BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

A Dividend Aristocrat is a stock that has exhibited a remarkable level of consistency, measured by the fact that only those S&P 500 companies that have increased their annual dividend for 25 straight years — or more — can be called one. The name was coined by cable TV personality and investor Jim Cramer

These companies have raised their dividends through good times and bad, including recessions, crashes, and pandemics. Being able to continue doing so is a tribute to their stability and strength. Now, the past 18 months have been a particularly difficult economic environment to operate in, and some companies were forced to slash or hold the line on their dividends as a result.

But others are just fine, like investment manager T. Rowe Price (NASDAQ: TROW), which increased its dividend for the 35th straight year in 2022. It is located in Baltimore Maryland not far from where I grew up. In fact, I used to play stick ball, as a kid, in the parking lot.

Posted on October 5, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

Appreciating the Rules

[By Carol Miller; RN, MBA]

Local counties and municipalities are the primary providers of state mental healthcare for patients who lack private insurance coverage for such care.

Both children and adults may be eligible to receive assistance.

These counties provide a wide range of psychiatric and counseling services to the residents in their community as well as other types of assistance such as:

treatment services related to substance abuse;

housing;

employment services;

information and education service;

referrals;

consultative services to schools, courts and other agencies;

after-care services; and other related activities.

Rules and Regulations

Accordingly, regulations from federal, state, and county governments have an impact on the day-to-day operations, procedures and processes of a county mental health center. Traditionally, there are three main types of regulations.

Federal Regulations — The United States healthcare system is guided by programs such as those established under the Centers for Medicare and Medicaid (in the case of county mental health programs, Medicaid is especially important), Americans with Disabilities Act (ADA), Occupational Safety and Health Administration (OSHA), Health Insurance Portability and Accountability Act (HIPAA), and others.

State Regulations — These include general legislative guidelines, state management of benefits and reimbursement of the Medicaid program, and state allocations of budgets, which impact the centers’ operations.

County Regulations — Each county defines its own County Mental Health Program and decides which services will be provided or excluded.

Assessment

County facilities generally include outpatient clinics, county mental health programs, short-term psychiatric facilities, day-care centers, de-toxification centers, residential rehabilitation centers for substance abuse, long-term care psychiatric facilities, and Veterans Affairs (VA) psychiatric centers. The county centers may be co-located with other county services such as social services, occupational rehabilitation services, information technology services, human resources, maintenance services, and others or may be independently located.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

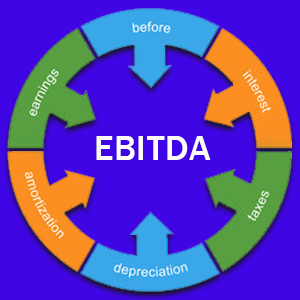

What Is Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA)?

***

EBITDA, or earnings before interest, taxes, depreciation, and amortization, is a measure of a company’s overall financial performance and is used as an alternative to net income in some circumstances. EBITDA, however, can be misleading because it strips out the cost of capital investments like property, plant, and equipment.

This metric also excludes expenses associated with debt by adding back interest expense and taxes to earnings. Nonetheless, it is a more precise measure of corporate performance since it is able to show earnings before the influence of accounting and financial deductions.

Simply put, EBITDA is a measure of profitability. While there is no legal requirement for companies to disclose their EBITDA, according to the U.S. generally accepted accounting principles (GAAP), it can be worked out and reported using the information found in a company’s financial statements.

The earnings, tax, and interest figures are found on the income statement, while the depreciation and amortization figures are normally found in the notes to operating profit or on the cash flow statement. The usual shortcut to calculate EBITDA is to start with operating profit, also called earnings before interest and tax (EBIT) then add back depreciation and amortization.

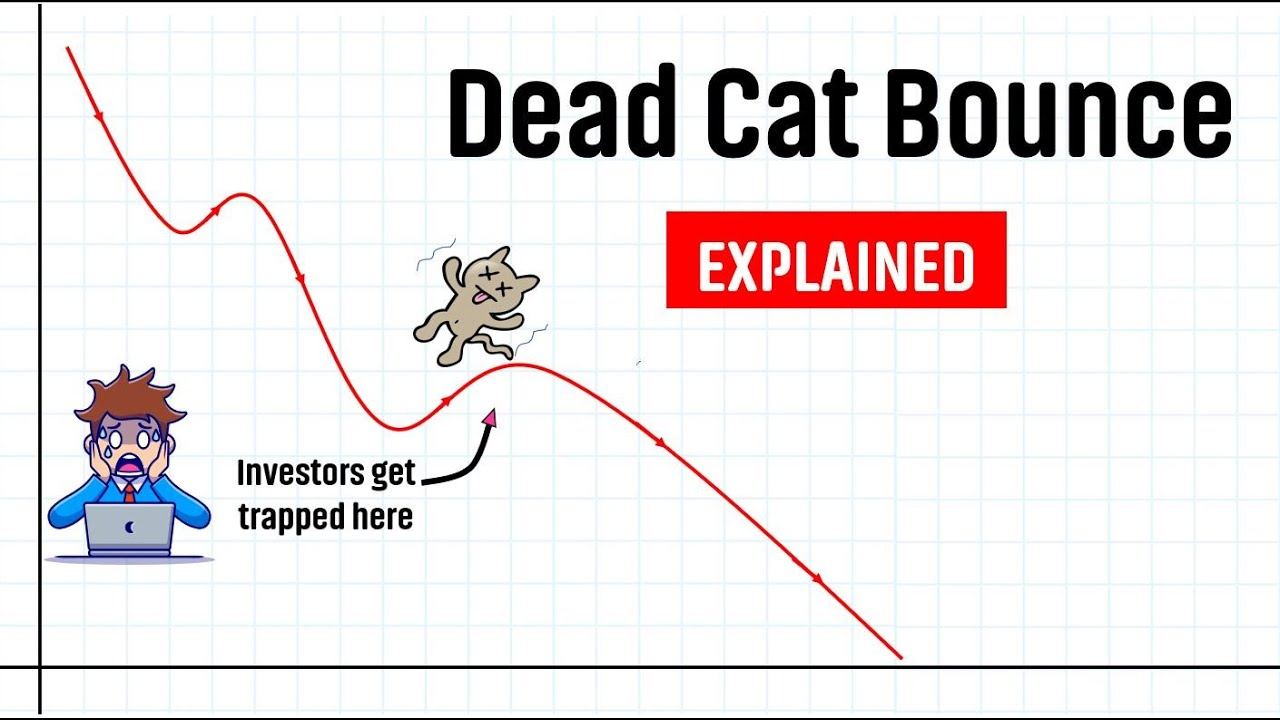

In finance, a dead cat bounce is a small, brief recovery in the price of a declining stock.

****

***

Derived from the idea that “even a dead cat will bounce if it falls from a great height”, the phrase, which originated on Wall Street, is also popularly applied to any case where a subject experiences a brief resurgence during or following a severe decline.

The dead cat bounce is a sudden and temporary increase in stock price caused by investors erroneously believing that the stock price’s reached its lowest.

The dead cat bounce can only be fully accurately determined with concrete data in hindsight.

Both falsely identifying a stock price trough (i.e., falling victim to a dead cat bounce) and falsely identifying a true price trough as a dead cat bounce will result in negative financial consequences.

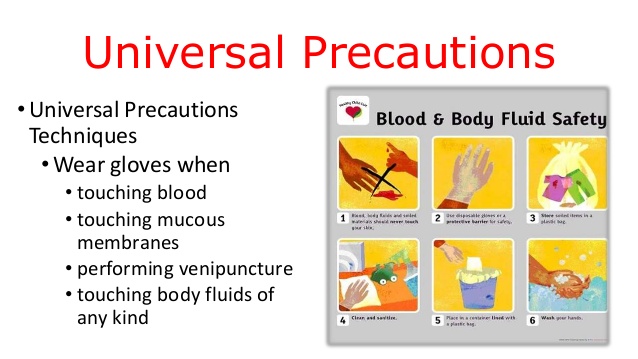

Universal Precautions refer to the medical practice of avoiding contact with patients’ bodily fluids, by means of the wearing of nonporous articles such as medical gloves, goggles, and face shields.

The infection control techniques were essentially good hygiene habits, such as hand washing and the use of gloves and other barriers, the correct handling of hypodermic needles, scalpels, and aseptic techniques.

Following the AIDS outbreak in the 1980s the US CDC formally introduced them in 1985–88. Every patient was treated as if infected and therefore precautions were taken to minimize risk.

There are more than 950,000 physicians in the United States. Yet, the brutal supply and demand, and demographic calculus of the matter is that there are just too many aging patients chasing too few doctors. Compensation and reimbursement is plummeting as Uncle Sam becomes the payer-of-choice for more than 52% of us. More so, going forward with the PP-ACA OR, perhaps not so much after the Trump election.

Furthermore, many large health care corporations, hospitals, and clinical and medical practices have not been market responsive to this change. Some physicians with top-down business models did not recognize the changing health care ecosystem or participatory medicine climate. Change is not inherent in the DNA of traditionalists. These entities and practitioners represented a rigid or “used-to-be” mentality, not a flexible or “want-to-be” mindset.

Yet today’s physicians and emerging Health 2.0 initiatives must possess a market nimbleness that cannot be recreated in a command-controlled or collectivist environment. Going forward, it is not difficult to imagine the following rules for the new virtual medical culture, and young physicians of the modern era.

A. Rule 1

Forget about large office suites, surgery centers, fancy equipment, larger hospitals, and the bricks and mortar that comprised traditional medical practices. One doctor with a great idea, good bedside manners, or competitive advantage can outfox a slew of insurance companies, Certified Public Accountants, or the Associate Management Accountant, while still serving patients and making money. It is now a unit-of-one economy where “ME Inc.,” is the standard. Physicians must maneuver for advantages that boost their standing and credibility among patients, peers, and payers.

Examples include patient satisfaction surveys, outcomes research analysis, evidence-based-medicine, direct reimbursement compensation, physician economic credentialing, and true patient-centric medicine. Physicians should realize the power of networking, vertical integration, and the establishment of virtual offices that come together to treat a patient and then disband when a successful outcome is achieved. Job security is earned with more successful outcomes; not a magnificent office suite or onsite presence.

B. Rule 2

Challenge conventional wisdom, think outside the traditional box, recapture your dreams and ambitions, disregard conventional gurus, and work harder than you have ever worked before. Remember the old saying, “if everyone is thinking alike, then nobody is thinking.” Do traditionalists or collective health care reform advocates react rationally or irrationally?

For example, some health care competition and career thought-leaders, such as Shirley Svorny, PhD, a professor of economics and chair of the Department of Economics at California State University, Northridge, wonder if a medical degree is a barrier—rather than enabler—of affordable health care. An expert on the regulation of health care professionals, including medical professional licensing, she has participated in health policy summits organized by Cato and the Texas Public Policy Foundation. She argues that licensure not only fails to protect consumers from incompetent physicians, but, by raising barriers to entry, makes health care more expensive and less accessible.

Institutional oversight and a sophisticated network of private accrediting and certification organizations, all motivated by the need to protect reputations and avoid legal liability, offer whatever consumer protections exist today.

C. Rule 3

Differentiate yourself among your health care peers. Do or learn something new and unknown by your competitors. Market your accomplishments and let the world know. Be a non-conformist. Conformity is an operational standard and a straitjacket on creativity. Doctors must create and innovate, not blindly follow entrenched medical societies into oblivion.

For example, the establishment of virtual medical schools and hospitals, where students, nurses, and doctors learn and practice their art on cyber entities that look and feel like real patients, can be generated electronically through the wonders of virtual reality units.

D. Rule 4

Realize that the present situation is not necessarily the future. Attempt to see the future and discern your place in it. Master the art of quick change with fast, but informed decision making. Do what you love, disregard what you do not, and let the fates have their way with you.

Assessment

I receive a couple of phone calls each month from young doctors on this topic. I ask them to decide if they are of the philosophical ilk to adhere to the above rules; or become another conformist and go along … to get along? In other words, get fly!

Or, become an employed, or government doctor. Just remember … the entity that gives you a job, can also take it away.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Sooner or later – as a practicing physician – you will want to ascertain and then demonstrate the cost effectiveness of your medical care. By using the process of Activity Based Cost (ABC) Management, you will be able to do so.

ALAS: But, if you’re using a traditional accounting system – like most all hospitals today that use the fictional “average wholesale cost” method – you won’t know a thing about your medical practice or clinic activity costs. Hence, again like most all hospitals, fees become simply vacuous.

QUESTION: We are in near bear market correction territory – especially for tech stocks – so what are the 2 major types of valuation approaches for common stock?

ANSWER: There are basically two different approaches for common stock valuation; top-down and bottom-up. Under either of the two fundamental approaches, a physician investor will have to work with individual company data. In reality, each of these approaches is used by investors and security analysts when doing fundamental analysis.

With the bottom-up approach, investors focus directly on a company’s prospects. Analysis of such information as the company’s products, its competitive position, and its financial status leads to an estimate of the company’s earnings potential, and, ultimately, its value in the market. Considerable time and effort are required to produce the type of detailed financial analysis needed to understand a firm’s standing. The emphasis in this approach is on finding companies with good long-term growth prospects, and making accurate earnings estimates.

The top-down approach is the opposite of the bottom-up approach. Investors begin with the economy and the overall market, considering such important factors as interest rates and inflation. They next consider likely industry prospects, or sectors of the economy that are likely to do particularly well (or particularly poorly). Finally, having decided that factors are favorable for investing, and having determined which parts of the overall economy are likely to perform well, individual companies are analyzed.

The concept of a self-taught and student motivated, but automated outcomes driven classroom may seem like a nightmare scenario for those who are not comfortable with computers. Now everyone can breathe a sigh of relief, because the Institute of Medical Business Advisors just launched an “automated” final examination review protocol that requires no programming skill whatsoever.

In fact, everything is designed to be very simple and easy to use. Once a student’s examination “blue-book” is received, computerized “robotic reviewers” correct student assignments and quarterly test answers. This automated examination model lets the robots correct tests and exams, while the students concentrate on guided self-learning.

According to Eugene Schmuckler PhD MBA MEd, Academic Provost of the CERTIFIED MEDICAL PLANNER® professional designation and certification program,

“This option allows the modern adult-learner save both time and money as s/he progresses toward the ultimate goal of board certification as a CMP® mark holder.”

The trend is growing and iMBA, Inc., is leading the way.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, urls and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

The most basic form of scambaiting sets out to waste a scammer’s time. At a minimum, scambaiters attempt to make scammers answer countless questions or perform pointless and random tasks. By keeping a scammer busy, scambaiters claim they’re preventing the scammer from defrauding a real victim.

Scambaiting may also be conducted with a specific purpose in mind. Sometimes scambaiters attempt to obtain an offender’s bank account information, for instance, which they then report to a financial institution. But there are other, less benevolent motives in the scambaiting community.

Thousands of scambaiters are organised on the 419eater forum, which describes itself as the “largest scambaiting community on earth”, with over 1.7 million forum threads. The forum was first established in 2003 to tackle the growing issue of 419 emails – a scam that promises people huge sums of cash in return for a small upfront fee.

419eater provides a particularly interesting case study because members are incentivised and rewarded for their scambaits through a unique system of icons, regarded as trophies, that they can obtain in their profile’s signature lines.

As a teacher educating is your job. It’s what you enjoy. There’s a fairly lax time schedule and resources are already built in the equation. Little accountability because the ultimate burden and measure of success is placed on the student to pass a test. If they don’t do well, it’s the student not directly the teacher who pays the price.

Now, I work with first year students who don’t know what a red blood cell looks like (biconcave disc, you thought I forgot, didn’t you) all the way to a chief resident who can probably do some surgeries better than me. It’s my job to take that first year student and turn them into a chief resident.

As an entrepreneur with limited resources, time, and energy, you don’t have the luxury to continuously teach, develop, and convince. You need people who simply get it especially in strategic positions. You don’t have the luxury of time or resources. You also are directly accountable if they don’t understand because you have a burn rate that probably just got worse. So how much “oxygen” do you allocate when trying to build your team?

Different story for Apple, Boeing and others that can create academies and educational tracks to teach and develop internally.

If you are economically literate – or read the ME-P regularly – you may be tired of hearing the familiar saw, “the single most important determinant of investment results over time is asset allocation.”

But, as most of us realize, this glosses over critical obstacles to building personal wealth—taxes, inflation, and spending policy. A doctor’s spending policy itself is as critical as asset allocation in preserving wealth, as well as for all investors who understand the trade-offs: there are both allocation and spending strategies that stand to preserve wealth and insulate against excessive equity risk at the same time.

Income versus Security

In proving his point a decade ago, the author—Roger Hertog in “Income Versus Security”— traced the growth of a $1 million portfolio during the period of 1960–1994. He showed that while an all-stock portfolio would have experienced a compound growth rate of 10.1%, an all-bond portfolio of 7.4%, and an all T-bill portfolio of 6.1%, these growth rates dropped to 8%, 5%, and 3.7%, respectively, after taxes and conservative transaction costs. When further reduced by inflation, they dropped to 3.1%, 0.2%, and -1%, respectively. Stocks still nearly tripled in real value after taxes.

Next, Hertog factored in spending. He showed that the greater the equity exposure, the more likely investors will preserve or increase their levels of real spending and wealth. Also, he demonstrated how a spending policy of a fixed percentage of the portfolio; or of spending all the income is ill-suited to estate building. He arrived at an optimum allocation of 60% stocks and 40% bonds with a policy of spending all stock dividends but only spending interest to the extent it exceeds inflation. This latter spending policy adjusts for the fact that in – unlike today but perhaps again in the near future – an inflationary environment a portion of bond interest is a return of principal. This type of asset allocation and spending policy resulted in the greatest amount of growth over the years and gained on inflation. Hertog contends that the 60/40 allocation provides an appealing combination of growth and protection.

IOW: It gives investors a milder ride.

Assessment

Over the 35-year period studied, a 60/40 mix returned almost as much as the all-stock portfolio both before taxes and after taxes and achieved some 75% of its real after-tax growth. Also, the portfolio’s worst year was only half as bad as the all-stock portfolio. Hertog believed that balancing with bonds softened the downside. But – what about the “flash-crash” of 2008-09?

Note: “Income Versus Security: Do You Have To Choose?” Roger Hertog, Trust & Estates, March 1997, pp. 44–62, Intertec Publishing Corporation.

Conclusion

And so, your thoughts and comments on this ME-P are appreciated. Is the bull market in bonds over? Do you believe Hertog? Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com and http://www.springerpub.com/Search/marcinko

Our Other Print Books and Related Information Sources:

Subscribe Now:Did you like this Medical Executive-Post, or find it helpful, interesting and informative? Want to get the latest ME-Ps delivered to your email box each morning? Just subscribe using the link below. You can unsubscribe at any time. Security is assured.

Posted on May 29, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

How It Works and What Physicians’ Must Watch Out For

Dr. David Edward Marcinko MBA CMP

“Buying on margin” is borrowing money from your stock-broker to buy a stock and using your investment as collateral. Physician-investors generally use margin to increase their purchasing power so that they can own more stock without fully paying for it. But, margin exposes all investors to the potential for higher losses.

This ME-P discusses the basics of buying on margin, some of the pitfalls inherent in margin buying, whether this financial tool is for you and how you can best use it.

Let’s say you buy a stock for $50 and the price of the stock rises to $75. If you bought the stock in a cash account and paid for it in full, you’ll earn a 50 percent return on your investment. But, if you bought the stock on margin – paying $25 in cash and borrowing $25 from your broker – you’ll earn a 100 percent return on the money you invested. Of course, you’ll still owe your brokerage $25 plus interest.

The downside to using margin is that if the stock price decreases, substantial losses can mount quickly. For example, let’s say the stock you bought for $50 falls to $25. If you fully paid for the stock, you’ll lose 50% of your money. But if you bought on margin, you’ll lose 100%, and you still must come up with the interest you owe on the loan.

Caution: In volatile markets, investors who put up an initial margin payment for a stock may, from time to time, be required to provide additional cash if the price of the stock falls. Investors have been shocked to learn that a broker has the right to sell the securities that were bought on margin – without any notification, and at a potentially substantial loss to the investor.

Caution:If your broker sells your stock after the price has plummeted, then you’ve lost out on the chance to recoup your losses if the market bounces back.

The Risks

Margin accounts can be very risky and they are not for everyone. Before opening a margin account, be aware that:

You can lose more money than you have invested;

You may have to deposit additional cash or securities in your account on short notice to cover market losses;

You may be forced to sell some or all of your securities when falling stock prices reduce the value of your securities; and

Your brokerage firm may sell some or all of your securities without consulting you to pay off the loan it made to you.

You can protect yourself by knowing how a margin account works and what happens if the price of the stock purchased on margin declines.

Tip: Your broker charges you interest for borrowing money; take into account how that will affect the total return on your investments.

Tip: Ask your broker whether it makes sense for you to trade on margin in light of your financial resources, investment objectives, and tolerance for risk.

Read Your Margin Agreement

To open a margin account, you must sign a margin agreement. The agreement may either be part of your account agreement or separate. The margin agreement states that you must abide by the rules of the Federal Reserve Board, the New York Stock Exchange, the National Association of Securities Dealers, Inc., and the firm where you have set up your margin account.

Caution:Carefully review the agreement before signing.

As with most loans, the margin agreement explains the terms and conditions of the margin account. The agreement describes how the interest on the loan is calculated, how you are responsible for repaying the loan, and how the securities you purchase serve as collateral for the loan. Carefully review the agreement to determine what notice, if any, your firm must give you before selling your securities to collect the money you have borrowed.

***

***

Know the Margin Rules

The Federal Reserve Board and many self-regulatory organizations (SROs), such as the NYSE and NASD, have rules that govern margin trading. Brokerage firms can establish their own requirements as long as they are at least as restrictive as the Federal Reserve Board and SRO rules.

Here are some of the key rules you should know:

Before You Trade – Minimum Margin. Before trading on margin, the NYSE and NASD, for example, require you to deposit with your brokerage firm a minimum of $2,000 or 100 percent of the purchase price, whichever is less. This is known as the “minimum margin.” Some firms may require you to deposit more than $2,000.

Amount You Can Borrow – Initial Margin. According to Regulation T of the Federal Reserve Board, you may borrow up to 50 percent of the purchase price of securities that can be purchased on margin. This is known as the “initial margin.” Some firms require you to deposit more than 50 percent of the purchase price.

Tip:Not all securities can be purchased on margin.

Amount You Need After You Trade – Maintenance Margin. After you buy stock on margin, the NYSE and NASD require you to keep a minimum amount of equity in your margin account. The equity in your account is the value of your securities less how much you owe to your brokerage firm. The rules require you to have at least 25 percent of the total market value of the securities in your margin account at all times. The 25 percent is called the “maintenance requirement.” In fact, many brokerage firms have higher maintenance requirements, typically between 30 to 40 percent and sometimes higher, depending on the type of stock purchased.

Example: You purchase $16,000 worth of securities by borrowing $8,000 from your firm and paying $8,000 in cash or securities. If the market value of the securities drops to $12,000, the equity in your account will fall to $4,000 ($12,000 – $8,000 = $4,000). If your firm has a 25 percent maintenance requirement, you must have $3,000 in equity in your account (25 percent of $12,000 = $3,000). In this case, you do have enough equity because the $4,000 in equity in your account is greater than the $3,000 maintenance requirement.

But, if your firm has a maintenance requirement of 40%, you would not have enough equity. The firm would require you to have $4,800 in equity (40% of $12,000 = $4,800). Your $4,000 in equity is less than the firm’s $4,800 maintenance requirement. As a result, the firm may issue you a “margin call,” since the equity in your account has fallen $800 below the firm’s maintenance requirement.

Margin Calls

If your account falls below the firm’s maintenance requirement, your broker generally will make a margin call to ask you to deposit more cash or securities into your account. If you are unable to meet the margin call, your firm will sell your securities to increase the equity in your account up to or above the firm’s maintenance requirement.

Tip: Your broker may not be required to make a margin call or otherwise tell you that your account has fallen below the firm’s maintenance requirement. Your broker may be able to sell your securities at any time without consulting you first. Under most margin agreements, even if your firm offers to give you time to increase the equity in your account, it can sell your securities without waiting for you to meet the margin call.

Margin accounts involve a great deal more risk than cash accounts, where you fully pay for the securities you purchase. You may lose more than your initial investment when buying on margin. If you cannot afford to do so, then margin buying is not for you.

Read the margin agreement, and ask your broker questions about how a margin account works and whether it’s appropriate for you to trade on margin. Your broker should explain the terms and conditions of the margin agreement.

Know how much you will be charged on money you borrow from your broker, and know how these costs affect your overall return.

Remember that your brokerage firm can sell your securities without notice to you when you don’t have sufficient equity in your margin account.

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

There’s an aspect to retirement that many physicians do not plan for … the transition from work and practice to retirement. Your work has been an important part of your life. That’s why the emotional adjustments of retirement may be some of the most difficult ones.

Examples:

For example, what would you like to do in retirement? Your retirement vision will be unique to you. You are retiring to something not from something that you envisioned. When you have more time, you would like to do more travelling, play golf or visit more often, family and friends. Would you relocate closer to your kids? Learn a new art or take a new class? Fund your grandchildren’s education? Do you have philanthropic goals? Perhaps you would like to help your church, school or favorite charity? If your net worth is above certain limits, it would be wise to take a serious look at these goals. With proper planning, there might be some tax benefits too. Then you have to figure how much each goal is going to cost you.

Lists

If have a list of retirement goals, you need to prioritize which goal is most important. You can rate them on a scale of 1 to 10; 10 being the most important. Then, you can differentiate between wants and needs. Needs are things that are absolutely necessary for you to retire; while wants are things that still allow retirement but would just be nice to have.

Recent studies indicate there are three phases in retirement, each with a different spending pattern [Richard Greenberg CFP®, Gardena CA, personal communication].

The three phases are:

The Early Retirement Years. There is a pent-up demand to take advantage of all the free time retirement affords. You can travel to exotic places, buy an RV and explore forty-nine states, go on month-long sailing vacations. It’s possible during these years that after-tax expenses increase during these initial years, especially if the mortgage hasn’t been paid off yet. Usually the early years last about ten years until most retirees are in their 70’s.

Middle Years. People decide to slow down on the exploration. This is when people start simplifying their life. They may sell their house and downsize to a condo or townhouse. They may relocate to an area they discovered during their travels, or to an area close to family and friends, to an area with a warm climate or to an area with low or no state taxes. People also do their most important estate planning during these years. They are concerned about leaving a legacy, taking care of their children and grandchildren and fulfilling charitable intent. This a time when people spend more time in the local area. They may start taking extension or college classes. They spend more time volunteering at various non-profits and helping out older and less healthy retirees. People often spend less during these years. This period starts when a retiree is in his or her mid to late 70’s and can last up to 20 years, usually to mid to late-80’s.

Late Years. This is when you may need assistance in our daily activities. You may receive care at home, in a nursing home or an assisted care facility. Most of the care options are very expensive. It’s possible that these years might be more expensive than your pre-retirement expenses. This is especially true if both spouses need some sort of assisted care. This period usually starts when the retiree is their 80’s; however they can sometimes start in the middle to the late 70’s.

[A] Planning issues – early career

Most retirement lifestyle issues do not have to be addressed at this point. Keeping a healthy, balanced lifestyle will help to ensure a more productive retirement. This is the time to focus on the financial aspects of retirement planning.

[B] Planning issues – mid career

If early retirement is a major objective, start thinking about activities that will fill up your time during retirement. Maintaining your health is more critical, since your health habits at this time will often dictate how healthy you will be in retirement.

[C] Planning issues – late career

Three to five years before you retire, start making the transition from work to retirement.

Try out different hobbies;

Find activities that will give you a purpose in retirement;

Establish friendships outside of the office or hospital;

Discuss retirement plans with your spouse.

If you plan to relocate to a new place, it is important to rent a place in that area and stay for few months and see if you like it. Making a drastic change like relocating and then finding you don’t like the new town or state might be very costly mistake. The key is to gradually make the transition.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on March 30, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

To all our valued physicians readers and subscribers

***

You have always been the shield defending and healing patients in our communities. Now more than ever, you have become a guiding light through uncertainty as we navigate toward a brighter future.

This is our chance to thank you for your hard work and incredible impact!

Pink sheets are an over-the-counter (OTC) market that connects broker-dealers electronically. There is no trading floor and the quotations are also all done electronically. Since there is no central trading floor or stock exchange like the New York Stock Exchange (NYSE), the pink sheet-listed companies do not have the same criteria to fulfill as the companies listed on national stock exchanges. Many stocks listed on the pink sheets are low-priced penny stocks that trade for under $5 a share.

Pink sheets got their name because the original pink sheets listing the stocks were actually printed and distributed on pink pieces of paper. Trading over-the-counter (OTC) refers to the process of how securities listed on the pink sheets are traded through a broker-dealer network.

Recent advances in biomedical and health sciences—from immunotherapy to treat cancer, to the highly effective COVID-19 vaccines—demonstrate the strengths and successes of the U.S. biomedical enterprise. Such advances present an opportunity to revolutionize how to prevent, treat, and even cure a range of diseases including cancer, infectious diseases, Alzheimer’s disease, and many others that together affect a significant number of Americans.

To improve the U.S. government’s capabilities to speed research that can improve the health of all Americans, President Biden is proposing the establishment of the Advanced Research Projects Agency for Health (ARPA-H). Included in the President’s FY2022 budget as a component of the National Institutes of Health (NIH) with a requested funding level of $6.5B available for three years, ARPA-H will be tasked with building high-risk, high-reward capabilities (or platforms) to drive biomedical breakthroughs—ranging from molecular to societal—that would provide transformative solutions for all patients.

The Ides of March was a day in the Roman calendar that corresponds to 15 March. It was marked by several religious observances and was notable for the Romans as a deadline for settling debts.

In 44 BC, it became notorious as the date of the assassination of Julius Caesar which made the Ides of March a turning point in Roman history.

The concept of a self-taught and student motivated, but automated outcomes driven classroom may seem like a nightmare scenario for those who are not comfortable with computers. Now everyone can breathe a sigh of relief, because the Institute of Medical Business Advisors just launched an “automated” final examination review protocol that requires no programming skill whatsoever.

In fact, everything is designed to be very simple and easy to use. Once a student’s examination “blue-book” is received, computerized “robotic reviewers” correct student assignments and quarterly test answers. This automated examination model lets the robots correct tests and exams, while the students concentrate on guided self-learning.

According to Eugene Schmuckler PhD MBA MEd, Dean of the CERTIFIED MEDICAL PLANNER® professional designation and certification program,

“This option allows the modern adult-learner save both time and money as s/he progresses toward the ultimate goal of board certification as a CMP® mark holder.”

The trend is growing and iMBA, Inc., is leading the way.

Posted on March 14, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

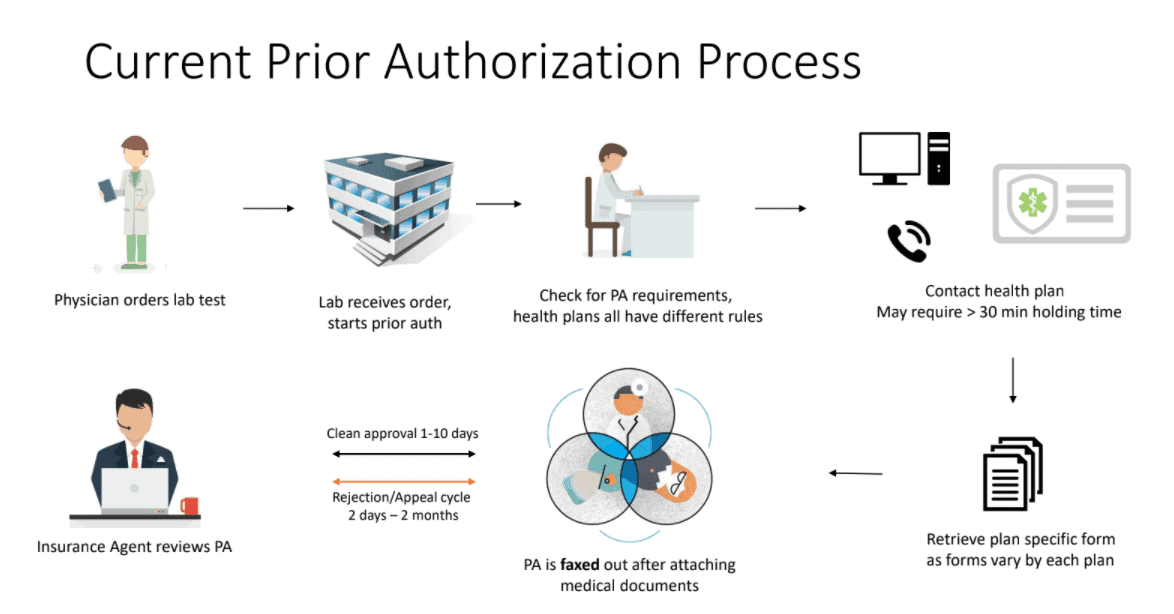

Prior Authorization and Patient Harm

• 34% of physicians report that PA has led to a serious adverse event for a patient in their care. • 24% of physicians report that PA has led to a patient’s hospitalization. • 18% of physicians report that PA has led to a life-threatening event or required intervention to prevent permanent impairment or damage. • 8% of physicians report that PA has led to a patient’s disability/permanent bodily damage, congenital anomaly/birth defect or death.

Beginning in 2022, there will be few situations in which a patient can receive a bill for out-of-network care they believed would be covered by their insurance company. This new rule should especially benefit patients in emergency situations who don’t have the time or luxury to dig up the details on every provider they encounter.

The No Surprises Act also requires insurance companies to provide patients with at least 90 days of coverage if an in-network provider moves out of network. That way, patients aren’t forced to switch providers immediately if such a move happens while they’re in the middle of a treatment plan.

Now, the No Surprises Act does have its limitations. Patients can still get a bill for out-of-network care if they visit an urgent care clinic for non-emergency purposes. Also, if consumers are informed that the care they’re about to receive is out of network and they give written consent to move forward, then they may get billed for that care even once the new rule takes effect.

Devaluation is the deliberate downward adjustment of the value of a country’s money related to another currency, group of currencies or currency standard. It is often confused with depreciation and is the opposite of revaluation which refers to the readjustment of a currency exchange rate.

The government of a country may decide to devalue its currency and like depreciation it is not the result of non-governmental activities.

One reason a country made devalue its currency is to combat a trade imbalance. Devaluation reduces the cost of a country’s export rendering them more competitive in the Global market which is which in turn increases the cost of imports.

If imports are more expensive domestic consumers are less likely to purchase them further strengthening domestic businesses because exports increase and imports decrease there is typically a better balance of payments because the trade deficit shrinks. In short a country that devalue its currency can produce is difficult because there is a greater demand for cheaper exports.

***

***

In accountancy, depreciation refers to two aspects of the same concept: first, the actual decrease of fair value of an asset, such as the decrease in value of factory equipment each year as it is used and wear, and second, the allocation in accounting statements of the original cost of the assets to periods in which the assets are used (depreciation with the matching principle).

Depreciation is thus the decrease in the value of assets and the method used to reallocate, or “write down” the cost of a tangible asset (such as equipment) over its useful life span. Businesses depreciate long-term assets for both accounting and tax purposes. The decrease in value of the asset affects the balance sheet of a business or entity, and the method of depreciating the asset, accounting-wise, affects the net income, and thus the income statement that they report.

BE AWARE ALL ADVISORS … NEXT GEN FINANCIAL ADVICE IS HERE?

Are you a financial planner, insurance agent or investment advisor seeking to assist your physician clients with medical practice enhancement solutions, along with healthcare targeted financial planning services, but don’t know where to turn for help?

OR, maybe you’ve already had a bad experience with a young physician or astute healthcare professional client that was actually more informed than you in these areas?

OR, a doctor/nurse client who demanded a true fiduciary advisor [not fee-based advice, with no dual licenses and no arbitration clauses] documented in writing].

The Physician Executive Summary is always included at the beginning of a formal business plan and represents a brief synopsis of the medical prarctice entire plan. Its appearance, grammar and style should be sharp and crisp as it represents an enticement for the reader to maintain interest and contribute intelligent or economic input into the new venture.

It should contain information about the practice, advertising and marketing opportunities, physician management, proposed financing with four Pro Forma financial statements, business operations and exit strategy. This last point, while unpleasant is often overlooked by naive practitioners. Business experts however, look favorably upon an escape plan and view it as the mark of mature professional that realizes the possibility of success as well as failure.

****

***

Ultimately, the plan must explain to potential investors how you will make the practice profitable and produce the required Return on Investment (ROI) for them. It must describe medical services, patient acceptance and benefits, provider qualifications and accomplishments, the amount of capital required, market size, potential practice growth rate, and market niche.

Additional information may include office location, proximity to labor, transportation, license requirements, business entity status, proprietary technology and potential working agreements with various insurance, managed care, ACA and HMO plans. If all of the above seems bewildering to the uninitiated, you are correct.

Remember however, that if you do not have, or can’t borrow the funds to begin a private practice, you will just have to become an employed practitioner until you can. It is therefore imperative to start off on the right foot, with a sound business plan, as you begin your medical career.

The International Franchise Association (IFA) estimates that that about $1 trillion in sales, or 40% of all retail sales, were made through franchised establishment last year. On the positive side, franchises offer a branded practice concept with management training and access to proprietary methods, marketing and advertising campaigns and a host of support.

Moreover, there are franchises available for virtually every healthcare product or service, including: diet, weight loss and fitness; vein care and laser surgery; vitamins, nutriceuticals and pharmaceuticals; plastic and cosmetic surgery; dermatology, tanning and skin care; home healthcare and extended, etc. Some well know established healthcare and medical franchises are: Doctors Express, Being There Senior Care, Home Care Assistance, Personal Training Institute, Inches-A-Weigh, Remedy Intelligent Staffing, Visiting Angels, Unlimited MedSearch, prnYourHealth and Any Lab Test Now, etc.

On the downside, franchises incur high start-up costs, rules and obligations, payment of franchise percentages and many contractual obligations. Questions to consider when contemplating this business entity include:

Franchise stability, track record, licensing and costs.

Training, support and proximity of other franchises.

Independence, ownership laws, contracts and dispute resolutions,

Screening methods, market size and potential market share.

Replacement cost and transferability?

For more information on Uniform Franchise Offerings Circulars (UFOCs) contact www.FranChoice.com or:

Posted on January 31, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Ann Miller RN MHACMP®

Executive Director

***

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism.

We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial.

And, our consultants “got fly”, just like U.

Read it! Write it! Post it! “Medical Executive-Post”.

Call or email us for your FREE advertising and sales consultation TODAY [770.448.0769]

Stock Markets: US stocks staged a big afternoon comeback for the second day in a row … but still not big enough to close in the green. American Express was the top performer in both the S&P and the Dow after the company reported its highest billings volume ever in Q4. And, enthusiasm over meme stocks more broadly appears to be dwindling along with cryptos. And, while NASDAQ took a hit, Microsoft reported quarterly sales of more than $50 billion for the first time ever.

Economy: The weight of the financial world is on Jerome Powell’s shoulders today. The Federal Reserve chair will provide an update on the central bank’s views on sky-high inflation and its plan for interest rate hikes this year (though none are expected until March).

Pandemic: Pfizer and BioNTech started clinical trials for an Omicron-specific vaccine yesterday. The results will help the pharma partners decide whether to replace their current jab formula with one that targets the most dominant Covid variant. The new vaccine is being tested both as a three-shot series for un-vaccinated participants and as a booster for the already vaccinated.

Whether you do contract work or have your own small business, tax deductions for the self-employed physician consultant and/or medical executive or nurse consultant, etc., can add up to substantial tax savings.

With self-employment comes freedom, responsibility, and a lot of expense. While most self-employed people celebrate the first two, they cringe at the latter, especially at tax time. They might not be aware of some of the tax write-offs to which they are entitled.

When it comes time to file your returns, don’t hesitate to claim the benefits you get for being the boss. As a self-employed success story, you’ve earned them.

FORM 1099NEC: Form 1099 NEC is one of several IRS tax forms used in the United States to prepare and file an information return to report various types of income other than wages, salaries, and tips. The term information return is used in contrast to the term tax return although the latter term is sometimes used colloquially to describe both kinds of returns.

“Many times an overlooked deduction is educational expenses. If one is taking courses or buying research material to be more effective in their work, this can be deductible.”

Individual Retirement Plans (IRAs)

One of the best tax write-offs for the self-employed physician consultant is a retirement plan. A person with no employees can set up an individual 401 (k). “You can contribute $19,500 in 2021 as a 401(k) deferral, plus 25 percent of net income.”

If you have employees, consider a SIMPLE (Savings Incentive Match Plan for Employees) IRA—an IRA-based plan that gives small employers a simplified method to make contributions to their employees’ retirement. As of 2021, an employee may defer up to $13,500 and employees over 50 may contribute an additional $3,000.

“A third retirement plan is Simplified Employee Pension IRA (SEP IRA).” The employer may contribute the lesser of 25 percent of income or $58,000 in 2021. If the employer has eligible employees, an equal percentage of their income must be contributed.

Recall that retirement plans are “absolutely the No. 1 tax deduction. The government is helping fund retirement.”

Business use of home or dwelling

Now, most self-employed taxpayers’ businesses start as home-based businesses. These people need to know portions of business costs are deductible and so “It is very important that you keep track of expenses relating to your housing costs.”

If your gross income from your business exceeds your total expenses, then you can deduct all of your expenses related to the business use of your home. If your gross income is less than your total expenses, your deduction will be limited to the difference between your gross income and the sum of all business expenses you would pay if the business was not in your home. Those expenses could include telephone lines, the Internet, and other costs to do business.

You must also have a home office that is truly used for work and the Internal Revenue Service may require you to document this.

***

Deducting automobile expenses

If you travel for business, even short distances within your own city, you may deduct the dollar value of business miles traveled on your tax return. The taxpayer may file the actual expense s/he incurred, or use the standard mileage rate prescribed by the IRS, which is 56 cents as of 2021. The IRS allowable mileage rates should be checked every year as they can change.

“If you decide to use actual car expenses, be sure to include payments, depreciation, registration, insurance, garage rent, licenses, repairs and maintenance, and parking and toll fees.” AND, “If you decide to use the standard mileage rate, it would be in your best interest to keep a log—daily, weekly or monthly—of miles driven to distinguish personal use from business use.”

Depreciation of property and equipment

Some self-employed people may purchase property and equipment for a business. If they expect that property to last longer than one year, it should be depreciated on the tax return.

Claims regarding property, according to the IRS, must meet the following criteria: You must own the property and it must be used or held to generate income. The property should have an estimated useful life, meaning you should be able to guess how long you can generate income with it. It may not have a useful life of one year or less, and may not be purchased and disposed of in the same year.

Certain repairs on property used for business may also be deducted.

Educational expenses

Any educational expense is potentially tax-deductible.

“Many times an overlooked deduction is educational expenses. “If one is taking courses or buying research material to be more effective in their work, this can be deductible.”

Think about any books, web courses, local college courses, or other classes or materials that you have purchased to improve your job or business. It’s easy to forget a work-related webinar or business e-book that was purchased online, so remember to save e-receipts.

Also recall that subscriptions to trade or professional publications and donations to business organizations, both of which are frequently necessary for the continuation and growth of your business.

Other areas to explore

Other deductions that can be easily missed are advertising and promotional expenses, banking fees, and air, bus, or train fare. Restaurant meals and other entertainment costs may be written off as long as they are necessary business expenses.

And, consider health insurance premiums, which in most cases represent a credit rather than a tax deduction. “A credit goes directly against one’s taxes, rather than a reduction of income.”

Regardless of which expenses you discover that you may write off, the most important thing is to keep accurate records throughout the year. Save receipts, including e-mail receipts, and file or log them so you have easy access to them at tax time. Not only does keeping receipts, mileage logs, and other expense records make filing taxes easier, but it also facilitates a system that allows you to track changes from year to year.

***

Long-term tax-saving strategies

Don’t just look at last-minute write-offs when considering self-employment tax deductions. Think about laying down some long-term strategies for money savings from year to year—particularly if you are a high earner.

“Accountants typically tell you what you have to pay but they don’t always tell you strategies to reduce your payments.”

To reduce your gross taxable income, consider setting up a defined-benefit pension plan. This plan is based on your age and income: The older you are and the higher your earnings, the more you are allowed to contribute. An alternative plan is an age-weighted profit-sharing plan, which is similar and can benefit those who have several employees.

Another strategy for high-earning business owners who own their own building through a limited liability company or similar business structure is to pay themselves rent. This rent is used to pay down the mortgage, but it is also considered a business expense for tax purposes.

Self-employed professionals required to have liability insurance should consider setting up their own insurance company. A captive insurance company is one that insures the risks of the business—or businesses, in the case of a cooperative. Its premiums can be tax-deductible.

But, if money accumulates and claims are minimal, the money taken out is taxable under capital gains. This is not a retirement strategy, but that it can save you money by allowing you to “pay yourself” instead of an insurance company and still deduct the premiums.

Assessment

With any of these more complicated, long-term strategies, consult with a business attorney, CPA/EA or financial planner to ensure you have the best plan possible for your business.

Just like real estate, butter has been around for thousands of years. Sometime in the 1800’s someone decided that there was a need for something that looked like butter, tasted similar to butter, but wasn’t butter. Along came margarine. Real estate investment trusts (REITs) are the margarine of the real estate investing world.

NAREIT, the National Association of Real Estate Investment Trusts, answers the question

“What is a REIT?” in the following way:

“A REIT, or Real Estate Investment Trust, is a type of real estate company modeled after mutual funds. REITs were created by Congress in 1960 to give all Americans – not just the affluent – the opportunity to invest in income producing real estate in a manner similar to how many Americans invest in stocks and bonds through mutual funds. Income-producing real estate refers to land and the improvements on it – such as apartments, offices or hotels. REITs may invest in the properties themselves, generating income through the collection of rent or they may invest in mortgages or mortgage securities tied to the properties, helping to finance the properties and generating interest income.”

While REITs typically own real estate, investors in REITs do not. REITs are paper assets that represent interest in a company that owns and operates income producing properties. In essence they are real estate flavored stock. As such, REITs are generally highly correlated with the stock market.

***

***

TERMINOLOGY

When discussing REITs, you encounter the following terminology – public, private, traded, and non-traded. Public REITs can be designated as non-traded or traded depending on whether or not they are traded on a stock exchange.

Since traded REITs are traded on the stock exchange, they enjoy a high degree of liquidity just like any other stock. Unfortunately, traded REITs tend to follow the economic cycles and can closely correlate with the stock market. This can lead to a higher degree of volatility than what is usually seen with physical real estate. Additionally, they do not afford the investor the tax-advantages that come with investments in physical real estate.

Private REITs and non-traded public REITs are not traded on an exchange. These are usually offered to accredited investors through broker-dealer networks. These REITs are illiquid and generally have high fees. They have been plagued with transparency issues as well as conflicts of interest. Valuation of this stock is difficult and can be misleading to the investor. Due diligence is very important as the quality of non-traded REITs can vary widely.

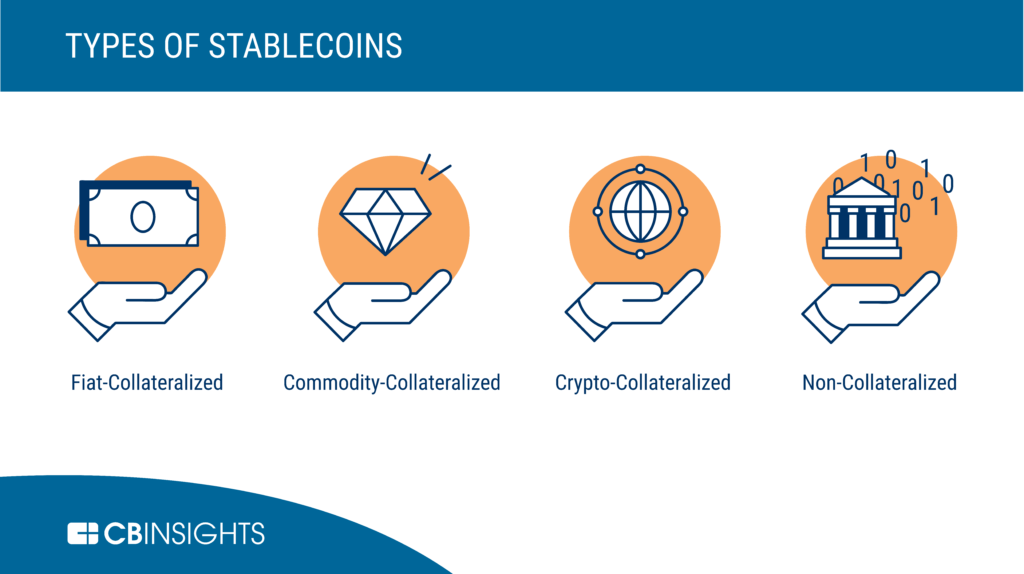

DEFINITION: Stablecoins are blockchain-based digital currencies that have been created with the aim to have a stable value. Stablecoins achieve price-stability through various different methods such as a peg against a fiat currency or a commodity, through collateralization against other cryptocurrencies or through algorithmic coin supply management.

Every stable coin includes a specific set of mechanisms that mostly behave in the same way. In general, stable coins keep collateral of the asset and manage the supply. In this way, they incentivize the market, which allows trade of the coin for no more or less than $1.

A stable coin can be considered the best depending on several factors: It should be stable. PAX is one the most stable stablecoin. It should be liquid and available on most exchanges. It should be backed by FIAT. PAX is 100% collateralized in US bank accounts. It should be regulated. It should be redeemable.

The physician, nurse, or other medical professional should easily recognize that there are a vast array of opportunities, obstacles, and pitfalls when it comes to managing one’s finances. Still, with some modicum of effort, the basic aspects of insurance, investments, taxes, accounting, portfolio management, retirement and estate planning, debt reduction, asset protection and practice management can be largely self-taught. Yet, it is realized that nuances and subtleties can make a well-intentioned financial plan fall short. The devil truly is in the details. Moreover, none of these areas can be addressed in isolation. It is common for a solution in one area to cause a new set of problems in another.

Accordingly, most health care practitioners would be well served to hire [independent, hourly compensated and prn] financial help. Unlike some medical problems, financial issues may not cause any “pain” or other obvious symptoms. Medical professionals tend to have far more complex financial situations than most lay people. Despite the complexities of the new world of health reform, far too many either do nothing; or give up all control totally, to an external advisor. This either/or mistake can be costly in many ways, and should be avoided.

In reality, and at various time in their careers, the medical professional needs a team comprised of at least a financial analyst, lawyer, management consultant, risk manager [actuary, mathematician or insurance counselor] and accountant. At various points in time, each member of the team, or significant others, will properly assume a role of more or less importance, but the doctor must usually remain the “quarterback” or leader; in the absence of a truly informed other, or Certified Medical Planner™.

This is necessary because only the doctor has the personal self-mandate with skin in the game, to take a big picture view. And, rightly or wrongly, investments dominate the information available regarding personal finance and the attention of most physicians. One is much more likely to need or want to discuss the financial markets with their financial advisor than private letter rulings by the IRS, or with their estate planning attorney or tax accountant. While hiring for expertise is a good idea, there is sinister way advisors goad doctors into using all their retail services; all of the time. That artifice is – the value of time.

True integrated physician focused and financial planning is at its core a service business, not a product or sales endeavor. And, increasingly money is more likely to be at the top of the list for providers as the healthcare environment is contracting.

So, eschewing the quarterback model of advice, and choosing to self-educate thru this book and elsewhere, may be one of the best efforts a smart physician can make.

Fibonacci, also known as Leonardo Bonacci, Leonardo of Pisa, or Leonardo Bigollo Pisano, was an Italian mathematician from the Republic of Pisa, considered to be “the most talented Western mathematician of the Middle Ages”

Today, 11/23, is the second holiest day of the year for math nerds after Pi Day. Why? Because it’s Fibonacci Day. If you forgot about the Fibonacci series from middle school, it goes 0, 1, 1, 2, 3, 5, 8, 13, 21, and so on, formed by taking the sum of the previous two numbers to create the next number in the sequence.

Fibonacci numbers can be found in many aspects of the natural world, including petal arrangements in flowers, the shape of hurricanes, a honeybee’s family tree, and even DNA molecules.

So yeah, to quote Jack Black in School of Rock, “Math is a really cool thing.”

Although standard definitions will tell you that it is a ‘monetary policy’ used by central banks to stimulate the national economy, in reality it is more as follows:

– A cleverly disguised word that simply means ‘money printing’.

Once you do retire, and put your physician or medical career behind you, it’s important to realize that, at some point, the IRS expects you to draw down your 401(k) balance. Starting at age 72, you need to take required minimum distributions (RMDs).

Your annual RMD amount depends on the balance of your 401(k) and a formula that determines your life expectancy.

***

***

QUERY: But – What happens if you don’t take your RMD for the year?

ANSWER: Well, you could end up paying a penalty. In fact, it’s a pretty hefty penalty of up to 50% of the amount you were supposed to withdraw. Paying that penalty can be pretty costly for someone living in retirement. As long as you’re vigilant and stay on top of the situation, though, you can avoid the penalty as well as these other costly 401(k) mistakes.

Almost everything you own and use for personal or investment purposes is a capital asset. Examples include a home, personal-use items like household furnishings, and stocks or bonds held as investments. When you sell a capital asset, the difference between the adjusted basis in the asset and the amount you realized from the sale is a capital gain or a capital loss.

Generally, an asset’s basis is its cost to the owner, but if you received the asset as a gift or inheritance, refer to Topic No. 703 for information about your basis.

For information on calculating adjusted basis, refer to Publication 551, Basis of Assets. You have a capital gain if you sell the asset for more than your adjusted basis. You have a capital loss if you sell the asset for less than your adjusted basis. Losses from the sale of personal-use property, such as your home or car, aren’t tax deductible.

Churning: The practice of a provider seeing a patient more often than is medically necessary, primarily to increase revenue through an increased number of visits. A practice, in violation of SEC rules, where a salesperson affects a series of transactions in a customer’s account which are excessive in size and/or frequency in relation to the size and investment objectives of the account. An insurance agent who is churning an account is normally seeking to maximize the income (in commissions, sales credits or mark-ups) derived from the account.

FRONT-RUNNING: Form of market manipulation where a broker/dealer delays processing of a large customer trade in an underlying security until the firm can execute an options trade in that security in anticipation of the client’ s trade impact on the underlying security.

Pump and dump: A a form of securities fraud that involves artificially inflating the price of an owned stock through false and misleading positive statements, in order to sell the cheaply purchased stock at a higher price. Once the operators of the scheme “dump” their overvalued shares, the price falls and investors lose their money.

DEFINITION: The meaning of meme stocks is sort of self-explanatory: hyped stocks that perform well. But from a fundamental perspective, they shouldn’t do well at all.

For example, Reddit forums and social media hype drive meme stocks. Speculators on Twitter and Reddit united together to trade their favorite companies in hopes of driving them “to the moon.”

It may not be fair to call them speculators. These hype beasts want to buy and hold stocks of companies that might not have a great long-term outlook.

Brokerages like Robinhood helped level the playing field with apps and ‘easier’ access. That’s giving retail traders more opportunity. Robinhood traders can buy with just a few clicks on their smartphones and use partial positions to buy chunks of stocks.

If you’ve ever listened to an early morning financial news broadcast, you’ve heard a reference to “futures” and how they affect the stock market before it opens. Physicians Investors follow the futures because it provides an indication of where stocks are headed at the opening bell. One of the most widely followed futures is the Dow Futures, whose underlying value is based on the Dow Jones Industrial Average, an index of 30 major U.S. companies.

***

***

DEFINITION: After the markets close at 4 pm New York time, implied open prices of the Dow Jones Industrial Average, S&P 500 Index, and NASDAQ, which fluctuate from minute to minute, can be calculated.

Considering the DJIA as an example, the basis of calculating implied open is the price of a “DJX index option futures contract “.

The first World Financial Planning Day was held on October 4, 2017. The Financial Planning Standards Board (FPSB) hosts the day. Every year, the FPSB partners with the International Organization of Securities Commissions (IOSCO).

***

Today, it is always held during the first Wednesday of October during IOSCO’s World Investor Week.

***

QUERY: But, what about the entire ecosystem of personal and professional financial planning, investing, risk, business and medical practice management for physicians and healthcare professionals? A vital, unique and complicated niche!

ANSWER: According to the Institute of Medical Business Advisors, Inc., WFP Day is every day for CERTIFIED MEDICAL PLANNER® professional certification holders.

So – If you are in this WFPD industry – Become a fiduciary focused board CERTIFIED MEDICAL PLANNER with extreme healthcare industry ecosystem specificity.

:focal(1365x816:1366x817)/https://tf-cmsv2-smithsonianmag-media.s3.amazonaws.com/filer/3a/70/3a70f58d-dabc-4d54-ba16-1d1548594720/2560px-fibonaccispiralsvg.jpg)

{kind=link}