BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

More than 20 years ago I crafted a comprehensive holistic financial plan for a young doctor colleague who was born in 1959. In fact, he was not even a medical student at the time; so “canned off-the-shelf plans”, computer generated software or generic spread sheets were not a viable creation option. It was all a granular, detailed, specific and cognitive work-product. Today, he is a board-certified internist.

So, in 2023, it is right and just to take a look back and see how well, or poorly, we’ve fared.

Now, I appreciate more than most how financial planning is a “process”; and not an isolated event. Yet, all sorts of “advisors” and “consultants” create and charge hefty fees for same, and on-going monitoring, every day.

The ME-P Challenge

Nevertheless, I challenge all you mid-career or senior financial planners /advisors to this competition; regardless of degree, certification or designation.

“Show me your financial plan” – AND – “I’ll show you my financial plan”

Here Comes the Judge

Then, our community of ME-P readers, subscribers, visitors and “judges” will decide the winner.

The contest is open to any financial advisor, planner, consultant, wealth manager, CFP®, CFA, insurance agent, CPA or CLU, ChFC, or stock-broker, etc., who is not afraid of transparency in his or her work product and purported expertise.

***[Creating and Evaluating a physician focused financial plan]

***

Assessment

So, just send in a copy of any “blinded” physician-focused financial plan that is about 21 years old. We will post for all to see and review …. warts and all … including my own; three part mega-plan!

The winner will receive bragging rights, academic swagger, and expert promotion to our entire ME-P ecosystem and network of medical, business, law and graduate school communities; as well as physicians, nurses, healthcare executives and allied health care professionals.

An informed sought-after and lucrative sector – indeed!

IOW: Free publicity and positive “new-wave” PR – PRICELESS!

Of course, as an educator and professor of health economics and finance, we are pleased to present you with the deep medical business knowledge and detailed financial,managerial and accounting techniques used, with some real-life “tips and pearls” developed over the last two decades of R&D, right here:

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on November 12, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

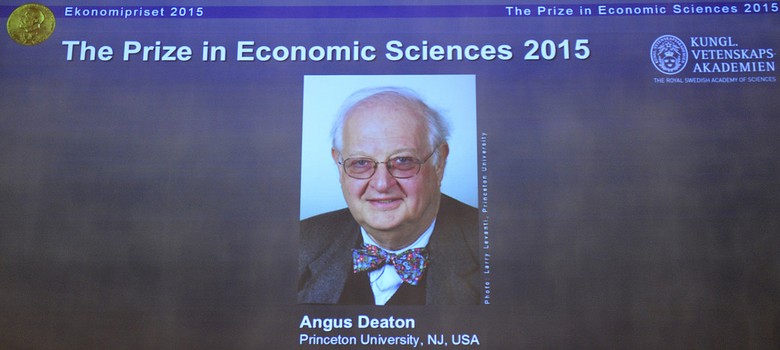

Angus Deaton’s 1980s studies, including one called “Why is consumption so smooth?” gave birth to a concept called the Deaton Paradox — in short, sharp shocks to income didn’t seem to cause similarly large shocks to consumption.

IOW: Consumption varies surprisingly smoothly despite sharp variations in income.

According to David Henderson, this was an important development in understanding the actions of consumers, causing economists to rethink the “permanent income hypothesis” developed by Milton Friedman, which suggested that people spend based on their lifetime income.

And, Mike Bird wrote a good article on Deaton the highlighted the Nobel Prize in Economics Committee.

Classic Definition: Despite rising costs, health care often is of poor quality. Evidence from a classic medical improvement outcomes study assessed care of patients with several chronic diseases. This study found that patients’ functional health status outcomes are similar to care rendered by specialists and generalists but that generalists use far fewer resources. Similar outcome at lower cost represents higher value.

Modern Circumstance: Current solutions to improving care quality may do more harm than good if they focus more on diseases than on people. Efforts to improve the parts (evidence-based care of specific diseases) may not necessarily improve the whole (the health of people and populations).

Expanding access to specialty care, for example, has been proposed as both a source of and a solution for deficiencies in quality of care. Primary care is touted as an essential building block of a high-value health care system even as it is undermined by systems attempting to improve the quality, effectiveness, and value of their health care..

Paradox Example: The above contradictions plague improvement efforts in health care systems around the world, particularly the United States The paradox is that compared with specialty care or with systems dominated by specialty medical care, primary care is associated with the following: (1) poorer quality care for individual diseases, yet (2) similar functional health status at lower cost for people with chronic disease, and (3) better quality, better health, greater health equity and lower costs for whole peoples and populations.

And so, this contradiction plagues improvement efforts in health care systems around the world, particularly the United States.

Posted on November 11, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

On September 28th, 2024, California Governor Gavin Newsom vetoed Assembly Bill (AB) 3129, which sought to regulate private equity (PE) transactions involving healthcare organizations by requiring certain transactions to be reviewed by, and to receive approval from, the California Attorney General (AG).

In his veto message, Governor Newsom stated that the state’s Office of Health Care Affordability (OHCA), established in 2022, has the power to review and evaluate healthcare transactions (including the ones at issue in AB 3129). While OHCA does not have the power to block proposed transactions, as the AG would have had under AB 3129, it can refer transactions to the AG for further examination. Put simply, the governor’s veto seems to stem from concern that taking power away from the newly-created OHCA could muddy the waters in healthcare transaction regulation.

While there is a possibility that the California legislature could override Governor Newsom’s veto, it appears unlikely as of the publication of this Alert. However, the overall popularity of this bill in the legislature (as evidenced by the fairly wide margins with which it passed) indicates that PE groups looking to transact in the healthcare space – both in California and across the U.S. – should be on high alert, as regulators are increasingly turning their focus on the role of PE in healthcare.

According to Wikipedia, a fundamental tenet of the paradox is that the customer, i.e. the potential purchaser of the information describing a technology (or other information having some value, such as facts), wants to know the technology and what it does in sufficient detail as to understand its capabilities or have information about the facts or products to decide whether or not to buy it. Once the customer has this detailed knowledge, however, the seller has in effect transferred the technology to the customer without any compensation. This has been argued to show the need for patent protection [HIPPA].

If the buyer trusts the seller or is protected via contract, then they only need to know the results that the technology will provide, along with any caveats for its usage in a given context. A problem is that sellers lie, they may be mistaken, one or both sides overlook side consequences for usage in a given context, or some unknown-unknown affects the actual outcome.

In what some are calling the next iteration of the internet, the metaverse is an unfamiliar digital world where you could be an avatar navigating computer-generated places and interacting with others in real time. In this space, the constraints of our physical, bricks and mortar world and travel habits fade. And new opportunities and challenges emerge.

Google in healthcare: The search giant has repeatedly successfully transferred its in-depth knowledge of algorithms in the field of medicine, particularly since it acquired DeepMind.

Apple in healthcare: Apple will keep on working on expanding the health features of its devices, Apple Watch and iPhones included.

Microsoft in healthcare: Microsoft’s cloud solutions provide integrated capabilities that make it easier to improve the healthcare experience.

Amazon in healthcare: Amazon will make further use of its vast knowledge of online shopping trends and behavior and will keep on providing what people need, from medicine to wearables.

IBM in healthcare: IBM has a lot to offer in federated learning, blockchain, and quantum computing.

Nvidia in healthcare: NVIDIA seems incredibly focused on its approach to healthcare. We can expect NVIDIA to be a leader in the use of artificial intelligence in healthcare.

Facebook in healthcare: The Metaverse developed by Facebook/Meta has incredible potential to revolutionize healthcare.

All this technology has huge potential because it uses both virtual reality (VR) and augmented reality (AR) technology to work in virtual spaces: All signs point to the metaverse being widely used as a disruptive change in healthcare, from better surgical precision to therapeutic uses to social-distance accommodations and more.

But along with these improvements come new problems that will change what we know about modern healthcare. The metaverse is a paradigm shift in healthcare that everyone involved needs to be aware of. This is because it changes how medical infrastructure is built, how startup costs are covered, and how data security and privacy are handled.

Classic: Investment purchases and private expenditures of healthcare firms, the value of related construction, and the change in inventory during the year.

Modern: Gross Revenue Per Day is the average amount charged by a hospital for one day of inpatient care (gross inpatient revenue divided by patient-census days).

Gross Revenue Per Discharge: The average amount charged by a hospital to treat an inpatient from admission to discharge (gross inpatient revenue divided by discharges).

Gross Revenue Per Visit: The average amount charged by a hospital for an outpatient visit (gross outpatient revenue divided by outpatient visits).

Posted on November 5, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

After its AI-related earnings disappointed Wall Street last quarter, Big Tech doubled down in the latest period:

Amazon spent $22.6 billion on property and equipment like data centers and chips. That’s an 81% spike from the same time last year.

Meta raised its low-end guidance for capex (capital expenditures), which could reach $40 billion by the end of the year. It beat earnings estimates, even with AR glasses subsidiary Reality Labs costing $4.4 billion in operating losses.

Apple is still betting on Apple Intelligence to boost sales. Most revenue came from the new iPhone 16, Apple Watch, and AirPods, but Apple services like TV+ and iCloud also grew massively to account for a quarter of the business.

Google crushed earnings estimates and revealed that more than 25% of all new code it writes is generated by AI (and reviewed by engineers).

Posted on November 5, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Among consideration for CVS is splitting up its assets: CVS Pharmacy, pharmacy benefit managerCVS Caremark, and insurance arm Aetna. The company has reportedly been in talks with bankers about the move, Reuters reported early this month.

Just as Nvidia will replace Intel, Sherwin Williamswill replaceDow Inc. on the Dow (how embarrassing, getting kicked off an index you share a name with). Sherwin Williams popped 4.59%, while Dow Inc. fell 2.08%.

Peloton pedaled 3.59% higher on a double upgrade from Bank of America analysts, who like the bike company’s higher profit outlook and hiring of new CEO Peter Stern from Ford.

Yum! China, the company that operates Pizza Hut and KFC restaurants in China, climbed 7.12% after announcing that new store openings translated into better-than-expected revenue and earnings last quarter.

STOCKS DOWN

Nuclear energy stocks took a big hit today after the Federal Energy Regulatory Commission ruled that Talen Energycould not increase the amount of energy its nuclear plant in Susquehanna, PA, produces in order to power an Amazon data center. Talen fell 2.23%, Vistra Corp sank 3.18%, and Constellation Energy plummeted 12.46%.

Clinical data from a Viking Therapeutics trial shows its weight-loss pill is effective. Shares soared then sank 13.36% as investors took profits.

The S&P 500®index (SPX) dipped 16.11 points (–0.28%) to 5,712.69; the $DJI dropped 257.59 points (–0.61%) to 41,794.60; and the $COMP lost 59.93 points (–0.33%) to 18,179.98.

The 10-year Treasury note yield (TNX) fell five basis points to 4.31%.

The CBOE Volatility Index® (VIX)edged up to 22.11, still below last week’s peaks.

Posted on November 3, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

Two recent court actions may serve as harbingers for the future of healthcare fraud and abuse laws. In September 2024, a federal judge in the Southern District of West Virginia ordered parties in a qui tamFalse Claims Act and Stark Law case to brief the court on the implications of Loper Bright Enterprises v. Raimondo on the interpretation of the Stark Law to the case at hand.

That same month, a federal judge in the Middle District of Florida dismissed a qui tam lawsuit on a novel theory that the False Claims Act’s whistleblower provisions are unconstitutional.

This Health Capital Topics article discusses these cases and the potential impact on federal fraud and abuse laws. (Read more…)

In-network refers to a health care provider that has a contract with your health plan to provide health care services to its plan members at a pre-negotiated rate. Because of this relationship, you pay a lower cost-sharing when you receive services from an in-network doctor.

What does out-of-network mean?

Out-of-network refers to a health care provider who does not have a contract with your health insurance plan. If you use an out-of-network provider, health care services could cost more since the provider doesn’t have a pre-negotiated rate with your health plan. Or, depending on your health plan, the health care services may not be covered at all.

Classic: Any medical provider, supplier or facility that is in-network is one that has contracted with your health insurer to provide services;as above.

Modern: Depending on your plan, if you visit an out-of-network provider, it may not be covered or might be only partially covered. When making appointments with various doctors and service providers, you may notice some are listed as “in-network” while others are “out-of-network.”

THINK: Medicare Advantage {Part C] Plans

Example: You can expect a higher deductible and out-of-pocket limit at out-of-network providers. Your coinsurance and co-payment may also be higher for out-of-network providers.

Classic Definition: Employers write checks that cover most health insurance premiums for employees and their dependents. But as the late Princeton health economist Uwe Reinhardt PhD once explained, employer-sponsored insurance is like a pickpocket taking money out of your wallet at a bar and buying you a drink. You appreciate the cocktail until you realize you paid for it yourself.

Modern Circumstance: With health coverage, employers write the check to the insurer, but employees bear the cost of the premium — the entire premium, not just the portion listed as their contribution on their pay stub. The premium money that goes to the insurance company is cash that employers would otherwise deposit in employees’ accounts like the rest of their salary.

Paradox Example: The fallacy paradox is in thinking an employer’s contribution comes out of profits. In fact, higher health insurance premiums mean lower wages for workers. Since 1999, health insurance premiums have increased 147 percent and employer profits have increased 148 percent. But in that time, average wages have hardly moved, increasing just 7 percent. Clearly workers’ wages, not corporate profits, have been paying for higher health insurance premiums. Health care costs are one — though not the only — reason wages have stagnated over the last few decades. With health insurance costs rising faster than growth in the economy, more labor costs go to benefits like health insurance and less to take-home pay. Yet the paradox that employees don’t pay for their own health insurance is widespread:

The first reason is that individuals cannot be sure what causes their wages to change or remain stagnant for decades.

The second reason is that employers want Americans to believe that they pay for their workers’ health insurance.

The third reason is that there are those who profit from the employment-based system: drug companies, device manufacturers, specialty physicians and high-income individuals.

And so, they all want you to believe companies are being magnanimous in giving you insurance, but they are not!

Posted on October 29, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Healthcare’s future as HSBC Innovation Banking collaborated with LINUS and HLTH to help prepare the healthcare ecosystem for the future. The Health 2035 report goes in depth with discussions between visionaries in the ecosystem and studies of young physicians’ forecasts for what the state of care will be in the year 2035. Download the report.

Trump Media & Technology Group soared 21.59% following a major rally at Madison Square Garden, an appearance on Joe Rogan’s podcast, and rising chances of winning the election. Fun fact: After this latest stock surge, Trump Media is now worth almost as much as social media network X.

Nio surged 10.46% thanks to an upgrade from Macquerie, whose analysts believe that the EV startup could see strong growth from new vehicle launches next year.

Spotify has earned a spot on Wells Fargo’s top pick playlist, with analysts confident the stock could rise over 20%. Shares rose 1.27%.

Lower oil prices hurt energy stock, but are a big boost for companies that spend a lot on fuel. CarnivalCorp rose 4.83%, RoyalCaribbeanCruises climbed 1.35%, and AmericanAirlines popped 3.42%.

Stocks Down

Philips floundered 15.95% after the Dutch consumer goods manufacturer missed on earnings and lowered its full-year forecast.

Boeing continued to fall yet another 2.79%, this time on the news that it is raising $19 billion through a stock offering in the hopes that it fends off a credit rating downgrade.

Oil stocks took a beating thanks to a big decline for crude prices. DiamondbackEnergy fell 3.36%, APACorp. dropped 4.51%, ExxonMobil sank 0.49%, and BP lost 1.48%.

The S&P 500® index (SPX)rose15.40points (0.27%) to 5,823.52; the Dow Jones Industrial Average® ($DJI) added 273.17 points (0.65%) to 42,387.57; and the NASDAQ Composite® ($COMP) gained 48.58 points (0.26%) to 18,567.19.

The 10-year Treasury note yield (TNX) climbed six basis points to 4.29%, the highest close since July 9.

A young clinician representative advising to consider the cost versus value of medicine. Health care concept for economic cost-effectiveness analysis, driving down medical costs, improved access.

***

Value Based CareClassic Definition: Value-based care is a type of payment model that pays doctors and hospitals for treating patients in the right place, at the right time and with just the right amount of care. You can look at it as a financial incentive to motivate healthcare providers to meet specific performance measures related to the quality and efficiency of the process. The same way, it penalizes weaker experiences, such as medical errors. The concept is often counter-intuitive.

Modern Circumstance: As healthcare costs continue to rise, value-based care has been growing in popularity compared to the traditional fee-for-service method.

Think: HMOs, PPOs, capitation payments and Medicare Advantage [Part C].

Paradox Examples:

Payment: A physician paid through fee-for-service compensation might like to see a packed medical office waiting room. More patients and services equate to higher pay. But, the same doctor paid through a VBC contract might wish to see an emptier waiting room as s/he will get the exact same daily pay for seeing fewer patients and working much less.

Prospectivity: Traditional Fee-for-Service medicine treats sick patients. VBC medicine seeks to keep patients healthy and out of the doctor’s office.

Posted on October 24, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

A “New” Clinical Numeric

DR. DAVID EDWARD MARCINKO MBA MEd

This physician-led medical website http://www.thennt.com/ seeks to explain to patients and physicians how well a particular treatment or medicine is likely to work based on a statistical model called the “Number Needed to Treat.”

Calculation

This is not really a new calculation, as it has been know for many years. In fact, I review and teach it in several of my undergraduate, graduate and business school courses [healthcare administration, statistics, epidemiology, infection control, community, public and population health, etc], and have been doing so for a few years now. My students are always amazed by it.

Brief Definition

The NNT is “a measurement of the impact of a medicine or therapy by estimating the number of patients that need to be treated in order to have an impact on one person.”

Detailed Definition

According to wikipedia; the number needed to treat (NNT) is an epidemiological measure used in assessing the effectiveness of a health-care intervention, typically a treatment with medication. The NNT is the number of patients who need to be treated in order to prevent one additional bad outcome (i.e. the number of patients that need to be treated for one to benefit compared with a control in a clinical trial). It is defined as the inverse of the absolute risk reduction.

The NNT was first described in 1988. The ideal NNT is 1, where everyone improves with treatment and no-one improves with control. The higher the NNT, the less effective is the treatment. Variants are sometimes used for more specialized purposes.

One example is number needed to vaccinate. NNT values are time-specific. For example, if a study ran for 5 years and it was found that the NNT was 100 during this 5 year period, in one year the NNT would have to be multiplied by 5 to correctly assume the right NNT for only the one year period (in the example the one year NNT would be 500).

And so, your thoughts and comments on this ME-P are appreciated. Give em’ a click and tell us what you think http://www.thennt.com? Do you use the concept of NNT in your clinical medical practice; why or why not? Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Channel Surfing

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

PRUDENT BUYER: The efficient purchaser of market balance between value and cost.

PRUDENT MAN RULE: An 1830 court case stating that a person in a fiduciary capacity (a trustee, executor, custodian, etc) must conduct him/herself faithfully and exercise sound judgment when investing monies under care. “He is to observe how men of prudence, discretion and intelligence manage their own affairs, not in regard to speculation, but in regard to the permanent distribution of their funds, considering the probable income as well as the probable safety of the capital to be invested.” Allows for mutual funds and variable annuities.

PRUDENT INVESTOR RULE: A fiduciary is required to conduct him/herself faithfully and exercise sound judgment when investing monies and take measured and reasonable investment risks in return for potential future rewards. Allows for mutual funds, stocks, bonds, variable annuities asset allocation & Modern Portfolio Theory.

Although some might view a budget as unnecessarily restrictive, sticking to a spending plan can be a useful tool in enhancing the wealth of a medical practice. So, I will emphasize keys to smart budgeting and how to track spending and savings in these tough economic times.

There is an aphorism that suggests, “Money cannot buy happiness.” Well, this may be true enough but there is also a corollary that states, “Having a little sure reduces the unhappiness.”

Unfortunately, today there is more than a little financial unhappiness in all medical specialties. The challenges range from the commoditization of medicine, aging demographics, Medicare reimbursement cutbacks and increased competition to floundering equity markets, the home mortgage crisis, the squeeze on credit and declines in the value of a practice. Few doctors seem immune to this “perfect storm” of economic woes.

Far too many physicians are hurting and it is not limited to above-average earning professionals. However, one can strive to reduce the pain by following some basic budgeting principles. By adhering to these principles, physicians can eliminate the “too many days at the end of the month” syndrome and instead develop a foundation for building real wealth and security, even in difficult economic climates like we face today.

There are three major budget types. A flexible budget is an expenditure cap that adjusts for changes in the volume of expense items. A fixed budget does not. Advancing to the next level of rigor, a zero-based budget starts with essential expenses and adds items until the money is gone. Regardless of type, budgets can be extremely effective if one uses them at home or the office in order to spot money troubles before they develop.

For the purpose of wealth building, doctors may think of this budget as a quantitative expression of an action plan. It is an integral part of the overall cost-control process for the individual, his or her family unit or one’s medical practice.

Preparing a net income statement (lifestyle cash flow budget) is often difficult because many doctors perceive it as punitive. Most doctors do not live a disciplined spending lifestyle and they view a budget as a compromise to it. However, a cash flow budget is designed to provide comfort when there is surplus income that can be diverted for other future needs. For example, if you treat retirement savings as just another periodic bill, you are more likely to save for it.

You may construct a personal cash budget by recording each cash receipt and cash disbursement on a spreadsheet. Only the date, amount and a brief description of the transaction are necessary. The cash budget is a simple tool that even doctors who lack accounting acumen can use. Since it is possible to track the cash-in and cash-out in the same format used for a standard check register, most doctors find that the process takes very little time. Such a budget will provide a helpful look at how well you are staying within available resources for a given period.

We then continue with an analysis of your operating checkbook and a review of various source documents such as one’s tax return, credit card statements, pay stubs and insurance policies. A typical statement will show all cash transactions that occur within one year. It is helpful to establish a monthly equivalent to all items of income and expense. For the purposes of getting started, note items of income and expense by the frequency you are accustomed to receiving or spending them.

What You Should Know About The ‘Action Plan’ Cash Budget

For a medical office, the first operations budget item might be salary for the doctor and staff. Operating assets and other big ticket items come next. Some of our doctors/clients review their office P&L statements monthly, line by line, in an effort to reduce expenses. Then they add back those discretionary business expenses they have some control over.

Now, do you still run out of money before the end of the month? If so, you had better cut back on entertainment, eating dinner out or that fancy, new but unproven piece of medical equipment. This sounds draconian until you remind yourself that your choice is either: live frugally later or live a simpler lifestyle now and invest the difference.

As a young doctor, it may be a difficult trade-off. By mid-life, however, you are staring retirement in the face. That is why the action plan depends on your actions concerning monetary scarcity, a plan that one can implement and measure using simple benchmarks or budgeting ratios. By using these statistics, perhaps on an annual basis, the doctor can spot problems, correct them and continue planning actively toward stated goals like building long-term wealth.

Useful Calculations To Assess Your Budgeting Success

In the past, generic budgeting ratios would emphasize not spending more than 15 to 20 percent of your net salary on food or 8 percent on medical care. Now these estimates have given way to more rigorous numbers. Personal budget ratios, much like medical practice financial ratios, represent comparable benchmarks for parameters such as debt, income growth and net worth. Although these ratios are still broad, the following represent some useful personal budgeting ratios for physicians.

• Basic liquidity ratio = liquid assets / average monthly expenses. Cash-on-hand should approach 12 to 24 months or more in the case of a doctor employed by a financially insecure HMO or fragile medical group practice. Yes, chances are you have heard of the standard notion of setting enough cash aside to cover three months in a rainy day scenario. However, we have decried this older laymen standard for many years in our textbooks, white papers and speaking engagements as being wholly insufficient for the competitively unstable environment of modern healthcare.

• Debt to assets ratio = total debt / total assets. This percentage is high initially but should decrease with age as the doctor approaches a debt-free existence

• Debt to gross income ratio = annual debt repayments / annual gross income. This represents the adequacy of current income for existing debt repayments. Doctors should try to keep this below 20 to 25 percent.

• Debt service ratio = annual debt repayment / annual take-home pay. Physicians should aim to keep this ratio below 25 to 30 percent or face difficulty paying down debt.

• Investment assets to net worth ratio = investment assets / net worth. This budget ratio should increase over time as retirement approaches.

• Savings to income ratio = savings / annual income. This ratio should also increase over time as one retires major obligations like medical school debt, a practice loan or a home mortgage.

• Real growth ratio = (income this year – income last year) / (income last year – inflation rate). This budget ratio should grow faster than the core rate of inflation.

• Growth of net worth ratio = (net worth this year – net worth last year) / net worth last year – inflation rate). Again, this budgeting ratio should stay ahead of inflation.

In other words, these ratios will help answer the question: “How am I doing?”

Pearls For Sticking To A Budget

Far from the burden that most doctors consider it to be, budgeting in one form or another is probably one of the greatest tools for building wealth. However, it is also one of the greatest weaknesses among physicians who tend to live a certain lifestyle.

In fact, we have found that less than one in 10 medical professionals have a personal budget. Fear, or a lack of knowledge, is a major cause of procrastination. Fortunately, the following guidelines assist in reversing this microeconomic disaster.

1. Set reasonable goals and estimate annual income. Do not keep large amounts of cash at home or office. Deposit it in an FDIC insured money-market account for safety. Do not deposit it in a money market mutual fund with net asset value (NAV) that may “break the buck” and fall below the one-dollar level. Track actual bills and expenses.

2. Do not pay bills early, do not have more taxes withheld from your salary than needed and develop spending estimates to pay fixed expenses first. Fixed expenses are usually contractual and usually include housing, utilities, food, Social Security, medical, debt repayments, homeowner’s or renter’s insurance, auto, life and disability insurance, etc. Reduce fixed expenses when possible. Ultimately, all expenses get paid and become variable in the long run.

3. Make it a priority to reduce variable expenses. Variable expenses are not contractual and may include clothing, education, recreational, travel, vacation, gas, cable TV, entertainment, gifts, furnishings, savings, investments, etc. Trim variable expenses by 5 to 20 percent.

4. Use “carve-outs or “set-asides” for big ticket items and differentiate true wants from frivolous needs.

5. Calculate both income and expenses as a percentage of your total budget. Determine if there is a better way to allocate resources. Review the budget on a monthly basis to notice any variance. Determine if the variance was avoidable, unavoidable or a result of inaccurate assumptions. Take corrective action as needed.

6. Know the difference between saving and investing. Savers tend to be risk adverse while investors understand risk and take steps to mitigate it. Watch mutual fund commissions and investment advisory fees, which cut into return-rates. Keep investments simple and diversified (stocks, bonds, cash, index, no-load mutual and exchange traded funds, etc.).

Sooner or later, despite the best of budgeting intentions, something will go awry. A doctor will be terminated or may be the victim of a reduction-in-force (RIF) because of cost containment initiatives.4 A medical practice partnership may dissolve or a local hospital or surgery center may close, hurting your practice and livelihood. Someone may file a malpractice lawsuit against you, a working spouse may be laid off or you may get divorced. Regardless of the cause, budgeting crisis management encompasses two different perspectives: awareness and execution.

First, if you become aware that you may lose your job, the following proactive steps will be helpful to your budget and overall financial condition.

• Decrease retirement contributions to the required minimum for company/practice match. • Place retirement contribution differences in an after-tax emergency fund. • Eliminate unnecessary payroll deductions and deposit the difference to cash. • Replace group term life insurance with personal term or universal life insurance. • Take your old group term life insurance policy with you if possible. • Establish a home equity line of credit to verify employment. • Borrow against your pension plan only as a last resort.

If you have lost your job or your salary has been depressed, negotiate your departure and get an attorney if you believe you lost your position through breach of contract or discrimination. Then execute the following steps to recalculate your budget and boost your wealth rebuilding activities.

• Prioritize fixed monthly bills in the following order: rent or mortgage; car payments; utility bills; minimum credit card payments; and restructured long-term debt.

• Consider liquidating assets to pay off debts in this order: emergency fund, checking accounts, investment accounts or assets held in your children’s names.

• Review insurance coverage and increase deductibles on homeowner’s and automobile insurance for needed cash.

• Then sell appreciated stocks or mutual funds; personal valuables such as furnishings, jewelry and real estate; and finally, assets not in pension or annuities if necessary.

• Keep or rollover any lump sum pension or savings plan distribution directly to a similar savings plan at your new employer, if possible, when you get rehired.

• Apply for unemployment insurance.

• Review your medical insurance and COBRA coverage after a “qualifying event” such as job loss, firing or even after quitting. It is a bit expensive due to a 2 percent administrative fee surcharge but this may be well worth it for those with preexisting conditions or who are otherwise difficult to insure. One may continue COBRA for up to 18 months.

• Consider a high deductible Health Savings Account (HSA), which allows tax-deferred dollars like a medical IRA, for a variety of costs not normally covered under traditional heath insurance plans. Self-employed doctors deduct both the cost of the premiums and the amount contributed to the HSA. Unused funds roll over until the age of 59½, when one can use the money as a supplemental retirement benefit.

• Eliminate unnecessary variable, charitable and/or discretionary expenses, and become very frugal.

Final Notes

The behavioral psychologist, Gene Schmuckler, PhD, MBA, sometimes asks exasperated doctors to recall the story of the old man who spent a day watching his physician son treating HMO patients in the office. The doctor had been working at his usual feverish pace all morning. Although he was working hard, he bitterly complained to his dad that he was not making as much money as he used to make. Finally, the old man interrupted him and said, “Son, why don’t you just treat the sick patients?” The doctor-son looked at his father with an annoyed expression and responded, “Dad, can’t you see, I do not have time to treat just the sick ones.”

Always remember to add a bit of emotional sanity into your budgeting and economic endeavors.

Regardless of one’s age or lifestyle, the insightful doctor realizes that it is never too late to take control of a lost financial destiny through prudent wealth building activities. Personal and practice budgeting is always a good way to start the journey.

NOTE: Dr. Marcinko is a former Certified Financial Planner and current Certified Medical Planner™. He has been a medical management advisor for more than a decade. He is the CEO of http://www.MarcinkoAssociates.com

The authors acknowledge the assistance of Mackenzie H. Marcinko PhD in the preparation of this article.

Posted on October 19, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

ACCORDING TO AUSTRIAN ECONOMISTS

BY PER BYLUND

Colleague Peter R. Quinones and Per Bylund return to the show to talk about the role of the entrepreneur not only in society, but according to the Austrian School of Economics. Medical perspectives are implied.

Posted on October 19, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

CVS Health may be breaking up…with itself. The board of directors at CVS Health—the parent company of CVS Pharmacy, pharmacy benefit managerCVS Caremark, and insurance unit Aetna—are working with a group of bankers to review the company’s strategy, which according to Reuters, may lead to a split between its pharmacy division and Aetna.

Apple climbed 1.23% on a Bloomberg report that iPhone 16 demand has been shockingly strong in China.

Verizon Communications will purchase $1 billion worth of US Cellular’s wireless spectrum licenses. Verizon rose just 0.34%—but it’s a huge deal for US Cellular, which popped 7.22%, and Telephone and Data Systems, which owns 82% of US Cellular, and soared 15.40%.

Intuitive Surgical rose to a new all-time high, climbing 10.01% on strong earnings powered by sales of its da Vinci device.

Lamb Weston, the company behind the french fries you overindulge in every time you go out to dinner, is being pushed by activist investor Jana Partners toward exploring a sale. Shareholders rejoiced, and the stock rose 10.17%.

Stocks Down

CVS Health sank 5.23% on the news that CEO Karen Lynch will be replaced by David Joyner after three years at the helm of the struggling pharmacy/retailer. Joyner ran the company’s pharmacy service business for the last two years.

WD-40 seems like the staple of all consumer staples, but the company missed on both revenue and earnings estimates last quarter. Shares fell 4.79% on the news.

American Express dropped 3.15% after the credit card company reported a rare miss today, beating bottom-line estimates but missing revenue forecasts last quarter.

MGP Ingredients makes all the booze you drink under different brand names, but people aren’t drinking enough. The beverage maker issued preliminary earnings that included a 24% drop in sales. Shares tanked 24.16%.

Here’s where the major stock market benchmarks ended:

The S&P 500® index (SPX)rose 23.20 points (0.40%) to 5,864.67, a new record high close, to end the week up 0.85%; the Dow Jones Industrial Average® ($DJI) added 36.86 points (0.09%) to 43,275.91, also another record high finish, to end the week up 0.96%; and the $COMP gained 115.94 points (0.63%) to 18,489.55 to end the week up 0.80%.

The 10-year Treasury note yield (TNX) fell two basis points to 4.07%.

The CBOE Volatility Index® (VIX) fell to 18.17, the lowest since September 30.

A new survey results may prompt health systems to second-guess some of their future plans. A recent University of Michigansurvey found 74% of adults ages 50+ have “very little or no trust” in health info generated by AI. Maybe it’s not time to roll out chatbots on patient portals just yet.

Posted on October 18, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Are doctors using publicly available tools like ChatGPT? The answer, Fierce Healthcare finds, is yes. In the first in-depth look of its kind into physician use of public genAI tools, Fierce Healthcare spoke with nearly two dozen doctors, students, AI experts and regulators, and helped conduct a survey of more than 100 physicians. The reporting confirms that some doctors are turning to tools intended for non-clinical uses to make clinical decisions.

A collaborative survey between Fierce Healthcare and physician social network Sermo found that 76% of respondents reported using general-purpose LLMs in clinical decision-making. With no standardized guidelines, lagging physician training and regulators racing to try to keep up with rapidly changing technology, guardrails to protect patients appear to be years behind current rates of utilization.

Posted on October 18, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Chip stocks recovered lost ground today thanks to a strong earnings report from TSMC (more on that below). Nvidia led the group higher, rising 0.89% to yet another new all-time high.

Blackstone rose 6.30% to a new record high after the world’s largest alternative asset manager reported an excellent quarter.

Expedia popped 4.75% after a report by the Financial Times revealed that Uber had explored an acquisition of the travel site. Expedia shareholders cheered the news, while Uber shares sank 2.45%.

Stocks Down

Robinhood fell 2.27% after announcing its new Legend trading platform geared specifically toward advanced traders.

Lucid Group plummeted 17.99% on the news that the EV automaker is offering over 262 million shares of its common stock in an attempt to raise funds.

CSX dropped 6.71% after missing both top- and bottom-line estimates last quarter thanks in no small part to hurricanes Helene and Milton.

Health insurance stocks took a beating today due to a not-great earnings report from ElevanceHealth (more on that below, too). Centene Corp. fell 9.09%, while Molina Healthcare tumbled 12.55%.

The S&P 500® index (SPX) slipped 1.00point (–0.02%) to 5,841.47; the $DJI added 161.35 points (0.37%) to 43,239.05; and the NASDAQ Composite®($COMP) rose 6.53 points (0.04%) to 18,373.61.

The 10-year Treasury note yield (TNX) climbed eight basis points to 4.1%.

The CBOE Volatility Index® (VIX) sank to 18.97 by late Thursday, a two-week low.

The average amount owed on “upside down” auto loans, in which the balance is more than the car is worth, hit a record high of $6,458 in the third quarter, according to Edmunds, a site that helps consumers research and buy cars

Posted on October 17, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Authors of the seminal textbook Why Nations Fail, Daron Acemoglu, James Robinson, and former International Monetary Fund chief economist Simon Johnson will split the roughly $1 million cash prize for their research, which found a link between a country’s prosperity and the institutions it established during European colonization.

Places developed either “inclusive” or “extractive” institutions based on population density. The former allowed for inclusive governance (i.e., democracy), while the latter extracted resources to benefit a small group of elites.

Countries that developed inclusive institutions have experienced long-term prosperity; those with exclusive institutions haven’t. “Broadly speaking, the work that we have done favors democracy,” Acemoglu said.

Eample: In the twin cities of Nogales, on the US-Mexico border, the north and south parts of the transborder city have the same climate and the same resources, but the section in the US is far richer because of the country’s institutions, according to the researchers.

Critics. Some academics argue the Nobel winners’ premise ignores the effects of culture on prosperity. Others point to an irrefutable counterexample: China continues to experience explosive growth despite having an autocratic government.

Posted on October 15, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters &The Medicare Team

Medicare open enrollment—which runs from October 15th through December 7th this year—is your chance to check in on your Medicare plan and, if needed, change it.

***

***

Mark your calendars — Medicare Open Enrollment starts October 15th! Did you know new benefits are coming to Medicare drug coverage next year?

Also starting next year, you can choose to participate in a program that spreads your out-of-pocket drug costs across the calendar year, instead of paying all at once at the pharmacy. It’s called the Medicare Prescription Payment Plan — and you can opt in with your plan throughout the 2025 plan year. Contact your plan for more details.

Remember, Medicare plans can change from one year to the next, and so can your health needs. Preview and compare all your health and drug options and see if you can save!

Posted on October 13, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

AVERAGE REVENUE PER CASE

By Staff Reporters

***

Podiatry is 3rd in Average Revenue Per Case in ASCs

***

***

Orthopedic surgery topped the pack for ASC revenue per case, according to VMG Health’s “Multi-Specialty ASC Benchmarking Study” for 2022.

The specialty was only the fourth most-represented among ASC cases, however. Nationally, gastroenterology was the most-represented specialty among ASCs, with 32 percent of all cases, followed by ophthalmology, with 26 percent, and pain management and orthopedics, with 22 and 21 percent, respectively.

Posted on October 11, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

With the annual enrollment period for Medicare Advantage (MA) plans slated to open in less than two months, many MA plans are cutting benefits and provider payments, while approving fewer claims. Further, after a decade of accelerated growth in the MA market, several MA plan executives have announced MA market exits and decreases in membership for the upcoming plan year.

This Health Capital Topics article discusses recently announced MA market exits, the reasons for those exits, and the current environment in which MA plans are operating. (Read more...)

Posted on October 11, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

Understanding Horizontal and Vertical Integration

ENCORE PRESENTATION

[By Robert James Cimasi MHA, AVA, CMP™]

Health Capital Consultants, LLC

St. Louis MO

Several potential benefits are associated with the integration of companies in the same or related industries. These synergistic benefits depend upon the type of companies and their integration strategies, as well as whether the anticipated transaction is a manifestation of horizontal consolidation or vertical integration.

Horizontal consolidation is “the acquisition and consolidation of like organizations or business ventures under a single corporate management, in order to produce synergy, reduce redundancies and duplication of efforts or products, and achieve economies of scale while increasing market share.”

Vertical integration involves the joining of organizations that are fundamentally different in their product and/or services offerings, i.e., “the aggregation of dissimilar but related business units, companies, or organizations under a single ownership or management in order to provide a full range of related products and services.”

Healthcare Locality

As healthcare is essentially a local business, horizontal integration within the local market has been limited by antitrust laws. Therefore, in order to control greater market share, a hospital’s strategy has required vertical integration. Healthcare providers and organizations have placed much emphasis on the benefits of vertical system integration in the last 10 or more years, whereby a single healthcare organization owns all of the elements needed to provide a continuum of care for all the needs of a given patient population. Much of this effect has stemmed from the desire to be able provide a “continuum of care,” i.e., to be able to single source contract for the healthcare needs of a patient population and to profit from implementing preventative healthcare and utilization management measures. The relative economic benefits of this type of vertical integration versus horizontal integration strategies remain the subject of great debate in academia and among the strategic managers of other industries. One lesson that may be drawn from other industries is that neither of these forms of integration is universally applicable or beneficial to every organization and market. There are also great costs to integration, which must be outweighed by the benefits. Each specific benefit should be identified and researched when examining the probable effects of integration, consolidation, mergers or divestitures as a competitive strategy.

Rapid Consolidation Periods

During the rapid consolidation and integration of healthcare providers, insurers, and purchasers, in recent years, there was much discussion of a concept termed “managed competition.” This term appears to have been an outgrowth of the term “managed care” and was viewed by many as the logical result of the integration of healthcare markets nationally. The concept of “managed competition” apparently related to an idealized vision of competition between very large, integrated providers (organized into integrated delivery systems), large, national managed care payors, and purchasing group coalitions that could achieve a balance of power between these interacting groups. However, many believe that the result of such an arrangement would more likely be a reduction in competition between members of each of these three groups and the creation of powerful bureaucratic and intractable organizations. Further, this scenario does not appear to effectively remove any of the existing barriers to competition and therefore doesn’t introduce any additional incentives for innovation to produce value for consumers which, of course, is the “sine qua non” of competition.

Disadvantages

The disadvantages of integration are becoming apparent, including:

the loss of autonomy;

increased bureaucracy;

difficulty in aligning incentives; and

other failed expectations.

Many organizations that sought strategic advantage through integration are ending those arrangements and now divesting acquired organizations.

Other Industries

In other industries, specialized providers of goods and services are increasingly able to offer customers a full range of services through affiliation and affinity with other independent specialists, made more seamless through the use of increasingly sophisticated communications and computing technologies. However, this move to “dis-integration” must also be carefully considered if organizations are not to make further costly organizational changes inspired by a rushed judgment of general market trends.

Porter Speaks

Michael Porter (et al.) wrote in the Harvard Business Review that,

In industry after industry, the underlying dynamic is the same: competition compels companies to deliver increasing value to customers. The fundamental driver of this continuous quality improvement and cost reduction is innovation. Without incentives to sustain innovation in health care, short-term cost savings will soon be overwhelmed by the desire to widen access, the growing health needs of an aging population, and the unwillingness of Americans to settle for anything less than the best treatments available. Inevitably, the failure to promote innovation will lead to lower quality or more rationing of care — two equally undesirable results.

Assessment

Therefore, if the emerging healthcare industry is to respond successfully to the Affordable Care Act [ACA] and related market pressures to reduce costs, then the healthcare market must first create incentives for innovation. The barriers to competition cannot include barriers to innovation as many do now. Physicians, nurses, healthcare purchasers, managers, and legislators must ensure innovation takes the forefront of any reform, if it is to be effective.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

A class action lawsuit has been filed in Minnesota against UnitedHealth Group (NYSE:UNH) over allegations that the health insurer and its subsidiary, NaviHealth, used a faulty algorithm to deny rehabilitation care for Medicare Advantage beneficiaries. California-based Clarkson Law Firm filed the lawsuit in the U.S. District Court of Minnesota on Tuesday following an investigative report published by the health-focused news site Stat.

It alleges that UnitedHealth and its subsidiary, NaviHealth, used the computer algorithm named nH Predict to “systematically deny claims” of patients recovering from debilitating illnesses in nursing homes. According to the lawsuit, despite its 90% error rate, the company used the algorithm to deny claims, knowing that only 0.2% would appeal its decision. According to Stat, Humana (HUM), the nation’s second-largest player in the Medicare Advantage market behind UnitedHealth (UNH), also uses nH Predict. UnitedHealth (UNH) denied it used the NaviHealth predict tool to arrive at coverage decisions.

***

***

Ironically, UnitedHealth’s (NYSE:UNH) Optum Rx unit announced plans to move eight insulin products to “preferred” status on formularies to further expand the number of patients benefiting from $35 or less monthly out-of-pocket costs for the lifesaving therapy.

Optum Rx, UNH’s pharmacy benefit manager (PBM), said that effective January 1, 2024, all short- and rapid-acting insulins will move to Tier 1 in commercial formularies, a list of drugs the company maintains to indicate coverage for insured patients.

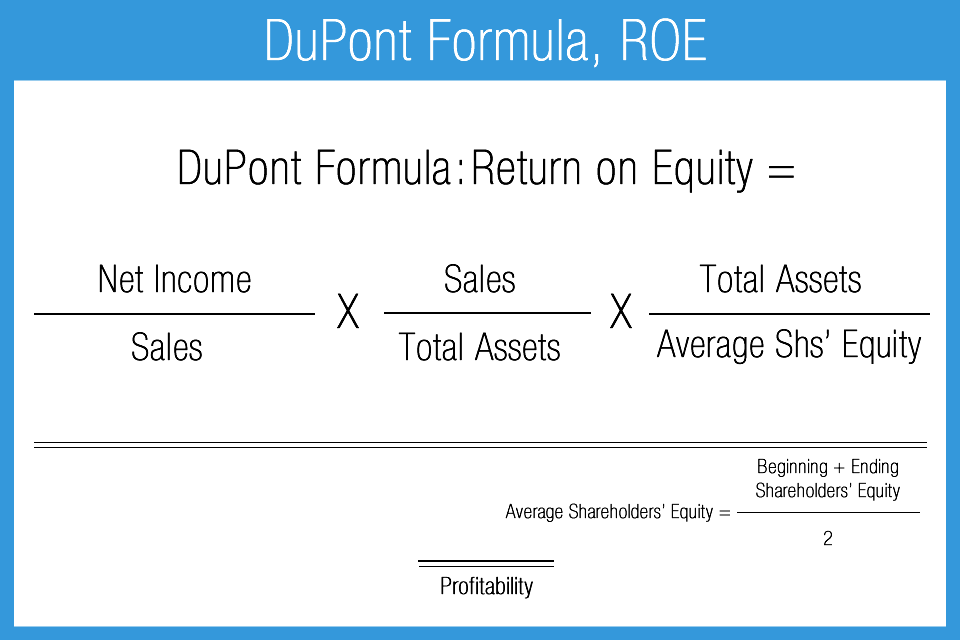

According to the Dupont Decomposition Equation – which involves the conglomeration of net operating income, revenues, expenses and average operating assets – ROI and economic profit is increased in three prioritized ways:

Cost and expense reductions.

Revenue increases [Rev]

Reduced average operating assets [AOO]

Note: ROI = NOI / Rev X Rev / AOO

Cost and expense reductions

Although many hospitals have reduced expenses, postponed projects and put clinical or information technology projects on hold because of the current healthcare conundrum, this may be unwise and quality may suffer. And, mental health care programs are almost always the first cost center to be reduced in tough times.

Upgrades today, especially with concurrent marketing and advertising promotions, may well be considered a strategic competitive advantage, and at bargain basement prices for those with cash or credit. This cost reduction is easy because it gives the biggest buck-bang in the ROI equation, and is the first line of ROI augmentation by savvy administrators and CEOs. It is also intuitive and wholly “wrung-out” in the marketplace, to date.

Revenue increases

On the other hand, revenues can usually be only incrementally increased by improving services like emergency care, urgent care, wellness, out-patient and/or surgical departments. This is the more difficult part of the equation and yields a positive, but lesser return in the ROI equation.

The following medical practice procedures will markedly increase upfront office collections:

Train staff to handle exceptions. What is your policy if the patient payment is significant? Will you allow 25% payments—one today and three over the next three months? Communicate your policy to all staff. What will you do if a patient shows up without an insurance card? There will be other exceptions. Train employees to call the appropriate practice-management contact when an exception does not fit in the categories you provide and make sure those managers are responsive.

Understand that not everyone will shine in collections. The value of this new front-desk function should be reflected in job descriptions and wages. Track staff performance and hold employees accountable for collection goals. The most successful practices collect in the 90% range.

Provide professional signage that states your basic policy. “Payments are due at time of service.” Avoid typewritten, lengthy explanations taped to walls or desks that look like clutter.

Reduced average operating assets

Finally, any delay in updating facilities – while easy and may reduce operating assets – there is little ROI advantage and profit potential. Of course, facility asset upgrades mean borrowing funds through tax-exempt bonds – the main source of debt for most hospitals – and is currently difficult or impossible in this climate. Loans from banks, private investors, angels, venture capitalists or other financial institutions are similarly difficult to obtain. Thus, this part of the equation may often be neglected; as is the case now.

The modern medical practice is both similar, and unlike, other businesses today. This disparity often adds to confusion for the private practitioner. And so, the experts at iMBA Inc, list the top 25 most urgent questions in practice financial management, asked by clients to date.

Assessment

Since inception in 2000, the Institute of Medical Business Advisors Inc., has become one of North America’s leading professional health consulting and valuation firms; and focused provider of textbooks, CDs, tools, templates, onsite and distance education for the health economics, administration and financial management policy space. As competition and litigation support activities increase and the cognitive demands of the global marketplace change, iMBA Inc is well positioned with offices in five states and Europe, to meet the needs of medical colleagues, related advisory clients and corporate customers today; and into the future.

And so, your thoughts and comments on this Medical Executive-Post are appreciated. Tell us what you think. Send in your own questions. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, be sure to subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

Subscribe Now: Did you like this Medical Executive-Post, or find it helpful, interesting and informative? Want to get the latest ME-Ps delivered to your email box each morning? Just subscribe using the link below. You can unsubscribe at any time. Security is assured.

Sponsors Welcomed

And, credible sponsors and like-minded advertisers are always welcomed.

Posted on October 4, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

[By staff reporters]

An important concept in macroeconomics

When Federal Reserve officials meet to decide whether to raise interest rates again, one question will be front and center according to Neil Irwin?

***

[Rate of Change of Wages against Unemployment

United Kingdom 1913–1948 from Phillips (1958)]

***

Question: How much faith should be placed in a line on a graph first drawn by a New Zealand economist nearly six decades ago, based on data on wages and employment in Britain dating to the 1860s?

So, if you believe in the traditional Phillips curve, as some at the Fed do, inflation should be taking off any day now?

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on October 4, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

IN PRIVATE EQUITY AND MEDICINE

By Staff Reporters

***

***

PRIVATE EQUITY

In private equity, the J curve is used to illustrate the historical tendency of private equity funds to deliver negative returns in early years and investment gains in the outlying years as the portfolios of companies mature.

And, according to Wikipedia, in the early years of the fund, a number of factors contribute to negative returns including management fees, investment costs and under-performing investments that are identified early and written down. Over time the fund will begin to experience unrealized gains followed eventually by events in which gains are realized (e.g., IPOs, mergers and acquisitions, leveraged recapitalizations).

Historically, the J curve effect has been more pronounced in the US, where private equity firms tend to carry their investments at the lower of market value or investment cost and have been more aggressive in writing down investments than in writing up investments. As a result, the carrying value of any investment that is under performing will be written down but the carrying value of investments that are performing well tend to be recognized only when there is some kind of event that forces the PE to mark up the investment.

The steeper the positive part of the J curve, the quicker cash is returned to investors. A private equity firm that can make quick returns to investors provides investors with the opportunity to reinvest that cash elsewhere. Of course, with a tightening of credit markets, private equity firms have found it harder to sell businesses they previously invested in. Proceeds to investors have reduced. J curves have flattened dramatically. This leaves investors with less cash flow to invest elsewhere, such as in other private equity firms. The implications for private equity could well be severe. Being unable to sell businesses to generate proceeds and fees means some in the industry have predicted consolidation among private equity firms.

MEDICINE

In medicine, the “J curve” refers to a graph in which the x-axis measures either of two treatable symptoms (blood pressure or blood cholesterol level) while the y-axis measures the chance that a patient will develop cardiovascular disease (CVD). It is well known that high blood pressure or high cholesterol levels increase a patient’s risk.

Paradoxically, what is less well known is that plots of large populations against CVD mortality often take the shape of a J curve which indicates that patients with very low blood pressure and/or low cholesterol levels are also at increased risk.

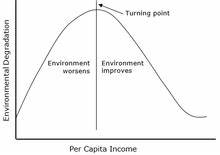

In economics, a Kuznets curve (/ˈkʌznɛts/) graphs the hypothesis that as an economy develops, market forces first increase and then decrease economic inequality.

Posted on October 3, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

NEBULOUS DEFINITIONS

By Staff Reporters

***

***

The simplest model of a market involves two things, supply and demand, and the price and quantity of the goods sold in the market are a function of both. When a natural disaster hits like Hurricane Helene, the immediate effect can be two-fold. In such situations, it is not unusual that the demand for certain products may increase. For example, if everyone is trying to leave the area, demand for gas may rise. The other effect is that supply for certain products may decrease. And, it may be more costly to transport gas in areas affected by a natural disaster, thus decreasing the supply of gas and in turn, increasing the price.

When supply decreases, the price of the good increases. And when demand increases, again the price of the good increases. So we would predict that the market price of gas, for example, would increase in areas recently affected by a hurricane. And in fact we do see this.

Price-gouging occurs when companies raise prices to unfair levels. There is no rule for what qualifies as price-gouging, but it is not an uncommon occurrence. For example in medicine, EpiPen costs is a current example of price increases that have been labeled unfair.

Note: An epinephrine auto-injector (or adrenaline auto-injector, also known by the trade mark EpiPen) is a medical device for injecting a measured dose or doses of epinephrine (adrenaline) by means of auto-injector technology. It is most often used for the treatment of anaphylaxis. The first epinephrine auto-injector was brought to market in 1983.

Posted on October 3, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Rosh Hashanah, the Jewish New Year, begins tonight and ends on Friday. Shana Tova to those celebrating.

Microsoft overhauled its Copilot AI assistant, adding voice and vision capabilities to make it more personalized.

A new report from Deloitte reveals improving health equity could increase the country’s GDP by $2.8 trillion by 2040 and increase U.S.-based corporate profits by $763 billion.

And … Johnson & Johnson’s is not moving forward with implementation of its proposed rebate model after HRSA push-back.

Caesars Entertainment popped 5.27% after it announced it will buy back $500 million in common shares while also offering $1 billion in senior notes to raise money.

Joby Aviation surged 27.92% on the news that Toyota will invest another $500 million in the aviation startup as it attempts to build a flying electric taxi.

Lamb Weston Holdings rose 2.62% thanks to a strong earnings report and a comprehensive restructuring plan for the french fry titan.

Novavax soared 19.16% following a glowing report from Jefferies analysts citing the pharma company’s strong vaccine sales.

What’s down stocks

Tesla sank 3.49% after revealing that auto deliveries for the third quarter came in lower than analysts expected.

Ford fell 2.51% for pretty much the same reason, reporting disappointing sales growth in the third quarter.

It’s never a good thing when a company pulls its guidance, and that was certainly true for Nike today. Shares dropped 6.77% after the company postponed its investor day and reported a 10% year over year decline in sales.

Nike’s report was so bad that shares of Foot Locker and Dick’s Sporting Goods fell 2.97% and 0.23%, respectively.

Humana plummeted 11.79% on the news that membership in its 4 star-rated Medicare Advantage plans plunged 94%.

Conagra Brands dropped 8.07% after the packaged food giant missed on both sales and earnings estimates last quarter.

The S&P 500® index (SPX)was little changed at 5,709.54; the Dow Jones Industrial Average ($DJI) rose 39.55 points (0.09%) to 42,196.52; the NASDAQ Composite® ($COMP) gained 14.76 points (0.08%) to 17,925.12.

The 10-year Treasury note yield (TNX) added 5 basis points to 3.78%.

The CBOE Volatility Index® (VIX) edged 0.4 points lower to 18.86.

CVS is laying off nearly 3,000. The healthcare giant is conducting a strategic review as its stock has fallen more than 20% this year, the Wall Street Journal reported

Posted on October 2, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

SIGMOID CURVE

By Staff Reporters

***

DEFINITION

The S curve refers to a chart that is used to describe, visualize, and predict the performance of a project or business overtime. More specifically, it is a logistic curve that plots the progress of a variable by relating it to another variable over time.

The term S curve was developed as a result of the shape that the data takes. Projects on the S curve often experience a slow growth at the beginning, rapid growth in the middle, and slow growth and at the end. The maximum point of acceleration is called the point of inflexion. It is at this point that the project or business returns to the initial slow growth it started from.

Posted on October 2, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Humana, the country’s second largest Medicare Advantage insurer, is aggressively culling its plan offerings after several quarters of spending more than expected on its members’ medical care, and getting hammered on Wall Street for it. The company will scrap Medicare Advantage plans in 2025 that currently cover about 560,000 members.

Markets: Stocks embraced the start of spooky season by falling yesterday, ending a hot streak as investors mulled the rising tensions in the Middle East.

General Motors: Reported slightly better-than-expected sales during the third quarter, thanks in part to increased sales of small crossovers and electric vehicles. The automaker reported a 2.2% decrease in sales, compared with a year earlier, an improvement over auto industry forecasts that projected a decline of more than 3% in the quarter.

Meanwhile:Nike’s beleaguered stock was up a bit ahead of its first earnings report since the company announced a CEO change. It withdrew its full-year guidance and postponed its investor day as longtime company veteran Elliott Hill prepares to take the top job at the sneaker giant. Instead, executives said Nike will provide quarterly guidance for the rest of the year. Shares of Nike fell about 7% in early trading Wednesday.

Posted on October 1, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

Despite inflation cooling down, employer health plan costs are heating up, according to a September analysis from consulting firm consulting firm Mercer.

CVS popped 2.38% after the Wall Street Journal reported that major shareholder Glenview Capital Management will meet with company executives to discuss potential strategies to improve the sagging stock.

Nio drove 2.45% higher thanks to a $2 billion cash injection from key shareholders into the Chinese EV company.

STOCKS DOWN

Stellantis, the European company behind Chrysler, Dodge, and Jeep sank 12.49% after it warned that sales in the second half of its fiscal year will come in lower than expected. The bad news pulled down shares of competitors Aston Martin (which fell 24.51%), Ford (a 2% drop),and GM (3.53% lower today).

Carnival beat top and bottom line estimates last quarter, and posted record revenue for the third quarter. But shares stumbled 0.32% on management’s forecast that earnings in the fourth quarter will disappoint. Rival cruise companies all dropped in sympathy: Royal Caribbean fell 0.10%, while Norwegian Cruise Line Holdings tumbled 2.10%.

Here’s where the major stock market benchmarks ended:

The SPX gained 24.26 points (0.42%) to 5,762.48; the Dow Jones Industrial Average® ($DJI) rose 17.15 points (0.04%) to 42,330.15; the NASDAQ Composite® ($COMP) added 69.58 points (0.38%) to 18,189.17.

The 10-year Treasury note yield (TNX) climbed five basis points to 3.8%, near the high of its recent range.

The CBOE Volatility Index® (VIX) eased to 16.66 after climbing above 17 earlier today but remains up from a week ago.

Posted on September 28, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

***

By Michael Accad MD

***

In this article, I wish to introduce the reader to the theory of entrepreneurship advanced by Frank Knight (1885–1972), and show that the common, everyday work of the physician could be considered a form of entrepreneurial activity in the Knightian sense.

On June 8, 2023, the Centers for Medicare and Medicaid Services (CMS) announced the establishment of Making Care Primary (MCP) Model, a voluntary primary care model that will be tested in Colorado, Massachusetts, Minnesota, New Mexico, North Carolina, New York, New Jersey, and Washington.