BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

The paradox of thrift (saving) states that an increase in autonomous saving leads to a decrease in aggregate demand and thus a decrease in gross output which will in turn lower total saving. The paradox is that total saving may fall because of individuals’ attempts to increase their saving, and, broadly speaking, that increase in saving may be harmful to an economy.

Both the narrow and broad claims are paradoxical within the assumption underlying the fallacy of composition, namely that which is true of the parts must be true of the whole. The narrow claim transparently contradicts this assumption, and the broad one does so by implication, because while individual thrift is generally averred to be good for the economy, the paradox of thrift holds that collective thrift may be bad for the economy.

Posted on April 12, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Costco started selling gold bars to its members last August, and Wells Fargo analysts believe that the product is now bringing in between $100 million and $200 million a month. The retailer doesn’t reveal the price of the 1-ounce bullion to nonmembers online, but it’s estimated to be ~2% above the spot price gold trades at, per CNBC—and that price has soared since Costco got into the gold game. The price of gold has gone up 13% this year and reached record highs as investors pile in amid inflation worries.

The big numbers from the Consumer Price Index data released on Thursday

In March, inflation rose 3.5% from the year before, up from 3.2% in February.

The “core” CPI reading, which excludes volatile food and fuel prices, came in even higher, rising 3.8% on an annual basis. That’s the same as in February, but this time it’s serious.

Half of the increases came from rising gas prices and housing.

After seeing inflation fall by 3% over the course of 2023, Fed officials believed that higher inflation readings in January and February 2024 represented a hiccup in an otherwise downward trajectory. However, with the March reading also coming in hotter than anticipated, analysts say this is more than a fluke. That means hopes for a June interest rate cut are dashed. Even the US Postal Service plans to raise the price of “forever” stamps to $0.73 in July. Get yours now. And the Mexican peso is on an absolute tear, leaving the US dollar behind.

The S&P 500® index (SPX) advanced 38.42 points (0.7%) to 5,199.06; the Dow Jones Industrial Average® ($DJI) lost 2.43 points to 38,459.08; the NASDAQ Composite gained 271.84 points (1.7%) to 16,442.20.

The 10-year Treasury note yield (TNX) rose nearly 2 basis points to 4.578%.

The CBOE Volatility Index® (VIX) fell 0.89 to 14.91.

Chip maker strength lifted the Philadelphia Semiconductor Index (SOX) more than 2% and extended the benchmark’s year-to-date gain to more than 17%. Communications services and transportation shares were also among the strongest sectors. Financial shares were mixed ahead of expected quarterly results Friday from some major banks including JPMorgan Chase (JPM), Citigroup (C), and Wells Fargo (WFC).

Posted on April 11, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST– Today’sNewsletter

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

NEW YORK (Reuters) -The U.S. accounting watchdog on Wednesday said it has hit KPMG Netherlands with a $25 million civil penalty, a record for the regulator, in response to “egregious” and widespread exam cheating at the foreign affiliate of the major audit firm.

As millions of Americans approach age 66, they face the inevitable question, is it time to retire? The physician population is aging alongside the general population—more than 40% of physicians in the U.S. will be 65 years or older within the next decade. In the case of surgeons, there is little guidance on how to best ensure their competency throughout their career and at the same time maintain patient safety while preserving mature physician dignity.

It is a scenario playing out nationwide. From Oregon to Pennsylvania, hundreds of communities have in recent years either stopped adding fluoride to their water supplies or voted to prevent its addition. Supporters of such bans argue that people should be given the freedom of choice. The broad availability of over-the-counter dental products containing the mineral makes it no longer necessary to add to public water supplies, they say. The Centers for Disease Control and Prevention says that while store-bought products reduce tooth decay, the greatest protection comes when they are used in combination with water fluoridation.

More health systems are going to be opting out of Medicare Advantage (MA) plans, George Hill, a managing director at Deutsche Bank in Boston, predicted Monday at a “Wall Street Comes to Washington” webinar hosted by the Brookings Institution. “I think you’re going to see more large provider organizations threaten to opt out of networks, particularly as it relates to MA,” Hill said, adding that there are a number of reasons for this. “Prior authorizations are the problem, claims denials are a huge problem, delayed payments and rates are the problem — barriers in access to care in all varieties are the problem.”

The latest budget update from the nonpartisan Congressional Budget Office (CBO) found that the federal government has spent more on paying interest on the national debt than on the military in fiscal year 2024. The CBO’s budget report for March showed that the U.S. has spent $412 billion on military programs at the Department of Defense through the first half of FY-2024, according to preliminary figures from CBO and the Treasury Department.

Consumer price increases remained high last month, boosted by gas, rents, and car insurance, the government said Wednesday in a report that will likely give pause to the Federal Reserve as it weighs when and by how much to cut interest rates this year. Prices outside the volatile food and energy categories rose 0.4% from February to March, the same accelerated pace as in the previous month. Measured from a year earlier, these core prices were up 3.8%, unchanged from the year-over-year rise in February. The Fed closely tracks core prices because they tend to provide a good read of where inflation is headed.

Here’s where the major benchmarks ended:

The S&P 500® index (SPX) dropped 49.27 points (1.0%) to 5,160.64; the Dow Jones Industrial Average lost 422.16 points (1.1%) to 38,461.51; the NASDAQ Composite® ($COMP) fell 136.28 points (0.8%) to 16,170.36.

The 10-year Treasury note yield (TNX) soared more than 18 basis points to 4.548%.

The CBOE Volatility Index® (VIX) jumped 0.82 to 15.80.

Interest-rate-sensitive sectors like banks, real estate, and utilities led Wednesday’s decliners. The KBW Regional Bank Index (KRX) tumbled 5% to its lowest point since late November. The small-cap Russell 2000® Index (RUT) lost 2.5%. Energy shares were among the few gainers as WTI Crude Oil (/CL) futures rebounded after three-straight losing sessions.

In other markets, the U.S. dollar index (DXY) jumped 1% to a five-month high amid expectations interest rates will remain elevated.

Posted on April 10, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Is Business Finally Embracing Medical Values?

[By Render S. Davis MHA CHE]

[By David Edward Marcinko MBA MEd]

In the evolutionary shifts in models for medical care, physicians have been asked to embrace business values of efficiency and cost effectiveness, sometimes at the expense of their professional judgment and personal values.

While some of these changes have been inevitable as our society sought to rein in out-of-control costs, it is not unreasonable for physicians to call on payers, regulators and other business parties to the health care delivery system to raise their ethical bar.

Tit-for-Tat

Harvard University physician-ethicist Linda Emmanuel noted that “health professionals are now accountable to business values (such as efficiency and cost effectiveness), so business persons should be accountable to professional values including kindness and compassion.”

***

[Medicine versus Business]

***

Assessment

Within the framework of ethical principles, John La Puma, M.D., wrote in Managed Care Ethics, that “business’s ethical obligations are integrity and honesty.

Medicine’s are those plus altruism, beneficence, non-maleficence, respect, and fairness.”

About the Author

Render Davis was a Certified Healthcare Executive, now retired from Crawford Long Hospital at Emory University, in Atlanta, GA He served as Assistant Administrator for General Services, Policy Development, and Regulatory Affairs from 1977-95. He is a founding board member of the Health Care Ethics Consortium of Georgia and served on the consortium’s Executive Committee, Advisory Board, Futility Task Force, Strategic Planning Committee, and chaired the Annual Conference Planning Committee, for many years.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Written by doctors and healthcare professionals, this textbook should be mandatory reading for all medical school students—highly recommended for both young and veteran physicians—and an eliminating factor for any financial advisor who has not read it. The book uses jargon like ‘innovative,’ ‘transformational,’ and ‘disruptive’—all rightly so! It is the type of definitive financial lifestyle planning book we often seek, but seldom find. —LeRoy Howard MA CMPTM,Candidate and Financial Advisor, Fayetteville, North Carolina I taught diagnostic radiology for over a decade. The physician-focused niche information, balanced perspectives, and insider industry transparency in this book may help save your financial life. —Dr. William P. Scherer MS, Barry University, Ft. Lauderdale, Florida This book was crafted in response to the frustration felt by doctors who dealt with top financial, brokerage, and accounting firms. These non-fiduciary behemoths often prescribed costly wholesale solutions that were applicable to all, but customized for few, despite ever-changing needs. It is a must-read to learn why brokerage sales pitches or Internet resources will never replace the knowledge and deep advice of a physician-focused financial advisor, medical consultant, or collegial Certified Medical Planner™ financial professional. —Parin Khotari MBA,Whitman School of Management, Syracuse University, New York In today’s healthcare environment, in order for providers to survive, they need to understand their current and future market trends, finances, operations, and impact of federal and state regulations. As a healthcare consulting professional for over 30 years supporting both the private and public sector, I recommend that providers understand and utilize the wealth of knowledge that is being conveyed in these chapters. Without this guidance providers will have a hard time navigating the supporting system which may impact their future revenue stream. I strongly endorse the contents of this book.—Carol S. Miller BSN MBA PMP,President, Miller Consulting Group, ACT IAC Executive Committee Vice-Chair at-Large, HIMSS NCA Board Member This is an excellent book on financial planning for physicians and health professionals. It is all inclusive yet very easy to read with much valuable information. And, I have been expanding my business knowledge with all of Dr. Marcinko’s prior books. I highly recommend this one, too. It is a fine educational tool for all doctors.—Dr. David B. Lumsden MD MS MA,Orthopedic Surgeon, Baltimore, Maryland There is no other comprehensive book like it to help doctors, nurses, and other medical providers accumulate and preserve the wealth that their years of education and hard work have earned them. —Dr. Jason Dyken MD MBA,Dyken Wealth Strategies, Gulf Shores, Alabama I plan to give a copy of this book written ‘by doctors and for doctors’ to all my prospects, physician, and nurse clients. It may be the definitive text on this important topic. —Alexander Naruska CPA,Orlando, Florida

Health professionals are small business owners who need to apply their self-discipline tactics in establishing and operating successful practices. Talented trainees are leaving the medical profession because they fail to balance the cost of attendance against a realistic business and financial plan. Principles like budgeting, saving, and living below one’s means, in order to make future investments for future growth, asset protection, and retirement possible are often lacking. This textbook guides the medical professional in his/her financial planning life journey from start to finish. It ranks a place in all medical school libraries and on each of our bookshelves. —Dr. Thomas M. DeLauro DPM,Professor and Chairman – Division of Medical Sciences, New York College of Podiatric Medicine

Physicians are notoriously excellent at diagnosing and treating medical conditions. However, they are also notoriously deficient in managing the business aspects of their medical practices. Most will earn $20-30 million in their medical lifetime, but few know how to create wealth for themselves and their families. This book will help fill the void in physicians’ financial education. I have two recommendations: 1) every physician, young and old, should read this book; and 2) read it a second time! —Dr. Neil Baum MD,Clinical Associate Professor of Urology, Tulane Medical School, New Orleans, Louisiana

I worked with a Certified Medical Planner™ on several occasions in the past, and will do so again in the future. This book codified the vast body of knowledge that helped in all facets of my financial life and professional medical practice. —Dr. James E. Williams DABPS, Foot and Ankle Surgeon, Conyers, Georgia

This is a constantly changing field for rules, regulations, taxes, insurance, compliance, and investments. This book assists readers, and their financial advisors, in keeping up with what’s going on in the healthcare field that all doctors need to know. —Patricia Raskob CFP® EA ATA, Raskob Kambourian Financial Advisors, Tucson, Arizona I particularly enjoyed reading the specific examples in this book which pointed out the perils of risk … something with which I am too familiar and have learned (the hard way) to avoid like the Black Death. It is a pleasure to come across this kind of wisdom, in print, that other colleagues may learn before it’s too late— many, many years down the road. —Dr. Robert S. Park MD, Robert Park and Associates Insurance, Seattle, Washington

Although this book targets physicians, I was pleased to see that it also addressed the financial planning and employment benefit needs of nurses; physical, respiratory, and occupational therapists; CRNAs, hospitalists, and other members of the health care team….highly readable, practical, and understandable. —Nurse Cecelia T. Perez RN, Hospital Operating Room Manager, Ellicott City, Maryland

Personal financial success in the PP-ACA era will be more difficult to achieve than ever before. It requires the next generation of doctors to rethink frugality, delay gratification, and redefine the very definition of success and work–life balance. And, they will surely need the subject matter medical specificity and new-wave professional guidance offered in this book. This book is a ‘must-read’ for all health care professionals, and their financial advisors, who wish to take an active role in creating a new subset of informed and pioneering professionals known as Certified Medical Planners™. —Dr. Mark D. Dollard FACFAS, Private Practice, Tyson Corner, Virginia As healthcare professionals, it is our Hippocratic duty to avoid preventable harm by paying attention. On the other hand, some of us are guilty of being reckless with our own financial health—delaying serious consideration of investments, taxation, retirement income, estate planning, and inheritances until the worry keeps one awake at night. So, if you have avoided planning for the future for far too long, perhaps it is time to take that first step toward preparedness. This in-depth textbook is an excellent starting point—not only because of its readability, but because of his team’s expertise and thoroughness in addressing the intricacies of modern investments—and from the point of view of not only gifted financial experts, but as healthcare providers, as well … a rare combination. —Dr. Darrell K. Pruitt DDS, Private Practice Dentist, Fort Worth, Texas This text should be on the bookshelf of all contemporary physicians. The book is physician-focused with unique topics applicable to all medical professionals. But, it also offers helpful insights into the new tax and estate laws, fiduciary accountability for advisors and insurance agents, with investing, asset protection and risk management, and retirement planning strategies with updates for the brave new world of global payments of the Patient Protection and Affordable Care Act. Starting out by encouraging readers to examine their personal ‘money blueprint’ beliefs and habits, the book is divided into four sections offering holistic life cycle financial information and economic education directed to new, mid-career, and mature physicians.

This structure permits one to dip into the book based on personal need to find relief, rather than to overwhelm. Given the complexity of modern domestic healthcare, and the daunting challenges faced by physicians who try to stay abreast of clinical medicine and the ever-evolving laws of personal finance, this textbook could not have come at a better time. —Dr. Philippa Kennealy MD MPH, The Entrepreneurial MD, Los Angeles, California Physicians have economic concerns unmatched by any other profession, arriving ten years late to the start of their earning years. This textbook goes to the core of how to level the playing field quickly, and efficaciously, by a new breed of dedicated Certified Medical Planners™. With physician-focused financial advice, each chapter is a building block to your financial fortress. —Thomas McKeon, MBA, Pharmaceutical Representative, Philadelphia, Pennsylvania An excellent resource … this textbook is written in a manner that provides physician practice owners with a comprehensive guide to financial planning and related topics for their professional practice in a way that is easily comprehended. The style in which it breaks down the intricacies of the current physician practice landscape makes it a ‘must-read’ for those physicians (and their advisors) practicing in the volatile era of healthcare reform. —Robert James Cimasi, MHA ASA FRICS MCBA CVA CM&AA CMP™, CEO-Health Capital Consultants, LLC, St. Louis, Missouri Rarely can one find a full compendium of information within a single source or text, but this book communicates the new financial realities we are forced to confront; it is full of opportunities for minimizing tax liability and maximizing income potential. We’re recommending it to all our medical practice management clients across the entire healthcare spectrum. —Alan Guinn, The Guinn Consultancy Group, Inc., Cookeville, Tennessee Dr. David Edward Marcinko MBA CMP™ and his team take a seemingly endless stream of disparate concepts and integrate them into a simple, straightforward, and understandable path to success. And, he codifies them all into a step-by-step algorithm to more efficient investing, risk management, taxation, and enhanced retirement planning for doctors and nurses. His text is a vital read—and must execute—book for all healthcare professionals and physician-focused financial advisors. —Dr. O. Kent Mercado, JD, Private Practitioner and Attorney, Naperville, Illinois

Kudos. The editors and contributing authors have compiled the most comprehensive reference book for the medical community that has ever been attempted. As you review the chapters of interest and hone in on the most important concerns you may have, realize that the best minds have been harvested for you to plan well… Live well. —Martha J. Schilling; AAMS® CRPC® ETSC CSA, Shilling Group Advisors, LLC, Philadelphia, Pennsylvania I recommend this book to any physician or medical professional that desires an honest no-sales approach to understanding the financial planning and investing world. It is worthwhile to any financial advisor interested in this space, as well. —David K. Luke, MIM MS-PFP CMP™, Net Worth Advisory Group, Sandy, Utah Although not a substitute for a formal business education, this book will help physicians navigate effectively through the hurdles of day-to-day financial decisions with the help of an accountant, financial and legal advisor. I highly recommend it and commend Dr. Marcinko and the Institute of Medical Business Advisors, Inc. on a job well done. —Ken Yeung MBA CMP™, Tseung Kwan O Hospital, Hong Kong I’ve seen many ghost-written handbooks, paperbacks, and vanity-published manuals on this topic throughout my career in mental healthcare. Most were poorly written, opinionated, and cheaply produced self-aggrandizing marketing drivel for those agents selling commission-based financial products and expensive advisory services. So, I was pleasantly surprised with this comprehensive peer-reviewed academic textbook, complete with citations, case examples, and real-life integrated strategies by and for medical professionals. Although a bit late for my career, I recommend it highly to all my younger colleagues … It’s credibility and specificity stand alone. —Dr. Clarice Montgomery PhD MA,Retired Clinical Psychologist In an industry known for one-size-fits-all templates and massively customized books, products, advice, and services, the extreme healthcare specificity of this text is both refreshing and comprehensive. —Dr. James Joseph Bartley, Columbus, Georgia

My brother was my office administrator and accountant. We both feel this is the most comprehensive textbook available on financial planning for healthcare providers. —Dr. Anthony Robert Naruska DC,Winter Park, Florida

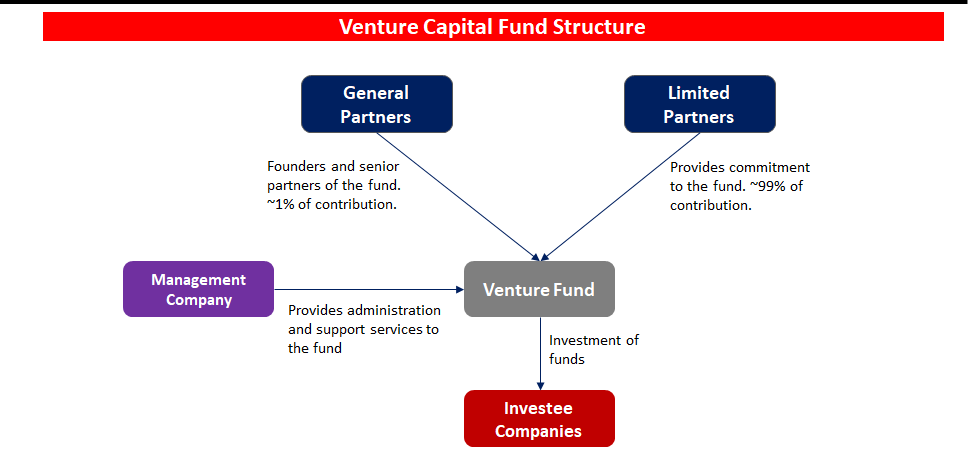

Private equity and venture capital investments typically involve ownership of shares in a company and represent title to a portion of the company’s future earnings. However, private equity is an equity interest in a company or venture whose stock is not yet traded on a stock exchange.

Venture capital is typically a special case of private equity in which the investment is in a company or venture that has little financial history or is embarking on a high risk/high potential reward business strategy.

Like real estate, private equity and venture capital investments generally share a general lack of liquidity and a lack of comparability across different individual investments. The lack of liquidity comes from the fact that private equity and venture capital investments are typically not tradable on a stock exchange until the company has an IPO.

The lack of comparability is due to the fact that most private equity and venture capital investments are the result of direct negotiation between the investor/venture capitalist and the existing owners of the company /venture.

With widely divergent terms and provisions across different investments, it is difficult to make general claims regarding the characteristics of private equity and venture capital investments.

The Institute of Medical Business Advisors Inc identified several reasons based on observations working with medical professional and physician clients over the years.

A late start

By the time doctors finish medical school and residency they’re typically in their middle or late thirties. Many have families to feed, and substantial student loans to pay off. It will be years before they can even start accumulating wealth. Consider that physicians typically enter careers at later ages, often with larger debts from training. Some specialties may not lead a case until 10 years of practice, and many specialties have limited longevity. Peak earning years may also be shorter for health care providers than other professionals. Financial survival skills are paramount for converting the limited earnings time period to personal financial security.

Challenging socio-political environment

It is increasingly challenging to practice medicine. With the Medicare Trust Fund slated to go bust in 2019, the Center for Medicare and Medicare Service (CMS) is increasingly resorting to cutting physician reimbursements and implementing capitation and bundled value based medical payments models. The medical reimbursement effects of the PP-ACA are not yet fully discerned; but appear to continue the decline in compensation. And to illustrate this potential governmental control, in what other industry can participants debate the simple question, “who is the customer?”

Lifestyle expectations

Society expects a doctor to live like a doctor, dress like a doctor, and drive like a doctor. Meeting social expectations can be quite expensive.

Time and energy

A doctor can’t be just a doctor any more. S/he also has to deal with ever increasing regulatory mandates, paperwork requirements by state and federal agencies and capricious insurance companies. It is estimated that for every hour spent on patient care, and additional half-hour is spent on paperwork. To-date, the use of electronic medical records has exacerbated; not ameliorated this problem. The demand on their time is mind-boggling. A typical doctor works a ten- to twelve-hour day. After work and family, they simply don’t have time and energy left to do comprehensive financial planning.

Financially naïve

Doctors are smart. They’re highly trained in their area of expertise. But, that doesn’t translate into understanding about finance or economics. Because they are smart, it’s easy for them to think they can easily master and execute concepts of personal financial planning, as well. Often, they don’t.

Lack of trust and delegation

Many doctors don’t trust financial advisors working for major Wall Street banks. They have the good instinct to realize that their interests are not aligned. Not knowing there are independent advisors out there who observe a strict fiduciary standard, they tend to do everything by themselves.

In fact, Paul Larson CFP®, President-CEO of the firm LARSON Financial Group LLC, noted a disquieting trend among physician client in his firm [personal communication]. Almost 90% of them fail to take care of their own family finances in a comprehensive manner; while only 10% are succeeding. The strategies in this chapter and book are common to their success.

Too Trusting

Another aspect of naivety, many physicians do not realize that the financial advisory industry lacks the same discipline and regulation that the average physician operates in. A primary care doctor would never even attempt a complicated surgery on a patient, but is trained to refer such patients to a specialist in the field with the proper training and experience. Financial Advisors often come from a sales background and are trained to keep a client in house even if the advisor is lacking in expertise. Also, many physicians are not trained to discern a qualified financial advisor from a sales person dressed up like a financial advisor. It is illegal to call yourself a physician in the United States unless you have the credentials to back it up; yet, anyone in the US can legally call themselves a financial advisor or a financial planner.

It’s never a source of pride stepping out of a dirty car or truck, especially for image conscious doctors. But, keeping your vehicle looking like new, for the doctor’s parking lot, is tough work. Sure, you may take it through the drive-thru car wash every now and then, but that isn’t the deep cleaning that your car deserves.

All in the Details

Detailing, on the other hand, is promised to give your beloved vehicle that ‘new-car’ feeling all over again. It isn’t easy work, but the results are amazing. While you could detail your car at home, is it really worth it? Let’s take a look at why letting the pros detail your vehicle is the way to go – or – not!

Working at the Car Wash

When you wash your vehicle at a drive-thru car wash, you may be doing more harm than good. If the car wash has brushes or pieces of cloth that scrub your vehicle as it goes through, these components can easily scratch your car’s finish. All of the bits of dirt from cars before can be trapped in the cloth and brushes, and as they scrub your vehicle, they act as sandpaper, permanently marring your paint.

One step better is hand washing your car at home, but even then, you must be careful to not just become a humanized version of the car wash. Using two buckets is a good start, with one bucket being a rinse bucket to remove the dirt from your sponge, and the other containing the soap.

SOAP Suds – Not SOAP Notes

Also, be careful of the type of soaps and car care products being used. The interior and exterior cleaners found at the local parts store are often of decent quality, but they aren’t always the best, and they must be used properly. Even then, for a normal car owner, detailing a car can become an all-day task, sometimes with less than perfect results.

Don’t forget to use a clay bar or brick followed by your favorite Carnuba wax, too.

The Pros

So, why should you let the pros handle your detailing needs? They should know exactly what specialty products are right for your vehicle to get the perfect results every time. And, they know the techniques that will yield showroom-finish results while you don’t have to even touch your car.

And, while you won’t want to clean out all the dried soda, coffee stains, or leftover cheeseburger wrappers from under your seat, they will gladly do it for you – for a price.

Imagine

Just picture getting into a blindingly shiny, clean vehicle with an interior that looks equally as pristine. No more purchasing all kinds of car care products that don’t deliver results. No more spending hours in the driveway getting soaked and frustrated. No more wasted time. Pros know what it takes to detail your vehicle to concourse standards.

But then, it is just a job for them. It is a labor of love for me. Am I neurotic or compulsive?

My near showroom and mint conditioned 2000 Jaguar XJ-V8-L is a full-size luxury sedan, offers sporting drive characteristics, mixed with a classic style and interior comfort. It was available in multiple trims which all came very well equipped with upscale amenities.

And, this extended wheelbase version offers much more rear seat leg room for long and winding Georgia road trips. The standard steel engine [not nikasil] in this XJ is a 4.0L V8 which produces 290 hp. The upper and lower timing chain tensioners are original, second generation metal, not plastic.

There is also a supercharged version of this vehicle which bumps output to an impressive 370 hp. Even with all of its power and weight, my XJ-8-L is still rated at over 20 mpg on the highway. Ammenities and upgrades include a mobile phone, Magellan GPS, LoJack theft recovery system, CD and MP-3 players, with internal and external cable antenna for satellite radio.

What a Cat? She is my third favorite female after my intelligent and beautiful wife, and smart and lovely daughter.

Conclusion

Are you a DIYer, like me? Nothing says you care more than doing it yourself.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

TERMS & DEFINITIONS FOR PHYSICIANSAND ALL INVESTORS:

PRUDENT BUYER: The efficient purchaser of market balance between value and cost.

PRUDENT MAN RULE: An 1830 court case stating that a person in a fiduciary capacity (a trustee, executor, custodian, etc) must conduct him/herself faithfully and exercise sound judgment when investing monies under care. “He is to observe how men of prudence, discretion and intelligence manage their own affairs, not in regard to speculation, but in regard to the permanent distribution of their funds, considering the probable income as well as the probable safety of the capital to be invested.” Allows for mutual funds and variable annuities.

PRUDENT INVESTOR RULE: A fiduciary is required to conduct him/herself faithfully and exercise sound judgment when investing monies and take measured and reasonable investment risks in return for potential future rewards. Allows for mutual funds, stocks, bonds, variable annuities asset allocation & Modern Portfolio Theory.

EDITOR’SNOTE: We interviewed noted authority Ben Aikin AIF® on this topic more than a decade ago. He was ahead of his time regarding fiduciary accountability and we appreciate his insights.

Posted on March 28, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Related Influential Thought-Leaders

Dr. Brad Klontz CSAC CFP®

Dr. Ted Klontz PsyD

Dr. Eugene Schmuckler MBA MEd CTS

Dr. Kenneth Shubin-Stein FACP CFA

Dr. David Edward Marcinko MEd MBA CMP™

***

***

James O. Prochaska PhD, Professor of Psychology and Director of the Cancer Prevention Research Center at the University of Rhode Island, developed the Trans-Theoretic Model of Behavior Change [TTM] which has been evolving since in 1977. Nominated as one of the five most influential authors in Psychology, by the Institute for Scientific Information and the American Psychological Society, Dr. Prochaska is author of more than 300 papers on behavior change for health promotion and disease prevention.

TTM Stages of Change

In his Trans-Theoretical Model, behavior change is a “process involving progress through a series of these stages:

Pre-Contemplation (Not Ready) – “People are not intending to take action in the foreseeable future, and can be unaware that their behavior is problematic”

Contemplation (Getting Ready) – “People are beginning to recognize that their behavior is problematic, and start to look at the pros and cons of their continued actions”

Preparation (Ready) – “People are intending to take action in the immediate future, and may begin taking small steps toward behavior change”

Action – “People have made specific overt modifications in changing their problem behavior or in acquiring new healthy behaviors”

Maintenance – “People have been able to sustain action for a while and are working to prevent relapse”

Termination – “Individuals have zero temptation and they are sure they will not return to their old unhealthy habit as a way of coping”

Relapse

In addition, researchers conceptualized “relapse” (recycling) which is not a stage in itself but rather the “return from Action or Maintenance to an earlier stage.” In medical care, these stages of behavior change have applicability to anti-hypertension and lipid lowering medication use, as well as depression prevention, weight control and smoking cessation.

***

***

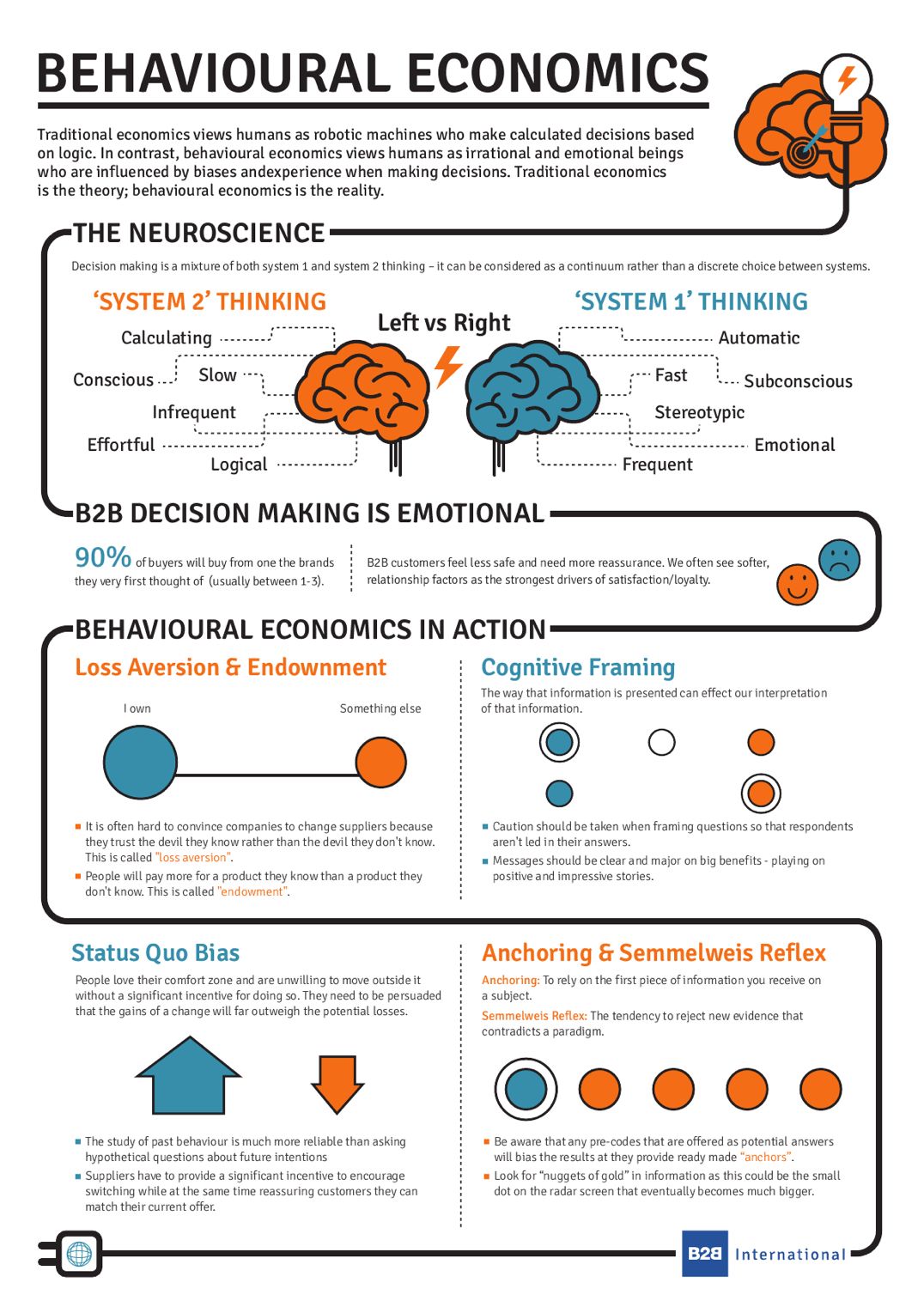

Uniting Psychology and Financial Behavior

More recently, validating the emerging alliance between psychology (human behavior) and finance (economics) are two Americans who won the Royal Swedish Academy of Science’s 2002 Nobel Memorial Prize in Economic Science. Their research was nothing short of an explanation for the idiosyncrasies incumbent in human financial decision-making outcomes.

Enter Kahneman and Smith

Daniel Kahneman, PhD, professor of psychology at Princeton University, and Vernon L. Smith, PhD, professor of economics at George Mason University in Fairfax, Va., shared the prize for work that provided insight on everything from stock market bubbles, to regulating utilities, and countless other economic activities. In several cases, the winners tried to explain apparent financial paradoxes.

For example, Professor Kahneman made the economically puzzling discovery that most of his subjects would make a 20-minute trip to buy a calculator for $10 instead of $15, but would not make the same trip to buy a jacket for $120 instead of $125, saving the same $5.

in vitro and in-vivo Economics

Initially, in the 1960’s, Smith set out to demonstrate how economic theory worked in the laboratory (in vitro), while Kahneman was more interested in the ways economic theory mis-predicted people in real-life (in-vivo). He tested the limits of standard economic choice theory in predicting the actions of real people, and his work formalized laboratory techniques for studying economic decision making, with a focus on trading and bargaining.

Later, Smith and Kahneman together were among the first economists to make experimental data a cornerstone of academic output. Their studies included people playing games of cooperation and trust, and simulating different types of markets in a laboratory setting. Their theories assumed that individuals make decisions systematically, based on preferences and available information, in a way that changes little over time, or in different contexts.

University of Chicago

By the late 1970’s, Richard H. Thaler, PhD, an economist at the University of Chicago also began to perform behavioral experiments further suggesting irrational wrinkles in standard financial theory and behavior, enhancing the still embryonic but increasingly popular theories of Kahneman and Smith.

Other economists’ laboratory experiments used ideas about competitive interactions pioneered by game theorists like John Forbes Nash Jr., PhD, who shared the Nobel in 1994, as points of reference.

Assessment

But, Kahneman and Smith often concentrated on cases where people’s actions departed from the systematic, rational strategies that Nash envisioned. Psychologically, this was all a precursor to the informal concept of life or holistic financial planning. Kahneman was awarded the Medal of Freedom, by President Barack Obama, on November 20, 2013.

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Managerial and medical cost accounting is not governed by generally accepted accounting principles (GAAP) as promoted by the Financial Accounting Standards Board (FASB) for CPAs. Rather, a healthcare organization costing expert may be a Certified Cost Accountant (CCA) or Certified Managerial Accountant (CMA) designated by the Cost Accounting Standards Board (CASB), an independent board within the Office of Management and Budget’s (OMB) Office of Federal Procurement Policy (OFPP).

The Cost Accounting Standards Board

CASB consists of five members, including the OFPP Administrator who serves as chairman and four members with experience in government contract cost accounting (two from the federal government, one from industry, and one from the accounting profession). The Board has the exclusive authority to make, promulgate, and amend cost accounting standards and interpretations designed to achieve uniformity and consistency in the cost accounting practices governing the measurement, assignment, and allocation of costs to contracts with the United States.

Codified at 48 CFR

CASB’s regulations are codified at 48 CFR, Chapter 99. The standards are mandatory for use by all executive agencies and by contractors and subcontractors in estimating, accumulating, and reporting costs in connection with pricing and administration of, and settlement of disputes concerning, all negotiated prime contract and subcontract procurement with the United States in excess of $500,000. The rules and regulations of the CASB appear in the federal acquisition regulations.

North American Industry Classification System (NAICS) codes are used to categorize data for the federal government. In acquisition they are particularly critical for size standards. The NAICS codes are revised every five years by the Census Bureau. As of October 1, 2007, the federal acquisition community began using the 2007 version of the NAICS codes at www.census.gov/epcd/www/naics.html

Cost Accounting Standards

Healthcare organizations and consultants are obligated to comply with the following cost accounting standards (CAS) promulgated by federal agencies:

CAS 501 requires consistency in estimating, accumulating, and reporting costs.

CAS 502 requires consistency in allocating costs incurred for the same purpose.

CAS 505 requires proper treatment of unallowable costs.

CAS 506 requires consistency in the periods used for cost accounting.

The requirements of these standards are different from those of traditional financial accounting, which are concerned with providing static historical information to creditors, shareholders, and those outside the public or private healthcare organization.

Assessment

Functionally, most healthcare organizations also contain cost centers, which have no revenue budgets or mission to earn revenues for the organization. Examples include human resources, administration, housekeeping, nursing, and the like. These are known as responsibility centers with budgeting constraints but no earnings. Furthermore, shadow cost centers include certain non-cash or cash expenses, such as amortization, depreciation and utilities, and rent. These non-centralized shadow centers are cost allocated for budgeting purposes and must be treated as costs http://www.CertifiedMedicalPlanner.org

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

A young concierge medical practice is a business with challenges in these Customer [Patient] Relationship Management’s [CRM] areas that are critical for success.

Areas of Most Challenge

Maturity of Processes:

Processes are often associated with bureaucracy or stuffy hierarchical healthcare systems that are anathema to emerging concierge medical practices. At small practices, doctors are often owners who fiercely pride themselves on flat structures, autonomy and flexibility. However, processes are imperative to conduct a streamlined practice that can be woven around a CM culture that still ensures practice business is conducted in a systematic manner.

Organization Structure:

Young concierge medical practices have challenges managing growth while grappling to incorporate an organization structure that promotes the elite private practice culture.

Multi-tasking, rapidly growing work places:

Young CM practices are often characterized by employees who multi-task and assume several roles to make their resources stretch farther. Especially in the current healthcare reform climate, young practice employees take up a broader set of responsibilities. In addition, as young private CM practices grow, they may become anguished with a growing office workplace that may not be equipped with an evolving infrastructure to cope. They have a fierce need to carefully control growth with tightly managed resources.

Changing business needs and strategy:

In an era after the golden age of traditional medicine, profitability is critical for emerging concierge practices. It is imperative to be nimble and change marketing strategies as socio-political and competitive climates dictate. A good C[P] RM system is tightly integrated, but loosely coupled, to allow CM practices to communicate appropriately with patients.

Little room for Slack:

Small concierge medical practices do not have as much established name-brand equity as larger, established practices of any model type, and patients are less willing to tolerate mistakes. Concierge practices have to run a much tighter ship and build impeccable patient experiences.

Fierce Competition:

The cash or retainer medicine landscape today looks very different from just five years ago. Competition is becoming fierce and practices are fighting for mindshare and patients. Young practices are competing with older concierge practices – large traditional practices, micro-practices, behemoth healthcare systems, enterprise-wide medical corporations and every other practice model in-between – to attract and retain patients with private resources.

Assessment

The above characteristics form the basis of a compelling strategy to embrace C[P]RM and streamline patient relationships and cash revenue opportunities. Concierge practices still need to build scalable marketing programs that can easily ramp up and down effortlessly as needs and economic environments demand. But, they do need to establish marketing metrics and processes that can demonstrate the Return on Investment (ROI) on their CRM, and marketing programs, and for getting critical cash-paying patient buy-in.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

The fact that every physician in private medical practice, without a business education, leaves approximately a million dollars on the table and is unaware of it is well known to business experts who work with medical doctors experiencing financial difficulties.

Business experts such as Dan S. Kennedy, Peter Drucker, Michael Gerber, Maxwell Maltz, Neil Baum, William Hanson,Huss and Coleman, Steven Hacker, Thomas Stanley, Chris Hurn, Napoleon Hill, and Dave Ramsey, among others, understand the financial problems faced by medical practices and how to solve them.

The more expensive something is – the less likely you are to use it. This relationship between price and product utility is graphed as an “inverted U.”

Posted on March 25, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

The Virtual Doctor Will See You Now!

By Dr. David Edward Marcinko MBA CMP™

[Publisher-in-Chief]

Recently, I was invited to speak at a regional convention. No surprise there as I have been doing so – around the world – for more than twenty years – webcasts included. And, I was asked to submit the usual paraphernalia; a formal CV, audio-visual needs, travel arrangements and times, PPE, and a personal photo which were all dutifully supplied.

Then, I was asked to supply something that flabbergasted me; I became slack-jawed, actually.

DEM’s Avatar

Imagine my surprise when I was asked for an avatar; not just a digital photograph. So – having none – I had one made and now submit it for your review.

Photograph of Dr. David Edward Marcinko @ home

Avatar of Dr. David Edward Marcinko @ work

***

Assessment

So, how do I virtually look – better or worse – glasses or contact lens? It seems as though some folks are more interested in the virtual me; than the real me. Go figure!

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

Our Other Print Books and Related Information Sources:

Venture capital funding in the digital health space cooled a bit in 2022 following a red-hot 2021. Overall, digital health companies raised $15.3 billion last year, down from the $29.1 billion raised in 2021—but still above the $14.1 billion raised in 2020, according to Rock Health a seed fund that supports digital health startups.

Nevertheless, analysts predict VC investors and bankers will still put a good amount of money into digital health in 2024 and 2025, especially in alternative care, drug development, health information technology technology, EMRs and software that reduces physician workload.

Of course. an essential first part of attracting VC interest and money is the crafting and presentation of your formal business plan [“elevator pitch”]; as well as the needed technical and managerial experience. This is crucial for success and exactly where we can assist.

(“Informed Voice of a New Generation of Fiduciary Advisors for Healthcare”)

For most lay folks, personal financial planning typically involves creating a personal budget, planning for taxes, setting up a savings account and developing a debt management, retirement and insurance recovery plan. Medicare, Social Security and Required Minimal Distribution [RMD] analysis is typical for lay retirement. Of course, we can assist in all of these activities, but lay individuals can also create and establish their own financial plan to reach short and long-term savings and investment goals.

But, as fellow doctors, we understand better than most the more complex financial challenges doctors can face when it comes to their financial planning. Of course, most physicians ultimately make a good income, but it is the saving, asset and risk management tolerance and investing part that many of our colleagues’ struggle with. Far too often physicians receive terrible guidance, have no time to properly manage their own investments and set goals for that day when they no longer wish to practice medicine.

For the average doctor or healthcare professional, the feelings of pride and achievement at finally graduating are typically paired with the heavy burden of hundreds of thousands of dollars in student loan debt.

You dedicated countless hours to learning, studying, and training in your field. You missed birthdays and holidays, time with your families, and sacrificed vacations to provide compassionate and excellent care for your patients. Amidst all of that, there was no time to give your finances even a second thought.

Between undergraduate, medical school, and then internship and residency, most young physicians do not begin saving for retirement until late into their 20s, if not their 30s. You’ve missed an entire decade or more of allowing your money and investments to compound and work for you. When it comes to addressing your financial health and security, there’s no time to waste.

Did you know that the American Medical Association is calling on medical schools and residency programs to include specific information about healthcare economics and financing in their curricula.

But, is health economics heterodoxic, or not? And; what about demand-derived economics in medicine?

Posted on March 5, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

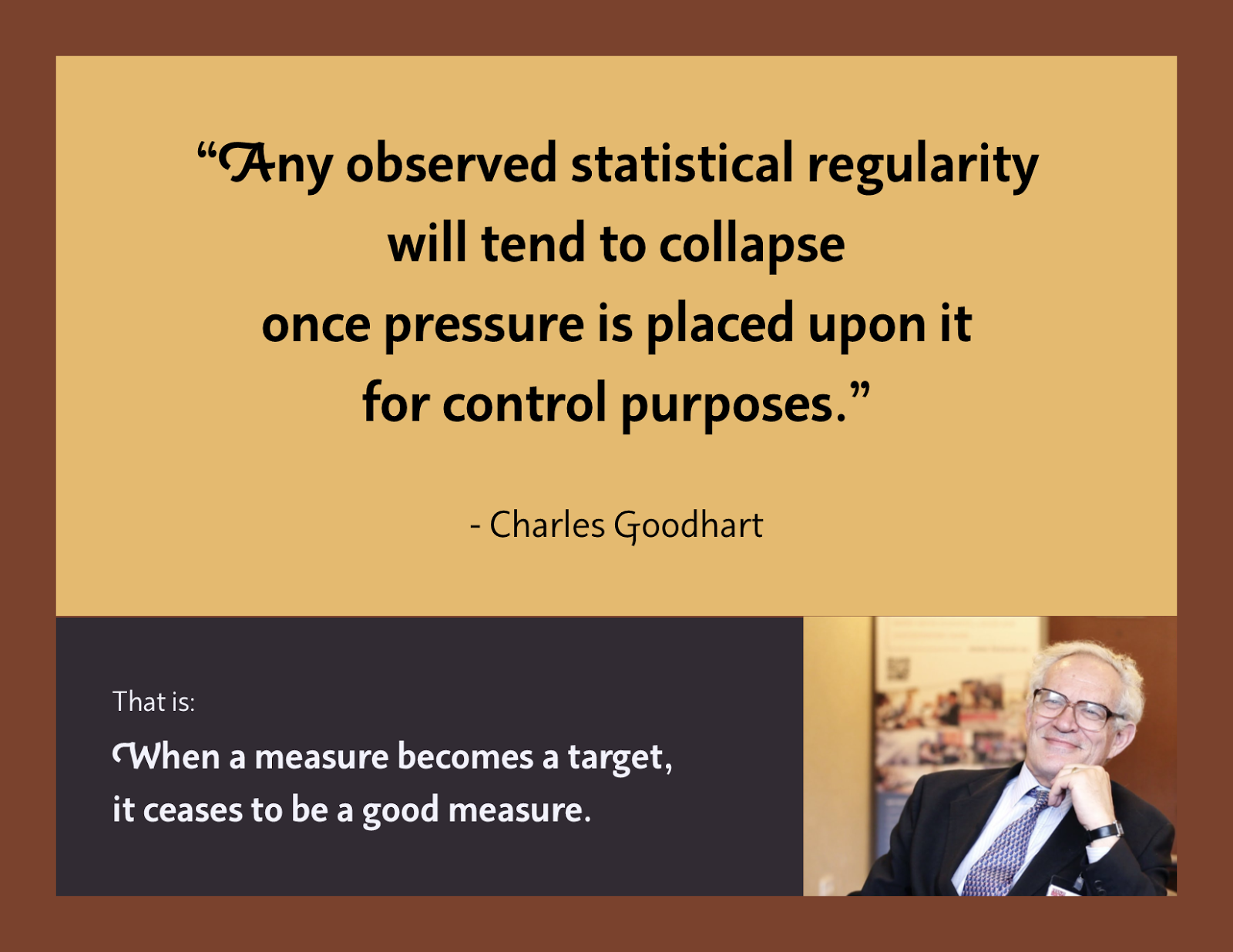

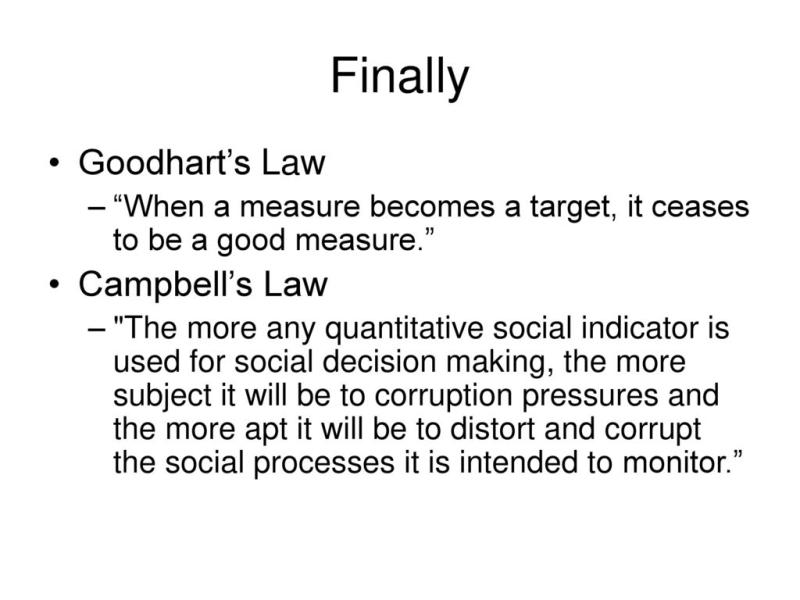

The Goodhart Principle, and related

[By staff reporters]

***

Goodhart’s law is a sociological analogue of Heisenberg’s uncertainty principle in quantum mechanics. Measuring a system usually disturbs it. The more precise the measurement, and the shorter its timescale, the greater the energy of the disturbance and the greater the unpredictability of the outcome.

***

***

***

CAMPBELL’S LAW:

“The more any quantitative social indicator is used for social decision-making, the more subject it will be to corruption pressures and the more apt it will be to distort and corrupt the social processes it is intended to monitor.”

As fellow doctors, we understand better than most the more complex financial challenges physicians can face when it comes to their financial planning. Of course, most physicians ultimately make a good income, but it is the saving, asset and risk management tolerance and investing part that many of our colleagues’ struggle with. Far too often physicians receive terrible guidance, have no time to properly manage their own investments and set goals for that day when they no longer wish to practice medicine.

For the average doctor or healthcare professional, the feelings of pride and achievement at finally graduating are typically paired with the heavy burden of hundreds of thousands of dollars in student loan debt.

You dedicated countless hours to learning, studying, and training in your field. You missed birthdays and holidays, time with your families, and sacrificed vacations to provide compassionate and excellent care for your patients. Amidst all of that, there was no time to give your finances even a second thought.

Between undergraduate, medical school, and then internship and residency, most young physicians do not begin saving for retirement until late into their 20s, if not their 30s. You’ve missed an entire decade or more of allowing your money and investments to compound and work for you. When it comes to addressing your financial health and security, there’s no time to waste.

And you may be misled by unscrupulous “advisors”.

For example:

Question: Do you know the difference between a “Fee-Only” and a “Fee-Based financial advisor? Not knowing may cost you tens of thousands of dollars, or more, in excessive advisory fees.

In a January 24th letter, AHA and other national hospital organizations voiced support for the Safety from Violence for Healthcare Employees (SAVE) Act (H.R. 2584/S. 2768), bipartisan legislation that would provide federal protections for health care workers similar to those that apply to aircraft and airport workers.

“Although our members have for many years had protocols in place designed to protect their employees and promote a safe environment for patient care, the number of violent attacks against health care workers has increased markedly in recent years,” the letters to House and Senate sponsors note. “Recent studies indicate that 44% of nurses have reported being subjected to physical violence and 68% have reported verbal abuse. These experiences affect the individual provider, who may suffer from both physical and psychological trauma, and they can also interfere with care delivery when providers fear for their personal safety, are distracted by disruptive patients or family members, or are traumatized from prior violent interactions. These types of incidents also consume scarce hospital and health system resources, which in turn could impact the care available for other patients.”

Managed care insurers have profited handsomely from Medicare Advantage plans, scoring billions in annual profits. They credit this financial wizardry to their use of sophisticated data analytics, preventative care, cost optimization, provider networks, evidence and value-based care and risk mitigation strategies. However, doctors, hospitals, and medical providers assert something else.

In fact, Medicare Advantage plans have been making headlines in 2024, but not in a positive light, at least for health insurance companies. Medicare is a government-sponsored health insurance benefit; generally for retired people aged 65 and older.

For most, the money for Medicare Part B medical insurance or Part C Medicare Advantage plans is withdrawn directly from Social Security benefits monthly, coupled with a relatively small monthly payment from the patient. Nearly half of the Medicare population is enrolled in Part C Medicare Advantage plans.

***

***

However, there have been rumblings in the medical sector between medical providers and medical insurers coming to a head. So, where do you stand?

Informational essays of most current interest to healthcare professionals. Check back periodically for practical updates. Our catalogue library of major books, texts, case models and dictionaries is suggested for additional financial, economic, business and medical practice management information and education.

Posted on February 19, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Get ’em … While They are Hot!

By Ann Miller RN MHA

[ME-P Executive Director]

Just click on the book icon to order; get any one or all three! You’ll be glad you did.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

Bank of America just acknowledged that the personal information of 57,028 of its customers has been compromised. This breach, attributed to a failure at Infosys McCamish Systems (IMS), a provider of insurance business process solutions engaged by the bank, poses a substantial risk of identity theft to the affected individuals.

The data breach notification, filed in Maine, reveals that sensitive information related to Bank of America’s deferred compensation plans was inadvertently accessed. IMS, in a notification letter to customers, disclosed that the compromised data encompasses a range of critical personal details. The accessed information includes customers’ names, addresses, business email addresses, dates of birth, Social Security numbers, and other account specifics. Such data is typically all required for an identity thief to execute fraudulent activities under another person’s name.

IMS’s admission that it might never be able to precisely identify what information was accessed underscores the severity and potential long-term consequences of the breach. This uncertainty adds an additional layer of anxiety for customers, highlighting the challenges in mitigating the aftermath of such security failures.

Finally, Walmart and Home Depot will be the star of the show this week they report their earnings for the holiday quarter. Nvidia will also try to keep its historic hot streak going when it reports on Wednesday—expectations are through the roof.

Despite the convenience of avoiding probate, a TOD account does not inherently provide tax benefits or protections against estate or inheritance taxes.

Upon your death, estate taxes may apply if the total value of your estate exceeds the federal exemption threshold, which is $13.61 million in 2024. Most people won’t come anywhere close to this level. However, a handful of states do impose inheritance taxes, which are paid by beneficiaries, though these exemption amounts are also generously high.

For capital gains, beneficiaries get a step-up in basis to the fair market value of the assets at the date of your death, which can provide significant tax benefits if the assets have appreciated in value.

“”Medical economics and finance is an integral component of the health care industrial complex. Its language is a diverse and broad-based concept covering many other industries: accounting, insurance, mathematics and statistics, public health, provider recruitment and retention, Medicare, health policy, forecasting, aging and long-term care, are all commingled arenas.

The Dictionary of Health Economics and Finance will be an essential tool for doctors, nurses and clinicians, benefits managers, executives and health care administrators, as well as graduate students and patients? With more than 5,000 definitions, 3,000 abbreviations and acronyms, and a 2,000 item oeuvre of resources, readings, and nomenclature derivatives? it covers the financial and economics language of every health care industry sector.”” – From the Preface byDavid Edward Marcinko “

Posted on February 13, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

The Medical Practice Walk-through – A Necessity?

Dr. David E. Marcinko MBA

The most effective means for any professional appraiser to confirm his or her understanding of business value, and how internal controls over financial and managerial reporting is designed and operated in a medical practice, is to evaluate and test its effectiveness.

This includes making inquiries about and observing the personnel who actually perform the managerial duties and controls; reviewing documents that are used in – and that result from – the application of the controls; and comparing supporting documentation to the accounting records.

In performing an onsite office walkthrough, professional valuators examine and review transactions in a medical practices information system to the point where it is reflected in the company’s financial reports.

Practice onsite walkthroughs provide the valuator with evidence to:

·Confirm the medical process flow of transactions

·Understand the management design components of a medical practice valuation related to the prevention or detection of fraud, over utilization, excessive expenses, etc

·Learn about office workforce processes by determining whether points at which misstatements related to each relevant financial statement assertion that could occur have been identified

·Document whether office controls have been placed in operation.

Of course, an onsite walk-through is the premier component of any comprehensive medical practice valuation engagement.

CONCLUSION: What are your thoughts on onsite valuation visits; pro or con?

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

Three healthcare industry groups—America’s Health Insurance Plans (AHIP), the American Medical Association (AMA), and the National Association of Accountable Care Organizations (NAACOS)—released the 36-page playbook on July 25th, 2023. Adoption of the best practices in the playbook is voluntary; the playbook is intended to encourage the adoption of value-based care arrangements in the private sector, according to a news release from the three groups.

Under a value-based care model, providers are reimbursed based on patient outcomes rather than the quantity of services provided like in the traditional fee-for-service model. The value-based care model has been around since the late 1960s. But, widespread adoption has been slow—less than half of the primary care physicians said in a 2022 survey from the Commonwealth Fund that they had received any value-based payments.

ACOs are groups of doctors, hospitals, and other health care providers, who come together voluntarily to give coordinated high-quality care to their Medicare patients. The goal of coordinated care is to ensure that patients get the right care at the right time, while avoiding unnecessary duplication of services and preventing medical errors.

When an ACO succeeds both in delivering high-quality care and spending health care dollars more wisely, the ACO will share in the savings it achieves for the Medicare program.

Now, suppose that in a new Accountable Care Organization [ACO] contract, a certain medical practice was awarded a new global payment or capitation styled contract that increased revenues by $100,000 for the next fiscal year. The practice had a gross margin of 35% that was not expected to change because of the new business. However, $10,000 was added to medical overhead expenses for another assistant and all Account’s Receivable (AR) are paid at the end of the year, upon completion of the contract.

Cost of Medical Services Provided (COMSP):

The Costs of Medical Services Provided (COMSP) for the ACO business contract represents the amount of money needed to service the patients provided by the contract. Since gross margin is 35% of revenues, the COMSP is 65% or $65,000. Adding the extra overhead results in $75,000 of new spending money (cash flow) needed to treat the patients. Therefore, divide the $75,000 total by the number of days the contract extends (one year) and realize the new contract requires about $ 205.50 per day of free cash flows.

Assumptions

Financial cash flow forecasting from operating activities allows a reasonable projection of future cash needs and enables the doctor to err on the side of fiscal prudence. It is an inexact science, by definition, and entails the following assumptions:

All income tax, salaries and Accounts Payable (AP) are paid at once.

Durable medical equipment inventory and pre-paid advertising remain constant.

Gains/losses on sale of equipment and depreciation expenses remain stable.

Gross margins remain constant.

The office is efficient so major new marginal costs will not be incurred.

Physician Reactions:

Since many physicians are still not entirely comfortable with global reimbursement, fixed payments, capitation or ACO reimbursement contracts; practices may be loath to turn away short-term business in the ACA era. Physician-executives must then determine other methods to generate the additional cash, which include the following general suggestions:

1. Extend Account’s Payable

Discuss your cash flow difficulties with vendors and emphasize their short-term nature. A doctor and her practice still has considerable cache’ value, especially in local communities, and many vendors are willing to work them to retain their business

2. Reduce Accounts Receivable

According to most cost surveys, about 30% of multi-specialty group’s accounts receivable (ARs) are unpaid at 120 days. In addition, multi-specialty groups are able to collect on only about 69% of charges. The rest was written off as bad debt expenses or as a result of discounted payments from Medicare and other managed care companies. In a study by Wisconsin based Zimmerman and Associates, the percentages of ARs unpaid at more than 90 days is now at an all time high of more than 40%. Therefore, multi-specialty groups should aim to keep the percentage of ARs unpaid for more than 120 days, down to less than 20% of the total practice. The safest place to be for a single specialty physician is probably in the 30-35% range as anything over that is just not affordable.

The slowest paid specialties (ARs greater than 120 days) are: multi-specialty group practices; family practices; cardiology groups; anesthesiology groups; and gastroenterologists, respectively. So work hard to get your money, faster. Factoring, or selling the ARs to a third party for an immediate discounted amount is not usually recommended.

3. Borrow with Short-Term Bridge Loans

Obtain a line of credit from your local bank, credit union or other private sources, if possible in an economically constrained environment. Beware the time value of money, personal loan guarantees, and onerous usury rates. Also, beware that lenders can reduce or eliminate credit lines to a medical practice, often at the most inopportune time.

4. Cut Expenses

While this is often possible, it has to be done without demoralizing the practice’s staff.

5. Reduce Supply Inventories

If prudently possible; remember things like minimal shipping fees, loss of revenue if you run short, etc.

6. Taxes

Do not stop paying withholding taxes in favor of cash flow because it is illegal.

Hyper-Growth Model:

Now, let us again suppose that the practice has attracted nine more similar medical contracts. If we multiple the above example tenfold, the serious nature of potential cash flow problem becomes apparent. In other words, the practice has increased revenues to one million dollars, with the same 35% margin, 65% COMSP and $100,000 increase in operating overhead expenses. Using identical mathematical calculations, we determine that $750,000 / 365days equals $2,055.00 per day of needed new free cash flows! Hence, indiscriminate growth without careful contract evaluation and cash flow analysis is a prescription for potential financial disaster.

Posted on February 7, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

THE FUTURE OF ELDER CARE FOR ENTREPRENEURIAL DOCTORS?

By Dr. David Edward Marcinko MBA

***

***

I was delighted to read a scientific paper that goes beyond just detailing a complex topic and encourages us to broaden our horizons, imagine what the future of elder care could hold and define our roles in shaping it’s future.

It was sent to me my colleague Bertalan Meskó, MD PhD [The Medical Futurist]

Colleagues know that I enjoy personal coaching and public speaking and give as many talks each year as possible, at a variety of medical society and financial services conferences around the country and world.

These include lectures and visiting professorships at major academic centers, keynote lectures for hospitals, economic seminars and health systems, keynote lectures at city and statewide financial coalitions, and annual keynote lectures for a variety of internal yearly meetings.

I’m a late career entry and 55 year old burned out doctor who wants out. Can I retire in 2 years with a pension of $6,100 a month (net). I have $825,000 in my 401(k) and 457 plan and a mortgage of $95,000 at 5.30%. I am not planning to move and will retire in place.

SOME THOUGHTS AND ANSWERS?

Congratulations on you solid retirement fund on top of a pending pension.

The first step you should take is to create a detailed budget for your retirement years. Consider expected living costs, healthcare expenses, travel and any other major expenses. Many folks make the mistake of setting up a monthly budget, but keep out significant milestones that are often costly, such as paying for a child’s college education or wedding.

Next, you should figure out your plan for housing. Mortgage payments, upkeep and taxes are important considerations. There was no mention of mortgage equity.

Another factor to take into account is state and Federal tax projections. If the 401(k) funds are all pre-tax dollars, any distributions will be taxable and there may be penalties if funds are withdrawn prior to 59 ½ years old. That will impact your retirement plan if you’re preparing to retire at 57-58.

It also sounds like you haven’t taken into account your Social Security allowance. It’s possible that your pension is one that comes with a government pension offset which would explain why you didn’t include it. On the other hand, maybe you’re thinking it’s far out enough that it doesn’t factor into your calculations?

Finally, you may want to look for a fee-only financial advisor that is paid directly by the client and doesn’t receive commissions for recommending financial products. So, advice is less biased. And get a fiduciary advisor which means they are required to put your best interests ahead of their own.

Also, someone with medical niche specificity. Good Luck!

***

NOTE: This is not an offer to buy or sell any security or interest. All investing involves risk, including loss of principal. Working with an adviser may come with potential downsides such as payment of fees (which will reduce returns). There are no guarantees that working with an adviser will yield positive returns. The existence of a fiduciary duty does not prevent the rise of potential conflicts of interest.

Marketing plays a vital role in successful practice ventures. How well you market your practice, along with a few other considerations, will ultimately determine your degree of success or failure.

The key element of a successful marketing plan is to know your patients – their likes, dislikes and expectations. By identifying these factors, you can develop a strategy that will allow you to arouse and fulfill their wants and needs.

The Beginning

Identify your patients by their age, sex, income/educational level and residence. At first, target only those patients who are more likely to want or need your medical services. As your patient base expands, you may need to consider modifying the marketing plan to include other patient types or medical services.

Your marketing plan should be included in your medical business plan and contain answers to the questions asked below:

·Who are your patients; define your target market(s)?

·Are your markets growing; steady; or declining?

·How is the practice unique?

·What is its market position?

·Where will we implement the marketing strategy?

·How much revenue, expense and profit will the practice achieve?

·Are your markets large enough to expand?

·How will you attract, hold, increase your market share?

·If a franchise, how is your market segmented?

·How will you promote your practice and services?

Practice Competition

Competition is a way of life. We compete for jobs, promotions, scholarships to institutions of higher learning, medical school, residency and fellowship programs, and in almost every aspect of our lives.

When considering these and other factors, we can conclude that medical practice is a highly competitive, volatile arena. Because of this volatility and competitiveness, it is important to know your medical competitors. Questions like these can help you determine:

·Who are your five nearest direct physician competitors?

·Who are your indirect physician competitors?

·How are their practices: steady; increasing; or decreasing?

·What have you learned from their operations or advertising?

·What are their strengths and weaknesses?

·How do their services differ from yours?

***

***

Patient Targeting

Patient targeting generally describes the strategic competitive advantage and/or professional synergy that is specific and unique to the practice. Intuitively, it answers such questions as:

·Who is the target market?

·How is the practice unique?

·What is its market position?

·Where will we implement the marketing strategy?

· How much revenue, expense and profit will the practice achieve?

The science of modern marketing however, is based on intense competition largely derived from the interplay of five forces, codified in the early 1980s, by Professor Michael F. Porter of Harvard Business School. They are placed in this section of the business plan and include the following:

Power of suppliers: The bargaining power of physicians has weakened markedly in the last managed care decade. Reasons include demographics, technology, over/under supply and a lack of business acumen.

Power of buyers: Corporate buyers of employee healthcare are demanding increased quality and decreased premium costs within the entire healthcare industry. The extents to which these conduits succeed in their bargaining efforts depend on several factors:

·Switching Costs: Notable emotional switching costs include the turmoil caused by uprooting a trusted medical provider relationship.

·Integration Level: The practitioner must decide early on whether or not he will horizontally integrate as a solo practitioner, or vertically integrate into a bigger medical healthcare complex.