BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on February 18, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

IRS Tax Implications

By Staff Reporters

***

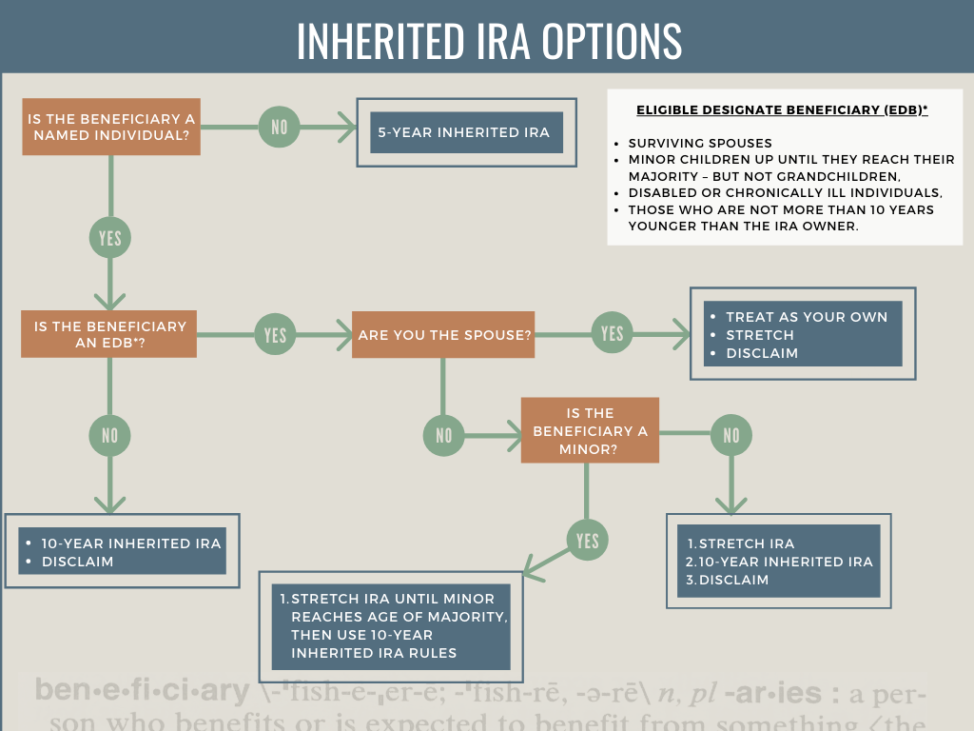

If you inherited a tax-deferred retirement plan, such as a traditional IRA, you’ll have to pay taxes on the money. But you can make the tax hit less onerous.

Spouses can roll the money into their own IRAs and postpone distributions—and taxes—until they’re 70½. All other beneficiaries who want to continue to benefit from tax-deferred growth must roll the money into a separate account known as an inherited IRA. Make sure the IRA is rolled directly into your inherited IRA. If you take a check, you won’t be allowed to deposit the money. Rather, the IRS will treat it as a distribution and you’ll owe taxes on the entire amount.

Once you’ve rolled the money into an inherited IRA, you must take required minimum distributions every year—and pay taxes on the money—based on your age and life expectancy. Deadlines are critical: You must take your first RMD by December 31st. of the year following the death of your parent (or whoever left you the account). Otherwise, you’ll be required to deplete the entire account within five years after the year following your parent’s death.

The December 31st. deadline is also important if you are one of several beneficiaries of an inherited IRA. If you fail to split the IRA among the beneficiaries by that date, your RMDs will be based on the life expectancy of the oldest beneficiary, which may force you to take larger distributions than if the RMDs were based on your age and life expectancy.

You can take out more than the RMD, but setting up an inherited IRA gives you more control over your tax liabilities. You can, for example, take the minimum amount required while you’re working, then increase withdrawals when you’re retired and in a lower tax bracket.

Did you inherit a Roth IRA? And so, as long as the original owner funded the Roth at least five years before he or she died, you don’t have to pay taxes on the money. You can’t, however, let it grow tax-free forever. If you don’t need the money, you can transfer it to an inherited Roth IRA and take RMDs under the same rules governing a traditional inherited IRA. But with a Roth, your RMDs won’t be taxed.

Posted on February 18, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

GLOBALMARKETS: Stabilized on Friday after the threat of a potential Russian invasion of Ukraine propelled the Dow to its worst day of 2022. Australia’s S&P/ASX 200 and Japan’s benchmark Nikkei closed down 1% and 0.4%, respectively, while South Korea’s Kospi was little changed. Chinese markets were mixed. As the benchmark Shanghai Composite Index gained 0.7%, Hong Kong’s Hang Seng Index dropped 1.9%. In Europe, stocks were little changed at the open. London’s FTSE 100 and France’s CAC 40 each rose 0.2%, while Germany’s DAX ticked up 0.1%.

DOMESTIC MARKETS: The Dow plummeted 622 points, or 1.8% — hitting its lowest level so far this year in the process. The S&P 500 fell 2.1% and the NASDAQ was down 2.9%. All three indices are now in the red for the week. Finally, US futures pointed up slightly with Dow futures, S&P 500 futures and NASDAQ futures rising 0.6%, 0.7% and 0.8%, respectively.

FOMC: Jim Bullard, the president of the St. Louis Federal Reserve and member of the Federal Open Market Committee, said that the Federal Reserve wants to pursue the best policy as members debate how quickly they should raise interest rates. He called for a full percentage point interest rate hike by July, 2022. And, billionaire investor Carl Icahn predicts the Fed’s money-printing party will end badly because the government can’t control inflation

Posted on February 17, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

MCOL Cyber Attacks

By Staff Reporters

***

Critical Insight: 2021 with 5 Findings

• In 2021, 45 million individuals were affected by healthcare cyber-attacks, up from 34 million in 2020. • The total number of affected increased 32% over 2020, meaning that more records are exposed per breach each year. • Breaches only rose 2.4% from 663 in 2020 to 679 in 2021 but still hit historic highs. • Hacking/IT incidents continue as the most common cause of breaches with an increase of 10% in 2021. • Hacking incidents at outpatient/specialty clinics saw a 41% increase in these types of breaches in 2021.

Posted on February 17, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

****

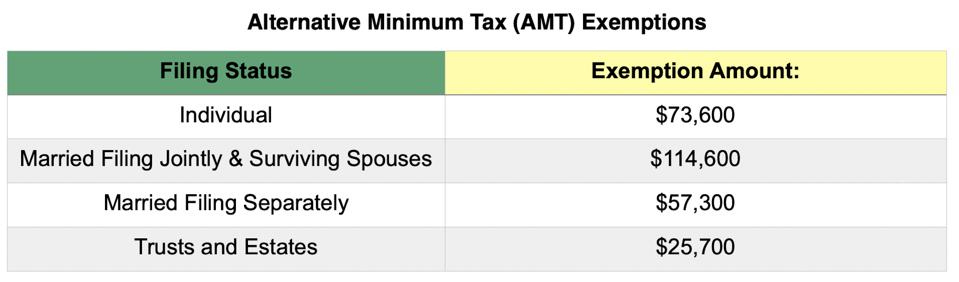

Alternative Minimum Tax

DEFINITION: The alternative minimum tax (AMT) is a tax imposed by the United States federal government in addition to the regular income tax for certain individuals, estates, and trusts. As of tax year 2018, the AMT raises about $5.2 billion, or 0.4% of all federal income tax revenue, affecting 0.1% of taxpayers, mostly in the upper income ranges.

Posted on February 17, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

BIOTECHNOLOGY: According to Bloomberg, former high flying biotechnology favorites Mirati Therapeutics Inc. and Sage Therapeutics Inc. have lost more than half their value from record highs, hurt by growing pessimism on new medicines as well as the higher rate environment damaging most stocks.

MARKETS: Stocks went down, then back up, and closed pretty much where they started. The e-commerce platform Shopify is another pandemic winner that’s been absolutely crushed during the “reopening”: Its stock has fallen to its lowest level since June 2020.

PPI: The producer price index rose 1% over the prior month.

Covid: Dr. Zayid Al-Aly reported that even a mild COVID-19 infection increasedthe risk of having cardiovascular problems — including heart rhythm irregularities, potentially deadly clots in the legs and lungs, heart failure, heart attack and stroke, within a year after being infected.

MICROSOFT: Microsoft CEO Satya Nadella is on a major shopping spree. The company’s planned purchase of video game maker Activision Blizzard, with a price tag of nearly $70 billion, is Microsoft’s biggest and boldest acquisition. But it’s hardly the only notable deal in the Nadella era. Microsoft scooped up advertising tech business Xandr from CNN owner AT&T late last year for a reported $1 billion. The company also shelled out nearly $20 billion for cloud software firm Nuance earlier in 2021. That’s on top of numerous other billion dollar deals Microsoft has made since Nadella took the helm in 2014, including the acquisitions of Minecraft developer Mojang, Bethesda games studio owner ZeniMax Media, open source coding site GitHub and business social media network LinkedIn. The LinkedIn deal was previously Microsoft’s largest, with a value of $26.2 billion. Now there are reports Microsoft is looking to buy Mandiant, the cybersecurity software firm formerly known as FireEye that is currently valued at about $4.5 billion.

Posted on February 16, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Entry-level Revenue Cycle Recruitment Takes 84 Days on Average

A recent AKASA survey of 514 chief financial officers and revenue cycle leaders at hospitals and health systems in the U.S. found:

• Entry-level revenue cycle talent (0-5 years): On average, costs $2,167 for recruitment and takes 84 days to fill vacant roles. • Mid-level revenue cycle talent (6-10 years): On average, costs $3,581 for recruitment and takes 153 days to fill vacant roles. • Senior-level revenue cycle talent (10+ years): On average, costs $5,699 for recruitment and takes 207 days to fill vacant roles.

The Physician Executive Summary is always included at the beginning of a formal business plan and represents a brief synopsis of the medical prarctice entire plan. Its appearance, grammar and style should be sharp and crisp as it represents an enticement for the reader to maintain interest and contribute intelligent or economic input into the new venture.

It should contain information about the practice, advertising and marketing opportunities, physician management, proposed financing with four Pro Forma financial statements, business operations and exit strategy. This last point, while unpleasant is often overlooked by naive practitioners. Business experts however, look favorably upon an escape plan and view it as the mark of mature professional that realizes the possibility of success as well as failure.

****

***

Ultimately, the plan must explain to potential investors how you will make the practice profitable and produce the required Return on Investment (ROI) for them. It must describe medical services, patient acceptance and benefits, provider qualifications and accomplishments, the amount of capital required, market size, potential practice growth rate, and market niche.

Additional information may include office location, proximity to labor, transportation, license requirements, business entity status, proprietary technology and potential working agreements with various insurance, managed care, ACA and HMO plans. If all of the above seems bewildering to the uninitiated, you are correct.

Remember however, that if you do not have, or can’t borrow the funds to begin a private practice, you will just have to become an employed practitioner until you can. It is therefore imperative to start off on the right foot, with a sound business plan, as you begin your medical career.

Posted on February 16, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

MARKETS: The Dow jumped 422 points, or 1.2%. The S&P 500 surged 1.5% and the NASDAQ was 2.5% higher.

OIL: US oil futures tumbled 3.7% to just under $92 a barrel. That’s despite the fact that Russia stressed that major military exercises would continue.

CPI: The Producer Price Index rose 1% last month, marking a significant acceleration from December’s 0.2% jump.

Meta: As Varietyreports, the company has agreed to pay $90 million to settle a 2012 class action lawsuit accusing it of violating users’ privacy. Facebook allegedly overstepped its bounds in 2010 and 2011 by using tracking cookies that monitored browsing after users signed out despite promises to the contrary.

MODERNA: Moderna Inc (NASDAQ: MRNA) shares were down more than 40% since the start of the year and continues to trend lower. Vaccine stocks are facing selling pressure as the COVID-19 omicron variant fades, but Moderna investors have been expressing concerns about recent stock sales from CEO Stéphane Bancel, as well as the presumed deletion of his Twitter account.

Posted on February 16, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

Berkeley’s Lester Center for Entrepreneurship

Entrepreneurship is a Calling

***

By Steve Blank

During the Cold War with the Soviet Union, science and engineering at both Stanford and U.C. Berkeley were heavily funded to develop Cold War weapon systems. Stanford’s focus was Electronic Intelligence and those advanced microwave components and systems were useful in a variety of weapons systems. Starting in the 1950’s, Stanford’s engineering department became “outward facing” and developed a culture of spinouts and active faculty support and participation in the first wave of Silicon Valley startups.

At the same time Berkeley was also developing Cold War weapons systems. However its focus was nuclear weapons – not something you wanted to be spinning out. So Berkeley started a half century history of “inward facing innovation” focused on the Lawrence Livermore nuclear weapons lab. (See the presentation here.)

Given its inward focus, Berkeley has always been the neglected sibling in Silicon Valley entrepreneurship. That has changed in the last few years.

Today the U.C. Berkeley Haas Business School is a leader in entrepreneurship education. It has replaced how to write a business plan with hands-on Lean Startup methods. It’s teaching the LaunchPad® and the I-Corps for the National Science Foundation and National Institutes of Health, as well as corporate entrepreneurship courses.

We are in the middle of a shift in entrepreneurship education from teaching the waterfall model of startup development (enshrined in business plans) to teaching the lean startup model

The Lean LaunchPad process works across a wide range of domains – from science and engineering to healthcare, energy, government, the social sector and for corporate innovation

Customer Development works outside Silicon Valley. In fact, it works globally

The Lean LaunchPad is a business process that teaches entrepreneurs and innovators to make business-focused, evidence-based decisions under conditions of chaos and uncertainty. It’s a big idea.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

“When a practicing physician thinks about their risk exposure resulting from providing patient care, medical malpractice risk immediately comes to mind. But; malpractice and liability risk is barely the tip of the iceberg, and likely not even the biggest risk in the daily practice of medicine. There are risks from having medical records to keep private, risks related to proper billing and collections, risks from patients tripping on your office steps, risks from medical board actions, risk arising from divorce, and the list goes on and on. These liabilities put a doctor’s hard earned assets and career in a very vulnerable position.

These new books from Dr. David Marcinko and Prof. Hope Hetico show doctors the multiple types of risk they face and provides examples of steps to take to minimize them. They are written clearly and to the point, and are a valuable reference for any well-managed practice. Every doctor who wants to take preventive action against the risks coming at them from all sides needs to read these books.”

Richard Berning MD FACC [New Haven, Connecticut, USA]

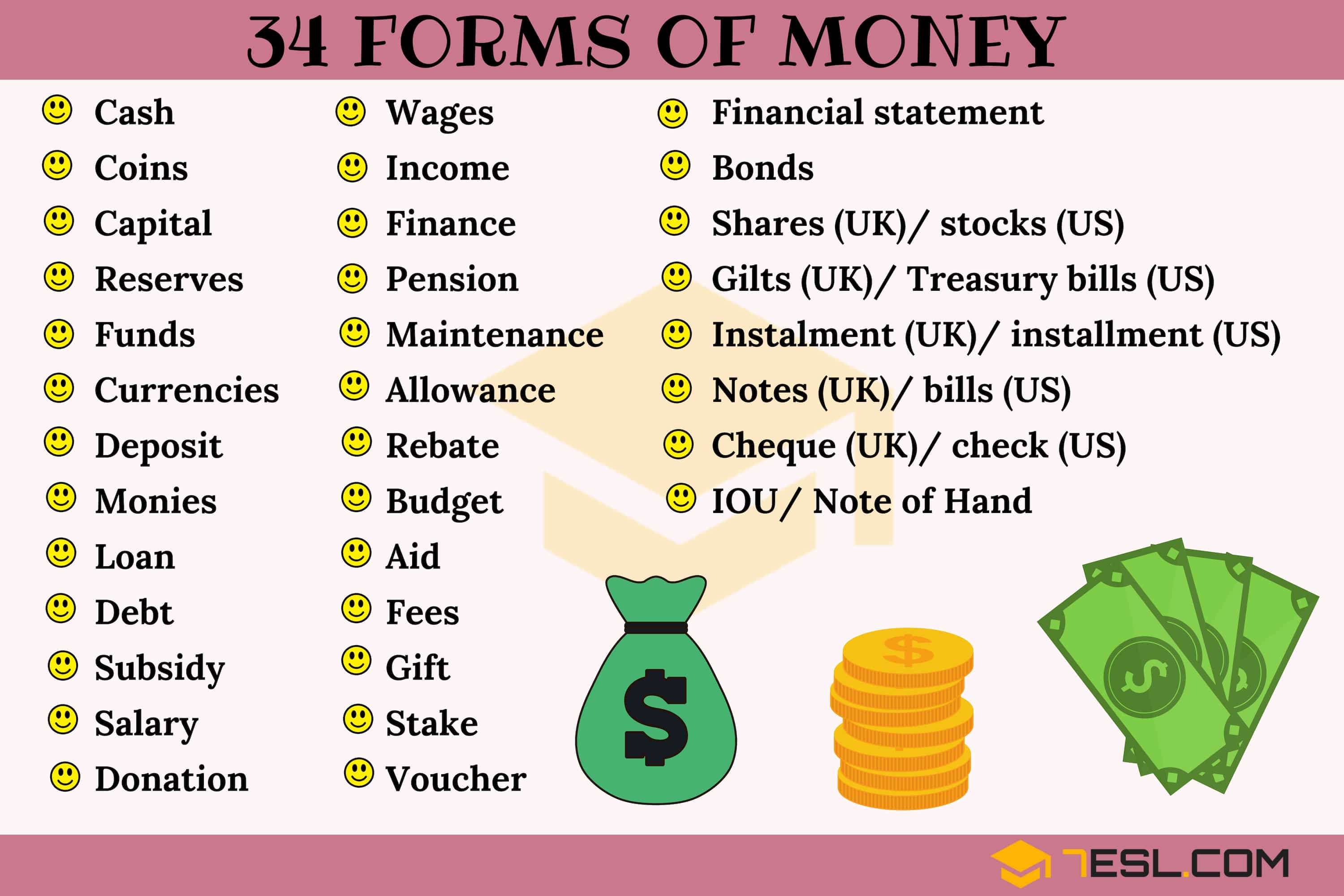

People really love money since it is needed to buy just about everything. In fact, we actually published a formal print dictionary on health economics and finance terms that is very popular with physician investors and medical colleagues; it is a favorite of economic students as well!

And, money is by far one of those words that has more slang or terms for it than any others. This proves that cash or money, does not have be boring when speaking about it. Just keep in mind that these slang synonyms are in plural form. They are also words mostly used for US currency.

Perhaps the fact that money is so important may help to explain why there are so many different ways to say it. These 95 slang words for money and their meanings are really worth taking a look at. This list not only contains the countless ways to speak, write or say the word money, but also what are the meanings behind each phrase or term.

Posted on February 15, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

By Staff Reporters

***

MARKETS: Stocks ticked lower as investors fretted over an upcoming interest rate hike from the Federal Reserve and a potential Russian invasion of Ukraine. With all the chatter of conflict in Europe, everyone’s watching whether oil prices will hit $100 a barrel—they didn’t budge yesterday.

CRYPTO: SEC Chair Gary Gensler said thr crypto firm BlockFi would pay $100 million to the SEC and 32 states over charges that it had violated securities law. The penalty is the agency’s largest ever against a cryptocurrency company. BlockFi, a banklike crypto company backed by Peter Thiel, didn’t admit or deny the SEC’s findings but did agree to stop opening new lending accounts to customers in the US.

METAVERSE: For doctors, nurses and healthcare professionals who’ve spent the last few years hunched over laptops smiling pleasantly into a Zoom meetings, burnout has been pervasive. Zoom fatigue is now a widely recognized work-induced malady studied by university researchers, and many remote workers say they have trouble balancing work and their personal lives. With images on screens surrounding remote healthcare workers like a labyrinthine maze of fun-house mirrors, it might seem like the last thing a burned out medical provider needs is to strap on a VR headset to detach from the rigors of the digital medical workplace.

Nevertheless, some health care organizations are transporting their workers to the metaverse—a network of connected, 3D, virtual environments where people can interact through avatars and spatial audio—as a means of combating stress. But, for any organization curious about the metaverse, Jeremy Bailenson, a professor of communication and the founding director of the Virtual Human Interaction Lab at Stanford University, advises having a specific task in mind, such as addressing burnout or building camaraderie. “VR wins when it solves a hard problem,” he said.

The broader question of how organizations will further incorporate virtual reality into their mental health programs and rapport-building exercises is largely unanswered at this point, he added. Bailenson believes VR is a “home run for clinical use cases.” But “for this general burnout, it’s probably going to be a good tool for some people, but not a magic pill.”

Posted on February 14, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

According to Tejvan Pettinger, a public good has two characteristics:

Non-rivalry: This means that when a good is consumed, it doesn’t reduce the amount available for others. – E.g. benefiting from a street light doesn’t reduce the light available for others but eating an apple would.

Non-excludability: This occurs when it is not possible to provide a good without it being possible for others to enjoy. For example, if you erect a dam to stop flooding – you protect everyone in the area (whether they contributed to flooding defenses or not.

A public good is often (though not always) under-provided in a free market because its characteristics of non-rivalry and non-excludability mean there is an incentive not to pay. In a free market, firms may not provide the good as they have difficulty charging people for their use.

Posted on February 14, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

OIL: The threat of a Russian invasion of Ukraine is shaking up a fragile global oil market, pushing prices to $94 barrel as supplies will struggle to cushion the effect from any significant disruption in Russian fossil fuel exports. The headlines that moved markets last week—the Fed’s response to inflation, corporate earnings, tensions in Ukraine—will remain top of mind for investors this coming week. Analysts predict that if Russia were to invade Ukraine, oil could top $100 a barrel for the first time since 2014. And, the average national gasoline price is about $3.50/gallon.

DOMESTICMARKETS: Walmart, Airbnb, Nvidia, Roblox, and DraftKings will close out one of the most volatile earnings seasons in recent memory.

ASIAN MARKETS: Major Asian stock markets opened lower as investors sought safer bets ahead of a possible Russian military attack on the Ukraine. In Tokyo, the Nikkei 225 index dropped roughly 2 percent in the first hours of trading. South Korea’s KOSPI fell by a similar amount. And, while China’s big tech firms are under much regulatory pressure, they are also facing strong competition.

INVESTMENT BANKING: Roger Ng, the former head of investment banking in Malaysia for Goldman Sachs, will stand trial in New York beginning today. He’s accused of playing a prominent role in a massive laundering scheme that plundered billions from Malaysia’s sovereign wealth fund, 1MDB. Embezzled funds were used to buy a Beverly Hills hotel, a $200 million super-yacht, and even to help finance the film, Wolf of Wall Street.

Posted on February 14, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

Insights For Doctors and All Investors

***

By Vitaliy Katsenelson CFA

***

NOTE: This piece is a little more technical, and contains a bit more stock-market jargon, than most essays you get from me. While how we build portfolios is important to us and our clients, we realize that the puts and takes might bore many readers.

Posted on February 13, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

The Crypto Bowl and the Dot Com Bowl?

By Staff Reporters

***

CRYPTO CURRENCY: Tonight, about 117 million people will watch celebrities pitch cryptocurrency on the Super Bowl. In what’s being dubbed the “Crypto Bowl,” a batch of crypto exchanges including FTX, Coinbase, and Crypto.com, will air Super Bowl commercials at a cost of up to $7 million per 30-second spot. The game is even being held at a stadium named after SoFi, a company that offers crypto trading.\

This isn’t the first time startups from an emerging industry have used the Super Bowl to introduce themselves to a mass audience. Does anyone remember the 2000 Super Bowl between the Rams and the Titans? That was known as the “Dot-Com Bowl.” Startups that were part of the dot-com wave of the early internet bought nearly 20% of the total ad slots in what is considered the peak of that tech bubble.

Well, that bubble burst. In fact, according to journalist Neal Freyman, of the 14 dot-com companies that purchased Super Bowl ads that year, four are still active, five were acquired, and five (including Pets.com, OnMoney.com, and Epidemic.com) are either defunct or their status is unclear.

DEFINITION: The Medicare Payment Advisory Commission is an independent, non-partisan legislative branch agency headquartered in Washington, D.C. MedPAC was established by the Balanced Budget Act of 1997.

*** In a January 2022 meeting of MedPAC, commissioners reviewed various recommendations related to the Medicare fee schedule for various health sectors, and unanimously agreed to update Medicare payments to hospitals and keep physician payment rates the same for 2023. This Health Capital Topics article will review the recommendations made by MedPAC for each of the health sectors and their respective payment systems. (Read more…)

Posted on February 12, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

What it is – How it Works

By Staff Reporters

****

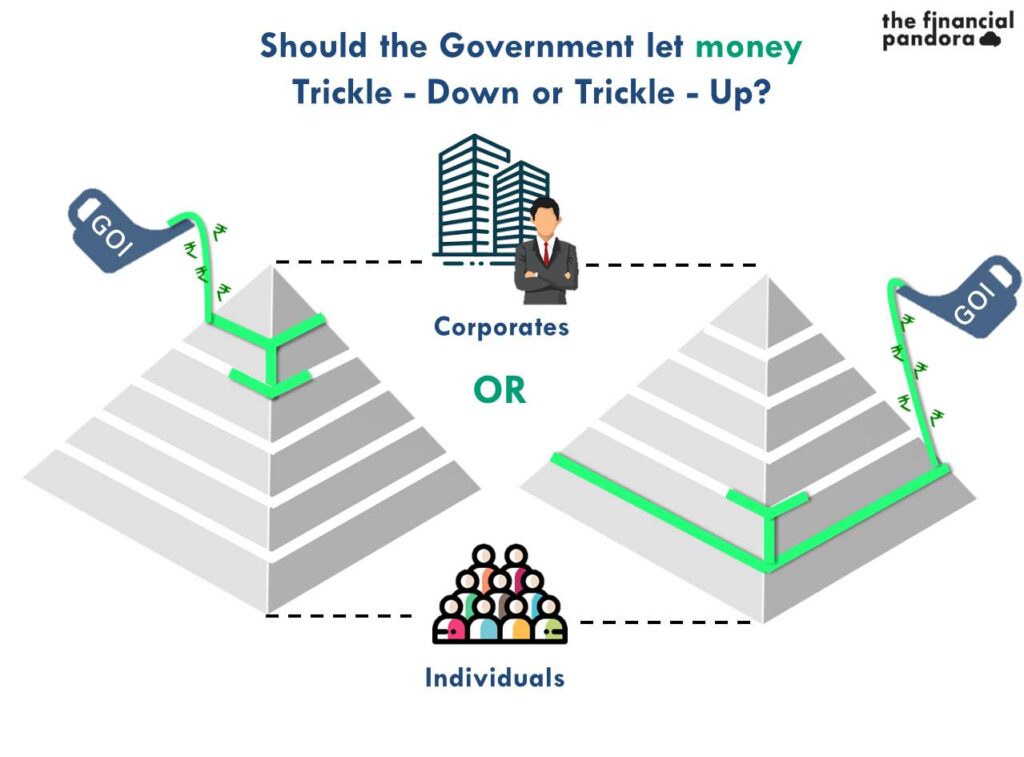

DEFINITION: Trickle-down economics is a colloquial term for supply-side economic policies. In recent history, the term has been used by critics of supply-side economic policies, such as “Reaganomics”. Whereas general supply-side theory favors lowering taxes overall, trickle-down theory more specifically advocates for a lower tax burden on the upper end of the economic spectrum. Empirical evidence shows that the proposition is regressive and has never managed to achieve all of its stated goals as described by the Reagan administration.

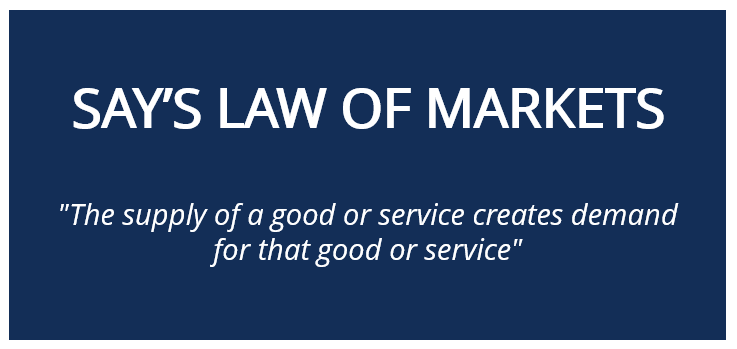

SAY’S LAW: In classical economics, Say’s law, or the law of markets, is the claim that the production of a product creates demand for another product by providing something of value which can be exchanged for that other product. Thus, production is the source of demand

Posted on February 11, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

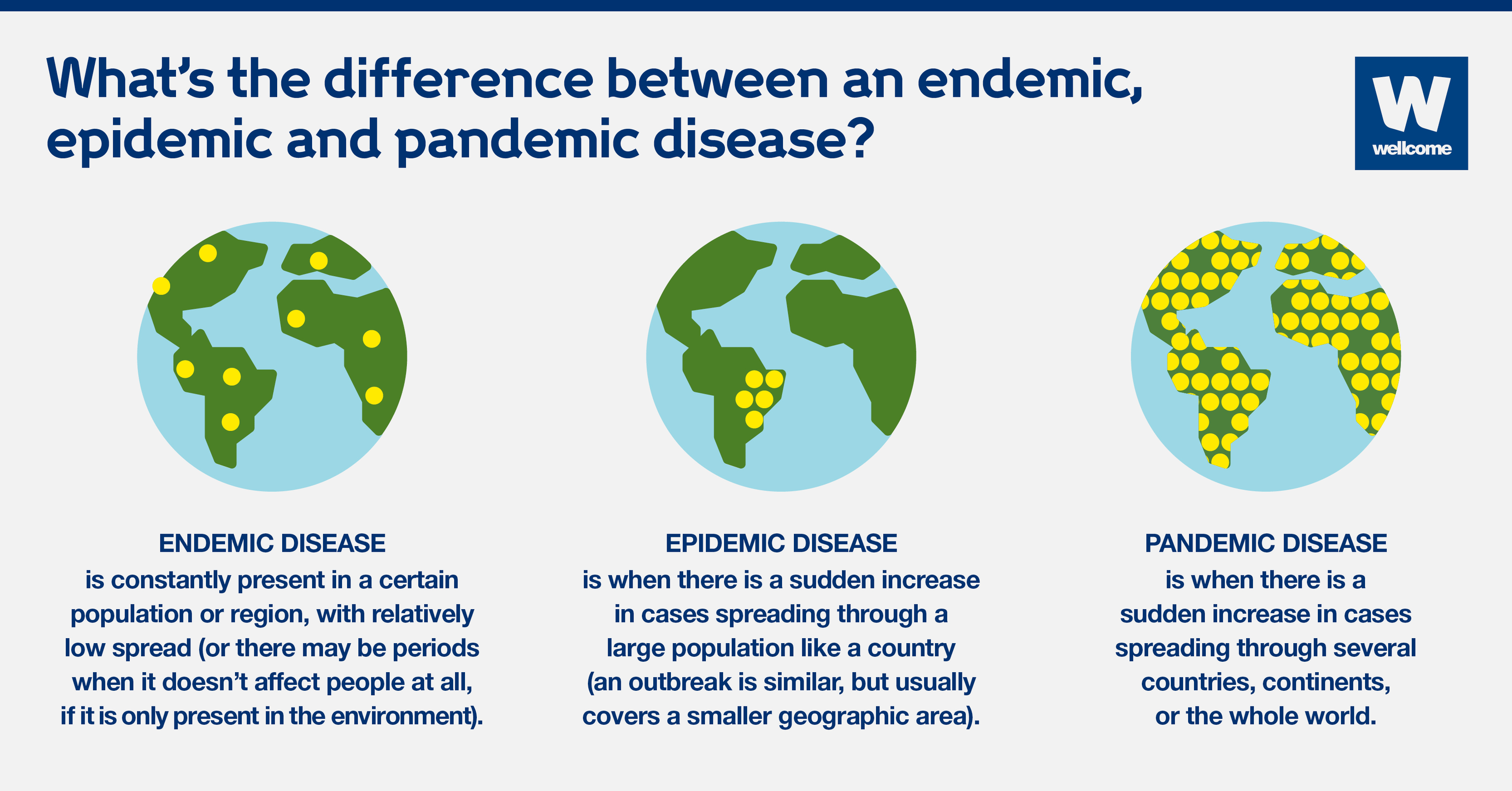

Endemic: A constant presence and/or usual prevalence of a disease or infection, such as the Corona virus, within a geographic area. (Hyperendemic is a situation in which there are persistent high levels of disease occurrence.)

Posted on February 11, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

What it Is – How it Works

By Staff Reporters

***

DEFINITION: In classical economics, Say’s law, or the law of markets, is the claim that the production of a product creates demand for another product by providing something of value which can be exchanged for that other product. Thus, production is the source of demand.

Posted on February 11, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Bonds: The 10-year US Treasury bond yield touched 2% for the first time since the summer of 2019 and stocks traded sharply lower after a key inflation figure rose to its highest level in nearly 40 years. The last time the 10-year yield was above 2% was in July 2019. Bond yields and prices move in opposition to each other.

CPI:The Consumer Price Index’s 7.5% annual surge at the start of 2022 was the biggest leap since 1982 and topped already elevated expectations for a 7.3% rise, based on Bloomberg consensus data. On a month-over-month basis, the CPI unexpectedly posted a 0.6% increase for a back-to-back month, whereas economists had been looking for a deceleration. Core inflation, which strips out volatile food and energy prices, also exceeded estimates, showing a 6.0% year-over-year jump in January.

Markets: The Dow was down 526 points while the broader S&P 500 fell 87 points. The NASDAQ Composite was also down 305 points.

Posted on February 10, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Average Annual Growth Rates of Spending, Utilization, and Prices

• Spending per person: commercial insurers (3.2% per year); Medicare fee for service (1.8% per year) • Utilization per person: commercial insurers (0.4% per year); Medicare fee for service (0.5% per year) • Prices paid to providers: commercial insurers (2.7% per year); Medicare fee for service (1.3% per year).

Notes: For hospitals and physicians’ services, 2013-2018 Source: Congressional Budget Office – January 2022

Posted on February 10, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

SYNOPSIS: The home office deductionallows qualified taxpayers to deduct certain home expenses when they file taxes. And, now that some doctors and many of us are working remotely, you may be wondering whether working from home will yield any tax breaks. If your small medical or healthcare consulting or other business qualifies you for a home office tax deduction, should you be concerned about triggering an audit? How does a business qualify in the first place; etc?

Well, to claim the home office deduction on their 2021 tax return, taxpayers generally must exclusively and regularly use part of their home or a separate structure on their property as their primary place of business.

***

If I work from home, do I qualify for a home office tax deduction?

If you’re an employee working remotely rather than an employer or business owner, you unfortunately don’t qualify for the home office tax deduction (however, please note that it is still available to some as a state tax deduction). Prior to the Tax Cuts and Job Acts (TCJA) tax reform passed in 2017, employees could deduct unreimbursed employee business expenses, which included the home office deduction. However, for tax years 2018 through 2025, the itemized deduction for employee business expenses has been eliminated.

If I’m self-employed, should I take the home office tax deduction?

You may have heard that taking the home office deduction sends a red flag to the IRS and ups your chances of being audited. Although there may have been some merit to this advice in the past, changes in the tax rules in the late 1990s made it easier for people who work out of their homes to qualify for these write-offs. So if you qualify, by all means, take it.

Do I qualify for the home office tax deduction?

Generally speaking, to qualify for the home office deduction, you must meet one of these criteria:

Exclusive and regular use: You must use a portion of your house, apartment, condominium, mobile home, boat or similar structure for your business on a regular basis. This also includes structures on your property, such as an unattached studio, barn, greenhouse or garage. It doesn’t include any part of a taxpayer’s property used exclusively as a hotel, motel, inn, or similar business.

Principal place of business: Your home office must be either the principal location of your business or a place where you regularly meet with customers or clients. Some exceptions to this rule include day care and storage facilities.

What is “exclusive use”?

The biggest roadblock to qualifying for these deductions is that you must use a portion of your home exclusively and regularly for your business.

The law is clear and the IRS is serious about the exclusive-use requirement. Say you set aside a room in your home for a full-time business and you work in it ten hours a day, seven days a week. If you let your children use the office to do their homework, you violate the exclusive-use requirement and forfeit the chance for home office deductions.

The exclusive-use rule doesn’t mean:

You’re forbidden to make a personal phone call from the office.

You have to rush outside whenever a family member needs a moment of your time.

Although individual IRS auditors may be more or less strict on this point, some advisers say you meet the spirit of the exclusive-use test as long as personal activities invade the home office no more than they would be permitted to in an office building. The office can also be a section of a room if the division is clear — thanks to a partition, for example — and you can show that personal activities are excluded from the business section.

What is “regular use”?

There’s no specific definition of what constitutes regular use. Clearly, if you use an otherwise empty room only occasionally and its use is incidental to your business, you’d fail this test. If you work in the home office a few hours or so each day, however, you might pass. This test is applied to the facts and circumstances of each case the IRS challenges.

What does “principal place of business” mean?

In addition to passing the exclusive- and regular-use tests, your home office must be either the principal location of that business or a place for regular customer or client meetings.

If your home office is in a separate, unattached structure — a detached garage converted into an office, for example — you don’t have to meet the principal-place-of-business or the deal-with-clients test. As long as you pass the exclusive- and regular-use tests, you can qualify for home business write-offs.

What if your business has just one home office, but you do most of your work elsewhere?

Remember that the requirement is that your home office is your principal place of business, not your principal workplace. As long as you use the home office to conduct your administrative or management chores and you don’t make substantial use of any other fixed location to conduct those tasks, you can pass this test.

If you’re an employee of another company but also have your own part-time business based in your home, you can pass this test even if you spend much more time at the office where you work as an employee.

This rule makes it much easier to claim home office deductions for individuals who conduct most of their income-earning activities somewhere else (such as outside salespeople or tradespeople).

***

***

What qualifies as a business?

As with the regular-use test, whether your endeavors qualify as a business depends on the facts and circumstances. The more substantial the activities, in terms of time and effort invested and income generated, the more likely you are to pass the test.

Making money from your efforts is a prerequisite, but for purposes of this tax break, profit alone isn’t necessarily enough. If you use your den solely to take care of your personal investment portfolio, for example, you can’t claim home office deductions because your activities as an investor don’t qualify as a business.

Taxpayers who use a home office exclusively to manage rental properties may qualify for home office tax status but as property managers rather than investors.

What if I operate a child care or storage facility?

The exclusive-use test doesn’t apply if you use part of your house to:

Provide day care services for children, older adults or individuals with disabilities. If you care for children in your home between 7 a.m. and 6 p.m. each day, for example, you can use that part of the house for personal activities the rest of the time and still claim business deductions. To qualify for the tax break, your home care business must meet any applicable state and local licensing requirements.

Store product samples or inventory you sell in your business. Assume your home-based business is the retail sale of home-cleaning products and that you regularly use half of your basement to store inventory. Occasionally using that part of the basement to store personal items wouldn’t cancel your home office deduction. To qualify for this exception, your home must be the principal location of your business.

How do I calculate the home office tax deduction?

Your home office business deductions are based on either the percentage of your home used for the business or a simplified square footage calculation.

The most exact way to calculate the business percentage of your house is to measure the square footage devoted to your home office as a percentage of the total area of your home. If the office measures 150 square feet, for example, and the total area of the house is 1,200 square feet, your business percentage would be 12.5%.

An easier calculation is acceptable if the rooms in your home are all about the same size. In that case, you can figure out the business percentage by dividing the number of rooms used in your business by the total number of rooms in the house.

Special rules apply if you qualify for home office deductions under the day care exception to the exclusive-use test.

Your business-use percentage must be reduced because the space is available for personal use part of the time.

To do that, you compare the number of hours the child care business is operated, including preparation and cleanup time, to the total number of hours in the year (8,760).

Assume you use 40% of your house for a nursing daycare business that operates 12 hours a day, five days a week for 50 weeks of the year.

12 hours x 5 days x 50 weeks = 3,000 hours per year.

3,000 hours ÷ 8,760 total hours in the year = 0.34 (34%) of available hours.

34% of available hours x 40% of the house used for business = 13.6% business write-off percentage.

Simplified square footage method

Beginning with 2013 tax returns, the IRS began offering a simplified option for claiming the deduction. This new method uses a prescribed rate multiplied by the allowable square footage used in the home.

For 2021, the prescribed rate is $5 per square foot with a maximum of 300 square feet.

If the office measures 150 square feet, for example, then the deduction would be $750 (150 x $5).

The space must still be dedicated to business activities.

With either method, the qualification for the home office deduction is determined each year. Your eligibility may change from one year to the next. Finally, please note that only certain expenses such as rent, mortgage interest and property taxes qualify for the deduction, and the deduction is limited to $10,000.

Bonds: A bond selloff eased up a day ahead of an eagerly anticipated inflation report as investors absorbed another batch of earnings reports. The DJIA rose 300 points higher, but tech-related stocks lead the rally on Wall Street as bond yields stabilized and treasury yields paused their run higher ahead of the red-hot inflation report estimates.

Markets: The S&P 500 closed as a rally in Facebook-parent Meta helped the broader tech sector build on recent gains just as the S&P 500 rose 1.5%. The Dow Jones Industrial Average added 0.8%, or 306 points, the NASDAQ jumped 2.1%. And, Meta Platforms (NASDAQ: FB) jumped more than 5% as investors appeared to the buy the dip in the social media company, which hit fresh 52-week lows a day earlier. For the second-straight day, a rally in semiconductor stocks also pushed tech higher, with Nvidia (NASDAQ: NVDA) racking up a 5% gain as analysts downplayed the $1.25 billion hit to the company after its deal to acquire UK chip-maker ARM fell through.

Posted on February 9, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

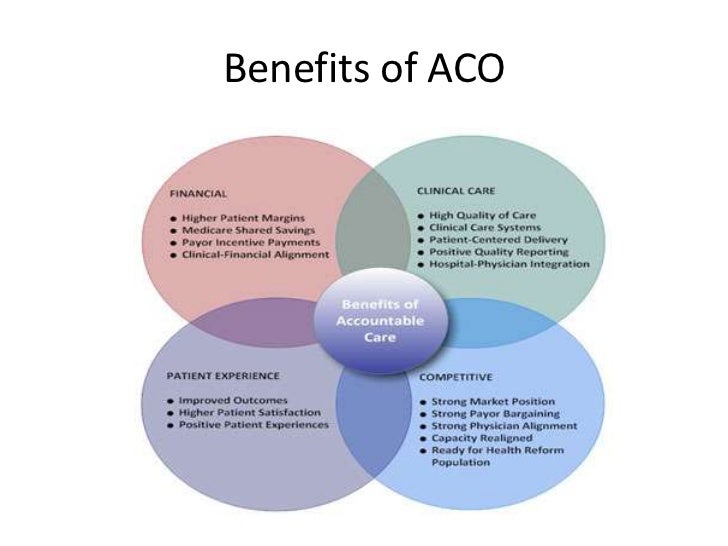

DEFINITION: An accountable care organization is a healthcare organization that ties provider reimbursements to quality metrics and reductions in the cost of care. ACOs in the United States are formed from a group of coordinated health-care practitioners. They use alternative payment models, normally, capitation.

Posted on February 9, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

By Staff Reporters

***

Markets: Solid corporate earnings boosted Wall Street and all the major indexes are now higher for the week. Pfizer dipped after posting lower-than-expected Q4 revenue but it did bring in $36.8 billion in sales in 2021.

Economy: The US trade deficit rose to a record $859 billion in 2021 (up 27% from the year prior) due to a surge in imports and higher prices for those imports.

Bitcoin: Authorities arrested a husband and wife accused of attempting to launder 119,754 stolen bitcoin—valued at $4.5 billion. Along with the arrest of the couple, Ilya Lichtenstein and Heather Morgan, the Justice Department announced that it had seized more than 94,000 of the allegedly stolen bitcoin, valued at $3.6 billion—the largest financial seizure in the agency’s history.

Apple: Announces Tap to Pay. In a bid to encourage more smartphone intimacy, the company is releasing a feature that allows customers to spend money by simply tapping an iPhone against a merchant’s iPhone—effectively turning the device into a checkout register.

The International Franchise Association (IFA) estimates that that about $1 trillion in sales, or 40% of all retail sales, were made through franchised establishment last year. On the positive side, franchises offer a branded practice concept with management training and access to proprietary methods, marketing and advertising campaigns and a host of support.

Moreover, there are franchises available for virtually every healthcare product or service, including: diet, weight loss and fitness; vein care and laser surgery; vitamins, nutriceuticals and pharmaceuticals; plastic and cosmetic surgery; dermatology, tanning and skin care; home healthcare and extended, etc. Some well know established healthcare and medical franchises are: Doctors Express, Being There Senior Care, Home Care Assistance, Personal Training Institute, Inches-A-Weigh, Remedy Intelligent Staffing, Visiting Angels, Unlimited MedSearch, prnYourHealth and Any Lab Test Now, etc.

On the downside, franchises incur high start-up costs, rules and obligations, payment of franchise percentages and many contractual obligations. Questions to consider when contemplating this business entity include:

Franchise stability, track record, licensing and costs.

Training, support and proximity of other franchises.

Independence, ownership laws, contracts and dispute resolutions,

Screening methods, market size and potential market share.

Replacement cost and transferability?

For more information on Uniform Franchise Offerings Circulars (UFOCs) contact www.FranChoice.com or:

Notes: U.S. value obtained from National Health Expenditure data. Data from Australia, Belgium, Canada, Japan and Switzerland are from 2019. Data for Australia, France, and Japan are estimated. Data for Austria, Canada, Germany, Netherlands, and Sweden are provisional. Health consumption does not include investments in structures, equipment, or research. Data for 2020 except as noted. Source: KFF analysis of National Health Expenditure (NHE) and OECD data, January 21, 2022

Posted on February 8, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

By Staff Reporters

***

Markets: Stocks were mixed but Bitcoin rallied for the fifth-straight day as investors may be warming up to riskier assets again. And, Nvidia overtook Meta to become the seventh-largest US company by market cap (it’s reportedly abandoning its $40 billion megadeal to acquire the chip designer Arm).

Housing:The median home-sale price reached a record high of $365,000 in January, according to Redfin. That’s a 16% jump from the previous January and a 28% increase from January 2019.

IRS: After receiving backlash from privacy advocates and bipartisan lawmakers, the IRS is abandoning its use of third-party facial recognition software ID.me.

GAS: Prices up 8% since last week and 12% more than a month ago.

Posted on February 7, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Markets: Major stock market indexes, the S&P 500 and NASDAQ posted their best week so far this year. And, potential buyers for Peloton include Amazon, Nike, Apple, Google, Netflix, Microsoft, or a private equity firm.

Inflation: The monthly inflation report will drop on Thursday, and consumer prices are projected to have jumped 0.5% from the previous month and 7.3% over the past year—the biggest increase since 1982.

Earnings: From Snap’s 59% gain to Meta’s 26% wipeout. the companies reporting this week—Pfizer, Disney, Coca-Cola, Pepsi, Twitter and Zillow know that any small stain on their financials could lead to a stock plunge.

Oil: The big news is that US oil prices topped $90 for the first time since 2014, despite attempts by the Biden administration to keep them down. Gas prices are back up to their highest levels in more than seven years.

Covid: The US death toll from Covid-19 has now surpassed 900,000. And, Omicron has gotten more people around the world sick at the same time than at any point since the 1918–1919 flu pandemic, the WSJ points out.

Economy: The jobs report stunned experts by adding 467,000 jobs last month, far more than expected and a sign of an extraordinarily strong labor market.

Posted on February 7, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

DEFINITION: A stock split or stock divide increases the number of shares in a company. For example, after a 2-for-1 split, each investor will own double the number of shares, and each share will be worth half as much. A stock split causes a decrease of market price of individual shares, but does not change the total market capitalization of the company: stock dilution does not occur.

Google parent company Alphabet said it would split its stock 20–1. That means in July 2022, Alphabet shareholders will receive 19 more shares for every one that they own. It doesn’t mean they’ll be 20x richer—the price of the stock they hold will drop a proportional amount. If the stock split were to happen now, Alphabet’s share price would fall from $2,865 to $143.

Why does it matter?

In many ways, it doesn’t. A stock split does not change the value of the company. It’s simply a way to increase the number of shares outstanding.

Think of it like slicing a pizza. At a share price of almost $3,000, Alphabet’s slices were a wide a monstrosity. With the stock split, it’s cutting company ownership into smaller portions. But, in the end, the pizza isn’t growing—there are just more slices to be shared.

So why do it? By making the slices of its company smaller, it hopes that more people will look at them and say, “Well I guess one couldn’t hurt.” Alphabet said the goal of the stock split is to attract more small-time investors who might have been intimidated by buying in at such a steep share price.

Only 27 other stocks in the S&P 500 have share prices above $500 besides Alphabet.

And, there’s evidence this bit of corporate inception can be effective. To see why, let’s look at what happened when two other tech giants, Tesla and Apple, split their stock recently.

When Apple split its stock 4–1 in July 2020, retail investors upped their purchases from $150 million per week to nearly $1 billion, according to Vanda Research.

When Tesla split its stock 5–1 in August 2020, retail investing jumped from $30–$40 million/week to $700 million.

There may be another play for Alphabet here—and that is to pad its resume for inclusion in the iconic Dow Jones Industrial Average. Because the Dow is weighted by share price (an antiquated system, to be sure), Alphabet at its current price would overwhelm all of the companies. It would become the Alphabet Industrial Average. At $247, it becomes a much more attractive candidate for the Dow.

Posted on February 6, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

Guide to Telehealth – Then, Now, Tomorrow? By Rebecca Chi

Healthcare providers have employed various forms of telehealth since long before the start of the coronavirus pandemic. Telehealth delivers knowledge and expertise to people and places that need it. A movement that largely began as a way to improve access to healthcare in rural communities saw explosive growth in 2020. Today, telehealth is in wide use and here to stay.

***

What is telehealth? The US Health Resources and Services Administration defines telehealth as any electronic information and telecommunications technology that is used to support and promote long-distance clinical healthcare, patient and professional health-related education, public health and health administration. Telehealth technologies benefit providers, healthcare organizations and patients.

The importance of telehealth The key to maintaining population health and lowering expenditures is delivering timely access to high-quality care.

The US is struggling to improve the quality of healthcare and make the needed shift to value-based models. Innovative telehealth solutions that addressed our country’s worsening healthcare access problem reached the point of widespread adoption in 2020, when the pandemic pushed the healthcare system to its limits.

Telehealth increases convenience of care and access while decreasing costs and maximizing physician time. Providers, payers and employers are increasingly adopting various and connected types of telehealth solutions to improve healthcare operations and patient outcomes. Patients embrace the convenience, safety, accessibility and flexibility of telehealth options.

Posted on February 6, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

****

***

It’s February – American Heart Month – a time when the nation spotlights heart disease, the No. 1 killer of Americans.

President Lyndon B. Johnson, among the millions of people in the country who’d had heart attacks, issued the first proclamation in 1964. Since then, U.S. presidents have annually declared February American Heart Month.

Throughout the month, the American Heart Association’s “Heart to Heart: Why Losing One Woman Is Too Many” campaign will raise awareness about how 1 in 3 women are diagnosed with heart disease annually.

The first Friday of American Heart Month, Feb. 5, is also National Wear Red Day as part of the AHA’s Go Red for Women initiative. Coast to coast, landmarks, news anchors and neighborhoods go red to raise awareness and support for the fight against heart disease. For more information on the event and other activities during the month, visit goredforwomen.org.

This year, the federally designated event is even more important due to the impact of the coronavirus on the public’s heart health, including potential harmful effects on the heart and vascular system, according to recent research.

Also, during the COVID-19 pandemic, many people have delayed or avoided going to hospitals for heart attacks and strokes – netting poorer outcomes and prompting the AHA to create “Don’t Die of Doubt,” a national awareness campaign that reminds people that hospitals are the safest place to go when you have symptoms.

And while in lock-down, more people have engaged in unhealthy lifestyle behaviors, such as eating poorly, drinking more alcohol and limiting physical activity, that can contribute to heart disease.

Meanwhile, heart disease continues to be the greatest health threat to Americans and is still the leading cause of death worldwide, according to the AHA’s Heart Disease and Stroke Statistics – 2021 Update.

The update, published in the association’s flagship journal Circulation, reports that nearly 18.6 million people across the globe died of cardiovascular disease in 2019, the latest year for which worldwide statistics are calculated. That’s a 17.1% increase over the past decade. And 523.2 million cases of cardiovascular disease were reported in 2019, a 26.6% increase over 2010.

During American Heart Month, the AHA and other organizations reinforce the importance of heart health, the need for more research and efforts to ensure that millions of people live longer and healthier.

In most cases, heart disease is preventable when people adopt a healthy lifestyle, which includes not smoking, maintaining a healthy weight, controlling blood sugar and cholesterol, treating high blood pressure, getting at least 150 minutes of moderate-intensity physical activity a week and getting regular checkups.

Posted on February 5, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

****

***

The most recent numbers show that more than 45 million of us itemized deductions on our 1040s—claiming $1.2 trillion dollars’ worth of tax deductions. That’s right: $1,200,000,000,000! That same year, taxpayers who claimed the standard deduction accounted for $747 billion. Some of those who took the easy way out probably shortchanged themselves. (If you turned age 65 in 2021 or earlier, remember that you deserve a bigger standard deduction than younger folks.)

Here are our 10 most overlooked tax deductions. Claim them if you deserve them, and keep more money in your pocket. Good advice for all physicians, nurse and medical professionals, too.

1. State sales taxes

This write-off makes sense primarily for those who live in states that do not impose an income tax. Especially Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming. Here’s why this is a factor. You must choose between deducting state and local income taxes or state and local sales taxes. For most citizens of income-taxing-states, the state and local income tax deduction is usually the better deal.

For those of you in an income-tax free state, there are two ways to claim the sales tax deduction on your tax return. One, you can use the IRS tables provided for your state to determine what you can deduct. In addition, if you purchased a vehicle, boat, airplane, home or did major home renovations, you may be able to add the state sales tax you paid on these items to the amount shown in the IRS tables up to the limit for your state. Or two, you can you can keep track of all of the sales tax you paid throughout the year and use that.

The best way to see what you can deduct is to use the IRS’s Sales Tax Calculator for this. Keep in mind, the total of your itemized deductions for all of your state and local taxes is limited to $10,000 per year.

2. Reinvested dividends

This isn’t really a tax deduction, but it is a subtraction that can save you a lot of money. And it’s one that many taxpayers miss. If, like most investors, you have mutual fund dividends automatically invested in extra shares, remember that each reinvestment increases your “tax basis” in the stock or mutual fund. That, in turn, reduces the amount of taxable capital gain (or increases the tax-saving loss) when you sell your shares.

Forgetting to include the reinvested dividends in your cost basis—which you subtract from the proceeds of sale to determine your gain—means overpaying your taxes.

3. Out-of-pocket charitable contributions

It’s hard to overlook the big charitable gifts you made during the year by check or payroll deduction. But the little things add up, too, and you can write off out-of-pocket costs you incur while doing good deeds. Ingredients for casseroles you regularly prepare for a qualified nonprofit organization’s soup kitchen, for example, or the cost of stamps you buy for your school’s fundraiser count as a charitable contribution. If you drove your car for charity in 2021, remember to deduct 14 cents per mile.

4. Student loan interest paid by you or someone else

In the past, if parents or someone else paid back a medical school or other loan incurred by a student, no one got a tax break. To get a deduction, the law said that you had to be both liable for the debt and actually pay it yourself. But now there’s an exception. You may know that you might be eligible to take a deduction but even if someone else pays back the loan, the IRS treats it as though they gave you the money, and you then paid the debt. So, a student who’s not claimed as a dependent can qualify to deduct up to $2,500 of student loan interest paid by you or by someone else.

5. Moving expenses

While most taxpayers lost the ability to deduct moving expenses beginning in 2018, one main group of people who can still claim their moving expenses to the IRS. Who are they? Military personnel. If you’re an active duty military member who is relocating, you can still deduct these expenses —if you don’t receive reimbursement from the government for the move.

Also, as long as the move is permanent —and your relocation was ordered by the military — you don’t have to pay tax on qualified moving expense reimbursements. So start getting those receipts out now – because you can claim travel and lodging expenses for you and your family, moving household goods, and the costs for shipping your cars and your beloved pets! And that’s good news for the men and women we thank for bravely serving our country.

6. Child and Dependent Care Tax Credit

A tax credit is so much better than a tax deduction—it reduces your tax bill dollar for dollar. So missing one is even more painful than missing a deduction that simply reduces the amount of income that’s subject to tax.

But it’s easy to overlook the Child and Dependent Care Credit if you pay your child care bills through a reimbursement account at work. For 2020, the law allows you to run up to $5,000 of such expenses through a tax-favored reimbursement account at work. Up to $6,000 in care expenses can qualify for the credit, but the $5,000 from a tax favored account can’t be used. So if you run the maximum $5,000 through a plan at work but spend more for work-related child care, you can claim the credit on up to an extra $1,000. That would cut your tax bill by at least $200 using the minimum 20 percent of the expenses. The credit percentage goes up for lower income households.

However, there are big changes for 2021, The American Rescue Plan signed into law on March 11, 2021 brought significant changes to the amount and way that the child and dependent care tax credit can be claimed only for tax year 2021. The new law not only increases the credit, but also the amount of taxpayers that will benefit from the credit’s highest rate and it also makes it fully refundable. This means that, unlike previous years, you can still get the credit even if you don’t owe taxes. Changes to the Child and Dependent Care Credit that apply only for tax year 2021 (the taxes you file in 2022) include:

The highest credit percentage increased from 35% to 50% of qualifying expenses

Qualifying child and dependent care expenses increased from $3,000 to $8,000 for one qualifying person and from $6,000 to $16,000 for two or more qualifying individuals

The adjusted gross income (AGI) level at which the credit percentage is reduced is increased from $15,000 to $125,000

For example, prior to the 2021 tax year, a taxpayer with one qualifying person, $3,000 in qualifying expenses and an AGI of $60,000 would qualify for a nonrefundable credit of approximately $600 (20% x $3,000). By contrast, under the new law for tax year 2021 only, a taxpayer with the same circumstances can potentially claim a refundable credit of approximately $1,500 (50% x $3,000).

Also for tax year 2021, the maximum amount that can be contributed to a dependent care flexible spending account and the amount of tax-free employer-provided dependent care benefits is increased from $5,000 to $10,500.

7. Earned Income Tax Credit (EITC)

Millions of lower-income people take this credit every year. However, 25% of taxpayers who are eligible for the Earned Income Tax Credit fail to claim it, according to the IRS. Some people miss out on the credit because the rules can be complicated. Others simply aren’t aware that they qualify.

The EITC is a refundable tax credit—not a deduction— with maximum amounts for different filing statuses ranging from $1,502 to $6,728 for 2021. The credit is designed to supplement wages for low-to-moderate income workers. But the credit doesn’t just apply to lower income people. Tens of millions of individuals and families previously classified as “middle class”—including many medical colleagues and white-collar workers—are now considered “low income” because they:

lost a job

took a pay cut

or worked fewer hours during the year

The exact refund you receive depends on your income, marital status and family size. To get a refund from the EITC you must file a tax return, even if you don’t owe any taxes. Moreover, if you were eligible to claim the credit in the past but didn’t, you can file any time during the year to claim an EITC refund for up to three previous tax years.

8. State tax you paid last spring

Did you owe taxes when you filed your 2020 state tax return in 2021? Then remember to include that amount with your state tax itemized deduction on your 2021 return, along with state income taxes withheld from your paychecks or paid via quarterly estimated payments. Beginning in 2018, the deduction for state and local taxes is limited to a maximum of $10,000 per year.

9. Refinancing mortgage points

When you buy a house, you often get to deduct points paid to obtain your mortgage all at one time. When you refinance a mortgage, however, you have to deduct the points over the life of the loan. That means you can deduct 1/30th of the points a year if it’s a 30-year mortgage—that’s $33 a year for each $1,000 of points you paid. Doesn’t seem like much, but why throw it away?

Also, in the year you pay off the loan—because you sell the house or refinance again—you get to deduct all the points not yet deducted, unless you refinance with the same lender.

10. Jury pay paid to employer

Some employers continue to pay employees’ full salary while they are doing their civic duty, but ask that they turn over their jury fees to the company. The only problem is that the IRS demands that you report those fees as taxable income. If you give the money to your employer you have a right to deduct the amount so you aren’t taxed on money that simply passes through your hands.

Posted on February 5, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Markets: The stock market was downright crazy last week. A day after Meta [Facebook] suffered the worst one-day drop in value in US stock market history (losing more than $230 billion), Amazon set the record for the biggest one-day gain on Wall Street (adding $191 billion). As for the major indexes, the S&P 500 and NASDAQ posted their best week so far this year.

Economy: The jobs report stunned experts by adding 467,000 jobs last month, far more than expected and a sign of an extraordinarily strong labor market. In even better news, the government said it had under-counted the number of jobs added in November and December by more than 700,000.

Posted on February 5, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

An interval fund is a type of closed-end fund with shares that do not trade on the secondary market. Instead, the fund periodically offers to buy back a percentage of outstanding shares at net asset value (NAV). The rules for interval funds, along with the types of assets held, make this investment largely illiquid compared with other funds.

Posted on February 4, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

A recent Johns Hopkins analysis of 676 U.S. health systems found that these 4 health systems contributed to healthcare overuse the most:

• St. Dominic Health Services in Jackson, Mississippi • USMD Health System in Irving, Texas • Community Medical Centers in Clovis, California • Care New England Health System in Providence, Rhode Island

Posted on February 4, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

By Staff Reporters

***

In a spin-off, a company would distribute a number of shares to its investors. Each investor would receive shares of the new company for every share they owned.

In a split-off, investors would be allowed to directly trade none, all, or part of their owned shares. The exchange would likely retire outstanding shares for remaining investors. But investors must be convinced to voluntarily make that trade, so “sweeteners” are often included.

An equity carve-out, also known as a split-off IPO or a partial spin-off, is a type of corporate reorganization, in which a company creates a new subsidiary and subsequently IPOs it, while retaining management control

But, Snap Inc. and Pinterest Inc. came roaring back after upbeat results eased fears that a slowdown at rival Facebook reflected an industry-wide social media slump.

IRS: Regardless of the stock markets, the IRS just assembled a ‘surge team’ of 1,200 staffers to tackle filing backlogs and the busy tax season this year.

COVID-19: Medicare to start paying for at-home tests.

JOBS: The January jobs report due this morning will have several Covid issues that will make the numbers extremely confusing to interpret (folks out sick with Omicron, for example).

Posted on February 3, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

Decentralized Autonomous Organizations in Health Care?

By Staff Reporters

****

DEFINITION: A decentralized autonomous organization (DAO), sometimes called a decentralized autonomous corporation (DAC), is an organization represented by rules encoded as a computer program that is transparent, controlled by the organization members and not influenced by a central government. A DAO’s financial transaction record and program rules are maintained on a blockchain.

Posted on February 3, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

What it is?

By Staff Reporters

***

Some doctors and other taxpayers may receive IRS Letter 6475, which references the third Economic Impact Payment. While most recipients eligible for this stimulus check have already received their money in full, some taxpayers might now be eligible or entitled to more money based on their 2021 tax information by claiming a Recovery Rebate Credit on their upcoming tax return. Those people will need this form to confirm how much of the third stimulus check they already received from the government, if they received any at all. Learn more here.

Posted on February 3, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

This is just the fourth National Women Physicians Day, on February 3rd . The event celebrates Elizabeth Blackwell’s birthday; she was the first female medical doctor in the U.S. It’s a time to honor women doctors across the country, and the progress they’ve made since Blackwell’s time.

***

Nationally, there are still fewer female doctors than male doctors, but the progress is steady. In 2017, for the first time in history, women made up more than half of all those in medical schools.