BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Pink sheets are an over-the-counter (OTC) market that connects broker-dealers electronically. There is no trading floor and the quotations are also all done electronically. Since there is no central trading floor or stock exchange like the New York Stock Exchange (NYSE), the pink sheet-listed companies do not have the same criteria to fulfill as the companies listed on national stock exchanges. Many stocks listed on the pink sheets are low-priced penny stocks that trade for under $5 a share.

Pink sheets got their name because the original pink sheets listing the stocks were actually printed and distributed on pink pieces of paper. Trading over-the-counter (OTC) refers to the process of how securities listed on the pink sheets are traded through a broker-dealer network.

Recent advances in biomedical and health sciences—from immunotherapy to treat cancer, to the highly effective COVID-19 vaccines—demonstrate the strengths and successes of the U.S. biomedical enterprise. Such advances present an opportunity to revolutionize how to prevent, treat, and even cure a range of diseases including cancer, infectious diseases, Alzheimer’s disease, and many others that together affect a significant number of Americans.

To improve the U.S. government’s capabilities to speed research that can improve the health of all Americans, President Biden is proposing the establishment of the Advanced Research Projects Agency for Health (ARPA-H). Included in the President’s FY2022 budget as a component of the National Institutes of Health (NIH) with a requested funding level of $6.5B available for three years, ARPA-H will be tasked with building high-risk, high-reward capabilities (or platforms) to drive biomedical breakthroughs—ranging from molecular to societal—that would provide transformative solutions for all patients.

Posted on March 22, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

Managerial Accounting

By Dr. David E. Marcinko MBA

Recently, several major banking institutions have addressed the problem of escalating debt upon graduating physicians, mid-life practitioners and even seasoned healthcare providers; despite historically low rates for prime customers.

Unfortunately, one may still wonder how many clinicians truly appreciate the risks associated with usurious interest rates for homes, cars, medical equipment and other consumer items; as we offer the following review to reduce this peril.

Posted on March 17, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

Advancing the Science of Medicine with a Priceless, No Cost Option

Everything we know about the human body comes from studying whole body donors. At MedCure, they connect you or your loved ones to the physicians, surgeons, and researchers who are continuing this vital work. Their discoveries and innovations help people live longer, make treatments less invasive, and create new ways to prevent illness or disease.

They are constantly overwhelmed by the incredible generosity and selflessness of donors. MedCure honors their gifts by covering, upon acceptance, all expenses related to the donation process. These costs include transportation from the place of passing, cremation, and a certified copy of the death certificate, as well as the return of cremated remains to the family or a scattering of the ashes at sea. By request, they can provide a family letter that shares more detailed information on how you or your loved one contributed to medical science.

Devaluation is the deliberate downward adjustment of the value of a country’s money related to another currency, group of currencies or currency standard. It is often confused with depreciation and is the opposite of revaluation which refers to the readjustment of a currency exchange rate.

The government of a country may decide to devalue its currency and like depreciation it is not the result of non-governmental activities.

One reason a country made devalue its currency is to combat a trade imbalance. Devaluation reduces the cost of a country’s export rendering them more competitive in the Global market which is which in turn increases the cost of imports.

If imports are more expensive domestic consumers are less likely to purchase them further strengthening domestic businesses because exports increase and imports decrease there is typically a better balance of payments because the trade deficit shrinks. In short a country that devalue its currency can produce is difficult because there is a greater demand for cheaper exports.

***

***

In accountancy, depreciation refers to two aspects of the same concept: first, the actual decrease of fair value of an asset, such as the decrease in value of factory equipment each year as it is used and wear, and second, the allocation in accounting statements of the original cost of the assets to periods in which the assets are used (depreciation with the matching principle).

Depreciation is thus the decrease in the value of assets and the method used to reallocate, or “write down” the cost of a tangible asset (such as equipment) over its useful life span. Businesses depreciate long-term assets for both accounting and tax purposes. The decrease in value of the asset affects the balance sheet of a business or entity, and the method of depreciating the asset, accounting-wise, affects the net income, and thus the income statement that they report.

Paul Edward Farmer (October 26, 1959 – February 21, 2022) was an American medical anthropologist and physician. Farmer held an MD and PhD from Harvard University, where he was the Kolokotrones University Professor and the chair of the Department of Global Health and Social Medicine at Harvard Medical School. He was the co-founder and chief strategist of Partners In Health (PIH), an international non-profit organization that since 1987 has provided direct health care services and undertaken research and advocacy activities on behalf of those who are sick and living in poverty. He was professor of medicine and chief of the Division of Global Health Equity at Brigham and Women’s Hospital.

Dr. Farmer had written extensively on health and human rights, the role of social inequalities in the distribution and outcome of infectious diseases, and global health.

The Physician Executive Summary is always included at the beginning of a formal business plan and represents a brief synopsis of the medical prarctice entire plan. Its appearance, grammar and style should be sharp and crisp as it represents an enticement for the reader to maintain interest and contribute intelligent or economic input into the new venture.

It should contain information about the practice, advertising and marketing opportunities, physician management, proposed financing with four Pro Forma financial statements, business operations and exit strategy. This last point, while unpleasant is often overlooked by naive practitioners. Business experts however, look favorably upon an escape plan and view it as the mark of mature professional that realizes the possibility of success as well as failure.

****

***

Ultimately, the plan must explain to potential investors how you will make the practice profitable and produce the required Return on Investment (ROI) for them. It must describe medical services, patient acceptance and benefits, provider qualifications and accomplishments, the amount of capital required, market size, potential practice growth rate, and market niche.

Additional information may include office location, proximity to labor, transportation, license requirements, business entity status, proprietary technology and potential working agreements with various insurance, managed care, ACA and HMO plans. If all of the above seems bewildering to the uninitiated, you are correct.

Remember however, that if you do not have, or can’t borrow the funds to begin a private practice, you will just have to become an employed practitioner until you can. It is therefore imperative to start off on the right foot, with a sound business plan, as you begin your medical career.

People really love money since it is needed to buy just about everything. In fact, we actually published a formal print dictionary on health economics and finance terms that is very popular with physician investors and medical colleagues; it is a favorite of economic students as well!

And, money is by far one of those words that has more slang or terms for it than any others. This proves that cash or money, does not have be boring when speaking about it. Just keep in mind that these slang synonyms are in plural form. They are also words mostly used for US currency.

Perhaps the fact that money is so important may help to explain why there are so many different ways to say it. These 95 slang words for money and their meanings are really worth taking a look at. This list not only contains the countless ways to speak, write or say the word money, but also what are the meanings behind each phrase or term.

The International Franchise Association (IFA) estimates that that about $1 trillion in sales, or 40% of all retail sales, were made through franchised establishment last year. On the positive side, franchises offer a branded practice concept with management training and access to proprietary methods, marketing and advertising campaigns and a host of support.

Moreover, there are franchises available for virtually every healthcare product or service, including: diet, weight loss and fitness; vein care and laser surgery; vitamins, nutriceuticals and pharmaceuticals; plastic and cosmetic surgery; dermatology, tanning and skin care; home healthcare and extended, etc. Some well know established healthcare and medical franchises are: Doctors Express, Being There Senior Care, Home Care Assistance, Personal Training Institute, Inches-A-Weigh, Remedy Intelligent Staffing, Visiting Angels, Unlimited MedSearch, prnYourHealth and Any Lab Test Now, etc.

On the downside, franchises incur high start-up costs, rules and obligations, payment of franchise percentages and many contractual obligations. Questions to consider when contemplating this business entity include:

Franchise stability, track record, licensing and costs.

Training, support and proximity of other franchises.

Independence, ownership laws, contracts and dispute resolutions,

Screening methods, market size and potential market share.

Replacement cost and transferability?

For more information on Uniform Franchise Offerings Circulars (UFOCs) contact www.FranChoice.com or:

The business cycle is also known as the economic cycle and reflects the expansion or contraction in economic activity. Understanding the business cycle and the indicators used to determine its phases may influence investment or economic business decisions and financial or medical planning expectations. Although often depicted as the regular rising and falling of an episodic curve, the business cycle is very irregular in terms of amplitude and duration.

Moreover, many elements move together during the cycle and individual elements seldom carry enough momentum to cause the cycle to move. However, elements may have a domino effect on one another, and this is ultimately drives the cycle. We can also have a large positive cycle, coincident with a smaller but still negative cycle, as seen in the current healthcare climate of today.

First Phase: Trough to Recovery (production driven)

Scenario: A depressed GNP leads to declining industrial production and capacity utilization. Decreased workloads result in improved labor productivity and reduced labor (unit) costs until actual producer (wholesale) prices decline.

Second Phase: Recovery to Expansion (consumer driven)

Scenario: CPI declines (due to reduced wholesale prices) and consumer real income rises, improving consumer sentiment and actual demand for consumer goods.

Third Phase: Expansion to Peak (production driven)

Scenario: GNP rises leading to increased industrial production and capacity utilization. But, labor productivity declines and unit labor costs and producer (wholesale) prices rise.

Fourth Phase: Peak to Contraction (consumer driven)

Scenario: CPI rises making consumer real income and sentiment erode until consumer demand, and ultimately purchases, shrink dramatically. Recessions may occur and economists have an alphabet used to describe them.

For example, with a V, the drop and recovery is quick. For U, the economy moves up more sluggishly from the bottom. A W is what you would expect: repeated recoveries and declines. An L shaper recession describes a prolonged dry economic spell or even depression.

NOTE: Historically, contractions have had a shorter duration than expansions.

Bull and Bear Markets for Medical Professionals

A bull market is generally one of rising stock prices, while a bear market is the opposite. There are usually two bulls for every one bear market over the long term.

More specifically, a bear market is defined as a drop of twenty percent or more in a market index from its high, and can vary in duration and severity. While a bull market has no such threshold requirement to exist, other than they exist between these two periods of sharp decline.

Whither the Bear?

As a doctor, your action plan in a bear market depends on many variables, with perhaps your age being the most important:

In your 30s:

Pay off debts, school or practice loans.

Invest in safe money market mutual funds, cash or CDs.

Start retirement plan or 401-K account.

In your 40s:

Increase your pension plan or 401-K contributions.

Stay weighted more toward equity investments.

Review your goals, risk tolerance and portfolio.

In your 50s:

Position assets for ready cash instruments.

Diversify into stock, bonds and cash.

Retirement:

Maintain 3 years of ready cash living expenses.

Reduce, but still maintain your exposure to equities.

ASSESSMENT: So, where are we right now in the economic business cycle? Your thoughts are appreciated.

Whether you do contract work or have your own small business, tax deductions for the self-employed physician consultant and/or medical executive or nurse consultant, etc., can add up to substantial tax savings.

With self-employment comes freedom, responsibility, and a lot of expense. While most self-employed people celebrate the first two, they cringe at the latter, especially at tax time. They might not be aware of some of the tax write-offs to which they are entitled.

When it comes time to file your returns, don’t hesitate to claim the benefits you get for being the boss. As a self-employed success story, you’ve earned them.

FORM 1099NEC: Form 1099 NEC is one of several IRS tax forms used in the United States to prepare and file an information return to report various types of income other than wages, salaries, and tips. The term information return is used in contrast to the term tax return although the latter term is sometimes used colloquially to describe both kinds of returns.

“Many times an overlooked deduction is educational expenses. If one is taking courses or buying research material to be more effective in their work, this can be deductible.”

Individual Retirement Plans (IRAs)

One of the best tax write-offs for the self-employed physician consultant is a retirement plan. A person with no employees can set up an individual 401 (k). “You can contribute $19,500 in 2021 as a 401(k) deferral, plus 25 percent of net income.”

If you have employees, consider a SIMPLE (Savings Incentive Match Plan for Employees) IRA—an IRA-based plan that gives small employers a simplified method to make contributions to their employees’ retirement. As of 2021, an employee may defer up to $13,500 and employees over 50 may contribute an additional $3,000.

“A third retirement plan is Simplified Employee Pension IRA (SEP IRA).” The employer may contribute the lesser of 25 percent of income or $58,000 in 2021. If the employer has eligible employees, an equal percentage of their income must be contributed.

Recall that retirement plans are “absolutely the No. 1 tax deduction. The government is helping fund retirement.”

Business use of home or dwelling

Now, most self-employed taxpayers’ businesses start as home-based businesses. These people need to know portions of business costs are deductible and so “It is very important that you keep track of expenses relating to your housing costs.”

If your gross income from your business exceeds your total expenses, then you can deduct all of your expenses related to the business use of your home. If your gross income is less than your total expenses, your deduction will be limited to the difference between your gross income and the sum of all business expenses you would pay if the business was not in your home. Those expenses could include telephone lines, the Internet, and other costs to do business.

You must also have a home office that is truly used for work and the Internal Revenue Service may require you to document this.

***

Deducting automobile expenses

If you travel for business, even short distances within your own city, you may deduct the dollar value of business miles traveled on your tax return. The taxpayer may file the actual expense s/he incurred, or use the standard mileage rate prescribed by the IRS, which is 56 cents as of 2021. The IRS allowable mileage rates should be checked every year as they can change.

“If you decide to use actual car expenses, be sure to include payments, depreciation, registration, insurance, garage rent, licenses, repairs and maintenance, and parking and toll fees.” AND, “If you decide to use the standard mileage rate, it would be in your best interest to keep a log—daily, weekly or monthly—of miles driven to distinguish personal use from business use.”

Depreciation of property and equipment

Some self-employed people may purchase property and equipment for a business. If they expect that property to last longer than one year, it should be depreciated on the tax return.

Claims regarding property, according to the IRS, must meet the following criteria: You must own the property and it must be used or held to generate income. The property should have an estimated useful life, meaning you should be able to guess how long you can generate income with it. It may not have a useful life of one year or less, and may not be purchased and disposed of in the same year.

Certain repairs on property used for business may also be deducted.

Educational expenses

Any educational expense is potentially tax-deductible.

“Many times an overlooked deduction is educational expenses. “If one is taking courses or buying research material to be more effective in their work, this can be deductible.”

Think about any books, web courses, local college courses, or other classes or materials that you have purchased to improve your job or business. It’s easy to forget a work-related webinar or business e-book that was purchased online, so remember to save e-receipts.

Also recall that subscriptions to trade or professional publications and donations to business organizations, both of which are frequently necessary for the continuation and growth of your business.

Other areas to explore

Other deductions that can be easily missed are advertising and promotional expenses, banking fees, and air, bus, or train fare. Restaurant meals and other entertainment costs may be written off as long as they are necessary business expenses.

And, consider health insurance premiums, which in most cases represent a credit rather than a tax deduction. “A credit goes directly against one’s taxes, rather than a reduction of income.”

Regardless of which expenses you discover that you may write off, the most important thing is to keep accurate records throughout the year. Save receipts, including e-mail receipts, and file or log them so you have easy access to them at tax time. Not only does keeping receipts, mileage logs, and other expense records make filing taxes easier, but it also facilitates a system that allows you to track changes from year to year.

***

Long-term tax-saving strategies

Don’t just look at last-minute write-offs when considering self-employment tax deductions. Think about laying down some long-term strategies for money savings from year to year—particularly if you are a high earner.

“Accountants typically tell you what you have to pay but they don’t always tell you strategies to reduce your payments.”

To reduce your gross taxable income, consider setting up a defined-benefit pension plan. This plan is based on your age and income: The older you are and the higher your earnings, the more you are allowed to contribute. An alternative plan is an age-weighted profit-sharing plan, which is similar and can benefit those who have several employees.

Another strategy for high-earning business owners who own their own building through a limited liability company or similar business structure is to pay themselves rent. This rent is used to pay down the mortgage, but it is also considered a business expense for tax purposes.

Self-employed professionals required to have liability insurance should consider setting up their own insurance company. A captive insurance company is one that insures the risks of the business—or businesses, in the case of a cooperative. Its premiums can be tax-deductible.

But, if money accumulates and claims are minimal, the money taken out is taxable under capital gains. This is not a retirement strategy, but that it can save you money by allowing you to “pay yourself” instead of an insurance company and still deduct the premiums.

Assessment

With any of these more complicated, long-term strategies, consult with a business attorney, CPA/EA or financial planner to ensure you have the best plan possible for your business.

The modes of persuasion, modes of appeal or rhetorical appeals (Greek: pisteis) are strategies of rhetoric that classify a speaker’s or writer’s appeal to their audience. These include ethos, pathos, and logos.

Rhetorical appeal with persuasion elements are often key attributes for doctors, medical professionals, lawyers, CPAs, and all sorts of financial advisors and medical management consultants, etc.

Just like real estate, butter has been around for thousands of years. Sometime in the 1800’s someone decided that there was a need for something that looked like butter, tasted similar to butter, but wasn’t butter. Along came margarine. Real estate investment trusts (REITs) are the margarine of the real estate investing world.

NAREIT, the National Association of Real Estate Investment Trusts, answers the question

“What is a REIT?” in the following way:

“A REIT, or Real Estate Investment Trust, is a type of real estate company modeled after mutual funds. REITs were created by Congress in 1960 to give all Americans – not just the affluent – the opportunity to invest in income producing real estate in a manner similar to how many Americans invest in stocks and bonds through mutual funds. Income-producing real estate refers to land and the improvements on it – such as apartments, offices or hotels. REITs may invest in the properties themselves, generating income through the collection of rent or they may invest in mortgages or mortgage securities tied to the properties, helping to finance the properties and generating interest income.”

While REITs typically own real estate, investors in REITs do not. REITs are paper assets that represent interest in a company that owns and operates income producing properties. In essence they are real estate flavored stock. As such, REITs are generally highly correlated with the stock market.

***

***

TERMINOLOGY

When discussing REITs, you encounter the following terminology – public, private, traded, and non-traded. Public REITs can be designated as non-traded or traded depending on whether or not they are traded on a stock exchange.

Since traded REITs are traded on the stock exchange, they enjoy a high degree of liquidity just like any other stock. Unfortunately, traded REITs tend to follow the economic cycles and can closely correlate with the stock market. This can lead to a higher degree of volatility than what is usually seen with physical real estate. Additionally, they do not afford the investor the tax-advantages that come with investments in physical real estate.

Private REITs and non-traded public REITs are not traded on an exchange. These are usually offered to accredited investors through broker-dealer networks. These REITs are illiquid and generally have high fees. They have been plagued with transparency issues as well as conflicts of interest. Valuation of this stock is difficult and can be misleading to the investor. Due diligence is very important as the quality of non-traded REITs can vary widely.

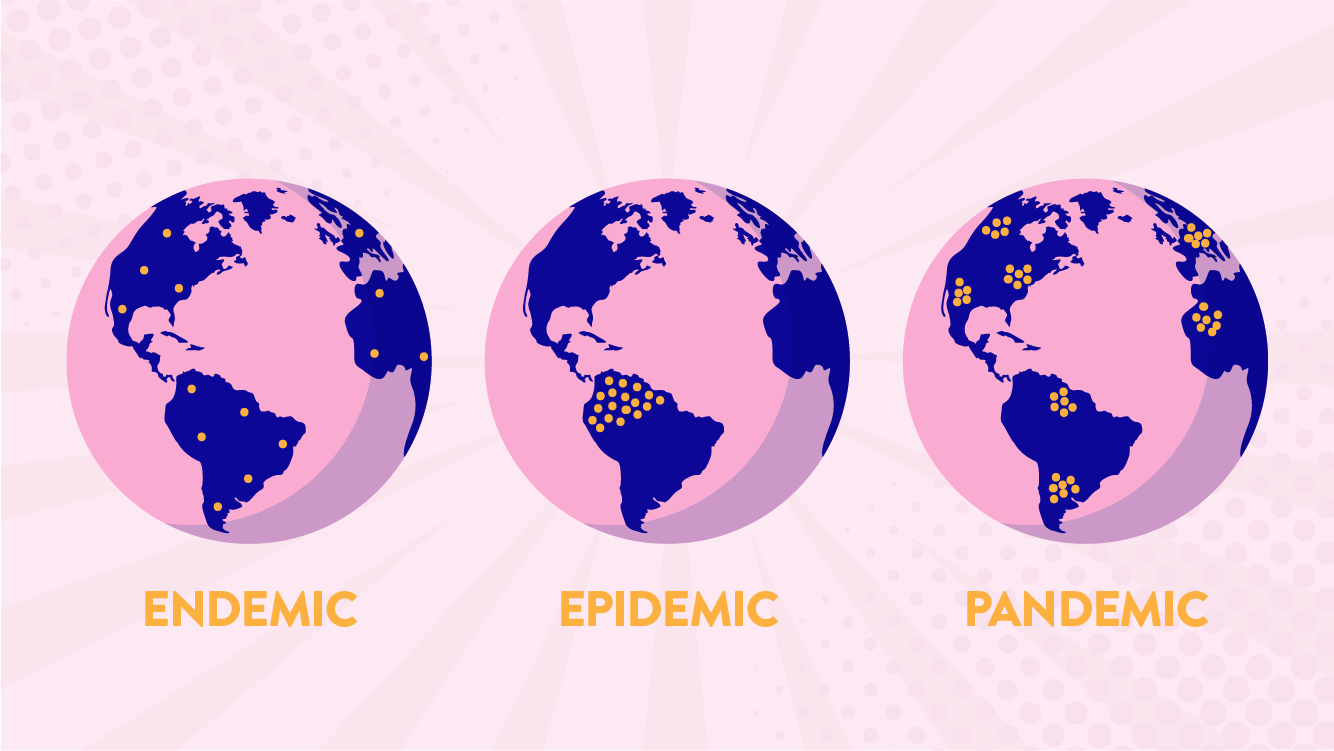

A Pandemic (from Greek πᾶν pan “all” and δῆμος demos “people”) is an epidemic of disease that has spread across a large region; for instance multiple continents, or even worldwide. A widespread endemic disease that is stable in terms of how many people are getting sick from it is not a pandemic.

Further, flu pandemics generally exclude recurrences of seasonal flu. Throughout history, there have been a number of pandemics, such as smallpox and tuberculosis. One of the most devastating pandemics was the Black Death, which killed an estimated 100 million people in the 14th century. Some recent pandemics include: HIV, Spanish flu, 2009 flu pandemic and H1N1.

An Epidemic is the rapid spread of infectious disease to a large number of people in a given population within a short period of time, usually two weeks or less.

For example, in meningococcal infections, an attack rate in excess of 15 cases per 100,000 people for two consecutive weeks is considered an epidemic.

Epidemics is the outbreak of the disease in a community while pandemic is the outbreak of the disease globally.

SARS was an epidemic while AIDS was an pandemic.

Pandemic disease has the same origin or source where so ever it gets spread while the same disease is spreading with different sources in each country, it refers to epidemic.

Epidemic when extending to greater levels becomes a pandemic.

ENDEMIC: If you translate it literally, endemic means “in the population.” It derives from the Greek endēmos, which joins en, meaning “in,” and dēmos, meaning “population.” “Endemic” is often used to characterize diseases that are generally found in a particular area; malaria, for example, is said to be endemic to tropical and subtropical regions. This use differs from that of the related word epidemic in that it indicates a more or less constant presence in a particular population or area rather than a sudden, severe outbreak within that region or group.

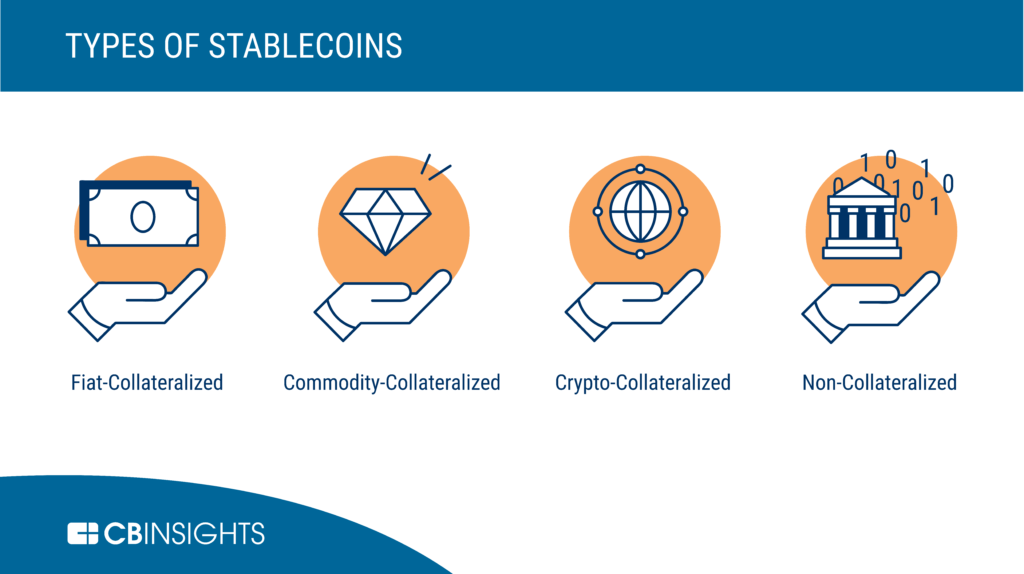

DEFINITION: Stablecoins are blockchain-based digital currencies that have been created with the aim to have a stable value. Stablecoins achieve price-stability through various different methods such as a peg against a fiat currency or a commodity, through collateralization against other cryptocurrencies or through algorithmic coin supply management.

Every stable coin includes a specific set of mechanisms that mostly behave in the same way. In general, stable coins keep collateral of the asset and manage the supply. In this way, they incentivize the market, which allows trade of the coin for no more or less than $1.

A stable coin can be considered the best depending on several factors: It should be stable. PAX is one the most stable stablecoin. It should be liquid and available on most exchanges. It should be backed by FIAT. PAX is 100% collateralized in US bank accounts. It should be regulated. It should be redeemable.

The physician, nurse, or other medical professional should easily recognize that there are a vast array of opportunities, obstacles, and pitfalls when it comes to managing one’s finances. Still, with some modicum of effort, the basic aspects of insurance, investments, taxes, accounting, portfolio management, retirement and estate planning, debt reduction, asset protection and practice management can be largely self-taught. Yet, it is realized that nuances and subtleties can make a well-intentioned financial plan fall short. The devil truly is in the details. Moreover, none of these areas can be addressed in isolation. It is common for a solution in one area to cause a new set of problems in another.

Accordingly, most health care practitioners would be well served to hire [independent, hourly compensated and prn] financial help. Unlike some medical problems, financial issues may not cause any “pain” or other obvious symptoms. Medical professionals tend to have far more complex financial situations than most lay people. Despite the complexities of the new world of health reform, far too many either do nothing; or give up all control totally, to an external advisor. This either/or mistake can be costly in many ways, and should be avoided.

In reality, and at various time in their careers, the medical professional needs a team comprised of at least a financial analyst, lawyer, management consultant, risk manager [actuary, mathematician or insurance counselor] and accountant. At various points in time, each member of the team, or significant others, will properly assume a role of more or less importance, but the doctor must usually remain the “quarterback” or leader; in the absence of a truly informed other, or Certified Medical Planner™.

This is necessary because only the doctor has the personal self-mandate with skin in the game, to take a big picture view. And, rightly or wrongly, investments dominate the information available regarding personal finance and the attention of most physicians. One is much more likely to need or want to discuss the financial markets with their financial advisor than private letter rulings by the IRS, or with their estate planning attorney or tax accountant. While hiring for expertise is a good idea, there is sinister way advisors goad doctors into using all their retail services; all of the time. That artifice is – the value of time.

True integrated physician focused and financial planning is at its core a service business, not a product or sales endeavor. And, increasingly money is more likely to be at the top of the list for providers as the healthcare environment is contracting.

So, eschewing the quarterback model of advice, and choosing to self-educate thru this book and elsewhere, may be one of the best efforts a smart physician can make.

Posted on November 16, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

TO H.R. RECRUITERS, UNIVERSITY HIRING MANAGERS & SEARCH COMMITTEES

Sooth My Academic Teaching and Classroom Withdrawal Pangs! “MY TEACHING PHILOSOPHY”

I’m screening for my next university Dean, Chair or teaching Professorship opportunity.

Currently, an endowed Resident-Scholar completing a text book production assignment complete with aligned case models, tests, quizzes, rubrics, curriculum teaching portfolio, and accreditation review.

Two-decades of domestic and international teaching experience and credentials in health economics, finance, investing, business, policy, risk management, IT and administration. Hundreds of peer-reviewed and trade publications [TNTC] with 30 major textbooks redacted in more than a thousand university libraries [NIH, Library Congress and National Institute Health, etc]. Public and population health global speaker and thought leader. Wall Street experience as start-up founder, entrepreneur and CXO.

Ideal mentor for under graduate thru post-doctoral and fellowship students [PhD, DBA, MD/DO, MHA and MBA, etc].

Compensation important, but fit is paramount as servant-leader.

[+] RANKED: Google Scholar and “H” Index

CV available upon request.

Although standard definitions will tell you that it is a ‘monetary policy’ used by central banks to stimulate the national economy, in reality it is more as follows:

– A cleverly disguised word that simply means ‘money printing’.

Once you do retire, and put your physician or medical career behind you, it’s important to realize that, at some point, the IRS expects you to draw down your 401(k) balance. Starting at age 72, you need to take required minimum distributions (RMDs).

Your annual RMD amount depends on the balance of your 401(k) and a formula that determines your life expectancy.

***

***

QUERY: But – What happens if you don’t take your RMD for the year?

ANSWER: Well, you could end up paying a penalty. In fact, it’s a pretty hefty penalty of up to 50% of the amount you were supposed to withdraw. Paying that penalty can be pretty costly for someone living in retirement. As long as you’re vigilant and stay on top of the situation, though, you can avoid the penalty as well as these other costly 401(k) mistakes.

Posted on November 10, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

For Doctors and Advisors

BOOK REVIEWS WITH FOREWORD

Reviews

Written by doctors and healthcare professionals, this textbook should be mandatory reading for all medical school students―highly recommended for both young and veteran physicians―and an eliminating factor for any financial advisor who has not read it. The book uses jargon like ‘innovative,’ ‘transformational,’ and ‘disruptive’―all rightly so! It is the type of definitive financial lifestyle planning book we often seek, but seldom find. ―LeRoy Howard MA CMPTM,Candidate and Financial Advisor, Fayetteville, North Carolina I taught diagnostic radiology for over a decade. The physician-focused niche information, balanced perspectives, and insider industry transparency in this book may help save your financial life. ―Dr. William P. Scherer MS, Barry University, Ft. Lauderdale, Florida This book was crafted in response to the frustration felt by doctors who dealt with top financial, brokerage, and accounting firms. These non-fiduciary behemoths often prescribed costly wholesale solutions that were applicable to all, but customized for few, despite ever-changing needs. It is a must-read to learn why brokerage sales pitches or Internet resources will never replace the knowledge and deep advice of a physician-focused financial advisor, medical consultant, or collegial Certified Medical Planner™ financial professional. ―Parin Khotari MBA,Whitman School of Management, Syracuse University, New York In today’s healthcare environment, in order for providers to survive, they need to understand their current and future market trends, finances, operations, and impact of federal and state regulations. As a healthcare consulting professional for over 30 years supporting both the private and public sector, I recommend that providers understand and utilize the wealth of knowledge that is being conveyed in these chapters. Without this guidance providers will have a hard time navigating the supporting system which may impact their future revenue stream. I strongly endorse the contents of this book.

―Carol S. Miller BSN MBA PMP,President, Miller Consulting Group, ACT IAC Executive Committee Vice-Chair at-Large, HIMSS NCA Board Member This is an excellent book on financial planning for physicians and health professionals. It is all inclusive yet very easy to read with much valuable information. And, I have been expanding my business knowledge with all of Dr. Marcinko’s prior books. I highly recommend this one, too. It is a fine educational tool for all doctors.

―Dr. David B. Lumsden MD MS MA,Orthopedic Surgeon, Baltimore, Maryland There is no other comprehensive book like it to help doctors, nurses, and other medical providers accumulate and preserve the wealth that their years of education and hard work have earned them. ―Dr. Jason Dyken MD MBA, Dyken Wealth Strategies, Gulf Shores, Alabama I plan to give a copy of this book written ‘by doctors and for doctors’ to all my prospects, physician, and nurse clients. It may be the definitive text on this important topic. ―Alexander Naruska CPA, Orlando, Florida

Health professionals are small business owners who need to apply their self-discipline tactics in establishing and operating successful practices. Talented trainees are leaving the medical profession because they fail to balance the cost of attendance against a realistic business and financial plan. Principles like budgeting, saving, and living below one’s means, in order to make future investments for future growth, asset protection, and retirement possible are often lacking. This textbook guides the medical professional in his/her financial planning life journey from start to finish. It ranks a place in all medical school libraries and on each of our bookshelves. ―Dr. Thomas M. DeLauro DPM, Professor and Chairman – Division of Medical Sciences, New York College of Podiatric Medicine

Physicians are notoriously excellent at diagnosing and treating medical conditions. However, they are also notoriously deficient in managing the business aspects of their medical practices. Most will earn $20-30 million in their medical lifetime, but few know how to create wealth for themselves and their families. This book will help fill the void in physicians’ financial education. I have two recommendations: 1) every physician, young and old, should read this book; and 2) read it a second time! ―Dr. Neil Baum MD, Clinical Associate Professor of Urology, Tulane Medical School, New Orleans, Louisiana

I worked with a Certified Medical Planner™ on several occasions in the past, and will do so again in the future. This book codified the vast body of knowledge that helped in all facets of my financial life and professional medical practice. ―Dr. James E. Williams DABPS, Foot and Ankle Surgeon, Conyers, Georgia

Almost everything you own and use for personal or investment purposes is a capital asset. Examples include a home, personal-use items like household furnishings, and stocks or bonds held as investments. When you sell a capital asset, the difference between the adjusted basis in the asset and the amount you realized from the sale is a capital gain or a capital loss.

Generally, an asset’s basis is its cost to the owner, but if you received the asset as a gift or inheritance, refer to Topic No. 703 for information about your basis.

For information on calculating adjusted basis, refer to Publication 551, Basis of Assets. You have a capital gain if you sell the asset for more than your adjusted basis. You have a capital loss if you sell the asset for less than your adjusted basis. Losses from the sale of personal-use property, such as your home or car, aren’t tax deductible.

DEFINITION: The meaning of meme stocks is sort of self-explanatory: hyped stocks that perform well. But from a fundamental perspective, they shouldn’t do well at all.

For example, Reddit forums and social media hype drive meme stocks. Speculators on Twitter and Reddit united together to trade their favorite companies in hopes of driving them “to the moon.”

It may not be fair to call them speculators. These hype beasts want to buy and hold stocks of companies that might not have a great long-term outlook.

Brokerages like Robinhood helped level the playing field with apps and ‘easier’ access. That’s giving retail traders more opportunity. Robinhood traders can buy with just a few clicks on their smartphones and use partial positions to buy chunks of stocks.

Posted on October 19, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

YOU DECIDE AND OPINE

By Dr. David E. Marcinko MBA

The Plot Thickens

Autumn is here, and leaves aren’t the only thing falling.

After seven months of higher monthly closes, plus one record-setting high early in the month, the benchmark S&P 500® Index wobbled its way to a 5% pullback in September. The causes were many—uncertainty emanating from Washington, inflation, supply chain problems, and softer earnings growth forecasts—and now the horizon is looking foggy as we gaze ahead toward the final months of 2021.

Shipping bottlenecks and a near-record number of job openings are raising costs and putting upward pressure on wages, which may start to hurt profit margins, and the twin specters of inflation and higher interest rates are making investors wonder when the Federal Reserve might step in to raise interest rates.

But, if there’s a potential bright spot, we have to look across the sea to the Eurozone, where the signs point toward an era of increased government spending that could be positive for global economic growth.

If you’ve ever listened to an early morning financial news broadcast, you’ve heard a reference to “futures” and how they affect the stock market before it opens. Physicians Investors follow the futures because it provides an indication of where stocks are headed at the opening bell. One of the most widely followed futures is the Dow Futures, whose underlying value is based on the Dow Jones Industrial Average, an index of 30 major U.S. companies.

***

***

DEFINITION: After the markets close at 4 pm New York time, implied open prices of the Dow Jones Industrial Average, S&P 500 Index, and NASDAQ, which fluctuate from minute to minute, can be calculated.

Considering the DJIA as an example, the basis of calculating implied open is the price of a “DJX index option futures contract “.

How much will it cost you to start a dental practice – with Business Plan?

There are many costs to consider to set up a successful dental practice. Note that the following values are not the exact amount but an average of setting up a dental practice:

Purchase price – this includes valuation fees of between $1,000-4,500, solicitor fees of between $4,000 – 17,000, accountancy and bank fees of around $3,000, and bank solicitors, which can be up to $3,500. Many of these can be reduced or obliterated.

Materials – $40,000

Lab fees – $36,000

Staff costs – $82,000

Other costs (associates fees) – [$245,000 – $295,000]

Other Factors

“Big” Tech – Many startup doctors want to include CBCT or CAD/CAM or 3D printing in their startup, any of which can add $25,000-$175,000. In other situations, waiting is the best option.

Cabinetry Preferences – Costs for cabinetry can range from $5,000 to $175,000.

Practice Management Software (PMS) – Pricing will range from a few thousand dollars to $25,000; OR none at all.

Mechanical Delivery – Typically referred to as chairs, lights, and units, this category of dental equipment costs will range between $5,000 and $100,000 based on your startup plans.

Vision – Ignore the so-called “experts” who will try to create a cookie-cutter model for your equipment costs. That is the thinking of corporate dentistry. You want a customized private practice vision that allows you to create a model matching your standards. Prioritize your vision, so your values and philosophy will lead your dental equipment budget and purchasing decisions. Your equipment budget will be—and should be—customized.

A cap on how much the US government can borrow to finance its operations.

It was introduced during World War I so that Congress wouldn’t have to approve every bond issuance by the Treasury Department as it had done previously—freeing up more time for name-calling.

The debt ceiling has been suspended dozens of times over the years, including 3x during the Trump administration.

Without suspending the debt ceiling, the US wouldn’t be able to borrow money to pay its bills—and things would get ugly if that happened. The federal government would have to slash spending for programs like Medicaid, local governments would find it harder to borrow, and financial markets could go haywire.

In short, a failure to act would “produce widespread economic catastrophe,” Treasury Secretary Janet Yellen wrote in the Wall Street Journal.

Important note: The debt ceiling doesn’t account for new spending, like the $3.5 trillion proposal the Democrats have on the table. Instead, it’s about spending Congress has already authorized, such as paying out Social Security. Over the years, the debt ceiling has become a “political weapon,” according to the AP, as each party tries to blame the other for their spending habits and for heaping more debt on the US.

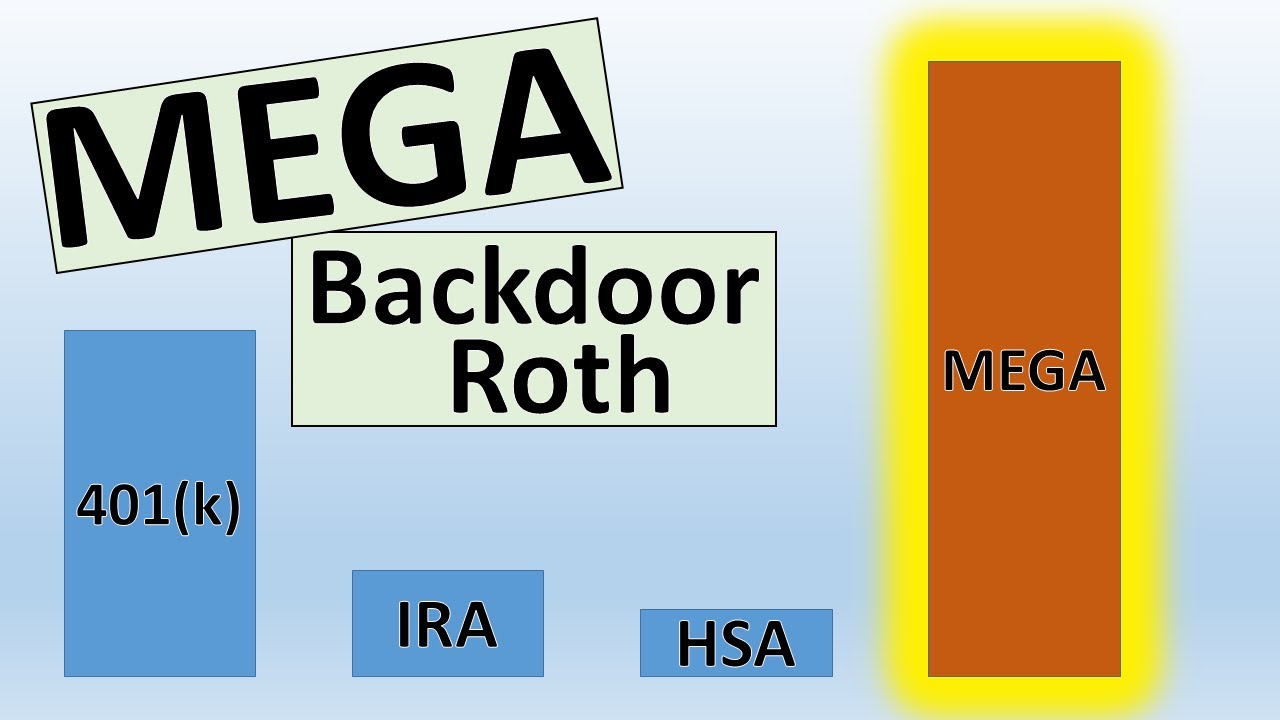

If you’re a physician looking to get ahead on planning for retirement, you’re likely familiar with individual retirement accounts, or IRAs. An IRA is a tax-advantaged vehicle that helps you grow your retirement savings. Roth IRAs are particularly attractive, because you don’t pay taxes on withdrawals in retirement.

There’s one problem: you can’t contribute to a Roth IRA directly if you make above a certain income. A backdoor IRA, though, can solve your problem by allowing you to convert a traditional IRA into a Roth.

Here’s how it works:

First, place your contribution in a traditional IRA—which has no income limits.

Then, move the money into a Roth IRA using a Roth conversion.

But make sure you understand the tax consequences before using this strategy.

The mega backdoor Roth allows you to put up to $38,500 in a Roth IRA or Roth 401(k) in 2021, on top of the regular contribution limits for those accounts. If you have a Roth 401(k) at work (and the plan allows for the mega option as described below), generally you can choose whether the final destination of your mega contributions is the Roth 401(k) or a Roth IRA. If your employer offers only a traditional 401(k), then your mega contributions would end up in a Roth IRA.

Here’s a quick summary of what you need to have in place for the ideal mega backdoor Roth strategy:

A 401(k) plan that allows “after-tax contributions.” After-tax contributions are a separate bucket of money from your traditional and Roth 401(k) contributions. About 43% of 401(k) plans allow after-tax contributions, according to a 2017 survey of large and midsize employers by consulting firm Willis Towers Watson.

Your employer offers either in-service distributions to a Roth IRA — that is, you can take money out of the 401(k) plan while you’re still working at the company — or lets you move money from the after-tax portion of your plan into the Roth 401(k) part of the plan. If you’re not sure, ask your human resources department or plan administrator.

You’ve got money left over to save, even after maxing out your regular 401(k) and Roth IRA contributions.

Do your children have income-generating assets in a custodial account?

If so, be sure you understand the so-called kiddie tax.

This law was passed to discourage wealthier individuals from transferring assets to their children to take advantage of their lower tax rates. The kiddie tax has seen many iterations but current rules tax a minor child’s unearned income—including capital gains distributions, dividends, and interest income—at the parents’ tax rate if it exceeds the annual limit ($2,200 in 2021).

The tax applies to dependent children under the age of 18 at the end of the tax year (or full-time students younger than 24) and works like this:

The first $1,100 of unearned income is covered by the kiddie tax’s standard deduction, so it isn’t taxed.

The next $1,100 is taxed at the child’s marginal tax rate.

Anything above $2,200 is taxed at the parents’ marginal tax rate.

So – If your child also has earned income, say from a summer job or legitimate work in your medical office or practice, the rules become more complicated.

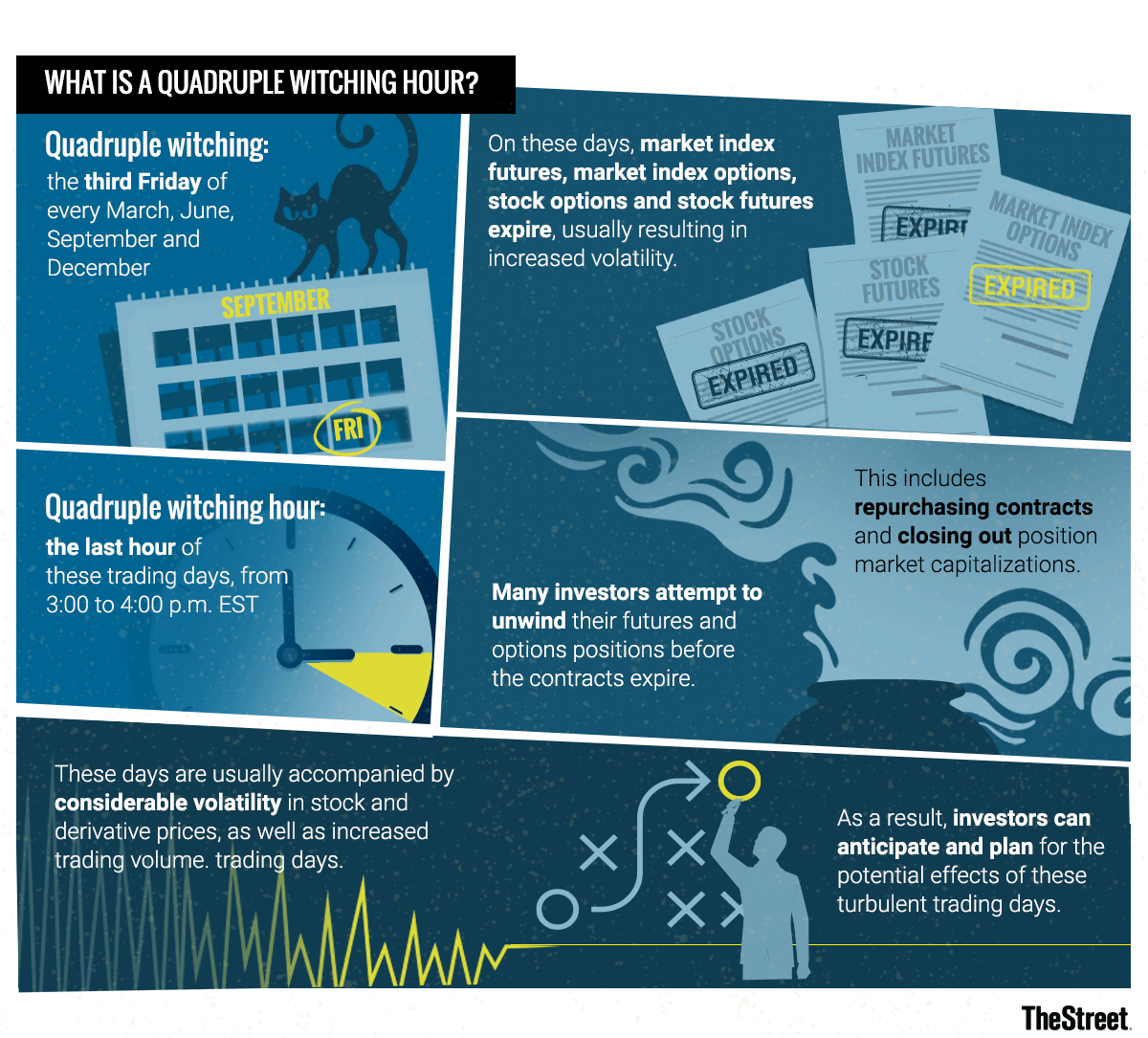

Markets: While yesterday was somewhat of a snoozefest on Wall Street, today should be more interesting. In a quarterly event known as “quadruple witching,” stock options, index options, stock futures, and index futures all expire on the same day, which can produce fireworks.

The phrase quadruple witching brings to mind stories that begin, “It was a dark and stormy night…” or folkloric visions of witches flying chaotically on broomsticks across the brightness of a moon.

In the context of investing, quadruple witching also refers to possible chaos but chaos in the financial markets. Such chaos can erupt due to four different types of contracts on financial assets expiring on the same day. The quadruple witching hour is the last hour of the trading session on that day. The question is whether investors can make abnormally robust profits on quadruple witching days due to market fluctuations.

What Is Quadruple Witching?

Quadruple witching refers to four days during the calendar year when the contracts on four different kinds of financial assets expire. The days are the third Friday of March, June, September and December. The assets on which the contracts expire on that day are stock options, single stock futures, stock index futures and stock index options. Options contracts also expire monthly. Futures contracts expire quarterly.

Because all four types of contracts expire on the same day, the quadruple witching day usually sees a heavier volume of trading. This is why the reference to chaos is made about this witching day. Market volume is increased partly due to offsetting trades that are made automatically. Volume on quadruple witching days has increased roughly two-thirds of the time since 2005.

Recent Quadruple Witching Expiration Day

On June 18, 2021, a quadruple witching day, a near-record volume of single-stock equity options was set to expire at the end of the day in the amount of $818 billion. As a result, a near-record of single stock open interest of about $3 trillion stood on June 18, 2021. Open interest refers to how many contracts are open during any given point during the day. It is an important metric for traders to watch since a large amount of open interest can move the value of the underlying stock.

Taking a distribution from a tax qualified retirement plan, such as a 401(k), prior to age 59 1/2 is generally subject to a 10 percent early withdrawal tax penalty.

However, the IRS rule of 55 may allow you to receive a distribution after attaining age 55 (and before age 59 1/2 ) without triggering the early penalty if your plan provides for such distributions.

The distribution would still be subject to an income tax withholding rate of 20 percent, however. (If it turns out that 20 percent is more than you owe based on your total taxable income, you will get a refund after filing your yearly tax return.)

There’s an aspect to retirement that many physicians do not plan for … the transition from work and practice to retirement. Your work has been an important part of your life. That’s why the emotional adjustments of retirement may be some of the most difficult ones.

For example, what would you like to do in retirement? Your retirement vision will be unique to you. You are retiring to something not from something that you envisioned. When you have more time, you would like to do more traveling, play golf or visit more often, family and friends. Would you relocate closer to your kids? Learn a new art or take a new class? Fund your grandchildren’s education? Do you have philanthropic goals? Perhaps you would like to help your church, school or favorite charity? If your net worth is above certain limits, it would be wise to take a serious look at these goals. With proper planning, there might be some tax benefits too. Then you have to figure how much each goal is going to cost you.

If have a list of retirement goals, you need to prioritize which goal is most important. You can rate them on a scale of 1 to 10; 10 being the most important. Then, you can differentiate between wants and needs. Needs are things that are absolutely necessary for you to retire; while wants are things that still allow retirement but would just be nice to have.

Recent studies indicate there are three phases in retirement, each with a different spending pattern [Richard Greenberg CFP®, Gardena CA, personal communication]. The three phases are:

The Early Retirement Years. There is a pent-up demand to take advantage of all the free time retirement affords. You can travel to exotic places, buy an RV and explore forty-nine states, go on month-long sailing vacations. It’s possible during these years that after-tax expenses increase during these initial years, especially if the mortgage hasn’t been paid off yet. Usually the early years last about ten years until most retirees are in their 70’s.

Middle Years. People decide to slow down on the exploration. This is when people start simplifying their life. They may sell their house and downsize to a condo or townhouse. They may relocate to an area they discovered during their travels, or to an area close to family and friends, to an area with a warm climate or to an area with low or no state taxes. People also do their most important estate planning during these years. They are concerned about leaving a legacy, taking care of their children and grandchildren and fulfilling charitable intent. This a time when people spend more time in the local area. They may start taking extension or college classes. They spend more time volunteering at various non-profits and helping out older and less healthy retirees. People often spend less during these years. This period starts when a retiree is in his or her mid to late 70’s and can last up to 20 years, usually to mid to late-80’s.

Late Years. This is when you may need assistance in our daily activities. You may receive care at home, in a nursing home or an assisted care facility. Most of the care options are very expensive. It’s possible that these years might be more expensive than your pre-retirement expenses. This is especially true if both spouses need some sort of assisted care. This period usually starts when the retiree is their 80’s; however they can sometimes start in the mid to late 70’s.

If early retirement is a major objective, start thinking about activities that will fill up your time during retirement. Maintaining your health is more critical, since your health habits at this time will often dictate how healthy you will be in retirement.

Planning Issues – Mid Career

If early retirement is a major objective, start thinking about activities that will fill up your time during retirement. Maintaining your health is more critical, since your health habits at this time will often dictate how healthy you will be in retirement

Planning Issues – Late Career

Three to five years before you retire, start making the transition from work to retirement.

Try out different hobbies;

Find activities that will give you a purpose in retirement;

Establish friendships outside of the office or hospital;

Discuss retirement plans with your spouse.

If you plan to relocate to a new place, it is important to rent a place in that area and stay for few months and see if you like it. Making a drastic change like relocating and then finding you don’t like the new town or state might be very costly mistake. The key is to gradually make the transition.

An IRA in which distributions continue after the primary beneficiary’s death.

For an IRA to be inherited, the primary beneficiary must have already been receiving the required minimum distribution; the distributions either continue or are re-calculated based upon the secondary beneficiary’s life expectancy.

If the secondary beneficiary is the widow(er) of the primary beneficiary, she/he may roll over the inherited IRA into her/his own IRA without penalty.

Posted on September 13, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

ABOUT NOSE SWAB KITS

***

BY. DR. DAVID EDWARD MARCINKO MBA

What is an at-home Covid test?

There are two types of tests for COVID-19. Viral tests tell you if you have a current infection, and antibody tests tell you if you’ve been previously infected.

If you’re experiencing symptoms or think you’ve been exposed to COVID-19, contact your health care provider or your state or local public health department to find out where you can get tested. Tests are available at many health centers and some pharmacies. Call in advance to see if an appointment is required. The testing process and timeline for results vary by location.

But – Rather than having a doctor or health professional get all up in your nostrils, you can swab yourself and get the results in less than an hour. At-home rapid tests (known as “antigen” tests) are less reliable than the lab-based PCR [polymerase chain reaction] test, but experts say they can be an extremely useful tool for allowing life to proceed semi-normally.

NOTE: PCR means polymerase chain reaction. It’s a test to detect genetic material from a specific organism, such as a virus. The test detects the presence of a virus if you have the virus at the time of the test. The test could also detect fragments of the virus even after you are no longer infected.

Problem is, in the US over-the-counter rapid tests are expensive and scarce.

Abbott Laboratories sells a two-pack for $24, and Quidel’s QuickVue sells a test for $15. But even if you are willing to shell out for one, good luck finding a rapid test on pharmacy store shelves or on e-commerce websites, where they’re often sold out.

The saver’s credit is a tax credit that’s intended to promote retirement savings among low- and moderate-income workers. It can reduce an eligible taxpayer’s federal income taxes when they save in a qualified retirement plan. It may be especially useful to medical students, nurses, interns, residents and fellows.

****

***

In 2021, the maximum credit is worth $1,000 for individuals and $2,000 for married couples filing jointly, although it phases out for higher earners. To qualify for the credit, individuals must have an adjusted gross income of $32,500 or less. The income threshold for married couples is $65,000.

Because the credit is non-refundable, eligible taxpayers are able to use it to effectively reduce their tax bill to zero – but it cannot provide them with a tax refund.

Current reimbursement structures involve the submission and payment of medical CPT® coded claims. But, some doctors feel they need to “up-code” to maximize revenue or “down-code” for fear of having a claim denied. Contradictory business goals bastardize the system into a payer versus provider tug-of-war, with patient care as a potential bargaining chip. Instituting quality metrics should be included in this equation and, a hybrid reimbursement model may be a viable option while integrating quality care metrics and reducing costs for all stakeholders.

This hybrid reimbursement system might use a two-payment structure.

For the first payment, claims would be paid at hypothetical rate of 60% within one week of submission.

The second payment, consisting of the remaining zero to 40% of some total maximum allowable fee, be paid quarterly. It would be based on scores like patient satisfaction and stewardship of healthcare resources by analyzing a statistically valid sample of patient encounters taken from the electronic health record.

Such a hybrid system would remove unnecessary steps, like re-submitting claims, and would lower the operational and administrative costs of claims processing. These changes would decrease operational cost and drive quality stewardship of the healthcare dollar.

Posted on September 8, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

QUICK DEFINITION – INVESTING BASICS

MUTUAL COMPANY: A company that has no capital stock or stockholders. Rather, it is owned by its policy-owners and managed by a board of directors chosen by the policy-owners.

Any earnings, in addition to those necessary for the operation of the company and contingency reserves, are returned to the policy-owners in the form of policy dividends.

STOCK COMPANY: A joint-stock company is a business entity in which shares of the company’s stock can be bought and sold by shareholders.

Each shareholder owns company stock in proportion, evidenced by their shares (certificates of ownership). Shareholders are able to transfer their shares to others without any effects to the continued existence of the company.

Posted on September 6, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

DOCTORS MUST KNOW THE DIFFERENCE

Dr. David Marcinko MBA CMP®

J. Christopher Miller; JD

HISTORY

Do you remember when Andy DuFresne confronts the chief guard of his prison in The Shawshank Redemption and tells him to divert an inherited sum of money into his wife’s name? Even sixty-five years after the 1949 setting of that conversation, a common means of protecting assets from the reach of creditors is to transfer property into a spouse’s name. Assuming that the spouse is not also at substantial risk of being the target of lawsuits because of the spouse’s profession or lifestyle, it is an effective means of accomplishing that goal. Creditors with valid judgments against an individual may only attach and seize those assets owned by that individual. Anything worth doing is worth doing right, however, and there are several pointers to structuring asset ownership in a way that maximizes its protective value.

STATES

A small number of states, such as Hawaii, Pennsylvania, and Florida, have statutes that automatically protect property jointly owned by spouses from creditors of either spouse, but often not from creditors of both spouses together. Property that benefits from this characterization is held in as a “tenancy by the entirety,” and prevents only one spouse from transferring away property that the married couple obtained together. Again, variation in state law determines just how beneficial the formation of a “tenancy by the entirety” can be from an asset protection standpoint. This protection comes from a public interest in the preservation of marital assets, such that one spouse’s indiscretion may not harm the position of the other spouse.

The most significant limits to the advantage provided by the tenancies of the entirety are first, that the creditors with claims against both spouses may seize such jointly held property, and second, that upon the first death between the spouses, the property flows directly to the surviving spouse alone, who then no longer has the benefit of the creditor protection. Moreover, in April of 2002, the U.S. Supreme Court sharply curtailed the benefit provided by tenancies by the entirety by ruling that it does not shield an asset from the federal authorities, even if the tax liability was incurred only by one spouse.[1]

Some states in the South and West are community property states, which is similar to, but not the same as, tenancy by the entirety. Under the community property theory, all property acquired by either spouse during the residency in that state (or in some states, prior to or during the residency), will be considered jointly owned property even if titled to an individual spouse. Merely by moving to one of these community property states, a person can automatically shift assets, thus reducing the quantity of assets subject to the creditors of the wealthier spouse.

PROPERTY

Community property and land owned as tenants-by-the-entirety is different from a third type of ownership called Joint Tenancy with Rights of Survivorship, sometimes abbreviated as “JTWROS”. Joint tenancy with rights of survivorship may ease some burdens associated with probating a decedent’s estate, but this form of ownership is not ideal when viewed through the asset protection prism.

An alternative is to hold assets in the name of one spouse or the other, or as “tenants-in-common.” Tenancy-in-common is best described as a situation in which each spouse owns a one-half undivided share in the property, but does not have the automatic right to full ownership at the death of the other spouse.

Three advantages flow from this form of ownership:

Neither spouse owns the property exclusively.

A creditor seizing the interest of one spouse would not have a valuable asset because it could not evict the remaining spouse, so creditors will attack these assets only as a last resort to satisfy their claims. However, a lien recorded against either fractional interest would have to be satisfied upon its sale, so that the net proceeds would be reduced by the amount of the lien. For this reason, tenancy-in-common is only a temporary means of protecting an asset from an adverse judgment, and not quite the same as fully separate ownership. This flaw is one reason why many estate planners recommend the funding of property into the name of a spouse or family member less vulnerable to adverse judgments.

If either spouse were to die, only half of the property would be subject to estate tax.

Ownership of property as tenants-in-common helps in the estate planning arena by facilitating the process of equalizing the assets held by each spouse. Changes made during 2010 and 2013 to the estate tax laws have pushed the federal estate tax exemption above $5 million, so fewer individuals (less than ½ of 1% of the general public by some estimates) will realize an actual tax savings from such planning. Even more appealing is that surviving spouses can now claim the unused exemption left behind by a deceased spouse. Estate tax concerns are now playing a much smaller role in recommending how spouses own their property.

A dying spouse has the ability to control how his or her interest is distributed.

In many simple Wills, all property of a spouse is given by bequest to the surviving spouse. Such a bequest could include partial ownership interests in real estate. If the surviving spouse is concerned about asset protection, this additional property would not be beneficial because it would easily be sacrificed to the survivor’s creditors. One way of avoiding this result is to build an estate plan in which each spouse bequests the partial interest owned by that spouse to a trust. At the first death between two spouses, the trust will hold the partial ownership interest for the benefit of the surviving spouse. The trust holding the partial residence interest preserves the deterrent faced by creditors of the surviving spouse because seizure of the surviving spouse’s interest would not terminate the spouse’s right to use the land provided for in the trust.

A different set of rules applies to property held jointly by medical professionals who are not married to each other. If property is owned jointly among siblings or business associates instead of a business entity, the owners should make sure that the deed names them as tenants-in-common. Otherwise, each successive death among the owners will shift the ownership to the survivors, and leave the family of the deceased owner with no lasting value from the owner’s investment into the property and its improvements.

LONG TERM

Assets should be held in a way that protects them from creditors for the long term. The form of asset holdings should thus be a significant part of the discussions held with professional advisors, so that the protection lasts beyond your death or that of your spouse. Structure the protected assets so that they do not flow back to you if your spouse should pass away. In this manner, integrated asset protection, estate planning, and financial planning unite to protect the family’s interests by extending the benefits of creditor protection for the long term.

ASSESSMENT: Your comments are appreciated.

****

[1] See United States v. Craft, 535 U.S. 274 (Apr. 17, 2002).

Use National Financial Awareness Day to your Advantage

Aug. 14th is National Financial Awareness Day. Financial awareness is about more than just understanding the basics on how money works. It’s also about evaluating your own budget, savings and investments to make sure your finances are working for your needs.

So if it’s been a while since your last financial “check up,” National Financial Awareness Day can be the extra push you’ve needed to finally take a look under the hood.

Posted on August 11, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

Review

This is a handy, word-packed reference book with health information technology terminology of the past, present, and future. The paperback book is small and compact in size but amazingly full of words, abbreviations, and even names of leaders in the health information technology industry. While any book like this will require updating on a periodic basis, many of the terms will remain relevant for a good period of time. I found the dictionary very useful and recommend it as a good addition to the reference shelf in the office or library.

—Doody’s Book Review

From the Back Cover

Over10,000 Detailed Entries!

“”There is a myth that all stakeholders in the healthcare space understand the meaning of basic information technology jargon. In truth, the vernacular of contemporary medical information systems is unique, and often misused or misunderstood? Moreover, an emerging national Heath Information Technology (HIT) architecture; in the guise of terms, definitions, acronyms, abbreviations and standards; often puts the non-expert medical, nursing, public policy administrator or paraprofessional in a position of maximum uncertainty and minimum productivity ?The Dictionary of Health Information Technology and Security will therefore help define, clarify and explain…You will refer to it daily.””

–– Richard J. Mata, MD, MS, MS-CIS, Certified Medical Planner? (Hon), Chief Medical Information Officer [CMIO], Ricktelmed Information Systems, Assistant Professor Texas State University, San Marcos

![DR. DAVID EDWARD MARCINKO FACFAS MBA CFP MBBS [Hon] [Executive Summary] - PDF Free Download](https://educationdocbox.com/docs-images/75/71938560/images/7-0.jpg)

/u-s-debt-ceiling-why-it-matters-past-crises-9ee4f4a3337c4203997fb191a9858b8c.gif)

:strip_icc():format(webp)/what-is-the-rule-of-55-2894280-v1-fa6b42c5a8f647e8aa5776a550c121a5-1fc39bd85b914af9b2682601f2cefdf6.png)