BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on November 12, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The SPX rose 5.81 points (0.10%) to 6,001.35; the Dow Jones Industrial Average® ($DJI) added 304.14 points (0.69%) to 44,293.13, a new all-time closing high; and the NASDAQ Composite®($COMP) gained 11.99 points (0.06%) to 19,298.76.

The 10-year Treasury note yield (TNX) didn’t trade today due to the Veterans Day holiday.

The CBOE Volatility Index® (VIX) inched up to 15.05.

Posted on November 11, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

On September 28th, 2024, California Governor Gavin Newsom vetoed Assembly Bill (AB) 3129, which sought to regulate private equity (PE) transactions involving healthcare organizations by requiring certain transactions to be reviewed by, and to receive approval from, the California Attorney General (AG).

In his veto message, Governor Newsom stated that the state’s Office of Health Care Affordability (OHCA), established in 2022, has the power to review and evaluate healthcare transactions (including the ones at issue in AB 3129). While OHCA does not have the power to block proposed transactions, as the AG would have had under AB 3129, it can refer transactions to the AG for further examination. Put simply, the governor’s veto seems to stem from concern that taking power away from the newly-created OHCA could muddy the waters in healthcare transaction regulation.

While there is a possibility that the California legislature could override Governor Newsom’s veto, it appears unlikely as of the publication of this Alert. However, the overall popularity of this bill in the legislature (as evidenced by the fairly wide margins with which it passed) indicates that PE groups looking to transact in the healthcare space – both in California and across the U.S. – should be on high alert, as regulators are increasingly turning their focus on the role of PE in healthcare.

Derivatives are securities whose performance and/or structure is derived from the performance and/or structure of other assets, interest rates, or indexes. If used moderately and in appropriate situations, derivatives can help stabilize portfolios and/or enhance returns. However, if used in excess and/or in inappropriate circumstances, they can be harmful, potentially causing portfolio instability and/or losses. Derivatives are similar to medicine in their behavior–usually safe when used as directed, potentially toxic when abused.

There are many different types of derivative securities and many different ways to use them. Some derivative securities, such as mortgage-related and other asset-backed securities, are in many respects like any other investment, although they may be more volatile or less liquid than more traditional debt securities.

Futures and options are commonly used for traditional hedging purposes to attempt to protect portfolios from exposure to changing interest rates, securities prices or currency exchange rates, and for cash management purposes as a low-cost method of gaining exposure to a particular securities market without investing directly in those securities.

Certain other derivative securities may be described as structured investments. A structured investment is a security whose value or performance is linked to an underlying index or other security or asset class. Structured investments include collateralized mortgage obligations (CMOs). Structured investments also include securities backed by other types of collateral.

Currency Hedging is a risk-management strategy, as part of a foreign investment strategy, currency hedging is designed to reduce the impact from changes in the relative values of currencies involved in the foreign investment strategy.

In any foreign investment strategy, a significant part of the potential risk and return comes from exposure to relative currency value fluctuations. If exposure to those currency fluctuations is minimized, investors can experience more of a “pure play” exposure to the foreign investments. There is a variety of possible currency hedging strategies, ranging from swaps, options, and spot contracts to simply buying foreign currencies.

Currency Overlay is a financial trading strategy used to separate the management of currency risk from other portfolio strategies. A currency overlay manager can seek to hedge the risk from adverse movements in exchange rates, and/or attempt to profit from tactical currency views.

Posted on November 8, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The Federal Reserve cut interest rates by 0.25 percentage points Thursday, the second consecutive cut after a two-year rate-hike run to curb post-pandemic inflation.

Lyft announced impressive earnings results thanks to more commuters using the ride-hailing service, as well as upbeat guidance for the future. Shares rose 22.92%.

Shareholders worried about a housing market slowdown hurting Zillow had nothing to fear: The real estate website crushed earnings estimates, and shares popped 23.77%.

Warner Bros. Discovery enjoyed its biggest single-quarter surge in subscribers ever thanks to streaming service Max, which sent shares soaring 11.81%.

UnderArmour rocketed 23.33% higher after its cost-savings plan paid off last quarter and management guided for a strong quarter ahead.

Planet Fitness surprised shareholders with a solid quarter for the gym giant, as well as forecasts of more growth ahead. Shares climbed 11.26%.

Prison operators GEOGroup and CoreCivic both surged on Trump’s election, and their rally continued today—in-spite of very different paths forward for each stock. GEO Group gained 13.63%, while CoreCivic rose 25.60%.

What’s down

Trump Media & Technology Group was one of the biggest winners on election night, and although the stock soared over the last few days, investors decided to take profits today. Shares sank 22.97%.

Wolfspeed plummeted 39.24% after announcing larger-than-expected losses last quarter, poor forecasts for next quarter, and layoffs to cut costs.

Match Group shareholders were heartbroken to hear that Tinder’s revenue fell last quarter, though strong revenue growth from Hinge helped ease the pain. Shares dropped 17.87%.

Virgin Galactic isn’t just a mean nickname from your high school years—it’s also a space stock that can’t make money to save its life. Shares fell 11.87%.

The S&P 500®index (SPX) rose 44.06 points (0.74%) to 5,973.10; the Dow Jones Industrial Average® ($DJI) fell 0.59 points (0.00%) to 43,729.34; and the NASDAQ Composite®($COMP) gained 285.99 points (1.51%) to 19,269.46.

The 10-year Treasury note yield (TNX) fell nine basis points to 4.34%, with most of the drop coming long before the Fed decision.

The CBOE Volatility Index® (VIX) continued its post-election plunge to 15.21.

Stocks surged and stayed higher all yesterday day on news of Donald Trump’s presidential victory. The Dow rocketed over 1,350 points as soon as markets opened, and all three indexes ended the day at record highs.

Treasuryyields have paralleled Trump’s chances of taking the White House for the last few weeks, and his election sent them soaring to over 4.46% at one point today.

Oil and gold both fell as the dollar rose after Trump’s win. The greenback popped on the promise of Trump’s protectionist tariff policies and the lower likelihood of the Fed cutting interest rates as fast as previously expected.

Bitcoin surged as traders celebrated the beginning of the new, friendlier regulatory environment that Trump promised during his campaign.

Retained Earnings Risk: Profits generated by a company that are not distributed to stockholders as dividends. Instead, they are either reinvested in the business or kept as a reserve for specific objectives, such as paying off debt or purchasing equipment. Retained earnings risks are also called “undistributed profits,” “undistributed earnings,” or “earned surplus.”

Risk-Weighted (or risk-adjusted) Assets: Within the context of measuring the financial stability of banks and other financial institutions, the risk-weighted assets figure is an aggregate of a financial institution’s assets (usually loans to its customers) after the loans have been individually adjusted for their risk. This involves multiplying each loan by a factor that reflects its risk. Low-risk loans are multiplied by a low number, high-risk by high. The aggregate number can then be used to calculate the financial institution’s capital ratio. Lower risk-weighted assets typically result in higher capital ratios, and higher risk-weighted assets usually translate to lower capital ratios.

Sequence-of-Returns Risk: The risk of market conditions impacting the overall returns of an investment portfolio during the period when a retiree is first starting to withdrawal money from investments as income. For example, if a retiree has to withdrawal income from his or her portfolio when market prices are depressed, the portfolio may lose out on the potential returns that income could have made once market prices recovered.

Posted on November 6, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

First-time homebuyers in 2024 had a median income of $97,000, and their median age was 38. OpenAI and Jeff Bezos invested in Physical Intelligence, a robot startup with the aim of “bringing general-purpose AI into the physical world.”

Cybersecurity darling Palantir soared 23.38% to a record high thanks to strong earnings, high AI demand, and big spending from the Department of Defense.

Astera Labs skyrocketed 37.70% after the semiconductor parts maker (and one of Nvidia’s key suppliers) announced strong earnings.

Crypto stocks had a great day thanks to a widespread cryptocurrency rally. Coinbase rose 4.13%, MicroStrategy gained 2.16%, and RiotPlatforms jumped 8.13%.

Stocks Down

Trump Media & Technology Grouparrested its recent downturn and popped 12% at one point today, but gave all those gains up and ended the day down 1.16%.

You’d think the end of a multi-week labor dispute costing billions of dollars would be a relief for shareholders, but Boeing still sank 2.62% on news that it’s reached an agreement with striking machinists.

It’s a me, lower revenue forecasts! Nintendo fell 1.68% after announcing that sales of its Switch console are starting to sag.

Some of the smaller semiconductor stocks on the market took a beating today. NXP Semiconductor dropped 5.17% after announcing weaker-than-expected Q4 guidance, Lattice Semiconductor tumbled 1.37% after missing on sales forecasts and announcing job cuts, and while Cirrus Logic beat expectations this quarter, it still fell 7.09% on lower forecasts.

The S&P 500®index (SPX) rose 70.07 points (1.23%) to 5,782.76; the Dow Jones Industrial Average® ($DJI) added 427.28 points (1.02%) to 42,221.88; and the NASDAQ Composite®($COMP) increased 259.19 points (1.43%) to 18,439.17.

The 10-year Treasury note yield (TNX) dropped two basis points to 4.29%.

The CBOE Volatility Index® (VIX) slipped to 20.72.

Posted on November 5, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Among consideration for CVS is splitting up its assets: CVS Pharmacy, pharmacy benefit managerCVS Caremark, and insurance arm Aetna. The company has reportedly been in talks with bankers about the move, Reuters reported early this month.

Just as Nvidia will replace Intel, Sherwin Williamswill replaceDow Inc. on the Dow (how embarrassing, getting kicked off an index you share a name with). Sherwin Williams popped 4.59%, while Dow Inc. fell 2.08%.

Peloton pedaled 3.59% higher on a double upgrade from Bank of America analysts, who like the bike company’s higher profit outlook and hiring of new CEO Peter Stern from Ford.

Yum! China, the company that operates Pizza Hut and KFC restaurants in China, climbed 7.12% after announcing that new store openings translated into better-than-expected revenue and earnings last quarter.

STOCKS DOWN

Nuclear energy stocks took a big hit today after the Federal Energy Regulatory Commission ruled that Talen Energycould not increase the amount of energy its nuclear plant in Susquehanna, PA, produces in order to power an Amazon data center. Talen fell 2.23%, Vistra Corp sank 3.18%, and Constellation Energy plummeted 12.46%.

Clinical data from a Viking Therapeutics trial shows its weight-loss pill is effective. Shares soared then sank 13.36% as investors took profits.

The S&P 500®index (SPX) dipped 16.11 points (–0.28%) to 5,712.69; the $DJI dropped 257.59 points (–0.61%) to 41,794.60; and the $COMP lost 59.93 points (–0.33%) to 18,179.98.

The 10-year Treasury note yield (TNX) fell five basis points to 4.31%.

The CBOE Volatility Index® (VIX)edged up to 22.11, still below last week’s peaks.

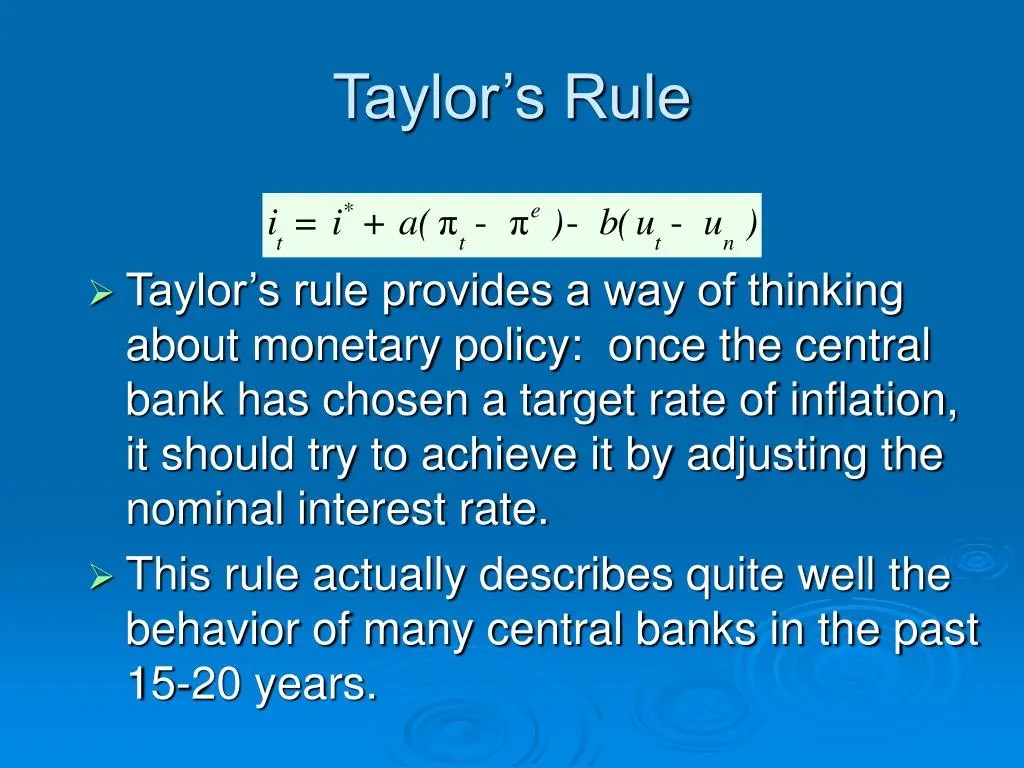

Named for a U.S. economist, the JB Taylor Rule is a mathematical monetary-policy formula that recommends how much a central bank should change its nominal short-term interest rate target (such as the U.S. Federal Reserve’s federal funds rate target) in response to changes in economic conditions, particularly inflation and economic growth. It’s typically viewed as guideline for raising short-term interest rates as inflation and potentially inflationary pressures increase. The rule recommends a relatively high interest rate (“tight” monetary policy) when inflation is above its target or when the economy is above its full employment level, and a relatively low interest rate (“easy” monetary policy) under the opposite conditions.

To illustrate, the monetary policy of the FOMC, changed throughout the 20th century. The period between the 1960s and the 1970s is evaluated by Taylor and others as a period of poor monetary policy; the later years typically characterized as stagflation. The inflation rate was high and increasing, while interest rates were kept low. Since the mid-1970s monetary targets have been used in many countries as a means to target inflation.

However, in the 2000s the actual interest rate in advanced economics, notably in the US, was kept below the value suggested by the Taylor rule.

HFRI: Fund of Funds invests with multiple managers through funds or managed accounts. The strategy designs a diversified portfolio of managers with the objective of significantly lowering the risk (volatility) of investing with an individual manager.

The Fund of Funds manager may allocate funds to numerous managers within a single strategy, or with numerous managers in multiple strategies. The investor has the advantage of diversification among managers and styles with significantly less capital than investing with separate managers.

Posted on November 2, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Ford paused production of its F-150 Lightning electric truck from mid-November to early January as demand for the once-coveted EV dwindles.

Peloton named Peter Stern, the co-founder of Apple Fitness+, as its next CEO.

Starbucksis bringing back Sharpied names on cups for the first time in four years as new CEO Brian Niccol tries to shake up the struggling coffee chain.

Boeing offered striking machinists yet another new contract offer, including a 38% pay raise over the next four years. The union will vote on the contract on Monday. Shares climbed 3.54%.

Avis Budget motored 10.92% higher despite missing forecasts on both earnings and revenue. Shareholders celebrated the rental car company’s strong growth expectations from management and took advantage of a cheap valuation.

Globalstar rocketed 32.38% after the satellite communications company announced an expanded deal with Apple.

Charter Communications soared 11.87% after losing fewer subscribers than expected, which is like a back-handed compliment in the investing world.

STOCKS DOWN

Trump Media & Technology Group remains on the roller coaster, falling another 13.53% today as early exit polls show Vice President Kamala Harris with a lead in several key states.

Wayfair may have met earnings expectations last quarter, but the online home goods retailer also lost customers and fulfilled fewer orders. Shares fell 6.26%.

Super Micro Computer continued to sell off after the resignation of its financial auditor, an almost-sure sign of fraud. Shares sank another 10.51%.

The S&P 500®index (SPX) rose 23.35 (0.41%) to 5,728.80 to end the week down 1.37%; the Dow Jones Industrial Average® ($DJI) added 288.73 points (0.69%) to 42,052.19 to end the week down 0.15%; and the NASDAQ Composite®($COMP) gained 144.76 points (0.80%) to 18,239.92 to end the week down 1.50%.

The 10-year Treasury note yield (TNX) climbed eight points to 4.36%, the highest since early July.

The CBOE Volatility Index® (VIX)remained elevated at 21.88.

Posted on November 1, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Comcast popped 3.39% on the news that it is exploring a separation of its cable business. The network operator got a boost this quarter from the Olympics, but still lost 365,000 cable TV customers.

Peloton Interactive pedaled 27.82% higher after the bike maker beat earnings expectations and introduced a new CEO.

Carvana accelerated 19.23% on an impressive beat-and-raise earnings report that caps off the car seller’s incredible comeback.

Booking Holdings, owner of Kayak and Priceline, hit a record high after the travel company reported shockingly strong earnings. Shares rose 4.76%

What was down

Trading in shares of Trump Media & Technology Group was halted yet again today after the meme stock sank dramatically to start the day. Shares ended the trading session down 11.72%.

Estee Lauder plummeted 20.84% on a triple whammy of bad news: The cosmetics retailer missed earnings estimates, pulled its forecast, AND cut its dividend. Ouch.

Super Micro Computer continued to tumble today, declining another 11.97% as the fallout from the resignation of its financial auditor raises the threat of the semiconductor stock getting delisted from the Nasdaq.

eBay sank 8.18% after beating earnings expectations but issuing disappointing earnings guidance heading into the holiday season.

The SPX fell 108.22 (–1.86%) to 5,705.45; the Dow Jones Industrial Average® ($DJI) dropped 378.08 points (–0.90%) to 41,763.46; and the NASDAQ Composite®($COMP) lost 512.78 points (–2.76%) to 18,095.15 and has now fallen in two of the last four months.

The 10-year Treasury note yield (TNX) added two basis points to 4.28%.

The VIX rose to 22.6, the highest since October 8.

What Is CREDIT? Credit is a contractual agreement in which a borrower receives a sum of money or something else of value and commits to repaying the lender later, typically with interest. Credit is also the creditworthiness or credit history of an individual or a company. Good credit tells lenders you have a history of reliably repaying what you owe on loans. Establishing good credit is essential to getting a loan.

***

Credit Analysis is a form of financial analysis used primarily to determine the financial strength of the issuer of a security, and the ability of that issuer to provide timely payment of interest and principal to investors in the issuer’s debt securities. Credit analysis is typically an important component of security analysis and selection in credit-sensitive bond sectors such as the corporate bond market and the municipal bond market.

Credit Default Swap Index (CDX) is a credit derivative, based on a basket of CDS, which can be used to hedge credit risk or speculate on changes in credit quality.

Credit Default Swaps (CDS) are credit derivative contracts between two counter parties that can be used to hedge credit risk or speculate on changes in the credit quality of a corporation or government entity.

Credit Quality reflects the financial strength of the issuer of a security, and the ability of that issuer to provide timely payment of interest and principal to investors in the issuer’s securities. Common measurements of credit quality include the credit ratings provided by credit rating agencies such as Standard & Poor’s and Moody’s. Credit quality and credit quality perceptions are a key component of the daily market pricing of fixed-income securities, along with maturity, inflation expectations and interest rate levels.

Credit Rating Agency (CRA) is a company that assigns credit ratings for issuers of certain types of debt obligations as well as the debt instruments themselves. In the United States, the Securities and Exchange Commission (SEC) permits investment banks and broker-dealers to use credit ratings from “Nationally Recognized Statistical Rating Organizations” (NRSRO) for similar purposes. As of January 2012, nine organizations were designated as NRSROs, including the “Big Three” which are Standard and Poor’s, Moody’s Investor Services and Fitch Ratings.

A Credit Rating Downgrade by a credit rating agency (such as Standard & Poor’s, Moody’s or Fitch), of reducing its credit rating for a debt issuer and/or security. This is based on the agency’s evaluation, indicating, to the agency, a decline in the issuer’s financial stability, increasing the possibility of default (defined below). A downgrade should not to be confused with a default; a debt security can be downgraded without defaulting. (And, conversely, a debt issuer can suddenly default without being downgraded first–credit ratings and credit rating agencies are not infallible.)

Credit Ratings are measurements of credit quality provided by credit rating agencies). Those provided by Standard & Poor’s typically are the most widely quoted and distributed, and range from AAA (highest quality; perceived as least likely to default) down to D (in default). Securities and issuers rated AAA to BBB are considered/perceived to be “investment-grade”; those below BBB are considered/perceived to be non-investment-grade or more speculative.

Credit Risk is the risk that the inability or perceived inability of the issuers of debt securities to make interest and principal payments will cause the value of those securities to decrease. Changes in the credit ratings of debt securities could have a similar effect.

Credit Risk Transfer Securities (CRTS) are the unsecured obligations of the GSEs (Government Sponsored Enterprises). Although cash flows are linked to prepays and defaults of the reference mortgage loans, the securities are unsecured loans, backed by general credit rather than by specified assets.

Posted on October 30, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Trump Media & Technology Group rocketed higher at the opening bell, prompting the Nasdaq to halt trading on what has quickly become the meme stock du jour. Shares ended the day 8.76% higher.

23andMe clawed 1.86% higher after introducing three new board members about a month after the entire board resigned.

VF Corp, parent company of clothing brands JanSport, Vans, and North Face, surged 27.01% thanks to an impeccable earnings report that revealed its turnaround plans are coming to fruition.

Trex, the stuff your dad built an awesome deck out of, saw sales fall last quarter but still managed to beat earnings expectations. Shares popped 6.19%.

STOCKS DOWN

JetBlue Airways sank 17.08% in spite of reporting a smaller loss than analysts expected. The problem is all the turbulence that lies ahead.

D.R. Horton is the largest homebuilder by market cap, so when it says that 2025 will be a bad year, investors should listen. Shares dropped 7.29% on the news.

Crocs stumbled 19.17% after beating earnings but announcing that its fiscal year would be bogged down by poor sales of its HeyDude shoe brand.

Stanley Black & Decker fell 8.77% after missing on both profits and sales, citing weaker consumer spending.

Xerox plummeted 17.41% after the company that can’t make a printer that works for longer than 3 months without needing a new ink cartridge announced weaker sales than expected.

The S&P 500® index (SPX) rose 9.40(0.16%) to 5,832.92; the Dow Jones Industrial Average® ($DJI) fell 154.52 points (–0.36%) to 42,233.05; and the $COMP added points 145.55 (0.78%) to 18,712.75.

The 10-year Treasury note yield (TNX) finished unchanged at 4.27% after reaching nearly 4.34% earlier today.

Posted on October 29, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Healthcare’s future as HSBC Innovation Banking collaborated with LINUS and HLTH to help prepare the healthcare ecosystem for the future. The Health 2035 report goes in depth with discussions between visionaries in the ecosystem and studies of young physicians’ forecasts for what the state of care will be in the year 2035. Download the report.

Trump Media & Technology Group soared 21.59% following a major rally at Madison Square Garden, an appearance on Joe Rogan’s podcast, and rising chances of winning the election. Fun fact: After this latest stock surge, Trump Media is now worth almost as much as social media network X.

Nio surged 10.46% thanks to an upgrade from Macquerie, whose analysts believe that the EV startup could see strong growth from new vehicle launches next year.

Spotify has earned a spot on Wells Fargo’s top pick playlist, with analysts confident the stock could rise over 20%. Shares rose 1.27%.

Lower oil prices hurt energy stock, but are a big boost for companies that spend a lot on fuel. CarnivalCorp rose 4.83%, RoyalCaribbeanCruises climbed 1.35%, and AmericanAirlines popped 3.42%.

Stocks Down

Philips floundered 15.95% after the Dutch consumer goods manufacturer missed on earnings and lowered its full-year forecast.

Boeing continued to fall yet another 2.79%, this time on the news that it is raising $19 billion through a stock offering in the hopes that it fends off a credit rating downgrade.

Oil stocks took a beating thanks to a big decline for crude prices. DiamondbackEnergy fell 3.36%, APACorp. dropped 4.51%, ExxonMobil sank 0.49%, and BP lost 1.48%.

The S&P 500® index (SPX)rose15.40points (0.27%) to 5,823.52; the Dow Jones Industrial Average® ($DJI) added 273.17 points (0.65%) to 42,387.57; and the NASDAQ Composite® ($COMP) gained 48.58 points (0.26%) to 18,567.19.

The 10-year Treasury note yield (TNX) climbed six basis points to 4.29%, the highest close since July 9.

Posted on October 27, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Vitaliy Katenselson CFA

***

***

Today, we’re diving into two thought-provoking questions:

1. What’s a famous investment rule I don’t agree with? 2. Which key characteristics should a good investor have?

1. A Famous Investment Rule I Don’t Agree With: “Buy and Hold”

Buy and hold becomes a religion during bull markets. Then, holding a stock because you bought it is often rewarded through higher and higher valuations. There’s a Pavlovian bull market reinforcement – every time you don’t sell (hold) a stock, it goes higher.

Buying is a decision. So is holding, but it should not be a religion but a decision. The value of any company is the present value of its cash flows. When the present value of cash flows (per share) is less than the price of the stock, the stock should not be “held” but sold.

WarrenBuffett is looked upon as the deity of buy and hold.

Look at Coca Cola when it hit $40 in 1999. Its earnings power at the time was about $0.80. It was trading at 50 times earnings. It was significantly overvalued, considering that most of the growth for this company was in the past.

Fast-forward almost a quarter of a century – literally a generation. Today the stock is at $60. It took more than a decade to reclaim its 1999 high. Today, Coke’s earnings power is around $1.50–1.90. Earnings have stagnated for over a decade. If you did not sell the stock in 1999, you collected some dividends, not a lot but some. The stock is still trading at 30–40x earnings. Unless they discover that Coke cures diabetes (not causes it), its earnings will not move much. It’s a mature business with significant health headwinds against it.

“Long-term” and “buy-and-hold” investing are often confused.

People should not own stocks unless they have a long-term time horizon. Long-term investing is an attitude, an analytical approach. When you build a discounted cash flow model, you are looking decades ahead. However, this doesn’t mean that you should stop analyzing the company’s valuation and fundamentals after you buy the stock, as they may change and affect your expected return. After you put in a lot of analytical work and buy the stock, you should not simply switch off your brain and become a mindless buy-and-hold investor.

This doesn’t mean you shouldn’t be patient, which I’ll discuss next; but holding, not selling, a stock is a decision.

2. Key Characteristics of a Good Investor

I’m going to sound a bit more preachy than usual, but it’s very difficult to answer this question in any other way.

You need three Ps – passion, patience, process.

Passion

Investing is not a 9-to-5 job; it’s a 24/7 adventure. Unlike flipping burgers or processing insurance claims, where you can clock in at 9 AM, fall into a stupor, and then reawaken at 5 PM when you clock out.

This should be your test: If you catch yourself treating investing as a 9-to-5 job, then you have little passion for it.

If this is the case, don’t do it (this probably applies to any choice of a profession). You don’t stand a chance against people for whom investing is a never-ending puzzle to be solved on their life’s journey. All of my investment friends are dripping with passion for investing; they are obsessed with it. None of them are in it only for the money.

You won’t last long in this profession if you’re not passionate about stocks. Patience

Investing is like real life – the connection between effort and result is nonlinear. It is very loose.

You may be making all of the right rational decisions: You are buying stocks that lie within your EQ/IQ spectrum, and they are significantly undervalued, but the market simply doesn’t care. It just keeps sending your stocks down. To make things even more frustrating, while your stocks are declining, speculators who treat the stock market as a craps table at Caesars Palace are killing it, making money hand over fist. It’s painful. It is excruciatingly painful if you have the wrong client base.

This is where patience comes in. My father told me this story, which happened right before I was born.

My family lived in Murmansk, a city 125 miles north of the Arctic Circle in northwest Russia. My mom went to give birth to my brothers and me in Saratov, a city in central Russia, about 1200 miles from Murmansk. She wanted to be closer to her parents. My father could not leave work, so he stayed in Murmansk.

A few weeks before I was born, he went to visit his best friend, Alexander. He told him that he was worried about my mom and the birth. His friend told him something that I remember to this day (with a chuckle): “Naum, you did your part; you cannot go back and correct what you did. Now you just have to wait.”

Investing is patience punctuated by decisions.

As the French mathematician Blaise Pascal said, “All of humanity’s problems stem from man’s inability to sit quietly in a room alone.”

One more thought here: I try to take the temperature of my emotions and the mental activity of my brain. When I find myself overheating, with the stock market occupying my entire brain, I forcibly disconnect and unplug myself from it. The quality of my thoughts and decisions when my brain is overheating is likely to be low. So, I go for a walk in the park, read a fiction book, go see a movie, or visit an art museum. Process

Managing someone else’s money is an incredible responsibility, which you may not fully appreciate during bull markets. But sideways and bear markets will remind you quickly.

I don’t want to over-glorify what we do – we are not curing cancer or saving people from burning buildings. But IMA clients entrust us with their life savings and tell me, “Vitaliy, please don’t screw it up.”

My decisions may determine whether our clients get to retire, pay for their medical expenses, or help their kids buy houses.

Staying rational when the world around you is melting up with greed or melting down in fear isn’t a capacity that one accidentally stumbles upon. You engineer it through a series of small, repeatable decisions – your investment process.

Posted on October 25, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Applications to MBA programs are up 12% in 2024 after declining for two years, according to the Graduate Management Admission Council, which surveys business school admissions offices.

Apple and Goldman Sachs were ordered to pay $89 million by the Consumer Financial Protection Bureau for failing to address thousands of consumer disputes of Apple Card transactions.

Apple is cutting production of Vision Pro due to slow sales. The tech giant is scaling down production of its $3,500 Vision Pro VR headset and might halt assembly of new ones next month,

UPS delivered a strong earnings report, with revenue beating analyst expectations for the first time in two years. Shares popped 5.28%.

ServiceNow rose 5.41% to a new all-time high thanks to a beat-and-raise third-quarter earnings report powered by higher AI demand for the enterprise software company.

Whirlpool climbed 11.20% after announcing solid earnings and reiterating guidance for the rest of the fiscal year, reassuring worried shareholders.

Molina Healthcare soared 17.67% after beating both top and bottom line estimates in the third quarter, thanks to the health insurer reaping the rewards of higher Medicaid payouts.

STOCKS DOWN

IBM dropped 6.17% on disappointing third-quarter results, missing on both top and bottom line forecasts thanks to lower consulting and infrastructure revenue.

Peloton pedaled higher yesterday after Greenlight Capital’s David Einhorn declared that the company was undervalued while he was pedaling on a Peloton. The stunt only worked for a quick sprint, though, with shares back down 2.07% today.

TKO Group Holdings got hit with a piledriver after the owner of the WWE and UFC announced it is acquiring several entertainment companies, including Professional Bull Riders. Investors bucked shares off 8.69%.

Keurig Dr. Pepper fizzled 4.80% thanks to lower sales last quarter, though the company is trying to bolster revenue by acquiring energy drink maker Ghost.

Air taxi startup Lilium crashed 61.50% on the news that its main subsidiaries have run out of cash and are filing for insolvency.

The S&P 500® index (SPX) rose 12.44 points (0.21%) to 5,809.86; the $DJI fell 140.59 points (–0.33%) to 42,374.36; and the NASDAQ Composite® ($COMP) added 138.83 points (0.76%) to 18,415.49.

The 10-year Treasury note yield fell four basis points to 4.20%.

The CBOE Volatility Index® (VIX) was about flat at 19.18.

Posted on October 24, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Quote: “It looks like the global battle against inflation has largely been won, even if price pressures persist in some countries. In most countries, inflation is now hovering close to central bank targets…The decline in inflation without a global recession is a major achievement.”—IMF (CNN Business)

Spirit Airlines is back from the dead, soaring 46.67% on a Wall Street Journal report that it may end up merging with FrontierAirlines after all. Frontier Airlines rose 0.76% on the news.

AT&T climbed 4.65% after it beat earnings expectations in the third quarter, though it missed on revenue.

Starbucks fell hard late yesterday but recovered a bit this afternoon after new CEO Brian Niccol said the coffee chain is suspending its 2025 fiscal outlook. Shares rose 0.86% today.

Coca-Cola fizzled 2.07% after beating both top and bottom line expectations. The problem is that the only reason the soda giant performed well was because it raised prices, while demand for soft drinks slowed.

Enphase Energy plummeted 14.92% after the solar stock missed on both earnings and revenue expectations last quarter.

Boeing is a very familiar name in the “What’s down” section, and its latest earnings report did nothing to help. The manufacturing giant notched a $6 billion loss last quarter, and shares fell 1.76%.

The SPX fell 53.78 points (–0.92%) to 5,797.42; the Dow Jones Industrial Average® ($DJI) lost 409.94 points (–0.96%) to 42,514.95; and the NASDAQ Composite ($COMP) dropped 296.47 points (–1.60%) to 18,276.65.

The 10-year Treasury note yield gained four basis points to 4.24%.

Although some might view a budget as unnecessarily restrictive, sticking to a spending plan can be a useful tool in enhancing the wealth of a medical practice. So, I will emphasize keys to smart budgeting and how to track spending and savings in these tough economic times.

There is an aphorism that suggests, “Money cannot buy happiness.” Well, this may be true enough but there is also a corollary that states, “Having a little sure reduces the unhappiness.”

Unfortunately, today there is more than a little financial unhappiness in all medical specialties. The challenges range from the commoditization of medicine, aging demographics, Medicare reimbursement cutbacks and increased competition to floundering equity markets, the home mortgage crisis, the squeeze on credit and declines in the value of a practice. Few doctors seem immune to this “perfect storm” of economic woes.

Far too many physicians are hurting and it is not limited to above-average earning professionals. However, one can strive to reduce the pain by following some basic budgeting principles. By adhering to these principles, physicians can eliminate the “too many days at the end of the month” syndrome and instead develop a foundation for building real wealth and security, even in difficult economic climates like we face today.

There are three major budget types. A flexible budget is an expenditure cap that adjusts for changes in the volume of expense items. A fixed budget does not. Advancing to the next level of rigor, a zero-based budget starts with essential expenses and adds items until the money is gone. Regardless of type, budgets can be extremely effective if one uses them at home or the office in order to spot money troubles before they develop.

For the purpose of wealth building, doctors may think of this budget as a quantitative expression of an action plan. It is an integral part of the overall cost-control process for the individual, his or her family unit or one’s medical practice.

Preparing a net income statement (lifestyle cash flow budget) is often difficult because many doctors perceive it as punitive. Most doctors do not live a disciplined spending lifestyle and they view a budget as a compromise to it. However, a cash flow budget is designed to provide comfort when there is surplus income that can be diverted for other future needs. For example, if you treat retirement savings as just another periodic bill, you are more likely to save for it.

You may construct a personal cash budget by recording each cash receipt and cash disbursement on a spreadsheet. Only the date, amount and a brief description of the transaction are necessary. The cash budget is a simple tool that even doctors who lack accounting acumen can use. Since it is possible to track the cash-in and cash-out in the same format used for a standard check register, most doctors find that the process takes very little time. Such a budget will provide a helpful look at how well you are staying within available resources for a given period.

We then continue with an analysis of your operating checkbook and a review of various source documents such as one’s tax return, credit card statements, pay stubs and insurance policies. A typical statement will show all cash transactions that occur within one year. It is helpful to establish a monthly equivalent to all items of income and expense. For the purposes of getting started, note items of income and expense by the frequency you are accustomed to receiving or spending them.

What You Should Know About The ‘Action Plan’ Cash Budget

For a medical office, the first operations budget item might be salary for the doctor and staff. Operating assets and other big ticket items come next. Some of our doctors/clients review their office P&L statements monthly, line by line, in an effort to reduce expenses. Then they add back those discretionary business expenses they have some control over.

Now, do you still run out of money before the end of the month? If so, you had better cut back on entertainment, eating dinner out or that fancy, new but unproven piece of medical equipment. This sounds draconian until you remind yourself that your choice is either: live frugally later or live a simpler lifestyle now and invest the difference.

As a young doctor, it may be a difficult trade-off. By mid-life, however, you are staring retirement in the face. That is why the action plan depends on your actions concerning monetary scarcity, a plan that one can implement and measure using simple benchmarks or budgeting ratios. By using these statistics, perhaps on an annual basis, the doctor can spot problems, correct them and continue planning actively toward stated goals like building long-term wealth.

Useful Calculations To Assess Your Budgeting Success

In the past, generic budgeting ratios would emphasize not spending more than 15 to 20 percent of your net salary on food or 8 percent on medical care. Now these estimates have given way to more rigorous numbers. Personal budget ratios, much like medical practice financial ratios, represent comparable benchmarks for parameters such as debt, income growth and net worth. Although these ratios are still broad, the following represent some useful personal budgeting ratios for physicians.

• Basic liquidity ratio = liquid assets / average monthly expenses. Cash-on-hand should approach 12 to 24 months or more in the case of a doctor employed by a financially insecure HMO or fragile medical group practice. Yes, chances are you have heard of the standard notion of setting enough cash aside to cover three months in a rainy day scenario. However, we have decried this older laymen standard for many years in our textbooks, white papers and speaking engagements as being wholly insufficient for the competitively unstable environment of modern healthcare.

• Debt to assets ratio = total debt / total assets. This percentage is high initially but should decrease with age as the doctor approaches a debt-free existence

• Debt to gross income ratio = annual debt repayments / annual gross income. This represents the adequacy of current income for existing debt repayments. Doctors should try to keep this below 20 to 25 percent.

• Debt service ratio = annual debt repayment / annual take-home pay. Physicians should aim to keep this ratio below 25 to 30 percent or face difficulty paying down debt.

• Investment assets to net worth ratio = investment assets / net worth. This budget ratio should increase over time as retirement approaches.

• Savings to income ratio = savings / annual income. This ratio should also increase over time as one retires major obligations like medical school debt, a practice loan or a home mortgage.

• Real growth ratio = (income this year – income last year) / (income last year – inflation rate). This budget ratio should grow faster than the core rate of inflation.

• Growth of net worth ratio = (net worth this year – net worth last year) / net worth last year – inflation rate). Again, this budgeting ratio should stay ahead of inflation.

In other words, these ratios will help answer the question: “How am I doing?”

Pearls For Sticking To A Budget

Far from the burden that most doctors consider it to be, budgeting in one form or another is probably one of the greatest tools for building wealth. However, it is also one of the greatest weaknesses among physicians who tend to live a certain lifestyle.

In fact, we have found that less than one in 10 medical professionals have a personal budget. Fear, or a lack of knowledge, is a major cause of procrastination. Fortunately, the following guidelines assist in reversing this microeconomic disaster.

1. Set reasonable goals and estimate annual income. Do not keep large amounts of cash at home or office. Deposit it in an FDIC insured money-market account for safety. Do not deposit it in a money market mutual fund with net asset value (NAV) that may “break the buck” and fall below the one-dollar level. Track actual bills and expenses.

2. Do not pay bills early, do not have more taxes withheld from your salary than needed and develop spending estimates to pay fixed expenses first. Fixed expenses are usually contractual and usually include housing, utilities, food, Social Security, medical, debt repayments, homeowner’s or renter’s insurance, auto, life and disability insurance, etc. Reduce fixed expenses when possible. Ultimately, all expenses get paid and become variable in the long run.

3. Make it a priority to reduce variable expenses. Variable expenses are not contractual and may include clothing, education, recreational, travel, vacation, gas, cable TV, entertainment, gifts, furnishings, savings, investments, etc. Trim variable expenses by 5 to 20 percent.

4. Use “carve-outs or “set-asides” for big ticket items and differentiate true wants from frivolous needs.

5. Calculate both income and expenses as a percentage of your total budget. Determine if there is a better way to allocate resources. Review the budget on a monthly basis to notice any variance. Determine if the variance was avoidable, unavoidable or a result of inaccurate assumptions. Take corrective action as needed.

6. Know the difference between saving and investing. Savers tend to be risk adverse while investors understand risk and take steps to mitigate it. Watch mutual fund commissions and investment advisory fees, which cut into return-rates. Keep investments simple and diversified (stocks, bonds, cash, index, no-load mutual and exchange traded funds, etc.).

Sooner or later, despite the best of budgeting intentions, something will go awry. A doctor will be terminated or may be the victim of a reduction-in-force (RIF) because of cost containment initiatives.4 A medical practice partnership may dissolve or a local hospital or surgery center may close, hurting your practice and livelihood. Someone may file a malpractice lawsuit against you, a working spouse may be laid off or you may get divorced. Regardless of the cause, budgeting crisis management encompasses two different perspectives: awareness and execution.

First, if you become aware that you may lose your job, the following proactive steps will be helpful to your budget and overall financial condition.

• Decrease retirement contributions to the required minimum for company/practice match. • Place retirement contribution differences in an after-tax emergency fund. • Eliminate unnecessary payroll deductions and deposit the difference to cash. • Replace group term life insurance with personal term or universal life insurance. • Take your old group term life insurance policy with you if possible. • Establish a home equity line of credit to verify employment. • Borrow against your pension plan only as a last resort.

If you have lost your job or your salary has been depressed, negotiate your departure and get an attorney if you believe you lost your position through breach of contract or discrimination. Then execute the following steps to recalculate your budget and boost your wealth rebuilding activities.

• Prioritize fixed monthly bills in the following order: rent or mortgage; car payments; utility bills; minimum credit card payments; and restructured long-term debt.

• Consider liquidating assets to pay off debts in this order: emergency fund, checking accounts, investment accounts or assets held in your children’s names.

• Review insurance coverage and increase deductibles on homeowner’s and automobile insurance for needed cash.

• Then sell appreciated stocks or mutual funds; personal valuables such as furnishings, jewelry and real estate; and finally, assets not in pension or annuities if necessary.

• Keep or rollover any lump sum pension or savings plan distribution directly to a similar savings plan at your new employer, if possible, when you get rehired.

• Apply for unemployment insurance.

• Review your medical insurance and COBRA coverage after a “qualifying event” such as job loss, firing or even after quitting. It is a bit expensive due to a 2 percent administrative fee surcharge but this may be well worth it for those with preexisting conditions or who are otherwise difficult to insure. One may continue COBRA for up to 18 months.

• Consider a high deductible Health Savings Account (HSA), which allows tax-deferred dollars like a medical IRA, for a variety of costs not normally covered under traditional heath insurance plans. Self-employed doctors deduct both the cost of the premiums and the amount contributed to the HSA. Unused funds roll over until the age of 59½, when one can use the money as a supplemental retirement benefit.

• Eliminate unnecessary variable, charitable and/or discretionary expenses, and become very frugal.

Final Notes

The behavioral psychologist, Gene Schmuckler, PhD, MBA, sometimes asks exasperated doctors to recall the story of the old man who spent a day watching his physician son treating HMO patients in the office. The doctor had been working at his usual feverish pace all morning. Although he was working hard, he bitterly complained to his dad that he was not making as much money as he used to make. Finally, the old man interrupted him and said, “Son, why don’t you just treat the sick patients?” The doctor-son looked at his father with an annoyed expression and responded, “Dad, can’t you see, I do not have time to treat just the sick ones.”

Always remember to add a bit of emotional sanity into your budgeting and economic endeavors.

Regardless of one’s age or lifestyle, the insightful doctor realizes that it is never too late to take control of a lost financial destiny through prudent wealth building activities. Personal and practice budgeting is always a good way to start the journey.

NOTE: Dr. Marcinko is a former Certified Financial Planner and current Certified Medical Planner™. He has been a medical management advisor for more than a decade. He is the CEO of http://www.MarcinkoAssociates.com

The authors acknowledge the assistance of Mackenzie H. Marcinko PhD in the preparation of this article.

Posted on October 19, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

CVS Health may be breaking up…with itself. The board of directors at CVS Health—the parent company of CVS Pharmacy, pharmacy benefit managerCVS Caremark, and insurance unit Aetna—are working with a group of bankers to review the company’s strategy, which according to Reuters, may lead to a split between its pharmacy division and Aetna.

Apple climbed 1.23% on a Bloomberg report that iPhone 16 demand has been shockingly strong in China.

Verizon Communications will purchase $1 billion worth of US Cellular’s wireless spectrum licenses. Verizon rose just 0.34%—but it’s a huge deal for US Cellular, which popped 7.22%, and Telephone and Data Systems, which owns 82% of US Cellular, and soared 15.40%.

Intuitive Surgical rose to a new all-time high, climbing 10.01% on strong earnings powered by sales of its da Vinci device.

Lamb Weston, the company behind the french fries you overindulge in every time you go out to dinner, is being pushed by activist investor Jana Partners toward exploring a sale. Shareholders rejoiced, and the stock rose 10.17%.

Stocks Down

CVS Health sank 5.23% on the news that CEO Karen Lynch will be replaced by David Joyner after three years at the helm of the struggling pharmacy/retailer. Joyner ran the company’s pharmacy service business for the last two years.

WD-40 seems like the staple of all consumer staples, but the company missed on both revenue and earnings estimates last quarter. Shares fell 4.79% on the news.

American Express dropped 3.15% after the credit card company reported a rare miss today, beating bottom-line estimates but missing revenue forecasts last quarter.

MGP Ingredients makes all the booze you drink under different brand names, but people aren’t drinking enough. The beverage maker issued preliminary earnings that included a 24% drop in sales. Shares tanked 24.16%.

Here’s where the major stock market benchmarks ended:

The S&P 500® index (SPX)rose 23.20 points (0.40%) to 5,864.67, a new record high close, to end the week up 0.85%; the Dow Jones Industrial Average® ($DJI) added 36.86 points (0.09%) to 43,275.91, also another record high finish, to end the week up 0.96%; and the $COMP gained 115.94 points (0.63%) to 18,489.55 to end the week up 0.80%.

The 10-year Treasury note yield (TNX) fell two basis points to 4.07%.

The CBOE Volatility Index® (VIX) fell to 18.17, the lowest since September 30.

A new survey results may prompt health systems to second-guess some of their future plans. A recent University of Michigansurvey found 74% of adults ages 50+ have “very little or no trust” in health info generated by AI. Maybe it’s not time to roll out chatbots on patient portals just yet.

Posted on October 17, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Goldman Sachs’ profit jumped 45% in monster quarter. The investment bank made $3 billion of profit on revenue of nearly $13 billion in Q3, it reported yesterday, surpassing even the rosiest of expectations. Bloomberg reported that it was the best quarter ever for Goldman’s stock trading unit, putting the group on track for a record year.

Walgreenssaid it will close 1,200 US stores, about one in seven locations, by 2027. The retailer will shutter 500 stores by the end of next year.

Trump Media & Technology Group has had a wild week, falling nearly 10% yesterday before trading of the stock was halted, then popping 15.52% today. Election hype, a Trump-sponsored cryptocurrency, and Truth+, a new streaming service, are keeping shareholders on their toes.

Abbott Laboratories rose 1.53% thanks to a stronger-than-expected earnings report powered by the company’s impressive medical device sales.

Aspen Aerogels makes insulating material for batteries, which sounds boring to everyone but the Department of Energy. The DOE signed a conditional commitment to loan the company up to $670 million, sending shares 13.24% higher.

DOWN STOCKS

Novavax plummeted 19.44% after the FDA put a hold on the pharma company’s flu and Covid vaccine combination.

Interactive Brokers enjoyed higher revenue and more trading from its user base last quarter, but earnings per share came in under expectations, and shares sank 4.05%.

The SPX rose27.21points (0.47%) to 5,842.47; the Dow Jones Industrial Average® ($DJI) added 337.28 points (0.79%) to 43,077.70; and the NASDAQ Composite®($COMP) increased 51.49 points (0.28%) to 18.367.08.

The 10-year Treasury note yield (TNX) fell two basis points to just below 4.02%, the lowest close since October 4.

The CBOE Volatility Index® (VIX) dropped moderately to 19.58, still elevated considering stock market strength.

Posted on October 15, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Maximum lifespans. The upper limit of human life expectancy is leveling out, according to a new study published in the journal Nature Aging. Back in 1990, life-extending tech and health measures were increasing the average global lifespan by about 2.5 years per decade, but that dropped to 1.5 years per decade in the 2010s and closer to zero in the US, where there are more drug overdoses, shootings, and medical care inequities.

Stocks kicked off the first full week of earnings season at full throttle. The S&P 500 rose to a new intraday record, the Dow closed above 43,000 for the first time ever, and the NASDAQ climbed steadily throughout the trading session.

Bitcoin soared on the news of China’s additional stimulus spending that broke this weekend. Although the Chinese government’s plans are light on details at the moment, the promise of more support for the world’s second largest economy was enough to get crypto traders hyped.

Interestingly enough, those same promises of Chinese stimulus sent oil tumbling to start the day. The selling was exacerbated by OPEC’s announcement that crude demand will fall lower than expected in 2024 and 2025.

Gold sank a hair today as traders weighed Chinese stimulus against a stronger dollar.

The S&P 500® index (SPX) rose44.82points (0.77%) to 5,859.85, a new closing high; the Dow Jones Industrial Average® ($DJI) increased 201.36 points (0.47%) to 43,065.22, also a new closing high; and the NASDAQ Composite®($COMP) added 159.74 points (0.87%) to 18,502.69.

The 10-year Treasury note yield (TNX) did not trade today due to the holiday.

The CBOE Volatility Index® (VIX) slipped to 19.9, its first drop below 20 since October 4.

A slate of corporate earnings reports coming from Goldman Sachs, Bank of America, and Citigroup in the financial sector, along with healthcare giants Johnson & Johnson, Walgreens, and UnitedHealth. And throughout the week: Morgan Stanley will report on Wednesday, Netflix reports on Thursday, and Procter & Gamble and American Express drop their financials on Friday. It’ll pose a big test for the stock market’s $8 trillion rally this year.

Posted on October 14, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

U.S. stock markets, including the New York Stock Exchange and the NASDAQ remain open and follow a regular schedule today.

The bond markets will be closed, however.

***

***

Stocks ended last week on a high note, closing out their fifth straight week of gains. The Dow was pushed to yet another new all-time high by strong earnings from JPMorgan, while the S&P 500 was in the green and rose to its own record close, and the NASDAQ clawed its way out of the red by early Friday afternoon.

Bond yields took a breather, falling below 4.1% thanks to a better-than-expected PPI report that helped offset inflation fears that had re-arisen after a worse-than-expected CPI report.

Gold rose as well on PPI news, since the data pointed to a better chance of more rate cuts ahead.

Oil fell a bit but gained over the last two weeks on geopolitical tensions and destruction in the Gulf of Mexico following the two major hurricanes.

According to colleague Dan Ariely PhD, a Zero Sum Bias [ZSB] is the mistaken belief that one person’s gain is another’s loss. It’s like thinking the world is a giant pie with only so many slices. This mindset fuels competition and jealousy, making us forget that collaboration can create more pie. It’s why we sometimes root against others instead of working together.

Question: Is the stock market a zero-sum game? You frequently hear media refer to games and markets as zero-sum games.

Answer: Well, yes, we define the stock market as a zero-sum game, both in the short and in the long term, although it technically is incorrect. A zero-sum game is where one person’s gain is another person’s loss – thus there is no wealth created and the overall benefit is zero. This doesn’t apply to stocks, but it’s a zero-sum game in relation to a stock market benchmark.

For example, short-term trading in stocks is theoretically not a zero-sum game, and neither is long-term investing. But short-term trading is close to a zero-sum game, and long-term investing is a zero-sum game if we use a broad index as a benchmark.

Essentially, in other words, the stock market functions as an expansive network of zero-sum transactions; each trade engages a buyer and a seller–their perspectives on a security’s future value contrasting. These opposing views propel market prices: they mirror not only risk transfer but also potential reward—a dynamic process indeed! Traders and investors must grasp the crucial zero-sum aspect; it underscores trading’s inherent competitiveness. Effectively anticipating market trends and actions from other participants: therein lies success in this environment.

Posted on October 13, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Yom Kippur. Wishing a meaningful and easy fast to our readers who observe.

Boeing plans to lay off 10% of its workforce, or ~17,000 people, to cut costs as its factory workers’ strike continues.

The Nobel Peace Prize was awarded to Nihon Hidankyo, a Japanese organization of survivors of the atomic bombings of Hiroshima and Nagasaki, that advocates against nuclear weapons.

Markets: After big banks—which are often viewed as a proxy for the economy’s health—kicked off earnings season strong, the S&P 500 and the Dow hit new records, capping off stocks’ fifth winning week in a row.

Stock spotlight: Elon Musk’s presentation of Tesla’s long-awaited Robocab didn’t go as badly as that time the Cybertruck’s “unbreakable” window got smashed on stage, but investors were unimpressed by its lack of key details.

Hailing the news were Uber and Lyft, which rose after Tesla failed to present a looming threat.

JPMorgan says the soft landing is here. Reporting its first quarterly earnings since the Fed’s big interest rate cut, America’s biggest bank earned more than expected from loans and boosted what it forecasts it’ll earn for the year.

In other banking news, Wells Fargo also beat earnings expectations.

Posted on October 11, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The Consumer Price Index rose 2.4% in the 12-month period that ended in September, while a gauge that strips out food and energy prices was 3.3%, the government said yesterday.

Stat: 7%. That’s how much employer health insurance premiums increased this year, after rising by the same margin last year. Family coverage this year costs roughly $25,500 for employers and employees. (the Wall Street Journal)

Celsius Holdings, makers of those disgusting energy drinks your 12-year-old cousin chugs, soared 14.42% after analysts from Stifel and Piper Sandler gave it a vote of confidence.

Crowdstrike enjoyed a rare bump 5.56% higher today after RBC Capital analysts named the company one of the top software stocks of 2025. Speaking of, Delta Air Lines announced it took a $380 billion hit last quarter due to the Crowdstrike outage. Shares of the airline sank 1.16% after earnings.

CVS Health rose 1.35% after an upgrade from Barclays analysts who think the company’s Medicare business should recover nicely.

GXO Logistics, a supply-chain management company, popped 14.11% on a report from Bloomberg that the company is exploring a potential sale.

Stocks down

10X Genomics, which sounds like the bad guys that accidentally release a military-grade virus in a zombie movie, fell 24.70% after it announced preliminary results that disappointed shareholders.

Toronto-Dominion Bank dropped 5.29% on the news that not only will the Canadian bank pay US regulators $3 billion in penalties, but its retail business growth will be limited in the US. All that for failing to stop drug cartels from laundering money.

First Solar sank 9.29% after Jefferies analysts cut their price target on the solar power panel maker, citing production delays hurting the company’s bottom line. The report sent shares of competitors Enphase Energy and SolarEdge Technologies tumbling 5.82% and 4.32%, respectively.

PayPal lost 3.27% thanks to a report from Bernstein analysts who downgraded the stock on fears that Venmo could lose market share to competitors.

The S&P 500® index (SPX) lost 11.99 points (–0.21%) to 5,780.05; the Dow Jones Industrial Average® ($DJI) fell 57.88 points (–0.14%) to 42,454.12; and the NASDAQ Composite® ($COMP) dropped 9.56 points (–0.05%) to 18,282.05.

The 10-year Treasury note yield (TNX) rose three basis points to 4.1%, the highest since July 31 and closing in on the 100-day moving average.

The CBOE Volatility Index® (VIX) was flat at 20.87.

PepsiCo cut its full-year organic revenue guidance as consumers reduced their spending on drinks and snacks, and the company posted “its second straight quarter of weaker-than-expected sales,” CNBC reported.

Posted on October 9, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Activist investor takes $1 billion stake in Pfizer. The firm Starboard Value has amassed a stake in the pharma giant, which has struggled after reaching new heights during the pandemic, in hopes of turning the company around.

If you can’t beat ‘em, join ‘em: WW International, akaWeightWatchers,soared 46.95% after the company announced it will begin offering GLP-1 weight-loss drugs.

Nvidia rose 4.05% after the Foxconn CEO told CNBC that AI demand is still incredibly strong.

Palantir popped 6.58% after the CTO of the data analytics firm appeared on CNBC and told everyone that his company is making mad money.

Welcome to the club: S&P Global announced that DocuSign is replacing MDU Resources Group in the S&P MidCap 400 index, while MDU is moving to the S&P SmallCap 600 index. Docusign rose 6.55% on the news, while MDU gained 2.44%.

Humana finally caught a break when a Bernstein analyst upgraded the stock today, writing that the health insurer has been hurt enough. Shares rose 2.92%.

What’s down

What goes up must come down: Chinese stocks, which have enjoyed an impressive rally recently, came tumbling back to Earth today after the country’s state planner didn’t announce any new stimulus measures. Bilibili fell 12.93%, JD.com lost 7.52%, Alibaba sold off 6.67%, and Nio dropped 8.10%.

Today’s oil selloff pummeled energy stocks: Valero Energy lost 5.31%, while Marathon Petroleum stumbled 7.66%.

The SPX rose 55.19 points (0.97%) to 5,751.15; the Dow Jones Industrial Average® ($DJI) added 126.13 points (0.30%) to 42,080.37; and the NASDAQ Composite® ($COMP) gained 259.01 points (1.45%) to 18,182.92.

The 10-year Treasury note yield (TNX) rose one basis point to 4.03%.

The CBOE Volatility Index® (VIX) sank to 21.24, still above its long-term average.

Posted on October 8, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

October continues to be a tough month for stocks, with all three major indexes spending yesterday afternoon in the red. The Dow in particular had a horrible day and dropped over 500 points, while major tech stocks were pushed lower by a series of analyst downgrades.

Oil continued its hot streak yesterday, rising above $77 on the back of geopolitical conflict in the Middle East. That helped ensure that, while everything else fell, energy was the only positive sector in the S&P 500.

Gold has often found itself rising in tandem with crude, though it broke that habit, with the shiny safe haven dropping a hair as investors digest the idea that the Fed’s next interest rate cut may be smaller than they thought.

Bitcoin broke above $64,000 for a moment yesterday only to be yanked back down, as crypto traders ride out the recent volatility.

Posted on October 5, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

PayPal completed its first transaction using its proprietary stablecoin to pay an invoice to Ernst & Young. It’s a milestone for the payments company’s advance into cryptocurrency.

The free IRS tax filing software, which was piloted in 12 states for the 2024 tax season, will be available in 24 states for 2025.

Your loss is our gain: Shares of airline stocks popped on the news of Spirit’s problems. Delta Air Lines ascended 3.84%, United Airlines climbed 6.47%, and Frontier Group Holdings soared 16.43%.

Albemarle popped 8.25% on the rumor that mining behemoth Rio Tinto may try to make an acquisition of the lithium miner. Other potential takeover targets rose as well, including Arcadium (up 10%) and SQM (up 3%).

Abercrombie & Fitch rose 9.10% thanks to an upgrade from JP Morgan analysts, who are bullish about the fashion retailer’s recent momentum.

Ubisoft Entertainment skyrocketed 29.87% on the news that the video game maker’s parent company and founders are considering a buyout.

Homebuilder stocks sank on today’s strong jobs report, which propelled treasury yields higher, which means that mortgage rates aren’t getting any lower. D.R. Horton dropped 2.91%, Lennar fell 2.52%, and Toll Brothers lost 2.57%.

Transportation stocks fell thanks to an agreement between port owners and longshoremen to put the recent strike on pause. Moller-Maersk lost 5.37%, while Zim IntegratedShipping Services stumbled 12.55%.

The S&P 500® index (SPX) climbed 51.13 points (0.9%) to 5,751.07 up 0.22% for the week;the Dow Jones Industrial Average® ($DJI) added 341.16 points (0.81%) to 42,352.75, up 0.09% for the week; and the NASDAQ Composite® ($COMP) rose 219.37 points (1.22%) to 18,137.85, up 0.1% for the week.

The 10-year Treasury note yield (TNX) soared 13 basis points to 3.98%, finishing the week up 23 basis points. The 2-year yield rose 37 basis points this week.

The CBOE Volatility Index® (VIX)fell to 18.58 but remains elevated from last month’s lows, likely on geopolitical concerns.

Only 2% of the homes hit by Hurricane Helene in Georgia, North Carolina, and South Carolina had a policy protecting them against catastrophic flooding, according to an analysis by Politico and E&E News.

The US Hiring Pace picked up strongly in September and the unemployment rate ticked down to 4.1%, signs the U.S. economy had continued momentum in a month the Federal Reserve delivered its first interest-rate cut in four years. U.S. employers added 254,000 jobs last month, the Labor Department said Friday.