BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on October 20, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Markets: The S&P 500hit an all-time high yesterday, closing out its sixth consecutive week of gains for its longest streak of 2024. The Dow and NASDAQ also closed in the green.

The largest Medicare Advantage insurers have prioritized profits over patient care by increasing the use of prior authorization in recent years to frequently deny post-acute care services to older adults, according to a report published Oct. 17th by the Senate Permanent Subcommittee on Investigations.

The drugstore chain CVS is in the process of shuttering “roughly 300” locations across the country in 2024, a spokesperson confirmed to Good Housekeeping. That includes the dozens of pharmacies in Target stores.

Posted on October 16, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Maximum lifespans. The upper limit of human life expectancy is leveling out, according to a new study published in the journal Nature Aging. Back in 1990, life-extending tech and health measures were increasing the average global lifespan by about 2.5 years per decade, but that dropped to 1.5 years per decade in the 2010s and closer to zero in the US, where there are more drug overdoses, shootings, and medical care inequities.

Sphere Entertainment popped 6.33% on the news that a second Sphere will be built in Abu Dhabi. London was originally supposed to be the location of a second venue, but they’ve already got the Eye, and didn’t need more circular tourist attractions.

Oklo, a Sam Altman-backed nuclear energy startup, rose another 16.04% on the news that Google will purchase nuclear power to turbocharge its AI infrastructure.

Charles Schwab climbed 6.10% after the bank announced a top and bottom line beat last quarter, as well as higher revenue projections for the full fiscal year.

Boeing somehow gained 2.26% after announcing it is raising $35 billion to support its struggling finances as the machinist union strike enters its second month.

Wolfspeed, which sounds like a super power in a YA novel, soared 21.27% on the news that the US government will provide the chipmaker with up to $750 million in government grants.

STOCKS DOWN

Semiconductor stocks got a double whammy in the last 48 hours. First, Bloomberg revealed that US officials are considering limiting the sale of AI chips outside the country. Then, ASMLmissed its Q3 sales estimates (more on that below). Nvidia shares slid 4.52%, AMD fell 5.22%, and Intel dropped 3.33%.

Citigroup beat earnings estimates this quarter, but shareholders punished the bank for setting aside more money in case of higher loan losses ahead. Shares dropped 5.11%.

Coty, parent company of numerous beauty brands like CoverGirl, fell 10.74% to a new 52-week low after it warned of a sales slowdown in the coming quarters.

Enphase Energy tumbled 9.29% after RBC analysts downgraded the solar power stock, citing growing competition from the likes of Tesla as well as slowing demand for solar batteries.

Speaking of energy, oil stocks plummeted on news of Israel’s targeting of Iranian military assets rather than crude production facilities. ExxonMobil fell 3.01%, Chevron dropped 2.67%, and ValeroEnergy sank 4.62%.

Here’s where the major benchmarks ended yesterday:

The S&P 500® index (SPX) fell 44.59 points (–0.76%) to 5,815.26; the Dow Jones Industrial Average® ($DJI) dropped 324.80 points (–0.75%) to 42,740.42; and the NASDAQ Composite®($COMP) lost 187.09 points (–1.01%) to 18,315.59.

The 10-year Treasury note yield (TNX) fell three basis points to 4.04%, the lowest close in a week.

The CBOE Volatility Index® (VIX) climbed to 20.72, an elevated level.

Millions of seniors will lose access to their Medicare Advantage plans after major insurer cuts in the aftermath of the Inflation Reduction Act. Experts spoke with Newsweek about what’s going on and what steps seniors can take to get the coverage they need.

Posted on October 15, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters &The Medicare Team

Medicare open enrollment—which runs from October 15th through December 7th this year—is your chance to check in on your Medicare plan and, if needed, change it.

***

***

Mark your calendars — Medicare Open Enrollment starts October 15th! Did you know new benefits are coming to Medicare drug coverage next year?

Also starting next year, you can choose to participate in a program that spreads your out-of-pocket drug costs across the calendar year, instead of paying all at once at the pharmacy. It’s called the Medicare Prescription Payment Plan — and you can opt in with your plan throughout the 2025 plan year. Contact your plan for more details.

Remember, Medicare plans can change from one year to the next, and so can your health needs. Preview and compare all your health and drug options and see if you can save!

Posted on October 11, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

With the annual enrollment period for Medicare Advantage (MA) plans slated to open in less than two months, many MA plans are cutting benefits and provider payments, while approving fewer claims. Further, after a decade of accelerated growth in the MA market, several MA plan executives have announced MA market exits and decreases in membership for the upcoming plan year.

This Health Capital Topics article discusses recently announced MA market exits, the reasons for those exits, and the current environment in which MA plans are operating. (Read more...)

Posted on October 2, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Humana, the country’s second largest Medicare Advantage insurer, is aggressively culling its plan offerings after several quarters of spending more than expected on its members’ medical care, and getting hammered on Wall Street for it. The company will scrap Medicare Advantage plans in 2025 that currently cover about 560,000 members.

Markets: Stocks embraced the start of spooky season by falling yesterday, ending a hot streak as investors mulled the rising tensions in the Middle East.

General Motors: Reported slightly better-than-expected sales during the third quarter, thanks in part to increased sales of small crossovers and electric vehicles. The automaker reported a 2.2% decrease in sales, compared with a year earlier, an improvement over auto industry forecasts that projected a decline of more than 3% in the quarter.

Meanwhile:Nike’s beleaguered stock was up a bit ahead of its first earnings report since the company announced a CEO change. It withdrew its full-year guidance and postponed its investor day as longtime company veteran Elliott Hill prepares to take the top job at the sneaker giant. Instead, executives said Nike will provide quarterly guidance for the rest of the year. Shares of Nike fell about 7% in early trading Wednesday.

Posted on September 25, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

California state officials filed a lawsuit against one of the world’s top oil giants accusing Exxon Mobil of driving global pollution by running a “decades-long campaign of deception” that dramatically overstated the effectiveness of plastic recycling. The suit seeks“multiple billions of dollars” in civil damages from Exxon Mobil—a main producer of the petrochemicals used to make single-use plastics—California Attorney General Rob Bonta said.

Smartsheet popped 6.47% on the news that Blackstone and Vista Equity Partners will pay $8.4 billion in cash to take the software maker private.

Freeport-McMoRan gained 7.95% after the Chinese government announced stimulus plans. Shareholders are hopeful that more economic activity means more business for the copper miner.

Liberty Broadband soared 25.92% thanks to its counterproposal to CharterCommunications, asking for a higher payout before an acquisition takes place. Charter shares fell 2.49%.

Visa fell 5.36% as the US government sued it over an alleged debit card monopoly.

Regeneron Pharmaceuticals dropped 4.21% due to a federal judge’s ruling that it cannot block a new product from rival pharma company Amgen that mimics its eye-care drug Eylea.

The S&P 500® index (SPX) added 14.36 points (0.25%) to 5,732.93; the Dow Jones Industrial Average® ($DJI) rose 83.57 points (0.20%) to 42,208.22; the NASDAQ Composite® ($COMP) gained 100.25 points (0.56%) to 18,074.52.

The 10-year Treasury note yield (TNX) finished unchanged at 3.74%.

The CBOE Volatility Index® (VIX) keeps setting new lows for September, dropping to 15.49.

Boeing offers 30% raise in attempt to end strike. With 30,000 factory workers on strike and 737 production halted for a second week, the embattled aviation company offered to hike wages for union members higher than the original 25% increase over four years they voted to reject.

German Chancellor Olaf Scholz warned Italian bank UniCredit against “unfriendly” acts after the bank upped its stake in Germany’s Commerzbank, eclipsing the country as its largest shareholder.

Posted on September 23, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Former: CEO and Founder Superior Consultant Company, Inc. [SUPC-NASD]

EDITOR’S NOTE:I first met Rich in B-school, when I was a student, back in the day. He was the Founder and CEO of Superior Consultant Holdings Corp. Rich graciously wrote the Foreword to one of my first textbooks on financial planning for physicians and healthcare professionals. Today, Rich is a successful entrepreneur in the technology, health and finance space.

-Dr. David E. Marcinko MBA MEd CMP®

***

By Richard Helppie

Today for your consideration – How to fix the healthcare financing methods in the United States?

I use the term “methods” because calling what we do now a “system” is inaccurate. I also focus on healthcare financing, because in terms of healthcare delivery, there is no better place in the world than the USA in terms of supply and innovation for medical diagnosis and treatment. Similarly, I use the term healthcare financing to differentiate from healthcare insurance – because insurance without supply is an empty promise.

This is a straightforward, 4-part plan. It is uniquely American and will at last extend coverage to every US citizen while not hampering the innovation and robust supply that we have today. As this is about a Common Bridge and not about ideology or dogma, there will no doubt be aspects of this proposal that every individual will have difficulty with. However, on balance, I believe it is the most fair and equitable way to resolve the impasse on healthcare funding . . . .

Let me start in an area sure to raise the ire of a few. And that is, we have to start with eliminating the methods that are in place today. The first is the outdated notion that healthcare insurance is tied to one’s work, and the second is that there are overlapping and competing tax-supported bureaucracies to administer that area of healthcare finance.

Step 1 is to break the link between employment and health insurance. Fastest way to do that is simply tax the cost of benefits for the compensation that it is. This is how company cars, big life insurance policies and other fringe benefits were trimmed. Eliminating the tax-favored treatment of employer-provided healthcare is the single most important change that should be made.

Yes, you will hear arguments that this is an efficient market with satisfied customers. However, upon examination, it is highly risky, unfair, and frankly out of step with today’s job market.

Employer provided health insurance is an artifact from the 1940’s as an answer to wage freezes – an employer could not give a wage increase, but could offer benefits that weren’t taxed. It makes no sense today for a variety of reasons. Here are a few:

1. Its patently unfair. Two people living in the same apartment building, each making the same income and each have employer provided health insurance. Chris in unit 21 has a generous health plan that would be worth $25,000 each year. Pays zero tax on that compensation. Pat, in unit 42 has a skimpy plan with a narrow network, big deductibles and hefty co-pays. The play is worth $9,000 each year. Pat pays zero tax.

3. The insurance pools kick out the aged. Once one becomes too old to work, they are out of the employer plan and on to the retirement plan or over to the taxpayers (Medicare).

4. The structure is a bad fit. Health insurance and healthy living are longitudinal needs over a long period of time. In a time when people change careers and jobs frequently, or are in the gig economy, they are not any one place long enough for the insurance to work like insurance.

5. Creates perverse incentives. The incentives are weighted to have employers not have their work force meet the standards of employees so they don’t have to pay for the health insurance. Witness latest news in California with Uber and Lyft.

6. Incentives to deny claims abound. There is little incentive to serve the subscriber/patient since the likelihood the employer will shop the plan or the employee will change jobs means that stringing out a claim approval is a profitable exercise.

7. Employers have difficulty as purchasers. An employer large enough to supply health insurance has a diverse set of health insurance needs in their work force. They pay a lot of money and their work force is still not 100% happy.

Net of it, health insurance tied to work has outlived its usefulness. Time to end the tax-favored treatment of employer-based insurance. If an employer wants to provide health insurance, they can do it, but the value of that insurance is reflected in the taxable W-2 wages – now Pat and Chris will be treated equally.

Step 2 is to consolidate the multiple tax-supported bureaus that supply healthcare. Relieve the citizens from having to prove they are old enough, disabled enough, impoverished enough, young enough. Combine Medicare, Medicaid, CHIP, Tricare and even possibly the VA into a single bureaucracy. Every American Citizen gets this broad coverage at some level. Everyone pays something into the system – start at $20 a year, and then perhaps an income-adjusted escalator that would charge the most wealthy up to $75,000. Collect the money with a line on Form 1040.

I have not done the exact math. However, removing the process to prove eligibility and having one versus many bureaucracies has to generate savings. Are you a US Citizen? Yes, then here is your base insurance. Like every other nationalized system, one can expect longer waits, fewer referrals to a specialist, and less innovation. These centralized systems all squeeze supply of healthcare services to keep their spend down. The reports extolling their efficiencies come from the people whose livelihoods depend on the centralized system. However, at least everyone gets something. And, for life threatening health conditions, by and large the centralized systems do a decent job. With everyone covered, the fear of medical bankruptcy evaporates. The fear of being out of work and losing healthcare when one needs it most is gone.

So if you are a free market absolutist, then the reduction of vast bureaucracies should be attractive – no need for eligibility requirements (old enough, etc.) and a single administration which is both more efficient, more equitable (everyone gets the same thing). And there remains a private market (more on this in step 3) For those who detest private insurance companies a portion of that market just went away. There is less incentive to purchase a private plan. And for everyone’s sense of fairness, the national plan is funded on ability to pay. Bearing in mind that everyone has to pay something. Less bureaucracies. Everyone in it together. Funded on ability to pay.

Step 3 is to allow and even encourage a robust market for health insurance above and beyond the national plan – If people want to purchase more health insurance, then they have the ability to do so. Which increases supply, relieves burden on the tax-supported system, aligns the US with other countries, provides an alternative to medical tourism (and the associated health spend in our country) and offers a bit of competition to the otherwise monopolistic government plan.

Its not a new concept, in many respects it is like the widely popular Medigap plans that supplement what Medicare does not cover.

No one is forced to make that purchase. Other counties’ experience shows that those who choose to purchase private coverage over and above a national plan often cite faster access, more choice, innovation, or services outside the universal system, e.g., a woman who chooses to have mammography at an early age or with more frequency than the national plan might allow. If the insurance provider can offer a good value to the price, then they will sell insurance. If they can deliver that value for more than their costs, then they create a profit. Owners of the company, who risk their capital in creating the business may earn a return.

For those of you who favor a free market, the choices are available. There will be necessary regulation to prevent discrimination on genetics, pre-existing conditions, and the like. Buy the type of plan that makes you feel secure – just as one purchases automobile and life insurance.For those who are supremely confident in the absolute performance of a centralized system to support 300+ million Americans in the way each would want, they should like this plan as well – because if the national plan is meeting all needs and no one wants perhaps faster services, then few will purchase the private insurance and the issuers will not have a business. Free choice. More health insurance for those who want it. Competition keeps both national and private plans seeking to better themselves.

Step 4 would be to Permit Access to Medicare Part D to every US Citizen, Immediately

One of the bright spots in the US Healthcare Financing Method is Medicare Part D, which provides prescription drug coverage to seniors. It is running at 95% subscriber satisfaction and about 40% below cost projections.

Subscribers choose from a wide variety of plans offered by private insurance companies. There are differences in formularies, co-pays, deductibles and premiums.

So there you have it, a four part plan that would maintain or increase the supply of healthcare services, universal insurance coverage, market competition, and lower costs. Its not perfect but I believe a vast improvement over what exists today. To recap:

1. Break the link between employment and healthcare insurance coverage, by taxing the benefits as the compensation they are.

2. Establish a single, universal plan that covers all US citizens paid for via personal income taxes on an ability-to-pay basis. Eliminate all the other tax-funded plans in favor of this new one.

3. For those who want it, private, supplemental insurance to the national system, ala major industrialized nations.

4. Open Medicare Part D (prescription drugs) to every US citizen. Today.

Posted on September 13, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Nima Khodakarami PhD and Benjamin Ukert PhD

Evidence from Texas

***

***

Medical care services before the health service is performed—became standard practice beginning with Medicare and Medicaid legislation in the 1960s.

Although research has uncovered disparities in prior coverage for cancer patients based on race, little has been known to date on the role of prior authorization in increasing or decreasing these disparities.

To learn more about the issue, Benjamin Ukert, Ph.D., an assistant professor of health policy and management in the Texas A&M University School of Public Health, and a colleague at Penn State conducted a retrospective study of data provided by a major national commercial insurance provider on 18,041 patients diagnosed with cancer between Jan. 1st, 2017, and April 1st, 2020.

The study is published in the journal Health Services Research.

Posted on September 6, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

On July 26, 2024, the U.S. Department of Justice (DOJ) filed a complaint in intervention against Murphy Medical Center, doing business as Erlanger Western Carolina Hospital, and Chattanooga-Hamilton County Hospital Authority, doing business as the Erlanger Health System and Erlanger Medical Center. The government’s complaint, filed in the U.S. District Court for the Western District of North Carolina, alleges that Erlanger violated the Stark Law, and subsequently submitted false claims to the Medicare program in violation of the False Claims Act (FCA).

Posted on August 31, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Elastic NV plummeted 26.49% after the software maker announced a weak quarterly report and forecast worse quarters ahead.

Alnylam Pharmaceuticals stumbled 8.47% in spite of announcing positive Phase 3 trial results for its new heart disease drug. Shareholders don’t think the new drug is as groundbreaking as it could’ve been compared to offerings from competitors like BridgeBio, which popped 13.12% on the news.

The SPX climbed 56.44 points (1.01%) to 5,648.40, roughly flat for the week; the $DJI rose 228.03 points (0.55%) to 41,563.08, up almost 1% for the week; the NASDAQ Composite®($COMP) added 197.19 points (1.13%) to 17,713.62, down nearly 1% from a week ago.

The 10-year Treasury note yield (TNX) climbed three basis points to 3.91% but fell about 20 basis points in August.

The CBOE Volatility Index® (VIX) fell moderately to 14.96, well below levels above 30 recorded earlier this month.

The Centers for Medicare and Medicaid Services (CMS) has been doing victory laps since announcing discounts on August 15 for 10 of the most expensive Medicare Part D drugs, a change that is set to go into effect in 2026. These discounts, called maximum fair prices (MFPs), kick off annual negotiations between the CMS and drug manufacturers. The negotiations were made possible by the Inflation Reduction Act (IRA), which also brings other changes such as Medicare Part D benefit redesign.

Visualize: How private equity tangled banks in a web of debt, from the Financial Times.

And, Remember NFTs? This is an excellent history of OpenSea, the largest NFT marketplace, and all the chaos within its walls.

Posted on August 17, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Here’s where the major stock market benchmarks ended:

The S&P 500® index (SPX) rose slightly, up 11 points (0.2%) to end the day at 5,554.25, finishing up 3.9% for the week; the Dow Jones Industrial Average® ($DJI) jumped 96.7 points (0.24%) to close the week at 40,659.76, up 2.9% from last Friday; the NASDAQ Composite®($COMP) gained 37.2 points (0.21%) to 17,631.72, up 5.3% for the week.

The 10-year Treasury note yield (TNX) fell three basis points to just above 3.89%.

Bavarian Nordic, which makes an m-pox vaccine, jumped 15.64%, continuing its surge after the World Health Organization on Wednesday declared a public emergency over the disease’s spread in Africa.

Bayer popped 8.36% after the firm won a legal dispute against claims that its weedkiller Roundup causes cancer.

Rocket Lab rose 12.52% after the aerospace company announced it shipped two spacecraft to Cape Carnival in preparation for a launch to Mars.

H&R Block had its best day since 2022 (up 12.24%) after raising its dividend by 17% and announcing a $1.5 billion share buyback.

Maravai LifeSciences leaped 21.46% on reports that the drugmaker received a takeover offer from Repligen Corp.

What’s down

On the flip side of that last gainer, Repligen Corp. plummeted 9.26% on the takeover news.

Astera Labs dropped 5.52% after several investment firms, including Evercore and JPMorgan, lowered their price target for the chipmaker.

ReNew Energy Global dropped 5.91% after the company reported it missed earnings and revenue expectations yesterday.

The Biden administration announced yesterday that Medicare used its newfound power to negotiate with drug makers to win landmark discounts for 10 widely prescribed drugs to treat ailments like heart disease, cancer, and diabetes. The Inflation Reduction Act, signed into law two years ago, allows the federal health insurance program to directly bargain with pharma companies for the first time.

Visualize: How private equity tangled banks in a web of debt, from the Financial Times.

Posted on August 11, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

On July 10, 2024, the Centers for Medicare & Medicaid Services (CMS) released its proposed Medicare Physician Fee Schedule (MPFS) for calendar year (CY) 2025.

In addition to the agency’s suggested cut to physician payments, the proposed rule also announced new covered services. According to CMS, the proposed rule “reflect[s] a broader Administration-wide strategy to create a more equitable health care system that results in better accessibility, quality, affordability, empowerment, and innovation for all Medicare beneficiaries.” (Read more…)

Posted on August 10, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

FTX was ordered to pay $12.7 billion to customers. All customers will recoup their deposits that were locked when the crypto exchange went under in 2022, the Commodity Futures Trading Commission just said last Thursday.

Take-Two Interactive Software surged 4.35% after it beat earnings estimates last quarter, but no word yet on how its Gearbox acquisition is helping its bottom line, nor when GTA 6 is going to be released.

Expedia traveled 10.21% higher due to an earnings beat, with the company sidestepping a consumer spending slowdown quite nicely.

What’s down

e.l.f. Beauty tanked 14.46% despite beating earnings estimates and guiding for a better fiscal year than expected, as investors worry about tough competition.

Capri Holdings slid 4.86% as the company founded by Michael Kors faces slowing sales from cash-strapped consumers.

The S&P 500® index (SPX) rose 25 points (0.5%) to 5,344.16, ending the week little changed; the Dow Jones Industrial Average® ($DJI) rose 51 points (0.1%) to 39,497.54 to end the week down about 0.6%; the NASDAQ Composite® ($COMP) ended 85 points higher (0.5%) at 16,745.30, leaving it about 0.2% lower for the week.

The 10-year Treasury note yield (TNX) dropped five basis points to 3.944%.

The Cboe Volatility Index (VIX) declined three points (13%) to 20.7.

Google and Meta teamed up to target teens with ads for Instagram on YouTube, going against Google’s own rules, the Financial Times reported.

Posted on July 21, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

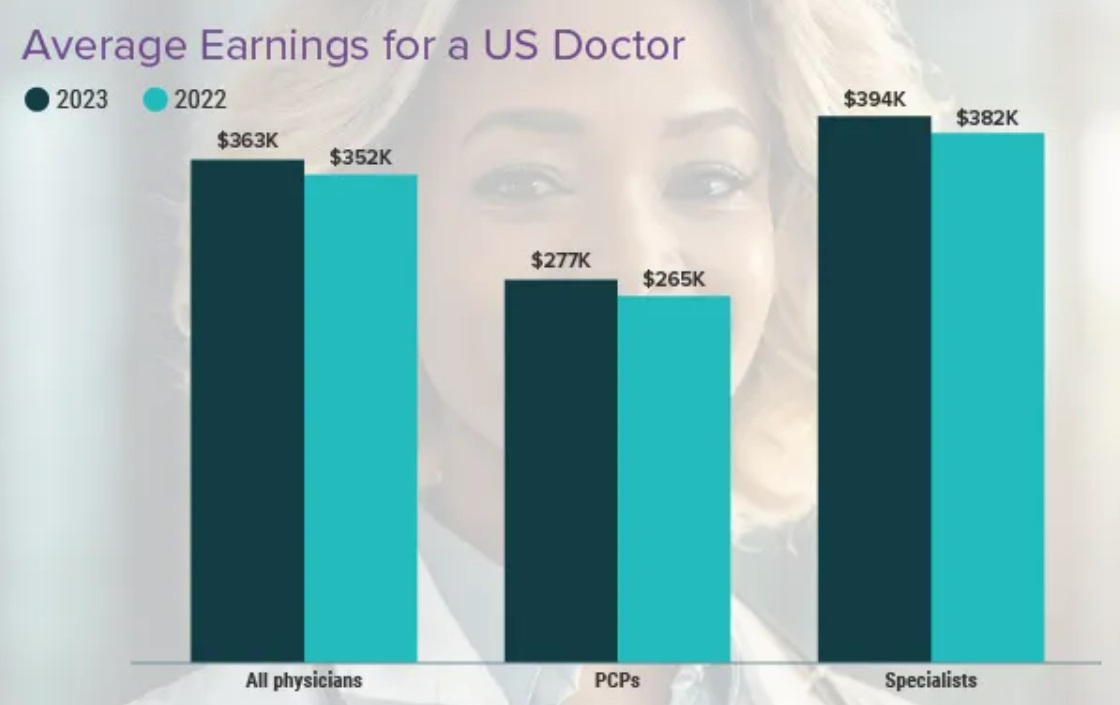

Orthopedic doctors and surgeons earn on average 558 thousand U.S. dollars annually. This makes Orthopedic doctors and surgeons the most well-compensated physicians in the United States as of 2024, followed by plastic surgeons. Plastic surgeons were, by far, the highest earning physicians in the U.S. in 2023. An orthopedic physician specializes in injuries and diseases involving bones, muscles, joints, nerves and other parts of the musculoskeletal system.

Although orthopedic doctors and surgeons have the highest average annual salary, from 2023 to 2024 their compensation actually decreased by 3 percent. In comparison, compensation for physicians specialized in physical medicine and rehabilitation increased 11 percent during this time, while plastic surgeons saw the largest decrease of 13 percent. The region with the highest annual compensation for physicians was West North Central in 2024, with physicians earning some 404 thousand U.S. dollars in this region.

Medicare Rates in 2025 Would Cut Pay For Docs by About 3%

And so, Federal officials on July 11th proposed Medicare rates that effectively would cut physician pay by about 3% in 2025, touching off a fresh round of protests from medical associations. The 2025 draft base rate, or conversion factor, is slated to drop to $32.36 from the current level of $33.29, the Centers for Medicare & Medicaid Services said.

This proposed cut is mostly due to the 5-year freeze in the physician schedule base rate mandated by the 2015 Medicare Access and CHIP Reauthorization Act (MACRA). Congress designed MACRA with an aim of shifting clinicians toward programs that would peg pay increases to quality measures.

Posted on July 9, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST –TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The CBOE Volatility Index® (VIX) climbed slightly to 12.37.

The S&P 500 index®(SPX) rose 5.66points (0.1%) to 5,572.85; the Dow Jones Industrial Average® ($DJI) dropped 31.08 points (0.1%) to 39,344.79; the NASDAQ Composite® ($COMP) gained 50.98 points (0.3%) to 18,403.74.

The 10-year Treasury note yield (TNX) was roughly flat at 4.27%.

Intel popped 6.15% after an analyst at Melius Research declared the company could be one of the big AI winners in the second half of this year.

Morphic Holding skyrocketed 75.06% on the news that Eli Lilly will acquire the drugmaker for $3.2 billion in cash.

SolarEdge climbed 9.26% thanks to an upgrade from “underperform” to “neutral” by Bank of America analysts, who see big upside and few downside risks ahead.

Lucid rose 7.85% on the news that its deliveries rose 70% in the second quarter.

What’s down

ServiceNow dipped 5.04% after Guggenheim analysts downgraded the cloud computing company to “sell,” citing growing risks in the second half of this year.

Stat: 27. That’s a tally of some of the hospital mergers, acquisitions, joint ventures, affiliations, and partnerships that have been canceled since January 2022. (Becker’s Hospital Review)

Read: Health insurers received $50 billion from Medicare for diseases that doctors did not treat over three years, according to a recent analysis. (Wall Street Journal)

Posted on June 10, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Markets: Stocks dropped ever so slightly to end last week as investors tried to make sense of the big jobs report. Lots of jobs = good, but lots of jobs also = interest rates likely staying the same for awhile longer (more below). AMC had a rough day, tumbling 15% as the latest meme stock craze started to fizzle.

Blue Kansas City Exiting MA Market by 2025 Due to ‘Regulatory Demands’

Blue Cross and Blue Shield of Kansas City (Blue KC) is leaving the Medicare Advantage (MA) market at the end of 2024, the insurer announced recently. The company blamed “heightened regulatory demands and rising market and financial pressures” for the decision but said it is still focused on employer-sponsored health plans, and Medicare supplement and Affordable Care Act plans in the state.

“We explored every alternative path for our MA members and are disappointed we must exit this line of business,” said Erin Stucky, Blue KC President and CEO, in a statement. “We value our MA members and are committed to providing uninterrupted, quality service to our current MA membership through the end of 2024.”

Cue Health, founded in 2010, started with great hopes as it promised a way to accurately test for Covid-19 without needing a lab. “We designed and developed a new molecular testing platform bringing lab complexity to an easy-to-use, portable device. Now you can get the best of lab molecular testing — speed, accuracy, and versatility – at home, the office, or on the go,” the company shared on its website. The company went public (with the ticker (HLTH) ) in 2021 at $16 and rose to $20.55 and carried that massive $2.3 billion valuation. Through 2023 and into this year, Cue unsuccessfully tried to shore up operations, get new products to market, and find new capital.

In May, however, the FDA advised customers not to use two of its products at all because they did not deliver accurate results. Finally, its board and executives threw in the towel. On May 28th, the company announced it was ceasing operations and filed for bankruptcy in Delaware’s U.S. Bankruptcy Court. The company’s assets will be sold off at an undetermined date, and the proceeds will be distributed to creditors.

***

Inflation data from the Fed meeting on Wednesday: Inflation data for May arrives in the morning, and it’s expected to show price growth held steady at 3.4% annually. In the afternoon, the FOMC will wrap up its meeting with a Jerome Powell press conference. The Fed is pretty much a lock to hold interest rates at their current level.

Posted on June 2, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Understanding the Difference

By Rick Kahler CFP®

Retirement planning is one of the issues that commonly lead clients to consult financial advisers.

One of its essential aspects is creating a plan to save and invest in order to provide a comfortable retirement income. Ideally, this starts many years ahead of retirement, even as early as your first paycheck.

As retirement comes closer, planning for it expands to take in a host of other considerations, such as deciding when to retire, where to live, and what kind of lifestyle you hope to have. When retirement becomes a reality, the focus shifts to carrying out the plan.

Preparing

All of this planning is crucial. Yet, for both financial advisers and clients, it’s good to keep in mind that planning has its limits. In the post-retirement years, it may be helpful to think in terms of preparing for old age rather than planning for it.

The older we get, the more important this distinction between planning and preparing becomes. Too many life-changing things can happen without regard to our best-laid plans. Often they occur unexpectedly, resulting in emergency situations where urgent decisions have to be made. A stroke or a fall, a diagnosis of terminal illness, a broken hip that leaves someone unable to go back to independent living—and suddenly, right now, the family needs to find an assisted living facility, arrange for live-in help, or sell a home.

What are some of the ways to prepare for these contingencies?

Explore housing options well ahead of time. Find out what assisted living, home care, and nursing home services and facilities are available where you live and whether they have waiting lists. Have family conversations about possibilities like relocating or sharing households:

Research the financial side of these options. Investigate the cost of hiring help at home, assisted living facilities, and nursing care centers. Find out what is and is not covered by Medicare and long-term care insurance. For example, people are sometimes surprised to learn that Medicare does not pay for nursing home care other than short-term medical stays.

Designate someone to take over decision-making, and do the paperwork. Execute documents like a living will, medical power of attorney, and contingent power of attorney. Update them as necessary, and give copies to your doctors, your financial planner, and appropriate family members.

Start relatively early to downsize. Well before you’re ready to let go of possessions or move into smaller housing, start considering what to do with your “stuff.” Focus on the decisions rather than the distribution. There’s no need to get rid of possessions prematurely, but decide what you want to do with them—and put in writing. Do this while it’s still your choice, rather than something your family members do while you’re in the hospital or nursing home

Do your best to practice flexibility and acceptance. No matter how strongly you want to live in your own home until the end of your life, for example, it may not be possible. The physical limitations of aging can limit our choices, and even the best options available may not be what we would like them to be. It is a profound gift to yourself and your family members to accept these realities with as much grace as you can muster.

***

***

Assessment

Finally, please don’t underestimate the importance of planning financially for retirement. Because the bottom line is that you can’t plan for all the things that might happen as you age, but you can prepare to deal with them. One of the most useful tools to cope with those contingencies is having enough money.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on May 30, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

WHAT IS THE “MEDICARE COST CONTROL EFFICIENCY” PARADOX?

The 800 Pound Gorilla in the Medical Treatment Room

By Staff Reporters

Blogger Ezra Klein opined more than a decade ago that one of the dirty little secrets of the health-care system is that Medicare has done a much better job controlling costs than private health insurers. It is a paradox!

DEFINITION: A paradox is a seemingly absurd or self-contradictory statement or proposition that when investigated may prove to be well founded or true.

***

***

QUERY:But, what about Medicare, cost control efficiency, today?

Posted on May 9, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

It’s the first anniversary of the Medicaid unwinding for many states, a process that kicked off when federal rules that had kept people on Medicaid and the Children’s Health Insurance Program (CHIP) through the pandemic expired. And while states could redetermine eligibility again, things have “unwound” more than some experts predicted. Children were kicked off the rolls at higher rates than adults, according to a new study the Urban Institute released May 2. Twelve states—Montana, Iowa, South Dakota, Alabama, Idaho, Georgia, Texas, Arkansas, Oklahoma, Florida, Mississippi, Colorado—exceeded 100% of their total projections for disenrolling children.

The S&P 500® index (SPX) was little changed at 5,187.67; the Dow Jones Industrial Average gained 172.13 points (0.4%) to 39,056.39; the NASDAQ Composite® ($COMP) declined 29.80 points (0.2%) to 16,302.76.

The 10-year Treasury note yield (TNX) rose more than 3 basis points to 4.496%.

The CBOE Volatility Index® (VIX) fell 0.23 to 13.00.

Retail and real estate shares were among the weakest areas Wednesday, while banks and utilities were firm. Utility shares extended a nearly month-long rally, which may in part reflect greater expectations for Fed rate cuts. Lower interest rates can make utility shares with high dividend yields relative to Treasuries more appealing. The Dow Jones Utility Average ($DJU) rose 0.5% to end at its highest level since late July and is up 12% from a mid-April low.

And, Shopify’s value plunged by nearly $20 billion after the online payments company released a gloomy forecast for this quarter. It’s the latest pandemic darling to stumble: According to the Financial Times, the firms that skyrocketed during lockdowns have lost a collective $1.5 trillion in value since the end of 2020.

Steward Health Care System, the largest U.S. physician-owned hospital operator, is expected to file for chapter 11 bankruptcy as soon as Sunday, according to a WSJ report, which cited people familiar with the matter. Steward Health Care is the largest tenant of Medical Properties Trust (NYSE: MPW). Steward Health Care hired restructuring advisers to improve its liquidity and restore its balance sheet in January 2024.

Posted on May 3, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd CMP

***

***

Medicare [Dis] Advantage Plans [Medicare Part C] commenced in 2003 or so and I have railed against them since then. First, for their low physician payments. And then as a patient advocate for the last decade. And, today, for both reasons. As a doctor and independent health insurance agent myself, believe me when I speak thusly.

Now, while Medicare Advantage plans are undoubtedly not the right choice for everyone, insurance companies still say there are some folks who will get exactly what they need from the plans and at a moderate price.

Nevertheless, Ernesto Jaboneta, the IT Director of California-based Medicare insurance agency Agent Pitstop, acknowledged there are many predatory salespeople who will jump to have you join a plan that doesn’t end up helping you in the long run. Still, there are precautions you can take to make falling into this trap less likely.

“The first thing anyone can do is invite along a family member or trusted friend to any appointments with an insurance agent,” Jaboneta told Newsweek. “Don’t feel pressured to decide right away.”

Before you commit to anything, you should compare plans and find out if your doctors will remain in your network. And if you’re unsure about some of the information you received from an insurance agent, you can also call 1-800-MEDICARE for more assistance.

Jaboneta also said there’s a big difference between captive insurance agents and independent agents, as well, and seniors should take note of this.

“A captive agent is an insurance agent who works directly for an insurance carrier,” Jaboneta said. “They have no incentive to compare options outside their own company, which is different than an independent agent who can compare all the options available. In many cases, when a beneficiary calls into an insurance company to find information, they will be talked into enrolling.”

The open enrollment period lasts from October 15th to December 8th, but there’s another enrollment period from January 1st to March 31st for anyone unhappy with their Medicare Advantage plan who wants to switch or revert to Medicare.

INVESTING UPDATE: Managed-care companies are reporting that seniors on Medicare Advantage Part C plans used far more medical services than expected in the final months of 2023. The announcements have sparked two separate selloffs over the past week: The first came January 12th, when UnitedHealth Group announced its fourth-quarter earnings. The second came after Humana just laid out preliminary fourth-quarter results, and said the high utilization trends would have a material impact on its 2024 performance “if current trends continue.”

Posted on April 30, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Humana Plans to Leave Some Medicare Advantage Markets in 2025

Humana expects to exit Medicare Advantage (MA) markets in 2025, company executives told investors. The company reported its first quarter earnings April 24th. Humana posted $741 million in net income in the first quarter of 2024, beating investor expectations, but pulled its 2025 earnings guidance.

On an April 24th 2024 call with investors, Humana executives said it will look to pull back benefits and exit some markets, as CMS continues phasing in risk adjustment changes. CMS published its final MA rate notice for 2025 earlier this month. The agency slightly cut benchmark payments and continued phasing in coding changes. Humana previously said the agency’s rates were lower than its expectations.

Other payers have signaled they will likely cut benefits to accommodate the rate notice.

You’ve got a sense of your ideal retirement age. And you’ve probably made certain plans based on that timeline. But what if you’re forced to retire sooner than you expect? Aging baby-boomers, corporate medicine, the medical practice great resignation and/or the pandemic, etc?

Early retirement is nothing new, but it’s clear how much the COVID-19 pandemic has affected an aging workforce. Whether due to downsizing, objections to vaccine mandates, concerns about exposure risks, other health issues, or the desire for more leisure time, the retired general population grew by 3.5 million over the past two years—compared to an annual average of 1 million between 2008 and 2019—according to the Pew Research Center.1 At the same time, a survey conducted by the National Institute on Retirement Security revealed that more than half of Americans are concerned that the COVID-19 pandemic has impacted their ability to achieve a secure retirement.2

***

***

There’s no need to panic, but those numbers make one thing clear, says Rob Williams, managing director of financial planning, retirement income, and wealth management for the Schwab Center for Financial Research. Flexible and personalized financial planning that addresses how you’d cope if you had to retire early can help you make the best use of all your resources.

So – Here are six steps to follow. We’ll use as an example a person who’s seeing if they could retire five years early, but the steps remain the same regardless of your individual time frame.

Step 1: Think strategically about pension and Social Security benefits

For most retirees, Social Security and (to a lesser degree) pensions are the two primary sources of regular income in retirement. You usually can collect these payments early—at age 62 for Social Security and sometimes as early as age 55 with a pension. However, taking benefits early will mean that you get smaller monthly benefits for the rest of your life. That can matter to your bottom line, even if you expect Social Security to be merely the icing on your retirement cake.

On the Social Security website, you can find a projection of what your benefits would be if you were pushed to claim them several years early. But if you’re part of a two-income couple, you may want to make an appointment at a Social Security office or with a financial professional to weigh the potential options.

For example, when you die, your spouse is eligible to receive your monthly benefit if it’s higher than his or her own. But if you claim your benefits early, thus receiving a reduced amount, you’re likewise limiting your spouse’s potential survivor benefit.

If you have a pension, your employer’s pension administrator can help estimate your monthly pension payments at various ages. Once you have these estimates, you’ll have a good idea of how much monthly income you can count on at any given point in time.

***

Step 2: Pressure-test your 401(k)

In addition to weighing different strategies to maximize your Social Security and/or pension, evaluate how much income you could potentially derive from your personal retirement savings—and there’s a silver lining here if you’re forced to retire early.

Rule of 55

Let’s say you leave your job at any time during or after the calendar year you turn 55 (or age 50 if you’re a public safety employee with a government defined-benefit plan). Under a little-known separation-of-service provision, often referred to as the “rule of 55,” you may be able take distributions (though some plans may allow only one lump-sum withdrawal) from your 401(k), 403(b), or other qualified retirement plan free of the usual 10% early-withdrawal penalties. However, be aware that you’ll still owe ordinary income taxes on the amount distributed.

This exception applies only to the plan (including any consolidated accounts) that you were contributing to when you separated from service. It does not extend to IRAs.

4% rule

There’s also a simple rule of thumb suggesting that if you spend 4% or less of your savings in your first year of retirement and then adjust for inflation each year following, your savings are likely to last for at least 30 years—given that you make no other changes to your withdrawals, such as a lump sum withdrawal for a one-time expense or a slight reduction in withdrawals during a down market.

To see how much monthly income you could count on if you retired as expected in five years, multiply your current savings by 4% and divide by 12. For example, $1 million x .04 = $40,000. Divide that by 12 to get $3,333 per month in year one of retirement. (Again, you could increase that amount with inflation each year thereafter.) Then do the same calculation based on your current savings to see how much you’d have to live on if you retired today. Keep in mind that your money will have to last five years longer in this instance.

Knowing the monthly amount your current savings can generate will give you a clearer sense of whether you’ll have a shortfall—and how large or small it might be. Use our retirement savings calculator to test different saving amounts and time frames.

Step 3: Don’t forget about health insurance, doctor!

Nobody wants to spend down a big chunk of their retirement savings on unanticipated healthcare costs in the years between early retirement and Medicare eligibility at age 65. If you lose your employer-sponsored health insurance, you’ll want to find some coverage until you can apply for Medicare.

Your options may include continuing employer-sponsored coverage through COBRA, insurance enrollment through the Health Insurance Marketplace at HealthCare.gov, or joining your spouse’s health insurance plan. You may also find discounted coverage through organizations you belong to—for example, the AARP.

Step 4: Create a post-retirement budget

To make sure your retirement savings will cover your expenses, add up the monthly income you could get from pensions, Social Security, and your savings. Then, compare the total to your anticipated monthly expenses (including income taxes) if you were to retire five years early and are eligible, and choose to file, for Social Security and pension benefits earlier.

Take into account various life events and expenditures you may encounter. You may not pay off your mortgage by the date you’d planned. Your spouse might still be working (which can add income but also prolong certain expenses). Or your children might not be out of college yet.

You’re probably fine if you anticipate that your monthly expenses will be lower than your income. But if you think your expenses would be higher than your early-retirement income, some suggest that you take one or more of these measures:

Retire later; practice longer.

Save more now to fill some of the potential gap.

Trim your budget so there’s less of a gap down the road.

Consider options for medical consulting or part-time work—and begin to explore some of those opportunities now.

To the last point, finding a physician job later in life can be challenging, but certain employment agencies specialize in this area. If you can find work you like that covers a portion of your expenses, you’ll have the option of delaying Social Security and your company pension to get higher payments later—and you can avoid dipping into your retirement savings prematurely.

When you retire early, you have to walk a fine line with your portfolio’s asset allocation—investing aggressively enough that your money has the potential to grow over a long retirement, but also conservatively enough to minimize the chance of big losses, particularly at the outset.

“Risk management is especially important during the first few years of retirement or if you retire early,” Rob notes, because it can be difficult to bounce back from a loss when you’re drawing down income from your portfolio and reducing the overall number of shares you own.

To strike a balance between growth and security, start by making sure you have enough money stashed in relatively liquid, relatively stable investments—such as money market accounts, CDs, or high-quality short-term bonds—to cover at least a year or two of living expenses. Divide the rest of your portfolio among stocks, bonds, and other fixed-income investments. And don’t hesitate to seek professional help to arrive at the right mix.

Many people are unaccustomed to thinking about their expenses because they simply spend what they make when working, Rob says. But one of the most valuable decisions you can make about your life in retirement is to reevaluate where your money is going now.

This serves two aims. First, it’s a reality check on the spending plan you’ve envisioned for retirement, which may be idealized (e.g., “I’ll do all the home maintenance and repairs!”). Second, it enables you to adjust your spending habits ahead of schedule—whichever schedule you end up following. This gives you more control and potentially more income.

Step 6: Reevaluate your current spending

For example, if you’re not averse to downsizing, moving to a less expensive home could reduce your monthly mortgage, property tax, and insurance payments while freeing up equity that could also be invested to provide additional monthly income.

“When you are saving for retirement, time is on your side”. You lose that advantage when you’re forced to retire early, but having a backup plan that anticipates the possibility of an early retirement can make the unknowns you face a lot less daunting.

Posted on April 12, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Essay on the Eight-Hundred Pound Gorilla in the Medical Treatment Room

By Dr. David E. Marcinko MBA MEd CMP

[Editor-in-Chief]

According to economist Austin Frakt PhD, and others, there is a school of thought that says Congress is incapable of controlling costs in the Medicare and Medicaid System [CMS].

And, then there is the reality known by all practicing medical professionals regardless of specialty orientation or degree designation. That is to say, CMS really can control healthcare costs and with great ferocity and efficiency, and to non-public sectors as well …. PARADOXICAL?

On Getting What You Wish For

Blogger Ezra Klein opines that one of the dirty little secrets of the health-care system is that Medicare has done a much better job controlling costs than private health insurers.

Of course, we doctors know that the real problem is that Medicare seemingly [think Seinfeld’s character George Costanza] controls costs all too well; but not really. It is just that CMS pays doctors too little and thus it appears costs are controlled. What really is happening is that physician fees are being reduced carte’ blanche.

Nevertheless, and regardless of semantics, CMS will never control costs much more efficiently than private insurance companies or doctors will simply abandon Medicare for related payment models like direct reimbursement or concierge medicine. This is happening right now. Physicians, osteopaths and podiatrists etc, are opting out of Medicare in increasingly large numbers. In a world where there’s only Medicare and Medicare to control costs, doctors can either take the pay cut or stop seeing patients, and stop being doctors. “Taking what they are given – because they’re working for a livin.”

So sorry that this seems like a forehead-palm moment for Ezra, but not for healthcare practitioners or the ME-P!

Too Much Demand Elsewhere

And, as we see from other countries, many young bright folks want to be doctors, even if being a doctor doesn’t make one particularly wealthy [high demand and high eventual supply produces lower provider costs in the long term?]. Think medical tourism.

Not so much the case anymore in this country [lower demand and lower eventual supply produces higher reimbursement costs to the doctor survivors in the very long term?].

Our Domestic World

But, we are not elsewhere. In fact, in our present domestic healthcare ecosystem, when Medicare decides to control costs, many doctors can simply stop accepting Medicare patients, and the politicians will lose their jobs. One political party then declares that Medicare is rationing and will hurt senior citizens. The other party capitulates and pays MDs more [SGR]. Then, the federal budget looks bad as it does now. The circle is complete when one party asserts that Medicare actually can’t contain costs but the private insurance companies will. It all fails, in an unending circular Boolean-like loop of illogic.

Listen Up!

So, listen up AARP, politicians, CMS and seniors as I admonish you to be careful what you wish for [medical cost controls]. It might just come true. As Ezra rightly says; rinse, repeat – rinse, repeat – ad nausea. You simply can’t have it both ways. You either choose to spend less and offend certain cohorts, or spend more and offend different factions. Either way, you’re going to piss someone off. A good healthcare reimbursement system would try to make that decision rationally [a-politically]. But, at least it would make an economics driven decision; wouldn’t it?

Assessment

Is CMS really the eight hundred pound cost-controlled gorilla in the increasingly large Medicare treatment room? Why or why not? Now, relative to the ACA of 2010, please read: The Case for Public Plan Choice in National Health Reform [Key to Cost Control and Quality Coverage], by Jacob S. Hacker, PhD. Link:Jacob Hacker Public Plan Choice

Conclusion

And so, your thoughts and comments on this ME-P are appreciated. Do we have a Medicare cost control efficiency paradox? Or, are the economists just reveling in the publication banal? Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

Subscribe Now: Did you like this Medical Executive-Post, or find it helpful, interesting and informative? Want to get the latest ME-Ps delivered to your email box each morning? Just subscribe using the link below. You can unsubscribe at any time. Security is assured.

Sponsors Welcomed: And, credible sponsors and like-minded advertisers are always welcomed.

Posted on April 3, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Medicare Part C papers, glasses and stethoscope.

***

Humana and other managed-care stocks were down sharply in trading Tuesday after the Centers for Medicare and Medicaid Services announced an average 3.7% increase in revenue for Medicare Advantage plans in 2025. That amount is the same as the proposed increase the government had announced in January, but it came as a shock to investors who were hoping for a slight bump.

Humana (HUM) shares fell sharply in early Tuesday trading, while rivals UnitedHealth UNH and CVS Health (CVS) traded firmly in the red, as the health insurance industry received yet another blow to its 2024 profit forecasts. All three major health insurance groups have trailed the broader market this year, with Humana down nearly 25%, amid concern that profit margins will be hit by a surge in medical costs tied to a rise in elective procedures. Those procedures had been delayed by the Covid pandemic.

The S&P 500 index fell 37.96 points (0.7%) to 5,205.81; the Dow Jones Industrial Average lost 396.61 points (1.0%) to 39,170.24; the NASDAQ Composite slipped 156.38 points (1.0%) to 16,240.45.

The 10-year Treasury note yield was up almost 3 basis points to 4.357%.

The CBOE Volatility Index® (VIX) rose 0.96 to 14.61.

Retailer, biotechnology, and regional bank shares were among the weakest performers Tuesday, leading a broad market slump in which declining stocks outnumber advancers by a greater than three-to-one ratio. The small-cap Russell 2000® Index (RUT) lost 1.8% and settled at a two-week low.

Energy companies, by contrast, extended recent strength behind an ongoing climb in WTI Crude Oil (/CL) futures, which surpassed $85 per barrel for the first time since late October. The Philadelphia Oil Service Index (OSX) advanced 2.1% and ended at a 5-½-month high. Oil prices have surged this year due to OPEC production cuts and concern over supply disruptions stemming from the Middle East conflict.

Posted on April 3, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

PATIENT COMPLICATION RATES

By Staff Reporters

***

***

Hospitals under private equity (PE) ownership reported higher rates of patient complications when compared to other facilities, according to a recent JAMA study—raising questions about how the business model might affect staffing and subsequent quality of care.

The surveyed Medicare beneficiaries saw a 25.4% increase in “hospital-acquired conditions,” which the Centers for Medicare and Medicaid Services defines as falls, infections, and other adverse events, when they received treatment at a PE-acquired hospital compared to those run under other forms of ownership.

On the whole, the study found that Medicare enrollees at hospitals under PE control were not only younger and less likely to additionally qualify for Medicaid but also more likely to experience complications.

Posted on April 2, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Federal health officials said they would offer emergency funding to physicians, physical therapists, and other professionals that provide outpatient healthcare, following a cyberattack that crippled the nation’s largest processor of medical claims and left many organizations in financial distress. The Centers for Medicare and Medicaid Services also announced that it would make advance payments available to suppliers that bill through Medicare Part B, which serves a wide array of healthcare organizations.

***

***

Officials had previously announced a similar program to make emergency payments available for hospitals that had been ensnared by the February 21st hack of Change Healthcare, a unit of UnitedHealth Group, and have struggled to get paid for more than two weeks. The emergency funds represent upfront payments made to healthcare providers and suppliers based on their expected future claims.

Posted on April 1, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

On March 9th, 2024, President Biden signed into law a $460 billion spending package to continue funding the federal government for the remainder of the 2024 fiscal year. Contained within the spending package was legislation to cut in half the 2024 Medicare physician payment update of approximately -3.4%.

This Health Capital Topics article discusses the payment update, other healthcare provisions contained in the bipartisan spending bills, and responses from stakeholders. (Read more…)

The producer price index (PPI) rose 0.6% for the month, according to the Bureau of Labor Statistics—double the Dow Jones estimate, CNBC reported. February’s larger-than-expected PPI uptick follows a more modest 0.3% increase in January and a 0.1% decline in December. On an annual basis, the PPI increased 1.6%, “the largest rise since moving up 1.8% for the 12 months ended September 2023,” according to the BLS.

The market had a good Tuesday, with stocks climbing as investors await word from the Fed meeting today on any changes to interest rates. The bank is expected to keep rates the same for now, but could signal when (or how often) it’ll lower them later in the year. Meanwhile, Nordstrom shares surged following a report that the retailer’s founding family wants to take it private.

The S&P 500 index added 29.09 points (0.6%) to 5,178.51; the Dow Jones Industrial Average® ($DJI) gained 320.33 points (0.8%) to 39,110.76; the NASDAQ Composite® ($COMP) rose 63.34 points (0.40%) to 16,166.79.

The 10-year Treasury note yield (TNX) eased four basis points to just under 4.3%.

The CBOE Volatility Index® (VIX) lost 0.50 to 13.83.

The energy sector was the top performer after crude oil prices notched multi-month highs ahead of weekly inventory data from the American Petroleum Institute. After a 2% rally to start the trading week, Brent Crude Oil (/BZ) futures, the global benchmark, added another 0.6% Tuesday.

Industrials, consumer discretionary, and utilities were among the other strong sectors. Communications, real estate, and materials finished modestly lower.

Posted on February 13, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

HAPPY MARDI GRAS

By Staff Reporters

***

***

In welcome news for physicians, a bipartisan group of senators will get to work on Medicare payment reform. The lawmakers plan to propose changes to the physician fee schedule and updates to the 2015 MACRA law.

***

Stat: $3+ billion. That’s how much restitution New York State Attorney General Letitia James is now seeking from Digital Currency Group, Genesis Global Capital, and Gemini, the crypto exchange run by the Winklevoss twins, for allegedly defrauding more than 230,000 investors, after initially suing in October (CNBC).

The S&P 500 index fell 4.77 points (0.1%) to 5,021.84; the Dow Jones Industrial Average gained 125.69 points (0.3%) to 38,797.38; the NASDAQ Composite lost 48.12 points (0.3%) to 15,942.55.

The 10-year Treasury note yield (TNX) dropped more than 1 basis point to 4.173%.

The CBOE Volatility Index® (VIX) rose 1.00 to 13.93.

Despite the mixed performance of large-cap stock indexes, several other market sectors got off to a strong start this week. Banking and retail were among the strongest performers, and the small-cap Russell 2000® Index (RUT) surged 1.8% to end at its highest level since late December.

Tech shares erased early gains, with the Philadelphia Semiconductor Index (SOX) fading to a 0.2% loss after earlier rising to a record intra-day high.

Peterson noted shares of many semiconductor companies are well into technically overbought territory, which often can lead to sharp pullbacks, though the timing of such a move is difficult to pinpoint. He cited unusually elevated Relative Strength Index (RSI) readings, at 90-plus, for two AI darlings: Arm Holdings (ARM) and Super Micro Computer (SMCI).

Posted on January 27, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

American Medical Association (AMA) leaders lauded the Medicare Payment Advisory Commission (MedPAC) this month for backing increased physician payment rates for 2025.

AMA President Jesse Ehrenfeld praised MedPAC, a nonpartisan independent legislative agency that advises Congress on the Medicare program, for endorsing a draft recommendation that urges lawmakers to increase physician payment rates to reflect inflation. He cast the move as “a critical first step toward the necessary work of reforming the broken Medicare payment system.”

“Long-term reforms from Congress are overdue to close the unsustainable gap between what Medicare pays physicians and the actual costs of delivering high-quality care. When adjusted for inflation in practice costs, Medicare physician pay declined 26% from 2001 to 2023,” he said in a statement.

Posted on January 24, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Theranos founder and ex-CEO Elizabeth Holmes was just banned from US federal health care programs for nine decades, according to the US the health department. Holmes was sentenced in November 2022 to 11 years in prison following a trial that determined she knew her blood-testing startup, which was founded in 2003 and which claimed to be able to test for a range of diseases and risks with one finger prick, produced inaccurate and faulty results. Before government probes, Theranos raised hundreds of millions of dollars, named prominent former U.S. officials to its board, and explored a partnership with the U.S. military to use its tests on the battlefield.

So, just what is a Federal Health Care Program?

Federal Health Care Program means any plan or program that provides health benefits, whether directly, through insurance, or otherwise, which is funded directly, in whole or in part, by the United States Government, including, but not limited to, Medicare, Medicaid/MediCal, managed Medicare/Medicaid/MediCal, TriCare/VA/CHAMPUS, SCHIP, Federal Employees Health Benefit Plan, Indian Health Services, Health Services for Peace Corp Volunteers, Railroad Retirement Benefits Black Lung Program, Services Provided to Federal Prisoners, and Pre- Existing Condition Insurance Plans (PCIPs).

Posted on January 19, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Statistic 187,000: That’s how many first time unemployment claims were filed last week, a surprise decline and the lowest since September 2022. The resilient labor market is continuing to chug along as companies continue to hold on to the workers they have.

***

Managed-care companies are reporting that seniors on Medicare Advantage Part C plans used far more medical services than expected in the final months of 2023. The announcements have sparked two separate selloffs over the past week: The first came January 12th, when UnitedHealth Group announced its fourth-quarter earnings. The second came Thursday, after Humana laid out preliminary fourth-quarter results, and said the high utilization trends would have a material impact on its 2024 performance “if current trends continue.”

In response, three largest sponsors of Medicare Advantage plans, UnitedHealth Group, CVS Health, and Humana, have seen their shares fall 3.2%, 7.5%, and 14.3% so far this year, respectively, as of midday Thursday. The S&P 500 is down 0.6% over the same period, while Cigna Group—which is reportedly near a deal to sell its relatively small Medicare Advantage business—is up 1%.

***

Here’s where the major benchmarks ended:

The S&P 500 index rose 41.73 points (0.9%) to 4,780.94; the Dow Jones Industrial Average® (DJI) gained 201.94 points (0.5%) to 37,468.61; the NASDAQ Composite increased 200.03 points (1.4%) to 15,055.65.

The 10-year Treasury note yield (TNX) rose nearly 4 basis points to 4.142%.

The CBOE Volatility Index® (VIX) fell 0.66 to 14.13.

Gains in Taiwan Semiconductor and its industry counterparts sent the Philadelphia Semiconductor Index (SOX) up 3.4% to a three-week high. In a further illustration of tech sector strength, the Nasdaq-100® (NXD), which includes the NASDAQ’s largest non-financial companies, rose 1.5% to a record closing high. Banking and utility shares were among the market’s weakest performers.

Posted on December 26, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

On December 13, 2023, the Centers for Medicare & Medicaid Services (CMS) released its annual report on healthcare spending in the U.S., highlighting the growth in private insurance and Medicaid spending in 2022, which was offset by the declines in supplemental federal funding as a result of the COVID-19 pandemic.

The final FOMC meeting of the year will take place this week, and like most work meetings in mid-December, not a whole lot is going to happen. Chair Jerome Powell is widely expected to leave interest rates unchanged as inflation continues its descent to a 2% target. But 2024 planning is in full swing, and investors are desperate to learn when the Federal Reserve thinks it will need to cut rates next year.

***

Here is where the major stock index benchmarks ended:

The S&P 500 index was up 18.07 points (0.4%) at 4,622.44; the Dow Jones Industrial Average® (DJI) was up 157.06 points (0.4%) at 36,404.93; the NASDAQ Composite was up 28.51 points (0.2%) at 14,432.49.

The 10-year Treasury note yield (TNX) was little-changed at 4.239%.

The CBOE® Volatility Index (VIX) was up 0.28 at 12.63.

In addition to retailers, semiconductor company shares also posted outsized gains Monday, boosted in part by a jump of nearly 10% in Broadcom (AVGO). The Philadelphia Semiconductor Index (SOX) gained more than 3% and ended near a two-year high. Transportation companies were also strong.

In other markets, Natural Gas futures (/NG) plunged more than 6% to a six-month low, reflecting warmer-than-normal U.S. temperatures and excess supplies.

Finally, the so-called Magnificent Seven stocks of Apple, Microsoft, Alphabet, Amazon.com, Nvidia, Tesla and Meta Platforms each fell at least 0.8%. Meta led the declines, dropping 2.2%. But only one out of 11 S&P 500 sectors fell. Even the information technology sub-index ticked higher, reflecting gains outside of the largest companies in the sector.

Apple regains a $3 trillion market cap and is on track to end the year as the world’s most valuable company for the 5th time in a row.

Today marks the 82nd anniversary of the attack on Pearl Harbor that drew the US into WWII.

Here’s where the major benchmarks ended:

The S&P 500® index (SPX) was down 17.84 points (0.4%) at 4,549.34; the Dow Jones Industrial Average® (DJI) was down 70.13 points (0.2%) at 36,054.43; the NASDAQ Composite® (COMP) was down 83.20 points (0.6%) at 14,146.71.

The 10-year Treasury note yield (TNX) was down about 5 basis points at 4.117%.

The CBOE® Volatility Index (VIX) was up 0.10 at 12.95.