BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

We make second investment portfolio opinions affordable

Approximately 1 million allopathic physicians, 150,000 dentists, 200,000 osteopaths, 15,000 podiatrists and 6 million nurses often find it difficult to get an unbiased and fiduciary second opinion on their retirement or brokerage accounts. By offering second opinions for a flat fee, the monetary barriers that prevented colleagues from receiving a second opinion in the past have been removed.

We make second investment portfolio opinions convenient

Here’s how we work: you book an initial appointment with us, answer a few preliminary questions and email us your portfolio information. We then provide a second opinion. It is then up to you to incorporate or not.

We make second investment portfolio opinions timely

Financial markets, jobs and colleague age change like the weather. It is not always okay to wait a week, year or more, to seek a professional second financial portfolio opinion. You need to receive an opinion now. That’s where we come in. We are standing by, ready to take your email [MarcinkoAdvisors@outlook.com] and schedule a free initial consultation within two or three days, or less.

We make second investment portfolio opinions accurate

Fiduciary and non-sales orientated second opinions have the power to change financial lives in the long term. We’ve seen it happen many times. What characterizes a good second opinion? Three things: the opinion must be individualized to your investment portfolio[s], informed and results-oriented. That’s the informed fiduciary approach we take. We are colleagues and look forward to working with you.

As many medical, dental and podiatric colleagues are aware, Environmental, Social and Governance (ESG) investing refers to a set of standards for a company’s behavior used by socially conscious investors to screen potential investments. Over the last decade, or so, I have seen many investors pursing this laudable aim.

Yet, more than 80% of private equity fund managers have now stepped away from at least one deal due to ESG concerns, according to the 2023 BDO Private Capital Survey. The reasons are complex, and point towards fund managers’ sentiment towards risk-reward in the current economic environment.

This retreat from ESG is due to backlash from conservatives who are critical of the idea that mutual fund managers should be considering any other factor but a company’s share holders in their investment decisions. Accusations of “Greenwashing” have also plagued many ESG funds, which is when an asset management firm charging higher fees or a specific thematic fund without actually delivering a unique investment strategic competitive advantage.

Greenwashing is the process of conveying a false impression or misleading information about how a company’s products are environmentally sound. Greenwashing involves making an unsubstantiated claim to deceive consumers and / or investors into believing that a company’s products are environmentally friendly or have a greater positive environmental impact than they actually do. Greenwashing may also occur when a company attempts to emphasize sustainable aspects of a product to overshadow the company’s involvement in environmentally damaging practices.

According to internationally known linguistics and cognitive science Professor,Mackenzie Hope Marcinko PhD of the University of Delaware, greenwashing is performed through the use of environmental imagery, misleading labels, cognitive biases and tendencies hiding tradeoffs. Greenwashing is also a play on the term “Whitewashing,” which means using false information to intentionally hide wrongdoing, errors or an unpleasant situation in an attempt to make it seem less bad than it really is.

To be sure, uncertainty around ESG regulations in the USA is leading financial deal makers to tread carefully. For example, Jim ClaytonMBA, aprivate equity advisor also from the University of Delaware recently stated:

“We’re a year past when the SEC said they were going to issue ESG reporting standards for public filers which has created more noise in the system.”

“People are nervous about what I would call ESG-intense exposed industries, in other words, those with “heavy carbon footprints”.

And, a federal judge in Texas said that American Airlines violated federal law by basing investment decisions for its employee retirement plan on environmental, social, and other non-financial factors. The ruling in January 2025 by US District Judge Reed O’Connor appeared to be the first of its kind amid growing backlash by conservatives to an uptick in socially-conscious investing. O’Connor said American had breached its legal duty to make investment decisions based solely on the financial interests of 401(k) plan beneficiaries by allowing BlackRock, its asset manager and a major shareholder, to focus on environmental, social and corporate governance (ESG) factors.

Even the State of Florida pulled $2 billion from the investment management firm BlackRock in the largest divestment ever made. Florida Governor Ron DeSantis claimed that by taking ESG standards into account when making investment decisions, the firm isn’t prioritizing the financial bottom line for Floridians.

Assessment

But, for a few years at least, things were indeed good. In 2020 and 2021, ESG funds outperformed the market by ~4.3%.

Conclusion

So, always remember [caveat emptor]: let the buyer beware!

2. Marcinko, DE; Comprehensive Financial Planning Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™] Productivity Press, New York, 2017

3. Marcinko, DE: Dictionary of Health Economics and Finance. Springer Publishing Company, NY 2006.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Life planning and behavioral finance as proposed for physicians and integrated by the Institute of Medical Business Advisors Inc., is unique in that it emanates from a holistic union of personal financial planning, human physiology and medical practice management, solely for the healthcare space. Unlike pure life planning, pure financial planning, or pure management theory, it is both a quantitative and qualitative “hard and soft” science, with an ambitious economic, psychological and managerial niche value proposition never before proposed and codified, while still representing an evolving philosophy. Its’ first-mover practitioners are called Certified Medical Planners™.

Financial Life Planning is an approach to financial planning that places the history, transitions, goals, and principles of the client at the center of the planning process. For the financial advisor or planner, the life of the client becomes the axis around which financial planning develops and evolves.

Financial Life Planning is about coming to the right answers by asking the right questions. This involves broadening the conversation beyond investment selection and asset management to exploring life issues as they relate to money.

Financial Life Planning is a process that helps advisors move their practice from financial transaction thinking, to life transition thinking. The first step is aimed to help clients “see” the connection between their financial lives and the challenges and opportunities inherent in each life transition.

But, for informed physicians, life planning’s quasi-professional and informal approach to the largely isolate disciplines of financial planning and medical practice management is inadequate. Today’s practice environment is incredibly complex, as compressed economic stress from HMOs managed care, financial insecurity from insurance companies, ACOs and VBC, Washington DC and Wall Street; liability fears from attorneys, criminal scrutiny from government agencies, and IT mischief from malicious electronic medical record [eMR] hackers. And economic bench marking from hospital employers; lost confidence from patients; and the Patient Protection and Affordable Care Act [PP-ACA] more than a decade ago. All promote “burnout” and converge to inspire a robust new financial planning approach for physicians and most all medical professionals.

The iMBA Inc., approach to financial planning, as championed by the Certified Medical Planner™ professional certification designation program, integrates the traditional concepts of financial life planning, with the increasing complex business concepts of medical practice management. The former topics are presented in this textbook, the later in our recent companion text: The Business of Medical Practice [Transformational Health 2.0 Skills for Doctors].

***

***

For example, views of medical practice, personal lifestyle, investing and retirement, both what they are and how they may look in the future, are rapidly changing as the retail mentality of medicine is replaced with a wholesale and governmental philosophy. Or, how views on maximizing current practice income might be more profitably sacrificed for the potential of greater wealth upon eventual practice sale and disposition.

Or, how the ultimate fear represented by Yale University economist Robert J. Shiller, in The New Financial Order: Risk in the 21st Century, warns that the risk for choosing the wrong profession or specialty, might render physicians obsolete by technological changes, managed care systems or fiscally unsound demographics. OR, if a medical degree is even needed for future physicians?

Say, what medical license?

Dr. Shirley Svorny, chair of the economics department at California State University, Northridge, holds a PhD in economics from UCLA. She is an expert on the regulation of health care professionals who participated in health policy summits organized by Cato and the Texas Public Policy Foundation. She argues that medical licensure not only fails to protect patients from incompetent physicians, but, by raising barriers to entry, makes health care more expensive and less accessible. Institutional oversight and a sophisticated network of private accrediting and certification organizations, all motivated by the need to protect reputations and avoid legal liability, offer whatever consumer protections exist today.

Yet, the opportunity to revise the future at any age through personal re-engineering, exists for all of us, and allows a joint exploration of the meaning and purpose in life. To allow this deeper and more realistic approach, the informed transformation advisor and the doctor client, must build relationships based on trust, greater self-knowledge and true medical business management and personal financial planning acumen.

[A] The iMBA Philosophy

As you read this ME-P website, we hope you will embrace the opportunity to receive the focused and best thinking of some very smart people. Hopefully, along the way you will self-saturate with concrete information that proves valuable in your own medical practice and personal money journey. Maybe, you will even learn something that is so valuable and so powerful, that future reflection will reveal it to be of critical importance to your life. The contributing authors certainly hope so.

At the Institute of Medical Business Advisors, and thru the Certified Medical Planner™ program, we suggest that such an epiphany can be realized only if you have extraordinary clarity regarding your personal, economic and [financial advisory or medical] practice goals, your money, and your relationship with it. Money is, after only, no more or less than what we make of it.

Ultimately, your relationship with it, and to others, is the most important component of how well it will serve you.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com

Most individual physician portfolios are simply a list of stocks. Doctors with such lists usually know the cost of each position and when they acquired it. It is not unusual to find inherited low cost stocks in the account that have been held for many years.

When you inherit securities, a new cost basis is established (the price of the stock on the date of death or six months later—the executor of the estate makes this determination). Even though there would be no capital gain liability if the stock were sold immediately after date of death, most people simply don’t do anything, just hold the stock. Of course taxes should be considered when selling securities but the investment merit should be the overriding factor.

***

***

Doctor and Accountant Opinions

In a personal communication, Mr. L. Eddie Dutton, CPA said, “First make an investment decision and if it fits into the tax plan, so much the better. Doctors often wonder where they will get the money to pay the taxes. I say to get it from the sale of the appreciated stock and cry all the way to the bank with your profit.”

Dr. Ernest Duty MD, a very successful private investor advises “Ask yourself this question: If you had the money instead of the stock, would you buy the stock? If your answer is ‘Yes’ then, hold on to the stock but if you say ‘No, I wouldn’t buy that stock today’ then, sell it” [personal communication].

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: E-MAILCONTACT: MarcinkoAdvisors@outlook.com

Posted on May 25, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITION

By Staff Reporters

***

***

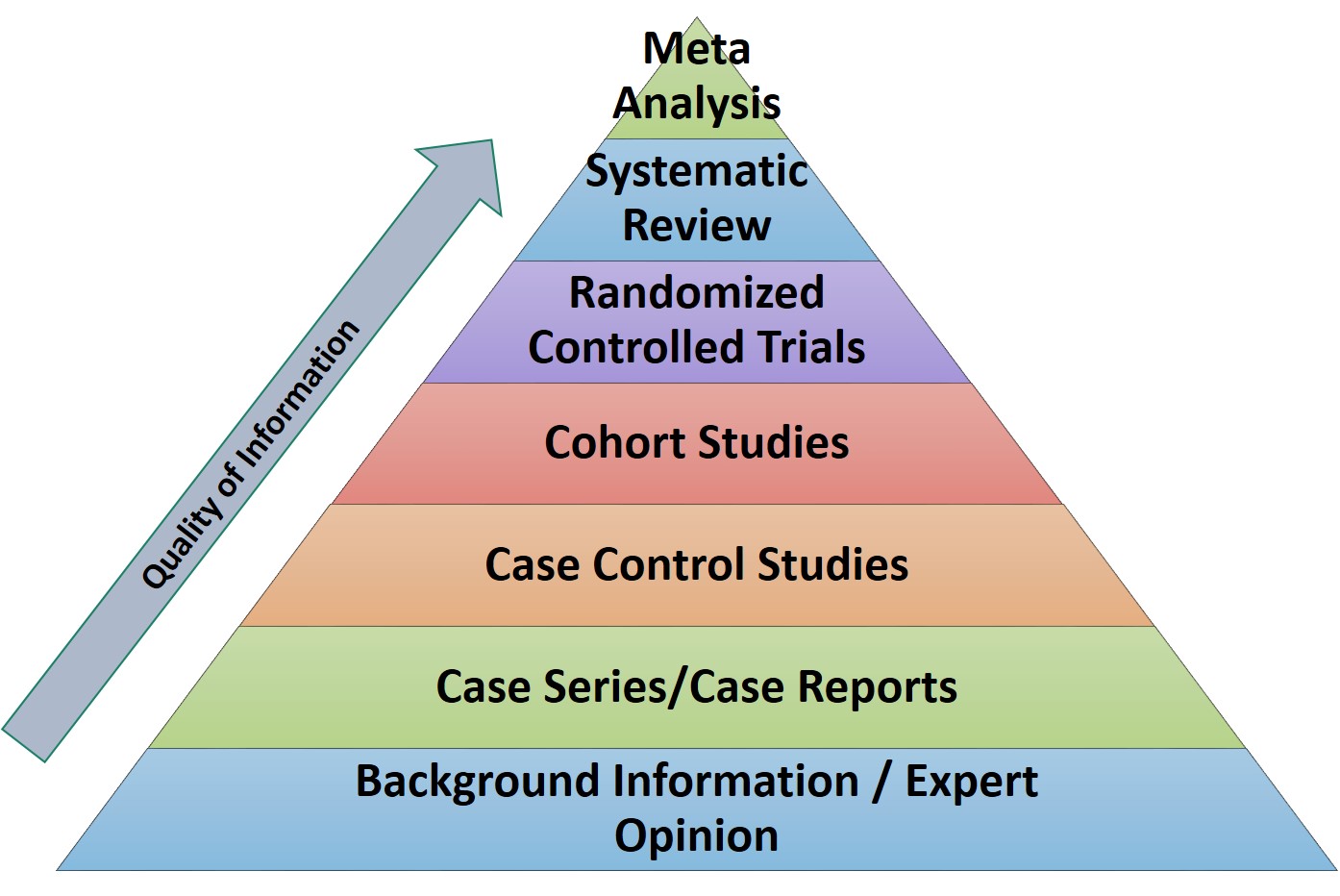

Meta-analysis is a quantitative, formal, epidemiological study design used to systematically assess previous research studies to derive conclusions about that body of research. Outcomes from a meta-analysis may include a more precise estimate of the effect of treatment or risk factor for disease, or other outcomes, than any individual study contributing to the pooled analysis. The examination of variability or heterogeneity in study results is also a critical outcome.

The benefits of meta-analysis include a consolidated and quantitative review of a large, and often complex, sometimes apparently conflicting, body of literature. The specification of the outcome and hypotheses that are tested is critical to the conduct of meta-analyses, as is a sensitive literature search. A failure to identify the majority of existing studies can lead to erroneous conclusions; however, there are methods of examining data to identify the potential for studies to be missing; for example, by the use of funnel plots.

Rigorously conducted meta-analyses are useful tools in evidence-based medicine. The need to integrate findings from many studies ensures that meta-analytic research is desirable and the large body of research now generated makes the conduct of this research feasible.

Cognitive science is the interdisciplinary study of the mind and cognition. According to linguistics Professor Mackenzie H. Marcinko PhD, it combines various aspects from neuroscience, computer science, psychology, philosophy, linguistics, anthropology, and other fields, into a comprehensive study on the nature of intelligence.

Linguistics is the scientific study of language and its structure, including the study of morphology, syntax, phonetics, and semantics. Specific branches of linguistics include sociolinguistics, dialectology, psycholinguistics, computational linguistics, historical-comparative linguistics and applied linguistics.

Now, language and linguistics are closely related fields of study but they have distinct focuses.

Language refers to the system of communication used by humans, encompassing spoken, written, and signed forms. It is a means of expressing thoughts, ideas, and emotions.

On the other hand, linguistics is the scientific study of language itself. It examines the structure, sounds, meaning, and evolution of languages, as well as how they are acquired and used by individuals and communities.

While language is a broader concept that encompasses various forms of communication, linguistics delves into the intricate details and mechanics of language, aiming to understand its underlying principles and patterns.

Every year on May 10th, the world comes together to observe World Lupus Day.

Lupus is a disease that occurs when your body’s immune system attacks your own tissues and organs (autoimmune disease). Inflammation caused by lupus can affect many different body systems — including your joints, skin, kidneys, blood cells, brain, heart and lungs. Lupus can be difficult to diagnose because its signs and symptoms often mimic those of other ailments. The most distinctive sign of lupus — a facial rash that resembles the wings of a butterfly unfolding across both cheeks — occurs in many but not all cases of lupus. Some people are born with a tendency toward developing lupus, which may be triggered by infections, certain drugs or even sunlight. While there’s no cure for lupus, treatments can help control symptoms.

In 2025, this important day continues its mission of raising awareness about lupus, supporting those affected, and promoting further research into this complex autoimmune condition.

The phrase “sell in May and go away” suggests that investors should sell their stocks in May and avoid the market during the summer months, as historical data indicates poorer stock performance during this period.

***

It’s Friday morning, so you’re probably clocking out once you’re done reading this ME-P. And who could blame you, after such a wild month of watching your portfolio zig & zag with every headline.

In fact, why not just sell all your stocks and walk away entirely? You’ve got to admit, it’s tempting. After all, markets have completed an incredible round trip since Liberation Day—you could just call it even, start celebrating Cinco de Mayo a bit late, and maybe check your portfolio again sometime around August.

“Sell in May and go away” might sound like appealing advice these days, especially considering that the market usually spends the next six months under-performing: The S&P 500 gains just 1.8% on average from May through October, the worst-performing stretch of the year historically.

These ‘worst six months’ have gained in eight of the last 10 years,” he recently wrote. He continued: “Not to mention the month of May has been higher nine of the past 10 years, so maybe we should call it,

Financial Advisor, Planner and Insurance Agent Information

By Staff Reporters

***

***

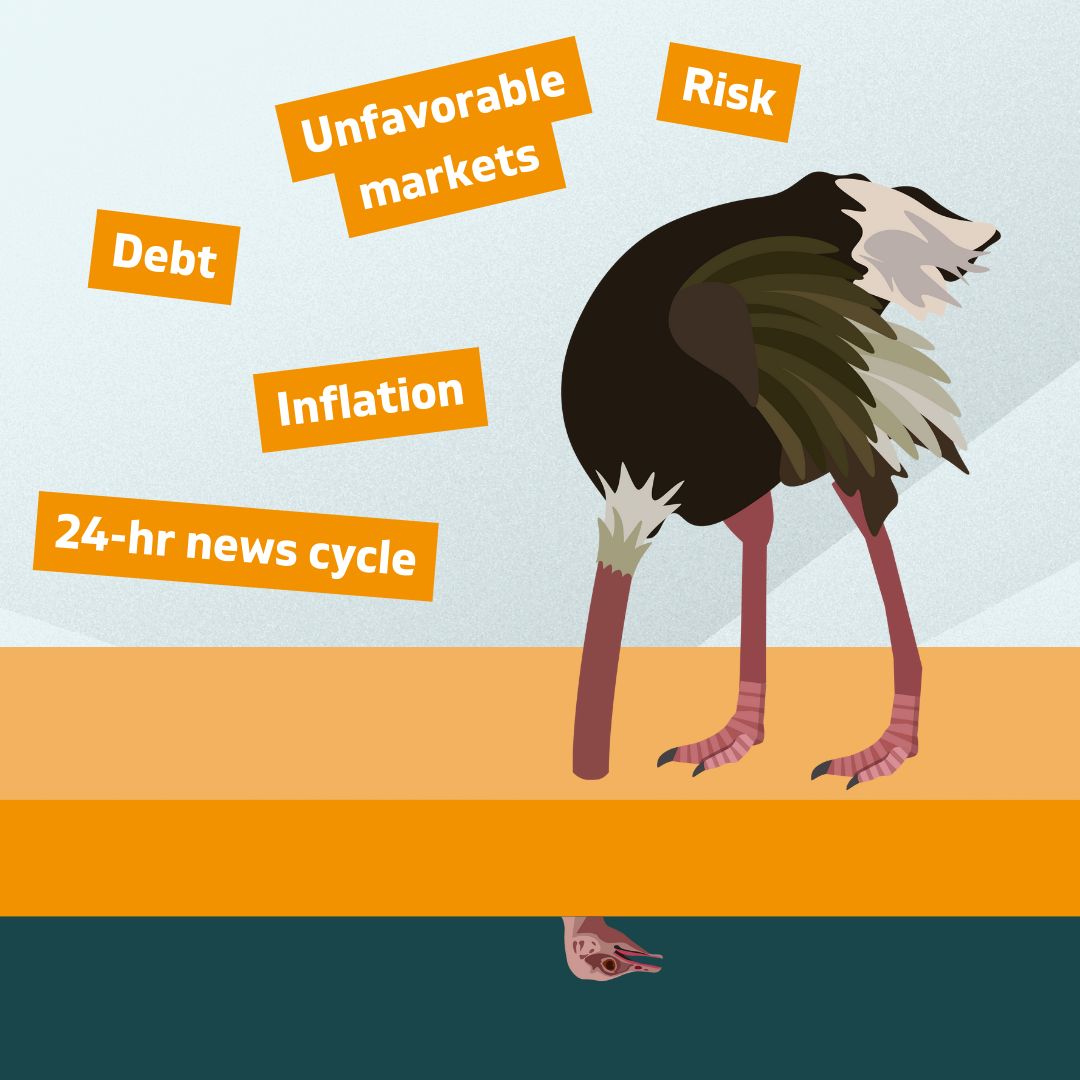

Ostrich Bias is a behavioral phenomenon describing the tendency of individuals to avoid or ignore information that they perceive as negative or threatening. This term is derived from the popular but inaccurate belief that ostriches bury their heads in the sand when faced with danger, even though they do not exhibit such behavior.

Evidence: There is neuro-scientific evidence of the ostrich effect. Sharot et al. (2012) investigated the differences in positive and negative information when updating existing beliefs. Consistent with the ostrich effect, participants presented with negative information were more likely to avoid updating their beliefs; wills, estate plans, investment portfolios, and insurance policies, etc..

Moreover, they found that the part of the brain responsible for this cognitive bias was the left IFG – inferior frontal gyrus – by disrupting this part of the brain with TMS – transcranial magnetic stimulation – participants were more likely to accept the negative information provided.

EXAMPLE: The Ostrich Bias can cause someone to avoid looking at their bills, because they’re worried about seeing how far behind they are on home mortgage payments, credit cards, education or auto loans, etc.

COMMENTS APPRECIATED

The Medical Executive-Post is a news and information aggregator and social media professional network for medical and financial service professionals.

Feel free to submit education content to the site as well as links, text posts, images, opinions and videos which are then voted up or down by other members. Comments and dialog are especially welcomed.

Daily posts are organized by subject. ME-P administrators moderate the activity. Moderation may also conducted by community-specific moderators who are unpaid volunteers.

Posted on May 6, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Doctor David Edward Marcinko; MBA MEd

***

***

National Teachers’ Day is observed on the first Tuesday of the first full week of May (May 6th) and we’re more than ready to show our appreciation to those who have taught us. Everyone has had that favorite teacher that has helped inspire them. This day meant to honor them was actually made by a teacher.

None other than First Lady Eleanor Roosevelt herself. Eleanor Roosevelt was more than Franklin D. Roosevelt’s wife, she has a history of civic duty and was an advocate for fellow teachers. Her love for education began at a young age when she was privately tutored and encouraged by her aunt Anna “Barnie” Roosevelt. No matter how high she rose on the social ladder, she never forgot where she came from.

Much like a springy inflatable structure often resembling a four-sided building and used by children for jumping for sport and fun, stocks staged a much-needed bounce-house back week on hopes that the trade war would de-escalate, with the S&P 500 climbing for four straight days to close 4.6% higher.

Whether the rally continues this week may depend on the Magnificent Seven earnings on tap—each of those Big Tech stocks has fallen at least 6.5% this year, shedding a combined $2.5 trillion in market value, per the Wall Street Journal.

A Certified Public Accountant (CPA) is a licensed professional who has passed an examination administered by a state’s Board of Accountancy. State CPA exams are created under guidelines issued by The American Institute of Certified Public Accountants (AICPA). The Uniform CPA Exam can only be taken by accountants who already have professional experience in the field and a bachelor’s degree.CPAs are not fiduciaries.

Not all accountants are CPAs. Accountants who are CPAs are licensed by their state’s Board of Accountancy after passing the Uniform CPA Exam. CPAs prepare reports that accurately reflect the business dealings of the companies and individuals that hire them. Many prepare tax returns for individuals or businesses and advise them on ways to minimize taxes. Obtaining the CPA designation requires a bachelor’s degree, typically with a major in business administration, finance, or accounting. Other majors are acceptable if the applicant meets the minimum requirements for accounting courses.

Enrolled Agent

Although not a CPA, an Enrolled Agent [EA] is a person who has earned the privilege of representing taxpayers before the Internal Revenue Service [IRS]. This is done by either passing a three-part comprehensive IRS test covering individual and business tax returns, or through experience as a former IRS employee. Enrolled agent status is the highest credential the IRS awards. Individuals who obtain this elite status must adhere to ethical standards and complete 72 hours of continuing education courses every three years.

Certified Managerial Accountant

A Certified Management Accountant (CMA), which is issued by the Institute of Management Accountants (IMA), builds on financial accounting proficiency by adding management skills that aid in making strategic business decisions based on financial data.

Oftentimes, the reports and analyses prepared by certified management accountants (CMAs) will go above and beyond those required by generally accepted accounting principles (GAAP).

For example, in addition to a company’s required GAAP financial statements, CMAs may prepare additional management reports that provide specific insights useful to corporate decision-makers, such as performance metrics on specific company departments, products, or even employees.

Certified Financial Analyst

A Certified Financial Analyst [CFA] is a globally-recognized professional designation offered by the CFA Institute, an organization that measures and certifies the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management, and security analysis. From 1963 through November 2023, more than 3.7 million candidates had taken the CFA exam. The overall pass rate was 45%. From 2014 through 2023, the 10-year average pass rate was 43%.1

CFA Institute. The CFA Institute was formerly the Association for Investment Management and Research (AIMR).

The CFA charter is one of the most respected designations in finance and is widely considered to be the gold standard in the field of investment analysis. To become a charter holder, candidates must pass three difficult exams, have a bachelors degree, and have at least 4,000 hours of relevant professional experience over a minimum of three years. Passing the CFA Program exams requires strong discipline and an extensive amount of studying.

There are more than 200,000 CFA charter holders worldwide in 164 countries.The designation is handed out by the CFA Institute, which has 11 offices worldwide and 160 local member societies.

Several years ago a group of highly trusted and deeply experienced financial advisors, insurance service professionals and estate planners noted that far too many of their mature retiring physician clients, using traditional stock brokers, management consultants and financial advisors, seemed to be less successful than those who went it alone. These Do-it-Yourselfers [DIYs] had setbacks and made mistakes, for sure. But, the ME Inc doctors seemed to learn from their mistakes and did not incur the high management and service fees demanded from general or retail one-size-fits-all “advisors.”

In fact, an informal inverse related relationship was noted, and dubbed the “Doctor Effect.” In others words, the more consultants an individual doctor retained; the less well they did in all disciplines of the financial planning and medical practice management, continuum.

Of course, the reason for this discrepancy eluded many of them as Wall Street brokerages and wire-houses flooded the media with messages, infomercials, print, radio, TV, texts, tweets, dinners and internet ads to the contrary. Rather than self-learn the basics, the prevailing sentiment seemed to purse the holy grail of finding the “perfect financial advisor.” This realization confirmed the industry culture which seemed to be:

Bread for the advisor – Crumbs for the client!

And so, Marcinko Associates formed a cadre’ of technology focused and highly educated multi-degreed doctors, nurses, financial advisors, attorneys, accountants, psychologists and educational visionaries who decided there must be a better way for their healthcare colleagues to receive financial planning advice, products and related advisory services within a culture of fiduciary responsibility.

We trust you agree with this specific niche knowledge, and collegial consulting philosophy, as illustrated thru our firm and these two books.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Carried interest accounts for the bulk of private equity fund managers’ compensation. It is calculated as a share of fund profits, historically 20% above a threshold rate of return for limited partners.

In contrast with most other forms of employment compensation and business income, carried interest earned from fund investments held for at least three years is taxed as a long-term capital gain at a rate below the top marginal income tax rate.

Critics of the provision contend it taxes highly compensated private equity managers at a lower rate than comparably paid providers of labor or business services.

Defenders of carried interest argue taxing it as income would be unfair because it represents capital gains even if they’re not derived from recipients’ capital.

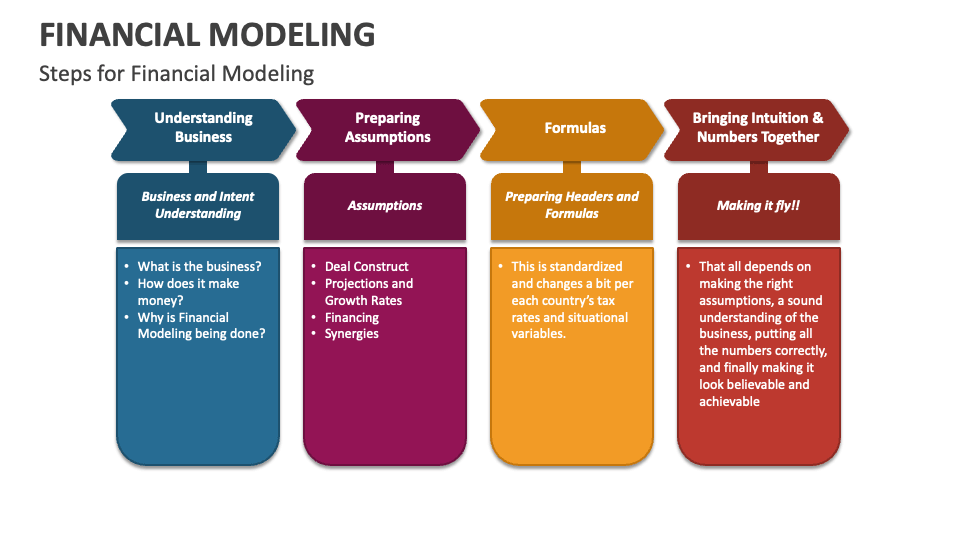

Financial Modeling is one of the most highly valued, but thinly understood, skills in financial analysis. The objective of financial modeling is to combine accounting, finance, and business metrics to create a forecast of a company’s future results.

According to Jeff Schmidt, a financial model is simply a spreadsheet, usually built in Microsoft Excel, that forecasts a business’s financial performance into the future. The forecast is typically based on the company’s historical performance and assumptions about the future and requires preparing an income statement, balance sheet, cash flow statement, and supporting schedules (known as a three-statement model, one of many types of approaches to financial statement modeling). From there, more advanced types of models can be built such as discounted cash flow analysis (DCF model), leveraged buyout (LBO), mergers and acquisitions (M&A), and sensitivity analysis

***

DEFINED TERMS

Discounted Cash Flow (DCF): A valuation method used to estimate the value of an investment based on its expected future cash flows, adjusted for the time value of money. It’s like deciding whether a treasure chest is worth diving for now, based on the gold coins you’ll be able to cash in later.

Sensitivity Analysis: This involves changing one variable at a time to see how it affects an outcome. Imagine tweaking your coffee-to-water ratio each morning to achieve the perfect brew strength.

Budget – A budget is the amount of money a department, function, or business can spend in a given period of time. Usually, but not always, finance does this annually for the upcoming year.

Rolling Forecast – A rolling forecast maintains a consistent view over a period of time (often 12 months). When one period closes, finance adds one more period to the forecast.

Topside – A topside adjustment is an overlay to a forecast. This is typically completed by the corporate or headquarter team. As individual teams submit a forecast, the consolidated result might not make sense or align with expectations. When this occurs, the high-level teams use a topside adjustment to streamline or adjust the consolidated view.

Monte Carlo Simulation: Picture yourself at the casino, but instead of gambling your savings away, you’re using this technique to predict different outcomes of your business decisions based on random variables. It’s like playing financial roulette with the odds in your favor.

What-If Analysis: Ever daydream about what would happen if you took that leap of faith with your business? This tool allows you to explore various scenarios without risking a dime. It’s like trying on outfits in a virtual dressing room before making a purchase.

Leveraged Buyout (LBO) Model: This is a bit like orchestrating a heist, but legally. It’s about acquiring a company using borrowed money, with plans to pay off the debts with the company’s own cash flows. High stakes, high rewards.

Mergers and Acquisitions (M&A) Model: Picture two puzzle pieces coming together. This model evaluates how combining companies can create a new, more valuable entity. It’s the corporate version of a matchmaker.

Three Statement Model: The holy trinity of financial modeling, linking the income statement, balance sheet, and cash flow statement. It’s like weaving a tapestry where each thread is crucial to the overall picture.

Capital Asset Pricing Model (CAPM): A formula that calculates the expected return on an investment, considering its risk compared to the market. It’s like choosing the best roller coaster in the park, balancing thrill and safety.

Cash Flow Forecasting: This is your financial weather forecast, predicting the cash flow climate of your business. It helps you plan for sunny days and save for the rainy ones.

Cost of Capital: The price of financing your business, whether through debt or equity. It’s like the interest rate on your growth engine, pushing you to maximize every dollar invested.

Debt Schedule: A timeline of your business’s debts, showing when and how much you owe. It’s your roadmap to becoming debt-free, one milestone at a time.

Equity Valuation: Determining the value of a company’s shares. It’s like assessing the worth of a rare gemstone, ensuring investors pay a fair price for a piece of the treasure.

Financial Leverage: Using debt to amplify returns on investment. It’s like using a lever to lift a heavy object, increasing force but also risk.

Forecast Model: A crystal ball for your finances, projecting future performance based on past and present data. It’s your guide through the financial wilderness, helping you navigate with confidence.

Operating Model: A detailed blueprint of how a business generates value, mapping out operational activities and their financial impact. It’s like laying out the inner workings of a clock, ensuring every gear turns smoothly.

Revenue Growth Model: This tracks potential increases in sales over time, charting a course for expansion. It’s like plotting your ascent up a mountain, anticipating the effort required to reach the summit.

Profitability ratios measure a company’s ability to generate income relative to revenue, balance sheet assets, operating costs, and equity. Common profitability financial ratios include the following:

The gross margin ratio compares the gross profit of a company to its net sales to show how much profit a company makes after paying its cost of goods sold:

Gross margin ratio = Gross profit / Net sales

The operating margin ratio, sometimes known as the return on sales ratio, compares the operating income of a company to its net sales to determine operating efficiency:

Operating margin ratio = Operating income / Net sales

The return on assets ratio measures how efficiently a company is using its assets to generate profit:

Return on assets ratio = Net income / Total assets

The return on equity ratio measures how efficiently a company is using its equity to generate profit:

Return on equity ratio = Net income / Shareholder’s equity

Posted on April 4, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING US STOCK MARKET NEWS

By ME-P Staff Reporters

***

***

Stocks in the U.S. opened sharply lower on Friday, extending a slide from the previous trading session triggered by President Trump’s announcement of sweeping new tariffs on U.S. imports earlier this week.

The S&P 500 fell 144 points, or 2.5%, to 5,252 as of 9:34 a.m. EST. The Dow Jones Industrial Average tumbled 1,006 points, or 2.5%, and the NASDAQ Composite slid 3.1%.

The indexes’ free-fall Thursday was their biggest one-day drop since 2020, with more than $2 trillion in investor wealth erased from the S&P 500. The S&P 500 and Dow each sank more than 4% yesterday, while the tech-heavy NASDAQ plunged nearly 6%.

NOTE: Drops of this magnitude aren’t unheard of on Wall Street, but they’re rare. Over the last 25 years, the S&P 500 has fallen 4% in a single day 38 times, according to Adam Turnquist, chief technical strategist for brokerage firm LPL Financial.

Posted on March 29, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

EDITOR-IN-CHIEF

By Dr. David Edward Marcinko; FACFAS MBA MEd

***

***

NATIONAL PHYSICIANS WEEK

National Physicians Week sets out March 25-31 to honor the healers dedicated to the art of medicine. In 2017, National Physicians Week highlighted the shortage of physicians in the United States against a growing landscape of minorities joining the ranks.

#NationalPhysiciansWeek

“In hindsight, I am proud of what we have accomplished in a short period of time, including raising the recognition of our group and spotlighting the years of sacrifice by those in our profession to serve our patients. We are poised to initiate actionable efforts to engage and educate our physician community.”

Cite: Dr. Kimberly Funches Jackson, President

Today in 2025, let’s explore the invaluable contributions of physicians, celebrate their hard work during National Physicians Week, and highlight the essential role that locum doctors play in enhancing healthcare delivery.

A Week to Honor All Physicians

National Physicians Week is a celebration of the remarkable work that doctors do every single day. From diagnosing complex conditions to providing life-saving treatments, physicians dedicate themselves to improving the health and well-being of their patients. It’s a week for healthcare professionals, patients, and communities to come together and show appreciation for the doctors who make a difference in our lives.

Physicians work long hours, face immense pressure, and make critical decisions daily. Their contributions go beyond the walls of the hospital, as many are also involved in research, teaching, and community outreach.

So, this week, it’s important to acknowledge not only their professional expertise but also the compassion and resilience they exhibit in their work.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com

Avram Noam Chomsky is an American professor known for his traditional work in linguistics and political activism. Sometimes called “the father of modern linguistics”, Chomsky is also one of the founders of the field of cognitive science. He is a laureate professor of linguistics at the University of Arizona and an professor emeritus at MIT.

And so, modern linguists today approach their work with scientific rigor and perspective [STEM], although they use methods that were once thought to be solely an academic discipline of the humanities.

Contrary to this humanitarian belief, according to Professor Mackenzie Hope Marcinko PhD of the University of Delaware, linguistics is now multidisciplinary. It overlaps each of the human sciences including psychology, neurology, anthropology, and sociology. Linguists conduct formal studies of sound structure, grammar and meaning, but also investigate the history of language families, and research language acquisition.

A hostile takeover happens when an entity takes control of a company without the knowledge and against the wishes of the company’s management. A hostile takeover is an acquisition strategy requiring that the entity acquire and control more than 50% of the voting shares issued by the company.

In mergers and acquisitions (M&A), a hostile takeover is the acquisition of a target company by an acquiring company that goes directly to the target company’s shareholders, either by making a tender offer or through a proxy vote.

Ideally, an entity interested in acquiring a company should seek approval from the target company’s Board of Directors. The difference between a hostile and a friendly takeover is that, in a friendly takeover, the target company’s board of directors approve of the transaction and recommend shareholders vote in favor of the deal.

Defenses against a hostile takeover

These defense mechanisms can be preemptive or reactive, depending on how prepared the company is for the possibility of a hostile bid.

Poison pill is one of the most common defenses against a hostile takeover. Officially known as a “shareholder rights plan,” the poison pill allows existing shareholders to purchase additional shares at a discount, diluting the ownership interest of the acquiring company. The goal is to make it prohibitively expensive for the acquirer to complete the takeover.

A golden parachute is another defense strategy, which involves providing lucrative compensation packages (bonuses, severance pay, stock options, etc.) to key executives in the event they are terminated as a result of the takeover. This creates a financial disincentive for the acquiring company, as it would need to pay out these large sums upon completing the takeover.

In a Crown jewel defense, the target company sells or threatens to sell its most valuable assets—its “crown jewels”—if the takeover is completed. This reduces the attractiveness of the company to the acquirer, as the most desirable assets would no longer be part of the deal.

The Pac-Man defenses a more aggressive strategy in which the target company turns the tables by attempting to buy shares of the acquiring company, effectively launching a counter-takeover. While rare, this defense can deter hostile bids by making the takeover battle more costly and complex.

A White-Knight defense involves the target company seeking out a more favorable acquirer, or “white knight,” to make a friendly takeover bid. This allows the target company to avoid the hostile acquirer while still securing the benefits of a merger or acquisition.

The hostile takeover between Sanofi-Aventis and Genzyme Corp. occurred in 2010 when Sanofi, a French pharmaceutical company, wanted to buy Genzyme, a US biotech firm specializing in rare diseases. Genzyme resisted the offer, leading to conflict. Sanofi started a public campaign to pressure Genzyme’s shareholders into selling.

After months of negotiations, the two companies reached a deal in 2011. Sanofi agreed to pay $74 per share, with additional payments tied to Genzyme’s future performance, bringing the total deal value to around $20.1 billion. This acquisition allowed Sanofi to expand into the lucrative market for rare disease treatment.

The genetic testing company 23andMe went from biotech superstar to the brink of collapse. And, its most valuable asset might be its controversial customer DNA data trove.

Now, 23andMe filed for bankruptcy late Sunday night and announced the resignation of its chief executive officer Anne Wojcicki who is stepping down from her position but remains on the board of directors.

Wojcicki has so far tried unsuccessfully to rescue the business by buying it back and capping a precipitous fall for the DNA-testing company.

Absolute Return – the goal is to have a positive return, regardless of market direction. An absolute return strategy is not managed relative to a market index.

Accredited Investor – wealthy individual or well-capitalized institutions covered under Regulation D of the Securities Act of 1933.

Alpha – the return to a portfolio over and above that of an appropriate benchmark portfolio (the manager’s “value added”).

Arbitrage – any strategy that invests long in an asset, and short in a related asset, hoping the prices will converge.

Attribution – the process of “attributing” returns to their sources. For example, did the returns to a portfolio (over and above some benchmark) come from stock selection, industry/sector over- or under-weighting or factor weighting. Software programs are helpful in reporting an attribution.

Beta – a measure of systematic (i.e., non-diversifiable) risk. The goal is to quantify how much systematic risk is being taken by the fund manager vis-à-vis different risk factors, so that one can estimate the alpha or value-added on a risk-adjusted basis.

Correlation – a measure of how strategy returns move with one another, in a range of –1 to +1. A correlation of –1 implies that the strategies move in opposite directions. In constructing a portfolio of hedge funds, one usually wants to combine a number of non-correlated strategies (with decent expected returns) to be well diversified.

Drawdown – the percentage loss from a fund’s highest value to its lowest, over a particular time frame. A fund’s “maximum drawdown” is often looked at as a measure of potential risk.

Hurdle Rate – the return where the manager begins to earn incentive fees. If the hurdle rate is 5% and the fund earns 15% for the year, then incentive fees are applied to the 10% difference.

Leverage – one uses leverage if he borrows money to increase his position in a security. If one uses leverage and makes good investment decisions, leverage can magnify the gain. However, it can also magnify a loss.

Opportunistic – a general term that describes an aggressive strategy with a goal of making money (as opposed to holding on to the money one already has).

***

***

Pairs Trading – usually refers to a long/short strategy where one stock is bought long, and a similar stock is sold short, often within the same industry. Buying the stock of Home Depot and shorting Lowe’s in an equal amount would be an example.

Portfolio Simulation – involves testing an investment strategy by “simulating” it with a database and analytic software. Often referred to as “backtesting” a strategy. The simulated returns of the strategy are compared to those of a benchmark over a specific time frame to see if it can beat that benchmark.

Sharpe Ratio – a measure of risk-adjusted return, computed by dividing a fund’s return over the risk-free rate by the standard deviation of returns. The idea is to understand how much risk was undertaken to generate the alpha.

Short Rebate – if you borrow stock and then sell it short, you have cash in your account. The short rebate is the interest earned on that cash.

R-Squared – a measure of how closely a portfolio’s performance varies with the performance of a benchmark, and thus a measure of what portion of its performance can be explained by the performance of the overall market or index. Hedge fund investors want to know how much performance can be explained by market exposure versus manager skill.

Transportable Alpha – the alpha of one active strategy can be combined with another asset class. For example, an equity market-neutral strategy’s value-added can be “transported” to a fixed income asset class by simply buying a fixed income futures contract. The total return comes from both sources.

Value at Risk – a technique which uses the statistical analysis of historical market trends and volatilities to estimate the likelihood that a specific portfolio’s losses will exceed a certain amount.

Tax avoidance—An action taken to lessen tax liability and maximize after-tax income.

Tax evasion—The failure to pay or a deliberate underpayment of taxes.

Underground economy—Money-making activities that people don’t report to the government, including both illegal and legal activities.

Voluntary compliance—A system of compliance that relies on individual citizens to report their income freely and voluntarily, calculate their tax liability correctly, and file a tax return on time.

Posted on March 19, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

Rocking Financial Planning … Old School Advice!

By Dr. David E. Marcinko MBBS MBA MEd CMP®

The economic platitude of the past, such as don’t spend more than 15-20 percent of your net salary on food, or 5-10 percent on medical care, among others, have given rise to the more individualized personal financial ratio concept. Personal ratios, like business ratios, represent benchmarks to compare such parameters as debt, income growth and net worth.

According to Edward McCarthy MIB CFP® – a personal financial expert from Warwick, Rhode Island whom I interviewed about a decade ago – the following represented useful ratios for the lay as well as medical professional [personal communication].

The Ratios:

Basic Liquidity Ratio = liquid assets / average monthly expenses. Should be 4-6 months, or even longer, in the case of a medical professional employed by a financially insecure HMO. In a low interest rate environment, iMBA Inc offers 12-24 months for consideration.

Debt to Assets Ratio = total debt / total assets. A percentage which is high initially, and should decrease with age as the medical professional approaches a debt free existence

Debt to Gross Income Ratio = annual debt repayments / annual gross income. A percentage representing the adequacy of current income for existing debt repayments. Medial professionals should try to keep this below 25-30%.

Debt Service Ratio = annual debt re-payment / annual take-home pay. Medical professionals should try to keep this ratio below about 40%, or have difficulty paying down debt.

Investment Assets to Net Worth-Ratio = investment assets / net worth. This ratio should increase over time, as retirement for the medical professional approaches.

Savings to Income Ratio = savings / annual income. This ratio should also increase over time, especially as major obligations are retired.

Real Growth Ratio = (income this year – income last year) / (income last year – inflation rate). It is desirable for the medical professional to keep this ratio growing faster than the core rate f inflation.

Growth of Net-Worth Ratio = (net worth this year – net worth last year) / net worth last year – inflation rate. Again, this ratio should stay ahead of inflation.By calculating these ratios, perhaps on an annual basis, the medical professional can spot problems, correct them, and continue progressing toward stated financial goals.

Assessment

Now, after ten years, are these traditional ratios and advice still valid today: why or why not?

***

***

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

9. We act with honesty, integrity and are always straightforward. 8. We strive to be innovative, creative, iconoclastic, and flexible. 7. We admit and learn from mistakes and don’t repeat them. 6. We work hard always as competitors are trying to catch up. 5. We treat others with dignity and respect. 4. We are the onus of consulting advice for the well being of others. 3. We fight complacency as former success is in the past. 2. The best management styles are timeless, not timely. 1. Our clients are colleagues and always come first.

SPEAKING: Dr. David Edward Marcinko MBA MEd will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements.

***

***

CONTACT: Ann Miller RN MHA at: MarcinkoAdvisors@outlook.com

“Malta has quietly leveraged the rising tide of the financial transparency imperative to attract hedge funds.“

There was a time when the quaint island sought to play on the traditional terrain, offering anonymity and a “laissez-faire regulatory regime,” not to mention very low taxes, as in no capital gains taxes and no taxes on dividends; all while English speaking and USD currency denominated.

***

***

While many leading domiciles for offshore hedge funds remain in the Caribbean – notably the Cayman Islands, the British Virgin Islands, Bermuda, and the Bahamas – the island of Malta is drawing attention, especially from European funds.

SO – HOW MUCH IS A “FINANCIAL ADVISOR” REALLY WORTH?

This blog holds a rather uncomplimentary opinion of financial advisors, and the financial services and brokerage industry as a whole; deserved, or not? The entire site hints at this attitude as well, in favor of a going it alone or ME, Inc investing when possible. Nevertheless, it is reasonable to wonder how much boost in net-returns might an educated and informed, fee transparent and honest, fiduciary focused “financial advisor” add to a clients’ investment portfolio; all things being equal [ceteris paribus].

And, can it be quantified?

Well, according to Vanguard Brokerage Services®, perhaps as much as 3%? In a decade long paper from the Valley Forge, PA based mutual fund and ETF giant, Vanguard said financial advisors can generate returns through a framework focused on five wealth management principles:

• Being an effective behavioral coach: Helping clients maintain a long-term perspective and a disciplined approach is arguably one of the most important elements of financial advice. (Potential value added: up to 1.50%).

• Applying an asset location strategy: The allocation of assets between taxable and tax-advantaged accounts is one tool an advisor can employ that can add value each year. (Potential value added: from 0% to 0.75%).

• Employing cost-effective investments: This component of every advisor’s tool kit is based on simple math: Gross return less costs equals net return. (Potential value added: up to 0.45%).

• Maintaining the proper allocation through rebalancing: Over time, as investments produce various returns, a portfolio will likely drift from its target allocation. An advisor can add value by ensuring the portfolio’s risk/return characteristics stay consistent with a client’s preferences. (Potential value added: up to 0.35%).

• Implementing a spending strategy: As the retiree population grows, an advisor can help clients make important decisions about how to spend from their portfolios. (Potential value added: up to 0.70%).

Source: Financial Advisor Magazine, page 20, April 2014.

Assessment

However, Vanguard notes that while it’s possible all of these principles could add up to 3% in net returns for clients, it’s more likely to be an intermittent number than an annual one because some of the best opportunities to add value happen during extreme market lows and highs when angst or giddiness [fear and greed] can cause investors to bail on their well-thought-out investment plans.

And, is the study applicable to doctors and allied healthcare providers? Doe Vanguard have a vested interest in the topic. What about fee based versus fee-only financial advice?

Conclusion

Finally, recognize the plethora of other financial planning life-cycle topics addressed in this ME-P were not included in the Vanguard investment portfolio-only study a decade ago.

And what about today with contemporaneous internet advising, chat-rooms, linkedin, robo-advisors, reddit and the like?

According to Patricia Salber MD [personal communication], there are a number of reasons why direct patient access to laboratory medical results is a good idea:

Between 8 and 26% of abnormal test results, including those suspicious for cancer, are not followed up in a timely manner. Direct access could help reduce the number of times this occurs

Self-management, particularly of chronic illness has known benefits. Just like the QS people, many folks with chronic illness obtain and manage to self-acquired lab results every day via gluco-meters, home pulmonary function tests, blood pressure measurements, and so forth. Direct access to laboratory-acquired data, one could argue is a continuation of that personal responsibility

Patients want to be notified about their results in what they perceive as a timely fashion. In one study, patients who received direct notification of their bone density tests results were more likely to perceive they had timely notification compared to usual care even though there was no measurable effect on actual treatment received after three months

Being more responsible for test results could encourage consumers to try to learn more about the meaning of the test results, conceivably increasing their health literacy.

But, the arguments against direct access discussed include the following:

Patients prefer their physicians contact them directly when they have abnormal test results, although the major studies published in 2005 and 2009, preceded the extraordinary use of the internet to access health information that exists today.

There is concern over whether patients will know what to do when they receive the results – will they make erroneous interpretations or fail to contact their docs? This could be, but the intent of the proposed rule is shared access to the results. We suspect if the rule become law, docs will develop better notification mechanisms so that they reach the patient before the patient directly accesses the results or lab companies will design better lab test notifications with easy-to-understand interpretations or a whole new industry will appear that can provide instantly available individualized lab interpretation…or maybe all three of these would happen and that would be a very good thing.

Unknown impact of dual notification (doctors and patients) of lab test results on physician behavior…would docs simply shift responsibility for initiating follow-up care from themselves to their patients?

Would direct access of life-changing lab tests, such as HIV or malignancy, lead to unnecessary patient anxiety – or worse? (Conversely, is there less anxiety, desperation, or suicidal ideation if the bad news is delivered face to face?

Individuals likely may contact their physicians immediately after getting the lab results asking for a telephonic or face-to-face interpretation … it is not known how this would impact physician workload and/or potential for reimbursement [personal communication, Richard Hudson DO, Atlanta, GA].

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com

Posted on March 15, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

At least eight agencies are investigating a recent fire at a Bayer executive’s New Jersey home as a possible arson, authorities said. The fire happened around 7:30 a.m. March 4th “at an occupied residence on East Lane in Madison,” the Morris County Prosecutor’s Office told CNN yesterday.

US stocks bounced back sharply on Friday to cap a volatile week on Wall Street as the risk of a government shutdown eased while investors stayed on watch for the next move in an escalating trade war. The S&P 500 (^GSPC) climbed more than 2.1% after the benchmark index sank on Thursday to close in correction territory. The NASDAQ Composite (^IXIC) jumped over 2.6% as tech stocks soared. The Dow Jones Industrial Average (^DJI) moved up more than 600 points, or 1.6%.

Yesterday March 14th was Pi Day! (Yes, the mathematical constant, although we fully support celebrating with actual pie.) Put simply, Pi—aka π—is the ratio of a circle’s circumference to its diameter. It also sneaks its way into medicine. For one, it’s part of Poiseuille’s Law, an equation that helps explain how fluid flows through tubes, including arteries and IV lines. So, whether you’re crunching numbers or crunching on a slice, Pi is definitely worth celebrating

And, today is the Ides of March!

Visualize: How private equity tangled banks in a web of debt, from the Financial Times.

Posted on March 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEdCMP®

***

***

Your Executor or personal representative is named in your Will and is responsible for management of assets subject to probate. A basic checklist of the duties of the personal representative looks like this:

Gather all estate assets;

Collect all amounts owed the decedent;

Notify creditors and paying all valid debts;

Selling assets as needed to pay expenses or as directed by the Will;

Distribute assets to beneficiaries;

File decedents final federal income tax return;

File an estate tax return if the estate is large enough; and

File inventories and annual returns with the probate court, if required.

The position requires a lot of responsibility and involves many duties and a considerable commitment of time. The personal representative must petition the probate court for formal appointment.

Selection of your personal representative should not be made lightly, or as a favor to a friend. It requires a lot of work and very often for little or no pay. Friends and family typically will not charge the estate for their time and work. Outside advisers like attorneys and accountants will not hesitate to bill for their work effort. A few items for your selection criteria should be:

Longevity – the person should have a likelihood of being able to serve after your death;

Skill in managing legal and financial affairs;

Familiarity with your estate and wishes;

Integrity and loyalty; and

Impartiality and absence of conflicts of interest.

Alternatives to family or friends might be a corporate executor, such as a bank, an attorney, or other adviser. Similar criteria should be used in the selection of a trustee.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Posted on March 7, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

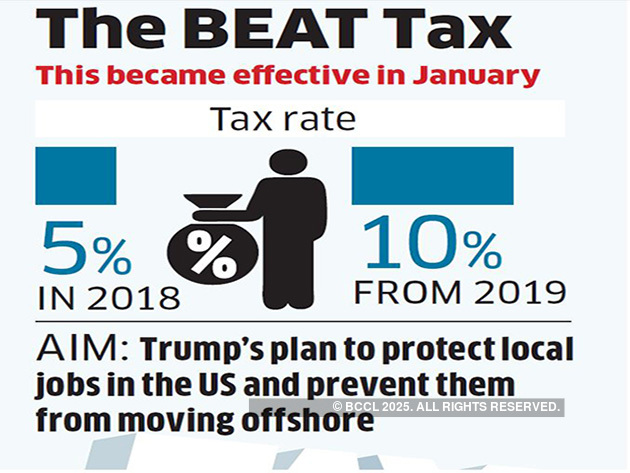

Base-Erosion Anti-Abuse Tax (BEAT): The 2017 tax reforms moved the U.S. from a worldwide taxation system to a quasi-territorial system, so foreign earnings are no longer included in a company’s domestic tax base.

To discourage companies operating in the U.S. from avoiding tax liability by shifting profits out of the country, Congress imposed a 10% minimum tax called Base-Erosion Anti-Abuse Tax (BEAT). The BEAT rate will increase from 10% to 12.5% in 2026.

Leverage ratios measure the amount of capital that comes from debt. In other words, leverage financial ratios are used to evaluate a company’s debt levels. Common leverage ratios include the following:

The debt ratio measures the relative amount of a company’s assets that are provided from debt:

Debt ratio = Total liabilities / Total assets

The debt to equity ratio calculates the weight of total debt and financial liabilities against shareholders’ equity:

Debt to equity ratio = Total liabilities / Shareholder’s equity

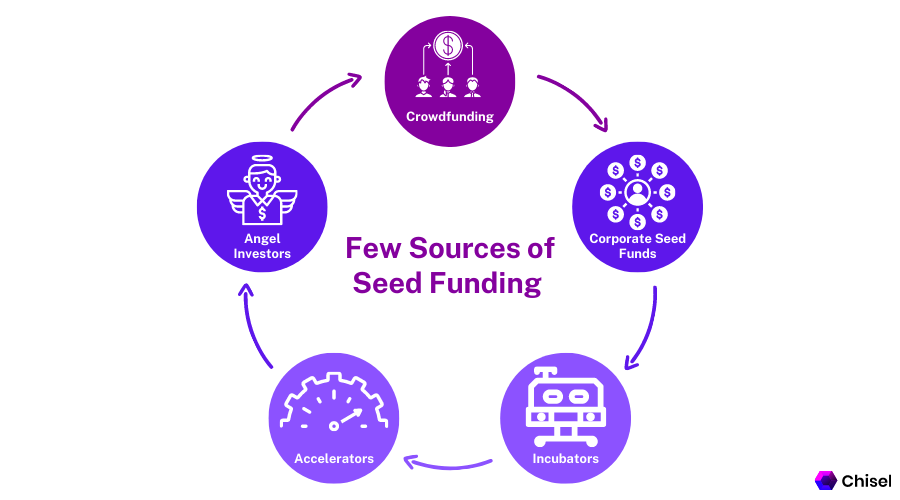

The term seed suggests that this is a very early investment, meant to support the business until it can generate cash of its own, or until it is ready for further investments. Seed money options include friends and family funding, seed venture capital funds, angel funding, and crowdfunding.

Types of Seed funding

Friends and family funding: This type of seed funding involves raising money from friends and family members.

Angel investing: As mentioned above, angel investors are wealthy individuals who provide seed funding in exchange for equity ownership.

Seed accelerators: These are programs that provide startups with seed funding, mentorship, and resources to help them grow their businesses.

Crowdfunding: This type of funding allows startups to raise money from a large number of people, typically through an online platform.

Incubators: These are organizations that provide startups with seed funding, office space, and resources to help them grow their businesses.

Government grants: Some government agencies provide seed funding for startups working on specific projects or in specific industries.

Corporate ventures: Some big companies set up venture arms to provide seed funding to startups in their industry or complementary field.

Micro-Venture Capital: A type of venture capital that provides seed funding to new startups and early-stage companies with a small amount of money.

In 1972, Nobel Laureate Kenneth J. Arrow, PhD shocked academe’ by identifying health economics as a separate and distinct field. Yet, the seemingly disparate insurance, tax, risk management and financial planning principles that he also studied are just now becoming transparent to some medical professionals and their financial advisors. Despite the fact that a basic, but hardly promoted premise of this new wave financial planning era, is imprecision.

Nevertheless, to informed cognoscenti like Certified Medical Planners™, the principles served as predecessors to the modern physician-focused financial advisory niche sector. In 2004, Arrow was selected as one of eight recipients of the National Medal of Science for his innovative views.

And now, as a long bull market may be over, and if the current “new-normal” prevails – meaning a 4.5% real annualized rate of return on equities and a 1.5% real rate on bonds – wealth accumulation for all may be reduced.

An Imprecise Science

There is a major variable, dominant in any marketplace that pushes an economy in a forward direction. It is called consumerism. This became apparent while waiting in a doctor’s office one recent afternoon.

Scenario:

The front office receptionist, who appeared to be about 21 years old, was breaking for lunch and her replacement, who appeared not much older, came over to assist. Realizing the propensity for a long wait, one was taken by the size of waiting room and the number of patients coming in and out of the office. [Americans consume healthcare and a lot of it]. There was another notable peculiarity. The sample prescription bags being carried out the door were no match for the bags under everyone’s eyes, including the doctor’s. The office staff was probably working overtime, if not two jobs, and the doctor was working harder and faster in a managed care system.

Assessment

Why? So they all could afford to buy and voraciously consume for their children and themselves. Americans indeed work longer hours than any other industrialized nation.

Conclusion

Finally, as women medical professionals entered the workforce in unprecedented numbers, the stock markets reached an all time high in 2025, even as money was spent at a feverish pace as the Federal Reserve pumped out money in inflammatory fashion.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com

Investing in Growth Stocks – Catching the Momentum [BIG-MO]

The growth style of investing focuses on companies with strong earnings and accelerating capital growth. A growth investor will make investment decisions based on forecasts of continuing growth in earnings. Growth investing emphasizes qualitative criteria, including value judgments about the company, its markets, its management, and its ability to extract future earnings growth from the particular industry.

Quantitative indicators of interest to the growth investor include high Price/Earnings ratios, Price/Sales ratios, and low dividend yields. A high P/E ratio suggests that the market is prepared to pay more per share in anticipation of future earnings. A low dividend yield suggests that the company is reinvesting rather than distributing profits. These indicators are considered in relation to the company’s immediate competitors. The companies with the highest P/E ratios relative to their industry will often be dominant within their market segment and have strong growth prospects. Growth investors will generally focus on premium and leading-edge companies.

***

***

Some industry sectors by their nature have stronger growth characteristics, particularly more innovative and speculative industries.

For example, during the bull market run on the U.S. stock markets during the late 1990s, the technology sector was a major area of growth investment. On observing strong earnings growth, a growth investor will decide whether to buy shares based on whether the company’s growth is going to continue at its present rate, to increase, or to decrease. If it is expected to increase, the growth investor will consider it a candidate for purchase. The key research question is: at what point will the company’s growth flatten out, or fall? If a company’s growth rate slows or reverses, it is no longer attractive to a growth investor. Growth investors are normally prepared to pay a premium for what they believe to be high quality shares. The potential downside in growth investing is that if a company goes into sudden decline and the share price falls, you can lose capital value rapidly.

Growth stocks, like the current “Magnificent-Seven“, carry high expectations of above-average future growth in earnings and above-average valuations. Investors expect these stocks to perform well in the future and are willing to pay high P/E multiples for this expected growth. The danger is that the price may become too high. Generally, once a company sports a P/E ratio above 50, the risk significantly escalates. Many technology growth stocks traded at a P/E ratio of above 100 during 1999. This is unsustainable. No company in the history of the stock market has been able to maintain such a high P/E level for a sustained period of time.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

While health care is not “do-it-yourself,” an informed patient can be an asset. A poorly informed patient, on the other hand, clearly complicates treatment. Assume the responsibility of being the primary information source and educator for your patient. To help deal with a self-diagnosing patient, consider the following as suggested by: David B. Troxel, MD, Medical Consultant to The Doctors Company:

Encourage patients to always check with you about the accuracy of information obtained from external sources. Use the intake time to find out what Internet information the patient has found.

Directly discuss what the patient has read, even if the patient’s external source is a good one in your professional opinion. The exchange enhances your relationship with the patient and can increase treatment compliance. Welcome questions, and help put the patient’s information in the appropriate context.

Provide your patient with a list of Web sites that provide accurate information, such as the Centers for Disease Control and Prevention (www.cdc.gov). Make sure the patient understands the limitations of the Internet.

Document in the patient’s chart your diagnosis, your treatment management plan, and medication prescribed, as well as the reasons behind your decisions.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Marcinko Associates is a financial guide. We help answer your questions in an empowering way. We educate and empower medical colleagues to understand their financial picture and to make better financial decisions. We strive to simplify everything, clear up confusion, and address specific needs and goals.

Whatever your financial situation, we do not shame, criticize, or sell. We enrich, educate and empower. We work with medical colleagues at every stage of their financial journey, through big life personal changes to annual employment reviews, in order to help them understand, invest, and protect their money and autonomy.

And, like the famed ‘Tibetan Sherpas“, we guide physician entrepreneurs from medical practice business plan creation, funding, start-up operations and strategic management improvement to maximize profits and stream-line patient care quality initiatives.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

9. We act with honesty, integrity and are always straightforward. 8. We strive to be innovative, creative, iconoclastic, and flexible. 7. We admit and learn from mistakes and don’t repeat them. 6. We work hard always as competitors are trying to catch up. 5. We treat others with dignity and respect. 4. We are the onus of consulting advice for the well being of others. 3. We fight complacency as former success is in the past. 2. The best management styles are timeless, not timely. 1. Our clients are colleagues and always come first.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Posted on February 20, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

SAVE A LIFE

By Dr. David Edward Marcinko MBA MEd and Staff Reporters

***

***