BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on May 31, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

What’s Up?

[By staff reporters]

According to Wikipedia, the hemline index is a theory presented by economist George Taylor in 1926. The theory suggests that hemlines on women’s dresses rise along with stock prices.

In good economies, we get such results as miniskirts (as seen in the 1920s and the 1960s), or in poor economic times, as shown by the 1929 Wall Street Crash, hems can drop almost overnight.

Non-peer-reviewed research in 2010 supported the correlation, suggesting that “the economic cycle leads the hemline with about three years”.

***

***

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

Posted on May 30, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

WHAT IS THE “MEDICARE COST CONTROL EFFICIENCY” PARADOX?

The 800 Pound Gorilla in the Medical Treatment Room

By Staff Reporters

Blogger Ezra Klein opined more than a decade ago that one of the dirty little secrets of the health-care system is that Medicare has done a much better job controlling costs than private health insurers. It is a paradox!

DEFINITION: A paradox is a seemingly absurd or self-contradictory statement or proposition that when investigated may prove to be well founded or true.

***

***

QUERY:But, what about Medicare, cost control efficiency, today?

Posted on May 28, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Payment for order flow, or PFOF, is a tactic some brokerages use to rake in piles of cash. Payment for order flow (PFOF) is a form of compensation, usually in terms of fractions of a penny per share, that a brokerage firm receives for directing orders for trade execution to a particular market maker or exchange. Payment for order flow is common in options markets, and is increasingly found in equity (stock market) transactions.

The “P” in PFOF stands for “payment.” That’s because PFOF gets stock brokers paid. It starts when brokers direct trade orders to a particular e-trading firm (like Mountain Securities, for example) instead of routing the trades straight to exchanges. At that point, the e-trading firm may be able to collect the difference between the bid and the ask price, and the brokerages get a cut of that profit. It’s the proverbial “You scratch your broker’s back through their bespoke Ermenegildo Zegna suit, and they’ll scratch yours.”

According to Lillian Stone, some industry experts argue that PFOF is a conflict of interest. (The practice came under scrutiny last year when US brokers made billions on meme stock trading.) You want your broker to get you the best possible prices during a trade, right? Well, if your broker is incentivized to work with one specific e-trading firm, there’s a chance you may not get the sweetest deal—but they’ll line their pockets all the same.

As human beings, our brains are booby-trapped with psychological barriers that stand between making smart financial decisions and making dumb ones. The good news is that once you realize your own mental weaknesses, it’s not impossible to overcome them.

In fact, Mandi Woodruff, a financial reporter whose work has appeared in Yahoo! Finance, Daily Finance, The Wall Street Journal, The Fiscal Times and the Financial Times among others; related the following mind-traps in a September 2013 essay for the finance vertical Business Insider; as these impediments are now entering the lay-public zeitgeist.

***

Anchoring happens when we place too much emphasis on the first piece of information we receive regarding a given subject. For instance, when shopping for a wedding ring a salesman might tell us to spend three months’ salary. After hearing this, we may feel like we are doing something wrong if we stray from this advice, even though the guideline provided may cause us to spend more than we can afford.

Myopia makes it hard for us to imagine what our lives might be like in the future. For example, because we are young, healthy, and in our prime earning years now, it may be hard for us to picture what life will be like when our health depletes and we know longer have the earnings necessary to support our standard of living. This short-sightedness makes it hard to save adequately when we are young, when saving does the most good.

Gambler’s fallacy occurs when we subconsciously believe we can use past events to predict the future. It is common for the hottest sector during one calendar year to attract the most investors the following year. Of course, just because an investment did well last year doesn’t mean it will continue to do well this year. In fact, it is more likely to lag the market.

Avoidance is simply procrastination. Even though you may only have the opportunity to adjust your health care plan through your employer once per year, researching alternative health plans is too much work and too boring for us to get around to it. Consequently, we stick with a plan that may not be best for us.

Loss aversion affected many investors during the stock market crash of 2008. During the crash, many people decided they couldn’t afford to lose more and sold their investments. Of course, this caused the investors to sell at market troughs and miss the quick, dramatic recovery.

Overconfident investing happens when we believe we can out-smart other investors via market timing or through quick, frequent trading. Data convincingly shows that people who trade most often underperform the market by a significant margin over time.

Mental accounting takes place when we assign different values to money depending on where we get it from. For instance, even though we may have an aggressive saving goal for the year, it is likely easier for us to save money that we worked for than money that was given to us as a gift.

Herd mentality makes it very hard for humans to not take action when everyone around us does. For example, we may hear stories of people making significant profits buying, fixing up, and flipping homes and have the desire to get in on the action, even though we have no experience in real estate.

While financial planning rules of thumbs are useful to people as general guidelines, they may be too oversimplified in many situations, leading to underestimating or overestimating an individual’s needs. This may be especially true for physicians and many medical professionals. Rules of thumb do not account for specific circumstances or factors occurring at a particular time, or that could change over time, which should be considered for making sound financial decisions.

For example, in a tight job market, an emergency fund amounting to six months of household expenses does not consider the possibility of extended unemployment. I’ve always suggested 2-3 years for doctors. Venture capitalist lay-offs of physicians during the pandemic confirm this often criticized benchmark opinion of mine.

As another example, buying life insurance based on a multiple of income does not account for the specific needs of the surviving family, which include a mortgage, the need for college funding and an extended survivor income for a non-working spouse. Again a huge home mortgage, or several children or dependents, may be the financial bane of physician colleaguesand life insurance.

A home purchase should cost less than an amount equal to two and a half years of your annual income. I think physicians in practice for 3-5 years might go up to 3.5X annual income; ceteras paribus.

Save at least 10-15% of your take-home income for retirement. Seek to save 20% or more.

Have at least five times your gross salary in life insurance death benefit. Consider 10X this amount in term insurance if young, and/or with several children or other special circumstances.

Pay off your highest-interest credit cards first. Agreed.

The stock market has a long-term average return of 10%. Agreed, but appreciated risk adjusted rates of return..

You should have an emergency fund equal to six months’ worth of household expenses. Doctors should seek 2-3 years.

Your age represents the percentage of bonds you should have in your portfolio. Risk tolerance and assets may be more vital.

Your age subtracted from 100 represents the percentage of stocks you should have in your portfolio. Risk tolerance and assets may still be more vital.

A balanced portfolio is 60% stocks, 40% bonds. With historic low interest rates, cash may be a more flexible alternative than bonds; also avoid most bond mutual funds as they usually never mature.

There are also rules of thumb for determining how much net worth you will need to retire comfortably at a normal retirement age. Here is the calculation that Investopedia uses to determine your net worth:

If you are employed and earning income: ((your age) x (annual household income)) / 10.

If you are not earning income or you are a student: ((your age – 27) x (annual household income)) / 10.

Posted on May 11, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Economic Implications of Pain, Suffering and Imminent Death

***

By Eric Bricker MD

Examples of Inelastic Demand in Healthcare Are: 1) Emergencies 2) Patented Medications for Diseases That Have No Other Alternative Drugs 3) Doctor Specialties Where the Patient Has No Choice in the Services Such As Radiologists, Anesthesiologists and Pathologists [RAP]

Posted on May 11, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

About Frank Knight PhD

[By staff reporters]

In economics, Knightian uncertainty is a lack of any quantifiable knowledge about some possible occurrence, as opposed to the presence of quantifiable risk (e.g., that in statistical noise or a parameter’s confidence interval). The concept acknowledges some fundamental degree of ignorance, a limit to knowledge, and an essential unpredictability of future events.

“Uncertainty must be taken in a sense radically distinct from the familiar notion of Risk, from which it has never been properly separated…. The essential fact is that ‘risk’ means in some cases a quantity susceptible of measurement, while at other times it is something distinctly not of this character; and there are far-reaching and crucial differences in the bearings of the phenomena depending on which of the two is really present and operating…. It will appear that a measurable uncertainty, or ‘risk’ proper, as we shall use the term, is so far different from an unmeasurable one that it is not in effect an uncertainty at all.”

Although some doctors might view a budget as unnecessarily restrictive, sticking to a spending plan can be a useful tool in enhancing the wealth of a practice. And so, I will emphasize keys to smart budgeting and how to track spending and savings in these tough economic times; like today with the stock market busts, venture capitalists invading health care, corona virus the pandemic, aging baby boomer physicians and the great resignation; etc.

There is an aphorism that suggests, “Money cannot buy happiness.” Well, this may be true enough but there is also a corollary that states, “Having a little money can sure reduces the unhappiness.”

Unfortunately, today there is still more than a little financial unhappiness in all medical specialties. The challenges range from the commoditization of medicine, aging demographics, Medicare reimbursement cutbacks, ACA, and increased competition to floundering equity markets, the squeeze on credit and declines in the value of a practice. Few doctors seem immune to this “perfect storm” of economic woes. And then Covid-19, corona, and covid.

Far too many physicians are hurting and it is not limited to above-average earning professionals. However, one can strive to reduce the pain by following some basic budgeting principles. By adhering to these principles, physicians can eliminate the “too many days at the end of the month” syndrome and instead develop a foundation for building real wealth and security, even in difficult economic climates like we face today.

There are three major budget types. A flexible budget is an expenditure cap that adjusts for changes in the volume of expense items. A fixed budget does not. Advancing to the next level of rigor, a zero-based budget starts with essential expenses and adds items until the money is gone. Regardless of type, budgets can be extremely effective if one uses them at home or the office in order to spot money troubles before they develop.

For the purpose of wealth building, doctors may think of this budget as a quantitative expression of an action plan. It is an integral part of the overall cost-control process for the individual, his or her family unit or one’s medical practice.1

How To Prepare A Personal Cash Flow Budget

Preparing a net income statement (lifestyle cash flow budget) is often difficult because many doctors perceive it as punitive. Most doctors do not live a disciplined spending lifestyle and they view a budget as a compromise to it. However, a cash flow budget is designed to provide comfort when there is surplus income that can be diverted for other future needs. For example, if you treat retirement savings as just another periodic bill, you are more likely to save for it.

You may construct a personal cash budget by recording each cash receipt and cash disbursement on a spreadsheet. Only the date, amount and a brief description of the transaction are necessary. The cash budget is a simple tool that even doctors who lack accounting acumen can use. Since it is possible to track the cash-in and cash-out in the same format used for a standard check register, most doctors find that the process takes very little time. Such a budget will provide a helpful look at how well you are staying within available resources for a given period.

We then continue with an analysis of your operating checkbook and a review of various source documents such as one’s tax return, credit card statements, pay stubs and insurance policies. A typical statement will show all cash transactions that occur within one year. It is helpful to establish a monthly equivalent to all items of income and expense. For the purposes of getting started, note items of income and expense by the frequency you are accustomed to receiving or spending them.

What You Should Know About The ‘Action Plan’ Cash Budget

For a medial office, the first operations budget item might be salary for the doctor and staff. Operating assets and other big ticket items come next. Some doctors/clients review their office P&L statements monthly, line by line, in an effort to reduce expenses. Then they add back those discretionary business expenses they have some control over.

Now, do you still run out of money before the end of the month? If so, you had better cut back on entertainment, eating dinner out or that fancy, new but unproven piece of medical equipment. This sounds draconian until you remind yourself that your choice is either: live frugally later or live a simpler lifestyle now and invest the difference.

As a young doctor, it may be a difficult trade-off. By mid-life, however, you are staring retirement in the face. That is why the action plan depends on your actions concerning monetary scarcity, a plan that one can implement and measure using simple benchmarks or budgeting ratios. By using these statistics, perhaps on an annual basis, the podiatrist can spot problems, correct them and continue planning actively toward stated goals like building long-term wealth.2

Useful Calculations To Assess Your Budgeting Success

In the past, generic budgeting ratios would emphasize not spending more than 15 to 20 percent of your net salary on food or 8 percent on medical care. Now these estimates have given way to more rigorous numbers. Personal budget ratios, much like medical practice financial ratios, represent comparable benchmarks for parameters such as debt, income growth and net worth. Although these ratios are still broad, the following represent some useful personal budgeting ratios for physicians.

• Basic liquidity ratio = liquid assets / average monthly expenses. Cash-on-hand should approach 12 to 24 months or more in the case of a doctor employed by a financially insecure HMO or fragile medical group practice. Yes, chances are you have heard of the standard notion of setting enough cash aside to cover three months in a rainy day scenario. However, we have decried this older laymen standard for many years in our textbooks, white papers and speaking engagements as being wholly insufficient for the competitively unstable environment of modern healthcare.

• Debt to assets ratio = total debt / total assets. This percentage is high initially but should decrease with age as the doctor approaches a debt-free existence

• Debt to gross income ratio = annual debt repayments / annual gross income. This represents the adequacy of current income for existing debt repayments. Doctors should try to keep this below 20 to 25 percent.

• Debt service ratio = annual debt repayment / annual take-home pay. Physicians should aim to keep this ratio below 25 to 30 percent or face difficulty paying down debt.

• Investment assets to net worth ratio = investment assets / net worth. This budget ratio should increase over time as retirement approaches.

• Savings to income ratio = savings / annual income. This ratio should also increase over time as one retires major obligations like medical school debt, a practice loan or a home mortgage.

• Real growth ratio = (income this year – income last year) / (income last year – inflation rate). This budget ratio should grow faster than the core rate of inflation.

• Growth of net worth ratio = (net worth this year – net worth last year) / net worth last year – inflation rate). Again, this budgeting ratio should stay ahead of the specter of rising inflation.

In other words, these ratios will help answer the question: “How am I doing?”

Pearls For Sticking To A Budget

Far from the burden that most doctors consider it to be, budgeting in one form or another is probably one of the greatest tools for building wealth. However, it is also one of the greatest weaknesses among physicians who tend to live a certain lifestyle.3

In fact, I have found that less than one in 10 medical professionals have a personal budget. Fear, or a lack of knowledge, is a major cause of procrastination. Fortunately, the following guidelines assist in reversing this microeconomic disaster.

1. Set reasonable goals and estimate annual income. Do not keep large amounts of cash at home or office. Deposit it in an FDIC insured money-market account for safety. Do not deposit it in a money market mutual fund with net asset value (NAV) that may “break the buck” and fall below the one-dollar level. The new limit is $250,000. Track actual bills and expenses.

2. Do not pay bills early, do not have more taxes withheld from your salary than needed and develop spending estimates to pay fixed expenses first. Fixed expenses are usually contractual and usually include housing, utilities, food, Social Security, medical, debt repayments, homeowner’s or renter’s insurance, auto, life and disability insurance, etc. Reduce fixed expenses when possible. Ultimately, all expenses get paid and become variable in the long run.

3. Make it a priority to reduce variable expenses. Variable expenses are not contractual and may include clothing, education, recreational, travel, vacation, gas, cable TV, entertainment, gifts, furnishings, savings, investments, etc. Trim variable expenses by 5 to 20 percent.

4. Use “carve-outs or “set-asides” for big ticket items and differentiate true wants from frivolous needs.

5. Calculate both income and expenses as a percentage of your total budget. Determine if there is a better way to allocate resources. Review the budget on a monthly basis to notice any variance. Determine if the variance was avoidable, unavoidable or a result of inaccurate assumptions. Take corrective action as needed.

6. Know the difference between saving and investing. Savers tend to be risk adverse while investors understand risk and take steps to mitigate it. Watch mutual fund commissions and investment advisory fees, which cut into return-rates. Keep investments simple and diversified (stocks, bonds, cash, index, no-load mutual and exchange traded funds, etc.).4

How To Budget In The Midst Of A [Corona] Crisis

Sooner or later, despite the best of budgeting intentions, something will go awry. A doctor will be terminated or may be the victim of a reduction-in-force (RIF) because of cost containment initiatives of the corona pandemic. A medical practice partnership may dissolve or a local hospital or surgery center may close, hurting your practice and livelihood. Someone may file a malpractice lawsuit against you, a working spouse may be laid off or you may get divorced. Regardless of the cause, budgeting crisis management encompasses two different perspectives: awareness and execution.

First, if you become aware that you may lose your job, the following proactive steps will be helpful to your budget and overall financial condition.

• Decrease retirement contributions to the required minimum for company/practice match. • Place retirement contribution differences in an after-tax emergency fund. • Eliminate unnecessary payroll deductions and deposit the difference to cash. • Replace group term life insurance with personal term or universal life insurance. • Take your old group term life insurance policy with you if possible. • Establish a home equity line of credit to verify employment. • Borrow against your pension plan only as a last resort.

If you have lost your job or your salary has been depressed, negotiate your departure and get an attorney if you believe you lost your position through breach of contract or discrimination. Then execute the following steps to recalculate your budget and boost your wealth rebuilding activities.

• Prioritize fixed monthly bills in the following order: rent or mortgage; car payments; utility bills; minimum credit card payments; and restructured long-term debt.

• Consider liquidating assets to pay off debts in this order: emergency fund, checking accounts, investment accounts or assets held in your children’s names.

• Review insurance coverage and increase deductibles on homeowner’s and automobile insurance for needed cash.

• Then sell appreciated stocks or mutual funds; personal valuables such as furnishings, jewelry and real estate; and finally, assets not in pension or annuities if necessary.

• Keep or rollover any lump sum pension or savings plan distribution directly to a similar savings plan at your new employer, if possible, when you get rehired.

• Apply for unemployment insurance.

• Review your medical insurance and COBRA coverage after a “qualifying event” such as job loss, firing or even after quitting. It is a bit expensive due to a 2 percent administrative fee surcharge but this may be well worth it for those with preexisting conditions or who are otherwise difficult to insure. One may continue COBRA for up to 18 months.

• Consider a high deductible Health Savings Account (HSA), which allows tax-deferred dollars like a medical IRA, for a variety of costs not normally covered under traditional heath insurance plans. Self-employed doctors deduct both the cost of the premiums and the amount contributed to the HSA. Unused funds roll over until the age of 59½, when one can use the money as a supplemental retirement benefit.

• Eliminate unnecessary variable, charitable and/or discretionary expenses, and become very frugal.

Final Notes

The behavioral psychologist, Gene Schmuckler, PhD, MBA, sometimes asks exasperated doctors to recall the story of the old man who spent a day watching his physician son treating HMO patients in the office. The doctor had been working at his usual feverish pace all morning. Although he was working hard, he bitterly complained to his dad that he was not making as much money as he used to make. Finally, the old man interrupted him and said, “Son, why don’t you just treat the sick patients?” The doctor-son looked at his father with an annoyed expression and responded, “Dad, can’t you see, I do not have time to treat just the sick ones.”5

Always remember to add a bit of emotional sanity into your budgeting and economic endeavors.6

Regardless of one’s age or lifestyle, the insightful doctor realizes that it is never too late to take control of a lost financial destiny through prudent wealth building activities. Personal and practice budgeting is always a good way to start the journey.7

The Author:

Dr. Marcinko is a former university endowed chairman and professor, former certified financial planner and has been a medical management advisor for more than two decades. He is the CEO of www.MedicalBusinessAdvisors.com, a health economics and business finance consulting firm.

References:

1. Marcinko DE (Ed). The Business of Medical Practice (Advanced Profit Maximizing Techniques for Savvy Doctors). Springer Publishers, New York, NY, 2000 and 2004 2. Marcinko DE (Ed). Financial Planning for Physicians and Advisors, Jones and Bartlett Publishers, Sudbury, MA, 2005 3. Marcinko DE (Ed). Risk Management and Insurance Panning for Physicians and Advisors, Jones and Bartlett Publishers, Sudbury, MA, 2006. 4. Marcinko DE, Hetico HR. The Dictionary of Health Insurance and Managed Care. Springer Publishing, New York, 2007. 5. Marcinko DE, Hetico HR. The Dictionary of Health Economics and Finance. Springer Publishing, New York, 2008. 6. Marcinko DE, Hetico HR. Healthcare Organizations (Financial Management Strategies). Standard Technical Publishers, Blaine, WA, 2009. Additional Reference 7. Schmuckler E. Bridging Financial Planning and Human and Human Psychology. In, Marcinko DE (Ed): Financial Planning for Physicians and Healthcare Professionals. Aspen Publications, New York, NY, 2001, 2002 and 2003.

DEFINITION: Mental accounting attempts to describe the process whereby people code, categorize and evaluate economic outcomes. The concept was first named by Richard Thaler. Mental accounting deals with the budgeting and categorization of expenditures. People budget money into mental accounts for expenses or expense categories

Mental Accounting is the act of bucketizing investments and then reviewing the performance of the individual buckets separately (e.g. investing at low savings rate while paying high credit card interest rates).

***

Examples of mental accounting are: (1) matching costs to benefits (wanting to pay for vacation before taking it and getting paid for work after it was done, even though from perspective of time value of money the opposite should be preferred0, (2) aversion to debt (don’t like long-term debt for short-term benefit), (3) sunk-cost effect (illogically considering non-recoverable costs when making forward-going decisions).

In investing, treating buckets separately and ignoring interaction (correlations) induces people not to sell losers (even though they get tax benefits), prevent them from investing in the stock market because it is too risky in isolation (however much less so when looked at as part of the complete portfolio including other asset classes and labor income and occupied real estate), thus they “do not maximize the return for a given level of risk taken).

U.S. medical education began in the late eighteenth century as an apprenticeship program in which physicians taught their trade to a few pupils, a pedagogical learning style which relied heavily upon the capacity, skills, and knowledge of the individual physician.[1] However, as learning newly discovered information and utilizing new technologies became more necessary to the industry’s practice, many physicians found the apprenticeship system no longer adequate as a manner of educating the next generation of physicians.[2] As a result, the conventional concept of medical education that originated in the U.S. in the 1750s was manifested through informal courses and demonstrations by private individuals or for-profit institutions. Those individuals who were not satisfied with a typical U.S. medical education, consisting of two identical 16-week lecture terms, might venture to Europe for a more formalized and detailed manner of learning.[3]

One of these students who studied in Europe was William Shippen, who began teaching an informal course on midwifery when he returned to the American colonies in 1762.[4] He later addressed the limitations of what might be taught in one informal course when he began teaching a lecture series on anatomy to help educate those who wished to be a physician, but could not travel abroad. John Morgan, a classmate of Shippen, noticed the potential of his friend’s endeavor and proposed the idea to create a professorship for the practice of medicine to the board of trustees of the College of Philadelphia.[5] Just across town, Thomas Bond, who conceived the idea of, and successfully established, the Pennsylvania Hospital with Benjamin Franklin, recognized the value to allowing medical students to participate in bedside training.[6] When Bond agreed to a partnership with the College of Philadelphia, the University of Pennsylvania became home to America’s first medical school.[7]

In 1893, Johns Hopkins University also made history by housing the first medical school that was able to operate out of a university-owned hospital.[8] The medical school not only encouraged clinical research to be performed by every member of their faculty, but the program also included a clinical research clerkship for every student during their rotation.[9] This program quickly became the model to which schools aspired and set the foundation for national medical education by connecting science and medical research with clinical medicine.[10]

With these early examples of medical schools, America’s field of medical education and clinical medicine made monumental strides. However, the societal pressures, caused by the U.S.’s population growth and demand for educated physicians,[11] did not allow many other universities to build on Johns Hopkins’ or the University of Pennsylvania’s foundation model, and led to the development of medical schools that had their own unique set of entrance and graduation requirements. While some focused entirely on medicine, other schools (termed Studia Generalia) also incorporated law, theology, and philosophy in their curricula.[12] In an attempt to both understand and make uniform the field of medical education, the American Medical Association (AMA) founded the Council on Medical Education (CME) in 1904.[13] The CME created minimum national educational standards for training physicians, and subsequently found that many schools did not meet these established standards.[14] However, the CME did not share the ratings of any of these medical schools “outside the medical fraternity.”[15]

In 1910, the AMA commissioned the Carnegie Foundation for Advancement of Teaching to conduct a study of medical education and schools.[16] Abraham Flexner conducted the inquiry and detailed his findings in what became known as The Flexner Report.[17] In his review of the U.S. medical education system, Flexner found that many of the proprietary medical schools met the AMA’s educational goals, but an imbalance existed between the pursuit of science and medical education.[18] Professors were focused solely on student throughput, and did not ensure a high level of medical training that reflected the developments in the medical industry.[19] As aptly noted by Dr. John Roberts in his book entitled The Doctor’s Duty to the State, “[m]any of you remember the struggle to wrest from medical teachers the power to create medical practitioners with almost no real knowledge of medicine. The medical schools of that day were, in many instances, conducted merely as money-makers for the professors.”[20] As the AMA gained more influence over the provision of healthcare in the U.S., the value and power of medical education also gained recognition. Notably, teaching hospitals had the power to influence the development of their disciplines through their research initiatives, the quality of care they provided, and their ability to operate as an economy of scale, allowing them to dictate the evolution of medical education.[21]

Since the establishment of the first medical school in the U.S., medical education has been the foundation for shaping standards of care in the practice of medicine and defining medical errors as deviations from the norms of clinical care.[22] When Thomas Bond helped establish the University of Pennsylvania medical school, he envisioned a normal day where the physician:

“…meets his pupils at stated times in the Hospital, and when a case presents adapted to his purpose, he asks all those Questions which lead to a certain knowledge of the Disease and parts affected; and if the Disease baffles the power of Art and the Patient falls a Sacrifice to it, he then brings his Knowledge to the Test, and fixes Honour [sic] or discredit on his Reputation by exposing all the Morbid parts to View, and Demonstrates by what means it produced Death, and if perchance he finds something unexpected, which Betrays an Error in Judgement [sic], he like a great and good man immediately acknowledges the mistake, and, for the benefit of survivors, points out other methods by which it might have been more happily treated.”[23]

Originally, students were to study and learn from medical errors and adverse events through medical education as a means of improving the quality of care. However, it is difficult to effectively implement any significant advancement learned through the research and investigation of prior errors in a timely and cost-effective manner. Additionally, physician supply shortages have only increased the amount of patients that a physician must see daily, while simultaneously decreasing the amount of time they can spend with each patient. Although medical education continues to be one of the central underpinnings to the development of the medical industry, outside pressures that shape the clinical practice of physicians continue to limit physician effectiveness in providing quality care to patients.[24]

While improving the quality and rigor of medical education has been a constant focus throughout the history of U.S. medical education, the challenges of replicating it on a scale that produces enough qualified physicians to meet the growing demands of the U.S. population, with constantly changing technologies, has consistently been a central issue. Notably, in the 13 years preceding 1980, the ratio of actively practicing physicians to patients increased by 50%.[25] This increased physician-to-patient ratio led to concerns over quality of care and cost-effectiveness, which in turn caused the creation of a government committee to evaluate physician manpower allocation and distribution. The Graduate Medical Education National Advisory Committee (GMENAC) was first chartered in April 1976, and later extended through September 1980.[26] Its purpose was to “analyze the distribution among specialties of physicians and medical students and to evaluate alternative approaches to ensure an appropriate balance,”as well as to“encourage bodies controlling the number, types, and geographic location of graduate training positions to provide leadership in achieving the recommended balance.”[27] GMENAC produced seven volumes of recommendations regarding physician manpower supply,[28] through the development of several models by which to determine the projected number of physicians that would be needed in the future by different subspecialties to achieve “a better balance of physicians.”[29] Ignoring critics of the report, U.S. medical schools adjusted their enrollment numbers in response to the GMENAC’s recommendations, causing a significant decrease in the supply of new physicians going into the 21st century.

***

[1] “Healthcare Valuation: The Four Pillars of Healthcare Value,” Volume 1, Robert James Cimasi, MHA, ASA, FRRICS, MCBA, CVA, CM&AA, John Wiley & Sons, Hoboken, NJ: 2014, p. 22-23.RR

[2] “Before There Was Flexner,” American Medical Student Association, 2014,

[8] “Time to Heal: American Medical Education from the Turn of the Century to the Era of Managed Care,” By Kenneth M. Ludmerer, New York, NY:

Oxford University Press, 1999, p. 18-19.

[9] “Time to Heal: American Medical Education from the Turn of the Century to the Era of Managed Care,” By Kenneth M. Ludmerer, New York, NY:

Oxford University Press, 1999, p. 18-19.

[10] “Science and Social Work: A Critical Appraisal,” By Stuart A. Kirk, and William James Reid, New York, NY: Columbia University Press, 2002, Chapter 1, p. 2-3.

[11] “The Flexner Report on Medical Education in the United States and Canada in 1910,” By Abraham Flexner, Bethesda, MD: Science and Health

Publications, Inc., p. 6-7.

[12] “Western Medicine: An Illustrated History,” By Irvine Loudon, New York, NY: Oxford University Press, 1997, p. 58.

[13] “Western Medicine: An Illustrated History,” By Irvine Loudon, New York, NY: Oxford University Press, 1997, p. 58.

[14] “Western Medicine: An Illustrated History,” By Irvine Loudon, New York, NY: Oxford University Press, 1997, p. 58.

[15] “Western Medicine: An Illustrated History,” By Irvine Loudon, New York, NY: Oxford University Press, 1997, p. 58.

[16] “U.S. Health Policy and Politics: A Documentary History,” By Kevin Hillstrom, Thousand Oaks, CA: CQ Press, 2012, p. 141.

[17] “The Flexner Report on Medical Education in the United States and Canada in 1910,” By Abraham Flexner, Bethesda, MD: Science and Health

Publications, Inc., p. 3-19.

[18] “The Flexner Report on Medical Education in the United States and Canada in 1910,” By Abraham Flexner, Bethesda, MD: Science and Health

Publications, Inc., p. 3-19.

[19] “The Flexner Report on Medical Education in the United States and Canada in 1910,” By Abraham Flexner, Bethesda, MD: Science and Health

Publications, Inc., p. 3-19.

[20] “The Doctor’s Duty to the State: Essays on The Public Relations of Physicians,” By John B. Roberts, AM, MD, Chicago, IL: American Medical Association Press, 1908, p. 23.

[21] “Time to Heal: American Medical Education from the Turn of the Century to the Era of Managed Care,” By Kenneth M. Ludmerer, New York, NY:

Oxford University Press, 1999, p. 19.

[22] “Science and Social Work: A Critical Appraisal,” By Stuart A. Kirk, and William James Reid, New York: Columbia University Press, 2002, Chapter 1, p. 2-3.

[23] “Dr. Thomas Bond’s Essay on the Utility of Clinical Lectures,” By Carl Bridenbaugh, Journal of the History of Medicine (Winter 1947), p. 14; “The Flexner Report on Medical Education in the United States and Canada in 1910,” By Abraham Flexner, Bethesda, MD: Science and Health

Publications, Inc., p. 4.

[24] “Time to Heal: American Medical Education from the Turn of the Century to the Era of Managed Care,” By Kenneth M. Ludmerer, New York, NY:

Oxford University Press, 1999, p. xxi.

[25] “How many doctors are enough?” By J.E. Harris, Health Affairs, Vol. 5, No. 4 (1986), p.74.

[26] “Report of the Graduate Medical Education National Advisory Committee to the Secretary, Department of Health and Human Services – Volume VII,” Graduate Medical Education National Advisory Committee, Washington, DC: U.S. Government Printing Office, 1981, p. 5, 16.

[27] “Report of the Graduate Medical Education National Advisory Committee to the Secretary, Department of Health and Human Services – Volume VII,” Graduate Medical Education National Advisory Committee, Washington, DC: U.S. Government Printing Office, 1981, p. 73.

[28] “Report of the Graduate Medical Education National Advisory Committee to the Secretary, Department of Health and Human Services – Volume VII,” Graduate Medical Education National Advisory Committee, Washington, DC: U.S. Government Printing Office, 1981, p. 5-6.

[29] “GMENAC: Its Manpower Forecasting Framework,” By D.R. McNutt, American Journal of Public Health, Vol. 71, No. 10 (October 1981), p. 1119.

[30] “Crossing the Quality Chasm: A New Health System for the 21st Century,” Institute of Medicine, National Academy of Sciences, 2001, front matter.

[31] “Overview of Medical Errors and Adverse Events,” By Maité Garrouste-Orgeas, et al., Annals of Intensive Care, Vol. 2, No. 2 (2012), p. 6.

The investment profession has come a long way since the door-to-door stock salesmen of the 1920s sold a willing public on worthless stock certificates. The stock market crash of 1929 and ensuing Great Depression of the 1930s forever changed the way investment operations are run. A bewildering array of laws and regulations sprung up, all geared to protecting the individual investor from fraud. These laws also set out specific guidelines on what types of investment can be marketed to the general public – and allowed for the creation of a set of investment products specifically not marketed to the general public. These early-mid 20th century lawmakers specifically exempted from the definition of “general public,” for all practical purposes, those investors that meet certain minimum net worth guidelines.

The lawmakers decided that wealth brings the sophistication required to evaluate, either independently or together with wise counsel, investment options that fall outside the mainstream. Not surprisingly, an investment industry catering to such wealthy individuals, such as doctors and healthcare professionals, and qualifying institutions has sprung up.

EARLY DAYS

The original hedge fund was an investment partnership started by A.W. Jones in 1949. A financial writer prior to starting his investment management career, Mr. Jones is widely credited as being the prototypical hedge fund manager. His style of investment in fact gave the hedge fund its name – although Mr. Jones himself called his fund a “hedged fund.” Mr. Jones attempted to “hedge,” or protect, his investment partnership against market swings by selling short overvalued securities while at the same time buying undervalued securities. Leverage was an integral part of the strategy. Other managers followed in Mr. Jones’ footsteps, and the hedge fund industry was born.

In those early days, the hedge fund industry was defined by the types of investment operations undertaken – selling short securities, making liberal use of leverage, engaging in arbitrage and otherwise attempting to limit one’s exposure to market swings. Today, the hedge fund industry is defined more by the structure of the investment fund and the type of manager compensation employed.

The changing definition is largely a sign of the times. In 1949, the United States was in a unique state. With the memory of Great Depression still massively influencing common wisdom on stocks, the post-war euphoria sparked an interest in the securities markets not seen in several decades. Perhaps it is not so surprising that at such a time a particularly reflective financial writer such as A.W. Jones would start an investment operation featuring most prominently the protection against market swings rather than participation in them.

Apart from a few significant hiccups – 1972-73, 1987 and 2006-07 being most prominent – the U.S. stock markets have been on quite a roll for quite a long time now. So today, hedge funds come in all flavors – many not hedged at all. Instead, the concept of a private investment fund structured as a partnership, with performance incentive compensation for the manager, has come to dominate the mindscape when hedge funds are discussed. Hence, we now have a term in “hedge fund” that is not always accurate in its description of the underlying activity. In fact, several recent events have contributed to an even more distorted general understanding of hedge funds.

During 1998, the high profile Long Term Capital Management crisis and the spectacular currency losses experienced by the George Soros organization both contributed to a drastic reversal of fortune in the court of public opinion for hedge funds. Most hedge fund managers, who spend much of their time attempting to limit risk in one way or another, were appalled at the manner with which the press used the highest profile cases to vilify the industry as dangerous risk-takers. At one point during late 1998, hedge funds were even blamed in the lay press for the currency collapses of several developing nations; whether this was even possible got short thrift in the press.

Needless to say, more than a few managers have decided they did not much appreciate being painted with the same “hedge fund” brush. Alternative investment fund, private investment fund, and several other terms have been promoted but inadequately adopted. As the memory of 1998 and 2007 fades, “hedge fund” may once again become a term embraced by all private investment managers.

Photo by Alexander Mils

ASSESSMENT: Physicians, and all investors, should be aware, however, that several different terms defining the same basic structure might be used. Investors should therefore become familiar with the structure of such funds, independent of the label. The Securities Exchange Commission calls such funds “privately offered investment companies” and the Internal Revenue Service calls them “securities partnerships.”

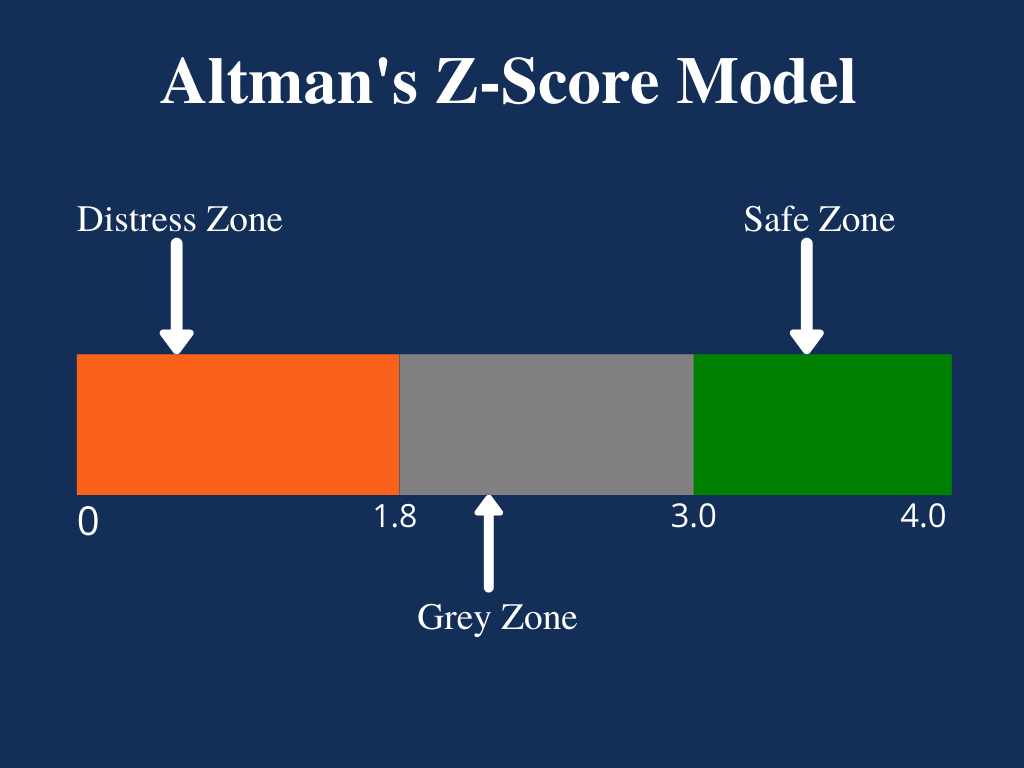

The Zeta Model is a mathematical model that estimates the chances of a public company going bankrupt within a two-year time period. The number produced by the model is referred to as the company’s Z-score (or zeta score) and is considered to be a reasonably accurate predictor of future bankruptcy.

The model was published in 1968 by New York University professor of finance Edward I. Altman. The resulting Z-score uses multiple corporate income and balance sheet values to measure the financial health of a company.

Posted on May 3, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd CMP

***

***

Medicare [Dis] Advantage Plans [Medicare Part C] commenced in 2003 or so and I have railed against them since then. First, for their low physician payments. And then as a patient advocate for the last decade. And, today, for both reasons. As a doctor and independent health insurance agent myself, believe me when I speak thusly.

Now, while Medicare Advantage plans are undoubtedly not the right choice for everyone, insurance companies still say there are some folks who will get exactly what they need from the plans and at a moderate price.

Nevertheless, Ernesto Jaboneta, the IT Director of California-based Medicare insurance agency Agent Pitstop, acknowledged there are many predatory salespeople who will jump to have you join a plan that doesn’t end up helping you in the long run. Still, there are precautions you can take to make falling into this trap less likely.

“The first thing anyone can do is invite along a family member or trusted friend to any appointments with an insurance agent,” Jaboneta told Newsweek. “Don’t feel pressured to decide right away.”

Before you commit to anything, you should compare plans and find out if your doctors will remain in your network. And if you’re unsure about some of the information you received from an insurance agent, you can also call 1-800-MEDICARE for more assistance.

Jaboneta also said there’s a big difference between captive insurance agents and independent agents, as well, and seniors should take note of this.

“A captive agent is an insurance agent who works directly for an insurance carrier,” Jaboneta said. “They have no incentive to compare options outside their own company, which is different than an independent agent who can compare all the options available. In many cases, when a beneficiary calls into an insurance company to find information, they will be talked into enrolling.”

The open enrollment period lasts from October 15th to December 8th, but there’s another enrollment period from January 1st to March 31st for anyone unhappy with their Medicare Advantage plan who wants to switch or revert to Medicare.

INVESTING UPDATE: Managed-care companies are reporting that seniors on Medicare Advantage Part C plans used far more medical services than expected in the final months of 2023. The announcements have sparked two separate selloffs over the past week: The first came January 12th, when UnitedHealth Group announced its fourth-quarter earnings. The second came after Humana just laid out preliminary fourth-quarter results, and said the high utilization trends would have a material impact on its 2024 performance “if current trends continue.”

It is critical to understand and to measure the total cost of capital. Lack of understanding and appreciation of the total cost of capital is widespread, particularly among not-for-profit hospital executives. The capital structure includes long-term debt and equity; total capital is the sum of these two. Each of these components has cost associated with it. For the long-term debt portion, this cost is explicit: it is the interest rate plus associated costs of placement and servicing.

Equity portion

For the equity portion, the cost is not explicit and is widely misunderstood. In many cases, hospital capital structures include significant amounts of equity that has accumulated over many years of favorable operations. Too many executives wrongly attribute zero cost to the equity portion of their capital structure. Although it is correct that generally accepted accounting principles continue to assign a zero cost to equity, there is opportunity cost associated with equity that needs to be considered. This cost is the opportunity available to utilize that capital in alternative ways.

***

***

In general, the cost attributed to equity is the return expected by the equity markets on hospital equity. This can be observed by evaluating the equity prices of hospital companies whose equity is traded on public stock exchanges. Usually the equity prices will imply cost of equity in the range of 10% to 14%.

Almost always, the cost of equity implied by hospital equity prices traded on public stock exchanges will substantially exceed the cost of long-term debt. Thus, while many hospital executives will view the cost of equity to be substantially less than the cost of debt (i.e., to be zero), in nearly all cases, the appropriate cost of equity will be substantially greater than the cost of debt.

Hospitals need to measure their weighted average cost of capital (WACC).

WACC is the cost of long-term debt multiplied by the ratio of long-term debt to total capital plus the cost of equity multiplied by the ratio of equity to total capital (where total capital is the sum of long-term debt and equity).

WACC is then used as the basis for capital charges associated with all capital investments. Capital investments should be expected to generate positive returns after applying this capital charge based on the WACC. Capital investments that don’t generate returns exceeding the WACC consume enterprise value; those that generate returns exceeding WACC increase enterprise value.

Assessment

Hospital executives need to be rewarded for increasing enterprise value.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on May 1, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

***

By Dr. David Edward Marcinko MBAMEd CMP

***

According to George Washington University, a hospital chargemaster is a comprehensive list of a hospital’s products, procedures, and services. Everything from prescription drugs to supplies for diagnostic tests has a unique price listing in the chargemaster, making it a go-to document for hospital administrators such as CFOs, clinical documentation improvement specialists, and revenue directors.

Chargemaster usage dates back to the mid-20th century. At that time, fee-for-service (FFS) health insurance plans, which allow patients to direct their medical care by choosing physicians and facilities and paying a portion of the billed total, had just emerged in the U.S. healthcare system.

The chargemaster originally served as something akin to an FFS dictionary, with an entry for virtually anything billable under that economic model of healthcare.

Over time, FFS itself has evolved and been challenged by alternatives like value-based care (VBC). Chargemasters built for FFS have changed accordingly, and they remain fixtures of the modern hospital revenue cycle. A standard chargemaster is a large electronic file containing multiple elements for each entry. These attributes usually include:

The charge for a single unit of the service in question

A Current Procedural Terminology (CPT) code; CPT is the official medical code set of the American Medical Association

Potentially, a Healthcare Common Practice Coding System (HCPCS) code; HCPCS is based on CPT

Alternative CPT and HCPCS codes if needed, e.g. one corresponding only to specific payers

A revenue code associated with the charge

Flag(s) indicating if the entry is scheduled for deletion, active or inactive

An internal reference number within the ledger for accounting purposes

It is critical for physician executives to understand and to measure the total cost of hospital capital. Lack of understanding and appreciation of the total cost of capital is widespread, particularly among not-for-profit hospital and physician executives. The capital structure includes long-term debt and equity; total capital is the sum of these two, and, each of these components has cost associated with it.

For the long-term debt portion, this cost is explicit—it is the interest rate plus associated costs of placement and servicing. For the equity portion, the cost is not explicit and is widely misunderstood. In many cases, hospital capital structures include significant amounts of equity that has accumulated over many years of favorable operations.

Far too many executives wrongly attribute zero cost to the equity portion of their capital structure. Although it is correct that generally accepted accounting principles continue to assign a zero cost to equity, there is opportunity cost associated with equity that needs to be considered. This cost is the opportunity available to utilize that capital in alternative ways.

***

***

In general, the cost attributed to equity is the return expected by the equity markets on hospital equity. This can be observed by evaluating the equity prices of hospital companies whose equity is traded on public stock exchanges. Usually, the equity prices will imply cost of equity in the range of 10%–14%. Almost always, the cost of equity implied by hospital equity prices traded on public stock exchanges will substantially exceed the cost of long-term debt. Thus, while many hospital executives will view the cost of equity to be substantially less than the cost of debt (i.e., to be zero) in nearly all cases, the appropriate cost of equity will be substantially greater than the cost of debt.

Hospitals need to measure their weighted average cost of capital (WACC). WACC is the cost of long-term debt multiplied by the ratio of long-term debt to total capital plus the cost of equity multiplied by the ratio of equity to total capital (where total capital is the sum of long-term debt and equity).

WACC is then used as the basis for capital charges associated with all capital investments. Capital investments should be expected to generate positive returns after applying this capital charge based on the WACC. Capital investments that do not generate returns exceeding the WACC consume enterprise value; those that generate returns exceeding WACC increase enterprise value. Therefore, physician and hospital executives need to be rewarded for increasing enterprise value.

Posted on April 26, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Big Artificial Intelligence Spending Boosts Meta’s Cost Structure!

Meta [Facebook, FB] reported record Q1 revenue yesterday, but it was overshadowed by the billions the company is spending in its efforts to win the AI race and to try to make the metaverse happen. Investors were displeased with the company’s forecast that its spending will rise by $10 billion to support AI development, sending Meta’s stock price down 15% after hours.

Now, the metaverse is a vision of a virtual reality where people can socialize, work, play, and explore in immersive digital spaces.

But CEO Mark Zuckerberg urged them to keep the faith, saying, “We’ve historically seen a lot of volatility in our stock during this phase of our product playbook.”

First held on April 22, 1970, it now includes a wide range of events coordinated globally by EARTHDAY.ORG (formerly Earth Day Network) including 1 billion people in more than 193 countries.[ The official theme for 2024 is “Planet vs. Plastics.” 2025 will be the 55th anniversary of Earth Day.

Posted on April 17, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

If you need a reprieve to prevent the government from raiding your bank account, you’re not alone—the IRS expects 19 million people to file for an extensionthis year. The agency will automatically grant you a six-month extension, although it’s recommended you remit a payment by April 15th if you expect to owe money to avoid interest and penalties. The good news is you probably won’t have to fork over as much as Mark Cuban, who said he is sending the IRS $288 million today and is proud to pay his fair share.

The stock market is coming off its worst week of the year, and the road ahead is no less bumpy. A direct military confrontation between Iran and Israel has investors on edge about a wider regional war that threatens energy supplies. Amid the uncertainty, safe-haven assets are seeing major interest: The US dollar just had its best week in more than 18 months.

Questions – from doctors – like these remind me that the workings of the financial services industry which I tend to take for granted but can be confusing to people outside the field.

The following analogy may help to explain.

Orchestra Analogy

Think of an orchestra. The investment adviser is the equivalent of the director/conductor and the money managers are the instrumentalists. Each one is a specialist who plays a particular type of instrument, and it takes a variety of these specialists to make up the orchestra.

Specialists

The broad specialties are the types of instruments, such as strings, brass, winds, and percussion. These are the equivalent of fund managers who specialize in asset classes like equities, bonds, real estate, commodities, and absolute returns.

Sub-Specialists

Within each specialty are a variety of subspecialists. Winds, for example, include clarinets, oboes, and saxophones—which are further divided into alto, soprano, tenor, and bass. The brass section has French horns, trumpets, and trombones. The divisions and sub-divisions go on and on. Similarly, within the various asset classes are a great many mutual fund managers who specialize in narrower subcategories.

Conductor

The task of the orchestra conductor-director is to pick, not just the best musicians, but the best mix of musicians. A group with only trumpets or every subspecialty of percussion, no matter how skilled, isn’t an orchestra. Before auditioning a single musician, the director’s first task is to clarify the purpose of the ensemble being created. A different mix of instruments will be required for a symphony, a marching band, an intimate chamber group, or a dance band. It all depends on what the audience wants.

The conductor-director needs to weigh the various musicians’ abilities against their cost and their specific specialties against the needs of the orchestra. When the right mix of players has been chosen, the director needs to pick the appropriate music, assemble the group, and rehearse. The director’s talent, experience, and leadership skills all serve to help the right players produce the right sound for their audiences.

***

***

It takes similar coordination and skill to put together the right mix of asset classes and mutual fund managers to produce the best results for various clients, especially since there are some 17,000 mutual funds to choose from.

Fees

Just as both the orchestra director and the musicians are paid based on their skills and their work, both mutual fund managers and investment advisers are paid based on the assets they manage. Mutual fund managers earn 0.05% to 3.0%. Financial advisers earn 0.30% to 3.0%. An informed consumer could pay as low as 0.35% while an uninformed consumer could pay up to 6% a year, which would eat up most of the investment returns.

One essential responsibility for an adviser, then, is to choose mutual fund managers whose fees are low.

However, the cost of the mutual fund manager isn’t the be-all and end-all. One must also weigh performance, just as an orchestra director might pay more to get an outstanding musician who would add significant value to the performances.

Example:

For example, my firm’s overall average fee for mutual fund managers is 0.5%. We could get that as low as 0.1%, which might be impressive at first glance.

However, we would give up 0.25% to 1.00% of net return in some areas, resulting in poorer outcomes for the clients.

***

***

Assessment

Skilled direction of an orchestra is obviously more art than science. Skilled coordination of mutual fund managers is the same. Both require knowledge, integrity, and commitment to the quality of the final product.

Channel Surfing the ME-P

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on April 13, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Medial Office Equipment Interest Rate Costs

Dr. David E. Marcinko; MBA, MEd, CMP™

[Publisher in Chief]

Physicians, administrators and healthcare entrepreneurs are aware of the compounding effect of interest.However, since interest is deductible as a medical office business expense, many seem to forget about it despite the fact that it must be continually paid until the asset is either purchased or otherwise disposed.

So, what are the various types of interest rates important to the medical practitioner and commodity – money?

[1] Simple Interest

Simple interest is merely the pro rata interest on a loan or deposit and represents the most basic interest rate type.

For example, for every $100 Dr. Bill borrows at 12 percent annual interest, he pays twelve dollars per year. The interest is calculated by multiplying the principal or original amount, by the interest rate in decimal form (100 x .12).

[2] Add-On Interest

Add on interest immediately attaches the annual interest amount, to the principal amount, at the beginning of the payment period. Payments are then made according to the number of years required.

The following formula is useful:

Add-on-Interest minus Payment = Total Interest on Balance/Number of Payments

For example, if Dr. William Needy borrows $10,000 at 8 percent add-on interest, he will repay $10,000 plus $ 800 ($10,000 x 8%) or $10,800, divided by twelve months, for a total of $900 per month, since $ 900/month x 12 months equals $10,800.

[3] Discounted Interest

When using the discounted interest method, the interest amount is deducted from the principal right up front. Notice that this is the opposite of add-on-interest that is applied up front.

For example, if Dr. Bill borrows the same $ 10,000 at a discounted interest rate of 8 percent, he will only receive a $9,200 loan, since $10,000 – $800 is $9,200.

Obviously, the discount method is the most expense way to borrow money.

[4] Annual Percentage Rate

Most financial institutions advertise an annual percentage rates (APR) for loans, deposits and investments. The APR is the periodic interest rate multiplied by the number of periods a year. If the APR is 12 percent, and interest is compounded monthly, you receive (or pay) 1 percent of your balance each month, and the balance shifts with each compounding.

For example, if Dr. Bill deposits $ 100 dollars at 12 percent APR compounded monthly, he receives $ 1 interest the first month (1% of $100), $1.10 the second month (1% of $101), and so forth. If compounding is daily, the interest accumulates at the rate of 1/365 of the APR each day.

Unless interest is compounded annually, the APR will be lower than the effective annual interest rate, discussed below.

[5] Effective Interest Rate

It is important to differentiate between the effective interest rate and the APR, which is often the most prominent figure in advertisements for medical business equipment, consumer goods and financial services (loans, annuities, IRAs, CDs, investment analysis, college funding or retirement planning). Although the APR is the periodic interest rate multiplied by the number of periods per year, the effective annual interest rate is the periodic rate, compounded.

In our case, if the APR is 12 percent, compounded monthly, the monthly interest rate is 1 percent and the effective annual rate is the monthly rate compounded for 12 periods.

Therefore, if your calculation is for a single year, you can treat the effective rate as simple interest. If you deposit (or borrow) $1,000 at 12 percent APR, the effective rate is 12.68 percent, and interest for the first year is about $126.80 (12.68% of $1,000).

For longer periods, you can use the effective interest rate as the periodic interest rate, compounded annually.

[a] “Rule of 72” (Double your Money)

The number of periods required to double a lump sum of money can be quickly estimated by using what is known as the “Rule of 72”. To get the number of periods, usually years, just divide 72 by the periodic interest rate, expressed as a whole number (not a decimal).

For example, if the annual interest rate is 10 percent, it will take about 7.2 years (72/10) to double any lump cache of money. Conversely, you can also calculate the interest rate required to double your money in a given period by dividing 72 by the term.

Thus, to double your money in ten years, you need to earn about 7.2 percent annual interest (72/10) = 7.2%).

[b] “Rule of 78”

According to this method, interest is front end loaded like a home mortgage, or office condominium, to discourage prepayment of a loan and consequently preserve the lender’s profit. In other words, it is a method of calculating installment loan interest rebates.

The number 78 comes from an approved method of accelerated tax depreciation, known as the “Sum of the Years Digits” (SOYD) method (i.e., 12 + 11 + 10 + 9 . . . = 78). This fact is important because, throughout the period of a loan, even though the payments are all the same, the portions that are interest and principal are very different.

Using this method for a one year loan shows that, in the first payment, 15.38 percent of the interest due is paid off, and by the sixth month, 73.08 percent of the interest is paid off. This means, that if a physician makes a one year equipment loan with a total interest charge of $ 100 and pays the loan off in full with the sixth payments, he or she will not get an interest rebate of $ 50, but only $ 26.92, since $ 73.08 of the interest has already been prepaid.

Most ethical lenders use simple interest rates for loan rebates, and the Rule of 78 is unfair according to many authorities.

[c] “Rule of 116”

A derivative of the Rule of 72 is the Rule of 116. This determines the number of years it takes for a principal amount to be tripled and is calculated by dividing the annual interest rate into 116.

The Rules of 72 and 78 are very handy for figuring the amount of interest payments made or growth of funds invested. They can also be used in reverse to calculate at what rate of interest money must be invested to double or triple in a certain number of years.

[6] Medical Equipment Payback Cost Analysis

The payback period, expressed in years, is the length of time that it takes for the medical equipment investment to recoup its initial cost out of the cash receipts it generates. The basic premise is that the quicker the cost of an investment can be recovered, the better the investment is. It is most often used when considering equipment whose useful life is short and unpredictable.

When the same cash flow occurs every year, the formula is as follows:

Investment Required / Net Annual Cash Inflow = Payback Period

Thus, in today’s tightening medical reimbursement atmosphere, practice cost control and expense reduction is the easiest method to increase medical office profitability. Keeping the cost of the commodity money in the form of interest rate charges, as low as possible, will assist in this endeavor

Assessment

And so, how have these rules affected your medical office borrowing costs; if at all? Does these principles apply to the medical student loan crisis, today?

Posted on April 9, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Versus Di-Versification

BUSINESS MANAGEMENT: The term “diworsification” was coined by legendary investor Peter Lynch in his book, One up on Wall Street, to describe the over-expansion of a company into new growth projects and businesses they do not fully understand and which do not align with the company’s core competencies.

PORTFOLIO MANAGEMENT: The term diworsification has since grown to also refer to over-diversifying an investment portfolio in such a way that it reduces the overall risk-return characteristics.

Posted on April 4, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Bertalan Meskó, MDPhD

***

***

What are you going to do 10-20 years from now? We toyed with the idea and came up with a list of healthcare jobs we think will be born in the coming decades. In case you want to become an organ designer or an end-of-life therapist. OR telesurgery VR planner.

And before you say I’m looking too far into the future, let me remind you that researchers are experimenting with a computer made of DNA-coated microbeads, with wireless charging of electronic implants, an Osaka hospital uses smart glasses to connect remote teams, while the FDA cleared an A.I. software automatically flagging cases of pneumothorax.

I hope you will find the newsletter useful!

Best regards, Bertalan Meskó, MD PhD The Medical Futurist

Posted on April 2, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

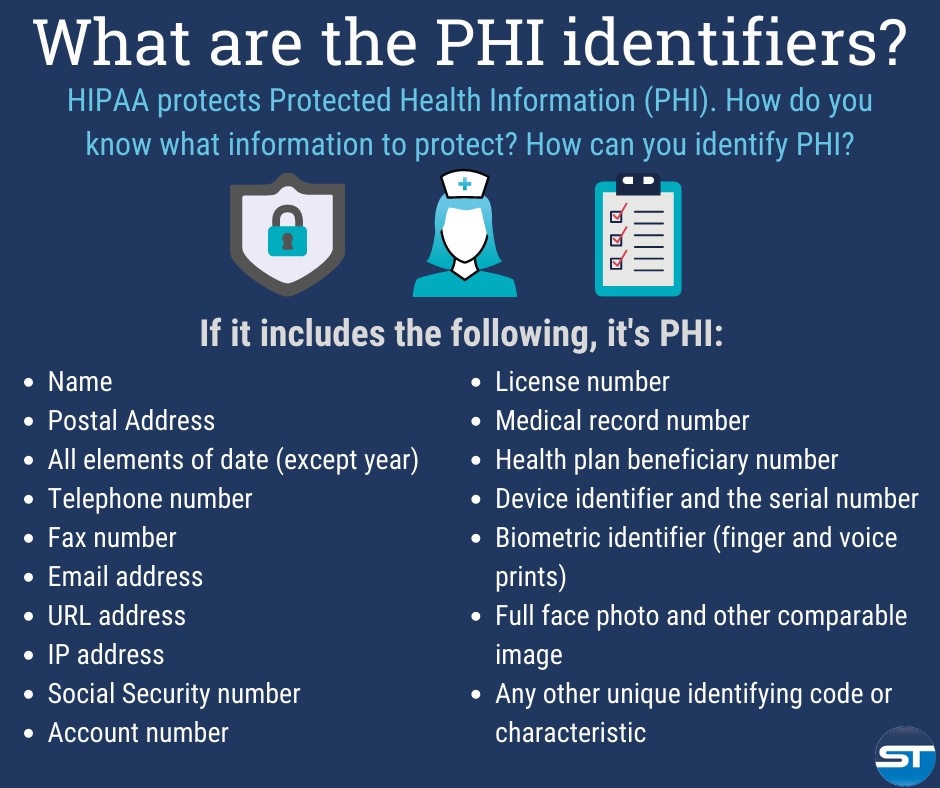

The Designated Medical Record Set [DMRS]: Contains medical and billing records and any other records that a physician, hospital, clinic and/or medical practice utilizes for making decisions about a patient; a hospital, emerging healthcare organization, or other healthcare organization. It serves to define which set of information comprises “protected health information” and which set does not; or contains medical or mixed billing records, and any other information that a physician and/or medical practice utilizes for making decisions about a patient.

It is up to the hospital or healthcare organization to define which set of information comprises “protected health information” and which does not though logically this should not differ from locale to locale. The patient has the right to know who in the lengthy data chain has seen their Protected Health Information. This sets up an audit challenge for the medical organization, especially if the accountability is programmed, and other examiners view the document without cause.

Posted on March 29, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

DIVIDEND REINVESTMENT PLANS

By Staff Reporters

***

DEFINITION

DRIPs are merely an automated strategy in which a company’s dividends are reinvested into additional shares of that company. Instead of being paid dividends in cash, you get additional shares of ownership in the company.

There are three ways to get involved in DRIPs: directly through the company, through your broker, or through a transfer agent.

Company-run DRIPs are generally only available through large, blue-chip dividend stocks.That’s because smaller companies don’t want to take on the overhead costs of tracking all their shareholders and going through the paperwork headache of calculating how much each one gets in dividends and additional fractional shares. The company benefits from gaining an additional source of capital, but most of all in creating a more stable base of shareholders, ones who are less likely to panic and sell during a market decline. This can help decrease the volatility of a company’s shares.

Finally, most large discount brokers, such as Scottrade, TD Ameritrade, and E*Trade, also offer DRIPs, though with different requirements and limitations.

While dividend reinvestment is powerful, there are a couple reasons why you might not want to reinvest your dividends.

DRIPs Drawback 1: You may need the dividend income The most obvious reason is that you need the income. If you’re in the “distribution” phase of your investing life, dividends are a perfect source of passive income. Income from qualified dividends is taxed at the long-term capital gains rate (currently 15% for investors who are in the 25% to 35% tax bracket for ordinary income, 0% for taxpayers in a lower bracket and 20% for those in the highest bracket). So if you’re going to be looking to your portfolio for income every month anyway, it makes sense to have that cash deposited in your account.

DRIPs Drawback 2: You may need to reallocate your positions You might also choose to stop reinvesting your dividends for allocation reasons. Reinvesting your dividends, through DRIP plans or otherwise, will cause your stock positions to grow over time, and if you’ve owned a particular issue for a long time, it may already be a large enough percentage of your portfolio. Higher-yielding positions will grow faster, which can throw your allocations out of whack pretty quickly. So once a stock position is as big as you want it to get (for now) feel free to turn off dividend reinvestment for that position, and either enjoy the extra income or save up the cash to invest in other stocks.

DRIPs Drawback 3: You may not want to buy that stock at that time Finally, you may also have stock-specific reasons not to reinvest dividends—if a stock is temporarily overvalued, or you simply don’t want to buy any more of it at current prices.

But bottom line, reinvesting dividends through a broker or by signing up for DRIP plans directly through the dividend-paying companies, is a surprisingly powerful tool to passively improve your investment returns.

***

NOTE: Former Microsoft CEO Steve Ballmer is on pace to earn $1 billion in dividends annually from his massive 4% stake in the software company.

Steve Ballmer is on pace to collect annual dividend payments of $1 billion from Microsoft.

He is the former CEO of Microsoft and is the largest individual shareholder of the software giant.