BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on November 16, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

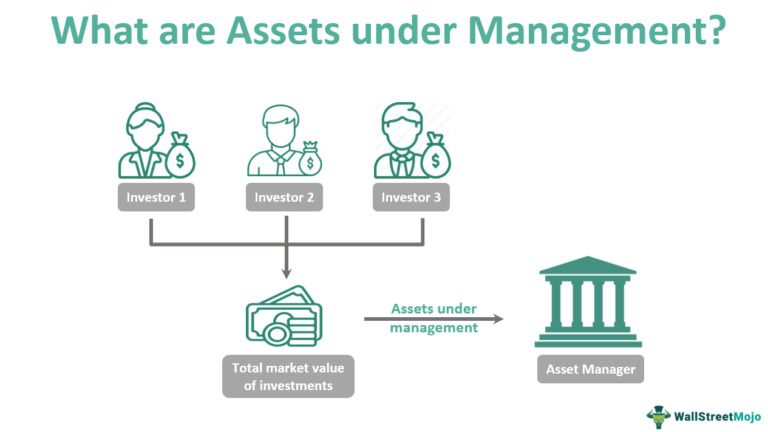

American Depository Receipts Defined

In the modern era of globalization, financial instruments that connect investors across borders have become indispensable. Among these, American Depository Receipts (ADRs) stand out as a powerful mechanism that allows U.S. investors to participate in foreign equity markets without the complexities of international trading. ADRs not only simplify access to global companies but also enhance the ability of foreign corporations to raise capital in the United States. This essay explores the origins, structure, regulatory frameworks, benefits, risks, and real-world examples of ADRs, highlighting their role in the integration of global finance.

Historical Development

The concept of ADRs emerged in 1927 when J.P. Morgan introduced the first ADR for the British retailer Selfridges. At the time, American investors faced significant hurdles in purchasing foreign shares, including currency conversion, unfamiliar trading practices, and regulatory differences. ADRs solved these problems by creating a U.S.-based certificate that represented ownership in foreign shares, denominated in dollars, and traded on American exchanges.

Over the decades, ADRs expanded rapidly, especially during the post-World War II era when globalization accelerated. By the late 20th century, ADRs had become a mainstream tool for accessing international equities, with companies from Europe, Asia, and Latin America increasingly using them to tap into U.S. capital markets.

Structure and Mechanics

An ADR is issued by a U.S. depositary bank, which holds the underlying shares of a foreign company in custody. Each ADR corresponds to a specific number of shares—sometimes one, sometimes multiple, or even a fraction. Investors buy and sell ADRs in U.S. dollars, and dividends are paid in dollars as well, eliminating the need for currency conversion.

Key structural features include:

Depositary Banks: Institutions such as J.P. Morgan, Citibank, and Bank of New York Mellon act as custodians and issuers of ADRs.

ADR Ratios: The number of foreign shares represented by one ADR can vary, allowing flexibility in pricing.

Trading Platforms: ADRs can be listed on major exchanges like the NYSE or NASDAQ, or traded over-the-counter.

Regulatory Framework

ADRs are subject to U.S. securities regulations, which vary depending on the level of ADR issued:

Level I ADRs: Traded over-the-counter, requiring minimal disclosure. They are primarily used for visibility rather than fundraising.

Level II ADRs: Listed on U.S. exchanges, requiring compliance with SEC reporting standards, including reconciliation of financial statements to U.S. GAAP or IFRS.

Level III ADRs: Allow foreign companies to raise capital directly in U.S. markets through public offerings. These require the highest level of regulatory compliance, including registration with the SEC and adherence to corporate governance standards.

This tiered system ensures that investors receive appropriate levels of transparency while giving foreign companies flexibility in their approach to U.S. markets.

Benefits for Investors

ADRs offer numerous advantages to American investors:

Convenience: Investors can buy shares in foreign companies without dealing with foreign exchanges or currencies.

Diversification: ADRs provide access to global firms across industries, enhancing portfolio diversification.

Transparency: ADRs listed on U.S. exchanges must comply with SEC regulations, ensuring reliable financial reporting.

Liquidity: ADRs trade on familiar platforms, making them easily accessible to retail and institutional investors alike.

Benefits for Companies

Foreign corporations also benefit significantly from ADRs:

Access to Capital: ADRs open the door to the world’s largest pool of investors.

Global Visibility: Listing in the U.S. enhances reputation and credibility.

Improved Liquidity: Shares become more widely traded, increasing market efficiency.

Investor Base Diversification: Companies can attract both domestic and international investors, reducing reliance on local markets.

Risks and Challenges

Despite their advantages, ADRs carry certain risks:

Currency Risk: ADR values are tied to foreign shares denominated in local currencies, making them vulnerable to exchange rate fluctuations.

Political and Economic Risk: Instability in the issuing company’s home country can affect performance.

Taxation: Dividends may be subject to foreign withholding taxes before conversion to U.S. dollars.

Regulatory Differences: Even with SEC oversight, differences in accounting standards and corporate governance can pose challenges.

Case Studies

1. Alibaba Group (China) Alibaba’s ADRs, listed on the NYSE in 2014, marked one of the largest IPOs in history, raising $25 billion. This demonstrated the power of ADRs to connect Chinese companies with American investors, despite regulatory complexities between the two countries.

2. Toyota Motor Corporation (Japan) Toyota’s ADRs have long provided U.S. investors with access to one of the world’s largest automakers. By listing ADRs, Toyota expanded its investor base and strengthened its global presence.

3. Royal Dutch Shell (Netherlands/UK) Shell’s ADRs illustrate how multinational corporations use ADRs to maintain visibility in U.S. markets while managing complex cross-border structures.

The Role of ADRs in Global Finance

ADRs embody the globalization of capital markets. They facilitate cross-border investment, enhance market efficiency, and foster economic integration. For investors, ADRs represent a gateway to international diversification. For companies, they provide access to the deepest capital markets in the world.

Conclusion

American Depositary Receipts are more than just financial instruments; they are symbols of global interconnectedness. By bridging the gap between U.S. investors and foreign companies, ADRs have reshaped the landscape of international finance. They balance convenience with exposure to global risks, offering both opportunities and challenges. As globalization continues to evolve, ADRs will remain a vital tool for investors and corporations alike, reinforcing their role as a cornerstone of modern capital markets.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

BASIC DEFINITIONS

***

***

The velocity of money is a fundamental concept in macroeconomics that measures how quickly money circulates through the economy. It reflects the frequency with which a unit of currency is used to purchase goods and services within a given time period. This metric is crucial for understanding economic activity, inflation, and the effectiveness of monetary policy.

At its core, the velocity of money is calculated using the formula:

This equation shows how many times money turns over in the economy to support a given level of economic output. For example, if the GDP is $20 trillion and the money supply (say, M2) is $10 trillion, the velocity is 2—meaning each dollar is used twice in a year to purchase goods and services.

There are different measures of money supply used in this calculation, most commonly M1 and M2. M1 includes the most liquid forms of money, such as cash and checking deposits, while M2 includes M1 plus savings accounts and other near-money assets. The choice of which measure to use depends on the context and the specific economic analysis being conducted.

The velocity of money is influenced by several factors:

Consumer and business confidence: When people feel optimistic about the economy, they are more likely to spend rather than save, increasing velocity.

Interest rates: Higher interest rates can encourage saving and reduce spending, lowering velocity. Conversely, lower rates can stimulate borrowing and spending.

Inflation expectations: If people expect prices to rise, they may spend more quickly, increasing velocity.

Technological and structural changes: Innovations in digital payments and shifts in consumer behavior can also affect how quickly money moves.

Historically, the velocity of money has fluctuated with economic cycles. During periods of economic expansion, velocity tends to rise as spending increases. In contrast, during recessions or periods of uncertainty, velocity often falls as consumers and businesses hold onto cash. For instance, during the 2008 financial crisis and the early stages of the COVID-19 pandemic, velocity dropped sharply due to reduced consumer spending and increased saving.

In recent years, the U.S. has experienced persistently low velocity, even amid significant increases in the money supply. This phenomenon has puzzled economists and raised questions about the effectiveness of monetary policy. Despite aggressive stimulus measures, much of the new money has remained in savings or financial markets rather than circulating through the real economy.

Understanding the velocity of money is essential for policymakers. A low velocity may signal weak demand and justify expansionary fiscal or monetary policies. Conversely, a high velocity could indicate overheating and the need for tightening measures to prevent inflation.

In conclusion, the velocity of money is a dynamic indicator of economic vitality. It helps economists and central banks assess the flow of money, the strength of demand, and the potential for inflation.

While often overlooked by the public, it plays a vital role in shaping economic policy and understanding the broader health of the economy.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Physicians are increasingly facing car repossessions in 2025 due to rising debt, high vehicle prices, and economic pressures that are reshaping the financial landscape for medical professionals.

Traditionally viewed as financially secure, doctors are now among the growing number of Americans struggling to keep up with auto loan payments. The surge in car repossessions—expected to reach a record 10.5 million assignments by the end of 2025—has not spared the medical community. While physicians often earn higher-than-average incomes, they also carry significant financial burdens, including student loan debt, practice overhead, and personal expenses. These pressures are being amplified by macroeconomic forces such as inflation, high interest rates, and stagnant reimbursement rates.

One of the key contributors to this trend is the soaring cost of vehicles. In 2025, the average price of a new car in the U.S. surpassed $50,000, a dramatic increase from just a decade ago. For physicians who rely on vehicles for commuting between hospitals, clinics, and private practices, owning a reliable car is not a luxury—it’s a necessity. However, the combination of high sticker prices and elevated interest rates—averaging 7.3% for used cars and 11.5% for new cars—has made financing increasingly difficult.

***

***

Even high-income professionals are not immune to the broader auto loan crisis. Subprime auto loan delinquencies reached 6.6% in early 2025, the highest rate in over 30 years.While physicians typically fall into the prime or super-prime credit categories, many are still affected by cash flow disruptions, especially those in private practice or rural areas where patient volumes and insurance reimbursements have declined. Additionally, younger doctors with substantial student debt may find themselves overleveraged, making it harder to keep up with car payments.

The emotional and professional toll of a car repossession can be significant. Beyond the embarrassment and logistical challenges, losing a vehicle can disrupt a physician’s ability to provide care, attend emergencies, or maintain a consistent work schedule. This can lead to further income loss, creating a vicious cycle of financial instability.

To combat this trend, some physicians are turning to financial advisors to restructure their debt, refinance auto loans, or downsize to more affordable vehicles. Others are advocating for systemic reforms, such as student loan forgiveness, higher Medicare reimbursements, and better financial literacy training during medical education.

In conclusion, the rise in car repossessions among doctors is a stark reminder that no profession is immune to economic volatility. As the cost of living continues to climb and financial pressures mount, even those in traditionally stable careers must adapt to protect their assets and livelihoods.

Addressing this issue requires both individual financial planning and broader policy changes to ensure that physicians can continue to serve their communities without the looming threat of personal financial collapse.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 12, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

Say’s Law, named after the French economist Jean‑Baptiste Say, is a foundational idea in classical economics. Often summarized as “supply creates its own demand,” the law suggests that the act of producing goods and services inherently generates the income necessary to purchase them. This principle shaped economic thought throughout the 19th century and continues to influence debates about markets, government intervention, and the causes of economic crises.

Origins and Meaning Jean‑Baptiste Say introduced his law in the early 1800s in his Treatise on Political Economy. He argued that production is the source of demand: when producers create goods, they pay wages, rents, and profits, which in turn become purchasing power. In this view, general overproduction is impossible because every supply of goods corresponds to an equivalent demand. If imbalances occur, they are temporary and limited to specific sectors, not the economy as a whole.

Core Principles Say’s Law rests on several assumptions:

Markets are self‑correcting: Any surplus in one area leads to adjustments in prices and production.

Money is neutral: It serves only as a medium of exchange, not as a driver of demand.

Production drives prosperity: Economic growth depends on increasing output, not stimulating consumption.

No long‑term unemployment: Since supply creates demand, workers displaced in one industry will eventually find employment elsewhere.

These ideas aligned with classical economists’ belief in minimal government intervention and the efficiency of free markets.

Influence on Classical Economics Say’s Law became a cornerstone of classical economics, reinforcing the belief that recessions or depressions were temporary and self‑correcting. Economists like David Ricardo and John Stuart Mill adopted versions of the law, using it to argue against policies aimed at stimulating demand. The law supported laissez‑faire approaches, suggesting that governments should avoid interfering with markets, as production itself would ensure economic balance.

Criticism and Keynesian Revolution Say’s Law faced its greatest challenge during the Great Depression of the 1930s. Widespread unemployment and idle factories contradicted the idea that supply automatically generates demand. John Maynard Keynes famously rejected Say’s Law in his General Theory of Employment, Interest, and Money (1936). Keynes argued that demand, not supply, drives economic activity. He showed that insufficient aggregate demand could lead to prolonged recessions, requiring government intervention through fiscal and monetary policies.

Keynes’s critique marked a turning point in economics. While Say’s Law emphasized production, Keynesian economics highlighted consumption and demand management. This shift reshaped economic policy, leading to active government roles in stabilizing economies.

Modern Perspectives Today, Say’s Law is not accepted in its original form, but elements of it remain relevant. Supply‑side economists, for example, argue that policies encouraging production—such as tax cuts and deregulation—can stimulate growth. In contrast, Keynesians stress the importance of demand management. The debate reflects a broader tension in economics: whether prosperity depends more on producing goods or ensuring people have the means and willingness to buy them.

Conclusion: Say’s Law was a bold attempt to explain the self‑sustaining nature of markets. While its claim that “supply creates its own demand” proved too simplistic in the face of modern economic realities, it remains a vital part of the history of economic thought. The controversy surrounding Say’s Law highlights the evolving nature of economics, where theories are tested against real‑world crises and adapted to new circumstances. Even today, discussions of supply‑side versus demand‑side policies echo the enduring influence of Say’s original insight.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The singularity promises to revolutionize medicine by accelerating diagnostics, treatment, and longevity—but it also demands ethical vigilance and systemic transformation.

The concept of the technological singularity refers to a hypothetical future moment when artificial intelligence (AI) surpasses human intelligence, triggering exponential advances in technology. In medicine, this could mark a turning point where AI-driven systems outperform human clinicians in diagnosis, treatment planning, and even biomedical research. While the singularity remains speculative, its implications for healthcare are profound and multifaceted.

One of the most promising impacts is in diagnostics and precision medicine. AI systems trained on vast datasets of medical images, genetic profiles, and patient histories could detect diseases earlier and more accurately than human doctors. For example, algorithms already outperform radiologists in identifying certain cancers from imaging scans. As we approach the singularity, these systems may evolve into autonomous diagnostic agents capable of real-time analysis and personalized recommendations, tailored to each patient’s unique biology.

Another transformative area is drug discovery and development. Traditional pharmaceutical research is slow and costly, often taking over a decade to bring a new drug to market. AI could dramatically shorten this timeline by simulating molecular interactions, predicting therapeutic targets, and optimizing clinical trial designs. With superintelligent systems, the pace of innovation could accelerate to the point where treatments for currently incurable diseases—like Alzheimer’s or certain cancers—become feasible within months.

The singularity also opens doors to radical longevity and human enhancement. Advances in nanotechnology, genomics, and regenerative medicine may converge to extend human lifespan significantly. AI could help decode the aging process, identify biomarkers of cellular decline, and engineer interventions that slow or reverse it. Some theorists even envision a future where aging is treated as a curable condition, and mortality becomes a choice rather than a biological inevitability.

However, these breakthroughs come with serious ethical and societal challenges. Data privacy, algorithmic bias, and access inequality are critical concerns. If singularity-level AI is controlled by a few corporations or governments, it could exacerbate global health disparities. Moreover, the replacement of human clinicians with machines raises questions about empathy, trust, and accountability in care. Who is responsible when an AI makes a life-altering mistake?

To navigate this future responsibly, medicine must embrace interdisciplinary collaboration. Ethicists, technologists, clinicians, and policymakers must work together to ensure that AI systems are transparent, equitable, and aligned with human values. Regulatory frameworks must evolve to keep pace with innovation, and medical education must prepare practitioners to work alongside intelligent machines.

In conclusion, the singularity represents both a promise and a peril for medicine. It offers unprecedented opportunities to enhance human health, but also demands careful stewardship to avoid unintended consequences.

As we edge closer to this horizon, the challenge will be not just technological, but deeply human: to harness intelligence beyond our own in service of healing, compassion, and justice.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Posted on November 10, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

Taxation is a cornerstone of modern governance, providing the financial resources necessary for governments to deliver public services, maintain infrastructure, and support social programs. While paying taxes is a legal obligation, individuals and businesses often seek ways to reduce their tax burden. This pursuit gives rise to two distinct concepts: tax avoidance and tax evasion. Though they may sound similar, the difference between them is profound, hinging on legality, ethics, and consequences.

Tax avoidance refers to the use of lawful strategies to minimize tax liability. It involves taking advantage of deductions, exemptions, credits, and other provisions explicitly allowed by tax laws. For example, individuals may contribute to retirement accounts, claim mortgage interest deductions, or invest in tax-free municipal bonds. Businesses may structure operations to benefit from tax incentives or credits designed to encourage innovation, sustainability, or job creation. In essence, tax avoidance is legal tax planning—a way to reduce obligations while staying within the boundaries of the law.

***

***

By contrast, tax evasion is illegal. It involves deliberately misrepresenting or concealing information to avoid paying taxes. Common forms of evasion include underreporting income, overstating deductions, hiding assets offshore, or falsifying records. Unlike avoidance, which is permitted and often encouraged, evasion constitutes fraud against the government. The consequences are severe: individuals and corporations found guilty of tax evasion may face hefty fines, penalties, and even imprisonment.

The distinction between the two lies in compliance versus deception. Tax avoidance complies with the letter of the law, even if it sometimes exploits loopholes. Tax evasion, however, breaks the law outright. This difference is critical not only legally but also ethically. While avoidance is lawful, aggressive avoidance strategies—especially by wealthy individuals or multinational corporations—can raise moral questions. Critics argue that such practices undermine fairness, shifting the tax burden onto ordinary citizens. Governments often respond by reforming tax codes to close loopholes and ensure equity.

Tax evasion, on the other hand, is universally condemned. It erodes trust in the tax system, deprives governments of essential revenue, and places greater strain on compliant taxpayers. Moreover, evasion can damage reputations, leading to loss of credibility and public backlash for businesses or individuals caught engaging in fraudulent practices.

In summary, tax avoidance is legal and strategic, while tax evasion is illegal and punishable. Both aim to reduce tax liability, but they differ fundamentally in method and consequence. Avoidance leverages lawful opportunities provided by tax codes, whereas evasion relies on deception and concealment. Understanding this distinction is vital for taxpayers, as crossing the line from avoidance into evasion can result in serious legal and financial repercussions. Ultimately, responsible tax planning requires not only knowledge of the law but also an awareness of ethical considerations, ensuring that efforts to minimize taxes do not compromise legality or fairness.

In the competitive world of financial services, attracting and retaining clients is a constant challenge. To stand out, many financial advisors employ strategic marketing tactics known as “loss leaders”—free or discounted services designed to showcase value and build trust. These offerings serve as entry points for potential clients, allowing advisors to demonstrate expertise and initiate long-term relationships.

One of the most common loss leaders is the free initial consultation. This no-obligation meeting gives prospective clients a chance to discuss their financial goals, ask questions, and get a feel for the advisor’s approach. For the advisor, it’s an opportunity to assess the client’s needs and present tailored solutions. While no revenue is generated from this meeting, it often leads to paid engagements once the client feels confident in the advisor’s capabilities.

Another popular tactic is offering a complimentary financial plan or portfolio review. These services provide tangible insights into a client’s current financial situation and suggest improvements. By delivering real value upfront, advisors build credibility and demonstrate their analytical skills. Clients who receive actionable advice are more likely to continue working with the advisor on a paid basis.

Educational content also plays a key role in loss leader strategy. Advisors frequently host free webinars, workshops, or seminars on topics like retirement planning, tax strategies, or investment basics. These events not only educate attendees but also position the advisor as a thought leader. Attendees often leave with a better understanding of their financial needs and a desire to seek personalized guidance.

In the digital realm, advisors may offer free tools and assessments on their websites. These include retirement readiness calculators, risk tolerance quizzes, and budgeting templates. Such tools engage users and provide personalized feedback, creating a natural segue into one-on-one consultations. Additionally, offering free newsletters or eBooks helps advisors stay top-of-mind while delivering ongoing value.

Some advisors go further by waiving fees for introductory services, such as account setup or the first few months of investment management. This lowers the barrier to entry and encourages hesitant clients to try the service. Once clients experience the benefits, they’re more likely to commit long-term.

Loss leaders are not limited to high-net-worth individuals. Advisors targeting younger or less affluent clients may offer free debt management plans or budgeting assistance. These services address immediate concerns and build loyalty among clients who may become more profitable as their financial situations improve.

Ultimately, loss leaders are about building relationships. By offering something of value without immediate compensation, financial advisors demonstrate their commitment to helping clients succeed. This fosters trust, encourages engagement, and often leads to lasting partnerships. In a field where reputation and reliability are paramount, loss leaders serve as powerful tools for growth and differentiation.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 9, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

Thought

By Dr. David Edward Marcinko MBA MEd

***

***

Thought experiments have long been a powerful tool in science and philosophy, allowing thinkers to explore complex ideas without the need for immediate empirical testing. Among the most famous is Schrödinger’s Cat,devised in 1935 by physicist Erwin Schrödinger to highlight the strange implications of quantum mechanics. In this scenario, a cat is placed in a sealed box with a radioactive atom, a Geiger counter, and a vial of poison. If the atom decays, the Geiger counter triggers the release of poison, killing the cat. According to the Copenhagen interpretation of quantum mechanics, until the box is opened and observed, the atom exists in a superposition of decayed and undecayed states. Consequently, the cat is simultaneously alive and dead until observation collapses the wavefunction. This paradox illustrates the difficulty of applying quantum principles to macroscopic objects and remains a central discussion point in debates about the nature of reality.

Schrödinger’s Cat is not unique in its ability to provoke deep reflection. Throughout history, scientists and philosophers have used thought experiments to challenge assumptions and clarify theories. For example, Galileo’s falling bodies experiment imagined two objects of different weights tied together and dropped from a tower. By reasoning through the scenario, Galileo demonstrated that heavier objects do not fall faster than lighter ones, contradicting Aristotelian physics and paving the way for Newtonian mechanics.

Another influential thought experiment is Einstein’s elevator, which he used to develop the theory of general relativity. Einstein imagined an observer inside a sealed elevator, unable to see outside. If the elevator were accelerating upward in space, the observer would feel pressed to the floor, just as if gravity were acting on them. This equivalence between acceleration and gravity became the foundation of Einstein’s revolutionary insight that gravity is not a force but the curvature of spacetime.

In thermodynamics, Maxwell’s demon presents a paradox about the second law of entropy. James Clerk Maxwell imagined a tiny demon controlling a door between two chambers of gas. By selectively allowing fast-moving molecules to pass one way and slow-moving molecules the other, the demon could seemingly decrease entropy without expending energy. This thought experiment sparked debates about the nature of information, energy, and the limits of physical laws, influencing modern discussions in statistical mechanics and information theory.

Philosophy also abounds with thought experiments. Descartes’ evil demon questioned whether our perceptions could be manipulated, casting doubt on the certainty of knowledge. More recently, John Searle’s Chinese Room challenged the idea that computers can truly “understand” language, distinguishing between syntax and semantics in artificial intelligence.

In conclusion, Schrödinger’s Cat remains a symbol of quantum strangeness, but it is part of a broader tradition of thought experiments that have shaped human understanding. From Galileo’s tower to Einstein’s elevator, Maxwell’s demon to Searle’s room, these imaginative scenarios allow us to probe the boundaries of knowledge, test the coherence of theories, and confront paradoxes that empirical experiments alone cannot resolve. They remind us that science is not only about observation but also about the creative power of the human mind to envision possibilities beyond immediate reality.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Diworsification is a term coined by Peter Lynch to describe when investors over‑diversify their portfolios, adding too many holdings and ultimately reducing returns instead of improving them.

Diversification has long been heralded as one of the cornerstones of sound investing. By spreading capital across different asset classes, industries, and geographies, investors can reduce risk and protect themselves against the volatility of individual securities. Yet, as with many strategies, there exists a point where the benefits diminish and the practice becomes counterproductive. This phenomenon, known as diworsification, was popularized by legendary investor Peter Lynch to describe the tendency of investors and corporations to dilute their strengths by expanding too broadly.

At its core, diworsification occurs when the pursuit of safety leads to excessive complexity. For individual investors, this often manifests in portfolios bloated with dozens or even hundreds of stocks, mutual funds, or exchange‑traded funds. While the intention is to minimize risk, the result is frequently a portfolio that mirrors the market index but with higher costs and less focus. Instead of achieving superior returns, the investor ends up with average performance weighed down by management fees, trading expenses, and the difficulty of monitoring so many positions. In essence, the investor has sacrificed the potential for meaningful gains in exchange for a false sense of security.

Corporations are not immune to this trap. In the corporate world, diworsification describes the tendency of firms to expand into unrelated businesses, diluting their competitive advantage. A company that excels in consumer electronics, for example, may attempt to branch into unrelated industries such as food services or real estate. Without the expertise, synergies, or strategic fit, these ventures often fail to deliver value, distracting management and eroding shareholder wealth. History is replete with examples of conglomerates that grew too large, too fast, only to later divest their non‑core businesses in recognition of the inefficiencies created.

The dangers of diworsification are not merely theoretical. They highlight the importance of discipline in both investing and corporate strategy. For investors, the lesson is clear: diversification should be purposeful, not indiscriminate. A well‑constructed portfolio might include a mix of equities, bonds, and alternative assets, but each holding should serve a specific role—whether it is growth, income, or risk mitigation. Beyond a certain point, adding more securities does not reduce risk meaningfully; instead, it complicates decision‑making and reduces the chance of outperforming the market.

Similarly, for corporations, strategic focus is paramount. Expansion should be guided by core competencies and long‑term vision rather than the allure of short‑term growth. Firms that resist the temptation to chase every opportunity are better positioned to strengthen their brand, innovate within their domain, and deliver sustainable value to shareholders.

In conclusion, diworsification serves as a cautionary tale against the excesses of diversification. While spreading risk is essential, overdoing it can undermine performance and clarity. Both investors and corporations must strike a balance between breadth and focus, ensuring that every addition to a portfolio or business strategy enhances rather than dilutes overall strength. In other words, “diversification means you will always have to say you’re sorry.”

True wisdom lies not in owning everything, but in owning the right things.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

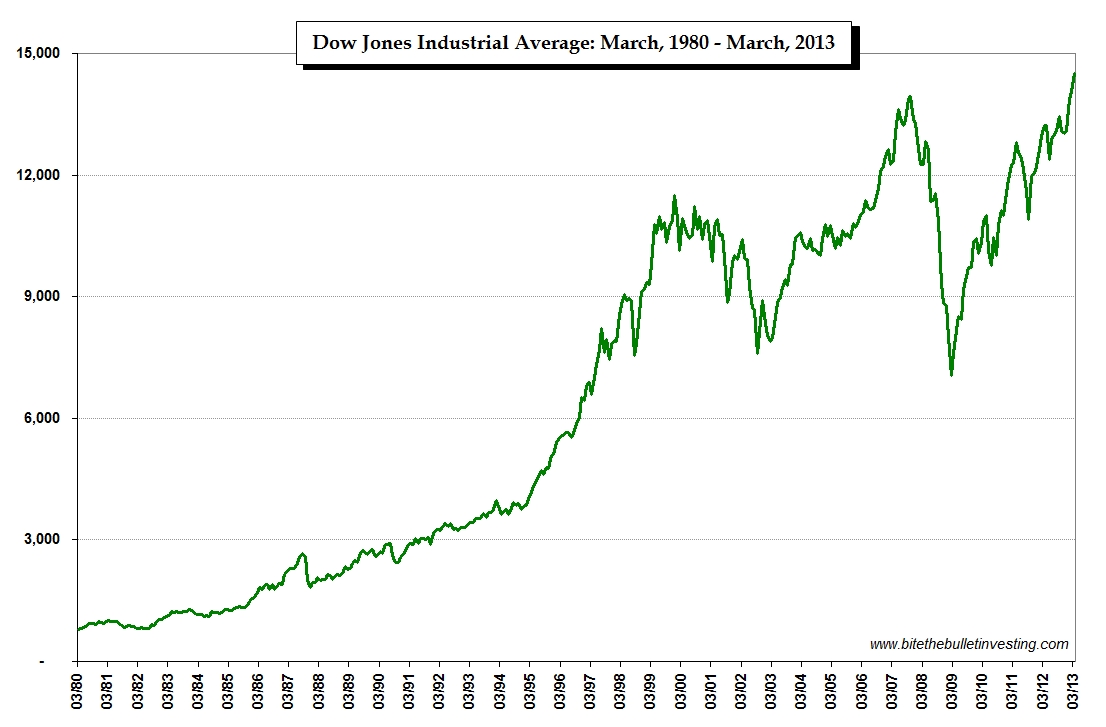

The thirty companies included in the Dow Jones Industrial Average are listed in the updated chart below.

The list is sorted by each component’s weight in the index. The weight of each company is determined by the price of the stock. A $100 stock will be weighted more than a $30 stock. If a stock splits its corresponding weighting in the Dow Jones will be reduced as its price will be about half of what it was prior to the split.

Historian Cyril Parkinson’s wrote in his book Parkinson’s Law,

“The time spent on any item of the agenda will be in inverse proportion to the sum [of money] involved.”

EXAMPLE: Parkinson described a fictional finance committee with three tasks: approval of a $10 million nuclear reactor, $400 for an employee bike shed, and $20 for employee refreshments in the break room.

The committee approves the $10 million nuclear reactor immediately, because the number is too big to contextualize, alternatives are too daunting to consider, and no one on the committee is an expert in nuclear power.

Bike Shed Effect: The bike shed gets considerably more debate. Committee members argue whether a bike rack would suffice and whether a shed should be wood or aluminum, because they have some experience working with those materials at home.

Employee refreshments take up two-thirds of the debate, because everyone has a strong opinion on what’s the best coffee, the best cookies, the best chips, etc.

Absurd: The world is filled with these absurdities. In personal finance, Ramit Sethi recently said we should stop asking $3 questions (should I buy coffee?) and ask more $30,000 questions (should I buy a smaller home?). Most people don’t, because it’s hard and intimidating. In any given moment the easiest way to deal with a big problem is to ignore it and fill your time thinking about a smaller one.

***

***

Assessment: Your thoughts and comments related to the post Corona Virus Pandemic, meetings and time management and psychology are appreciated.

Posted on November 4, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

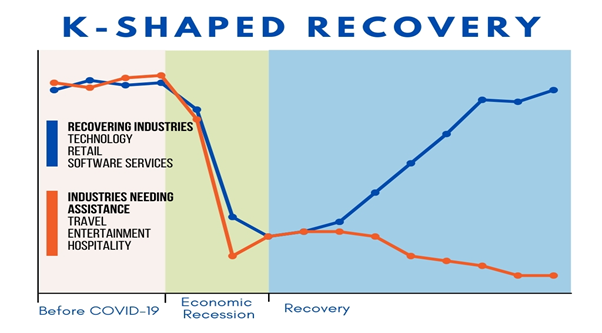

The term “K-shaped economy” emerged during the COVID-19 pandemic to describe a recovery marked by stark divergence—where some sectors and social groups rebound rapidly while others continue to decline. Unlike traditional V-shaped or U-shaped recoveries, which imply uniform economic improvement, the K-shaped model reflects a split trajectory: the upward arm of the “K” represents those who thrive, while the downward arm captures those left behind. This phenomenon has profound implications for economic policy, social equity, and long-term stability.

At the heart of the K-shaped economy is inequality. High-income individuals, white-collar professionals, and large corporations often benefit from technological advances, remote work flexibility, and access to capital. For example, tech giants like Apple, Microsoft, and Alphabet saw record profits during the pandemic, fueled by digital transformation and cloud services. Meanwhile, lower-income workers—especially in hospitality, retail, and service industries—faced job losses, reduced hours, and limited access to healthcare or financial safety nets. This divergence widened existing income and wealth gaps, exacerbating social tensions.

Sectoral performance also illustrates the K-shaped divide. Industries such as e-commerce, software, and logistics surged, while travel, entertainment, and small businesses struggled. The rise of automation and artificial intelligence further tilted the scales, favoring companies that could invest in innovation while displacing low-skilled labor. In education, students from affluent families adapted to online learning with ease, while those from disadvantaged backgrounds faced digital barriers and learning loss. These disparities underscore how economic recovery is not just uneven—it’s structurally imbalanced.

Geography plays a role too. Urban centers with diversified economies and strong tech sectors rebounded faster than rural or manufacturing-heavy regions. Housing markets in affluent areas soared, driven by low interest rates and remote work migration, while renters and first-time buyers faced affordability crises. Even within cities, neighborhoods with better infrastructure and public services recovered more quickly, deepening the urban-suburban divide.

Policymakers face a daunting challenge in addressing the K-shaped recovery. Traditional stimulus measures may not reach the most vulnerable populations without targeted interventions. Expanding access to education, healthcare, and digital infrastructure is essential to leveling the playing field. Progressive taxation, wage support, and small business aid can help bridge the gap, but require political will and fiscal discipline. Central banks must balance inflation control with inclusive growth, avoiding policies that disproportionately benefit asset holders.

The long-term consequences of a K-shaped economy are significant. Persistent inequality can erode trust in institutions, fuel populism, and hinder social mobility. Economic growth may slow if large segments of the population remain underemployed or financially insecure. To build a resilient and inclusive future, governments, businesses, and civil society must collaborate to ensure that recovery lifts all boats—not just the yachts.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on November 3, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko; MBA MEd

***

***

Classic Definition: In “The Exercise Paradox,” Herman Pontzer asserts that greater physical activity does not allow people to control weight. He goes on to describe studies on how the human body burns calories that help to explain why this is so.

Modern Circumstance: But in one of these studies, “couch potatoes” expended an average of around 200 fewer calories a day, compared with moderately active subjects. A difference of 200 fewer calories a day equates to more than 20 fewer pounds a year. Year after year after year, that really adds up.

Paradox Example: Cyclists participating in the Tour de France are said to ingest more than 5,000 calories a day. This would seem to be way too much. So why do they do it? And why don’t they become obese?

The Medical Executive-Post is a news and information aggregator and social media professional network for medical and financial service professionals. Feel free to submit education content to the site as well as links, text posts, images, opinions and videos which are then voted up or down by other members. Comments and dialog are especially welcomed. Daily posts are organized by subject. ME-P administrators moderate the activity. Moderation may also conducted by community-specific moderators who are unpaid volunteers.

Turning 50 with little to no savings can be daunting, especially for a doctor who has spent decades in a demanding profession. Yet, all is not lost. With strategic planning, discipline, and a willingness to adapt, a broke 50-year-old physician can still build a solid retirement foundation by age 65.

First, it’s essential to confront the financial reality. This means calculating current income, expenses, debts, and any assets, however small. A clear picture allows for realistic goal-setting. The target should be to save aggressively—ideally 30–50% of income—over the next 15 years. While this may seem steep, doctors often have above-average earning potential, even in their later years, which can be leveraged.

Next, lifestyle adjustments are crucial. Downsizing housing, eliminating unnecessary expenses, and avoiding new debt can free up significant cash flow. If possible, relocating to a lower-cost area or refinancing existing loans can also help. Every dollar saved should be redirected into retirement accounts such as a 401(k), IRA, or a solo 401(k) if self-employed. Catch-up contributions for those over 50 allow for higher annual deposits, which can accelerate growth.

Investing wisely is non-negotiable. A diversified portfolio with a mix of stocks, bonds, and alternative assets can provide both growth and stability. Working with a fiduciary financial advisor ensures that investments align with retirement goals and risk tolerance. Time is limited, so the focus should be on maximizing returns without taking reckless risks.

Increasing income is another powerful lever. Many doctors can boost earnings through side gigs like telemedicine, consulting, teaching, or locum tenens work. These flexible options can add tens of thousands annually without requiring a full career shift. Additionally, monetizing expertise—writing, speaking, or creating online courses—can generate passive income streams.

Debt reduction must be prioritized. High-interest loans, especially credit card debt, can erode savings potential. Paying off these balances aggressively while avoiding new liabilities is key. For student loans, exploring forgiveness programs or refinancing options may offer relief.

Finally, mindset matters. Retirement at 65 doesn’t have to mean complete cessation of work. It can mean transitioning to part-time roles, passion projects, or advisory positions that provide income and fulfillment. The goal is financial independence, not necessarily total inactivity.

In conclusion, while starting late is challenging, a broke 50-year-old doctor can still retire comfortably at 65. It requires a blend of financial discipline, income optimization, smart investing, and lifestyle changes. With focus and determination, the next 15 years can be transformative—turning a precarious situation into a secure and dignified retirement.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

Posted on October 25, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

PODCAST: National Prescription Drug Take Back Day

October 25, 2025

By Dr. David Edward Marcinko MBA MEd

***

The National Prescription Drug Take Back Day aims to provide a safe, convenient, and responsible means of disposing of prescription drugs, while also educating the general public about the potential for abuse of medications.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

President Donald Trump signed a pardon on Wednesday for convicted crypto executive Changpeng Zhao, who founded the Binance crypto exchange, White House Press Secretary Karoline Leavitt said in a statement. “President Trump exercised his constitutional authority by issuing a pardon for Mr. Zhao, who was prosecuted by the Biden Administration in their war on cryptocurrency,” Leavitt said. “In their desire to punish the cryptocurrency industry, the Biden Administration pursued Mr. Zhao despite no allegations of fraud or identifiable victims.”

Zhao was sentenced to four months in prison after reaching a deal with the Justice Dept. to plead guilty to charges of enabling money laundering at Binance, which he ran at the time. The U.S. also ordered Binance to pay more than $4 billion in fines and forfeiture, while Zhao agreed to pay $50 million in fines. A spokesperson for Binance did not immediately respond to a request for comment yesterday.

***

The History of Cryptocurrency: From Concept to Revolution

Cryptocurrency has transformed the global financial landscape, offering a decentralized alternative to traditional banking systems. Its history is rooted in decades of technological innovation, philosophical ideals, and economic experimentation.

🌐 Early Foundations

The concept of digital currency predates Bitcoin by several decades. In 1982, cryptographer David Chaum published a groundbreaking paper on secure digital transactions, laying the foundation for future developments in electronic money. Chaum later founded DigiCash in the 1990s, which introduced the idea of anonymous digital payments using cryptographic protocols. Although DigiCash eventually failed, it was a crucial stepping stone in the evolution of cryptocurrency.

The Birth of Bitcoin

The true revolution began in 2008 when an anonymous figure—or group—known as Satoshi Nakamoto released the Bitcoin whitepaper titled “Bitcoin: A Peer-to-Peer Electronic Cash System.” This document proposed a decentralized digital currency that used blockchain technology to record transactions transparently and securely without the need for a central authority.

On January 3, 2009, Nakamoto mined the first block of the Bitcoin blockchain, known as the Genesis Block. The first real-world Bitcoin transaction occurred in May 2010, when programmer Laszlo Hanyecz paid 10,000 BTC for two pizzas—an event now celebrated annually as Bitcoin Pizza Day.

Blockchain and Beyond

Bitcoin’s success inspired the development of other cryptocurrencies and blockchain platforms. Ethereum, launched in 2015 by Vitalik Buterin, introduced smart contracts—self-executing agreements coded directly into the blockchain. This innovation expanded the use of cryptocurrency beyond simple transactions to decentralized applications (dApps), finance (DeFi), and even digital art (NFTs).

Other notable cryptocurrencies include Litecoin, Ripple (XRP), and Cardano, each offering unique features such as faster transaction speeds, improved scalability, or enhanced privacy.

***

***

⚖️ Challenges and Controversies

Despite its promise, cryptocurrency has faced significant hurdles. Regulatory uncertainty, security breaches, and market volatility have raised concerns among governments and investors. High-profile hacks, such as the Mt. Gox exchange collapse in 2014, highlighted the risks associated with digital assets.

Governments around the world have responded differently—some embracing crypto innovation, others imposing strict regulations or outright bans. The rise of central bank digital currencies (CBDCs) reflects an effort to merge the benefits of crypto with the stability of fiat systems.

🚀 The Future of Crypto

Today, cryptocurrency is more than a niche technology—it’s a global phenomenon. Major companies accept Bitcoin, institutional investors hold crypto assets, and blockchain is being integrated into industries from healthcare to supply chain management.

As the technology matures, the focus is shifting toward scalability, sustainability, and interoperability. Whether it becomes a mainstream financial tool or remains a disruptive alternative, cryptocurrency has undeniably reshaped how we think about money, trust, and digital ownership.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on October 22, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

Diwali, Deepavali or Dipavali

By Dr. David Edward Marcinko MBA Med

Diwali, Deepavali or Dipavali is the Hindu festival of lights, which is celebrated every autumn in the northern hemisphere.

One of the most popular festivals of Hinduism, Diwali symbolizes the spiritual “victory of light over darkness, good over evil and knowledge over ignorance”.

***

***

During the celebration, temples, homes, shops and office buildings are brightly illuminated. The preparations, and rituals, for the festival typically last five days, with the climax occurring on the third day coinciding with the darkest night of the Hindu Lunisolar month Kartika.

In the Gregorian calendar, the festival generally falls between mid-October and mid-November.

🏦 100 Minus Age Rule: Subtract your age from 100 to estimate the percentage of your portfolio to invest in stocks. The rest goes to bonds or safer assets.

Rule of 110 or 120: A modern twist—subtract your age from 110 or 120 to allow for more stock exposure in a low-interest environment.

Diversify, Don’t Speculate: Spread investments across asset classes to reduce risk.

Don’t Invest What You Can’t Afford to Lose: Especially for speculative assets like crypto or startups.

📈 Growth & Returns

Rule of 72: Divide 72 by your annual return rate to estimate how many years it takes to double your money.

Time in the Market Beats Timing the Market: Staying invested long-term usually outperforms trying to predict short-term moves.

Start Early, Compound Often: The earlier you invest, the more compound interest works in your favor.

🧾 Budgeting & Saving

50/30/20 Rule: Allocate 50% of income to needs, 30% to wants, and 20% to savings/investments.

Emergency Fund Rule: Save 3–6 months of living expenses before investing aggressively.

Pay Yourself First: Automatically invest a portion of your income before spending.

🧠 Behavioral & Strategy Tips

Buy What You Understand: Don’t invest in companies or assets you don’t comprehend.

Avoid Emotional Decisions: Fear and greed are the enemies of smart investing.

Rebalance Annually: Adjust your portfolio to maintain your target asset allocation.

Don’t Chase Past Performance: What worked last year may not work this year.

🏦 Retirement & Withdrawal

The 4% Rule: Withdraw 4% of your retirement savings annually to make it last ~30 years.

Save 15% of Income for Retirement: A common target for long-term financial security.

Max Out Tax-Advantaged Accounts First: Prioritize 401(k), IRA, or Roth IRA before taxable accounts.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The U.S. healthcare system is often criticized for its high costs, unequal access, and inconsistent outcomes. With nearly 30 million Americans uninsured and many more underinsured, the question arises: could socialized medicine be the solution to these systemic issues?

Socialized medicine refers to a system where the government owns and operates healthcare facilities and employs medical professionals, funded primarily through taxation. While the term is often used pejoratively in American discourse, countries like the United Kingdom and Sweden have long embraced such models. These systems guarantee universal access to healthcare, regardless of income or employment status.

One of the strongest arguments in favor of socialized medicine is its potential to reduce overall healthcare costs. In the U.S., administrative expenses, profit margins, and fragmented billing systems contribute to exorbitant prices. A centralized system could streamline operations, negotiate better drug prices, and eliminate the need for private insurance middlemen. Countries with socialized systems typically spend less per capita on healthcare while achieving comparable or better health outcomes.

Moreover, socialized medicine could address the issue of healthcare access. In the current U.S. model, losing a job often means losing health insurance. Even with the Affordable Care Act, many Americans face high premiums and deductibles. A government-run system would ensure that healthcare is a right, not a privilege, and that no one is denied care due to financial constraints.

***

***

However, critics argue that socialized medicine could lead to longer wait times, reduced innovation, and lower quality of care. They point to examples in Canada and the U.K. where patients sometimes wait weeks or months for non-emergency procedures. Additionally, skeptics fear that government control could stifle competition and reduce incentives for medical advancement.

Yet, these concerns may be overstated. Many countries with socialized systems still foster innovation through public-private partnerships and maintain high standards of care. France, for example, combines universal coverage with private providers and consistently ranks among the top healthcare systems globally.

Transitioning to socialized medicine in the U.S. would be a monumental task, requiring political will, public support, and a reimagining of healthcare financing. It would disrupt entrenched interests, including insurance companies and pharmaceutical firms. But if the goal is to create a more equitable, efficient, and humane system, socialized medicine deserves serious consideration.

In conclusion, while not a panacea, socialized medicine offers a compelling framework for addressing the deep-rooted problems in U.S. healthcare. By prioritizing access, affordability, and public health over profit, it could pave the way for a healthier and more just society.

SPEAKING: ME-P Editor Dr. David Edward Marcinko MBA MEd will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Do you ever wish you could acquire specific information for your career activities without having to complete a university Master’s Degree or finish our entire Certified Medical Planner™ professional designation program? Well, Micro-Certifications from the Institute of Medical Business Advisors, Inc., might be the answer. Read on to learn how our three Micro-Certifications offer new opportunities for professional growth in the medical practice, business management, health economics and financial planning, investing and advisory space for physicians, nurses and healthcare professionals.

Micro-Certification Basics

Stock-Brokers, Financial Advisors, Investment Advisors, Accountants, Consultants, Financial Analyists and Financial Planners need to enhance their knowledge skills to better serve the changing and challenging healthcare professional ecosystem. But, it can be difficult to learn and demonstrate mastery of these new skills to employers, clients, physicians or medical prospects. This makes professional advancement difficult. That’s where Micro-Certification and Micro-Credentialing enters the online educational space. It is the process of earning a Micro-Certification, which is like a mini-degree or mini-credential, in a very specific topical area.

Micro-Certification Requirements

Once you’ve completed all of the requirements for our Micro-Certification, you will be awarded proof that you’ve earned it. This might take the form of a paper or digital certificate, which may be a hard document or electronic image, transcript, file, or other official evidence that you’ve completed the necessary work.

Uses of Micro-Certifications

Micro-Certifications may be used to demonstrate to physicians prospective medical clients that you’ve mastered a certain knowledge set. Because of this, Micro-Certifications are useful for those financial service professionals seeking medical clients, employment or career advancement opportunities.

Examples of iMBA, Inc., Micro-Certifications

Here are the three most popular Micro-Certification course from the Institute of Medical Business Advisors, Inc:

1. Health Insurance and Managed Care: To keep up with the ever-changing field of health care physician advice, you must learn new medical practice business models in order to attract and assist physicians and nurse clients. By bringing together the most up-to-date business and medical prctice models [Medicare, Medicaid, PP-ACA, POSs, EPOs, HMOs, PPOs, IPA’s, PPMCs, Accountable Care Organizations, Concierge Medicine, Value Based Care, Physician Pay-for-Performance Initiatives, Hospitalists, Retail and Whole-Sale Medicine, Health Savings Accounts and Medical Unions, etc], this iMBA Inc., Mini-Certification offers a wealth of essential information that will help you understand the ever-changing practices in the next generation of health insurance and managed medical care.

2. Health Economics and Finance: Medical economics, finance, managerial and cost accounting is an integral component of the health care industrial complex. It is broad-based and covers many other industries: insurance, mathematics and statistics, public and population health, provider recruitment and retention, health policy, forecasting, aging and long-term care, and Venture Capital are all commingled arenas. It is essential knowledge that all financial services professionals seeking to serve in the healthcare advisory niche space should possess.

3. Health Information Technology and Security: There is a myth that all physician focused financial advisors understand Health Information Technology [HIT]. In truth, it is often economically misused or financially misunderstood. Moreover, an emerging national HIT architecture often puts the financial advisor or financial planner in a position of maximum uncertainty and minimum productivity regarding issues like: Electronic Medical Records [EMRs] or Electronic Health Records [EHRs], mobile health, tele-health or tele-medicine, Artificial Intelligence [AI], benefits managers and human resource professionals.

Other Topics include: economics, finance, investing, marketing, advertising, sales, start-ups, business plan creation, financial planning and entrepreneurship, etc.

How to Start Learning and Earning Recognition for Your Knowledge

Now that you’re familiar with Micro-Credentialing, you might consider earning a Micro-Certification with us. We offer 3 official Micro-Certificates by completing a one month online course, with a live instructor consisting of twelve asynchronous lessons/online classes [3/wk X 4/weeks = 12 classes]. The earned official completion certificate can be used to demonstrate mastery of a specific skill set and shared with current or future employers, current clients or medical niche financial advisory prospects.

Mini-Certification Tuition, Books and Related Fees

The tuition for each Mini-Certification live online course is $1,250 with the purchase of one required dictionary handbook. Other additional guides, white-papers, videos, files and e-content are all supplied without charge. Alternative courses may be developed in the future subject to demand and may change without notice.

***

Contact: For more information, or to speak with an academic representative, please contact Ann Miller RN MHA CMP™ at Email: MarcinkoAdvisors@msn.com [24/7].

Posted on October 17, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

A paradox is a logically self-contradictory statement or a statement that runs contrary to one’s expectation. It is a statement that, despite apparently valid reasoning from true or apparently true premises, leads to a seemingly self-contradictory or a logically unacceptable conclusion. A paradox usually involves contradictory-yet-interrelated elements that exist simultaneously and persist over time. They result in “persistent contradiction between interdependent elements” leading to a lasting “unity of opposites”.

THE TELE-MEDICINE PARADOX

Classic Definition: Refers specifically to the treatment of various medical conditions without seeing the patient in person. Healthcare providers may use electronic and internet platforms like live video, audio, PCs, tablets, or instant messaging to address a patient’s concerns and diagnose their condition remotely.

Modern Circumstance: This may include giving medical advice, walking them through at-home exercises, or recommending them to a local provider or facility. Even more exciting is the emergence of telemedicine apps which give patients access to care right from their phones or computer screens.

Paradox Examples: Treating certain conditions remotely can be challenging. Tele-medicine is often used to treat common illnesses, manage chronic conditions, or provide specialist services. If a patient is dealing with an emergent or serious condition, the remote provider suggests they seek in-person medical care.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The October 2025 Stock Market Crash: A Perfect Storm of Geopolitics and Investor Panic

The weekend of October 10–12, 2025, marked one of the most dramatic downturns in global financial markets in recent memory. What began as a series of unsettling headlines quickly snowballed into a full-blown market crash, sending shockwaves through economies and portfolios worldwide. This event was not the result of a single catalyst but rather a convergence of geopolitical tensions, speculative excess, and investor psychology.

At the heart of the crisis was a sudden escalation in U.S.–China trade relations. President Donald Trump abruptly canceled a scheduled diplomatic meeting with Chinese President Xi Jinping and announced a sweeping 100% tariff on all Chinese imports. This move reignited fears of a prolonged trade war, reminiscent of the economic standoff that rattled markets in the late 2010s. Investors, already jittery from months of uncertainty, interpreted the announcement as a signal of deteriorating global cooperation and retaliatory economic measures to come.

The impact was immediate and severe. Major U.S. indices plummeted: the S&P 500 dropped 2.7%, the Nasdaq fell 3.6%, and the Dow Jones Industrial Average lost 1.9%. These declines marked the worst single-day performance since April and triggered automatic trading halts in several sectors. The selloff was not confined to the United States; European and Asian markets mirrored the panic, with steep losses across the board.

Compounding the crisis was a massive liquidation in the cryptocurrency market. As traditional assets tumbled, investors rushed to offload digital holdings, leading to the largest crypto wipeout in history. Trillions of dollars in value evaporated within hours, further destabilizing investor confidence and draining liquidity from the broader financial system.

Another underlying factor was growing concern over the valuation of artificial intelligence (AI) stocks. The International Monetary Fund (IMF) had recently issued a warning that the AI sector was exhibiting signs of a speculative bubble, drawing parallels to the dot-com era. With many AI companies trading at astronomical price-to-earnings ratios, the crash exposed the fragility of investor sentiment and the dangers of overexuberance in emerging technologies.

Perhaps most telling was the psychological shift among investors. The weekend saw widespread capitulation, with many choosing to exit the market entirely rather than weather further volatility. This behavior—marked by fear-driven decision-making and herd mentality—is often a hallmark of deeper financial crises. It underscores the importance of trust and stability in maintaining market equilibrium.

In conclusion, the October 2025 stock market crash was a multifaceted event driven by geopolitical shocks, speculative risk, and emotional contagion. It serves as a stark reminder of how interconnected and fragile global markets have become. As policymakers and investors assess the damage, the focus must shift toward restoring confidence, recalibrating risk, and ensuring that future growth is built on sustainable foundations rather than speculative fervor.

COMMENTS APPRECIATED

SPEAKING: ME-P Editor Dr. David Edward Marcinko MBA MEd will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

“THE INVESTOR’S CHIEF problem—even his worst enemy—is likely to be himself.” So wrote Benjamin Graham, the father of modern investment analysis.

With these words, written in 1949, Graham acknowledged the reality that investors are human. Though he had written an 800 page book on techniques to analyze stocks and bonds, Graham understood that investing is as much about human psychology as it is about numerical analysis.

In the decades since Graham’s passing, an entire field has emerged at the intersection of psychology and finance. Known as behavioral finance, its pioneers include Daniel Kahneman, Amos Tversky and Richard Thaler. Together, they and their peers have identified countless human foibles that interfere with our ability to make good financial decisions. These include hindsight bias, recency bias and overconfidence, among others. On my bookshelf, I have at least as many volumes on behavioral finance as I do on pure financial analysis, so I certainly put stock in these ideas.

At the same time, I think we’re being too hard on ourselves when we lay all of these biases at our feet. We shouldn’t conclude that we’re deficient because we’re so susceptible to biases. Rather, the problem is that finance isn’t a scientific field like math or physics. At best, it’s like chaos theory. Yes, there is some underlying logic, but it’s usually so hard to observe and understand that it might as well be random. The world of personal finance is bedeviled by paradoxes, so no individual—no matter how rational—can always make optimal decisions.

As we plan for our financial future, I think it’s helpful to be cognizant of these paradoxes. While there’s nothing we can do to control or change them, there is great value in being aware of them, so we can approach them with the right tools and the right mindset.

Here are just seven of the paradoxes that can bedevil financial decision-making:

There’s the paradox that all of the greatest fortunes—Carnegie, Rockefeller, Buffett, Gates—have been made by owning just one stock. And yet the best advice for individual investors is to do the opposite: to own broadly diversified index funds.

There’s the paradox that the stock market may appear overvalued and yet it could become even more overvalued before it eventually declines. And when it does decline, it may be to a level that is even higher than where it is today.

There’s the paradox that we make plans based on our understanding of the rules—and yet Congress can change the rules on us at any time, as it did just last year.

There’s the paradox that we base our plans on historical averages—average stock market returns, average interest rates, average inflation rates and so on—and yet we only lead one life, so none of us will experience the average.

There’s the paradox that we continue to be attracted to the prestige of high-cost colleges, even though a rational analysis that looks at return on investment tells us that lower-cost state schools are usually the better bet.

There’s the paradox that early retirement seems so appealing—and has even turned into a movement—and yet the reality of early retirement suggests that we might be better off staying at our desks.

There’s the paradox that retirees’ worst fear is outliving their money and yet few choose the financial product that is purpose-built to solve that problem: the single-premium immediate annuity.

How should you respond to these paradoxes? As you plan for your financial future, embrace the concept of “loosely held views.”

In other words, make financial plans, but continuously update your views, question your assumptions and rethink your priorities.