BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on September 26, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I. and Staff Reporters

***

***

Bonds: The 10-year Treasury yield popped on solid economic data yesterday, including weekly jobless claims falling to their lowest since mid-July and Q2 GDP rising unexpectedly.

Stocks: But good news for the labor market and economy is bad news for anyone hoping the Federal Reserve cuts interest rates next month, and the major indexes sank for a third day in a row yesterday. All eyes now turn to today’s key PCE reading.

Crypto: Digital assets continued to tumble yesterday with ether falling below $4,000 for the first time in months. There may be more pain ahead: $22 billion in crypto options expire today.

The study of behavioral economics has revealed much about how different biases can affect our finances—often for the worse.

Take loss aversion: Because we feel a financial setback more acutely than a commensurate gain, we often cling to failed investments to avoid realizing the loss. Another potential hazard is present bias, or the tendency to prefer instant gratification over long-term reward, even if the latter gain is greater.

When it comes to money, sometimes it’s difficult to make rational decisions. Here, are three behavioral financial biases that could be impeding financial goals.

ANCHORING BIAS

Anchoring Bias happens when we place too much emphasis on the first piece of information we receive regarding a given subject. Anchoring is the mental trick your brain plays when it latches onto the first piece of information it gets, no matter how irrelevant. You might know this as a ‘first impression’ when someone relies on their own first idea of a person or situation.

Example: When shopping for a wedding ring a salesman might tell us to spend three months’ salary. After hearing this, we may feel like we are doing something wrong if we stray from this financial advice, even though the guideline provided may cause us to spend more than we can afford.

Example: Imagine you’re buying a car, and the salesperson starts with a high price. That number sticks in your mind and influences all your subsequent negotiations. Anchoring can skew our decisions and perceptions, making us think the first offer is more important than it is. Or, subsequent offers lower than they really are.

Example: Imagine an investor named Jane who purchased 100 shares of XYZ Corporation at $100 per share several years ago. Over time, the stock price declined to $60 per share. Jane is anchored to her initial price of $100 and is reluctant to sell at a loss because she keeps hoping the stock will return to her original purchase price. She continues to hold onto the stock, even as it declines, due to her anchoring bias. Eventually, the stock price drops to $40 per share, resulting in significant losses for Jane.

In this example, Jane’s nchoring bias to the original purchase price of $100 prevents her from rationalizing to sell the stock and cut her losses, even though market conditions have changed. So, the next time you’re haggling for your self, a potential customer or client, or making another big financial decision, be aware of that initial anchor dragging you down.

HERD MENTALITY BIAS

Herd Mentality Bias makes it very hard for humans to not take action when everyone around us does.

Example: We may hear stories of people making significant monetary profits buying, fixing up, and flipping homes and have the desire to get in on the action, even though we have no experience in real estate.

Example: During the dotcom bubble of the late 1990’s many investors exhibited a herd mentality. As technology stocks soared to astronomical valuations, investors rushed to buy these stocks driven by the fear of missing out on the gains others were enjoying. Even though some of these stocks had questionable fundamentals, the herd mentality led investors to follow the crowd.

In this example, the herd mentality contributed to the overvaluation of technology stocks. Eventually, it led to the dot-com bubble’s burst, causing significant losses for those who had unthinkingly followed the crowd without conducting proper research or analysis.

OVERCONFIDENT INVESTING BIAS

Overconfident Investing Bias happens when we believe we can out-smart other investors via market timing or through quick, frequent trading. This causes the results of a study to be unreliable and hard to reproduce in other research settings.

Example: Data convincingly shows that people and financial planners/advisors and wealth managers who trade most often under-perform the market by a significant margin over time. Active traders lose money.

Example: Overconfidence Investing Bias moreover leads to: (1) excessive trading (which in turn results in lower returns due to costs incurred), (2) underestimation of risk (portfolios of decreasing risk were found for single men, married men, married women, and single women), (3) illusion of knowledge (you can get a lot more data nowadays on the internet) and (4) illusion of control (on-line trading).

ASSESSMENT

Finally, questions remain after consuming this cognitive bias review.

Question: Can behavioral cognitive biases be eliminated by financial advisors in prospecting and client sales endeavors?

A: Indeed they can significantly reduce their impact by appreciating and understanding the above and following a disciplined and rational decision-making sales process.

Question: What is the role of financial advisors in helping clients and prospects address behavioral biases?

A: Financial advisors can provide an objective perspective and help investors recognize and address their biases. They can assist in creating well-structured investment and financial plans, setting realistic goals, and offering guidance to ensure investment decisions align with long-term objectives.

Question:How important is self-discipline in overcoming behavioral biases?

A; Self-discipline is crucial in overcoming behavioral biases. It helps investors and advisors adhere to their investment plans, avoid impulsive decisions, and stay focused on long-term goals reducing the influence of emotional and cognitive biases.

CONCLUSION

Remember, it is far more useful to listen to client beliefs, fears and goals, and to suggest options and offer encouragement to help them discover their own path toward financial well-being. Then, incentivize them with knowledge of the above psychological biases to your mutual success!

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

REFERENCES:

Marcinko, DE; Dictionary of Health Insurance and Managed Care. Springer Publishing Company, New York, 2007.

Marcinko, DE: Comprehensive Financial Planning Strategies for Doctors and Advisors: Best Practices from Leading Consultants and Certified Medical Planners™. Productivity Press, NY, 2016.

Marcinko, DE: Risk Management, Liability and Insurance Strategies for Doctors and Advisors: Best Practices from Leading Consultants and Certified Medical Planners™. Productivity Press, NY, 2017.

Nofsinger, JR: The Psychology of Investing. Rutledge Publishing, 2022

Winters, Scott: The 10X Financial Advisor: Your Blueprint for Massive and Sustainable Growth. Absolute Author Publishing House, 2020.

Despite their high salaries, not all doctors are wealthy, and some live paycheck to paycheck. Here are 5 reasons why many doctors today are broke, according to https://medschoolinsiders.com

1 | Believing They Are Universally Smart

The first reason so many doctors are broke is that many doctors believe they are universally smart. While most doctors have deep specialized knowledge, there’s a big difference between being smart in your profession and being smart with money. A physician’s schooling is quite thorough when it comes to the human body, but med school doesn’t include a prerequisite class on how to handle finances.

Graduating medical school is a major feat and certainly demonstrates superior work ethic and cognitive abilities. But many new doctors believe these accomplishments transcend all aspects of life. If you’re smart enough to earn an MD, you’re certainly smart enough to handle your finances, but only once you properly and intentionally educate yourself.

The truth is doctors, especially traditional graduates, haven’t had an opportunity to manage large sums of money until they become fully trained attending physicians and start pulling in low to mid six figures in income. Prior to that, there was very little of it to manage.

Far too many aspiring doctors, and students in general, don’t take the time to learn financial basics, in part because it’s uncomfortable and seems like something they can figure out “later”, whenever that may be. Their poor spending habits and lack of investment knowledge carry over into their careers, causing many to make irresponsible decisions.

The second factor is overspending too soon, and this comes up at two points in training.

First, it’s natural to want to start spending more as soon as you get into residency and start making a little more money. After all, you’ve been a broke student for 8 or more years, and now you’re finally making a reasonable and reliable wage. But that’s where young doctors get into trouble. Residency pays, but not nearly as much as you will be making once you become an attending physician. The average resident makes about $60K a year, and if you begin spending all of that money right away, thinking you’ll handle your loans once you become an attending, you delay paying off your medical school debt, which means the compounding effect through your student loan interest rate works against you.

Now that $250,000 in student loans has ballooned to over $350,000 by the time you finish residency. The compounding effect, which can be one of your greatest allies in your financial life, becomes an equally powerful enemy when working against you through debt. But of course, pinching pennies is easier said than done, especially when you’re in residency and are surrounded by peers in different professions. They’ve been earning good money much longer than you have, and they can afford more luxurious lifestyles.

They may not be worried about indulging in fine dining or how much a hotel costs when traveling. Students in college and medical school are often confident they will resist the temptations, but the desire to keep up with your friends and family can be difficult to ignore, which causes many to overspend before they technically have the money to do so.

The same is true of attending physicians. As soon as those six-figure salaries come rolling in, many physicians go overboard with spending, trying to make up for lost time and to treat yourself.

Now, we are not suggesting you shouldn’t reward yourself for completing residency, but that reward shouldn’t be a Lamborghini. It’s best to continue living like a resident in your first few years after becoming an attending to pay off loans, put a down payment on a home, and get your financial foundation built before loosening the purse strings.

3 | Decreasing Salaries

Third, doctors continue to make less money than they did before. And this includes nearly all 44 medical specialties. For example, while physician compensation technically rose from $343k to $391k between 2017 and 2022, this rise does not keep up with inflation. The real average compensation in 2022 was less than $325k—a $20k decrease in purchasing power in only six years.

For doctors who are already spending to the limits of their salaries with huge mortgages, car payments, business costs, and other luxuries, a decreased salary can have a huge impact. You might be able to cut back by going on fewer vacations or eating out less frequently, but many accrued costs are locked in, such as a mortgage payment, car loan, or leased rental space for your practice.

4 | Increasing Costs of Private Practice

In the past, running a private practice was much simpler, but recent stricter guidelines and regulations have made it difficult for solo practices to keep up. While regulations like the Health Insurance Privacy and Portability Act, or HIPAA, and mandatory Electronic Medical Records, or EMRs, are necessary to protect patients, they make costs higher for physicians who run their own private practice. These physicians need to spend their own money to set up and maintain EMRs as well as invest in security to ensure patient data is protected.

With the steep rise of inflation we’ve seen over the past couple of years, everything is more expensive, which means costs, such as business space, equipment, and even office supplies, have gone up for private practice physicians while salaries have not. 2013 to 2020 saw an annual inflation rate of anywhere from 0.7% to 2.3%. This skyrocketed to an annual inflation rate of 7.0% in 2021 and another 6.5% in 2022. In fact, the cost of running a private practice has increased by almost 40% between 2001 and 2021.

These increased costs are exacerbated by another problem plaguing private practices; decreased reimbursement. While costs increased by almost 40%, Medicare reimbursement only increased by 11%. When doctors see patients who are insured, the insurance companies pay the physicians for their time. For Medicare, the new proposed rules for 2023 would cut reimbursement by around 5%. When adjusting for inflation, Medicare reimbursement decreased by 20% in the last 20 years.

These costs add up, making it extremely difficult for physicians to thrive financially while running a private practice.

5 | Tuition Debt

Lastly, we can’t talk about a doctor’s finances without mentioning the exorbitant debt so many graduating physicians are left with. It won’t shock you to hear that med school is expensive. Extremely expensive. The average cost of tuition for a single year is nearly $60k, with significant variance from school to school, and that’s before accounting for living expenses.

In-state applicants pay less than out-of-state applicants, and students at private schools typically pay more than students at public medical schools. The astronomical costs mean the vast majority of students can’t pay for medical school out of their own pockets. And unless your family is part of the 1%, even with your parents footing the bill, it’s difficult to cover tuition, let alone rent, groceries, transportation, tech, social activities, exam fees, and application costs.

The average total student debt after college and med school is over $250k. But keep in mind that’s the average, which includes 27% of students who graduate with no debt at all. This means the vast majority of students leave medical school owing much more than $250k.

For some perspective, in 1978, the average debt for graduating MDs was $13,500, which, when adjusted for inflation, is a little over $60,000. There are multiple ways to eventually repay these loans, but time and discipline are essential to ensure this money is paid off as quickly as possible.

According to financial advisor Dr. David Edward Marcinko MEd MBA CMP™; consider the following:

Place a portion of your salary (15-20% or more) into a savings account, and another portion (10-20% or more) into wise investments [stocks, bonds, mutual funds, and/or ETFs].

Pay off your bills each month, and then use leftover spending money to purchase fun things like vacations and fancy dinners, within your means. Shop sales, buy used clothes, and use credit card points for travel.

Hire an excellent tax professional and meet with an investment advisor once or twice a year about your investment status and strategy. http://www.MarcinkoAssociates.com

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

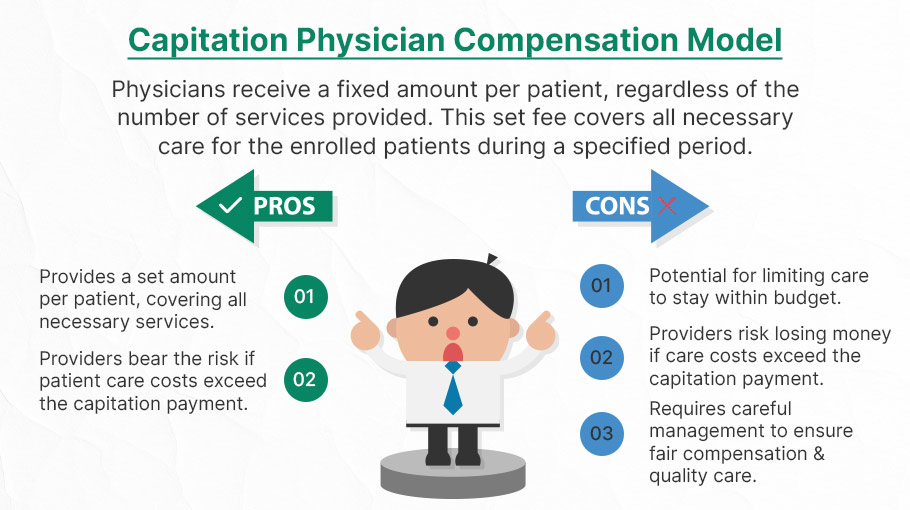

Capitation is a type of healthcare payment system in which a physician or hospital is paid a fixed amount of money per patient for a prescribed period by an insurer or physician association. The cost is based on the expected healthcare utilization costs for a group of patients for that year.

With capitation, the physician—otherwise known as the primary care physician— is paid a set amount for each enrolled patient whether a patient seeks care or not. The PCP is usually contracted with an HMO whose role it is to recruit patients.

According to Richard Eskow, CEO of Health Knowledge Systems of Los Angeles, capitated medical reimbursement has been used in one form or another, in every attempt at healthcare reform since the Norman Conquest. Some even say an earlier variant existed in ancient China [personal communication].

Initially, when Henry I assumed the throne of the newly combined kingdoms of England and Normandy, he initiated a sweeping set of healthcare reforms. Historical documents, though muddled, indicate that soon thereafter at least one “physician,” John of Essex, received a flat payment honorarium of one penny per day for his efforts. Historian Edward J. Kealey opined that sum was roughly equal to that paid to a foot-soldier or a blind person. Clearer historical evidence suggests that American doctors in the mid-19th century were receiving capitation-like payments. No less an authoritative figure than Mark Twain, in fact, is on record as saying that during his boyhood in Hannibal, MO his parents paid the local doctor $25/year for taking care of the entire family regardless of their state of health.

Later, Sidney Garfield MD [1905-1984] is noted as one of the great under-appreciated geniuses of 20th century American medicine stood in the shadow cast by his more celebrated partner, Henry J. Kaiser. Garfield was not the first physician to embrace the notion of prepayment capitation, nor was he the first to understand that physicians working together in multi-specialty groups could, through collaboration and continuity of care, outperform their solo practice colleagues in almost every measure of quality and efficiency. The Mayo brothers, of course, had prior claim to that distinction. What Garfield did, was marry prepayment to group practice, providing aligned financial incentives across every physician and specialty in his medical group, as well as a culture of group accountability for the care of every member of the affiliated health plan. He called it “the new economics of medicine,” and at its heart was a fundamentally new paradigm of care that emphasized – prevention before treatment – and health before sickness. Under his model: the fewer the sick – the greater the remuneration. And: the less serious the illness, the better off the patient and the doctors.

Such ideas were heresy to the reigning fee-for-service, solo practice, ideologues of the mainstream medical establishment of the 1940s and ‘50s, of course. Throughout the period, Garfield and his group physicians were routinely castigated by leaders of the AMA and county medical associations as socialistic and unethical. The local medical associations in Garfield’s expanding service areas – the San Francisco Bay Area, Los Angeles, and Portland, Oregon – blocked group practice physicians from association membership, effectively shutting them out of local hospitals, denying them patient referrals or specialty society accreditation. Twice in the 1940s, formal medical association charges were brought against Garfield personally, at one time temporarily succeeding in suspending his license to practice medicine.

Of course, capitation payments made a comeback in the first cost-cutting managed care era of the 1980-90s because fee-for-service medicine created perverse incentives for physicians by paying more for treating illnesses and injuries than it does for preventing them — or even for diagnosing them early and reducing the need for intensive treatment later. Nevertheless, the modern managed care industry’s experience with capitation wasn’t initially a good one. The 1980-90s saw a number of HMOs attempt to put independent physicians, especially primary care doctors, into a capitation reimbursement model. The result was often negative for patients, who found that their doctors were far less willing to see them — and saw them for briefer visits — when they were receiving no additional income for their effort. Attempts were also made to aggregate various types of health providers — including hospitals and physicians in multiple specialties — into “capitation groups” that were collectively responsible for delivering care to a defined patient group. These included healthcare facilities and medical providers of all types: physicians, osteopaths, podiatrists, dentists, optometrists, pharmacies, physical therapists, hospitals and skilled nursing homes, etc.

However, the healthcare industry isn’t collective by nature, and these efforts tended to be too complicated to succeed. One lesson that these experiments taught is that provider behavior is difficult to change unless the relationship between that behavior and its consequences is fairly direct and easy to understand.

Today, the concept of prepayment and medical capitation is to uncouple compensation from the actual number of patients seen, or treatments and interventions performed. This is akin to a fixed price restaurant menu, as opposed to an àla carte eatery.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on September 12, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I. and Staff Reporters

***

***

BIAS

Bias is a prejudice in favor of or against one thing, person, or group compared with another, usually in a way considered to be unfair.

MYOPIA

Myopia (nearsightedness) is a common condition that’s usually diagnosed before age 20. It affects your distance vision — you can see objects that are near, but you have trouble viewing objects that are farther away like grocery store aisle markers or road signs. Myopia treatments include glasses, contact lenses or surgery.

MYOPIA BIAS

Myopia Bias makes it hard for us to imagine what our lives might be like in the future.

FinancialExample: When we are young, healthy and in our prime economic earning years it may be hard for us to picture what life will be like when our health depletes and we no longer have the earnings necessary to support our standard of living.

Irony: This short-sightedness makes it hard to save adequately when we are young … when saving does the most good.

Posted on September 10, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITIONS

By Staff Reporters

***

***

Rate Review & the 80/20 Rule

The health care law provides 2 ways to hold insurance companies accountable and help keep your costs down: Rate Review and the 80/20 rule.

Rate Review

Rate Review helps protect you from unreasonable rate increases. Insurance companies must now publicly explain any rate increase of 15% or more before raising your premium. This does not apply to grandfathered plans.

The 80/20 Rule generally requires insurance companies to spend at least 80% of the money they take in from premiums on health care costs and quality improvement activities. The other 20% can go to administrative, overhead, and marketing costs.

The 80/20 rule is sometimes known as Medical Loss Ratio, or MLR. If an insurance company uses 80 cents out of every premium dollar to pay for your medical claims and activities that improve the quality of care, the company has a Medical Loss Ratio of 80%.

Insurance companies selling to large groups (usually more than 50 employees) must spend at least 85% of premiums on care and quality improvement.

If your insurance company doesn’t meet these requirements, you’ll get a rebate on part of the premium that you paid.

Will I get a rebate check from my insurance company?

If your insurance company doesn’t meet its 80/20 targets for the year, you’ll get back some of the premium that you paid.

You may see the rebate in a number of ways:

A rebate check in the mail

A lump-sum deposit into the same account that was used to pay the premium, if you paid by credit card or debit card

A direct reduction in your future premium

Your employer may also use one of the above rebate methods, or apply the rebate in a way that benefits employees

If you or your employer will get a rebate, your insurance company must notify you by August 1.

If you have an individual insurance policy, you’ll get the rebate directly from your insurance company.

For small group and large group plans, the rebate is usually paid to the employer. It may use one of the above rebate methods, or apply the rebate in a way that benefits employees.

FYI: The 80/20 rebate rules don’t apply when an insurance company has fewer than 1000 enrollees in a particular state or market.

For Rate Review: These requirements don’t apply to grandfathered plans. Check your plan’s materials or ask your employer or your benefits administrator to find out if your health plan is grandfathered.

For the 80/20 Rule: These rights apply to all individual, small group, and large group health plans, whether your plan is grandfathered or not.

According to Medical Economics, there were 10 clinic and physician practices filing bankruptcy in 2024, making it the highest level of the last six years, according to a new analysis of cases with liabilities of at least $10 million.

Meanwhile, the Steward Health Care System bankruptcy, which was based in Massachusetts but making headlines across the nation, has become “the largest hospital sector bankruptcy by far in the last 30 years,” according to a new analysis by Gibbins Advisors, based in Nashville, Tennessee.

Health care bankruptcy filings totaled 57 last year, down from 79 in 2023, said “Healthcare Restructuring: Trends and Outlook.” The report analyzed Chapter 11 health care bankruptcy cases with liabilities of at least $10 million, since 2019.

Last year’s total was down 28% from 2023’s peak, but greater than the 2019 to 2022 average of 42 filings a year, the report said.

Bankruptcy, often considered a last financial resort, is a legal process that can help alleviate outstanding debts for individuals and businesses. Reasons to file for bankruptcy can include divorce, job loss, exorbitant medical bills or credit card debt.

There are several types of bankruptcy — six, as a matter of fact. The two most common types of bankruptcy for individuals are Chapter 7 and Chapter 13.

But there are four other types as well: Chapter 9, Chapter 11, Chapter 12 and Chapter 15. And, the type of bankruptcy filed depends on the situation.

Regardless of which type, the process is typically the same: You’ll usually retain an attorney and make your case before a judge, who will then erase some debts or set up a repayment plan.

Also note that an eligibility requirement — for all bankruptcy chapters — is that you must undergo credit counseling within the 180 days before filing.

Posted on September 7, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

A recent study of hospital physician acquisition and employment found that such acquisitions decrease competition and raise prices. A National Bureau of Economic Research (NBER) working paper, released in July 2025, “empirically analyze[d] the effects of mergers between complementary firms on competition and pricing,” and found hospital prices increased by an average of 3.3%, while physician prices increased by an average of 15.1%.

This Health Capital Topics article reviews the study’s findings and implications for the healthcare industry. (Read more…)

Posted on September 4, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I. and Staff Reporters

***

***

Stocks: Markets slowed along yesterday with the S&P 500 and NASDAQ buoyed after a pivotal antitrust ruling for Alphabet pushed big tech stocks higher across the board.

Bonds: The 30-year Treasury pushed 5% yesterday as traders fret about the Fed’s independence and the odds of interest rate cuts.

Commodities: Oil sank on reports that OPEC+ is contemplating increasing its crude output next month, while gold reached yet another new record high as uncertainty swirling around the future of tariffs continued to rise. JPMorgan analysts now think the precious metal could climb as high as $4,250 by the end of next year.

Posted on August 27, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Bonds: Long-term Treasury yields rose and short-term yields fell after President Trump fired Fed Governor Lisa Cook opening the gap between 5-year and 30-year yields to its widest point in three years.

Stocks: Equities barely budged on the latest FOMC drama with investors’ attention fully focused on Nvidia earnings tomorrow afternoon.

Trade Craft: President Trump vowed retaliation against countries that apply a digital services tax against US tech companies. He may also slap a 200% tariff on China if that country restricts trade on rare earth magnets.

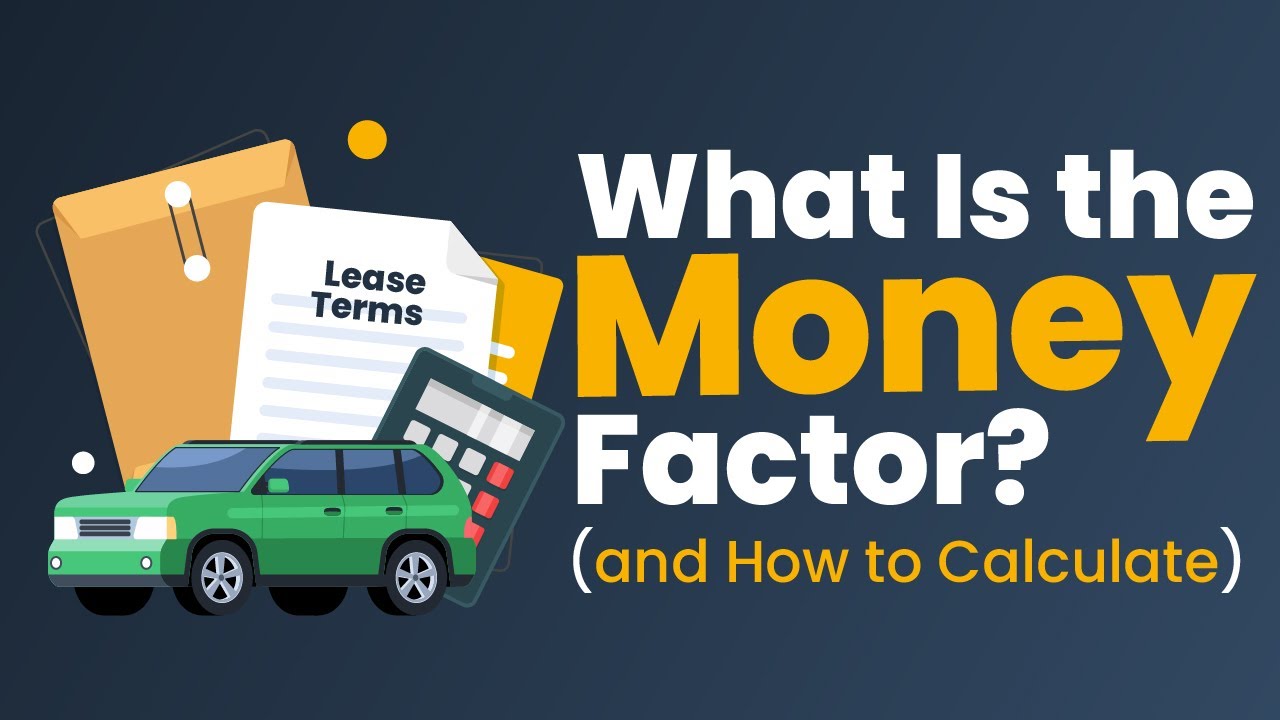

The so-called money factor (abbreviated as MF on invoices) is a number in a decimal form that dealers use to calculate the APR of a car lease. It’s a major part of your monthly payment and dealers are known to jack up the money factor to pad their profits.

Most doctors don’t ask to see it because they’re not aware of it or don’t know how to calculate it. Ask to see the money factor, then multiply it by 2,400.

For example, if the money factor is .00150, you multiply it by 2,400 to get 3.6%. If that’s higher than the prevailing rate, you have room to talk them down.

How to reduce it

So how do you get a good interest rate when you lease a vehicle? The same way you do when borrowing for any other reason, whether it’s buying a home or applying for a personal loan: by having good credit. This may reduce your interest rate because you’ll represent a lower risk to a lender.

A high residual value on the car could also help you get a better interest rate. A higher residual value means you’d have lower monthly payments because there would be less depreciation on the vehicle. Since interest is applied to your monthly payment, a lower monthly payment would equate to reduced interest charges.

The money factor is one of the many numbers you may want to learn about when leasing a car. It’s one of the transactional costs that come with leasing, and allows dealers and finance companies to make a profit on every lease they execute. As a consumer, it’s a smart idea to learn the financial implications of this number and how it’ll affect your overall costs over the course of a multi-year lease.

***

***

If the interest rate is too high, you may need to shop around for a better rate, negotiate with the dealer or lender to lower the money factor, or consider leasing another vehicle that’s more in line with your budget. Either way, make sure you explore all your financial options before taking a car off the lot.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on August 12, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Stocks: Markets struggled to pick a direction as investors took a wait-and-see approach ahead of today’s CPI reading—even as Wall Street worries about the data’s reliability.

Trade: President Trump asked China, the world’s largest soybean buyer, to quadruple its soybean purchases from the US. He also extended the trade war truce with China by 90 days

Commodities: Gold had its worst day in three months as traders waited for the White House to clarify its new tariffs on the key commodity—only for Trump to announce that it won’t be tariffed at all. Meanwhile, Chinese battery giant CATL halted operations at a mine that produces 4% of the world’s lithium, sending prices of the precious metal soaring.

Trade: President Trump signed an executive order late yesterday unleashing a wave of new tariffs on 69 US trading partners that will go into effect on August 7th. Here’s a handy list of tariffs and their economic effects for anyone else having trouble keeping track of all these new numbers.

Markets: Stocks opened lower and kept falling thanks to a double whammy of new tariff rates and a shocking slowdown in the labor market, while bond yields tumbled.

Commodities: Goldjumped as the likelihood of a rate cut rose due to the latest jobs report, while oil sank on reports that OPEC+ may announce a crude production boost as soon as this weekend.

Posted on July 31, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

***

On July 14, 2025, the Centers for Medicare & Medicaid Services (CMS) released its proposed Medicare Physician Fee Schedule (MPFS) for calendar year (CY) 2026.

In addition to the agency’s suggested increase to physician payments, the proposed rule also announces a new payment model and more tele-health flexibilities.

According to CMS, the “proposed rule is one of several proposed rules that reflect a broader Administration-wide strategy to create a health care system that results in better quality, efficiency, empowerment, and innovation for all Medicare beneficiaries.” (Read more…)

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Classic Definition: Research from Ernst-Young [Nikhil Lele and Yang Shim] uncovered a chasm between how consumer patients think they’re doing financially, and the actual state of their finances. Even more striking, their study suggested that improving consumers’ financial health will become one of the top imperatives in reframing consumer financial services.

Modern Circumstance: For example, the study asked consumers to rate their own financial health, and 83 percent rated themselves “good,” “very good” or “excellent.” Now, contrast this figure with what is known about their actual situation:

60 percent of Americans say they are financially stressed.

56 percent of Americans have less than $10,000 saved for retirement.

40 million American families have no retirement savings at all.

40 percent of Americans are not prepared to meet a $400 short-term emergency.

Paradox Example: Fortunately, even though the vast majority of consumers rate themselves as financially healthy, the study found that most still want to improve. Importantly for health economists, the attractive 25-34 and 35-49 year-old age groups were most likely to be extremely or very interested in improving their financial and economic health.

Paradox Example: Massively affluent consumer patients are even more interested in improving this paradox than their mass market counterparts.

Posted on July 26, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

On July 15, 2025, the Centers for Medicare & Medicaid Services (CMS) released the proposed rule for the Outpatient Prospective Payment System (OPPS) and Ambulatory Surgical Center (ASC) Payment System for calendar year (CY) 2026.

Among other items, the agency proposes increasing payments to all outpatient providers, eliminating the Inpatient Only (IPO) List, and changing quality reporting programs.

This Health Capital Topics article reviews the proposed updates and changes to outpatient reimbursement. (Read more…)

Posted on July 25, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Stocks: President Trump said there’s a “50/50 chance” of a deal with the EU ahead of next week’s deadline. Investors decided they like those odds, and pushed the NASDAQ and S&P 500 to yet another new closing record high—in fact, the S&P 500 set a new record every day this week. Meanwhile, trade deal talks with Brazil have reportedly stalled.

Commodities: Oil fell to a three-week low today as Iran signaled a willingness to come to the negotiating table with European powers for nuclear talks.

Hopes of trade deals and less need for a safe haven investment pushed gold prices lower.

Posted on July 21, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Rick Kahler MSFP CFP™

***

***

When Maria needed $400,000 for a down payment on a new home, her broker at a large Wall Street firm offered a solution: “Don’t sell investments and trigger capital gains. Just take out a margin loan.”

A margin loan is a line of credit from a brokerage firm, secured by the client’s investment portfolio. It offers quick access to cash with no immediate tax consequences and minimal paperwork. But the convenience comes at a cost. As of mid-2025, margin loan interest rates range from 6.25% to over 11%.

Margin loan recommendations are often presented by brokers as tax-savvy strategies that allow clients to access “tax-free” cash while keeping their portfolios intact. In many cases, however, the math benefits the advisor more than the investor. The cost of borrowing often exceeds what an investor is likely to earn by holding on.

For example, let’s assume an interest rate of 7.5% on Maria’s $400,000 margin loan. While borrowing delayed the payment of $20,000 in capital gains tax, she will eventually have to pay that tax anyway unless she holds the investments until her death. Two years later, with portfolio returns of 4% annually, she had earned around $32,000 from the $400,000 in investments she might have sold. Meanwhile, she had paid $60,000 in interest—leaving her some $28,000 worse off. That’s without factoring in ongoing interest payments, or the risks of a margin call if the investments securing the loan drop in value.

Why do advisors keep recommending margin loans? Because selling investments reduces the portfolio size and the advisor’s fee. Borrowing keeps the portfolio intact and the compensation unchanged—while the firm receives additional income from interest on the loan. In some cases, advisors suggest using margin loans to buy more investments, increasing both the portfolio and the fee they collect.

None of this is illegal. But when the borrowing cost is higher than expected returns and the advisor benefits financially, the ethics are questionable. The client takes the risk, while the advisor keeps the revenue.

This kind of conflict appears more often in portfolios where compensation is tied to asset volume and the company’s primary culture rewards gathering assets over delivering unbiased advice. By contrast, fee-only financial planning and investment advisors typically operate on simpler hourly, flat, or tiered fee structures. Their compensation doesn’t depend on whether a client borrows, sells, or holds. The culture of the firm focuses on conflict-free advice aligned with the client’s best interest.

Wall Street brokers are often held to a fiduciary standard, but structure still matters. In 2024 the SEC reported their examinations of brokers would continue to focus on advisor recommendations unduly influenced by the company’s compensation and incentives.

There are rare situations where a margin loan may be appropriate. A client with large unrealized gains might use a short-term margin loan to minimize taxes. An elderly investor might borrow tax-free rather than sell assets that will receive a step-up in basis at their death. Even in those cases, the math must be exact and the client must clearly understand the risks, including the possibility of a margin call.

If your advisor recommends a margin loan, especially to buy more investments, ask strong questions. What’s the interest rate? What return is realistic? What are the tax consequences of selling? How does this affect the advisor’s income?

In a high-rate, low-return environment, margin loans rarely favor the client. The exceptions are narrow. The risks are significant. And the conflict of interest is measurable.

Sometimes the smartest move is the simplest: sell what you need, pay the tax, and leave leverage out of your plan.

Posted on July 18, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Lucid exploded 36.24% higher on the news that the EV maker is partnering with Uber to roll out the ridesharing company’s new robotaxis.

PepsiCo popped 7.45% thanks to a strong quarter for the snack and soda giant, while shareholders cheered the details of its turnaround plan.

UnitedAirlines may have missed Wall Street’s revenue forecast, but its profits were enough to impress investors. Shares rose 3.11%.

Reports that Union Pacific is thinking about acquiring a rival sent shares of fellow train operators CSX and NorfolkSouthern up 3.73% and 3.65%, respectively.

Sarepta Therapeutics soared 19.53% after the biotech announced it will lay off 500 employees and restructure its entire business.

Quantumscape continued its hot streak, rising yet another 19.82% thanks to its recent battery breakthrough.

Speaking of hot streaks, OpenDoorTechnologies rose another 10.74% as retail traders pour into what is quickly becoming the next big meme stock.

Stocks down

GE Aerospace crushed earnings expectations and raised its fiscal guidance, but it still wasn’t enough to impress investors, who pushed shares of the engine maker down 2.10%.

USBancorp sank 1.03% after revenue and net interest income missed forecasts last quarter.

AbbottLaboratories beat on both top and bottom line guidance, but still fell 8.53% after the pharma company narrowed its fiscal forecasts.

President Trump is expected to sign an executive order in the coming days designed to help make private-market investments more available to U.S. retirement plans, according to people familiar with the matter. The order would instruct the Labor Department and the Securities and Exchange Commission to provide guidance to employers and plan administrators on including investments like private assets in 401(k) plans.

The Fed Drama: A White House official said President Trump will likely fire Jerome Powell soon. Stockssank at the thought of the Fed head being shown the door, offsetting the pleasant surprise of a flat wholesale inflation reading.

Markets: Stocks managed to recoup their losses after Trump said it’s “highly unlikely” that he will fire Powell, but bonds remained shaken.

Crypto: Bitcoin bounced higher after the crypto bills currently under consideration in the House of Representatives cleared a key hurdle.

Overconfident Investing Bias happens when we believe we can out-smart other investors via market timing or through quick, frequent trading. This causes the results of a study to be unreliable and hard to reproduce in other research settings.

Example: Data convincingly shows that people and financial planners/advisors and wealth managers who trade most often under-perform the market by a significant margin over time. Active traders lose money.

Example: Overconfidence Investing Bias moreover leads to: (1) excessive trading (which in turn results in lower returns due to costs incurred), (2) underestimation of risk (portfolios of decreasing risk were found for single men, married men, married women, and single women), (3) illusion of knowledge (you can get a lot more data nowadays on the internet) and (4) illusion of control (on-line trading).

Posted on July 2, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Power station: Crude oil prices reversed as tensions in the Middle East cooled, but AI likely raises electricity demand over the longer term, creating investment opportunities and risks.

Oil supplies now exceed demand, noted Michelle Gibley, director of international research at the Schwab Center for Financial Research, in her latest analysis, though “AI is transforming the energy sector,” raising power shortage concerns.

Solar stocks got a reprieve today after the Senate dropped the excise tax on clean energy projects. Sunrun soared 10.51%, EnphaseEnergy rose 3.18%, SolarEdgeTechnologies popped 7.16%, and ArrayTechnologies climbed 12.54%.

Apple tumbled this summer after investors were disappointed by its AI rollout, but rose 1.29% on the news that the company may pivot to using Anthropic or OpenAI in iPhones instead of building something in-house.

Wolfspeed, the best name for a company that makes computer chips, exploded 98.09% after the company officially filed for Chapter 11 bankruptcy.

Hasbro got a nice 4.29% bump thanks to Goldman Sachs analysts, who are big old nerds who think Magic: The Gathering will boost the toymaker’s sales.

Ford popped 4.61% after the automaker reported an impressive 14% increase in sales last quarter.

Casino stocks soared on the news that gaming revenue in Macau rose 19% in June. WynnResorts climbed 8.85%, Las Vegas Sands added 8.95%, and MGMResorts gained 7.24%.

What’s down

AMC Entertainment tumbled 9.03% after the one-time meme stock announced its new debt restructuring plan.

ProgressSoftware sank 13.03% after the business application software company reported mixed results last quarter, beating on profit but missing on revenue.

JobyAviation fell 7.01% after traders took profits following the air taxi company’s big pop yesterday.

AeroVironment dropped 11.42% after defense contractor announced it’s offering $750 million in common stock and $600 million in convertible senior notes to pay off its debt.

Diabetes device makers tumbled on the news that the government may change the reimbursement rate for glucose monitors and insulin pumps. Insulet lost 4.52%, Dexcom fell 4.25%, and BetaBionics sank 4.26%.

Posted on June 29, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Markets: That feeling when you have a $10 trillion rally. To wit:

The S&P 500 closed at a record high this week despite a brief dip as trade tensions with Canada ratcheted up. That puts the index about 20% up from its April low, when the broad tariff announcement sent it spiraling, and up ~5% for the year.

NVIDIA also hit an all-time high, and it keeps edging closer to becoming the first company to hit a $4 trillion valuation.

Posted on June 24, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Markets: Stocks climbed yesterday as oil prices fell, with investors reacting positively to what appeared to be limited retaliation from Iran in response to the US bombing its nuclear facilities over the weekend.

Meanwhile, Tesla had its biggest jump in two months following the successful, albeit limited, rollout of its robotaxi service in Austin.

Posted on June 23, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

As economist Jason Furman pointed out, 250 years ago the Continental Congress created a brand-new currency and authorized the printing of $2 million worth to help George Washington pay his soldiers and procure weapons and supplies for the war effort.

Markets: Until now, Wall Street has mostly shrugged off the Israel–Iran conflict in the Middle East, with the S&P 500 and NASDAQ closing just a hair lower for the week on Friday. But, investors’ thinking might—or might not—change this coming week, after the US entered the war on Saturday with strikes on key Iranian nuclear infrastructure.

And, eyes are on oil prices, which, due to the war, are having their most volatile stretch since Russia invaded Ukraine in 2022.

A psychological paradox is a figure of speech that can seem silly or contradictory in form, yet it can still be true, or at least make sense in the context given.

This is sometimes used to illustrate thoughts or statements that differ from traditional ideas. So, instead of taking a given statement literally, an individual must comprehend it from a different perspective. Using paradoxes in speeches and writings can also add wit and humor to one’s work, which serves as the perfect device to grab a reader or a listener’s attention and/or persuade them to action, sales and closing statements. But paradoxes for the financial sector can be quite difficult to explain by definition alone, which is why it is best to refer to a few examples to further your understanding.

One good psychological paradox example is The Paradox of Thrift which suggests that while saving money is generally considered a prudent financial behavior, excessive saving during times of economic downturn can actually hinder economic recovery. When consumers collectively reduce their spending and increase their savings, it creates a decrease in aggregate demand. This reduction in demand can lead to lower production levels, job losses, and ultimately a decline in economic output. In other words, what may be individually rational behavior (financial saving) can have negative consequences for the overall economy.

The following paradoxical contradictions will help financial advisors guide clients to close more sales to the benefit of both.

____

In the intricate world of finance sales, advisors are often at the crossroads of various paradoxes that challenge client decision-making. While the journey towards financial security involves calculated strategies, it’s the nuanced understanding of paradoxes that can help the advisor close more sales.

____

But, what seems trueabout money often turns out to be false, according to colleague Finance Professor John Goodell, PhD from the University Akron:

The more we try to trade our way to profits, the less likely we are to profit.

The more boring an investment—think index funds—the more exciting the long-run performance will probably be.

The more exciting an investment—name your latest Wall Street concoction, Special Purpose Acquisition Company [SPAC] or anything crypto—the less exciting the long-term results typically are.

The only certainty is uncertainty and the only constant is change. Today’s market decline will eventually become a bull market, and today’s market leaders will eventually yield to other stocks.

Big market trends play a huge role in investment results, and yet trying to time macroeconomic cycles or guess which market sectors will outperform is a fool’s errand. Many big market rotations are set in motion by something wholly unanticipated, like a virus pandemic or a war.

To be happy when wealthy, we also need to be happy with far less money. The fact is, above a relatively modest income level, no amount of extra money will change our level of happiness. More money might even make us miserable, as many lottery winners have discovered.

The more we hate an investing trait—or any trait for that matter—the more likely it is that we’re resisting seeing that trait in ourselves. It’s what Carl Jung MD called the Shadowof Undesirable Personality Aspects that we hide from ourselves. Do prospects get irritated listening to your unsolicited financial advice? There’s a good chance that you often give unsolicited financial advice but don’t like to admit it.

The more we learn about investing, the more we realize we don’t know anything. We should just buy index funds and instead spend our time worrying about stuff we can actually control.

The more an investor is convinced he’s right, the more likely he is to be wrong. Short sellers, in particular, are likely to succumb to this paradoxical trap.

The more options we have, the less satisfied we’ll be with each one. This is the Paradox of Choice; revised. Anyone who has spent hours “optimizing” his or her portfolio knows this all too well. Its close cousin is information overload, another frustration paradox when investing.

The more afraid we are of losing money, the more likely we are to take unwitting risks that lose us money. Sitting in cash seems wise during market selloffs. But the truth is, none of us can reliably time the market. Pull up any chart of the stock market over any period longer than a decade and you’ll see that the riskiest decision is sitting in cash, which gets destroyed by inflation.

The more we think about our investments and look at our financial accounts, the more likely we are to damage our results by buying high because of greed and selling low because of fear. It can pay to look away.

ASSESSMENT

How should you respond to these financial paradoxes? As you plan for your own financial future, as well as your own client prospecting endeavors, embrace the concept of “loosely held views.”

In other words, make financial and client acquisitions plans, but continuously update your views, question your assumptions and paradoxes and rethink your priorities. Years of experience with clients certainly support the futility of trying to help them change their financial behavior by telling them what they “should” know or do.

CONCLUSION

Remember, it is far more useful to listen to client beliefs, fears and goals, and to suggest options and offer encouragement to help them discover their own path toward financial well-being. Then, incentivize them with knowledge of the above psychological paradoxes to your mutual success!

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

Marcinko, DE and Hetico, HR: Comprehensive Financial Planning Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™]. CRC Productivity Press, New York, 2016.

Marcinko, DE: Dictionary of Health Economics and Finance. Springer Publishing Company, New York. 2006

Marcinko, DE and Hetico, HR: Risk Management, Liability Insurance, and Asset Protection Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™]. CRC Productivity Press, New York, 2015.

Posted on June 20, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By AI

***

***

Stocks: Investors looked past the escalating conflict between Iran and Israel, even as President Trump mulled his options for a US intervention, and stocks rose ahead of today’s Federal Reserve meeting.

Economy: Trump called Jerome Powell “a stupid person” hours before the Fed Chair decided to keep interest rates where they were Stocks fell thanks to the Fed’s prediction that inflation will rise to 3.1% by the end of the year, above previous forecasts of 2.8%.

Commodities: Gold fell just a hair as analysts called the commodity’s top, while platinum climbed to a four-year high.

The average directional movement index (ADX) was developed in 1978 by J. Welles Wilder as a technical indicator of trend strength in a series of prices of a financial instrument. ADX has become a widely used indicator for technical analysts, and is provided as a standard in collections of indicators offered by various trading platforms.

The ADX is a combination of two other indicators developed by Wilder, the positive directional indicator (abbreviated +DI) and negative directional indicator (-DI). The ADX combines them and smooths the result with a smoothed moving average.

The average directional index (ADX) is a technical indicator used by traders to determine the strength of a financial security’s price trend. It helps them reduce risk and increase profit potential by trading in the direction of a strong trend. Many traders consider the ADX to be the ultimate trend gauge because it is so reliable.

ADX quantifies trend strength by measuring the degree of directional movement in price. ADX calculations are based on a moving average of price range expansion or contraction over a given period. The default setting is 14 periods, although other settings can be used.

ADX can be used with any financial security, including stocks, exchange-traded funds, and futures.

Posted on June 9, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By AI

***

***

Wall Street is stable right now as the technology trade has come roaring back.

The S&P 500 climbed above 6,000 points for the first time since February, while all three indexes posted their fifth winning week in the last seven. The S&P is now just over 2% from its all-time high.

Meanwhile, recent IPOs are party rocking, especially the stablecoin issuer Circle that went public last Thursday.

Posted on June 7, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By AI

BREAKING NEWS

***

***

Job growth is slowing, but still bigger than expected

US employers added 139,000 jobs last month, government data released yesterday shows—that’s less than the down-wardly revised 147,000 new jobs that were added in April, but more than economists had predicted. Meanwhile, the unemployment rate held steady.

Overall, the highly anticipated jobs report reflects employers growing more cautious in the face of the economic uncertainty brought on by the trade war, but so far, there doesn’t seem to be a steep drop off in the labor market. That could give the Fed reason to stay in wait-and-see mode on interest rates, though President Trump still used the occasion to urge Jerome Powell to cut rates “a full point” on Truth Social.