BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

A capital call is a notice sent to investors requesting that they contribute additional capital to a private equity fund. Capital calls are made when the fund manager has identified a new investment opportunity that requires additional funds.

Investors must be prepared to respond to capital calls with the required funds in a timely manner, as failure to do so could result in penalties or even the loss of their investment.

Carried Interest: Understanding the Concept

Carried interest is a form of incentive fee paid to private equity fund managers. This fee is calculated as a percentage of the profits generated by the fund’s investments.

Carried interest is often criticized as a tax loophole, as it is treated as capital gains, which are taxed at a lower rate than ordinary income.

Deal Flow: What it Means for Investors

Deal flow refers to the number of potential investment opportunities that a private equity firm evaluates. A robust deal flow is important for private equity firms, as it provides a pipeline of potential investments to consider.

Investors may want to investigate a private equity firm’s deal flow as part of their due diligence process, as a strong deal flow can indicate the firm has a good track record of finding attractive investment opportunities.

Due Diligence: A Key Step in Private Equity Investing

Due diligence is the process of evaluating a potential investment opportunity to assess its viability. This process involves a thorough investigation of the company’s financials, operations, and management team.

Due diligence is a critical step in the private equity investment process, as it helps to identify potential risks associated with an investment opportunity. Investors who skip due diligence do so at their own risk.

Exit Strategy: How Private Equity Firms Make Money

Exit strategy refers to the plan that private equity firms have in place to cash out of their investments. Private equity firms typically exit investments through an initial public offering (IPO), a sale to another company, or a management buyout.

Exit strategy is critical to the private equity investment process, as it is how investors ultimately make returns on their investments.

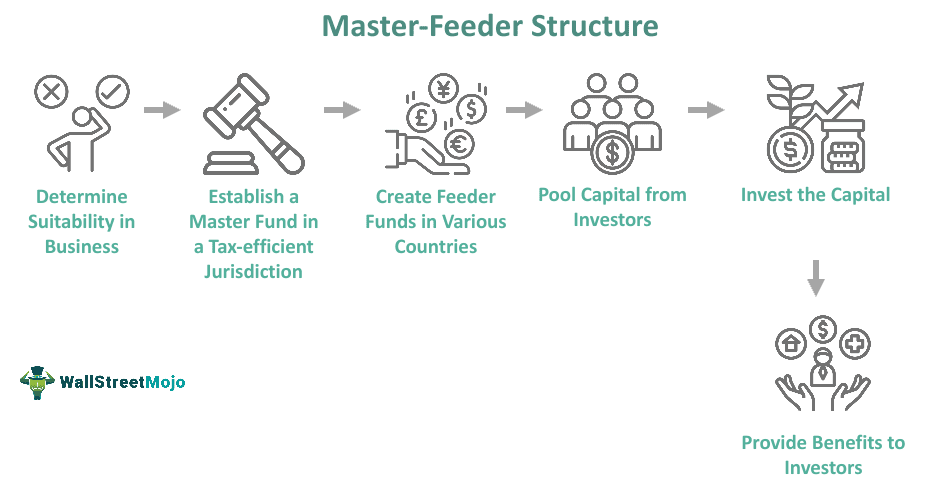

Fund of Funds: An Overview

A fund of funds is a type of investment fund that invests in other investment funds. In the private equity space, fund of funds typically invest in a portfolio of private equity funds.

Fund of funds can be a good way for investors to gain exposure to a wider range of private equity investments with less risk than investing in individual funds.

General Partner vs Limited Partner: What’s the Difference?

The general partner is the party responsible for managing the private equity fund and making investment decisions. Limited partners, on the other hand, are typically passive investors who provide capital but have little involvement in the investment process.

The distinction between general partners and limited partners is important for investors to understand, as it can impact their level of involvement in the investment process.

Investment Horizon: A Crucial Factor in Private Equity Investments

Investment horizon refers to the length of time an investor plans to hold an investment. In the private equity space, investment horizons can be several years or even a decade.

Investment horizon is a critical factor for investors to consider, as it impacts the level of liquidity they will have and the returns they can expect to make on their investment.

Leveraged Buyout (LBO): Definition and Examples

A leveraged buyout is a type of acquisition where the acquiring company uses a significant amount of debt to finance the purchase. The idea is that the acquired company’s assets will be used as collateral to secure the debt.

Leveraged buyouts can be an effective way for private equity firms to acquire companies with minimal capital investment. However, the use of leverage also increases the risk associated with these types of acquisitions.

Management Fee vs Performance Fee: Understanding the Two

The management fee is the fee paid to the general partner for managing the private equity fund. The performance fee, or carried interest, is paid based on the fund’s performance and returns generated for investors.

The distinction between management fees and performance fees is important for investors to understand, as it affects the level of fees they will be responsible for paying.

Pitchbook: A Guide to Creating an Effective Pitchbook

A pitchbook is a presentation used by private equity firms to pitch their investment strategy to potential investors. An effective pitchbook should be clear, well-organized, and provide a compelling rationale for why investors should consider investing in the fund.

Investors reviewing a fund’s pitchbook should look for evidence of a well-thought-out investment strategy and a track record of successful investments.

Private Placement Memorandum (PPM): What it is and Why It Matters

A private placement memorandum is a legal document provided to potential investors that details the terms of the private equity fund. It includes information on the fund’s investment strategy, expected returns, fees, and risks associated with the investment.

Reviewing a fund’s private placement memorandum is a critical step in the due diligence process, as it provides investors with a comprehensive understanding of the investment opportunity.

Recapitalization: A Strategy for Restructuring a Company

Recapitalization is a strategy used by private equity firms to restructure a company’s capital structure. This can involve issuing debt to pay off equity holders or issuing equity to pay off debt holders.

Recapitalization is often used to improve a company’s financial position and increase its value, making it a key tool in the private equity arsenal.

Valuation Techniques Used in Private Equity Investing

Valuation techniques are used to determine the value of a private company. These techniques can include discounted cash flow analysis, market multiples analysis, and asset-based valuation.

Understanding valuation techniques is important for investors, as it allows them to evaluate the relative value of investment opportunities and make informed investment decisions.

A concept of tax fairness that states that people with different amounts of wealth or different amounts of income should pay tax at different rates. Wealth includes assets such as houses, cars, stocks, bonds, and savings accounts. Income includes wages, interest and dividends, and other payments.

A business authorized by the IRS to participate in the IRS e-file Program. The business may be a sole proprietorship, a partnership, a corporation, or an organization. Authorized IRS e-file Providers include Electronic Return Originators (EROs), Transmitters, Intermediate Service Providers, and Software Developers. These categories are not mutually exclusive. For example, an ERO can at the same time, be a Transmitter, a Software Developer, or an Intermediate Service Provider, depending on the function being performed.

Assuming all other dependency tests are met, the citizen or resident test allows taxpayers to claim a dependency exemption for persons who are U.S. citizens for some part of the year or who live in the United States, Canada, or Mexico for some part of the year.

Amount that taxpayers can claim for a “qualifying child” or “qualifying relative”. Each exemption reduces the income subject to tax. The exemption amount is a set amount that changes from year to year. One exemption is allowed for each qualifying child or qualifying relative claimed as a dependent.

This allows tax refunds to be deposited directly to the taxpayer’s bank account. Direct Deposit is a fast, simple, safe, secure way to get a tax refund. The taxpayer must have an established checking or savings account to qualify for Direct Deposit. A bank or financial institution will supply the required account and routing transit numbers to the taxpayer for Direct Deposit.

The transmission of tax information directly to the IRS using telephones or computers. Electronic filing options include (1) Online self-prepared using a personal computer and tax preparation software, or (2) using a tax professional. Electronic filing may take place at the taxpayer’s home, a volunteer site, the library, a financial institution, the workplace, malls and stores, or a tax professional’s place of business.

Electronic preparation means that tax preparation software and computers are used to complete tax returns. Electronic tax preparation helps to reduce errors.

The Authorized IRS e-file Provider that originates the electronic submission of an income tax return to the IRS. EROs may originate the electronic submission of income tax returns they either prepared or collected from taxpayers. Some EROs charge a fee for submitting returns electronically.

Free from withholding of federal income tax. A person must meet certain income, tax liability, and dependency criteria. This does not exempt a person from other kinds of tax withholding, such as the Social Security tax.

Amount that taxpayers can claim for themselves, their spouses, and eligible dependents. There are two types of exemptions-personal and dependency. Each exemption reduces the income subject to tax. While each is worth the same amount, different rules apply to each.

A program sponsored by the IRS in partnership with participating states that allows taxpayers to file federal and state income tax returns electronically at the same time.

The federal government levies a tax on personal income. The federal income tax provides for national programs such as defense, foreign affairs, law enforcement, and interest on the national debt.

Provides benefits for retired workers and their dependents as well as for disabled workers and their dependents. Also known as the Social Security tax.

To mail or otherwise transmit to an IRS service center the taxpayer’s information, in specified format, about income and tax liability. This information-the return-can be filed on paper, electronically (e-file).

Determines the rate at which income is taxed. The five filing statuses are: single, married filing a joint return, married filing a separate return, head of household, and qualifying widow(er) with dependent child.

Spending and income records and items to keep for tax purposes, including paycheck stubs, statements of interest or dividends earned, and records of gifts, tips, and bonuses. Spending records include canceled checks, cash register receipts, credit card statements, and rent receipts.

A foster child is any child placed with a taxpayer by an authorized placement agency or by court order. Eligible foster children may be claimed by taxpayers for tax benefits.

Money, goods, services, and property a person receives that must be reported on a tax return. Includes unemployment compensation and certain scholarships. It does not include welfare benefits and nontaxable Social Security benefits.

You must meet the following requirements: 1. You are unmarried or considered unmarried on the last day of the year. 2. You paid more than half the cost of keeping up a home for the year. 3. A qualifying person lived with you in the home for more than half the year (except temporary absences, such as school). However, a dependent parent does not have to live with the taxpayer.

Taxes on income, both earned (salaries, wages, tips, commissions) and unearned (interest, dividends). Income taxes can be levied on both individuals (personal income taxes) and businesses (business and corporate income taxes).

Performs services for others. The recipients of the services do not control the means or methods the independent contractor uses to accomplish the work. The recipients do control the results of the work; they decide whether the work is acceptable. Independent contractors are self-employed.

A person who represents the concerns or special interests of a particular group or organization in meetings with lawmakers. Lobbyists work to persuade lawmakers to change laws in the group’s favor.

An economic system based on private enterprise that rests upon three basic freedoms: freedom of the consumer to choose among competing products and services, freedom of the producer to start or expand a business, and freedom of the worker to choose a job and employer.

You are married and both you and your spouse agree to file a joint return. (On a joint return, you report your combined income and deduct your combined allowable expenses.)

You must be married. This method may benefit you if you want to be responsible only for your own tax or if this method results in less tax than a joint return. If you and your spouse do not agree to file a joint return, you may have to use this filing status.

Used to provide medical benefits for certain individuals when they reach age 65. Workers, retired workers, and the spouses of workers and retired workers are eligible to receive Medicare benefits upon reaching age 65.

When the amount of a credit is greater than the tax owed, taxpayers can only reduce their tax to zero; they cannot receive a “refund” for any excess nonrefundable credit.

Allow taxpayers to “sign” their tax returns electronically. The PIN, a five-digit self-selected number, ensures that electronically submitted tax returns are authentic. Most taxpayers can qualify to use a PIN.

Taxes on property, especially real estate, but also can be on boats, automobiles (often paid along with license fees), recreational vehicles, and business inventories.

Benefits that cannot be withheld from those who don’t pay for them, and benefits that may be “consumed” by one person without reducing the amount of the product available for others. Examples include national defense, streetlights, and roads and highways. Public services include welfare programs, law enforcement, and monitoring and regulating trade and the economy.

To be a qualifying child, the dependent must meet eight tests: (1) relationship, (2) age, (3) residence, (4) support, (5) citizenship or residency, (6) joint return, (7) qualifying child of more than one person, and (8) dependent taxpayer.

There are tests that must be met to be a qualifying relative, they are: (1) not a qualifying child, (2) member of household or relationship, (3) citizenship or residency, (4) gross income, (5) support, (6) joint return, and (7) dependent taxpayer.

If your spouse died in 2010, you can use married filing jointly as your filing status for 2010 if you otherwise qualify to use that status. The year of death is the last year for which you can file jointly with your deceased spouse. You may be eligible to use qualifying widow(er) with dependent child as your filing status for two years following the year of death of your spouse. For example, if your spouse died in 2010, and you have not remarried, you may be able to use this filing status for 2011 and 2012. This filing status entitles you to use joint return tax rates and the highest standard deduction amount (if you do not itemize deductions). This status does not entitle you to file a joint return.

Compensation received by an employee for services performed. A salary is a fixed sum paid for a specific period of time worked, such as weekly or monthly.

Similar to Social Security and Medicare taxes. The self-employment tax rate is 15.3 percent of self-employment profit. The self-employment tax is calculated on Schedule SE—Self-Employment Tax. The self-employment tax is reported on Form 1040, U.S. Individual Income Tax Return.

If on the last day of the year, you are unmarried or legally separated from your spouse under a divorce or separate maintenance decree and you do not qualify for another filing status.

Provides benefits for retired workers and their dependents as well as for the disabled and their dependents. Also known as the Federal Insurance Contributions Act (FICA) tax.

Develops software for the purposes of (1) formatting electronic tax return information according to IRS specifications, and/or (2) transmitting electronic tax return information directly to the IRS.

For dependency test purposes, support includes food, clothing, shelter, education, medical and dental care, recreation, and transportation. It also includes welfare, food stamps, and housing provided by the state. Support includes all income, taxable and nontaxable.

Interest income that is not subject to income tax. Tax-exempt interest income is earned from bonds issued by states, cities, or counties and the District of Columbia.

The amount of tax that must be paid. Taxpayers meet (or pay) their federal income tax liability through withholding, estimated tax payments, and payments made with the tax forms they file with the government.

Money and goods received for services performed by food servers, baggage handlers, hairdressers, and others. Tips go beyond the stated amount of the bill and are given voluntarily.

Taxes on economic transactions, such as the sale of goods and services. These can be based on a set of percentages of the sales value (ad valorem-sales taxes), or they can be a set amount on physical quantities (“per unit”-gasoline taxes).

The concept that people in different income groups should pay different rates of taxes or different percentages of their incomes as taxes. “Unequals should be taxed unequally.”

A system of compliance that relies on individual citizens to report their income freely and voluntarily, calculate their tax liability correctly, and file a tax return on time.

This provides free income tax return preparation for certain taxpayers. The VITA program assists taxpayers who have limited or moderate incomes, have limited English skills, or are elderly or disabled. Many VITA sites offer electronic preparation and transmission of income tax returns.

Compensation received by employees for services performed. Usually, wages are computed by multiplying an hourly pay rate by the number of hours worked.

Money, for example, that employers withhold from employees paychecks. This money is deposited for the government. (It will be credited against the employees’ tax liability when they file their returns.) Employers withhold money for federal income taxes, Social Security taxes and state and local income taxes in some states and localities.

Telephonic or electronic advice for medical professionals that is:

Objective, affordable, medically focused and personalized

Rendered by a pre-screened financial consultant or medical management advisor

Offered on a pay-as-you-go basis, by phone or secure e-mail transmission

The iMBA Discussion Forum™ is a physician-to-advisor telephone or e-mail portal that connects independent financial professionals and medical management consultants, with doctors or healthcare executives desiring affordable and unbiased financial or business advice on an as-needed, pay-per-use basis.

Medical professionals and healthcare executives can now receive direct access to pre-screened iMBA professionals in the areas of Practice Enhancement, Investing, Financial Planning, Asset Allocation, Portfolio Management Taxes, Insurance, Mortgage and Lending, Practice Management, Information Technology, Human Resources and Employee Benefits. To assist our doctor / healthcare executive members, we can be contracted with per-minute or per-project fees, and contacted by client phone, email or secure instant messaging.

The iMBA Discussion Forum™ is designed to fill a growing need for medically focused financial or managerial advice that traditional consultants have not been able to serve. Most financial “consultants” either charge high sales commissions, or levy a percentage of fees for managing client assets. And, management consultants tend to extend their scope of engagement to tangential areas not originally needed, or wanted.

Typically, financial advisors also require clients to meet minimum asset level thresholds ($500,000 to $750,000, or more), or pay thousands of dollars in consulting fees to receive their services. These fee structures have created inherent conflicts of interest and significant barriers for an increasing number of time-compressed and economically constrained physicians or healthcare executives.

Now, with the iMBA Discussion Forum™, all physicians and executive clients can receive unbiased financial advice, and objective business opinions, on their own terms, anytime-anywhere.

The iMBA Discussion Forum™ eliminates conflicts of interest by providing advice on a per-use basis, so you pay only for what you want and need. iMBA does not sell financial or business products. The result is a unique “no pressure”, and “no conflicts-of-interest experience.”

Get started with your consultation, now! Receive only the advice you need and pay for, from a medically focused and qualified doctor-advisor looking after your best interests.

Contact Us Now! How the iMBA Discussion Forum Works:

Contact Us

Request an iMBA Discussion Forum™ Conference Schedule

Pre-Pay a Small Retainer of $1,500

Receive Scheduled Advice via Conference Call or email transmission

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

New stock market indices are frequently created to track emerging sectors, regional markets, or particular investment strategies. However, some of the recent and notable stock market indices introduced in recent years focus on new trends or themes such as technology, sustainability, and ESG (Environmental, Social, and Governance) factors. Here are a few noteworthy examples:

1. S&P 500 ESG Index (2021)

One of the newer and increasingly popular indices is the S&P 500 ESG Index, launched in 2021. This index tracks the performance of the companies within the S&P 500 that meet certain environmental, social, and governance (ESG) criteria. The S&P 500 ESG Index aims to provide a more sustainable and socially responsible alternative to the traditional S&P 500 index. It excludes companies involved in industries like tobacco, firearms, or fossil fuels, reflecting the growing interest in socially responsible investing.

2. Nasdaq-100 ESG Index (2021)

Another significant ESG-focused index is the Nasdaq-100 ESG Index, also introduced in 2021. This index tracks the Nasdaq-100, which is typically made up of the 100 largest non-financial companies listed on the Nasdaq stock exchange, but it filters those companies to include only those with strong ESG scores. Given the rapid growth of ESG investing, indices like this one are becoming increasingly important for socially-conscious investors.

3. Global X Metaverse ETF Index (2022)

The Global X Metaverse ETF Index, introduced in 2022, is another example of a new market index targeting a specific, emerging sector. This index focuses on companies involved in the development of the metaverse, which encompasses technologies like virtual reality (VR), augmented reality (AR), and other digital experiences. As the concept of the metaverse gains popularity, this index is designed to provide investors with exposure to companies working within this new virtual space.

4. FTSE All-World High Dividend Yield ESG Index (2022)

This is an example of a more niche index, combining high-dividend yield investing with ESG factors. Introduced by FTSE Russell in 2022, this index is designed for investors looking for companies with high dividend yields while also considering sustainability and ethical investment criteria. It is part of a broader trend where investors seek to combine solid financial returns with socially responsible practices.

5. Bitcoin and Digital Assets Indices

As cryptocurrency continues to grow in prominence, more indices focused on digital assets and cryptocurrency have emerged. For instance, the S&P Bitcoin Index and the Nasdaq Crypto Index were created to provide benchmarks for the growing market of cryptocurrencies and blockchain technology companies. These indices help investors track the performance of digital currencies and crypto-related stocks or funds.

Why Are New Indices Created?

New stock market indices are created for several reasons:

Emerging Market Trends: As new sectors like the metaverse, AI, and ESG investing become more relevant, indices are developed to capture the performance of these new areas.

Investor Demand: As investors look for more targeted strategies, whether for ethical investing or to gain exposure to emerging technologies, indices are created to meet those demands.

Financial Innovation: As financial products like ETFs (Exchange-Traded Funds) gain popularity, they require benchmarks or indices to track performance.

Conclusion

While the S&P 500 ESG Index and Nasdaq-100 ESG Index are among the newest mainstream indices focusing on socially responsible investing, there are also many other niche indices targeting rapidly growing sectors like the metaverse, cryptocurrencies, and digital assets. These indices reflect the evolving nature of global markets and the increasing interest in themes such as sustainability and technological innovation. With such rapid change in the financial landscape, it’s likely that even more specialized indices will continue to emerge in the coming years.

Did you know that desperate doctors of all ages are turning to knowledgeable financial advisors and medical management consultants for help? Symbiotically too, generalist advisors are finding that the mutual need for knowledge and extreme niche synergy is obvious.

***

***

But, there was no established curriculum or educational program; no corpus of knowledge or codifying terms-of-art; no academic gravitas or fiduciary accountability; and certainly no identifying professional designation that demonstrated integrated subject matter expertise for the increasingly unique healthcare focused financial advisory niche … Until Now!

So, if you are looking to supplement your knowledge, income and designations; and find other qualified professionals you may want to consider the CMP® program.

Enter the Certified Medical Planner™ charter professional designation. And, CMPs™ are FIDUCIARIES, 24/7.

Channel Surfing the ME-P

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

***

***

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

The Origins and Current Status of Cryptocurrency: A 2025 Perspective

Introduction

Cryptocurrency has evolved from a niche technological experiment into a global financial force. In just over a decade, it has disrupted traditional banking, inspired new economic models, and sparked debates about the future of money. As of 2025, cryptocurrencies are not only investment assets but also tools for innovation, decentralization, and financial inclusion. This essay explores the origins of cryptocurrency, its evolution, and its current status in the global economy.

Origins of Cryptocurrency

The Pre-Bitcoin Era

Before Bitcoin, digital currency was a theoretical concept explored by cryptographers and computer scientists. In the 1980s, David Chaum introduced DigiCash, an early form of electronic money that prioritized privacy. Though innovative, DigiCash failed commercially due to lack of adoption and centralization.

Other attempts, like Hashcash and B-money, laid the groundwork for decentralized systems but never materialized into functioning currencies. These efforts, however, contributed key ideas that would later be incorporated into Bitcoin.

In 2008, an anonymous figure (or group) known as Satoshi Nakamoto published the Bitcoin white paper: “Bitcoin: A Peer-to-Peer Electronic Cash System.” This document proposed a decentralized currency that used blockchain technology to validate transactions without a central authority.

Bitcoin officially launched in January 2009 with the mining of the genesis block. Early adopters were cryptographers, libertarians, and tech enthusiasts. The first real-world Bitcoin transaction occurred in 2010 when Laszlo Hanyecz paid 10,000 BTC for two pizzas — now commemorated as Bitcoin Pizza Day.

Bitcoin’s design solved the double-spending problem and introduced a transparent, immutable ledger. Its supply was capped at 21 million coins, making it deflationary by design.

Evolution and Expansion

Rise of Altcoins

Bitcoin’s success inspired the creation of alternative cryptocurrencies, or “altcoins.” Litecoin (2011), Ripple (2012), and Ethereum (2015) introduced new functionalities. Ethereum, in particular, revolutionized the space by enabling smart contracts — self-executing agreements coded directly onto the blockchain.

Smart contracts laid the foundation for decentralized applications (dApps), decentralized finance (DeFi), and non-fungible tokens (NFTs). These innovations expanded crypto’s use cases beyond simple transactions.

ICO Boom and Regulatory Pushback

In 2017, the crypto market experienced a massive bull run fueled by initial coin offerings (ICOs). Startups raised billions by issuing tokens, often without clear business models or regulatory oversight. While some projects succeeded, many failed or turned out to be scams.

Governments responded with crackdowns. The U.S. Securities and Exchange Commission (SEC) began classifying certain tokens as securities, requiring registration and compliance. China banned ICOs and crypto exchanges altogether.

Despite the volatility, the 2017–2018 cycle cemented crypto’s place in mainstream finance and attracted institutional interest.

Cryptocurrency in the 2020s

COVID-19 and the Digital Gold Narrative

The COVID-19 pandemic in 2020 accelerated crypto adoption. As governments printed trillions in stimulus, concerns about inflation grew. Bitcoin was increasingly viewed as “digital gold” — a hedge against fiat currency devaluation.

Major companies like Tesla, MicroStrategy, and Square added Bitcoin to their balance sheets. PayPal and Visa began supporting crypto transactions. The narrative shifted from speculation to legitimacy.

Ethereum and the DeFi Explosion

Ethereum’s ecosystem exploded with the rise of DeFi platforms like Uniswap, Aave, and Compound. These services allowed users to lend, borrow, and trade assets without intermediaries. Total value locked (TVL) in DeFi surpassed $100 billion by 2021.

Ethereum also became the backbone of the NFT boom. Artists, musicians, and creators used NFTs to monetize digital content, leading to record-breaking sales and mainstream attention.

As of 2025, the global cryptocurrency market has added over $600 billion in value year-to-date, with a total market capitalization exceeding $2.5 trillion.

Posted on January 26, 2026 by Dr. David Edward Marcinko MBA MEd CMP™

***

***

By Dr. David Edward Marcinko MBA MEd

***

Milton Friedman: Champion of Free Markets

Milton Friedman was a towering figure in the field of economics, renowned for his unwavering advocacy of free-market capitalism and limited government intervention. Born in 1912 in New York City and raised in Rahway, New Jersey, Friedman rose from modest beginnings to become a Nobel laureate and a leading voice of the Chicago School of Economics.

Friedman’s academic journey began at Rutgers University, where he earned a degree in mathematics and economics. He later pursued graduate studies at the University of Chicago and Columbia University, where he was mentored by prominent economists like Simon Kuznets. His intellectual foundation laid the groundwork for a career that would challenge prevailing economic thought and reshape public policy.

One of Friedman’s most significant contributions was his development of monetarism, a theory emphasizing the role of governments in controlling the money supply to manage inflation and economic stability. In contrast to Keynesian economics, which advocated for active fiscal policy and government spending, Friedman argued that excessive government intervention often led to inefficiencies and inflation. His research demonstrated that inflation is “always and everywhere a monetary phenomenon,” a principle that became central to modern macroeconomic policy.

Friedman’s influence extended beyond academia. His 1962 book, Capitalism and Freedom, articulated a powerful case for economic liberty as a foundation for political freedom. He argued that voluntary exchange and competitive markets were essential for individual choice and prosperity. The book also introduced the Friedman Doctrine, which posited that the primary responsibility of business is to increase its profits, a view that sparked ongoing debates about corporate social responsibility.

In 1976, Friedman was awarded the Nobel Memorial Prize in Economic Sciences for his work on consumption analysis, monetary history, and stabilization policy. His Permanent Income Hypothesis, which suggests that people base their consumption on expected long-term income rather than current income, revolutionized understanding of consumer behavior.

Friedman’s ideas had profound policy implications. He was a vocal critic of the draft and successfully advocated for an all-volunteer military. He also proposed the concept of school vouchers, allowing parents to choose schools for their children, which laid the foundation for modern school choice movements. His work influenced leaders like Ronald Reagan and Margaret Thatcher, who embraced free-market reforms during their administrations.

Despite his acclaim, Friedman’s views were not without controversy. Critics argued that his emphasis on deregulation and privatization sometimes overlooked social equity and environmental concerns. Nonetheless, his legacy remains deeply embedded in economic thought and public discourse.

Milton Friedman passed away in 2006, but his ideas continue to shape debates on economic policy, freedom, and the role of government. His belief in the power of markets and individual choice remains a cornerstone of classical liberalism and a guiding light for economists and policymakers around the world.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Gold has long been regarded as a cornerstone of wealth preservation, and its role within modern investment portfolios continues to attract scholarly attention. As both a tangible asset and a financial instrument, gold embodies characteristics that distinguish it from equities, fixed income securities, and other commodities. Its historical resilience, inflation-hedging capacity, and diversification benefits render it a subject of considerable importance in portfolio construction and risk management.

Historical and Monetary Significance

Gold’s enduring appeal is rooted in its function as a monetary standard and store of value. For centuries, gold underpinned global currency systems, most notably through the gold standard, which provided stability in international trade and monetary policy. Although fiat currencies have supplanted gold in official circulation, its symbolic and practical role as a measure of wealth persists. This historical continuity reinforces investor confidence in gold as a reliable repository of value during periods of economic uncertainty.

Inflation Hedge and Safe-Haven Asset

A substantial body of empirical research demonstrates that gold serves as a hedge against inflation and currency depreciation. When consumer prices rise and fiat currencies weaken, gold tends to appreciate, thereby preserving purchasing power. Moreover, gold’s status as a safe-haven asset is particularly evident during geopolitical crises, financial market turbulence, and systemic shocks. In such contexts, investors reallocate capital toward gold, seeking protection from volatility in traditional asset classes. This defensive quality underscores gold’s utility in stabilizing portfolios during adverse conditions.

Diversification and Risk Management

From the perspective of modern portfolio theory, gold offers diversification benefits due to its low correlation with equities and bonds. Incorporating gold into a portfolio reduces overall variance and enhances risk-adjusted returns. Studies suggest that even modest allocations—typically ranging from 5 to 10 percent—can improve portfolio resilience by mitigating downside risk. This non-correlation is especially valuable in environments characterized by heightened uncertainty, where traditional diversification strategies may prove insufficient.

Investment Vehicles and Accessibility

Gold’s versatility as an investment is reflected in the variety of instruments available to investors. Physical bullion, in the form of coins and bars, provides tangible ownership but entails storage and insurance costs. Exchange-traded funds (ETFs) offer liquidity and ease of access, while mining equities provide leveraged exposure to gold prices, albeit with operational risks. Futures contracts and derivatives enable sophisticated strategies, though they demand expertise and tolerance for volatility. The breadth of these vehicles ensures that gold remains accessible across diverse investor profiles.

Limitations and Critical Considerations

Despite its strengths, gold is not without limitations. Unlike equities or bonds, gold does not generate income, such as dividends or interest. This absence of yield can constrain long-term portfolio growth, particularly in low-inflation environments. Furthermore, gold prices are subject to volatility, influenced by investor sentiment, central bank policies, and global demand dynamics. Overexposure to gold may therefore hinder portfolio performance, underscoring the necessity of balanced allocation.

Conclusion

Gold’s dual identity as a historical store of value and a contemporary financial instrument secures its relevance in portfolio construction. Its inflation-hedging capacity, safe-haven qualities, and diversification benefits justify its inclusion as a strategic asset. Nevertheless, prudent management is essential, given its lack of yield and susceptibility to volatility. Within a scholarly framework of portfolio theory, gold emerges not as a panacea but as a complementary asset, enhancing resilience and stability in the face of evolving economic landscapes.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The contrasting economic philosophies of John Maynard Keynes and Friedrich Hayek have shaped not only macroeconomic policy but also approaches to investing. While both thinkers sought to understand and improve economic systems, their views diverge sharply on the role of government, market behavior, and investor decision-making.

Keynesian economics emphasizes the importance of aggregate demand in driving economic growth. Keynes argued that markets are not always self-correcting and that government intervention is necessary during downturns to stimulate demand. In the context of investing, Keynesian theory supports counter-cyclical strategies. Investors following this approach might increase exposure to equities during recessions, anticipating that fiscal stimulus will boost corporate earnings and market performance. Keynes himself was a successful investor, known for his contrarian style and long-term focus. He advocated for active portfolio management, believing that markets are driven by psychological factors and herd behavior, which create mispricings that savvy investors can exploit.

In contrast, Hayekian economics is rooted in classical liberalism and the belief in spontaneous order. Hayek argued that markets are efficient information processors and that decentralized decision-making leads to better outcomes than centralized planning. From an investment standpoint, Hayekian theory favors passive strategies and minimal interference. Investors aligned with Hayek’s philosophy might prefer index funds or diversified portfolios that reflect market signals rather than attempting to time the market or predict government actions. Hayek was skeptical of the ability of any individual or institution to possess enough knowledge to outsmart the market consistently.

The Keynesian approach tends to be more optimistic about the power of policy to influence markets. For example, during economic crises, Keynesians may expect stimulus packages to revive demand and thus invest in sectors likely to benefit from increased government spending. Hayekians, on the other hand, may view such interventions as distortions that lead to malinvestment and eventual corrections. They might invest more cautiously during periods of heavy government involvement, anticipating inflation, asset bubbles, or regulatory overreach.

Risk perception also differs between the two schools. Keynesians may see risk as cyclical and manageable through diversification and active management. Hayekians view risk as inherent and unpredictable, best mitigated through adherence to market fundamentals and long-term discipline.

In practice, modern investors often blend elements of both approaches. For instance, they may use Keynesian insights to anticipate short-term market movements while relying on Hayekian principles for long-term portfolio construction. The rise of behavioral finance has also added nuance, validating Keynes’s view of irrational market behavior while reinforcing Hayek’s skepticism of centralized forecasting.

Ultimately, the choice between Keynesian and Hayekian investing reflects deeper beliefs about how economies function and how much control investors—or governments—really have. Keynesians embrace adaptability and intervention, while Hayekians champion restraint and trust in the market’s invisible hand. Both offer valuable lessons, and understanding their differences can help investors navigate complex financial landscapes with greater clarity.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Posted on January 11, 2026 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

The 3-5-7 investing rule is a practical framework designed to help traders and investors manage risk, maintain discipline, and improve long-term profitability. Though not a formal financial regulation, it serves as a guideline for structuring trades and portfolios with clear boundaries. The rule is especially popular among retail traders and those seeking a simple yet effective way to navigate volatile markets.

At its core, the 3-5-7 rule breaks down into three components:

3% Risk Per Trade: This principle advises that no single trade should risk more than 3% of your total capital. For example, if your trading account holds $10,000, the maximum loss you should accept on any one trade is $300. This limit helps protect your portfolio from catastrophic losses and ensures that even a series of losing trades won’t wipe out your account.

5% Exposure Across All Positions: This part of the rule suggests that your total exposure across all open trades should not exceed 5% of your capital. It encourages diversification and prevents over-leveraging. By capping overall exposure, traders can avoid being overly reliant on a few positions and reduce the impact of market-wide downturns.

7% Profit Target: The final component sets a goal for each successful trade to yield at least 7% profit. This ensures that your winning trades are significantly larger than your losing ones. Even with a win rate below 50%, maintaining a favorable risk-reward ratio can lead to consistent profitability over time.

Together, these numbers form a balanced strategy that emphasizes risk control and reward optimization. The 3-5-7 rule is particularly useful in volatile markets, where emotional decision-making can lead to impulsive trades. By adhering to predefined limits, traders can stay focused and avoid common pitfalls like revenge trading or chasing losses.

One of the key advantages of the 3-5-7 rule is its adaptability. Traders can adjust the percentages based on their risk tolerance, market conditions, and account size. For instance, during periods of high volatility, one might reduce the per-trade risk to 2% or lower. Conversely, in stable markets, slightly higher exposure might be acceptable. The rule is not rigid but serves as a flexible foundation for building a disciplined trading strategy.

Moreover, the 3-5-7 rule promotes consistency. By applying the same criteria to every trade, investors can evaluate performance more objectively and refine their approach over time. It also helps in setting realistic expectations and avoiding the trap of overconfidence after a few successful trades.

In conclusion, the 3-5-7 investing rule is a simple yet powerful tool for managing risk and enhancing trading discipline. It provides a structured approach to position sizing, portfolio exposure, and profit targeting. Whether you’re a novice trader or a seasoned investor, incorporating this rule into your strategy can lead to more confident, calculated, and ultimately successful trading decisions.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

Posted on November 14, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

Silver occupies a distinctive position within the realm of investment assets, functioning simultaneously as a precious metal and an industrial commodity. This dual nature imbues silver with characteristics that make it a valuable component of a diversified portfolio, offering both defensive qualities and growth potential. While its volatility necessitates careful consideration, silver’s unique attributes warrant attention from investors seeking balance between risk mitigation and opportunity.

Silver as a Hybrid Asset

Unlike gold, which is primarily regarded as a store of value, silver derives a substantial portion of its demand from industrial applications. It is indispensable in sectors such as electronics, renewable energy, and medical technology, with photovoltaic cells in solar panels representing a particularly significant driver of consumption. This industrial utility ensures that silver’s price is influenced not only by macroeconomic uncertainty but also by technological innovation and global manufacturing trends. Consequently, silver provides investors with exposure to both traditional safe-haven dynamics and cyclical industrial growth.

Accessibility and Cost Efficiency

Silver’s affordability relative to gold enhances its appeal to a broad spectrum of investors. Physical silver, in the form of coins and bars, allows individuals with modest capital to participate in the precious metals market. Moreover, financial instruments such as exchange-traded funds (ETFs) and mining equities provide liquid and scalable avenues for investment. This accessibility ensures that silver can serve as an entry point into alternative assets, particularly for those seeking to hedge against inflation without committing substantial resources.

Inflation Hedge and Currency Protection

Historically, silver has demonstrated resilience during periods of inflation and currency depreciation. As fiat currencies lose purchasing power, tangible assets such as silver tend to appreciate, preserving wealth for investors. Although gold is often considered the primary hedge, silver’s similar properties, combined with its lower cost, render it a practical complement. In times of geopolitical instability or monetary expansion, silver can function as a safeguard against systemic risks.

Volatility and Associated Risks

Despite its advantages, silver is characterized by pronounced price volatility. Its smaller market size relative to gold renders it more susceptible to speculative trading and abrupt shifts in investor sentiment. Furthermore, fluctuations in industrial demand can amplify short-term price movements. While this volatility can generate significant returns, it also exposes investors to heightened risk. Accordingly, silver is best employed as a long-term holding within a diversified portfolio rather than as a vehicle for short-term speculation.

Portfolio Diversification and Investment Vehicles

Incorporating silver into a portfolio enhances diversification by introducing an asset class with low correlation to equities and fixed income securities. This non-correlation reduces overall portfolio risk and provides stability during market downturns. Investors may access silver through several channels: physical bullion for tangible ownership, ETFs for liquidity, mining stocks for leveraged exposure, and futures contracts for advanced strategies. Each vehicle entails distinct risk-reward profiles, enabling investors to tailor their approach according to objectives and tolerance.

Conclusion

Silver’s dual identity as both a precious metal and an industrial commodity distinguishes it from other investment assets. Its affordability, inflation-hedging capacity, and diversification benefits make it a compelling addition to portfolios. While volatility requires prudent management, silver’s potential to balance defensive and growth-oriented strategies underscores its enduring relevance in contemporary investment practice.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

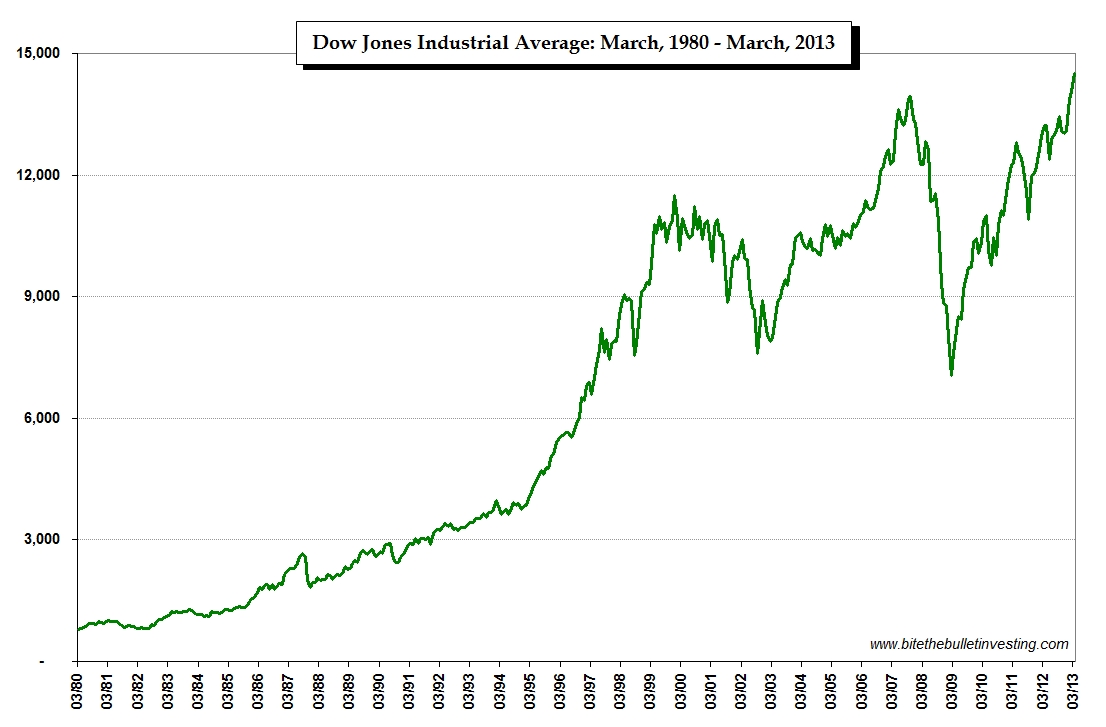

The thirty companies included in the Dow Jones Industrial Average are listed in the updated chart below.

The list is sorted by each component’s weight in the index. The weight of each company is determined by the price of the stock. A $100 stock will be weighted more than a $30 stock. If a stock splits its corresponding weighting in the Dow Jones will be reduced as its price will be about half of what it was prior to the split.

The NASDAQ, short for the National Association of Securities Dealers Automated Quotations, is one of the largest and most influential stock exchanges in the world. Founded in 1971, it was the first electronic stock market, revolutionizing how securities were traded by replacing traditional floor-based systems with computerized trading platforms. This innovation made transactions faster, more transparent, and accessible to a broader range of investors.

Unlike the New York Stock Exchange (NYSE), which historically operated through physical trading floors, the NASDAQ is entirely virtual. It connects buyers and sellers through a sophisticated network of computers, allowing for rapid execution of trades. This digital-first approach has made it particularly attractive to technology companies and growth-oriented firms, earning it a reputation as the go-to exchange for innovative and high-tech businesses.

Companies Listed on the NASDAQ The NASDAQ is home to some of the most prominent and influential companies in the world. Giants like Apple, Microsoft, Amazon, Google (Alphabet), Meta (formerly Facebook), and Tesla all trade on the NASDAQ. These companies are part of the NASDAQ-100, an index that tracks the performance of the 100 largest non-financial companies listed on the exchange. The NASDAQ Composite Index, which includes over 3,000 stocks, provides a broader snapshot of the market’s overall health and direction.

How It Works The NASDAQ operates as a dealer’s market, meaning transactions are facilitated by market makers—firms that stand ready to buy or sell securities at publicly quoted prices. These market makers help maintain liquidity and ensure that trades can be executed efficiently. Prices are determined by supply and demand, and the electronic nature of the exchange allows for real-time updates and high-speed trading.

Significance in the Global Economy The NASDAQ plays a vital role in the global financial system. It provides companies with access to capital by allowing them to issue shares to the public, and it offers investors a platform to buy and sell those shares. The performance of the NASDAQ is often seen as a barometer for the health of the technology sector and, more broadly, the innovation economy. When the NASDAQ rises, it typically signals investor confidence in growth and future earnings; when it falls, it may reflect concerns about economic stability or company performance.

Global Reach and Influence Though based in the United States, the NASDAQ’s influence extends worldwide. Many international companies choose to list on the NASDAQ to gain exposure to U.S. investors and benefit from the prestige associated with being part of a leading global exchange. Its technological infrastructure and regulatory standards make it a model for other exchanges around the world.

In summary, the NASDAQ is more than just a stock exchange—it’s a symbol of innovation, speed, and global connectivity. Its pioneering approach to electronic trading has reshaped the financial landscape, and its roster of companies continues to drive technological progress and economic growth across the globe.

Historian Cyril Parkinson’s wrote in his book Parkinson’s Law,

“The time spent on any item of the agenda will be in inverse proportion to the sum [of money] involved.”

EXAMPLE: Parkinson described a fictional finance committee with three tasks: approval of a $10 million nuclear reactor, $400 for an employee bike shed, and $20 for employee refreshments in the break room.

The committee approves the $10 million nuclear reactor immediately, because the number is too big to contextualize, alternatives are too daunting to consider, and no one on the committee is an expert in nuclear power.

Bike Shed Effect: The bike shed gets considerably more debate. Committee members argue whether a bike rack would suffice and whether a shed should be wood or aluminum, because they have some experience working with those materials at home.

Employee refreshments take up two-thirds of the debate, because everyone has a strong opinion on what’s the best coffee, the best cookies, the best chips, etc.

Absurd: The world is filled with these absurdities. In personal finance, Ramit Sethi recently said we should stop asking $3 questions (should I buy coffee?) and ask more $30,000 questions (should I buy a smaller home?). Most people don’t, because it’s hard and intimidating. In any given moment the easiest way to deal with a big problem is to ignore it and fill your time thinking about a smaller one.

***

***

Assessment: Your thoughts and comments related to the post Corona Virus Pandemic, meetings and time management and psychology are appreciated.

Posted on November 3, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko; MBA MEd

***

***

Classic Definition: In “The Exercise Paradox,” Herman Pontzer asserts that greater physical activity does not allow people to control weight. He goes on to describe studies on how the human body burns calories that help to explain why this is so.

Modern Circumstance: But in one of these studies, “couch potatoes” expended an average of around 200 fewer calories a day, compared with moderately active subjects. A difference of 200 fewer calories a day equates to more than 20 fewer pounds a year. Year after year after year, that really adds up.

Paradox Example: Cyclists participating in the Tour de France are said to ingest more than 5,000 calories a day. This would seem to be way too much. So why do they do it? And why don’t they become obese?

The Medical Executive-Post is a news and information aggregator and social media professional network for medical and financial service professionals. Feel free to submit education content to the site as well as links, text posts, images, opinions and videos which are then voted up or down by other members. Comments and dialog are especially welcomed. Daily posts are organized by subject. ME-P administrators moderate the activity. Moderation may also conducted by community-specific moderators who are unpaid volunteers.

Product costing deals with determining the total costs involved in the production of a good or service. Costs may be broken down into subcategories, such as variable, fixed, direct, or indirect costs. Cost accounting is used to measure and identify those costs, in addition to assigning overhead to each type of product created by the company.

Managerial accountants calculate and allocate overhead charges to assess the full expense related to the production of a good. The overhead expenses may be allocated based on the number of goods produced or other activity drivers related to production, such as the square footage of the facility. In conjunction with overhead costs, managerial accountants use direct costs to properly value the cost of goods sold and inventory that may be in different stages of production.

Marginal costing (sometimes called cost-volume-profit analysis) is the impact on the cost of a product by adding one additional unit into production. It is useful for short-term economic decisions. The contribution margin of a specific product is its impact on the overall profit of the company. Margin analysis flows into break-even analysis, which involves calculating the contribution margin on the sales mix to determine the unit volume at which the business’s gross sales equals total expenses. Break-even point analysis is useful for determining price points for products and services.

Cash Flow Analysis

Managerial accountants perform cash flow analysis in order to determine the cash impact of business decisions. Most companies record their financial information on the accrual basis of accounting. Although accrual accounting provides a more accurate picture of a company’s true financial position, it also makes it harder to see the true cash impact of a single financial transaction. A managerial accountant may implement working capital management strategies in order to optimize cash flow and ensure the company has enough liquid assets to cover short-term obligations.

When a managerial accountant performs cash flow analysis, he will consider the cash inflow or outflow generated as a result of a specific business decision. For example, if a department manager is considering purchasing a company vehicle, he may have the option to either buy the vehicle outright or get a loan. A managerial accountant may run different scenarios by the department manager depicting the cash outlay required to purchase outright upfront versus the cash outlay over time with a loan at various interest rates.

Inventory Turnover Analysis

Inventory turnover is a calculation of how many times a company has sold and replaced inventory in a given time period. Calculating inventory turnover can help businesses make better decisions on pricing, manufacturing, marketing, and purchasing new inventory. A managerial accountant may identify the carrying cost of inventory, which is the amount of expense a company incurs to store unsold items.

If the company is carrying an excessive amount of inventory, there could be efficiency improvements made to reduce storage costs and free up cash flow for other business purposes.

Constraint Analysis

Managerial accounting also involves reviewing the constraints within a production line or sales process. Managerial accountants help determine where bottlenecks occur and calculate the impact of these constraints on revenue, profit, and cash flow. Managers then can use this information to implement changes and improve efficiencies in the production or sales process.

Financial Leverage Metrics

Financial leverage refers to a company’s use of borrowed capital in order to acquire assets and increase its return on investments. Through balance sheet analysis, managerial accountants can provide management with the tools they need to study the company’s debt and equity mix in order to put leverage to its most optimal use.

Performance measures such as return on equity, debt to equity, and return on invested capital help management identify key information about borrowed capital, prior to relaying these statistics to outside sources. It is important for management to review ratios and statistics regularly to be able to appropriately answer questions from its board of directors, investors, and creditors.

Accounts Receivable (AR) Management

Appropriately managing accounts receivable (AR) can have positive effects on a company’s bottom line. An accounts receivable aging report categorizes AR invoices by the length of time they have been outstanding. For example, an AR aging report may list all outstanding receivables less than 30 days, 30 to 60 days, 60 to 90 days, and 90+ days.

Through a review of outstanding receivables, managerial accountants can indicate to appropriate department managers if certain customers are becoming credit risks. If a customer routinely pays late, management may reconsider doing any future business on credit with that customer.

Budgeting, Trend Analysis, and Forecasting

Budgets are extensively used as a quantitative expression of the company’s plan of operation. Managerial accountants utilize performance reports to note deviations of actual results from budgets. The positive or negative deviations from a budget also referred to as budget-to-actual variances, are analyzed in order to make appropriate changes going forward.

Managerial accountants analyze and relay information related to capital expenditure decisions. This includes the use of standard capital budgeting metrics, such as net present value and internal rate of return, to assist decision-makers on whether to embark on capital-intensive projects or purchases. Managerial accounting involves examining proposals, deciding if the products or services are needed, and finding the appropriate way to finance the purchase. It also outlines payback periods so management is able to anticipate future economic benefits.

Managerial accounting also involves reviewing the trendline for certain expenses and investigating unusual variances or deviations. It is important to review this information regularly because expenses that vary considerably from what is typically expected are commonly questioned during external financial audits. This field of accounting also utilizes previous period information to calculate and project future financial information. This may include the use of historical pricing, sales volumes, geographical locations, customer tendencies, or financial information.

Nepo babies often go broke due to a mix of financial mismanagement, lack of resilience, and the illusion of inherited success. Their privileged upbringing can mask the need for discipline, adaptability, and long-term planning—traits essential for sustaining wealth.

The term nepo baby—short for nepotism baby—refers to children of celebrities or influential figures who benefit from family connections to launch careers, especially in entertainment, fashion, or media. While these individuals often start with significant advantages, including wealth, fame, and access, many struggle to maintain financial stability over time. The reasons are complex and rooted in both personal and systemic factors.

First, many nepo babies lack financial literacy. Growing up in environments where money flows freely, they may never learn budgeting, investing, or the value of money. Without these skills, they’re prone to overspending, poor investments, and unsustainable lifestyles. Lavish purchases—designer clothes, luxury cars, expensive homes—can quickly drain even sizable inheritances if not managed wisely.

Second, the illusion of guaranteed success can be dangerous. Nepo babies often enter industries where their family name opens doors, but that doesn’t guarantee longevity. Fame is fickle, and public interest can fade. If they don’t develop their own talents or work ethic, they may find themselves unemployable once the novelty wears off. This overreliance on family reputation can lead to complacency, making it harder to adapt when challenges arise.

Third, many nepo babies face identity crises and public scrutiny. Constant comparisons to their successful parents can erode confidence and create pressure to live up to unrealistic expectations. Some rebel by distancing themselves from their family’s legacy, while others try to prove themselves in unrelated fields. Either way, this struggle can lead to erratic career choices and unstable income streams.

Fourth, fame without privacy can fuel destructive habits. The entertainment world is rife with stories of young stars—many of them nepo babies—falling into substance abuse, reckless behavior, or toxic relationships. These issues not only affect mental health but also lead to legal troubles and financial loss. Without strong support systems or accountability, it’s easy to spiral.

Finally, inherited wealth can disappear quickly without proper estate planning. Trust funds and inheritances may be mismanaged or depleted by taxes, lawsuits, or poor financial advisors. Some nepo babies assume the money will last forever and fail to plan for long-term sustainability. Others are exploited by opportunistic friends or partners who take advantage of their naivety.

In contrast, those who succeed often do so by acknowledging their privilege, developing their own skills, and surrounding themselves with trustworthy mentors. They treat their inherited platform as a launchpad—not a safety net—and work to build something lasting.

In short, nepo babies go broke not because they lack opportunity, but because opportunity without discipline is a recipe for downfall. Wealth and fame are fleeting without the grit to sustain them. The lesson here isn’t just about celebrity—it’s a universal truth: success inherited must still be earned.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

Posted on October 30, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

Cryonics is a scientific and philosophical endeavor that seeks to preserve human life by freezing individuals at ultra-low temperatures after legal death, with the hope that future medical advancements may allow for revival and healing. Though still a speculative and controversial field, cryonics has captured the imagination of futurists, scientists, and ethicists alike.

What Is Cryonics?

Cryonics involves the process of cryopreservation—cooling the body, or sometimes just the brain, to -196°C using liquid nitrogen. The goal is to halt all biological activity, particularly decay, immediately after death. This is not the same as freezing; rather, it involves vitrification, a process that turns bodily fluids into a glass-like state to prevent ice crystal formation, which can damage cells. Once preserved, the body is stored indefinitely in a cryogenic chamber until such time that revival is theoretically possible.

***

***

Scientific and Technological Challenges

Despite its futuristic appeal, cryonics remains highly experimental. No human has ever been revived from a cryopreserved state, and current technology cannot reverse the damage caused by the preservation process itself. While scientists have successfully frozen and revived small biological samples like sperm and embryos, scaling this to entire human bodies presents enormous challenges.

The hope lies in future breakthroughs in nanotechnology, regenerative medicine, and artificial intelligence that could repair cellular damage and cure the diseases that led to death in the first place.

Posted on October 25, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

PODCAST: National Prescription Drug Take Back Day

October 25, 2025

By Dr. David Edward Marcinko MBA MEd

***

The National Prescription Drug Take Back Day aims to provide a safe, convenient, and responsible means of disposing of prescription drugs, while also educating the general public about the potential for abuse of medications.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

President Donald Trump signed a pardon on Wednesday for convicted crypto executive Changpeng Zhao, who founded the Binance crypto exchange, White House Press Secretary Karoline Leavitt said in a statement. “President Trump exercised his constitutional authority by issuing a pardon for Mr. Zhao, who was prosecuted by the Biden Administration in their war on cryptocurrency,” Leavitt said. “In their desire to punish the cryptocurrency industry, the Biden Administration pursued Mr. Zhao despite no allegations of fraud or identifiable victims.”

Zhao was sentenced to four months in prison after reaching a deal with the Justice Dept. to plead guilty to charges of enabling money laundering at Binance, which he ran at the time. The U.S. also ordered Binance to pay more than $4 billion in fines and forfeiture, while Zhao agreed to pay $50 million in fines. A spokesperson for Binance did not immediately respond to a request for comment yesterday.

***

The History of Cryptocurrency: From Concept to Revolution

Cryptocurrency has transformed the global financial landscape, offering a decentralized alternative to traditional banking systems. Its history is rooted in decades of technological innovation, philosophical ideals, and economic experimentation.

🌐 Early Foundations

The concept of digital currency predates Bitcoin by several decades. In 1982, cryptographer David Chaum published a groundbreaking paper on secure digital transactions, laying the foundation for future developments in electronic money. Chaum later founded DigiCash in the 1990s, which introduced the idea of anonymous digital payments using cryptographic protocols. Although DigiCash eventually failed, it was a crucial stepping stone in the evolution of cryptocurrency.

The Birth of Bitcoin

The true revolution began in 2008 when an anonymous figure—or group—known as Satoshi Nakamoto released the Bitcoin whitepaper titled “Bitcoin: A Peer-to-Peer Electronic Cash System.” This document proposed a decentralized digital currency that used blockchain technology to record transactions transparently and securely without the need for a central authority.

On January 3, 2009, Nakamoto mined the first block of the Bitcoin blockchain, known as the Genesis Block. The first real-world Bitcoin transaction occurred in May 2010, when programmer Laszlo Hanyecz paid 10,000 BTC for two pizzas—an event now celebrated annually as Bitcoin Pizza Day.

Blockchain and Beyond

Bitcoin’s success inspired the development of other cryptocurrencies and blockchain platforms. Ethereum, launched in 2015 by Vitalik Buterin, introduced smart contracts—self-executing agreements coded directly into the blockchain. This innovation expanded the use of cryptocurrency beyond simple transactions to decentralized applications (dApps), finance (DeFi), and even digital art (NFTs).

Other notable cryptocurrencies include Litecoin, Ripple (XRP), and Cardano, each offering unique features such as faster transaction speeds, improved scalability, or enhanced privacy.

***

***

⚖️ Challenges and Controversies

Despite its promise, cryptocurrency has faced significant hurdles. Regulatory uncertainty, security breaches, and market volatility have raised concerns among governments and investors. High-profile hacks, such as the Mt. Gox exchange collapse in 2014, highlighted the risks associated with digital assets.

Governments around the world have responded differently—some embracing crypto innovation, others imposing strict regulations or outright bans. The rise of central bank digital currencies (CBDCs) reflects an effort to merge the benefits of crypto with the stability of fiat systems.

🚀 The Future of Crypto

Today, cryptocurrency is more than a niche technology—it’s a global phenomenon. Major companies accept Bitcoin, institutional investors hold crypto assets, and blockchain is being integrated into industries from healthcare to supply chain management.

As the technology matures, the focus is shifting toward scalability, sustainability, and interoperability. Whether it becomes a mainstream financial tool or remains a disruptive alternative, cryptocurrency has undeniably reshaped how we think about money, trust, and digital ownership.