BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on May 1, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

May Day is a European festival of ancient origins marking the beginning of summer, usually celebrated on 1 May, around halfway between the Northern Hemisphere’s Spring equinox and June solstice. Festivities may also be held the night before, known as May Eve. Traditions often include gathering wildflowers and green branches, weaving floral garlands, crowning a May Queen and setting up a Maypole, May Tree or May Bush, around which people dance. Bonfires are also part of the festival in some regions.

***

Here’s where the major benchmarks ended:

The S&P 500 index fell 80.48 points (1.6%) to 5,035.69; the Dow Jones Industrial Average® ($DJI) lost 570.17 points (1.5%) to 37,815.92, down 5% for the month; the NASDAQ Composite declined 325.26 points (2.0%) to 15,657.82.

The 10-year Treasury note yield jumped more than 7 basis points to 4.682%.

The CBOE Volatility Index® (VIX) rose 0.98 to 15.65.

Energy shares were among the weakest performers Tuesday, behind a drop in WTI Crude Oil (/CL) futures, which fell a third consecutive session and briefly dropped under $81 per barrel. The Philadelphia Oil Service Index (OSX) tumbled 4.5% to a seven-week low. The small-cap Russell 2000® Index (RUT) shed 2.1% and ended with a loss of 7.1% for the month.

But, it was a better day for Mounjaro maker Eli Lilly, which climbed nearly 6% after its popular weight loss drugs pushed it to raise its 2024 forecast.

A class-action complaint was filed against MultiPlan and major payers like UnitedHealth Group and CVS Health’s Aetna, arguing payers’ claims data was being used to generate low reimbursement rates.

Posted on April 30, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

It’ll be a big week for hot takes on the US economy, after the Federal Reserve meeting Tuesday and Wednesday and the April jobs report dropping Friday. Because inflation has been sticking around, the FOMC is expected to hold interest rates steady at this meeting and for the foreseeable future. On the jobs front, economists are projecting another strong month for employment growth.

In 2022, with bipartisan support, Congress passed the CHIPS and Science Act, an ambitious plan to juice domestic manufacturing of a product vital to national security: semiconductors. Two years later, the government has doled out more than half of the CHIPS Act’s $39 billion in incentives. According to the Financial Times …

Chip companies and their suppliers have announced US investments of $327 billion over the next 10 years, per the Semiconductor Industry Association.

Construction of manufacturing facilities for computing and electronics devices has jumped 15x, government data shows.

By 2030, the US will likely produce around 20% of the world’s most advanced chips, according to USCommerce Secretary Gina Raimondo. Right now, it’s making 0%.

The proposed factories are massive and could transform regional economies. Micron, which received $6.1 billion in federal grants last week, plans to invest $100 billion in a manufacturing campus near Syracuse.

The S&P 500® index (SPX) rose 16.21 points (0.3%) to 5,116.17, its highest close in over two weeks; the Dow Jones Industrial Average® ($DJI) gained 146.43 points (0.4%) to 38,386.09, the NASDAQ Composite® ($COMP) advanced 55.18 points (0.4%) to 15,983.08.

The 10-year Treasury note yield (TNX) fell more than 5 basis points to 4.616%.

The CBOE Volatility Index® (VIX) declined 0.36 to 14.67.

Communication services shares were among the market’s weakest performers Monday, reversing last Friday’s upswing as Alphabet (GOOGL) dropped more than 3% and Meta Platforms (META) lost 2.4%. Banks and retailers were also soft. The Philadelphia Semiconductor Index (SOX) climbed for the sixth-straight day and ended near a three-week high even though its biggest member, Nvidia (NVDA), ended little changed.

In other markets, the U.S. Dollar Index ($DXY) faded from early gains but is still up about 1% in April, driven by expectations domestic rates will remain high. “The U.S. dollar’s strength continues to reflect the relative strength of the economy and the wide interest rate differentials between the United States and other major developed markets,” Schwab Center for Financial Research analysts said in a report.

Despite last week’s strength, the S&P 500 index and the NASAQ Composite are still down 2.6% and 2.4%, respectively, for April and on track to break five-month winning streaks.

Humana expects to exit Medicare Advantage (MA) markets in 2025, company executives told investors. The company reported its first quarter earnings April 24th. Humana posted $741 million in net income in the first quarter of 2024, beating investor expectations, but pulled its 2025 earnings guidance.

Posted on April 29, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

Dr. David Edward Marcinko MBAMEd CMP

***

National Supply Chain Management Day is celebrated on April 29th every year to mark the binding importance of the global supply chain in the everyday lives of people. National Supply Chain Day brings all stakeholders together to share recent developments in the field. Introduced in 2020 by a Georgia-based packaging outlet, this holiday aims to raise awareness about the way a supply chain affects all of us, and how we can be better partners and benefactors of the global supply chain management system.

***

***

One of the most iconic symbols of the COVID economy was the epic backlog of container ships waiting to dock at the ports of Los Angeles and Long Beach. At one point this year, that backup was longer than the line at Trader Joe’s on a Saturday, stretching 109 ships deep and almost 60 miles from the coast.

But now, the shipping situation is almost back to normal. As of last week, the number of ships waiting to drop off their goods stood at just four, according to the WSJ. Plus, the cost of sending a 40-foot container from Shanghai to LA has plummeted from its peak of more than $12,000 to almost $2,000, nearing its pre-COVID average.

The fact that goods are once again flowing smoothly through US ports is a hopeful sign that inflation, which was instigated in part by supply chain snarls, could start to abate.

Modern Portfolio Theory approaches investing by examining the complete market and the full economy. MPT places a great emphasis on the correlation between investments.

DEFINITION:

Correlation is a measure of how frequently one event tends to happen when another event happens. High positive correlation means two events usually happen together – high SAT scores and getting through college for instance. High negative correlation means two events tend not to happen together – high SATs and a poor grade record.

No correlation means the two events are independent of one another. In statistical terms two events that are perfectly correlated have a “correlation coefficient” of 1; two events that are perfectly negatively correlated have a correlation coefficient of -1; and two events that have zero correlation have a coefficient of 0.

Correlation has been used over the past twenty years by institutions and financial advisors to assemble portfolios of moderate risk. In calculating correlation, a statistician would examine the possibility of two events happening together, namely:

If the probability of A happening is 1/X;

And the probability of B happening is 1/Y; then

The probability of A and B happening together is (1/X) times (1/Y), or 1/(X times Y).

There are several laws of correlation including;

Combining assets with a perfect positive correlation offers no reduction in portfolio risk. These two assets will simply move in tandem with each other.

Combining assets with zero correlation (statistically independent) reduces the risk of the portfolio. If more assets with uncorrelated returns are added to the portfolio, significant risk reduction can be achieved.

Combing assets with a perfect negative correlation could eliminate risk entirely. This is the principle with “hedging strategies”. These strategies are discussed later in the book.

In the real world, negative correlations are very rare

Most assets maintain a positive correlation with each other. The goal of a prudent investor is to assemble a portfolio that contains uncorrelated assets. When a portfolio contains assets that possess low correlations, the upward movement of one asset class will help offset the downward movement of another. This is especially important when economic and market conditions change.

As a result, including assets in your portfolio that are not highly correlated will reduce the overall volatility (as measured by standard deviation) and may also increase long-term investment returns. This is the primary argument for including dissimilar asset classes in your portfolio. Keep in mind that this type of diversification does not guarantee you will avoid a loss. It simply minimizes the chance of loss.

In the table provided by Ibbotson, the average correlation between the five major asset classes is displayed. The lowest correlation is between the U.S. Treasury Bonds and the EAFE (international stocks). The highest correlation is between the S&P 500 and the EAFE; 0.77 or 77 percent. This signifies a prominent level of correlation that has grown even larger during this decade. Low correlations within the table appear most with U.S. Treasury Bills.

Some of the pioneers of behavioral finance are Drs. Kahneman, Twersky and Thaler. This short introduction to the subject is based on John Nofsinger’s little book entitled “Psychology of Investing” an excellent quick read for all medical professionals or anyone who is interested in learning more about behavioral finance.

Rational Decisions?

Much of modern finance is built on the assumption that investors “make rational decisions” and “are unbiased in their predictions about the future”, however this is not always the case.

Cognitive errors come from (1) prospect theory (people feel good/bad about gain/loss of $500, but not twice as good/bad about a gain/loss of $1,000; they feel worse about a $500 loss than feel good about a $500 gain); (2) mental accounting (meaning that people tend to create separate buckets which they examine individually), (3) Self-deception (e.g. overconfidence), (4) heuristic simplification (shortcuts) and (4) mood can affect ability to reach a logical conclusion.

John Nofsinger’s Book

The following are some of the major chapter headings in Nofsinger’s book, and represent some of the key behavioral finance concepts.

Overconfidence leads to: (1) excessive trading (which in turn results in lower returns due to costs incurred), (2) underestimation of risk (portfolios of decreasing risk were found for single men, married men, married women, and single women), (3) illusion of knowledge (you can get a lot more data nowadays on the internet) and (4) illusion of control (on-line trading).

Pride and Regret leads to: (1) disposition effect (not only selling winners and holding on to the losers, but selling winners too soon- confirming how smart I was, and losers to late- not admitting a bad call, even though selling losers increases one’s wealth due to the tax benefits), (2) reference points (the point from where one measures gains or losses is not necessarily the purchase price, but may perhaps be the most recent 52 week high and it is most likely changing continuously- clearly such a reference point will affect investor’s judgment by perhaps holding on to “loser” too long when in fact it was a winner.)

Considering the Past in decisions about the future, when future outcomes are independent of the past lead to a whole slew of more bad decisions, such as: (1) house money effect (willing to increase the level of risk taken after recent winnings- i.e. playing with house’s money), (2) risk aversion or snake-bite effect (becoming more risk averse after losing money), (3) trying to break-even (at times people will increase their willing to take higher risk to try to recover their losses- e.g. double or nothing), (4) endowment or status quo effect (often people are only prepared to sell something they own for more than they would be willing to buy it- i.e. for investments people tend to do nothing, just hold on to investments they already have) (5) memory and decision making ( decisions are affected by how long ago did the pain/pleasure occur or what was the sequence of pain and pleasure), (6) cognitive dissonance (people avoid important decisions or ignore negative information because of pain associated with circumstances).

Mental Accounting is the act of bucketizing investments and then reviewing the performance of the individual buckets separately (e.g. investing at low savings rate while paying high credit card interest rates).

Examples of mental accounting are: (1) matching costs to benefits (wanting to pay for vacation before taking it and getting paid for work after it was done, even though from perspective of time value of money the opposite should be preferred0, (2) aversion to debt (don’t like long-term debt for short-term benefit), (3) sunk-cost effect (illogically considering non-recoverable costs when making forward-going decisions). In investing, treating buckets separately and ignoring interaction (correlations) induces people not to sell losers (even though they get tax benefits), prevent them from investing in the stock market because it is too risky in isolation (however much less so when looked at as part of the complete portfolio including other asset classes and labor income and occupied real estate), thus they “do not maximize the return for a given level of risk taken).

In building portfolios, assets included should not be chosen on basis of risk and return only, but also correlation; even otherwise well educated individuals make the mistake of assuming that adding a risky asset to a portfolio will increase the overall risk, when in fact the opposite will occur depending on the correlation of the asset to be added with the portfolio (i.e. people misjudge or disregard interactions between buckets, which are key determinants of risk).

This can lead to: (1) building behavioral portfolios (i.e. safety, income, get rich, etc type sub-portfolios, resulting in goal diversification rather than asset diversification), (2) naïve diversification (when aiming for 50:50 stock:bond allocation implementing this as 50:50 in both tax-deferred (401(k)/RRSP) accounts and taxable accounts, rather than placing the bonds in the tax-deferred and stocks in taxable accounts respectively for tax advantages), (3) naïve diversification in retirement accounts (if five investment options are offered then investing 1/5th in each, thus getting an inappropriate level of diversification or no diversification depending on the available choices; or being too heavily invested in one’s employer’s stock).

Representativenes may lead investors to confusing a good company with a good investment (good company may already be overpriced in the market; extrapolating past returns or momentum investing), and familiarity to over-investment in one’s own employer (perhaps inappropriate as when stock tanks one’s job may also be at risk) or industry or country thus not having a properly diversified portfolio.

Emotions can affect investment decisions: mood/feelings/optimism will affect decision to buy or sell risky or conservative assets, even though the mood resulted from matters unrelated to investment. Social interactions such as friends/coworkers/clubs and the media (e.g. CNBC) can lead to herding effects like over (under) valuation.

Financial Strategies

Nofsinger finishes with a final chapter which includes strategies for:

(i) beating the biases: (1) Understand the biases, (2) define your investment objectives, (3) have quantitative investment criteria, i.e. understand why you are buying a specific investor (or even better invest in a passive fashion), (4) diversify among asset classes and within asset classes (and don’t over invest in your employer’s stock), and (5) control your investment environment (check on stock monthly, trade only monthly and review progress toward goals annually).

(ii) using biases for the good: (1) set new employee defaults for retirement plans to being enrolled, (2) get employees to commit some percent of future raises to automatically go toward retirement (save-more-tomorrow).

Assessment

Buy the book (you can get used copies through Amazon). As indicated it is a quick read and occasionally you may even want to re-read it to insure you avoid the biases or use them for the good. Also, the book has long list of references for those inclined to delve into the subject more deeply.

You might even ask “How does all this Behavioral Finance coexist with Efficient Market theory?” and that’s a great question that I’ll leave for another time.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on April 27, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Here’s where the major stock market benchmarks ended:

The S&P 500 index gained 51.54 points (1.0%) to 5,099.96, up 2.7% for the week; the Dow Jones Industrial Average® ($DJI) increased 153.86 points (0.4%) to 38,239.66, up 0.7% for the week; the NASDAQ Composite jumped 316.14 points (2.0%) to 15,927.90, up 4.2% for the week.

The 10-year Treasury note yield (TNX) lost about 4 basis points to 4.665%.

The CBOE Volatility Index® (VIX) fell 0.34 to 15.03.

Alphabet’s rally helped communication services reverse Thursday’s downturn, which was driven by disappointing quarterly results from Meta Platforms (META). The S&P 500 Communication Services index ($SP500#50) surged 4.7% Friday and ended the week with a 2.7% gain. Semiconductor shares were also strong, led by a 6% gain in Nvidia (NVDA). The Russell 2000® Index (RUT) added 1.1% Friday and posted a 2.8% advance for the week.

In other markets, WTI Crude Oil (/CL) futures rose slightly Friday, ending around $83.65 per barrel and shutting down a three-week losing streak.

Midi Health, a health clinic geared toward women in midlife, raised $60 million in Series B funding to expand its network to 150 clinicians by the end of the year, among other efforts. (MobiHealthNews)

“We’re fooling ourselves if we think that’s cheap or can be done less expensively.”—Carmela Coyle, president and CEO of the California Hospital Association, on hospital finances and cutting costs (AP)

The federal government implemented new staffing rules to improve patient care, but most nursing homes won’t be able to meet that demand. (KFF Health News/NPR)

The Biden administration is considering a change that would downgrade cannabis from a Schedule I drug to a Schedule III drug this year. The reclassification would have major effects on the business of cannabis, but for that to happen, the Drug Enforcement Agency needs proof of medical effectiveness.

Posted on April 26, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

New GDP numbers out yesterday show a worrying combo of stubborn inflation + waning growth that dampens hopes for a potential interest rate cut. Per the latest data from the Bureau of Economic Analysis, the first quarter of 2024 was a confounding one:

GDP increased at a 1.6% annualized rate, far below projections of 2.4% and notably down from 3.4% at the end of 2023.

While slow growth would typically signal that the Fed could cut rates, another metric complicates matters: Consumer prices (excluding volatile categories), a solid indicator of inflation, shot up to a much higher than anticipated 3.7%.

***

Meta reported record Q1 revenue yesterday, but it was overshadowed by the billions of dollars the company is spending in its efforts to win the Artificial Intelligence race and make the Metaverse happen. Investors were unhappy with the company’s forecast that its spending will rise by $10 billion dollars to support Artificial Intelligence development, sending Meta’s stock price down 15% after hours.

Here’s where the major benchmarks ended:

The S&P 500 index fell 23.21 points (0.5%) to 5,048.42; the Dow Jones Industrial Average lost 375.12 points (1.0%) to 38,085.80; the NASDAQ Composite® ($COMP) shed 100.99 points (0.6%) to 15,611.76.

The 10-year Treasury note yield (TNX) rose about 5 basis points to 4.704%.

The CBOE Volatility Index® (VIX) fell 0.64 to 15.33.

Communication services shares were the weakest S&P 500 sector Thursday behind the plunge in Meta Platforms. Late Wednesday, the Facebook parent provided lighter-than-expected second-quarter revenue guidance, while CEO Mark Zuckerberg discussed spending in currently unprofitable pursuits such as artificial intelligence (AI) and mixed reality. Meta’s first-quarter earnings and revenue both came above analysts ‘ estimates, however.

Meta’s slump helped send the S&P 500 Communication Services index ($SP500#50) down 4%. Banks were also particularly soft amid concern that persistently high interest rates may compress lender margins. Semiconductor and transportation shares were among the few pockets of strength.

But, Alphabet, Microsoft, and Snap reported Q1 earnings yesterday, and were generally good. Alphabet issued its first-ever dividend and authorized $70 billion in stock buybacks, after it beat Wall Street’s revenue expectations. Microsoft also beat revenue forecasts on the strength of its cloud services. And Snap shares soared after it topped estimates and impressed investors with its 422 million global daily active users. It was a much-needed boost for the sector after Meta spooked the market with how much it’s spending on AI.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

Our Other Print Books and Related Information Sources:

Posted on April 25, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Otherwise known as “National Prescription Drug Take Back Day,” National Drug Take Back Day on April 25th is sponsored by the Drug Enforcement Agency. Its goal is to keep the public aware of the dangers of prescription drug use and misuse. Many Americans don’t know how to safely dispose of the prescription drugs that have been sitting in the medicine cabinet past their prime. Using these expired drugs, or using someone else’s, is dangerous and puts both the public and the environment at risk.

Spotify made money in Q1. According to Morning Brew, the streaming music giant grew its revenue last quarter by 20% to $3.8 billion on a record $180 million in profit, it announced yesterday. The smash report comes after Spotify cut costs last year, which included laying off more than a quarter of its workforce. The company also raised prices in 2023 for the first time in a decade as it further expanded beyond music into audio books and other categories. Spotify shares soared ~11% following the news.

***

Here’s where the major benchmarks ended:

The S&P 500 index® (SPX) rose 1.08 points (0.02%) to 5,071.63; the Dow Jones Industrial Average® ($DJI) fell 42.77 points (0.1%) to 38,460.92; the NASDAQ Composite® ($COMP) added 16.11 points (0.1%) to 15,712.75.

The 10-year Treasury note yield rose more than 4 basis points to 4.644%.

The CBOE Volatility Index® (VIX) rose 0.28 to 15.97.

Transportation shares were among the market’s weakest performers Wednesday behind a drop of more than 10% in Old Dominion Freight Line (ODFL), which reported lighter-than-expected quarterly revenue. The shipper’s nosedive helped send the Dow Jones Transportation Average ($DJT) down 2.3%. Consumer staples, semiconductors, and utilities posted moderate advances. The Dow Jones Utility Index ($DJU) gained for the sixth straight day and ended at a three-and-a-half-month high.

***

The National Association of Realtors’ $418 million settlement over an alleged conspiracy to inflate commissions received preliminary approval yesterday. It’s a new world order: Sellers won’t have to pay buyers’ agents anymore. There’s been talk of a metaphorical death of real estate agents, or a mass extinction; the jury is still out, but RE/MAX cofounder and chairman Dave Liniger doesn’t seem too concerned.

The Labor Department announced it has finalized its Retirement Security Rule, which aims to protect American workers who are saving for retirement and relying on advice from fiduciaries for it. The new rule will update the definition of an investment advice fiduciary under the Employee Retirement Income Security Act and the Internal Revenue Code.

Clinicians don’t always get it right, and their mistakes can be costly: Studies show misdiagnoses lead to roughly 800,000 patient deaths or permanent disabilities each year in the US and cost the healthcare system an estimated $20 billion annually. Cleveland Clinic is using telehealth to try to combat misdiagnoses via its virtual second opinions program, which has saved an average of $8,705 per patient by avoiding unnecessary treatments, according to an analysis released in March.

Posted on April 24, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Stat: 740. That’s how many employees Nike will lay off at its Oregon HQ before the end of June. In February, Nike CEO John Donahoe informed employees of the company’s plan to reduce 2% of its workforce, which would mean around 1,600 employees in total. (USA Today)

Let’s say you leave your job at any time during or after the calendar year you turn 55 (or age 50 if you’re a public safety employee with a government defined-benefit plan). Under a little-known separation-of-service provision, often referred to as the “rule of 55,” you may be able take distributions (though some plans may allow only one lump-sum withdrawal) from your 401(k), 403(b), or other qualified retirement planfree of the usual 10% early-withdrawal penalties. However, be aware that you’ll still owe ordinary income taxes on the amount distributed. This exception applies only to the plan (including any consolidated accounts) that you were contributing to when you separated from service. It does not extend to IRAs.

The S&P 500 index rose 59.95 points (1.2%) to 5,070.55; the Dow Jones Industrial Average gained 263.71 points (0.7%) to 38,503.69; the NASDAQ Composite® ($COMP) surged 245.33 points (1.6%) to 15,696.64.

The 10-year Treasury note yield (TNX) decreased about 2 basis points to 4.602%.

The CBOE Volatility Index® (VIX) fell 1.25 to 15.69.

Similar to Monday, chipmakers were among the market’s strongest areas, carrying the Philadelphia Semiconductor Index (SOX) to a 2.2% advance. Retailers and communication services shares were also strong. The Dow Jones Utility Index ($DJU) gained for the fifth straight day and ended at its highest level in over three months. The Russell 2000® Index (RUT) surged nearly 2%.

Posted on April 23, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The March Consumer Price Index, which the Bureau of Labor Statistics released last week, revealed that core inflation hit 3.8% Year over Year in March, rising for the first time in 12 months. That’s moving in the wrong direction for the Fed, whose goal is to bring inflation down to 2%.

The S&P 500 index rose 43.37 points (0.9%) to 5,010.60; the Dow Jones Industrial Average® ($DJI) gained 253.58 points (0.7%) to 38,239.98; the NASDAQ Composite advanced 169.30 points (1.1%) to 15,451.31.

The 10-year Treasury note yield (TNX) was little changed at 4.617%.

The CBOE Volatility Index® (VIX) fell 1.41 to 16.39.

Chipmaker strength lifted the Philadelphia Semiconductor Index (SOX) up 1.7% Monday, partially reclaiming last week’s 9.2% tumble. Banking shares were also among the strongest sectors, while the Russell 2000® Index (RUT) advanced 1%. WTI crude futures earlier dropped to just a few cents above $82 per barrel, the lowest intraday price since late March.

“Telemedicine has a lot of potential to bridge barriers and make it convenient for people to access healthcare. But it’s limited by lack of tools. Your doctor can’t reach through the computer screen.”—Akshaya Anand, co-founder of Korion Health, on the startup’s efforts to create an electronic stethoscope for clinicians to record heart and lung movement (Maryland Today)

Posted on April 20, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

A group of 15 financial officers representing 13 states issued a warning to Bank of America over its alleged practices of “politicized de-banking” targeting conservatives. In a letter to Bank of America CEO Brian Moynihan, the officials said the bank’s practices threaten its own financial health and reputation with customers while simultaneously harming the U.S. economy and Americans’ civil liberties. They pointed to examples of Bank of America shuttering the accounts belonging to Christian groups and leaders and joining a net-zero climate alliance in addition to its poor viewpoint diversity rating.

Texas and Missouri will soon have about two dozen Walmart health centers, the retail giant announced this month, adding to its 50-site roster. The company plans to open eight clinics in the Houston metro area, 10 sites in the Dallas-Fort Worth area, and four facilities in Kansas City by the end of 2024, Modern Healthcare reported.

Hospitals reported the strongest quarter of mergers and acquisitions since 2020, according to consulting firm Kaufman Hall. Four of the 20 announced transactions in the first quarter of 2024 were “megamergers” and brought in $12 billion in revenue in that time period, per the firm’s analysis. The era of consolidation is here.

The S&P 500 index fell 43.89 points (0.9%) to 4,967.23, down 3% for the week; the Dow Jones Industrial Average gained 211.02 points (0.6%) to 37,986.40, little changed for the week; the NASDAQ Composite lost 319.49 points (2.1%) to 15,282.01, down 5.5% for the week.

The 10-year Treasury note yield (TNX) dropped more than 2 basis points to 4.623%, still up about 10 basis points for the week.

The CBOE Volatility Index® (VIX) rose 0.71 to 18.71.

Nvidia (NVDA) plunged 10% to lead the chip sector lower, sending the Philadelphia Semiconductor Index (SOX) down 4.1% to a two-and-a-half-month low. Communication Services shares were also among the weakest sectors, fueled by Netflix weakness. There were several pockets of strength, however. Banking shares posted firm gains Friday behind stronger-than-expected quarterly results from some regional lenders. Utilities also advanced.

The S&P 500 has fallen 5.5% from a record close March 28, more than halfway to the 10% threshold that’s traditionally viewed as a correction. The NASDAQ Composite is down 7.1% from a record close on April 11th.

Posted on April 19, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

If the practice makes a reasonable effort to collect from a patient who is experiencing financial hardship (e.g., job loss due to COVID-19), providers may be able to offer a discount (e.g., settle for 70% of the amount owed) without violating Stark Law, says Reed Tinsley, CPA, healthcare consultant in Houston, Texas. “But remember that just because even if someone doesn’t have a job, they could still have money,” he adds. “There are a lot of people out there with big savings accounts.”

Source: Lisa A. Eramo, MA, Keith A. Reynolds, Physicians Practice [4/3/24]

23andMe cofounder and CEO Anne Wojcicki wants to take the once-hot DNA company private. 23andMe said a Special Committee would evaluate the proposal in light of other options. The company’s valuation has tumbled since its stock market debut in 2021. The struggling DNA company once valued in the billions — was essentially worthless as of Wednesday.

But,shares soared Thursday less than three years after it began selling shares. Wojcicki told board members she is proposing to acquire the company in a potential go-private transaction, according to a filing with the Securities and Exchange Commission.

The S&P 500 index fell 11.09 points (0.2%) to 5,011.12; the Dow Jones Industrial Average® ($DJI) rose 22.07 points (0.1%) to 37,775.38; the NASDAQ Composite lost 81.88 points (0.5%) to 15,601.50.

The 10-year Treasury note yield (TNX) gained almost 5 basis points to 4.633%.

The CBOE Volatility Index® (VIX) dropped 0.22 to 17.99.

Weakness in chip maker shares pushed the Philadelphia Semiconductor Index (SOX) down 1.7% to a two-month low. Biotechnology and consumer discretionary shares were also among the weakest sectors. Energy companies eroded as WTI Crude Oil (/CL) futures dropped for a third straight trading day and closed at a three-week low.

The S&P 500 is on track for its third consecutive weekly decline, its weakest stretch since September, while the NASDAQ Composite appears headed for a fourth straight weekly slide.

Posted on April 18, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Pharmacy Benefits Managers often need more transparency regarding their pricing structures and the rebates they negotiate with drug manufacturers. Some argue that PBMs might receive hidden fees or undisclosed profits from drug manufacturers in exchange for favorable positioning on their formularies (lists of covered medications). This can be seen as a form of kickback, which is illegal.

Lawmakers Express Fury Toward UnitedHealth in Change Attack Hearing on the fallout surrounding the unprecedented cyberattack on Change Healthcare in late February. Individuals representing the American Hospital Association, private cybersecurity groups and providers testified before members of the House Energy and Commerce Committee on April 16th to discuss the healthcare industry’s response to the attack and how the federal government should act.

In March, the cyber criminal organization received $22 million in bitcoins, though UnitedHealth Group has not addressed whether the company paid the ransom. On April 15th, ransomware group RansomHub posted files on its dark web leak site comprising of personal and protected health information on patients whose data was taken in the hack. The files also include contracts and agreements between Change and its clients, marking the first time hackers have posted data from the attack.

Stocks started the day strong yesterday but ended up slumping before the market closed as investors pulled back on tech stocks, including Nvidia. United Airlines took off after releasing a strong forecast for the year despite saying it took a $200 million hit because of Boeing’s troubles.

Here’s where the major benchmarks ended:

The S&P 500 index lost 29.20 points (0.6%) to 5,022.21; the Dow Jones Industrial Average declined 45.66 points (0.1%) to 37,753.31; the NASDAQ Composite dropped 181.88 points (1.2%) to 15,683.37.

The 10-year Treasury note yield (TNX) decreased more than 7 basis points to 4.585%.

The CBOE Volatility Index® (VIX) fell 0.20 to 18.20.

ASML’s slump helped send the Philadelphia Semiconductor Index (SOX) down 3.3% to its lowest level since late February. Transportation shares were also under pressure after trucking company J.B. Hunt Transport Services (JBHT) dropped 8.1% in the wake of disappointing quarterly numbers. Energy shares slipped as WTI Crude Oil (/CL) futures fell 3% to a three-week low.

Did you know that desperate doctors of all ages are turning to knowledgeable financial advisors and medical management consultants for help? Symbiotically too, generalist advisors are finding that the mutual need for knowledge and extreme niche synergy is obvious.

***

***

But, there was no established curriculum or educational program; no corpus of knowledge or codifying terms-of-art; no academic gravitas or fiduciary accountability; and certainly no identifying professional designation that demonstrated integrated subject matter expertise for the increasingly unique healthcare focused financial advisory niche … Until Now!

So, if you are looking to supplement your knowledge, income and designations; and find other qualified professionals you may want to consider the CMP® program.

Enter the Certified Medical Planner™ charter professional designation. And, CMPs™ are FIDUCIARIES, 24/7.

Channel Surfing the ME-P

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

***

***

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

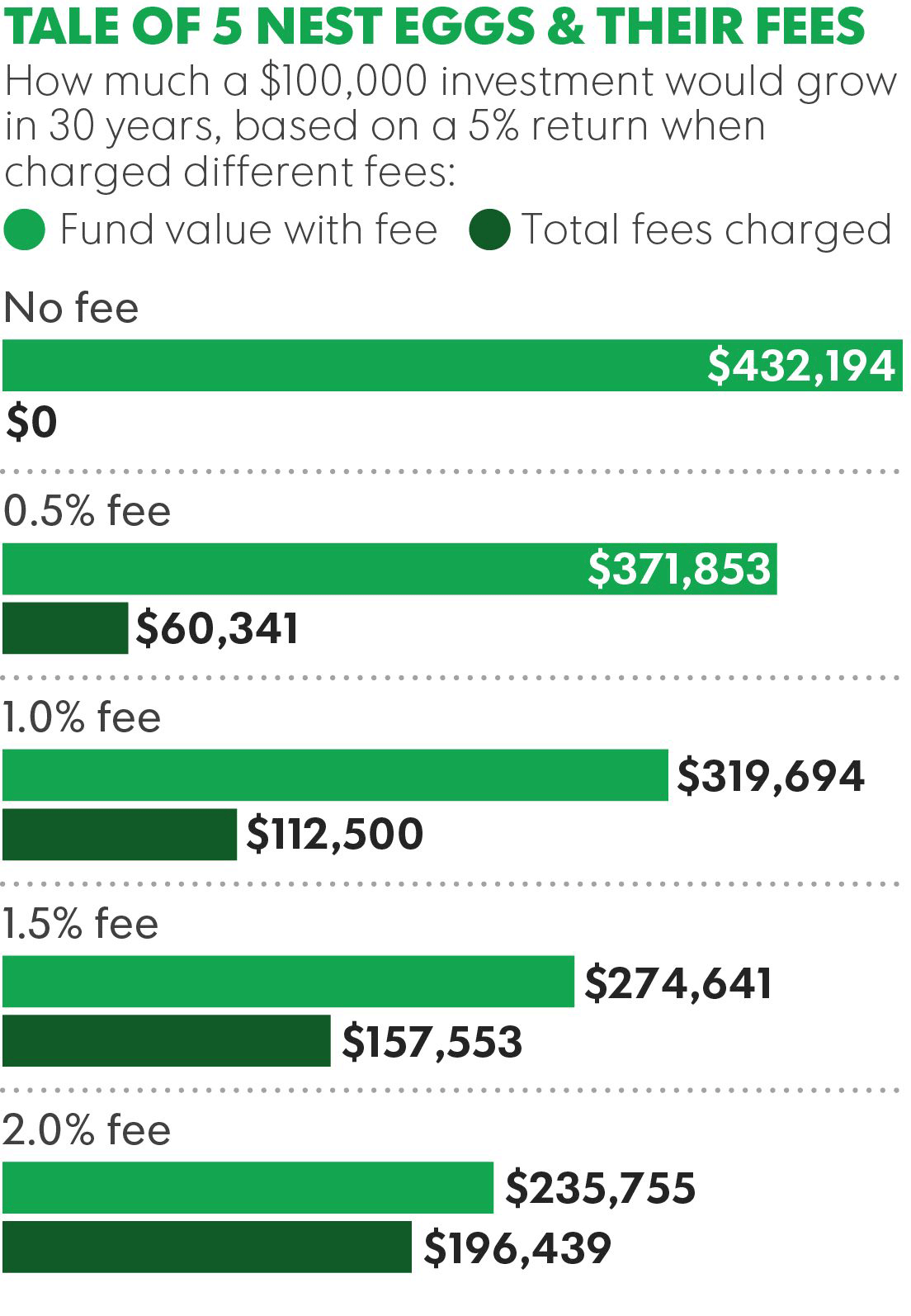

Many financial planning websites mention fees, as required, but still remain opaque to potential clients because the advisor wants to control the discussion and understandably wishes to avoid the website shopper phenomenon.

But, physicians and all investors can still control the discussion, and still provide transparency, because posting up front pricing information doesn’t mean presenting information in a vacuum!

For example, a 1%/year fee doesn’t have to just be 1%; it can be 1%, compared to an industry average cost of X%, where the average cost of an actively managed mutual fund is Y%.

***

***

Similarly, it doesn’t have to be a retainer fee of $1,000/year; it can be a retainer fee for less than the cost of a monthly cable bill! And, a financial plan doesn’t cost $1,500; it costs 8-12 hours of staff time to craft extensive, customized solutions; but saves the doctor-client so much more!

And, if services have a range of potential prices, they might be provided with some insight into the factors that impact the price. Modern young and internet savvy doctors expect this sort of information.

Posted on April 17, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Stat: 10%. That’s the percentage of Tesla employees that will be impacted by its global workforce reduction. Elon Musk sent an email to employees on Monday informing them of the layoffs, which he said were made to “reduce costs and increase productivity,” according to the WSJ. The move comes as the electric vehicle maker deals with a wider slowdown in EV sales. (the Wall Street Journal)

UnitedHealth Group, reeling from the Change cyberattack, recorded a loss of $1.4 billion in the first quarter. Still, its EPS exceeded expectations and the stock is trading up.

And … physicians made steady pay gains last year, but increases were undercut by inflation rates. See how other specialties fared, according to a report from Medscape.

The social determinants of health can impact a woman’s chance of being up to date with her mammogram, according to a recent Centers for Disease Control and Prevention report. Women are less likely to get a mammogram if they feel socially isolated, have lost a job or don’t have reliable transportation.

And…A major House subcommittee is considering whether to issue another short-term extension on telehealth flexibilities as they continue to evaluate cost and quality issues or to enact permanent changes to virtual care reimbursement. The American Telemedicine Association is pushing Congress to make permanent the Medicare telehealth flexibilities implemented during the COVID-19 pandemic.

The S&P 500® index (SPX) declined 10.41 points (0.2%) to 5,051.41, its lowest close in almost two months; the Dow Jones Industrial Average® ($DJI) advanced 63.86 points (0.2%) to 37,798.97; the NASDAQ Composite® ($COMP) eased 19.77 points (0.1%) to 15,865.25.

The 10-year Treasury note yield gained almost 4 basis points to 4.667%.

The CBOE Volatility Index® (VIX) fell 0.83 to 18.40.

Scaled-back expectations for Fed rate cuts continued to burden interest-rate-sensitive sectors, such as banks and utilities. The KBW Regional Bank Index (KRX) lost 1.4% and ended near a five-month low. The small-cap Russell 2000® Index (RUT) dropped 0.4% and ended at a two-month low.

In other markets, the U.S. dollar index (DXY) strengthened for the fifth consecutive trading day and hit its highest level since late October, reflecting expectations rates will stay elevated.

A closed-end fund (CEF) or closed-ended fund is a collective investment model based on issuing a fixed number of shares which are not redeemable from the fund.

Unlike open-end funds, new shares in a closed-end fund are not created by managers to meet demand from investors. Instead, the shares can be purchased and sold only in the market, which is the original design of the mutual fund, which predates open-end mutual funds but offers the same actively-managed pooled investments.

Posted on April 16, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Here’s where the major stock market benchmarks ended:

The S&P 500 index fell 61.59 points (1.2%) to 5,061.82; the Dow Jones Industrial Average lost 248.13 points (0.7%) to 37,735.11; the NASDAQ Composite® ($COMP) dropped 290.08 points (1.8%) to 15,885.02.

The 10-year Treasury note yield (TNX) surged almost 12 basis points to 4.618%.

The CBOE Volatility Index® (VIX) rose 1.92 to 19.23.

Interest-rate-sensitive sectors like real estate and utilities were among the weakest performers Monday. Technology shares were also under pressure. The small-cap Russell 2000® Index (RUT) shed 1.4% and ended at a two-month low.

In other markets, the U.S. dollar index (DXY) strengthened for the fourth consecutive trading day and hit its highest level since early November, reflecting expectations rates will stay elevated. Volatility based on the VIX jumped near 19.50, its highest level since late October.

Monday’s session also produced technical damage on the charts of benchmarks like the S&P 500, which closed under its 50-day simple moving average, currently around 5,114, for the first time since early November. The S&P 500 has dropped almost 4% from a record intraday high posted March 28th.

And, after a tough funding year for digital health startups, the first quarter of 2024 saw a flurry of deals announced—a “positive signal” that the funding landscape is looking up, according to Adriana Krasniansky, head of research at digital health strategy group and venture fund Rock Health’s advisory arm. Overall, the number of digital health funding deals (133) that closed in Q1 was the highest in six quarters, though the average deal size ($20.6 million) was smaller, according to a Rock Health report. Total funding for digital health startups was $2.7 billion, the lowest level since 2019. An increase in the frequency of deals—even if they’re smaller—is a good sign, according to Krasniansky.

Dental startup Tend aims to simplify the patient billing process via a partnership with health tech startup Cedar, the companies announced on April 11th, 2024. The US spends roughly $165 billion per year on dental services as of 2022, according to professional organization the American Dental Association—but the payment experience can be “opaque” and “confusing,” Matthew Fitzgerald, chief marketing officer at Tend, told Healthcare Brew. “From the outset, Tend has sought to innovate the dental experience by leveraging technology and hospitality to build a company around the patient,” Tend CEO Troy Bage said in a statement. “By partnering with Cedar, we’ll be able to streamline and simplify the payment process for all our members—further enhancing their overall experience with Tend, while unlocking new ways for us to elevate engagement.”

Posted on April 15, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

“Worried about an IRS audit? Avoid what’s called a red flag. That’s something the IRS always looks for. For example, say you have some money left in your bank account after paying taxes. That’s a red flag.“

― Jay Leno

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Americans are saving less at their lowest pace in more than a year, and are apparently spending more than the growth of their incomes, according to an analysis by Wells Fargo that was shared with Newsweek.

In February, the personal savings rate hit 3.6 percent, “marking the lowest rate at which households saved in 14 months,” Wells Fargo economists noted in the Thursday report, adding that spending outpaced income growth for the month. The savings rate is higher than the below 3 percent level it fell to following the COVID-19 pandemic, but is nevertheless way down from the pre-pandemic rate of 6 percent.

The deadline for most people to file a 2023 tax return with the IRS is fast approaching; returns are due by 11:59 p.m., in your time zone, on Monday, April 15th today, with some exceptions. Taxpayers in Massachusetts and Maine have until April 17th to file and pay taxes because of the Patriots’ Day and Emancipation Day holidays. There are also extensions in some areas impacted by extreme weather. Individuals and businesses impacted by the October 7th attack on Israel have also been given an extension, the IRS announced. There are extensions for certain active-duty military members and citizens living abroad.

Nike announced plans to lay off around 1,600 employees, or about 2% of its global workforce, as part of a $2 billion cost-cutting strategy. CEO John Donahoe said performance has not been the best and took responsibility. Donahoe said, “This is a painful reality and not one that I take lightly.”

Stellantis is the world’s fourth-largest automaker by sales, behind Toyota, Volkswagen Group, and Hyundai Motor Group. The company designs, manufactures, and sells automobiles bearing its 14 brands: Abarth, Alfa Romeo, Chrysler, Citroën, Dodge, DS, Fiat, Jeep, Lancia, Maserati, Opel, Peugeot, Ram, and Vauxhall. Their headquarters is located in Amsterdam, and they have over 300,000 employees in 130 countries.

***

The Biden administration wants to make changes to private Medicare insurance plans that officials say will help seniors find plans that best suit their needs, promote access to behavioral health care and increase use of extra benefits such as fitness and dental plans. “We want to ensure that taxpayer dollars actually provide meaningful benefits to enrollees,” said Health and Human Services Secretary Xavier Becerra. If finalized, the proposed rules rolled out Monday could also give seniors faster access to some lower-cost drugs. Administration officials said the changes, which are subject to a 60-day comment period, build on recent steps taken to address what they called confusing or misleading advertisements for Medicare Advantage [Part C] plans. Just over half of those eligible for Medicare get coverage through a private insurance plan rather than traditional, government-run Medicare.

***

Healthcare varies substantially by state based on dozens of factors. The same is valid for cities. Some of this is due to the availability of medical facilities. Some have to do with health habits. Some have to do with incomes and poverty levels. People who live in poor states, based on income, almost always have unhealthy populations. A new study from Renew Bariatrics shows the “Healthiest (and Unhealthiest) States in the US—2024 Rankings,” and reviews alcohol use, diabetes, drug overdoses, mental health, isolation, tobacco use, exercise, and the presence of heart disease, obesity, and cancer. These, taken together, create an index from 0 to 100, with 100 being the worst possible score. These are the most expensive states to live in.

Posted on April 14, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Texas Governor Greg Abbott has issued a sharp warning about proposed changes to Medicaid, claiming they could “strip millions of Americans” from access to healthcare. In February 2023, the Centers for Medicare & Medicaid Services (CMS) issued a new proposed rule that would change long-standing practices for how states fund the non-federal share of Medicaid payments. In particular, the CMS is pushing for greater oversight of how states use of healthcare provider taxes to help fund their programs.

Democratic lawmakers Sen. Richard Blumenthal and Rep. Andy Kim have partnered up with RepublicanRep. Jen Kiggans to introduce legislation aiming to give army reservists and members of the National Guard that also work for the federal government options on the type of health care plans they can receive. The bill, which could impact thousands of federal employees that are also in the U.S. Army, plans to give this group of Americans the ability to decide whether they want military or civilian health care. The lawmakers said in a shared statement that their proposal will fix current regulations that limit service members who also work for the government to enroll in the cheaper Tricare Reserve Select (TRS) health plan when they also qualify for federal health plans.

Stocks tanked last Friday after the big banks reported underwhelming earnings and the sheen from the Magnificent Seven’s AI-driven surge earlier this week wore off. Meanwhile, oil prices continue to rise near six-month highs as concern grows over geopolitical tensions in the Middle East. The tech sector was highlighted in this market, particularly due to the exceptional performance of a group of mega-cap tech giants last year nicknamed the “Magnificent Seven.” This elite group includes Apple (AAPL), Amazon (AMZN), Alphabet (GOOGL), Meta Platforms (META), Microsoft (MSFT), Nvidia (NVDA) and Tesla (TSLA).

Posted on April 13, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Medial Office Equipment Interest Rate Costs

Dr. David E. Marcinko; MBA, MEd, CMP™

[Publisher in Chief]

Physicians, administrators and healthcare entrepreneurs are aware of the compounding effect of interest.However, since interest is deductible as a medical office business expense, many seem to forget about it despite the fact that it must be continually paid until the asset is either purchased or otherwise disposed.

So, what are the various types of interest rates important to the medical practitioner and commodity – money?

[1] Simple Interest

Simple interest is merely the pro rata interest on a loan or deposit and represents the most basic interest rate type.

For example, for every $100 Dr. Bill borrows at 12 percent annual interest, he pays twelve dollars per year. The interest is calculated by multiplying the principal or original amount, by the interest rate in decimal form (100 x .12).

[2] Add-On Interest

Add on interest immediately attaches the annual interest amount, to the principal amount, at the beginning of the payment period. Payments are then made according to the number of years required.

The following formula is useful:

Add-on-Interest minus Payment = Total Interest on Balance/Number of Payments

For example, if Dr. William Needy borrows $10,000 at 8 percent add-on interest, he will repay $10,000 plus $ 800 ($10,000 x 8%) or $10,800, divided by twelve months, for a total of $900 per month, since $ 900/month x 12 months equals $10,800.

[3] Discounted Interest

When using the discounted interest method, the interest amount is deducted from the principal right up front. Notice that this is the opposite of add-on-interest that is applied up front.

For example, if Dr. Bill borrows the same $ 10,000 at a discounted interest rate of 8 percent, he will only receive a $9,200 loan, since $10,000 – $800 is $9,200.

Obviously, the discount method is the most expense way to borrow money.

[4] Annual Percentage Rate

Most financial institutions advertise an annual percentage rates (APR) for loans, deposits and investments. The APR is the periodic interest rate multiplied by the number of periods a year. If the APR is 12 percent, and interest is compounded monthly, you receive (or pay) 1 percent of your balance each month, and the balance shifts with each compounding.

For example, if Dr. Bill deposits $ 100 dollars at 12 percent APR compounded monthly, he receives $ 1 interest the first month (1% of $100), $1.10 the second month (1% of $101), and so forth. If compounding is daily, the interest accumulates at the rate of 1/365 of the APR each day.

Unless interest is compounded annually, the APR will be lower than the effective annual interest rate, discussed below.

[5] Effective Interest Rate

It is important to differentiate between the effective interest rate and the APR, which is often the most prominent figure in advertisements for medical business equipment, consumer goods and financial services (loans, annuities, IRAs, CDs, investment analysis, college funding or retirement planning). Although the APR is the periodic interest rate multiplied by the number of periods per year, the effective annual interest rate is the periodic rate, compounded.

In our case, if the APR is 12 percent, compounded monthly, the monthly interest rate is 1 percent and the effective annual rate is the monthly rate compounded for 12 periods.

Therefore, if your calculation is for a single year, you can treat the effective rate as simple interest. If you deposit (or borrow) $1,000 at 12 percent APR, the effective rate is 12.68 percent, and interest for the first year is about $126.80 (12.68% of $1,000).

For longer periods, you can use the effective interest rate as the periodic interest rate, compounded annually.

[a] “Rule of 72” (Double your Money)

The number of periods required to double a lump sum of money can be quickly estimated by using what is known as the “Rule of 72”. To get the number of periods, usually years, just divide 72 by the periodic interest rate, expressed as a whole number (not a decimal).

For example, if the annual interest rate is 10 percent, it will take about 7.2 years (72/10) to double any lump cache of money. Conversely, you can also calculate the interest rate required to double your money in a given period by dividing 72 by the term.

Thus, to double your money in ten years, you need to earn about 7.2 percent annual interest (72/10) = 7.2%).

[b] “Rule of 78”

According to this method, interest is front end loaded like a home mortgage, or office condominium, to discourage prepayment of a loan and consequently preserve the lender’s profit. In other words, it is a method of calculating installment loan interest rebates.

The number 78 comes from an approved method of accelerated tax depreciation, known as the “Sum of the Years Digits” (SOYD) method (i.e., 12 + 11 + 10 + 9 . . . = 78). This fact is important because, throughout the period of a loan, even though the payments are all the same, the portions that are interest and principal are very different.

Using this method for a one year loan shows that, in the first payment, 15.38 percent of the interest due is paid off, and by the sixth month, 73.08 percent of the interest is paid off. This means, that if a physician makes a one year equipment loan with a total interest charge of $ 100 and pays the loan off in full with the sixth payments, he or she will not get an interest rebate of $ 50, but only $ 26.92, since $ 73.08 of the interest has already been prepaid.

Most ethical lenders use simple interest rates for loan rebates, and the Rule of 78 is unfair according to many authorities.

[c] “Rule of 116”

A derivative of the Rule of 72 is the Rule of 116. This determines the number of years it takes for a principal amount to be tripled and is calculated by dividing the annual interest rate into 116.

The Rules of 72 and 78 are very handy for figuring the amount of interest payments made or growth of funds invested. They can also be used in reverse to calculate at what rate of interest money must be invested to double or triple in a certain number of years.

[6] Medical Equipment Payback Cost Analysis

The payback period, expressed in years, is the length of time that it takes for the medical equipment investment to recoup its initial cost out of the cash receipts it generates. The basic premise is that the quicker the cost of an investment can be recovered, the better the investment is. It is most often used when considering equipment whose useful life is short and unpredictable.

When the same cash flow occurs every year, the formula is as follows:

Investment Required / Net Annual Cash Inflow = Payback Period

Thus, in today’s tightening medical reimbursement atmosphere, practice cost control and expense reduction is the easiest method to increase medical office profitability. Keeping the cost of the commodity money in the form of interest rate charges, as low as possible, will assist in this endeavor

Assessment

And so, how have these rules affected your medical office borrowing costs; if at all? Does these principles apply to the medical student loan crisis, today?

Posted on April 13, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Medical colleague and our financial planning for physicians textbook contributor Michael Burry MD predicted a second inflation surge, and price growth re-accelerated in March,. 2024.

The “Big Short” investor first warned of inflation in April 2020, over two years before it peaked.

Burry expected a recession, rate cuts, and stimulus spending to reignite inflation.

A growing number of drugs are in short supply around the U.S., according to pharmacists.

In the first three months of the year, there were 323 active medication shortages, surpassing the previous high of 320 shortages in 2014, according to a survey by the American Society of Health-System Pharmacists (ASHP) and Utah Drug Information Service. It also amounts to the most shortages since the trade group started keeping track in 2001. “All drug classes are vulnerable to shortages. Some of the most worrying shortages involve generic sterile injectable medications, including cancer chemotherapy drugs and emergency medications stored in hospital crash carts and procedural areas,” ASHP said in a statement.

Scheduling an appointment with a primary care doctor who belongs to a large health system might cause an increase in health care spending, according to a recent study. Such physicians tend to make more referrals to specialists, and emergency room visits and hospitalizations sometimes increase, according to the research out of Harvard T.H. Chan School of Public Health.

In short, physicians who work for health care systems like hospitals are more likely to recommend that patients use other services within those systems, compared with independent physicians. For the study — which was published in JAMA Health Forum, a journal of the American Medical Association — researchers analyzed the experiences of more than 4 million patients in Massachusetts.

UnitedHealth ChairmanStephen Hemsley and other executives sold $102 million in company stock months before a federal antitrust probe became public, Bloomberg reported.

***

Small physician practices are still struggling in the wake of February’s Change Healthcare cyberattack, according to an American Medical Association (AMA) survey released Wednesday.

More than half of ~1,400 respondents (55%) reported that they’ve had to use personal funds to cover their practice’s expenses due to the cyberattack’s effects on cash flow. Practices across the country have been unable to fill prescriptions or process insurance claims as Change Healthcare systems went offline, Healthcare Brew previously reported. About two-thirds of respondents said they’ve experienced restrictions to core functions, such as suspending claim payments (36%), not being able to submit claims (32%), and not being able to obtain electronic remittance advice (39%), according to the survey.

The S&P 500 index fell 75.65 points (1.5%) to 5,123.41, down 1.6% for the week; the Dow Jones Industrial Averagelost 475.84 points (1.2%) to 37,983.24, down 2.4% for the week; the NASDAQ Composite® ($COMP) dropped 267.10 points (1.6%) to 16,175.09, down 0.5% for the week.

The 10-year Treasury note yield (TNX) fell more than 5 basis points to 4.52%, still up about 12 basis points for the week.

The CBOE Volatility Index® (VIX) rose 2.38 to 17.30.

Semiconductor shares were also among the weakest performers Friday as chip makers reversed Thursday’s sharp gains. The Philadelphia Semiconductor Index (SOX) dropped more than 3% and ended with its third straight weekly decline. Energy companies were also under pressure after crude oil prices retreated from the morning rally. Oil futures are still up 20% this year. The small-cap Russell 2000® Index (RUT) lost 1.9% and posted a 2.9% drop for the week.

In other markets, the U.S. dollar index (DXY) strengthened to a five-month high and gained 1.7% this week, reflecting beliefs the hotter-than-expected inflation readings earlier this week will keep interest rates elevated. Volatility based on the VIX jumped to its highest level since late October.

The paradox of thrift (saving) states that an increase in autonomous saving leads to a decrease in aggregate demand and thus a decrease in gross output which will in turn lower total saving. The paradox is that total saving may fall because of individuals’ attempts to increase their saving, and, broadly speaking, that increase in saving may be harmful to an economy.

Both the narrow and broad claims are paradoxical within the assumption underlying the fallacy of composition, namely that which is true of the parts must be true of the whole. The narrow claim transparently contradicts this assumption, and the broad one does so by implication, because while individual thrift is generally averred to be good for the economy, the paradox of thrift holds that collective thrift may be bad for the economy.

Posted on April 12, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Costco started selling gold bars to its members last August, and Wells Fargo analysts believe that the product is now bringing in between $100 million and $200 million a month. The retailer doesn’t reveal the price of the 1-ounce bullion to nonmembers online, but it’s estimated to be ~2% above the spot price gold trades at, per CNBC—and that price has soared since Costco got into the gold game. The price of gold has gone up 13% this year and reached record highs as investors pile in amid inflation worries.

The big numbers from the Consumer Price Index data released on Thursday

In March, inflation rose 3.5% from the year before, up from 3.2% in February.

The “core” CPI reading, which excludes volatile food and fuel prices, came in even higher, rising 3.8% on an annual basis. That’s the same as in February, but this time it’s serious.

Half of the increases came from rising gas prices and housing.

After seeing inflation fall by 3% over the course of 2023, Fed officials believed that higher inflation readings in January and February 2024 represented a hiccup in an otherwise downward trajectory. However, with the March reading also coming in hotter than anticipated, analysts say this is more than a fluke. That means hopes for a June interest rate cut are dashed. Even the US Postal Service plans to raise the price of “forever” stamps to $0.73 in July. Get yours now. And the Mexican peso is on an absolute tear, leaving the US dollar behind.

The S&P 500® index (SPX) advanced 38.42 points (0.7%) to 5,199.06; the Dow Jones Industrial Average® ($DJI) lost 2.43 points to 38,459.08; the NASDAQ Composite gained 271.84 points (1.7%) to 16,442.20.

The 10-year Treasury note yield (TNX) rose nearly 2 basis points to 4.578%.

The CBOE Volatility Index® (VIX) fell 0.89 to 14.91.

Chip maker strength lifted the Philadelphia Semiconductor Index (SOX) more than 2% and extended the benchmark’s year-to-date gain to more than 17%. Communications services and transportation shares were also among the strongest sectors. Financial shares were mixed ahead of expected quarterly results Friday from some major banks including JPMorgan Chase (JPM), Citigroup (C), and Wells Fargo (WFC).

Posted on April 11, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST– Today’sNewsletter

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

NEW YORK (Reuters) -The U.S. accounting watchdog on Wednesday said it has hit KPMG Netherlands with a $25 million civil penalty, a record for the regulator, in response to “egregious” and widespread exam cheating at the foreign affiliate of the major audit firm.

As millions of Americans approach age 66, they face the inevitable question, is it time to retire? The physician population is aging alongside the general population—more than 40% of physicians in the U.S. will be 65 years or older within the next decade. In the case of surgeons, there is little guidance on how to best ensure their competency throughout their career and at the same time maintain patient safety while preserving mature physician dignity.

It is a scenario playing out nationwide. From Oregon to Pennsylvania, hundreds of communities have in recent years either stopped adding fluoride to their water supplies or voted to prevent its addition. Supporters of such bans argue that people should be given the freedom of choice. The broad availability of over-the-counter dental products containing the mineral makes it no longer necessary to add to public water supplies, they say. The Centers for Disease Control and Prevention says that while store-bought products reduce tooth decay, the greatest protection comes when they are used in combination with water fluoridation.

More health systems are going to be opting out of Medicare Advantage (MA) plans, George Hill, a managing director at Deutsche Bank in Boston, predicted Monday at a “Wall Street Comes to Washington” webinar hosted by the Brookings Institution. “I think you’re going to see more large provider organizations threaten to opt out of networks, particularly as it relates to MA,” Hill said, adding that there are a number of reasons for this. “Prior authorizations are the problem, claims denials are a huge problem, delayed payments and rates are the problem — barriers in access to care in all varieties are the problem.”

The latest budget update from the nonpartisan Congressional Budget Office (CBO) found that the federal government has spent more on paying interest on the national debt than on the military in fiscal year 2024. The CBO’s budget report for March showed that the U.S. has spent $412 billion on military programs at the Department of Defense through the first half of FY-2024, according to preliminary figures from CBO and the Treasury Department.

Consumer price increases remained high last month, boosted by gas, rents, and car insurance, the government said Wednesday in a report that will likely give pause to the Federal Reserve as it weighs when and by how much to cut interest rates this year. Prices outside the volatile food and energy categories rose 0.4% from February to March, the same accelerated pace as in the previous month. Measured from a year earlier, these core prices were up 3.8%, unchanged from the year-over-year rise in February. The Fed closely tracks core prices because they tend to provide a good read of where inflation is headed.

Here’s where the major benchmarks ended:

The S&P 500® index (SPX) dropped 49.27 points (1.0%) to 5,160.64; the Dow Jones Industrial Average lost 422.16 points (1.1%) to 38,461.51; the NASDAQ Composite® ($COMP) fell 136.28 points (0.8%) to 16,170.36.

The 10-year Treasury note yield (TNX) soared more than 18 basis points to 4.548%.

The CBOE Volatility Index® (VIX) jumped 0.82 to 15.80.

Interest-rate-sensitive sectors like banks, real estate, and utilities led Wednesday’s decliners. The KBW Regional Bank Index (KRX) tumbled 5% to its lowest point since late November. The small-cap Russell 2000® Index (RUT) lost 2.5%. Energy shares were among the few gainers as WTI Crude Oil (/CL) futures rebounded after three-straight losing sessions.

In other markets, the U.S. dollar index (DXY) jumped 1% to a five-month high amid expectations interest rates will remain elevated.