BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Multiple‑choice tests are everywhere—schools, professional certifications, job assessments, even driver’s license exams. They’re popular because they can measure a wide range of knowledge quickly, but for the test‑taker, they can feel deceptively tricky. A question with four options looks simple on the surface, yet the difference between two answers may hinge on a single word. Doing well on a multiple‑choice test isn’t just about knowing the material; it’s about approaching the test strategically. With the right mindset and techniques, you can turn what feels like a guessing game into a controlled, confident performance.

The first step in mastering a multiple‑choice test happens before you even look at the questions: managing your time and your mindset. Walking into a test with a calm, focused attitude gives you a huge advantage. Anxiety narrows your thinking, while confidence opens it up. A few deep breaths, a quick mental reset, and a reminder that you’re prepared can shift your entire experience. Once the test begins, skim through it quickly to get a sense of its length and difficulty. This brief overview helps you pace yourself and avoid spending too much time on any single question.

When you begin answering, read each question carefully—more carefully than you think you need to. Multiple‑choice tests often rely on subtle wording. A single phrase like “most likely,” “least effective,” or “except” can completely change what the question is asking. Many students lose points not because they don’t know the material, but because they misread the prompt. Slow down enough to understand the question before you even glance at the answer choices. Sometimes, it helps to cover the options and try to answer the question in your head first. If your internal answer matches one of the choices, that’s a strong sign you’re on the right track.

Once you start evaluating the answer choices, eliminate the obviously wrong ones. Even if you’re unsure of the correct answer, narrowing the field increases your odds and helps you think more clearly. Some choices are designed to distract you—answers that sound familiar, include key terms from the question, or resemble something you studied but don’t actually fit. Cross out anything that is clearly incorrect, overly extreme, or unrelated to the core of the question. This process of elimination is one of the most powerful tools in multiple‑choice testing.

***

***

Another important strategy is to watch out for patterns in the answer choices. Test writers often include distractors that are partially correct or correct in a different context. If two answers seem almost identical, they’re probably not both right; look for the subtle difference that makes one more accurate. Conversely, if one answer is noticeably longer or more detailed than the others, it may be the correct one, since test writers sometimes add qualifiers to ensure accuracy. These patterns aren’t foolproof, but they can help when you’re stuck between options.

Context clues within the test itself can also be surprisingly helpful. Sometimes, one question will indirectly answer another. If you notice repeated terms, definitions, or concepts, use that information to your advantage. Tests are written by humans, and humans tend to repeat themselves. Just be careful not to over‑interpret patterns; use them as hints, not guarantees.

When you encounter a question that completely stumps you, don’t panic. Mark it, skip it, and move on. Getting stuck early can drain your time and confidence. Often, answering other questions jogs your memory or clarifies your thinking, and when you return to the difficult one later, it feels more manageable. This approach keeps your momentum going and prevents frustration from derailing your performance.

Guessing, when necessary, should be strategic rather than random. If you’ve eliminated even one or two options, your odds improve significantly. Look for clues in the wording: answers with absolute terms like “always” or “never” are often incorrect because they leave no room for exceptions. More moderate phrasing tends to be safer. If two answers contradict each other, one of them is likely correct. And if you truly have no idea, choose the option that seems most consistent with the overall logic of the test. A calm, reasoned guess is far better than a panicked one.

As you work through the test, keep an eye on your pacing. Divide the total time by the number of questions to get a rough sense of how long you can spend on each one. If you’re spending too long on a single question, move on. It’s better to answer all the questions you know first and return to the harder ones with whatever time remains. This approach ensures you don’t leave easy points on the table.

***

***

When you finish the last question, resist the urge to submit immediately. Use any remaining time to review your answers. Look especially for questions where you felt uncertain or rushed. However, avoid the temptation to change answers impulsively. Research and experience both show that your first instinct is often correct. Only change an answer if you have a clear, specific reason—such as noticing a misread word or recalling a relevant fact.

Finally, remember that multiple‑choice tests reward clarity of thinking as much as content knowledge. The more you practice these strategies, the more natural they become. Over time, you’ll start to recognize patterns, avoid common traps, and approach each test with greater confidence. Multiple‑choice tests may never be fun, but with the right techniques, they become far less intimidating and far more manageable.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The breakup of the Medical Act represents one of the most significant turning points in the evolution of modern healthcare governance. For decades, the Act served as a foundational framework that regulated medical practice, established professional standards, and defined the relationship between the state, medical institutions, and practitioners. Its dissolution did not occur suddenly; rather, it emerged from a complex interplay of political pressures, professional disputes, and shifting societal expectations. Understanding the breakup requires examining both the structural weaknesses within the Act itself and the broader forces that made its continuation untenable.

At its core, the Medical Act was designed to centralize authority over medical licensing and professional conduct. When it was first introduced, this centralization was seen as a necessary step toward ensuring uniform standards and protecting the public from unqualified practitioners. Over time, however, the rigidity of the Act became a source of tension. Medical knowledge expanded rapidly, new specialties emerged, and healthcare delivery became increasingly complex. Yet the Act remained anchored in assumptions that no longer reflected the realities of modern medicine. Many practitioners argued that the Act constrained innovation, limited professional autonomy, and failed to adapt to new models of care.

One of the major catalysts for the breakup was the growing dissatisfaction among medical professionals who felt that the Act imposed excessive bureaucratic oversight. Licensing procedures, disciplinary mechanisms, and continuing education requirements were often criticized as outdated or overly punitive. Younger practitioners, in particular, viewed the Act as an obstacle to entering the profession, citing long delays, inconsistent evaluation standards, and a lack of transparency. These frustrations fueled calls for reform, but attempts to revise the Act repeatedly stalled due to political disagreements and resistance from established institutions that benefited from the status quo.

Another factor contributing to the breakup was the increasing involvement of non‑physician healthcare providers in delivering essential services. Nurses, physician assistants, pharmacists, and other allied health professionals sought expanded scopes of practice to meet rising patient demand. However, the Medical Act was built around a physician‑centric model that did not easily accommodate these shifts. As collaborative care models became more common, the Act’s limitations became more apparent. Conflicts emerged over authority, responsibility, and professional boundaries, creating friction within the healthcare system. The inability of the Act to adapt to these new dynamics weakened its legitimacy and fueled arguments for its dissolution.

Public expectations also played a significant role. Patients became more informed, more vocal, and more demanding of accountability. They expected transparency in medical decision‑making, greater access to care, and more equitable treatment across communities. Yet the Medical Act was often criticized for protecting professional interests rather than prioritizing patient welfare. High‑profile cases involving malpractice, discrimination, or regulatory failures eroded public trust. Advocacy groups argued that the Act lacked sufficient mechanisms for patient representation and that its disciplinary processes were opaque and slow. As public pressure mounted, political leaders found it increasingly difficult to defend the existing framework.

***

***

The breakup of the Medical Act was ultimately driven by a convergence of these pressures. When reform efforts repeatedly failed, stakeholders began to explore alternative regulatory models. Some advocated for decentralization, arguing that regional or specialty‑specific bodies could respond more effectively to local needs. Others pushed for a more integrated system that would regulate all healthcare professionals under a unified framework, promoting collaboration and reducing duplication. The eventual dissolution of the Act opened the door to these new possibilities, though not without controversy.

The consequences of the breakup have been far‑reaching. On one hand, it created opportunities for modernization. New regulatory structures have been more flexible, more responsive to emerging trends, and more inclusive of diverse healthcare professions. Licensing processes have been streamlined, interdisciplinary collaboration has improved, and patient advocacy has gained a stronger voice in governance. Many practitioners feel that the new system better reflects the realities of contemporary healthcare and supports innovation rather than hindering it.

On the other hand, the transition has not been without challenges. The breakup initially created uncertainty, as practitioners and institutions navigated shifting rules and responsibilities. Some critics argue that decentralization has led to inconsistencies in standards, making it harder to ensure uniform quality of care. Others worry that the new system may lack the strong oversight mechanisms that once protected the public. Balancing flexibility with accountability remains an ongoing struggle, and debates continue over how best to regulate a rapidly evolving healthcare landscape.

In many ways, the breakup of the Medical Act symbolizes a broader transformation in society’s understanding of healthcare. It reflects a shift away from rigid, hierarchical models toward more dynamic, collaborative, and patient‑centered approaches. While the dissolution of such a longstanding framework inevitably brought disruption, it also created space for innovation and reform. The legacy of the Medical Act lives on in the structures that replaced it, shaped by the lessons learned from its strengths and its shortcomings.

Ultimately, the breakup was not merely a legal or administrative event; it was a reflection of changing values, expectations, and realities. As healthcare continues to evolve, the story of the Medical Act serves as a reminder that regulatory systems must remain adaptable, transparent, and responsive to the needs of both practitioners and the public.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

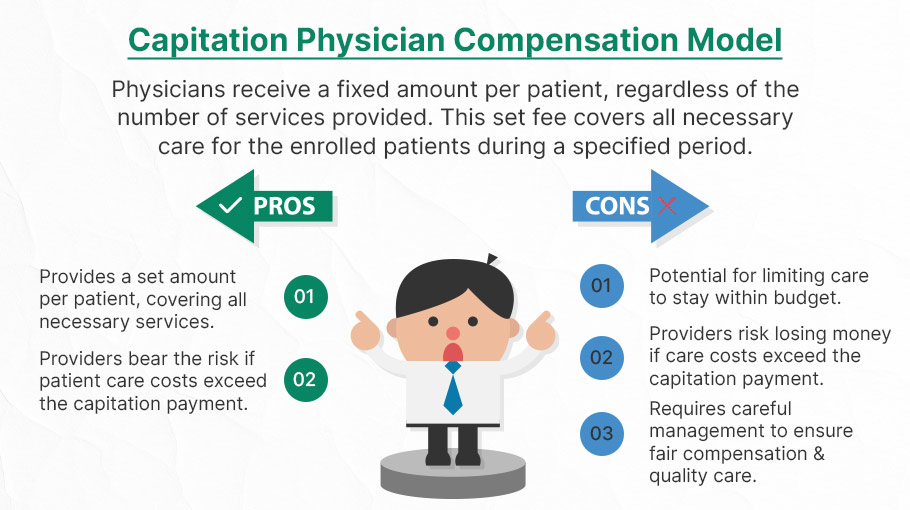

Risk‑based medical payment models have become one of the most significant shifts in modern health‑care financing. They move providers away from the traditional fee‑for‑service structure, where every test, visit, or procedure generates a separate payment, and toward arrangements that reward value, outcomes, and cost‑conscious care. This shift reflects a broader recognition that paying for volume alone can unintentionally encourage overuse, fragmentation, and rising costs. Risk‑based models attempt to realign incentives so that providers are financially accountable for the quality and efficiency of the care they deliver.

At the core of these models is the idea of financial risk transfer. Instead of insurers or government programs bearing the full cost of patient care, providers accept some degree of responsibility for spending that exceeds predetermined benchmarks. The level of risk can vary widely. Upside‑only arrangements allow providers to share in savings if they keep costs below expectations, while downside risk requires them to repay losses if spending surpasses targets. Full‑risk or global‑capitation models go even further, giving providers a fixed per‑patient payment to cover all necessary services. The more risk a provider assumes, the greater the potential reward—but also the greater the potential financial exposure.

***

***

One of the most widely used risk‑based models is the accountable care organization, or ACO. In an ACO, groups of physicians, hospitals, and other clinicians coordinate care for a defined population. They are measured on quality metrics such as preventive care, chronic disease management, and patient experience. If they meet quality standards while keeping total spending below a benchmark, they share in the savings. If they take on two‑sided risk, they may also owe money back when costs exceed expectations. The structure encourages collaboration, data sharing, and proactive management of high‑risk patients, all of which are difficult to achieve in a purely fee‑for‑service environment.

Bundled payments represent another important risk‑based approach. Instead of paying separately for each component of a treatment episode, such as a surgery and its follow‑up care, a bundled payment provides a single, predetermined amount for the entire episode. Providers must work together to deliver care efficiently within that budget. If they can do so while maintaining quality, they keep the difference as savings. If complications or inefficiencies drive costs above the bundle price, they absorb the loss. Bundled payments are particularly effective for procedures with predictable care pathways, such as joint replacements or cardiac interventions, and they encourage standardization and reduction of unnecessary variation.

Capitation, one of the oldest risk‑based models, assigns providers a fixed per‑member, per‑month payment to cover all or most services. This model creates strong incentives for preventive care, early intervention, and careful resource management. When implemented well, capitation can support integrated care delivery and long‑term population health strategies. However, it also requires robust infrastructure, accurate risk adjustment, and safeguards to ensure that cost control does not come at the expense of necessary care. Providers must be able to manage complex patients effectively, and payment rates must reflect the true needs of the population.

Risk adjustment is a critical component across all risk‑based models. Without it, providers who care for sicker or more socially complex patients could be unfairly penalized. Risk adjustment uses demographic and clinical data to estimate expected costs for each patient, ensuring that benchmarks and payments reflect the underlying health status of the population. Accurate risk adjustment protects against adverse selection and supports fairness, but it also requires sophisticated data systems and careful oversight to prevent gaming or upcoding.

Despite their promise, risk‑based payment models face challenges. Providers must invest in care‑management teams, data analytics, and interoperable technology to succeed. Smaller practices may struggle with the administrative and financial demands of taking on risk. Patients may also experience confusion if networks narrow or if care pathways become more structured. Policymakers and payers must balance incentives for efficiency with protections that ensure access and quality.

***

***

Even with these complexities, risk‑based models continue to expand because they offer a path toward a more sustainable and patient‑centered health‑care system. By rewarding outcomes rather than volume, they encourage providers to focus on prevention, coordination, and long‑term health. They also create opportunities for innovation in care delivery, from telehealth to home‑based services to integrated behavioral health. As health‑care costs continue to rise, risk‑based payment models represent a strategic attempt to align financial incentives with the goals of better care, healthier populations, and more efficient use of resources.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The Doctor of Science (ScD) degree occupies a distinctive place within the landscape of advanced academic and professional education. Although less commonly discussed than the PhD, the ScD represents a rigorous pathway for individuals seeking to contribute original, high‑level research to scientific and technical fields. Its history, structure, and contemporary relevance reveal a degree designed to cultivate deep expertise, methodological sophistication, and the capacity to solve complex problems through systematic inquiry.

At its core, the ScD is a research doctorate. Like the PhD, it requires candidates to demonstrate mastery of a discipline, identify a meaningful research question, and produce a dissertation that advances knowledge. The distinction between the two degrees is often more cultural than structural. In many institutions, the ScD is awarded in fields with a strong quantitative or applied scientific orientation, such as engineering, public health, computer science, or biostatistics. This association with technical disciplines has shaped the perception of the ScD as a degree emphasizing analytical rigor and practical impact.

The structure of ScD programs typically mirrors that of PhD programs: coursework, comprehensive examinations, and a multi‑year research project culminating in a dissertation. However, the ScD often places additional emphasis on methodological training and the application of scientific principles to real‑world challenges. Students may engage in interdisciplinary collaborations, work with industry or government partners, or contribute to large‑scale research initiatives. This applied orientation reflects the degree’s historical roots in scientific problem‑solving and its ongoing relevance in fields where research is closely tied to practice.

***

***

One of the defining features of the ScD is its flexibility across institutions. Some universities treat the ScD and PhD as interchangeable, differing only in name. Others reserve the ScD for specific departments or use it to signal a particular research tradition. This variability can create confusion, but it also highlights the degree’s adaptability. Rather than being constrained by a single definition, the ScD evolves to meet the needs of the disciplines it serves. In engineering, for example, the ScD may emphasize design, modeling, and innovation. In public health, it may focus on epidemiological methods, population‑level analysis, and the development of evidence‑based interventions.

Despite these variations, the ScD consistently demands a high level of intellectual independence. Candidates are expected not only to master existing knowledge but also to generate new insights. This process requires creativity, persistence, and the ability to navigate uncertainty. The dissertation, as the capstone of the degree, serves as a demonstration of these qualities. It is both a scholarly contribution and a testament to the candidate’s readiness to join the community of researchers and practitioners who shape scientific progress.

The value of the ScD extends beyond academia. Graduates often pursue careers in government agencies, research institutes, private industry, and nonprofit organizations. Their training equips them to analyze complex systems, design data‑driven solutions, and lead interdisciplinary teams. In an era defined by rapid technological change and global challenges—from climate science to public health—these skills are increasingly essential. The ScD prepares individuals not only to understand scientific problems but to address them with rigor and creativity.

Another important dimension of the ScD is its role in promoting scientific leadership. The degree cultivates the ability to communicate research findings, mentor emerging scholars, and contribute to the development of scientific policy and practice. Graduates may become faculty members, research directors, or technical experts whose work influences both scientific understanding and societal outcomes. The ScD thus serves as a bridge between advanced scholarship and practical impact.

In contemporary discussions about doctoral education, the ScD stands as a reminder that scientific inquiry is both a theoretical and applied endeavor. While the PhD remains the most widely recognized research doctorate, the ScD offers an alternative pathway that aligns closely with the needs of technical and scientific fields. Its emphasis on methodological depth, interdisciplinary collaboration, and real‑world application makes it a compelling option for individuals committed to advancing science in ways that directly benefit society.

Ultimately, the Doctor of Science degree represents a commitment to rigorous research and meaningful contribution. It embodies the belief that scientific knowledge, when pursued with discipline and imagination, has the power to illuminate complex problems and drive innovation. For students drawn to this mission, the ScD offers a challenging and rewarding journey into the heart of scientific discovery.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

A multiple‑choice test is one of the most widely used assessment formats in education, professional certification, and psychological measurement. Its defining feature is simple: each question presents a prompt and a set of possible answers, from which the test‑taker must select the correct or best option. Although the structure appears straightforward, the multiple‑choice test is a sophisticated tool shaped by decades of research on learning, cognition, and measurement. Understanding what a multiple‑choice test is requires looking beyond its surface format and examining its purpose, design, strengths, limitations, and the ways it influences how people learn and demonstrate knowledge.

The Structure and Purpose of Multiple‑Choice Tests

At its core, a multiple‑choice test is designed to measure knowledge, skills, or reasoning in a standardized and efficient way. Each question—often called an “item”—contains two main parts: the stem and the alternatives. The stem presents the problem, scenario, or question. The alternatives include one correct answer, known as the key, and several incorrect answers, known as distractors. The test‑taker’s task is to identify the key among the distractors.

This structure serves a clear purpose: to evaluate whether someone can recognize accurate information or apply knowledge to a specific situation. Because the answer choices are predetermined, scoring can be objective and consistent. This makes multiple‑choice tests particularly useful in large‑scale settings such as school exams, professional licensing tests, and standardized assessments. They allow thousands—or even millions—of people to be evaluated using the same criteria, with results that can be compared fairly across individuals and groups.

Designing Effective Multiple‑Choice Questions

Although the format seems simple, writing high‑quality multiple‑choice questions is a demanding process. A good item must be clear, unambiguous, and aligned with the skill or concept being assessed. The stem should present a meaningful problem rather than a trivial fact, and the distractors must be plausible enough to challenge someone who has not fully mastered the material.

The best multiple‑choice questions do more than test memorization. They can assess higher‑order thinking by asking test‑takers to analyze scenarios, apply principles, evaluate evidence, or solve problems. For example, a question in a biology exam might present a real‑world situation and ask which explanation best fits the observed data. In this way, multiple‑choice tests can measure complex reasoning when they are carefully constructed.

Another important aspect of design is fairness. A well‑designed test avoids cultural bias, overly tricky wording, or clues that unintentionally reveal the answer. The goal is to measure knowledge or skill—not reading speed, test‑taking tricks, or familiarity with a particular cultural reference. Achieving this level of fairness requires careful review, pilot testing, and revision.

***

***

Strengths of Multiple‑Choice Tests

One of the major strengths of multiple‑choice tests is efficiency. They allow instructors and institutions to assess a large amount of content in a relatively short time. Because scoring is objective, results can be processed quickly and consistently, reducing the potential for human error or subjective judgment.

Another advantage is reliability. When items are well‑designed, multiple‑choice tests can produce stable and repeatable results. This reliability is crucial in high‑stakes settings such as medical licensing exams or university admissions, where decisions must be based on trustworthy measures.

Multiple‑choice tests also offer diagnostic value. Patterns of correct and incorrect responses can reveal which concepts students understand and which require further instruction. For teachers, this information can guide lesson planning and targeted support. For learners, it can highlight strengths and weaknesses, helping them focus their study efforts more effectively.

Finally, multiple‑choice tests can assess a wide range of cognitive skills. While they are often associated with factual recall, they can also measure comprehension, application, analysis, and even aspects of critical thinking. The key is thoughtful item design that challenges students to use knowledge rather than simply recognize it.

Limitations and Criticisms

Despite their strengths, multiple‑choice tests are not without limitations. One common criticism is that they encourage guessing. Because the correct answer is always present, a test‑taker might select it by chance rather than through understanding. While this effect can be reduced by including more distractors or using statistical scoring methods, it cannot be eliminated entirely.

Another limitation is that multiple‑choice tests may oversimplify complex skills. Some abilities—such as writing, creativity, collaboration, or open‑ended problem solving—cannot be captured well through fixed response options. For example, evaluating a student’s ability to construct a persuasive argument or design an experiment requires formats that allow for extended responses.

Multiple‑choice tests can also create a narrow focus on test preparation. When students know they will be assessed through this format, they may prioritize memorizing isolated facts rather than developing deeper understanding. This phenomenon, sometimes called “teaching to the test,” can limit the richness of learning experiences.

Additionally, poorly written items can introduce bias or confusion. Ambiguous wording, irrelevant details, or distractors that are obviously incorrect can distort results. In such cases, the test may measure test‑taking ability more than actual knowledge.

The Role of Multiple‑Choice Tests in Learning

Multiple‑choice tests influence not only how knowledge is measured but also how it is learned. When used thoughtfully, they can reinforce learning by encouraging retrieval practice—the act of recalling information from memory. Research shows that retrieval strengthens memory and improves long‑term retention. Taking a multiple‑choice test can therefore help students learn, not just demonstrate what they know.

However, the impact depends on how the tests are integrated into instruction. Frequent low‑stakes quizzes can support learning by providing regular opportunities for practice and feedback. In contrast, high‑stakes exams that determine grades or advancement may create anxiety and narrow students’ focus to short‑term performance.

Multiple‑choice tests can also support metacognition. When students review their results, they gain insight into what they understand and where they need improvement. This self‑awareness is a key component of effective learning.

Why Multiple‑Choice Tests Persist

Despite ongoing debates about their limitations, multiple‑choice tests remain a central part of modern assessment. Their persistence is not simply a matter of convenience. They offer a combination of efficiency, reliability, and scalability that few other formats can match. In large educational systems, they provide a practical way to evaluate learning across diverse populations.

Moreover, advances in test design have expanded what multiple‑choice tests can measure. Computer‑based testing allows for adaptive assessments that adjust difficulty based on performance, providing a more precise measure of ability. Scenario‑based items can simulate real‑world decision‑making, making the test more authentic and meaningful.

Conclusion

A multiple‑choice test is far more than a set of questions with predetermined answers. It is a carefully designed tool for measuring knowledge, reasoning, and understanding. Its structure allows for efficient, objective, and reliable assessment, making it invaluable in educational and professional contexts. At the same time, its limitations remind us that no single format can capture the full range of human abilities.

When used thoughtfully, multiple‑choice tests can support learning, provide meaningful feedback, and help institutions make informed decisions. Understanding what they are—and what they are not—allows educators and learners to use them more effectively. Ultimately, the multiple‑choice test endures because it strikes a balance between practicality and precision, offering a structured way to evaluate what people know in an increasingly complex world.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

A forensic accountant is a financial professional who blends traditional accounting expertise with investigative skills to uncover, analyze, and explain financial irregularities. While many people associate accounting with routine bookkeeping or tax preparation, forensic accounting operates in a very different arena—one where money trails intersect with legal disputes, fraud schemes, and complex financial conflicts. The role requires not only technical knowledge of accounting principles but also the curiosity of an investigator and the clarity of a communicator who can translate intricate financial data into understandable conclusions.

At its core, forensic accounting involves the examination of financial information for use in legal settings. The word “forensic” itself means “suitable for use in court,” which captures the essence of the profession. Forensic accountants are often called upon when financial information must be scrutinized with a level of detail and rigor that can withstand legal scrutiny. Their work may support civil litigation, criminal investigations, insurance claims, business valuations, or internal corporate inquiries. Because of this, they frequently collaborate with attorneys, law enforcement agencies, regulatory bodies, and corporate leadership.

One of the most recognized responsibilities of a forensic accountant is the detection and investigation of fraud. Fraud can take many forms—embezzlement, financial statement manipulation, asset misappropriation, or complex schemes involving shell companies and hidden transactions. Forensic accountants use a combination of analytical procedures, data mining techniques, and professional skepticism to identify patterns that suggest wrongdoing. They may trace the flow of funds through multiple accounts, reconstruct destroyed or incomplete records, or analyze inconsistencies in financial statements. Their goal is not only to uncover what happened but also to determine how it happened and who was responsible.

Beyond fraud detection, forensic accountants play a crucial role in litigation support. In legal disputes involving financial matters, attorneys rely on forensic accountants to provide objective, evidence‑based analysis. This may include calculating economic damages, evaluating the value of a business, assessing lost profits, or determining the financial impact of a breach of contract. In divorce proceedings, forensic accountants may help identify hidden assets or evaluate the true income of a spouse. Their findings often become part of expert reports submitted to the court, and they may be called to testify as expert witnesses. In this capacity, they must present complex financial information in a clear, concise manner that judges and juries can understand.

Another important aspect of forensic accounting is prevention. Organizations increasingly recognize the value of proactive measures to reduce the risk of fraud and financial misconduct. Forensic accountants may design internal controls, conduct risk assessments, or evaluate corporate governance practices to help organizations strengthen their defenses. By identifying vulnerabilities before they are exploited, they contribute to a healthier financial environment and help protect stakeholders from potential losses.

The skill set required for forensic accounting is broad and demanding. Technical proficiency in accounting and auditing is essential, but equally important are analytical thinking, attention to detail, and strong communication skills. Forensic accountants must be able to interpret large volumes of financial data, identify anomalies, and draw logical conclusions. They must also be comfortable working with digital tools, as modern investigations often involve electronic records, data analytics, and specialized software. Integrity and objectivity are critical, given the legal implications of their work and the trust placed in their findings.

The profession also requires adaptability. Every case is different, and forensic accountants must be prepared to navigate unfamiliar industries, evolving fraud techniques, and changing regulatory environments. They may work in public accounting firms, government agencies, law enforcement units, insurance companies, or as independent consultants. Regardless of the setting, the common thread is their role as financial detectives who bring clarity to situations where the truth is obscured by complexity or deception.

In summary, a forensic accountant is far more than a traditional number‑cruncher. They are investigators, analysts, communicators, and trusted advisors who operate at the intersection of finance and law. Their work uncovers hidden truths, supports the pursuit of justice, and helps organizations safeguard their financial integrity. As financial systems grow more complex and fraud schemes become more sophisticated, the role of the forensic accountant continues to expand in importance. Their unique blend of skills makes them indispensable in a world where transparency and accountability are more critical than ever.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The Net Investment Income Tax (NIIT) occupies a distinctive place in the modern U.S. tax landscape. Introduced as part of the Affordable Care Act, it was designed to generate revenue from higher‑income households by taxing certain forms of unearned income. Although it affects a relatively small portion of taxpayers, its implications reach into investment strategy, tax planning, and broader debates about fairness and economic policy. Understanding how the NIIT works—and why it exists—offers insight into the evolving relationship between tax policy and wealth in the United States.

At its core, the NIIT is a 3.8 percent surtax applied to specific types of investment income for individuals whose modified adjusted gross income exceeds statutory thresholds. These thresholds—$200,000 for single filers and $250,000 for married couples filing jointly—are not indexed for inflation. As a result, over time, more taxpayers may find themselves subject to the tax even if their real purchasing power has not increased. This “bracket creep” is one of the subtle but important features of the NIIT, shaping its long‑term reach.

The tax applies only to “net investment income,” a term that includes interest, dividends, capital gains, rental income, royalties, and passive business income. It does not apply to wages, self‑employment earnings, or distributions from qualified retirement plans. The logic behind this distinction is straightforward: the NIIT targets income derived from wealth rather than labor. In practice, this means that two taxpayers with identical total income may face different NIIT liabilities depending on how much of their income comes from investments versus work.

The mechanics of the NIIT involve a comparison between two amounts: net investment income and the excess of modified adjusted gross income over the applicable threshold. The tax is applied to whichever of these two figures is smaller. This structure ensures that the NIIT functions as a surtax on high‑income households without taxing investment income for those below the threshold. It also means that taxpayers with large investment portfolios but modest overall income may avoid the tax entirely, while those with high wages and relatively small investment income may still owe it.

One of the most significant effects of the NIIT is its influence on investment behavior. Because the tax applies to capital gains, it can affect decisions about when to sell appreciated assets. Taxpayers may choose to time sales to avoid pushing their income above the threshold in a given year. Others may shift toward tax‑exempt investments, such as municipal bonds, or toward assets that generate unrealized rather than realized gains. The NIIT therefore becomes not just a revenue tool but a factor shaping the broader investment landscape.

The tax also interacts with other parts of the tax code in ways that can be complex. For example, rental real estate income is generally subject to the NIIT unless the taxpayer qualifies as a real estate professional and materially participates in the activity. Trusts and estates face their own NIIT rules, often reaching the surtax threshold at much lower income levels than individuals. These layers of complexity mean that the NIIT is often a central topic in tax planning for high‑income households, especially those with diverse investment portfolios.

Beyond its technical features, the NIIT reflects broader policy debates about equity and the distribution of tax burdens. Supporters argue that it helps ensure that high‑income individuals contribute a fair share to the cost of public programs, particularly those related to health care. Because investment income is disproportionately concentrated among wealthier households, the NIIT is seen as a way to align tax policy with ability to pay. Critics, however, contend that the tax discourages investment, adds unnecessary complexity, and imposes an additional layer of taxation on income that may already be subject to corporate taxes or other levies.

Despite these debates, the NIIT has become a stable part of the federal tax system. It raises billions of dollars annually and plays a role in funding health‑related initiatives. As discussions about tax reform continue, the NIIT often resurfaces as policymakers consider how best to balance revenue needs with economic incentives. Whether it remains unchanged, is expanded, or is modified in future legislation, the NIIT will continue to shape the financial decisions of high‑income taxpayers and contribute to the ongoing conversation about how the United States taxes wealth.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The history of U.S. recessions reflects the nation’s evolving economy, shaped by wars, financial crises, policy shifts, and global events. Since 1857, the U.S. has experienced over 30 recessions, each offering lessons in resilience and reform.

The United States has endured a long and varied history of economic recessions, defined as periods of significant decline in economic activity lasting more than a few months. These downturns are typically marked by falling GDP, rising unemployment, and reduced consumer spending. Since the mid-19th century, recessions have been triggered by a range of factors—from banking panics and inflation to global conflicts and pandemics.

The earliest recorded U.S. recession began in 1857, sparked by a banking crisis and declining international trade. This was followed by the Long Depression of 1873–1879, which lasted a staggering 65 months, making it the longest in U.S. history. The downturn was triggered by the collapse of a major bank and a speculative bubble in railroad investments.

The Great Depression remains the most severe economic crisis in American history. Beginning in 1929 after the stock market crash, it lasted until 1933 and saw unemployment soar to 25%. The Depression reshaped U.S. economic policy, leading to the creation of Social Security, the FDIC, and other New Deal programs aimed at stabilizing the economy and protecting citizens.

Post-World War II recessions were generally shorter and less severe. The 1945 recession, for example, lasted eight months and was caused by the transition from wartime to peacetime production. The 1973–75 recession, however, was more prolonged, driven by an oil embargo and stagflation—a combination of stagnant growth and high inflation.

The early 1980s recession was triggered by the Federal Reserve’s aggressive interest rate hikes to combat inflation. Though painful, it ultimately helped stabilize prices and set the stage for a long period of growth. The early 1990s recession followed a savings and loan crisis and a slowdown in defense spending after the Cold War.

The Great Recession of 2007–2009 was the most significant downturn since the Great Depression. It was caused by the collapse of the housing bubble and widespread failures in financial institutions. Unemployment peaked at 10%, and the crisis led to sweeping reforms in banking and mortgage lending practices.

Most recently, the COVID-19 recession in 2020 was the shortest in U.S. history, lasting just two months. Despite its brevity, it was severe, with unemployment briefly reaching 14.7% due to lockdowns and global supply chain disruptions.

Throughout its history, the U.S. has shown remarkable resilience in recovering from recessions. Each downturn has prompted changes in fiscal and monetary policy, regulatory reform, and shifts in public perception about the role of government and markets. As the economy becomes more interconnected globally, future recessions may be shaped by international events as much as domestic ones.

SPEAKING: ME-P Editor Dr. David Edward Marcinko MBA MEd will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Did you know that desperate doctors of all ages are turning to knowledgeable financial advisors and medical management consultants for help? Symbiotically too, generalist advisors are finding that the mutual need for knowledge and extreme niche synergy is obvious.

***

***

But, there was no established curriculum or educational program; no corpus of knowledge or codifying terms-of-art; no academic gravitas or fiduciary accountability; and certainly no identifying professional designation that demonstrated integrated subject matter expertise for the increasingly unique healthcare focused financial advisory niche … Until Now!

So, if you are looking to supplement your knowledge, income and designations; and find other qualified professionals you may want to consider the CMP® program.

Enter the Certified Medical Planner™ charter professional designation. And, CMPs™ are FIDUCIARIES, 24/7.

Channel Surfing the ME-P

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

***

***

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

The economics of information explores how knowledge—or the lack of it—affects decision-making, market behavior, and resource allocation. It reveals why perfect competition rarely exists and why information itself can be a powerful economic asset.

Economics of Information: Understanding the Value and Impact of Knowledge

In traditional economic models, markets are often assumed to operate under perfect information—where all participants have equal access to relevant data. However, in reality, information is often incomplete, asymmetric, or costly to obtain. The field known as economics of information emerged to address these discrepancies, fundamentally reshaping how economists understand markets, incentives, and efficiency.

One of the core concepts in this field is information asymmetry, where one party in a transaction possesses more or better information than the other. This imbalance can lead to adverse selection and moral hazard. For example, in the insurance market, individuals who know they are high-risk are more likely to seek coverage, while insurers may struggle to differentiate between high- and low-risk clients. Similarly, in lending, borrowers may have private knowledge about their ability to repay, which lenders cannot easily verify.

To mitigate these problems, economists have developed mechanisms such as signaling and screening. Signaling occurs when the informed party takes action to reveal their type—like a job applicant earning a degree to signal competence. Screening, on the other hand, involves the uninformed party designing tests or contracts to elicit information—such as offering different insurance packages to separate risk levels.

Another important area is the cost of acquiring information. Gathering data, analyzing trends, or verifying facts requires time and resources. This leads to decisions being made under uncertainty, where individuals rely on heuristics or limited data. The economics of information examines how these costs influence behavior, pricing, and market structure. For instance, consumers may not compare every available product due to search costs, allowing firms to maintain price dispersion.

The rise of digital technology has intensified the relevance of this field. In the age of big data, companies like Google and Amazon thrive by collecting and analyzing vast amounts of user information. This data allows them to personalize services, predict behavior, and gain competitive advantages. However, it also raises concerns about privacy, market power, and inequality—issues that economists of information are increasingly addressing.

Moreover, information goods—such as software, media, and research—have unique economic properties. They are often non-rivalrous and can be reproduced at near-zero marginal cost. This challenges traditional pricing models and calls for innovative approaches like freemium strategies, bundling, and subscription services.

In public policy, the economics of information plays a crucial role in designing regulations, transparency standards, and consumer protections. Governments must balance the need for open access to information with incentives for innovation and investment. For example, patent laws aim to encourage research by granting temporary monopolies, while disclosure requirements in finance promote market integrity.

In conclusion, the economics of information reveals that knowledge is not just a passive input but a dynamic force shaping economic outcomes. By understanding how information is produced, distributed, and used, economists can better explain real-world phenomena and design systems that promote fairness, efficiency, and innovation.

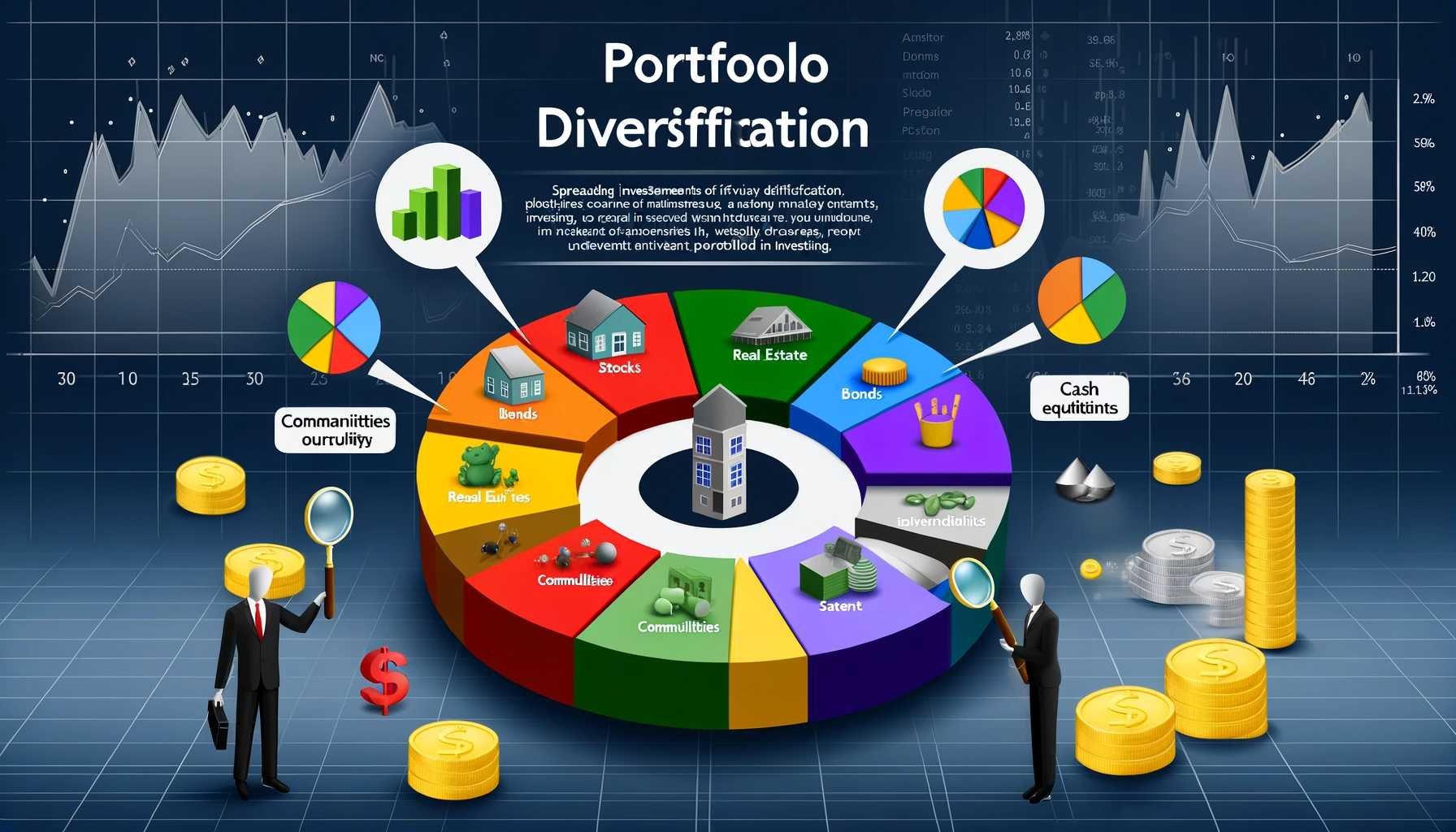

In the world of financial advising, few principles are as foundational—and as misunderstood—as diversification. Clients often come to advisors hoping for bold moves and big wins. Yet the most prudent strategy we offer is not a thrilling stock pick or a market-timing miracle, but a quiet, calculated spread of risk. Diversification, in essence, is the art of saying “sorry” in advance—for not chasing every hot trend, for not going all-in, and for not promising perfection. But it’s also the strategy that earns trust, builds resilience, and delivers long-term value.

Diversification means allocating assets across different sectors, geographies, and investment vehicles to reduce exposure to any single point of failure. For financial advisors, it’s not just a portfolio tactic—it’s a philosophy of humility. It acknowledges that markets are unpredictable, that no one can consistently forecast winners, and that protecting capital is just as important as growing it.

Clients may initially resist this approach. They might question why their portfolio includes lagging sectors or why we’re not doubling down on tech or crypto. This is where our role as educators becomes critical. We explain that diversification isn’t about avoiding risk—it’s about managing it. It’s the reason why, when tech stumbles, healthcare or consumer staples might hold steady. It’s why international exposure can buffer domestic volatility. And it’s why fixed income still matters, even in a rising-rate environment.

The challenge for advisors is that diversification rarely feels heroic. It doesn’t make headlines. It doesn’t deliver overnight gains. Instead, it delivers consistency. It smooths out the ride. It allows clients to sleep at night. And over time, it compounds into something powerful: confidence.

***

***

One of the most effective ways to communicate this is through behavioral coaching. We remind clients that diversification is designed to protect them from their own impulses—from chasing trends, reacting to headlines, or panicking during downturns. It’s a guardrail against emotional investing. And when markets inevitably wobble, diversified portfolios give us the credibility to say, “This is why we planned ahead.”

Moreover, diversification is a relationship tool. It shows clients that we’re not betting their future on a single idea. We’re building something durable. We’re thinking about their retirement, their children’s education, their legacy. And we’re doing it with a strategy that’s built to last.

In short, diversification may feel like an apology to the thrill-seeker in every investor. But it’s also a promise: that we’re here to protect, to guide, and to deliver results that matter—not just today, but for decades to come.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

Pet insurance offers financial protection and peace of mind for pet owners, helping cover unexpected veterinary costs and ensuring pets receive timely care. It’s a growing industry that reflects the deepening bond between humans and their animal companions.

Pet insurance is a specialized health coverage designed to offset the cost of veterinary care for pets. As veterinary medicine advances, treatments for pets have become more sophisticated—and expensive. From emergency surgeries to chronic illness management, the financial burden can be overwhelming for pet owners. Pet insurance helps mitigate these costs, allowing owners to prioritize their pet’s health without worrying about the price tag.

One of the primary benefits of pet insurance is financial security. Veterinary bills can range from hundreds to thousands of dollars depending on the condition. For example, treating a torn ACL in a dog can cost upwards of $3,000, while cancer treatments may exceed $10,000. With pet insurance, a significant portion of these expenses can be reimbursed, reducing out-of-pocket costs and making advanced care more accessible.

Another advantage is flexibility in care. Pet insurance empowers owners to choose treatments based on medical need rather than financial constraints. Whether it’s a late-night emergency or a long-term condition like diabetes or arthritis, insurance gives pet parents the freedom to pursue the best care options available.

Policies typically cover accidents, illnesses, surgeries, medications, and sometimes routine care like vaccinations and dental cleanings. However, coverage varies widely by provider and plan. Most policies exclude pre-existing conditions and have waiting periods before coverage begins. It’s crucial for pet owners to read the fine print and understand what’s included and what’s not. The cost of pet insurance depends on factors such as the pet’s species, breed, age, and location. Monthly premiums can range from $20 to $70 for dogs and $10 to $40 for cats. While this may seem like an added expense, it can be a worthwhile investment in the long run—especially for breeds prone to genetic conditions or pets with active lifestyles.

Pet insurance also reflects a broader cultural shift in how society views pets. No longer just animals, pets are considered family members. This emotional bond drives owners to seek the best possible care, and insurance helps make that care attainable. It’s not just about saving money—it’s about ensuring quality of life for beloved companions.

Critics argue that pet insurance isn’t always cost-effective, especially if a pet remains healthy. So, pet insurance may not be worth it if:

Your pet is a senior or has health problems.

A big vet bill wouldn’t be a financial hardship for you.

You’d rather take the risk of an expensive diagnosis than pay for insurance you might never use.

However, the unpredictability of accidents and illness makes it a valuable safety net. Like any insurance, it’s about preparing for the unexpected.

In conclusion, pet insurance is a practical and compassionate tool for modern pet ownership. It offers financial relief, expands treatment options, and supports the emotional commitment people have to their pets.

As veterinary costs continue to rise, pet insurance provides a way to protect both your wallet and your furry friend’s well-being.; maybe!

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

In the competitive world of financial services, attracting and retaining clients is a constant challenge. To stand out, many financial advisors employ strategic marketing tactics known as “loss leaders”—free or discounted services designed to showcase value and build trust. These offerings serve as entry points for potential clients, allowing advisors to demonstrate expertise and initiate long-term relationships.

One of the most common loss leaders is the free initial consultation. This no-obligation meeting gives prospective clients a chance to discuss their financial goals, ask questions, and get a feel for the advisor’s approach. For the advisor, it’s an opportunity to assess the client’s needs and present tailored solutions. While no revenue is generated from this meeting, it often leads to paid engagements once the client feels confident in the advisor’s capabilities.

Another popular tactic is offering a complimentary financial plan or portfolio review. These services provide tangible insights into a client’s current financial situation and suggest improvements. By delivering real value upfront, advisors build credibility and demonstrate their analytical skills. Clients who receive actionable advice are more likely to continue working with the advisor on a paid basis.

Educational content also plays a key role in loss leader strategy. Advisors frequently host free webinars, workshops, or seminars on topics like retirement planning, tax strategies, or investment basics. These events not only educate attendees but also position the advisor as a thought leader. Attendees often leave with a better understanding of their financial needs and a desire to seek personalized guidance.

In the digital realm, advisors may offer free tools and assessments on their websites. These include retirement readiness calculators, risk tolerance quizzes, and budgeting templates. Such tools engage users and provide personalized feedback, creating a natural segue into one-on-one consultations. Additionally, offering free newsletters or eBooks helps advisors stay top-of-mind while delivering ongoing value.

Some advisors go further by waiving fees for introductory services, such as account setup or the first few months of investment management. This lowers the barrier to entry and encourages hesitant clients to try the service. Once clients experience the benefits, they’re more likely to commit long-term.

Loss leaders are not limited to high-net-worth individuals. Advisors targeting younger or less affluent clients may offer free debt management plans or budgeting assistance. These services address immediate concerns and build loyalty among clients who may become more profitable as their financial situations improve.

Ultimately, loss leaders are about building relationships. By offering something of value without immediate compensation, financial advisors demonstrate their commitment to helping clients succeed. This fosters trust, encourages engagement, and often leads to lasting partnerships. In a field where reputation and reliability are paramount, loss leaders serve as powerful tools for growth and differentiation.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Classic Definition: Scientific research depends on the referencing and citing of other research.

Modern Circumstance: The Google Scholar Paradox is that research which gets cited most often is whatever shows up in the top results of Google Scholar searches; regardless of its contribution to the field.

Paradox Example: The Google Scholar effect is a phenomenon when some medical and healthcare researchers pick and cite works appearing in the top results on Google Scholar regardless of their contribution to the citing publication.

Paradoxically they automatically assume these works’ credibility and believe that editors, reviewers, and readers expect to see these citations.

Insurance agents are primarily paid through commissions, but may also earn salaries, bonuses, and fees depending on their employment model and the types of policies they sell.

Insurance agents play a vital role in helping individuals and businesses navigate the complex world of insurance. Their compensation structures vary widely, influenced by factors such as the type of insurance they sell, whether they work independently or for a company, and the specific agreements they have with insurers. Understanding how insurance agents are paid is essential for consumers who want to make informed decisions and for aspiring agents considering a career in the industry.

The most common form of compensation for insurance agents is commission-based pay. Agents earn a percentage of the premium paid by the customer when they successfully sell a policy. These commissions can vary depending on the type of insurance. For example, first-year commissions for auto and homeowners insurance typically range from 5% to 20%, while commercial property and casualty policies may offer 10% to 15%. Life insurance policies often provide higher initial commissions, sometimes exceeding 50% of the first-year premium, followed by smaller renewal commissions in subsequent years.

There are two main types of insurance agents: captive agents and independent agents. Captive agents work exclusively for one insurance company and usually receive a combination of salary and commissions. Their compensation may also include performance bonuses and incentives tied to sales targets. Independent agents, on the other hand, represent multiple insurers and rely more heavily on commissions. They have the flexibility to offer a wider range of products, but their income is directly tied to their ability to sell policies and maintain client relationships.

***

***

In addition to commissions, some agents earn fees for services such as policy reviews, risk assessments, or consulting. These fees are more common in commercial insurance or financial planning contexts, where agents provide specialized expertise. However, fee-based compensation is less prevalent in personal lines of insurance like auto or home coverage.

Bonuses and incentives are another component of agent compensation. Insurance companies often reward agents for meeting sales quotas, retaining clients, or selling specific types of policies. These bonuses can significantly boost an agent’s income, but they may also create potential conflicts of interest if agents prioritize higher-paying products over client needs.

Some agents, particularly those employed by large firms or call centers, receive a fixed salary. This model provides stability but may limit earning potential compared to commission-based roles. Salaried agents may still receive performance bonuses or profit-sharing depending on company policy.

Ultimately, an insurance agent’s earnings depend on their business model, experience, and ability to build a loyal client base. While commissions remain the cornerstone of insurance compensation, the rise of fee-based services and hybrid models reflects a shift toward more transparent and client-focused practices.

Consumers should feel empowered to ask agents about their compensation structure to ensure they receive unbiased advice tailored to their needs.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

A paradox is a figure of speech that can seem silly or contradictory in form, yet it can still be true, or at least make sense in the context given. This is sometimes used to illustrate thoughts or statements that differ from traditional ideas. So, instead of taking a given statement literally, an individual must comprehend it from a different perspective. Using paradoxes in speeches and writings can also add wit and humor to one’s work, which serves as the perfect device to grab a reader or a listener’s attention.

But paradoxes can be quite difficult to explain by definition alone, which is why it is best to refer to a few examples to further your understanding.

A good paradox example is in the famous television show House. Here, Dr. House is a rude, selfish, and narcissistic character who alienates everyone around him, even his own colleagues. However, he is also a brilliant doctor who is committed to saving lives. Regardless of his mean exterior, Dr. House is a moral and compassionate man who cares about his patients. The paradox here is how the character strives to save people’s lives despite his ruthless personality and behavior.

Modern health care appears to be rich in contradictions, and it is claimed to be paradoxical in a number of ways. In particular health care is held to be a paradox itself: it is supposed to do good; but is also accused of doing harm.

The expression “first do no harm,” which is a Latin phrase, is not part of the original or modern versions of the Hippocratic Oath, which was originally written in Greek (“primum non nocere,” the Latin translation from the original Greek.)

The Hippocratic Oath, written in the 5th century BCE, does contain language suggesting that the physician and his assistants should not cause physical or moral harm to a patient.

The first known published version of “do no harm” dates to medical texts from the mid-19th century, and is attributed to the 17th century English physician Thomas Sydenham.

Difference between Paradox and Oxymoron

Most people tend to confuse a paradox with an oxymoron, and it’s not hard to see why. Most oxymoron examples appear to be compressed version of a paradox, in which it is used to add a dramatic effect and to emphasize contrasting thoughts. Although they may seem greatly similar in form, there are slight differences that set them apart.

A paradox consists of a statement with opposing definitions, while an oxymoron combines two contradictory terms to form a new meaning. But because an oxymoron can play out with just two words, it is often used to describe a given object or idea imaginatively. As for a paradox, the statement itself makes you question whether something is true or false. It appears to contradict the truth, but if given a closer look, the truth is there but is merely implied.

The Paradox in Medicine and Health Care

Dr. Bernard Brom [Editor: SA Journal of Natural Medicine] suggests modem medicine is riddled with paradoxes. Most doctors live with these paradoxes without being aware of the conflict of interest that these paradoxes represent. Intrinsic to a general understanding of science is the idea that science frees us from misunderstanding and guides us towards clear decision making.

Most veteran doctors with experience know that medical science still does not give definitive answers, that each individual is unique, that one can never be sure how a patient will respond to a particular drug, or what the outcome of a particular operation will be. Human beings are not machines and therefore do not respond according to Newtonian logic, and therefore a paradox in medicine is not surprising. Medicine is an art which uses scientific techniques and approaches. It is, however, important to face these paradoxes. It is both humbling and enlightening, enriching those who consider the implications deeply enough.

The Compensation versus Value Paradox

Regardless of specialty, degree designation or delivery model, private practice physician salary is traditionally inversely related to independent medical practice business value.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Valuing a medical practice involves assessing its financial performance, assets, and intangible factors like goodwill and patient loyalty to determine its fair market worth.

Determining the value of a medical practice is a nuanced process that blends financial analysis with strategic insight. Whether you’re preparing to sell, merge, or bring in a partner, understanding how to value your practice ensures informed decision-making and fair negotiations.

There are several recognized methods for valuing a medical practice, each suited to different scenarios. The most common include the income approach, market approach, asset-based approach, and the rule-of-thumb method.

The income approach focuses on the practice’s ability to generate future earnings. This method involves analyzing historical financial statements, projecting future cash flows, and discounting them to present value using a risk-adjusted rate. It’s particularly useful when the practice has stable revenue and predictable expenses. Key metrics include net income, physician productivity, and reimbursement rates.

The market approach compares the practice to similar ones that have recently sold. It relies on data from comparable transactions, adjusted for differences in size, specialty, location, and profitability. This method is ideal when reliable market data is available, though such data can be scarce for niche specialties or rural practices.

The asset-based approach calculates the value of tangible and intangible assets. Tangible assets include medical equipment, office furniture, and real estate. Intangible assets—like patient records, brand reputation, and goodwill—are harder to quantify but can significantly impact value. Goodwill, for instance, reflects the practice’s reputation, patient loyalty, and referral networks.

The rule-of-thumb method uses industry benchmarks, such as a multiple of annual revenue or earnings. For example, a general practice might be valued at 60–80% of annual gross revenue. While quick and easy, this method oversimplifies and may not reflect the unique strengths or weaknesses of a specific practice.https:/https://medicalexecutivepost.com/2025/03/17/medial-practice-valuation-adjustments//medicalexecutivepost.com/2025/03/17/medial-practice-valuation-adjustments/

Beyond these methods, several qualitative factors influence valuation. These include the size and diversity of the patient base, the practice’s specialty, use of technology (like EHR systems or telemedicine), and whether key physicians will remain post-sale. A practice heavily reliant on one provider may be less valuable than one with a strong team and succession plan.

Timing also matters. Economic conditions, regulatory changes, and shifts in healthcare reimbursement can affect practice value. Tax implications and deal structure—such as asset sale vs. stock sale—should also be considered during negotiations.

Ultimately, valuing a medical practice is both art and science. Engaging a professional appraiser or valuation expert can help ensure accuracy and objectivity. They bring experience, access to market data, and the ability to tailor valuation methods to your specific situation.

In summary, a comprehensive valuation considers financial performance, assets, market trends, and intangible factors. By understanding these elements, practice owners can make strategic decisions that reflect the true worth of their medical enterprise.