BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Tax avoidance—An action taken to lessen tax liability and maximize after-tax income.

Tax evasion—The failure to pay or a deliberate underpayment of taxes.

Underground economy—Money-making activities that people don’t report to the government, including both illegal and legal activities.

Voluntary compliance—A system of compliance that relies on individual citizens to report their income freely and voluntarily, calculate their tax liability correctly, and file a tax return on time.

Posted on March 20, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Stat: $1.2 billion. That’s how much San Diego-based Scripps Health plans to spend building a new hospital in San Marcos, California. (Becker’s Hospital Review)

Read: What WHO Director-General Tedros Adhanom Ghebreyesus said about USAID cuts. (Stat)

Pharm fresh: Check out in-depth strategies designed to help increase engagement between pharma reps and primary care clinicians. It’s all right here in Pri-Med’s research. Read the report.

Shares of Charles Schwab Corp. SCHW+1.51% rallied 1.51% to $78.73 Wednesday, on what proved to be an all-around favorable trading session for the stock market, with the S&P 500 IndexSPX+1.08% rising 1.08% to 5,675.29 and the Dow Jones Industrial AverageDJIA+0.92% rising 0.92% to 41,964.63.

Posted on March 19, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

Rocking Financial Planning … Old School Advice!

By Dr. David E. Marcinko MBBS MBA MEd CMP®

The economic platitude of the past, such as don’t spend more than 15-20 percent of your net salary on food, or 5-10 percent on medical care, among others, have given rise to the more individualized personal financial ratio concept. Personal ratios, like business ratios, represent benchmarks to compare such parameters as debt, income growth and net worth.

According to Edward McCarthy MIB CFP® – a personal financial expert from Warwick, Rhode Island whom I interviewed about a decade ago – the following represented useful ratios for the lay as well as medical professional [personal communication].

The Ratios:

Basic Liquidity Ratio = liquid assets / average monthly expenses. Should be 4-6 months, or even longer, in the case of a medical professional employed by a financially insecure HMO. In a low interest rate environment, iMBA Inc offers 12-24 months for consideration.

Debt to Assets Ratio = total debt / total assets. A percentage which is high initially, and should decrease with age as the medical professional approaches a debt free existence

Debt to Gross Income Ratio = annual debt repayments / annual gross income. A percentage representing the adequacy of current income for existing debt repayments. Medial professionals should try to keep this below 25-30%.

Debt Service Ratio = annual debt re-payment / annual take-home pay. Medical professionals should try to keep this ratio below about 40%, or have difficulty paying down debt.

Investment Assets to Net Worth-Ratio = investment assets / net worth. This ratio should increase over time, as retirement for the medical professional approaches.

Savings to Income Ratio = savings / annual income. This ratio should also increase over time, especially as major obligations are retired.

Real Growth Ratio = (income this year – income last year) / (income last year – inflation rate). It is desirable for the medical professional to keep this ratio growing faster than the core rate f inflation.

Growth of Net-Worth Ratio = (net worth this year – net worth last year) / net worth last year – inflation rate. Again, this ratio should stay ahead of inflation.By calculating these ratios, perhaps on an annual basis, the medical professional can spot problems, correct them, and continue progressing toward stated financial goals.

Assessment

Now, after ten years, are these traditional ratios and advice still valid today: why or why not?

***

***

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

SO – HOW MUCH IS A “FINANCIAL ADVISOR” REALLY WORTH?

This blog holds a rather uncomplimentary opinion of financial advisors, and the financial services and brokerage industry as a whole; deserved, or not? The entire site hints at this attitude as well, in favor of a going it alone or ME, Inc investing when possible. Nevertheless, it is reasonable to wonder how much boost in net-returns might an educated and informed, fee transparent and honest, fiduciary focused “financial advisor” add to a clients’ investment portfolio; all things being equal [ceteris paribus].

And, can it be quantified?

Well, according to Vanguard Brokerage Services®, perhaps as much as 3%? In a decade long paper from the Valley Forge, PA based mutual fund and ETF giant, Vanguard said financial advisors can generate returns through a framework focused on five wealth management principles:

• Being an effective behavioral coach: Helping clients maintain a long-term perspective and a disciplined approach is arguably one of the most important elements of financial advice. (Potential value added: up to 1.50%).

• Applying an asset location strategy: The allocation of assets between taxable and tax-advantaged accounts is one tool an advisor can employ that can add value each year. (Potential value added: from 0% to 0.75%).

• Employing cost-effective investments: This component of every advisor’s tool kit is based on simple math: Gross return less costs equals net return. (Potential value added: up to 0.45%).

• Maintaining the proper allocation through rebalancing: Over time, as investments produce various returns, a portfolio will likely drift from its target allocation. An advisor can add value by ensuring the portfolio’s risk/return characteristics stay consistent with a client’s preferences. (Potential value added: up to 0.35%).

• Implementing a spending strategy: As the retiree population grows, an advisor can help clients make important decisions about how to spend from their portfolios. (Potential value added: up to 0.70%).

Source: Financial Advisor Magazine, page 20, April 2014.

Assessment

However, Vanguard notes that while it’s possible all of these principles could add up to 3% in net returns for clients, it’s more likely to be an intermittent number than an annual one because some of the best opportunities to add value happen during extreme market lows and highs when angst or giddiness [fear and greed] can cause investors to bail on their well-thought-out investment plans.

And, is the study applicable to doctors and allied healthcare providers? Doe Vanguard have a vested interest in the topic. What about fee based versus fee-only financial advice?

Conclusion

Finally, recognize the plethora of other financial planning life-cycle topics addressed in this ME-P were not included in the Vanguard investment portfolio-only study a decade ago.

And what about today with contemporaneous internet advising, chat-rooms, linkedin, robo-advisors, reddit and the like?

Posted on March 17, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BANK IDENTIFICATION NUMBER – DEFINED

By Staff Reporters

***

***

What Is a BIN Attack?

The BIN, or the Bank Identification Number, is the first six digits on a credit card. These are always tied to its issuing institution – usually a bank. In a BIN attack, fraudsters use these six numbers to algorithmically try to generate all the other legitimate numbers, in the hopes of generating a usable card number.

How Does a BIN Attack Work?

Fraudsters conduct BIN attacks by generating hundreds of thousands of possible credit card numbers and testing them out.

A fraudster looks up the BIN of the bank they will target. Ranging from four to six digits, this information is in the public domain and is thus easy to source.

Using dedicated software such as an auto-dialer, they generate thousands, often tens of thousands, combinations of possible existing card numbers by this issuer.

At this point, these credentials need to be tested. The fraudster identifies a suitable online shop or donation page.

They start card testing by attempting a small payment with each generated card number.

They keep track of the small percentage of card details that worked, which they are ready to use in earnest for their fraudulent pursuits.

***

***

Remember that the fraudster will start off with only six digits, yet there are many more card details required for a successful transaction. If those are entered erroneously, the transaction will decline. This includes the CVV number, the expiration date, as well as likely address verification service (AVS) failures. Card testing transactions are executed remotely in a fast fashion, so distance checks should also be a hint as well as velocity alerts.

Fraudsters may use bad merchant accounts directly for this purpose, or more frequently involve multiple online stores and services during a BIN attack, as their attempts keep getting blocked at most outlets.

When analyzing a set of financial statements to determine practice value, adjustments (normalizations) generally are needed to produce a clearer picture of likely future income and distributable cash flow. It also allows more of an “apples to apples” line item comparison. This normalization process usually consists of making three main adjustments to a medical practice’s net income (profit and loss) statement.

1. Non-Recurring Items: Estimates of future distributable cash flow should exclude non-recurring items. Proceeds from the settlement of litigation, one-time gains/losses from the selling of assets or equipment, and large write-offs that are not expected to reoccur, each represent potential nonrecurring items. The impact of nonrecurring events should be removed from the practice’s financial statements to produce a clearer picture of likely future income and cash flow.

2. Perquisites: The buyer of a medical practice may plan to spend more or less than the current doctor-owner for physician executive compensation, travel and entertainment expenses, and other perquisites of current management. When determining future distributable cash flow, income adjustments to the current level of expenditures should be made for these items.

3. Non-cash Expenses: Depreciation expense, amortization expense, and bad debt expense are all non-cash items which impact reported profitability. When determining distributable cash flow, you must analyze the link between non-cash expenses and expected cash expenditures.

The annual depreciation expense is a proxy for likely capital expenditures over time. When capital expenditures and depreciation are not similar over time, an adjustment to expected cash flow is necessary. Some practices reduce income through the use of bad debt expense rather than direct write-offs. Bad debt expense is a non-cash expense that represents an estimate of the dollar volume of write-offs that are likely to occur during a year. If bad debt expense is understated, practice profitability will be overstated.

***

***

Balance Sheet Adjustments

Adjustments also can be made to a practice’s balance sheet to remove non-operating assets and liabilities, and to restate asset and liability value at market rates (rather than cost rates). Assets and liabilities that are unrelated to the core practice being valued should be added to or subtracted from the value, depending on whether they are acquired by the buyer.

Examples include the asset value less outstanding debt of a vacant parcel of land, and marketable securities that are not needed to operate the practice. Other non-operating assets, such as the cash surrender value of officer life insurance, generally are liquidated by the seller and are not part of the business transaction.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com

Health actuaries analyze potential risks, profits and trends that will affect their employers, which are often in the health insurance, government health services and medical provider industries. They advise companies on issuing policies to consumers based on risks, calculated premiums and upcoming changes in health-care costs.

It’s common for an actuary to have a bachelor’s degree or higher in actuary studies, mathematics or statistics. Coursework on medical terminology and hierarchy of the medical field is also beneficial. In addition to academic education, certification is also necessary to reach “professional status,” which is required by most employers.

***

***

The professional organization, Society of Actuaries, certifies actuaries in the health and medical field. Their statistical work is commonly done with predictive tables, probability tables and life tables that are created on customized statistical analysis software such as Stata or XLSTAT.

The actuary field as a whole is growing faster than other fields, according to the Bureau of Labor Statistics [BLS]. In 2020, it expanded by 27 percent. The average annual salary for an actuary in 2010 was $87,650. More specifically, in the health insurance field, the salary was slightly higher at $91,000.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com

Posted on March 16, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

DEFINITION

***

***

According to Wikipedia, a tontine (/ˈtɒntaɪn, -iːn, ˌtɒnˈtiːn/) is an investment linked to a living person which provides an income for as long as that person is alive. Such schemes originated as plans for governments to raise capital in the 17th century and became relatively widespread in the 18th and 19th centuries.

Tontines enable subscribers to share the risk of living a long life by combining features of a group annuity with a kind of mortality lottery. Each subscriber pays a sum into a trust and thereafter receives a periodical payout. As members die, their payout entitlements devolve to the other participants, and so the value of each continuing payout increases. On the death of the final member, the trust scheme is usually wound up.

Tontines are still common in France. They can be issued by European insurers under the Directive 2002/83/EC of the European Parliament. The Pan-European Pension Regulation passed by the European Commission in 2019 also contains provisions that specifically permit next-generation pension products that abide by the “tontine principle” to be offered in the 27 EU member states.

Questionable practices by U.S. life insurers in 1906 led to the Armstrong Investigation in the United States restricting some forms of tontines. Nevertheless, in March 2017, The New York Times reported that tontines were getting fresh consideration as a way for people to get steady retirement income.

Posted on March 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS

By Staff Reporters

***

***

The Consumer Price Index (CPI) for February found that the cost of goods and services rose 0.2% on the month. The annual rate of inflation was also up 2.8% — slightly less than expected.

Here’s a breakdown of several price changes for February:

Food: increase 0.2%

Energy: increase 0.2%

Electricity: increase 1.0%

New vehicles: decrease 0.1%

Used vehicles: increase 0.9%

Apparel: increase 0.6%

Shelter: increase 0.3%

Transportation: decrease 0.8%

Medical care services: increase 0.3%

The Bureau of Labor Statistics reported that according to its indexes, over the month the cost of medical care rose 0.3%, physicians’ services were 0.4% higher, hospital services added 0.1%, and prescription-drug costs were unchanged.

Posted on March 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEdCMP®

***

***

Your Executor or personal representative is named in your Will and is responsible for management of assets subject to probate. A basic checklist of the duties of the personal representative looks like this:

Gather all estate assets;

Collect all amounts owed the decedent;

Notify creditors and paying all valid debts;

Selling assets as needed to pay expenses or as directed by the Will;

Distribute assets to beneficiaries;

File decedents final federal income tax return;

File an estate tax return if the estate is large enough; and

File inventories and annual returns with the probate court, if required.

The position requires a lot of responsibility and involves many duties and a considerable commitment of time. The personal representative must petition the probate court for formal appointment.

Selection of your personal representative should not be made lightly, or as a favor to a friend. It requires a lot of work and very often for little or no pay. Friends and family typically will not charge the estate for their time and work. Outside advisers like attorneys and accountants will not hesitate to bill for their work effort. A few items for your selection criteria should be:

Longevity – the person should have a likelihood of being able to serve after your death;

Skill in managing legal and financial affairs;

Familiarity with your estate and wishes;

Integrity and loyalty; and

Impartiality and absence of conflicts of interest.

Alternatives to family or friends might be a corporate executor, such as a bank, an attorney, or other adviser. Similar criteria should be used in the selection of a trustee.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Posted on March 13, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITION

By Staff Reporters

***

***

1035 Exchange

DEFINITION: A method of exchanging insurance-related assets without triggering a taxable event. Cash-value life insurance policies and annuity contracts are two products that may qualify for a 1035 exchange.

***

A 1035 exchange is a feature in the tax code that permits individuals to transfer funds from an existing life insurance endowment, or annuity policy to a new one without tax consequences.

These transactions are not subject to tax deductions or tax credits but rather tax deferrals, meaning that individuals would only pay taxes on any earnings once they receive money from the policy later.

Without this provision, policyholders would have to close their previous accounts and be subjected to both taxes and surrender charges before they could open a new account.

Posted on March 12, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

The IRS 1099-k Tax Form

By Staff Reporters and IRS

***

***

Third party payment platforms are required to send you a 1099-K tax form if you made more than $5,000 on the platform in 2024. This reporting change will give the IRS a clearer picture of how much you earned in untaxed income this year to help ensure you pay your taxes properly. For the 2025 tax year, the threshold will drop to $2,500.

The IRS originally rolled out a plan to implement new reporting requirements for anyone earning over $600 via payment apps in 2023. After two years of delays, the tax agency has decided to implement a phased rollout, lifting the reporting threshold to $5,000 for the 2024 tax year.

If you earn freelance or self-employment income, you’re likely no stranger to 1099 tax forms. You’re required to report any net earnings over $400 to the IRS when you file your tax return, even if you don’t receive a 1099. The 1099-K tax change places a reporting requirement on payment apps so the IRS can keep better tabs on income earnings that might otherwise go unreported.

Monetarism is the belief that changes in the money supply are the main determinant of changes in inflation, associated especially with Milton Friedman, an American economist. Cases of hyperinflation have indeed been associated with the rapid printing of money. But when governments adopted monetarist policies in the late 1970s and early 1980s, they found money supply hard to control and also struggled to decide which measure of money supply was best to target. Monetarist policies were abandoned in favor of inflation targeting.

Monetary financing is the direct financing of government spending by the central bank. This happened during the hyperinflation in Germany in 1923 and was thus regarded as anathema for a long period afterwards. As a result, some commentators viewed quantitative easing after the financial crisis of 2007-09 with great suspicion. Technically, however, QE is not monetary financing, because central banks only buy government bonds in the secondary market and because they pay interest on reserves (the money they create).

Monetary policy The use, normally by the central bank, of interest rates and other tools to try to influence the economy. Interest rates are raised when the bank is trying to control inflation and lowered when inflation is low and it is trying to revive the economy. The financial crisis of 2007-09 led central banks to face the zero lower bound. This prompted many of them to use a new tool, quantitative easing, which was designed to bring down long-term rates or bond yields.

Posted on March 7, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

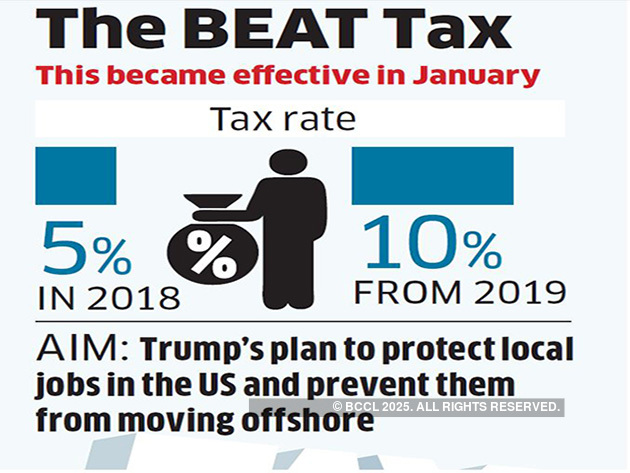

Base-Erosion Anti-Abuse Tax (BEAT): The 2017 tax reforms moved the U.S. from a worldwide taxation system to a quasi-territorial system, so foreign earnings are no longer included in a company’s domestic tax base.

To discourage companies operating in the U.S. from avoiding tax liability by shifting profits out of the country, Congress imposed a 10% minimum tax called Base-Erosion Anti-Abuse Tax (BEAT). The BEAT rate will increase from 10% to 12.5% in 2026.

Leverage ratios measure the amount of capital that comes from debt. In other words, leverage financial ratios are used to evaluate a company’s debt levels. Common leverage ratios include the following:

The debt ratio measures the relative amount of a company’s assets that are provided from debt:

Debt ratio = Total liabilities / Total assets

The debt to equity ratio calculates the weight of total debt and financial liabilities against shareholders’ equity:

Debt to equity ratio = Total liabilities / Shareholder’s equity

During its January 2025 meeting, the Medicare Payment Advisory Commission (MedPAC) reviewed and endorsed recommendations for Medicare payment reform and updates. Among other decisions, the commission recommended revisions to the annual Medicare Physician Fee Schedule (MPFS) update methodology and increased pay rates to hospitals under the Inpatient Prospective Payment System (IPPS).

This Health Capital Topics article reviews MedPAC’s recommendations, responses from industry stakeholders, and the likelihood that the commission’s recommendations will be enacted by Congress. (Read more…)

Posted on March 4, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

Electronic Data Gathering, Analysis, and Retrieval

By Staff Reporters

***

***

EDGAR (Electronic Data Gathering, Analysis, and Retrieval) is an internal database system operated by the U.S. Securities and Exchange Commission (SEC) that performs automated collection, validation, indexing, and accepted forwarding of submissions by companies and others who are required by law to file forms with the SEC. The database contains a wealth of information about the commission and the securities industry which is freely available to the public via the Internet.

In September 2017, SEC Chairman Jay Clayton revealed the database had been hacked and that companies’ data may have been used by criminals for insider trading.

Posted on March 3, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITION

By Staff Reporters

***

***

The IRS three-year rule, formally known as the statute of limitations, establishes a three-year window from the date you file your tax return or the due date of the return, whichever is later. During this period, both you and the IRS can make changes to your tax return. This means you have three years to claim a refund if you discover you overpaid, and the IRS has three years to audit your return or assess additional taxes if they find discrepancies.

This rule isn’t just about setting deadlines — it’s about creating a fair playing field. It gives taxpayers enough time to discover and correct mistakes while also allowing the IRS a reasonable time frame to verify the accuracy of returns. The clock typically starts ticking on April 15th of the year following the tax year, unless you filed early or received an extension.

However, there are important exceptions to this rule. If you underreport your income by more than 25%, the IRS gets six years to audit your return. And if you never file a return or file a fraudulent one, there is no statute of limitations. The IRS can come knocking at any time.

For most taxpayers, though, once three years have passed, the IRS can no longer come back and demand more money.

In general, a roadshow is a series of meetings or presentations in which key members of a private company, usually executives, pitch the initial public offering, or IPO, to prospective investors. Effectively, the company is taking its branding message on the road to meet with investors in different cities, hence the name.

The IPO roadshow presentation is an important part of the IPO process in which a company sells new shares to the public for the first time. Whether a company’s IPO succeeds or not can hinge on interest generated among investors before the stock makes its debut on an exchange.

There are also some cases where company executives will embark on a road show to meet with investors to talk about their company, even if they’re not planning an IPO.

Pros and Cons of a Roadshow

According to Rebecca Lake, if the company goes public and no one buys its shares, then the IPO ends up being a flop, which can affect the company’s success in the near and long term. If the company experiences an IPO pop, in which its price goes much higher than its initial offering price, it could be a sign that underwriters mispriced the stock.

A roadshow is also important for helping determine how to price the company’s stock when the IPO launches. If the roadshow ends up being a smashing success, for example, that can cause the underwriters to adjust their expectations for the stock’s IPO price.

On the other hand, if the roadshow doesn’t seem to be generating much buzz around the company at all, that could cause the price to be adjusted downward.

In a worst-case scenario, the company may decide to pull the plug on the IPO altogether or to go a different route, such as a private IPO placement.

Posted on February 28, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

CLARINET LESSONS

By Staff Reporters

***

***

In 1962, a parent was able to deduct the cost of their child’s clarinet lessons and the instrument itself, after they were prescribed by an orthodontist to fix the child’s overbite, according to a report by Boston University School of Law.

Unsurprisingly, it initially went to court, where it was ruled that it qualified as a legitimate medical expense (despite not being the most traditional treatment).

So, when it comes to the IRS, it’s not always about prescriptions or surgeries — sometimes, even clarinet lessons can count.

Posted on February 26, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS

By Staff Reporters

***

***

WASHINGTON, Feb 25 (Reuters) – U.S. President Donald Trump signed an executive order on Tuesday aiming to improve price transparency on healthcare costs by directing federal agencies to strictly enforce a 2019 order he signed during his first term.

The order directs the Departments of the Treasury, Labor, and Health and Human Services to within 90 days come up with a framework to enforce Trump’s 2019 executive order forcing health insurers and hospitals to disclose healthcare cost details.

***

***

This includes requiring the disclosure of actual prices not estimates, update existing guidance or proposing new regulations that ensure price information is standardized, and updating or issuing enforcement policies that guarantee compliance.

“You’re not allowed to even talk about it when you’re going to a hospital or see a doctor. And this allows you to go out and talk about it,” Trump told reporters as he signed the order. “It’s been unpopular in some circles because people make less money, but it’s great for the patient.”

Posted on February 25, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITION

“Show Me the Money”

By Staff Reporters

***

***

In some situations, an inheritance might complicate an estate and add to the estate tax burden. If there are sufficient assets and income to accomplish financial goals, more assets are not needed. A disclaimer may be useful. This is an unqualified refusal to accept a gift or inheritance, that is, when you “just say no”. You have decided not to accept a sizable gift made under a will, trust or other document.

When you disclaim the property, certain requirements must be met:

The disclaimer must be irrevocable;

The refusal must be in writing;

The refusal must be received within nine months;

You must not have accepted any interest in the property; and

As a result of the refusal, the property will pass to someone else.

The property passes under the terms of the decedents will, as if you had predeceased the decedent. If the filer of the disclaimer has control, the property will be included in the disclaimant’s estate and can only be passed to another as a gift for as an inheritance. The intent of the disclaimer is to renounce and never take control of the property.

It has been said that most ordinary people should have at least three to six months of living expenses (not including taxes) in a cash-equivalent reserve fund that is easily accessible (i.e., liquid). The amount needed for a one-month reserve is equal to the amount of expenses for the month, rather than the amount of monthly income. This is because during no-income months there is no income tax.

However, the situation might not be the same for physicians in today’s harsh economic climate.

The New Realities

Now, some physician-focused financial advisors, financial planners and Certified Medical Planners™ suggest even more reserve fund savings; up to two years. That’s because many factors come into play when determining how much a particular doctor’s family should have.

For example:

Does the family have one income or two? If the doctor is in a dual-income family with stable incomes and they live on a single income, the need for a liquid reserve is less.

How stable is the doctor’s income source? If a sole provider with an unstable income who spends all of the income each month, the need for a liquid cash reserve is high.

Does the doctor own the practice, work in a clinic, medical group, hospital or healthcare system? In other words – employee (less control) or employer (more control).

What is the doctor’s medical specialty and how has managed care penetrated his locale, or affected her focus? What about a DO, DDS/DMD or DPM, etc.

How does the family use its income each month; does it have a saver, spender, or investor mentality?

Does the family anticipate the possibility of large expenses occurring in the future (medical practice start-up costs or practice purchase; children, medical school student debts; auto or home loans; and/or liability suits, etc)?

Pan physician lifestyle?

The Past

In the ancient past, a doctor may have opted for a nine-twelve month reserve if the need for security was high – and a six-to-nine month reserve if the need for security was low. But today, even more may be needed. How about 15-18 months, or more? Perhaps even 24 months!

So, the following questions may be helpful in determining the amount of reserve needed by the physician:

1. How long would it take you to find another job in your medical specialty if you suddenly found yourself unemployed – same for your spouse?

2. Would you have to relocate – same for your spouse?

3. How much do you spend each month on fixed or discretionary expenses and would you be willing to lower your monthly expenses if you were unemployed?

Assessment

Once the amount of reserve is determined, the doctor should use the appropriate investment vehicles for the funds.

At minimum, the reserve should be invested in a money market fund. For larger reserves, an ultra-short-term bond fund might be appropriate for amounts over three-six months. While even larger reserves might be kept in a short term bond fund depending on interest rates and trends.

So, what do the initials M.D. really mean? … More Dough!

How much reserve do you have and where is it stashed?

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Marcinko Associates is a financial guide. We help answer your questions in an empowering way. We educate and empower medical colleagues to understand their financial picture and to make better financial decisions. We strive to simplify everything, clear up confusion, and address specific needs and goals.

Whatever your financial situation, we do not shame, criticize, or sell. We enrich, educate and empower. We work with medical colleagues at every stage of their financial journey, through big life personal changes to annual employment reviews, in order to help them understand, invest, and protect their money and autonomy.

And, like the famed ‘Tibetan Sherpas“, we guide physician entrepreneurs from medical practice business plan creation, funding, start-up operations and strategic management improvement to maximize profits and stream-line patient care quality initiatives.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

9. We act with honesty, integrity and are always straightforward. 8. We strive to be innovative, creative, iconoclastic, and flexible. 7. We admit and learn from mistakes and don’t repeat them. 6. We work hard always as competitors are trying to catch up. 5. We treat others with dignity and respect. 4. We are the onus of consulting advice for the well being of others. 3. We fight complacency as former success is in the past. 2. The best management styles are timeless, not timely. 1. Our clients are colleagues and always come first.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Understanding how economic behavior factors into health and health care decisions can benefit anyone interested in this field. However, the following groups of individuals may benefit most from the study of health economics:

Medical providers: Doctors, nurses, and assistants can evaluate new treatments, technologies, and services to determine ways to deliver value-based care. Medical providers benefit from understanding the economics behind these developments [MD/DO, DPM, DDS/DMD, RN, PA, etc].

Administrators: Health care administrators process insurance co-payments and manage financial metrics for health care providers. Learning the intricacies of health care economics can provide the necessary context as they liaise with insurance providers and use new technologies to process payments.

Policymakers or public health officials: Those who are in charge of policy decisions at the local, state, federal, or international levels benefit from understanding the economic relationship between stakeholders and the general public.

Business leaders: Because many Americans receive private insurance, health care becomes a major expense for employers. Business leaders must understand the health economics outlook to appease their employees, shareholders, and even their customers.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Posted on February 20, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

UPDATE

By PayPal and Staff Reporters

***

***

NOTE: Information provided by PayPal is not intended to be and should not be construed as tax advice. For questions about your specific tax situation, please consult a tax professional.

Payment processors, including PayPal, are required to provide information to the US Internal Revenue Service (IRS) about customers who receive payments for the sale of goods and services above the reporting threshold in a calendar year.

Will I have to pay taxes when sending and receiving money on PayPal – what exactly is changing?

The Internal Revenue Service (IRS) announced transitional reporting requirements for payments received for goods and services. These requirements will lower the Form 1099-K reporting threshold over a 3-year period from the previous threshold of more than $20,000 in goods and services transactions and more than 200 goods and services transactions in a calendar year. We’ve summarized the IRS thresholds for Form 1099-K below.

Posted on February 20, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BREAKING NEWS OF NEW DEADLINE

By Staff Reporters

***

***

The Treasury Department has set a new deadline of March 21st 2025 for millions of businesses to fulfill a new reporting requirement on “beneficial ownership information,” after a court order allowed the federal agency to start enforcing the measure.

The Corporate Transparency Act, which Congress enacted in 2021, requires small businesses to disclose the identity of people who directly or indirectly own or control the company. The measure aims to prevent criminals from hiding illicit activity conducted through shell companies or opaque ownership structures, according to the Treasury.

Posted on February 19, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

US stocks were mixed on Tuesday to begin a holiday-shortened week of trading, with potential policy moves by the Federal Reserve and President Donald Trump in focus.

The benchmark S&P 500 (^GSPC) rose nearly 0.2%, with most of the games coming in the final 10 minutes of trading, to hit a fresh record close of 6,129.58. Meanwhile, the Dow Jones Industrial Average (^DJI) and NASDAQ Composite (^IXIC) finished barely in the green.

Stocks on Wall Street were largely cautious after Monday’s closure for Presidents Day as investors debate the future path of interest rates. Fed officials over the long weekend signaled a firm belief that rates should stay at current levels to combat rising inflation.

Treasury yields stepped higher as investors sought more clues to the chances of rate cuts this year, given recent data failed to give a clear steer. The benchmark 10-year yield (^TNX) rose to trade around 4.54%.

Posted on February 15, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

What Is a Pig Butchering Scam?

Pig butchering scams get their colorful (and gory) name from the process of fattening hogs before slaughtering them. Except in this case, it’s a scammer making friends with you before taking your money. These cons have four distinct phases:

Initial contact is made by a scammer. The scammers are often enslaved by organized crime rings who force them to contact potential victims through social media platforms, dating apps, online networking sites, and job boards.

Fattening, a phase where the scammer gets to know and builds trust with a victim. They may pretend to be romantically interested in the victim, befriend the victim, or offer the victim a job.

Slaughter refers to the phase where the con pays off. Scammers may persuade victims to send them money, invest in a fake company or cryptocurrency, or reveal sensitive personal information that can be used for identity theft. Over time, scammers ask for large sums of money threatening to end contact if victims refuse to pay.

Shaming and disappearance. Scammers will continue their relationship with the victim until the victim is unable to pay or catches onto the scam. Scammers may taunt their victims to shame them into silence, or they may simply vanish along with any accounts, websites, or apps they’ve been using.

How to Avoid Pig Butchering Scams:

To avoid becoming a victim of a pig butchering type scam, watch for these red flags and know how to protect yourself:

Unexpected contact: Never respond to unsolicited messages from unknown contacts, even about seemingly benign topics, especially via text message and on encrypted messaging applications.

Refusal to participate in video chats: If someone you’ve been messaging with consistently declines to interact face-to-face, they likely aren’t the person from the profile photo.

Request for financial information: Don’t share any personal financial information with individuals you’ve never met in person. If a new virtual friend or romantic connection starts making financial inquiries, put the brakes on the relationship.

Invitation to invest in specific financial products: Be wary of any unsolicited investment advice or tips, particularly from someone you’ve only spoken to online and even if they suggest you trade through your own account. Always question what a source has to gain from sharing tips with you and whether the transaction fits with your financial goals and investment strategy.

Unknown or confusing investment opportunity: Carefully evaluate the product, as well as the person and/or company requesting your investment. Along with a basic search, try adding words like “scam” or “fraud” to see what results come up. Consider running recommendations by a third party or an investment professional who has no stake in the investment, and use FINRA BrokerCheck to see if the promoter is a registered investment professional.

Unfamiliar trading platforms: Do extensive research before moving any money, particularly in an emerging market like cryptocurrency, which has hundreds of exchanges and new avenues for trading continuing to evolve. Who controls the platform? What security measures are in place? How can you withdraw funds if needed? If you don’t know the answers to those questions, don’t put your assets there.

Exaggerated claims and elevated emotions: Take a closer look at any investment that offers much higher than average returns or is touted as “guaranteed.” Fraudsters will also often use their knowledge about you to appeal to your emotions—something like, “Don’t you want to have money to send your kids to college?”

Sense of urgency about an upcoming news announcement or share price increase: Remember that insider trading is illegal, and you should never trade in shares of a company on the basis of material, nonpublic information.

If you think you’ve been a victim of a pig butchering stock scam, submit a regulatory tip to FINRA. If you think you’ve been the victim of internet fraud, file a report with the FBI’s Internet Crime Complaint Center.

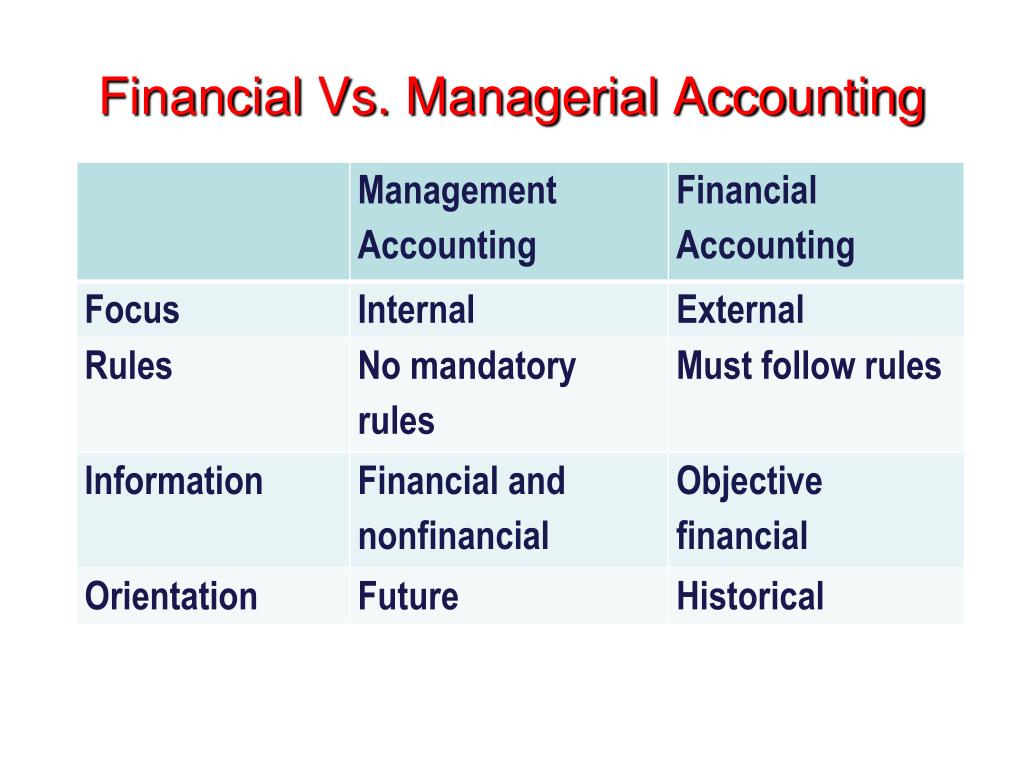

Financial accounting and managerial accounting are two distinct branches of the accounting field, each serving different purposes and stakeholders. Financial accounting focuses on creating external reports that provide a snapshot of a company’s financial health for investors, regulators, and other outside parties. Managerial accounting, meanwhile, is an internal process aimed at aiding managers in making informed business decisions.

Objectives of Financial Accounting

Financial accounting is primarily concerned with the preparation and presentation of financial statements, which include the balance sheet, income statement, and cash flow statement. These documents are meticulously crafted to reflect the company’s financial performance over a specific period, providing insights into its profitability, liquidity, and solvency. The objective is to offer a clear, standardized view of the financial state of the company, ensuring that external entities have a reliable basis for evaluating the company’s economic activities.

The process of financial accounting also involves the meticulous recording of all financial transactions. This is achieved through the double-entry bookkeeping system, where each transaction is recorded in at least two accounts, ensuring that the accounting equation remains balanced. This systematic approach provides accuracy and accountability, which are paramount in financial reporting. CPA = Certified Public Accountant.

Objectives of Managerial Accounting

Managerial accounting is designed to meet the information needs of the individuals who manage organizations. Unlike financial accounting, which provides a historical record of an organization’s financial performance, managerial accounting focuses on future-oriented reports. These reports assist in planning, controlling, and decision-making processes that guide the day-to-day, short-term, and long-term operations.

At the heart of managerial accounting is budgeting. Budgets are detailed plans that quantify the economic resources required for various functions, such as production, sales, and financing. They serve as benchmarks against which actual performance can be measured and evaluated. This enables managers to identify variances, investigate their causes, and implement corrective actions. Another objective of managerial accounting is cost analysis. Managers use cost accounting methods to understand the expenses associated with each aspect of production and operation. By analyzing costs, they can determine the profitability of individual products or services, control expenditures, and optimize resource allocation.

Performance measurement is another key objective. Managerial accountants develop metrics and key performance indicators (KPIs) to assess the efficiency and effectiveness of various business processes. These performance metrics are crucial for setting goals, evaluating outcomes, and aligning individual and departmental objectives with the overall strategy of the organization. CMA = Certified Managerial Accountant

Reporting Standards in Financial Accounting

The bedrock of financial accounting is the adherence to established reporting standards, which ensure consistency, comparability, and transparency in financial statements. Globally, the International Financial Reporting Standards (IFRS) are widely adopted, setting the guidelines for how particular types of transactions and other events should be reported in financial statements. In the United States, the Financial Accounting Standards Board (FASB) issues the Generally Accepted Accounting Principles (GAAP), which serve a similar purpose. These standards are not static; they evolve in response to changing economic realities, stakeholder needs, and advances in business practices.

For instance, the shift towards more service-oriented economies and the rise of intangible assets have led to updates in revenue recognition and asset valuation guidelines. The convergence of IFRS and GAAP is an ongoing process aimed at creating a unified set of global standards that would benefit multinational corporations and investors by reducing the complexity and cost of complying with multiple accounting frameworks.

A new report from the Global Financial Literacy Excellence Center shows that the average American scored just 48% on a financial literacy test, with groups scoring as low as 37% in certain areas. Since the report’s inception in 2017, the results have been relatively stable: Americans have scored 48% to 52% correctly on the annual study.

But only 16% of Americans scored between 75% and 100% on the test in 2024. This alarming statistic has far-reaching consequences for companies, the wider economy, and more than half all Americans.

Accounts payable are short-term obligations to be paid by an organization. It arises from trading activities and other business-related expenses during the business, including parties from whom we have purchased goods or services and costs incurred for which money is yet to be paid, generally in the same financial year.

#2 – Accounts Receivable

Accounts Receivable form part of current assets and refer to amounts due from parties to whom we have sold goods or services or incurred expenses on their behalf for which money is yet to be realized. It may include debtors, bills receivable, etc., which can be converted into cash in the short term to ensure the organization’s liquidity.

#3 – Balance Sheet

A Balance Sheet is a reconciliation of assets (current and fixed) and liabilities (current and noncurrent), and capital invested in an organization. Stakeholders such as creditors, shareholders, and banks, which have granted loans to the organization and government, use the Balance Sheet to analyze the financial position, growth, and stability.

#4 – Current Assets

Current assets refer to an organization’s realizable resources in the short term, generally during the same financial year. They include cash/bank balance and assets that can convert into cash, ranging from short-term loans and advances, sundry debtors, short-term investments, etc.

#5 – Equity

Equity is the amount invested in the business by its owners, in the form of capital in the case of sole proprietorship and partnerships, or shares (equity and preference) of varying denominations in companies (public or private).

#6 – Expenses

All the money outflow (present or future) incurred for procuring goods and services to affect sales in a business (direct expenses) and incidental to the business (indirect expenses) as well as ancillary to the running of an organization are referred to as expenses

#7 – Fixed Assets

Fixed assets are tangible resources that an organization uses for carrying out daily operations of a business, such as land, plant and equipment, furniture and fixtures, buildings, machinery, etc., which are not purchased to be sold in the short term.

#8 – Ledger

Ledger is the book of entry for recording transactions in such a way that we come to know the outstanding debit or credit balance of an account in our business for which we record the opening balance, transactions made in that account, and the closing balance to find out the exact position of that particular account.

#9 – Income Statement

The Income statement forms part of the financial statements and tells us the exact position of our gross and net profit at a particular cut-off date. It is done by recording all the direct incomes and closing stock on the credit side and all direct expenses and opening stock on the debit side to find the gross profit and all the indirect incomes and indirect expenses similarly to find out the net profit.

#10 – Liabilities

Liabilities are the present (short term) and future(long term) obligations of an organization which represents the debts due to be paid for goods and services procured for the business in the past and include sundry creditors, short term loans and advances, bills payable, etc. which come under short term liabilities and debentures, term loans from a bank, long term loans and advances, etc. which come under long term liabilities.

#11 – Net Income

The profit or loss arrived at after deducting all direct and indirect expenses from all the direct and indirect incomes equals to net income made by a business which is the earning done by the business at a cut-off date and is very useful in comparing the growth and financial position of an organization from previous years as well as for adopting measures for the betterment of the profitability levels of the business.

#12 – Revenue

The gross income earned by the organization from carrying out core business activities without deduction of any expenses is termed as revenue earned by the organization, which also indicates the sale and other incomes in total.

#13 – Credit

Wherever an account is credited, it reduces the balance of an account in the case of real accounts, creates an obligation to pay an individual in the case of personal accounts, and increases the income side if a nominal account is credited.

#14 – Debit

Wherever an account is debited, it increases the balance of an account in the case of real accounts, creating an obligation to receive money from an individual in the case of personal accounts and increasing the expenses side if a nominal account is debited.

#15 – Audit

An audit is an examination of books of accounts prepared by an organization to validate the entries recorded and ensure the accuracy and correctness of the financial statements along with finding out any discrepancies in the books, including frauds, if any, hidden by the employees of the organization.

The desire for security and feelings of insecurity are the same thing.

The idea of security, financial or otherwise, is an illusion; human life is inherently insecure. But, this doesn’t mean we shouldn’t be prudent with risk and diligent financial planning with strategies like saving and investing.

However, according to colleague Eugene Schmuckler PhD, MBA,MEd seeking security is like many things; the more you try to grasp and obsess about financial security, the more quickly you will reach a point of diminishing returns. You will feel increasingly less secure at a certain point.

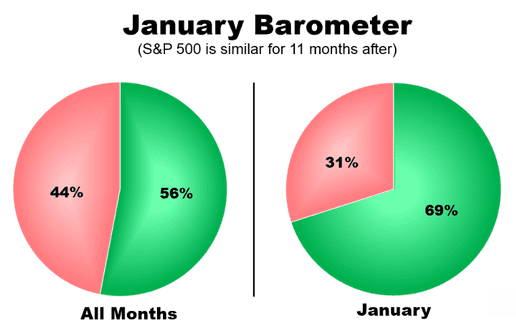

According to Rob Lenihan, of TheStreet, the January Barometer is a theory that says the investment performance of the S&P 500 in January is representative of the predicted performance of the entire year. The theory says that if stocks are higher in January, they should be higher for the year, and if they are lower in the first month, they’ll be lower for the year.

The S&P 500 finished down on January 31st, but the broad market ended up 2.6% for the month, so maybe we should heed the words of Wall Street legend Yale Hirsch, who first came up with the concept in 1972 in his Stock Trader’s Almanac, a widely read investment guide. Hirsch, by the way, also gave the world the Santa Claus Rally, which describes a rise in stock prices during the last five trading days in December and the first two trading days in the following January.

Analyst Stephen Guilfoyle said early this month in a post for TheStreet Pro that Santa Claus posted a loss this year, which was Santa’s second consecutive year in the red.

“No sweat,” the veteran trader said in his January 9th TheStreet Pro column. “That’s just a seasonal trade, and 2024 was a very nice year for U.S. equities in a broad sense.”

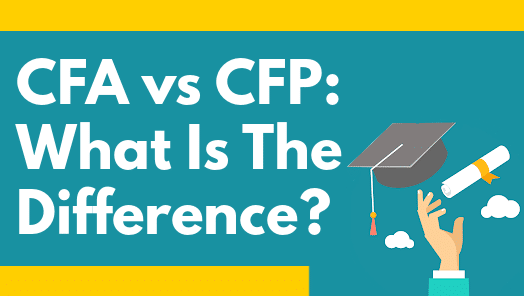

A certified financial planner (CFP®) helps individuals plan their financial futures. CFPs are not focused only on investments; they help their clients achieve specific long-term financial goals, such as saving for retirement, buying a house, or starting a college fund for their children.

To become a CFP®, a person must complete a course of study and then pass a two-part examination. The exam covers wealth management, tax palnning, insurance, retirement planning, estate planning, and other basic personal finance topics. These topics are all important for someone seeking to help clients achieve financial goals.

Chartered Financial Analyst (CFA)

A CFA, on the other hand, conducts investing in larger settings, normally for large investment firms on both the buy side and the sell side, mutual funds or hedge funds. CFAs can also provide internal financial analysis for corporations that are not in the investment industry. While a CFP® focuses on wealth management and planning for individual clients, a CFA focuses on wealth management for a corporation.

To become a CFA, a person must complete a rigorous course of study and pass three examinations over the course of two or more years. In addition, the candidate must adhere to a strict code of ethics and have four years of work experience in an investment decision-making setting.

Generative artificial intelligence (AI) is the utilization of algorithms to create content—such as text, code, imagery, videos, and even simulations—in mere seconds. The goal of AI in general is to mimic the intelligence of humans to perform tasks. “Generative” AI aims to learn from data without the assistance of humans. While today’s generative AI bots are not yet prepared for widespread utilization in patient care settings, AI is garnering significant interest in the healthcare industry as providers begin to test its capabilities in clinics and offices.

This article reviews the role that generative AI is beginning to play in the U.S. healthcare system, the potential of AI in healthcare, and concerns related to the technology.

(“Informed Voice of a New Generation of Fiduciary Advisors for Healthcare”)

For most lay folks, personal financial planning typically involves creating a personal budget, planning for taxes, setting up a savings account and developing a debt management, retirement and insurance recovery plan. Medicare, Social Security and Required Minimal Distribution [RMD] analysis is typical for lay retirement. Of course, we can assist in all of these activities, but lay individuals can also create and establish their own financial plan to reach short and long-term savings and investment goals.

But, as fellow doctors, we understand better than most the more complex financial challenges doctors can face when it comes to their financial planning. Of course, most physicians ultimately make a good income, but it is the saving, asset and risk management tolerance and investing part that many of our colleagues’ struggle with. Far too often physicians receive terrible guidance, have no time to properly manage their own investments and set goals for that day when they no longer wish to practice medicine.

For the average doctor or healthcare professional, the feelings of pride and achievement at finally graduating are typically paired with the heavy burden of hundreds of thousands of dollars in student loan debt.

You dedicated countless hours to learning, studying, and training in your field. You missed birthdays and holidays, time with your families, and sacrificed vacations to provide compassionate and excellent care for your patients. Amidst all of that, there was no time to give your finances even a second thought.

Between undergraduate, medical school, and then internship and residency, most young physicians do not begin saving for retirement until late into their 20s, if not their 30s. You’ve missed an entire decade or more of allowing your money and investments to compound and work for you. When it comes to addressing your financial health and security, there’s no time to waste.

MBA is the common abbreviation for a Master of Business Administration degree, and recipients typically stop attending school after receiving it.

However, those who are interested in conducting business research may decide to pursue a doctorate in business or management. Such students can earn a Ph.D. or a Doctor of Business Administration degree, commonly known as a DBA.

What ‘MSHA’ Stands For?

Master of Health Administration (MHA) and Master of Science in Health Administration (MSHA) are largely equivalent designations for degree programs that focus primarily on leadership and management of hospitals, healthcare organizations, and businesses that operate in the healthcare sector.

In contrast, an MBA in Health Administration is a Master of Business Administration degree program with a concentration, track, or specialization that provides students with several courses in topics specific to healthcare management and administration. Most of the coursework in an MBA program is devoted to general training in business functions, such as accounting, finance, logistics, marketing, personnel and project management.

MHA and MHSA programs devote all or most of their curriculum to studying the healthcare system, healthcare policy, and the application of business principles in the field of healthcare. MBA in Healthcare Administration programs devote only a portion of their curricula to topics specific to the healthcare sector.

While IAs and FAs may seem the same, they are not the same. The Financial Industry Regulatory Authority (FINRA) and the Securities Exchange Commission (SEC) have clearly defined investment advisors as distinct from financial advisors.

The term financial advisor is a generic one that can encompass many different financial professionals, although it most commonly refers to stock brokers (individuals or companies that buy and sell securities).

Investment advisor, on the other hand, is a legal term and thus has a more clear-cut definition – or at least as clear as legalese is apt to be.

KEY DIFFERENCES:

Financial advisors help with all aspects of your finances, including saving, budgeting, insurance, retirement planning, and taxes.

Investment advisors focus specifically on choosing and managing investment portfolios.

Financial advisors offer broader financial guidance, while investment advisors concentrate solely on investments.

Investment advisors are held to the fiduciary standard, while financial advisors who work as brokers may operate under different rules.

The CPA and CMA designations cater to distinct professional focuses within the accounting and finance fields. A CPA is often seen as the gold standard for public accounting, emphasizing auditing, tax, and regulatory compliance. This certification is highly regarded for roles that require a deep understanding of financial reporting and external auditing. CPAs are frequently employed by public accounting firms, government agencies, and corporations that need to ensure their financial statements adhere to strict regulatory standards.

On the other hand, the CMA designation is tailored for professionals who aim to excel in management accounting and strategic financial management. CMAs are trained to analyze financial data to inform business decisions, focusing on internal processes and performance management. This makes the CMA particularly valuable for roles in corporate finance, strategic planning, and management consulting. Companies looking to optimize their internal financial operations and drive business strategy often seek out CMAs for their expertise in cost management, budgeting, and financial analysis.

The educational and experiential requirements for these certifications also differ. To become a CPA, candidates typically need to complete 150 semester hours of college education, which often includes a bachelor’s degree in accounting or a related field. Additionally, CPAs must pass the Uniform CPA Examination and meet specific state licensing requirements, which usually include a certain amount of professional experience.

In contrast, the CMA certification requires a bachelor’s degree in any discipline, two years of relevant work experience, and passing the two-part CMA exam. This flexibility in educational background can make the CMA more accessible to a broader range of professionals.

The ICE 3-Month USD LIBOR interest rate is the average interest rate at which a selection of banks in London are prepared to lend to one another in American dollars with a maturity of 3 months.

The Bank of America US High Yield Constrained Index is a market value-weighted index of all domestic high-yield bonds and Yankee high-yield bonds (issued by a foreign entity and denominated in U.S. dollars), including deferred interest bonds and payment-in-kind securities.

The ICE BofA BB-B US High Yield Constrained Index is composed of U.S. dollar-denominated corporate debt publicly issued in the U.S. market rated BB through B, based on an average of Moody’s, S&P and Fitch ratings, with issuer exposure capped at 2%.

ICE BofA U.S. Convertible Index tracks the performance of publicly issued, exchange-listed US dollar denominated convertible securities of US companies with at least $50 million face amount outstanding and at least one month remaining to the final conversion date. Index constituents are market capitalization-weighted and rebalanced monthly.

ICE BofA ML MOVE Index is a widely used measure of bond market volatility, similar to the VIX Index for stocks. The MOVE Index (also known as the Merrill Lynch Option Volatility Estimate) is a yield-curve-weighted index that tracks the market’s expectation of volatility in the U.S. bond market based on 1-month Treasury options.

ICE Exchange-Listed Preferred & Hybrid Securities Index tracks the performance of exchange-listed US dollar denominated hybrid debt, preferred stock and convertible preferred stock publicly issued by corporations in the US domestic market. Preferred stock and notes must have a minimum amount outstanding of $100 million; convertible preferred stock must have at least $50 million face amount outstanding. Index constituents are market capitalization-weighted subject to certain constraints. The index is re-balanced monthly.

The Bloomberg U.S. Universal Index represents the union of the U.S. Aggregate Index, U.S. Corporate High Yield Index, Investment Grade 144A Index, Eurodollar Index, U.S. Emerging Markets Index, and the non-ERISA eligible portion of the CMBS Index.

The index covers USD-denominated, taxable bonds that are rated either investment grade or high-yield. Some Bloomberg U.S. Universal Index constituents may be eligible for one or more of its contributing sub-components that are not mutually exclusive. These securities are not double-counted in the index.

The Bloomberg U.S. Universal Index was created on January 1st, 1999, with index history back-filled to January 1st, 1990.

HFRX Equity Hedge Index serves as a daily-priced proxy for alternative strategies that maintain positions long and short, primarily in equity and equity derivative securities.

HFRX Fixed Income – Credit Index serves as a daily-priced proxy for alternative strategies that provide exposure to credit strategies. Credit strategies refers to a wide range of sub-strategies and may include corporate, sovereign, distressed, asset-backed, capital structure arbitrage, and other relative value approaches. Strategies may also include and utilize equity securities, credit derivatives, commodities, or currencies.

Academic Team of Internationally Known Contributors

D. E. Marcinko & Associates is one of the most academically published authorities on the topic of financial planning and private wealth management for physicians, nurses and medical professionals. We have published 33 major peer reviewed textbooks redacted in the Library of Medicine, Institute of Health and the Library of Congress, in four languages, with over 5,025 online white papers, web-posts and related publications. These cover a range of financial planning topics from medical malpractice, risk management and insurance, to investment policy statement analysis and endowment funding management, and to taxation, retirement, estate and legacy planning.

Financial planning, business and strategic management, FMV for practice and clinics and related “hard” topics are included.

***

We also include “soft” subjects from investor psychology, ethics and lost fortunes to luxury spending, from understanding the middle-class millionaire to the political philosophies of physicians and the affluent. Our corpus of work is regularly consulted by doctors, medical, business, graduate and nursing schools, to elite advisors, private and investment bankers, wealth managers, venture capitalists, academics and the press.

Carry-oriented currencies are higher-yielding currencies of countries where interest rates are generally higher than those of countries with lower-yielding currencies.

These higher-yielding currencies are targeted for “carry trades,” where investors borrow money in a low-interest rate currency and invest in a higher yielding currency, potentially profiting from the difference in interest rates.

Posted on January 11, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Credit report with score on a desk

***

Credit analysis is a form of financial analysis used primarily to determine the financial strength of the issuer of a security, and the ability of that issuer to provide timely payment of interest and principal to investors in the issuer’s debt securities. Credit analysis is typically an important component of security analysis and selection in credit-sensitive bond sectors such as the corporate bond market and the municipal bond market.

Credit default swap index (CDX) is a credit derivative, based on a basket of CDS, which can be used to hedge credit risk or speculate on changes in credit quality.

Credit default swaps (CDS) are credit derivative contracts between two counterparties that can be used to hedge credit risk or speculate on changes in the credit quality of a corporation or government entity.

Credit quality reflects the financial strength of the issuer of a security, and the ability of that issuer to provide timely payment of interest and principal to investors in the issuer’s securities. Common measurements of credit quality include the credit ratings provided by credit rating agencies such as Standard & Poor’s and Moody’s. Credit quality and credit quality perceptions are a key component of the daily market pricing of fixed-income securities, along with maturity, inflation expectations and interest rate levels.

Credit Rating Agency (CRA) is a company that assigns credit ratings for issuers of certain types of debt obligations as well as the debt instruments themselves. In the United States, the Securities and Exchange Commission (SEC) permits investment banks and broker-dealers to use credit ratings from “Nationally Recognized Statistical Rating Organizations” (NRSRO) for similar purposes. As of January 2012, nine organizations were designated as NRSROs, including the “Big Three” which are Standard and Poor’s, Moody’s Investor Services and Fitch Ratings.

Credit rating downgrade, by a credit rating agency (Standard & Poor’s, Moody’s or Fitch) means reducing its credit rating for a debt issuer and/or security. This is based on the agency’s evaluation, indicating, to the agency, a decline in the issuer’s financial stability, increasing the possibility of default. A downgrade should not to be confused with a default; a debt security can be downgraded without defaulting. And, conversely, a debt issuer can suddenly default without being downgraded first–credit ratings and credit rating agencies are not infallible.

Credit ratings are measurements of credit quality provided by credit rating agencies. Those provided by Standard & Poor’s typically are the most widely quoted and distributed, and range from AAA (highest quality; perceived as least likely to default) down to D (in default). Securities and issuers rated AAA to BBB are considered/perceived to be “investment-grade”; those below BBB are considered/perceived to be non-investment-grade or more speculative.

Credit risk is the inability or perceived inability of the issuers of debt securities to make interest and principal payments will cause the value of those securities to decrease. Changes in the credit ratings of debt securities could have a similar effect.

Credit Risk Transfer Securities (CRTS) are unsecured obligations of the GSEs (Government Sponsored Enterprises). Although cash flows are linked to prepays and defaults of the reference mortgage loans, the securities are unsecured loans, backed by general credit rather than by specified assets.