BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on November 19, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

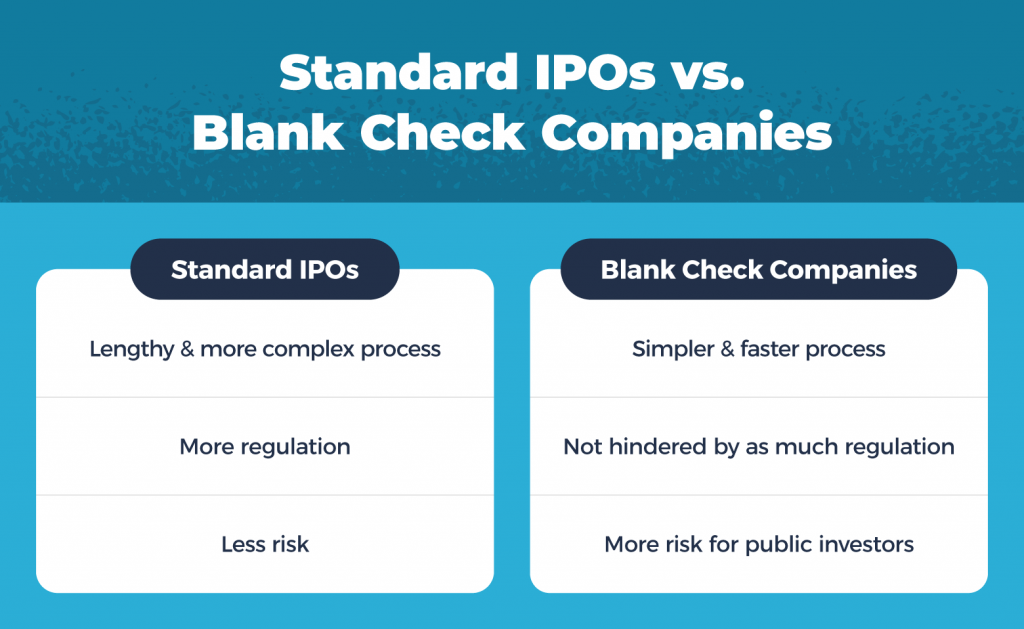

A Special Purpose Acquisition Company (SPAC) is a corporate entity created solely to raise capital through an initial public offering (IPO) with the intention of merging with or acquiring an existing private company. Unlike traditional firms, SPACs have no commercial operations at the time of their IPO. They exist as shell companies, holding investor funds in trust until a suitable target is identified. This unique structure has earned them the nickname “blank check companies.”

How SPACs Work

The lifecycle of a SPAC typically unfolds in three stages:

Formation and IPO: Sponsors—often experienced investors or industry executives—form the SPAC and take it public, raising funds from investors.

Target Search: The SPAC has a limited time frame, usually 18–24 months, to identify and negotiate with a private company to merge with.

De-SPAC Transaction: Once a merger is completed, the private company effectively becomes public, bypassing the traditional IPO process.

This process allows private firms to access public markets more quickly and with fewer regulatory hurdles compared to conventional IPOs.

Advantages of SPACs

SPACs gained traction because they offered several benefits:

Speed and Certainty: Traditional IPOs can be lengthy and uncertain, while SPACs provide a faster route to public markets.

Flexibility in Valuation: Unlike IPOs, SPACs can negotiate valuations directly with target companies.

Access to Expertise: Sponsors often bring industry knowledge and networks that can help the acquired company grow.

Investor Opportunity: Investors can participate early, with the option to redeem shares if they dislike the proposed merger.

Risks and Criticisms

Despite their appeal, SPACs are not without controversy:

Sponsor Incentives: Sponsors typically receive a significant stake (often 20%) at a low cost, which can misalign their interests with ordinary investors.

Uncertain Targets: Investors commit funds without knowing which company will be acquired, creating risk.

Performance Concerns: Studies show that many SPACs underperform after completing mergers, with share prices often declining.

Regulatory Scrutiny: Authorities have warned investors to carefully evaluate SPACs, especially regarding projections of future performance, which are less restricted than in IPOs.

Historical Context and Trends

SPACs first appeared in the 1990s but remained niche until the early 2020s, when they experienced a boom. In 2020 and 2021, hundreds of SPAC IPOs raised billions of dollars, fueled by market liquidity and investor enthusiasm. High-profile deals, such as DraftKings and Virgin Galactic, brought attention to the model. However, by the mid-2020s, enthusiasm cooled due to poor post-merger performance and tighter regulations.

Conclusion

SPACs represent a fascinating innovation in financial markets, offering an alternative to traditional IPOs. Their advantages in speed, flexibility, and access to capital made them attractive during periods of market optimism. Yet, their risks—misaligned incentives, uncertain outcomes, and regulatory challenges—have tempered investor enthusiasm. While SPACs are unlikely to disappear entirely, their future will depend on whether they can evolve into a more transparent and sustainable mechanism for taking companies public.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Investment bankers are not really bankers at all. The fact that the word banker appears in the name is partially responsible for the false impressions that exist in the medical community regarding the functions they perform.

For example, they are not permitted to accept deposit, provide checking accounts, or perform other activities normally construed to be commercial banking activities. An investment bank is simply a firm that specializes in helping other corporations obtain money they need under the most advantageous terms possible. When it comes to the actual process of having securities issued, the corporation approaches an investment banking firm, either directly, or through a competitive selection process and asks it to act as adviser and distributor.

Investment bankers, or under writers, as they are sometimes called, are middlemen in the capital markets for corporate securities. The corporation requiring the funds discusses the amount, type of security to be issued, price and other features of the security, as well as the cost to issuing the securities. All of these factors are negotiated in a process known as negotiated underwriting. If mutually acceptable terms are reached, the investment banking firm will be the middle man through which the securities are sold to the general public. Since such firms have many customers, they are able to sell new securities, without the costly search that individual corporations may require to sell its own security.

Thus, although the firm in need of additional capital must pay for the service, it is usually able to raise the additional capital at less expense through the use of an investment banker, than by selling the securities itself. The agreement between the investment banker and the corporation may be one of two types. The investment bank may agree to purchase, or underwrite, the entire issue of securities and to re-offer them to the general public. This is known as a firm commitment.

When an investment banker agrees to underwrite such a sale; it agrees to supply the corporation with a specified amount of money. The firm buys the securities with the intention to resell them. If it fails to sell the securities, the investment banker must still pay the agreed upon sum.

Thus, the risk of selling rests with the underwriter and not with the company issuing the securities.

The alternative agreement is a best efforts agreement in which the investment banker makes his best effort to sell the securities acting on behalf of the issuer, but does not guarantee a specified amount of money will be raised. When a corporation raises new capital through a public offering of stock, one might inquire where the stock comes from. The only source the corporation has is authorized, but previously un-issued stock. Anytime authorized, but previously un-issued stock (new stock) is issued to the public, it is known as a primary offering.

If it’s the very first time the corporation is making the offering, it’s also known as the Initial Public Offering (IPO). Anytime there is a primary offering of stock, the issuing corporation is raising additional equity capital.

A secondary offering, or distribution, on the other hand, is defined as an offering of a large block of outstanding stock. Most frequently, a secondary offering is the sale of a large block of stock owned by one or more stockholders. It is stock that has previously been issued and is now being re-sold by investors. Another case would be when a corporation re-sells its treasury stock.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

UnitedHealth Group soared almost 12%, its biggest one-day gain in nearly five years, after getting the “Buffett Bounce.” Buffett’s Berkshire Hathaway revealed it bought ~5 million shares worth nearly $1.6 billion, giving a much-needed vote of confidence to the struggling health giant.

The White House is considering buying part of Intel, Bloomberg reported this week, which would be the latest big business deal the president pursues on behalf of the government. The Trump administration might acquire a stake in the struggling computer chip-maker using CHIPS Act funding—nearly $11 billion of which was already earmarked for Intel.

Saudi Arabia’s Public Investment Fund took an $8 billion write-down on five mega-projects it’s building, due to lower oil prices and higher costs.

Pimco, the asset management giant, warned that President Trump’s plan to IPO Fannie Mae and Freddie Mac could push mortgage rates higher.

Posted on July 26, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

On July 15, 2025, the Centers for Medicare & Medicaid Services (CMS) released the proposed rule for the Outpatient Prospective Payment System (OPPS) and Ambulatory Surgical Center (ASC) Payment System for calendar year (CY) 2026.

Among other items, the agency proposes increasing payments to all outpatient providers, eliminating the Inpatient Only (IPO) List, and changing quality reporting programs.

This Health Capital Topics article reviews the proposed updates and changes to outpatient reimbursement. (Read more…)

Bonds: The 10-year yield fell after CPI came in lower than analysts expected. The Treasury Department’s auction of 10-year bonds also went well, with strong participation from traders a key sign of demand for fixed income. Zero Coupon: https://medicalexecutivepost.com/2024/11/12/bonds-zero-coupon/

FIVE INVESTING MISTAKES OF DOCTORS; PLUS 1 VITAL TIP

As a former US Securities and Exchange Commission [SEC] Registered Investment Advisor [RIA] and business school professor of economics and finance, I’ve seen many mistakes that doctors must be aware of, and most importantly, avoid. So, here are the top 5 investing mistakes along with suggested guideline solutions.

Mistake 1: Failing to Diversify Investment but Beware Di-Worsification

A single investment may become a large portion of your portfolio as a result of solid returns lulling you into a false sense of security. The Magnificent Seven stocks are a current example:

Apple, up +5,064%% since 1/18/2008

Amazon, up +30,328% since 9/6/2002

Alphabet, up +1,200% since 7/20/2012

Tesla, up +21,713% since 11/16/2012

Meta, up +684% since 2/20/2015

Microsoft, up +22% since 12/21/2023

Nvidia, up +80,797% since 4/15/2005

Guideline: The Magnificent Seven [7] has grown from 9% of the S&P 500 at the end of 2013 to 31% at the end of 2024! That means even if you don’t own them, you’re still very exposed if you have an Index Fund [IF] or Exchange Traded Fund [ETF] that tracks the market. Accordingly, diversification is the only free lunch in investing which can reduce portfolio risk. But, remember the Wall Street insider aphorism that states: “Di-Versification Means Always Having to Say Your Sorry.”

The term “Di-Worsification” was coined by legendary investor Peter Lynch in his book, One Up On Wall Street to refer to over-diversifying an investment portfolio in such a way that it reduces your overall risk-return characteristics. In other words, the potential return rises with an increase in risk and invested money can render higher profits only if willing to accept a higher possibility of losses [1].

A podiatrist can easily fall into the trap of chasing securities or mutual funds showing the highest return. It is almost an article of faith that they should only purchase mutual funds sporting the best recent performance. But in fact, it may actually pay to shun mutual funds with strong recent performance. Unfortunately, many struggle to appreciate the benefits of their investment strategy because in jaunty markets, people tend to run after strong performance and purchase last year’s winners.

Similarly, in a market downturn, investors tend to move to lower-risk investment options, which can lead to missed opportunities during subsequent market recoveries. The extent of underperformance by individual investors has often been the most awful during bear markets. Academic studies have consistently shown that the returns achieved by the typical stock or bond fund investors have lagged substantially.

Guideline: Understand chasing performance does not work.Continually monitor your investments and don’t feel the need to invest in the hottest fund or asset category. In fact, it is much better to increase investments in poor performing categories (i.e. buy low). Also keep in remind rebalancing of assets each year is key. If stocks perform poorly and bonds do exceptionally well, then rebalance at the end of the year. In following this strategy, this will force a doctor into buying low and selling high each year.

Often doctors make their investment decisions under the belief that stocks will consistently give them solid double-digit returns. But the stock markets go through extended long-term cycles.

In examining stock market history, there have been 6 secular bull markets (market goes up for an extended period) and 5 secular bear markets (market goes down) since 1900. There have been five distinct secular bull markets in the past 100+ years. Each bull market lasted for an extended period and rewarded investors.

For example, if an investor had started investing in stocks either at the top of the markets in 1966 or 2000, future stock market returns would have been exceptionally below average for the proceeding decade. On the other hand, those investors fortunate enough to start building wealth in 1982 would have enjoyed a near two-decade period of well above average stock market returns. They key element to remember is that future historical returns in stocks are not guaranteed. If stock market returns are poor, one must consider that he or she will have to accept lower projected returns and ultimately save more money to make up for the shortfall. For example,

The May 6th, 2010, flash crash, also known as the crash of 2:45, was a United States trillion-dollar stock market plunge which started at 2:32 pm EST and lasted for approximately 36 minutes.

And, investors who have embraced the “buy the dip” strategy in 2025 have been handsomely rewarded, with the S&P 500 delivering its strongest post-pull back returns in over three decades.

According to research from Bespoke Investment Group, the S&P 500 has gained an average of 0.36% in the trading session following a down day so far in 2025. The only year with a comparable performance was 2020, which saw a 0.32% average post-dip gain [2].

The most recent example came on May 27, 2025 when the S&P 500 surged more than 2% after falling 0.7% in the final session before the holiday weekend. The rally was sparked by President Trump’s decision to scale back huge previously threatened tariffs on EU —a recurring catalyst behind many of 2025’s rebound.

Guideline: Beware of projecting forward historical returns. Doctors should realize that the stock markets are inherently volatile and that, while it is easy to rely on past historical averages, there are long periods of time where returns and risk deviate meaningfully from historical averages.

Some doctors believe they are “smarter than the market” and can time when to jump in and buy stocks or sell everything and go to cash. Wouldn’t it be nice to have the clairvoyance to be out of stocks on the market’s worst days and in on the best days?

Using the S&P 500 Index, our agile imaginary doctor-investor managed to steer clear of the worst market day each year from January 1st, 1992 to March 31st, 2012. The outcome: s/he compiled a 12.42% annualized return (including reinvestment of dividends and capital gains) during the 20+ years, sufficient to compound a $10,000 investment into $107,100.

But what about another unfortunate doctor-investor that had the mistiming to be out of the market on the best day of each year. This ill-fated investor’s portfolio returned only 4.31% annualized from January 1992 – March 2012, increasing the $10,000 portfolio value to just $23,500 during the 20 years. The design of timing markets may sound easy, but for most all investors it is a losing strategy.

More contemporaneously on December 18th 2024, the DJIA plummeted 2.5%, while the S&P 500 declined 3% and the NASDAQ tumbled 3.5%

Guideline: If it looks too good to be true, it probably is. While jumping into the market at its low and selling right at the high is appealing in theory, we should recognize the difficulties and potential opportunity and trading costs associated with trying to time the stock market in practice. In general, colleagues are be best served by matching their investment with their time horizon and looking past the peaks / valleys along the way.

Mistake 5: Failing to Recognize the Impact of Fees and Expenses

A free dinner seminar or a polished stock-broker sales pitch may hide the total underlying costs of an investment. So, fees absolutely matter.

The first costing step is determining what the fees actually are. In a mutual fund, these costs are found in the company’s obligatory “Fund Facts”. This manuscript clearly outlines all the fees paid–including up front fees (commissions and loads), deferred sales charges and any switching fees. Fund management expense ratios are also part of the overall cost. Trading costs within the fund can also impact performance.

Here is a list of the traditional mutual fund fees:

Front End Load: The commission charged to purchase a fund through a stock broker or financial advisor. The commission reduces the amount you have available to invest. Thus, if you start with $100,000 to invest, and the advisor charges up to an 8 percent front end load, you end up actually investing $92,000.

Deferred Sales Charge (DSC) or Back End Load: Imposed if you sell your position in the mutual fund within a pre-specified period of time (normally one – five years). It is initiated at a higher start percentage (i.e. as high as 10 percent) and declines over a specific period of time.

Operating Fees: Costs of the mutual fund including the management fee rewarded to the manager for investment services. It also includes legal, custodial, auditing and marketing fees.

Annual Administration Fee: Many mutual fund companies also charge a fee just for administering the account – usually under $100-150 per year.

Guideline: Know and understand all fees.

For example: A 1 percent disparity in fees may not seem like much but it makes a considerable impact over a long time period.

Consider a $100,000 portfolio that earns 8 percent before fees, grows to $320,714 after 20 years if the investor pays a 2 percent operating fee. In comparison, if s/he opted for a fund that charged a more reasonable 1 percent fee, after 20 years, the portfolio grows to be $386,968 – a divergence of over $66,000!

This is the value of passive or index investing. In the case of an index fund, fees are generally under 0.5 percent, thus offering even more savings over a long period of time.

One Vital Tip: Investing Time is on Your Side

Despite thousands of TV shows, podcasts, textbooks, opinions and university studies on investing, it really only has three simple components. Amount invested, rate of return and time. By far, the most important item is time! For example:

Nvidia: if you invested $1,000 in 2009, you’d have $338,103 today.

Apple: if you invested $1,000 in 2008, you’d have $48,005 today.

Netflix: if you invested $1,000 in 2004, you’d have $495,679 today.

Unfortunately, this list of investing mistakes is still being made by many doctors. Fortunately, by recognizing and acting to mitigate them, your results may be more financially fruitful and mentally quieting.

REFERENCES:

1. Lynch, Peter: One Up on Wall Street [How to Use What You Already Know to Make Money in the Market]: Simon and Shuster (2nd edition) New York, 2000.

1. Marcinko, DE; Comprehensive Financial Planning Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™] Productivity Press, New York, 2017.

2. Marcinko, DE: Dictionary of Health Economics and Finance. Springer Publishing Company, New York, 2006.

3. Marcinko, DE; Risk Management, Liability Insurance, and Asset Protection Strategies for Doctors and Advisors [Best Practices from Leading Consultants and Certified Medical Planners™] CRC Press, New York, 2015.

BIO: As a former university Professor and Endowed Department Chair in Austrian Economics, Finance and Entrepreneurship, the author was a NYSE Registered Investment Advisor and Certified Financial Planner for a decade. Later, he was a private equity and wealth manager

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on June 9, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By AI

***

***

Wall Street is stable right now as the technology trade has come roaring back.

The S&P 500 climbed above 6,000 points for the first time since February, while all three indexes posted their fifth winning week in the last seven. The S&P is now just over 2% from its all-time high.

Meanwhile, recent IPOs are party rocking, especially the stablecoin issuer Circle that went public last Thursday.

Virtual chronic care provider Omada Health has filed to go public in the United States, the latest in a string of healthcare listings expected this year. Omada did not disclose the details as to how much it plans to raise from its IPO.

The San Francisco, California-based company, which last raised $192 million in a Series E funding round in 2022, reported a 38% increase in revenue to $169.8 million for 2024, according to its IPO paperwork. For the first quarter of 2025, the company posted a 56.6% year-on-year jump in revenue to $55 million. Omada has applied to list its common stock on the NASDAQ under the symbol “OMDA”.

Healthcare IPOs on U.S. exchanges have fetched $7.1 billion in 2024, compared with $2.8 billion a year earlier, according to data compiled by LSEG.

Posted on May 2, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The National Nurses in Business Association (NNBA) is the premier nursing organization for nurse entrepreneurs, and a springboard for nurses transitioning from employees to entrepreneurs and business owners. The NNBA is an invaluable resource for existing nurse business owners seeking to expand, and maximize their business success.

Members’ resumes include thousands of nurse owned businesses, local, national and international awards, and millions of dollars in revenue. The experience, knowledge and impact of the NNBA community is amazing, as well as the support provided to fellow nurse entrepreneurs and aspiring entrepreneurs.

As the forerunner of the nurse entrepreneur movement, the NNBA provides valuable business information customized for nurses on how to start, plan, expand and grow your nurse owned business. They provide expert guidance, marketing and promotional opportunities, and continuing education in professional growth and career development.

When you buy a share of stock, you are taking ownership in a company. Collectively, the company is owned by all the shareholders, and each share represents a claim on assets and earnings. If the company distributes profits to its shareholders, you should receive a proportionate share of the earnings.

Stocks are often categorized by the size of the company, or their market capitalization. The market capitalization is determined by multiplying the number of outstanding shares by the current share price. The most common market cap classes are small-cap (valued from $100 million to $1 billion), mid-cap ($1 billion to $10 billion), and large cap ($10 billion to $100 billion).

Stocks are also categorized by their sector, or the type of business the company conducts. Common sectors include utilities, consumer staples, energy, communications, financial, health care, transportation, and technology.

***

***

Stocks are often viewed as being in one of two categories — growth or value.

Growth stocks are ones that are associated with high quality, successful companies that are expected to continue growing at a better-than-average rate as compared to the rest of the market.

Value stocks are ones that have generally solid fundamentals, but are currently out of favor with the market. This may be due to the company being relatively new and unproven in the market, or because the company has recently experienced a decline due to the company’s sector being affected negatively. An example of this would be if the federal government was to levy a new tax on all cell phones, thus negatively affecting all cell phone company stocks.

History has shown that, over time, stocks have provided a better return than bonds, real estate, and other savings vehicles. As a result, stocks may be the ideal investment for investors with long-term goals.

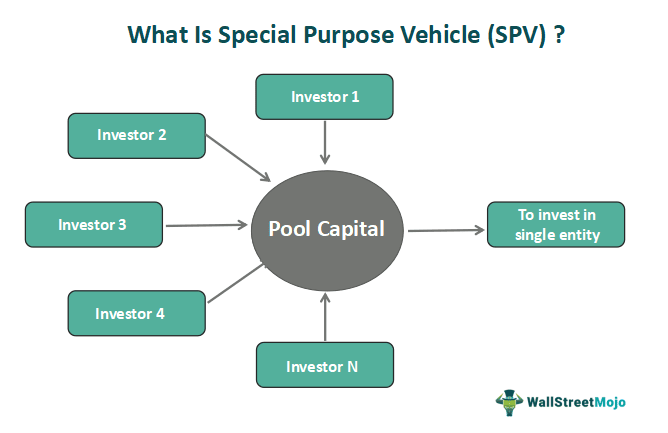

Its purpose is to isolate the parent company from any potential credit or financial risk that may arise from the SPV and is often used to pursue riskier projects, securitize debt, or transfer assets. Since an SPV is separate from the parent company, it isn’t affected by the parent’s performance, and the parent isn’t typically affected by the performance of the SPV. If the parent goes bankrupt and is no longer in existence, the SPV can carry on.

This makes an SPV bankruptcy remote. This also means that the parent company is unaffected by the loss if the SPV fails.

Posted on April 7, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Initial Public Offering Defined

IPO stands for initial public offering. It is when a company takes a portion of their shares and makes them available for the general public to buy on the open market. It is a way for the company to raise money by selling those shares to the general public. You can usually access shares from an IPO by working directly with an investment bank.

Paused IPOs

Private companies StubHub and Klarna each paused their imminent plans to go public.

Klarna, which was set to IPO on this Monday, was expected to jump-start the frozen IPO market this year with an expected ~$15 billion valuation.

StubHub, meanwhile, reportedly wants to wait for the market to calm down before resuming its plans to go public.

In general, a roadshow is a series of meetings or presentations in which key members of a private company, usually executives, pitch the initial public offering, or IPO, to prospective investors. Effectively, the company is taking its branding message on the road to meet with investors in different cities, hence the name.

The IPO roadshow presentation is an important part of the IPO process in which a company sells new shares to the public for the first time. Whether a company’s IPO succeeds or not can hinge on interest generated among investors before the stock makes its debut on an exchange.

There are also some cases where company executives will embark on a road show to meet with investors to talk about their company, even if they’re not planning an IPO.

Pros and Cons of a Roadshow

According to Rebecca Lake, if the company goes public and no one buys its shares, then the IPO ends up being a flop, which can affect the company’s success in the near and long term. If the company experiences an IPO pop, in which its price goes much higher than its initial offering price, it could be a sign that underwriters mispriced the stock.

A roadshow is also important for helping determine how to price the company’s stock when the IPO launches. If the roadshow ends up being a smashing success, for example, that can cause the underwriters to adjust their expectations for the stock’s IPO price.

On the other hand, if the roadshow doesn’t seem to be generating much buzz around the company at all, that could cause the price to be adjusted downward.

In a worst-case scenario, the company may decide to pull the plug on the IPO altogether or to go a different route, such as a private IPO placement.

Private equity consists of investments made directly into private companies that are not quoted on a public exchange. The majority of private equity consists of institutional investors and accredited investors who can commit large sums of money for long periods of time.

Private equity investments often demand long holding periods to allow for a turnaround of a distressed company or a liquidity event such as an initial public offering or sale to a public company.

Posted on November 7, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

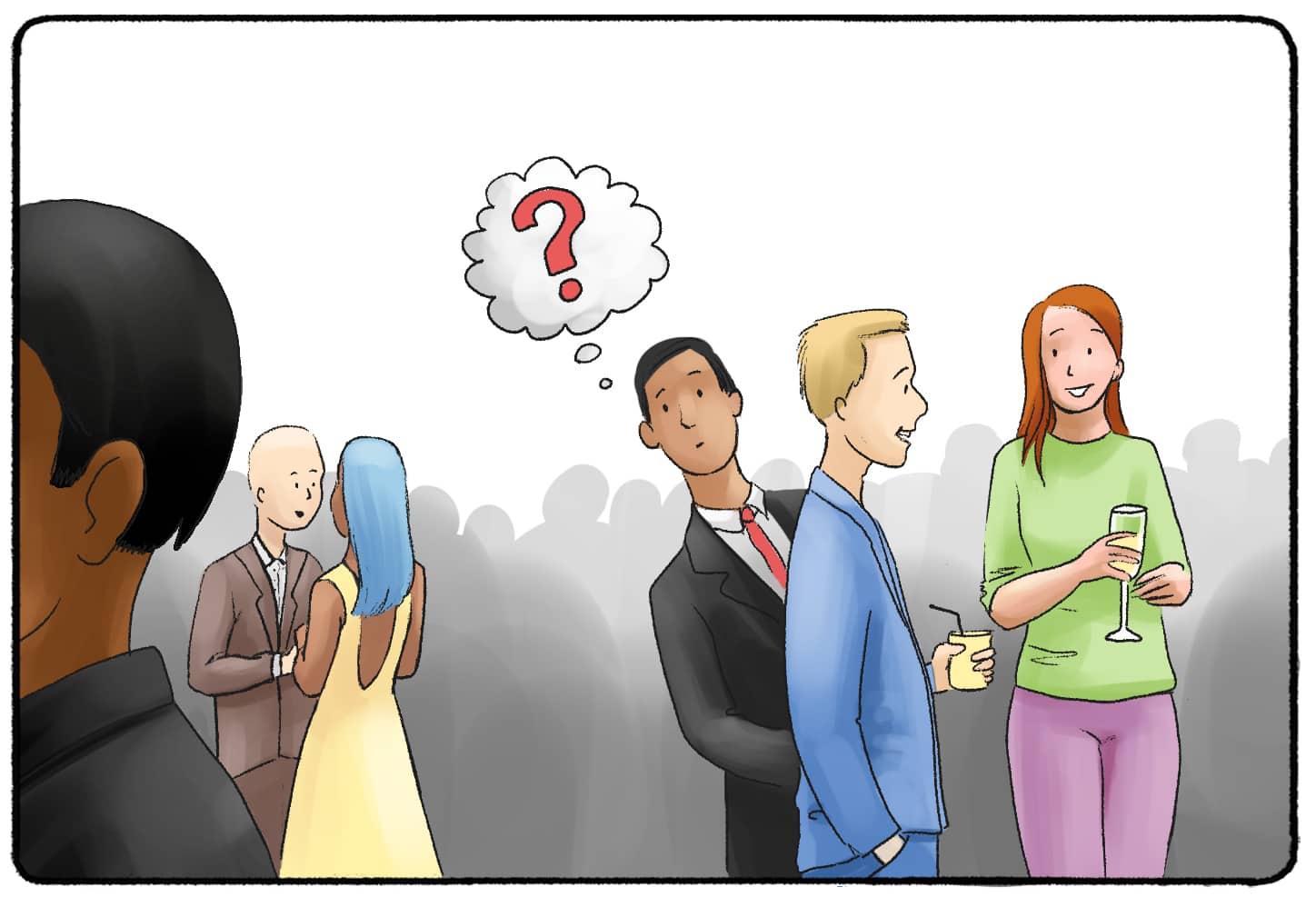

The cocktail party effect is the ability of the human hearing and auditory system to focus one’s listening attention on a particular speaker in a noisy environment, such as a crowded party. This allows people to focus on a specific conversation while filtering out other nearby conversations and background noise.

Consider that you’re at a crowded party, noise everywhere, but you hear your name mentioned across the room. How? Welcome to the Cocktail Party Effect.

Your brain is like a highly trained butler, filtering out the background chatter to catch something personally relevant. It’s not just your name, either; it could be juicy gossip or a mention of free pizza or an exciting new stock tip you’ve been considering; or even an IPO.

So, according to psychologist colleague Dan Ariely PhD, this selective attention keeps us sane in a noisy world, helping us focus on the things that matter – like whether that person just said “free drinks” or “freeloading, or “free-stock trading.”

Initial public offerings, known as IPOs, tend to attract a lot of investor interest – especially when the company is well-known. However, that excitement isn’t always matched by investment returns.

“Tips and Pearls”

So, here are some tips to consider before you decide to invest in an IPO:

• Don’t let the excitement surrounding an IPO cloud your judgment. Too often, there is little financial information about the companies themselves, and many are not profitable. This can translate into extremely volatile stock prices.

• While an IPO’s stock price tends to rise on the day it begins trading, investors who bought shares at the end of the first day haven’t always fared well. The stocks have often fallen below the closing first-day price after six months.

High volatility and a falling stock price are not generally a recipe for attractive investor returns.

So what steps should you take if you’re still interested in an IPO?

1. Understand that the opening price will likely be different from the official IPO price. New issues can experience extreme volatility in the first few hours and days of trading in the secondary market. When the company’s stock opens for secondary trading and becomes more widely available, the price can be significantly different from the IPO price set by the security underwriters. In addition, new issues often do not begin trading the moment the market opens.

2. Use a limit order. This can help you avoid paying more for the stock than you intended. Once you understand the risks of purchasing a stock during its first public trading days, work with your financial advisor to determine the highest price you’re willing to pay for the stock, and then set that amount as your limit.

3. Remember that an IPO must be priced before an order can be accepted. For example, Edward Jones typically does not accept orders until after an IPO has been priced, which is usually the morning the new issue begins trading. In addition, your financial advisor is not permitted to accept market orders for any IPO prior to its trading in the secondary market.

Remember to always do your homework before deciding on any investment, including an IPO. This includes working with your financial advisor or accountant to determine whether the investment is suitable for your portfolio.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements.

Subscribe: MEDICAL EXECUTIVE POST for curated news, essays, opinions and analysis from the public health, economics, finance, marketing, IT, business and policy management ecosystem.

Posted on September 4, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Fundamentals of Physician Investing

By Daniel B. Moisand CFP®, and ME-P staff

It used to be that the only way to get investments and investment information was through paying commissions to a traditional broker. Then in the 70’s (specifically, May, 1975) the brokerage industry went through significant deregulation allowing for the discounting of commissions. Charles Schwab and Company, among others, was able to eliminate the advice component and offer trades at dramatically reduced rates. The full service brokerage business responded by emphasizing the scope of their services namely research and advice in order to compete. The demand for both has continued to grow, even though research information is now readily available through many sources. These brokerage firms continue to thrive despite their poor performance in analyzing tech stocks and the Enron and Global Grossing debacles. More recent debacles in 2008-09, the flash crash a decade ago and more recent developments are legion, as well.

Fundamental Flaws

The fundamental flaw with these firms is the array of conflicts of interest between the firm and its customers. While the incentive to trade has been well chronicled as a conflict, these firms have not let consumer’s demand for a better-aligned compensation arrangement go unnoticed. Fee-based account relationships have proliferated accordingly. In theory, this type of arrangement, usually a percentage of assets, gives an incentive for performance and service rather than trade activity. This certainly has merit. However, conflicts remain that should be considered.

Pay to Play

The practice of paying brokers, higher levels of compensation for in-house products was commonplace. Today, explicitly higher payouts still exist but are less common. Instead, many firms use the sale of proprietary mutual funds and other products as part of management’s compensation. Other forms of non-monetary compensation such as a better office can be used as incentive for the brokers. The greater profitability of these in-house offerings will keep this conflict around for some time.

Subtle Conflicts of Interest

Less obvious is the conflict between the investment banking arm, the research department, and the retail brokerage operations of a firm. Even firms with no proprietary funds to sell may grapple with this issue. Here, research is pressured to say favorable things about a particular company’s stock by the investment bankers in hopes of obtaining more of that company’s business. When a firm brings a company public odds are great that a “strong buy” rating will come with the IPO. Of course, the lesson remains – consider the source.

Assessment

Traditional brokers have a somewhat higher standard of accountability than the on-line firms as to their accountability. If you buy the stock of a company that goes bankrupt through an on-line broker you have little recourse. After all, that was your choice. If a full-service broker recommended the stock to you, that broker will have to defend the recommendation.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on July 31, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Bill Ackman’s fund postpones IPO

The billionaire hedge fund boss and frequent main character on X has delayed the stock market debut of the closed-end fund Pershing Square USA, which was scheduled for early next week, a notice on the New York Stock Exchange’s website said.

The decision to wait came days after Ackman said in a letter to investors that the firm was downsizing its expectations for the share sale from a target of about $25 billion (which would have made it the largest-ever IPO of its kind) to something between $2.5 billion and $4 billion.

Ackman has a similar fund already trading shares in Europe and has hinted he might take his larger firm, Pershing Square, public as soon as next year.

Posted on July 26, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

What’s the difference between an IPO, a special purpose acquisition company (SPAC), and a direct listing?

[By staff reporters]

IPOs are a 6–12 month journey where a company works with investment banks and underwriters, who buy a bunch of shares and then sell them to investors in the public market during the actual IPO. Early investors are able to liquidate their shares, and the company raises new funds.

Direct listings skip the underwriting hullabaloo. But without that stability guarantee, direct listings can result in a more volatile opening. Some companies, like Coinbase, find that it’s worth it to keep their hard-earned money out of bankers’ hands.

SPACs, aka “blank-check companies,” offer yet another alternative path to public markets. A SPAC is a shell company that raises money through the traditional IPO process, then merges with a private company and takes it public.

At Marcinko & Associates, we appreciate that Venture Capital funding for entrepreneurs in the digital health space cooled a bit in 2020-22 following a red-hot 2018-20. And, overall, digital health companies raised $15.3 billion last year, down from the $29.1 billion raised in 2021—but still above the $14.1 billion raised in 2020, according to Rock Health a seed fund that supports digital health startups.

Nevertheless, other analysts predict VC investors and Investment Bankers will still put a good amount of money into digital health in 2024 thru 2027, especially in alternative care, drug development, health information technology, artificial intelligence, EMRs and software that reduces physician workload.

An essential first part of attracting VC interest and IB money is the crafting and presentation of your formal business plan [“elevator pitch”]; as well as the needed technical and managerial experience. This too is crucial for success and exactly where we can assist.

Of course, companies focused on scaling and growing will have different needs across the business lifecycle.

And so, no matter where you are in your journey—from seeking early funding to making final preparations for your IPO—we have equity and insightful administration solutions for you and can assist at any stage of your growth spectrum.

A Primer for Physician Investors and Medical Professionals

By: Dr. David Edward Marcinko; MBA, MEd, CMP™

[Editor-in-Chief]

[PART 2 OF 8]

NOTE: This is an eight part ME-P series based on a weekend lecture I gave more than a decade ago to an interested group of graduate, business and medical school students. The material is a bit dated and some facts and specifics may have changed since then. But, the overall thought-leadership information of the essay remains interesting and informative. We trust you will enjoy it.

Introduction

Despite the SEC restrictions, noted in Part I of this series, some idea of potential demand for a new security issue can be gauged and have a bearing on pricing decisions.

For example, as CEO of a medical instrument company, or interested investor, would you rather see a great deal of interest in a potential new issue or not very much interest? There is however, one kind of advertisement that the underwriter can publish during the cooling off period. It’s known as a tombstone ad. The ad makes it clear that it is only an announcement and does not constitute an offer to sell or solicit the issue, and that such an offering can only be made by prospectus. SEC Rule 134 of the 1933 Act itself, refers to a tombstone ad as “communication not deemed a prospectus” because it makes reference to the prospectus in the ad. Tombstones have received their name because of the sparse nature of details found in them.

However, the most popular use of the tombstone ad is to announce the effectiveness of a new issue, after it has been successfully issued. This promotes the success of both he underwriter, as well as the company.

Since distributing securities involves potential liability to the investment bank, it will do everything possible to protect itself. So, near the end of the cooling off period, a meeting is held between the underwriter and the corporation. It is known as a due diligence meeting. At this meeting they both discuss amendments that are going to be necessary to make the registration statement complete and accurate. The corporate officers, and the underwriters sign, the final registration statement. They have civil liability for damages that result from omissions of material facts or

Mis-statements of fact. They also have criminal liability if the distribution is done by use of fraudulent, manipulative, or deceptive means. Due diligence takes on a whole new meaning when incarceration from a half-hearted effort underwriting efforts can occur. The investment bank strives to ensure that there have been no material changes to the issuer or the terms of the issue since the registration statement was filed.

Again, as a physician, how would you feel if you were an investment banker raising capital for a new pharmaceutical company that had developed a drug product that was highly marketable. But, on the day after the issue was effective, there was a major news story indicating that the company was being sued for patent infringement? What effect do you think that would have on the market price of this new issue? It would probably plunge. How could this situation have been prevented? The due diligence meeting is more than a cocktail party or a gathering in a smoke filled room. Otherwise, the company would require specially trained people, to do a patent search lessening the likelihood of this scenario. At the due diligence meeting, work is done on the preparation of the final prospectus, but the investment bank does not set the public offering price or the effective date at this meeting. The SEC will eventually set the effective date for the registration and it is on that date that the final offering price will be determined.

Once the SEC sets the effective date, sales may be executed and money can be accepted by the investment bank. It is at this time that the final prospectus, similar to the red herring but without the red ink and with the missing numbers, is issued. A prospectus is an abbreviated form of the registration statement, distributed to purchasers, on and after the effective date of the registration. It is not the same as the registration statement. A typical registration statement consists of papers that stand more than a foot high; rarely does a prospectus go beyond 40 or 50 pages. All purchasers will receive a final prospectus and then it becomes permissible for the underwriter to provide sales literature.

In addition to the requirement that a prospectus must be delivered to a purchaser of new issues no later than with confirmation of the trade, there are two other requirements that healthcare executives investors should know.

90-day: When an issuer has an initial public offering (IPO), there is generally a lack of publicly available material relating to the operations of that issuer. Because of this, the SEC requires that all members of the underwriting group make available a prospectus on an IPO for a period of 90 days after the effective date.

4O-day: Once an issuer has gone public, there are a number of routine filings that must be made with the SEC so there is publicly available information regarding the financial condition of that issuer. Since additional information is now available, the SEC requires that, on all issues other than IPOs, any member of the underwriting group must make available a prospectus for a period of 40 days after the effective date.

In the event that the investment bankers misgauged the marketplace, and the issue moves quite slowly, it is possible that information contained in the prospectus would be rendered obsolete by the SEC. Specifically, the SEC requires that any prospectus used more than 9 months after the effective date, may not have any financial information more than 16 months old. It can however, be amended or stickered, with updated information, as needed.

###

8

###

Syndication Among Underwriters

Because the investment banking firm may be underwriting (distributing) a rather large dollar amount of securities, to spread its risk exposure, it may form a group made up of other investment bankers or underwriters, known as a syndicate. The syndicate is headed by a syndicate manager, or lead underwriter, and it is his job to decide whether to participate in the offering. If so, the managing underwriter will sign a non-binding agreement called a letter of intent. .

If all has gone well and the market place is sufficiently interested in the security, and the SEC has been satisfied with respect to the registration statement, it is time for all parties to the offering to formalize their relationships with a contract including the basic understandings reflected in the letter of intent. Three principal underwriting contracts are involved in the usual public offering, each serving a distinct purpose. These are the: Agreement among Underwriters, Underwriting Agreement, and the Dealer Agreement.

In the Agreement Among Underwriters (AAU), the underwriters committing to a portion of the issue, enter into an agreement establishing the nature and terms of their relationship with each other. It designates the syndicate manager to act on their behalf, particularly to enter into an Underwriting Agreement with the issuer, and to conduct the offering on behalf of each of them. The AAU will designate the managing underwriter’s compensation (management fee) for managing the offering.

The authority to manage the offering includes the authority to: agree with the issuer as to the public offering price; decide when to commence the offering; modify the offering price and selling commission; control all advertising; and, control the timing and effectiveness of the registration statement by quickly responding to deficiency letters. Each underwriter agrees to purchase a portion of the underwritten securities, which is known as each under-writer’s allotment (allocation). It is normally signed severally, but not jointly, meaning each underwriter is obligated to sell his allocation but bears no financial obligation for any unsold allotment of another underwriter. This is referred to as a divided account or a Western account. Much less frequently, an undivided or Eastern account, will be used. Each underwriter is responsible for unsold allotments of others, based upon a proportionate share of the offering.

The above comments referred to firm commitment underwriting. Another type of underwriting commitment however, is known as best efforts underwriting. Under the terms of best efforts underwriting, the underwriters make no commitment to buy or sell the issue, they simply do the best they can, acting as an agent for the issuer, and having no liability to the issuer if none of the securities are sold. There is no syndicate formed with a best efforts underwriting. The investment bankers form a selling group, with each member doing his best to sell his allotment. Two variations of a best efforts underwriting are: the all-or-none, and the mini-max (part-or-none) underwriting. Under the provisions of an all-or-none offering, unless all of the shares can be distributed within a specified period of time, the offering will terminate and no subscriptions or orders will be accepted or filled. Under mini-max, unless a set minimum amount is sold, the offering will be terminated.

SEC Rule 15c2-4 requires the underwriter to set up an escrow account for any money received before the closing date, in the event that it is necessary to return the money to prospective purchasers. If the “minimum”, or the “all” contingencies are met, the monies in escrow go to the issuer with the underwriters retaining their appropriate compensation. In order to make sure that investors are properly protected, the escrow account must be maintained at a bank for the benefit of the investors until every appropriate event or contingency has occurred. Then, the funds are properly returned to the investors. If the money is to be placed into an interest bearing account, it must have a maturity date no later than the closing date of the offering, or the account must be redeemable at face with no prepayment penalty as regards principal.

Underwriter Compensation Hierarchy

As we have seen, in a firm commitment the underwriter buys the entire issue from the issuer and then attempts to resell it to the public. The price at which the syndicate offers the securities to the public is known as the public offering price. It is the price printed on the front page of the prospectus.

However, the managing underwriter pays the issuer a lower price than this for the securities. The difference between that lower price and the public offering price is known as the spread or underwriting discount. Everyone involved in the sale of a new issue is compensated by receiving part of the spread. The amount of the spread is the subject of negotiations between the issuer and the managing underwriter, but usually is within a range established by similar transactions between comparable issuers and underwriters. The spread is also subject to NASD [now FINRA] review and approval before sales may commence. The spread is broken down by the underwriters so that a portion of it is paid to the managing underwriter for finding and packaging the issue and managing the offering (usually called the manager’s fee); and a portion is retained by each underwriter (called the underwriting or syndicate allowance) to compensate the syndicate members for their expenses, use of money, and assuming the risk of the underwriting. The remaining portion is allocated to the selling group and is called selling concession. It is often useful to remember the compensation hierarchy pecking order in the following way:

Spread (syndicate manager).

Underwriters allowance (syndicate members)

Selling concession (selling group members)

Re-allowance (any other firm)

While the above deal with corporate equity, the only other significant item with respect to corporate debt is the Trust Indenture Act of 1939. This Federal law applies to public issues of debt securities in excess of $5,000,000. The thrust of this act is to require an indenture with an independent trustee (usually a bank or trust company) who will report to the holders of the debt securities on a regular basis.

Successful marketing of a new issue is a marriage between somewhat alien factors: compliance and numerous Federal, state, and self-regulatory rules and statutes; along with finely honed and profit-motivated sales techniques. It’s not too hard to see that there could be a real, or apparent, conflict of interest here. Most successful investment bankers have built their excellent reputations upon their ability to properly balance these two objectives consistently, year after year.

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on April 19, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

StubHub is an American ticket exchange and resale company. It provides services for buyers and sellers of tickets for sports, concerts, theater, and other live entertainment events. By 2015, it was the world’s largest ticket marketplace. While the company does not currently disclose its financials, in 2015 it had over 16 million unique visitors and nearly 10 million live events per month. StubHub was founded in 2000 by Eric Baker and Jeff Fluhr. The company was acquired by eBay for $310 million in 2007, and again acquired in 2020 by Viagogo.

StubHub reportedly plans to go public this summer?

According to The Information, the ticketing giant was last valued at $16.5 billion in 2021, but could still call off the public listing if it fails to land that figure.

The news comes amid a post-pandemic resurgence for live events, boosted by massive tours from Beyoncé and Taylor Swift. Though StubHub revenue jumped 40% in 2023 from the year before, it’s saddled with more than $2 billion in debt, which could test investors’ willingness to buy.

Rival ticketing service SeatGeek is also said to be mulling an IPO later this year.

Investment banking is so back. All of the biggest banks have reported their first-quarter 2024 results, and their earnings have been as good as, if not better than, expected. Higher interest rates ate into the spoils—Bank of America reported yesterday that its profit dropped 18% compared to the same period last year—but investment banking arms did well, especially since many banks increased their fees, and deal making and IPOs started to pick up again. But despite perking up, investment banking activity is still below where it used to be. Strong consumer spending also helped banks out, with credit card income rising and people and businesses continuing to need loans.

[PART 1 OF 8]

NOTE: This is an eight part ME-P series based on a weekend lecture I gave more than a decade ago to an interested group of graduate, business and medical school students. The material is a bit dated and some facts and specifics may have changed since then. But, the overall thought-leadership information of the essay remains interesting and informative. We trust you will enjoy it.

Introduction

The history, function and processes of the investment banking industry, and the rules and regulations of the securities industry and their respective markets, as well as the use of brokerage accounts, margin and debt, will be briefly reviewed in this ME-P series.

An understanding of these concepts is required of all doctors and medical professionals as they pursue a personal investment strategy.

INVESTMENT BANKING AND SECURITIES UNDERWRITING

New economy corporate events of the past several years have provided many financial signs and symptoms that indicate a creeping securitization of the for-profit healthcare industrial complex. Similarly, fixed income medical investors should understand how Federal and State regulations impact upon personal and public debt needs. For, without investment banking firms, it would be almost impossible for private industry, medical corporations and government to raise needed capital.

Introduction

When a corporation such as a physician practice management company (PPMC), or similar entity needs, to raise capital for growth or expansion, there are two methods. Raising debt or equity. If equity is used, the corporation can market securities directly to the public by contacting its current stockholders and asking them to purchase the new securities in a rights offering, by advertising or by hiring salespeople. Although this last example is somewhat exaggerated, it illustrates that there is a cost to selling new securities, which may be considerable if the firm itself undertakes the task.

For this reason, most corporations employ help in marketing new securities by using the services of investment bankers who sell new securities to the general public. Although the investment banking is an exciting and vital industry, many SEC rules regulating it are not. Nevertheless, it is important for all physician executives to understand basic concepts of the industry if raising public money is ever a possibility or anticipated goal. It is also important for individual healthcare investors to understand something about securities underwriting to reduce the likelihood of fraudulent investment schemes or ill-conceived transactions which ultimately result in monetary loss.

Fundamentals of the Investment Banking Industry

Investment bankers are not really bankers at all. The fact that the word banker appears in the name is partially responsible for the false impressions that exist in the medical community regarding the functions they perform.

For example, they are not permitted to accept deposit, provide checking accounts, or perform other activities normally construed to be commercial banking activities. An investment bank is simply a firm that specializes in helping other corporations obtain the money they need under the most advantageous terms possible.

When it comes to the actual process of having securities issued, the corporation approaches an investment banking firm, either directly, or through a competitive selection process and asks it to act as adviser and distributor. Investment bankers, or under writers, as they are sometimes called, are middlemen in the capital markets for corporate securities.

The medical corporation requiring the funds discuss the amount, type of security to be issued, price and other features of the security, as well as the cost to issuing the securities. All of these factors are negotiated in a process known as known as negotiated underwriting. If mutually acceptable terms are reached, the investment banking firm will be the middle man through which the securities are sold to the general public. Since such firms have many customers, they are able to sell new securities, without the costly search that individual corporations may require to sell its own security. Thus, although the firm in need of additional capital must pay for the service, it is usually able to raise the additional capital at less expense through the use of an investment banker, than by selling the securities itself.

The agreement between the investment banker and the corporation may be one of two types. The investment bank may agree to purchase, or underwrite, the entire issue of securities and to re-offer them to the general public. This is known as a firm commitment.

When an investment banker agrees to underwrite such a sale, it agrees to supply the corporation with a specified amount of money. The firm buys the securities with the intention to resell them. If it fails to sell the securities, the investment banker must still pay the agreed upon sum. Thus, the risk of selling rests with the underwriter and not with the company issuing the securities.

The alternative agreement is a best efforts agreement in which the investment banker makes his best effort to sell the securities acting on behalf of the issuer, but does not guarantee a specified amount of money will be raised.

When a corporation raises new capital through a public offering of stock, on might inquire from where does the stock come? The only source the corporation has is authorized, but previously un-issued stock. Anytime authorized, but previously un-issued stock (new stock) is issued to the public, it is known as a primary offering. If it’s the very first time the corporation is making the offering, it’s also known as the Initial Public Offering (IPO). Anytime there is a primary offering of stock, the issuing corporation is raising additional equity capital.

A secondary offering, or distribution, on the other hand, is defied as an offering of a large block of outstanding stock. Most frequently, a secondary offering is the sale of a large block of stock owned by one or more stockholders. It is stock that has previously been issued and is now being re-sold by investors. Another case would be when a corporation re-sells its treasury stock.

Prior to any further discussions of investment banking, there are several industry terms that’s should be defined.

For example, an agent buys or sells securities for the account and risk of another party, and charges a commission. In the securities business, the terms broker and agent are used synonymously. This is not true of the insurance industry.

On the other hand, a principal is one who acts as a dealer rather than an agent or broker. A dealer buys and sells for his own account Finally, the dealer makes money by buying at one price and selling at a higher price. Thus, it is easy to understand how an investment banking firm earns money handling a best efforts offering; they make a commission on every share they sell.

The Securities Act of 1933 (Act of Full Disclosure)

When a corporation makes a public offering of its stock, it is bound by the provisions of the Securities Act of 1933, which is also known as the Act of Full Disclosure. The primary requirement of the Act is that the corporation must file a registration statement (full disclosure) with the Securities and Exchange Commission (SEC); containing some of the following items:

Description of the business entity raising the money.

Biographical data regarding officers and directors of the issuer.

Listing of share holdings of officers, directors, and holders of more than 10% of the issuer’s securities (insiders).

Financial statements including a breakdown of existing capitalization (existing debt and equity structure).

Intended use of offering proceeds.

Legal proceedings involving the issuer, such as suits, antitrust actions or strikes.

Acting in its capacity as an adviser to the corporation, the investment banking firm files out the registration statement with the SEC. It then takes the SEC a period of time to review the information in the registration statement. This is the “cooling off period” and the issue is said to be “in registration” during this time. When the Act written in 1933, Congress thought that 20 days would be enough time from the filing date, until the effective date the sale of securities is permitted.

In reality, it frequently takes much longer than 20 days for the SEC to complete its review. But, regardless of how long it lasts, it’s known as the cooling off period. At the end of the cooling off period, the SEC will either accept the issue or they will send a letter back to the issuer, and the underwriter, explaining that there is incomplete information in the registration statement. This letter is known as a deficiency letter. It will postpone the effectiveness of the registration statement until the deficiency is remedied. Even if initially, or eventually approved, an effective registration does not mean that the SEC has approved the issue.

For example, the following well known disclaimer statement written in bold red ink, is required to be placed in capital letters on the front cover page of every prospectus:

###

THESE SECURITIES HAVE NOT BEEN APPROVED OR DISAPPROVED BY THE SECURITIES AND EXCHANGE COMMISSION NOR HAS THE COMMISSION PASSED UPON THE ACCURACY OR ADEQUACY OF THIS PROSPECTUS. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

###

During the cooling off period, the investment bank tries to create interest in the market place for the issue. In order to do that, it distributes a preliminary prospectus, more commonly known as a “red herring”. It is known as a red herring because of the red lettering on the front page. The statement on the very top with the date is printed in red as well as the statements on the left hand margin of the preliminary prospectus.

The cost of printing the red herring is borne by the investment bank, since they are trying to market it.. The red herring includes information from the registration statement that will be most helpful for potential medical investors trying to make a decision. It describes the company and the securities to be issued; includes the firm’s financial statements; its current activities; the regulatory bodies to which it is subject; the nature of its competition; the management of the corporation, and what the expected proceeds will be used for. Two very important items missing from the red herringare the public offering price and the effective date of the issue, as neither are known for certain at this point in time.

The public offering price is generally determined on the date that the securities become effective for sale (effective date). Waiting until the last minute enables the investment bankers to price the new issue in line with current market conditions. Since the investment banker uses the red herring to try to create interest in the market place, stock brokers [aka: Registered Representatives (RRs) with a Series # 7 general securities license – After a 2 hour multiple-choice computerize test, I held this license for a decade ) will send copies of the red herring to their clients for whom they feel the issue is a suitable investment. The SEC is very strict on what can be said about an issue, in registration.

In fact, during the pre-filing period (the time when the negotiations are going on between the issuer\and underwriter), absolutely nothing can be said about it to anyone. For example, if the regulators find out that your stock broker discussed with you the fact that his firm was negotiating with an issuer for a possible public offering, he could be fined, or jailed.

During the cooling off period (the time when the red herring is being distributed), nothing may be sent to you; not a research report, nor a recommendation from another firm, or even the sales literature. The only thing you are permitted to receive is the red herring. The red herring is used to acquaint prospects with essential information about the offering. If you are interested in purchasing the security, then you will receive an “indication of interest”, but you can still not make a purchase or send money.

No sales may be made until the effective date; all that can be used to generate interest is the red herring.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES

Private equity and venture capital investments typically involve ownership of shares in a company and represent title to a portion of the company’s future earnings. However, private equity is an equity interest in a company or venture whose stock is not yet traded on a stock exchange.

Venture capital is typically a special case of private equity in which the investment is in a company or venture that has little financial history or is embarking on a high risk/high potential reward business strategy.

Like real estate, private equity and venture capital investments generally share a general lack of liquidity and a lack of comparability across different individual investments. The lack of liquidity comes from the fact that private equity and venture capital investments are typically not tradable on a stock exchange until the company has an IPO.

The lack of comparability is due to the fact that most private equity and venture capital investments are the result of direct negotiation between the investor/venture capitalist and the existing owners of the company /venture.

With widely divergent terms and provisions across different investments, it is difficult to make general claims regarding the characteristics of private equity and venture capital investments.

Posted on February 26, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

On Tuesday, February 20th, the S&P Dow Jones Indices, which oversees additions and subtractions to the highly followed Dow Jones Industrial Average, announced that, as of the start of trading on Monday, February, 26th pharmacy chain Walgreens Boots Alliance (NASDAQ: WBA) would be getting the literal boot.

Meanwhile, e-commerce kingpinAmazon (NASDAQ: AMZN) will be taking its place.

And, Redditfiled to go public last week in an IPO that will resemble the platform itself—unusual, chaotic, and reliant on its opinionated users. Planned for next month, Reddit’s public listing will be the first social media IPO since Pinterest in 2019 and the first major tech IPO of the year.

Posted on January 20, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Drugmakers kicked off 2024 by raising the list prices for Ozempic, Mounjaro and dozens of other widely used medicines. Companies including Novo Nordisk, the maker of Ozempic, and Eli Lilly, which sells Mounjaro, raised list prices on 775 brand-name drugs during the first half of January 2024, according to an analysis for The Wall Street Journal by 46brooklyn Research, a nonprofit drug-pricing analytics group.

The drugmakers raised prices of their medicines by a median 4.5%, though the prices of some drugs rose by around 10% or higher, according to the research group. The median increase is higher than the rate of inflation, which ticked up to 3.4% in December.

***

Reddit’s IPO is reportedly due in March. According to Reuters, the social media platform’s long-awaited initial public offering will launch by the end of March after it makes its public filing in late February. It’ll be the first big social media IPO since 2019, when Pinterest went public. All eyes will fall on Reddit’s own users, who are known to fuel meme stock rallies—namely AMC and GameStop—and could help prop up the company’s debut on the stock market. Valued at about $10 billion as of 2021, Reddit reportedly will sell 10% of its shares as it competes with TikTok and Facebook for attention and ad dollars.

Here’s where the major benchmarks ended:

The S&P 500 index rose 58.87 points (1.2%) to 4,839.81, up 1.2% for the week; the Dow Jones Industrial Average gained 395.19 points (1.1%) to 37,863.80, up 0.7% for the week; the NASDAQ Composite® (COMP) increased 255.32 points (1.7%) to a two-year high of 15,310.97, up 2.3% for the week.

The 10-year Treasury note yield (TNX) fell about 1 basis point to 4.132%.

The CBOE Volatility Index® (VIX) fell 0.83 to 13.30.

Strength in Nvidia and other chipmakers like Advance Micro Devices (AMD), which surged 6%, lifted the Philadelphia Semiconductor Index (SOX) 4% to a record high close. Regional banks were also among the market’s strongest performers, as the KBW Regional Banking Index (KRX) added nearly 2%. Food and beverage companies and utilities were among the weakest performers.

Markets: The Magnificent Seven technology mega-cap stocks—Microsoft, Apple, Alphabet, Nvidia, Tesla, Meta, and Amazon—have surged 75% this year, while the other 493 companies in the S&P 500 have gained 12%. The Magnificent Seven now account for nearly 30% of the entire index’s value, per the WSJ.

Stock spotlight: Speaking of the S&P 500, it’s getting a prominent new member—Uber will join the index today. With a market cap of $127 billion, Uber is the most valuable company that hadn’t yet been included in the S&P 500, and it celebrated by notching a 52-week high last week.

Posted on November 7, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

WeWork = Did Not Work!

By Staff Reporters

***

***

WeWork, the coworking company just filed for Chapter 11 bankruptcy protection in New Jersey after years of struggles that began with a failed IPO in 2019. It aborted the IPO after investors got a look at its finances and just how much power WeWork’s eccentric founder Adam Neumann possessed.

In 2019, the company was valued at $47 billion, but it has since fallen steadily, and this year, its stock has plunged by 98%, giving it a ~$45 million value as of last week.

The markets are down again and stocks continued their September slump with tech companies getting hit especially hard as investors fretted about another possible Fed rate hike because of data showing prices for manufacturing and services trending upward. It was a mixed bag for the meme stock faithful, with AMC hitting an all-time low after releasing a plan to sell new shares and GameStop rising after-hours thanks to better-than-expected sales last quarter.

This all may demonstrate that private companies looking to fund growth in this high-interest rate environment are facing a tough time raising capital amidst falling valuations, according to a new Deloitte survey.

The problem is particularly acute for smaller companies. Many of the companies challenged by capital raising saw themselves putting out the “For Sale” sign within the next six months, which could lead to an M&A boom later this year.

“The No. 1 largest factor that people saw as a challenge or a barrier was a decrease in valuations of their business,” Wolfe Tone, vice chair and US and Global Deloitte Private leader, told CFO Brew. “Clearly, increasing interest rates and pricing was closely behind that. Liquidity challenges not far behind that.”

Private companies have been looking to raise capital to fund a range of growth initiatives; meeting talent needs and expanding tech capabilities are at the top of the list, Tone said. Not far behind was “increasing productivity and improving cost structures.”

Posted on October 2, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

The stock markets ended Q3 last week with a whimper despite new data showing that the Fed’s favorite CPI inflation measure cooled in August. September was the worst month of the year for the S&P 500 and the NASDAQ. But Blue Apron soared on the news that it’s being bought by Wonder Group, a food delivery startup helmed by a former Walmart exec.

America’s debt today stands at $33 trillion, a figure some politicians, finance mavens and everyday citizens find astonishingly high.

***

Carmot Therapeutics, which is developing drugs for diabetes and weight-loss, is reportedly mulling an IPO or possible sale to a large pharmaceutical company at a valuation of at least $1B. The biotech company has two injectable GLP-1 drug candidates in Phase 2 development for type 1 and type 2 diabetes, according to the company’s website.