BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Investment bankers are not really bankers at all. The fact that the word banker appears in the name is partially responsible for the false impressions that exist in the medical community regarding the functions they perform.

For example, they are not permitted to accept deposit, provide checking accounts, or perform other activities normally construed to be commercial banking activities. An investment bank is simply a firm that specializes in helping other corporations obtain money they need under the most advantageous terms possible. When it comes to the actual process of having securities issued, the corporation approaches an investment banking firm, either directly, or through a competitive selection process and asks it to act as adviser and distributor.

Investment bankers, or under writers, as they are sometimes called, are middlemen in the capital markets for corporate securities. The corporation requiring the funds discusses the amount, type of security to be issued, price and other features of the security, as well as the cost to issuing the securities. All of these factors are negotiated in a process known as negotiated underwriting. If mutually acceptable terms are reached, the investment banking firm will be the middle man through which the securities are sold to the general public. Since such firms have many customers, they are able to sell new securities, without the costly search that individual corporations may require to sell its own security.

Thus, although the firm in need of additional capital must pay for the service, it is usually able to raise the additional capital at less expense through the use of an investment banker, than by selling the securities itself. The agreement between the investment banker and the corporation may be one of two types. The investment bank may agree to purchase, or underwrite, the entire issue of securities and to re-offer them to the general public. This is known as a firm commitment.

When an investment banker agrees to underwrite such a sale; it agrees to supply the corporation with a specified amount of money. The firm buys the securities with the intention to resell them. If it fails to sell the securities, the investment banker must still pay the agreed upon sum.

Thus, the risk of selling rests with the underwriter and not with the company issuing the securities.

The alternative agreement is a best efforts agreement in which the investment banker makes his best effort to sell the securities acting on behalf of the issuer, but does not guarantee a specified amount of money will be raised. When a corporation raises new capital through a public offering of stock, one might inquire where the stock comes from. The only source the corporation has is authorized, but previously un-issued stock. Anytime authorized, but previously un-issued stock (new stock) is issued to the public, it is known as a primary offering.

If it’s the very first time the corporation is making the offering, it’s also known as the Initial Public Offering (IPO). Anytime there is a primary offering of stock, the issuing corporation is raising additional equity capital.

A secondary offering, or distribution, on the other hand, is defined as an offering of a large block of outstanding stock. Most frequently, a secondary offering is the sale of a large block of stock owned by one or more stockholders. It is stock that has previously been issued and is now being re-sold by investors. Another case would be when a corporation re-sells its treasury stock.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

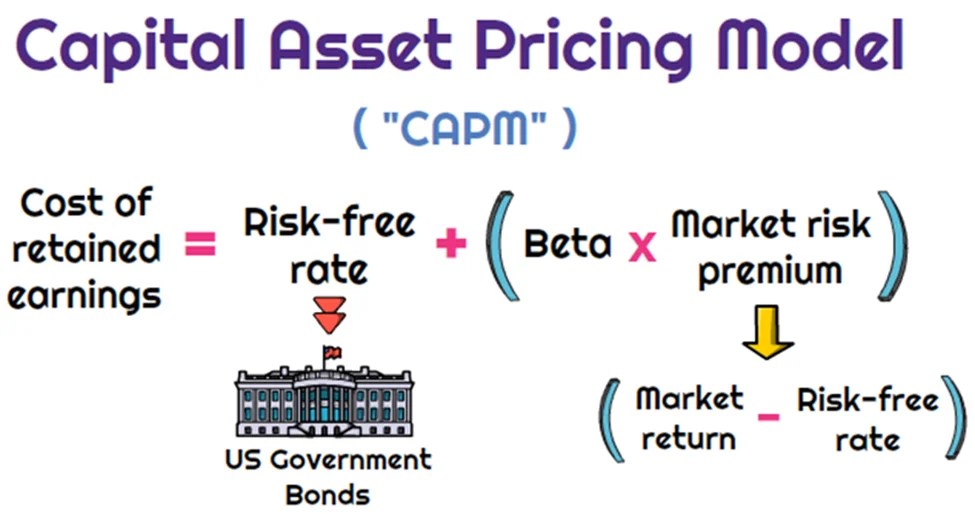

Dr. Harry Markowitz is credited with developing the framework for constructing investment portfolios based on the risk-return tradeoff. William Sharpe, John Lintner, and Jan Mossin are credited with developing the Capital Asset Pricing Model (CAPM).

CAPM is an economic model based upon the idea that there is a single portfolio representing all investments (i.e., the market portfolio) at the point of the optimal portfolio on the Capital Market Line (CML) and a single source of systematic risk, beta, to that market portfolio. The resulting conclusion is that there should be a “fair” return investors should expect to receive given the level of risk (beta) they are willing to assume.

The excess return, or return above the risk-free rate, that may be expected from an asset is equal to the risk-free return plus the excess return of the market portfolio times the sensitivity of the asset’s excess return to the market portfolio excess return. Beta, then, is a measure of the sensitivity of an asset’s returns to the market as a whole. A particular security’s beta depends on the volatility of the individual security’s returns relative to the volatility of the market’s returns, as well as the correlation between the security’s returns and the markets returns.

While a stock may have significantly greater volatility than the market, if that stock’s returns are not highly correlated with the returns of the overall market (i.e., the stock’s returns are independent of the overall market’s returns), then the stock’s beta would be relatively low. A beta in excess of 1.0 implies that the security is more exposed to systematic risk than the overall market portfolio, and likewise, a beta of less 1.0 means that the security has less exposure to systematic risk than the overall market.

MPT has helped focus investors on two extremely critical elements of investing that are central to successful investment strategies.

First, MPT offers the first framework for investors to build a diversified portfolio. Furthermore, an important conclusion that can be drawn from MPT is that diversification does in fact help reduce portfolio risk.

Thus, MPT approaches are generally consistent with the first investment rule of thumb, “understand and diversify risk to the extent possible.”

Additionally, the risk/return tradeoff (i.e., higher returns are generally consistent with higher risk) central to MPT based strategies has helped investors recognize that if it looks too good to be true, it probably is.

Passive Investing

Passive investing is a monetary plan in which an investor invests in accordance with a pre-determined strategy that doesn’t necessitate any forecasting of the economy or an individual company’s prospects. The primary premise is to minimize investing fees and to avoid the unpleasant consequences of failing to correctly predict the future. The most accepted method to invest passively is to mimic the performance of a particular index. Investors typically do this today by purchasing one or more ‘index funds’. By tracking an index, an investor will achieve solid diversification with low expenses.

An ivestor could potentially earn a higher rate of return than an investor paying higher management fees. Passive management is most widespread in the stock markets. But with the explosion of exchange traded funds on the major exchanges, index investing has become more popular in other categories of investing. There are now literally hundreds of different index funds.

Passive management is based upon the Efficient Market Hypothesis theory. The Efficient Market Hypothesis (EMH) states that securities are fairly priced based on information regarding their underlying cash flows and that investors should not anticipate to consistently out-perform the market over the long-term.

The Efficient Market Hypothesis evolved in the 1960s from the Ph.D. dissertation of Eugene Fama. Fama persuasively made the case that in an active market that includes many well-informed and intelligent investors, securities will be appropriately priced and reflect all available information. If a market is efficient, no information or analysis can be expected to result in out-performance of an appropriate benchmark. There are three distinct forms of EMH that vary by the type of information that is reflected in a security’s price:

Weak Form

This form holds that investors will not be able to use historical data to earn superior returns on a consistent basis. In other words, the financial markets price securities in a manner that fully reflects all information contained in past prices.

Semi-Strong Form

This form asserts that security prices fully reflect all publicly available information. Therefore, investors cannot consistently earn above normal returns based solely on publicly available information, such as earnings, dividend, and sales data.

Strong Form

This form states that the financial markets price securities such that, all information (public and non-public) is fully reflected in the securities price; investors should not expect to earn superior returns on a consistent basis, no matter what insight or research they may bring to the table.

While a rich literature has been established regarding whether EMH actually applies in any of its three forms in real world markets, probably the most difficult evidence to overcome for backers of EMH is the existence of a vibrant money management and mutual fund industry charging value-added fees for their services.

The notion of passive management is counterintuitive to many investors. Passive investing proponents follow the strong market theory of EMH. These proponents argue several points including;

In the long term, the average investor will have a typical before-costs performance equal to the market average. Therefore the standard investor will gain more from reducing investment costs than from attempting to beat the market over time.

The efficient-market hypothesis argues that equilibrium market prices fully reflect all existing market information. Even in the case where some of the market information is not currently reflected in the price level, EMH indicates that an individual investor still cannot make use of that information. It is widely interpreted by many academics that to try and systematically “beat the market” through active management is a fools game.

Not everyone believes in the efficient market. Numerous researchers over the previous decades have found stock market anomalies that indicate a contradiction with the hypothesis. The search for anomalies is effectively the hunt for market patterns that can be utilized to outperform passive strategies. Such stock market anomalies that have been proven to go against the findings of the EMH theory include;

Low Price to Book Effect

January Effect

The Size Effect

Insider Transaction Effect

The Value Line Effect

All the above anomalies have been proven over time to outperform the market. For example, the first anomaly listed above is the Low Price to Book Effect. The first and most discussed study on the performance of low price to book value stocks was by Dr. Eugene Fama and Dr. Kenneth R. French. The study covered the time period from 1963-1990 and included nearly all the stocks on the NYSE, AMEX and NASDAQ. The stocks were divided into ten subgroups by book/market and were re-ranked annually. In the study, Fama and French found that the lowest book/market stocks outperformed the highest book/market stocks by a substantial margin (21.4 percent vs. 8 percent). Remarkably, as they examined each upward decile, performance for that decile was below that of the higher book value decile. Fama and French also ordered the deciles by beta (measure of systematic risk) and found that the stocks with the lowest book value also had the lowest risk.

Today, most researchers now deem that “value” represents a hazard feature that investors are compensated for over time. The theory being that value stocks trading at very low price book ratios are inherently risky, thus investors are simply compensated with higher returns in exchange for taking the risk of investing in these value stocks. The Fama and French research has been confirmed through several additional studies. In a Forbes Magazine 5/6/96 column titled “Ben Graham was right–again,” author David Dreman published his data from the largest 1500 stocks on Compustat for the 25 years ending 1994. He found that the lowest 20 percent of price/book stocks appreciably outperformed the market.

One item a medical professional should be aware of is the strong paradox of the efficient market theory. If each investor believes the stock market were efficient, then all investors would give up analyzing and forecasting. All investors would then accept passive management and invest in index funds. But if this were to happen, the market would no longer be efficient because no one would be scrutinizing the markets. In actuality, the efficient market hypothesis actually depends on active investors attempting to outperform the market through diligent research.

The case for passive investing and in favor of the EMH is that a preponderance of active managers do actually underperform the markets over time. The latest study by Standard and Poor’s (S&P) confirms this fact. S&P recently compared the performance of actively-managed mutual funds to passive market indexes twice per year. The 2012 S&P study indicated that indexes were once again outperforming actively-managed funds in nearly every asset class, style and fund category. The lone exception in the 2012 report was international equity, where active outperformed the index that S&P chose. The study examined one-year, three-year and five-year time periods. Within the U.S. equity space, active equity managers in all the categories failed to outperform the corresponding benchmarks in the past five year period. More than 65 percent of the large-cap active managers lagged behind the S&P 500 stock index. More than 81 percent of mid-cap mutual funds were outperformed by the S&P MidCap 400 index.

Lastly, 77 percent of the small-cap mutual funds were outperformed by the S&P SmallCap 600 index. U.S. bond active managers fared no better that equity managers over a five year period. More than 83 percent of general municipal mutual funds under-performed the S&P National AMT-Free Municipal Bond index, 93 percent of government long-term funds under-performed the Barclays Long Government index, nearly 95 percent of high yield corporate bond funds under-performed the Barclays High Yield index. Although the performance measurements for index investing are very strong, many analysts find three negative elements of passive investing;

Downside Protection: When the stock market collapses like in 2008, an index investor will assume the same loss as the market. In the case of 2008, the S&P 500 stock index fell by more than 50 percent, offering index investors no downside protection.

Portfolio Control: An index investor has no control over the holdings in the fund. In the event that a certain sector becomes over-owned (i.e. technology stocks in 2000), an index investor maintains the same weight as the index.

Average Returns: An index investor will never have the opportunity to outperform the market, but will always follow. Although the markets are very efficient, an investor can perhaps take advantage of market anomalies and invest with those managers who have maintained a long-term performance edge over the respective index.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

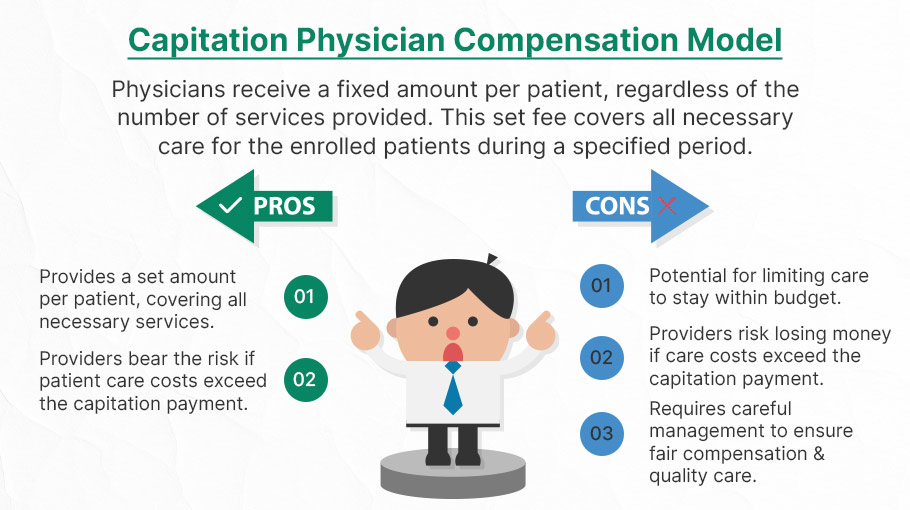

Capitation is a type of healthcare payment system in which a physician or hospital is paid a fixed amount of money per patient for a prescribed period by an insurer or physician association. The cost is based on the expected healthcare utilization costs for a group of patients for that year.

With capitation, the physician—otherwise known as the primary care physician— is paid a set amount for each enrolled patient whether a patient seeks care or not. The PCP is usually contracted with an HMO whose role it is to recruit patients.

According to Richard Eskow, CEO of Health Knowledge Systems of Los Angeles, capitated medical reimbursement has been used in one form or another, in every attempt at healthcare reform since the Norman Conquest. Some even say an earlier variant existed in ancient China [personal communication].

Initially, when Henry I assumed the throne of the newly combined kingdoms of England and Normandy, he initiated a sweeping set of healthcare reforms. Historical documents, though muddled, indicate that soon thereafter at least one “physician,” John of Essex, received a flat payment honorarium of one penny per day for his efforts. Historian Edward J. Kealey opined that sum was roughly equal to that paid to a foot-soldier or a blind person. Clearer historical evidence suggests that American doctors in the mid-19th century were receiving capitation-like payments. No less an authoritative figure than Mark Twain, in fact, is on record as saying that during his boyhood in Hannibal, MO his parents paid the local doctor $25/year for taking care of the entire family regardless of their state of health.

Later, Sidney Garfield MD [1905-1984] is noted as one of the great under-appreciated geniuses of 20th century American medicine stood in the shadow cast by his more celebrated partner, Henry J. Kaiser. Garfield was not the first physician to embrace the notion of prepayment capitation, nor was he the first to understand that physicians working together in multi-specialty groups could, through collaboration and continuity of care, outperform their solo practice colleagues in almost every measure of quality and efficiency. The Mayo brothers, of course, had prior claim to that distinction. What Garfield did, was marry prepayment to group practice, providing aligned financial incentives across every physician and specialty in his medical group, as well as a culture of group accountability for the care of every member of the affiliated health plan. He called it “the new economics of medicine,” and at its heart was a fundamentally new paradigm of care that emphasized – prevention before treatment – and health before sickness. Under his model: the fewer the sick – the greater the remuneration. And: the less serious the illness, the better off the patient and the doctors.

Such ideas were heresy to the reigning fee-for-service, solo practice, ideologues of the mainstream medical establishment of the 1940s and ‘50s, of course. Throughout the period, Garfield and his group physicians were routinely castigated by leaders of the AMA and county medical associations as socialistic and unethical. The local medical associations in Garfield’s expanding service areas – the San Francisco Bay Area, Los Angeles, and Portland, Oregon – blocked group practice physicians from association membership, effectively shutting them out of local hospitals, denying them patient referrals or specialty society accreditation. Twice in the 1940s, formal medical association charges were brought against Garfield personally, at one time temporarily succeeding in suspending his license to practice medicine.

Of course, capitation payments made a comeback in the first cost-cutting managed care era of the 1980-90s because fee-for-service medicine created perverse incentives for physicians by paying more for treating illnesses and injuries than it does for preventing them — or even for diagnosing them early and reducing the need for intensive treatment later. Nevertheless, the modern managed care industry’s experience with capitation wasn’t initially a good one. The 1980-90s saw a number of HMOs attempt to put independent physicians, especially primary care doctors, into a capitation reimbursement model. The result was often negative for patients, who found that their doctors were far less willing to see them — and saw them for briefer visits — when they were receiving no additional income for their effort. Attempts were also made to aggregate various types of health providers — including hospitals and physicians in multiple specialties — into “capitation groups” that were collectively responsible for delivering care to a defined patient group. These included healthcare facilities and medical providers of all types: physicians, osteopaths, podiatrists, dentists, optometrists, pharmacies, physical therapists, hospitals and skilled nursing homes, etc.

However, the healthcare industry isn’t collective by nature, and these efforts tended to be too complicated to succeed. One lesson that these experiments taught is that provider behavior is difficult to change unless the relationship between that behavior and its consequences is fairly direct and easy to understand.

Today, the concept of prepayment and medical capitation is to uncouple compensation from the actual number of patients seen, or treatments and interventions performed. This is akin to a fixed price restaurant menu, as opposed to an àla carte eatery.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on September 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

BREAKING NEWS

Law enforcement officials in Utah released a video of the suspected shooter in the assassination of Turning Point USA co-founder and CEO Charlie Kirk, saying that the person wore Converse tennis shoes and left a hand print and a shoe print at the scene.

The suspect in Charlie Kirk’s assassination has been identified as Tyler Robinson, a 22-year-old Utah resident. Law enforcement sources told the Daily Mail that Robinson was taken into custody as the alleged assassin who killed Kirk at a rally at Utah Valley University on Wednesday.

Before today, forensic podiatry has even made it into the public zeitgeist with the hit TV show “Bones” which premiered on September 13, 2005, and concluded on March 28, 2017, airing for 246 episodes over 12 seasons. The show was based on forensic anthropology and forensic archaeology, with each episode focusing on the mystery behind human body remains brought in for examination and identification.

In one show, eight pairs of dismembered feet washed ashore after a flood on the U.S.-Canada border, but things didn’t add up when only seven pairs of feet were identified as research corpses from a nearby university body farm.

When the fictional Canadian forensic podiatrist Dr. Douglas Filmore took the remains back to Canada, he had to form a jurisdictional alliance with the United States to match the pairs of feet and identify the victims. A rare and expensive pair of sneakers led the team to the victim’s murderer.

In 2016, an actual forensic podiatry club was started at the Barry University School of Podiatric Medicine. And, a formal class covering aspects of forensic podiatry is held at the New York College of Podiatric Medicine. Students exit the class with an in depth knowledge of forensic podiatry and other legal knowledge applicable to current cases.

More expertly, real-life colleague Michael Steven Nirenberg DPMactually testified in the murder trial of defendants Kailie Brackett and Donnell Dana with the state calling three witnesses to testify, including the podiatrist who claimed Brackett’s footprints match the ones found in blood at the apartment of the victim, Kimberly Neptune. The forensic podiatrist focused on the footprints discovered at Neptune’s apartment, using prints and images of the defendant’s feet taken by law enforcement. After study, he claimed the prints at the scene bore a resemblance to Kailie Brackett’s in the width of the foot. The defense questioned the field of forensic podiatry and pressed Dr. Nirenberg on whether the measurements would be altered depending on how thick the sock covering the foot was woven.

Dr. Nirenberg was also interviewed on National Public Radio’s Morning Edition on April 14th 2023 about the gait of the bombing suspect associated with the capital riot on Wednesday January 6th, 2021. Dr. Nirenberg is president of the American Society of Forensic Podiatry and co-editor of the textbook: “Forensic Gait Analysis: Principles and Practice”. The bombing suspect had placed bombs at the DNC and RNC headquarters in Washington, DC on the night before. NPR asked Dr. Nirenberg to comment on the features of the person’s gait.

Additionally, Nirenberg was interviewed by Nancy Grace on her TV show Crime Stories. Grace interviewed Nirenberg about his forensic podiatry work in helping to solve the murder of a mother of 3 who was killed in a church. The case remains unsolved. The episode, “Fitness-Mom Missy Bevers Bludgeoned Dead in Creekside Church” aired June 6th, 2024 and is available online at Merit+ TV.

And, Netflix’s 2023 docu-series, “Till Murder Do Us Part”, recounts the killings of Derek and Nancy Haysom by including a series of interviews with a cast of real people. The four-part docu-series revolves around the unpacking of how a wealthy couple was murdered in Virginia in 1985. It also focuses on how the suspects, Elizabeth Haysom, and her boyfriend, Jens Soehring, betrayed each other during the trial. Dr. Sarah Reel DPM was the forensic podiatrist who was involved with Jens’ and Elizabeth’s footprint examination. Dr. Reel pointed out that, statistically, there was no difference “between a bare footprint and a socked footprint.” The doctor suggested that Jens’ reference footprint matched closely with the crime scene footprint.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

When owners of a security spread false information to pump up the price of the security and subsequently sell off their shares, making a profit—the “dump.”

Refer to attempts by investors to move the price of a stock opportunistically by selling large numbers of shares short. The investors pocket the difference between the initial price and the new, lower price after this maneuver. This technique is illegal under SEC rules, which stipulate that every short sale must be on an uptick. For more information on this complex tactic, read on in this piece from the Wharton School of Business.

Wash Trading

Involves the simultaneous or near-simultaneous sale and repurchase of the same security for the purpose of generating activity and increasing the price.

When fraudsters manipulate the market through matched orders, they enter trades to buy or sell securities with the knowledge that a matching order on the opposite side has been or will be entered. During his tenure at the Commission, our partner Jordan Thomas was involved in a case where the SEC won summary judgement and obtained settlements with an astonishing 16 defendants who engaged in matched trades, among other illicit tactics.

Painting the Tape

Painting the tape refers to placing successive orders in small amounts at increasing or decreasing prices.

Spoofing & Layering

High frequency traders are known to use the tactics of Spoofing & Layering to manipulate share prices. Spoofing is the placing of a bid or offer with the intent to cancel before execution. Layering is a form of spoofing in which the trader places multiple orders on one side of the book, in order to create a false impression of heavy buying or selling.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Although 97% of people aren’t yet millionaires, many could eventually meet that target if they start investing sooner rather than later; especially doctors [MD, DO, DPM, DDS or DMD].

A 20-year-old, for instance, needs to invest just $330 a month into an asset class that delivers a 7% to 8% annual return to reach $1.26 million by the time s/he turns 65 years old. The luxury of time significantly boosts your chances of becoming a millionaire.

This doesn’t mean it’s too late for middle-aged savers to reach that millionaire milestone, but it will take a significantly greater investment. If a 50-year-old doctor hasn’t started saving for retirement, s/he would need to invest $3,958 a month at a steady 7% return to reach $1.26 million by retirement.

However, according to one Goldman Sachs report, investors could expect the S&P 500 to deliver just 3% annualized nominal returns over the next 10 years.

After an average 13% yearly return for the past decade, a new strategy outside of the stock market may be needed for that level of outsized gain, especially if you’re late to investing.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Ikea Effect Bias describes the tendency of people to place a higher value on products they have partially created or assembled themselves. This phenomenon is named after the Swedish furniture retailer Ikea, known for selling furniture in flat-pack kits that customers must assemble at home.

he IKEA effect was identified and named by Michael Norton of Harvard Business School, Daniel Mochon of Yale University and colleague Dan Ariely PhD of Duke University, who published the results of three studies in 2011. They described the IKEA effect as “labor alone can be sufficient to induce greater liking for the fruits of one’s labor: even constructing a standardized bureau, an arduous, solitary task, can lead people to overvalue their (often poorly constructed) creations.”

Example: A prospect is more likely to pursue his/her own financial plan than that one from an informed financial planner, CPA or professional advisor.

2011 study found that subjects were willing to pay 63% more for furniture they had assembled themselves than for equivalent pre-assembled items.

IN FINANCE AND INVESTING

The IKEA effect can contribute to reducing panic selling. Investors typically reduce their stock market exposure after a financial crash which often results in “buy high, sell low” strategy that is detrimental to long-run wealth accumulation.

Ashtiani et al.’s study proposes a nudge utilizing the IKEA effect to counteract this phenomenon: “actively involving investors in the selection process of the risky investments, while restricting their selections in a way that preserves a large degree of diversification.”

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on September 1, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

Dear Medical Executive-Post Readers and Subscribers

***

HISTORY OF LABOR DAY

The first Labor Day holiday was celebrated on Sept. 5th, 1882, in New York City, in accordance with the plans of the Central Labor Union. President Grover Cleveland signed a law on June 28th, 1894, that made the first Monday in September of each year a national holiday, according to the Department of Labor.

***

***

MY SEPTEMBER HEALTH RE-SET

To give my health a boost after Labor Day, I’m taking a complete break from alcohol, sugar, cookies, ice cream, coffee and tea for the entire month of September. Besides that, I’ll also prioritize sleep and increase my exercise from 7 to at least 10 times [hours] a week. This will allow me to focus on my diet and mental well-being. It’s essentially a month of health and wellness rejuvenation.

I’ve chosen to focus on alcohol and sugar because I want to challenge the idea that moderate drinking is part of a healthy lifestyle. In reality, only those who maintain a healthy lifestyle can afford to enjoy alcohol in moderation. But, sugar is everywhere and must be minimized for Type II diabetes and weight control.

Moreover, the long-term and excessive intake of sugary beverages and refined sugars can negatively impact your overall caloric intake and create a domino effect on your health. For example, excess sugar in the body can turn into fat deposits and lead to fatty liver disease.

A low sugar diet can help you lose weight and also help you manage and/or prevent diabetes, heart disease and stroke, reduce inflammation, and even improve your mood and the health of your skin. That’s why the low sugar approach is a key tenet of other well-known healthy eating patterns, such as the Mediterranean diet and the DASH diet.

QUESTION: And so, do you also commit to such “factory resets” now and then? Please comments.

Do, enjoy the Labor Day Weekend, Bar-B-Ques with friends, family and colleagues. And, I hope you continue to find the Medical Executive-Post useful!

Many thanks for your likes and referrals. Dr. David Edward Marcinko MBA MEd CMP [Editor and Chief]

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on August 28, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL PROVIDER PAYMENTS LOWERED

***

***

Statistic: $2.8+ billion dollars

That’s how much Blue Cross and Blue Shield plans agreed to pay to settle litigation over claims they conspired to lower payments to providers. (Healthcare Dive)

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

A silent, non-directed, ghost, blind, faux, or “mirror” PPO, HMO, or other provider model is not really a formalized managed care organization [MCO] at all. Rather, it was simply an intermediary attempt, and Ponzi-like scheme, to negotiate practitioner fees downward, by promising a higher volume of patients in exchange for the discount.

Of course, the intermediary [discount-broker] then resells the packaged contract product to any willing insurance company, HMO, PPO or other payer, thereby pocketing the difference as a nice profit. Sometime, these virtual organizations are just indemnity companies in disguise.

NOTE: The term indemnity insurance refers to an insurance policy that compensates an insured party for certain unexpected damages or losses up to a certain limit—usually the amount of the loss itself. Insurance companies provide coverage in exchange for premiums paid by the insured parties.

These policies are commonly designed to protect professionals and business owners when they are found to be at fault for a specific event such as misjudgment or malpractice. They generally take the form of a letter o indemnity.

***

As part of a silent PPO scheme, insurers try to pass off the discount as legitimate on Explanation of Benefit [EOB] forms. Physicians should not fall for this ploy, since pricing pressure will be forced even lower in the next round of “real” PPO negotiations!

Medical providers should also be on guard for silent HMOs, MCOs and any other silent insurance variation, since these virtual organizations do not exist, except as exploitable arbitrage situations for the middleman.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

It is normal for physician litigants to develop a case of “buyer’s remorse” after any mediation or divorce settlement. They may feel disappointed after entering into a settlement agreement or feel that they received a bad deal.

Mediation: Some advantages of divorce mediation over divorce litigation include:

◊ Mediation is generally faster and less costly.

◊ Mediation is voluntary, private and confidential.

◊ Mediation facilitates creative and realistic solutions.

◊ Mediation allows parties to control their agreements.

◊ Mediation eliminates a win-lose atmosphere and result.

◊ Mediation provides a forum for addressing future disputes.

◊ Mediation fosters communication and helps mend relationships.

***

***

Settlement

And so, in a vast majority of cases, mediation and settlement is probably a good deal. In fact, it is probably a great deal because you are receiving something without having to risk losing. Remember, trial can be a crap-shoot, and nothing is worse than losing it all at the time of trial.

Bench trial verdict by a trial judge.

Jury trial verdict by your “peers.”

Instead, you entered into a settlement agreement and now your divorce case is over.

But beware since trying to get out of a settlement agreement reached at mediation or settlement is virtually impossible.

Why? Well, there is a strong interest by the court to enforce mediation and settlement agreements. The court wants your divorce case to be over and off its docket. There are a few very narrow exceptions; for example, if one party was truly coerced because someone held a gun to their head. But that rarely happens, and it certainly doesn’t happen to most doctors or dentists.

Of course, you can fight against your mediation or settlement agreement if you like, but you won’t get too far. There’s an old adage in the law that a bad settlement is better than a great trial. That’s because no one knows how a judge or jury will rule come time of trial.

***

***

This buyers remorse phenomenon also isn’t uncommon among people who receive sudden wealth, whether through divorce settlements, inheritances, lottery winnings, or other windfalls.

Assessment

Financial advisors often see clients struggle with “sudden wealth syndrome”—the inability to properly manage a large sum of money they’re not accustomed to having.

Common mistakes include:

Lifestyle inflation without sustainable income to support it.

Poor investment decisions or lack of investment planning.

Emotional spending following traumatic life events like divorce.

Failure to set aside money for taxes on the settlement.

Not creating a long-term financial plan for the money.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on August 22, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

Medicine today is vastly different than a generation ago, and all health care professionals need new skills to be successful and reduce the emerging risks outlined in this textbook, as well as the “unknown-unknowns” elsewhere. Traditionally, the physician was viewed as the “captain of the ship”. Today, their role may be more akin to a ship’s navigator, using clinical, teaching skills and knowledge to chart the patient’s course through a confusing morass of insurance requirements, fees, choices, rules and regulations to achieve the best attainable clinical outcomes.

This new leadership paradigm includes many classic business school principles, now modified to fit the decade long PP-ACA, the era of health reform, and modern technical connectivity and EMRs.

Thus, the physician must be a subtle guide on the side; not bombastic sage on the stage. These, newer health 3.0 leadership philosophies might include:

•Negotiation – working to optimize appropriate treatment plans; ie., quality of life versus quantity of life, •Team play – working in concert with other allied healthcare professionals to coordinate care delivery ,ithin a clinically appropriate and cost-effective framework; •Working within the limits of competence – avoiding the pitfalls of the medical generalist versus the specialist that may restrict access to treatment, medications, physicians and facilities by clearly acknowledging when a higher degree of service is needed on behalf of the patient – all while embracing holistic primary care; •Respecting different cultures and values – inherent in the support of the medical Principle of Autonomy is the acceptance of values that may differ from one’s own. As the US becomes more culturally hetero geneous, medical providers are called upon to work within, and respect, the socio-cultural and/or spiritual framework of patients, students and their families; •Seeking clarity on what constitutes marginal care – within a system of finite resources; providers are called upon to openly communicate with patients regarding access to marginal medical information and/or treatments. •Supporting evidence-based practice – healthcare providers, should utilize outcomes data to reduce variation in treatments to achieve higher efficiencies and improved care delivery thru evidence based medicine [EBM]; •Fostering transparency and openness in communications – healthcare professionals should be willing, and prepared, to discuss all aspects of care, especially when discussing end-of-life issues or when problems arise; •Exercising decision-making flexibility – treatment algorithms, templates and clinical pathways are useful tools when used within their scope; but providers must have the authority to adjust the plan if circumstances warrant.

Becoming skilled in the art of listening and interpreting — In her ground-breaking book, Narrative Ethics: Honoring the Stories of Illness, Rita Charon, MD PhD, a professor at Columbia University, writes of the extraordinary value of using the patient’s personal story in the treatment plan. She notes that, “medicine practiced with narrative competence will more ably recognize patients and diseases; convey knowledge and regard, join humbly with colleagues, and accompany patients and their families through ordeals of illness.” In many ways, attention to narrative returns medicine full circle to the compassionate and caring foundations of the patient-physician relationship.

These thoughts represent only a handful of examples to illustrate the myriad of new skills that tomorrows’ healthcare professionals must master in order to meet their timeless professional obligations of compassionate care and contemporary treatment effectiveness; all within the context modern risk management principles.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on August 20, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

LEADERSHIP versus MANAGEMENT

***

***

By Dr. David Edward Marcinko MBA MEd

By Professor Gary A. Cook PhD

By Professor Eugene Schmuckler PhD MBA MEd CTS

Many of us have encountered a person who may intellectually be at upper levels, but whose ability to interact with others appears to that of one who is highly immature. This is the individual who is prone to becoming angry easily, verbally attacks co-workers, is perceived as lacking in compassion and empathy, and cannot understand why it is difficult to get others to cooperate with them and their agendas.

THINK: Sheldon Cooper PhD D.Sc MA BA of the The Big Bank Theory TV show.

The concept of Emotional Intelligence [EQ] was brought into the public domain when Daniel Goleman authored a book entitled, Emotional Intelligence.” According to Goleman, emotional intelligence consists of four basic non-cognitive competencies: self awareness, social awareness, self management and social skills. These are skills which influence the manner in which people handle themselves and their relationships with others. Goleman’s position was that these competencies play a bigger role than cognitive intelligence in determining success in life and in the workplace. He and others contend that emotional intelligence involves abilities that may be categorized into five domains:

Self awareness: Observing and recognizing a feeling as it happens.

Managing emotions: Handling feelings so that they are appropriate; realizing what is behind a feeling; finding ways to handle fears and anxieties, anger and sadness.

Motivating oneself; Channeling emotions in the service of a goal; emotional self control; delaying gratification and stifling impulses.

Empathy: Sensitivity to others’ feelings and concerns and taking their perspective appreciating the differences in how people feel about things.

Handling relationships: Managing emotions in others; social competence & social skills.

In 1995, Goleman then expanded on the works of Howard Gardner, Peter Salovey and John Mayer. He further defined Emotional Intelligence as a set of competencies demonstrating the ability one has to recognize his or her behaviors, moods and impulses and to manage them best, according to the situation. Mike Poskey, in “The Importance of Emotional Intelligence in the Workplace.” continued this definition by stating that emotional intelligence is considered to involve emotional empathy; attention to, and discrimination of one’s emotions; accurate recognition of one’s own and others’ moods; mood management or control over emotions; response with appropriate emotions and behaviors in various life situations (especially to stress and difficult situations); and balancing of honest expression of emotions against courtesy, consideration, and respect.

Source: Emotional Intelligence: what is and why it matters” – Cary Cherniss, PhD, presented at the annual conference of the Society of Industrial and Organizational Psychology, April 2000.

EQ differs from what has generally been considered intelligence which is described in terms of one’s IQ.

Traditional views of intelligence focused on cognition, memory and problem solving. Even today individuals are evaluated on the basis of cognitive skills. Entrance tests for medical, law, business, undergraduate and graduate schools base admissions in large part on the scores of the SAT, GMAT, LSAT, MCAT, etc. Without question, cognitive ability is critical but has been demonstrated, it is not a very good predictor of future direct job performance and indirect liability management. In fact, in 1940, David Wechsler the developer of a widely used intelligence test made reference to “non-intellective” elements. By this Wechsler meant affective, personal and social factors.

Source: Non-Intellective factors in intelligence. Psychological Bulletin, 37, 444-445.

Goleman became aware of the work of Salovey and Mayer having trained under David McClelland and was influenced by McClelland’s concern with how little traditional tests of cognitive intelligence predicted success in life. In fact, a study of 80 PhDs in science underwent a battery of personality tests, IQ tests and interviews in the 1950s while they were graduate students at Berkeley. Forty years later they were re-evaluated and it turned out that social and emotional abilities were four times more important than IQ in determining professional success and prestige.

Source: Feist & Barron: Emotional Intelligence and academic intelligence in career and life success. Paper presented at the Annual Convention of the American Psychological Society, San Francisco, 1996.

Undoubtedly, we want to have individuals work with us who have persistence which enables to them have the energy, drive, and thick skin to develop and close new business, or to work with the patients and other members of the staff. It is important to note that working alongside one with a “good” personality may be fun, energetic, and outgoing.

However, a “good personality does not necessarily equate to success. An individual with a high EQ can manage his or her own impulses, communicate effectively, manage change well, solve problems, and use humor to build rapport in tense situations. This clarity in thinking and composure in stressful and chaotic situations is what separates top performers from weak performers.

Poskey outlined a set of five emotional intelligence competencies that have proven to contribute more to workplace achievement than technical skills, cognitive ability, and standard personality traits combined.

***

***

A. Social Competencies: Competencies that Determine How We Handle Relationships

Intuition and Empathy – Our awareness of others’ feelings, needs, and concern. He suggested that this competency is important in the workplace for the following reasons:

Understanding others: an intuitive sense of others’ feelings and perspectives, and showing an active interest in their concerns and interests

Patient service orientation: the ability to anticipate, recognize and meet customer’s’ (patients) needs

People development: ability to sense what others need in order to grow, develop, and master their strengths

Leveraging diversity: cultivating opportunities through diverse people.

B. Political Acumen and Social Skills: Our adeptness at inducing desirable responses in others. This competency is important for the following reasons:

Influencing: using effective tactics and techniques for persuasion and desired results.

Communication: sending clear and convincing messages that are understood by others

Leadership: inspiring and guiding groups of people

Change catalyst: initiating and/or managing change in the workplace

Conflict resolution: negotiating and resolving disagreements with people

Collaboration and cooperation: working with coworkers and business partners toward shared goals

Team capabilities: creating group synergy in pursuing collective goals.

C. Personal Competencies: Competencies that determine how we manage ourselves

D. Self Awareness: Knowing out internal states, preferences, resources, and intuitions. This competency is important for the following reasons.

Emotional awareness: recognizing one’s emotions and their effects and impact on those around us

Accurate self-assessment: knowing one’s strengths and limits

Self-confidence: certainty about one’s self worth and capabilities

Self-Regulation: managing one’s internal states, impulses, and resources. This competency is important in the workplace for the following reasons.

Self-control: managing disruptive emotions and impulses

Trustworthiness: maintaining standards of honesty and integrity

Conscientiousness: taking responsibility and being accountable for personal performance

Adaptability: flexibility in handling change

Innovation: being comfortable with an openness to novel ideas, approaches, and new information.

E. Self-Expectations and Motivation: Emotional tendencies that guide or facilitate reaching goals. This competency is important in the workplace for the following reasons.

Achievement drive: striving to improve or meet a standard of excellence we impose on ourselves

Commitment: aligning with the goals of the group or the organization

Initiative: readiness to act on opportunities without having to be told

Optimism: Persistence in pursuing goals despite obstacles and setbacks

A note of caution is necessary. Goleman and Salovey both stated that emotional intelligence on its own is not a strong predictor of job performance. Instead they contend that it provides the bedrock for competencies that are predictors.

Obviously, EQ is an important attribute and it behooves each of us to promote emotional intelligence in the workplace. A number of guidelines have been developed for the Consortium for Research on Emotional Intelligence in Organizations by Goleman and Cherniss. The guidelines cover 21 phases which include preparation, training, transfer and evaluation.

Assess the organization’s needs: Determine the competencies that are most critical for effective job performance in a particular type of job. In doing so, us a valid method, such as the comparison of the behavioral interviews of superior performs and average performers. Also make sure the competencies to be developed are congruent with the organization’s culture and overall strategy.

Assess the individual: This assessment should be based on the key competencies needed for a particular job, and the data should come from multiple sources using multiple methods to maximize credibility and validity.

Deliver assessments with care: Give the individual information on his/her strengths and weaknesses. In doing so, try to be accurate and clear. Also, allow plenty of time for the person to digest and integrate the information. Provide feedback in a safe and supportive environment in order to minimize resistance and defensiveness. Avoid making excuses or downplaying the seriousness of deficiencies.

Maximize choice: People are motivated to change when they freely choose to do so. As much as possible, allow people to decide whether or not they will participate in the development process, and have them change goals themselves.

Encourage people to participate: People will be more likely to participate in development efforts if they perceive them to be worthwhile and effective. Organizational policies and procedures should encourage people to participate in development activity, and supervisors should provide encouragement and the necessary support. Motivation will be enhanced if people trust the credibility of those who encourage them to undertake the training.

Link learning goals to personal values: People are most motivated to pursue change that fits with their values and hopes. If a change matters little to people, they won’t pursue it. Help people understand whether a given change fits with what matters most to them.

Adjust expectations: Builds positive expectations by showing learners that social and emotional competence can be improved and that such improvement will lead to valued outcomes. Also, make sure that the learner has a realistic expectation of what the training process will involve.

Gauge readiness: Assess whether the individual is ready for training. If the person is not ready because of insufficient motivation or other reasons, make readiness the focus of intervention efforts.

Foster a positive relationship between the trainers and learners: Trainers who are warm, genuine, and empathic our best able to engage the learners in the change process. Select trainers who have these qualities, and make sure that they use them when working with the learners.

Make change self-directed: Learning is more effective when people direct their own learning program, tailoring it to their unique needs and circumstances. In addition to allowing people to set their own learning goals, let them continue to be in charge of their learning throughout the program, and tailor the training approach to the individual’s learning style.

Set clear goals: People need to be clear about what the competence is, how to acquire it, and how to show it on the job. Spell out the specific behaviors and skills that make up the target competence. Make sure that the goals are clear, specific, and optimally challenging.

Break goals into manageable steps: change. That is more likely to occur if the change process is divided into manageable steps. Encourage both trainers and trainees to avoid being overly ambitious.

Provide opportunities to practice: Lasting change requires sustained practice on the job and elsewhere in life. An automatic habit is being unlearned and different responses are replacing it. Use naturally occurring opportunities for practice at work, and in life. Encourage the trainees to try the new behaviors repeatedly and consistently over a period of months.

Give performance feedback: Ongoing feedback encourages people and direct change. Provide focused and sustained feedback as the learners practice new behaviors. Make sure that supervisors, peers, friends, family members-or some combination of these- give periodic feedback on progress.

Rely on experiential methods: Active, concrete, experiential methods tend to work best for learning social and emotional competencies. Development activities that engage all the senses and our dramatic and powerful can be especially effective.

Build in support: Change is facilitated through ongoing support of others who are going through similar changes. Programs should encourage the formation of groups where people give each other support, throughout the change effort. Coaches and mentors also can be valuable in helping support the desired change.

Use models: Use modern webinars, patient portals, live or videotaped models that clearly show how the competency can be used in realistic situations. Encourage learners to study, analyze, and emulate the models.

Enhance insight: Self-Awareness is the cornerstone of emotional and social competence. Help learners acquire greater understanding about how their thoughts, feelings, and behavior affect themselves and others.

Prevent relapse: Use relapse prevention, which helps people use lapses and mistakes as lessons to prepare themselves for further efforts.

Moreover:

Encourage use of skills on the job: Supervisors, peers and subordinates should reinforce and reward learners for using their new skills on the job. Coaches and mentors also can serve this function. Also, provide prompts and cues, such as through periodic follow-ups. Change also is more likely to indoor. When high status persons, such as supervisors and upper-level management model it.

Develop an organizational culture that supports learning: Change will be more enduring if the organization’s culture and tone support the change and offer a safe atmosphere for experimentation.

Finally, see if the development effort has lasting effects evaluated. When possible, find a true set of measures of the competence or skill, as shown on the job, before and after training, and also at least two months later. One-year follow-ups also are highly desirable. In addition to charting progress on the acquisition of competencies, also assess the impact on important job related outcomes, such as performance measures, and indicators of adjustments such as absenteeism, grievances, health status, etc.

Managers V. Leaders

These abilities are important for one to be successful as a manager and even more so as a leader, or physician executive. But, before we begin an examination of strategic leadership, it is necessary to make a deeper distinction between a manager and a leader. There are many different definitions as well as descriptions regarding leadership and management.

Many people talk as though leadership and management is the same thing. Fundamentally, they are quite different. Management focuses on work. We manage work activities such as money, time, paperwork, materials, equipment, and personnel, among other things. As can be found in any basic book on management, management focuses on planning, organizing, controlling, coordinating, budgeting, finance and money management as well as decision making. In effect, managers are generally those individuals who have been given their authority by virtue of their role. It is the function of a manager to ensure that the work gets done as well as to oversee the activities of others. In many healthcare organizations we find that those individuals elevated to a managerial position occur as a result of being a high performer on their previous assignment. A manager receives authority on the basis of role; while a leader’ authority is more innate in nature.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on August 19, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

In today’s dynamic economic landscape, the concept of a “side hustle” has evolved from a mere trend to an essential component of personal financial strategy for many individuals; even doctors.

A side hustle is a way to earn extra income outside of your primary job or main source of employment. It typically involves part-time work, freelancing, small businesses, or gig-based activities that can be pursued flexibly in your free time. Unlike traditional employment, side hustles often offer more autonomy, creative freedom, and the potential to monetize skills, hobbies, or passions.

***

***

Doctor Gigs?

So, if you’re a doctor, dentist or podiatrist considering a side hustle, focus on something sustainable and long-term. Ask yourself: What am I already good at? What do people already ask me to help with? The best side hustles don’t require reinventing the wheel — just monetizing the one you’ve already been pushing uphill.

But, avoid gigs that require a huge upfront investment or promise overnight success. Instead, look for something that offers flexibility, ideally something that works with your schedule, not against your sanity.

Track your earnings and how much time you’re putting in. Side income should support your goals, whether that’s paying off debt, saving for a trip or just breathing easier when office rent comes due.

But, if it’s draining your energy from your medical practice with little to show for it, it might be time to rethink the hustle.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

UnitedHealth Group soared almost 12%, its biggest one-day gain in nearly five years, after getting the “Buffett Bounce.” Buffett’s Berkshire Hathaway revealed it bought ~5 million shares worth nearly $1.6 billion, giving a much-needed vote of confidence to the struggling health giant.

The White House is considering buying part of Intel, Bloomberg reported this week, which would be the latest big business deal the president pursues on behalf of the government. The Trump administration might acquire a stake in the struggling computer chip-maker using CHIPS Act funding—nearly $11 billion of which was already earmarked for Intel.

Saudi Arabia’s Public Investment Fund took an $8 billion write-down on five mega-projects it’s building, due to lower oil prices and higher costs.

Pimco, the asset management giant, warned that President Trump’s plan to IPO Fannie Mae and Freddie Mac could push mortgage rates higher.

Whatever the statistics regarding physician standard of living, the reality is that within most marriages the husband more frequently takes responsibility for understanding and managing the finances. Additionally, women are more likely to remain in the marital home following a separation, thus inheriting a large fixed expense that may prove be an excessive, albeit short-term burden to them. At the time the decision is made to separate or divorce, many women do not have an understanding of how to manage their household budget, or how to manage their assets and liabilities.

An issue many divorcing physicians face is that the other spouse (in the past the wife), may have concentrated their energies on managing the home, while the physician concentrated on earning and managing the finances. The problems of the spouse of a physician are often compounded in divorce; not only do they not understand their personal finances, but that their absence from the work force has made them financially dependent on the other.

At what probably be the most emotionally taxing time in their lives, they are forced to play catch-up.

***

***

Taking a more active role in their own financial planning during the marriage may help the spouse of a physician avoid some of the financial pitfalls of separation and divorce.

NOTE: Barbara Stanny provides an excellent overview and reading bibliography on how people can get smart about money in her book Prince Charming Isn’t Coming. [1]

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

An important component of hospital credit analysis is essentiality. Hospitals are unusual businesses that many times possess some form of essentiality to their communities. Health care is important to the economic vitality of every community. Many hospitals have served their communities for many years; it is not uncommon to find hospitals that have been continuously operating for more than 100 years in the same community.

Most hospitals are not-for-profit. In not-for-profit hospitals, no private party actually “owns” the hospital; control is vested in various boards, but no one explicitly owns a not-for-profit hospital. In a broad sense, communities own not-for-profit hospitals. They are considered “charities” with a “charitable purpose.” Though a not-for-profit hospital may not have owners, it has many “stakehold-ers,” parties that have vested interests in the continuing success of the hospital.

Many hospitals have broad and vast webs of stakeholders. Stakeholders are why hospitals rarely close or are shut down. Too many stakeholders have interests in the continuing successful operation of hospitals.

Another dimension of the essentiality analysis is service analysis. How significant are the hospital’s services? If the hospital shuts down, what population segments would suffer? How significant is the population that would suffer? How much would they suffer?

And so, hospital stakeholder relationships need to be considered in the analysis of essentiality. How strong are these relations? How many are there? How important is the continuing success of this hospital to these stakeholders?

Analysis of hospital’s stakeholders and services should provide a credible view of the degree of essentiality associated with a hospital. Higher degrees of essentiality suggest higher likelihoods that hospitals, one way or another, will meet their commitments, particularly their payment commitments.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

According to Wikipedia, Phantom debt or zombie debt is a debt that is old, defaulted, or not owed and is somehow still being pursued for collection to be paid by the presumed debtor. It generally refers to debt that is more than 3 years old, is long forgotten about or belonged to someone else – like someone with the same name or a deceased parent. The amount owed can grow to hundreds or thousands of dollars more than what was originally owed.

An example of this is from George Miller. George missed an 11 cent Verizon bill and seven years later it had grown to $4,000.00.

Sometimes it was never owed, was owed by a deceased parent, or that was previously owed by the presumed debtor, but was previously paid in full, settled, discharged via bankruptcy or a dismissed court case, is beyond the statute of limitations, or is otherwise not legally collectible, but that a collection agency or other similar service is aggressively attempting to collect, often fraudulently.

While the concept of phantom debt is quite old, it has gotten a lot of attention since the 1990s.

Very often, collectors of phantom debt use intimidating, abusive, or otherwise illegal tactics in an attempt to collect phantom debt that include frequent phone calls, calls to the victim’s place of employment, or threats of scary consequences against the victim that sometimes include arrest and/or criminal prosecution. In the USA, such tactics violate the Fair Debt Collection Practices Act [FDCPA]

The source of phantom debt may be from collectors who buy the debt from other collectors for pennies on the dollar, some of which take action that is not legal in order to collect that debt. Unlawful techniques used include suing or threatening to sue, re-aging the debt on the victim’s credit report to circumvent limits on reporting, or falsely promising to remove a negative credit report entry in exchange for a partial payment.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Doctors and dentists earn money by treating patients. CPAs and Attorneys have clients, and retail stores buy items low and sell them at higher prices. This is called a business model.

More formally, a business model identifies the products or services the business plans to sell, the target market, and any anticipated expenses, in order to outline how to generate a profit. Business models are important for both new and established businesses. They help companies attract investment, recruit talent, and motivate management and staff.

Businesses should regularly update their business model, or they’ll fail to anticipate trends and challenges ahead. Business models also help investors to evaluate companies that interest them and employees to understand the future of a company they may aspire to join.

***

The Business Model of Pharmacy Benefits Managers

In the United States, health insurance providers often hire a third party to handle price negotiations, insurance claims, and distribution of prescription drugs. Providers that use such pharmacy benefit managers include commercial health plans, self-insured employer plans, Medicare Part D [drug] plans, the Federal Employees Health Benefits Program, and state government employee plans. PBMs are designed to aggregate the collective buying power of en-rollees through their client health plans, enabling plan sponsors and individuals to obtain lower prices for their prescription drugs. PBMs negotiate price discounts from retail pharmacies, rebates from pharmaceutical manufacturers, and mail-service pharmacies which home-deliver prescriptions without consulting face-to-face with a pharmacist.

Pharmacy benefit management companies can make revenue in several ways.

First, they collect administrative and service fees from the original insurance plan.

Then, they can also collect rebates from the manufacturer.

Traditional PBMs do not disclose the negotiated net price of the prescription drugs, allowing them to resell drugs at a public list price (also known as a sticker price), which is higher than the net price they negotiate with the manufacturer. This practice is known as “spread pricing”. The industry argues that savings are trade secrets. Pharmacies and insurance companies are often prohibited by PBMs from discussing costs and reimbursements. This leads to lack of transparency.

***

***