BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on September 26, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

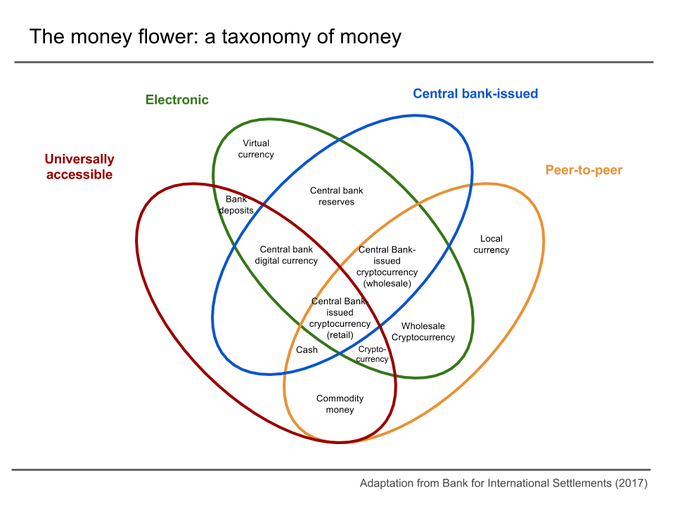

Belgium’s Society for Worldwide InterBank Financial Telecommunications

A TIMELY FINANCIAL TOPIC

***

By Staff Reporters

***

Belgium’s Society for Worldwide Interbank Financial Telecommunications (SWIFT) runs a messaging service that facilitates transactions across 11,000+ financial institutions globally. Think of it as the “Gmail of global banking.”

Entities in every country except North Korea use SWIFT to shuffle trillions of dollars’ worth of funds across borders. And Russia is a SWIFT power user—as a major supplier of energy and other goods, it ranks sixth globally for payment messages sent on SWIFT. So if Russia were cut off from SWIFT, “the nation would essentially be severed from much of the global financial system,” the NYT wrote.

Posted on September 8, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

Welcome to The Common Bridge

By Richard Helppie

***

Hello, welcome to the Common Bridge.

We’ve got a great topic for you today. It’s all about taxes and the IRS and with us today, two experts from Plante Moran. Welcome, Rachel Keller and Brett Bissonnette, welcome to the Common Bridge. The Common Bridge, of course, is available@substack.com. Please go to substack.com. Enter the Common Bridge in your search engine. Subscribe if you wish, either a paid subscription or a free subscription.

Of course, the Common Bridge is available on all of your podcast outlets. Look for us there and on YouTube TV. And of course, with our friends over at Mission Control radio on your radio garden app. We all listen to debates and commentary about law and policy and especially taxes. And every law, every policy and of course tax regulation require mechanisms to ensure compliance.

Well, our President Joseph R. Biden has stated that the IRS needs to be properly funded in order to carry out its mission on our very complex tax code. Taxpayers have been puzzled by missing records, slow refund late fees for things they paid and other matters including slowness in the support that they get directly from the IRS. So today, we’re going to chat with these two experts who are in the field today actively advising people from all stripes about tax law and tax regulation. They spent a lot of their time interacting with the IRS and making sure that their clients are in compliance with the tax law. So we anticipate some education and maybe some policy ideas.

From Plante Moran, we welcome Rachel Keller and Brett Bissonnette — Welcome to the Common Bridge.

-Richard Helppie

EDITOR’S NOTE: Richard D. Helppie Former: CEO and Founder Superior Consultant Company, Inc. [SUPC-NASD]

Posted on August 15, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Stephen Kelley, CSA

***

***

As a Registered Investment Adviser (RIA) with a Series #65 securities license, we hold a fiduciary duty to you. This means that we are legally bound to put your interests above those of anyone else, including ourselves.

Now you might reasonably think that anyone offering financial advice or services to clients is required to be a fiduciary. Sadly, if you thought that, you’d be wrong. Some estimates claim that only 15 percent of advisors have a fiduciary duty to their clients. The Paladin Registry puts the number even lower, estimating that just one in 12 (8.3 percent) advisors have a fiduciary responsibility.

For the most part, stockbrokers (also called “Registered Representatives,” “Account Executives,” “Financial Advisors,” or “Wealth Managers”) are not fiduciaries, even though they are allowed to portray themselves as full-service investment advisors. If your stockbroker/registered representative/account executive/financial advisor/wealth manager holds a series seven [#7] securities license, then it’s probable that they aren’t a fiduciary.

This was made amply clear in the movie, “The Wolf of Wall Street,” a biopic about Jordan Belfort, a stockbroker who made his fortune selling junk stocks and bonds to middle-class investors: in other words, by cheating them. Much of it was perfectly legal. The SEC went after Belfort’s company, Stratton Oakmont, for nearly a decade before it was able to shut it down. The point being that even in the face of egregious wrongdoing, theft, fraud and a virtual sea of drugs and blatant hedonism, the securities laws in this country are so loose that it took billions in theft and a decade of suspected and known fraud to step in and stop the abuse. And this movie was based on a true story.

That’s why a fiduciary duty is so important to a client. Being a fiduciary is a legal distinction. A Registered Investment Advisor (RIA) or Investment Advisor Representative (IAR) who holds a Series #65 securities license, subject to the Investment Advisers Act of 1940, is a fiduciary. The legal investment advising standards that govern a non-fiduciary stockbroker and a fiduciary Registered Investment Advisor are very different.

A Registered Investment Advisor is legally required to follow the “trust” standard — the highest known in law — which requires it to place the interests of its clients ahead of its own and fulfill critical fiduciary duties of trust and confidence. Under the fiduciary trust standard, a Registered Investment Advisor must provide its “best advice” to a client. A non-fiduciary stockbroker (like the coveted Series #7 of “The Wolf of Wall Street”) follows only the “suitability” standard, which doesn’t require a stockbroker to place the interests of his clients ahead of its own. Under the non-fiduciary suitability standard, a stockbroker need provide only “suitable advice” to his clients — even if the stockbroker knows that the advice is not the best advice for the client.

***

The table below helps summarize which professionals are fiduciaries.

Posted on August 10, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Charles Schwab

***

***

Stay alert for investment scams involving cryptocurrency

At Schwab, we’re committed to helping you protect your assets. One way we do that is by raising awareness of the increase in fraudulent investment schemes (“scams”) involving cryptocurrencies and digital assets. While investing involves taking some risks, being scammed shouldn’t be one of them.

What do scams look like? Investment scams target investors by promising quick, guaranteed returns. Although “investment pitches” vary, using fraudulent cryptocurrency investment opportunities to entice targets is a common approach.

Once targeted investors indicate interest, they are often instructed to wire funds abroad or to a third party’s personal account, or to transfer cryptocurrency. Fake websites and/or applications often create the illusion of a legitimate trading or investment platform and gain trust. However, once funds have been transferred, they are difficult to trace and retrieve.

5 Investment Scam Red Flags

• Guaranteed” high investment returns, supposedly with little or no risk, and sounding too good to be true. • Unlicensed or unregistered sellers. Use Investor.gov to check out the background of anyone offering you an investment in securities. • Skyrocketing account values. Investments that appear to rapidly increase in value are often fake. • Fake testimonials. Scammers often pay people to provide fake reviews, so never rely solely on testimonials in making an investment decision. • Fake contacts. Take caution if someone approaches you through social media with an investment opportunity. Pretending to be a friend or to have a mutual acquaintance is a common tactic used to gain trust.

Posted on August 10, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The US Senate passed their climate, health and tax package, including nearly $80 billion in funding for the IRS.

The Inflation Reduction Act allocates $79.6 billion to the agency over the next 10 years, with more than half of the money going to enforcement, with the IRS aiming to collect more from corporate and high-net-worth tax dodgers.

The remainder of the funding is earmarked for operations, taxpayer services, technology, development of a direct free e-file system and more. Collectively, those improvements are projected to bring in $203.7 billion in revenue from 2022 to 2031, according to recent estimates from the Congressional Budget Office.

The biggest revenue-raiser of the IRA is a 15% minimum tax on corporations with profits of $1 billion or more, which is expected to generate $258 billion over 10 years. This addresses the problem of the rampant tax dodging among large companies that has mostly benefited wealthy shareholders and executives. The bill includes a 1% excise tax on companies’ stock buybacks, raising an estimated additional $74 billion. This will discourage corporations from siphoning resources into share repurchases that largely benefit shareholders and executives with stock-based pay. Those resources could instead go toward worker wages or other productive investments. And the bill would boost IRS enforcement to ensure the ultra-rich pay.

Finally, the Inflation Reduction Act would also extend a tax limitation on pass-through businesses for two more years. The limitation on how businesses can use losses to reduce taxes is supposed to expire at the start of 2027. A pass-through or flow-through business is one that reports its income on the tax returns of its owners. That income is taxed at their individual income tax rates. Examples of pass-throughs include sole proprietorships, some limited liability companies, partnerships and S-corporations.

Posted on August 3, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Claire

***

***

While the Inflation Reduction Act of 2022 looks good on paper, it will actually do more harm than good if it passes. The plan would hurt working-class taxpayers and small business owners across the country.

Posted on August 1, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

According to founder and real estate investing company CARROLL, his company has raised rents up to 30% over the past year. Of course, costs are going up as well. “So as our costs go up — our costs of interest, our costs of renovations, our cost of our employees,” Carroll told Fox Business. “We need to push those increases along through rent increase.” Because of rising property prices, renting has become the only option for a lot of people. “We are seeing a supply-demand imbalance,” he adds. “And now they have a lack of buyers because of mortgage rates. So, again, this has all kind of been a perfect storm for the multifamily business.” While it’s hard to say whether rent increases are sustainable, Carroll says that his company’s occupancy rates are at all-time high.

The stock market could be gearing up for new record highs before year-end as the 2022 bear market is over, Fundstrat’s Tom Lee just said. The biggest takeaway for me on events of this week? Convincing and arguably decisive evidence the ‘bottom is in’ — the 2022 bear market is over.” Lee’s confidence stems from the fact that between a negative GDP print, another 75-basis-point interest rate hike from the Fed, and more natural gas volatility due to Russia’s Nord Stream pipeline drama, a lot of bad news occurred this week and yet the S&P 500 and Nasdaq 100 managed to stage a 3% rally. “When bad news doesn’t take down markets, it is time for investors to assess.” In fact, despite a strong US dollar and heightened economic uncertainty, companies are reporting better-than-feared results. With 52% of the S&P 500 having reported second-quarter earnings already, 73% beat profit estimates by a median 7%.

***

Meanwhile, investors will be closely monitoring July’s Nonfarm Payrolls print, with analysts estimating a slowdown in hiring, forecasting the addition of 250K jobs which would be the lowest since December of 2020, while the unemployment rate is expected to hold steady at 3.6%. Other important economic data include final S&P Global PMIs, ISM Manufacturing and Non-Manufacturing PMIs, exports, imports, JOLTS job openings, construction spending and factory orders. Finally, the earnings season continues with a slew of major companies reporting quarterly results, including Eli Lilly and Company (NYSE:LLY), Gilead Sciences Inc (NASDAQ:GILD), Uber Technologies Inc (NYSE:UBER), Caterpillar Inc (NYSE:CAT) and Amgen Inc (NASDAQ:AMGN).

Finally, Bitcoin gained 19% since the beginning of July, which caused the crypto’s Relative Strength Index to correct from 29% on July 1 to the 60% level as of press time. The momentum coming back into Bitcoin has caused the fear and green index measurement to improve slightly from “extreme fear” in June, measuring in at 11, to “fear” in July, measuring in at 39.

Posted on July 31, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Although the future of Social Security remains in doubt, some congressional lawmakers are ensuring that most Social Security recipients get their money and then some. Sen. Bernie Sanders (I-Vt.) introduced the Social Security Expansion Act (SSEA) in June. The bill would allot $200 more per month for each Social Security recipient — a 12% boost in money, according to CBS News.

So who will receive these Social Security increases?

The people who are currently eligible for Social Security or anyone who turns 62 in 2023, which is the earliest age to collect Social Security, will be eligible to receive the extra $200 a month with their benefits.

***

Now, at present for Social Security, 12.4% is taken out of each paycheck for people earning up to $147,000, with half paid by the employer and half paid by the worker. So, if you make $147,000 or less, you are paying 6.2% into Social Security. If you make, say, $1.47 million, you only pay 0.6% of your income to Social Security.

If the pending new SS bill is approved, the same rate would be taxed on individuals making $250,000 or more. Those making $147,000 or less would continue to pay the same rate as well, with a do-nut hole between the $147,000 and $250,000 — although that $147,000 typically goes up each year, as it is based on average income.

The increased funding — along with a change in the cost-of-living-adjustments (COLA) to the Consumer Price Index for the Elderly (CPI-E) — would help to increase benefits by an estimated $200 per month, or $2,400 per year, which bears out, according to an analysis by the Social Security Administration (SSA).

Posted on July 28, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Eric Bricker MD

Healthcare Stock and IPO Investing Can Be Confusing. The Story of Privia Health is a Good Case Study in Understanding the Underlying Economics in Healthcare Investing:

Posted on July 26, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

By Staff Reporters

***

***

The $7.25 federal minimum wage is now 13 years old after last being raised in July 2009. The value of the minimum wage has fallen by 40% since the 1960s. And, $7.25 in July 2009 would be worth around $10 now after adjusting for inflation.

In the next jobs report, Turn predicted that the unemployment rate will fall to a seasonal low of 3.5% due to a 64.7% increase in hiring in June, a trend that could continue through July. Turn predicted a significant shift away from filling hourly, pandemic-related jobs, such as warehouse positions, after hiring for traditional economic roles likes retail workers and janitorial services surged 210% in June. Turn also predicted a rise in hiring for semi-skilled hourly and salaried jobs in July such as mechanics and nurses. While hiring for these positions accounted for just 11.5% of monthly jobs over the past 12 months, Turn predicted that these jobs will make up 22% of all new hires in July.

AT&T Inc. and Verizon Communications Inc. shocked investors with their second-quarter results last week — the former warning about the high cost of phone giveaways and the latter failing to meet growth targets. The news sparked a sell-off that erased some $40 billion in market value from the three industry leaders. Now T-Mobile US Inc. is cast as the potential Goldilocks in this drama — if its second-quarter results are just right. T-Mobile reports financial results tomorrow before markets open. Investors will be eager to see if the wireless industry is starting to see a slowdown in consumer spending due to decade-high inflation, or if some of the troubles might be more self inflicted.

Posted on July 24, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The World Health Organization declared the outbreak of monkeypox to be a public health emergency of international concern. “The global monkeypox outbreak represents a public health emergency of international concern,” WHO Director-General Dr. Tedros Adhanom Ghebreyesus said during a briefing in Geneva. At the virtual press conference, Ghebreyesus also said that the outbreak has spread around the world “rapidly” and that officials understand “too little” about the disease.

And, the U.S. Dollar had an incredible run throughout 2022, appreciating against most major currencies as the world’s central banks continue to combat rising inflation. This year alone, the dollar is up 15% against the Japanese yen, 10% against the British pound, and 5% compared to China’s Renminbi. The Wall Street Journal’s Dollar Index, which measures the dollar against 16 other major currencies, has also had its best first half performance since 2010 this year, rising more than 10% year-to-date. And for the lucky Americans who could find cheap airfare to Europe (and made it through with all their luggage), the dollar even reached equal standing with the euro for the first time in two decades earlier this month.

Posted on July 22, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

By Staff Reporters

President Biden tested positive for the coronavirus, raising health concerns for the 79-year-old president and underscoring how the virus remains a persistent, if muted, threat in a country trying to put the pandemic in the past.

U.S. Indices

Change

Close

Dow Jones

+162.06

32036.90

NASDAQ

+161.96

12059.61

S&P500

+39.05

3998.95

SCHWAB1000

+129.50

13230.70

Senator Elizabeth Warren along with 22 more Democratic lawmakers are pushing the IRS to create its own free tax filing service. The bill also aims to allow eligible taxpayers to choose a “return-free option,” providing a pre-populated filing. “The average American spends 13 hours and $240 every year to file their taxes — that’s too much time and too much money,” Warren said in a press release. But some tax professionals say it’s not a realistic plan for the overburdened agency.

A case of polio has been identified in an un-vaccinated adult in Rockland County, according to a news release from the New York State Department of Health. The agency confirmed that the infection was transmitted from someone who received the oral polio vaccine, which has not been administered in the United States since 2000. Officials believe the virus may have originated outside the United States, where the oral vaccine is still administered.

he New York Times opinion columnist Paul Krugman published a mea culpa in column form flat out admitting he was wrong for thinking inflation wouldn’t be that bad. In his piece, titled, “I Was Wrong About Inflation,” the economics professor noted that he was on “Team Relaxed” when it came to fears of inflation and acknowledged that was a “very bad call.” Krugman began by recounting the “intense debate among economists about the likely consequences of the American Rescue Plan, the $1.9 trillion package enacted by a new Democratic president and a (barely) Democratic Congress.” He mentioned how he originally didn’t see the massive government spending bill as that dangerous for the economy. “Some warned that the package would be dangerously inflationary; others were fairly relaxed. I was Team Relaxed. As it turned out, of course, that was a very bad call,” he confessed.

Posted on June 19, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Healthcare Partnerships – 5 Takeaways

• This year had the largest percentage of announced “mega merger” transactions in the last six years at 16.3% and, in more than one out of every 10 transactions, the smaller partner had a credit rating of A- or higher in 2021. • Since 2011, average smaller partner size by annual revenue has increased at a compound annual growth rate (CAGR) of approximately 8.0%. • Transactions involving a not-for-profit partner represented 87% of announced transactions. • Transactions involving rural or urban/rural sellers increased to 31% of announced transactions.

Posted on June 11, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

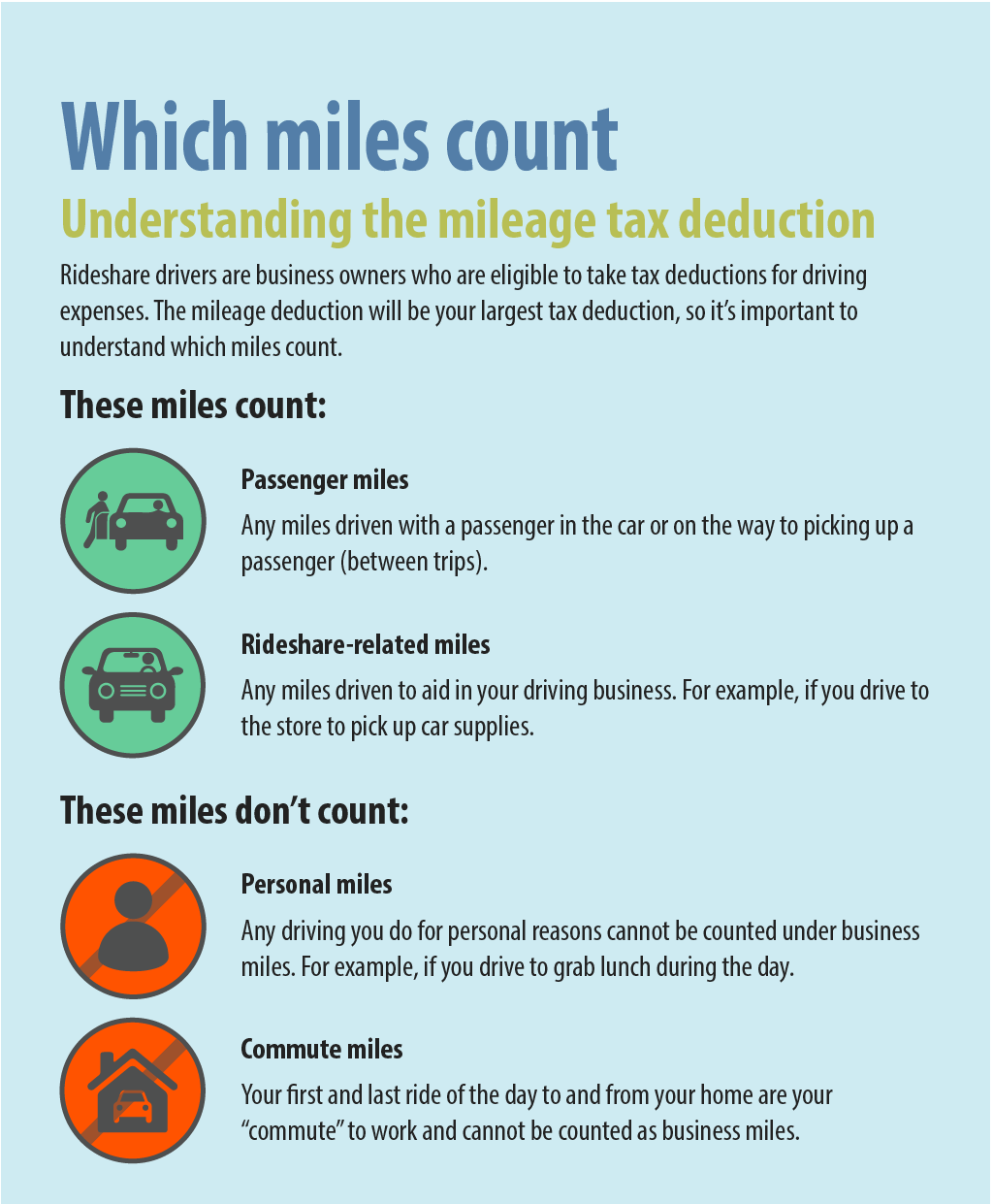

The federal tax deduction that businesses and self-employed taxpayers can use for their work-related miles on the road is suddenly getting more generous. The optional standard mileage rate for business-related driving is increasing to 62.5 cents a mile, starting in July, the Internal Revenue Service announced Thursday. That’s up from the 58.5-cents-a-mile rate first announced in December.

Rising inflation continues to frustrate consumers who are growing tired of shelling out more money. for example, Record gas prices helped push down the consumer sentiment index from 58.4 in May to 50.2 in June – the lowest recorded level since November 1952. The preliminary reading is comparable to the trough reached during the 1980 recession, according to Joanne Hsu, director of the university’s Surveys of Consumers. In May 1980, the sentiment reading hit 51.7, according to historical data. The final reading for June will be published on June 24th.

Markets: The S&P 500 is on the bear market watch list after a vicious sell-off yesterday capping off its worst week since January. Investors were disappointed by the inflation report that dropped Friday. Prices jumped 8.6% last month, which is a faster pace than in April and higher than expected. Rents, food, energy, and used cars all contributed to the price increases, putting even more pressure on the Fed to hike interest rates substantially throughout the summer and into the fall.

Posted on May 13, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

It’s Friday the 13th

***

***

The IRS destroyed data for an estimated 30 million filers in March 2021, according to the Treasury Inspector General for Tax Administration. The decision, prompted by a backlog of paper filings, has sparked anger in the tax community. “It just further damages the IRS’ reputation in the business community and in the public,” said Larry Harris, director of tax services at Parsec Financial.

More than $200 billion has been wiped off the cryptocurrency market today alone, as investors are sent into a panic. Ethereum, the world’s second largest digital currency plummeted by 20% in the space of 24 hours. Bitcoin, the original cryptocurrency started in 2009, dropped by 9%, but overall it is down 50% since its all time high in November. Chaos on the market has seen other currencies such as Shiba Inu and Dogecoin losing 30% and 25%, respectively. Meanwhile Terra Luna, which was among the top 10 most valuable cryptocurrencies had 98% of its value wiped out overnight, falling to below one dollar per coin.

Immediately after becoming the interim CEO of Starbucks (NASDAQ: SBUX), Howard Schultz suspended the company’s share-repurchase program. “This decision will allow us to invest more into our people and our stores — the only way to create long-term value for all stakeholders,” he said in a press release.

Snowflake, Meta, Microsoft and Uber — are all down from 20% to as much as 60% year to date. The technology stock sector, especially unprofitable firms and richly valued software names, have been hit the hardest as of late. The NASDAQ Composite slid more than 13% in April, dropping almost 30% from its all-time high.

President Biden, anticipating the milestone of one million American lives lost to Covid-19, said in a formal statement on Thursday that the United States must stay committed to fighting a virus that has “forever changed” the country.

Finally, Microsoft founder Bill Gatessaid on Tuesday that he tested positive for COVID-19 and is experiencing mild symptoms. In a series of tweets, the billionaire shared that he was “lucky to be vaccinated” and will be isolating until he’s healthy again.

Posted on April 15, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

TRIVIA QUESTION: What date has never been known as Tax Day?

A. March 1st B. March 15th C. April 15th D. May 1st

ANSWER: D—May 1st.

After the 16th Amendment cleared the way for the modern version of the federal income tax, the first filing deadline fell on March 1, 1913. Congress shifted Tax Day to March 15 after passing the Revenue Act of 1918, which introduced a progressive income tax structure to increase revenue during World War I. Since 1954, Tax Day for most Americans has been April 15 (or the next business day if the 15th falls on a weekend or holiday).

The term “step-up” refers to the difference in value and tax liability that an asset has when it is acquired and when it is transferred to an inheritor.

EXAMPLE #2: The proverbial millionaire Doctor Joe, for example, could buy a home for $350,000 and sell it for $1 million, after which he’d pay taxes on the $650,000 gain. But if Dr. Joe passes the home onto his daughter Ella, and she has it appraised at $1 million, its value has taken a “step up” in value to $1 million. If Ella sells the home for $1 million or less, she wouldn’t owe anything in taxes.

ASSESSMENT: For billionaires like Jeff Bezos, Bill Gates and Elon Musk who earn far more through their investments than their salaries, this loophole is a perfect way to shield their wealth. Intergenerational wealth has contributed to surging inequality in America, which grew wider during the pandemic. Since 2019, the wealth of the top 400 richest people in the US increased by $1.4 trillion, per research from Gabriel Zucman and Emmanuel Saez, a pair of left-leaning economists at the University of California, Berkeley.

“Often, for these people, wealth accumulates tax-free their entire lives,” Frank Clemente, executive director at the left-leaning advocacy group Americans for Tax Fairness, opined. President Joe Biden proposed ending this loophole and making billionaires “pay their fair share,” so why does it look like his party won’t touch it?

Posted on April 10, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

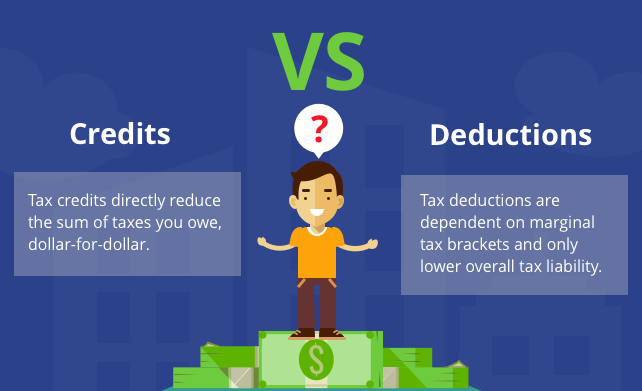

What is a tax deduction?

A deduction reduces the amount of income you pay taxes on, which means you could pay less in taxes. You subtract deductions from your income before calculating how much taxes you owe. How much a deduction saves you depends on your income tax bracket.

To calculate how much a deduction could reduce your taxes, you multiply the amount of the deduction by your marginal tax rate. For example, if a deduction is worth $5,000 and you are in the 10% tax bracket (the lowest), the deduction would reduce your taxes by $500.

A deduction’s value to you is tied to your tax rate. So if you’re paying a higher tax rate, you can reap more of a deduction’s benefit. The lower your tax rate, the less benefit a deduction will have for you. Imagine that you take a $5,000 deduction, but you’re in the 35% tax bracket — the second highest. Now you’re saving $1,750 in taxes.

On the other hand, a credit is a dollar-for-dollar reduction in the amount of tax you owe. For example, if you qualify for a $1,000 tax credit of some kind and owe $5,000 in taxes, that credit will reduce your tax burden to $4,000.

***

But – Do Not Claim Too Many Tax Deductions

Deductions are enticing to taxpayers because they can reduce the amount of your income before you calculate the tax you owe, which in turn might significantly lower how much you have to pay in taxes or increase your refund. But that doesn’t mean you should go wild writing things off on your tax returns, as experts say claiming too many deductions is the most common reason people end up getting audited by the IRS.

Don’t try writing off deductions that are no longer accepted by the IRS. The tax code has changed over the years, and there are some things the tax agency no longer recognizes. You should remember that some of the tax write-offs were terminated by the IRS, including deductions on alimony, moving expenses, and any expenses related to investing, hobbies, and tax preparation.

Posted on March 28, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

New Reporting Warning Issued

By Staff Reporters

***

Virtual currency transactions are taxable by law just like transactions in any other property. Taxpayers transacting in virtual currency may have to report those transactions on their tax returns.

All taxpayers must answer a question about virtual currency on their return.

On March 18th, the IRS issued a new alert warning all taxpayers that they must answer a section about virtual currency on their 2021 tax refund this year, even if they did not deal with any digital transactions. According to the agency, there is a question on the top of all versions of Form 1040 that asks, “At any time during 2021, did you receive, sell, exchange, or otherwise dispose of any financial interest in any virtual currency?”

“All taxpayers filing Form 1040, Form 1040-SR or Form 1040-NR must check one box answering either ‘Yes’ or ‘No’ to the virtual currency question,” the IRS explained. “The question must be answered by all taxpayers, not just taxpayers who engaged in a transaction involving virtual currency in 2021.”

Posted on March 16, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

****

The IRS considers taxpayers married if they are legally married under state law, live together in a state-recognized common-law marriage, or are separated but have no separation maintenance or final divorce decree as of the end of the tax year.

Of the 150.3 million tax returns filed in 2016, the latest year for which the IRS has published statistics, 3.07 million belonged to twosomes who filed separately.

These partners reported individual income and expenses on individual tax returns.

By filing separately, their similar incomes, miscellaneous deductions or medical expenses likely helped them save taxes.

***

Filing separately with similar incomes

A couple may pay the IRS less by filing separately when both physician spouses work and earn about the same amount.

When they compare the tax due amount under both joint and separate filing statuses, they may discover that combining their earnings puts them into a higher tax bracket.

Their savings depends on a variety of other factors, however, including their investment situation and whether they have children.

The “married filing separately” status cuts the deductions for IRA contributions and eliminates certain tax credits, among other tax breaks.

Using miscellaneous deductions by filing separately (for tax years prior to 2018)

Miscellaneous deductions can lower taxable income, but in order to enter them on Schedule A, they must add up to more than 2% of adjusted gross income (AGI).

Physician or other spouses with union dues, job-search costs, tax-preparation fees and un-reimbursed business expenses may find their miscellaneous deductions don’t qualify when their higher combined income raises their AGI.

A spouse who travel frequently for business could rack up a sizable tally in airline fees for baggage and itinerary changes that makes the miscellaneous deduction worth pursuing.

Beginning in 2018, these types of miscellaneous expenses are no longer deductible.

Filing separately to save with unforeseen expenses

Unless out-of-pocket medical expenses exceed 7.5% of AGI for 2021, they don’t qualify as a deduction.

Casualty losses must also total more than 10% of AGI and occur in a federally declared disaster area.

The spouse with the loss or substantial medical outlay calculates deductibility against his or her own lower AGI when the couple files separate returns. When one spouse can lower taxable income this way, married filing separately might trim a couple’s overall tax burden.

Filing separately to guard the future

When you don’t want to be liable for your partner’s tax bill, choosing the married-filing-separately status offers financial protection: the IRS won’t apply your refund to your spouse’s balance due. Separate returns make sense to prevent the IRS from seizing a spouse’s tax refund when the other has fallen behind on child support payments.

Couples in the process of divorcing may shun joint returns to avoid post-divorce complications with the IRS, while a spouse who questions her partner’s tax ethics may feel more comfortable living a separate tax life.

Couples living in community-property states should consider state law when deciding how to file.

Posted on February 28, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

****

IRS: The IRS sent out a notice on February 23rd, warning taxpayers about a price hike coming in the next few months. The tax agency said that interest rates will increase for the calendar quarter starting April 1st, 2022. You can accrue interest on two types of payments: over-payment or underpayment. So starting in April, over-payments will have an interest rate of 4 percent, except for corporations which will earn a 3 percent rate and a 1.5 percent rate for the portion of a corporate over-payment that exceeds $10,000. In terms of underpayments, the interest rate will increase to 4 percent overall and 6 percent for large corporate underpayments.

“Under the Internal Revenue Code, the rate of interest is determined on a quarterly basis,” the IRS website explained. The tax agency did not change interest rates in this last quarter, which began Jan. 1, 2022. Before they get changed in April, the rates are currently 3 percent for general over-payments and 2 percent for corporation over-payments, with a 0.5 percent rate for the portion of a corporate over-payment exceeding $10,000. The underpayment interest is 3 percent right now, expect for large corporations which have a 5 percent rate.

***

***

CURRENCY INFLATION: Inflation may occur when the Federal Reserve, or another central bank, adds fiat currency into circulation at a rate that exceeds that of the economy’s growth rate. That creates a situation in which there are more dollars bidding on fewer goods and services. The result is that goods and services cost more. One reason that inflation has been a constant in the US since 1933 is that the FOMC has continually increased the money supply. In response to the 2008 financial crisis, the Fed dropped its lending rate close to zero as a way to inject more liquidity into the economy, which led to increased inflation but not hyperinflation. While those increases have usually moved in step with growth, that hasn’t always been the case.

And so, in response to the COVID-19 pandemic and subsequent lock-downs, the Federal Reserve released the equivalent of $3.8 trillion in new liquidity in 2020. That amount was equal to roughly 20% of the dollars previously in circulation. And it is one reason why many investors were watching the CPI closely in 2021.

EARNING REPORTS:

Monday: India GDP data; Earnings from Lordstown Motors, Groupon, HP, SmileDirectClub and Zoom Video

Tuesday: US and China manufacturing data; Earnings from AutoZone, Baidu, Domino’s Pizza, Hostess Brands, J.M. Smucker, Kohl’s, Target, AMC Entertainment and Salesforce

Wednesday: European inflation data; Earnings from Abercrombie & Fitch, Dine Brands, Dollar Tree, Snowflake and Victoria’s Secret

Thursday: ISM Non-Manufacturing Index; Earnings from Best Buy, Weibo, Costco and Gap

Friday: US jobs report

10-Year: Treasuries rallied to 1.902%.

Oil: The rise in oil prices is spilling over at the gas pump: The average gas price in the US has jumped 10 cents, to $3.64/gallon, in the past two weeks.

Partial SWIFT ban: Western governments put aside their hesitations and proposed banning some Russian lenders from SWIFT, the global messaging service that facilitates cross-border transactions. It’s a move that could cause turmoil across global financial markets.

Devaluation is the deliberate downward adjustment of the value of a country’s money related to another currency, group of currencies or currency standard. It is often confused with depreciation and is the opposite of revaluation which refers to the readjustment of a currency exchange rate.

The government of a country may decide to devalue its currency and like depreciation it is not the result of non-governmental activities.

One reason a country made devalue its currency is to combat a trade imbalance. Devaluation reduces the cost of a country’s export rendering them more competitive in the Global market which is which in turn increases the cost of imports.

If imports are more expensive domestic consumers are less likely to purchase them further strengthening domestic businesses because exports increase and imports decrease there is typically a better balance of payments because the trade deficit shrinks. In short a country that devalue its currency can produce is difficult because there is a greater demand for cheaper exports.

***

***

In accountancy, depreciation refers to two aspects of the same concept: first, the actual decrease of fair value of an asset, such as the decrease in value of factory equipment each year as it is used and wear, and second, the allocation in accounting statements of the original cost of the assets to periods in which the assets are used (depreciation with the matching principle).

Depreciation is thus the decrease in the value of assets and the method used to reallocate, or “write down” the cost of a tangible asset (such as equipment) over its useful life span. Businesses depreciate long-term assets for both accounting and tax purposes. The decrease in value of the asset affects the balance sheet of a business or entity, and the method of depreciating the asset, accounting-wise, affects the net income, and thus the income statement that they report.

Posted on February 23, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

***

By Staff Reporters

***

MARKETS: The S&P 500 fell into a correction for the first time in two years, joining the NASDAQ Composite, as Russia sent troops into pro-Russian regions in Ukraine. The S&P 500 index ended down 1% at 4,304.76, below the correction level at 4,316.91, which would represent a 10% drop from its January 3rd record close. A correction is commonly defined by market technicians as a fall of at least 10% (but not greater than 20%) from a recent peak. The last time the S&P 500 entered a correction was February 27th 2020, when the market was being whipsawed by fears about the outbreak of the COVID pandemic.

And, this bearish market isn’t sparing 2021 winners like Home Depot, which fell the most in nearly two years after supply-chain bottlenecks squeezed its margins. HD was the Dow’s biggest gainer last year.

IRS: According to a news release issued by the IRS, taxpayers now have the option to verify their identities during live, virtual interviews with agents. The agency stresses that no bio-metric data will be required for those interviews.

However, taxpayers once again have the option to verify their identity using ID.me’s facial recognition services. Addressing privacy concerns, the IRS says new requirements are in place to ensure that images provided will be deleted upon verification. That would apply to any new IRS accounts created and those where selfies have already been collected.

Posted on February 22, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

Virtual Currency – Real Taxation

By Staff Reporters

What you need to report to the IRS

The IRS treats virtual currencies as property, which means they’re taxed similarly to stocks. If all you did was purchase cryptocurrency with U.S. dollars, and those assets have been sitting untouched in an exchange or your cryptocurrency wallet, you shouldn’t need to worry about reporting to the IRS.

***

Reporting is required when certain events come into play, most commonly:

Trading one cryptocurrency for another.

Selling cryptocurrency for fiat dollars (government-issued currency).

Using cryptocurrency to buy goods or services (e.g., paying for a cup of coffee with cryptocurrency).

A critical distinction to make is that triggering a taxable event doesn’t necessarily mean you’ll owe taxes, said Andrew Gordon, an Illinois-based certified public accountant and tax attorney. Just because you have to report a transaction doesn’t mean you’ll end up owing the IRS for it.

Posted on February 18, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

IRS Tax Implications

By Staff Reporters

***

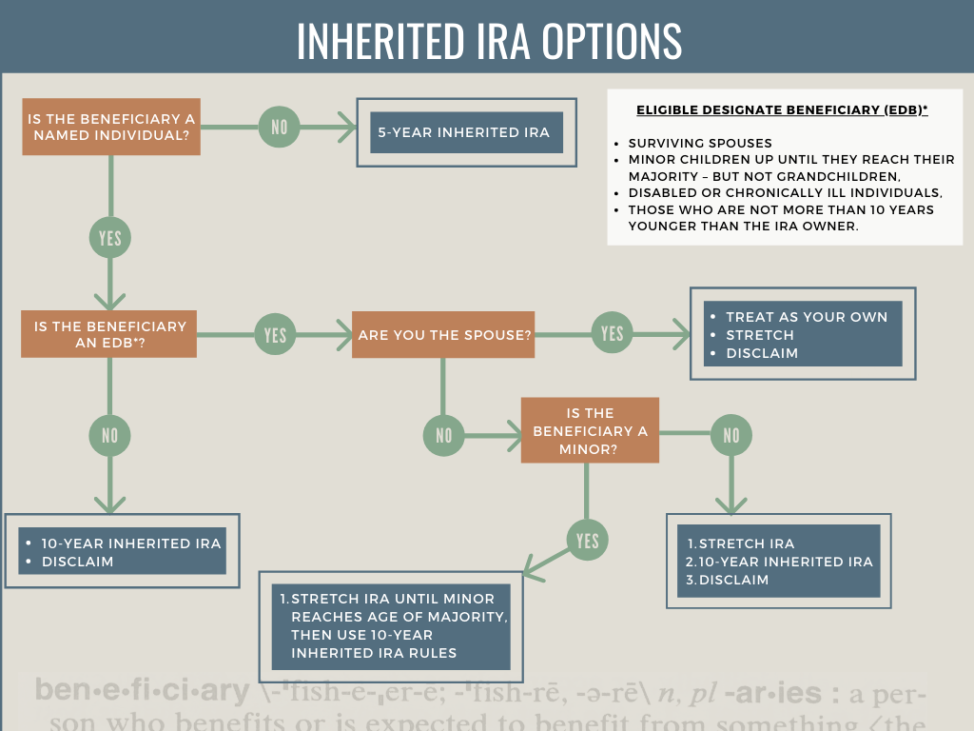

If you inherited a tax-deferred retirement plan, such as a traditional IRA, you’ll have to pay taxes on the money. But you can make the tax hit less onerous.

Spouses can roll the money into their own IRAs and postpone distributions—and taxes—until they’re 70½. All other beneficiaries who want to continue to benefit from tax-deferred growth must roll the money into a separate account known as an inherited IRA. Make sure the IRA is rolled directly into your inherited IRA. If you take a check, you won’t be allowed to deposit the money. Rather, the IRS will treat it as a distribution and you’ll owe taxes on the entire amount.

Once you’ve rolled the money into an inherited IRA, you must take required minimum distributions every year—and pay taxes on the money—based on your age and life expectancy. Deadlines are critical: You must take your first RMD by December 31st. of the year following the death of your parent (or whoever left you the account). Otherwise, you’ll be required to deplete the entire account within five years after the year following your parent’s death.

The December 31st. deadline is also important if you are one of several beneficiaries of an inherited IRA. If you fail to split the IRA among the beneficiaries by that date, your RMDs will be based on the life expectancy of the oldest beneficiary, which may force you to take larger distributions than if the RMDs were based on your age and life expectancy.

You can take out more than the RMD, but setting up an inherited IRA gives you more control over your tax liabilities. You can, for example, take the minimum amount required while you’re working, then increase withdrawals when you’re retired and in a lower tax bracket.

Did you inherit a Roth IRA? And so, as long as the original owner funded the Roth at least five years before he or she died, you don’t have to pay taxes on the money. You can’t, however, let it grow tax-free forever. If you don’t need the money, you can transfer it to an inherited Roth IRA and take RMDs under the same rules governing a traditional inherited IRA. But with a Roth, your RMDs won’t be taxed.

Posted on February 17, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

****

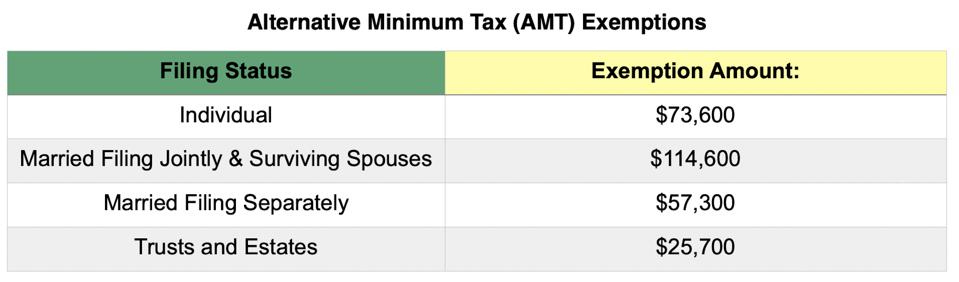

Alternative Minimum Tax

DEFINITION: The alternative minimum tax (AMT) is a tax imposed by the United States federal government in addition to the regular income tax for certain individuals, estates, and trusts. As of tax year 2018, the AMT raises about $5.2 billion, or 0.4% of all federal income tax revenue, affecting 0.1% of taxpayers, mostly in the upper income ranges.

Posted on February 12, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

What it is – How it Works

By Staff Reporters

****

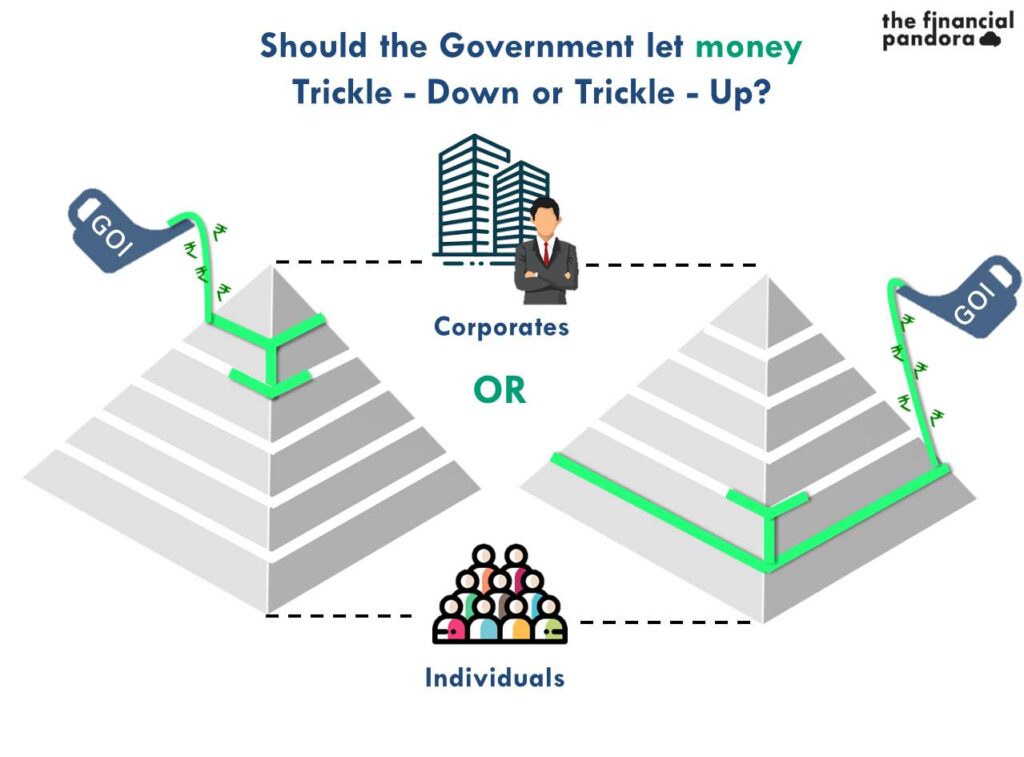

DEFINITION: Trickle-down economics is a colloquial term for supply-side economic policies. In recent history, the term has been used by critics of supply-side economic policies, such as “Reaganomics”. Whereas general supply-side theory favors lowering taxes overall, trickle-down theory more specifically advocates for a lower tax burden on the upper end of the economic spectrum. Empirical evidence shows that the proposition is regressive and has never managed to achieve all of its stated goals as described by the Reagan administration.

SAY’S LAW: In classical economics, Say’s law, or the law of markets, is the claim that the production of a product creates demand for another product by providing something of value which can be exchanged for that other product. Thus, production is the source of demand

Posted on February 10, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

SYNOPSIS: The home office deductionallows qualified taxpayers to deduct certain home expenses when they file taxes. And, now that some doctors and many of us are working remotely, you may be wondering whether working from home will yield any tax breaks. If your small medical or healthcare consulting or other business qualifies you for a home office tax deduction, should you be concerned about triggering an audit? How does a business qualify in the first place; etc?

Well, to claim the home office deduction on their 2021 tax return, taxpayers generally must exclusively and regularly use part of their home or a separate structure on their property as their primary place of business.

***

If I work from home, do I qualify for a home office tax deduction?

If you’re an employee working remotely rather than an employer or business owner, you unfortunately don’t qualify for the home office tax deduction (however, please note that it is still available to some as a state tax deduction). Prior to the Tax Cuts and Job Acts (TCJA) tax reform passed in 2017, employees could deduct unreimbursed employee business expenses, which included the home office deduction. However, for tax years 2018 through 2025, the itemized deduction for employee business expenses has been eliminated.

If I’m self-employed, should I take the home office tax deduction?

You may have heard that taking the home office deduction sends a red flag to the IRS and ups your chances of being audited. Although there may have been some merit to this advice in the past, changes in the tax rules in the late 1990s made it easier for people who work out of their homes to qualify for these write-offs. So if you qualify, by all means, take it.

Do I qualify for the home office tax deduction?

Generally speaking, to qualify for the home office deduction, you must meet one of these criteria:

Exclusive and regular use: You must use a portion of your house, apartment, condominium, mobile home, boat or similar structure for your business on a regular basis. This also includes structures on your property, such as an unattached studio, barn, greenhouse or garage. It doesn’t include any part of a taxpayer’s property used exclusively as a hotel, motel, inn, or similar business.

Principal place of business: Your home office must be either the principal location of your business or a place where you regularly meet with customers or clients. Some exceptions to this rule include day care and storage facilities.

What is “exclusive use”?

The biggest roadblock to qualifying for these deductions is that you must use a portion of your home exclusively and regularly for your business.

The law is clear and the IRS is serious about the exclusive-use requirement. Say you set aside a room in your home for a full-time business and you work in it ten hours a day, seven days a week. If you let your children use the office to do their homework, you violate the exclusive-use requirement and forfeit the chance for home office deductions.

The exclusive-use rule doesn’t mean:

You’re forbidden to make a personal phone call from the office.

You have to rush outside whenever a family member needs a moment of your time.

Although individual IRS auditors may be more or less strict on this point, some advisers say you meet the spirit of the exclusive-use test as long as personal activities invade the home office no more than they would be permitted to in an office building. The office can also be a section of a room if the division is clear — thanks to a partition, for example — and you can show that personal activities are excluded from the business section.

What is “regular use”?

There’s no specific definition of what constitutes regular use. Clearly, if you use an otherwise empty room only occasionally and its use is incidental to your business, you’d fail this test. If you work in the home office a few hours or so each day, however, you might pass. This test is applied to the facts and circumstances of each case the IRS challenges.

What does “principal place of business” mean?

In addition to passing the exclusive- and regular-use tests, your home office must be either the principal location of that business or a place for regular customer or client meetings.

If your home office is in a separate, unattached structure — a detached garage converted into an office, for example — you don’t have to meet the principal-place-of-business or the deal-with-clients test. As long as you pass the exclusive- and regular-use tests, you can qualify for home business write-offs.

What if your business has just one home office, but you do most of your work elsewhere?

Remember that the requirement is that your home office is your principal place of business, not your principal workplace. As long as you use the home office to conduct your administrative or management chores and you don’t make substantial use of any other fixed location to conduct those tasks, you can pass this test.

If you’re an employee of another company but also have your own part-time business based in your home, you can pass this test even if you spend much more time at the office where you work as an employee.

This rule makes it much easier to claim home office deductions for individuals who conduct most of their income-earning activities somewhere else (such as outside salespeople or tradespeople).

***

***

What qualifies as a business?

As with the regular-use test, whether your endeavors qualify as a business depends on the facts and circumstances. The more substantial the activities, in terms of time and effort invested and income generated, the more likely you are to pass the test.

Making money from your efforts is a prerequisite, but for purposes of this tax break, profit alone isn’t necessarily enough. If you use your den solely to take care of your personal investment portfolio, for example, you can’t claim home office deductions because your activities as an investor don’t qualify as a business.

Taxpayers who use a home office exclusively to manage rental properties may qualify for home office tax status but as property managers rather than investors.

What if I operate a child care or storage facility?

The exclusive-use test doesn’t apply if you use part of your house to:

Provide day care services for children, older adults or individuals with disabilities. If you care for children in your home between 7 a.m. and 6 p.m. each day, for example, you can use that part of the house for personal activities the rest of the time and still claim business deductions. To qualify for the tax break, your home care business must meet any applicable state and local licensing requirements.

Store product samples or inventory you sell in your business. Assume your home-based business is the retail sale of home-cleaning products and that you regularly use half of your basement to store inventory. Occasionally using that part of the basement to store personal items wouldn’t cancel your home office deduction. To qualify for this exception, your home must be the principal location of your business.

How do I calculate the home office tax deduction?

Your home office business deductions are based on either the percentage of your home used for the business or a simplified square footage calculation.

The most exact way to calculate the business percentage of your house is to measure the square footage devoted to your home office as a percentage of the total area of your home. If the office measures 150 square feet, for example, and the total area of the house is 1,200 square feet, your business percentage would be 12.5%.

An easier calculation is acceptable if the rooms in your home are all about the same size. In that case, you can figure out the business percentage by dividing the number of rooms used in your business by the total number of rooms in the house.

Special rules apply if you qualify for home office deductions under the day care exception to the exclusive-use test.

Your business-use percentage must be reduced because the space is available for personal use part of the time.

To do that, you compare the number of hours the child care business is operated, including preparation and cleanup time, to the total number of hours in the year (8,760).

Assume you use 40% of your house for a nursing daycare business that operates 12 hours a day, five days a week for 50 weeks of the year.

12 hours x 5 days x 50 weeks = 3,000 hours per year.

3,000 hours ÷ 8,760 total hours in the year = 0.34 (34%) of available hours.

34% of available hours x 40% of the house used for business = 13.6% business write-off percentage.

Simplified square footage method

Beginning with 2013 tax returns, the IRS began offering a simplified option for claiming the deduction. This new method uses a prescribed rate multiplied by the allowable square footage used in the home.

For 2021, the prescribed rate is $5 per square foot with a maximum of 300 square feet.

If the office measures 150 square feet, for example, then the deduction would be $750 (150 x $5).

The space must still be dedicated to business activities.

With either method, the qualification for the home office deduction is determined each year. Your eligibility may change from one year to the next. Finally, please note that only certain expenses such as rent, mortgage interest and property taxes qualify for the deduction, and the deduction is limited to $10,000.

Posted on February 5, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

****

***

The most recent numbers show that more than 45 million of us itemized deductions on our 1040s—claiming $1.2 trillion dollars’ worth of tax deductions. That’s right: $1,200,000,000,000! That same year, taxpayers who claimed the standard deduction accounted for $747 billion. Some of those who took the easy way out probably shortchanged themselves. (If you turned age 65 in 2021 or earlier, remember that you deserve a bigger standard deduction than younger folks.)

Here are our 10 most overlooked tax deductions. Claim them if you deserve them, and keep more money in your pocket. Good advice for all physicians, nurse and medical professionals, too.

1. State sales taxes

This write-off makes sense primarily for those who live in states that do not impose an income tax. Especially Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming. Here’s why this is a factor. You must choose between deducting state and local income taxes or state and local sales taxes. For most citizens of income-taxing-states, the state and local income tax deduction is usually the better deal.

For those of you in an income-tax free state, there are two ways to claim the sales tax deduction on your tax return. One, you can use the IRS tables provided for your state to determine what you can deduct. In addition, if you purchased a vehicle, boat, airplane, home or did major home renovations, you may be able to add the state sales tax you paid on these items to the amount shown in the IRS tables up to the limit for your state. Or two, you can you can keep track of all of the sales tax you paid throughout the year and use that.

The best way to see what you can deduct is to use the IRS’s Sales Tax Calculator for this. Keep in mind, the total of your itemized deductions for all of your state and local taxes is limited to $10,000 per year.

2. Reinvested dividends

This isn’t really a tax deduction, but it is a subtraction that can save you a lot of money. And it’s one that many taxpayers miss. If, like most investors, you have mutual fund dividends automatically invested in extra shares, remember that each reinvestment increases your “tax basis” in the stock or mutual fund. That, in turn, reduces the amount of taxable capital gain (or increases the tax-saving loss) when you sell your shares.

Forgetting to include the reinvested dividends in your cost basis—which you subtract from the proceeds of sale to determine your gain—means overpaying your taxes.

3. Out-of-pocket charitable contributions

It’s hard to overlook the big charitable gifts you made during the year by check or payroll deduction. But the little things add up, too, and you can write off out-of-pocket costs you incur while doing good deeds. Ingredients for casseroles you regularly prepare for a qualified nonprofit organization’s soup kitchen, for example, or the cost of stamps you buy for your school’s fundraiser count as a charitable contribution. If you drove your car for charity in 2021, remember to deduct 14 cents per mile.

4. Student loan interest paid by you or someone else

In the past, if parents or someone else paid back a medical school or other loan incurred by a student, no one got a tax break. To get a deduction, the law said that you had to be both liable for the debt and actually pay it yourself. But now there’s an exception. You may know that you might be eligible to take a deduction but even if someone else pays back the loan, the IRS treats it as though they gave you the money, and you then paid the debt. So, a student who’s not claimed as a dependent can qualify to deduct up to $2,500 of student loan interest paid by you or by someone else.

5. Moving expenses

While most taxpayers lost the ability to deduct moving expenses beginning in 2018, one main group of people who can still claim their moving expenses to the IRS. Who are they? Military personnel. If you’re an active duty military member who is relocating, you can still deduct these expenses —if you don’t receive reimbursement from the government for the move.

Also, as long as the move is permanent —and your relocation was ordered by the military — you don’t have to pay tax on qualified moving expense reimbursements. So start getting those receipts out now – because you can claim travel and lodging expenses for you and your family, moving household goods, and the costs for shipping your cars and your beloved pets! And that’s good news for the men and women we thank for bravely serving our country.

6. Child and Dependent Care Tax Credit

A tax credit is so much better than a tax deduction—it reduces your tax bill dollar for dollar. So missing one is even more painful than missing a deduction that simply reduces the amount of income that’s subject to tax.

But it’s easy to overlook the Child and Dependent Care Credit if you pay your child care bills through a reimbursement account at work. For 2020, the law allows you to run up to $5,000 of such expenses through a tax-favored reimbursement account at work. Up to $6,000 in care expenses can qualify for the credit, but the $5,000 from a tax favored account can’t be used. So if you run the maximum $5,000 through a plan at work but spend more for work-related child care, you can claim the credit on up to an extra $1,000. That would cut your tax bill by at least $200 using the minimum 20 percent of the expenses. The credit percentage goes up for lower income households.

However, there are big changes for 2021, The American Rescue Plan signed into law on March 11, 2021 brought significant changes to the amount and way that the child and dependent care tax credit can be claimed only for tax year 2021. The new law not only increases the credit, but also the amount of taxpayers that will benefit from the credit’s highest rate and it also makes it fully refundable. This means that, unlike previous years, you can still get the credit even if you don’t owe taxes. Changes to the Child and Dependent Care Credit that apply only for tax year 2021 (the taxes you file in 2022) include:

The highest credit percentage increased from 35% to 50% of qualifying expenses

Qualifying child and dependent care expenses increased from $3,000 to $8,000 for one qualifying person and from $6,000 to $16,000 for two or more qualifying individuals

The adjusted gross income (AGI) level at which the credit percentage is reduced is increased from $15,000 to $125,000

For example, prior to the 2021 tax year, a taxpayer with one qualifying person, $3,000 in qualifying expenses and an AGI of $60,000 would qualify for a nonrefundable credit of approximately $600 (20% x $3,000). By contrast, under the new law for tax year 2021 only, a taxpayer with the same circumstances can potentially claim a refundable credit of approximately $1,500 (50% x $3,000).

Also for tax year 2021, the maximum amount that can be contributed to a dependent care flexible spending account and the amount of tax-free employer-provided dependent care benefits is increased from $5,000 to $10,500.

7. Earned Income Tax Credit (EITC)

Millions of lower-income people take this credit every year. However, 25% of taxpayers who are eligible for the Earned Income Tax Credit fail to claim it, according to the IRS. Some people miss out on the credit because the rules can be complicated. Others simply aren’t aware that they qualify.

The EITC is a refundable tax credit—not a deduction— with maximum amounts for different filing statuses ranging from $1,502 to $6,728 for 2021. The credit is designed to supplement wages for low-to-moderate income workers. But the credit doesn’t just apply to lower income people. Tens of millions of individuals and families previously classified as “middle class”—including many medical colleagues and white-collar workers—are now considered “low income” because they:

lost a job

took a pay cut

or worked fewer hours during the year

The exact refund you receive depends on your income, marital status and family size. To get a refund from the EITC you must file a tax return, even if you don’t owe any taxes. Moreover, if you were eligible to claim the credit in the past but didn’t, you can file any time during the year to claim an EITC refund for up to three previous tax years.

8. State tax you paid last spring

Did you owe taxes when you filed your 2020 state tax return in 2021? Then remember to include that amount with your state tax itemized deduction on your 2021 return, along with state income taxes withheld from your paychecks or paid via quarterly estimated payments. Beginning in 2018, the deduction for state and local taxes is limited to a maximum of $10,000 per year.

9. Refinancing mortgage points

When you buy a house, you often get to deduct points paid to obtain your mortgage all at one time. When you refinance a mortgage, however, you have to deduct the points over the life of the loan. That means you can deduct 1/30th of the points a year if it’s a 30-year mortgage—that’s $33 a year for each $1,000 of points you paid. Doesn’t seem like much, but why throw it away?

Also, in the year you pay off the loan—because you sell the house or refinance again—you get to deduct all the points not yet deducted, unless you refinance with the same lender.

10. Jury pay paid to employer

Some employers continue to pay employees’ full salary while they are doing their civic duty, but ask that they turn over their jury fees to the company. The only problem is that the IRS demands that you report those fees as taxable income. If you give the money to your employer you have a right to deduct the amount so you aren’t taxed on money that simply passes through your hands.

Posted on February 3, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

What it is?

By Staff Reporters

***

Some doctors and other taxpayers may receive IRS Letter 6475, which references the third Economic Impact Payment. While most recipients eligible for this stimulus check have already received their money in full, some taxpayers might now be eligible or entitled to more money based on their 2021 tax information by claiming a Recovery Rebate Credit on their upcoming tax return. Those people will need this form to confirm how much of the third stimulus check they already received from the government, if they received any at all. Learn more here.

Posted on February 3, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Stock Markets: S&P 500, DJIA and NASDAQ booked their 4th straight day of gains with technology shares in focus.

And, Facebook rattled investors by posting a rare profit decline, driven by the company’s heavy spending on its vision for a so-called Metaverse while simultaneously confronting advertising challenges on its existing services. The company, formerly known as Facebook, posted net income of nearly $10.3 billion in the final three months of last year, a decline 8% from the same period in the prior year and below Wall Street analysts’ projections. For Meta, the disappointing earnings add to its challenges. It’s in the middle of a number of regulatory fights and also looking to justify its strategic shift to bet on an immersive internet known as the metaverse. Meanwhile, other platforms like TikTok and YouTube are gaining ground with younger users.

Several other social media companies also fell hard after the bell, including Twitter, Pinterest and Spotify, which also released disappointing results. And PayPal fell hard, too!

IRS: The Internal Revenue Service is adding about 1,200 employees to its rolls to help the agency navigate what will likely be one of the most challenging tax filing seasons in years.

Mike Milken: Is headed to the latest power base for U.S. financiers and politicians: South Florida. The income tax-free, palm tree-lined oasis is where New York’s ultra-wealthy have long decamped for the winter, but are increasingly making their permanent home. The 75-year-old billionaire kicks off the first Milken Institute South Florida Dialogues on Friday. The six-day preliminary agenda of island and mansion hopping has Ken Griffin talking national security in South Beach, and Sonia and Paul Tudor Jones hosting tennis matches at their oceanfront Palm Beach estate Casa Apava. The format is similar to the dialogues he’s presented in the Hamptons for years.

Posted on February 1, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

The IRS Tax Letter 6419 has been sent out to families who received the Child Tax Credit in 2021 and it explains how the advance tax credit will affect your filing this year. This may be of special importance to young physicians, nurses and all younger medical professionals.

Posted on February 1, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

****

***

Tax planning can be quite a tedious process, but there are benefits for all seniors to make it less taxing. And senor medical professionals should take particular note:

Free Advice: IRS-certified volunteers will help older taxpayers with tax return preparation and electronic filing between January 1st and April 15th each year.

No Withdrawal Penalties: Anyone aged 59 years or over can withdraw money from an IRA, without incurring the common 10% tax.

Catch-Up Contributions: Healthcare Workers aged 50 or older can defer income tax on an extra $6,500 or a total of $26,000 if contributed to a 401(k) plan, resulting in a tax savings of $6,240 for an older worker in the 24% tax bracket.

Additional IRA Contribution: Workers age 50 and older can contribute an additional $1,000 to an IRA, or a total of $7,000 in 2020.

Whether you do contract work or have your own small business, tax deductions for the self-employed physician consultant and/or medical executive or nurse consultant, etc., can add up to substantial tax savings.

With self-employment comes freedom, responsibility, and a lot of expense. While most self-employed people celebrate the first two, they cringe at the latter, especially at tax time. They might not be aware of some of the tax write-offs to which they are entitled.

When it comes time to file your returns, don’t hesitate to claim the benefits you get for being the boss. As a self-employed success story, you’ve earned them.

FORM 1099NEC: Form 1099 NEC is one of several IRS tax forms used in the United States to prepare and file an information return to report various types of income other than wages, salaries, and tips. The term information return is used in contrast to the term tax return although the latter term is sometimes used colloquially to describe both kinds of returns.

“Many times an overlooked deduction is educational expenses. If one is taking courses or buying research material to be more effective in their work, this can be deductible.”

Individual Retirement Plans (IRAs)

One of the best tax write-offs for the self-employed physician consultant is a retirement plan. A person with no employees can set up an individual 401 (k). “You can contribute $19,500 in 2021 as a 401(k) deferral, plus 25 percent of net income.”

If you have employees, consider a SIMPLE (Savings Incentive Match Plan for Employees) IRA—an IRA-based plan that gives small employers a simplified method to make contributions to their employees’ retirement. As of 2021, an employee may defer up to $13,500 and employees over 50 may contribute an additional $3,000.

“A third retirement plan is Simplified Employee Pension IRA (SEP IRA).” The employer may contribute the lesser of 25 percent of income or $58,000 in 2021. If the employer has eligible employees, an equal percentage of their income must be contributed.

Recall that retirement plans are “absolutely the No. 1 tax deduction. The government is helping fund retirement.”

Business use of home or dwelling

Now, most self-employed taxpayers’ businesses start as home-based businesses. These people need to know portions of business costs are deductible and so “It is very important that you keep track of expenses relating to your housing costs.”

If your gross income from your business exceeds your total expenses, then you can deduct all of your expenses related to the business use of your home. If your gross income is less than your total expenses, your deduction will be limited to the difference between your gross income and the sum of all business expenses you would pay if the business was not in your home. Those expenses could include telephone lines, the Internet, and other costs to do business.

You must also have a home office that is truly used for work and the Internal Revenue Service may require you to document this.

***

Deducting automobile expenses

If you travel for business, even short distances within your own city, you may deduct the dollar value of business miles traveled on your tax return. The taxpayer may file the actual expense s/he incurred, or use the standard mileage rate prescribed by the IRS, which is 56 cents as of 2021. The IRS allowable mileage rates should be checked every year as they can change.

“If you decide to use actual car expenses, be sure to include payments, depreciation, registration, insurance, garage rent, licenses, repairs and maintenance, and parking and toll fees.” AND, “If you decide to use the standard mileage rate, it would be in your best interest to keep a log—daily, weekly or monthly—of miles driven to distinguish personal use from business use.”

Depreciation of property and equipment

Some self-employed people may purchase property and equipment for a business. If they expect that property to last longer than one year, it should be depreciated on the tax return.

Claims regarding property, according to the IRS, must meet the following criteria: You must own the property and it must be used or held to generate income. The property should have an estimated useful life, meaning you should be able to guess how long you can generate income with it. It may not have a useful life of one year or less, and may not be purchased and disposed of in the same year.

Certain repairs on property used for business may also be deducted.

Educational expenses

Any educational expense is potentially tax-deductible.

“Many times an overlooked deduction is educational expenses. “If one is taking courses or buying research material to be more effective in their work, this can be deductible.”

Think about any books, web courses, local college courses, or other classes or materials that you have purchased to improve your job or business. It’s easy to forget a work-related webinar or business e-book that was purchased online, so remember to save e-receipts.

Also recall that subscriptions to trade or professional publications and donations to business organizations, both of which are frequently necessary for the continuation and growth of your business.

Other areas to explore

Other deductions that can be easily missed are advertising and promotional expenses, banking fees, and air, bus, or train fare. Restaurant meals and other entertainment costs may be written off as long as they are necessary business expenses.

And, consider health insurance premiums, which in most cases represent a credit rather than a tax deduction. “A credit goes directly against one’s taxes, rather than a reduction of income.”

Regardless of which expenses you discover that you may write off, the most important thing is to keep accurate records throughout the year. Save receipts, including e-mail receipts, and file or log them so you have easy access to them at tax time. Not only does keeping receipts, mileage logs, and other expense records make filing taxes easier, but it also facilitates a system that allows you to track changes from year to year.

***

Long-term tax-saving strategies

Don’t just look at last-minute write-offs when considering self-employment tax deductions. Think about laying down some long-term strategies for money savings from year to year—particularly if you are a high earner.

“Accountants typically tell you what you have to pay but they don’t always tell you strategies to reduce your payments.”

To reduce your gross taxable income, consider setting up a defined-benefit pension plan. This plan is based on your age and income: The older you are and the higher your earnings, the more you are allowed to contribute. An alternative plan is an age-weighted profit-sharing plan, which is similar and can benefit those who have several employees.

Another strategy for high-earning business owners who own their own building through a limited liability company or similar business structure is to pay themselves rent. This rent is used to pay down the mortgage, but it is also considered a business expense for tax purposes.

Self-employed professionals required to have liability insurance should consider setting up their own insurance company. A captive insurance company is one that insures the risks of the business—or businesses, in the case of a cooperative. Its premiums can be tax-deductible.

But, if money accumulates and claims are minimal, the money taken out is taxable under capital gains. This is not a retirement strategy, but that it can save you money by allowing you to “pay yourself” instead of an insurance company and still deduct the premiums.

Assessment

With any of these more complicated, long-term strategies, consult with a business attorney, CPA/EA or financial planner to ensure you have the best plan possible for your business.

Posted on January 25, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

FOR PHYSICIANS AND ALL OF US!

Br. Dr. David E. Marcinko MBA

By Staff Reporters

***

It’s been announced that January 24th 2022 is the official start of the tax filing season. This means it’s that time of year again to buy some pricey tax software and prepare your return on your own, hire a tax prep pro, CPA, or take advantage of the Free File Program from the IRS.