BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on October 24, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

A “New” Clinical Numeric

DR. DAVID EDWARD MARCINKO MBA MEd

This physician-led medical website http://www.thennt.com/ seeks to explain to patients and physicians how well a particular treatment or medicine is likely to work based on a statistical model called the “Number Needed to Treat.”

Calculation

This is not really a new calculation, as it has been know for many years. In fact, I review and teach it in several of my undergraduate, graduate and business school courses [healthcare administration, statistics, epidemiology, infection control, community, public and population health, etc], and have been doing so for a few years now. My students are always amazed by it.

Brief Definition

The NNT is “a measurement of the impact of a medicine or therapy by estimating the number of patients that need to be treated in order to have an impact on one person.”

Detailed Definition

According to wikipedia; the number needed to treat (NNT) is an epidemiological measure used in assessing the effectiveness of a health-care intervention, typically a treatment with medication. The NNT is the number of patients who need to be treated in order to prevent one additional bad outcome (i.e. the number of patients that need to be treated for one to benefit compared with a control in a clinical trial). It is defined as the inverse of the absolute risk reduction.

The NNT was first described in 1988. The ideal NNT is 1, where everyone improves with treatment and no-one improves with control. The higher the NNT, the less effective is the treatment. Variants are sometimes used for more specialized purposes.

One example is number needed to vaccinate. NNT values are time-specific. For example, if a study ran for 5 years and it was found that the NNT was 100 during this 5 year period, in one year the NNT would have to be multiplied by 5 to correctly assume the right NNT for only the one year period (in the example the one year NNT would be 500).

And so, your thoughts and comments on this ME-P are appreciated. Give em’ a click and tell us what you think http://www.thennt.com? Do you use the concept of NNT in your clinical medical practice; why or why not? Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Channel Surfing

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on October 24, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Quote: “It looks like the global battle against inflation has largely been won, even if price pressures persist in some countries. In most countries, inflation is now hovering close to central bank targets…The decline in inflation without a global recession is a major achievement.”—IMF (CNN Business)

Spirit Airlines is back from the dead, soaring 46.67% on a Wall Street Journal report that it may end up merging with FrontierAirlines after all. Frontier Airlines rose 0.76% on the news.

AT&T climbed 4.65% after it beat earnings expectations in the third quarter, though it missed on revenue.

Starbucks fell hard late yesterday but recovered a bit this afternoon after new CEO Brian Niccol said the coffee chain is suspending its 2025 fiscal outlook. Shares rose 0.86% today.

Coca-Cola fizzled 2.07% after beating both top and bottom line expectations. The problem is that the only reason the soda giant performed well was because it raised prices, while demand for soft drinks slowed.

Enphase Energy plummeted 14.92% after the solar stock missed on both earnings and revenue expectations last quarter.

Boeing is a very familiar name in the “What’s down” section, and its latest earnings report did nothing to help. The manufacturing giant notched a $6 billion loss last quarter, and shares fell 1.76%.

The SPX fell 53.78 points (–0.92%) to 5,797.42; the Dow Jones Industrial Average® ($DJI) lost 409.94 points (–0.96%) to 42,514.95; and the NASDAQ Composite ($COMP) dropped 296.47 points (–1.60%) to 18,276.65.

The 10-year Treasury note yield gained four basis points to 4.24%.

Frequently, we hear the axiom that asset allocation is the most important investment decision, explaining 93.6% of portfolio returns. The presumption has been that once the risk tolerance and time horizon have been established, investing is simply a matter of implementing a fixed mix of stocks, bonds, and cash using mutual funds selected for this purpose. This axiom is based on a famous study by Brinson, Hood, and Beebower (BHB) published in the Financial Analysts Journal in July/August 1986. It is the stuff of most modern business school and graduate students in economics and finance.

Enter the Critics

One critic claims that BHB’s conclusions and the interpretation of their conclusions are wrong, stating that because of several methodological problems, BHB needed to make certain assumptions for their analysis to go forward. They assumed that the average asset-class weights for the 10-year period studied are the same as the actual normal policy weights; that investments in foreign stocks, real estate, private placements, and venture capital can be proxied by a mix of stocks, bonds, and cash; and that the benchmarks for stocks, bonds, and cash against which fund performance was measured are appropriate. The author believes that each of these assumptions can lead to a faulty measurement of success or failure at market timing and stock selection.

The Jahnke Study

William Jahnke claims that BHB erred in their focus on explaining the variation of quarterly portfolio returns rather than portfolio returns over the 10-year period studied. According to the study, asset allocation policy explains only a small fraction of the range of 10-year portfolio returns earned by the pension funds reported in the study. The author concluded that this discrepancy is caused by the effect of compounding returns. He adds that BHB were wrong to use variance of quarterly returns rather than the standard deviation. Use of standard deviation would reduce the often cited 93.6% to about 79%. Moreover, BHB did not consider the cost of investing, such as operating expenses, management fees, brokerage commissions, and other trading costs, which are more significant for individual investors than for the pension plans studied. Jahnke claims that excessive costs can reduce wealth accumulation by 50%.

Note: (“The Asset Allocation Hoax,” William W. Jahnke, Journal of Financial Planning, February 1997, Institute of Certified Financial Planners [303] 759-4900).

Assessment

Finally, the author takes issue with establishing long-term fixed asset class weights. Asset allocation should be a dynamic process. Higher equity return expectations should in turn produce larger equity allocations, other things being equal.

Conclusion

Are doctors different than the average investor noted in this essay?

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on October 23, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

How would you restart your career in medicine?

[By Dr. David Edward Marcinko MBA MEd CMP™]

We’ve known this physician-client-friend for 10 years, and while he didn’t tell us what he wanted to discuss, we knew it was important.

After exchanging pleasantries, he shocked me: He said he’s totally unfulfilled in his current job and wants to do something new.

We were floored because he is an outstanding doctor – at the top of his game. From the outside looking in, he appears to be “living the dream”.

After that bombshell, we asked him the question we couldn’t get out of our mind: “Are you afraid?”

“Yes,” he said; “Afraid and relieved.”

His relief stemmed from the fact that he is going to shed the tremendous demands of being a doctor at the highest levels. He was afraid because he didn’t know what was next.

We thought afterward, “What a courageous and totally refreshing move.”

A Fantasy Reboot

That dialogue triggered a larger internal conversation within; and with others.

What would you do if you could start from scratch?

How would you proceed if you could just wipe the slate clean and restart your career in medicine?

For those quietly pondering a similar path, three great opportunities seem crystal clear.

First, we would create our own practice playbook. Discard the ready-made choices served up by your old practice. For the independent physician today, there’s almost infinite variety. The pleasure in creating your own approach is that there are so many options. Your patients will appreciate the greater choice and flexibility, too.

Second, we would whole-heartedly embrace technology; but not necessarily EHRs at this time. Rather, build your own HIT framework to complement your medical practice. Innovate across your entire operations – everything from medical records, to online appointment access, secure FAX machines, to patient portals and laboratory results reporting to your own mobile phone app. Freeing yourself from your current archaic technology will be life altering by itself.

Third, cull the difficult people from your life. These are the naysayers who weigh you down – superiors, colleagues or patients. Negativity is corrosive, and it always lingers. It also distracts you from giving others your best. While you’re at it, cull the skills you mastered to survive in your career so you can focus on those that really matter.

Case Model

So, we wanted to share one of the all-time greatest reboots we know because it shows what is possible if you believe in yourself.

A decade ago, one of our osteopathic physician clients delivered some bad news. She was quitting her job as a medical associate, to transition into her own direct pay concierge practice.

At the time, this was unheard of: No one walked away from a potential medical practice partnership to become a solo physician. But, Sue had a different vision. She wasn’t fulfilled and she knew it. With the support of her husband, she decided there was a better way. So she started from scratch.

How did it work out?

Unbelievably well – but NOT overnight!

With our meager assistance, Sue’s been cash flow positive for the last 7 years, and now earns more money than before, with less stress; and she is the captain of her ship. A few colleagues who have worked with her have even gone on to achieve comparable success. She’s become a role model to others too, and she remains one our heroes.

The Decision

Starting from scratch may or may not translate into more money, but it often means this: More happiness in your life. Sue’s decision, just like our friend who bared his soul to us over coffee, were both made for the right reasons.

We wish our friend well on his journey, confident knowing that a happy ending is just over the horizon for him, too.

Assessment

Send us your own success/failure story, so we might learn from you. Would you even stay in medicine or transition/begin another career; anew?

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on October 23, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

COGNITIVE BIASES

By Staff Reporters

***

***

The following are two common psychological biases. Some biases are learned while others are genetically determined (and often socially reinforced). They are prevalent in most areas in life.

Halo Effect

The halo effect is the cognitive bias where the perception of one positive trait influences the perception of other traits. It’s like assuming a good-looking person is also kind and smart. This mental shortcut simplifies our judgments but often leads to inaccurate assessments.

Marketers and politicians love the halo effect, using it to create a positive overall impression.

To counteract the halo effect, consciously separate individual traits and evaluate them independently. Remember: not everything that shines is gold.

Hero Placebo Effect

The hero placebo effect is the phenomenon where believing in the efficacy of a hero or leader enhances their perceived effectiveness. It’s like thinking a charismatic coach makes the team better just by being there. This belief can boost morale and performance, creating a self-fulfilling prophecy.

However, it can also lead to overestimating the hero’s actual impact. So, while it’s great to have inspiring leaders, remember: true success comes from collective effort, not just the aura of a single hero.

Posted on October 23, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The IRS has announced the annual inflation adjustments for the year 2025, including tax rate schedules, tax tables and cost-of-living adjustments. These are the official numbers for the tax year 2025—that tax year begins January 1, 2025. These are not the numbers that you’ll use to prepare your 2024 tax returns in 2025 (you’ll find those official 2024 tax numbers here). These are the numbers that you’ll use to prepare your 2025 tax returns in 2026.

Trump Media & Technology Group rose 9.87% to its highest level since July as the “Trump trade” wagering on the former president to regain the White House picks up steam.

Quest Diagnostics isn’t just a sad, windowless building where you get your blood drawn—it’s also been a pretty profitable investment. Shares rose 6.88% on strong earnings and revenue growth.

STOCKS DOWN

Stop us if you’ve heard this one before: Target is cutting the price of 2,000 products ahead of the holiday season. Shares sank 1.13% as shareholders digest what appears to be a desperate move to boost sales.

Verizon Communications dropped 5.03% after missing on both revenue and earnings estimates. But the real problem was slowing customer growth and phone sales.

Defense contractors were in the earnings spotlight today, and none of them did well. GE Aerospace tumbled 9.07% despite beating analyst forecasts and Lockheed Martin fell 6.12% after sales missed estimates.

Genuine Parts, better known as NAPA Auto Parts, plummeted 20.96% after earnings missed estimates and the company announced lower fiscal year forecasts.

The SPX fell 2.78 points (–0.05%) to 5,851.20; the Dow Jones Industrial Average® ($DJI) lost 6.71 points (–0.02%) to 42,924.89; and the $COMP gained 33.12 points (0.18%) to 18,573.13.

The 10-year Treasury note yield (TNX) added two basis points to 4.2%.

The CBOE Volatility Index® (VIX) fell to 18.15, down from above 20 a week ago.

Posted on October 22, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

COGNITIVE BIASES

By Staff Reporters

***

***

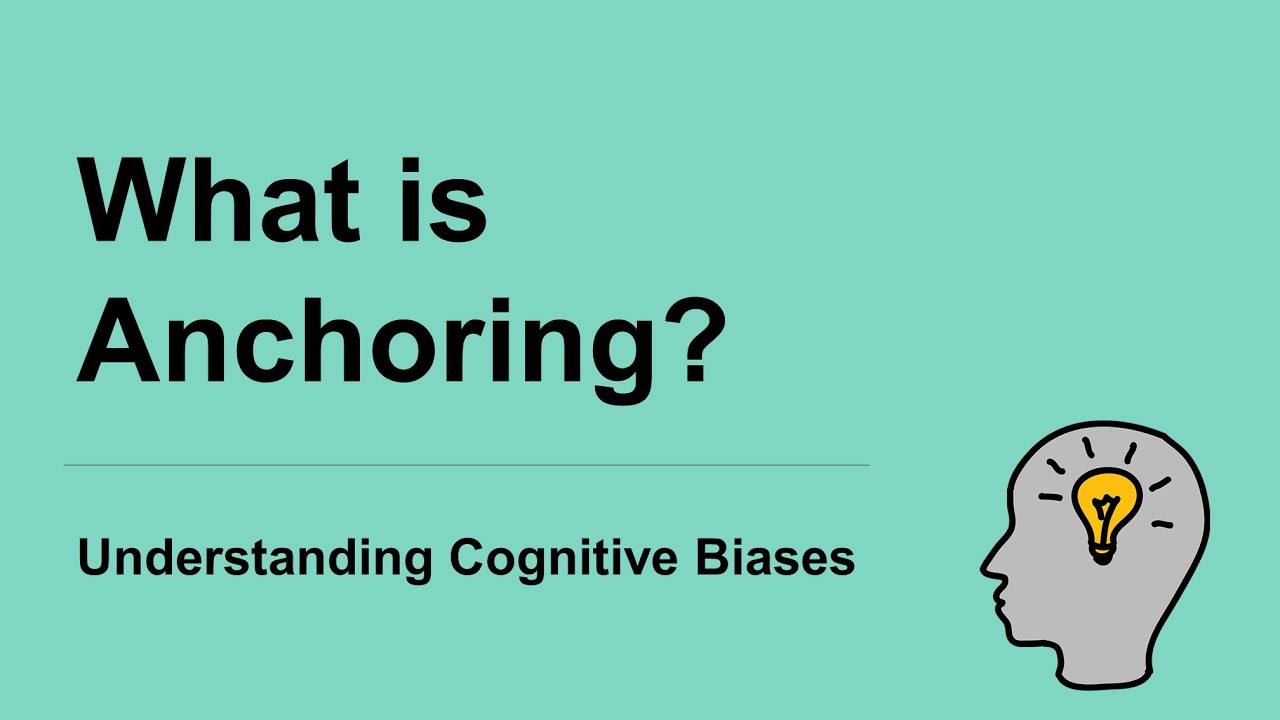

According to colleague Dan Ariely PhD,anchoring is the mental trick your brain plays when it latches onto the first piece of information it gets, no matter how irrelevant. You might know this as ‘ first impressions ’ – when someone relies on their own first idea of a person or situation.

Imagine you’re buying a car, and the salesperson starts with a high price. That number sticks in your mind and influences all your subsequent negotiations. Anchoring can skew our decisions and perceptions, making us think the first offer is more important than it is. Or, subsequent offers lower than they really are.

So, the next time you’re haggling or making a big decision, be aware of that initial anchor dragging you down.

Posted on October 22, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Re-Thinking a Popular Practice from the Past

By Dr. David Edward Marcinko; MBA, MEd, CMP™

[Publisher-in-Chief]

More personal than a corporate home care medical business model, most people view house calls as a popular practice from the past.

Although less than 5% of the nation’s doctors regularly make house calls today, the medical house call industry is swiftly picking up momentum once again. It is a move that is greatly benefiting physicians and patients alike.

Why House Calls?

It’s because we live in a society that has become technology focused. While this emergence has benefited many in terms of medical advancements, there are a growing number of patients who are uncomfortable with next-generation medical practices. These people, particularly the rapidly aging elders of the nation, want to be cared for in a friendly, nurturing, and convenient way. As people age and fall ill, it becomes increasingly difficult to leave the home for office visits. Not to mention, there are many handicapped patients as well who have to arrange for wheelchair vans or ambulances just to visit the doctor. The COVID pandemic and tele-health are illustrative.

Meeting a Niche Market Need

Thanks to the desire of physicians seeking to open their own medical house call practices, these patient needs are slowly being met. Some of these physicians are strictly open for house call visits only and have no physical office. They commonly take appointment requests via phone calls and emails with the overall goal to combine the service of an old-time, small town doctor with the latest technology designed to meet people’s emotional, and financial, needs. Patients are also able to save a considerable amount of time by not having to leave the house to go to the doctor’s office, and not having to fill prescriptions. After all, many medical house call physicians travel along with certain medications that can be dispensed on location. Narcotics, however, will likely still need to be filled with a paper or e-prescription.

While highly convenient for patients who wish to receive medical house call services, the reviving industry is fitting for physicians. In recent years, Medicare has increased its level or reimbursements for physicians who travel to patients. Just in the past few years alone, Medicare has been billed approximately $1.75 million annually for house calls.

Enter the DNPs and NPs

Even nurse practitioners [NPs] and Doctors of Nursing Practice [DNPs] who make a small number of house calls are typically unaware that they can maximize profit potential with medical house calls. Some NPs have even offset operating expenses by offering house calls to make their office based practice more appealing to their patients.

Also, significant advances in technology have enabled popular medical equipment to be smaller and portable. Physicians are able to perform standard procedures, such as skin biopsies and blood draws while outside the office. They are also able to easily access patient medical records through usage of a laptop, as well as resources such as the Physicians’ Desk Reference [PDS] through usage of a hand-held personal digital assistant or smart cell phone.

Assessment

For example, this firm educates patients and supports physicians who are ready to make a transition from office-based positions to medical house call practices. There are no royalty or membership fees, and this is not a franchise. It helps transition to a reportedly more pleasing, profitable way to practice medicine today.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

PRUDENT BUYER: The efficient purchaser of market balance between value and cost.

PRUDENT MAN RULE: An 1830 court case stating that a person in a fiduciary capacity (a trustee, executor, custodian, etc) must conduct him/herself faithfully and exercise sound judgment when investing monies under care. “He is to observe how men of prudence, discretion and intelligence manage their own affairs, not in regard to speculation, but in regard to the permanent distribution of their funds, considering the probable income as well as the probable safety of the capital to be invested.” Allows for mutual funds and variable annuities.

PRUDENT INVESTOR RULE: A fiduciary is required to conduct him/herself faithfully and exercise sound judgment when investing monies and take measured and reasonable investment risks in return for potential future rewards. Allows for mutual funds, stocks, bonds, variable annuities asset allocation & Modern Portfolio Theory.

Posted on October 22, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Here’s where the major stock market benchmarks ended:

The S&P 500® index (SPX) fell10.69points (–0.18%) to 5,853.98; the Dow Jones Industrial Average® ($DJI) lost 344.31 points (–0.80%) to 42,931.60; and the NASDAQ Composite®($COMP) rose 50.45 points (0.27%) to 18,540.01.

The 10-year Treasury note yield (TNX) climbed 11 basis points to 4.18%, outpacing a 7 basis-point rise for the 2-year Treasury note yield.

The CBOE Volatility Index®(VIX) climbed to 18.6 but remains below recent peaks.

Boeing popped 3.11% on the news that it has reached a tentative deal with the machinists union that has been on strike for over a month now. With Boeing’s earnings announcement coming Wednesday, shareholders are definitely breathing a sigh of relief.

Activist investor Starboard Value has taken a sizable stake in Tylenol-maker Kenvue, which was spun off of Johnson & Johnson just last year. Kenvue shares rose 5.52% on the news.

Warby Parker climbed 9.84% thanks to an upgrade from Goldman Sachs analysts, who like the company’s strong margin growth and improved operational efficiency.

Cigna will once again attempt to acquire fellow health insurerHumana. Shareholders on both sides didn’t like the idea: Shares of Cigna sank 4.69%, and Humana fell 2.51%.

UPS dropped 3.38% on a downgrade from Barclays analysts citing pressures on the company’s margins, including higher competition and weaker demand. Management will have a chance to respond when earnings drop on Thursday.

Southwest Airlines fell 1.74% after Bloomberg reported that the beleaguered airline wants to call a truce with activist investor Elliott Investment Management.

There is no shortage of analysis for anyone interested in investing. A search for the term “stock market analysis” turned up 16 million hits on Google and well over 200,000 hits each on Bing, and Yahoo.

***

***

The majority of stock market analysis can be lumped into three broad groups: fundamental, technical, and sentimental. Here’s a close look at SA.

Sentimental Analysis

Sentimental analysis attempts to measure the market in terms of the attitudes of investors. Sentimental analysis starts from the assumption that the majority of investors are wrong. In other words, that the stock market has the potential to disappoint when “masses of investors” believe prices are headed in a particular direction.

Sentiment analysts are often referred to as contrarians who look to invest against the majority view of the market.

For example, if the majority of professional market watchers expect a stock price to trend higher, sentiment analysts may look for prices to disappoint the majority and trend lower.

Which approach is best?

There is no clear answer to that question.

But it’s important to remember three things:

Past performance does not guarantee future results, actual results will vary, and the best approach may be to create a portfolio based on your time horizon, risk tolerance, and goals.

Keep in mind that the return and principal value of stock prices will fluctuate as market conditions change.

And shares, when sold, may be worth more or less than their original cost.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements.

Subscribe: MEDICAL EXECUTIVE POST for curated news, essays, opinions and analysis from the public health, economics, finance, marketing, IT, business and policy management ecosystem.

Posted on October 21, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

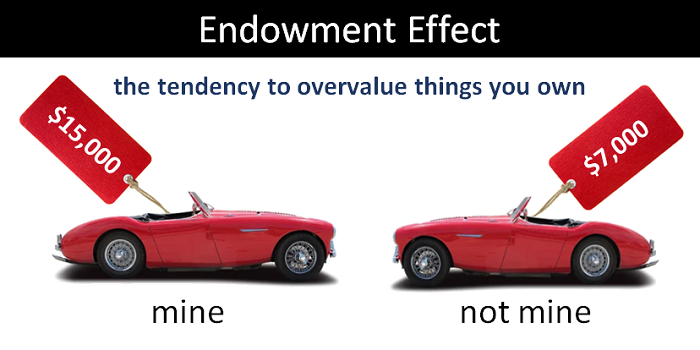

The Meaningful Endowment Effect is the tendency to value things more highly when they’re personally meaningful. It’s why a homemade gift can feel priceless while a store-bought one feels ordinary. Or, a coveted sports car, etc.

Our brains attach emotional significance to objects, inflating their value. This effect explains why we hang onto mementos and keepsakes, even if they’re not objectively valuable.

So, next time you’re de-cluttering, remember: it’s not just stuff, it’s meaningful stuff.

Although some might view a budget as unnecessarily restrictive, sticking to a spending plan can be a useful tool in enhancing the wealth of a medical practice. So, I will emphasize keys to smart budgeting and how to track spending and savings in these tough economic times.

There is an aphorism that suggests, “Money cannot buy happiness.” Well, this may be true enough but there is also a corollary that states, “Having a little sure reduces the unhappiness.”

Unfortunately, today there is more than a little financial unhappiness in all medical specialties. The challenges range from the commoditization of medicine, aging demographics, Medicare reimbursement cutbacks and increased competition to floundering equity markets, the home mortgage crisis, the squeeze on credit and declines in the value of a practice. Few doctors seem immune to this “perfect storm” of economic woes.

Far too many physicians are hurting and it is not limited to above-average earning professionals. However, one can strive to reduce the pain by following some basic budgeting principles. By adhering to these principles, physicians can eliminate the “too many days at the end of the month” syndrome and instead develop a foundation for building real wealth and security, even in difficult economic climates like we face today.

There are three major budget types. A flexible budget is an expenditure cap that adjusts for changes in the volume of expense items. A fixed budget does not. Advancing to the next level of rigor, a zero-based budget starts with essential expenses and adds items until the money is gone. Regardless of type, budgets can be extremely effective if one uses them at home or the office in order to spot money troubles before they develop.

For the purpose of wealth building, doctors may think of this budget as a quantitative expression of an action plan. It is an integral part of the overall cost-control process for the individual, his or her family unit or one’s medical practice.

Preparing a net income statement (lifestyle cash flow budget) is often difficult because many doctors perceive it as punitive. Most doctors do not live a disciplined spending lifestyle and they view a budget as a compromise to it. However, a cash flow budget is designed to provide comfort when there is surplus income that can be diverted for other future needs. For example, if you treat retirement savings as just another periodic bill, you are more likely to save for it.

You may construct a personal cash budget by recording each cash receipt and cash disbursement on a spreadsheet. Only the date, amount and a brief description of the transaction are necessary. The cash budget is a simple tool that even doctors who lack accounting acumen can use. Since it is possible to track the cash-in and cash-out in the same format used for a standard check register, most doctors find that the process takes very little time. Such a budget will provide a helpful look at how well you are staying within available resources for a given period.

We then continue with an analysis of your operating checkbook and a review of various source documents such as one’s tax return, credit card statements, pay stubs and insurance policies. A typical statement will show all cash transactions that occur within one year. It is helpful to establish a monthly equivalent to all items of income and expense. For the purposes of getting started, note items of income and expense by the frequency you are accustomed to receiving or spending them.

What You Should Know About The ‘Action Plan’ Cash Budget

For a medical office, the first operations budget item might be salary for the doctor and staff. Operating assets and other big ticket items come next. Some of our doctors/clients review their office P&L statements monthly, line by line, in an effort to reduce expenses. Then they add back those discretionary business expenses they have some control over.

Now, do you still run out of money before the end of the month? If so, you had better cut back on entertainment, eating dinner out or that fancy, new but unproven piece of medical equipment. This sounds draconian until you remind yourself that your choice is either: live frugally later or live a simpler lifestyle now and invest the difference.

As a young doctor, it may be a difficult trade-off. By mid-life, however, you are staring retirement in the face. That is why the action plan depends on your actions concerning monetary scarcity, a plan that one can implement and measure using simple benchmarks or budgeting ratios. By using these statistics, perhaps on an annual basis, the doctor can spot problems, correct them and continue planning actively toward stated goals like building long-term wealth.

Useful Calculations To Assess Your Budgeting Success

In the past, generic budgeting ratios would emphasize not spending more than 15 to 20 percent of your net salary on food or 8 percent on medical care. Now these estimates have given way to more rigorous numbers. Personal budget ratios, much like medical practice financial ratios, represent comparable benchmarks for parameters such as debt, income growth and net worth. Although these ratios are still broad, the following represent some useful personal budgeting ratios for physicians.

• Basic liquidity ratio = liquid assets / average monthly expenses. Cash-on-hand should approach 12 to 24 months or more in the case of a doctor employed by a financially insecure HMO or fragile medical group practice. Yes, chances are you have heard of the standard notion of setting enough cash aside to cover three months in a rainy day scenario. However, we have decried this older laymen standard for many years in our textbooks, white papers and speaking engagements as being wholly insufficient for the competitively unstable environment of modern healthcare.

• Debt to assets ratio = total debt / total assets. This percentage is high initially but should decrease with age as the doctor approaches a debt-free existence

• Debt to gross income ratio = annual debt repayments / annual gross income. This represents the adequacy of current income for existing debt repayments. Doctors should try to keep this below 20 to 25 percent.

• Debt service ratio = annual debt repayment / annual take-home pay. Physicians should aim to keep this ratio below 25 to 30 percent or face difficulty paying down debt.

• Investment assets to net worth ratio = investment assets / net worth. This budget ratio should increase over time as retirement approaches.

• Savings to income ratio = savings / annual income. This ratio should also increase over time as one retires major obligations like medical school debt, a practice loan or a home mortgage.

• Real growth ratio = (income this year – income last year) / (income last year – inflation rate). This budget ratio should grow faster than the core rate of inflation.

• Growth of net worth ratio = (net worth this year – net worth last year) / net worth last year – inflation rate). Again, this budgeting ratio should stay ahead of inflation.

In other words, these ratios will help answer the question: “How am I doing?”

Pearls For Sticking To A Budget

Far from the burden that most doctors consider it to be, budgeting in one form or another is probably one of the greatest tools for building wealth. However, it is also one of the greatest weaknesses among physicians who tend to live a certain lifestyle.

In fact, we have found that less than one in 10 medical professionals have a personal budget. Fear, or a lack of knowledge, is a major cause of procrastination. Fortunately, the following guidelines assist in reversing this microeconomic disaster.

1. Set reasonable goals and estimate annual income. Do not keep large amounts of cash at home or office. Deposit it in an FDIC insured money-market account for safety. Do not deposit it in a money market mutual fund with net asset value (NAV) that may “break the buck” and fall below the one-dollar level. Track actual bills and expenses.

2. Do not pay bills early, do not have more taxes withheld from your salary than needed and develop spending estimates to pay fixed expenses first. Fixed expenses are usually contractual and usually include housing, utilities, food, Social Security, medical, debt repayments, homeowner’s or renter’s insurance, auto, life and disability insurance, etc. Reduce fixed expenses when possible. Ultimately, all expenses get paid and become variable in the long run.

3. Make it a priority to reduce variable expenses. Variable expenses are not contractual and may include clothing, education, recreational, travel, vacation, gas, cable TV, entertainment, gifts, furnishings, savings, investments, etc. Trim variable expenses by 5 to 20 percent.

4. Use “carve-outs or “set-asides” for big ticket items and differentiate true wants from frivolous needs.

5. Calculate both income and expenses as a percentage of your total budget. Determine if there is a better way to allocate resources. Review the budget on a monthly basis to notice any variance. Determine if the variance was avoidable, unavoidable or a result of inaccurate assumptions. Take corrective action as needed.

6. Know the difference between saving and investing. Savers tend to be risk adverse while investors understand risk and take steps to mitigate it. Watch mutual fund commissions and investment advisory fees, which cut into return-rates. Keep investments simple and diversified (stocks, bonds, cash, index, no-load mutual and exchange traded funds, etc.).

Sooner or later, despite the best of budgeting intentions, something will go awry. A doctor will be terminated or may be the victim of a reduction-in-force (RIF) because of cost containment initiatives.4 A medical practice partnership may dissolve or a local hospital or surgery center may close, hurting your practice and livelihood. Someone may file a malpractice lawsuit against you, a working spouse may be laid off or you may get divorced. Regardless of the cause, budgeting crisis management encompasses two different perspectives: awareness and execution.

First, if you become aware that you may lose your job, the following proactive steps will be helpful to your budget and overall financial condition.

• Decrease retirement contributions to the required minimum for company/practice match. • Place retirement contribution differences in an after-tax emergency fund. • Eliminate unnecessary payroll deductions and deposit the difference to cash. • Replace group term life insurance with personal term or universal life insurance. • Take your old group term life insurance policy with you if possible. • Establish a home equity line of credit to verify employment. • Borrow against your pension plan only as a last resort.

If you have lost your job or your salary has been depressed, negotiate your departure and get an attorney if you believe you lost your position through breach of contract or discrimination. Then execute the following steps to recalculate your budget and boost your wealth rebuilding activities.

• Prioritize fixed monthly bills in the following order: rent or mortgage; car payments; utility bills; minimum credit card payments; and restructured long-term debt.

• Consider liquidating assets to pay off debts in this order: emergency fund, checking accounts, investment accounts or assets held in your children’s names.

• Review insurance coverage and increase deductibles on homeowner’s and automobile insurance for needed cash.

• Then sell appreciated stocks or mutual funds; personal valuables such as furnishings, jewelry and real estate; and finally, assets not in pension or annuities if necessary.

• Keep or rollover any lump sum pension or savings plan distribution directly to a similar savings plan at your new employer, if possible, when you get rehired.

• Apply for unemployment insurance.

• Review your medical insurance and COBRA coverage after a “qualifying event” such as job loss, firing or even after quitting. It is a bit expensive due to a 2 percent administrative fee surcharge but this may be well worth it for those with preexisting conditions or who are otherwise difficult to insure. One may continue COBRA for up to 18 months.

• Consider a high deductible Health Savings Account (HSA), which allows tax-deferred dollars like a medical IRA, for a variety of costs not normally covered under traditional heath insurance plans. Self-employed doctors deduct both the cost of the premiums and the amount contributed to the HSA. Unused funds roll over until the age of 59½, when one can use the money as a supplemental retirement benefit.

• Eliminate unnecessary variable, charitable and/or discretionary expenses, and become very frugal.

Final Notes

The behavioral psychologist, Gene Schmuckler, PhD, MBA, sometimes asks exasperated doctors to recall the story of the old man who spent a day watching his physician son treating HMO patients in the office. The doctor had been working at his usual feverish pace all morning. Although he was working hard, he bitterly complained to his dad that he was not making as much money as he used to make. Finally, the old man interrupted him and said, “Son, why don’t you just treat the sick patients?” The doctor-son looked at his father with an annoyed expression and responded, “Dad, can’t you see, I do not have time to treat just the sick ones.”

Always remember to add a bit of emotional sanity into your budgeting and economic endeavors.

Regardless of one’s age or lifestyle, the insightful doctor realizes that it is never too late to take control of a lost financial destiny through prudent wealth building activities. Personal and practice budgeting is always a good way to start the journey.

NOTE: Dr. Marcinko is a former Certified Financial Planner and current Certified Medical Planner™. He has been a medical management advisor for more than a decade. He is the CEO of http://www.MarcinkoAssociates.com

The authors acknowledge the assistance of Mackenzie H. Marcinko PhD in the preparation of this article.

Posted on October 20, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Yep – Even the Smart Folks!

By Lon Jefferies MBA CMP® CFP®

Dr. David Edward Marcinko MBA MEd CMP®

In the Business Insider, Mandi Woodruff describes nine mental blocks that cause smart people to do dumb things. Review the list and itemize the factors that have negatively impacted your finances.

The Factors

Anchoring happens when we place too much emphasis on the first piece of information we receive regarding a given subject. For instance, when shopping for a wedding ring a salesman might tell us to spend three months’ salary. After hearing this, we may feel like we are doing something wrong if we stray from this advice, even though the guideline provided may cause us to spend more than we can afford.

Myopia (or nearsightedness) makes it hard for us to imagine what our lives might be like in the future. For example, because we are young, healthy, and in our prime earning years now, it may be hard for us to picture what life will be like when our health depletes and we know longer have the earnings necessary to support our standard of living. This short-sightedness makes it hard to save adequately when we are young, when saving does the most good.

Gambler’s fallacy occurs when we subconsciously believe we can use past events to predict the future. It is common for the hottest sector during one calendar year to attract the most investors the following year. Of course, just because an investment did well last year doesn’t mean it will continue to do well this year. In fact, it is more likely to lag the market.

Avoidance is simply procrastination. Even though you may only have the opportunity to adjust your health care plan through your employer once per year, researching alternative health plans is too much work and too boring for us to get around to it. Consequently, we stick with a plan that may not be best for us.

Confirmation bias causes us to place more emphasis on information that supports the opinion we already have. Consequently, we tend to ignore or downplay opinions that don’t mirror our own, leading us to make uninformed decisions.

NOTE: An interesting example of the confirmation bias is the case of David Rosenberg, who is one of the most well-known perpetual bears on Wall Street. In October, Mr. Rosenberg’s analysis forced him to warm to the current investment environment. His fans and followers, rather than appreciating his research and ability to adjust to new information, criticized him for changing his opinion.

As it turned out Mr. Rosenberg had fans not because of his expert analysis, but because he added intellectual heft to his followers pessimism and quasi-political desire for the system to collapse. Their view was that things were in permanent decline and his analysis, charts, and voice added respectability to their pre-existing bias. Mr. Rosenberg has now lost his fan base not because he was wrong for the last four years, but because he changed his mind.

Loss aversion affected many investors during the crash of 2008. During the crash, many people decided they couldn’t afford to lose more and sold their investments. Of course, this caused the investors to sell at market troughs and miss the quick, dramatic recovery.

Overconfident investing happens when we believe we can out-smart other investors via market timing or through quick, frequent trading. Data convincingly shows that people who trade most often underperform the market by a significant margin over time.

Mental accounting takes place when we assign different values to money depending on where we get it from. For instance, even though we may have an aggressive saving goal for the year, it is likely easier for us to save money that we worked for than money that was given to us as a gift.

Herd mentality makes it very hard for humans to not take action when everyone around us does. For example, we may hear stories of people making significant profits buying, fixing up, and flipping homes and have the desire to get in on the action, even though we have no experience in real estate.

Assessment

The good news is that being aware of these tendencies can help us avoid mistakes. We’ll never be perfect, but avoiding detrimental decisions based on mental prejudices can give us an advantage in our financial and retirement planning efforts.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

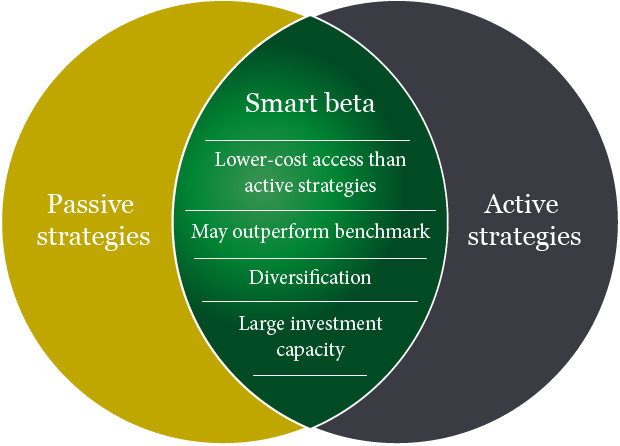

Offering a blend of active and passive styles of management, a smart beta portfolio is low cost due to the systematic nature of its core philosophy – achieving efficiency by way of tracking an underlying index (e.g., MSCI World Ex US). Combining with optimization techniques traditionally used by active managers, the strategy aims at risk/return potentials that are more attractive than a plain vanilla active or passive product.

Originally theorized by Harry Markowitz in his work on Modern Portfolio Theory (MPT), smart beta is a response to a question that forms the basis of MPT – how to best construct the optimally diversified portfolio. Smart beta answers this by allowing a portfolio to expand on the efficient frontier (post-cost) of active and passive. As a typical investor owns both the active and index fund, most would benefit from adding smart beta exposure to their portfolio in addition to their existing allocations.

Assessment: The smart beta approach is an arguably perfect intersection between traditional value investing and the efficient market hypothesis. But, is it worth the cost?

Posted on October 20, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The Gambler’s Fallacy occurs when we subconsciously believe we can use past events to predict the future. It is also called the Monte Carlo Fallacy, after the Casino de Monte-Carlo in Monaco where it was observed in 1913

For example, it is common for the hottest sector during one calendar year to attract the most investors the following year.

Of course, just because an investment did well last year doesn’t mean it will continue to do well this year. In fact, it is more likely to lag the market.

Posted on October 20, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Markets: The S&P 500hit an all-time high yesterday, closing out its sixth consecutive week of gains for its longest streak of 2024. The Dow and NASDAQ also closed in the green.

The largest Medicare Advantage insurers have prioritized profits over patient care by increasing the use of prior authorization in recent years to frequently deny post-acute care services to older adults, according to a report published Oct. 17th by the Senate Permanent Subcommittee on Investigations.

The drugstore chain CVS is in the process of shuttering “roughly 300” locations across the country in 2024, a spokesperson confirmed to Good Housekeeping. That includes the dozens of pharmacies in Target stores.

Posted on October 19, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

ACCORDING TO AUSTRIAN ECONOMISTS

BY PER BYLUND

Colleague Peter R. Quinones and Per Bylund return to the show to talk about the role of the entrepreneur not only in society, but according to the Austrian School of Economics. Medical perspectives are implied.

Posted on October 19, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

CVS Health may be breaking up…with itself. The board of directors at CVS Health—the parent company of CVS Pharmacy, pharmacy benefit managerCVS Caremark, and insurance unit Aetna—are working with a group of bankers to review the company’s strategy, which according to Reuters, may lead to a split between its pharmacy division and Aetna.

Apple climbed 1.23% on a Bloomberg report that iPhone 16 demand has been shockingly strong in China.

Verizon Communications will purchase $1 billion worth of US Cellular’s wireless spectrum licenses. Verizon rose just 0.34%—but it’s a huge deal for US Cellular, which popped 7.22%, and Telephone and Data Systems, which owns 82% of US Cellular, and soared 15.40%.

Intuitive Surgical rose to a new all-time high, climbing 10.01% on strong earnings powered by sales of its da Vinci device.

Lamb Weston, the company behind the french fries you overindulge in every time you go out to dinner, is being pushed by activist investor Jana Partners toward exploring a sale. Shareholders rejoiced, and the stock rose 10.17%.

Stocks Down

CVS Health sank 5.23% on the news that CEO Karen Lynch will be replaced by David Joyner after three years at the helm of the struggling pharmacy/retailer. Joyner ran the company’s pharmacy service business for the last two years.

WD-40 seems like the staple of all consumer staples, but the company missed on both revenue and earnings estimates last quarter. Shares fell 4.79% on the news.

American Express dropped 3.15% after the credit card company reported a rare miss today, beating bottom-line estimates but missing revenue forecasts last quarter.

MGP Ingredients makes all the booze you drink under different brand names, but people aren’t drinking enough. The beverage maker issued preliminary earnings that included a 24% drop in sales. Shares tanked 24.16%.

Here’s where the major stock market benchmarks ended:

The S&P 500® index (SPX)rose 23.20 points (0.40%) to 5,864.67, a new record high close, to end the week up 0.85%; the Dow Jones Industrial Average® ($DJI) added 36.86 points (0.09%) to 43,275.91, also another record high finish, to end the week up 0.96%; and the $COMP gained 115.94 points (0.63%) to 18,489.55 to end the week up 0.80%.

The 10-year Treasury note yield (TNX) fell two basis points to 4.07%.

The CBOE Volatility Index® (VIX) fell to 18.17, the lowest since September 30.

A new survey results may prompt health systems to second-guess some of their future plans. A recent University of Michigansurvey found 74% of adults ages 50+ have “very little or no trust” in health info generated by AI. Maybe it’s not time to roll out chatbots on patient portals just yet.

The Society of Physician Entrepreneurs (SoPE) was established as a community of interest in 2008 by several members of the American Academy of Otolaryngology – Head and Neck Surgery (AAO-HNS), including Dr. Arlen Meyers, the founding past President & CEO. SoPE became a separate and independent legal entity; incorporating in Washington, D.C. in January 2011. It is a 501 (c) 6 member organization with the stated purpose of providing support; idea stage through funding, for physician entrepreneurs with ideas on how to improve healthcare.

SoPE’s vision is to accelerate physician originated biomedical innovation.

The mission of SoPE is to foster scholarship in biomedical entrepreneurship and provide education, training and support; idea stage through funding, to primarily community-based physician entrepreneurs in the interest of better healthcare.

SoPE membership is open to all physicians and also accepts individuals as associate members; representatives of medical device, legal, venture capital, and other firms with an interest in serving and/or supporting physician entrepreneurs.

Posted on October 18, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Are doctors using publicly available tools like ChatGPT? The answer, Fierce Healthcare finds, is yes. In the first in-depth look of its kind into physician use of public genAI tools, Fierce Healthcare spoke with nearly two dozen doctors, students, AI experts and regulators, and helped conduct a survey of more than 100 physicians. The reporting confirms that some doctors are turning to tools intended for non-clinical uses to make clinical decisions.

A collaborative survey between Fierce Healthcare and physician social network Sermo found that 76% of respondents reported using general-purpose LLMs in clinical decision-making. With no standardized guidelines, lagging physician training and regulators racing to try to keep up with rapidly changing technology, guardrails to protect patients appear to be years behind current rates of utilization.

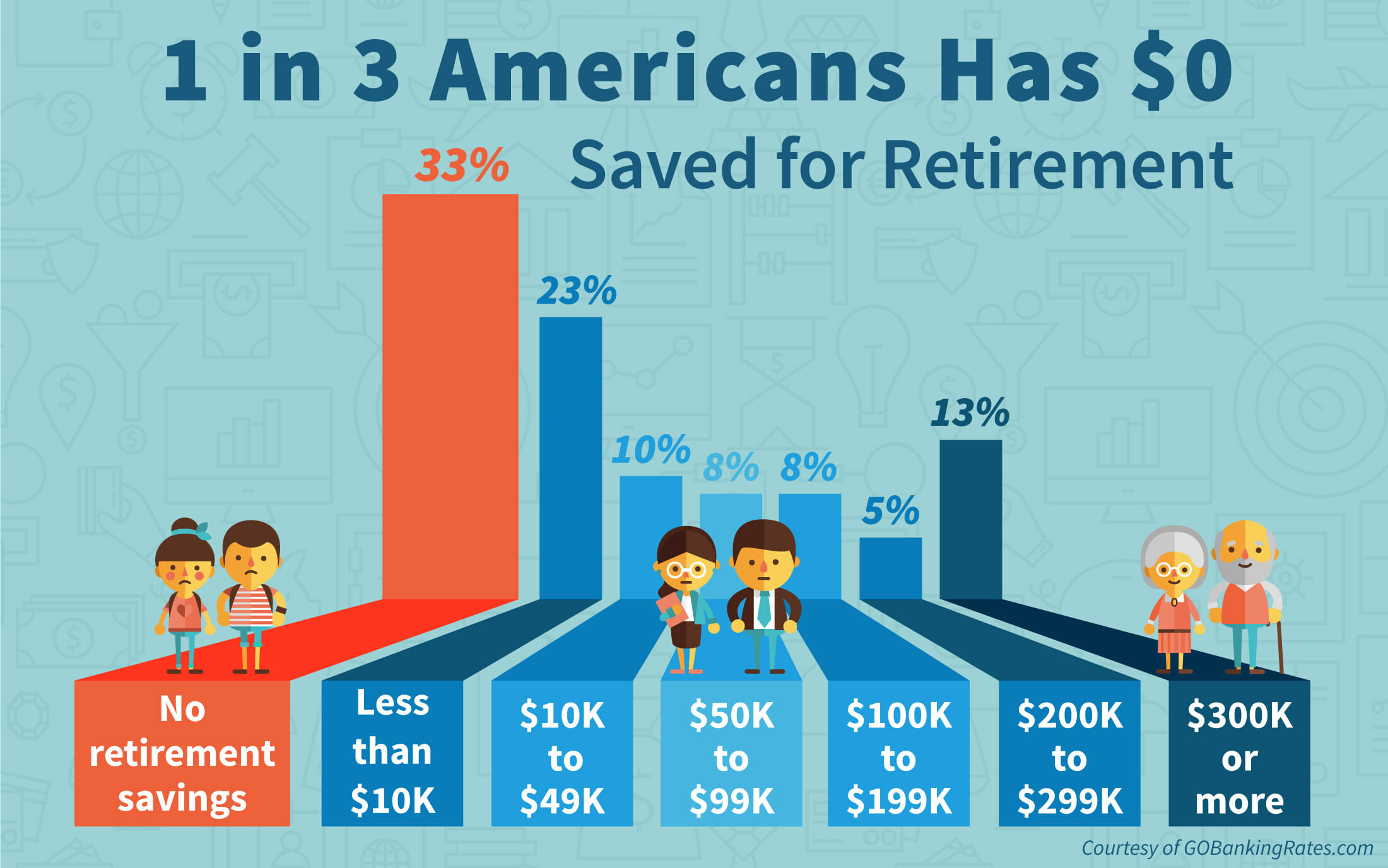

According to the National Institute on Retirement Security, almost 40 million households have no retirement savings at all. The Employee Benefit Research Institute (EBRI) estimates in its 2019 Retirement Security Projection Model that America’s current retirement savings deficit is $3.8 trillion.

What does that mean? Well, the EBRI report aggregates the savings deficit of all U.S. households headed by someone between the ages of 35 and 64, inclusive. In total, those households have $3.8 trillion fewer dollars in savings than they should have for retirement.

For more recent data, Fidelity Investments reported that in the third quarter of 2022 the average account balance for an IRA was $101,900. Employees with a 401(k) averaged $97,200, while those with a 403(b) had $87,400.

Fidelity also estimated that “an average retired couple age 65 in 2022 may need approximately $315,000 saved (after tax) to cover health care expenses in retirement.” Keeping in mind that more Americans are also living longer than ever before, they will face more challenges to cover medical expenses in retirement.

Posted on October 18, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Chip stocks recovered lost ground today thanks to a strong earnings report from TSMC (more on that below). Nvidia led the group higher, rising 0.89% to yet another new all-time high.

Blackstone rose 6.30% to a new record high after the world’s largest alternative asset manager reported an excellent quarter.

Expedia popped 4.75% after a report by the Financial Times revealed that Uber had explored an acquisition of the travel site. Expedia shareholders cheered the news, while Uber shares sank 2.45%.

Stocks Down

Robinhood fell 2.27% after announcing its new Legend trading platform geared specifically toward advanced traders.

Lucid Group plummeted 17.99% on the news that the EV automaker is offering over 262 million shares of its common stock in an attempt to raise funds.

CSX dropped 6.71% after missing both top- and bottom-line estimates last quarter thanks in no small part to hurricanes Helene and Milton.

Health insurance stocks took a beating today due to a not-great earnings report from ElevanceHealth (more on that below, too). Centene Corp. fell 9.09%, while Molina Healthcare tumbled 12.55%.

The S&P 500® index (SPX) slipped 1.00point (–0.02%) to 5,841.47; the $DJI added 161.35 points (0.37%) to 43,239.05; and the NASDAQ Composite®($COMP) rose 6.53 points (0.04%) to 18,373.61.

The 10-year Treasury note yield (TNX) climbed eight basis points to 4.1%.

The CBOE Volatility Index® (VIX) sank to 18.97 by late Thursday, a two-week low.

The average amount owed on “upside down” auto loans, in which the balance is more than the car is worth, hit a record high of $6,458 in the third quarter, according to Edmunds, a site that helps consumers research and buy cars

Financial planning as a concept has been around for a long time, but not as we know it today. When Loren Dunton set up the Society for Financial Counseling Ethics in 1969, or when the first graduating class of the College of Financial Planning graduated in 1973, financial planning was very different. It was centered around selling limited partnerships, which came to end with the Tax Reform Act of 1986.

However, financial planning re-emerged — all thanks to Richard Averitt III. The certified financial planner gave new meaning to financial planning, this time with a focus on who the client is and what their needs are. This approach was purely methodological in nature.

Soon after, financial planning picked up again. According to the Certified Financial Planner (C.F.P.) Board of Standards in Denver, today, there are more than 94,000 C.F.P.s worldwide, including over 48,000 in the U.S. Additionally, there are also organizations that have been set up for C.F.P.s, such as the Financial Planning Association (FPA), which has approximately 22,000 members.

And, don’t forget the emerging Certified Medical Planner™ professional fiduciary designation for physicians, dentists, nurses and allied healthcare clients.

Financial planning, as we know it now, includes investing, tax planning, retirement planning, and basically other ways to get your finances in order and create mindful budgets to ensure a safe and secure future. Getting a step ahead of your spending and finances is beneficial in the long run and Financial Planning Month in October is the perfect time to do that.

Posted on October 17, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Authors of the seminal textbook Why Nations Fail, Daron Acemoglu, James Robinson, and former International Monetary Fund chief economist Simon Johnson will split the roughly $1 million cash prize for their research, which found a link between a country’s prosperity and the institutions it established during European colonization.

Places developed either “inclusive” or “extractive” institutions based on population density. The former allowed for inclusive governance (i.e., democracy), while the latter extracted resources to benefit a small group of elites.

Countries that developed inclusive institutions have experienced long-term prosperity; those with exclusive institutions haven’t. “Broadly speaking, the work that we have done favors democracy,” Acemoglu said.

Eample: In the twin cities of Nogales, on the US-Mexico border, the north and south parts of the transborder city have the same climate and the same resources, but the section in the US is far richer because of the country’s institutions, according to the researchers.

Critics. Some academics argue the Nobel winners’ premise ignores the effects of culture on prosperity. Others point to an irrefutable counterexample: China continues to experience explosive growth despite having an autocratic government.

Posted on October 17, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David E. Marcinko MBAMEd CMP

SWARM INTELLIGENCE IN MEDICINE

***

Warm Learning or Swarm Intelligence, is how swarms of bees or birds move in response to their environment.

When applied to data there is “more peer-to-peer communications, more peer-to-peer collaboration, more peer-to-peer learning and that’s the reason why swarm learning will become more and more important as … as the center of gravity shifts” from centralized to decentralized data.

Medicine Example:

Consider this example, “A hospital trains their machine learning models on chest X-rays and sees a lot of tuberculosis cases, but very little of lung collapsed cases. So therefore, this neural network model, when trained, will be very sensitive to what’s detecting tuberculosis and less sensitive towards detecting lung collapse.”

“However, we get the converse of it in another hospital. So what you really want is to have these two hospitals combine their data so that the resulting neural network model can predict both situations better. But since you can’t share that data, swarm learning comes in to help reduce that bias of both the hospitals.”

And this means, “each hospital is able to predict outcomes, with accuracy and with reduced bias, as though you have collected all the patient data globally in one place and learned from it.”

Moreover, it’s not just hospital and patient data that must be kept secure. What swarm learning does is to try to avoid or reduce the sharing of data, or totally prevent the sharing of data, to [a model] where you only share the insights, or you share the learnings.

Posted on October 17, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

***

By Vitaliy N. Katsenelson, CFA

***

EDITOR’S NOTE: In this interview with investment website @GuruFocus, my colleague Vitaliy shares the full gamut of how he invests, where and why. He touches on the role of being eclectic when investing, how to invest abroad, and how value investors should think about macro-economics and finance, among many other important topics. Enjoy this fun and wide-ranging interview!

Posted on October 17, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Goldman Sachs’ profit jumped 45% in monster quarter. The investment bank made $3 billion of profit on revenue of nearly $13 billion in Q3, it reported yesterday, surpassing even the rosiest of expectations. Bloomberg reported that it was the best quarter ever for Goldman’s stock trading unit, putting the group on track for a record year.

Walgreenssaid it will close 1,200 US stores, about one in seven locations, by 2027. The retailer will shutter 500 stores by the end of next year.

Trump Media & Technology Group has had a wild week, falling nearly 10% yesterday before trading of the stock was halted, then popping 15.52% today. Election hype, a Trump-sponsored cryptocurrency, and Truth+, a new streaming service, are keeping shareholders on their toes.

Abbott Laboratories rose 1.53% thanks to a stronger-than-expected earnings report powered by the company’s impressive medical device sales.

Aspen Aerogels makes insulating material for batteries, which sounds boring to everyone but the Department of Energy. The DOE signed a conditional commitment to loan the company up to $670 million, sending shares 13.24% higher.

DOWN STOCKS

Novavax plummeted 19.44% after the FDA put a hold on the pharma company’s flu and Covid vaccine combination.

Interactive Brokers enjoyed higher revenue and more trading from its user base last quarter, but earnings per share came in under expectations, and shares sank 4.05%.

The SPX rose27.21points (0.47%) to 5,842.47; the Dow Jones Industrial Average® ($DJI) added 337.28 points (0.79%) to 43,077.70; and the NASDAQ Composite®($COMP) increased 51.49 points (0.28%) to 18.367.08.

The 10-year Treasury note yield (TNX) fell two basis points to just below 4.02%, the lowest close since October 4.

The CBOE Volatility Index® (VIX) dropped moderately to 19.58, still elevated considering stock market strength.

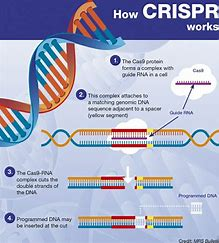

CRISPR is a family of DNA sequences found in the genomes of prokaryotic organisms such as bacteria and archaea. These sequences are derived from DNA fragments of bacteriophages that had previously infected the prokaryote. They are used to detect and destroy DNA from similar bacteriophages during subsequent infections

Posted on October 16, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

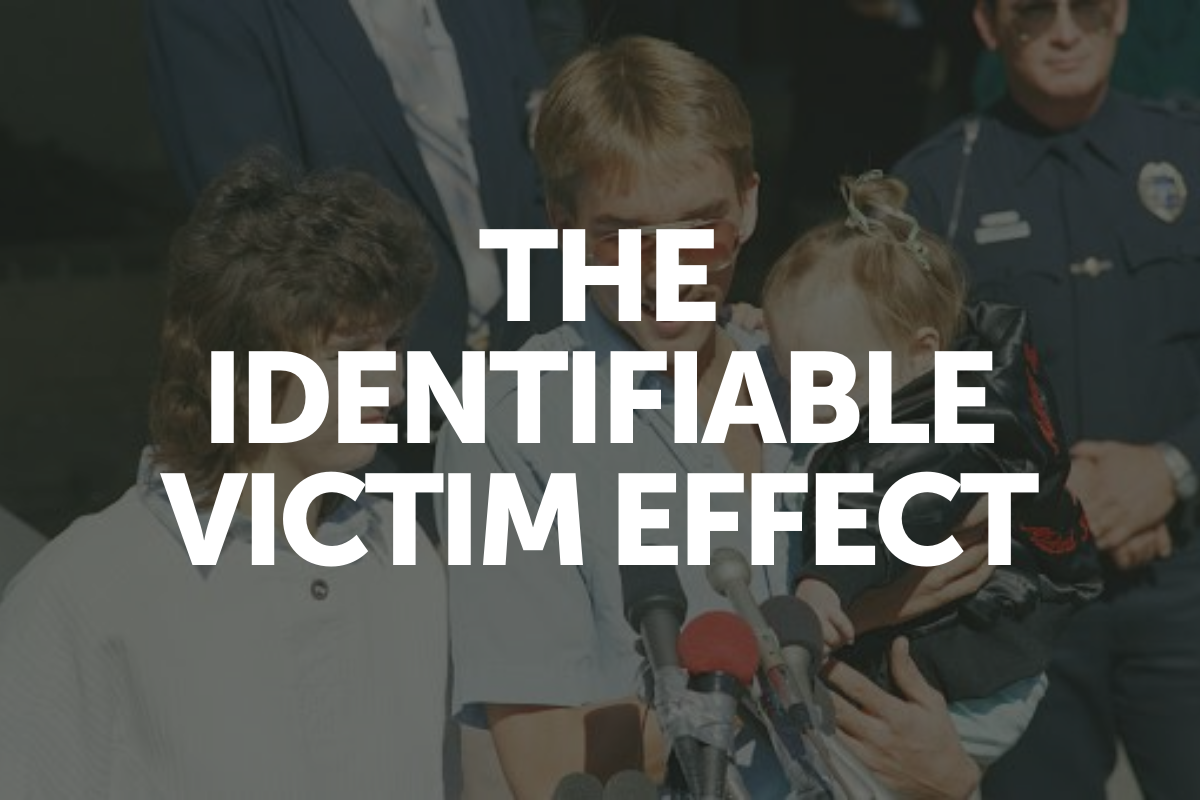

IDENTIFIABLE PERPETRATOR EFFECT

By Staff Reporters

***

***

According to colleague Dan Ariely PhD, the The Identifiable Victim Effect [IVE] is why we’re more moved by one person’s story than by statistics. It’s easier to empathize with a single, identifiable victim than with a faceless group. Charities know this and often highlight individual stories to tug at our heartstrings. It’s a powerful reminder that our compassion is wired for personal connections.

The identifiable victim effect has two components. People are more inclined to help an identified victim than an unidentified one, and people are more inclined to help a single identified victim than a group of identified victims. Although helping an identified victim may be commendable, the identifiable victim effect is considered a cognitive bias. From a consequential point of view, the cognitive error is the failure to offer N times as much help to N unidentified victims.

The identifiable victim effect has a mirror image that is sometimes called the identifiable perpetrator effect. Research has shown that individuals are more inclined to mete out punishment, even at their own expense, when they are punishing a specific, identified perpetrator.

So, when you hear a touching story that makes you want to help, remember: it’s your brain responding to the power of a single, human face.

Posted on October 16, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Maximum lifespans. The upper limit of human life expectancy is leveling out, according to a new study published in the journal Nature Aging. Back in 1990, life-extending tech and health measures were increasing the average global lifespan by about 2.5 years per decade, but that dropped to 1.5 years per decade in the 2010s and closer to zero in the US, where there are more drug overdoses, shootings, and medical care inequities.

Sphere Entertainment popped 6.33% on the news that a second Sphere will be built in Abu Dhabi. London was originally supposed to be the location of a second venue, but they’ve already got the Eye, and didn’t need more circular tourist attractions.

Oklo, a Sam Altman-backed nuclear energy startup, rose another 16.04% on the news that Google will purchase nuclear power to turbocharge its AI infrastructure.

Charles Schwab climbed 6.10% after the bank announced a top and bottom line beat last quarter, as well as higher revenue projections for the full fiscal year.

Boeing somehow gained 2.26% after announcing it is raising $35 billion to support its struggling finances as the machinist union strike enters its second month.

Wolfspeed, which sounds like a super power in a YA novel, soared 21.27% on the news that the US government will provide the chipmaker with up to $750 million in government grants.

STOCKS DOWN

Semiconductor stocks got a double whammy in the last 48 hours. First, Bloomberg revealed that US officials are considering limiting the sale of AI chips outside the country. Then, ASMLmissed its Q3 sales estimates (more on that below). Nvidia shares slid 4.52%, AMD fell 5.22%, and Intel dropped 3.33%.

Citigroup beat earnings estimates this quarter, but shareholders punished the bank for setting aside more money in case of higher loan losses ahead. Shares dropped 5.11%.

Coty, parent company of numerous beauty brands like CoverGirl, fell 10.74% to a new 52-week low after it warned of a sales slowdown in the coming quarters.

Enphase Energy tumbled 9.29% after RBC analysts downgraded the solar power stock, citing growing competition from the likes of Tesla as well as slowing demand for solar batteries.

Speaking of energy, oil stocks plummeted on news of Israel’s targeting of Iranian military assets rather than crude production facilities. ExxonMobil fell 3.01%, Chevron dropped 2.67%, and ValeroEnergy sank 4.62%.

Here’s where the major benchmarks ended yesterday:

The S&P 500® index (SPX) fell 44.59 points (–0.76%) to 5,815.26; the Dow Jones Industrial Average® ($DJI) dropped 324.80 points (–0.75%) to 42,740.42; and the NASDAQ Composite®($COMP) lost 187.09 points (–1.01%) to 18,315.59.

The 10-year Treasury note yield (TNX) fell three basis points to 4.04%, the lowest close in a week.

The CBOE Volatility Index® (VIX) climbed to 20.72, an elevated level.

Millions of seniors will lose access to their Medicare Advantage plans after major insurer cuts in the aftermath of the Inflation Reduction Act. Experts spoke with Newsweek about what’s going on and what steps seniors can take to get the coverage they need.

Posted on October 15, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters &The Medicare Team

Medicare open enrollment—which runs from October 15th through December 7th this year—is your chance to check in on your Medicare plan and, if needed, change it.

***

***

Mark your calendars — Medicare Open Enrollment starts October 15th! Did you know new benefits are coming to Medicare drug coverage next year?

Also starting next year, you can choose to participate in a program that spreads your out-of-pocket drug costs across the calendar year, instead of paying all at once at the pharmacy. It’s called the Medicare Prescription Payment Plan — and you can opt in with your plan throughout the 2025 plan year. Contact your plan for more details.

Remember, Medicare plans can change from one year to the next, and so can your health needs. Preview and compare all your health and drug options and see if you can save!

The science of the modern medical practice valuation can be traced to the Estate of Edgar A. Berg v. Commissioner (T. C. Memo 1991-279). In this case, the Court criticized CPAs as not being qualified to perform business valuations, failing to provide analysis of an appropriate discount rates, and making only general references to justify their “Opinion of Value.”

In rejecting accountants, the Court accepted IRS economists because of background, education and training, as well as discount rate calculations and reproducible evidence applied to the assets being examined. This marked the beginning of the Tax Court leaning toward the side with the most comprehensive appraisal. Previously, it had a tendency to “split the difference.” Now, some feel the Berg case launched the valuation profession; especially for contemporaneous health economists.

But, it was not until after 1995 that the IRS issued guidelines for the valuation of physician practices. As a result, the Uniform Standards of Professional Appraisal Practice [USPAP] requires that a blended constellation of three recognized valuation approaches (income, market, and cost approaches) be considered when estimating fair market value.

Operative Valuation Definitions

When pursuing any discussion of medical practice worth, two key elements must be understood: (1) the valuation process, and (2) fair market value. According to the Dictionary of Health Economics and Finance

Practice valuation is the “the formal process of determining the worth of a healthcare or other medical business entity, at a specific point in time, and the act or process of determining fair market value.”

Fair market value [FMV] is “a legal term generally meaning the price at which a willing buyer will buy, and a willing seller will sell an asset in an open free market with full disclosure.” IRS Revenue Ruling 59-60 clearly states that FMV “is essentially a future prophesy and must be based on facts available at the required date of appraisal”

Unfortunately, the value of a medical practice cannot be directly observed by activity in thinly traded private markets. Perhaps this is why we continually observe the following valuation blunders? They are committed by both sellers and buyers who are pursuing opposite objectives; sale price maximization versus price minimization?

Top 10 Blunders:

Not Understanding What a Medical Practice Valuation Is and Is Not

Valuations are not source document fraud audits.

Valuations are material representations providing a range of transferable worth.

Valuations are reproducible estimates based on economic assumptions.

Valuations are not “back-of-the envelope multiples” using specious benchmarks.

Valuations are defensible and “signed-off” attesting to USPAP/IRS formats.

Financial accounting value [book-value] is not fair market value.

Professional valuators represent only one party at arm’s length; not both sides.

Engagement solicitor and/or valuation payer is the client.

Unbiased valuators do not provide financing or equity-participation schemes. Although not standardized, the Institute of Medical Business Advisors, Inc uses the following three levels that approximate engagement types for the industry.

2. A Limited Valuation lacks additional suggested USPAP procedures. It is considered an “agreed-upon-procedure”, used in circumstances where the client is the only user [i.e., updating a buy-sell agreement, or practice buy-in for a valued associate] and not for external purposes. No onsite visit is needed. A formal Opinion of Value is not rendered.

3. Not Observing Industry Standards, Rules and Regulations

Specifically, in USPAP transactions involving physician practices, the IRS implied:

Ad-Hoc Valuation is low level engagement that provides a gross and non-specific approximation of value based on limited meters by involved parties. Neither a written report, nor an Opinion of Value is rendered. It is often used periodically as an internal organic growth / decline gauge.

A Comprehensive Valuation is an extensive service designed to provide an unambiguous Opinion of Value range. It is supported by all procedures that valuators deem relevant with mandatory onsite review. This “gold-standard” is suitable for contentious situations like divorce, partnership dissolution, estate planning and gifting, etc. The written Opinion of Value is applicable for litigation support activities like depositions and trial. It is also useful for external reporting to bankers, investors, the public and IRS, etc.