BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on March 8, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

BY JONATHAN MASER.N.

***

***

Being an entrepreneur is not necessarily easy, and many people that try to become entrepreneurs wind up failing. It’s important to recognize the risk of failure before you decide to walk down this path. Being an entrepreneur is very rewarding, and you can find success if you can do things right.

Keep reading to learn about common entrepreneurial mistakes that you can avoid to give yourself a better chance of realizing your entrepreneurial goals.

Posted on March 8, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

By Staff Reporters

***

***

Stocks: Fell sharply as the economic fallout of Russia’s war in Ukraine rattled investors. The Dow Jones Industrial Average fell almost 800 points Monday to close with a loss of 2.4 percent. The NASDAQ plunged 3.6 percent lower and the S&P 500 index closed with a loss of 3 percent. Companies in the finance, travel, entertainment, retail and construction industries fell sharply as skyrocketing oil prices raised fears of an economic slowdown, while energy companies rallied on the prospect of higher prices. Stocks have fallen for weeks amid rising concern about inflation and the economic blow-back of the invasion of Ukraine. The Dow is down 10.3 percent, the S&P is down 12.4 percent, and the NASDAQ is down 19 percent since the start of 2022.

Oil & Wheat: Prices for oil, natural gas and wheat have also risen dramatically after the U.S. and allies imposed unprecedented sanctions on the Russian economy, which could limit their access to key Russian exports. Oil hit $120 barrel. But, some investors are betting on oil to surge even more dramatically, as bullish bets on crude futures increase. Since Friday, $150-a-barrel call options for Brent contracts in June have doubled. Amid new potential sanctions on Russia’s energy sector, oil briefly surpassed $130 a barrel overnight.

Economy: Economists warned that higher energy and food prices will likely slow growth in the U.S. through the first half of the year and fuel higher inflation. Prices rose 7.5 percent over the 12 months ending in January, according to US Labor Department data, the highest rate in more than 40 years.

Posted on March 8, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

What It Is … and Why?

[By Staff Reporters]

History

IWD is now an official holiday in Afghanistan, Armenia, Azerbaijan, Belarus, Burkina Faso, Cambodia, China (for women only), Cuba, Georgia, Guinea-Bissau, Eritrea, Kazakhstan, Kyrgyzstan, Laos, Madagascar (for women only), Moldova, Mongolia, Montenegro, Nepal (for women only), Russia, Tajikistan, Turkmenistan, Uganda, Ukraine, Uzbekistan, Vietnam and Zambia.

The tradition sees men honoring their mothers, wives, girlfriends, colleagues, etc with flowers and small gifts.

In some countries IWD has the equivalent status of Mother’s Day where children give small presents to their mothers and grandmothers.

The Millennium

The new millennium has witnessed a significant change and attitudinal shift in both women’s and society’s thoughts about women’s equality and emancipation.

Many from a younger generation feel that ‘all the battles have been won for women’ while many feminists from the 1970’s know only too well the longevity and ingrained complexity of patriarchy. With more women in the boardroom, greater equality in legislative rights, and an increased critical mass of women’s visibility as impressive role models in every aspect of life, one could think that women have gained true equality.

The unfortunate fact is that women are still not paid equally to that of their male counterparts, women still are not present in equal numbers in business or politics, and globally women’s education, health and the violence against them is worse than that of men.

Celebrating the Positives

However, great improvements have been made. We do have female astronauts and prime ministers, school girls are welcomed into university, women can work and have a family, women have real choices. And so, the tone and nature of IWD has, for the past few years, moved from being a reminder about the negatives to a celebration of the positives.

Annually on 8th March, thousands of events are held throughout the world to inspire women and celebrate achievements. A global web of rich and diverse local activity connects women from all around the world ranging from political rallies, business conferences, government activities and networking events through to local women’s craft markets, theatric performances, fashion parades and more.

Global Reach

Many global corporations have also started to more actively support IWD by running their own internal events and through supporting external ones. For example, on 8 March search engine and media giant Google some years even changes its logo on its global search pages. Year on year IWD is certainly increasing in status.

The United States even designates the whole month of March as ‘Women’s History Month’.

Assessment

So make a difference, think globally and act locally! Make everyday International Women’s Day. Do your bit to ensure that the future for girls is bright, equal, safe and rewarding.

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on March 7, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

2. Long-term time horizon (both analytical and expectation to hold)

EDITOR’S NOTE: Although it has been some time since speaking live with busy colleague Vitaliy Katsenelson CFA, I review his internet material frequently and appreciate this ME-P series contribution. I encourage all ME-P readers to do the same and consider his value investing insights carefully.

By Vitaliy Katsenelson, CFA

***

***

The Six Commandments of Value Investing ***

2. Long-term time horizon (both analytical and expectation to hold) A long-term time horizon is extremely important for value investors for several reasons: First, it is impossible predict how a stock will be priced in the short run. Short-term stock behavior is random, and thus its forecasting (at least using tools available to investors) cannot be turned into a repeatable process.

Second, having a longer time horizon than Wall Street is a very important competitive advantage. The Street’s time horizon is very short – measured in months, maybe quarters, but rarely in years.

Money flows into mutual funds and hedge funds are driven by recent performance, so Wall Street is obsessed with the short term. This creates time arbitrage. Stocks get punished because their immediate future may look unattractive, but if you look at them as businesses, that short-term performance is just a pimple on your long-term timeline.

So, how do we embed a long-term time horizon into our process?

First, we always look at earnings and cash flows at least three (often five) years out. This forces us to look at the company’s normalized earnings power and ignores the short term. All our models focus on what the company will be worth based on its earnings power in three to five years. Then we discount (bring that future value forward to today at an 18%-40% discount rate, depending on the company’s quality) to see what we want to pay for this company today. Looking at the business at least three to five years out has a very important side effect: It adds “growth” to the portfolio from earnings and dividends. Stock returns come from three sources: price-to-earnings (P/E) expansion, earnings growth, and dividends.

P/E expansion is finite – it’s a one-time shot in the arm. Let’s say a stock’s P/E goes from an undervalued 12 to a fairly valued 15 – a 25% return. If this company doesn’t grow earnings and/or pay dividends, that 25% will be our total return. The risk of owning this type of “one-shot” stock is that without earnings growth or dividends, time is not on your side – you don’t get paid to wait.

If your time horizon is three years, that 25% return gets truncated to an annual return of only 8% a year. But if this company, in addition to trading at a depressed P/E, pays a 3% dividend and grows earnings 7% a year, that is an additional, repeatable 10% return a year. This elongation of the time horizon embeds growth in our portfolio and also forces us to demand a much higher discount for stocks that don’t pay dividends and don’t grow their earnings.

Posted on March 7, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

Markets: The war in Ukraine and upcoming Federal Reserve [FOMC] rate hikes took their toll on stocks—the DJIA took another licking for its fourth straight losing week and travel stocks were especially bludgeoned.

Energy: Due to the rapid run-up in oil prices, average US gas prices surged to $3.84 a gallon on Friday. At 11 cents higher than Thursday’s levels, it’s the fastest price increase since Hurricane Katrina in 2005.

MARKETS

NASDAQ:13,313.44-1.66%

S&P: 4,328.87-0.79%

DJIA: 33,614.80-0.53%

10-Year 1.732%-11.2 bps

Bitcoin: $38,879.81-8.69%

Delta: $34.52-5.58%

***

FUTURES: Dow futures lost 400 points, or 1.19%, while S&P 500 futures and NASDAQ 100 futures slid 1.5% and 1.91%, respectively.

OIL: West Texas Intermediate crude futures, the U.S. oil benchmark, traded as much as 10%, hitting $130 per barrel at one point before pulling back slightly. The international benchmark, Brent crude, traded 9% higher to $128.60, also the highest prices seen since 2008.

Posted on March 6, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

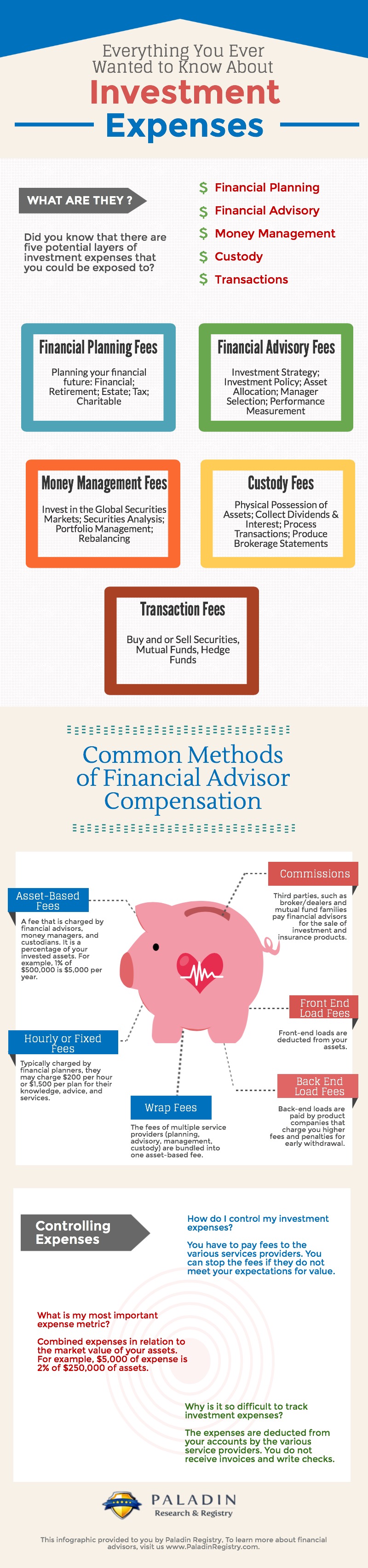

Peeling Back the Layers of Fees

By PALADIN [Research & Registry]

Channel Surfing the ME-P

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on March 6, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

1. A stock is partial ownership of a business

***

By Vitaliy N. Katsenelson CFA

EDITOR’S NOTE: Although it has been some time since speaking live with busy colleague Vitaliy Katsenelson CFA, I review his internet material frequently and appreciate this ME-P series contribution. I encourage all ME-P readers to do the same and consider his value investing insights carefully.

***

The Six Commandments of Value Investing

Introduction

I wrote the core of this chapter in preparation for a speech I gave at an investment conference. In my speech, I wanted to show how at my firm, we took the Six Commandments of Value Investing and embedded them in our investment operating system.

Since I was speaking to fellow value investors, this speech was written not to promote my firm but to educate. I was going to rewrite the speech for this chapter and make a bit less about us and more about you –but each attempt resulted in a dull chapter. So here is a much extended version of my original speech.

The Six Commandments

These are the Six Commandments of Value Investing. I don’t expect any value investors reading this to be surprised by any one of them. They were brought down from the mountain by Ben Graham in his book Security Analysis.

1) A stock is fractional ownership of a business (not trading sardines). 2) Long-term time horizon (both analytical and expectation to hold) 3) Mr. Market is there to serve us (know who’s the boss). 4) Margin of safety – leave room in your buy price for being wrong. 5) Risk is permanent loss of capital (not volatility). 6) In the long run stocks revert to their fair value.

These commandments are very important and they sound great, but in the chaos of our daily lives it is so easy for them to turn into empty slogans.

A slogan without execution is a lie. For these “slogans” not to be lies, we need to deeply embed them in our investment operating system – our analytical framework and our daily routines – and act on them.

The focus of this chapter goes far beyond explaining what these commandments are: My goal is to give you a practical perspective and to show you how we embed the Six Commandments in our investment operating system at my firm.

1. A stock is partial ownership of a business

The US and most foreign markets we invest in are very liquid. We can sell any stock in our portfolios with ease – a few clicks and a few cents per share commission and it’s gone. This instant liquidity, though it can be tremendously beneficial (we wish selling a house were that easy, fast, and cheap), can also have harmful unintended consequences: It tends to shrink the investor’s analytical time horizon and often transforms investors into pseudo-investors.

For true traders, stocks are not businesses but trading widgets. Pork bellies, orange futures, stocks are all the same to them. Traders try to find some kind of order or a pattern in the hourly and daily chaos (randomness) of financial markets. As an investor, I cannot relate to traders –not only do we not belong to the same religion, we live in very different universes. Over the years I’ve met many traders, and I count a few as my dear friends. None of them confuse what they do with investing. In fact, traders are very explicit that their rules of engagement with stocks are very different from those of investors.

I have little insight to share with traders in these pages. My message is really to market participants who on the surface look at stocks as if they were investments but who have been morphed by the allure of the market’s instant liquidity into pseudo-investors. They are not quite traders – because they don’t use traders’ tools and are not trying to find order in the daily noise – but they aren’t investors, either, because their time horizon has been shrunk and their analysis deformed by market liquidity.

The best way to contrast the investor with the pseudo-investor is by explaining what an investor is. A true investor would do the same analysis of a public company that he would do for a private one. He’d analyze the company’s business, guestimate earnings power and cash flows. Assess its moat – the ability to protect cash flows from competition. Try to look “around the corner” to various risks. Then figure out what the business is worth and decide what price he’d want to pay for it (your required discount to what the business is worth). For an investor, the analysis would be the same if his $100,000 was buying 20% of a private business or 0.002% of a public one. This is how your rational uncle would analyze a business – your Warren Buffett or Ben Graham.

How do we maintain this rational attitude and prevent the stock market from turning us into pseudo-investors? Very simple. We start by asking, “Would we want to own this business if the stock market was closed for 10 years?” (Thank you, Warren Buffett). This simple question changes how we look at stocks.

Now, the immediate liquidity that is so alluring in a stock, and that turns investors into pseudo-investors, is gone from our analysis. Suddenly, quality – valuation, cash flows, competitive advantage, return on capital, balance sheet, management – has a much different, more complete meaning.

Posted on March 6, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

Understanding the New-Wave Social Media that Fuels Them

[By Staff Writers]

All medical professionals, and some FAs and behavioral economists, realize that Maslow’s hierarchy of needs is often portrayed in the shape of a pyramid, with the largest and most fundamental levels of needs at the bottom, and the need for self-actualization at the top.

So, this infographic takes Maslow’s theory and looks at the electronic social media tools that fulfill these needs.

Yet, another new-paradigm assessment of social media for doctors, financial advisors … and us all.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on March 6, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

Gas prices just keep climbing higher, and a gallon of regular gas in the U.S. will likely average $4 before the end of the weekend. The national average for a gallon of regular gasoline rose to $3.92 Saturday, up from $3.84 on Friday, according to AAA.

Prices had risen 11 cents Friday, up from $3.73 on Thursday. That followed an 11-cent increase between Monday and Thursday. Prices averaged $3.60 a week ago and $3.44 a month ago. And, this week’s increases suggest it is likely the national average “could creep over $4/gallon tomorrow” .

Moreover, don’t look for gas prices to hold at $4 nationally. Many places are seeing gas of $5 or more already. The average price per gallon in California has surpassed $5 at $5.18, the most expensive market in the U.S., the AAA said.

Several other states have already surpassed the average $4 per gallon, according to AAA:

Last week, ProPublica published the story of how PayPal co-founder and tech investor Peter Thiel was able to turn a Roth IRA initially worth around $2,000 into a jaw-dropping $5 billion tax-free retirement stash in just 20 years.

The story is even more remarkable because Congress created the Roth IRA in 1997 to encourage middle-class Americans to save for their golden years. Most Americans have struggled to do even that; the average account was worth about $39,000 in 2018. But Thiel and other billionaires have managed to turn their mundane Roths into giant onshore tax shelters.

Thiel was able to launch his Roth into the stratosphere through a complicated strategy involving the purchase of nonpublic stock at bargain prices — the kind of deal most people can’t access. Experts say it risked running afoul of rules designed to prevent IRAs from becoming illegal tax shelters. (Thiel’s spokesman didn’t respond to questions.)

Other ultrawealthy Americans have used different means to build Roths worth tens or hundreds of millions of dollars. Senate Finance Chairman Ron Wyden is now looking at how to end the use of the Roth as “yet another tax dodge that allows mega millionaires and billionaires to avoid paying taxes.”

How are they able to do it while you can’t? Check out our explainer of one way the Roth works for the ultrawealthy and not for you.

Posted on March 4, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Stocks fell and oil prices eased back after another bumpy day of trading on Wall Street as markets remained anxious about the broader impact of Russia’s invasion of Ukraine.

Okta shares were down 8.06% while Snowflake plummeted 15.37%.

***

INTEL: Intel stock (NASDAQ: INTC) fell 2.5% after Morgan Stanley and Bank of America Securities cut their targets to $47, according to StreetInsider. The stock fell to a low of $47.62, not far from its 52-week low of $43.63. Morgan Stanley (NYSE:MS) analyst Joseph Moore also downgraded the stock to underweight from equal weight while BofA’s Vivek Arya maintained his under perform rating.

INDEXES: Major indexes veered up and down for much of the day before a late-day slide pushed them into the red. The S&P 500 shed a 0.7% gain to close 0.5% lower, while the Dow Jones Industrial Average fell 0.3%. The NASDAQ composite fell 1.6%, weighed down by technology stocks, which accounted for a big share of the market’s decline.

The Dow is down 0.9% for the week, on track for its fourth negative week in a row. The S&P 500 is down about 0.5% for the week, while the NASDAQ Composite is down more than 1%.

BUYBACKS: In the third quarter of 2021, Apple, Inc. (NASDAQ: AAPL) led all S&P 500 companies with $20.4 billion in buybacks. Alphabet, Inc. (NASDAQ: GOOG) (NASDAQ: GOOGL) was a distant second with $15 billion in buybacks, followed by Meta Platforms Inc (NASDAQ: FB) with $12.6 billion.

Over the last decade, no company has come close to Apple in the buyback department. Apple has bought back $487.6 billion in stock since 2012. Microsoft Corporation (NASDAQ: MSFT) is a very distant second with $147.1 billion in buybacks, followed by JPMorgan Chase & Co (NYSE: JPM) with $146.2 billion.

Why Buybacks Matter: It should come as no surprise to investors that all three of the stocks that have been most aggressive in buying back shares over the last 10 years have outperformed the SPDR S&P 500 ETF (NYSE: SPY) total return by a wide margin in that period.

BONDS: Bond yields were mostly steady. The yield on the 10-year Treasury slipped to 1.85% from 1.86% late Wednesday.

QPADEFINITION: The qualifying payment amount is generally the median of contracted rates for a specific service in the same geographic region within the same insurance market as of January 31, 2019. The rate will be adjusted per the Consumer Price Index for All Urban Consumers (CPI-U).

When trying to decide whether to buy a used car or a new one, it’s typically financially wiser to buy used. But if you want to buy new, you should plan to drive the car for 10 years or more.

Better yet – do not buy a new vehicle.

***

The 20/4/10 rule for buying a vehicle

If you have to borrow when buying a car, to avoid spending more than you can afford you should put down at least 20%, keep the loan limited to no more than four years (to avoid interest), and spend no more than 10% of your gross income on transportation costs (which includes the car payment, parking, gas, and insurance).

Posted on March 3, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Economy: Federal Reserve Chair Jerome Powell told Congress that “it’s too soon to say” how the war in Ukraine will affect the central bank’s plans, but for now it’s not enough to derail the FOMC from hiking interest rates later this month.

Markets: Stocks rose across the board with strong corporate fundamentals outshining geopolitical worries…at least for a day. Intel had a strong showing after its CEO got a shout-out in the State of the Union address (to be fair, we have no idea if those two things are related).

Posted on March 1, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

DARK : With Russia’s stock market closed, U.S. exchange-traded funds are signaling the scale of the rout facing the nation’s equity markets. The Bank of Russia halted trading in Moscow on Monday, one of several measures unleashed in a bid to shield the nation’s economy from sweeping SWIFT and other sanctions.

ETFs: According to Bloomberg, the VanEck Russia ETF (ticker RSX) and the iShares MSCI Russia Capped ETF (ERUS) plunged 30% and 27%, which was likely a create-to-lend activity where new shares are created for short sellers to borrow and bet against. That turned the two ETFs, which primarily track Russian energy stocks, into useful price-discovery tools for traders seeking to navigate the geopolitical turmoil caused by Russia’s invasion of Ukraine. “ETFs are suppose to be index trackers, but when that process breaks down, they take on the role of price-discovery vehicles — and it’s impressive how accurate they have been.”

Housing: Amounted to about 4% for the 12 months ending in January. Comparatively, Zillow reported that home values had risen by nearly 20% over that same period of time, while rents had increased by nearly 15%.

DomesticMarkets: Stocks were a mixed bag, but the S&P still suffered back-to-back losing months.

Posted on March 1, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

Dr. Eric Bricker Explains How Medicare Can Take Money Back from Hospitals if itWants. If the Hospital Thinks Medicare is Being Unfair, the Appeals Process Takes 3 Years!

Book Dr. David E. Marcinko MBA MBBSfor your Next Medical, Pharma or Financial Services Seminar orPersonal and Corporate Coaching Sessions

Dr. Marcinko enjoys personal coaching and public speaking and gives as many talks each year as possible, at a variety of medical society and financial services conferences around the country and world.

These include lectures and visiting professorships at major academic centers, keynote lectures for hospitals, economic seminars and health systems, endnote lectures at city and statewide financial coalitions, and annual engagements for a variety of internal and external yearly meetings.

Posted on February 28, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

****

IRS: The IRS sent out a notice on February 23rd, warning taxpayers about a price hike coming in the next few months. The tax agency said that interest rates will increase for the calendar quarter starting April 1st, 2022. You can accrue interest on two types of payments: over-payment or underpayment. So starting in April, over-payments will have an interest rate of 4 percent, except for corporations which will earn a 3 percent rate and a 1.5 percent rate for the portion of a corporate over-payment that exceeds $10,000. In terms of underpayments, the interest rate will increase to 4 percent overall and 6 percent for large corporate underpayments.

“Under the Internal Revenue Code, the rate of interest is determined on a quarterly basis,” the IRS website explained. The tax agency did not change interest rates in this last quarter, which began Jan. 1, 2022. Before they get changed in April, the rates are currently 3 percent for general over-payments and 2 percent for corporation over-payments, with a 0.5 percent rate for the portion of a corporate over-payment exceeding $10,000. The underpayment interest is 3 percent right now, expect for large corporations which have a 5 percent rate.

***

***

CURRENCY INFLATION: Inflation may occur when the Federal Reserve, or another central bank, adds fiat currency into circulation at a rate that exceeds that of the economy’s growth rate. That creates a situation in which there are more dollars bidding on fewer goods and services. The result is that goods and services cost more. One reason that inflation has been a constant in the US since 1933 is that the FOMC has continually increased the money supply. In response to the 2008 financial crisis, the Fed dropped its lending rate close to zero as a way to inject more liquidity into the economy, which led to increased inflation but not hyperinflation. While those increases have usually moved in step with growth, that hasn’t always been the case.

And so, in response to the COVID-19 pandemic and subsequent lock-downs, the Federal Reserve released the equivalent of $3.8 trillion in new liquidity in 2020. That amount was equal to roughly 20% of the dollars previously in circulation. And it is one reason why many investors were watching the CPI closely in 2021.

EARNING REPORTS:

Monday: India GDP data; Earnings from Lordstown Motors, Groupon, HP, SmileDirectClub and Zoom Video

Tuesday: US and China manufacturing data; Earnings from AutoZone, Baidu, Domino’s Pizza, Hostess Brands, J.M. Smucker, Kohl’s, Target, AMC Entertainment and Salesforce

Wednesday: European inflation data; Earnings from Abercrombie & Fitch, Dine Brands, Dollar Tree, Snowflake and Victoria’s Secret

Thursday: ISM Non-Manufacturing Index; Earnings from Best Buy, Weibo, Costco and Gap

Friday: US jobs report

10-Year: Treasuries rallied to 1.902%.

Oil: The rise in oil prices is spilling over at the gas pump: The average gas price in the US has jumped 10 cents, to $3.64/gallon, in the past two weeks.

Partial SWIFT ban: Western governments put aside their hesitations and proposed banning some Russian lenders from SWIFT, the global messaging service that facilitates cross-border transactions. It’s a move that could cause turmoil across global financial markets.

Devaluation is the deliberate downward adjustment of the value of a country’s money related to another currency, group of currencies or currency standard. It is often confused with depreciation and is the opposite of revaluation which refers to the readjustment of a currency exchange rate.

The government of a country may decide to devalue its currency and like depreciation it is not the result of non-governmental activities.

One reason a country made devalue its currency is to combat a trade imbalance. Devaluation reduces the cost of a country’s export rendering them more competitive in the Global market which is which in turn increases the cost of imports.

If imports are more expensive domestic consumers are less likely to purchase them further strengthening domestic businesses because exports increase and imports decrease there is typically a better balance of payments because the trade deficit shrinks. In short a country that devalue its currency can produce is difficult because there is a greater demand for cheaper exports.

***

***

In accountancy, depreciation refers to two aspects of the same concept: first, the actual decrease of fair value of an asset, such as the decrease in value of factory equipment each year as it is used and wear, and second, the allocation in accounting statements of the original cost of the assets to periods in which the assets are used (depreciation with the matching principle).

Depreciation is thus the decrease in the value of assets and the method used to reallocate, or “write down” the cost of a tangible asset (such as equipment) over its useful life span. Businesses depreciate long-term assets for both accounting and tax purposes. The decrease in value of the asset affects the balance sheet of a business or entity, and the method of depreciating the asset, accounting-wise, affects the net income, and thus the income statement that they report.

Posted on February 27, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Microsoft: Microsoft Corp.’s stock dropped 2.6% on Wednesday to close at a seven-month low of $280.07. On Thursday, the software giant’s stock opened down 2.8% at $272.51, hit an intra-day low of $271.52, then bounced 8.5% off that low to close up 5.1% on the day at $294.59. The difference between Microsoft’s bullish engulfing and that of Twitter and Meta is that the downtrend has lasted only three months, since the stock closed at a record $343.11 on November. 19th. On Friday, the stock edged up 0.9% to $297.31.

Salesforce: Shares of Saleforce.com Inc. sank 2.4% on Wednesday to close at a 19-month low of $190.54, or 38.5% below its Nov. 8, 2021 record close of $309.96. Then on Thursday, it opened down 3.0% at $184.74, but bounced sharply to close up 7.2% at $204.29. The customer relationship management software company’s stock rose another 1.9% on Friday to $208.09, but remained the worst performer of the Dow Jones Industrial Average’s 30 components over the past three months with a loss of 26.8%.

AMAZON: The stock traded down roughly 9% across 2021and it’s down roughly 19% from the high that it hit last year. Lapping incredible, pandemic-driven performance, Amazon is facing some tough growth comparisons. Massive technology and infrastructure investments are also putting some pressure on earnings in the near term, but the business remains excellently positioned to win the future, and it will almost certainly be one of the most influential companies of the next decade [maybe]?

BE AWARE ALL ADVISORS … NEXT GEN FINANCIAL ADVICE IS HERE?

Are you a financial planner, insurance agent or investment advisor seeking to assist your physician clients with medical practice enhancement solutions, along with healthcare targeted financial planning services, but don’t know where to turn for help?

OR, maybe you’ve already had a bad experience with a young physician or astute healthcare professional client that was actually more informed than you in these areas?

OR, a doctor/nurse client who demanded a true fiduciary advisor [not fee-based advice, with no dual licenses and no arbitration clauses] documented in writing].

After an understandable slowdown in 2020, due to the onset of the COVID-19 pandemic, merger & acquisition (M&A) activity in the healthcare industry accelerated in 2021, and the industry is expected to continue the high number of deals and high deal volume in 2022.

***

***

This Health Capital Topics article will review the U.S. healthcare industry’s M&A activity in 2021, and discuss what these trends may mean for 2022. (Read more…)

Posted on February 26, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

MARKETS: The Dow Jones Industrial Average surged 834.92 points, or 2.5%, to close at 34,058.75, with the blue-chip gauge notching its best daily gain since early November 2020.

S&P 500 rose 95.95 points, or 2.2%, to end at 4,384.65.

NASDAQ Composite Index added 221.04 points, or 1.6%, to finish at 13,694.62.

For the week, the Dow dipped by less than 0.1% while the S&P 500 rose 0.8% and NASDAQ Composite climbed 1.1%. The S&P 500 and NASDAQ benchmarks wiped out losses from earlier in the week.

Posted on February 25, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

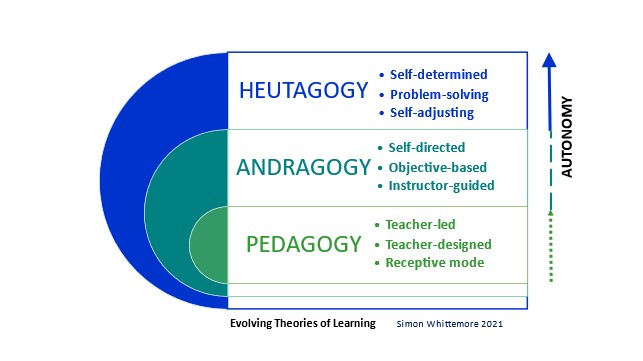

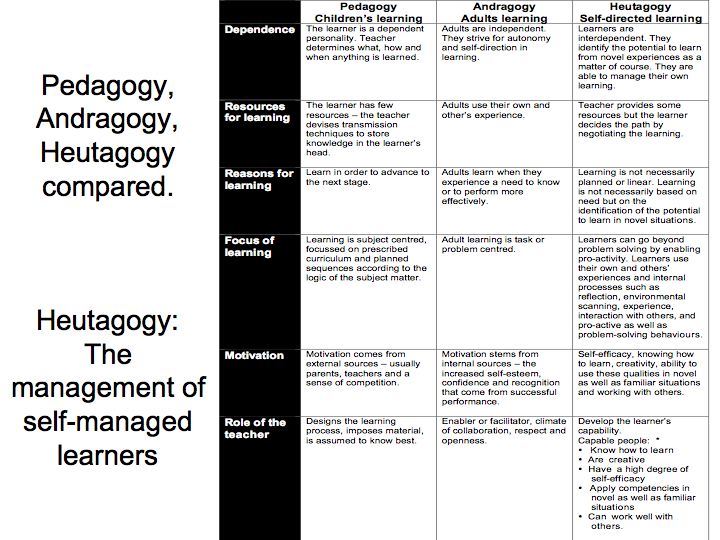

ON EDUCATION – The Difference Among Pedagogy, Andragogy, And Heutagogy

[By David E. Marcinko and Terry Heick]

***

Jackie Gerstein’s passionate thinking about learning is some of my favorite to read. She is rarely pulled down by trend or fad, but is unquestionably progressive and forward-thinking in her approaches to learning and thinking about learning.

She and I also share a passion: self-directed learning. (As does the original summarizer/author of the thinking embedded in table below, Lindy, McKeown Orwin).

I’m embarrassingly interested in any kind of learning at all–formal or informal, self-directed or teacher-centered, authentic or academic. Doesn’t mean I regard them all equally, but I do see a role for almost any system or approach that can cause, support, or glorify the processes of understanding.

Gerstein’s presentation, “Education 3.0 and the Pedagogy of Mobile Learning” uses the concept of mobile learning as a spearhead into a broader discussion of how people learn–different approaches, different domains, and different technologies.

With the progress of technology and the rise in mobile learning, now more than ever Self-Directed Learning–or Heutagogy–isn’t just possible, but natural, and almost awkward to not use, something Gerstein capture’s thoroughly and with her characteristic passion in the presentation below.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements.

Subscribe: MEDICAL EXECUTIVE POST for curated news, essays, opinions and analysis from the public health, economics, finance, marketing, IT, business and policy management ecosystem.

QUERY: But, did you ever wonder what to say when you’re standing next to a senior physician colleague who could help further your academic and educational work?

Now, for some granular specificity; let’s cue the elevator pitch with David Acosta MD and Daniel Hashimoto MD MS who demonstrate what to do (and what not to do) to successfully deliver your medical educator’s elevator pitch.

Posted on February 25, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

WAR IS ON!

By Staff Reporters

***

***

US Exchange: US stocks climbed out of a deep hole to close higher as investors piled into Big Tech names. One sector that got a boost from the war’s outbreak was cybersecurity: Firms like CrowdStrike surged in anticipation of more cyberattacks from Russia.

10 Year T-Bond: 1.971 down

Russian Exchange: The stock exchange in Moscow suspended trading yesterday but when dealing resumed, stocks went into free-fall. The MOEX index plunged as much as 45%, while the RTS index — which is denominated in dollars — was down more than 40% at 4.15 a.m. ET. The crash wiped about $75 billion off the value of Russia’s biggest companies.

Russian Banks and Oil: These companies were among the hardest hit in volatile trading, with shares in Sberbank — Russia’s largest lender — at one stage losing 57% of their value. Rosneft, in which BP owns a 19.75% stake, plunged as much as 58%. BP shares dropped 5% in London.

Posted on February 24, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

Start-Ups for the End of Life

By MIT Technology Review

One Main Street

Cambridge, MA 02142

Technology has changed the way we grieve, but it’s also starting to make a difference to the way we deal with death’s logistics, too.

The New York Times reports that startups—often run by millennials, it drily notes—are increasingly creating digital tools that help people plan for their demise.

***

***

***

Assessment

Though for those determined not to admit defeat, cryogenics is still an option:

KrioRus, the only company outside of the U.S. prepared to put your head on ice after you die, will do so for a modest $12,000. It still doesn’t know what to do further down the line, though.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on February 24, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

By Staff Reporters

***

OIL: Brent crude, the world benchmark, briefly climbed above $100 a barrel for the first time since 2014. US crude jumped 3.3% to $95.15 a barrel.

U.S. stock indexes: All closed sharply lower with the DJIA narrowly avoiding a slip into correction, as U.S. officials warned that Russian troops were poised to attack, and are attacking, the Ukraine raising anxieties among investors who are also wrangling with changing monetary policy and surging inflation.

How did stock indexes trade? The Dow Jones Industrial Average fell 464.85 points, or 1.4%, to end at 33,131.76. A finish below 33,119.69 would mark a 10% decline from the Dow’s Jan. 4 record close, meeting the commonly used definition of a correction. The S&P 500 index fell 79.26 points, or 1.8%, to around 4,225.50, deepening its stumble into correction territory. The NASDAQ Composite Index declined 344.03 points, or 2.6%, at 13,037.49, with 12,845.95 representing the level that would represent a bear market for the technology-laden index.

Asia: Hong Kong’s Hang Seng Index declined 3.2%. Korea’s Kospi dropped 2.7%. Japan’s Nikkei 225 lost 2.4% after coming back from a holiday. China’s Shanghai Composite moved 0.9% lower.

Posted on February 23, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

By Staff Reporters

***

***

A recent American College of Healthcare Executives’ survey of 310 hospital CEOs shows:

• 94% have personnel shortages in registered nursing field • 85% have personnel shortages in technicians field • 67% have personnel shortages in therapists field • 45% have personnel shortages in primary care physicians field • 43% have personnel shortages in physician specialists field • 31% have personnel shortages in physician extenders and specially certified nurses field

Posted on February 23, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

***

By Staff Reporters

***

An annual study of over 1,500 U.S. consumers, shows:

• 55% of consumers find it stressful paying a healthcare bill. • 53% of consumers find it stressful understanding their plan’s coverage and benefits. • 53% of consumers find it stressful comprehending what they owe. • 59% of consumers find it stressful reconciling a bill issue with their payer.

Posted on February 23, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

By Staff Reporters

***

MARKETS: The S&P 500 fell into a correction for the first time in two years, joining the NASDAQ Composite, as Russia sent troops into pro-Russian regions in Ukraine. The S&P 500 index ended down 1% at 4,304.76, below the correction level at 4,316.91, which would represent a 10% drop from its January 3rd record close. A correction is commonly defined by market technicians as a fall of at least 10% (but not greater than 20%) from a recent peak. The last time the S&P 500 entered a correction was February 27th 2020, when the market was being whipsawed by fears about the outbreak of the COVID pandemic.

And, this bearish market isn’t sparing 2021 winners like Home Depot, which fell the most in nearly two years after supply-chain bottlenecks squeezed its margins. HD was the Dow’s biggest gainer last year.

IRS: According to a news release issued by the IRS, taxpayers now have the option to verify their identities during live, virtual interviews with agents. The agency stresses that no bio-metric data will be required for those interviews.

However, taxpayers once again have the option to verify their identity using ID.me’s facial recognition services. Addressing privacy concerns, the IRS says new requirements are in place to ensure that images provided will be deleted upon verification. That would apply to any new IRS accounts created and those where selfies have already been collected.

Posted on February 23, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

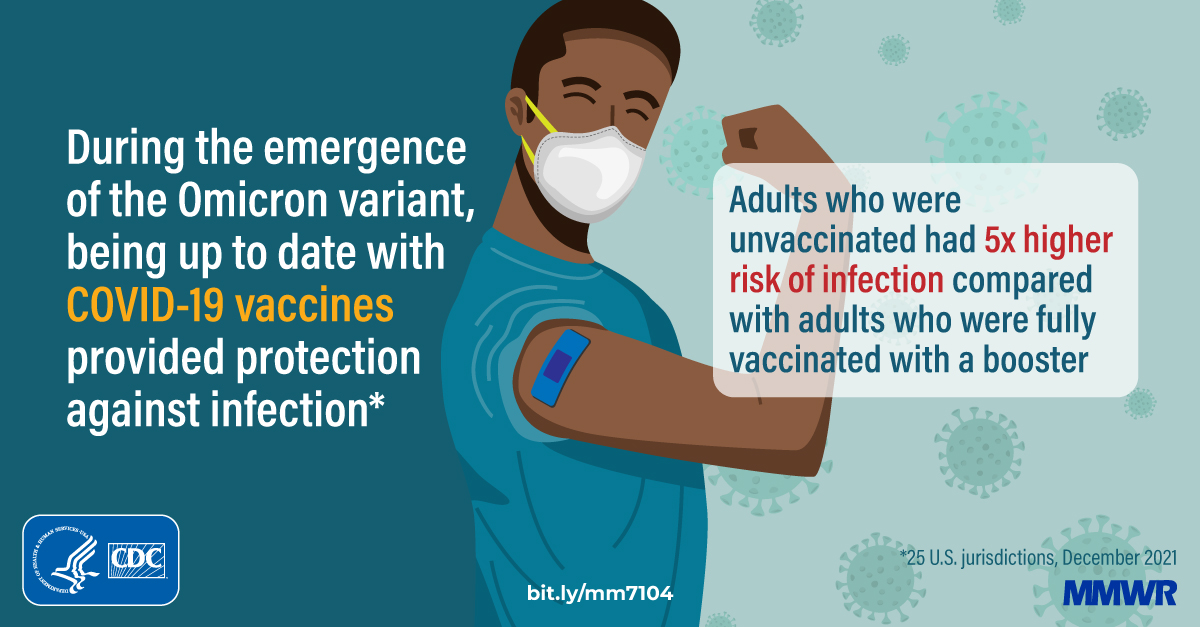

33.6% of COVID Infections Were in Unvaccinated Persons

According to a recent CDC study. Among 422,966 reported SARS-CoV-2 infections in LAC residents aged ≥18 years during November 7, 2021–January 8, 2022:

• 33.6% were in unvaccinated persons • 13.3% were in fully vaccinated persons with a booster • 53.2% were in fully vaccinated persons without a booster • Unvaccinated persons were most likely to be hospitalized, representing 2.8% of COVID infections • Unvaccinated persons were most likely to be admitted to an ICU, or 0.5% of COVID infections • Unvaccinated persons were most likely to be require intubation for mechanical ventilation, or 0.2% of COVID infections.

Posted on February 22, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

By Staff Reporters

***

***

56% of Patients Attempted to Stretch Out a Prescription According tot a Recent CoverMyMeds Survey of 1,000 patients. It found:

• 79% of patients said they’ve gone to the pharmacy only to discover a prescription cost more than they expected. • When faced with an affordability challenge, 56% of patients attempted to stretch out a prescription. • When faced with an affordability challenge, 52% of patients skipped bills or other essential items to afford medications. • When faced with an affordability challenge, 51% of patients sacrificed medications to pay bills and other essentials.

Posted on February 22, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

Virtual Currency – Real Taxation

By Staff Reporters

What you need to report to the IRS

The IRS treats virtual currencies as property, which means they’re taxed similarly to stocks. If all you did was purchase cryptocurrency with U.S. dollars, and those assets have been sitting untouched in an exchange or your cryptocurrency wallet, you shouldn’t need to worry about reporting to the IRS.

***

Reporting is required when certain events come into play, most commonly:

Trading one cryptocurrency for another.

Selling cryptocurrency for fiat dollars (government-issued currency).

Using cryptocurrency to buy goods or services (e.g., paying for a cup of coffee with cryptocurrency).

A critical distinction to make is that triggering a taxable event doesn’t necessarily mean you’ll owe taxes, said Andrew Gordon, an Illinois-based certified public accountant and tax attorney. Just because you have to report a transaction doesn’t mean you’ll end up owing the IRS for it.

Posted on February 22, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

By Staff Reporters

***

***

Markets: The domestic markets were closed yesterday as stocks around the world tumbled.

Crypto: Bitcoin was trading at $36,649 at 2:30 a.m. ET, falling nearly 6.5% in the last 24 hours, according to data from CoinDesk. The world’s most valuable cryptocurrency fell below $40,000 over the weekend, and has continued to slide as the Ukraine crisis intensifies. The currency has lost almost half its value since its November high of $68,990 due to geopolitical tensions, the prospect of interest rate hikes by the US Federal Reserve and curbs by some major economies on digital assets. Bitcoin’s peers have also been faring poorly. Ethereum, the world’s second most valuable cryptocurrency, fell over 8% in the last 24 hours and was trading at $2,520.

Putin: Russian President Vladimir Putin dramatically escalated the Ukrainian conflict. He recognized two separatist regions in eastern Ukraine as independent and ordered Russian troops to enter those areas, which may provide the pretext for an invasion of other parts of the country. Western leaders condemned the move as a violation of international law and the US said it will impose sanctions on those regions.

Paul Edward Farmer (October 26, 1959 – February 21, 2022) was an American medical anthropologist and physician. Farmer held an MD and PhD from Harvard University, where he was the Kolokotrones University Professor and the chair of the Department of Global Health and Social Medicine at Harvard Medical School. He was the co-founder and chief strategist of Partners In Health (PIH), an international non-profit organization that since 1987 has provided direct health care services and undertaken research and advocacy activities on behalf of those who are sick and living in poverty. He was professor of medicine and chief of the Division of Global Health Equity at Brigham and Women’s Hospital.

Dr. Farmer had written extensively on health and human rights, the role of social inequalities in the distribution and outcome of infectious diseases, and global health.

Posted on February 21, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

By Staff Reporters

***

Wall Street trading is closed for Presidents Day holiday. But stock futures were ceding earlier stronger ground, while havens such gold pared losses, after a Kremlin spokesman said no concrete plans for a summit between President Joe Biden and Russian President Vladimir Putin had been made.

MARKETS: IHS Markit’s flash euro area composite PMI (purchasing managers’ index) reading, seen as a reliable gauge of overall economic health, came in at a five-month high of 55.8 in February. The U.K.’s composite PMI came in at an eight-month high of 60.2 in February, up from 54.2 in January and well above forecasts.

European markets were choppy today today as investors monitored the Russia-Ukraine situation and unexpectedly strong economic data from the euro zone and U.K. The pan-European Stoxx 600 index was down 1% during afternoon trade, having gained as much as 0.6% at the start of the session. And, tech stocks dropped 2.4% as most sectors and major bourses slid into the red.

OIL: According to Sonali Paul of Reuters – Oil prices gained more than $1 in early trade on Monday from rising jitters over potential conflict between Russia and Ukraine, with the United States and European Union making clear Russia would face sanctions if it invaded its neighbor. European Commission President Ursula von der Leyen said Russia would be cut off from international financial markets and denied access to major exports needed to modernize its economy if it invaded Ukraine.

***

Brent crude futures were up $1.34, or 1.4%, at $94.88 a barrel at 2312 GMT after hitting a high of $95.00 in early trade.

NIKKEI: Shares in Asia-Pacific fell in Monday morning trade, as investors continue to watch the situation surrounding Ukraine.The Nikkei 225 in Japan slipped 2% in early trade while the TOPIX index shed 1.8%. South Korea’s KOSPI shed 1.64%. Australia’s S&P/ASX 200 slipped 0.82% in morning trade. And, MSCI’s broadest index of Asia-Pacific shares outside Japan traded 0.36% lower.

Capital markets require confidence that all market participants have fair access to the same relevant information about a company and its prospects. Laws governing the trading of securities have been in existence since stocks were first traded. It seems as if each piece of legislation, from the Securities and Exchange Act of the 1930’s through to the 2002 Sarbanes-Oxley Law fought the prior corruption as successfully as preparing an army to fight the last war.

Curiously, the issue of insider trading by members of Congress is not a partisan issue. If behavior is any indication, certain Republicans and Democrats are fond of having the ability to profit from access to material, nonpublic information. Others of both parties are introducing legislation to block illegal insider trading.

Congress has passed laws that prohibit people with insider knowledge from trading on non-public information, and from sharing that non-public information with others who may trade stocks based on that information. The former is known as “illegal insider trading” and the latter as “tipping.” There exists legal insider trading, which is bound by rules of disclosure and third-party decision makers, but we will leave that for another day. Illegal insider trading is enforced through Federal Agencies including the Securities and Exchange Commission (SEC), Internal Revenue Service (IRS) and the Department of Justice (DOJ), as well as by regulations on major stock exchanges such as the New York Stock Exchange (NYSE) and National Association of Securities Dealers Automated Quotation Systems (NASDAQ).

While there is universal agreement that executives, board members, employees and others with access to non-public information may not use that information to trade stocks, members of Congress and their staffs face few practical barriers. And in more recent months, members of the Federal Reserve and their staffs have made questionable, if not downright suspicious trades of stocks.

History is littered with cases of both average citizens and celebrities like Martha Stewart being prosecuted for insider trading. Stewart was ultimately prosecuted and jailed for obstruction after denying insider knowledge.

There are members of both the US Senate and US House of Representatives who want to stop illegal insider trading by their peers. For example, in 2012, President Barack Obama signed the Stop Trading on Congressional Knowledge (STOCK) Act to prevent insider trading by members of Congress and Congressional Staff. However, there have been no prosecutions under this statute to date. The reason is that the “Speech and Debate” clause prohibits questioning an elected Senator or Congressional Representative.

Moreover, much of the disclosure of material, non-public information that would establish a foundation for illegal insider trading occurs outside the public eye. Members of Congress cannot act on information obtained from companies themselves. The difficulty arises in proving that a member of Congress or Congressional staff knew of material, non-public information acquired in a confidential congressional meeting. Let me rephrase that. There is no way of knowing what transpired in the confidential committee meeting so there is no provable path to a stock trade benefiting the member of Congress or their staff.

Suppose two publicly traded defense contractors were bidding on a new weapons system. In a confidential committee, a Department of Defense (DOD) recommendation to accept the bid of company A versus Company B was made and endorsed by the committee. At that point, everyone with access to the non-public information about the weapons system bid would know that it would be good for the stock of Company A and bad for the stock of Company B.

Take this a step further. Company A and Company B are notified about the confidential decision and advised to keep this material, non-public information protected. At this point, if any executive, board member or employee with that knowledge traded in the stock of Company A or Company B they would be subject to prosecution, including fines and imprisonment. Also, if any person at the company provided that material, non-public information to another person, including a member of Congress, that action would be subject to investigation and potential prosecution.

Now suppose a Senator, Congressional Representative or staff member, after receiving the news of the weapons system award went to their broker, computer or telephone and bought stock in Company A while selling (or shorting in another way) Company B. Or perhaps communicated to a friend or family member on a trade “suggestion.” Relaying or exploiting information – material, non-public information — behavior that would land any other person in an investigation and make them subject to prosecution, cannot be practically pursued because there is no way to use the committee deliberations as evidence.

When Senators Richard Burr (R-NC), Kelly Loeffler (R-GA) and Diane Feinstein (D-CA) were accused of insider trading, instead of being subjected to investigation and potential prosecution through the SEC, IRS, or DOJ, their actions instead were reviewed by the Senate Ethics Committee. The Senate Ethics Committee, made up of other US Senators, found no wrongdoing. Let me rephrase that – other US Senators, who might benefit themselves from insider trading – decided to give suspicious behavior a pass. Even if the conduct of the Senators was on the up-and-up, the optics do not inspire confidence.

The US Senate does not have a monopoly on suspicious trading. For example, Congresswoman Lois Frankel (D-FL), was accused of trading stocks of companies in the fossil fuel industry while a sitting on a Congressional subcommittee that oversees funding for the Department of Energy.

Legislation to Block Insider Trading by Congress and the Federal Reserve

US Senators and Congressional Representatives have made proposals to improve public perception of their ranks with more practical solutions and stiffer penalties. Pre-eminent among the reformers is Senator Elizabeth Warren (D-MA), a person with a strong background in financial matters. Senator Warren appears to be the leading voice in calling for members of the Federal Reserve and their staffs to also be subject to laws prohibiting illegal insider trading and tipping. These restrictions are long overdue, as statements by the Fed has caused wild gyrations in the prices of securities. Senator Warren’s ideas are recommended reading on her web site at

. Enter “Insider Trading” on the search bar of the Senator’s web site for 61 references.

Senators Jeff Merkley (D-OR) and Sherrod Brown (D-OH) have offered the “Ban Conflicted Trading Act.” Under the legislation, elected persons and their staffs would be required to either sell or freeze their stock holdings, or put them in a blind trust. Introduced in 2018, the legislation has stalled. Last winter, Representative Alexandria Ocasio-Cortez (D-NY) and others have indicated they would introduce the same legislation in the House.

Earlier this month, Senators Jon Ossoff (D-GA) and Mark Kelly (D-AZ) introduced the Ban Congressional Stock Trading Act. If it becomes law, every member of Congress—as well as their spouses and dependent children—would be required to place their stock portfolios into a blind trust. One benefit of an outright ban or blind trusts would mean that clerical matters would no longer be a concern of those elected. Kelly himself, according to news reports, did not make a timely disclosure about a stock option exercise.

Senator Josh Hawley (R-MO) announced he will introduce the Banning Insider Trading in Congress Act. Wryly pointing out that politicians manage to outperform the stock market year after year, Hawley’s bill would prohibit members of Congress and their spouses from buying and trading individual stocks. Those who violate it would have to disgorge their profits.

Congress: Keep it simple and fix this

The singular, clear way to avoid abuses of insider information is to ban the trade of individual stocks and industry-specific Exchange Traded Funds (ETF) by members of Congress, Congressional staffs, members of the Federal Reserve and their staffs. Double blind trusts (where neither the owner or trustee knows identity of the other) would be an acceptable form of investing. Finally, add stronger criminal penalties for tipping insider information.

This is one of the few things that seem to enjoy bipartisan support, and would seemingly be welcomed by nonpartisans and those on the political poles as well.

Of course, like everything political, proposals of these types do not enjoy absolute, clear-cut support. As House Speaker Nancy Pelosi (D-CA) said about her opposition to such restrictions “We are a free market economy,” Pelosi, purported to be one of the 25 wealthiest members of Congress, continued, “They (Congress) should be able to participate in that.” Pelosi’s recent financial disclosure is said to have 48 transactions made by her family valued at a total of some $50 million so she is sympathetic to serving in Congress and participating in trading.

Posted on February 20, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

By Staff Reporters

Federal Reserve Chair Jerome Powell and his colleagues can expect to see their upcoming key inflation metric accelerate this week to a fresh four-decade high last seen when Paul Volcker led the U.S. central bank.

The personal consumption expenditures price index, which the Federal Reserve uses for its inflation target, likely jumped 6% in January from a year earlier, according to the median of a Bloomberg survey of economists. The core measure, which excludes food and fuel, is forecast to climb 5.2%.

And, less than a month before the FOMC’s next policy meeting, a sharper-than-projected advance in the price gauge could turn up the heat for a half-point increase in the benchmark interest rate. January’s consumer-price index rose more than forecast, with broad advances in the costs of goods and services.

Posted on February 19, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

MARKETS: Stocks closed down for a second straight week in the US— and sunk deeper into the red for 2022 so far — as investors assess the risks from escalating tensions in Ukraine and a shift in monetary policy by the Federal Reserve.

And, after another day of turbulence, the Dow and the S&P 500 both fell 0.7% (with the Dow ending Friday at 34,079) and the tech-heavy NASDAQ composite declined 1.2%. The NASDAQ has fallen farthest of the three major U.S. stock indexes to date, down 13.4% for the year, while the S&P 500 is off 8.8% and the Dow is down 6.2%.

Specifically, Intel’s shares declined $2.47, or 5.2%, while those of Boeing were off $4.38 (2.1%), combining for a roughly 45-point drag on the Dow. Salesforce.com Inc. Caterpillar and Honeywell International Inc. also contributed significantly to the decline.

STOCKS:

Shopify, which represented the Covid e-commerce boom, is down 62% from its peak.

Roblox, which represented the Covid gaming boom, is down 63%.

Netflix, which represented the Covid streaming boom, is down 43%.

Noteworthy: A $1 move in any of the Dow’s 30 components equates to a 6.59-point swing.

UKRAINE: Investors watched the latest developments in Ukraine, where Russia has been amassing troops on the border. The tensions are yet another concern for investors as they also try to determine how the economy will react to rising inflation and looming interest rate hikes.

Posted on February 18, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

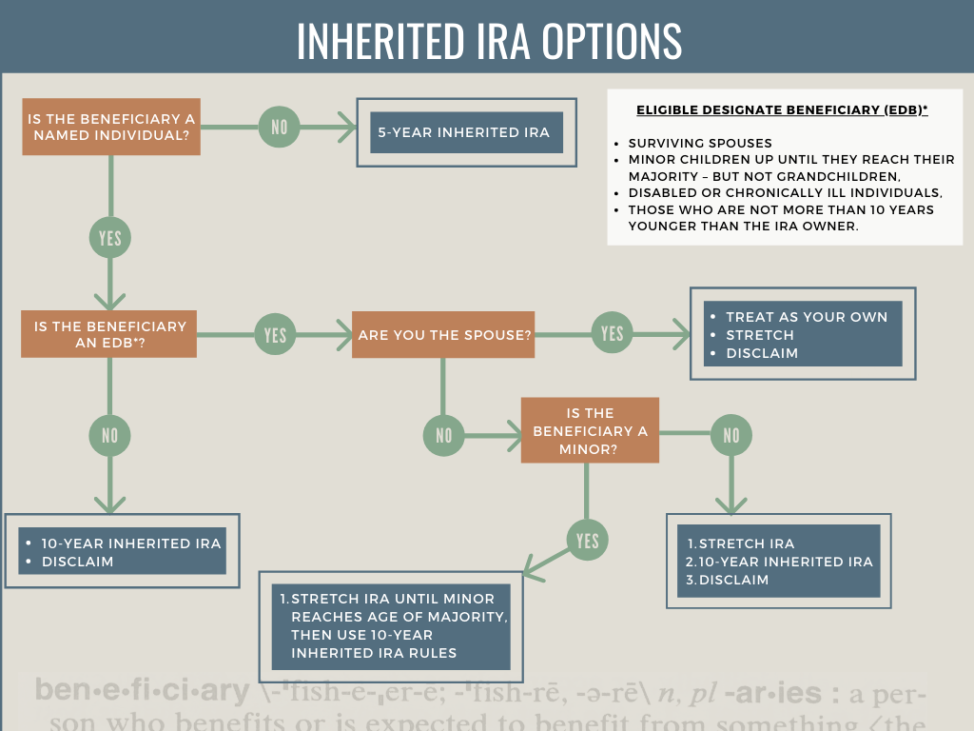

IRS Tax Implications

By Staff Reporters

***

If you inherited a tax-deferred retirement plan, such as a traditional IRA, you’ll have to pay taxes on the money. But you can make the tax hit less onerous.

Spouses can roll the money into their own IRAs and postpone distributions—and taxes—until they’re 70½. All other beneficiaries who want to continue to benefit from tax-deferred growth must roll the money into a separate account known as an inherited IRA. Make sure the IRA is rolled directly into your inherited IRA. If you take a check, you won’t be allowed to deposit the money. Rather, the IRS will treat it as a distribution and you’ll owe taxes on the entire amount.

Once you’ve rolled the money into an inherited IRA, you must take required minimum distributions every year—and pay taxes on the money—based on your age and life expectancy. Deadlines are critical: You must take your first RMD by December 31st. of the year following the death of your parent (or whoever left you the account). Otherwise, you’ll be required to deplete the entire account within five years after the year following your parent’s death.

The December 31st. deadline is also important if you are one of several beneficiaries of an inherited IRA. If you fail to split the IRA among the beneficiaries by that date, your RMDs will be based on the life expectancy of the oldest beneficiary, which may force you to take larger distributions than if the RMDs were based on your age and life expectancy.

You can take out more than the RMD, but setting up an inherited IRA gives you more control over your tax liabilities. You can, for example, take the minimum amount required while you’re working, then increase withdrawals when you’re retired and in a lower tax bracket.

Did you inherit a Roth IRA? And so, as long as the original owner funded the Roth at least five years before he or she died, you don’t have to pay taxes on the money. You can’t, however, let it grow tax-free forever. If you don’t need the money, you can transfer it to an inherited Roth IRA and take RMDs under the same rules governing a traditional inherited IRA. But with a Roth, your RMDs won’t be taxed.