BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

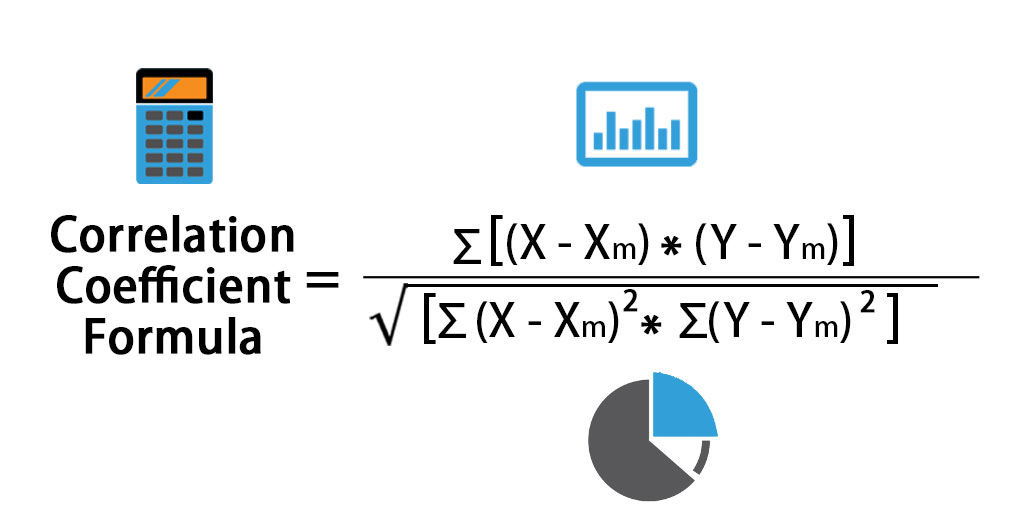

Correlation measures the relationship between two investments–the higher the correlation, the more likely they are to move in the same direction for a given set of economic or market events. Correlation, in the finance and investment industries, is a statistic that measures the degree to which two securities move in relation to each other. Correlations are used in advanced portfolio management, computed as the correlation coefficient which has a value that must fall between -1.0 and +1.0.

So if two securities are highly positively correlated, they will move in the same direction the vast majority of the time. Negatively correlated investments do the opposite–as one security rises, the other falls, and vice versa. No correlation means there is no relationship between the movement of two securities–the performance of one security has no bearing on the performance of the other.

Correlation is an important concept for portfolio diversification--combining assets with low or negative correlations can improve risk-adjusted performance over time by providing a diversity of payouts under the same financial conditions.

Posted on April 20, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

According to colleague Dan Ariely PhD, Bereavement Sex is one of those coping mechanisms that sounds strange but makes sense when you think about it. In the face of loss, our brains crave connection and comfort.

Engaging in sex after a significant loss can be a way to feel alive and regain a sense of control. It’s a testament to our complex emotional wiring, where grief and intimacy intertwine.

Choice Overload is the difficulty in making a decision when faced with too many options. It’s like standing in front of an ice cream counter with 31 flavors and feeling paralyzed.

Among personal decision-makers, a prevention focus is activated and people are more satisfied with their choices after choosing among few options compared to many options, i.e. choice overload. However, individuals can also experience a reverse choice overload effect when acting as proxy decision-maker, too.

It is widely accepted that having more choices is inherently positive. When there are more available options from which to choose, an individual is more likely to be able to select the particular option that is the best fit and most likely to satisfy them. Choice is typically thought to be related to personal freedom and enhanced well-being.

Therefore, according to colleague Neal Baum MD, for most individuals the ultimate goal is to constantly maximize their choices in life to increase their overall satisfaction and well-being. The decision-making process, however, is a complex cognitive task that does not always lead to positive outcomes.

Thus, while having options is generally good, too many choices can lead to anxiety and decision fatigue. This is why curated selections and recommendations are so popular – they simplify the decision-making process’ according to another colleague Dan Ariely PhD.

So, when you’re overwhelmed by choices, narrow them down to a manageable number and make your decision easier.

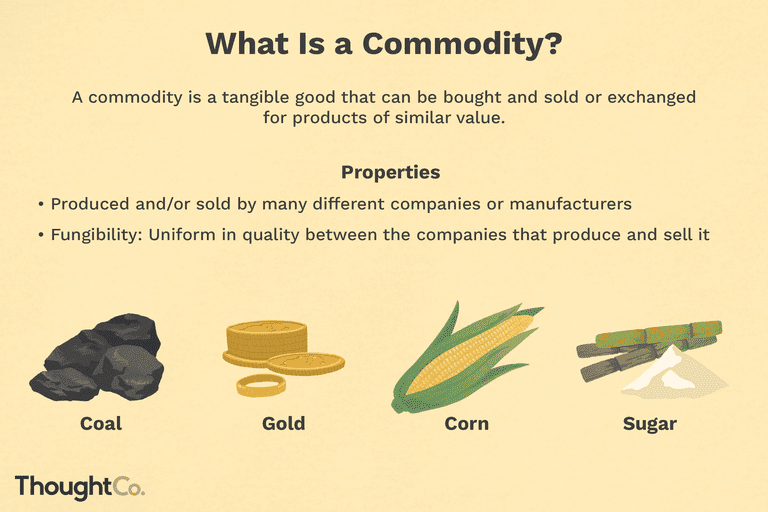

Commodities: Commodities are raw materials or primary agricultural products that can be bought or sold on an exchange or market. Examples include grains such as corn, foods such as coffee, and metals such as copper.

Commodity Futures: Agreements to buy or sell a specific amount of a commodity or financial instrument at a particular price on a stipulated future date related to basic raw materials such as precious metals and natural resources.

Commodity Intensity: Commodity intensity refers to commodity usage per unit of economic growth. An emerging, more manufacturing-based economy will usually be more commodity intensive in terms of its growth than will a more developed, service-oriented economy.

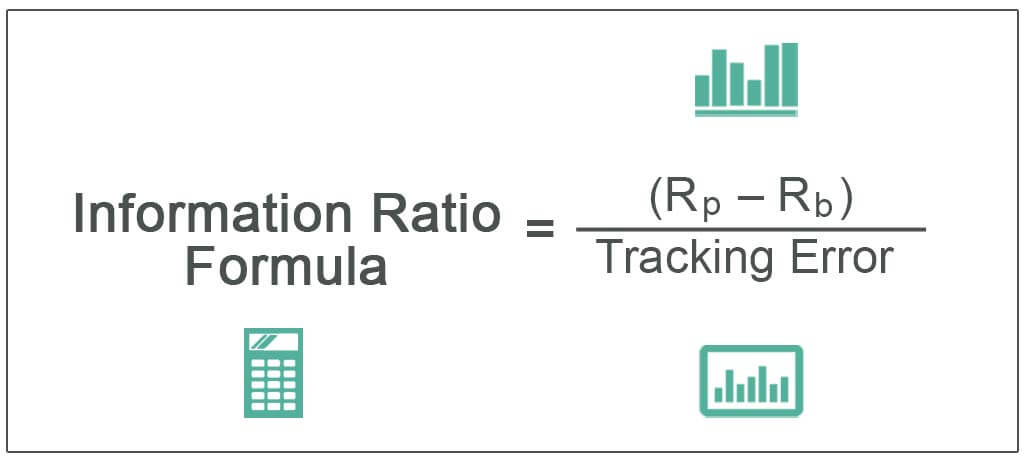

The Information Ratio (IR) is a risk-adjusted rate of return measure for comparing the performance of active investment managers over time. Its purpose is to help determine how much return an active portfolio manager has added per unit of active management risk.

Think of IR as a Sharpe Ratiofor active investment management; the IR is more focused than the Sharpe Ratio. Starting with the Sharpe Ratio’s formula, if we replace the excess return in the numerator with a portfolio’s active return (the average annualized return of an actively managed portfolio minus the average annualized return of the portfolio’s benchmark over a given period, adjusted for the portfolio’s market risk exposure), and you replace the Sharpe Ratio’s standard deviation of excess returns in the denominator with the standard deviation of a portfolio’s active returns over the period, you have the IR.

While the Sharpe Ratio expresses the amount of excess return per unit of overall risk, the IR computes only the active management-driven (alpha) returns per unit of alpha-driven risk. And while the Sharpe Ratio’s excess returns are calculated with regard to what is considered to be a relatively risk-free asset, such as a U.S. Treasury bill, the IR’s active returns are calculated with regard to each portfolio’s specific market benchmark.

The higher the IR, the better. The IR should be measured over a meaningful period of time, typically at least three to five years. The IR is not perfect–it can be influenced by external factors such as changes in market volatility. The standard deviation of active returns in the IR’s denominator is called tracking error. Tracking error will tend to increase in volatile markets for even the best active managers.

Market Capitalization: Market capitalization is the market value of all the equity of a company’s common and preferred shares. It is usually estimated by multiplying the stock price by the number of shares for each share class and summing the results.

Market Depth: The degree to which a market can execute large market orders without impacting the price of a security. For example, a “deep” market for a stock will have a sufficient number of both bid and ask orders to keep a big order from significantly moving the security’s price.

Market Maker: A market maker exists to “create a market” for specific company securities by being willing to buy and sell those securities at a specified displayed price and quantity to broker-dealer firms that are members of the exchange. These firms help keep financial markets liquid by making it easier for investors to buy and sell securities–they ensure that there is always someone to buy and sell to at the time of trade.

Market Neutral: Equity market neutral strategies seek to eliminate the risks of the equity market by holding up to 100% of net assets in long equity positions and up to 100% of net assets in short equity positions. These strategies attempt to exploit differences in stock prices by being long and short in stocks within the same sector, industry, market capitalization, etc. If successful, these strategies should generate returns independent of the equity market. Equity market neutral portfolios have two key sources of return:

the Treasury Bill return (the interest on proceeds from short sales held in cash as collateral)

the difference (the “spread”) between the return on the long positions and the return on the short positions. Stock picking, rather than broad market moves, should drive most of a market-neutral strategy’s total return (save for any return from the 100% cash position).

It’s important to point out that here is the risk of theoretical unlimited amount of loss with short selling, (i.e. the price of the short-sold stocks increases; the long position can only go down to $0).

Market Order: An order placed with a bank or brokerage firm to immediately buy or sell a security at the best available current price. May also be referred to as an “unrestricted order.”

Prepayment risk is typically used in reference to mortgage-backed securities. It refers to the risk that mortgage refinancing activity might increase when market interest rates decline, which is generally not favorable for MBS investors.

For example, when homeowners refinance their mortgages, MBS investors are “prepaid,” shortening the life of their investments and forcing investors to reinvest the proceeds under lower interest rate conditions than what were most likely prevailing at the time of the original MBS investment.

Price adjustments for prepayment risk are one factor that helps explain why MBS, despite their generally high credit quality, have higher yields than comparable-maturity Treasury securities.

Classic Definition: A comprehensive review of a physician, clinic, facility, medical provider or hospital’s charges to ensure Medicare billing compliance through complete and accurate HCPCS/CPT and UB-92 revenue code assignments for all items including supplies and pharmaceuticals. The charge master captures the costs of each procedure, service, supply, prescription drug, and diagnostic test provided at the hospital, as well as any fees associated with services, such as equipment fees and room charges

Modern Circumstance: A charge master quizlet (charge description master [CDM]) document that contains a computer-generated list of procedures, services, and supplies with charges for each. Charge master rates are essentially the health care market equivalent of Manufacturer’s Suggested Retail Price (MSRP) in the car buying market. Poor charge master maintenance can lead to overpayments or underpayments. It can also lead to claim rejections from insurance companies, poor patient experience, or compliance violations.

Paradox Examples:

Superbills: An encounter form that is the financial record source document used by healthcare providers and other personnel to record treated diagnoses and services rendered to the patient during the current encounter. It is also called a superbill.

Payment rates: Almost no one actually pays the publicized charge master rates. The vast majority of health care consumers are represented by a payer of some kind, such as a commercial health insurance company, Medicaid, or Medicare. Commercial insurers negotiate the actual prices they pay during the process of contracting with providers. Medicare and Medicaid establish their own payment levels independent of hospitals’ charge master lists – Medicare through the federal government and Medicaid through state governments.

Cash pay: The sad irony of the charge master is that the uninsured are the most likely to be billed charge master rates because they are not represented by a third-party payer.

Problematic features: Other items also impede the ability of payers to have a comprehensive and accurate understanding of hospitals’ financial positions. For example, nonprofit hospitals are required to report charity care, bad debt expenses, community benefit initiatives, and uncompensated care. When these expenses are reported at the charge master level, expenses can be paradoxically overstated, potentially making a hospital’s financial position look worse than it actually is.

Volatility indexes are forward-looking measures of the market’s expectations of volatility (or how much a stock index’s price moves). The CBOE manages and publishes three of the most widely used volatility indexes based on three major stock indexes:

The VIX Index tracks the expected 30-day future volatility of the S&P 500 Index.

The VXN Index tracks the expected 30-day future volatility of the NASDAQ-100 Index.

The VXD Index tracks the expected 30-day future volatility of the Dow Jones Industrial Average Index.

Classic Definition: A doctor announces to her hospitalized patient that there will be a painful medical test sometime during the following week. The patient begins to speculate about when it might occur, until another patient announces that there is no reason to worry because a medical surprise test is impossible.

The test cannot be given on Friday, because by the end of the day on Thursday we would know that the test must be given the next day. Nor can the test be given on Thursday, because, given that we know that the test cannot be given on Friday, by the end of the day on Wednesday we would know that the test must be given the next day. And likewise for Wednesday, Tuesday, and Monday!

Modern Circumstance: The patient spends a restful weekend not worrying about the test, yet is very surprised when it is given on Wednesday. How could this happen?

Paradox Example: There are various versions of this paradox; one of them, called the Hangman, concerns a condemned prisoner who is clever but ultimately overconfident. The implications of the paradox are as yet unclear, and there is virtually no agreement about how it should be solved.

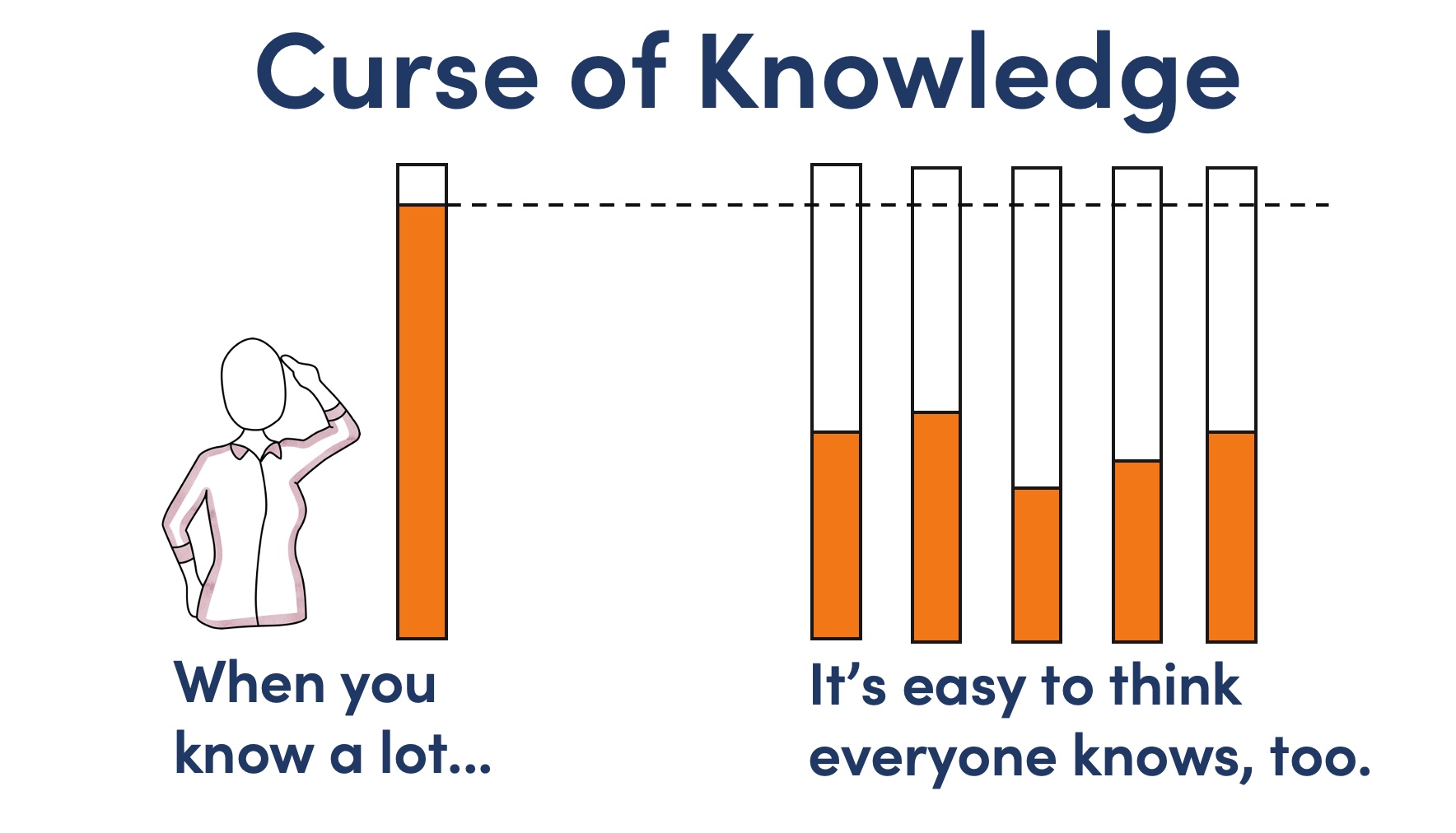

Similar in ways to the availability heuristic (Tversky & Kahneman, 1974) and to some extent, the false consensus effect, once you (truly) understand a new piece of information, that piece of information is now available to you and often becomes seemingly obvious. It might be easy to forget that there was ever a time you didn’t know this information and so, you assume that others, like yourself, also know this information: the curse of knowledge.

However, according to colleague Dan Ariely PhD, it is often an unfair assumption that others share the same knowledge. The hindsight bias is similar to the curse of knowledge in that once we have information about an event, it then seems obvious that it was going to happen all along.

I should have seen it [divorce, stock market crash/soar my smoking & lung cancer, unemployment, etc] coming!

The Physicians Foundation conducted a survey on physician practice patterns and perspectives a few years ago. Here are some key findings from the report:

• 31% of physicians identify as independent practice owners or partners. • Almost half (47%) of physicians plan to change career paths. • 78% of physicians sometimes, often or always experience feelings of burnout. • Nearly a quarter of physician time is spent on non-clinical paperwork.

Classic Definition: Employers write checks that cover most health insurance premiums for employees and their dependents. But as the late Princeton health economist Uwe Reinhardt PhD once explained, employer-sponsored insurance is like a pickpocket taking money out of your wallet at a bar and buying you a drink. You appreciate the cocktail until you realize you paid for it yourself.

Modern Circumstance: With health coverage, employers write the check to the insurer, but employees bear the cost of the premium — the entire premium, not just the portion listed as their contribution on their pay stub. The premium money that goes to the insurance company is cash that employers would otherwise deposit in employees’ accounts like the rest of their salary.

Paradox Example: The fallacy paradox is in thinking an employer’s contribution comes out of profits. In fact, higher health insurance premiums mean lower wages for workers. Since 1999, health insurance premiums have increased 147 percent and employer profits have increased 148 percent. But in that time, average wages have hardly moved, increasing just 7 percent. Clearly workers’ wages, not corporate profits, have been paying for higher health insurance premiums. Health care costs are one — though not the only — reason wages have stagnated over the last few decades. With health insurance costs rising faster than growth in the economy, more labor costs go to benefits like health insurance and less to take-home pay. Yet the paradox that employees don’t pay for their own health insurance is widespread:

The first reason is that individuals cannot be sure what causes their wages to change or remain stagnant for decades.

The second reason is that employers want Americans to believe that they pay for their workers’ health insurance.

The third reason is that there are those who profit from the employment-based system: drug companies, device manufacturers, specialty physicians and high-income individuals.

And so, they all want you to believe companies are being magnanimous in giving you insurance, but they are not!

Investors waited for the Magnificent 7 stock reports to begin rolling last evening. The NASDAQ rose to a new high on optimism while the Dow Jones fell, and the S&P 500 split the difference.

Alphabet announced earnings after the bell yesterday, Microsoft and MetaPlatforms reveal their latest quarters today, Amazon and Apple on Thursday afternoon.

The 10-year Treasury yield hit a 4-month high this afternoon before paring back a bit as traders struggle to find a signal in all the market noise.

Oil rebounded a bit from yesterday’s terrible day, though it still ended the trading session lower.

Ever tried making a decision when you’re angry or excited? According to colleague Dan Ariely PhD, that’s a hot state – when emotions run high and logic takes a backseat. It’s like trying to think clearly in the middle of a storm.

Be you a doctor, CPA, attorney, engineer, husband, wife, parent, teacher or all others. In a hot state, we’re impulsive, making choices we might regret later. It’s why cooling off before making big decisions is always a good idea.

So, when your emotions are boiling over, take a step back, breathe, and wait for the storm to pass. You’ll make better choices when you’re in a calm, cool state.

Posted on October 30, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Trump Media & Technology Group rocketed higher at the opening bell, prompting the Nasdaq to halt trading on what has quickly become the meme stock du jour. Shares ended the day 8.76% higher.

23andMe clawed 1.86% higher after introducing three new board members about a month after the entire board resigned.

VF Corp, parent company of clothing brands JanSport, Vans, and North Face, surged 27.01% thanks to an impeccable earnings report that revealed its turnaround plans are coming to fruition.

Trex, the stuff your dad built an awesome deck out of, saw sales fall last quarter but still managed to beat earnings expectations. Shares popped 6.19%.

STOCKS DOWN

JetBlue Airways sank 17.08% in spite of reporting a smaller loss than analysts expected. The problem is all the turbulence that lies ahead.

D.R. Horton is the largest homebuilder by market cap, so when it says that 2025 will be a bad year, investors should listen. Shares dropped 7.29% on the news.

Crocs stumbled 19.17% after beating earnings but announcing that its fiscal year would be bogged down by poor sales of its HeyDude shoe brand.

Stanley Black & Decker fell 8.77% after missing on both profits and sales, citing weaker consumer spending.

Xerox plummeted 17.41% after the company that can’t make a printer that works for longer than 3 months without needing a new ink cartridge announced weaker sales than expected.

The S&P 500® index (SPX) rose 9.40(0.16%) to 5,832.92; the Dow Jones Industrial Average® ($DJI) fell 154.52 points (–0.36%) to 42,233.05; and the $COMP added points 145.55 (0.78%) to 18,712.75.

The 10-year Treasury note yield (TNX) finished unchanged at 4.27% after reaching nearly 4.34% earlier today.

It is a multi-factor model measures the overall risk associated with a security relative to the market. And, it incorporates over 40 data metrics, including earnings growth, share turnover and senior debt rating.

Russell 1000® Growth Index: Measures the performance of those Russell 1000 Index companies (the 1,000 largest publicly traded U.S. companies, based on total market capitalization) with higher price-to-book ratios and higher forecasted growth values.

Russell 1000® Index: A market-capitalization weighted, large-cap index created by Frank Russell Company to measure the performance of the 1,000 largest publicly traded U.S. companies, based on total market capitalization.

Russell 1000® Value Index: Measures the performance of those Russell 1000 Index companies (the 1,000 largest publicly traded U.S. companies, based on total market capitalization) with lower price-to-book ratios and lower forecasted growth values.

Russell 2000® Growth Index: Measures the performance of those Russell 2000 Index companies (the 2,000 smallest of the 3,000 largest publicly traded U.S. companies, based on total market capitalization) with higher price-to-book ratios and higher forecasted growth values.

Russell 2000® Index: Market-capitalization weighted index created by Frank Russell Company to measure the performance of the 2,000 smallest of the 3,000 largest publicly traded U.S. companies, based on total market capitalization.

Russell 2000® Value Index: Measures the performance of those Russell 2000 Index companies (the 2,000 smallest of the 3,000 largest publicly traded U.S. companies, based on total market capitalization) with lower price-to-book ratios and lower forecasted growth values.

Russell 2500™ Growth Index: Measures the performance of those Russell 2500 Index companies (the 2,500 smallest of the 3,000 largest publicly traded U.S. companies, based on total market capitalization) with higher price-to-book ratios and higher forecasted growth values.

Russell 2500™ Index: A market-capitalization weighted index created by Frank Russell Company to measure the performance of the 2,500 smallest of the 3,000 largest publicly traded U.S. companies, based on total market capitalization.

Russell 2500™ Value Index: Measures the performance of those Russell 2500 Index companies (the 2,500 smallest of the 3,000 largest publicly traded U.S. companies, based on total market capitalization) with lower price-to-book ratios and lower forecasted growth values.

Russell 3000® Growth Index: Measures the performance of the broad growth segment of the U.S. equity universe. It includes those Russell 3000 companies with higher price-to-book ratios and higher forecasted growth values.

Russell 3000® Index: Measures the performance of the largest 3,000 U.S. companies representing approximately 98% of the investable U.S. equity market.

Russell 3000® Utilities Index: A sub-index of the Russell 3000 Index, is a capitalization weighted index of companies in industries heavily affected by government regulation, including among others, basic public service providers (electricity, gas and water), telecommunication services, and oil and gas companies.

Russell 3000® Value Index: Measures the performance of the broad value segment of the U.S. equity universe. It includes those Russell 3000 companies with lower price-to-book ratios and lower forecasted growth values.

Russell Midcap® Growth Index: Measures the performance of those Russell Midcap Index companies (the 800 smallest of the 1,000 largest publicly traded U.S. companies, based on total market capitalization) with higher price-to-book ratios and higher forecasted growth values.

Russell Midcap® Index: Measures the performance of the 800 smallest of the 1,000 largest publicly traded U.S. companies, based on total market capitalization.

Russell Midcap® Value Index: Measures the performance of those Russell Midcap Index companies (the 800 smallest of the 1,000 largest publicly traded U.S. companies, based on total market capitalization) with lower price-to-book ratios and lower forecasted growth values.

Russell Top 200® Index: Measures the performance of the 200 largest securities of the 3,000 publicly traded U.S. companies in the Russell 3000® Index, based on total market capitalization. It is not an investment product available for purchase.

Posted on October 29, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Healthcare’s future as HSBC Innovation Banking collaborated with LINUS and HLTH to help prepare the healthcare ecosystem for the future. The Health 2035 report goes in depth with discussions between visionaries in the ecosystem and studies of young physicians’ forecasts for what the state of care will be in the year 2035. Download the report.

Trump Media & Technology Group soared 21.59% following a major rally at Madison Square Garden, an appearance on Joe Rogan’s podcast, and rising chances of winning the election. Fun fact: After this latest stock surge, Trump Media is now worth almost as much as social media network X.

Nio surged 10.46% thanks to an upgrade from Macquerie, whose analysts believe that the EV startup could see strong growth from new vehicle launches next year.

Spotify has earned a spot on Wells Fargo’s top pick playlist, with analysts confident the stock could rise over 20%. Shares rose 1.27%.

Lower oil prices hurt energy stock, but are a big boost for companies that spend a lot on fuel. CarnivalCorp rose 4.83%, RoyalCaribbeanCruises climbed 1.35%, and AmericanAirlines popped 3.42%.

Stocks Down

Philips floundered 15.95% after the Dutch consumer goods manufacturer missed on earnings and lowered its full-year forecast.

Boeing continued to fall yet another 2.79%, this time on the news that it is raising $19 billion through a stock offering in the hopes that it fends off a credit rating downgrade.

Oil stocks took a beating thanks to a big decline for crude prices. DiamondbackEnergy fell 3.36%, APACorp. dropped 4.51%, ExxonMobil sank 0.49%, and BP lost 1.48%.

The S&P 500® index (SPX)rose15.40points (0.27%) to 5,823.52; the Dow Jones Industrial Average® ($DJI) added 273.17 points (0.65%) to 42,387.57; and the NASDAQ Composite® ($COMP) gained 48.58 points (0.26%) to 18,567.19.

The 10-year Treasury note yield (TNX) climbed six basis points to 4.29%, the highest close since July 9.

Posted on October 28, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Peak earnings season: Five of the Magnificent SevenStocks will be among the 181 companies reporting their earnings this week. Alphabet is in the Mag Seven lead-off spot on Tuesday, Microsoft and Meta step to the plate on Wednesday, and Apple and Amazon rounding out the lineup and this baseball metaphor on Thursday. These companies account for almost 25% of the S&P 500, which is up 40% over the past year and not far off its record closing number from earlier this month. But, the approaching election, it could be a volatile week in the stock markets.

***

Markets: Stocks are currently driving the narrative on Wall Street. Last week, bonds sold off in a big way (driving yields to their highest level since July) in a sign investors are dialing back expectations of more aggressive rate cuts from the Federal Reserve.

Stocks nevertheless handled the bond volatility with aplomb, and with help from Tesla’s 22% one-day rise, the NASDAQ is sitting within 2% of its record high.

Posted on October 27, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Vitaliy Katenselson CFA

***

***

Today, we’re diving into two thought-provoking questions:

1. What’s a famous investment rule I don’t agree with? 2. Which key characteristics should a good investor have?

1. A Famous Investment Rule I Don’t Agree With: “Buy and Hold”

Buy and hold becomes a religion during bull markets. Then, holding a stock because you bought it is often rewarded through higher and higher valuations. There’s a Pavlovian bull market reinforcement – every time you don’t sell (hold) a stock, it goes higher.

Buying is a decision. So is holding, but it should not be a religion but a decision. The value of any company is the present value of its cash flows. When the present value of cash flows (per share) is less than the price of the stock, the stock should not be “held” but sold.

WarrenBuffett is looked upon as the deity of buy and hold.

Look at Coca Cola when it hit $40 in 1999. Its earnings power at the time was about $0.80. It was trading at 50 times earnings. It was significantly overvalued, considering that most of the growth for this company was in the past.

Fast-forward almost a quarter of a century – literally a generation. Today the stock is at $60. It took more than a decade to reclaim its 1999 high. Today, Coke’s earnings power is around $1.50–1.90. Earnings have stagnated for over a decade. If you did not sell the stock in 1999, you collected some dividends, not a lot but some. The stock is still trading at 30–40x earnings. Unless they discover that Coke cures diabetes (not causes it), its earnings will not move much. It’s a mature business with significant health headwinds against it.

“Long-term” and “buy-and-hold” investing are often confused.

People should not own stocks unless they have a long-term time horizon. Long-term investing is an attitude, an analytical approach. When you build a discounted cash flow model, you are looking decades ahead. However, this doesn’t mean that you should stop analyzing the company’s valuation and fundamentals after you buy the stock, as they may change and affect your expected return. After you put in a lot of analytical work and buy the stock, you should not simply switch off your brain and become a mindless buy-and-hold investor.

This doesn’t mean you shouldn’t be patient, which I’ll discuss next; but holding, not selling, a stock is a decision.

2. Key Characteristics of a Good Investor

I’m going to sound a bit more preachy than usual, but it’s very difficult to answer this question in any other way.

You need three Ps – passion, patience, process.

Passion

Investing is not a 9-to-5 job; it’s a 24/7 adventure. Unlike flipping burgers or processing insurance claims, where you can clock in at 9 AM, fall into a stupor, and then reawaken at 5 PM when you clock out.

This should be your test: If you catch yourself treating investing as a 9-to-5 job, then you have little passion for it.

If this is the case, don’t do it (this probably applies to any choice of a profession). You don’t stand a chance against people for whom investing is a never-ending puzzle to be solved on their life’s journey. All of my investment friends are dripping with passion for investing; they are obsessed with it. None of them are in it only for the money.

You won’t last long in this profession if you’re not passionate about stocks. Patience

Investing is like real life – the connection between effort and result is nonlinear. It is very loose.

You may be making all of the right rational decisions: You are buying stocks that lie within your EQ/IQ spectrum, and they are significantly undervalued, but the market simply doesn’t care. It just keeps sending your stocks down. To make things even more frustrating, while your stocks are declining, speculators who treat the stock market as a craps table at Caesars Palace are killing it, making money hand over fist. It’s painful. It is excruciatingly painful if you have the wrong client base.

This is where patience comes in. My father told me this story, which happened right before I was born.

My family lived in Murmansk, a city 125 miles north of the Arctic Circle in northwest Russia. My mom went to give birth to my brothers and me in Saratov, a city in central Russia, about 1200 miles from Murmansk. She wanted to be closer to her parents. My father could not leave work, so he stayed in Murmansk.

A few weeks before I was born, he went to visit his best friend, Alexander. He told him that he was worried about my mom and the birth. His friend told him something that I remember to this day (with a chuckle): “Naum, you did your part; you cannot go back and correct what you did. Now you just have to wait.”

Investing is patience punctuated by decisions.

As the French mathematician Blaise Pascal said, “All of humanity’s problems stem from man’s inability to sit quietly in a room alone.”

One more thought here: I try to take the temperature of my emotions and the mental activity of my brain. When I find myself overheating, with the stock market occupying my entire brain, I forcibly disconnect and unplug myself from it. The quality of my thoughts and decisions when my brain is overheating is likely to be low. So, I go for a walk in the park, read a fiction book, go see a movie, or visit an art museum. Process

Managing someone else’s money is an incredible responsibility, which you may not fully appreciate during bull markets. But sideways and bear markets will remind you quickly.

I don’t want to over-glorify what we do – we are not curing cancer or saving people from burning buildings. But IMA clients entrust us with their life savings and tell me, “Vitaliy, please don’t screw it up.”

My decisions may determine whether our clients get to retire, pay for their medical expenses, or help their kids buy houses.

Staying rational when the world around you is melting up with greed or melting down in fear isn’t a capacity that one accidentally stumbles upon. You engineer it through a series of small, repeatable decisions – your investment process.

A young clinician representative advising to consider the cost versus value of medicine. Health care concept for economic cost-effectiveness analysis, driving down medical costs, improved access.

***

Value Based CareClassic Definition: Value-based care is a type of payment model that pays doctors and hospitals for treating patients in the right place, at the right time and with just the right amount of care. You can look at it as a financial incentive to motivate healthcare providers to meet specific performance measures related to the quality and efficiency of the process. The same way, it penalizes weaker experiences, such as medical errors. The concept is often counter-intuitive.

Modern Circumstance: As healthcare costs continue to rise, value-based care has been growing in popularity compared to the traditional fee-for-service method.

Think: HMOs, PPOs, capitation payments and Medicare Advantage [Part C].

Paradox Examples:

Payment: A physician paid through fee-for-service compensation might like to see a packed medical office waiting room. More patients and services equate to higher pay. But, the same doctor paid through a VBC contract might wish to see an emptier waiting room as s/he will get the exact same daily pay for seeing fewer patients and working much less.

Prospectivity: Traditional Fee-for-Service medicine treats sick patients. VBC medicine seeks to keep patients healthy and out of the doctor’s office.

Although some might view a budget as unnecessarily restrictive, sticking to a spending plan can be a useful tool in enhancing the wealth of a medical practice. So, I will emphasize keys to smart budgeting and how to track spending and savings in these tough economic times.

There is an aphorism that suggests, “Money cannot buy happiness.” Well, this may be true enough but there is also a corollary that states, “Having a little sure reduces the unhappiness.”

Unfortunately, today there is more than a little financial unhappiness in all medical specialties. The challenges range from the commoditization of medicine, aging demographics, Medicare reimbursement cutbacks and increased competition to floundering equity markets, the home mortgage crisis, the squeeze on credit and declines in the value of a practice. Few doctors seem immune to this “perfect storm” of economic woes.

Far too many physicians are hurting and it is not limited to above-average earning professionals. However, one can strive to reduce the pain by following some basic budgeting principles. By adhering to these principles, physicians can eliminate the “too many days at the end of the month” syndrome and instead develop a foundation for building real wealth and security, even in difficult economic climates like we face today.

There are three major budget types. A flexible budget is an expenditure cap that adjusts for changes in the volume of expense items. A fixed budget does not. Advancing to the next level of rigor, a zero-based budget starts with essential expenses and adds items until the money is gone. Regardless of type, budgets can be extremely effective if one uses them at home or the office in order to spot money troubles before they develop.

For the purpose of wealth building, doctors may think of this budget as a quantitative expression of an action plan. It is an integral part of the overall cost-control process for the individual, his or her family unit or one’s medical practice.

Preparing a net income statement (lifestyle cash flow budget) is often difficult because many doctors perceive it as punitive. Most doctors do not live a disciplined spending lifestyle and they view a budget as a compromise to it. However, a cash flow budget is designed to provide comfort when there is surplus income that can be diverted for other future needs. For example, if you treat retirement savings as just another periodic bill, you are more likely to save for it.

You may construct a personal cash budget by recording each cash receipt and cash disbursement on a spreadsheet. Only the date, amount and a brief description of the transaction are necessary. The cash budget is a simple tool that even doctors who lack accounting acumen can use. Since it is possible to track the cash-in and cash-out in the same format used for a standard check register, most doctors find that the process takes very little time. Such a budget will provide a helpful look at how well you are staying within available resources for a given period.

We then continue with an analysis of your operating checkbook and a review of various source documents such as one’s tax return, credit card statements, pay stubs and insurance policies. A typical statement will show all cash transactions that occur within one year. It is helpful to establish a monthly equivalent to all items of income and expense. For the purposes of getting started, note items of income and expense by the frequency you are accustomed to receiving or spending them.

What You Should Know About The ‘Action Plan’ Cash Budget

For a medical office, the first operations budget item might be salary for the doctor and staff. Operating assets and other big ticket items come next. Some of our doctors/clients review their office P&L statements monthly, line by line, in an effort to reduce expenses. Then they add back those discretionary business expenses they have some control over.

Now, do you still run out of money before the end of the month? If so, you had better cut back on entertainment, eating dinner out or that fancy, new but unproven piece of medical equipment. This sounds draconian until you remind yourself that your choice is either: live frugally later or live a simpler lifestyle now and invest the difference.

As a young doctor, it may be a difficult trade-off. By mid-life, however, you are staring retirement in the face. That is why the action plan depends on your actions concerning monetary scarcity, a plan that one can implement and measure using simple benchmarks or budgeting ratios. By using these statistics, perhaps on an annual basis, the doctor can spot problems, correct them and continue planning actively toward stated goals like building long-term wealth.

Useful Calculations To Assess Your Budgeting Success

In the past, generic budgeting ratios would emphasize not spending more than 15 to 20 percent of your net salary on food or 8 percent on medical care. Now these estimates have given way to more rigorous numbers. Personal budget ratios, much like medical practice financial ratios, represent comparable benchmarks for parameters such as debt, income growth and net worth. Although these ratios are still broad, the following represent some useful personal budgeting ratios for physicians.

• Basic liquidity ratio = liquid assets / average monthly expenses. Cash-on-hand should approach 12 to 24 months or more in the case of a doctor employed by a financially insecure HMO or fragile medical group practice. Yes, chances are you have heard of the standard notion of setting enough cash aside to cover three months in a rainy day scenario. However, we have decried this older laymen standard for many years in our textbooks, white papers and speaking engagements as being wholly insufficient for the competitively unstable environment of modern healthcare.

• Debt to assets ratio = total debt / total assets. This percentage is high initially but should decrease with age as the doctor approaches a debt-free existence

• Debt to gross income ratio = annual debt repayments / annual gross income. This represents the adequacy of current income for existing debt repayments. Doctors should try to keep this below 20 to 25 percent.

• Debt service ratio = annual debt repayment / annual take-home pay. Physicians should aim to keep this ratio below 25 to 30 percent or face difficulty paying down debt.

• Investment assets to net worth ratio = investment assets / net worth. This budget ratio should increase over time as retirement approaches.

• Savings to income ratio = savings / annual income. This ratio should also increase over time as one retires major obligations like medical school debt, a practice loan or a home mortgage.

• Real growth ratio = (income this year – income last year) / (income last year – inflation rate). This budget ratio should grow faster than the core rate of inflation.

• Growth of net worth ratio = (net worth this year – net worth last year) / net worth last year – inflation rate). Again, this budgeting ratio should stay ahead of inflation.

In other words, these ratios will help answer the question: “How am I doing?”

Pearls For Sticking To A Budget

Far from the burden that most doctors consider it to be, budgeting in one form or another is probably one of the greatest tools for building wealth. However, it is also one of the greatest weaknesses among physicians who tend to live a certain lifestyle.

In fact, we have found that less than one in 10 medical professionals have a personal budget. Fear, or a lack of knowledge, is a major cause of procrastination. Fortunately, the following guidelines assist in reversing this microeconomic disaster.

1. Set reasonable goals and estimate annual income. Do not keep large amounts of cash at home or office. Deposit it in an FDIC insured money-market account for safety. Do not deposit it in a money market mutual fund with net asset value (NAV) that may “break the buck” and fall below the one-dollar level. Track actual bills and expenses.

2. Do not pay bills early, do not have more taxes withheld from your salary than needed and develop spending estimates to pay fixed expenses first. Fixed expenses are usually contractual and usually include housing, utilities, food, Social Security, medical, debt repayments, homeowner’s or renter’s insurance, auto, life and disability insurance, etc. Reduce fixed expenses when possible. Ultimately, all expenses get paid and become variable in the long run.

3. Make it a priority to reduce variable expenses. Variable expenses are not contractual and may include clothing, education, recreational, travel, vacation, gas, cable TV, entertainment, gifts, furnishings, savings, investments, etc. Trim variable expenses by 5 to 20 percent.

4. Use “carve-outs or “set-asides” for big ticket items and differentiate true wants from frivolous needs.

5. Calculate both income and expenses as a percentage of your total budget. Determine if there is a better way to allocate resources. Review the budget on a monthly basis to notice any variance. Determine if the variance was avoidable, unavoidable or a result of inaccurate assumptions. Take corrective action as needed.

6. Know the difference between saving and investing. Savers tend to be risk adverse while investors understand risk and take steps to mitigate it. Watch mutual fund commissions and investment advisory fees, which cut into return-rates. Keep investments simple and diversified (stocks, bonds, cash, index, no-load mutual and exchange traded funds, etc.).

Sooner or later, despite the best of budgeting intentions, something will go awry. A doctor will be terminated or may be the victim of a reduction-in-force (RIF) because of cost containment initiatives.4 A medical practice partnership may dissolve or a local hospital or surgery center may close, hurting your practice and livelihood. Someone may file a malpractice lawsuit against you, a working spouse may be laid off or you may get divorced. Regardless of the cause, budgeting crisis management encompasses two different perspectives: awareness and execution.

First, if you become aware that you may lose your job, the following proactive steps will be helpful to your budget and overall financial condition.

• Decrease retirement contributions to the required minimum for company/practice match. • Place retirement contribution differences in an after-tax emergency fund. • Eliminate unnecessary payroll deductions and deposit the difference to cash. • Replace group term life insurance with personal term or universal life insurance. • Take your old group term life insurance policy with you if possible. • Establish a home equity line of credit to verify employment. • Borrow against your pension plan only as a last resort.

If you have lost your job or your salary has been depressed, negotiate your departure and get an attorney if you believe you lost your position through breach of contract or discrimination. Then execute the following steps to recalculate your budget and boost your wealth rebuilding activities.

• Prioritize fixed monthly bills in the following order: rent or mortgage; car payments; utility bills; minimum credit card payments; and restructured long-term debt.

• Consider liquidating assets to pay off debts in this order: emergency fund, checking accounts, investment accounts or assets held in your children’s names.

• Review insurance coverage and increase deductibles on homeowner’s and automobile insurance for needed cash.

• Then sell appreciated stocks or mutual funds; personal valuables such as furnishings, jewelry and real estate; and finally, assets not in pension or annuities if necessary.

• Keep or rollover any lump sum pension or savings plan distribution directly to a similar savings plan at your new employer, if possible, when you get rehired.

• Apply for unemployment insurance.

• Review your medical insurance and COBRA coverage after a “qualifying event” such as job loss, firing or even after quitting. It is a bit expensive due to a 2 percent administrative fee surcharge but this may be well worth it for those with preexisting conditions or who are otherwise difficult to insure. One may continue COBRA for up to 18 months.

• Consider a high deductible Health Savings Account (HSA), which allows tax-deferred dollars like a medical IRA, for a variety of costs not normally covered under traditional heath insurance plans. Self-employed doctors deduct both the cost of the premiums and the amount contributed to the HSA. Unused funds roll over until the age of 59½, when one can use the money as a supplemental retirement benefit.

• Eliminate unnecessary variable, charitable and/or discretionary expenses, and become very frugal.

Final Notes

The behavioral psychologist, Gene Schmuckler, PhD, MBA, sometimes asks exasperated doctors to recall the story of the old man who spent a day watching his physician son treating HMO patients in the office. The doctor had been working at his usual feverish pace all morning. Although he was working hard, he bitterly complained to his dad that he was not making as much money as he used to make. Finally, the old man interrupted him and said, “Son, why don’t you just treat the sick patients?” The doctor-son looked at his father with an annoyed expression and responded, “Dad, can’t you see, I do not have time to treat just the sick ones.”

Always remember to add a bit of emotional sanity into your budgeting and economic endeavors.

Regardless of one’s age or lifestyle, the insightful doctor realizes that it is never too late to take control of a lost financial destiny through prudent wealth building activities. Personal and practice budgeting is always a good way to start the journey.

NOTE: Dr. Marcinko is a former Certified Financial Planner and current Certified Medical Planner™. He has been a medical management advisor for more than a decade. He is the CEO of http://www.MarcinkoAssociates.com

The authors acknowledge the assistance of Mackenzie H. Marcinko PhD in the preparation of this article.

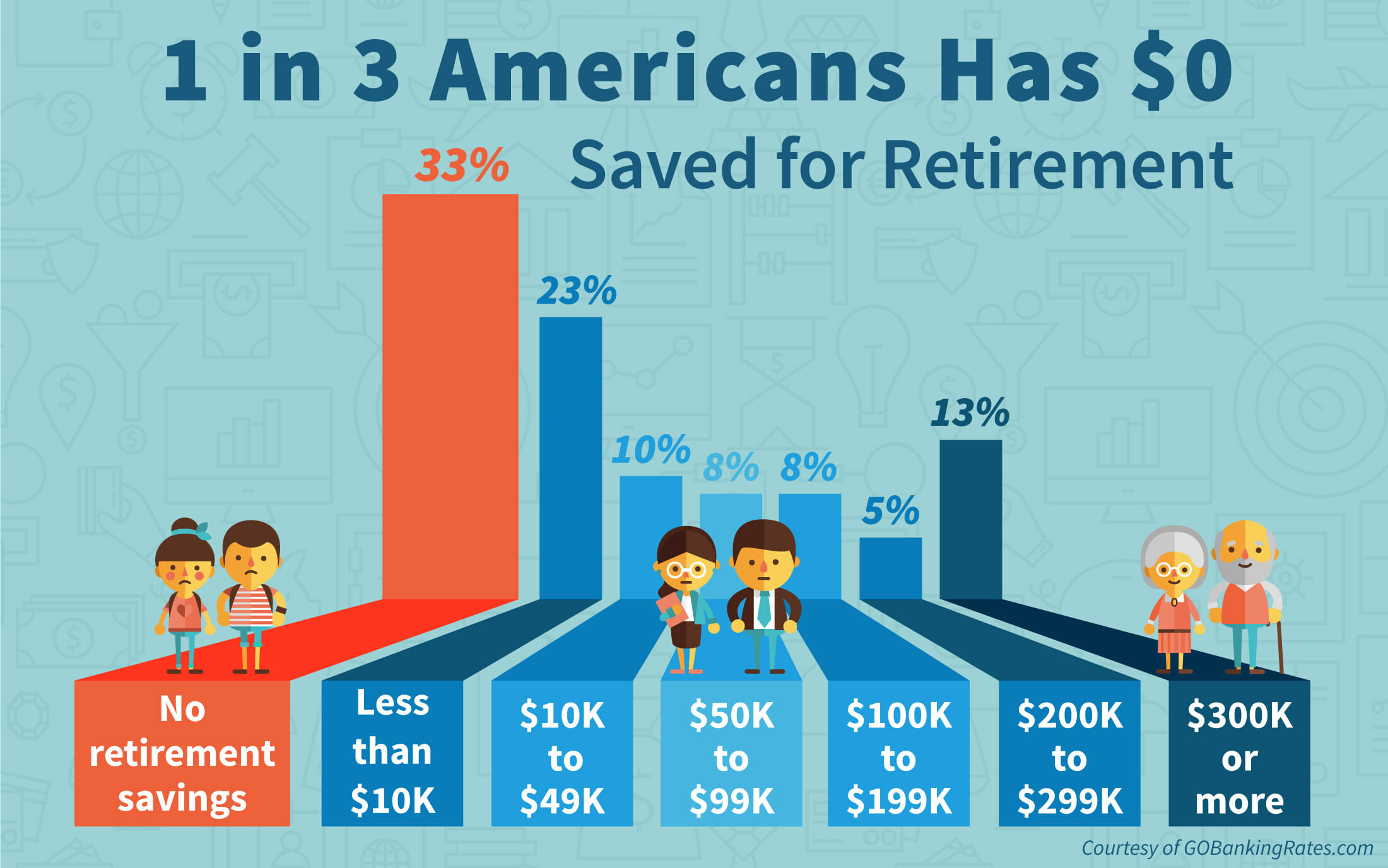

According to the National Institute on Retirement Security, almost 40 million households have no retirement savings at all. The Employee Benefit Research Institute (EBRI) estimates in its 2019 Retirement Security Projection Model that America’s current retirement savings deficit is $3.8 trillion.

What does that mean? Well, the EBRI report aggregates the savings deficit of all U.S. households headed by someone between the ages of 35 and 64, inclusive. In total, those households have $3.8 trillion fewer dollars in savings than they should have for retirement.

For more recent data, Fidelity Investments reported that in the third quarter of 2022 the average account balance for an IRA was $101,900. Employees with a 401(k) averaged $97,200, while those with a 403(b) had $87,400.

Fidelity also estimated that “an average retired couple age 65 in 2022 may need approximately $315,000 saved (after tax) to cover health care expenses in retirement.” Keeping in mind that more Americans are also living longer than ever before, they will face more challenges to cover medical expenses in retirement.

Posted on October 18, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Chip stocks recovered lost ground today thanks to a strong earnings report from TSMC (more on that below). Nvidia led the group higher, rising 0.89% to yet another new all-time high.

Blackstone rose 6.30% to a new record high after the world’s largest alternative asset manager reported an excellent quarter.

Expedia popped 4.75% after a report by the Financial Times revealed that Uber had explored an acquisition of the travel site. Expedia shareholders cheered the news, while Uber shares sank 2.45%.

Stocks Down

Robinhood fell 2.27% after announcing its new Legend trading platform geared specifically toward advanced traders.

Lucid Group plummeted 17.99% on the news that the EV automaker is offering over 262 million shares of its common stock in an attempt to raise funds.

CSX dropped 6.71% after missing both top- and bottom-line estimates last quarter thanks in no small part to hurricanes Helene and Milton.

Health insurance stocks took a beating today due to a not-great earnings report from ElevanceHealth (more on that below, too). Centene Corp. fell 9.09%, while Molina Healthcare tumbled 12.55%.

The S&P 500® index (SPX) slipped 1.00point (–0.02%) to 5,841.47; the $DJI added 161.35 points (0.37%) to 43,239.05; and the NASDAQ Composite®($COMP) rose 6.53 points (0.04%) to 18,373.61.

The 10-year Treasury note yield (TNX) climbed eight basis points to 4.1%.

The CBOE Volatility Index® (VIX) sank to 18.97 by late Thursday, a two-week low.

The average amount owed on “upside down” auto loans, in which the balance is more than the car is worth, hit a record high of $6,458 in the third quarter, according to Edmunds, a site that helps consumers research and buy cars

Financial planning as a concept has been around for a long time, but not as we know it today. When Loren Dunton set up the Society for Financial Counseling Ethics in 1969, or when the first graduating class of the College of Financial Planning graduated in 1973, financial planning was very different. It was centered around selling limited partnerships, which came to end with the Tax Reform Act of 1986.

However, financial planning re-emerged — all thanks to Richard Averitt III. The certified financial planner gave new meaning to financial planning, this time with a focus on who the client is and what their needs are. This approach was purely methodological in nature.

Soon after, financial planning picked up again. According to the Certified Financial Planner (C.F.P.) Board of Standards in Denver, today, there are more than 94,000 C.F.P.s worldwide, including over 48,000 in the U.S. Additionally, there are also organizations that have been set up for C.F.P.s, such as the Financial Planning Association (FPA), which has approximately 22,000 members.

And, don’t forget the emerging Certified Medical Planner™ professional fiduciary designation for physicians, dentists, nurses and allied healthcare clients.

Financial planning, as we know it now, includes investing, tax planning, retirement planning, and basically other ways to get your finances in order and create mindful budgets to ensure a safe and secure future. Getting a step ahead of your spending and finances is beneficial in the long run and Financial Planning Month in October is the perfect time to do that.

Posted on October 17, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Goldman Sachs’ profit jumped 45% in monster quarter. The investment bank made $3 billion of profit on revenue of nearly $13 billion in Q3, it reported yesterday, surpassing even the rosiest of expectations. Bloomberg reported that it was the best quarter ever for Goldman’s stock trading unit, putting the group on track for a record year.

Walgreenssaid it will close 1,200 US stores, about one in seven locations, by 2027. The retailer will shutter 500 stores by the end of next year.

Trump Media & Technology Group has had a wild week, falling nearly 10% yesterday before trading of the stock was halted, then popping 15.52% today. Election hype, a Trump-sponsored cryptocurrency, and Truth+, a new streaming service, are keeping shareholders on their toes.

Abbott Laboratories rose 1.53% thanks to a stronger-than-expected earnings report powered by the company’s impressive medical device sales.

Aspen Aerogels makes insulating material for batteries, which sounds boring to everyone but the Department of Energy. The DOE signed a conditional commitment to loan the company up to $670 million, sending shares 13.24% higher.

DOWN STOCKS

Novavax plummeted 19.44% after the FDA put a hold on the pharma company’s flu and Covid vaccine combination.

Interactive Brokers enjoyed higher revenue and more trading from its user base last quarter, but earnings per share came in under expectations, and shares sank 4.05%.

The SPX rose27.21points (0.47%) to 5,842.47; the Dow Jones Industrial Average® ($DJI) added 337.28 points (0.79%) to 43,077.70; and the NASDAQ Composite®($COMP) increased 51.49 points (0.28%) to 18.367.08.

The 10-year Treasury note yield (TNX) fell two basis points to just below 4.02%, the lowest close since October 4.

The CBOE Volatility Index® (VIX) dropped moderately to 19.58, still elevated considering stock market strength.

Posted on October 16, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Maximum lifespans. The upper limit of human life expectancy is leveling out, according to a new study published in the journal Nature Aging. Back in 1990, life-extending tech and health measures were increasing the average global lifespan by about 2.5 years per decade, but that dropped to 1.5 years per decade in the 2010s and closer to zero in the US, where there are more drug overdoses, shootings, and medical care inequities.

Sphere Entertainment popped 6.33% on the news that a second Sphere will be built in Abu Dhabi. London was originally supposed to be the location of a second venue, but they’ve already got the Eye, and didn’t need more circular tourist attractions.

Oklo, a Sam Altman-backed nuclear energy startup, rose another 16.04% on the news that Google will purchase nuclear power to turbocharge its AI infrastructure.

Charles Schwab climbed 6.10% after the bank announced a top and bottom line beat last quarter, as well as higher revenue projections for the full fiscal year.

Boeing somehow gained 2.26% after announcing it is raising $35 billion to support its struggling finances as the machinist union strike enters its second month.

Wolfspeed, which sounds like a super power in a YA novel, soared 21.27% on the news that the US government will provide the chipmaker with up to $750 million in government grants.

STOCKS DOWN

Semiconductor stocks got a double whammy in the last 48 hours. First, Bloomberg revealed that US officials are considering limiting the sale of AI chips outside the country. Then, ASMLmissed its Q3 sales estimates (more on that below). Nvidia shares slid 4.52%, AMD fell 5.22%, and Intel dropped 3.33%.

Citigroup beat earnings estimates this quarter, but shareholders punished the bank for setting aside more money in case of higher loan losses ahead. Shares dropped 5.11%.

Coty, parent company of numerous beauty brands like CoverGirl, fell 10.74% to a new 52-week low after it warned of a sales slowdown in the coming quarters.

Enphase Energy tumbled 9.29% after RBC analysts downgraded the solar power stock, citing growing competition from the likes of Tesla as well as slowing demand for solar batteries.

Speaking of energy, oil stocks plummeted on news of Israel’s targeting of Iranian military assets rather than crude production facilities. ExxonMobil fell 3.01%, Chevron dropped 2.67%, and ValeroEnergy sank 4.62%.

Here’s where the major benchmarks ended yesterday:

The S&P 500® index (SPX) fell 44.59 points (–0.76%) to 5,815.26; the Dow Jones Industrial Average® ($DJI) dropped 324.80 points (–0.75%) to 42,740.42; and the NASDAQ Composite®($COMP) lost 187.09 points (–1.01%) to 18,315.59.

The 10-year Treasury note yield (TNX) fell three basis points to 4.04%, the lowest close in a week.

The CBOE Volatility Index® (VIX) climbed to 20.72, an elevated level.

Millions of seniors will lose access to their Medicare Advantage plans after major insurer cuts in the aftermath of the Inflation Reduction Act. Experts spoke with Newsweek about what’s going on and what steps seniors can take to get the coverage they need.

Posted on October 15, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters &The Medicare Team

Medicare open enrollment—which runs from October 15th through December 7th this year—is your chance to check in on your Medicare plan and, if needed, change it.

***

***

Mark your calendars — Medicare Open Enrollment starts October 15th! Did you know new benefits are coming to Medicare drug coverage next year?

Also starting next year, you can choose to participate in a program that spreads your out-of-pocket drug costs across the calendar year, instead of paying all at once at the pharmacy. It’s called the Medicare Prescription Payment Plan — and you can opt in with your plan throughout the 2025 plan year. Contact your plan for more details.

Remember, Medicare plans can change from one year to the next, and so can your health needs. Preview and compare all your health and drug options and see if you can save!

It’s been a while since you’ve connected with us. Are you still interested in emerging financial planning, investing, medical practice management and health information technology insights from the Institute ofMedical Business, Advisors, Inc?

If so, please email us if you want to continue receiving daily updates about cutting-edge news and trends or if you’d like to be removed from our e-mailing list.

Your own related posts, comments and personal referrals are appreciated as well.

Thank You Dr. David Edward Marcinko MBA MEd CMP Editor-in-Chief MarcinkoAdvisors@msn.com

The ME-P constantly publishes new and unique content for the medical business management, health economics, HIT and financial planning, advisory and services community, and is always interested in accepting submissions from guest authors.

Because this blog is intended specifically for all medical professionals, business consultants and financial advisors, guest post content should pertain directly to the issues and challenges faced by all constituents and/or provide advanced education on a technical topic pertinent to practitioners.

Accordingly, we typically accepts guest posts from fellow physicians, financial planning [CFP, CMP, RIA, etc] and/or medical management practitioners, or consultants [JD, CPA, MBA, PhD, DBA, etc] or vendors who work directly with doctors/nurses on a full-time basis and have the requisite specialized knowledge and expertise for medical professional [non-clinical] needs and concerns.

Posted on August 1, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

Reach Industry Pros, Executives and Decision-Makers with Ease

By Ann Miller RN MHA [Executive-Director]

MarcinkoAdvisors@msn.com

The Medical Executive Post [ME-P] is the premier online community and marketing platform that allows you to profile your company’s product and services to financial advisors, stock brokers, insurance agents, financial planners, accountants, wealth-managers and their highly-targeted healthcare professional clients.

Highlight your company’s news, events, white papers, videos and contact information – all in one place – and update your information 24/7.

And, because we’ll promote your resources to the entire ME-P eco-space, it’s a highly efficient way to fortify your existing marketing programs with the critical decision makers you’re trying to reach.

Reader loyalty. Not only does the ME-P receive a mind-boggling number of page views and visits each month, its readers are loyal.

Reader stature. ME-P readers are experienced industry pros, executives and decision-makers.

Selective advertising. The ME-P is a free read that’s off the radar of the big-ad companies. Your ad here stands out as personal and different.

Supporting the ME-P makes a big difference and costs only a fraction of other online publications with far fewer readers.

Cost. CPM is ridiculously low compared to other sites.

E-mail us for a full packet, but give a look to these results from the ME-P’s annual reader survey:

89% of readers said the ME-P influences their perception of products and companies

34% said that ME-P sponsorship alone give them a higher interest or appreciation for those companies

754% said the ME-P has some, a good bit, or a lot of industry influence

Contact us and I’ll e-mail you a rate card. Your support makes a difference!

Text Ads

We have great sponsor packages, but maybe you want to run a short-term ad — a position listing, an announcement, or your booth number at an upcoming conference. Or, perhaps your company is between budget cycles and can’t commit to sponsorship yet. We’ve got an answer – ME-P text ads.

Text ads are up to five lines long and are highly cost-effective. You’ll get about 25-35,000 impressions per week, reaching the ME-P’s highly targeted and loyal audience of decision-makers. Think small text ads don’t work? They’ve made two Google kids billionaires!

PayPal Certified

All ME-P text ad costs are for one month, payable in advance online via PayPal. We’ll post it quickly and you’ll see results almost immediately.

Assessment

Why waste money on magazines that never get read and with months of lead time required? The best way to quickly reach the critical mass of the healthcare and financial services industry is right here on the ME-P.

So, advertise with the Medical Executive-Post and Reap the Benefits

Posted on April 6, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Ann Miller RN MHA

[Manager Editor]

MarcinkoAdvisors@msn.com

About iMBA Inc’s Next-Gen Advisors

[FREE Initial Review & RFP Consultation]

***

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about career, business, IT, practice, policy, personal financial planning and wealth building.

We have an attitude that’s fiercely independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial.

And, our new wave editors “got fly”, just like U.

Read it! Write it! Post it! “Medical Executive-Post”.

So, call or email for your FREE initial consultation with RFP review, TODAY.

The Institute of Medical Business Advisors, Inc provides a team of experienced, senior level consultants led by iMBA Chief Executive Officer Dr. David Edward Marcinko MBA CMP™ MBBS [Hon] and President Hope Rachel Hetico RN MHA CMP™ to provide going contact with our clients throughout all phases of each project, with most of the communications between iMBA and the key client participants flowing through this Senior Team. iMBA Inc., and its skilled staff of certified professionals have many years of significant experience, enjoy a national reputation in the healthcare consulting field, and are supported by an unsurpassed research and support staff of CPAs, MBAs, MPHs, PhDs, CMPs™, CFPs® and JDs to maintain a thorough and extensive knowledge of the healthcare environment. The iMBA team approach emphasizes providing superior service in a timely, cost-effective manner to our clients by working together to focus on identifying and presenting solutions for our clients’ unique, individual needs.

The iMBA Inc project team’s exclusive focus on the healthcare industry provides a unique advantage for our clients. Over the years, our industry specialization has allowed iMBA to maintain instantaneous access to a comprehensive collection of healthcare industry-focused data comprised of both historically-significant resources as well as the most recent information available. iMBA Inc’s specific, in-depth knowledge and understanding of the “value drivers” in various healthcare markets, in addition to the transaction marketplace for healthcare entities, will provide you with a level of confidence unsurpassed in the public health, health economics, management, administration, and financial planning and consulting fields.

iMBA Inc’s information resources and network of healthcare industry textbook resources enhanced by our professional consultants and research staff, ensure that the iMBA project team will maintain the highest level of knowledge regarding the current and future trends of the specific specialty market related to the project, as well as the healthcare industry overall, which serves as the “foundation” for each of our client engagements.

Happy Holidays from the Institute of Medical Business Advisors, Inc

At this special time of year, we give thanks for our clients and our employees, as well as all essential workers in hospitals, health centers and medical practices across the country.

May the holiday spirit be with you and your family throughout the season and everyday We look forward to serving you in 2024.

Posted on March 31, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Ann Miller RN MHA

***

***

Facebook’s latest release, Meta, is said to be the next evolution of social connection. A virtual, 3D network that allows connection and collaboration in ways many of us have never even considered! And while many are buzzing over how Meta will shape everything from education to healthcare – we are eager to get your opinion on our own ME-P ecosystem. Can patients trust Facebook and others again?

Are you interested in exploring a new platform for connection?

Have you subscribed to the ME-P?

We want to hear all about it! We’re actively collaborating to bring your perspectives to the discussion around the Metaverse and the patient, economics, finance and healthcare community.

If you have insights or experiences to share – just comment and/or let us know.

Thank you for your interest in sponsoring the Medical Executive-Post, the web’s only site integrating medical practice management with personal financial planning for all health care and financial services professionals.

Why should your company sponsor an ad, text message or banner on the ME-P?

Reader loyalty. Not only does the ME-P receive a mind-boggling number of page views and visits each month, its readers are loyal.

Reader stature. ME-P readers are experienced industry pros, executives and decision-makers.

Selective advertising. The ME-P is a free read that’s off the radar of the big-ad companies. Your ad here stands out as personal and different.

Supporting the ME-P makes a big difference and costs only a fraction of other online publications with far fewer readers.

Cost. CPM is ridiculously low compared to other sites.

E-mail us for a full packet, but give a look to these results from the ME-P’s annual reader survey:

89% of readers said the ME-P influences their perception of products and companies

34% said that ME-P sponsorship alone give them a higher interest or appreciation for those companies

75% said the ME-P has some, a good bit, or a lot of industry influence.

Contact me and I’ll e-mail you a rate card. Your support makes a difference!

Text Ads

We have great sponsor packages, but maybe you want to run a short-term ad — a position listing, an announcement, or your booth number at an upcoming conference. Or, perhaps your company is between budget cycles and can’t commit to sponsorship yet. We’ve got an answer – ME-P text ads.

Text ads are up to five lines long and are highly cost-effective. You’ll get about 25-35,000 impressions per week, reaching the ME-P’s highly targeted and loyal audience of healthcare professionals and financial services decision-makers. Think small text ads don’t work? They’ve made two Google kids billionaires!

PayPal Certified

All ME-P text ad costs are for one month, payable in advance via PayPal. We’ll post it quickly and you’ll see results almost immediately.

Assessment

Why waste money on magazines that never get read and with months of lead time required? The best way to quickly reach the critical mass of the healthcare management and financial services industry is right here on the ME-P.

Speaker: David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

Our Other Print Books and Related Information Sources:

Subscribe Now: Did you like this Medical Executive-Post, or find it helpful, interesting and informative? Want to get the latest ME-Ps delivered to your email box each morning? Just subscribe using the link below. You can unsubscribe at any time. Security is assured.

Posted on November 30, 2019 by Dr. David Edward Marcinko MBA MEd CMP™

Please Support Us

Dear Medical Executive-Post Reader,

With Thanksgiving 2019 upon us and the end of the year just ahead, we hope the ME-P can count on your support to continue providing innovative news, comments and expert insights for the integrated industries and interests we serve.

A Blessing?

But, why do we think you should count ME-P among this year’s blessings?

As always, it’s because of the impact of our work.

Examples:

For example, just last week we saw that impact on healthcare insurance reform from the ACA’s presidential election – to tax planning for doctors from our accountants and financial advisors – to behavioral economics, investing, retirement and estate planning – to eMRs and health information technology – and to the scheduling of more topic channels and many exciting new medical practice management and enhancement features and functions for the coming New Year 2016.

Much of this would not have been created and disseminated without the Medical Executive-Post.

Oh; and let’s not forget our career and unique job alerts, too! This is where the ME-P makes a real difference.

The Road Ahead for 2020

Looking ahead, the hubbub of campaigning has fallen silent (at least for a few days) as our focus turns to health policy, financial leadership and governing — and to the need to hold accountable all doctors and patients, financial advisors and clients, and those we have just elected.

In short, the ME-P constituency!

Giving

So, please take a moment over the holiday ahead to donate. We can have real impact, but it takes money, and we need your help.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements.

Subscribe: MEDICAL EXECUTIVE POST for curated news, essays, opinions and analysis from the public health, economics, finance, marketing, IT, business and policy management ecosystem.

Posted on July 24, 2015 by Dr. David Edward Marcinko MBA MEd CMP™

Our Searchable, and Ranking, Knowledge Portal

By Ann Miller RN MHA

[Executive Director]

We’ve collected all of our best research, solution information, and social buzz to create the Medical Executive-Post Portal and new virtual, and real, library.

From the new ME-P Portal, you can search, sort, and filter through our information archives to quickly find what you’re looking for—or feel free to browse and explore a variety of topics when you have a few minutes to spare.

From subject-specific original, or curated, blog posts and researched-based white papers, to solution overviews, e-Briefs, infographics, dictionaries, CD-ROMs, handbooks, major textbooks and more; you’ll find the answers to your healthcare economics, administration, financial planning and medical practice management and business questions here.

And explore a library of answers to your complex healthcare business decisions

Learn more – to earn more

Even better, our web-based platform serves up the content you want most in your preferred format. Choose a user-friendly text-file, web-based flip book, e-file, or download, save, and print a PDF – or order a soft back or hard cover book – it’s your choice.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES: