BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

An Internet Protocol (IP) address is a numerical identifier assigned to network interfaces participating in an IP‑based network. It functions as the cornerstone of packet‑switched communication, enabling devices to locate, identify, and exchange data across interconnected networks. At a technical level, an IP address encodes both host identity and network topology, allowing routers to forward packets efficiently through hierarchical addressing structures.

IP Address Structure and Protocol Versions

The two dominant versions of the Internet Protocol—IPv4 and IPv6—define the format and semantics of IP addressing.

IPv4, defined in RFC 791, uses a 32‑bit address space. These 32 bits are typically represented in dotted‑decimal notation, divided into four octets. The address space provides possible addresses, roughly 4.3 billion. IPv4 addresses are logically divided into network and host portions, historically using classful addressing (Classes A, B, C), though modern networks rely on Classless Inter‑Domain Routing (CIDR). CIDR allows arbitrary prefix lengths, expressed as a suffix such as /24, enabling more efficient allocation and route aggregation.

IPv6, defined in RFC 8200, expands the address space to 128 bits, represented in eight groups of hexadecimal values separated by colons. The enormous address space— possible addresses—supports hierarchical routing, stateless address autoconfiguration (SLAAC), and built‑in support for multicast and anycast addressing. IPv6 eliminates broadcast traffic entirely, replacing it with more efficient multicast mechanisms.

Address Types and Scopes

IP addresses can be categorized by scope and function:

Unicast: Identifies a single network interface. Most traffic on the internet is unicast.

Multicast: Identifies a group of interfaces; packets are delivered to all group members.

Broadcast (IPv4 only): Targets all hosts on a local network segment.

Anycast (primarily IPv6): Assigned to multiple interfaces; packets are routed to the nearest instance based on routing metrics.

Additionally, addresses can be public (globally routable) or private (RFC 1918 for IPv4, Unique Local Addresses for IPv6). Private addresses require Network Address Translation (NAT) to communicate with the public internet, a workaround that became essential due to IPv4 exhaustion.

Static vs. Dynamic Assignment

IP addresses may be assigned statically or dynamically:

Static addressing involves manual configuration and is common for servers, routers, and infrastructure requiring predictable reachability.

Dynamic addressing uses the Dynamic Host Configuration Protocol (DHCP). DHCP automates address assignment, lease renewal, and configuration of parameters such as default gateways and DNS servers.

In IPv6 networks, dynamic assignment may use DHCPv6 or SLAAC. SLAAC allows hosts to generate their own addresses using router advertisements and interface identifiers, reducing administrative overhead.

Routing and Packet Delivery

IP addresses are integral to routing—the process by which packets traverse networks. When a host sends a packet, it encapsulates data in an IP header containing source and destination addresses. Routers examine the destination address and consult their routing tables to determine the next hop. Routing protocols such as OSPF, BGP, and IS‑IS maintain these tables by exchanging topology information.

The hierarchical nature of IP addressing enables route aggregation, reducing the size of global routing tables. For example, a provider may advertise a single /16 prefix representing thousands of customer networks.

DNS and Address Resolution

Human‑readable domain names must be translated into IP addresses before communication can occur. The Domain Name System (DNS) performs this translation. When a user enters a URL, the system queries DNS resolvers, which return the corresponding A (IPv4) or AAAA (IPv6) records.

On local networks, the Address Resolution Protocol (ARP) maps IPv4 addresses to MAC addresses. IPv6 uses Neighbor Discovery Protocol (NDP) for similar functionality, leveraging ICMPv6 messages.

Security and Privacy Considerations

IP addresses reveal network topology and can expose approximate geographic location. Attackers may use them for reconnaissance, scanning, or targeted attacks. Techniques such as NAT, VPNs, and IPv6 privacy extensions help mitigate exposure by masking or rotating interface identifiers.

Conclusion

An IP address is far more than a simple identifier; it is a fundamental component of the Internet Protocol suite, enabling routing, addressing, and communication across global networks. Its structure, allocation mechanisms, and interaction with routing and resolution protocols form the backbone of modern digital infrastructure. As the internet continues to scale and diversify, the role of IP addressing—particularly IPv6—remains central to the performance, security, and scalability of global communication systems.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Risk management has become an essential component of modern medical practice, shaping how physicians deliver care, communicate with patients, and navigate an increasingly complex healthcare environment. While medicine has always involved uncertainty, today’s physicians face heightened scrutiny, evolving regulations, and rising patient expectations. Effective risk management is not merely about avoiding lawsuits; it is about fostering safer clinical environments, strengthening trust, and supporting high‑quality care. When approached proactively, it becomes a framework that protects both patients and practitioners.

At its core, risk management begins with recognizing the areas where errors, misunderstandings, or system failures are most likely to occur. Clinical decision‑making is an obvious focal point. Physicians must constantly balance diagnostic possibilities, weigh treatment options, and consider potential complications. Even with strong clinical judgment, risks arise when information is incomplete, when symptoms are ambiguous, or when time pressures limit thorough evaluation. To mitigate these challenges, physicians increasingly rely on structured clinical protocols, decision‑support tools, and multidisciplinary collaboration. These strategies help reduce variability in care and ensure that critical steps are not overlooked.

Communication is another central pillar of risk management. Many malpractice claims stem not from clinical mistakes but from breakdowns in communication—unclear explanations, unmet expectations, or perceived dismissiveness. Physicians who take the time to listen carefully, explain diagnoses and treatment plans in accessible language, and invite questions create a foundation of trust that can prevent conflict later. Informed consent is a particularly important aspect of this process. When patients fully understand the benefits, risks, and alternatives of a proposed intervention, they are better equipped to make decisions and less likely to feel blindsided if complications arise. Clear documentation of these conversations further strengthens the physician’s position and ensures continuity of care.

Documentation itself is a powerful risk‑management tool. Accurate, timely, and thorough medical records serve multiple purposes: they guide clinical decision‑making, support communication among care teams, and provide a factual account of events if questions arise later. Physicians who document not only what they did but why they made certain decisions create a transparent narrative that reflects thoughtful, patient‑centered care. Conversely, incomplete or inconsistent records can create vulnerabilities, even when the care provided was appropriate.

***

***

Another important dimension of risk management involves staying current with medical knowledge and regulatory requirements. Medicine evolves rapidly, and outdated practices can expose physicians to unnecessary risk. Continuing education, peer review, and participation in quality‑improvement initiatives help physicians maintain competence and identify areas for improvement. Regulatory compliance—whether related to privacy laws, prescribing rules, or reporting obligations—is equally critical. Violations, even unintentional ones, can lead to legal consequences and damage professional credibility.

Systems‑based risk management has also gained prominence. Many errors arise not from individual negligence but from flawed processes or communication gaps within healthcare organizations. Physicians who engage in system‑level improvements—such as refining hand off procedures, participating in morbidity and mortality reviews, or advocating for safer workflows—contribute to a culture of safety that benefits everyone. This collaborative approach recognizes that risk management is not solely the responsibility of individual clinicians but a shared commitment across the healthcare team.

Emotional intelligence plays a surprisingly influential role as well. When adverse events occur, patients and families often look to the physician for honesty, empathy, and reassurance. A compassionate response can de‑escalate tension and preserve the therapeutic relationship, even in difficult circumstances. Many institutions now encourage physicians to participate in disclosure training, which helps them navigate these conversations with clarity and sensitivity. Addressing the emotional impact on physicians themselves is equally important; burnout, fatigue, and stress can impair judgment and increase the likelihood of errors. Supporting physician well‑being is therefore an indirect but vital component of risk management.

Ultimately, effective risk management is not about practicing defensively or avoiding complex cases. It is about creating an environment where safety, transparency, and continuous improvement are woven into everyday practice. Physicians who embrace these principles are better equipped to navigate uncertainty, maintain strong patient relationships, and deliver care that aligns with both ethical and professional standards. In a healthcare landscape that continues to evolve, risk management remains a dynamic and indispensable part of responsible medical practice.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on February 2, 2026 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The Role of Artificial Intelligence in Insurance and Risk Management

Artificial Intelligence (AI) is revolutionizing the insurance and risk management industries by enhancing efficiency, accuracy, and customer experience. As data becomes increasingly central to decision-making, AI offers powerful tools to analyze vast datasets, predict outcomes, and automate complex processes. Its integration is reshaping traditional models and enabling insurers to better assess risk, detect fraud, and personalize services.

One of the most transformative applications of AI in insurance is in underwriting. Traditionally, underwriting relied on manual evaluation of risk factors, which was time-consuming and prone to human error. AI algorithms can now process structured and unstructured data—from medical records to social media activity—to assess risk profiles with greater precision. Machine learning models continuously improve as they ingest more data, allowing insurers to refine their risk assessments and pricing strategies dynamically.

Claims processing is another area where AI is making a significant impact. Through natural language processing (NLP) and image recognition, AI can automate the evaluation of claims, reducing the time and cost associated with manual reviews. For example, AI can analyze photos of vehicle damage to estimate repair costs or flag inconsistencies in a claim that may indicate fraud. This not only speeds up the claims cycle but also enhances fraud detection, a critical concern in the industry.

Risk management benefits from AI’s predictive capabilities. By analyzing historical data and identifying patterns, AI can forecast potential risks and suggest mitigation strategies. In property insurance, AI can assess the likelihood of natural disasters by combining satellite imagery with climate data. In health insurance, predictive analytics can identify individuals at higher risk of chronic conditions, enabling early interventions and reducing long-term costs.

***

***

Customer experience is also being transformed by AI. Chatbots and virtual assistants provide 24/7 support, answering queries, guiding users through policy selection, and even initiating claims. These tools improve accessibility and responsiveness, fostering customer satisfaction and loyalty. Moreover, AI-driven personalization allows insurers to tailor products and communications to individual preferences and behaviors, enhancing engagement.

Despite its advantages, the adoption of AI in insurance and risk management raises ethical and regulatory challenges. Data privacy is a major concern, as AI systems require access to sensitive personal information. Ensuring transparency in AI decision-making is also critical, especially when algorithms influence coverage eligibility or claim outcomes. Regulators are increasingly scrutinizing AI applications to ensure fairness, accountability, and compliance with legal standards.

In conclusion, AI is a game-changer for insurance and risk management, offering tools to streamline operations, improve accuracy, and enhance customer service. As the technology evolves, insurers must balance innovation with ethical responsibility, ensuring that A.I. serves both business goals and societal interests. The future of insurance lies in intelligent systems that not only manage risk but also anticipate and prevent it—ushering in a new era of proactive, data-driven protection.

Posted on January 30, 2026 by Dr. David Edward Marcinko MBA MEd CMP™

A FINANCIAL THEORY

By Staff Reporters

***

***

FINANCIAL THEORY

Theories of finance are essential for understanding and analyzing various financial phenomena. They provide the conceptual framework for investment strategies, risk management, and financial decision-making.

***

Merton’s Credit Risk Model: Innovations in Corporate Debt Valuation

Merton’s Model for Credit Risk, developed by Robert C. Merton in 1974, represents a significant advancement in the field of financial economics, particularly in the assessment of credit risk. Building upon the foundations of the Black-Scholes Model for options pricing, Merton’s approach introduced a novel method for valuing corporate debt and assessing the probability of default.

Merton’s model conceptualizes a company’s equity as a call option on its assets, with the strike price equivalent to the debt’s face value maturing at the debt’s due date. In this framework, if the value of the company’s assets falls below the debt’s face value at maturity, the firm defaults, as it is more beneficial for equity holders to hand over the assets to the debt holders rather than repay the debt. Conversely, if the asset value exceeds the debt value, the firm pays off its debt and equity holders retain control of the company.

The model calculates the risk of default by analyzing the volatility of the firm’s assets and the level of its liabilities. The key insight of the model is that the safer a company’s debt (lower probability of default), the less valuable the equity as a call option, and vice versa. This approach provides a more dynamic and market-based view of credit risk, as opposed to traditional static measures.

***

***

One of the model’s critical assumptions is that the firm’s assets follow a random walk and are normally distributed. The model also presumes that markets are efficient, and there is no friction in trading. Furthermore, Merton’s model assumes that the firm’s capital structure only comprises equity and zero-coupon debt, which simplifies the real-world complexities of corporate finance.

Despite these simplifications, Merton’s model has had a profound impact on the field of credit risk analysis. It laid the groundwork for the development of more sophisticated credit risk models and tools used in the financial industry, such as Moody’s KMV Model. These models have become integral in the risk management practices of banks and financial institutions, particularly in the assessment of counter-party risk and the pricing of risky debt.

In conclusion, Merton’s Model for Credit Risk has been instrumental in bridging the gap between corporate finance and asset pricing theory. It has provided a more comprehensive and market-based framework for understanding and managing credit risk, which has been pivotal for both academia and the financial industry. The model’s influence extends beyond credit risk analysis, affecting the broader areas of corporate finance, risk management, and financial regulation.

Gold has long been regarded as a cornerstone of wealth preservation, and its role within modern investment portfolios continues to attract scholarly attention. As both a tangible asset and a financial instrument, gold embodies characteristics that distinguish it from equities, fixed income securities, and other commodities. Its historical resilience, inflation-hedging capacity, and diversification benefits render it a subject of considerable importance in portfolio construction and risk management.

Historical and Monetary Significance

Gold’s enduring appeal is rooted in its function as a monetary standard and store of value. For centuries, gold underpinned global currency systems, most notably through the gold standard, which provided stability in international trade and monetary policy. Although fiat currencies have supplanted gold in official circulation, its symbolic and practical role as a measure of wealth persists. This historical continuity reinforces investor confidence in gold as a reliable repository of value during periods of economic uncertainty.

Inflation Hedge and Safe-Haven Asset

A substantial body of empirical research demonstrates that gold serves as a hedge against inflation and currency depreciation. When consumer prices rise and fiat currencies weaken, gold tends to appreciate, thereby preserving purchasing power. Moreover, gold’s status as a safe-haven asset is particularly evident during geopolitical crises, financial market turbulence, and systemic shocks. In such contexts, investors reallocate capital toward gold, seeking protection from volatility in traditional asset classes. This defensive quality underscores gold’s utility in stabilizing portfolios during adverse conditions.

Diversification and Risk Management

From the perspective of modern portfolio theory, gold offers diversification benefits due to its low correlation with equities and bonds. Incorporating gold into a portfolio reduces overall variance and enhances risk-adjusted returns. Studies suggest that even modest allocations—typically ranging from 5 to 10 percent—can improve portfolio resilience by mitigating downside risk. This non-correlation is especially valuable in environments characterized by heightened uncertainty, where traditional diversification strategies may prove insufficient.

Investment Vehicles and Accessibility

Gold’s versatility as an investment is reflected in the variety of instruments available to investors. Physical bullion, in the form of coins and bars, provides tangible ownership but entails storage and insurance costs. Exchange-traded funds (ETFs) offer liquidity and ease of access, while mining equities provide leveraged exposure to gold prices, albeit with operational risks. Futures contracts and derivatives enable sophisticated strategies, though they demand expertise and tolerance for volatility. The breadth of these vehicles ensures that gold remains accessible across diverse investor profiles.

Limitations and Critical Considerations

Despite its strengths, gold is not without limitations. Unlike equities or bonds, gold does not generate income, such as dividends or interest. This absence of yield can constrain long-term portfolio growth, particularly in low-inflation environments. Furthermore, gold prices are subject to volatility, influenced by investor sentiment, central bank policies, and global demand dynamics. Overexposure to gold may therefore hinder portfolio performance, underscoring the necessity of balanced allocation.

Conclusion

Gold’s dual identity as a historical store of value and a contemporary financial instrument secures its relevance in portfolio construction. Its inflation-hedging capacity, safe-haven qualities, and diversification benefits justify its inclusion as a strategic asset. Nevertheless, prudent management is essential, given its lack of yield and susceptibility to volatility. Within a scholarly framework of portfolio theory, gold emerges not as a panacea but as a complementary asset, enhancing resilience and stability in the face of evolving economic landscapes.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

What Medical School Didn’t Teach Doctors About Money

Medical school is designed to mold students into competent, compassionate physicians. It teaches anatomy, pathology, pharmacology, and clinical skills with precision and rigor. Yet, despite the depth of medical knowledge imparted, one critical area is often overlooked: financial literacy. For many doctors, the transition from student to professional comes with a steep learning curve—not in medicine, but in money. From managing debt to understanding taxes, investing, and retirement planning, medical school leaves a financial education gap that can have long-term consequences.

The Debt Dilemma

One of the most glaring omissions in medical education is how to manage student loan debt. The average medical student graduates with over $200,000 in debt, yet few are taught how to navigate repayment options, interest accrual, or loan forgiveness programs. Many doctors enter residency with little understanding of income-driven repayment plans or Public Service Loan Forgiveness (PSLF), missing opportunities to reduce their financial burden. Without guidance, some make costly mistakes—such as refinancing federal loans prematurely or choosing repayment plans that don’t align with their career trajectory.

Income ≠ Wealth

Medical students often assume that a high salary will automatically lead to financial security. While physicians do earn more than most professionals, income alone doesn’t guarantee wealth. Medical school rarely addresses the importance of budgeting, saving, and investing. As a result, many doctors fall into the “HENRY” trap—High Earner, Not Rich Yet. They spend lavishly, assuming their income will always cover expenses, only to find themselves living paycheck to paycheck. Without a solid financial foundation, even high earners can struggle to build net worth.

***

***

Taxes and Business Skills

Doctors are also unprepared for the complexities of taxes. Whether employed by a hospital or running a private practice, physicians face unique tax challenges. Medical school doesn’t teach how to track deductible expenses, optimize retirement contributions, or navigate self-employment taxes. For those who open their own clinics, the lack of business education is even more pronounced. Understanding profit margins, payroll, insurance billing, and compliance regulations is essential—but rarely covered in medical training.

Investing and Retirement Planning

Another blind spot is investing. Medical students are rarely taught the basics of compound interest, asset allocation, or retirement accounts. Many don’t know the difference between a Roth IRA and a traditional 401(k), or how to evaluate mutual funds and index funds. This lack of knowledge delays retirement planning and can lead to missed opportunities for long-term growth. Some doctors rely on financial advisors without understanding the fees or conflicts of interest involved, putting their wealth at risk.

Insurance and Risk Management

Medical school also fails to educate students on insurance—life, disability, malpractice, and health. Doctors need robust coverage to protect their income and assets, but many don’t know how to evaluate policies or understand terms like “own occupation” or “elimination period.” Inadequate coverage can leave physicians vulnerable to financial disaster in the event of illness, injury, or litigation.

Emotional and Behavioral Finance

Beyond technical knowledge, medical school overlooks the emotional side of money. Physicians often face pressure to maintain a certain lifestyle, especially after years of sacrifice. The desire to “catch up” can lead to impulsive spending, luxury purchases, and financial stress. Without tools to manage money mindset and behavioral habits, doctors may struggle with guilt, anxiety, or burnout related to finances.

The Case for Financial Education

Fortunately, awareness of this gap is growing. Organizations like Medics’ Money and podcasts such as “Docs Outside the Box” are working to fill the void by offering financial education tailored to physicians.

These resources cover everything from budgeting and debt management to investing and entrepreneurship. Some medical schools are beginning to incorporate financial literacy into their curricula, but progress is slow and inconsistent.

Conclusion

Medical school equips doctors to save lives, but it doesn’t prepare them to secure their own financial future. The lack of financial education leaves many physicians vulnerable to debt, poor investment decisions, and lifestyle inflation. To thrive both professionally and personally, doctors must seek out financial knowledge beyond the classroom. Whether through self-study, mentorship, or professional guidance, understanding money is as essential as understanding medicine. After all, financial health is a cornerstone of overall well-being—and every doctor deserves to master both.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on September 22, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Authentication:

The verification of the identity of an individual, system, machine, or any other unique entity

Authorization:

The process of allowing access to specific areas of a system based on the role and needs of the user

Committee Charter:

A document that defines the purposes and responsibilities of the oversight committee

Compliance Risk Profile:

The current and prospective risk to earnings or capital arising from violations of or nonconformance with laws, rules, regulations, prescribed practices, internal policies and procedures, or ethical standards

Control Assessment:

A high-level review and analysis of controls relating to a process; should encompass both current and missing controls

Controls:

Methods that preserve the integrity of important information, meet operational or financial targets, and/or communicate management policies (See also: Key Control, Secondary Control, Tertiary Control)

ERM Policy Statement:

Defines an organization’s approach to and method of enterprise risk management

Governance:

Processes and structures implemented to communicate, manage, and monitor organizational activities

Impact:

The influence and effect of a risk

Inherent Risk:

Risk that is inherent to a process, taking into consideration the likelihood and impact of a risk

Key Control:

A primary control that is essential for a business process; typically takes place during the process it applies to

Key Indicators:

Measurements that are important for organizations to monitor for potential issues; examples include key performance indicators (KPIs) and key risk indicators (KRIs)

Key Performance Indicator (KPI):

A measurement with a defined set of goals and tolerances that gauges the performance of an important business activity

Key Risk Indicator (KRI):

A proactive measurement for future and emerging risks that indicates the possibility of an event that adversely affects business activities

Likelihood:

The probability of a risk occurring

Mitigation Actions:

The necessary steps, or action items, to reduce the likelihood and/or impact of a potential risk

Operation Risk Profile:

1) The risk arising from the execution of an organization’s business processes; 2) The risk of loss resulting from failed or inadequate internal processes, systems, people, or other entities

Price Risk Profile:

The risk to earning or capital arising from adverse changes in portfolio values

Process:

1) The principle elements of essential business functions within work groups or business units; 2) A set of tasks completed by business continuity plan owners within a department

Reputation Risk Profile:

The current and prospective risk to earnings or capital arising from negative public opinion or perception

Residual Risk:

Risk remaining after considering the existing control environment

Risk:

A potential event or action that would have an adverse effect on the organization

Risk Appetite:

A statement that broadly considers the risk levels that management deems acceptable

Risk Assessment:

The prioritization of potential business disruptions based on the impact and likelihood of occurrence; includes an analysis of threats based on the impact to the organization, its customers, and financial markets

Risk Tolerance:

A metric that sets the acceptable level of variation around organizational objectives and provides assurance that the organization remains within its risk appetite

Secondary Control:

An important control that typically takes place after the process it applies to (i.e., reporting or ongoing monitoring)

Strategic Risk Profile:

The current and prospective risk to earnings or capital raising from adverse business decisions, improperly implemented decisions, or lack of responsiveness to industry changes

Tertiary Control:

A non-essential control that can still be applied effectively to a business process

Velocity:

The time it takes a risk event to manifest itself

Vulnerability:

An entity’s susceptibility to a risk event as determined by the entity’s preparedness, agility, and adaptability

Posted on September 19, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

What Is Pure Risk?

Pure risk is a category of risk that cannot be controlled and has two outcomes: complete loss or no loss at all. There are no opportunities for gain or profit when pure risk is involved. Pure risk is generally prevalent in situations such as natural disasters, fires, or death. These situations cannot be predicted and are beyond anyone’s control. Pure risk is also referred to as absolute risk.

***

1. Personal Risks

Now, there are basically 3 types of pure risks that concern individual physicians. These incur losses like loss of income, additional expenses and devaluation of property. There are 4 risk factors affecting them:

Premature death. This is death of a breadwinner who leaves behind financial responsibilities.

Old age / retirement. The risk of being retired without sufficient savings to support retirement years.

Health crisis. Individual with health problem may face a potential loss of income and increase in medical expenditures.

Unemployment. Jobless individual may have to live on their savings. If savings are depleted, a bigger crisis is awaiting.

2. Property Risks

This means the possibility of damage or loss to the property owned due to some cause. There are two types of losses involved.

Direct loss which means financial loss as a result of property damage.

Consequential loss which means financial loss due to the happenings of direct loss of the property.

For instance, a medical practice that burned down may incur repair costs as the direct loss. The consequential loss is being unable to run the practice business to generate income.

3. Liability Risks

A doctor is legally liable to his wrongful act that cause damage to a third party; physically, by reputation or property. S/he can be legally sued with no maximum in the compensation amount if found guilty.

Knowing how risks are classified, and the types of pure risks an individual is exposed to, will provide a fundamental overview on these risk topics and prepare you to further acquire the knowledge of how to deal with and manage them as a physician executive, leader, or manager.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

ORGANIZATIONAL BEHAVIOR ANDCLASSIFICATION OF RISKS

DEFINITION EMOTIONAL INTELLIGENCE: Emotional intelligence [EI] refers to the ability to identify and manage one’s own emotions, as well as the emotions of others. Emotional intelligence is generally said to include a few skills: namely emotional awareness, or the ability to identify and name one’s own emotions; the ability to harness those emotions and apply them to tasks like thinking and problem solving; and the ability to manage emotions, which includes both regulating one’s own emotions when necessary and helping others to do the same.

DEFINITIONAL ORGANIZATIONAL BEHAVIOR: Organizational behavior (OB) is the study of how individuals, groups, and organizations interact and influence one another. Though it is largely used within the field of business management as means to understand–and more effectively manage–groups of people. The reason businesses look to OB is because it can help organizations increase employee performance, while also creating a positive working environment.

CITE: Eugene Schmuckler; PhD MBA MEd CTS®

***

***

And so, as we review the concept of Emotional Intelligence and Organizational Behavior, it is possible to set up five EI/OB risk classes, based on the economic consequences of the occurrence of specific individual risks:

1. Prevented risks: Risks whose cost of occurrence is higher than their cost of management and whose occurrence may invoke additional legal sanctions. This class would include intentional torts and injuries caused by gross negligence.

2. Normally prevented risks: Risks whose cost of occurrence is greater than the cost of their management but whose occurrence will be considered only as negligent. This class includes most negligent injuries and most types of product liability actions.

3. Managed risks: Risks whose cost of occurrence is only slightly greater than their cost of management. The plaintiff usually has the burden of showing that the defendant owed the plaintiff a special duty to recover for one of these risks.

4. Un-Prevented risks: Risks whose cost of occurrence is less than their cost of management. The classic example of this class is the cost of railroad crossing barriers compared to the cost of people being hit by trains.

5. Un-Preventable risks: Risks whose occurrence is unmanageable. The assignment of a risk to one of these classes is a major problem in medical and healthcare quality control, because the class of a risk determines how much effort must be expended to prevent the risk. The misclassification of a prevented or normally prevented risk as a managed or un-prevented risk can result in large financial losses.

***

For example: A medical clinic that does not update obsolete equipment, such as inaccurate oxygen monitors, would be liable for any injuries attributable to the obsolete equipment. The classifications of risk must be reviewed periodically to determine if the cost of the risk-taking behavior has changed, thereby altering the classification.

***

***

For example: A small hospital in a rural area would not be expected to have the sophisticated equipment as a major hospital in a city. If an accident victim is brought into the rural facility, the hospital’s duty may be to transfer the patient to a better-equipped facility. The patient will face the risk of dying because of the delay in treatment, but the risk of insufficient treatments outweighs the risk of transfer. If the same victim were brought into a hospital in a major metropolitan center, the duty would be to treat the patient without a transfer. The risk of transfer has not changed, but the risk of insufficient treatment has disappeared.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on May 4, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

If getting answers from ChatGPT makes you feel dystopian, you may not want to hear about OpenAI CEO Sam Altman’s other co-founded venture, now rolling out stateside. It scans your eyeballs in exchange for cryptocurrency.

What in the Demolition Man? The device, which creates a unique user ID for your scan, is meant to address a problem that Altman had a hand in creating: how to verify identities and confirm humanity in a world full of artificial intelligence.

The project, called World (formerly Worldcoin), went live in other countries in 2023. Its US expansion, announced this week, featured retail outlets in five cities where you can get your eyes scanned:

Tools for Humanity, the company behind the orbs, says 12+ million people around the world have participated so far.

It claims to keep your data private, but authorities in more than a dozen places have suspended World’s operations or investigated its data practices, per the WSJ.

Posted on April 15, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

WARNING – WARNING

By Staff Reporters

***

***

A “retirement account scam” is a type of online fraud that occurs when a third party administrator (TPA) for retirement investment accounts is tricked into authorizing a money distribution to an imposter posing as the true account holder.

The imposter often starts the scam by calling the TPA, identifying himself or herself as an actual account holder, and requesting a withdrawal distribution form. Once the imposter receives the withdrawal distribution form, the imposter returns the completed form to the TPA. The form is completed with the account holder’s real personal identifying information (PII)—often stolen via schemes, data breaches, and other hacking offenses—and bank account information for an account controlled by the imposter or the imposter’s conspirators.

***

***

After the TPA processes the fraudulent request, the request is forwarded to the investment firm responsible for managing the account holder’s investments, and the funds—often the account holder’s life savings—are then directed to the imposter’s designated bank account.

The vast majority of physicians and medical professionals major in one of the hard science while in college; biology, engineering, chemistry, mathematics, computer science or physics; etc. Few take undergraduate courses in finance, business management, securities analysis, accounting or economics; although this paradigm is changing with modernity. These course are not particularly difficult for the pre-medical baccalaureate major, they are just not on the radar screen for time compressed and highly competitive students; nor are they needed for medical or nursing school admission, or the many related allied health professional schools.

In fact, William C. Roberts MD, originally from Emory University in Atlanta, and former editor for the Baylor University Medical Center Proceedings and The American Journal of Cardiology, opined just a decade ago:

“Of the 125 medical schools in the USA, only one of them to my knowledge offers a class related to saving or investing money.”

And so, it is important to review some basic principles of economics, finance and accounting as they relate to financial planning in thees two textbooks; and this ME-P.

Posted on April 5, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

WARNING – WARNING

By Dr. DavidEdwardMarcinko; MBA MEd

***

***

According to www.NPR.org, there are more than120,000 health care forums on the Internet with opinions ranging from pharmaceuticals, to sexual dysfunction, to acne. The same goes for commercial doctor blogs that promote lotions, balms and potions, diets and vitamins, minerals, herbs, drinks and elixirs, or various other ingest-ants, digest-ants or pharmaceuticals, etc.

And, to other doctors, the blogging craze is a new novelty where there are no rules, protocols, standards or precise figures on how many “medical-doctor” or related physician-blogs are “out there.” Unfortunately, too many recount gory ER scenes, or pictorially illustrate horrific medical conditions, or serious and traumatic injuries. Of course, others simply are medical practice websites, or those that entice patients into more lucrative plastic surgery or concierge medical practices. Some are from self-serving/credible plaintiff-seeking attorneys wishing to assist patients.

Not all physician blogs are geared toward practice information, marketing or medical sensationalism. In fact, just the opposite seems to be the case in extremely candid blogs, like “Ranting Docs”, “White Coat Rants,” “Grunt Docs”, “Cancer Doc,” “The Happy Hospitalist,” “Mom MD”, “Cross-Over Health”, “Angry Docs” and “M.D.O.D.,” which bills itself as “Random Thoughts from a Few Cantankerous American Physicians.”

According to some of these, they are more like personal journals, or public diaries, where doctors vent about reimbursement rates, difficult cases, medical mistakes, declining medical prestige and control, and/or what a “bummer” it is to have so many patients die; not pay, or who are indigent, noncompliant. We call these the “disgruntled doctor sites.” Some even talk about their own patients, coding issues, or various doctor-patient shenanigans.

But, according to psychiatrist and blogger Dr. Deborah Peel and others, the problem with blogging about patients is the danger that one will be able to identify themselves – the doctor – or that others who know them will be able to identify them.” Her affiliation, Patient Privacy Rights, rightly worries that patients might track back to the individual, and adversely affect their employment, health insurance or other aspects of life.

***

***

And, according to Dr. Jay S. Grife; MA Esq., it is certainly true that if a doctor violates a patient’s privacy there could be legal consequences. Under HIPAA, physicians could face fines or even jail time. In some states, patients can file a civil lawsuit if they believe a doctor has violated their privacy. Still, internet privacy issues are an evolving gray-area that if not wrong, may still be morally and ethically questionable [personal communication].

Our colleague Robert Wachter MD, author of the blog called “Wachter’s World,” says it’s important for doctors to be able to share cases, as long as they change the facts substantially. On the other hand, the author of “Wachter’s World” and a leading expert on patient safety alternately suggests “You might say we as doctors should never be talking about experiences with our patients online or in books or in articles.” But, he says that “patients shouldn’t take all the information on blogs at face value. Taken for what they are — unedited opinions, and in some cases entertainment — blogs can give readers some useful insight into the good, the bad and the ugly of the medical profession”. Link: http://www.the-hospitalist.org/blogs

Well, fair enough! But, doctors unhappy with their current medical career choice, or its modern evolution, should probably consider counseling or even career change guidance, re-education and re-engineering. It is very inappropriate to vent career frustrations in a public venue. It’s far better for the blog to be private and/or by invitation only; if at all [Personal communication].

We believe that a hybrid mash-up of both views can be wholly appropriate, or grossly inappropriate in some cases. Of course the devil is in the details; linguistics and semantics aside. Nevertheless; what is not addressed in electronic physician “mea-culpas” are the professional liability risks and concerns that are evolving in this quasi-professional, quasi-lay, communication forum.

***

***

Example: We have seen medical mistakes, and liability admissions of all sorts, freely and glibly presented. In fact,

“Some physicians find that the act of liability blogging as a professional confession that is useful in moving past their malpractice mistakes. And, it is also a useful way to begin a commitment to a better professional life of caring in the future. It helps eliminate the toxic residue and angst of professional liability and guilt. Moreover, as they are unburdened of past acts of omission or commission, doctors should remember to also forgive those who have wronged them. This helps greatly with the process and brings additional peace.”

However, although some may say that this electronic confession is good for the soul, it may not be good for your professional liability carrier, or you, when plaintiff’s attorneys release a legion of IT focused interns, or automated bots, searching online for your self-admissions and scouring for your self-incriminations. Of course, a direct connection to a specific patient may still not be made and no HIPAA violation is involved. But, a vivid imagination is not need needed to envision this type of blind medical malpractice discovery deposition query even now.

QUESTION:“Doctor Smith, I noted all the medical errors admitted on your blog. What other mistakes did you make in the care and treatment of my client?”

And so, the question of plausible deniability, or culpability, is easily raised. If you must journalize your thoughts for sanity or stress release; do it in print. And, don’t tell anyone about it so the diary won’t be subpoenaed. Then tear it up and throw it away. Remember, with risk management, “It is all about credibility.” Don’t trash yours! These thoughts may be especially important if you covet a medical career as a researcher, editor, educator, medical expert or something other than a working-class or employed physician.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com

Posted on April 2, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Ann Miller RN MHA CPHQ CMP™

***

***

Finally … Fiduciary second investing and financial planning opinions right here!

Telephonic or electronic advice for medical professionals that is:

Objective, affordable, medically focused and financially personalized

Rendered by a pre-screened financial consultant for doctors and medical professionals

Offered on a pay-as-you-go basis, by phone or secure e-mail transmission

The iMBA Discussion Forum™ is a physician-to-financial advisor telephone or e-mail portal that connects independent financial professionals to doctors, nurses or healthcare executives desiring affordable and unbiased financial planning advice.

Medical professionals and healthcare executives can now receive direct access to pre-screened iMBA professionals in the areas of Investing, Financial Planning, Asset Allocation, Portfolio Management, Insurance, Mortgage and Lending, Human Resources, Retirement Planning and Employee Benefits. To assist our medical professional and healthcare executive members, we can be contracted with per-minute or per-project fees, and contacted by client phone, email or secure instant messaging.

Merger risk arbitrage, while a subset of a larger strategy called event-driven arbitrage, represents a sufficient portion of the market-neutral universe to warrant separate discussion.

Merger arbitrage earned a bad reputation in the 1980s when Ivan Boesky and others like him came to regard insider trading as a valid investment strategy. That notwithstanding, merger arbitrage is a respected strategy and when executed properly, can be highly profitable. It bets on the outcomes of mergers, takeovers and other corporate events involving two stocks which may become one.

Example:

A classic example is acquisition of SDL Inc. (SDLI) by JDS Uniphase Corp (JDSU). On July 10, 2010 JDSU announced its intent to acquire SDLI by offering to exchange 3.8 shares of its own shares for one share of SDLI. At that time, the JDSU shares traded at $101 and SDLI at $320.5. It was apparent that there was almost 20 percent profit to be realized if the deal went through (3.8 JDSU shares at $101 are worth $383 while SDLI was worth just $320.5).

This apparent mispricing reflected the market’s expectation about the deal’s outcome. Since the deal was subject to the approval of the U.S. Justice Department and shareholders, there was some doubt about its successful completion.

Risk arbitrageurs who did their homework and properly estimated the probability of success bought shares of SDLI and simultaneously sold short shares of JDSU on a 3.8 to 1 ratio, thus locking in the future profit. Convergence took place about eight months later, in February 2011, when the deal was finally approved and the two stocks began trading at exact parity, eliminating the mis-pricing and allowing arbitrageurs to realize a profit.

***

***

Hedge Fund Research defines the strategy as follows:

Merger Arbitrage,also known as risk arbitrage, involves investing in securities of companies that are the subject of some form of extraordinary corporate transaction, including acquisition or merger proposals, exchange offers, cash tender offers and leveraged buy-outs. These transactions will generally involve the exchange of securities for cash, other securities or a combination of cash and other securities. Typically, a manager purchases the stock of a company being acquired or merging with another company, and sells short the stock of the acquiring company. A manager engaged in merger arbitrage transactions will derive profit (or loss) by realizing the price differential between the price of the securities purchased and the value ultimately realized when the deal is consummated. The success of this strategy usually is dependent upon the proposed merger, tender offer or exchange offer being consummated.

When a tender or exchange offer or a proposal for a merger is publicly announced, the offer price or the value of the securities of the acquiring company to be received is typically greater than the current market price of the securities of the target company. Normally, the stock of an acquisition target appreciates while the acquiring company’s stock decreases in value. If a manager determines that it is probable that the transaction will be consummated, it may purchase shares of the target company and in most instances, sell short the stock of the acquiring company. Managers may employ the use of equity options as a low-risk alternative to the outright purchase or sale of common stock. Many managers will hedge against market risk by purchasing S&P put options or put option spreads.

Posted on March 19, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Split-Dollar Life Insurance: An arrangement under which a life insurance policy’s premium, cash values, and death benefit are split between two parties—usually a corporation and a key employee or executive. Under such an arrangement an employer may own the policy and pay the premiums and give a key employee or executive the right to name the recipient of the death benefit.

***

***

Several factors will affect the cost and availability of life insurance, including age, health, and the type and amount of insurance purchased. Life insurance policies have expenses, including mortality and other charges. If a policy is surrendered prematurely, the policy holder also may pay surrender charges and have income tax implications. You should consider determining whether you are insurable before implementing a strategy involving life insurance.

Any guarantees associated with a policy are dependent on the ability of the issuing insurance company to continue making claim payments.

“Malta has quietly leveraged the rising tide of the financial transparency imperative to attract hedge funds.“

There was a time when the quaint island sought to play on the traditional terrain, offering anonymity and a “laissez-faire regulatory regime,” not to mention very low taxes, as in no capital gains taxes and no taxes on dividends; all while English speaking and USD currency denominated.

***

***

While many leading domiciles for offshore hedge funds remain in the Caribbean – notably the Cayman Islands, the British Virgin Islands, Bermuda, and the Bahamas – the island of Malta is drawing attention, especially from European funds.

Health actuaries analyze potential risks, profits and trends that will affect their employers, which are often in the health insurance, government health services and medical provider industries. They advise companies on issuing policies to consumers based on risks, calculated premiums and upcoming changes in health-care costs.

It’s common for an actuary to have a bachelor’s degree or higher in actuary studies, mathematics or statistics. Coursework on medical terminology and hierarchy of the medical field is also beneficial. In addition to academic education, certification is also necessary to reach “professional status,” which is required by most employers.

***

***

The professional organization, Society of Actuaries, certifies actuaries in the health and medical field. Their statistical work is commonly done with predictive tables, probability tables and life tables that are created on customized statistical analysis software such as Stata or XLSTAT.

The actuary field as a whole is growing faster than other fields, according to the Bureau of Labor Statistics [BLS]. In 2020, it expanded by 27 percent. The average annual salary for an actuary in 2010 was $87,650. More specifically, in the health insurance field, the salary was slightly higher at $91,000.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com

Posted on March 16, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

DEFINITION

***

***

According to Wikipedia, a tontine (/ˈtɒntaɪn, -iːn, ˌtɒnˈtiːn/) is an investment linked to a living person which provides an income for as long as that person is alive. Such schemes originated as plans for governments to raise capital in the 17th century and became relatively widespread in the 18th and 19th centuries.

Tontines enable subscribers to share the risk of living a long life by combining features of a group annuity with a kind of mortality lottery. Each subscriber pays a sum into a trust and thereafter receives a periodical payout. As members die, their payout entitlements devolve to the other participants, and so the value of each continuing payout increases. On the death of the final member, the trust scheme is usually wound up.

Tontines are still common in France. They can be issued by European insurers under the Directive 2002/83/EC of the European Parliament. The Pan-European Pension Regulation passed by the European Commission in 2019 also contains provisions that specifically permit next-generation pension products that abide by the “tontine principle” to be offered in the 27 EU member states.

Questionable practices by U.S. life insurers in 1906 led to the Armstrong Investigation in the United States restricting some forms of tontines. Nevertheless, in March 2017, The New York Times reported that tontines were getting fresh consideration as a way for people to get steady retirement income.

According to Patricia Salber MD [personal communication], there are a number of reasons why direct patient access to laboratory medical results is a good idea:

Between 8 and 26% of abnormal test results, including those suspicious for cancer, are not followed up in a timely manner. Direct access could help reduce the number of times this occurs

Self-management, particularly of chronic illness has known benefits. Just like the QS people, many folks with chronic illness obtain and manage to self-acquired lab results every day via gluco-meters, home pulmonary function tests, blood pressure measurements, and so forth. Direct access to laboratory-acquired data, one could argue is a continuation of that personal responsibility

Patients want to be notified about their results in what they perceive as a timely fashion. In one study, patients who received direct notification of their bone density tests results were more likely to perceive they had timely notification compared to usual care even though there was no measurable effect on actual treatment received after three months

Being more responsible for test results could encourage consumers to try to learn more about the meaning of the test results, conceivably increasing their health literacy.

But, the arguments against direct access discussed include the following:

Patients prefer their physicians contact them directly when they have abnormal test results, although the major studies published in 2005 and 2009, preceded the extraordinary use of the internet to access health information that exists today.

There is concern over whether patients will know what to do when they receive the results – will they make erroneous interpretations or fail to contact their docs? This could be, but the intent of the proposed rule is shared access to the results. We suspect if the rule become law, docs will develop better notification mechanisms so that they reach the patient before the patient directly accesses the results or lab companies will design better lab test notifications with easy-to-understand interpretations or a whole new industry will appear that can provide instantly available individualized lab interpretation…or maybe all three of these would happen and that would be a very good thing.

Unknown impact of dual notification (doctors and patients) of lab test results on physician behavior…would docs simply shift responsibility for initiating follow-up care from themselves to their patients?

Would direct access of life-changing lab tests, such as HIV or malignancy, lead to unnecessary patient anxiety – or worse? (Conversely, is there less anxiety, desperation, or suicidal ideation if the bad news is delivered face to face?

Individuals likely may contact their physicians immediately after getting the lab results asking for a telephonic or face-to-face interpretation … it is not known how this would impact physician workload and/or potential for reimbursement [personal communication, Richard Hudson DO, Atlanta, GA].

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com

Posted on March 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters and IRS

***

***

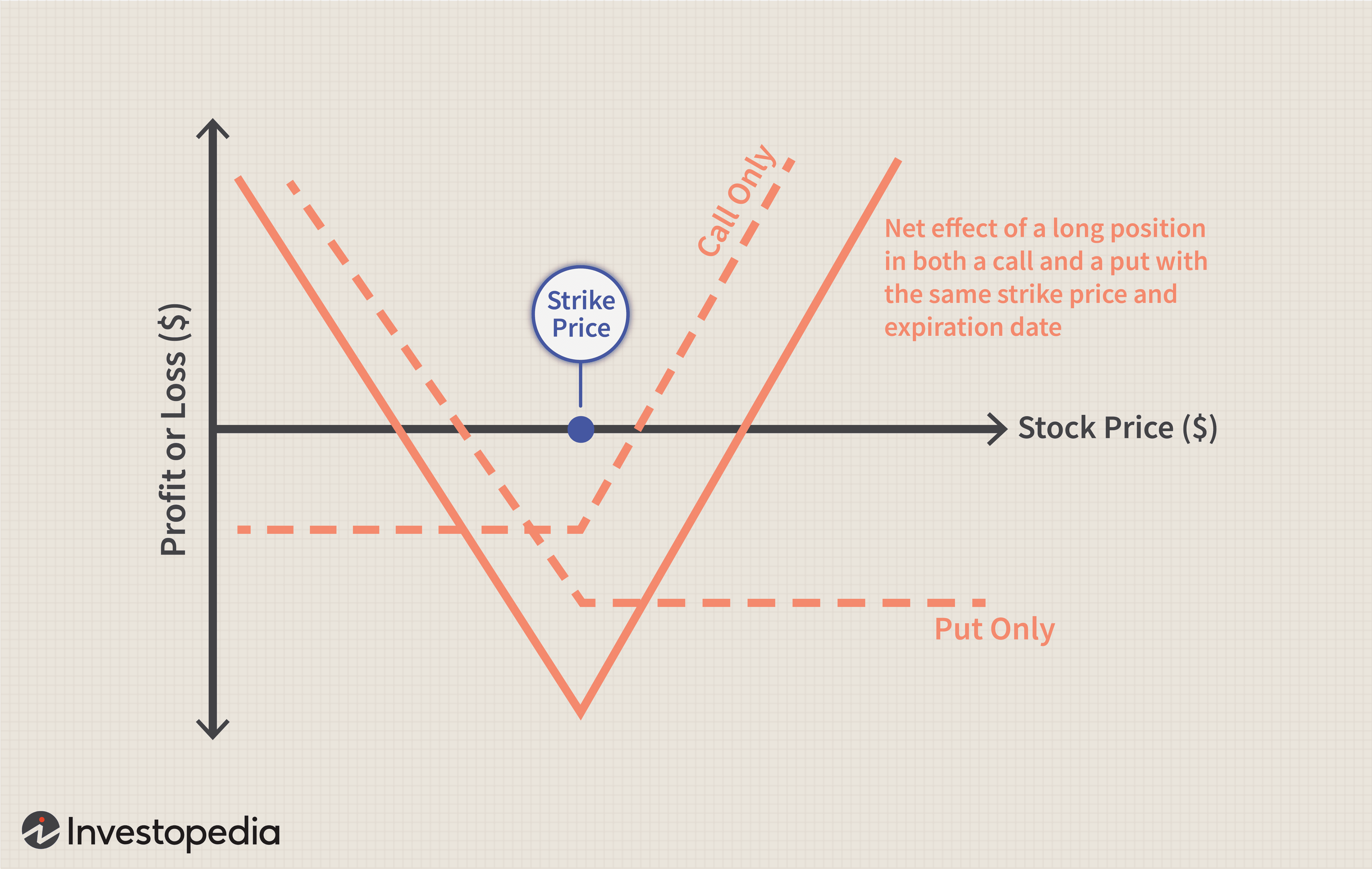

Straddles: A straddle is any set of offsetting positions on personal property. For example, a straddle may consist of a purchased option to buy and a purchased option to sell on the same number of shares of the security, with the same exercise price and period.

Personal property.

This is any actively traded property. It includes stock options and contracts to buy stock but generally does not include stock.

Straddle rules for stock.

Although stock is generally excluded from the definition of personal property when applying the straddle rules, it is included in the following two situations.

The stock is of a type that is actively traded, and at least one of the offsetting positions is a position on that stock or substantially similar or related property.

The stock is in a corporation formed or availed of to take positions in personal property that offset positions taken by any shareholder.

Note

For positions established before October 22, 2004, condition 1 above does not apply. Instead, personal property includes stock if condition 2 above applies or the stock was part of a straddle in which at least one of the offsetting positions was:

An option to buy or sell the stock or substantially identical stock or securities,

A securities futures contract on the stock or substantially identical stock or securities, or

A position on substantially similar or related property (other than stock).

Position

A position is an interest in personal property. A position can be a forward or futures contract or an option.

An interest in a loan denominated in a foreign currency is treated as a position in that currency. For the straddle rules, foreign currency for which there is an active inter bank market is considered to be actively traded personal property.

Offsetting position

This is a position that substantially reduces any risk of loss you may have from holding another position. However, if a position is part of a straddle that is not an identified straddle, do not treat it as offsetting to a position that is part of an identified straddle.

Presumed offsetting positions

Two or more positions will be presumed to be offsetting if:

The positions are established in the same personal property (or in a contract for this property), and the value of one or more positions varies inversely with the value of one or more of the other positions;

The positions are in the same personal property, even if this property is in a substantially changed form, and the positions’ values vary inversely as described in the first condition;

The positions are in debt instruments with a similar maturity, and the positions’ values vary inversely as described in the first condition;

The positions are sold or marketed as offsetting positions, whether or not the positions are called a straddle, spread, butterfly, or any similar name; or

The aggregate margin requirement for the positions is lower than the sum of the margin requirements for each position if held separately.

Related persons

To determine if two or more positions are offsetting, you will be treated as holding any position your spouse holds during the same period. If you take into account part or all of the gain or loss for a position held by a flow-through entity, such as a partnership or trust, you are also considered to hold that position.

RISK MANAGEMENT, LIABILITY INSURANCE AND ASSET PROTECTION ABBREVIATIONS

[Glossary of Important Acronyms]

Much has been written and much has been opined on the topic of medical risk management, insurance, asset protection and professional liability for physicians and healthcare providers in this textbook; and elsewhere.

But occasionally, we all still get lost in a wide array of abbreviations, acronyms, and initialisms that are constantly changing in this ecosystem.

And so, this glossary serves as a ready reference for those who want to know about these medical risk management definitions in a quick and ready fashion.

Acronyms and Abbreviations

AAASC American Association of Ambulatory Surgery Centers

AAHP American Association of Health Plans

ABN advance beneficiary notice

ABQAUR American Board of Quality Assurance and Utilization Review

ACE acute care episode

ACHCE American College of Health Care Executives

ACS American College of Surgeons

ADA Americans with Disabilities Act

ADC average daily census

ADL activities of daily living

ADT Admission/Discharge/Transfer

AHA American Hospital Association

AHIMA American Health Information Management Association

AHRQ Agency for Healthcare Research and Quality

AI average inventory

AIMR Association for Investment Management and Research

AIR assumed interest rate

ALE annualized loss expectancy

ALF assisted living facility

ALOS average length of stay

AMA American Medical Association

AMBAC AMBAC Indemnity Corporation

AMGA American Medical Group Association

ANSI American National Standards Institute

AP accounts payable

APA American Psychiatric Association

APC ambulatory payment classification

APG ambulatory payment group

APR annual percentage rate

AR accounts receivable

ASA American Society of Appraisers

ASC ambulatory surgery centers; also Accredited Standards Committee

ASHA American Surgical Hospital Association

ASO administrative services only

ASTC ancillary service technical component

ATM asynchronous transfer mode

AVG ambulatory visit group

BANTA best alternative to negotiated agreement

BBA Balanced Budget Act of 1997

BBRA Balanced Budget Refinement Act [1999]

BCP business continuity planning

BEA break-even analysis

BEP break-even point

BIPA Benefits Improvement and Protection Act [2000]

BLS Bureau of Labor Statistics

BPD border protection device

BS balance sheet

BSA Bank Secrecy Act

BVS business valuation standard

CA certificate authority

CAC Carrier Advisory Committee

CAS cost accounting standards

CASB Cost Accounting Standards Board

CC common criteria [for IT Security Evaluation —ISO/IEC 15408]; complication or comorbidity [for MS-DRGs]

CCA certified cost accountant

CCC cash conversion cycle

CCEVS common criteria evaluation and validation scheme

CCHIT Certification Commission for Healthcare Information Technology

CCU critical care unit

CDC Centers for Disease Control and Prevention

CDH consumer-directed healthcare

CDHP consumer-directed healthcare plan

CDPM Clinical Data Project Manager

CDSS clinical decision support system

CEO Chief Executive Officer

CF conversion factor

CFA Chartered Financial Analyst

CFO Chief Financial Officer

CFR Code of Federal Regulations

CHAMP Children’s Health and Medicare Protection Act of 2007

CHAMPUS Civilian Health and Medical Program of the Uniformed Services

CHE Certified Healthcare Executive

CHIPS Center for Healthcare Industry Performance Studies

CIA Corporate Integrity Agreement

CIO Chief Information Officer

CIP Customer Identification Program

CIS computer information systems

CLIA Clinical Laboratory Improvement Act

CLT capitation liability theory

CME continuing medical education

CMI case mix index

CMIO Chief Medical Information Officer

CMIS contribution margin income statement

CMN Certificate of Medical Necessity

CMP Certified Medical Planner ™

CMS Centers for Medicare and Medicaid Services [formerly HCFA]

COD cash on delivery

COGME Council of Graduate Medical Education

COH cash on hand

COLA cost of living allowance

CON Certificate of Need

COO Chief Operating Officer

COSO Committee of Sponsoring Organizations

COTS commercial off-the-shelf

CPHQ Certified Physician in Healthcare Quality

CPIM Certificate in Production and Inventory Management

CPI-U Consumer Price Index—urban

CPM critical (clinical) path method

CPOE computerized physician order entry [system]

CPR computer-based patient record

CPT current procedural terminology

CQI continuous quality improvement

CRL Certification Revocation List

CRM customer relationship management

CRVS California Relative Value Studies

CSO Chief Security Officer

CT scan computed tomography scan [also called CAT scan]

CUSIP Committee on Uniform Security Identification Procedures

Candid CIO: Will Weider, CIO of Ministry Health Care and Affinity Health System, offers his perspectives on administration issues in this blog.

Christina’s Considerations: Christina Thielst is a hospital and healthcare administrator and entrepreneur with a deep desire for continually improving the health of the community being served. This is her blog.

Healing Hospitals — Formerly Ask a Hospital President: F. Nicholas “Nick” Jacobs has more than 20 years experience in hospital management, with an acknowledged reputation for innovation and consumer-centered leadership.

Hospital Impact: Part of the Fierce network of health sites, this site is becoming popular among healthcare administrators for its news updates, tips and opinions on health care matters.

Leading the Way to Medical Excellence: the president of McLeod Health non-profit institutions provides weekly insights into his facilities and health care in general.

Let’s Talk Health Care: Bruce Bullen, Interim Chief Executive Officer at Harvard Pilgrim in Massachusetts, provides and open and ongoing conversation about health care administration.

Life as a Healthcare CIO: Dr. John Halamka records his experiences with infrastructure, applications, policies, management, and governance as he supports 3,000 doctors, 18,000 faculty and about three million patients.

Managed Care Matters: Joe Paduda shares his knowledge on managed care for group health, health policy, health research, and medical news for insurers, employers, and healthcare providers.

More than Medicine: Tom Quinn, president and CEO of Community General Hospital in Syracuse, New York, began his career as a hospital kitchen worker. His perspective on administration reflects his knowledge on how hospitals work from every angle.

Running a Hospital: A CEO of a large Boston hospital shares thoughts on hospitals, medicine and health care issues.

St. Joseph Medical Center: Chief Executive Officer at St. Joseph Medical Center in Missouri, Mr. Kashman, provides personal insight into administrative matters and general topics.

Todd’s Perspective: Todd Linden, president and CEO of Grinnell Regional Medical Center, offers insights into medical administration and guest bloggers provide insight into various departments.

Wachter’s World: This blog focuses on hospitals, hospitalists, quality, safety, policy and much more from Robert M. Wachter, MD, Professor and Associate Chairman of the Department of Medicine at the University of California, San Francisco.

Legal Matters

Drug and Device Law: This blog contains an attorney’s personal views (and those of several other Dechert attorneys) on topics that arise in the defense of pharmaceutical and medical device product liability litigation.

Drug Injury Watch: Learn more about drug injury lawsuits from an attorney who represents patients and their families.

FDA Law Blog: Hyman, Phelps & McNamara, P.C. is the largest dedicated food and drug law firm in the country. Their knowledge about laws and regulations governing drugs, medical devices, foods, dietary supplements, and cosmetics is helpful to anyone interested in these topics.

Health Care Law Blog: Bob Coffield’s expertise lies in helping businesses and health care providers weave through a variety of state and federal health care regulations and assisting them in business transactions.

Health Plan Law: This site contains information about group health plans, claims administration and related ERISA fiduciary issues. This site also contains tutorials.

HealthBlawg: this is David Harlow’s popular health care law blog, offering expert insights and easy-to-understand analysis.

Healthcare Law Blog: Holland & Hart’s healthcare practice provides insight into this arena, including HIPAA, Stark law, the Anti-kickback Statute and more.

HIPAA Blog: Join in on this discussion of medical privacy issues often buried in “political arcana.”

HIPAA, HiTech & HIT: This updated blog brings insight into legal issues, developments and other pertinent information that relates to the creation, use and exchange of electronic health records.

HIT Blawg: This blog is focused on national health information technology legal trends and current news on this topic.

Home Care Law Blog: Learn more about legal and policy issues in the home health care, private duty and hospice industries from Gilliland & Markette LLP.

Med Law Blog: This law blog focuses on topics that range from compliance to contracts and from employee benefits to HIPAA and HIT.

Physician Law: This blog provides and easy way to stay on top of current news, updates and useful tips relating to legal issues that affect physicians and non-institutional providers.

eHealth and Health IT

Chilmark Research: This blog provides perspectives on key IT trends in the healthcare sector.