BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] E-mail: MarcinkoAdvisors1738@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on July 30, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

15 Self-Funded Employers Analyzed Their Pharmacy Claims Data in Conjunction with the Commonwealth Fund and Discovered the Following Regarding their PBM FormularIES

Navigating a course where sound organizational management is intertwined with financial acumen requires a strategy designed by subject-matter experts. Fortunately, Financial Management Strategies for Hospital and Healthcare Organizations: Tools, Techniques, Checklists and Case Studiesprovides that blueprint. ―David B. Nash, MD, MBA,Jefferson Medical College, Thomas Jefferson University

It is fitting that Dr. David Edward Marcinko, MBA, CMP™ and his fellow experts have laid out a plan of action in Financial Management Strategies for Hospital and Healthcare Organizationsthat physicians, nurse-executives, administrators, institutional CEOs, CFOs, MBAs, lawyers, and healthcare accountants can follow to help move healthcare financial fitness forward in these uncharted waters. ―Neil H. Baum, MD, Tulane Medical School

The concept of a self-taught and student motivated, but automated outcomes driven classroom may seem like a nightmare scenario for those who are not comfortable with computers. Now everyone can breathe a sigh of relief, because the Institute of Medical Business Advisors just launched an “automated” final examination review protocol that requires no programming skill whatsoever.

In fact, everything is designed to be very simple and easy to use. Once a student’s examination “blue-book” is received, computerized “robotic reviewers” correct student assignments and quarterly test answers. This automated examination model lets the robots correct tests and exams, while the students concentrate on guided self-learning.

–Just Seeing the Cost of the Lab Test DECREASED the Number of Labs Ordered Per Patient by 9%.

–Doctors Also SUBSTITUTED a Lower Cost Lab Test for a Higher Cost Lab Test 10,000 Times.

The Doctors Were NOT Clinically Directed to Change Their Behavior.

The Doctors’ Pay Was NOT Affected by Their Lab Ordering Either Way.

This Study Illustrates How Giving Doctors Cost Information in a Setting of Clinical and Financial Independence AUTOMATICALLY Decreases Healthcare Waste.

Doctors Can Be Much Better Stewards of Healthcare Dollars … and the Technological Innovation Needed is Minimal.

Disclosure: Dr. Bricker is the Chief Medical Officer of Virtual Care Company First Stop Health.

Posted on July 24, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

Residents disproportionately affected by COVID-19

***

BY JAMES BLUMENSTOCK MA

Residents of nursing homes have been disproportionately affected by COVID-19. The nature of this coronavirus—which is particularly harmful to older adults and people with multiple chronic conditions—has left residents vulnerable.

Additionally, the pandemic has exacerbated existing challenges in our fragmented long-term care system, which is financed, regulated, and administered by states, the federal government, and private care facilities.

During this webinar, panelists discussed policy options to support high quality care for nursing home residents during the COVID-19 pandemic.

NOTE: This webinar is a project of the Alliance for Health Policy and NIHCM Foundation, in collaboration with The Commonwealth Fund.

There is Copay for Each Office Visit and Visits are Unlimited.

Direct Primary Care Doctors Are Most Frequently Family Practice Physicians, but Internal Medicine and Pediatricians Can Also Have Direct Primary Care Practices.

The Average Direct Primary Care Practice Has a Panel of 345 Patients, with a Goal of About 600 Patients at Full Capacity.

For Comparison, the Typical Fee-for-Service Primary Care Doctor Has a Patient Panel of 2,500.

57% of Direct Primary Care Practices Contract with Employers That Pay the Monthly Membership on the Employee’s Behalf.

Direct Primary Care is a Strategy to Increase the Quality of Care and Decrease Healthcare Costs for an Employee Health Plan.

Disclaimer: Dr. Bricker is the Chief Medical Officer of Virtual Care Company First Stop Health.

Posted on July 22, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

BOOK REVIEW

“The Dictionary of Health Insurance and Managed Care lifts the fog of confusion surrounding the most contentious topic in the health care industrial complex today. My suggestion therefore is to ‘read it, refer to it, recommend it, and reap’.”

—Michael J. Stahl, PhD, Physician Executive MBA Program [William B. Stokely Distinguished Professor of Business]

The University of Tennessee, College of Business Administration

Posted on July 21, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

TEXTBOOK RELEASE AND REVIEW

Reviews

Navigating a course where sound organizational management is intertwined with financial acumen requires a strategy designed by subject-matter experts. Fortunately, Financial Management Strategies for Hospital and Healthcare Organizations: Tools, Techniques, Checklists and Case Studiesprovides that blueprint. ―David B. Nash, MD, MBA,Jefferson Medical College, Thomas Jefferson University

It is fitting that Dr. David Edward Marcinko, MBA, CMP™ and his fellow experts have laid out a plan of action in Financial Management Strategies for Hospital and Healthcare Organizationsthat physicians, nurse-executives, administrators, institutional CEOs, CFOs, MBAs, lawyers, and healthcare accountants can follow to help move healthcare financial fitness forward in these uncharted waters. ―Neil H. Baum, MD, Tulane Medical School

The U.S. individual tax return is based around the concepts of Adjusted Gross Income (AGI) and Taxable Income (TI). AGI is the amount that shows up at the bottom of page one of Form 1040, individual income tax return. It is the sum of all of the taxpayer’s income less certain allowed adjustments (like alimony, one-half of self-employment taxes, a percentage of self-employed health insurance, retirement plan contributions and IRAs, moving expenses, early withdrawal penalties and interest on student loans). This amount is important because it is used to calculate various limitations within the area of itemized deductions (e.g., medical deductions: 10 percent of AGI; miscellaneous itemized deductions: 2 percent of AGI).

When a healthcare professional taxpayer hears the phrase “an above the line deduction”, the line being referenced is the AGI line on the tax return. Generally, it is better for a deduction to be an above the line deduction, because that number helps a taxpayer in two ways. First, it reduces AGI, and second, since it reduces AGI, it is also reducing the amounts of limitations placed on other deductions as noted above.

Obviously, if there is an above the line there is also a “below the line” deduction. These below the line deductions are itemized deductions (or the standard deduction if itemizing is not used) plus any personal exemptions allowed. AGI less these deductions provides the taxable income on which income tax is actually calculated. All of that being said, it is better for a deduction to be an above the line deduction. Although this is a bit dry, it helps to understand the concepts in order to know where items provide the most benefit to the medical professional taxpayer.

PERSONAL TAXATION CALCULATIONS

Gross Income (all income, from whatever source derived, including illegal activities, cash, indirect for the benefit of, debt forgiveness, barter, dividends, interest, rents, royalties, annuities, trusts, and alimony payments-no more)

Less non-taxable exclusions (municipal bonds, scholarships, inheritance, insurance

proceeds, social security and unemployment income [full or

partial exclusion], etc.).

Total Income

Less Deductions for AGI (alimony, IRA contributions, capital gains, 1/2 SE tax,

moving, personal, business and investment expenses, and

penalties, etc.).

Adjusted Gross Income (bottom Form 1040)

Less Itemized Deductions from AGI, (medical, charitable giving, casualty,

involuntary conversions, theft, job and miscellaneous expenses, etc.), or

Less Standard Deduction (based on filing status)

Less Personal Exemptions (per dependents, subject to phase outs)

Taxable Income

Calculate Regular Tax

Plus Additional Taxes (AMT, etc.)

Minus Credits (child care, foreign tax credit, earned income housing, etc.)

Health Insurance Carriers Are Misaligned by Owning PBMs That Make More Money in Rebate Kick-Backs When the Employee Health Plan Spends More Money on Expensive Prescription Drugs.

Doctors Are Misaligned When They *Are Employed by Hospitals That Tie Test and Procedure Ordering Volume to Doctor Compensation.

Hospitals are Misaligned When They Buy Physician Practices and Raise the Prices for In-Office Testing and Procedures by 300%… Even Though NOTHING Has Changed Other Than the Sign on the Door.

Accordingly, True Employee Health Plan Innovation is ALIGNMENT Innovation That Provides Care Outside the of the Status Quo Fee-for-Service System.

Onsite Clinics, Near Site Clinics, Direct Primary Care and Capitated Virtual Care All Provide Real Alignment Innovation for Employee Health Plans.

It seemed too good to be true—on June 7, the FDA approved a breakthrough medication for Alzheimer’s disease. At the time, the drug “could mark a new era in treating the leading cause of dementia and the sixth leading cause of death in the US”, according to some experts.

–OR NOT–

The FDA’s approval of the drug was met with widespread criticism. And the ensuing scandal has undermined the integrity of the agency’s approval process for new treatments.

Backlash to Aduhelm continued to escalate last week. On Thursday, influential hospitals Cleveland Clinic, NYC’s Mount Sinai Health System, and Providence in Washington State said they wouldn’t administer Aduhelm, citing concerns over its effectiveness and safety.

Review

According to Morning Brew, the FDA approving Aduhelm was like you deciding to watch a movie knowing that it had a 47% rating on Rotten Tomatoes. In November 2020, an expert panel advised the FDA against approving the drug after a pair of studies showed conflicting results about its effectiveness.

Instead the agency fast-tracked it, arguing that the benefits of treating a devastating disease like Alzheimer’s outweigh the risks. An Alzheimer’s drug hadn’t been approved by the FDA in 18 years.

Some experts who helped the FDA evaluate Aduhelm protested the decision. Harvard Medical School Professor Dr. Aaron Kesselheim, the third member of the 11-person advisory panel to resign in the wake of the FDA’s approval, said it was “probably the worst drug approval decision in recent U.S. history.”

Effectiveness is one concern around Aduhelm. Side effects, which include brain swelling and brain bleeding, are another. The final issue is the price tag: $56,000. That’s a lot, but it could cost even more since patients might have to pay for periodic tests that look for side effects.

A study by the healthcare nonprofit Altarum concluded that by the mid-2020s, Aduhelm would account for more than 1% of all national health spending, and that’s on the low end of projections.

Looking Ahead … the blowback has been so bad that the acting FDA chief has ordered a federal investigation to explore the perhaps too-cozy relationship between the scientists who approved the drug and the drug-maker, Biogen.

Still, “once the product is approved, the cat’s out of the bag, the horse is out of the barn,” Johns Hopkins Drug Safety Expert Dr. G. Caleb Alexander told the NYT. More than 600 sites across the US are getting ready to administer Aduhelm, and they’re expecting high demand.

Recruitment has become a refined art in recent years as practices and physicians themselves grow increasingly savvy about the finer points of marketing positions and securing employment. It’s more competitive than ever, too. Many organizations are going after the same physicians. Add to that a shortage of doctors in key specialties and certain geographical areas and the pressure becomes that much more intense. Moreover, the aging of the physician workforce, their increased dissatisfaction with managed care, and changes in doctors’ work expectations (they want more free time) have affected the demand and supply.

Additionally, both practicing physicians and residents fresh out of training have become more discerning and skillful in managing the search process. Candidates have learned to be selective based on how they’re treated on the phone, how they’re treated in person during site visits, or how smoothly the negotiations go. One small bump in the road and they could choose to go elsewhere. In truth, they look to rule organizations out, not in.

Even the smallest of practices must have an effective recruitment plan because they compete directly with the big guys — larger practices and hospitals that have polished their efforts and perfected their processes.

Facts about Physician Recruiters and Executive Search Firms

1) If you are job hunting, you should send your resume to recruiters

Different recruiters know about different positions. They do not usually know about the same ones. This is particularly true with retained firms. By sending your resume out widely, you will be placed in many different confidential databases and be alerted of many different positions. If you send your resume to only a few, it may be that none you send to will be working with positions which are suited for you. Throw your net widely.

If you change jobs, it is also wise to send follow-up letters to the recruiters and alert them of your new career move. Many search firms follow people throughout their careers and enjoy being kept up-to-date. It is a good idea to have your resume formatted in plain text so you can copy and paste it into email messages when requested to do so. Then, follow up with a nicely formatted copy on paper by postal mail.

Some estimate that only 1% to 3% of all resumes sent will result in actual job interviews. So, if you only send 50 resumes, you may only have less than 2 interviews, if that many. Send your resume to as many recruiters as you can. It is worth the postage or email time. Generally, recruiters will not share your resume with any employer or give your name to anyone else without obtaining your specific permission to do so. The recruiter will call first, talk to you about a particular position and then ask your permission to share your resume with that employer.

2) Your resume will be kept strictly confidential by the executive search firm.

It is safe to submit your resume to a search firm and not worry that the search firm will let it leak out that you are job hunting. Recruiters will call you each and every time they wish to present you to an employer in order to gain your permission. Only after they have gained your permission will they submit your name or resume to the identified employer. The wonderful aspect of working with search firms is that you can manage your career and your job search in confidence and privacy.

3) Fees are always paid by the employer, not the job candidate.

Recruiters and search firms work for the employer or hiring entity. The employer pays them a fee for locating the right physician for the job opening. This is important to remember, in that when you interact with executive recruiters, you are essentially interacting with an agent or representative of the employer. Recruiters are more loyal to employers than they are to job candidates because they work for the employer. This should not present a problem, but, should cause you to develop your relationship with the recruiter with the same integrity and professionalism that you would with the employer.

Recruiters are paid fees in one of two ways – retainer fees or contingency fees. This is an important distinction and will affect your process with both the employer and the recruiter. Some employers prefer working with contingency firms and some with retained firms. Both are respected by employers and useful in your job search, but, the two types of firms will not be handling the same positions with the same employers simultaneously.

A “retained” recruiter has entered an exclusive contract with an employer to fill a particular position. The retained recruiter, then, is likely to advertise a position, sharing the specifics of the position, location and employer openly. The retained firm feels a great obligation to fulfill the contract by finding the best person for the job.

A “contingency recruiter” on the other hand, usually does not have an exclusive relationship with the employer, and is only paid a fee if the job search is successful. Often, if the employer uses contingency firms, there will be more than one contingency firm competing to fill a certain position. As a job hunter, if you are sent to an interview by a contingency firm, you may find that you are competing with a larger number of applicants for a position. Generally, retained firms only send in from 3 to 5 candidates for a position.

Recruiters will be paid fees equal to about 25% to 35% of the resulting salary of the successful candidate plus expenses. This does not come out of the job candidate’s salary. This is paid to the recruiter through a separate relationship between the employer and the search firm. This may seem like a large fee, but, keep in mind that recruiters incur a great many expenses when searching for successful job candidates. They spend enormous amounts of money on computer systems, long distance calls, mail-outs, travel and interviews. Recruiters work very hard for these fees. Employers recognize the value of using recruiters and are more than willing to pay recruiters the fees. All you have to do is contact the recruiter to get the process moving.

4) Not all medical recruiters work only with physicians.

Some search firms work exclusively with physicians or in healthcare, while others may work in several fields at once. Some of the larger generalist firms will have one or more search consultants that specialize in healthcare. It is important for you, as a job hunter, to assess the recruiters’ knowledge of your field. If you use industry or medical specialty buzz words in describing your skills, experience or career aspirations, you may or may not be talking a language the recruiter understands fully. It is wise to explore fully with the recruiter his understanding of your field and area of specialization.

5) Recruiters and search consultants move around.

Recruiters, like many professionals, move to new firms during their careers. Often you will find that recruiters will work at several firms during their careers. Since it is much more effective to address your letters to a person rather than “to whom it may concern”, it is smart for job hunters to have accurate and up-to-date information about who is who and where, since this can change frequently. Search firms also move their offices, sometimes to another suite, street or state. If you have a list of recruiters that is over one year old, you will certainly waste some postage in mailing your resumes and cover letters. Many of your mail-outs will be returned to you stamped “non-deliverable”, unless you obtain an up-to-date list. A resource, like the Directory of Healthcare Recruiters is updated very frequently, usually monthly [www.pohly.com/dir3.html].

6) Most search firms work with positions all over the country.

If you are from a particular state, and want to remain in that state, don’t make the mistake of only sending your resume to recruiters in your state. Often the recruiters in your state are working on positions in other states, and recruiters in other states are working on positions in your state. This is usually the case. Very few recruiters work only in their local area, most work all around the US and some internationally. Regardless of your geographic preference, you should still send your resume to all the healthcare recruiters. If you really only want to remain in your area, you can specify that preference in your cover letter.

7) Recruiters primarily work with hard to fill positions or executive positions.

Some recruiters specialize in clinical positions for physicians, managed care executive positions, healthcare financial positions or health administration positions. Others may specialize in finding doctors, nurses or physical therapists. Generally, an employer does not engage a recruiter’s assistance in filling a position unless it is hard to fill. Sometimes employers will engage search firms to save them the valuable time of advertising or combing through dozens of resumes.

Contingency recruiters tend to work with more mid-level management and professional positions, but, this is not always the case. Retained firms generally work with the higher level clinical or administrative positions.

One thing you will be assured of is that if a recruiter is working on a position that means that the employer is willing to pay a fee. That usually means that the position is a valued position and one worth closer inspection on your part. Even in healthcare, with certain exceptions, our economy is an “employer’s market”. This means that employers receive a deluge of resumes for their open positions. Increasingly, employers are using recruitment firms to handle their openings and schedule the interviews because employers simply do not have the manpower or time to handle the many resumes they receive. Therefore, if a job hunter is submitted by a recruiter, that job hunter has a great advantage over all other applicants.

Posted on July 18, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

THE SHERLOCK COMPANY

This podcast features a brief discussion by colleague Doug B. Sherlock CFA, Senior Health Care Analyst and President, Sherlock Company http://www.sherlockco.com featuring his insights into the quarterly financial reports of health plans, for the first quarter 2021.

The Charges Were Regarding Illegal Payments and Kickbacks to Doctors that Were Thinly-Veiled as ‘Speaker Fees’ and Fancy Dinners.

Why Where the Doctors Not Held Accountable and What Does This Say About a Doctor’s Mentality on Money?

Learn the Psychology of Doctors and Money.

Understand How It Leads to Counterproductive Relationships Between Physicians and Drug Companies, Which Can Compromise the #1 Rule in Medicine: The Patient Comes First, Always.

Disclaimer: Dr. Bricker is the Chief Medical Officer of Virtual Care Company First Stop Health

Posted on July 16, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

HSA Update 2021

By Michael Thompson

High-deductible health plans have been popular, but it’s becoming clear they are not right for all employees, said Michael Thompson, president and chief executive officer of the National Alliance of Healthcare Purchaser Coalitions.

Specifically, Forrester Research Says That Customer Service is ‘Poor’ at Blue Cross of Texas and Illinois, Blue Shield of California, CareFirst Blue Cross, Anthem, United Healthcare, Cigna and Aetna.

Hospital Billing Customer Services Is Bad Too.

Hospital Billing Complexity is So Troublesome to Patients, that 40% Say They Avoid Preventive Care and Screening Tests Just to Avoid the Billing Headache.

Healthcare Customer Service is Terrible Because Health Insurance Companies and Hospitals Do Not Need Good Billing Customer Service to Be Successful, As Demonstrated by High and Rising Health Insurance Stock Prices and Large and Growing Hospital System Revenue.

For Health Insurance Companies and Hospitals, Not Fixing Their Poor Customer Service May Be a Calculated Business Decision.

Implications:To Help Make Their Employees’ Lives Better, Employers May Need to 1) Hire a Healthcare Navigation Company or 2) Deliver More Care to Their Plan Members Outside of the Traditional Health Insurance and Hospital Systems… and Avoid the Terrible Customer Service All Together.

Disclaimer: Dr. Bricker is the Chief Medical Officer of Virtual Care Company First Stop Health and is the Former Co-Founder of Compass Professional Health Services.

–The Private Equity Firm Offers an Up Front Lump Sum of Money and Administrative Services Such as Billing and Collections for the Practice.

–In Return, the Doctors in the Practice Agree to Have 30-40% of All Future Revenue Go to the Private Equity Firm.

The Up Front Lump Sum Can Be Equal to as Much as 10 – 20 Years of Income for a Physician.

The Older Doctors in the Practice Who Are Usually the Partners Frequently Take This Deal, Resulting in the Younger Partners Making Less Take-Home Pay.

Implication for Employers:

Private Equity Firms Create Larger Group Practices to Have Better Negotiating Leverage with Commercial Insurance Carriers and Obtain Higher Fee-for-Service Reimbursement.

Overall Healthcare Costs for Physician Services Go Up, While the Take-Home Pay for Doctors Goes Down… and the Private Equity Firm Keeps the Difference.

NOTE: The Older Doctors Who Are Paid the Lump Sum Are Still Required to Stay at the Practice for a Certain Number of Years After the Transaction.

Managed care is a prospective payment method where medical care is delivered regardless of the quantity or frequency of service, for a fixed payment, in the aggregate. It is not traditional fee-for-service medicine or the individual personal care of the past, but is essentially utilitarian in nature and collective in intent. Will new-age healthcare reform be even more draconian?

Unhappy Physicians

There are many reasons why doctors are professionally and financially unhappy, some might even say desperate, because of managed care; not to mention the specter of healthcare reform from the Obama administration. For example:

A staggering medical student loan debt burden of $100,000-250,000 is not unusual for new practitioners. The federal Health Education Assistance Loan (HEAL) program reported that for the Year 2000, it squeezed significant repayment settlements from its Top 5 list of deadbeat doctor debtors. This included a $303,000 settlement from a New York dentist, $186,000 from a Florida osteopath, $158,000 from a New Jersey podiatrist, $128,000 from a Virginia podiatrist, and $120,000 from a Virginia dentist. The agency also excluded 303 practitioners from Medicare, Medicaid, and other federal healthcare programs and had their cases referred for nonpayment of debt.

Because of the flagging economy, medical school applications nationwide have risen. “Previously, there were a lot of different opportunities out there for young bright people”; according to Rachel Pentin-Maki; RN, MHA”; not so today. In fact, Physicians Practice Digest recently stated, “Medicine is fast becoming a job in which you work like a slave, eke out a middle class existence, and have patients, malpractice insurers, and payers questioning your motives.” Remarkably, the Cornell University School of Continuing Education has designed a program to give prospective medical school students a real-world peek, both good and bad.

The Ripple Effects of Managed Care and Reform

“Many people who are currently making a great effort and investment to become doctors may be heading for a role and a way of life that are fundamentally different from what they expect and desire,” according to Stephen Scheidt, MD, director of the $1,000 Cornell fee program; why?

Fewer fee-for-service patients and more discounted patients.

More paperwork and scrutiny of decisions with lost independence and morale.

Reputation equivalency (i.e., all doctors in the plan must be good), or commoditization (i.e., a doctor is a doctor is a doctor).

The provider is at risk for (a) utilization and acuity, (b) actuarial accuracy, (c) cost of delivering medical care, and (d) adverse patient selection.

Practice costs are increasing beyond the core rate of inflation.

Medicare reimbursements are continually cut.

Early Opinions

Richard Corlin MD, opined back in 2002 that “these are circumstances that cannot continue because we are going to see medical groups disappearing.” Furthermore, he stated, “This is an emergency that lawmakers have to address.” Such cuts also stand to hurt physicians with private payers since commercial insurers often tie their reimbursement schedules to Medicare’s resources. “That’s the ripple effect here,” says Anders Gilberg, the Washington lobbyist for the Medical Group Management Associations (MGMA).

Assessment

And so, some desperate doctors are pursing these sources of relief, among many others:

A growing number of doctors are abandoning traditional medicine to start “boutique” practices that are restricted to patients who pay an annual retainer of $1,500 and up for preferred services and special attention. Franchises for the model are also available.

Regardless of location, the profession of medicine is no longer ego-enhancing or satisfying; some MDs retire early or leave the profession all together. Few recommend it, as a career anymore.

Assessment

To compound the situation, it is well known that doctors are notoriously poor investors and do not attend to their own personal financial well being, as they expertly minister to their patients’ physical illnesses.

Conclusion

And so, your thoughts and comments on this Medical Executive-Post are appreciated. Tell us what you think? Are you a desperate doctor? Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, be sure to subscribe to the ME-P. It is fast, free and secure.

Posted on July 12, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

MANAGEMENT STRATEGIES, OPERATIONAL TECHNIQUES, TOOLS, TEMPLATES AND CASE STUDIES

TEXTBOOKREVIEWS:

Hospitals and Health Care Organizationsis a must-read for any physician and other health care provider to understand the multiple, and increasingly complex, interlocking components of the U.S. health care delivery system, whether they are employed by a hospital system, or manage their own private practices.

The operational principles, methods, and examples in this book provide a framework applicable on both the large organizational and smaller private practice levels and will result in better patient care. Physicians today know they need to better understand business principles and this book by Dr. David E. Marcinko and Professor Hope Rachel Hetico provides an excellent framework and foundation to learn important principles all doctors need to know. ―Richard Berning, MD, Pediatric Cardiology

… Dr. David Edward Marcinko and Professor Hope Rachel Hetico bring their vast health care experience along with additional national experts to provide a health care model-based framework to allow health care professionals to utilize the checklists and templates to evaluate their own systems, recognize where the weak links in the system are, and, by applying the well-illustrated principles, improve the efficiency of the system without sacrificing quality patient care. … The health care delivery system is not an assembly line, but with persistence and time following the guidelines offered in this book, quality patient care can be delivered efficiently and affordably while maintaining the financial viability of institutions and practices. ―James Winston Phillips, MD, MBA, JD, LLM

Depression is Highest Among 18-25 Year Olds at 11%.

19% of US Adults Have Anxiety and 56% of Those with Anxiety Are Impaired By Their Condition.

12% of People with Diabetes Have Associated Depression… Resulting in Missed Appointments, Poorer Diet, Decreased Medication Adherence and Increased Complications.

To Address This Problem, The Intermountain Health System Incorporated a Mental Health Provider in Their Primary Care Clinics.

Results: Improved in Diabetes Care, Decreased Hospitalizations and Decreased ER Utilization.

Treating Mental Health Not Only Improves Mental Wellbeing, But Also Lowers Overall Healthcare Costs as Well.

Disclaimer: Dr. Bricker is the Chief Medical Officer of Virtual Care Company First Stop Health.

NOTE: If you or someone you know is considering suicide, please contact the National Suicide Prevention Lifeline at 1800-273-TALK (8255), text “help” to the Crisis Text Line at 741-741 or go to suicidepreventionlifeline.org.

Posted on July 10, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

Dr. David Edward Marcinko is Speaking Up

Dr. David Edward Marcinko MBA CMP® enjoys personal coaching and public speaking and gives as many talks each year as possible, at a variety of medical society and financial services conferences around the country and world.

These have included lectures and visiting professorships at major academic centers, keynote lectures for hospitals, economic seminars and health systems, keynote lectures at city and statewide financial coalitions, and annual keynote lectures for a variety of internal yearly meetings.

His talks tend to be engaging, iconoclastic, and humorous. His most popular presentations include a diverse variety of topics and typically include those in all iMBA, Inc’s textbooks, handbooks, white-papers and most topics covered on this blog.

Posted on July 10, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

It’s official, Dr. David Marcinko, your advocacy is making a big impact!

Just Nominated

Congratulations on your 10th annual WEGO Health Awards nomination. Whether you’re a patient advocate, influencer or collaborator, we’re honored to recognize your contributions to the online health community.

We created the WEGO Health Awards as a way to celebrate and thank the patients and caregivers who support, educate, and inspire others. It’s now our 10th season and the patient leader community is stronger than ever. We could not be more proud to include you as a nominee.

You can expect to hear from us each week with updates and important announcements.

1) The 90s HMOs: Lower Premiums, Lower Out-of-Pocket Costs, Many Many Rules Restricting Care.

2) The 2000s PPOs: High and Even Higher Premiums, Lower Out-of-Pocket Costs, Fewer Rules Restricting Care.

3) The 2010s CDHPs: Lower Premiums, HIGH Out-of-Pocket Costs, Fewer Rules Restricting Care.

The Last 30 Years Have Taught Us that Employer-Sponsored Health Plans CANNOT Have All 3–Low Premiums, Low Out-of-Pocket Costs and Few Care Restrictions.

In the 2020s, Employers Are Moving More of Their Employee Healthcare OUTSIDE of the Traditional Healthcare and Health Insurance System with On-Site Clinics, Near-Site Clinics, Virtual Urgent Care, Virtual Primary Care and Bundled-Payment Centers-of-Excellence.

Posted on July 8, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITION: CRISPR is a family of DNA sequences found in the genomes of prokaryotic organisms such as bacteria and archaea. These sequences are derived from DNA fragments of bacteriophages that had previously infected the prokaryote. They are used to detect and destroy DNA from similar bacteriophages during subsequent infections

For the first time, CRISPR technology has been used to successfully treat diseasein vivo, or inside the human body.

That big medical news was announced Saturday by the biotech startup Intellia Therapeutics and its partner Regeneron, which said their gene-editing techniques reduced the amount of harmful liver protein associated with a genetic nerve disorder.

What is CRISPR? It stands for “clustered regularly interspaced short palindromic repeats,” and it’s one of those things humans found in nature and then copied. Bacteria use CRISPR to repel viruses, but humans have harnessed it to ctrl+c, ctrl+v DNA sequences, potentially leading to a revolution in treating disease. The two scientists who made that breakthrough in 2012, Jennifer Doudna and Emmanuelle Charpentier, won the Nobel Prize in Chemistry last year (Doudna is also a cofounder of Intellia).

Quote du jour: “There’s a feeling like we’re walking through a door here into all kinds of new possibilities. And there’s not many moments in medicine where you get to experience that,” Intellia CEO John Leonard said. Looking ahead…expect Intellia shares, which have gained 233% since its 2016 IPO, to pop.

Posted on July 7, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

BOOK REVIEW

BY ERIC BRICKER MD

Our Brains Have a Reward Chemical Called Dopamine That Causes a Brief Pleasurable Feeling Followed by a Worsening of our Mood.

However, Our Brains Also Have a Contentment Chemical Called Serotonin That Causes Peace and a Calming of our Mood.

Substances and Behaviors That Stimulate Dopamine Include: Sugar, Caffeine, Alcohol, Nicotine, Illicit Drugs, Prescription Narcotics, Social Media Apps, Gambling and Sex.

Substances and Behaviors That Stimulate Serotonin Include: The Amino Acid Tryptophane, Positive Relationships with Others, Service to Others, Prayer and Meditation.

Corporations Tailor Their Products with Dopamine Stimulating Strategies to Increase Sales.

Facebook’s Chamath Palihapitiya Even Admitted on CNBC that Facebook Intentionally Designed its Social Media Platform to Stimulate Dopamine in the User’s Brain To Make Them Use the App More.

Unfortunately, the Constant Stimulation of Dopamine in Our Brains Has Increased Obesity, Metabolic Syndrome, Cancer, Cardiovascular Disease, Diabetes and Depression.

Lustig Estimates That 75% of the $4 Trillion Spent on US Healthcare is for These Diseases That Can Be Traced to Our ‘Hacked Minds.’

Posted on July 7, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

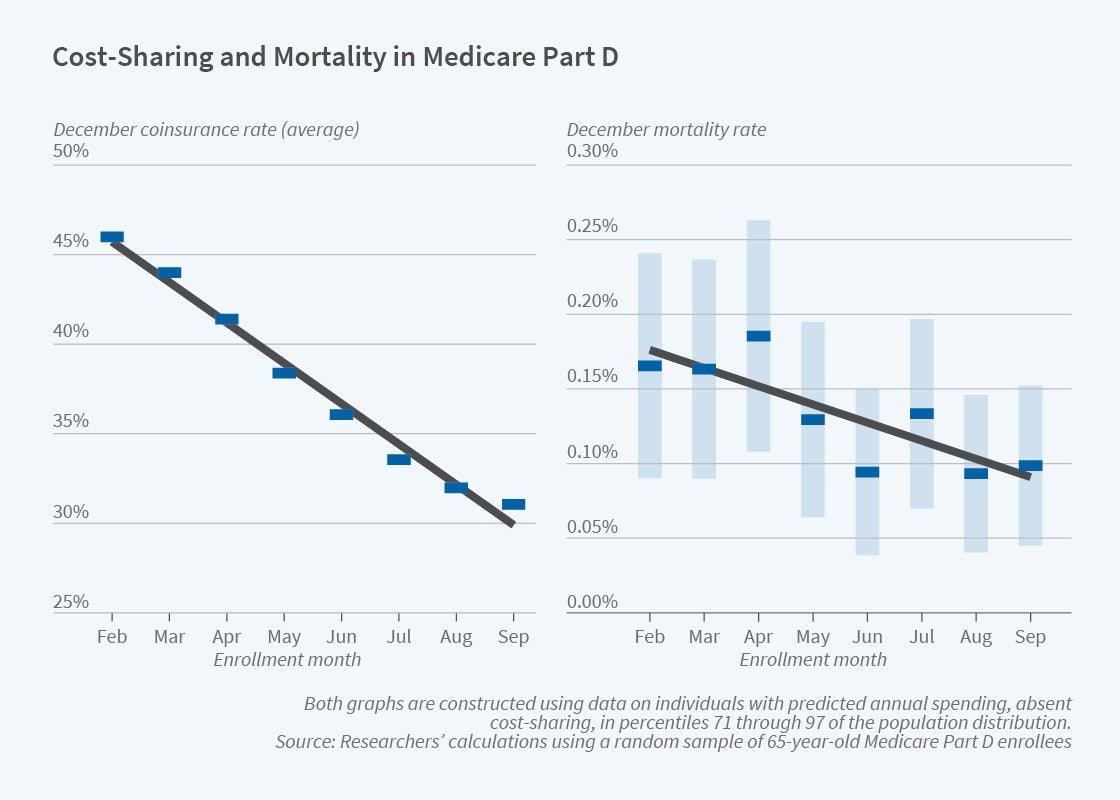

Raises Mortality among Medicare PART D Beneficiaries

QUERY: What are the health consequences when patients reduce their use of prescribed medications in response to higher out-of-pocket costs?

In The Health Costs of Cost-Sharing (NBER Working Paper 28439), researchers Amitabh Chandra, Evan Flack and Ziad Obermeyer use the distinctive out-of-pocket cost-sharing features of Medicare Part D to demonstrate that such reductions can increase mortality.

1) Prospecting: The Strategy of Aaron Ross in Dividing Prospecting into Seeds, Nets and Spears Was Effective in Generating Leads at Compass Professional Health Services.

2) Pitching: The Miller-Heiman Strategy of Identifying Economic, Outcome and Technical Buyers Allows for Effective Pitching to a Buying Team.

3) Closing: The Model of ‘Fit-Risk-Price’ is Essential To Understanding How and When to Close a Sale.

I recently learned from Bloomberg editor David Shipley that the American citizenship test wasn’t standardized until the 1950s, and before that aspiring citizens were quizzed on their understanding of American history by a judge. It was … pretty hard.

Here are several questions you might’ve been asked to become an American citizen in 1944. How would you do? Answers at the bottom of this post.

Which of the following states seceded during the Civil War? Florida, Maryland, Delaware, Kentucky*

Which of these cities has not been a capital of the US? NYC, Boston, Princeton, Philadelphia

Where must all bills intended to raise revenue originate? Popular referendum, the House, the Senate, the president

Which was not one of the original 13 colonies? South Carolina, Massachusetts, Georgia, Maine.

HAVE A GREAT MONDAY OFF

And, thank you if working today.

Citizenship test: 1) Florida seceded 2) Boston wasn’t a capital 3) Bills to raise revenue must originate in the House 4) Maine wasn’t an original colony

Posted on July 5, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

At Least in PartACCORDING TO THESE BOOKS

BY ERIC BRICKER MD

Understandably, Many Doctors Take Issue with This Accusation and Say They Treat Their Patients with Integrity and Accountability. Both Statements May Be TRUE … How is That Possible?

Because of ‘Bad Apples.’

While the Majority of Physicians May Put Their Patients First, There Are a Minority of Physicians that Put Money, Power, Prestige and Promotions Ahead of Patients. It’s These Bad Apples That Ruin Physician Culture.

Problem: Fee-for-Service Rewards Bad Apple Physicians, While Paying the High-Integrity Doctors as Well.

Assessment: If Doctors Want to Keep Fee-for-Service, Then the Bad Apples Must Be Reduced Through 1) Increased Transparency, 2) Greater Doctor Self-Regulation, 3) More Federal Oversight and 4) Increased Employer Investigation.

A “MEME” stock isn’t as easily defined as a growth or value stock, so to give it a definitive categorization would be inappropriate. Nor would actually categorizing it alongside growth and value stocks. They won’t be found in textbooks anytime soon, but to overlook their impact could potentially be an expensive oversight.

Posted on July 2, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

ELECTRIC HEALTH RECORDS

By White Hat Anonymous

Epic Systems, the country’s leading e-health record company, says an algorithm it developed can accurately flag sepsis in patients 76% of the time. The life-threatening disease, which arises from infections, is a major concern for hospitals: One-third of patients who die in hospitals have sepsis, per the CDC.

Generally, the earlier sepsis is diagnosed and treated, the better a patient’s chances of survival—and hundreds of hospitals use Epic Systems’s sepsis prediction model, The Verge reports.

The problem: According to a study published this week in JAMA Internal Medicine, Epic Systems may have gotten the success rate wrong: The model is only correct 63% of the time—“substantially worse than the performance reported by its developer,” the researchers wrote.

Part of the issue can be traced to the algorithm’s development, Stat News reports. It was trained to flag when doctors would submit bills for sepsis treatment—which doesn’t always line up with patients’ first signs of symptoms.

“It’s essentially trying to predict what physicians are already doing,” Dr. Karandeep Singh, study author.

When reached for comment, Epic Systems told us the researchers’ hypothetical scenario lacked “the required validation, analysis, and tuning that organizations need to do before deployment,” adding that the JAMA study’s findings differed from other research.

1) Some Individual Doctors Were Paid Upwards of $5.8 Million Dollars by Medicare in Just a Single Year!

2) The Specialists That Charged Medicare the Most Tended to Be Vascular Surgeons, Ophthalmologists, Oncologists and Cardiologists.

Implications for Employer-Sponsored Health Plans:

1) Medicare Data Can Be Used to Identify High Volume Physicians and Surgeons.

2) The Highest-Costing Doctors Are Concentrated in a Relatively Small Number of Specialties That Can Be Targeted for Detailed Review, Feedback and Possible Exclusion/Steerage Away.

ASSESSMENT: Your thoughts and comments are appreciated.

Many accountable care organizations (ACOs) received disappointing news on May 21, 2021, when the Centers for Medicare & Medicare Services (CMS) announced that it would not be extending the Next Generation ACO (NGACO) model for 2022.

After five years and a dwindling number of participating ACOs, experts were split on whether or not CMS should keep the model in place for another year. On one hand, stakeholders have argued for the NGACO model’s extension until it can be replaced with or integrated into another program; howowever, others asserted that resources could not be properly invested with only one more year left in the program. (Read more…)