BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on August 16, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

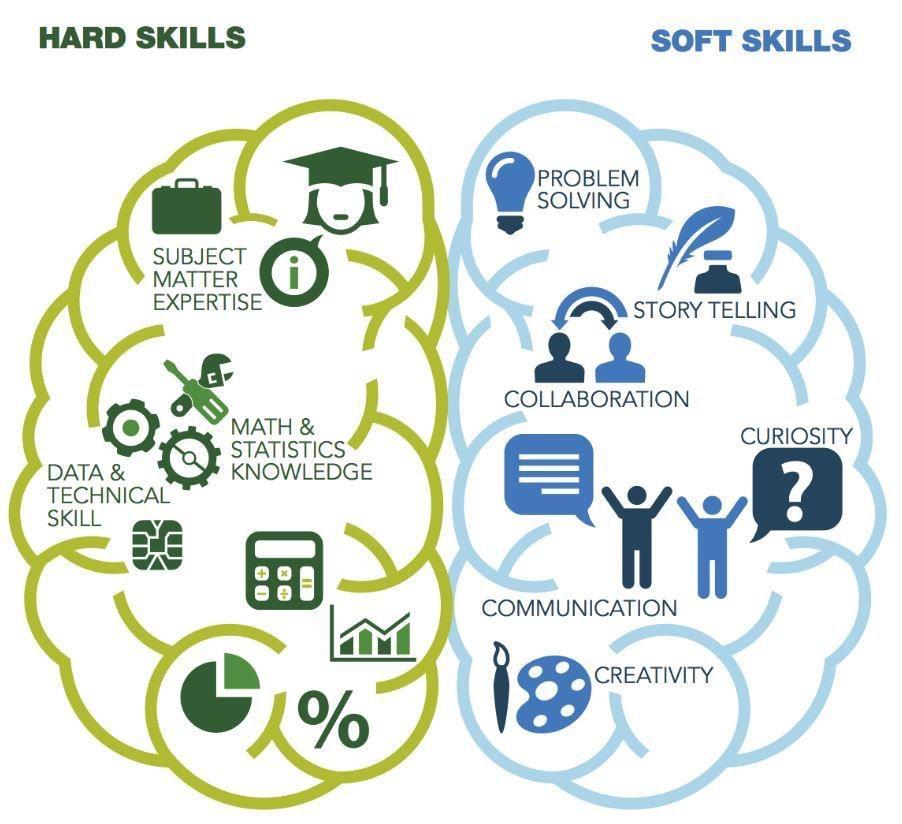

By Aleksandar Stojanović, MSc

Here’s a brief insight before the explanations:

𝗖𝗙𝗢𝘀 are heavily invested in strategic planning, leadership, and risk management, often overlooking the entire financial spectrum.

𝗖𝗼𝗻𝘁𝗿𝗼𝗹𝗹𝗲𝗿𝘀 play a key role in accounting, financial reporting, and regulatory compliance, ensuring financial integrity.

𝗙𝗣&𝗔 𝗠𝗮𝗻𝗮𝗴𝗲𝗿𝘀 focus on financial modeling, analytical skills, and business acumen to drive business growth.

𝗜𝗻𝘁𝗲𝗿𝗻𝗮𝗹 𝗔𝘂𝗱𝗶𝘁𝗼𝗿𝘀 specialize in risk management, regulatory compliance, and analytical tasks to ensure internal control.

𝗙𝗶𝗻𝗮𝗻𝗰𝗲 𝗔𝗻𝗮𝗹𝘆𝘀𝘁𝘀 are adept at financial modeling, analytics, and reporting to support data-driven decisions.

𝗔𝗰𝗰𝗼𝘂𝗻𝘁𝗮𝗻𝘁𝘀 emphasize accounting skills, financial reporting, and regulatory compliance for precise record-keeping.

***

***

Now, generally, CFOs and FP&A Managers might spend more time connecting to business stakeholders for strategic decisions, while Controllers and Internal Auditors focus more on regulatory and compliance tasks.

Finance Analysts and Accountants are more involved in financial modeling and reporting.

These titles and responsibilities can be interchanged in some job descriptions, and the weight of these skills also depends on the industry and project.

But this breakdown is still quite helpful when planning career paths or understanding the roles within a finance department.

Posted on August 11, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

GlobalLaunch

By Staff Reporters

***

***

Recently, PayPal debuted its stablecoin, PayPal USD (PYUSD), the first issued by a global financial platform. Stablecoin is a cryptocurrency pegged to a stable asset, in this case, the US dollar, which is meant to make it less volatile and safer than other digital tokens. Stablecoins have been around for decades but haven’t taken off in the consumer payment space—mainly because regulators aren’t convinced of the stability promise.

But, PayPal asserts that PYUSD will “reduce friction for in-experience payments in virtual environments” and allow faster and cheaper transfers between countries.

PYUSD works for peer-to-peer payments, both for checking out online and transferring value among digital wallets.

The currency is redeemable for dollars and is convertible to or from other digital currencies that PayPal supports.

And soon, you’ll be able to send your tokens between PayPal and Venmo, making it even more convenient to send money any where and any time..

MCLEAN, Virginia (Reuters) – U.S. Treasury Secretary Janet Yellen on Wednesday voiced more objections to Fitch Ratings’ downgrade of the main U.S. credit rating, calling it “entirely unwarranted” because it ignored improvements in governance metrics during the Biden administration and the country’s economic strength.

The S&P 500 Index was down 63.34 points (1.4%) at 4,513.39; the Dow Jones Industrial Average (DJIA) fell 348.16 points (1.0%) to 35,282.52; the NASDAQ Composite dropped 310.47 points (2.2%) at 13,973.45.

The 10-year Treasury note yield (TNX) rose about 3 basis points to 4.073%.

CBOE’ss Volatility Index (VIX) was up 2.2 at 16.13.

Consumer discretionary and energy shares were also weaker, with the latter pressured by a more-than 2% drop in crude oil futures.

The U.S. dollar index (DXY) strengthened for a fifth straight day and touched a four-week high, as investors shed riskier assets in favor of what are considered safe havens. Volatility based on the VIX hit its highest level since late May.

The 4% Rule is a practical rule of thumb that may be used by retirees to decide how much they should withdraw from their retirement funds each year; according to Investopedia.

The purpose of adopting the rule is to keep a steady income stream while maintaining an adequate overall account balance for future years. The withdrawals will consist primarily of interest and dividends on savings.

CHALLENGE: But, experts like Mike Kitces are divided on whether the 4% withdrawal rate is the best option. Many, including the creator of the rule, say that 5% is a better rule for all but the worst-case scenario.

According to Paige Minemyer of Fierce Healthcare, the Joe Biden administration is proposing cuts to physician payments in its annual fee schedule, and doctors are not happy. Major industry groups have roundly called for Congress to step in to prevent the Medicare reimbursement changes from going through. Last week, the Centers for Medicare & Medicaid Services (CMS) proposed a 3.34% cut to the fee schedule’s conversion factor, which is used to calculate Medicare payouts to docs.

In a statement, the American Medical Group Association (AMGA) said that Medicare payments already fail to keep up with “the increasing cost of delivering healthcare,” and further cuts would only exacerbate that problem. “AMGA members cannot absorb this proposed payment cut,” said AMGA President and CEO Jerry Penso, MD.

“Their expenses are continuing to increase, and Congress needs to act to ensure Medicare’s reimbursement reflects the cost of delivering high-quality care to patients.”

Posted on July 21, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

***

HEALTH DICTIONARY SERIES

ByAnn Miller RN MHA

[An Internet WIKI CROWD-SOURCED Curation Project]*

To keep up with the ever-changing healthcare industrial complex, we must learn new definitions and re-learn old terminology in order to correctly apply it to practice. By aggregating the most up-to-date abbreviations, acronyms, definitions and terms, the Health DictionarySeries offers a wealth of information to help understand the ever-changing terms-of-art in healthcare today.

Each 10,000 item handbook is essential for doctors, nurses, benefits managers and insurance agents, CPAs, and administrators; as well as graduate and under graduate students and professors. Our goal to for each dictionary to be designated as a Doody’s Core Title.

Dictionary of Health Insurance and Managed Care

With more than 8,000 definitions, 4,000 abbreviations and acronyms, and a 3,000 item oeuvre of resources, readings, and nomenclature derivatives, this dictionary covers the Medicare, managed care and Medicaid, private insurance, Veteran’s Administration and PP-ACA language of the entire health and long-term care insurance sector.

Dictionary of Health Economics and Finance

Health economics and finance is an integral component of the health care industrial complex. Its language is a diverse and broad-based concept covering many other industries: accounting, mathematics, the actuarial sciences, stochastics and statistics, salary reimbursements, physician payments, compensation and forecasting are all commingled arenas.

Dictionary of Health Information Technology Security

There is a myth that all healthcare stakeholders understand the meaning of information technology jargon. In truth, the vernacular of contemporary systems is unique, and often misused or misunderstood. Moreover, emerging Heath Information Technology (HIT) thru the HITECG initiatives; in the guise of terms, definitions, acronyms, abbreviations and standards; often puts the non-expert in a position of maximum uncertainty and minimum productivity.

*NOTE: A wiki website allows users to add or update content using their browser thru a hosted server created by the collaborative effort of site visitors. The Hawaiian term “wiki wiki” means “super fast.”

Posted on July 19, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Cash is king, especially in this tough interest rate environment. That’s proving true in the mergers and acquisitions market this year, according to PwC’sUS Deals 2023 midyear outlook, which says companies and private equity with cash in hand are making deals happen. There are “opportunities for corporates with strong balance sheets. Private equity sponsors with large amounts of dry powder also have been getting deals done,” according to PwC.

Deal makers need cash because lending has become tougher and more expensive to obtain. Additionally, “the IPO market has remained quiet for over a year.”

Even the private equity market, which often leans heavily on debt financing, is reaching for other ways to get deals done: “Some PE sponsors have turned to more creative financing solutions, including higher equity contribution, seller’s notes, paid in-kind financing and the private credit markets.”

The challenging market is also impacting deal size. PwC found that deal makers are eschewing big deals in favor of smaller opportunities. However, although the deals appear to be smaller, the volume of M&A activity is “relatively strong compared to” COVID pre-pandemic levels.

Posted on July 10, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Miss seeing terms like “adjusted profits” and “forward guidance” in the ME-P?

They’re coming back as earnings season got underway on Friday with big banks reporting. Tech companies, in particular, will have to impress to justify their expensive share prices.

According to Wikipedia, a tchotchke is a small bauble, doodad, doohickey, gewgaw, gismo knickknack, swag, thingamabob, thingamajig, toy, trinket, whatchamacallit, whosie-whatsit, widget, etc. Drug representative, various trade vendors and even prospecting financial advisors that give such cheap souvenirs to potential clients are even sometimes called “tchotchke dukes.” This industry practice is well known and wide spread.

Value-Less

Depending on context, the term has a connotation of worthlessness or disposability as well as tackiness, and has long been used in the regional speech of New York City and elsewhere.

The word may also refer to swag, in the sense of the logo pens, key rings and FOBs, t-shirts, golf balls, and other promotional freebies dispensed at trade shows, conventions, and similar large events. Most are largely value-less promotional pieces.

Valuable

Medical professionals of all types are fertile prospects for pharmaceutical representatives, insurance agents, financial advisors and like minded vendors. Most of these commissioned salesmen offer tchotchkes to their doctor clients and prospects as a reminder of their wares.

Assessment

And so, wouldn’t it be interesting for these vendors to offer their doctors something of real value? How about one of our Dictionaries of Health … in our series of three non-clinical handbooks? Affordable, memorable and valuable!

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

Posted on May 30, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

Answering Patient Messages

***

The study on ChatGPT “outperforming” doctors in answering patient questions quickly became the talk of the town. However, as is often the case, it was presented as a prime example of media sensationalism.

As we encounter more of these partially misinterpreted hypes – and rest assured, there will be many – we’ll need to navigate a sea of questions. Firstly, we must determine what AI can genuinely do better than healthcare professionals. Secondly, we need to consider how to identify unique areas where healthcare workers can assist patients, while AI automates repetitive and data-driven tasks.

Posted on May 29, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

COLLEGE 529 SAVINGS PLAN DAY

By Staff Reporters

***

***

May 29th is observed across the U.S. as 529 Day or 529 College Savings day. It was introduced to increase awareness of these plans and encourage families to start saving toward future education expenses.

Posted on May 24, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Anonymous

***

***

The HHS OIG Fall 2022 report was recently released to Congress. On page 20, there are many referrals to seven inappropriate payments to a variety of Medicare “Advantage” Plans. Topping the list is Humana. The OIG claims that Humana in the time period studied falsified records to receive $34.4M worth of payments they received from CMS for risk diagnosis code risk assessments. If even half this amount is true, it is unconscionable that Humana is not severely fined, their executives terminated and subjected to criminal proceedings, and they should be banned from the Medicare program for ten years. This is no different from how other healthcare providers are criminalized, so the question is, why is the insurance industry treated different and preferentially when they commit fraud?

These OIG studies are great reads, but up until now, they have done nothing to stop the insurance industry’s abusive practices of denying “clean claims”, denying claims after prior authorization, ignoring CCI edits, “losing” charts sent for review and then claiming higher error rates to Congress, paying providers often less than 50% of Medicare, and this the last draw… falsifying data so they can be paid more from CMS. When will this madness stop? When will providers have the gumption to actually act out the famous quote, “I’m mad as hell and I’m not going take it anymore!” (from the movie Network), and Peter Finch it!

Posted on May 20, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

***

***

By Staff Reporters

The OTCQB, also called “The Venture Market,” is the middle tier of the over-the-counter (OTC) market for U.S. stocks. It was created in 2010 and consists mainly of early-stage and developing U.S. and international companies that are not yet able to qualify for the OTCQX but are not as speculative as the lowest-tier Pink Sheets.

The OTCQB replaced the Financial Industry Regulatory Authority (FINRA)-operated OTC Bulletin Board (OTCBB) as the main market for trading OTC securities that report to a U.S. regulator. As it has no minimum financial standards, the OTCQB often includes shell companies, penny stocks, and small foreign issuers.

Posted on May 19, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Today is World Family Doctor Day—and the US needs more family doctors. By 2026, 21% of family medicine and other primary care physicians will have reached retirement age, while demand for primary care is expected to grow 4%.

World Family Doctor Day is on May 19th every year. Founded by the World Organization of Family Doctors (W.O.N.C.A.) in 2010, World Family Doctor Day has now grown into a global celebration of the importance of family doctors in health care. Taking part in this event is a great way to show appreciation for the important role family medicine plays in providing patients with individualized, comprehensive, and long-term health care. Family doctors around the world have made significant contributions to medicine — now is the time to recognize that. It’s also a moment to recognize the advancements in family medicine and the unique efforts of primary care teams worldwide.

So we, at the ME-P, hope all the family doctors take time to relax from their busy schedules and enjoy the springtime blooms as we trust those April showers brought lots of May flowers.

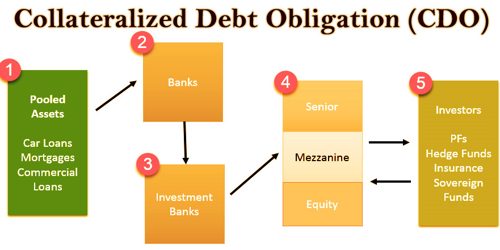

A collateralized debt obligation (CDO) is a type of structured asset-backed security (ABS). Originally developed as instruments for the corporate debt markets, after 2002 CDOs became vehicles for refinancing mortgage-backed securities (MBS).

Like other private label securities backed by assets, a CDO can be thought of as a promise to pay investors in a prescribed sequence, based on the cash flow the CDO collects from the pool of bonds or other assets it owns. Distinctively, CDO credit risk is typically assessed based on a probability of default (PD) derived from ratings on those bonds or assets.

A CMO is a debt security backed by mortgages. These mortgage pools are usually separated into different maturity classes called tranches (from the French word for “slice”). The securities were issued by private issuers, as well as the Federal Home Loan Mortgage Corporation (Freddie Mac). As the mortgages were usually government-guaranteed, CMOs usually carried AAA ratings until their current financial meltdown. The early versions of CMOs were known as “plain vanilla,” but recent developments gave us PACs (planned amortization certificates) and TACs (targeted amortization certificates); among too many others. They were all variations on how principal repayments in advance of maturity date were treated.

Posted on May 15, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

NARROW NETWORKS

By Staff Reporters

An increasing number of insurers now promote “narrow network” plans that can be less expensive than more traditional offerings. However, that added affordability comes with a tradeoff that could leave you with fewer options for covered medical services.

Understanding Narrow Networks: Narrow network plans are similar to the health maintenance organizations (HMOs). Like standard HMOs, these plans limit coverage to a select group of physicians, specialists and hospitals. However, narrow network plans can be even more restrictive in the number of providers they include. Those providers generally have been proven to have higher measured quality and better outcomes for patients. They also typically agree to lower reimbursements from insurers, which can mean lower premiums and out-of-pocket expenses for consumers. You’re more likely to see narrow networks — which include narrow pharmacy networks — if you shop for your own health insurance on HealthCare.gov or your state’s insurance exchange. They’re less common in the plan options provided by private employers.

Advantages Beyond the Savings The fact that narrow network plans include fewer providers doesn’t mean you’ll be getting lower quality care. In fact, many insurers require providers to have a proven track record that’s focused on their patients’ health outcomes. And they can offer a number of additional advantages, beyond just lower costs:

Coordinated care. Working within a single health system can mean better communication between your doctors. You might also have easier access to all your medical records through a dedicated online portal.

No referrals. Traditional HMO plans generally require a referral from your primary care physician for any consultations with a specialist. Many narrow network plans eliminate this requirement.

Added benefits. Many narrow network plans offer benefits designed to keep high-risk patients healthier. These can include options like free health coaching and live video services that enable remote, online medical consultations.

CONS: The biggest disadvantage to narrow network plans is less choice. Insurers keep these plans more affordable by negotiating lower reimbursements with health care providers. In return, those providers could see patient rosters grow, because smaller networks also mean less competition for those within the network. Smaller networks also can mean:

A need to change physicians. Your current primary care physician and specialists might not be included in the plan. This can mean starting over with new doctors who aren’t familiar with your particular health concerns.

Longer drives. With fewer choices, you may be forced into a longer commute to see an in-network physician. This could become a hardship for those in rural locations.

Lack of specialty options. A smaller network might not include the broad range of specialists large networks typically include.

Posted on May 10, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, Inc

***

***

On February 22, 2023, UnitedHealth Group’s (UHG’s) Optum division, the health insurance giant’s care delivery arm, acquired Crystal Run Healthcare, a New York based physician group of almost 400 physicians, nurse practitioners, and other providers

This significant move is just the latest in UHG’s concerted effort over the past few years to acquire outpatient providers, surgery centers, and physician groups. This Health Capital Topics article will briefly survey some of the insurer’s recent acquisitions and initiatives to expand their physician services network. (Read more…)

Under law, financial advisors and planners must provide you with a form ADV Part II or a brochure that covers the same information. Even if a brochure is provided, ask for the ADV. While it is acceptable, even desirable, for the brochure to be easier to read than the ADV, the ADV is what is filed with the appropriate state or SEC. If the brochure reads more like a slick sales brochure or the information in the brochure glosses over the items on the ADV to a high degree, one should consider eliminating the advisor from consideration.

Registering with a state or SEC gives an advisor a fiduciary duty to the client. This is a high standard under the law.

There are several types of advisors who are exempt from registering and filing an ADV.

First, there are registered representatives (brokers). Brokers have a fiduciary responsibility to their firms regardless of whether they are statutory employees or independent contractors. Not the client.

Second are attorneys and accountants whose advice is “incidental” to their legal or accounting practices. But, why would one hire someone whose advice is “incidental” to his primary profession? A top-notch advisor is a full-time professional and should be registered. One should insist that their advisor be registered.

The ADV will describe the advisor’s background and employment history, including any prior disciplinary issues. It will describe the ownership of the firm and outline how the firm and advisor are compensated. Any referral arrangements will be described. If an advisor has an interest in any of the investments to be recommended, it must be listed as well as the fee schedule. There is also a description of the types of investments recommended and the types of research information that is used.

ASSESSMENT: A review of the ADV should result in an alignment of what the advisor said during the interview and what is filed with the regulators. If there is a clear discrepancy, choose another advisor. If it is unclear, discuss the issue with the advisor.

Your thoughts and comments are appreciated.

SEC Headquarters 100 F Street, NE Washington, DC 20549 (202) 942-8088

Posted on April 28, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Economy: The US economy entered a 12 mph zone last quarter, slowing to an annual growth rate of 1.1% (short of estimates). While the growth figures were discouraging and a consequence of the Fed’s interest rate hikes, economists found some bright spots! It seems that consumers won’t stop shopping, resulting in a 3.7% increase in consumer spending. Still, some are waiting on that recession?

***

So – Here’s where the key indexes settled yesterday.

The S&P 500 Index was up 79.36 (2%) at 4135.35; the Dow Jones industrial average was up 524.29 (1.6%) at 33,826.16; the NASDAQ Composite was up 287.89 (2.4%) at 12,142.24.

The 10-year Treasury yield was up about 9 basis points at 3.524%.

CBOE’s Volatility Index was down 1.90 at 16.94.

Small-cap companies, which tend to struggle more when economic growth stalls, remained at the back of the pack, with the Russell 2000 up slightly over 1%.

The energy sector continued to rank among the weakest-performing sectors, as crude oil futures continued trading near lows for the month.

Treasury yields jumped to one-week highs after the first-quarter gross domestic product (GDP) report showed inflation remained elevated.

Posted on April 26, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

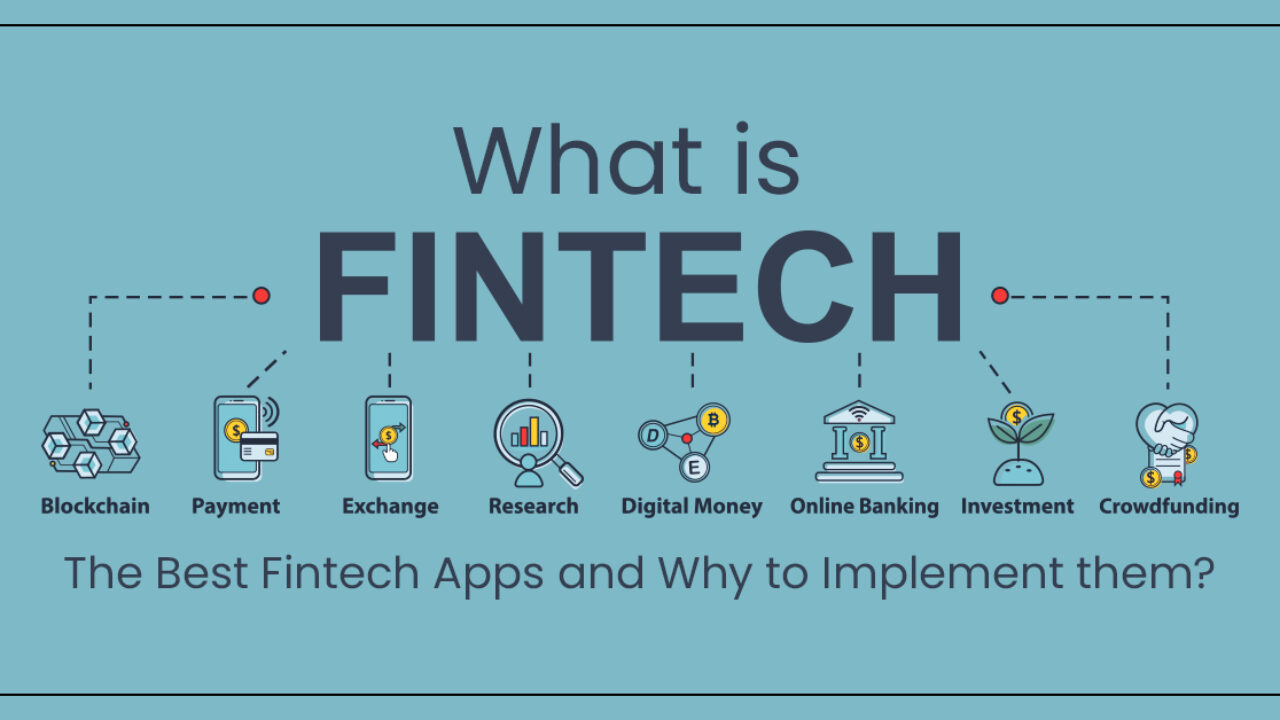

DEFINITION: Financial technology (abbreviated fintech or FinTech) is the technology and innovation that aims to compete with traditional financial methods in the delivery of financial services. Artificial intelligence, Blockchain, Cloud computing, and big Data are regarded as the “ABCD” (four key areas) of FinTech. The Fintech industry is an emerging industry that uses technology to improve activities in finance. The use of smartphones for mobile banking, investing, borrowing services,and cryptocurrency are examples of technologies aiming to make financial services more accessible to the general public.

***

Financial technology companies consist of both startups and established financial institutions and technology companies trying to replace or enhance the usage of financial services provided by existing financial companies.

Posted on April 25, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Physicians Who Accept Medicare, Medicaid at All-time Low of 65%

Reduced Medicare and Medicaid payments are having more physicians considering reducing those patient bases, according to Medscape’s “Physician Compensation Report” for 2023. Sixty-five percent of physicians surveyed said they would continue treating current Medicare or Medicaid patients and take on new ones, according to the report. Medscape said it is the lowest percentage it has seen in its annual compensation reports. Five years ago, 71 percent of physicians said they would continue treating current Medicare or Medicaid patients and take on new ones.

For the report, Medscape collected responses from 10,011 physicians across more than 29 specialties. The data was collected between Oct. 7, 2022, and Jan. 17, 2023. Eight percent of physicians surveyed said they would not take on new Medicare patients, and 5 percent said they would not take new Medicaid patients. Four percent said they will stop treating some or all of their current Medicare patients and will not take on new ones, and 3 percent said the same about Medicaid patients. Twenty-two percent said they have not yet decided how they will move forward regarding Medicare and Medicaid patients, according to the report.

Source: Andrew Cass, Becker’s Payer Issues [4/18/23]

Posted on April 22, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

FTX is acryptocurrency exchange that was launched in 2018. It specializes in trading products such as derivatives, leveraged tokens, options, and volatility products. It supports most commonly traded cryptocurrencies and is powered by a top liquidity provider. FTX stands for Futures Exchange, a market where users can invest in commodities and foreign exchange.

Quote: “We sometimes find $50m of assets lying around that we lost track of; such is life.”

The sudden collapse of FTX might have been a lot less surprising if you’d been privy to Sam Bankman-Fried’s messages to his fellow executives.

According to a report by the bankrupt crypto exchange’s new management, SBF allegedly found the company’s lack of proper accounting amusing. The report says he described the company’s related hedge fund Alameda Research as “hilariously beyond any threshold of any auditor being able to even get partially through an audit” and joked about misplacing millions.

Posted on April 21, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

(Bloomberg) — A US debt default would threaten “a basic anchor” of the global financial system and “must not happen,” BlackRock Inc. Vice Chairman Philipp Hildebrand warned Thursday at the Bloomberg New Economy Gateway Europe forum.

“All we can do is to pray that everyone in the United States understands how important the sanctity of the sovereign signature of the leading currency, of the leading bond market, of the leading economy in the world is,” Hildebrand, a former president of the Swiss central bank, said during an on-stage interview. “This is not something you want to mess with.”

The 10-year Treasury yield hit a four-week high above 3.60% earlier this week, up from a seven-month low of 3.278% on April 4th.

The S&P 500 Index was down 24.73 (0.6%) at 4129.79; the Dow Jones industrial average was down 110.39 (0.3%) at 33,786.62; the NASDAQ Composite was down 97.67 (0.8%) at 12,059.56.

The 10-year Treasury yield was down about 7 basis points at 3.534%.

CBOEs Volatility Index was up 0.73 at 17.19.

Energy companies were among the weakest performers Thursday, as crude oil prices extended this week’s sell-off, with benchmark WTI futures down more than 2% to under $78 per barrel—a low for the month.

The real estate and technology sectors also lagged, while consumer staples and transportation sectors held up better.

National Healthcare Decisions Day (NHDD) exists to inspire, educate and empower the public and providers about the importance of advance care planning. NHDD is an initiative to encourage patients to express their wishes regarding healthcare and for providers and facilities to respect those wishes, whatever they may be.

NHDD was founded in 2008 by Nathan Kottkamp, a Virginia-based health care lawyer, to provide clear, concise, and consistent information on healthcare decision-making to both the public and providers/facilities through the widespread availability and dissemination of simple, free, and uniform tools (not just forms) to guide the process.

NHDD is a series of independent events held across the country, supported by a national media and public education campaign. In all respects, NHDD is inclusive and brings a variety of players in the larger healthcare, legal, and religious community together to work on a common project, to the benefit of patients, families, and providers. A key goal of NHDD is to demystify healthcare decision-making and make the topic of advance care planning inescapable. Among other things, NHDD helps people understand that advance healthcare decision-making includes much more than living wills; it is a process that should focus first on conversation and choosing an agent.

As of June 2016, The Conversation Project has been responsible for the management, finances, and structure of NHDD. NHDD’s founder, Nathan Kottkamp, continues to be involved in NHDD and provides leadership by ensuring the maintenance of NHDD’s high quality resources and support for the community.

DEFINITION: What is advance care planning for financial advisors and lawyers?

Advance care planning involves discussing and preparing for future decisions about your medical care if you become seriously ill or unable to communicate your wishes with your estate planning attorney or financial advisor. Having meaningful conversations with your loved ones is the most important part of advance care planning. Many people also choose to put their preferences in writing by completing legal documents called advance directives.

What are advance directives?

Advance directives are legal documents that provide instructions for medical care and only go into effect if you cannot communicate your own wishes.

The two most common advance directives for health care are the living will and the durable power of attorney for health care.

Living will: A living will is a legal document that tells doctors how you want to be treated if you cannot make your own decisions about emergency treatment. In a living will, you can say which common medical treatments or care you would want, which ones you would want to avoid, and under which conditions each of your choices applies. Learn more about preparing a living will.

Durable power of attorneyfor health care: A durable power of attorney for health care is a legal document that names your health care proxy, a person who can make health care decisions for you if you are unable to communicate these yourself. Your proxy, also known as a representative, surrogate, or agent, should be familiar with your values and wishes. A proxy can be chosen in addition to or instead of a living will. Having a health care proxy helps you plan for situations that cannot be foreseen, such as a serious car accident or stroke. Learn more about choosing a health care proxy.

Think of your advance directives as living documents that you review at least once each year and update if a major life event occurs such as retirement, moving out of state, or a significant change in your health.

Advance care planning is not just for people who are very old or ill. At any age, a medical crisis could leave you unable to communicate your own health care decisions. Planning now for your future health care can help ensure you get the medical care you want and that someone you trust will be there to make decisions for you.

Advance care planning for people with dementia. Many people do not realize that Alzheimer’s disease and related dementias are terminal conditions and ultimately result in death. People in the later stages of dementia often lose their ability to do the simplest tasks. If you have dementia, advance care planning can give you a sense of control over an uncertain future and enable you to participate directly in decision-making about your future care. If you are a loved one of someone with dementia, encourage these discussions as early as possible. In the later stages of dementia, you may wish to discuss decisions with other family members, your loved one’s health care provider, or a trusted friend to feel more supported when deciding the types of care and treatments the person would want.

What happens if you do not have an advance directive?

If you do not have an advance directive and you are unable to make decisions on your own, the state laws where you live will determine who may make medical decisions on your behalf. This is typically your spouse, your parents if they are available, or your children if they are adults. If you are unmarried and have not named your partner as your proxy, it’s possible they could be excluded from decision-making. If you have no family members, some states allow a close friend who is familiar with your values to help. Or they may assign a physician to represent your best interests. To find out the laws in your state, contact your state legal aid office or state bar association.

Will an advance directive guarantee your wishes are followed?

An advance directive is legally recognized but not legally binding. This means that your health care provider and proxy will do their best to respect your advance directives, but there may be circumstances in which they cannot follow your wishes exactly. For example, you may be in a complex medical situation where it is unclear what you would want. This is another key reason why having conversations about your preferences is so important. Talking with your loved ones ahead of time may help them better navigate unanticipated issues.

There is the possibility that a health care provider refuses to follow your advance directives. This might happen if the decision goes against:

The health care provider’s conscience

The health care institution’s policy

Accepted health care standards

In these situations, the health care provider must inform your health care proxy immediately and consider transferring your care to another provider.

Other advance care planning forms and orders from doctors

You might want to prepare documents to express your wishes about a single medical issue or something else not already covered in your advance directives, such as an emergency. For these types of situations, you can talk with a doctor about establishing the following orders:

Do not resuscitate (DNR) order: A DNR becomes part of your medical chart to inform medical staff in a hospital or nursing facility that you do not want CPR or other life-support measures to be attempted if your heartbeat and breathing stop. Sometimes this document is referred to as a do not attempt resuscitation (DNR) order or an allow natural death (AND) order. Even though a living will might state that CPR is not wanted, it is helpful to have a DNR order as part of your medical file if you go to a hospital. Posting a DNR next to your hospital bed might avoid confusion in an emergency. Without a DNR order, medical staff will attempt every effort to restore your breathing and the normal rhythm of your heart.

Do not intubate (DNI) order: A similar document, a DNI informs medical staff in a hospital or nursing facility that you do not want to be on a ventilator.

Do not hospitalize (DNH) order: A DNH indicates to long-term care providers, such as nursing home staff, that you prefer not to be sent to a hospital for treatment at the end of life.

Out-of-hospital DNR order: An out-of-hospital DNR alerts emergency medical personnel to your wishes regarding measures to restore your heartbeat or breathing if you are not in a hospital.

Physician orders for life-sustaining treatment (POLST) and medical orders for life-sustaining treatment (MOLST) forms:These forms provide guidance about your medical care that health care professionals can act on immediately in an emergency. They serve as a medical order in addition to your advance directive. Typically, you create a POLST or MOLST when you are near the end of life or critically ill and understand the specific decisions that might need to be made on your behalf. These forms may also be called portable medical orders or physician orders for scope of treatment (POST). Check with your state department of health to find out if these forms are available where you live.

At enrollment, Medicare in the future could offer three advancedirectives with goals of care: DirectiveA: CONSENT to treat — inpatient medical treatment DirectiveB: CONSENT to comfort — home bound holistic care DirectiveC: CHOOSE against medical advice — outpatient palliative resources.

The Fed rate hikes that spelled doom for smaller fries like Silicon Valley Bank and Signature Bank were a boon to the big potatoes since they could charge more for loans. With the money they made from lending shooting up, JPMorgan, Citigroup, and Wells Fargo all zoomed past expectations for Q1.

JPMorgan, the biggest of the big, posted record revenues and saw its profits spike to $12.6 billion, 52% more than the same quarter last year.

Citigroup, the third largest US bank, scored $4.6 billion in profit, 7% higher than in Q1 2022.

Wells Fargo, the fourth largest, kept the hot streak going with a 32% increase in profits from the first quarter of ’22 to just under $5 billion.

The banking behemoths have made it through the chaos caused by the biggest bank failures since 2008 not just unscathed but stronger—though there’s some debate over whether they’ll be able to hang on to the many new deposits that came their way as customers fled from regional lenders.

But smaller banks are still struggling. And there were signs the three megabanks weren’t ready to declare total victory: They cautioned that credit is likely about to get more expensive and put aside a combined $2 billion in case a recession hits.

The domestic stock markets owe much of their resilience today to the strength of the biggest companies, which investors tend to favor when recessions appear likely, though financial stocks have lagged most of the year, according to Liz Ann Sonders, chief investment strategist at the Schwab Center for Financial Research. Indeed, small-cap stocks were notable laggards yesterday, with the Russell 2000 index falling more than 1%.

The markets appear convinced the Fed will raise its benchmark interest rate by another quarter of a point in May, taking it to a range of 5%–5.25%, even after the larger-than-expected de-celerations in both consumer and producer prices reported earlier this week.

The following is a round-up of yesterday’s market activity:

The S&P 500 Index was down 8.58 (0.2%) at 4137.64; the Dow Jones industrial average was down 143.22 (0.4%) at 33,886.47; the NASDAQ Composite was down 42.81 (0.4%) at 12,123.47.

The 10-year Treasury yield was up about 6 basis points at 3.515%.

CBOE’s Volatility Index was down 0.73 at 17.07.

Among S&P 500 sectors, real estate and utilities were among the weaker performers yesterday. Notwithstanding the day’s weakness, volatility expectations as measured by the VIX dropped to its lowest level since late 2021.

WTI crude oil futures rose modestly and have surged about 24% over the past four weeks, illustrating still-present inflationary forces.

Posted on April 14, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

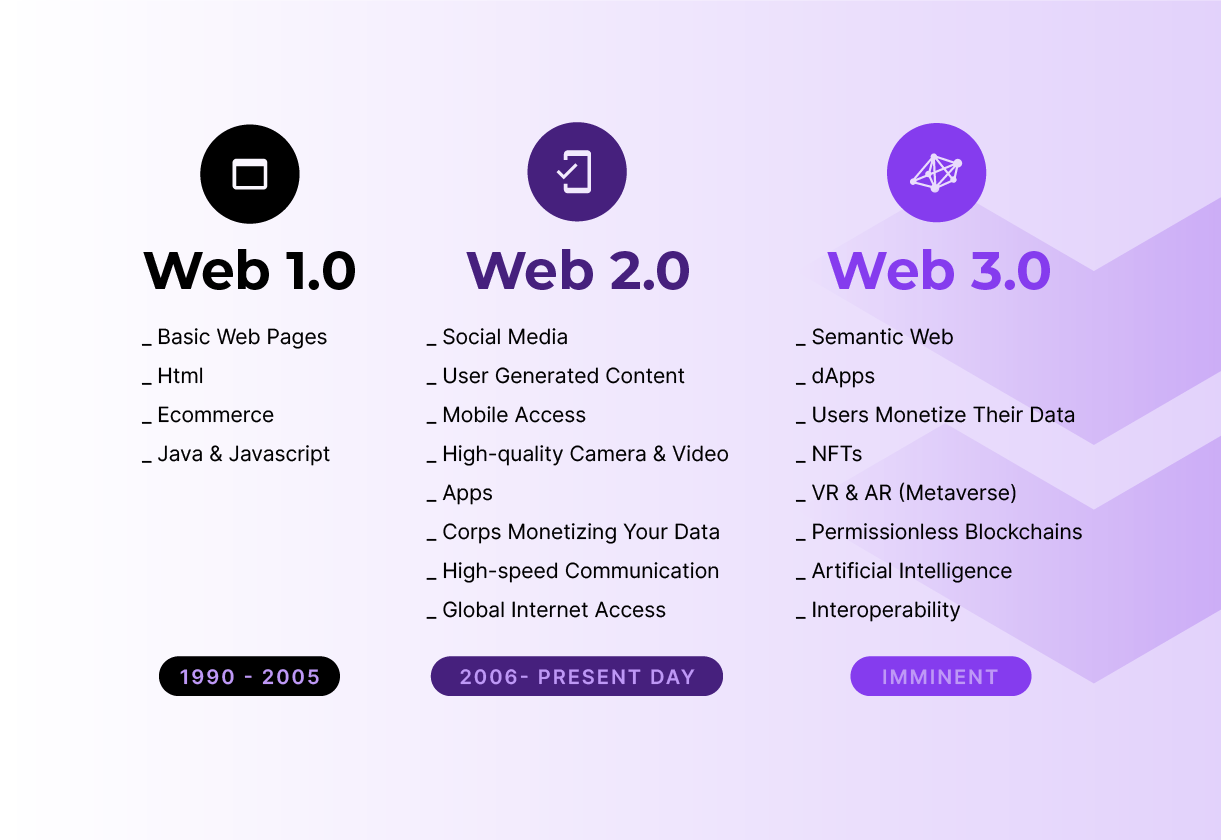

According to Wikipedia, the Web3 (also known as Web 3.0 and sometimes stylized as web3) is an idea for a new iteration of the World Wide Web based on blockchain technology, which incorporates concepts such as decentralization and token-based economics. Some technologists and journalists have contrasted it with Web 2.0, wherein they say data and content are centralized in a small group of companies sometimes referred to as “Big Tech“. The term “Web3” was coined in 2014 by Ethereum co-founder Gavin Wood, and the idea gained interest in 2021 from cryptocurrency enthusiasts, large technology companies, and venture capital firms.

***

***

Now, some experts argue that web3 will provide increased data security, scalability, and privacy for users and combat the influence of large technology companies.

Others have raised concerns about a decentralized web, citing the potential for low moderation and the proliferation of harmful content,the centralization of wealth to a small group of investors and individuals, or a loss of privacy due to more expansive data collection. Others, such as Elon Musk and Jack Dorsey, have argued that web3 only currently serves as a buzzword.

Posted on April 14, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

A rally on Wall Street yesterday is lifting stocks to their highest level in almost two months following the latest sign that inflation continues to cool. Yesterday’s report showed that prices paid to producers last month were 2.7% higher than a year earlier, the lowest inflation level there in more than two years. The hope on Wall Street is that easier inflation on the wholesale level will not only support profits for companies but also flow through to cooler inflation for consumers. A day earlier, a separate report said inflation for consumers slowed to 5%.

Inflation and how high the Federal Reserve will hike interest rates to tame it have been at the center of Wall Street’s struggles for more than a year. The Fed has hiked rates at such a feverish pace over the last year that it’s already slowed parts of the economy and caused strains to appear in the banking system.

And so, stocks climbed on the cooler-than-expected PPI, and perhaps some optimism around the Q1 earnings season, with several big banks reporting Friday. However, expectations around Fed policy didn’t budge much.

Bond yields were little changed and markets still see a 70% probability of the Fed enacting a quarter-point rate increase in May, according to the CME FedWatch tool.

The following is a round-up of yesterday’s market activity:

The S&P 500 Index was up 54.27 points (1.3%) at 4146.22; the Dow Jones industrial average was up 383.19 (1.1%) at 34,029.69; the NASDAQ Composite was up 236.93 (2.0%) at 12,166.27.

The 10-year Treasury yield was up about 3 basis points at 3.447%.

Posted on April 14, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

Of Characteristics and Commonalities

[By Dr. David Edward Marcinko MBA CMP™]

[By Eugene Schmuckler PhD MBA EMd CTS]

It does not matter if you are in the healthcare or financial services sector; or both.

Many psychologists and behavioral experts believe there are commonalities and characteristics applicable to all industries and sectors; including education which is a big part of what we do here at the Medical Executive Post.

Key Leadership Competencies – Definitions

And so, here is a list of key leadership competencies and definitions for your review.

Living by personal conviction – Means you know and are in touch with your values and beliefs, are not afraid to take a lonely or unpopular stance if necessary, are comfortable in tough situations, can be relied on in intense circumstances, are clear about where you stand, and will face difficult challenges with poise and self-assurance.

Possessing emotional intelligence – Means you recognize personal strengths and weaknesses; see the linkages between feelings and behaviors; manage impulsive feelings and distressing emotions; are attentive to emotional cues; show sensitivity and respect for others; challenge bias and intolerance; collaborate and share; are an open communicator; and can handle conflict, difficult people, and tense situations effectively. Emotional intelligence may often be labeled EQ, or emotional intelligence quotient.

Being visionary – Means that you see the future clearly, anticipate large-scale and local changes that will affect the organization and its environment, are able to project the organization into the future and envision multiple potential scenarios/outcomes, have a broad way of looking at trends, and are able to design competitive strategies and plans based on future possibilities.

Communicating vision – Means that you distill complex strategies into a compelling call to march, inspire and help others see a core reason for the organization to make change, talk beyond the day-to-day tactical matters that face the organization, show confidence and optimism about the future state of the organization, and engage others to join in.

Earning loyalty and trust – Means you are a direct and truthful person; are willing to admit mistakes; are sincerely interested in the concerns and dreams of others; show empathy and a generally helpful orientation toward others; follow promises with actions; maintain confidences and disclose information ethically and appropriately; and conduct work in open, transparent ways.

Listening like you mean it – Means you maintain a calm, easy-to-approach demeanor, are patient, open minded, and willing to hear people out; understand others and pick up the meaning of their messages; are warm, gracious and inviting; build strong rapport; see through the words that others express to the real meaning (i.e., cut to the heart of the issue); and maintain formal and informal channels of communication.

Giving feedback – Means you set clear expectations, bring important issues to the table in a way that helps others “hear” them, show an openness to facing difficult topics and sources of conflict, deal with problems and difficult people directly and frankly, provide timely criticism when needed, and provide feedback messages that are clear and unambiguous.

Mentoring others – Means you invest the time to understand the career aspirations of your direct reports, work with direct reports to create engaging mentoring plans, support staff in developing their skills, support career development in a non-possessive way (will support staff moving up and out as necessary for their advancement), find stretch assignments and other delegation opportunities that support skill development, and role model professional development by advancing your own skills.

Developing teams – Means you select executives who will be strong team players, actively support the concept of teaming, develop open discourse and encourage healthy debate on important issues, create compelling reasons and incentives for team members to work together, effectively set limits on the political activity that takes place outside the team framework, celebrate successes together as a unit, and commiserate as a group over disappointments.

Energizing staff – Means you set a personal example of good work ethic and motivation; talk and act enthusiastically and optimistically about the future; enjoy rising to new challenges; take on your work with energy, passion and drive to finish successfully; help others recognize the importance of their work; are enjoyable to work for; and have a goal oriented, ambitious and determined working style.

Generating informal power – Means you understand the roles of power and influence in organizations; develop compelling arguments or points of view based on knowledge of others’ priorities; develop and sustain useful networks up, down and sideways in the organization; develop a reputation as a go-to person; and effectively affect the thoughts and opinions of others, both directly and indirectly, through others.

Building consensus – Means you frame issues in ways that facilitate clarity from multiple perspectives, keep issues separated from personalities, skillfully use group decision techniques (e.g., Nominal Group Technique), ensure that quieter group members are drawn into discussions, find shared values and common adversaries, and facilitate discussions rather than guide them.

Making decisions effectively – Means you make decisions based on an optimal mix of ethics, values, goals, facts, alternatives and judgments; use decision tools (such as force-field analysis, cost-benefit analysis, decision trees, paired comparisons analysis) effectively and at appropriate times; and show a good sense of timing related to decision making.

Driving results – Means you mobilize people toward greater commitment to a vision, challenge people to set higher standards and goals, keep people focused on achieving goals, give direct and complete feedback that keeps teams and individuals on track, quickly take corrective action as necessary to keep everyone moving forward, show a bias toward action, and proactively work through performance barriers.

Stimulating creativity – Means you see broadly outside of the typical, are constantly open to new ideas, are effective with creative group processes (e.g., brainstorming, Nominal Group Technique, scenario building), see future trends and craft responses to them, are knowledgeable in business and societal trends, are aware of how strategies play out in the field, are well read, and make connections between industries and unrelated trends.

Cultivating adaptability – Means you quickly see the essence of issues and problems, effectively bring clarity to situations of ambiguity, approach work using a variety of leadership styles and techniques, track changing priorities and readily interpret their implications, balance consistency of focus against the ability to adjust course as needed, balance multiple tasks and priorities such that each gets appropriate attention, and work effectively with a broad range of people.

Is if often said that leaders rise to the occasion. What do you think?

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on April 13, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Stock share spotlight

Alibaba shares dipped yesterday thanks to China’s efforts to crack down on AI chatbots and fell even further after-hours when the Financial Times reported that SoftBank has sold off most of its stake in the company.

Posted on April 10, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

Types & Definitions

****

Financial Investing risk is any of various types of risk associated with financing, including financial transactions that include company loans in risk of default. Often it is understood to include only downside risk, meaning the potential for financial loss and uncertainty about its extent.

Although broad investing risks can be quickly summarized as “the failure to achieve spending and inflation-adjusted growth goals,” individual assets may face any number of other subsidiary risks:

Call risk – The risk, faced by a holder of a callable bond that a bond issuer will take advantage of the callable bond feature and redeem the issue prior to maturity. This means the bondholder will receive payment on the value of the bond and, in most cases, will be reinvesting in a less favorable environment (one with a lower interest rate)

Capital risk – The risk an investor faces that he or she may lose all or part of the principal amount invested.

Commodity risk – The threat that a change in the price of a production input will adversely impact a producer who uses that input.

Company risk – The risk that certain factors affecting a specific company may cause its stock to change in price in a different way from stocks as a whole.

Concentration risk – Probability of loss arising from heavily lopsided exposure to a particular group of counterparties

Counterparty risk – The risk that the other party to an agreement will default.

Credit risk – The risk of loss of principal or loss of a financial reward stemming from a borrower’s failure to repay a loan or otherwise meet a contractual obligation.

Currency risk – A form of risk that arises from the change in price of one currency against another.

Deflation risk – A general decline in prices, often caused by a reduction in the supply of money or credit.

Economic risk – the likelihood that an investment will be affected by macroeconomic conditions such as government regulation, exchange rates, or political stability.

Hedging risk – Making an investment to reduce the risk of adverse price movements in an asset.

Inflation risk – The uncertainty over the future real value (after inflation) of your investment.

Interest rate risk – Risk to the earnings or market value of a portfolio due to uncertain future interest rates.

Legal risk – risk from uncertainty due to legal actions or uncertainty in the applicability or interpretation of contracts, laws or regulations.

Liquidity risk – The risks stemming from the lack of marketability of an investment that cannot be bought or sold quickly enough to prevent or minimize a loss.

Posted on April 6, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Understanding FDIC insurance limits

The FDIC wants to make sure it can cover everyone with a bank account, so to make that happen, it caps how much money it insures. The FDIC says its standard is to cover up to “$250,000 per depositor, per insured bank, for each account ownership category.

Here’s an example: Let’s say you have $100,000 in your checking account and $150,000 in your savings, all at the same bank. The FDIC classifies those under the same category: single accounts.So you would have hit your FDIC deposit limit. Every additional cent deposited into either account would be uninsured. But if you have money in other banks or other deposit categories, you may have additional coverage.

Could the insured deposit cap get a lift?

At least four US lawmakers—two from each side of the aisle—said they would support raising the cap on FDIC-insured deposits in order to reassure frazzled bank customers that their deposits are safe. The current cap is $250,000 (up from $100k pre-financial crisis), but Democratic Sen. Elizabeth Warren said bumping it up “is a good move.” Opponents of raising the cap say it would only increase risk-taking and bad behavior by banks. Some even argue we should lower it.

Posted on April 6, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

“Sameach Pesach”

Holy [Maundy] Thursday

By Staff Reporters

***

Markets: The NASDAQ extended its losing streak for a third day yesterday amidst a mixed showing for stocks overall. Among the tech stocks having a rough day was cybersecurity giant Zscaler, as investors got new data suggesting the labor market may be cooling (setting off recession jitters again).

***

This week’s economic numbers “all point to a softening economy,” but not necessarily a “soft landing,” says Kevin Gordon, senior investment strategist at the Schwab Center for Financial Research. An economic slowdown that averts recession “is what the Fed is looking for, but the market is saying today—with both stock prices and bond yields lower—that recession fears are outweighing hopes for a soft landing,” Kevin says.

The S&P 500® Index fell 10.22 points (0.3%) to 4090.38; the Dow Jones industrial average rose 80.34 (0.2%) to 33482.72; the NASDAQ Composite fell 129.47 (1.1%) to 11996.86.

The 10-year Treasury yield fell about 3 basis points to 3.309%.

CBOEs Volatility Index was up 0.12 at 19.12.

Among S&P 500 sectors, consumer discretionary and industrial stocks led declines. One bright spot was the healthcare sector, which jumped nearly 2%, helped by gains in Johnson & Johnson (JNJ) and Eli Lilly (LLY). Recession concerns weighed particularly heavily on small-cap stocks, as the Russell 2000 index dropped near a two-week low. WTI crude futures fell slightly but remained above $80 a barrel and near two-month highs.

Gold futures extended this week’s rally and ended at a 13-month high.

Posted on April 5, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Happy Passover to all those celebrating tonight

***

Johnson & Johnson proposes monster $8.9 billion talc settlement. The healthcare giant offered $8.9 billion to settle lawsuits from tens of thousands of people who claim that its talc-based powders and other products gave them cancer. It’s a huge increase from the $2 billion J&J originally offered and would be one of the largest product liability settlements in history, according to the WSJ. To clinch the settlement, J&J needs support from more than 75% of the voting claimants—and it thinks it has it.

And here’s how the major indexes performed yesterday, Tuesday:

The S&P 500 Index fell 23.91 points (0.6%) to 4,100.60; the Dow Jones industrial average fell 198.77 (0.6%) to 33,402.38; the NASDAQ Composite fell 63.13 (0.5%) to 12,126.33.

The 10-year Treasury yield fell about 9 basis points to 3.346%.

Small-cap stocks were among the weakest performers Tuesday, with the Russell 2000 index sinking more than 2%. Industrial, energy, and financial stocks led decliners among S&P 500 sectors. Gold futures surged to a 13-month high, while the U.S. dollar index slipped.

Shares of Walmart fell as the largest U.S. retailer began its investor meeting Tuesday. Comments from Walmart executives could offer indications on the overall financial health and spending patterns of U.S. consumers. The company said in February that high prices and weak demand for discretionary items could be headwinds.

Posted on April 4, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Major U.S. stock indexes ended mixed, after the announcement of a surprise OPEC+ production cut sent crude oil prices to two-month highs and fueled inflation concerns that could keep the Federal Reserve in policy-tightening mode. This weekend, several OPEC+ members, including Saudi Arabia, announced production cuts totaling nearly 1.2 million barrels a day that are slated to start in May. In response, WTI crude futures soared above $80 a barrel. Word of the planned cuts also boosted expectations that the Fed could raise its benchmark interest rate again in May as the central bank extends efforts to tamp down inflation. The OPEC+ cuts “suggest more headline inflation pressure in the near-term,” says Jeffrey Kleintop, chief global investment strategist at Charles Schwab & Co. The potential for further waves of inflation will “keep central banks from declaring victory over excessive price gains,” he adds. “That’s another headwind for tech stocks and other ‘long duration’ equities that get more of their cash flow in the future than in the near term.”

The following is a round-up of today’s market activity:

The S&P 500® Index was up 15.2 (0.4%) at 4124.51, the highest close since Feb. 15; the Dow Jones industrial average was up 327 (1.0%) at 33601.15; the NASDAQ Composite was down 32.45 (0.3%) at 12189.45.

The 10-year Treasury yield was down about 7 basis points at 3.417%.

CBOE’s Volatility Index was down 0.14 at 18.56.

Oil producers and other energy companies led gainers Monday. Health care stocks also outperformed. Consumer discretionary and real estate were among the laggards.

Among individual stocks, Tesla (TSLA) shares tumbled over 6% following reports the electric car-maker delivered just 423,000 vehicles in the first quarter. Analysts had expected 430,000, according to research firm FactSet.

Looking ahead, medical companies, especially vaccine makers, may be worth watching this week with the World Vaccine Congress taking place in Washington, D.C. Some well-known vaccine makers include Moderna (MRNA), Johnson & Johnson (JNJ), and GlaxoSmithKline (GSK). Late last month, Walgreens Boots Alliance (WBA) reported a steep year-over-year decline in demand for COVID-19 vaccinations.

The U.S. dollar index fell slightly, while gold futures climbed above $2,000 per ounce to post their highest close in over two years.

Posted on April 2, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

A disastrous month of March is what Charles Schwab has just experienced. An avalanche of bad news fell on the firm. The stock fell 33% between Feb. 28 and Mar. 31. At the end of February, Charles Schwab’s shares were trading at around $77.92. A month later the price is now $52.38. The difference translates to more than $47 billion in market capitalization wiped out in just one month. According to Bloomberg News, this is Charles Schwab’s worst month since the October 1987 stock market crash, known as Black Monday. That day, the Dow Jones index lost 508 points, a decline of 22.6% and the largest daily decline in a stock market index at the time. Only the drop by 76% of the Icelandic stock market in 2008 would exceed this record.

VERSUS

With the first quarter of 2023 behind us, and despite wild fluctuation due to continuous rate hikes from the Fed and an unexpected bank panic, stocks and bonds managed to turn in a pretty, pretty, pretty good performance for the quarter. The S&P 500 gained 7%, and the Dow Jones Industrial Average gained 0.4%. But if the market’s metaphorical report card is impressive, tech companies were indisputably the honors students.

Wall Street rewarded tech companies’ layoffs and other cost cutting measures, giving tech stocks a resurgence. And with ChatGPT becoming a household name, investors have their money on generative AI as the next big bet. As of last night:

The tech-heavy NASDAQ Composite index rose a whopping 18% since January 1, its largest quarterly gain in two years.

Stocks of the tech giants leading the charge in AI-powered search, Microsoft and Alphabet, are up 20% and 16%, respectively.

Bank stocks were a delight for short sellers, who made $2 billion betting against the sector in the past three months.

Smaller institutions were most badly injured by the bank panic: The SPRD S&P Regional Banking ETF, which consists of non-behemoth banks, had more than a quarter of its value wiped out in Q1.

Large banks are feeling the pinch of rising interest rates: Global merger and acquisition deals suffered the biggest first-quarter decline since 2001, according to data analyzed by the Financial Times.

Posted on April 2, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

WORKPLACE MEDICAL VIOLENCE

By Staff Reporters

***

***

Workplace safety is no joke. Slips and trips can lead to a hospital visit—though at least it’s a quick commute for healthcare workers in states with high rates of workplace injuries. In fact, Maine, Oregon, and Vermont had the highest rates of nonfatal workplace accidents and injuries, according to an analysis shared with Healthcare Brew via email of 2021 US Bureau of Labor Statistics data compiled by High Rise Financial, a pre-settlement legal funding company.

What do these states also have in common? According to HealthcareBrew, nursing, ranked within the top 10 most popular professions in each state.

Maine had the highest rate of workplace accidents: 4.7 out of every 100 full-time workers in the state were involved in a nonfatal workplace accident in 2021, High Rise Financial found. That is 67.9% higher than the country’s yearly average. In 2021, 30,270 of the 592,000 registered employees in Maine were home healthcare workers or registered nurses. MaineHealth was the state’s largest private employer in 2021 with approximately 20,500 employees, per the Maine Center for Workforce Research and Information. But the state’s high accident rate isn’t a failure—it suggests that Maine workers are reporting accidents and injuries before they become more serious and require workers’ compensation, Maine Public Radio reported. The most recent data from 2011 shows that workers’ compensation losses cost hospitals nationwide $2 billion, the Occupational Safety and Health Administration found.

If tedious workplace safety rules sound like a pain, try having an accident. “Slips, trips, and falls,” especially without a wet floor warning sign, are the top causes of workplace accidents that are eligible for pre-settlement funding, according to the High Rise Financial analysis. Even a small slip could lead to a back injury, a broken bone, or a concussion—no banana peel needed.

It’s not all doom and gloom: The CDC has generously curated a list of songs with workplace safety and health themes to liven up your nine-to-five. Just be sure to wear nonslip shoes if you feel like dancing.

Posted on April 1, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

Medicare Advantage (MA) plans, also known as Part C plans, serve as a supplement or an alternative to Original (also called Traditional) fee-for-service (FFS) Medicare Part A and Part B coverage, but they are still part of the Medicare program.

Most of these plans also include Part D (drug) coverage. MA was created by Congress to offer seniors an alternative to Original Medicare – with an emphasis on treating and managing the health of the whole patient. MA plans are offered to Medicare beneficiaries by Medicare-approved private companies, known as MA Organizations (MAOs), that must follow rules set by Medicare. (Read more…)

Posted on March 27, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

Environmental, Social, and Corporate Governance

Florida is pulling $2 billion from BlackRock in the largest divestment ever made as part of the growing vendetta against Environmental, Social, and Governance (ESG) investing practices. Florida Governor Ron DeSantis and other Republican leaders claim that by taking ESG standards into account when making investment decisions, the firm isn’t prioritizing the bottom line. But, for a few years, things were good. In 2020 and 2021, ESG funds outperformed the market by ~4.3%.

DEFINITION: According to Wikipedia, ESG (environmental, social, and corporate governance) data reflect the externalities (costs to others) an organization is generating with respect to the environment, to society and to corporate governance. ESG data can be used by investors to assess the material risk the organization is taking and by the organization itself as metrics for strategic and managerial purposes. Investors may also use ESG data beyond assessing material risks to the organization in their evaluation of enterprise value, specifically by designing models based on assumptions that the identification, assessment and management of sustainability-related risks and opportunities in respect to all organizational stakeholders leads to higher long-term risk-adjusted return. Organizational stakeholders include but not limited to customers, suppliers, employees, leadership, and the environment.

Since 2020, there has been accelerating interest in overlaying ESG data with the Sustainable Development Goals (SDGs), developed based on work by United Nations beginning in the 1980s.

The term ESG was popularly used first in a 2004 report titled “Who Cares Wins”, which was a joint initiative of financial institutions at the invitation of UN. In less than 20 years, the ESG movement has grown from a corporate social responsibility initiative launched by the United Nations into a global phenomenon representing more than US$30 trillion in assets under management. In the year 2019 alone, capital totaling US$17.67 billion flowed into ESG-linked products, an almost 525 percent increase from 2015, according to Morningstar, Inc.. Critics claim ESG linked-products have not had and are unlikely to have the intended impact of raising the cost of capital for polluting firms, and have accused the movement of greenwashing.

DeSantis ran his most recent campaign on fighting the “woke ideology” he believes is infiltrating the state. As part of the fight, Florida passed a resolution in August that said ESG standards should be ignored when investing state funds.

And he’s not the only one:

Other Republican-controlled states, including Missouri and Louisiana, have moved almost $1.3 billion away from BlackRock for similar reasons.

Texas flagged BlackRock as a financial firm that boycotts the state’s energy industry (something BlackRock has denied).

Meanwhile, Democrats aren’t happy either…they criticize BlackRock and ESG investing in general for not going far enough (and for using lax standards that let oil giants onto lists of ESG investments).

Bottom line: According to the Morning Brew, BlackRock and Florida are now cursed to yell “How could you prioritize politics over returns?” back and forth for eternity, and the debate over ESG investing is far from over. Republicans are poised to take over the House—after a campaign season that BlackRock poured record cash into—so we’re likely to see more drama play out at the federal level soon.

Posted on March 26, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

A SURVEY-POLL

By Staff Reporters

***

A recent poll of 2,510 American adults by Ipsos found:

• 87% of Americans feel politicians have lost touch with what the public needs from their health care. • 86% of Americans agree that Congress should focus on cracking down on abusive health insurance practices that make it harder for people to get the care they need. • 71% of Americans would rather see Congress focus more on reducing the overall costs of health care coverage such as premiums, deductibles, and co-pays.

Posted on March 26, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

Tim Berners-Lee of the WWW

By Staff Reporters

***

***

* Profits are down, and they’re set to plummet even further. (Wired $) * A hedge fund that invested heavily in FTX is shutting down. (FT $) * Tim Berners-Lee thinks crypto is comparable to gambling. (CNBC)

Posted on March 23, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

AT1 BONDS =OH NO!

By Staff Reporters

***

***

DEFINITION: Junk bonds are bonds that carry a higher risk of default than most bonds issued by corporations and governments. A bond is a debt or promise to pay investors interest payments along with the return of invested principal in exchange for buying the bond. Junk bonds represent bonds issued by companies that are financially struggling and have a high risk of defaulting or not paying their interest payments or repaying the principal to investors. Junk bonds are also called high-yield bonds since the higher yield is needed to help offset any risk of default.

AT1 DEFINITION: Additional Tier 1 bonds are also known as “contingent convertibles,” or “CoCos”. They were created in the wake of the 2008 financial crisis as a way for failing banks to absorb losses, making a taxpayer-funded bailout less likely. They are a risky bet — if a lender gets into trouble, this class of bonds can be quickly converted into equity, or written down completely. Because they are higher-risk, AT1s offer a higher yield than most other bonds issued by borrowers with similar credit ratings, making them very risky. If AT1s are converted into equity, this supports a bank’s balance sheet and helps it to stay afloat. They also pave the way for a “bail-in”, or a way for banks to transfer risks to investors and away from taxpayers if they get into trouble.

UBS’s emergency takeover of Credit Suisse may have been necessary to avert a financial crisis, but at least one group is Yosemite Sam-level angry over how the deal shook out. Investors holding $17 billion worth of Credit Suisse’s additional tier-one bonds were shocked to discover that their $17 billion was now worth a grand total of…$0. The value of those bonds had been completely wiped out in the deal.

Additional tier-one bonds, or AT1 bonds for short, were established after the 2008 financial crisis to reduce the likelihood that taxpayers would have to bail out a failed bank. AT1s are considered riskier assets, but with that risk comes higher potential returns.

So, if these bondholders knew they were taking on risk, why are they so upset?

According to MorningBrew, mainly because, in this unusual deal, they got wiped out while shareholders didn’t. That’s not how the order of operations usually works:

When a write-down happens, shareholders traditionally suffer losses before bondholders get hit.

This deal flipped the food chain, and livid AT1 bondholders are now huddling up with lawyers about potential legal action.

OK – I was a Certified Financial Planner® before my academic team launched the Certified Medical Planner™ online and on-ground chartered education and board certification designation program a few years ago. I am now CFP reformed and in remission.

Enter the Certified Medical Planner™ CharteredDesignation

Today, we are of course, gratified that Certified Medical Planner™ mark notoriety is growing organically in the healthcare, as well as financial services, industry.

Even uber-blogger Mike Kitces MSFS, MTAX, CFP, CLU, ChFC, RHU, REBC, CASL has taken note of us in his musings on the Nerd’s Eye View website. And, the reality is that there are a growing number of CFP educational programs at the post-CFP niche market level.

But, none for healthcare industrial complex: for doctors … by doctors!

Popularity of our Text Books

However, it is our modern, innovative and proprietary Certified Medical Planner™ textbooks and dictionaries that have exploded in the academic marketplace.

In fact, they are now redacted in thousands of medical, graduate, law and B-schools and libraries, as well as colleges and universities throughout the nation. This includes the Library of Congress, National Institute of Health and the Library of Congress.

What Gives?

We have been told that this textbook popularity and publishing success is because of their balanced and peer-reviewed nature; something not very widespread in the financial services industry that is prone to gross and overstated advertising, salesmanship and marketing hyperbole. And, for this we are very gratified.

But, is there another reason our books are so popular?

A bit of networking and research suggests that interested folks may be eschewing the actual course work in favor of just the high quality textbooks! UGH!

So, what do you think? Matriculation with the professional mark versus self study without the designation mark. Please opine.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements.

Subscribe: MEDICAL EXECUTIVE POST for curated news, essays, opinions and analysis from the public health, economics, finance, marketing, IT, business and policy management ecosystem.

Posted on March 18, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

Blue Cross Blue Shield has deployed several trackers on its website, according to the web extension Ghostery, a tool that can tell you what kind of technology web pages are using.