BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on November 4, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

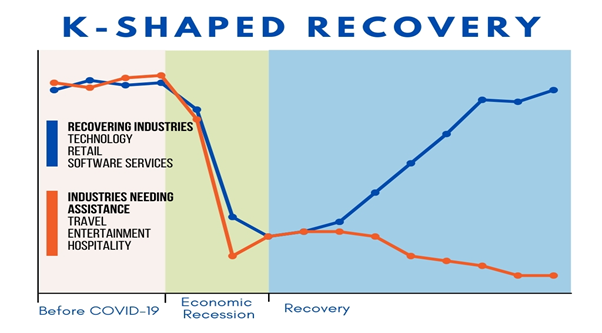

The term “K-shaped economy” emerged during the COVID-19 pandemic to describe a recovery marked by stark divergence—where some sectors and social groups rebound rapidly while others continue to decline. Unlike traditional V-shaped or U-shaped recoveries, which imply uniform economic improvement, the K-shaped model reflects a split trajectory: the upward arm of the “K” represents those who thrive, while the downward arm captures those left behind. This phenomenon has profound implications for economic policy, social equity, and long-term stability.

At the heart of the K-shaped economy is inequality. High-income individuals, white-collar professionals, and large corporations often benefit from technological advances, remote work flexibility, and access to capital. For example, tech giants like Apple, Microsoft, and Alphabet saw record profits during the pandemic, fueled by digital transformation and cloud services. Meanwhile, lower-income workers—especially in hospitality, retail, and service industries—faced job losses, reduced hours, and limited access to healthcare or financial safety nets. This divergence widened existing income and wealth gaps, exacerbating social tensions.

Sectoral performance also illustrates the K-shaped divide. Industries such as e-commerce, software, and logistics surged, while travel, entertainment, and small businesses struggled. The rise of automation and artificial intelligence further tilted the scales, favoring companies that could invest in innovation while displacing low-skilled labor. In education, students from affluent families adapted to online learning with ease, while those from disadvantaged backgrounds faced digital barriers and learning loss. These disparities underscore how economic recovery is not just uneven—it’s structurally imbalanced.

Geography plays a role too. Urban centers with diversified economies and strong tech sectors rebounded faster than rural or manufacturing-heavy regions. Housing markets in affluent areas soared, driven by low interest rates and remote work migration, while renters and first-time buyers faced affordability crises. Even within cities, neighborhoods with better infrastructure and public services recovered more quickly, deepening the urban-suburban divide.

Policymakers face a daunting challenge in addressing the K-shaped recovery. Traditional stimulus measures may not reach the most vulnerable populations without targeted interventions. Expanding access to education, healthcare, and digital infrastructure is essential to leveling the playing field. Progressive taxation, wage support, and small business aid can help bridge the gap, but require political will and fiscal discipline. Central banks must balance inflation control with inclusive growth, avoiding policies that disproportionately benefit asset holders.

The long-term consequences of a K-shaped economy are significant. Persistent inequality can erode trust in institutions, fuel populism, and hinder social mobility. Economic growth may slow if large segments of the population remain underemployed or financially insecure. To build a resilient and inclusive future, governments, businesses, and civil society must collaborate to ensure that recovery lifts all boats—not just the yachts.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 3, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

***

***

By Health Capital Consultants, LLC

On October 23, 2025, both Democratic and Republican lawmakers expressed support during a Senate Health, Education, Labor, and Pensions (HELP) Committee hearing for reforming the 340B Drug Discount Program. Although senators acknowledged that any reform would necessitate an intentional, considered approach to mitigate unintended consequences, the bipartisan agreement (particularly during a government shutdown deadlocked on healthcare) indicates that changes to the program may be on the horizon.

This Health Capital Topics article outlines the 340B program, discusses issues that have made the program controversial, and discusses potential reform options. (Read more…)

Product costing deals with determining the total costs involved in the production of a good or service. Costs may be broken down into subcategories, such as variable, fixed, direct, or indirect costs. Cost accounting is used to measure and identify those costs, in addition to assigning overhead to each type of product created by the company.

Managerial accountants calculate and allocate overhead charges to assess the full expense related to the production of a good. The overhead expenses may be allocated based on the number of goods produced or other activity drivers related to production, such as the square footage of the facility. In conjunction with overhead costs, managerial accountants use direct costs to properly value the cost of goods sold and inventory that may be in different stages of production.

Marginal costing (sometimes called cost-volume-profit analysis) is the impact on the cost of a product by adding one additional unit into production. It is useful for short-term economic decisions. The contribution margin of a specific product is its impact on the overall profit of the company. Margin analysis flows into break-even analysis, which involves calculating the contribution margin on the sales mix to determine the unit volume at which the business’s gross sales equals total expenses. Break-even point analysis is useful for determining price points for products and services.

Cash Flow Analysis

Managerial accountants perform cash flow analysis in order to determine the cash impact of business decisions. Most companies record their financial information on the accrual basis of accounting. Although accrual accounting provides a more accurate picture of a company’s true financial position, it also makes it harder to see the true cash impact of a single financial transaction. A managerial accountant may implement working capital management strategies in order to optimize cash flow and ensure the company has enough liquid assets to cover short-term obligations.

When a managerial accountant performs cash flow analysis, he will consider the cash inflow or outflow generated as a result of a specific business decision. For example, if a department manager is considering purchasing a company vehicle, he may have the option to either buy the vehicle outright or get a loan. A managerial accountant may run different scenarios by the department manager depicting the cash outlay required to purchase outright upfront versus the cash outlay over time with a loan at various interest rates.

Inventory Turnover Analysis

Inventory turnover is a calculation of how many times a company has sold and replaced inventory in a given time period. Calculating inventory turnover can help businesses make better decisions on pricing, manufacturing, marketing, and purchasing new inventory. A managerial accountant may identify the carrying cost of inventory, which is the amount of expense a company incurs to store unsold items.

If the company is carrying an excessive amount of inventory, there could be efficiency improvements made to reduce storage costs and free up cash flow for other business purposes.

Constraint Analysis

Managerial accounting also involves reviewing the constraints within a production line or sales process. Managerial accountants help determine where bottlenecks occur and calculate the impact of these constraints on revenue, profit, and cash flow. Managers then can use this information to implement changes and improve efficiencies in the production or sales process.

Financial Leverage Metrics

Financial leverage refers to a company’s use of borrowed capital in order to acquire assets and increase its return on investments. Through balance sheet analysis, managerial accountants can provide management with the tools they need to study the company’s debt and equity mix in order to put leverage to its most optimal use.

Performance measures such as return on equity, debt to equity, and return on invested capital help management identify key information about borrowed capital, prior to relaying these statistics to outside sources. It is important for management to review ratios and statistics regularly to be able to appropriately answer questions from its board of directors, investors, and creditors.

Accounts Receivable (AR) Management

Appropriately managing accounts receivable (AR) can have positive effects on a company’s bottom line. An accounts receivable aging report categorizes AR invoices by the length of time they have been outstanding. For example, an AR aging report may list all outstanding receivables less than 30 days, 30 to 60 days, 60 to 90 days, and 90+ days.

Through a review of outstanding receivables, managerial accountants can indicate to appropriate department managers if certain customers are becoming credit risks. If a customer routinely pays late, management may reconsider doing any future business on credit with that customer.

Budgeting, Trend Analysis, and Forecasting

Budgets are extensively used as a quantitative expression of the company’s plan of operation. Managerial accountants utilize performance reports to note deviations of actual results from budgets. The positive or negative deviations from a budget also referred to as budget-to-actual variances, are analyzed in order to make appropriate changes going forward.

Managerial accountants analyze and relay information related to capital expenditure decisions. This includes the use of standard capital budgeting metrics, such as net present value and internal rate of return, to assist decision-makers on whether to embark on capital-intensive projects or purchases. Managerial accounting involves examining proposals, deciding if the products or services are needed, and finding the appropriate way to finance the purchase. It also outlines payback periods so management is able to anticipate future economic benefits.

Managerial accounting also involves reviewing the trendline for certain expenses and investigating unusual variances or deviations. It is important to review this information regularly because expenses that vary considerably from what is typically expected are commonly questioned during external financial audits. This field of accounting also utilizes previous period information to calculate and project future financial information. This may include the use of historical pricing, sales volumes, geographical locations, customer tendencies, or financial information.

Posted on October 31, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

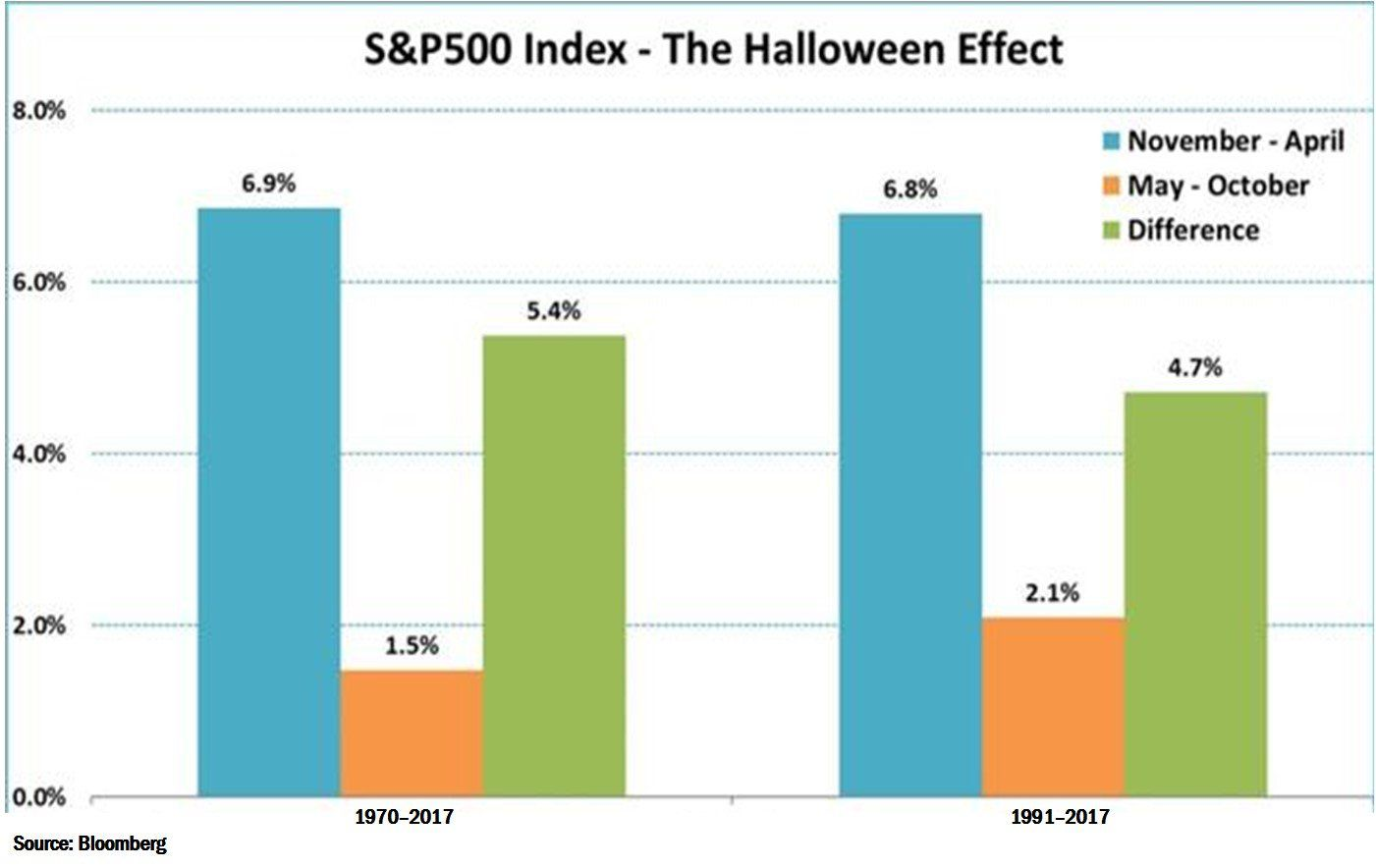

SELL IN MAY – AND GO AWAY

By Staff Reporters

***

***

Essentially, the HALLOWEEN INDICATOR is a market-timing strategy. It argues that, by buying into the stock market after Halloween and selling at the end of April, investors would generate a better annual return on their portfolio than if they had remained invested throughout the year. Sell in May and go away is an investment strategy for stocks based on a theory that the period from November to April inclusive has significantly stronger stock market growth on average than the other months

The practice of abandoning stocks beginning in May of each year is widely thought to have its origins in the United Kingdom. The privileged class would leave London and head to their country estates for the summer months, where they would largely ignore their investment portfolios. To this day, many stock market watchers have postulated that the corresponding impact of summer vacations on market liquidity and investors’ risk aversion is at least partly responsible for the difference in seasonal returns.

In what is considered to be a seminal piece of research on the subject, “The Halloween Indicator, ‘Sell in May and Go Away’: Another Puzzle,” authors Sven Bouman and Ben Jacobsen were among the first to document a strong seasonal effect in global stock markets. In 36 of the 37 developed and emerging markets they studied between 1973 and 1998, the authors found returns in the November through April period to be, on average, significantly higher than those in the May through October period, even after taking transaction costs into account. What puzzled the authors was the fact that, while the anomaly was widely known and seemed to offer considerable economic rewards, it had not been arbitraged away.

More recently, Jacobsen partnered with Cherry Zhang on a follow up study, titled, “The Halloween Indicator: Everywhere and All the Time,” and extended the research to 108 stock markets using all historical data available. The result was a sample of 55,425 monthly observations (including more than 300 years of UK data), which helped to rebut any criticisms of data mining and sample selection bias. The results were compelling, as the November through April “winter” period delivered returns that were, on average, 4.52% higher than the “summer” returns. The Halloween effect was evident in 81 out of 108 countries. The size of the Halloween effect varied across geographies. It was found to be stronger in developed and emerging markets than in frontier markets.

So, advice is subject to a fiduciary duty, while product sales (brokerage) activity is not. The ratio of fiduciary advice to brokerage sales is about 1:99. So, what does that tell you?

A Contentious and Complicated Issue

This issue is so contentious and complicated today that lawyers are needed to define each and every term, engagement, transaction, brokerage or advisory contract, etc. It is far too amazingly contorted and complicated for most; including me; and we have even discussed the industry machinations and political double-talk on this ME-P previously; from some vary sharp industry experts, too.

The “work-around” for these rules is industry “dual-registration”. Simply put, just get licensed to do both; as I did. Charge a commission when selling stuff and charge a fee for advice. And ideally, do both at the same time; while getting paid for both sides.

As a naïve luddite, I learned this little truism in financial planning school decades ago, and as a doctor and fiduciary for my patients at all times, almost vomited.

Of course, there were more sophisticated students in our classes who regurgitated the standard industry opinion: “We’ll give the client a financial plan for free IF we can sell commissioned products.”

Ideally this meant a fat and fully commissioned wrap account, whole-life insurance policy, LTCI policy; etc. Or, sell products and collect fat ongoing, and often unrecognizable AUM fees [fee-only], too!

From the stock broker-advisor’s POV, it was “Heads I win – tails you loose” for the client. Now, you know why I am a former or reformed certified financial planner.

The Physics Split

Know that as a pre-medical college student years earlier, I leaned about the Werner Heisenberg Uncertainty Principle, in physics class.

Of course, true Advice – is not Sales … and Sales is not Advice. Both should never be; simultaneously. So, let’s ditch dual registration and decide which to pursue … and then proceed accordingly. Both sales and advice have risks and benefits to client and producer; both have advantages and disadvantages to both; as well.

WHY? Just like the Werner Heisenberg Uncertainty Principle; it shouldn’t [shan’t] be both; at once.

NOTE: In quantum mechanics, the Heisenberg uncertainty principle is any of a variety of mathematical inequalities asserting a fundamental limit to the precision with which certain pairs of physical properties of a particle, known as complementary variables, such as position x and momentum p, can be known simultaneously.

So, in physics, I can tell you where you are -OR- how fast you are going; but not both. Thus, if it is product sales; it is not advice.

Today, since “dual registration” is still allowed, my suggestion to clients is to seek a fiduciary in all matters 24/7/354; get it in writing, and try to avoid arbitration and “best interest” or BICE clauses! Run from [fee-based and fee-only] AUM fees, too.

PS: I am not against Series #7 representatives and product sales. Salesmen/women often provide a valuable service and should be appropriately compensated. I only object when fees, costs, charges and commissions are duplicative, excessive and/or not fully disclosed to the client. Since excessive is an arbitrary term; full disclosure is the key ingredient.

Assessment

So – How am I wrong, mistaken and/or what did I miss? Do tell! Should We – Can We – Ditch Dual Registration [DDR]?

Oh! In the future, I also hope that State fiduciary standards will potentially cover both non-ERISA and ERISA situations, and employee plan participants will have access to full discovery rights, the one thing the industry fears most.

But, that’s a discussion for another day and time.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. https://medicalexecutivepost.com/dr-david-marcinkos-bookings/

Doctorate, or doctoral, is an umbrella term for many degrees — PhD among them — at the height of the academic ladder. Doctorate degrees fall under two categories, and here is where the confusion often lies.

The first category, Research (also referred to as Academic) includes, among others:

Doctor of Philosophy (PhD)

Doctor of Business Administration (DBA)

Doctor of Education (EdD)

Doctor of Theology (ThD)

The second category, Applied (also referred to as Professional) includes, among others:

Doctor of Medicine (MD)

Doctor of Podiatric Medicine (DPM)

Doctor Of Osteopathic Medicine (DO)

Doctor of Dental Surgery (DDS)

Doctor of Optometry (OD)

Doctor of Psychology (PsyD)

Juris Doctor (JD)

As you can see, applied doctorates are generally paired with very specific careers – medical doctors, podiatrists, dentists, optometrists, psychologists, and law professionals.

When it comes to outlining the differences between a PhD and doctorate, the real question should be, “What is the difference between a PhD and an applied doctorate?” The answer, again, can be found in the program outcomes. The online Doctor of Psychology at UAGC, for example, lists outcomes that are heavily focused on the ability to put theory into practice in a professional setting. For example:

Apply best practices in the field regarding professional values, ethics, attitudes, and behaviors

Exhibit culturally diverse standards in working professionally with individuals, groups, and communities who represent various cultural and personal backgrounds

Utilize a comprehensive psychology knowledge base grounded in theoretical models, evidence-based methods, and research in the discipline

Integrate leadership skills appropriate in the field of psychology

Critically evaluate applied psychology research methods, trends, and concepts

Bottom line: As the PhD is more academic, research-focused, and heavy on theory, an applied doctorate degree is intended to master a subject in both theory and practice.

Can a PhD Be Called a Doctor?

The debate over whether a PhD graduate should be called a doctor has existed for decades, and if you’re a member of this exclusive club, you’ll no doubt hear both sides of the argument during your lifetime. After all, if a PhD is a doctor, can a person with a doctoral degree in music – the Doctor of Musical Arts (DMA) – be called a doctor as well?

Those in favor argue that having “Dr.” attached to your name indicates that you are an expert and should be held in higher regard. For some, the debate is at the heart of modern gender disparity. For example, on social media and in some academic circles, there is an argument that female PhD holders should use the “Dr.” title in order to reject the notion that women are less worthy of adding the title to their name once they have earned a doctoral degree.

Posted on October 17, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

A paradox is a logically self-contradictory statement or a statement that runs contrary to one’s expectation. It is a statement that, despite apparently valid reasoning from true or apparently true premises, leads to a seemingly self-contradictory or a logically unacceptable conclusion. A paradox usually involves contradictory-yet-interrelated elements that exist simultaneously and persist over time. They result in “persistent contradiction between interdependent elements” leading to a lasting “unity of opposites”.

THE TELE-MEDICINE PARADOX

Classic Definition: Refers specifically to the treatment of various medical conditions without seeing the patient in person. Healthcare providers may use electronic and internet platforms like live video, audio, PCs, tablets, or instant messaging to address a patient’s concerns and diagnose their condition remotely.

Modern Circumstance: This may include giving medical advice, walking them through at-home exercises, or recommending them to a local provider or facility. Even more exciting is the emergence of telemedicine apps which give patients access to care right from their phones or computer screens.

Paradox Examples: Treating certain conditions remotely can be challenging. Tele-medicine is often used to treat common illnesses, manage chronic conditions, or provide specialist services. If a patient is dealing with an emergent or serious condition, the remote provider suggests they seek in-person medical care.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Investment fees still matter for physicians and all of us, despite dropping dramatically over the past several decades due to computer automation, algorithms and artificial intelligence, etc. And, they can make a big difference to your financial health. So, before buying any investment thru a financial advisor, planner, manager, stock broker, etc., it’s vital to understand these two often confusing costs.

***

***

Fee Only: Paid directly by clients for their services and can’t receive other sources of compensation, such as payments from fund providers. Act as a fiduciary, meaning they are obligated to put their clients’ interests first

Fee Based: Paid by clients but also via other sources, such as commissions from financial products that clients purchase. Brokers and dealers (registered representatives) are simply required to sell products that are “suitable” for their clients. Not a fiduciary.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Posted on October 11, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

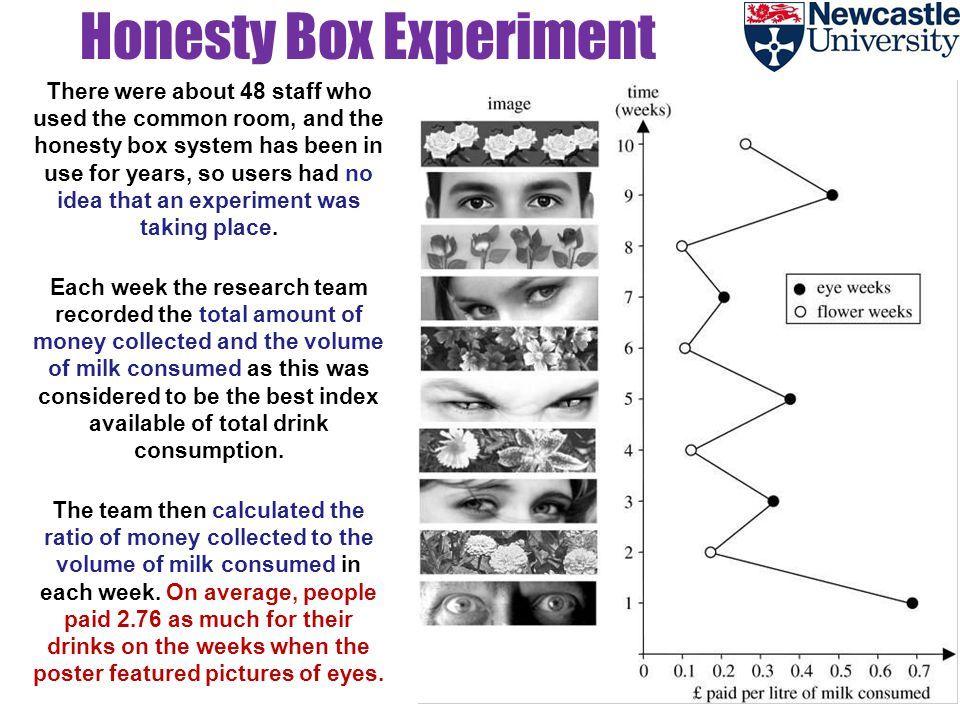

“BIG BROTHER” IS WATCHING

[From the Newcastle Division of Psychology]

By Dr. David Edward Marcinko MBA

***

It’s no surprise that people are more honest when they know that they’re being watched. But what about just reminding them of the idea of being watched, without them actually being watched?

For years, people at the University of Newcastle’s Division of Psychology have an honor (or trust) system where they are requested to deposit payment for coffee in an “honesty box.” There was a note saying how much they should pay.

In 2006, Melissa Bateson and colleagues decided to do a little experiment: they placed an image above the note. They alternate between two pictures: one week they would use a picture of eyes and the other week, flowers.

After 10 weeks, they plotted the amount of money received versus drinks consumed and found that people paid nearly three times as much for their drinks when eyes were displayed!

The Dow Jones Industrial Average (DJIA), often referred to simply as “the Dow,” is one of the oldest and most well-known stock market indices in the world. It was created in 1896 by Charles Dow, the co-founder of The Wall Street Journal, and is designed to represent the performance of the broader U.S. stock market, specifically focusing on 30 large, publicly traded companies. These companies are considered leaders in their respective industries and serve as a barometer for the overall health of the U.S. economy.

The Composition of the DJIA

The DJIA includes 30 companies, which are selected by the editors of The Wall Street Journal based on various factors such as market influence, reputation, and the stability of the company. These companies represent a wide array of sectors, including technology, finance, healthcare, consumer goods, and energy. Notably, the companies chosen for the DJIA are not necessarily the largest companies in the U.S. by market capitalization, but rather those that are most indicative of the broader economy. Some of the prominent companies listed in the DJIA include names like Apple, Microsoft, Coca-Cola, and Johnson & Johnson.

However, the list of 30 companies is not static. Over time, companies may be added or removed to reflect changes in the economic landscape. For example, if a company experiences significant decline or no longer represents a leading sector, it might be replaced with another company that better reflects modern economic trends. This periodic reshuffling ensures that the DJIA continues to be a relevant measure of economic activity.

How the DJIA is Calculated

The DJIA is a price-weighted index, which means that the value of the index is determined by the share price of the component companies, rather than their market capitalization. To calculate the DJIA, the sum of the stock prices of all 30 companies is divided by a special divisor. This divisor adjusts for stock splits, dividends, and other corporate actions to maintain the integrity of the index over time. The price-weighted method means that higher-priced stocks have a greater impact on the movement of the index, regardless of the overall size or economic weight of the company.

For instance, if a company with a higher stock price like Apple experiences a significant change in value, it will influence the DJIA more than a company with a lower stock price, even if the latter has a larger market capitalization. This makes the DJIA somewhat different from other indices, like the S&P 500, which is weighted by market cap and gives more weight to larger companies in terms of their economic impact.

Significance of the DJIA

The DJIA is widely regarded as a barometer of the U.S. stock market’s performance. Investors and analysts closely monitor the movements of the Dow to gauge the overall health of the economy. When the DJIA rises, it generally suggests that investors are optimistic about the economic outlook and that large companies are performing well. Conversely, when the DJIA falls, it often signals economic uncertainty or a downturn in market conditions.

Despite being a narrow index, with only 30 companies, the DJIA holds substantial sway in financial markets. It is widely covered in the media and is often cited in discussions about the state of the economy. In fact, the performance of the DJIA is considered a key indicator of investor sentiment and economic confidence.

However, the DJIA has its limitations. Since it only includes 30 companies, it does not necessarily represent the broader market or capture the performance of smaller companies. Other indices, like the S&P 500, which includes 500 companies, offer a more comprehensive view of the market’s performance.

Conclusion

The Dow Jones Industrial Average is a key metric for understanding the state of the U.S. economy and the stock market. Although it has evolved over the years, it continues to provide valuable insights into the performance of large, influential companies. While it is not a perfect reflection of the market as a whole, the DJIA remains one of the most important and widely recognized indices in global finance. Through its historical significance and its role in shaping market sentiment, the Dow has cemented its place as a cornerstone of financial analysis.

Posted on October 9, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Co-Pilot

***

***

Artificial Intelligence in Finance: Revolutionizing the Industry

Artificial Intelligence (AI) is rapidly transforming the financial services industry, reshaping how institutions operate, manage risk, and serve customers. By leveraging machine learning, natural language processing, and predictive analytics, AI is enabling smarter decision-making, greater efficiency, and enhanced customer experiences across banking, investing, insurance, and regulatory compliance.

One of the most impactful applications of AI in finance is in fraud detection and prevention. Traditional systems rely on rule-based algorithms that often fail to catch sophisticated schemes. AI, however, can analyze vast amounts of transaction data in real time, identifying patterns and anomalies that signal fraudulent behavior. Machine learning models continuously improve as they process more data, making them increasingly effective at detecting threats and reducing false positives.

AI also plays a pivotal role in algorithmic trading, where decisions are made at lightning speed based on complex data inputs. These systems can process news articles, social media sentiment, and market data to execute trades with precision. Hedge funds and investment banks use AI to optimize portfolios, forecast market trends, and identify arbitrage opportunities that human analysts might miss.

In personal finance and banking, AI enhances customer service through chatbots and virtual assistants. These tools handle routine inquiries, assist with transactions, and offer financial advice based on user behavior. AI-driven platforms like robo-advisors provide personalized investment strategies, adjusting portfolios automatically based on market conditions and individual goals. This democratizes access to financial planning, making it more affordable and scalable.

Credit scoring and lending have also been revolutionized by AI. Traditional credit models often rely on limited data and can be biased against certain demographics. AI can incorporate alternative data sources—such as utility payments, social media activity, and online behavior—to assess creditworthiness more accurately and inclusively. This opens up lending opportunities for underserved populations and reduces default risk for lenders.

In insurance, AI streamlines underwriting and claims processing. By analyzing historical data and customer profiles, AI can assess risk more precisely and tailor policies to individual needs. During claims, AI can automate document review, detect fraud, and expedite payouts, improving both operational efficiency and customer satisfaction.

Regulatory compliance, or RegTech, is another area where AI shines. Financial institutions face increasing scrutiny and complex regulations. AI tools can monitor transactions, flag suspicious activity, and ensure adherence to legal standards. Natural language processing helps parse regulatory documents and automate reporting, reducing the burden on compliance teams.

Despite its benefits, AI in finance raises ethical and operational challenges. Data privacy, algorithmic bias, and transparency are critical concerns. Financial institutions must ensure that AI systems are explainable, fair, and secure. Regulatory bodies are beginning to address these issues, but ongoing collaboration between technologists, policymakers, and industry leaders is essential.

In conclusion, artificial intelligence is not just enhancing finance—it’s redefining it. From fraud prevention to personalized banking, AI is driving innovation and efficiency. As the technology matures, its integration must be guided by ethical principles and robust governance to ensure that the financial system remains fair, resilient, and inclusive.

Artificial Intelligence and Investing: A Transformative Partnership

Artificial Intelligence (AI) is revolutionizing the world of investing, reshaping how decisions are made, risks are assessed, and portfolios are managed. As financial markets grow increasingly complex and data-driven, AI offers powerful tools to navigate this landscape with greater precision, speed, and insight.

At its core, AI refers to systems that can perform tasks typically requiring human intelligence—such as learning, reasoning, and problem-solving. In investing, this translates into algorithms that can analyze vast amounts of financial data, detect patterns, and make predictions with remarkable accuracy. Machine learning, a subset of AI, enables these systems to improve over time by learning from new data, making them especially valuable in dynamic markets.

One of the most significant applications of AI in investing is algorithmic trading. These systems can execute trades at lightning speed, responding to market fluctuations in milliseconds. By analyzing historical data and real-time market conditions, AI-driven trading platforms can identify optimal entry and exit points, often outperforming human traders. High-frequency trading firms have long relied on such technologies to gain competitive advantages.

AI also enhances portfolio management through robo-advisors—digital platforms that use algorithms to provide personalized investment advice. These tools assess an investor’s goals, risk tolerance, and time horizon, then construct and manage a diversified portfolio accordingly. Robo-advisors democratize access to financial planning, offering low-cost, automated solutions to individuals who might not afford traditional advisory services.

Risk assessment is another area where AI shines. By processing alternative data sources—such as social media sentiment, news articles, and satellite imagery—AI can uncover hidden risks and opportunities. For instance, a sudden spike in negative sentiment around a company on Twitter might signal reputational issues, prompting investors to reevaluate their positions. AI models can also forecast macroeconomic trends, helping investors anticipate shifts in interest rates, inflation, or geopolitical events.

Moreover, AI is transforming fundamental analysis. Natural language processing (NLP) allows machines to read and interpret earnings reports, SEC filings, and analyst commentary. This enables investors to extract insights from unstructured data that would be time-consuming to analyze manually. AI can even detect subtle linguistic cues that may indicate a company’s future performance or management’s confidence.

Despite its advantages, AI in investing is not without challenges. Models can be opaque, making it difficult to understand how decisions are made—a phenomenon known as the “black box” problem. There’s also the risk of overfitting, where algorithms perform well on historical data but fail in real-world scenarios. Ethical concerns, such as bias in data and the potential for market manipulation, must also be addressed.

In conclusion, AI is reshaping the investing landscape, offering tools that enhance efficiency, accuracy, and accessibility. While it’s not a panacea, its integration into financial markets marks a profound shift in how capital is allocated and wealth is managed. As technology continues to evolve, investors who embrace AI will be better positioned to thrive in an increasingly data-driven world.

Posted on October 4, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

On September 5, 2025, the Federal Trade Commission (FTC) voted to dismiss its appeals in two court cases, effectively terminating the Biden Administration’s pursuit of a comprehensive noncompete ban. The 3-1 Commission vote represents a fundamental shift in federal competition enforcement strategy.

This Health Capital Topics article reviews the history of the noncompete ban, the FTC’s recent activities regarding competition, and the implications for healthcare organizations. (Read more…)

Yourmedical practice. Your personal goals. Your financial plan. Our experienced confirmation guide.

***

***

When you know exactly where you are today, have a vision of where you want to be tomorrow, and have trusted counsel at your side, you have already achieved so much success. Marcinko Associates works to keep you at that level of confidence every day. We use a comprehensive economic process to uncover what’s most important to you and then develop a financial strategy that gives you the highest probability of achieving your monetary goals.

We assess, plan, and opine for your success

To accurately see where you are today, chart a strategic path to your goals and help you make the most informed decisions to keep you on financial track, our key services for physicians and high net worth medical clients include:

Investment Portfolio Review

Fee, Charge and Cost Review

Comprehensive Financial Planning

Insurance Reviews

Estate Planning

Investment and Asset Management Second Opinions

We take a deep dive into your financial retirement plans

Physicians and dental employers now have options for how to design and deliver retirement benefits and we can help you make the best choice for your healthcare business. Our services for retirement plans include:

Fee, Charges & Fiduciary Review

Portfolio Analysis

Single Employer Retirement Plan Advisory

Retirement Plans Risk Analysis

Capital Funding and Financing

Business Planning and Practice Valuations

Career Development

and more!

We take a broad and balanced look at your financial life life

We coordinate our recommendations with your other advisors, including attorneys, accountants, insurance professionals and others, to ensure each decision is consistent with your goals and overall strategy. For example, through our partnerships we offer physician colleagues deeper expanded advisory services, like:

In the case of financial investments, compounding interest relies on time to reveal its true magic.

Here’s how: a young investor can invest less money over a longer period of time than an older investor who invests more money over a shorter period and ends up with more in the end. Compounding returns grow exponentially, making time more than an ally – but a force of the universe driving growth.

Time is certainly our ally in investing, but according to ME-P Editor Dr. David Edward Marcinko MBA MEd, you’ll kick yourself wishing you had invested earlier when you witness compounding after a few years (or a decade).

Posted on September 18, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Carol Miller RN MBA

***

***

New-Wave Technology

To help hospitals and health systems comply with Health Insurance Portability and Accountability Act regulations, best practices are emerging for securing all electronic communication – cloud, wireless, and texting – of protected health information. These new technologies will continually be evolving with hospitals, providers and patients move to new means of communication. Below is a description of how each are impacted by HIPAA.

Cloud Solutions. Cloud solutions are becoming a needed commodity in treating patients today but also present a risk to privacy and security violation. Despite the advantages of cloud computing, organizations are often hesitant to use it because of concerns about security and compliance. Specifically, they fear potential unauthorized access to patient data and the accompanying liability and reputation damage resulting from the need to report HIPAA breaches. While these concerns are understandable, a review of data on HIPAA breaches published by the HHS shows that these concerns are misplaced. In fact, by using a cloud-based service with an appropriate security and compliance infrastructure, a facility can significantly reduce its compliance risk.

Because HIPAA compliance involves stringent privacy and security protections for electronic health information (PHI), many cloud providers are balking at signing new Business-Associate agreements. Most cloud-technology providers, such as Box and Dropbox, do not include the built-in privacy protections that guarantee HIPAA compliance. Because many cloud storage companies store plaintext data on their servers, PHI is especially vulnerable to breaches and compliance violations.

Mobility Solutions. The recent launches of Apple Health and Google Fit have stirred a lot of interest in health application development. It is important that hospitals and providers understand the laws around PHI and HIPAA compliance for any healthcare-focused mobile application or software. While not all healthcare applications fall under HIPAA rules, those that collect, store, or share personally identifiable health information with covered entities (such as hospitals and providers) must be HIPAA-compliant.

For years, hospitals have wanted to bring computers into exam rooms, waiting rooms, and treatment rooms to eliminate hard-to-read patient charts, making sure everyone treating the patient was seeing the same information, assuring that everything was recorded as it occurred, and enabling doctors, nurses, and technicians to stay connected to vital information and services wherever they were throughout the hospital. Many hospitals have adopted Computer on Wheels (COWs) or tablets but many of these were hard to use, had poor touchscreen interface and did not last long on a battery. Ipads seem to be the logical replacement as long as the iPad can comply with HIPAA rules.

HIPAA was written nearly 30 years ago, before mobile health applications were ever envisioned. Because of this, some areas of the law make it hard to determine which applications must be HIPAA- compliant and which are exempt. Considering the numerous ways security breaches can occur with a mobile device, it is not wonder that HHS is very leery about how PHI is handled on smartphones, wearables, and portable devices.

If the applications are going to send or share health data to a hospital, doctor or other covered entity, it MUST be HIPAA-compliant. Adhering to the Privacy and Security Rules of HIPAA is essential, especially considering the dangers that come with handling protected health data on a device. Examples include:

Phones, tablets, and wearables can be easily stolen and lost, meaning PHI could be compromised

Social media and email are easily accessible by the device, making it easy for users to post information that breaches HIPAA privacy laws.

Push notifications and other user communications can violate HIPAA laws if they contain PHI

Users may intentionally or unintentionally share personally identifiable information, even if the application’s intended use doesn’t account for it

Not all users take advanage of the password-protected screen-lock feature, making data visible and accessible to anyone who comes in contact with the device

Devices like the iPhone do not include physical keyboards, so users are more likely to use basic passwords that are not as safe as complex options.

This protected health information can include everything from medical records and images to scheduled appointment dates. Regardless of the device, it is important to take all the steps possible to comply with HIPAA guidelines.

Texting. Text (or SMS) messaging has become nearly ubiquitous on mobile devices. According to one survey, approximately 72 percent of mobile phone users send text messages. Clinical care is not immune from the trend, and in fact physicians appear to be embracing texting on par with the general population. Another survey found that 73 percent of physicians text other physicians about work.

(Source: Journal of AHIMA, “HIPAA Compliance for Clinician Texting”, by Adam Green, April 2012)

Texting can offer providers numerous advantages for clinical care. It may be the fastest and most efficient means of sending information in a given situation, especially with factors such as background noise, spotty wireless network coverage, lack of access to a desktop or laptop, and a flood of e-mails clogging inboxes. Further, texting is device neutral—it will work on personal or provider-supplied devices of all shapes and sizes. Because of these advantages, physicians may utilize texting to communicate clinical information, whether authorized to do so or not.

All forms of communication involve some level of risk. Text messaging merely represents a different set of risks that, like other communication technologies, needs to be managed appropriately to ensure both privacy and security of the information exchanged.

Text messages may reside on a mobile device indefinitely, where the information can be exposed to unauthorized third parties due to theft, loss, or recycling of the device. Text messages often can be accessed without any level of authentication, meaning that anyone who has access to the mobile phone may have access to all text messages on the device without the need to enter a password.

Texts also are generally not subject to central monitoring by the IT department. Although text messages communicated wirelessly are usually encrypted by the carrier, interception and decryption of such messages can be done with inexpensive equipment and freely available software (although a substantial level of sophistication is needed. If text messages are used to make decisions about patient care, then they may be subject to the rights of access and amendment. There is a risk of noncompliance with the privacy rule if the covered entity cannot provide patients with access to or amend such text messages.

According to 2012 data from CTIA–The Wireless Association, U.S. citizens alone exchange nearly 200 billion text messages every month. So it’s not surprising that an increasing number of clinicians are using text messaging to exchange clinical information, along with a wide range of other modes — smartphones, pagers, computerized physician order entry, emails, etc. Electronic communication is certainly faster, can be more efficient, enhances clinical collaboration and enables clinicians to focus on patient care. But with these benefits comes an increased risk of security breaches.

(Source: Clarifying the Confusion about HIPAA – Compliant Texting, by Megan Hardiman and Terry Edwards, May 2013)

Unfortunately, vendor hype about the Health Insurance Portability and Accountability Act is causing many hospitals and health systems to implement stop-gap measures that address part — but not all — of a problem. To identify all vulnerabilities, health care leaders need to consider not only text messaging, but all mechanisms by which protected health information in electronic form is transmitted — as well as the security of those mechanisms.

Mobile device-to-mobile device SMS text messages are generally not secure because they lack encryption. The sender does not know with certainty that his or her message is indeed received by the intended recipient. In addition, telecommunications vendor/wireless carrier may store the text messages. Recent HHS guidance indicates text messaging, as a means of communicating PHI, can be permissible under HIPAA depending in large part on the adequacy of the controls used. A hospital or provider may be approved for texting after performing a risk analysis or implementing a third-party messaging solution that incorporates measures to establish a secure communication platform that will allow texting on approved mobile devices.

A study reported in Computer World in May 2013 by the Ponemon Institute with 577 healthcare and It professional in facilities that ranged from fewer than 100 beds to over 500 beds stated that fifty-one percent of the respondents felt HIPAA compliance requirements can be a barrier to providing effective patient care. Specifically HIPAA reduces time available for patient care (85% of the respondents), makes access to electronic patient information difficult (79% of the respondents) and restricts the use of electronic mobile communications (56% of the respondents). The study stated “respondents agreed that the deficient communications tools currently in use decrease productivity and limit the time doctors have to spend with patients. “ They also stated “they recognized the value of implementing smartphones, text messaging and other modern forms of communications, but cited overly restrictive security policies as a primary reason why these technologies were not used.” Clinicians in the survey stated that only 45% of each workday is spent with patients; the remaining 55% is spent communicating and collaborating with other clinicians and using the electronic medical record and other clinical IT systems.

Several other statements made were:

Because of the need for security, hospitals and other healthcare organizations continue to use older, outdate technology such as pagers, email and facsimile machines. The use of older technology can also delay patient discharges – now taking an average of 102 minutes.

The Ponemon Institute estimated that the lengthy discharge process costs the U.S. hospital industry more than $3.189 billion a year in lost revenue, with another $5 billion lost through decrease doctor productivity and use of outdated technology. Secure text messaging could cut discharge time by 50 minutes.

(Source: Computer World, “HIPAA rules, outdate tech cost U.S. hospitals $3.38 B a year”, by Lucas Mearian, May, 2013)

Several suggestions offered for these preferred mobile devises are: 1) ensure encryption and access to individuals who need to have access; 2) use secure texting applications; and 3) even consider alerting employees with warnings before they send an email or share files that lets them know they are liable for the information sent.

Although 97% of people aren’t yet millionaires, many could eventually meet that target if they start investing sooner rather than later; especially doctors [MD, DO, DPM, DDS or DMD].

A 20-year-old, for instance, needs to invest just $330 a month into an asset class that delivers a 7% to 8% annual return to reach $1.26 million by the time s/he turns 65 years old. The luxury of time significantly boosts your chances of becoming a millionaire.

This doesn’t mean it’s too late for middle-aged savers to reach that millionaire milestone, but it will take a significantly greater investment. If a 50-year-old doctor hasn’t started saving for retirement, s/he would need to invest $3,958 a month at a steady 7% return to reach $1.26 million by retirement.

However, according to one Goldman Sachs report, investors could expect the S&P 500 to deliver just 3% annualized nominal returns over the next 10 years.

After an average 13% yearly return for the past decade, a new strategy outside of the stock market may be needed for that level of outsized gain, especially if you’re late to investing.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

According to Hello Divorce, alimony, often referred to as spousal support, is a court-ordered payment from one spouse to the other following a divorce or legal separation. Its existence is tied to the legal status of marriage. The underlying principle is that both spouses contributed to the marital standard of living, and the dissolution of the marriage should not cause an inequitable economic outcome for the lower-earning spouse. This support is not intended as a punishment but as a means of mitigating the financial impact of divorce.

The purpose of alimony can vary. In some cases, it is rehabilitative, providing temporary support while one spouse obtains education or job training to become self-sufficient. For longer marriages, it might serve to help maintain the standard of living established during the partnership. Alimony is a legal tool derived from family law statutes to address the financial interdependence created by marriage.

Note: The federal tax treatment for alimony changed with the Tax Cuts and Jobs Act of 2017. For any divorce or separation agreement executed after December 31st, 2018, alimony payments are no longer tax-deductible for the person paying them. The recipient of the support does not report the payments as taxable income. This change is permanent and does not expire with other provisions of the act.

What is Palimony

According to Wikipedia, Palimony refers to financial support that may be awarded after an unmarried couple separates. Unlike alimony, palimony is not rooted in family law but is a concept derived from contract law. An award depends on the existence of an agreement between the partners. This agreement can be a formal written contract or an oral or implied agreement for support in exchange for services, such as managing the household.

The legal basis for palimony was established by the 1976 California Supreme Court case, Marvin v. Marvin. In that case, the court ruled that unmarried cohabitants could make enforceable contracts for support, as long as the agreement was not based on sexual services. Because it is a contract claim, a palimony case is pursued in civil court, not family court. Palimony is not available in all states and is only recognized in a minority of jurisdictions.

Note: The tax implications of palimony are less defined than alimony because the IRS does not have a specific rule for it. How palimony is treated depends on the nature of the underlying claim. If the payments are a settlement for services rendered, they may be considered taxable income to the recipient. If the payments are characterized as a gift, they are not considered taxable income for the recipient.

Posted on September 1, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

Dear Medical Executive-Post Readers and Subscribers

***

HISTORY OF LABOR DAY

The first Labor Day holiday was celebrated on Sept. 5th, 1882, in New York City, in accordance with the plans of the Central Labor Union. President Grover Cleveland signed a law on June 28th, 1894, that made the first Monday in September of each year a national holiday, according to the Department of Labor.

***

***

MY SEPTEMBER HEALTH RE-SET

To give my health a boost after Labor Day, I’m taking a complete break from alcohol, sugar, cookies, ice cream, coffee and tea for the entire month of September. Besides that, I’ll also prioritize sleep and increase my exercise from 7 to at least 10 times [hours] a week. This will allow me to focus on my diet and mental well-being. It’s essentially a month of health and wellness rejuvenation.

I’ve chosen to focus on alcohol and sugar because I want to challenge the idea that moderate drinking is part of a healthy lifestyle. In reality, only those who maintain a healthy lifestyle can afford to enjoy alcohol in moderation. But, sugar is everywhere and must be minimized for Type II diabetes and weight control.

Moreover, the long-term and excessive intake of sugary beverages and refined sugars can negatively impact your overall caloric intake and create a domino effect on your health. For example, excess sugar in the body can turn into fat deposits and lead to fatty liver disease.

A low sugar diet can help you lose weight and also help you manage and/or prevent diabetes, heart disease and stroke, reduce inflammation, and even improve your mood and the health of your skin. That’s why the low sugar approach is a key tenet of other well-known healthy eating patterns, such as the Mediterranean diet and the DASH diet.

QUESTION: And so, do you also commit to such “factory resets” now and then? Please comments.

Do, enjoy the Labor Day Weekend, Bar-B-Ques with friends, family and colleagues. And, I hope you continue to find the Medical Executive-Post useful!

Many thanks for your likes and referrals. Dr. David Edward Marcinko MBA MEd CMP [Editor and Chief]

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on August 28, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL PROVIDER PAYMENTS LOWERED

***

***

Statistic: $2.8+ billion dollars

That’s how much Blue Cross and Blue Shield plans agreed to pay to settle litigation over claims they conspired to lower payments to providers. (Healthcare Dive)

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

A SPECIAL MEDICAL-EXECUTIVE-POST GUEST PRESENTATION

***

What Is a Special Purpose Vehicle (SPV)?

A special purpose vehicle is a subsidiary created by a parent company to isolate financial risk. It’s also called a special purpose entity (SPE). Its legal status as a separate company makes its obligations secure even if the parent company goes bankrupt. A special purpose vehicle is sometimes referred to as a bankruptcy-remote entity for this reason.

These vehicles can become a financially devastating way to hide company debt if accounting loopholes are exploited, as seen in the 2001 Enron scandal.

An ophthalmologist is a physician [MD, DO] who undergoes sub-specialty training in medical and surgical eye care. Following a medical degree, a doctor specializing in ophthalmology must pursue additional postgraduate residency training specific to that field. In the United States, following graduation from medical school, one must complete a four-year residency in ophthalmology to become an ophthalmologist. Following residency, additional specialty training (or fellowship) may be sought in a particular aspect of eye pathology.

Ophthalmologists prescribe medications to treat ailments, such as eye diseases, implement laser therapy, and perform surgery when needed. Ophthalmologists provide both primary and specialty eye care—medical and surgical. Most ophthalmologists participate in academic research on eye diseases at some point in their training and many include research as part of their career. Ophthalmology has always been at the forefront of medical research with a long history of advancement and innovation in eye care.

Optometrist

Optometrists focus on regular vision care and primary health care for the eye. After college, they spend 4 years in a professional program and get a doctor of optometry degree. But they don’t go to medical school. Some optometrists get additional clinical training or complete a specialty fellowship after optometry school. They:

Monitor eye conditions related to diseases like diabetes

Manage and treat conditions like dry eye and glaucoma

Provide low-vision aids and vision therapy

There are specialties among optometrists. They include:

Pediatric optometry. These providers work with babies, toddlers, and children, using special techniques to test their vision.

Neuro-optometry. If you have vision problems that result from a brain injury, this is the type of optometrist you might visit.

Low-vision optometry. If you have low vision—that means you can’t see well enough to perform your daily activities and your sight can’t be corrected by glasses or contact lenses, medicine, or surgery—low-vision optometrists offer devices and strategies that can improve your quality of life.

***

***

Optician

An optician is an eye care specialist who helps you choose the right eyeglasses, contact lenses or other vision correction devices. They can’t diagnose or treat conditions that affect your eyes or vision. They’ll work with you to get the right corrective lenses after your optometrist or ophthalmologist gives you a prescription.

Ocularist

An ocularist is an eye care specialist who provides care for people needing prosthetic eyes due to injury, infection or congenital disease (present at birth). Losing or damaging an eye can be a traumatic experience, and the need for a prosthetic can be overwhelming. Ocularists offer long-term care. They collaborate with your healthcare team to create or restore a more natural facial appearance with the goal of enhancing your health-related quality of life.

Trump says pharma tariffs could be as high as 250%

The president revealed that he plans to formally announce tariffs on the pharmaceutical industry “within the next week or so” in an attempt to force drug manufacturing to the US, he told CNBC several days ago.

Posted on August 6, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I and Staff Reporters

***

***

Illinois just became the first US state to regulate AI mental health services this week when Gov. JB Pritzker signed a law banning AI therapy.

The law forbids chatbots from acting as therapists and limits how human mental health professionals can use AI to aid their work. Companies face up to $10,000 in fines if they violate the law, according to Morning Brew.

The move comes as ChatGPT users—particularly younger ones—increasingly turn to the app for what amounts to free therapy. OpenAI recently made updates to its model to encourage users to use ChatGPT in a healthier way.

An acute care inpatient hospital is a health care organization or “anchor hospital” in which a patient is treated for an acute (immediate and severe) episode of illness or the subsequent treatment of injuries related to an accident or trauma, or during recovery from surgery. Specialized personnel using complex and sophisticated technical equipment and materials usually render acute professional care in a hospital setting. Unlike chronic care, acute care is often necessary for only a short time. Measures of acute health care utilization are represented by three separate rates:

Rate of admissions per 1000 patients.

Average length of stay per admission.

Total days of care per 1000 patients.

***

***

Psychiatric Hospital

A psychiatric hospital (behavioral health, mental hospital, or asylum) specializes in the treatment of patients with mental illness or drug-related illness or dependencies. Psychiatric wards differ only in that they are a unit of a larger hospital.

Specialty Hospital

A specialty hospital is a type of health care organization that has a limited focus to provide treatment for only certain illnesses such as cardiac care, orthopedic or plastic surgery, elder care, radiology / oncology services, neurological care, or pain management cases. These organizations are often owned by doctors who refer patients to them. In recent years, single-specialty hospitals have emerged in various locations in the United States. Instead of offering a full range of inpatient services, these hospitals focus on providing services relating to a single medical specialty or cluster of specialties.

Long-Term Care Hospital

A long-term care hospital is an entity that provides assistance and patient care for the activities of daily living (ADLs), including reminders and standby help for those with physical, mental, or emotional problems. This includes physical disability or other medical problems for 3 months or more (90 days). The criteria of five ADLs may also be used to determine the need for help with the following: meal preparation, shopping, light housework, money management, and telephoning. Other important considerations include taking medications, doing laundry, and getting around outside.

Rural Hospital

The parameters of a rural hospital are determined based on distance. A rural hospital is defined as a hospital serving a geographic area 10 or more miles from the nexus of a population center of 30,000 or more.

More specifically, a rural hospital means an entity characterized by one of the following:

Type A rural hospital—small and remote, has fewer than 50 beds, and is more than 30 miles from the nearest hospital

Type B rural hospital—small and rural, has fewer than 50 beds, and is 30 miles or less from the nearest hospital

Type C rural hospital—considered rural and has 50 or more beds

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

There’s an aspect to retirement that many physicians do not plan for … the transition from work and practice to retirement. Your work has been an important part of your life. That’s why the emotional adjustments of retirement may be some of the most difficult ones.

For example, what would you like to do in retirement? Your retirement vision will be unique to you. You are retiring to something not from something that you envisioned. When you have more time, you would like to do more traveling, play golf or visit more often, family and friends. Would you relocate closer to your kids? Learn a new art or take a new class? Fund your grandchildren’s education? Do you have philanthropic goals? Perhaps you would like to help your church, school or favorite charity? If your net worth is above certain limits, it would be wise to take a serious look at these goals. With proper planning, there might be some tax benefits too. Then you have to figure how much each goal is going to cost you.

If you have a list of retirement goals, you need to prioritize which goal is most important. You can rate them on a scale of 1 to 10; 10 being the most important. Then, you can differentiate between wants and needs. Needs are things that are absolutely necessary for you to retire; while wants are things that still allow retirement but would just be nice to have.

Recent studies indicate there are three phases in retirement, each with a different spending pattern [Richard Greenberg CFP®, Gardena CA, personal communication]. The three phases are:

The Early Retirement Years. There is a pent-up demand to take advantage of all the free time retirement affords. You can travel to exotic places, buy an RV and explore forty-nine states, go on month-long sailing vacations. It’s possible during these years that after-tax expenses increase during these initial years, especially if the mortgage hasn’t been paid off yet. Usually the early years last about ten years until most retirees are in their 70’s.

Middle Years. People decide to slow down on the exploration. This is when people start simplifying their life. They may sell their house and downsize to a condo or townhouse. They may relocate to an area they discovered during their travels, or to an area close to family and friends, to an area with a warm climate or to an area with low or no state taxes. People also do their most important estate planning during these years. They are concerned about leaving a legacy, taking care of their children and grandchildren and fulfilling charitable intent. This a time when people spend more time in the local area. They may start taking extension or college classes. They spend more time volunteering at various non-profits and helping out older and less healthy retirees. People often spend less during these years. This period starts when a retiree is in his or her mid to late 70’s and can last up to 20 years, usually to mid to late-80’s.

Late Years. This is when you may need assistance in our daily activities. You may receive care at home, in a nursing home or an assisted care facility. Most of the care options are very expensive. It’s possible that these years might be more expensive than your pre-retirement expenses. This is especially true if both spouses need some sort of assisted care. This period usually starts when the retiree is their 80’s; however they can sometimes start in the middle to the late 70’s.

***

***

[A] Planning issues – early career

Most retirement lifestyle issues do not have to be addressed at this point. Keeping a healthy, balanced lifestyle will help to ensure a more productive retirement. This is the time to focus on the financial aspects of retirement planning.

[B] Planning issues – mid career

If early retirement is a major objective, start thinking about activities that will fill up your time during retirement. Maintaining your health is more critical, since your health habits at this time will often dictate how healthy you will be in retirement

[C] Planning issues – late career

Three to five years before you retire, start making the transition from work to retirement.

Try out different hobbies;

Find activities that will give you a purpose in retirement;

Establish friendships outside of the office or hospital;

Discuss retirement plans with your spouse.

If you plan to relocate to a new place, it is important to rent a place in that area and stay for few months and see if you like it. Making a drastic change like relocating and then finding you don’t like the new town or state might be very costly mistake. The key is to gradually make the transition.

For physicians, like most folks, retirement is the stage in life when one chooses to leave the workforce and live off sources of income or savings that do not require active work. The age at which a person retires, their lifestyle during retirement, and the way they fund that lifestyle, will vary from one person to the next, depending on individual preferences and financial planning. Usually it is age 65.

Some doctors may opt for early retirement to enjoy their hobbies and travel, while others may continue working part-time to stay engaged and supplement their income. Effective retirement planning often involves a combination of savings, investments, and possibly pension benefits to ensure a comfortable and secure post-work life.

SPEAKING: ME-P Editor Dr. David Edward Marcinko MBA MEd will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Trade: President Trump signed an executive order late Friday unleashing a wave of new tariffs on 69 US trading partners that will go into effect on August 7th. Here’s a handy list of tariffs and their economic effects for readers of this ME-P.

Markets: Stocks opened lower Friday and kept falling thanks to a double whammy of new tariff rates and a shocking slowdown in the labor market, while bond yields tumbled.

Commodities: Goldjumped as the likelihood of a rate cut rose due to the latest jobs report, while oil sank on reports that OPEC+ may announce a crude production boost as soon as this weekend.

More Markets: Stocks may want to stop reading the news for a while after tanking Friday in response to President Trump laying out sweeping new global tariffs, as well as a jobs report that showed the labor market has been cooling down more than we realized. The dip left all three major averages down for the week.

Stock spotlight: Reddit, that platform that has once again been propping up meme stocks, managed to buck the trend and soar, following its report of better-than-expected quarterly earnings results.

Since the financial crisis in 2008, several start-up companies from Silicon Valley and Boston [Learn Vest, Betterment, Financial Guard, Quovo, WealthFront, Nest Egg Wealth. Wealth-Front and Personal Capital] have emerged with the mantra that individual investors, younger and informed clients will receive portfolio strategies, financial advice and performance metrics directly from various internet and online advisory platforms. Termed “robo-advisors” by some, their existence heralds the doom of financial advisors; or at least drives down the value of Financial Advisory guidance; reduces fees and holds them more accountable to clients.

On the other hand, detractors say the financial advice may not be as good because the personalization will not be there; but pricing fees will be more competitive, at least initially. Going forward price will get even lower and service better. And ultimately, as consumers get more information on line, product and service will improve and be delivered to them faster than thru traditional human channels of distribution. The era of quarterly client meetings with TAMPs is fading. Clients will have access to their portfolios; in real time, all the time.

Turnkey Asset Management Program (TAMP) Defined

A turnkey asset management program offers a fee-account technology platform that financial advisers, broker-dealers, insurance companies, banks, law firms, and CPA firms can use to oversee their clients’ investment accounts.

Turnkey asset management programs are designed to help financial professionals save time and allow them to focus on providing clients with service in their areas of expertise, which may not include asset management tasks like investment research and portfolio allocation. In other words, TAMPs let financial professionals and firms delegate asset management and research responsibilities to another party that specializes in those areas.

The growth of more traditional direct to investment platforms like E-Trade and Schwab has outpaced Financial Advisors and recently human advisors must have the technology and niche space specificity to survive in the future. Realistically, robo-advisors, Artificial Intelligence and traditional flesh-and-blood FAs will seamlessly merge into a hybrid platform indistinguishable to most all.