BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] E-mail: MarcinkoAdvisors1738@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Insurance agents are primarily paid through commissions, but may also earn salaries, bonuses, and fees depending on their employment model and the types of policies they sell.

Insurance agents play a vital role in helping individuals and businesses navigate the complex world of insurance. Their compensation structures vary widely, influenced by factors such as the type of insurance they sell, whether they work independently or for a company, and the specific agreements they have with insurers. Understanding how insurance agents are paid is essential for consumers who want to make informed decisions and for aspiring agents considering a career in the industry.

The most common form of compensation for insurance agents is commission-based pay. Agents earn a percentage of the premium paid by the customer when they successfully sell a policy. These commissions can vary depending on the type of insurance. For example, first-year commissions for auto and homeowners insurance typically range from 5% to 20%, while commercial property and casualty policies may offer 10% to 15%. Life insurance policies often provide higher initial commissions, sometimes exceeding 50% of the first-year premium, followed by smaller renewal commissions in subsequent years.

There are two main types of insurance agents: captive agents and independent agents. Captive agents work exclusively for one insurance company and usually receive a combination of salary and commissions. Their compensation may also include performance bonuses and incentives tied to sales targets. Independent agents, on the other hand, represent multiple insurers and rely more heavily on commissions. They have the flexibility to offer a wider range of products, but their income is directly tied to their ability to sell policies and maintain client relationships.

***

***

In addition to commissions, some agents earn fees for services such as policy reviews, risk assessments, or consulting. These fees are more common in commercial insurance or financial planning contexts, where agents provide specialized expertise. However, fee-based compensation is less prevalent in personal lines of insurance like auto or home coverage.

Bonuses and incentives are another component of agent compensation. Insurance companies often reward agents for meeting sales quotas, retaining clients, or selling specific types of policies. These bonuses can significantly boost an agent’s income, but they may also create potential conflicts of interest if agents prioritize higher-paying products over client needs.

Some agents, particularly those employed by large firms or call centers, receive a fixed salary. This model provides stability but may limit earning potential compared to commission-based roles. Salaried agents may still receive performance bonuses or profit-sharing depending on company policy.

Ultimately, an insurance agent’s earnings depend on their business model, experience, and ability to build a loyal client base. While commissions remain the cornerstone of insurance compensation, the rise of fee-based services and hybrid models reflects a shift toward more transparent and client-focused practices.

Consumers should feel empowered to ask agents about their compensation structure to ensure they receive unbiased advice tailored to their needs.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: MarcinkoAdvisors@outlook.com

Posted on November 5, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

In today’s competitive healthcare landscape, effective marketing is essential for the growth and sustainability of a medical practice. Gone are the days when word-of-mouth alone could sustain a clinic. Patients now seek providers who not only offer excellent care but also communicate their value clearly and consistently. Strategic marketing helps medical practices attract new patients, retain existing ones, and build a strong reputation in the community.

🎯 Understanding the Target Audience

The foundation of any successful marketing strategy is a deep understanding of the target audience. Medical practices must identify the demographics, needs, and preferences of their ideal patients. For example, a pediatric clinic will focus on parents, while a dermatology practice may target young adults concerned with skin health. Tailoring messages to resonate with these groups ensures that marketing efforts are relevant and effective.

🌐 Building a Strong Online Presence

In the digital age, a robust online presence is non-negotiable. A professional, user-friendly website serves as the virtual front door of the practice. It should include essential information such as services offered, provider bios, contact details, and online appointment scheduling. Search engine optimization (SEO) ensures the site ranks well on Google, making it easier for potential patients to find the practice.

Social media platforms like Facebook, Instagram, and LinkedIn offer additional avenues to engage with the community. Regular posts about health tips, staff spotlights, and patient testimonials humanize the practice and foster trust. Paid advertising on these platforms can also target specific demographics, increasing visibility and driving traffic to the website.

🗣️ Leveraging Patient Reviews and Testimonials

Online reviews are a powerful form of social proof. Encouraging satisfied patients to leave positive feedback on platforms like Google, Yelp, and Healthgrades can significantly influence prospective patients. Testimonials can also be featured on the practice’s website and social media channels. Responding to reviews—both positive and negative—demonstrates attentiveness and a commitment to patient satisfaction.

📬 Utilizing Email and Content Marketing

Email marketing remains a cost-effective way to stay connected with patients. Monthly newsletters can include health tips, updates on services, and reminders for annual checkups or vaccinations. Content marketing, such as blog posts and educational videos, positions the practice as a trusted authority in healthcare. This not only boosts SEO but also builds credibility and patient loyalty.

***

***

🤝 Community Engagement and Partnerships

Participating in local events, offering free health screenings, or partnering with schools and businesses can enhance visibility and goodwill. These efforts show that the practice is invested in the well-being of the community, which can translate into increased patient referrals and long-term relationships.

📊 Measuring Success

Finally, tracking the performance of marketing campaigns is crucial. Metrics such as website traffic, appointment bookings, social media engagement, and patient acquisition rates provide insights into what’s working and what needs adjustment. Regular analysis ensures that marketing efforts remain aligned with business goals.

Marketing a medical practice requires a thoughtful blend of digital tools, patient engagement, and community outreach. When done right, it not only drives growth but also reinforces the practice’s mission to provide compassionate, high-quality care.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

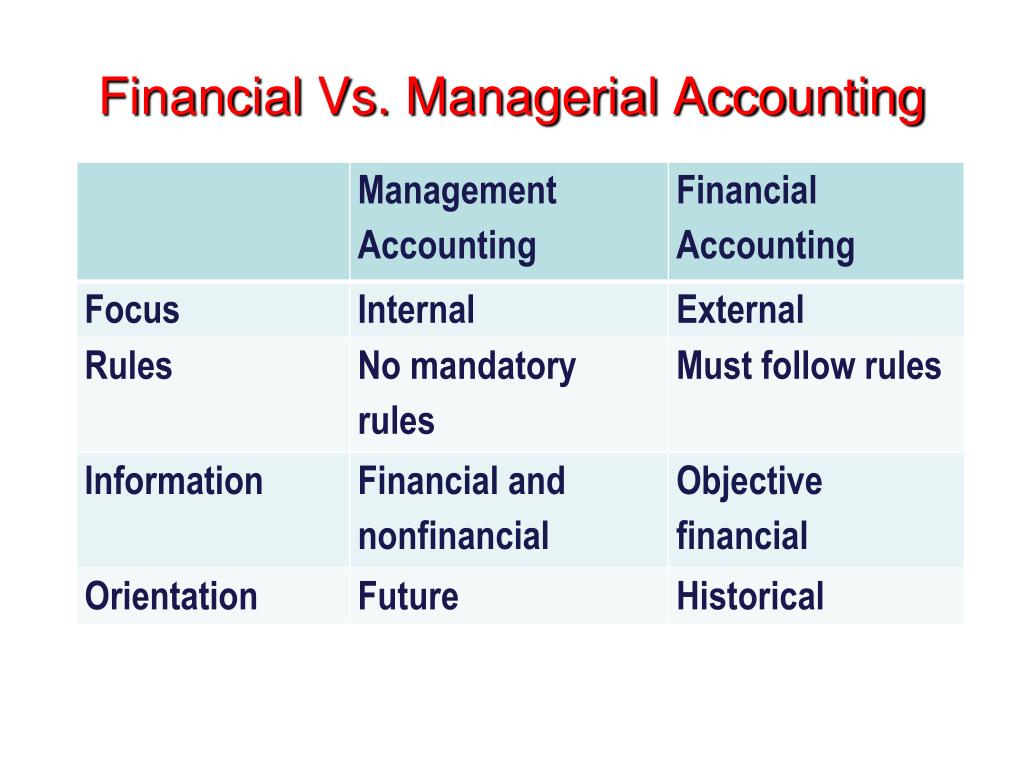

Product costing deals with determining the total costs involved in the production of a good or service. Costs may be broken down into subcategories, such as variable, fixed, direct, or indirect costs. Cost accounting is used to measure and identify those costs, in addition to assigning overhead to each type of product created by the company.

Managerial accountants calculate and allocate overhead charges to assess the full expense related to the production of a good. The overhead expenses may be allocated based on the number of goods produced or other activity drivers related to production, such as the square footage of the facility. In conjunction with overhead costs, managerial accountants use direct costs to properly value the cost of goods sold and inventory that may be in different stages of production.

Marginal costing (sometimes called cost-volume-profit analysis) is the impact on the cost of a product by adding one additional unit into production. It is useful for short-term economic decisions. The contribution margin of a specific product is its impact on the overall profit of the company. Margin analysis flows into break-even analysis, which involves calculating the contribution margin on the sales mix to determine the unit volume at which the business’s gross sales equals total expenses. Break-even point analysis is useful for determining price points for products and services.

Cash Flow Analysis

Managerial accountants perform cash flow analysis in order to determine the cash impact of business decisions. Most companies record their financial information on the accrual basis of accounting. Although accrual accounting provides a more accurate picture of a company’s true financial position, it also makes it harder to see the true cash impact of a single financial transaction. A managerial accountant may implement working capital management strategies in order to optimize cash flow and ensure the company has enough liquid assets to cover short-term obligations.

When a managerial accountant performs cash flow analysis, he will consider the cash inflow or outflow generated as a result of a specific business decision. For example, if a department manager is considering purchasing a company vehicle, he may have the option to either buy the vehicle outright or get a loan. A managerial accountant may run different scenarios by the department manager depicting the cash outlay required to purchase outright upfront versus the cash outlay over time with a loan at various interest rates.

Inventory Turnover Analysis

Inventory turnover is a calculation of how many times a company has sold and replaced inventory in a given time period. Calculating inventory turnover can help businesses make better decisions on pricing, manufacturing, marketing, and purchasing new inventory. A managerial accountant may identify the carrying cost of inventory, which is the amount of expense a company incurs to store unsold items.

If the company is carrying an excessive amount of inventory, there could be efficiency improvements made to reduce storage costs and free up cash flow for other business purposes.

Constraint Analysis

Managerial accounting also involves reviewing the constraints within a production line or sales process. Managerial accountants help determine where bottlenecks occur and calculate the impact of these constraints on revenue, profit, and cash flow. Managers then can use this information to implement changes and improve efficiencies in the production or sales process.

Financial Leverage Metrics

Financial leverage refers to a company’s use of borrowed capital in order to acquire assets and increase its return on investments. Through balance sheet analysis, managerial accountants can provide management with the tools they need to study the company’s debt and equity mix in order to put leverage to its most optimal use.

Performance measures such as return on equity, debt to equity, and return on invested capital help management identify key information about borrowed capital, prior to relaying these statistics to outside sources. It is important for management to review ratios and statistics regularly to be able to appropriately answer questions from its board of directors, investors, and creditors.

Accounts Receivable (AR) Management

Appropriately managing accounts receivable (AR) can have positive effects on a company’s bottom line. An accounts receivable aging report categorizes AR invoices by the length of time they have been outstanding. For example, an AR aging report may list all outstanding receivables less than 30 days, 30 to 60 days, 60 to 90 days, and 90+ days.

Through a review of outstanding receivables, managerial accountants can indicate to appropriate department managers if certain customers are becoming credit risks. If a customer routinely pays late, management may reconsider doing any future business on credit with that customer.

Budgeting, Trend Analysis, and Forecasting

Budgets are extensively used as a quantitative expression of the company’s plan of operation. Managerial accountants utilize performance reports to note deviations of actual results from budgets. The positive or negative deviations from a budget also referred to as budget-to-actual variances, are analyzed in order to make appropriate changes going forward.

Managerial accountants analyze and relay information related to capital expenditure decisions. This includes the use of standard capital budgeting metrics, such as net present value and internal rate of return, to assist decision-makers on whether to embark on capital-intensive projects or purchases. Managerial accounting involves examining proposals, deciding if the products or services are needed, and finding the appropriate way to finance the purchase. It also outlines payback periods so management is able to anticipate future economic benefits.

Managerial accounting also involves reviewing the trendline for certain expenses and investigating unusual variances or deviations. It is important to review this information regularly because expenses that vary considerably from what is typically expected are commonly questioned during external financial audits. This field of accounting also utilizes previous period information to calculate and project future financial information. This may include the use of historical pricing, sales volumes, geographical locations, customer tendencies, or financial information.

The Dow Jones Industrial Average (DJIA), often referred to simply as “the Dow,” is one of the oldest and most well-known stock market indices in the world. It was created in 1896 by Charles Dow, the co-founder of The Wall Street Journal, and is designed to represent the performance of the broader U.S. stock market, specifically focusing on 30 large, publicly traded companies. These companies are considered leaders in their respective industries and serve as a barometer for the overall health of the U.S. economy.

The Composition of the DJIA

The DJIA includes 30 companies, which are selected by the editors of The Wall Street Journal based on various factors such as market influence, reputation, and the stability of the company. These companies represent a wide array of sectors, including technology, finance, healthcare, consumer goods, and energy. Notably, the companies chosen for the DJIA are not necessarily the largest companies in the U.S. by market capitalization, but rather those that are most indicative of the broader economy. Some of the prominent companies listed in the DJIA include names like Apple, Microsoft, Coca-Cola, and Johnson & Johnson.

However, the list of 30 companies is not static. Over time, companies may be added or removed to reflect changes in the economic landscape. For example, if a company experiences significant decline or no longer represents a leading sector, it might be replaced with another company that better reflects modern economic trends. This periodic reshuffling ensures that the DJIA continues to be a relevant measure of economic activity.

How the DJIA is Calculated

The DJIA is a price-weighted index, which means that the value of the index is determined by the share price of the component companies, rather than their market capitalization. To calculate the DJIA, the sum of the stock prices of all 30 companies is divided by a special divisor. This divisor adjusts for stock splits, dividends, and other corporate actions to maintain the integrity of the index over time. The price-weighted method means that higher-priced stocks have a greater impact on the movement of the index, regardless of the overall size or economic weight of the company.

For instance, if a company with a higher stock price like Apple experiences a significant change in value, it will influence the DJIA more than a company with a lower stock price, even if the latter has a larger market capitalization. This makes the DJIA somewhat different from other indices, like the S&P 500, which is weighted by market cap and gives more weight to larger companies in terms of their economic impact.

Significance of the DJIA

The DJIA is widely regarded as a barometer of the U.S. stock market’s performance. Investors and analysts closely monitor the movements of the Dow to gauge the overall health of the economy. When the DJIA rises, it generally suggests that investors are optimistic about the economic outlook and that large companies are performing well. Conversely, when the DJIA falls, it often signals economic uncertainty or a downturn in market conditions.

Despite being a narrow index, with only 30 companies, the DJIA holds substantial sway in financial markets. It is widely covered in the media and is often cited in discussions about the state of the economy. In fact, the performance of the DJIA is considered a key indicator of investor sentiment and economic confidence.

However, the DJIA has its limitations. Since it only includes 30 companies, it does not necessarily represent the broader market or capture the performance of smaller companies. Other indices, like the S&P 500, which includes 500 companies, offer a more comprehensive view of the market’s performance.

Conclusion

The Dow Jones Industrial Average is a key metric for understanding the state of the U.S. economy and the stock market. Although it has evolved over the years, it continues to provide valuable insights into the performance of large, influential companies. While it is not a perfect reflection of the market as a whole, the DJIA remains one of the most important and widely recognized indices in global finance. Through its historical significance and its role in shaping market sentiment, the Dow has cemented its place as a cornerstone of financial analysis.

Posted on October 9, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Co-Pilot

***

***

Artificial Intelligence in Finance: Revolutionizing the Industry

Artificial Intelligence (AI) is rapidly transforming the financial services industry, reshaping how institutions operate, manage risk, and serve customers. By leveraging machine learning, natural language processing, and predictive analytics, AI is enabling smarter decision-making, greater efficiency, and enhanced customer experiences across banking, investing, insurance, and regulatory compliance.

One of the most impactful applications of AI in finance is in fraud detection and prevention. Traditional systems rely on rule-based algorithms that often fail to catch sophisticated schemes. AI, however, can analyze vast amounts of transaction data in real time, identifying patterns and anomalies that signal fraudulent behavior. Machine learning models continuously improve as they process more data, making them increasingly effective at detecting threats and reducing false positives.

AI also plays a pivotal role in algorithmic trading, where decisions are made at lightning speed based on complex data inputs. These systems can process news articles, social media sentiment, and market data to execute trades with precision. Hedge funds and investment banks use AI to optimize portfolios, forecast market trends, and identify arbitrage opportunities that human analysts might miss.

In personal finance and banking, AI enhances customer service through chatbots and virtual assistants. These tools handle routine inquiries, assist with transactions, and offer financial advice based on user behavior. AI-driven platforms like robo-advisors provide personalized investment strategies, adjusting portfolios automatically based on market conditions and individual goals. This democratizes access to financial planning, making it more affordable and scalable.

Credit scoring and lending have also been revolutionized by AI. Traditional credit models often rely on limited data and can be biased against certain demographics. AI can incorporate alternative data sources—such as utility payments, social media activity, and online behavior—to assess creditworthiness more accurately and inclusively. This opens up lending opportunities for underserved populations and reduces default risk for lenders.

In insurance, AI streamlines underwriting and claims processing. By analyzing historical data and customer profiles, AI can assess risk more precisely and tailor policies to individual needs. During claims, AI can automate document review, detect fraud, and expedite payouts, improving both operational efficiency and customer satisfaction.

Regulatory compliance, or RegTech, is another area where AI shines. Financial institutions face increasing scrutiny and complex regulations. AI tools can monitor transactions, flag suspicious activity, and ensure adherence to legal standards. Natural language processing helps parse regulatory documents and automate reporting, reducing the burden on compliance teams.

Despite its benefits, AI in finance raises ethical and operational challenges. Data privacy, algorithmic bias, and transparency are critical concerns. Financial institutions must ensure that AI systems are explainable, fair, and secure. Regulatory bodies are beginning to address these issues, but ongoing collaboration between technologists, policymakers, and industry leaders is essential.

In conclusion, artificial intelligence is not just enhancing finance—it’s redefining it. From fraud prevention to personalized banking, AI is driving innovation and efficiency. As the technology matures, its integration must be guided by ethical principles and robust governance to ensure that the financial system remains fair, resilient, and inclusive.

Artificial Intelligence and Investing: A Transformative Partnership

Artificial Intelligence (AI) is revolutionizing the world of investing, reshaping how decisions are made, risks are assessed, and portfolios are managed. As financial markets grow increasingly complex and data-driven, AI offers powerful tools to navigate this landscape with greater precision, speed, and insight.

At its core, AI refers to systems that can perform tasks typically requiring human intelligence—such as learning, reasoning, and problem-solving. In investing, this translates into algorithms that can analyze vast amounts of financial data, detect patterns, and make predictions with remarkable accuracy. Machine learning, a subset of AI, enables these systems to improve over time by learning from new data, making them especially valuable in dynamic markets.

One of the most significant applications of AI in investing is algorithmic trading. These systems can execute trades at lightning speed, responding to market fluctuations in milliseconds. By analyzing historical data and real-time market conditions, AI-driven trading platforms can identify optimal entry and exit points, often outperforming human traders. High-frequency trading firms have long relied on such technologies to gain competitive advantages.

AI also enhances portfolio management through robo-advisors—digital platforms that use algorithms to provide personalized investment advice. These tools assess an investor’s goals, risk tolerance, and time horizon, then construct and manage a diversified portfolio accordingly. Robo-advisors democratize access to financial planning, offering low-cost, automated solutions to individuals who might not afford traditional advisory services.

Risk assessment is another area where AI shines. By processing alternative data sources—such as social media sentiment, news articles, and satellite imagery—AI can uncover hidden risks and opportunities. For instance, a sudden spike in negative sentiment around a company on Twitter might signal reputational issues, prompting investors to reevaluate their positions. AI models can also forecast macroeconomic trends, helping investors anticipate shifts in interest rates, inflation, or geopolitical events.

Moreover, AI is transforming fundamental analysis. Natural language processing (NLP) allows machines to read and interpret earnings reports, SEC filings, and analyst commentary. This enables investors to extract insights from unstructured data that would be time-consuming to analyze manually. AI can even detect subtle linguistic cues that may indicate a company’s future performance or management’s confidence.

Despite its advantages, AI in investing is not without challenges. Models can be opaque, making it difficult to understand how decisions are made—a phenomenon known as the “black box” problem. There’s also the risk of overfitting, where algorithms perform well on historical data but fail in real-world scenarios. Ethical concerns, such as bias in data and the potential for market manipulation, must also be addressed.

In conclusion, AI is reshaping the investing landscape, offering tools that enhance efficiency, accuracy, and accessibility. While it’s not a panacea, its integration into financial markets marks a profound shift in how capital is allocated and wealth is managed. As technology continues to evolve, investors who embrace AI will be better positioned to thrive in an increasingly data-driven world.

Public Relations [PR] is differentiated than advertising in that an advertiser pays for and has control over the message. It differs from personal selling in that the message is non-personal, i.e., not directed to a particular individual patient. We pay for advertising but pray for public relations. Public relations are not controllable but it is free; advertising is not free. PR suggests that “good news or bad news”; just spell the doctors name correctly

Change Management is the discipline that guides how we prepare, equip and support individuals to successfully adopt to change in order to drive organizational success and outcomes.

For example, a senior doctor may retire, become ill, or a junior associate might become a practice partner. How will patients be affected?

Crisis Management is the precautions and identification of threats to an organization and its stakeholders, and the methods used by the organization to deal with these threats.

For example, recall in 1982, that Tylenol™ commanded 35 percent of the over-the-counter analgesic market in America and it represented nearly 17 percent of Johnson & Johnson’s profits. But, when seven people died from consuming the tainted drug, a national panic ensued. Moreover, Americans started to question the safety of all over-the-counter medications.

Fortunately, J&J commenced the proto-typical positive crisis response in the following way:

J&J acted quickly, with complete candidness about what happened and within hours of learning of the deaths, J&J installed toll-free numbers for consumers, sent alerts to healthcare providers nationwide, and stopped advertising the product. J&J recalled 31 million bottles of Tylenol™ capsules and offered replacement products free of charge. J&J did not wait for evidence to see whether the contamination might be more widespread.

J&J’s leadership was in the lead and seemed in full control throughout the crisis. The chairman was admired for his leadership to pull Tylenol™ capsules off the market and his forthrightness in dealing with the media. The Tylenol™ crisis led the news every night on every station for six weeks.

J&J placed consumers first. J&J spent more than $100 million for the recall and re-launch of Tylenol™. The stock which had been trading near a 52-week high just before the tragedy, dropped for a time, but recovered to its highs only two months later.

J&J accepted responsibility. The disaster could have been described in many different ways: as an assault on the company, as a problem somewhere in the process of getting Tylenol™ from J&J factories to retail stores, or as the acts of a crazed criminal. Yet, the company accepted full responsibility.

J&J sought to ensure that measures were taken to prevent a recurrence of the problem. J&J introduced tamper-proof packaging that would make it much more difficult for a similar incident to occur in the future.

J&J presented itself prepared to handle the short-term damage in the name of consumer safety. Within a year of the disaster, J&J’s share of the analgesic market, which had fallen to 7 percent from 37 percent following the poisoning, had climbed back to 30 percent.

This wildly successful response in now the stuff of graduate and business school case models for excellence in teaching!

PRM stands for Patient Relationship Management, which is a system for managing all interactions with current and potential patients, families, friends, referring physicians, clinics and hospitals. The goal is simple: improve relationships to grow your medical practice. PRM technology helps medical practices and clinics stay connected to patients, streamline processes, and improve profitability.

When people talk about PRM, they’re usually referring to a PRM system: software that helps track each interaction with a patient or elated others. That can include practice sales calls, treatment or service plans, marketing e-mails, website, social media and more. PRM tools can unify patient and practice data from many sources and even use Artificial Intelligence [AI] to help better manage relationships across the entire doctor– patient lifecycle – spanning departments described elsewhere in the Marketing, Advertising and Sales ME-Ps.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

References:

1. Purcarea, Victor: The impact of marketing strategies in healthcare systems. J. Med Life. 2019 Apr-Jun;12(2):93–96. doi: 10.25122/jml-2019-1003

READINGS:

Marcinko, DE and Hetico, HR: The Business of Medical Practice [3rd Edition]. Springer Publishing, New York, 2010.

Marcinko, DE and Hetico, HR: Hospitals & Healthcare Organizations [Management Strategies, Operational Techniques, Tools, Templates and Case Studies]. Productivity Press, New York, 2012.

Marcinko, DE and Hetico, HR: Financial Management Strategies for Hospitals and Healthcare Organizations [Tools, Techniques, Checklists and Case Studies]. Productivity Press, New York, 2012.

A Financial Self Discovery Questionnairefor Medical Professionals

For understanding your relationship with money, it is important to be aware of yourself in the contexts of culture, family, value systems and experience. These questions will help you. This is a process of self-discovery. To fully benefit from this exploration, please address them in writing. You will simply not get the full value from it if you just breeze through and give mental answers. While it is recommended that you first answer these questions by yourself, many people relate that they have enjoyed the experience of sharing them with others who are important to them.

As you answer these questions, be conscious of your feelings, actually describing them in writing as part of your process.

Childhood

What is your first memory of money?

What is your happiest moment with Money? Your most unhappy?

Name the miscellaneous money messages you received as a child.

How were you confronted with the knowledge of differing economic circumstances among people, that there were people “richer” than you and people “poorer” than you?

Cultural heritage

What is your cultural heritage and how has it interfaced with money?

To the best of your knowledge, how has it been impacted by the money forces? Be specific.

To the best of your knowledge, does this circumstance have any motive related to Money?

Speculate about the manners in which your forebears’ money decisions continue to affect you today?

Family

How is/was the subject of money addressed by your church or the religious traditions of your forebears?

What happened to your parents or grandparents during the Depression?

How did your family communicate about money?

How? Be as specific as you can be, but remember that we are more concerned about impacts upon you than historical veracity.

When did your family migrate to America (or its current location)?

What else do you know about your family’s economic circumstances historically?

Your parents

How did your mother and father address money?

How did they differ in their money attitudes?

How did they address money in their relationship?

Did they argue or maintain strict silence?

How do you feel about that today?

Please do your best to answer the same questions regarding your life or business partner(s) and their parents.

Childhood: Revisited

How did you relate to money as a child? Did you feel “poor” or “rich”? Relatively? Or, absolutely? Why?

Were you anxious about money? Did you receive an allowance? If so, describe amounts and responsibilities.

Did you have household responsibilities?

Did you get paid regardless of performance?

Did you work for money?

If not, please describe your thoughts and feelings about that.

***

***

Same questions, as a teenager, young adult, older adult.

Credit

When did you first acquire something on credit?

When did you first acquire a credit card?

What did it represent to you when you first held it in your hands?

Describe your feelings about credit.

Do you have trouble living within your means?

Do you have debt?

Adulthood

Have your attitudes shifted during your adult life? Describe.

Why did you choose your personal path? a) Would you do it again? b) Describe your feelings about credit.

Adult attitudes

Are you money motivated? If so, please explain why? If not, why not? How do you feel about your present financial situation? Are you financially fearful or resentful? How do you feel about that?

Will you inherit money? How does that make you feel?

If you are well off today, how do you feel about the money situations of others? If you feel poor, same question.

How do you feel about begging? Welfare? If you are well off today, why are you working?

Do you worry about your financial future?

Are you generous or stingy? Do you treat? Do you tip?

Do you give more than you receive or the reverse? Would others agree?

Could you ask a close relative for a business loan? For rent/grocery money?

Could you subsidize a non-related friend? How would you feel if that friend bought something you deemed frivolous?

Do you judge others by how you perceive they deal with their Money? Do you feel guilty about your prosperity? Are your siblings prosperous?

What part does money play in your spiritual life?

Do you “live” your Money values?

Conclusion

There may be other questions that would be useful to you. Others may occur to you as you progress in your life’s journey. The point is to know your personal money issues and their ramifications for your life, work, and personal mission.

This will be a “work-in-process” with answers both complex and incomplete. Don’t worry.

Just incorporate fine-tuning into your life’s process.

Posted on September 22, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Authentication:

The verification of the identity of an individual, system, machine, or any other unique entity

Authorization:

The process of allowing access to specific areas of a system based on the role and needs of the user

Committee Charter:

A document that defines the purposes and responsibilities of the oversight committee

Compliance Risk Profile:

The current and prospective risk to earnings or capital arising from violations of or nonconformance with laws, rules, regulations, prescribed practices, internal policies and procedures, or ethical standards

Control Assessment:

A high-level review and analysis of controls relating to a process; should encompass both current and missing controls

Controls:

Methods that preserve the integrity of important information, meet operational or financial targets, and/or communicate management policies (See also: Key Control, Secondary Control, Tertiary Control)

ERM Policy Statement:

Defines an organization’s approach to and method of enterprise risk management

Governance:

Processes and structures implemented to communicate, manage, and monitor organizational activities

Impact:

The influence and effect of a risk

Inherent Risk:

Risk that is inherent to a process, taking into consideration the likelihood and impact of a risk

Key Control:

A primary control that is essential for a business process; typically takes place during the process it applies to

Key Indicators:

Measurements that are important for organizations to monitor for potential issues; examples include key performance indicators (KPIs) and key risk indicators (KRIs)

Key Performance Indicator (KPI):

A measurement with a defined set of goals and tolerances that gauges the performance of an important business activity

Key Risk Indicator (KRI):

A proactive measurement for future and emerging risks that indicates the possibility of an event that adversely affects business activities

Likelihood:

The probability of a risk occurring

Mitigation Actions:

The necessary steps, or action items, to reduce the likelihood and/or impact of a potential risk

Operation Risk Profile:

1) The risk arising from the execution of an organization’s business processes; 2) The risk of loss resulting from failed or inadequate internal processes, systems, people, or other entities

Price Risk Profile:

The risk to earning or capital arising from adverse changes in portfolio values

Process:

1) The principle elements of essential business functions within work groups or business units; 2) A set of tasks completed by business continuity plan owners within a department

Reputation Risk Profile:

The current and prospective risk to earnings or capital arising from negative public opinion or perception

Residual Risk:

Risk remaining after considering the existing control environment

Risk:

A potential event or action that would have an adverse effect on the organization

Risk Appetite:

A statement that broadly considers the risk levels that management deems acceptable

Risk Assessment:

The prioritization of potential business disruptions based on the impact and likelihood of occurrence; includes an analysis of threats based on the impact to the organization, its customers, and financial markets

Risk Tolerance:

A metric that sets the acceptable level of variation around organizational objectives and provides assurance that the organization remains within its risk appetite

Secondary Control:

An important control that typically takes place after the process it applies to (i.e., reporting or ongoing monitoring)

Strategic Risk Profile:

The current and prospective risk to earnings or capital raising from adverse business decisions, improperly implemented decisions, or lack of responsiveness to industry changes

Tertiary Control:

A non-essential control that can still be applied effectively to a business process

Velocity:

The time it takes a risk event to manifest itself

Vulnerability:

An entity’s susceptibility to a risk event as determined by the entity’s preparedness, agility, and adaptability

Investment bankers are not really bankers at all. The fact that the word banker appears in the name is partially responsible for the false impressions that exist in the medical community regarding the functions they perform.

For example, they are not permitted to accept deposit, provide checking accounts, or perform other activities normally construed to be commercial banking activities. An investment bank is simply a firm that specializes in helping other corporations obtain money they need under the most advantageous terms possible. When it comes to the actual process of having securities issued, the corporation approaches an investment banking firm, either directly, or through a competitive selection process and asks it to act as adviser and distributor.

Investment bankers, or under writers, as they are sometimes called, are middlemen in the capital markets for corporate securities. The corporation requiring the funds discusses the amount, type of security to be issued, price and other features of the security, as well as the cost to issuing the securities. All of these factors are negotiated in a process known as negotiated underwriting. If mutually acceptable terms are reached, the investment banking firm will be the middle man through which the securities are sold to the general public. Since such firms have many customers, they are able to sell new securities, without the costly search that individual corporations may require to sell its own security.

Thus, although the firm in need of additional capital must pay for the service, it is usually able to raise the additional capital at less expense through the use of an investment banker, than by selling the securities itself. The agreement between the investment banker and the corporation may be one of two types. The investment bank may agree to purchase, or underwrite, the entire issue of securities and to re-offer them to the general public. This is known as a firm commitment.

When an investment banker agrees to underwrite such a sale; it agrees to supply the corporation with a specified amount of money. The firm buys the securities with the intention to resell them. If it fails to sell the securities, the investment banker must still pay the agreed upon sum.

Thus, the risk of selling rests with the underwriter and not with the company issuing the securities.

The alternative agreement is a best efforts agreement in which the investment banker makes his best effort to sell the securities acting on behalf of the issuer, but does not guarantee a specified amount of money will be raised. When a corporation raises new capital through a public offering of stock, one might inquire where the stock comes from. The only source the corporation has is authorized, but previously un-issued stock. Anytime authorized, but previously un-issued stock (new stock) is issued to the public, it is known as a primary offering.

If it’s the very first time the corporation is making the offering, it’s also known as the Initial Public Offering (IPO). Anytime there is a primary offering of stock, the issuing corporation is raising additional equity capital.

A secondary offering, or distribution, on the other hand, is defined as an offering of a large block of outstanding stock. Most frequently, a secondary offering is the sale of a large block of stock owned by one or more stockholders. It is stock that has previously been issued and is now being re-sold by investors. Another case would be when a corporation re-sells its treasury stock.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Ikea Effect Bias describes the tendency of people to place a higher value on products they have partially created or assembled themselves. This phenomenon is named after the Swedish furniture retailer Ikea, known for selling furniture in flat-pack kits that customers must assemble at home.

he IKEA effect was identified and named by Michael Norton of Harvard Business School, Daniel Mochon of Yale University and colleague Dan Ariely PhD of Duke University, who published the results of three studies in 2011. They described the IKEA effect as “labor alone can be sufficient to induce greater liking for the fruits of one’s labor: even constructing a standardized bureau, an arduous, solitary task, can lead people to overvalue their (often poorly constructed) creations.”

Example: A prospect is more likely to pursue his/her own financial plan than that one from an informed financial planner, CPA or professional advisor.

2011 study found that subjects were willing to pay 63% more for furniture they had assembled themselves than for equivalent pre-assembled items.

IN FINANCE AND INVESTING

The IKEA effect can contribute to reducing panic selling. Investors typically reduce their stock market exposure after a financial crash which often results in “buy high, sell low” strategy that is detrimental to long-run wealth accumulation.

Ashtiani et al.’s study proposes a nudge utilizing the IKEA effect to counteract this phenomenon: “actively involving investors in the selection process of the risky investments, while restricting their selections in a way that preserves a large degree of diversification.”

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on July 5, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By A.I.

***

***

Medical doctors, dentists, and podiatrists have to undergo extensive training before they can practice medicine independently. Once they receive training, there are opportunities to increase pay and prestige in the medical field through a series of promotions. As a doctor, how much training, experience and skills you have can determine your ability to move upward in these levels. But, personal branding strategies may even be more vital in today’s social media age?

***

Physician, medical and healthcare branding is more than just the creation of logos, taglines, or specific brand messaging. It’s about creating a meaningful connection between your mission, vision and values and the people served – from patients and their families to local and global communities.

While there are many different types of branding strategies in marketing science, they all share key elements that serve as the foundation for the strategy. These 9 elements for all physicians and medical professionals include the following:

Brand purpose: The reason the physician is in practice and what he/she is trying to achieve.

Brand vision: The ideas and goals behind the dentist which serve as inspiration for practice growth.

Brand values: The osteopaths beliefs and what they stand for.

Target audience: The demographic(s) and patient targets that the podiatrist is aiming to reach.

Market analysis: An analysis of the marketplace that identifies gaps where the chiropractor has an opportunity to position him/her self based on a unique value proposition.

Awareness goals: The initiatives the doctor will take in order to reach a target market patient demographic.

Brand personality: The human-like attributes of the physician that will help build relationships with patients, consumers and other physicians and practitioners.

Brand voice: The language and tone the doctor uses to communicate with patients, physicians and consumers.

Brand tagline: A memorable slogan that sums up the physician and their medical offering in a few choice words.

And so, physician branding is the development of a easily recognizable identity for a medical practice, clinic or healthcare organization that helps to shape perception by current and prospective patients and the wider world.

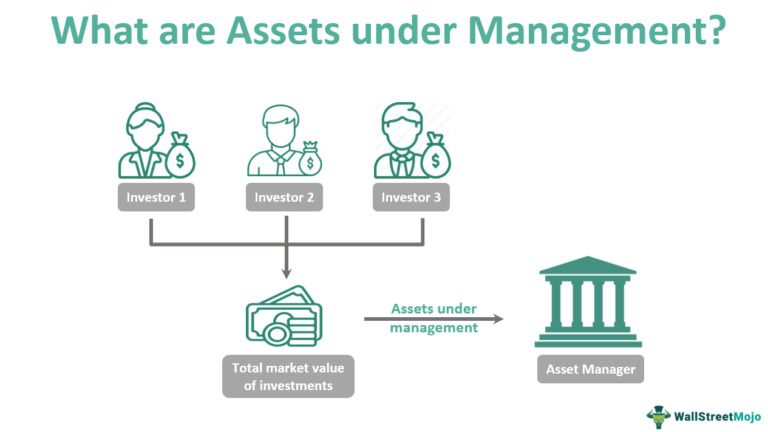

Assets under management (AUM) is a significant parameter in the financial world. It answers financial questions like – how many investments does a company manage? What is the net value of the investments that the company manages? Finally, how many investors have trusted their assets with the company? The higher the answer to these three questions, the more glory to the company.

A wealthy investor who is not concerned by higher fees but wants maximum returns of their asset will probably choose an asset manager based on its AUM. Thus, the AUM indicates the financial performance of the firm. Also, based on the funds under management, the firm collects fees from other clients.

So, what are the investments which qualify as AUM? Any liquid asset of the investor they have entrusted the asset manager with monitoring and control. For example, bank deposits, cash balances, equity shares, bonds, mutual funds, and other investments.

What are the services an asset manager provides to their clients? The most important function is decision-making. With the constant fluctuations and rapid movements in the market, an asset manager has to make decisions about holding or selling an investment. The firm communicates with the investors and advises them about the necessary action.

Once the decision is taken, the firm acts on the decision, i.e., the investor does not have to enter the field. In addition, the asset management company will buy, sell, and make any other transactions on behalf of the investor. Finally, the firm also renders services like accounting, tax reporting, proxy voting (equity shares), client reporting, and other financial services.

What are Assets Under Advisement?

Assets under advisement refer to assets on which your firm provides advice or consultation but for which your firm does either does not have discretionary authority or does not arrange or effectuate the transaction. Such services would include financial planning or other consulting services where the assets are used for the informational purpose of gaining a full perspective of the client’s financial situation, but you are not actually placing the trade.

Assets under advisement could also be those which you monitor for a client on a non-discretionary basis, where you may make recommendations but where the client is the party responsible for arranging or effecting the purchase or sale. A common example of this scenario is when an adviser reviews a participant’s 401(k) allocations. If the adviser does not have the authority or ability to effect changes in the portfolio, these assets are likely considered assets under advisement rather than regulatory assets under management.

Assets under advisement are permitted to be disclosed on Form ADV Part 2A as a separate asset figure from the assets under management. There is no requirement to disclose the assets under advisement figure, but some advisers opt to include the figure to give prospective clients a more complete picture of the firm’s responsibilities. If you choose to report your assets under advisement, be sure to make a clear distinction between this figure and your regulatory assets under management.

The Zweig Breadth Thrust may sound like an extremely difficult yoga position, but it’s actually a bullish technical indicator with an extraordinary record of 100% accuracy that was just triggered.

Created by investment advisor and author Martin Zweig, the indicator takes the 10-day moving average of the number of advancing stocks across the market and divides it by the number of advancing stocks plus the number of declining stocks. When the resulting percentage rises from below 40% to above 61.5% in 10 trading days, it’s a sign that stocks are rapidly going from oversold to overbought.

The math is a bit complicated, but Carson Research’s Chief Market Strategist Ryan Detrick certainly thinks highly of it.

According to the chart that he just posted on X, the Zweig Breadth Thrust has a perfect record of predicting market gains 6 and 12 months after it appears.

With the indicator triggering on Friday, here’s hoping that we can continue to trust the Zweig Thrust.

A Certified Public Accountant (CPA) is a licensed professional who has passed an examination administered by a state’s Board of Accountancy. State CPA exams are created under guidelines issued by The American Institute of Certified Public Accountants (AICPA). The Uniform CPA Exam can only be taken by accountants who already have professional experience in the field and a bachelor’s degree.CPAs are not fiduciaries.

Not all accountants are CPAs. Accountants who are CPAs are licensed by their state’s Board of Accountancy after passing the Uniform CPA Exam. CPAs prepare reports that accurately reflect the business dealings of the companies and individuals that hire them. Many prepare tax returns for individuals or businesses and advise them on ways to minimize taxes. Obtaining the CPA designation requires a bachelor’s degree, typically with a major in business administration, finance, or accounting. Other majors are acceptable if the applicant meets the minimum requirements for accounting courses.

Enrolled Agent

Although not a CPA, an Enrolled Agent [EA] is a person who has earned the privilege of representing taxpayers before the Internal Revenue Service [IRS]. This is done by either passing a three-part comprehensive IRS test covering individual and business tax returns, or through experience as a former IRS employee. Enrolled agent status is the highest credential the IRS awards. Individuals who obtain this elite status must adhere to ethical standards and complete 72 hours of continuing education courses every three years.

Certified Managerial Accountant

A Certified Management Accountant (CMA), which is issued by the Institute of Management Accountants (IMA), builds on financial accounting proficiency by adding management skills that aid in making strategic business decisions based on financial data.

Oftentimes, the reports and analyses prepared by certified management accountants (CMAs) will go above and beyond those required by generally accepted accounting principles (GAAP).

For example, in addition to a company’s required GAAP financial statements, CMAs may prepare additional management reports that provide specific insights useful to corporate decision-makers, such as performance metrics on specific company departments, products, or even employees.

Certified Financial Analyst

A Certified Financial Analyst [CFA] is a globally-recognized professional designation offered by the CFA Institute, an organization that measures and certifies the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management, and security analysis. From 1963 through November 2023, more than 3.7 million candidates had taken the CFA exam. The overall pass rate was 45%. From 2014 through 2023, the 10-year average pass rate was 43%.1

CFA Institute. The CFA Institute was formerly the Association for Investment Management and Research (AIMR).

The CFA charter is one of the most respected designations in finance and is widely considered to be the gold standard in the field of investment analysis. To become a charter holder, candidates must pass three difficult exams, have a bachelors degree, and have at least 4,000 hours of relevant professional experience over a minimum of three years. Passing the CFA Program exams requires strong discipline and an extensive amount of studying.

There are more than 200,000 CFA charter holders worldwide in 164 countries.The designation is handed out by the CFA Institute, which has 11 offices worldwide and 160 local member societies.

There’s often a disconnect between physicians, insurance agents and financial advisors and the patients and clients they’d like to serve. Both might ostensibly share the same goal but there’s often a big difference in perspective. Advisors / Physicians and would-be clients / patients likely have different communication styles, especially in an age where technology has greatly changed the way we talk with one another. Their expectations and priorities can also often dramatically diverge. Those structural gaps can hinder collaboration and trust.

To bridge this divide, you must understand how prospective clients and patients think nowadays and be able to adjust your M.A.S. approach accordingly.

THE BASICS

Marketing is the business process of identifying, anticipating and satisfying patient’s, client’s or customers’ needs and wants. It is your unique value proposition or strategic competitive advantage. Marketers can direct product to other businesses or directly to consumers. But, we believe it is actually your strategic competitive advantage [SCA] which differentiates yourself from competitors. It is the “moat” around your business.

Advertising is a marketing communication that employs an openly sponsored, non-personal message to promote or sell a product, service or idea. Sponsors of advertising are typically businesses wishing to promote their products or services. Advertising is communicated through various mass media outlet, including traditional media such as newspapers, magazines, television, radio, outdoor advertising or direct mail; and new media such as search results, blogs, social media, websites or text messages. The actual presentation of the message in a medium is referred to as an advertisement, or “ad” or advert for short. But, we believe that is simply how you disseminate your strategic competitive advantage [SCM] to potential clients.

Sales close the deal and collects money. Sales are activities related to selling or the number of goods or services sold in a given targeted time period. The seller, or the provider of the goods or services, completes a sale in response to an acquisition, appropriation, requisition, or a direct interaction with the buyer at the point of sale. There is a passing of title (property or ownership) of the item, and the settlement of a price, in which agreement is reached on a price for which transfer of ownership of the item will occur. The seller, not the purchaser, typically executes the sale and it may be completed prior to the obligation of payment. In the case of indirect interaction, a person who sells goods or service on behalf of the owner is known as a salesman or saleswoman or salesperson, but this often refers to someone selling goods in a store/shop, in which case other terms are also common, including salesclerk, shop assistant, and retail clerk.

***

***

DERIVATIVE THOUGHTS

Public Relations [PR] is differentiated than advertising from in that an advertiser pays for and has control over the message. It differs from personal selling in that the message is non-personal, i.e., not directed to a particular individual. We pay for advertising but pray for public relations. But public relations are not controllable but it is free, while advertising is not. PR suggests that “good news or bad news”; just spell the name correctly

Change Management is the discipline that guides how we prepare, equip and support individuals to successfully adopt to change in order to drive organizational success and outcomes.

Crisis Management is the precautions and identification of threats to an organization and its stakeholders, and the methods used by the organization to deal with these threats.

MODERNITY NOW

CRM stands for Customer Relationship Management, which is a system for managing all interactions with current and potential customers, clients or patients. The goal is simple: improve relationships to grow your business or medical practice. CRM technology helps companies stay connected to customers, streamline processes, and improve profitability.

When people talk about CRM, they’re usually referring to a CRM system: software that helps track each interaction you have with a prospect, patient or customer. That can include sales calls, treatment plans or service interactions, marketing e-mails, and more. CRM tools can unify customer and company data from many sources and even use Artificial Intelligene [AI] to help better manage relationships across the entire customer – patient lifecycle – spanning departments described in the M.A.S. basics, above.

Posted on April 18, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

U.S. stock and bond markets will be closed on Good Friday. Many global markets will also be closed Friday. Exceptions include Japan and mainland China, which will be open as usual. U.S. markets will reopen Monday. Many international markets will remain shut to mark Easter Monday, including Australia, Hong Kong, and exchanges in France, Germany and the U.K.

***

YESTERDAY 4/17/25

***

🟢 What’s up

TSMC eked out a 0.10% gain after the semiconductor maker reported a 60% increase in profits last quarter and downplayed the effects of tariffs.

Charles Schwab isn’t just the guy who made $2 billion from market chaos last week. It’s also the brokerage that reported record quarterly revenue, but shares only rose 0.65%.

Hertz climbed another 43.87%, tacking on another day of big wins after Bill Ackman’s Pershing Square Capital took a stake in the rental car company.

Trump Media & Technology Group popped 11.65% after the company asked the SEC to investigate a hedge fund with a $105 million short bet against it.

Chinese tea chain Chagee soared 15.86% in its first day of trading on the Nasdaq.

DR Horton missed analyst expectations last quarter and lowered its fiscal year guidance, but investors quickly forgave the country’s largest homebuilder and pushed shares up 3.16%.

What’s down

Alphabet took a 1.38% hit after a federal judge ruled that Google is a monopoly. This marks Alphabet’s second antitrust loss since last August.

Alcoa fell 6.98% after the aluminum mining behemoth announced it ate about $20 million in tariff-related costs last quarter, noting that this figure could rise to $90 million in the current quarter.

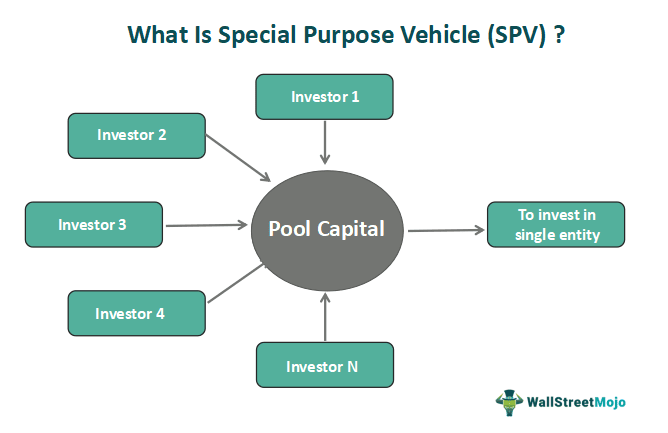

Its purpose is to isolate the parent company from any potential credit or financial risk that may arise from the SPV and is often used to pursue riskier projects, securitize debt, or transfer assets. Since an SPV is separate from the parent company, it isn’t affected by the parent’s performance, and the parent isn’t typically affected by the performance of the SPV. If the parent goes bankrupt and is no longer in existence, the SPV can carry on.

This makes an SPV bankruptcy remote. This also means that the parent company is unaffected by the loss if the SPV fails.

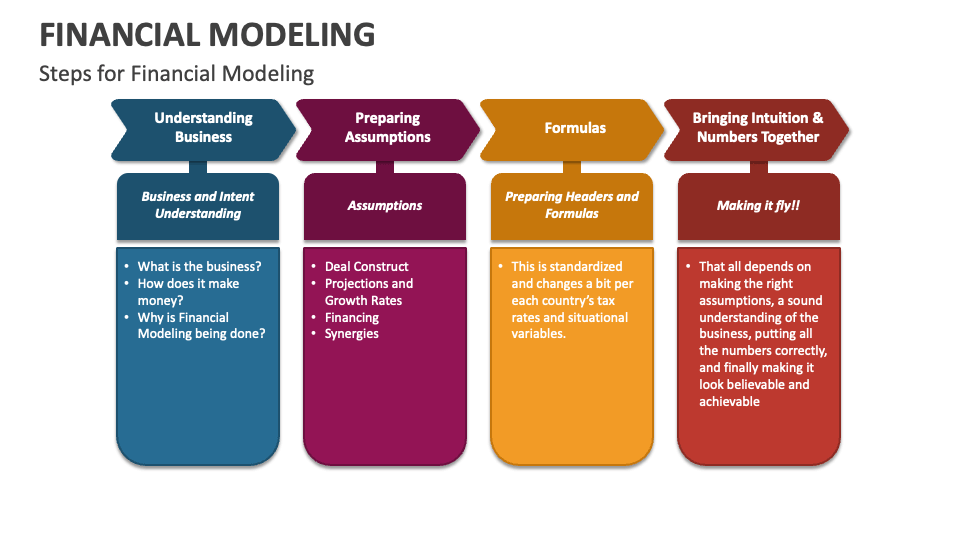

Financial Modeling is one of the most highly valued, but thinly understood, skills in financial analysis. The objective of financial modeling is to combine accounting, finance, and business metrics to create a forecast of a company’s future results.

According to Jeff Schmidt, a financial model is simply a spreadsheet, usually built in Microsoft Excel, that forecasts a business’s financial performance into the future. The forecast is typically based on the company’s historical performance and assumptions about the future and requires preparing an income statement, balance sheet, cash flow statement, and supporting schedules (known as a three-statement model, one of many types of approaches to financial statement modeling). From there, more advanced types of models can be built such as discounted cash flow analysis (DCF model), leveraged buyout (LBO), mergers and acquisitions (M&A), and sensitivity analysis

***

DEFINED TERMS

Discounted Cash Flow (DCF): A valuation method used to estimate the value of an investment based on its expected future cash flows, adjusted for the time value of money. It’s like deciding whether a treasure chest is worth diving for now, based on the gold coins you’ll be able to cash in later.

Sensitivity Analysis: This involves changing one variable at a time to see how it affects an outcome. Imagine tweaking your coffee-to-water ratio each morning to achieve the perfect brew strength.

Budget – A budget is the amount of money a department, function, or business can spend in a given period of time. Usually, but not always, finance does this annually for the upcoming year.

Rolling Forecast – A rolling forecast maintains a consistent view over a period of time (often 12 months). When one period closes, finance adds one more period to the forecast.

Topside – A topside adjustment is an overlay to a forecast. This is typically completed by the corporate or headquarter team. As individual teams submit a forecast, the consolidated result might not make sense or align with expectations. When this occurs, the high-level teams use a topside adjustment to streamline or adjust the consolidated view.

Monte Carlo Simulation: Picture yourself at the casino, but instead of gambling your savings away, you’re using this technique to predict different outcomes of your business decisions based on random variables. It’s like playing financial roulette with the odds in your favor.

What-If Analysis: Ever daydream about what would happen if you took that leap of faith with your business? This tool allows you to explore various scenarios without risking a dime. It’s like trying on outfits in a virtual dressing room before making a purchase.

Leveraged Buyout (LBO) Model: This is a bit like orchestrating a heist, but legally. It’s about acquiring a company using borrowed money, with plans to pay off the debts with the company’s own cash flows. High stakes, high rewards.

Mergers and Acquisitions (M&A) Model: Picture two puzzle pieces coming together. This model evaluates how combining companies can create a new, more valuable entity. It’s the corporate version of a matchmaker.

Three Statement Model: The holy trinity of financial modeling, linking the income statement, balance sheet, and cash flow statement. It’s like weaving a tapestry where each thread is crucial to the overall picture.

Capital Asset Pricing Model (CAPM): A formula that calculates the expected return on an investment, considering its risk compared to the market. It’s like choosing the best roller coaster in the park, balancing thrill and safety.

Cash Flow Forecasting: This is your financial weather forecast, predicting the cash flow climate of your business. It helps you plan for sunny days and save for the rainy ones.

Cost of Capital: The price of financing your business, whether through debt or equity. It’s like the interest rate on your growth engine, pushing you to maximize every dollar invested.

Debt Schedule: A timeline of your business’s debts, showing when and how much you owe. It’s your roadmap to becoming debt-free, one milestone at a time.

Equity Valuation: Determining the value of a company’s shares. It’s like assessing the worth of a rare gemstone, ensuring investors pay a fair price for a piece of the treasure.

Financial Leverage: Using debt to amplify returns on investment. It’s like using a lever to lift a heavy object, increasing force but also risk.

Forecast Model: A crystal ball for your finances, projecting future performance based on past and present data. It’s your guide through the financial wilderness, helping you navigate with confidence.

Operating Model: A detailed blueprint of how a business generates value, mapping out operational activities and their financial impact. It’s like laying out the inner workings of a clock, ensuring every gear turns smoothly.

Revenue Growth Model: This tracks potential increases in sales over time, charting a course for expansion. It’s like plotting your ascent up a mountain, anticipating the effort required to reach the summit.

Posted on March 31, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

[Reviewing Terms, Conditions and Selling Agreements]

By Dr. Charles F. Fenton III JD

***

***

Dealing with many issues concerning the actual contract that affect the purchase or sale of a medical practice can be daunting. For example, this chapter will not deal with issue of determining whether or not a physician should retire. Nor will it determine the proper Fair Market Value [FMV] of the practice. However, physicians may be assisted in both instances by a medically focused financial advisor, or valuation specialist. [AVA, CPA-CVA, Certified Medical Planner™; etc] working in conjunction with an experience health care contract attorney to act as an advocate and determine certain contingencies that might occur, and protect him/her from them.

THE PARTIES

The first determination is whether the party at interest is an individual, group of individuals, or an entity (such as a partnership, limited liability partnership, limited partnership, limited liability company, or corporation – whether an S corporation, C corporation or a professional corporation). In many instances, even if the party at interest is an individual is an entity, the individual or individuals behind the entity should be made parties to the agreement.

From the buyer’s perspective, the purchase of a medical practice is a highly person-oriented business. The practice value depends much upon the personality of the current treating physicians. If the current treating physicians are also the owners of the entity, then binding those individuals (especially as applies to the restrictive covenant) is of primary importance.

If the current treating physicians are not owners of the entity, but rather employees, then a determination of whether they will continue in their same positions or whether the buyer will be taking over the treatment of patients becomes the prime focus. If the current treating physicians will be continuing in their same positions, then their current employment contract must be reviewed to determine whether the rights of the seller will accrue to the buyer.

If the rights of the seller will not accrue to the buyer, then the Purchase and Sale Agreement must have a provision that makes the continued employment of those current-treating physicians a condition to consummation of the sale. In such instances, the new employment agreement might be an exhibit to the main agreement and executed contemporaneously with the main agreement.

If the current treating physicians will not be continuing in their same position and if the purchaser will be assuming treatment of the patients, then the main agreement must provide for the dissolution of the employment agreement and provision must be made for restricting the ability of those physicians from competing with the buyer. If the employment contract with the seller contains a restrictive covenant, then the buyer must ensure that such covenants will accrue to the buyers benefit. Otherwise, the buyer should insist that those physicians sign restrictive covenants. In such an instance, a portion of the purchase price may need to be allocated towards the consideration for those restrictive covenants and paid directly to those physicians.

DATE OF AGREEMENT AND CLOSING DATE

In general, it usually does not matter when the agreement is dated. It should usually be dated once all the terms are agreed to and the parties desire to bind each other and to be bound. In certain instance, the parties may have reached an agreement, but certain issues (such as the obtaining of a state license to practice medicine) may be outstanding. In such a case, then an option can be given by either the seller or the buyer to bind the other to sell or buy the practice upon exercise of the option. Giving an option can also push the agreement date into the future. The option will usually be given with token consideration (e.g., one hundred dollars) and will have a fixed expiration date (e.g., thirty to ninety days).

The determination of the closing date is more important than the date that the agreement is dated. Just like in the purchase of a house where certain issues (such as obtaining a mortgage and home inspection) must occur before closing, in the purchase of a practice, there may be certain issues which require time to undertake before the actual transfer can be consummated. For example, the buyer may still need to obtain financing or the landlord may need to approve the assignment of the lease.

RECITALS

The recitals – or “whereas” clauses – traditionally enunciate the reasons the parties are entering into the agreement. In the sale of the practice the recitals may simply state that the buyer wishes to buy the practice and the seller wishes to sell the practice. Yet, there is a modern growing tendency among contract attorneys to eliminate the “whereas” clauses as some attorneys feel that such language is antiquated. In such instances, the agreement will simply have a paragraph or two delineation of the “Purpose” of the agreement.

ARTICLES, SECTIONS, AND PARAGRAPHS

The agreement will often be divided and numbered in some logical fashion, either into articles, sections, paragraphs, or a combination of these. The reason for doing so is twofold. First, it allows ready reference to the numbered paragraph, and secondly it allows the agreement to be divided and grouped in logical associations.

BINDING THE PARTIES

The first paragraph of the first article will often bind the seller to sell and the buyer to buy the practice under the terms of the agreement. The rest of the agreement simply spells out those terms.

WHAT IS PURCHASED?

The agreement must disclose the items which are being transferred and the items which are not considered part of the agreement. This section should be crystal clear, so that anybody reading the contract (and hence a court which may be called upon to enforce the contract) and not privy to the preliminary negotiations will know what is part of the agreement and what is not part of the agreement.

[1] Sale of Stock vs. Sale of Assets

In most cases, well-informed financial advisors [FAs] will recommend that the buyer solely purchase the assets of the practice and not the stock of the practice. By purchasing selected assets, the buyer is ensured that he will not become responsible for the known or unknown liabilities of the corporation. In prior days, avoiding purchasing the stock of the corporation was a wise recommendation.

However, with the advent of managed care, the purchase of the stock of the corporation can provide the new practitioner with certain competitive advantages. It may take a new practitioner three to nine months to get onto enough managed care panels to make the practice profitable. Purchase of the stock of the corporation ensures the new practitioner of acquiring the Federal Tax Identification Number [TIN], Personal Identification Number [PIN], Drug Enforcement Agency [DEA], Centers for Medicare and Medicaid [CMS], Global Location Number [GLN] , National Provider Identifier [NPI], HIE-Form 834 transmission number, Durable Medical Equipment Number [DME] etc, of the corporate entity. Since most managed care corporations identify providers by the Federal TIN, purchase of the stock of the corporation should allow the new practitioner to be enrolled on managed care panels in a shorter period of time.

[2] Items Purchased