask another question.

Why not?

Certainly, there are good reasons why an advisor would not have the same asset allocation that they recommend for you. They may be significantly younger or older, or they may have a significantly more aggressive or adverse tolerance for risk. But if your advisor outsources your investments to SEI but uses Vanguard for themselves, I would want to explore that. Or if your advisor is about the same age as you are, but has a significantly different asset allocation and uses none of the investments she recommends that you invest in, I would want to know why.

If an advisor suggests that you put 35% of your investment funds into a private REIT but they don’t own a private REIT, what’s the reason? Or if they are recommending you own a managed futures limited partnership but they don’t own that same partnership or any managed futures funds. Or, maybe they are recommending the A shares of an actively managed mutual fund but themselves purchase passively managed institutional shares.

If you don’t feel comfortable or knowledgeable enough to ask questions like these about specific investments, it’s still important to find out about an advisor’s broader approach to investing. Do they recommend that you “buy and hold,” yet they actively time the market with their own portfolio? Or maybe they actively trade your portfolio while following a “buy and hold” strategy themselves.

Assessment

While portfolio specifics might vary, I want any investment advisor to buy into the same investment philosophy they are recommending to me. If they are going to be timing the market with my funds, I want them to be making the same market moves with their own funds.

If a “sauce” isn’t good enough for the advisor personally, it isn’t good enough to recommend to clients.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements.

Subscribe: MEDICAL EXECUTIVE POST for curated news, essays, opinions and analysis from the public health, economics, finance, marketing, IT, business and policy management ecosystem.

Posted on October 25, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Applications to MBA programs are up 12% in 2024 after declining for two years, according to the Graduate Management Admission Council, which surveys business school admissions offices.

Apple and Goldman Sachs were ordered to pay $89 million by the Consumer Financial Protection Bureau for failing to address thousands of consumer disputes of Apple Card transactions.

Apple is cutting production of Vision Pro due to slow sales. The tech giant is scaling down production of its $3,500 Vision Pro VR headset and might halt assembly of new ones next month,

UPS delivered a strong earnings report, with revenue beating analyst expectations for the first time in two years. Shares popped 5.28%.

ServiceNow rose 5.41% to a new all-time high thanks to a beat-and-raise third-quarter earnings report powered by higher AI demand for the enterprise software company.

Whirlpool climbed 11.20% after announcing solid earnings and reiterating guidance for the rest of the fiscal year, reassuring worried shareholders.

Molina Healthcare soared 17.67% after beating both top and bottom line estimates in the third quarter, thanks to the health insurer reaping the rewards of higher Medicaid payouts.

STOCKS DOWN

IBM dropped 6.17% on disappointing third-quarter results, missing on both top and bottom line forecasts thanks to lower consulting and infrastructure revenue.

Peloton pedaled higher yesterday after Greenlight Capital’s David Einhorn declared that the company was undervalued while he was pedaling on a Peloton. The stunt only worked for a quick sprint, though, with shares back down 2.07% today.

TKO Group Holdings got hit with a piledriver after the owner of the WWE and UFC announced it is acquiring several entertainment companies, including Professional Bull Riders. Investors bucked shares off 8.69%.

Keurig Dr. Pepper fizzled 4.80% thanks to lower sales last quarter, though the company is trying to bolster revenue by acquiring energy drink maker Ghost.

Air taxi startup Lilium crashed 61.50% on the news that its main subsidiaries have run out of cash and are filing for insolvency.

The S&P 500® index (SPX) rose 12.44 points (0.21%) to 5,809.86; the $DJI fell 140.59 points (–0.33%) to 42,374.36; and the NASDAQ Composite® ($COMP) added 138.83 points (0.76%) to 18,415.49.

The 10-year Treasury note yield fell four basis points to 4.20%.

The CBOE Volatility Index® (VIX) was about flat at 19.18.

Posted on October 24, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

QUESTION EVERYTHING?

By Staff Reporters

***

***

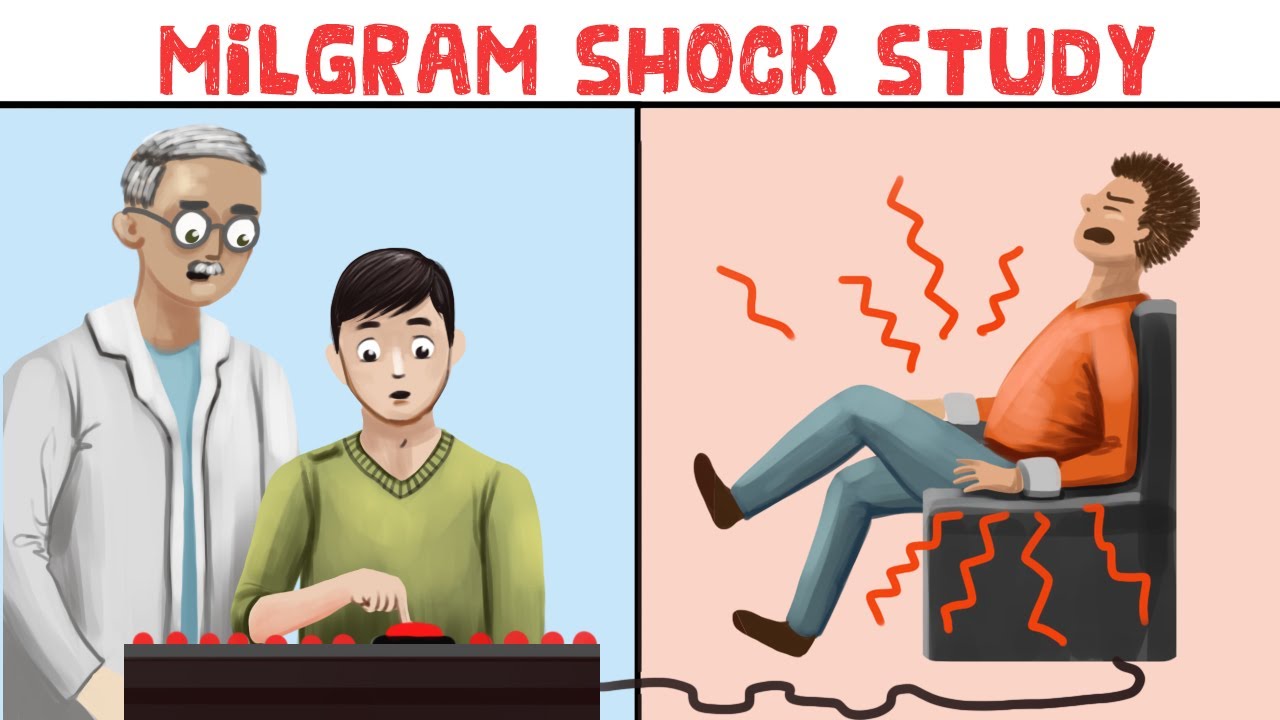

Question: Why do we follow orders, even when they seem wrong?

According to colleague Dan Ariely PhD,Obedience to Authority is a powerful force, making us do things we wouldn’t normally do. Think of the infamous Milgram experiment, where people shocked others because a guy in a lab coat told them to do so. It’s our brain’s way of outsourcing decision-making to someone else. While it can keep society orderly, it also explains why people sometimes follow questionable orders.

Milgram’s experiments posed the question: Would people obey orders, even if they believed doing so would harm another person?

Milgram’s findings suggested the answer was yes, they would. The experiments have long been controversial, both because of the startling findings and the ethical problems with the research. More recently, experts have re-examined the studies, suggesting that participants were often coerced into obeying and that at least some participants recognized that the other person was just pretending to be shocked. Such findings call into question the study’s validity and authenticity, but some replications suggest that people are surprisingly prone to obeying authority.

So, question authority [doctor, financial advisor, accountant, clergy, professor and lawyer, etc] – just not your GPS.

Posted on October 24, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Quote: “It looks like the global battle against inflation has largely been won, even if price pressures persist in some countries. In most countries, inflation is now hovering close to central bank targets…The decline in inflation without a global recession is a major achievement.”—IMF (CNN Business)

Spirit Airlines is back from the dead, soaring 46.67% on a Wall Street Journal report that it may end up merging with FrontierAirlines after all. Frontier Airlines rose 0.76% on the news.

AT&T climbed 4.65% after it beat earnings expectations in the third quarter, though it missed on revenue.

Starbucks fell hard late yesterday but recovered a bit this afternoon after new CEO Brian Niccol said the coffee chain is suspending its 2025 fiscal outlook. Shares rose 0.86% today.

Coca-Cola fizzled 2.07% after beating both top and bottom line expectations. The problem is that the only reason the soda giant performed well was because it raised prices, while demand for soft drinks slowed.

Enphase Energy plummeted 14.92% after the solar stock missed on both earnings and revenue expectations last quarter.

Boeing is a very familiar name in the “What’s down” section, and its latest earnings report did nothing to help. The manufacturing giant notched a $6 billion loss last quarter, and shares fell 1.76%.

The SPX fell 53.78 points (–0.92%) to 5,797.42; the Dow Jones Industrial Average® ($DJI) lost 409.94 points (–0.96%) to 42,514.95; and the NASDAQ Composite ($COMP) dropped 296.47 points (–1.60%) to 18,276.65.

The 10-year Treasury note yield gained four basis points to 4.24%.

Although some might view a budget as unnecessarily restrictive, sticking to a spending plan can be a useful tool in enhancing the wealth of a medical practice. So, I will emphasize keys to smart budgeting and how to track spending and savings in these tough economic times.

There is an aphorism that suggests, “Money cannot buy happiness.” Well, this may be true enough but there is also a corollary that states, “Having a little sure reduces the unhappiness.”

Unfortunately, today there is more than a little financial unhappiness in all medical specialties. The challenges range from the commoditization of medicine, aging demographics, Medicare reimbursement cutbacks and increased competition to floundering equity markets, the home mortgage crisis, the squeeze on credit and declines in the value of a practice. Few doctors seem immune to this “perfect storm” of economic woes.

Far too many physicians are hurting and it is not limited to above-average earning professionals. However, one can strive to reduce the pain by following some basic budgeting principles. By adhering to these principles, physicians can eliminate the “too many days at the end of the month” syndrome and instead develop a foundation for building real wealth and security, even in difficult economic climates like we face today.

There are three major budget types. A flexible budget is an expenditure cap that adjusts for changes in the volume of expense items. A fixed budget does not. Advancing to the next level of rigor, a zero-based budget starts with essential expenses and adds items until the money is gone. Regardless of type, budgets can be extremely effective if one uses them at home or the office in order to spot money troubles before they develop.

For the purpose of wealth building, doctors may think of this budget as a quantitative expression of an action plan. It is an integral part of the overall cost-control process for the individual, his or her family unit or one’s medical practice.

Preparing a net income statement (lifestyle cash flow budget) is often difficult because many doctors perceive it as punitive. Most doctors do not live a disciplined spending lifestyle and they view a budget as a compromise to it. However, a cash flow budget is designed to provide comfort when there is surplus income that can be diverted for other future needs. For example, if you treat retirement savings as just another periodic bill, you are more likely to save for it.

You may construct a personal cash budget by recording each cash receipt and cash disbursement on a spreadsheet. Only the date, amount and a brief description of the transaction are necessary. The cash budget is a simple tool that even doctors who lack accounting acumen can use. Since it is possible to track the cash-in and cash-out in the same format used for a standard check register, most doctors find that the process takes very little time. Such a budget will provide a helpful look at how well you are staying within available resources for a given period.

We then continue with an analysis of your operating checkbook and a review of various source documents such as one’s tax return, credit card statements, pay stubs and insurance policies. A typical statement will show all cash transactions that occur within one year. It is helpful to establish a monthly equivalent to all items of income and expense. For the purposes of getting started, note items of income and expense by the frequency you are accustomed to receiving or spending them.

What You Should Know About The ‘Action Plan’ Cash Budget

For a medical office, the first operations budget item might be salary for the doctor and staff. Operating assets and other big ticket items come next. Some of our doctors/clients review their office P&L statements monthly, line by line, in an effort to reduce expenses. Then they add back those discretionary business expenses they have some control over.

Now, do you still run out of money before the end of the month? If so, you had better cut back on entertainment, eating dinner out or that fancy, new but unproven piece of medical equipment. This sounds draconian until you remind yourself that your choice is either: live frugally later or live a simpler lifestyle now and invest the difference.

As a young doctor, it may be a difficult trade-off. By mid-life, however, you are staring retirement in the face. That is why the action plan depends on your actions concerning monetary scarcity, a plan that one can implement and measure using simple benchmarks or budgeting ratios. By using these statistics, perhaps on an annual basis, the doctor can spot problems, correct them and continue planning actively toward stated goals like building long-term wealth.

Useful Calculations To Assess Your Budgeting Success

In the past, generic budgeting ratios would emphasize not spending more than 15 to 20 percent of your net salary on food or 8 percent on medical care. Now these estimates have given way to more rigorous numbers. Personal budget ratios, much like medical practice financial ratios, represent comparable benchmarks for parameters such as debt, income growth and net worth. Although these ratios are still broad, the following represent some useful personal budgeting ratios for physicians.

• Basic liquidity ratio = liquid assets / average monthly expenses. Cash-on-hand should approach 12 to 24 months or more in the case of a doctor employed by a financially insecure HMO or fragile medical group practice. Yes, chances are you have heard of the standard notion of setting enough cash aside to cover three months in a rainy day scenario. However, we have decried this older laymen standard for many years in our textbooks, white papers and speaking engagements as being wholly insufficient for the competitively unstable environment of modern healthcare.

• Debt to assets ratio = total debt / total assets. This percentage is high initially but should decrease with age as the doctor approaches a debt-free existence

• Debt to gross income ratio = annual debt repayments / annual gross income. This represents the adequacy of current income for existing debt repayments. Doctors should try to keep this below 20 to 25 percent.

• Debt service ratio = annual debt repayment / annual take-home pay. Physicians should aim to keep this ratio below 25 to 30 percent or face difficulty paying down debt.

• Investment assets to net worth ratio = investment assets / net worth. This budget ratio should increase over time as retirement approaches.

• Savings to income ratio = savings / annual income. This ratio should also increase over time as one retires major obligations like medical school debt, a practice loan or a home mortgage.

• Real growth ratio = (income this year – income last year) / (income last year – inflation rate). This budget ratio should grow faster than the core rate of inflation.

• Growth of net worth ratio = (net worth this year – net worth last year) / net worth last year – inflation rate). Again, this budgeting ratio should stay ahead of inflation.

In other words, these ratios will help answer the question: “How am I doing?”

Pearls For Sticking To A Budget

Far from the burden that most doctors consider it to be, budgeting in one form or another is probably one of the greatest tools for building wealth. However, it is also one of the greatest weaknesses among physicians who tend to live a certain lifestyle.

In fact, we have found that less than one in 10 medical professionals have a personal budget. Fear, or a lack of knowledge, is a major cause of procrastination. Fortunately, the following guidelines assist in reversing this microeconomic disaster.

1. Set reasonable goals and estimate annual income. Do not keep large amounts of cash at home or office. Deposit it in an FDIC insured money-market account for safety. Do not deposit it in a money market mutual fund with net asset value (NAV) that may “break the buck” and fall below the one-dollar level. Track actual bills and expenses.